An Enlarging Europe: Chances for consultants of the old and new member states Dr. F. Arnulf Fleischer Budapest, November 8-10, 2006 FEACO European Annual Conference 2006 DÜSSELDORF BUDAPEST HAMBURG BUCHAREST LONDON MOSCOW MUNICH NEW YORK SHANGHAI SINGAPORE VIENNA MUMBAI

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

An Enlarging Europe:Chances for consultants

of the old and new member states

Dr. F. Arnulf Fleischer

Budapest, November 8-10, 2006

FEACO European Annual Conference 2006

DÜSSELDORF BUDAPESTHAMBURGBUCHAREST LONDONMOSCOW MUNICHNEW YORKSHANGHAISINGAPOREVIENNAMUMBAI

FEACO_2_061109_Conference_Budapest.ppt© Droege & Comp. 2006

Executive summary

Today’s and future Eastern European EU members are showing growing political stability and economic growth prospects, an view supported by e.g. rating agencies like Standards & Poor’s.

The Eastern European consulting market is in relation to the Western market still small, but offers significant growth potential.

Medium-sized Western consulting companies have to rely on networking and cooperation with local consultants in Eastern Europe to participate in the growth prospects.

Major consulting services are related to market entry and penetration, relocation of production facilities, efficiency improvements and restructuring.

A project example of a successful market entry project shows how the cooperation of Eastern and Western consultants works…

…and it does work if there is a win-win situation.

Source: Droege & Comp.

FEACO_3_061109_Conference_Budapest.ppt© Droege & Comp. 2006

D&C: International offices for global delivery

Americas Europe Asia

Market entry/expansion

Supply chainstrategy/relocation

Global organisation/post merger integration

Restructuring subsidiaries

Global sourcing

Typical project areas

Moscow

Singapore

ShanghaiMumbai*

New York

*opening Q4/06

Paris

WarsawLondonHamburg

DüsseldorfMunich

Vienna

Bucharest

Budapest

…

FEACO_4_061109_Conference_Budapest.ppt© Droege & Comp. 2006

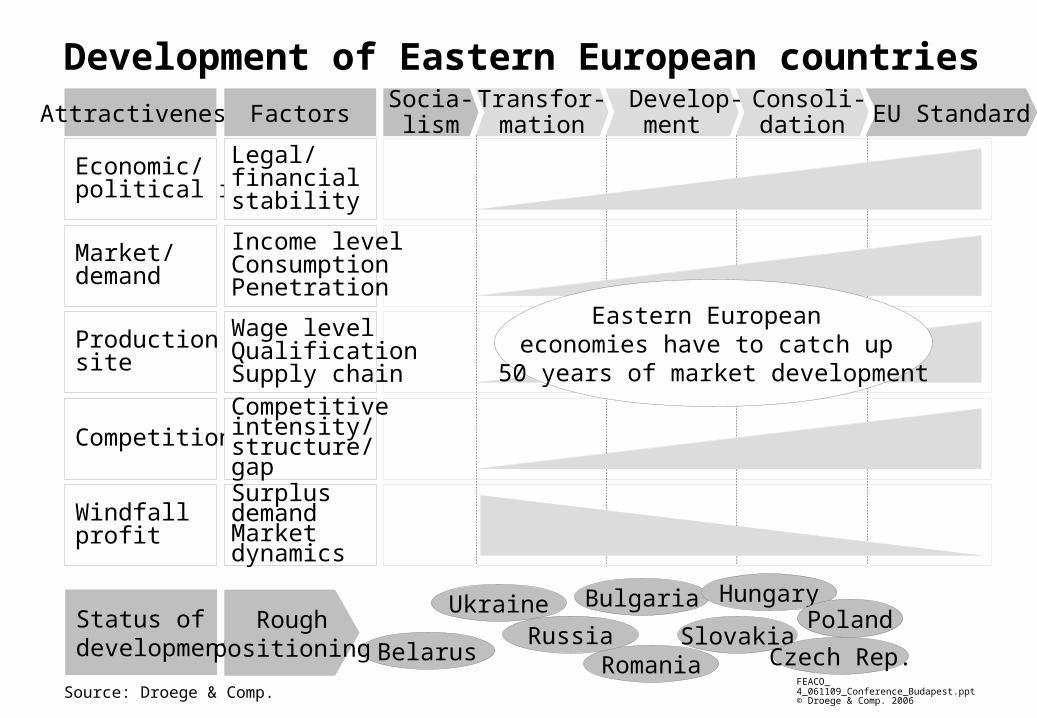

Development of Eastern European countriesSocia-lism

Transfor-mation

Develop-ment

Consoli-dationAttractiveness

Economic/political risks

Market/demand

Productionsite

Competition

Windfallprofit

Legal/financialstability

Income levelConsumptionPenetration

Wage levelQualificationSupply chainCompetitiveintensity/structure/gapSurplusdemandMarket dynamics

Factors

Status of development

Romania

Bulgaria Hungary

SlovakiaCzech Rep.

PolandUkraine

Russia

Source: Droege & Comp.

Eastern European economies have to catch up

50 years of market development

EU Standard

BelarusRough

positioning

FEACO_5_061109_Conference_Budapest.ppt© Droege & Comp. 2006

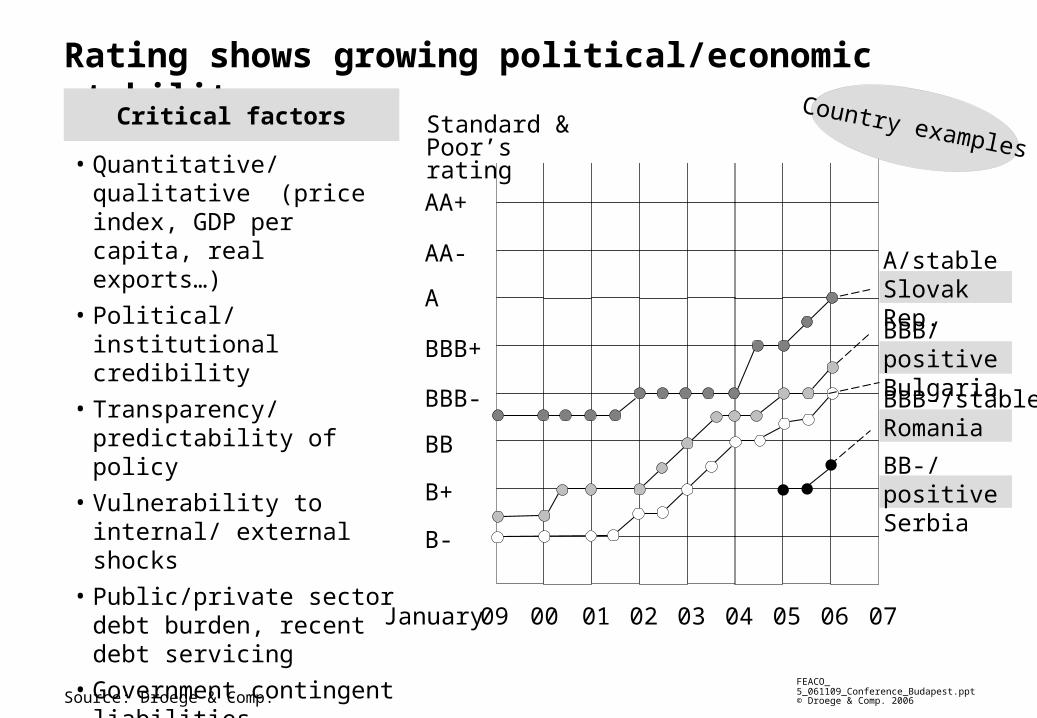

Rating shows growing political/economic stability

Source: Droege & Comp.

Critical factors

• Quantitative/qualitative (price index, GDP per capita, real exports…)

• Political/institutional credibility

• Transparency/predictability of policy

• Vulnerability to internal/ external shocks

• Public/private sector debt burden, recent debt servicing

• Government contingent liabilities

• Fiscal policy

AA+

AA-

A

BBB+

BBB-

BB

B+

B-

09 01 02 03 04 05 0600

January

Country examples

A/stable Slovak Rep.

BBB/positive Bulgaria

BBB-/stable Romania

BB-/positive Serbia

Standard & Poor’srating

07

FEACO_6_061109_Conference_Budapest.ppt© Droege & Comp. 2006

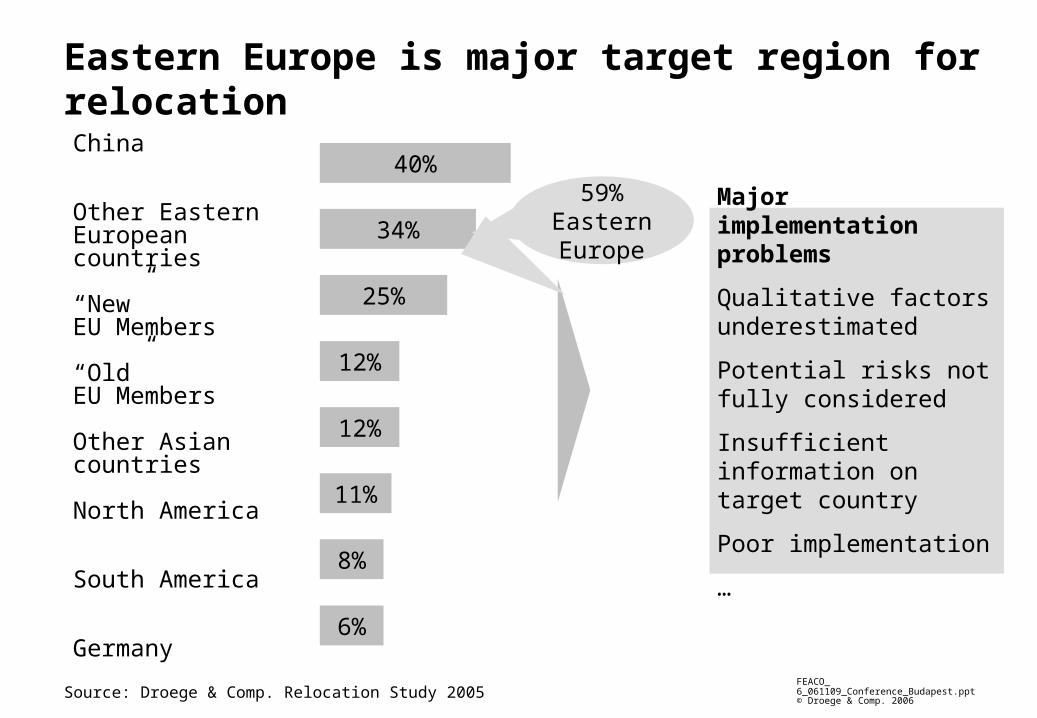

34%

Eastern Europe is major target region for relocation

Major implementation problems

Qualitative factors underestimated

Potential risks not fully considered

Insufficient information on target country

Poor implementation

…

40%China

Other EasternEuropean countries

“New” EU Members

“Old” EU Members

Other Asian countries

North America

South America

Germany

25%

12%

12%

11%

8%

6%

59% EasternEurope

Source: Droege & Comp. Relocation Study 2005

FEACO_7_061109_Conference_Budapest.ppt© Droege & Comp. 2006

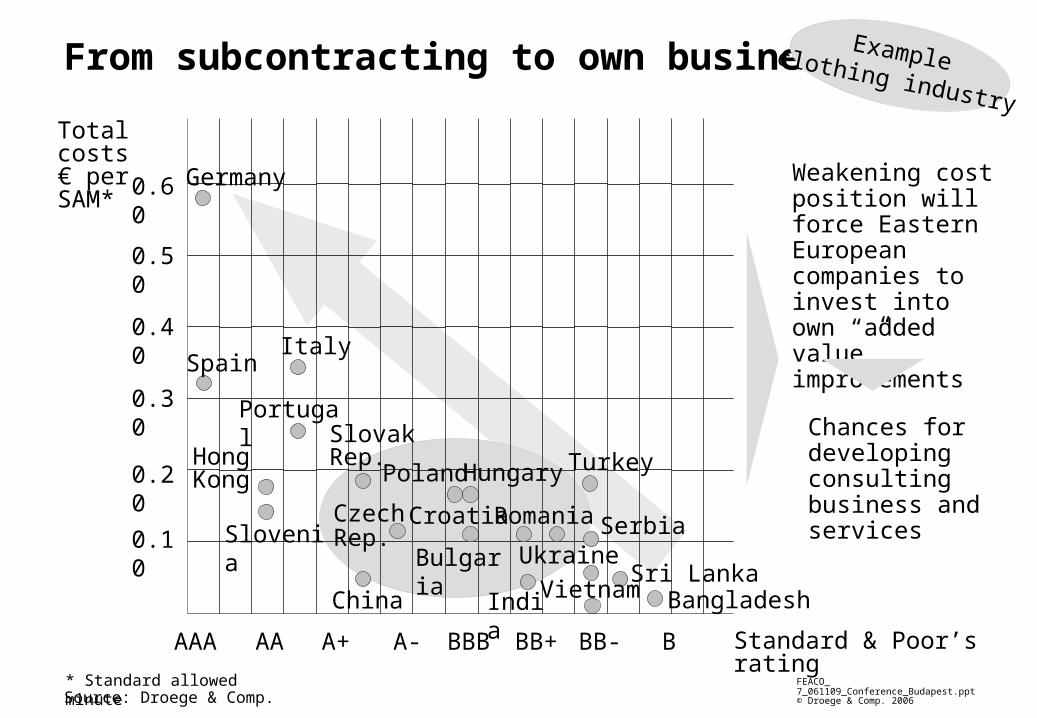

From subcontracting to own business

Source: Droege & Comp.

0.60

0.50

0.40

0.30

0.20

0.10

Exampleclothing industry

Total costs € per SAM*

Weakening cost position will force Eastern European companies to invest into own “added value” improvements

Chances for developing consulting business and services

AAA AA A+ A- BBB BB+ BB- B

Germany

Spain

Italy

Portugal

HongKong

Slovenia

China

SlovakRep.

CzechRep.

Poland

Hungary

Bulgaria

Croatia

Romania

India

Turkey

Serbia

Ukraine

Sri Lanka

Vietnam Bangladesh

* Standard allowed minute

Standard & Poor’s rating

FEACO_8_061109_Conference_Budapest.ppt© Droege & Comp. 2006

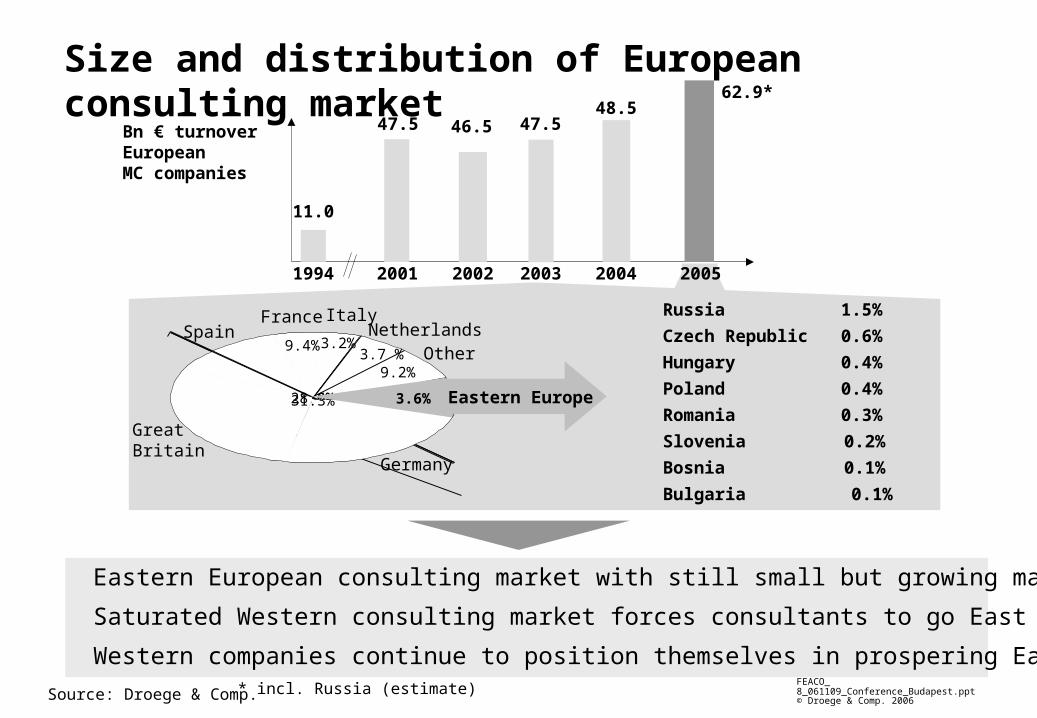

Eastern European consulting market with still small but growing market share

Saturated Western consulting market forces consultants to go East and also

Western companies continue to position themselves in prospering Eastern markets

Size and distribution of European consulting market

1994 2001 2002 2003

11.0

47.5 46.5

NetherlandsOther

ItalySpain

Great Britain

Germany

Russia 1.5%

Czech Republic 0.6%

Hungary 0.4%

Poland 0.4%

Romania 0.3%

Slovenia 0.2%

Bosnia 0.1%

Bulgaria 0.1%

11.0%28.6%

3.2% 3.7 %

9.4%

9.2%

47.5

2004 2005

48.5 62.9*

France

31.3% Eastern Europe3.6%

* incl. Russia (estimate)Source: Droege & Comp.

Bn € turnoverEuropeanMC companies

FEACO_9_061109_Conference_Budapest.ppt© Droege & Comp. 2006

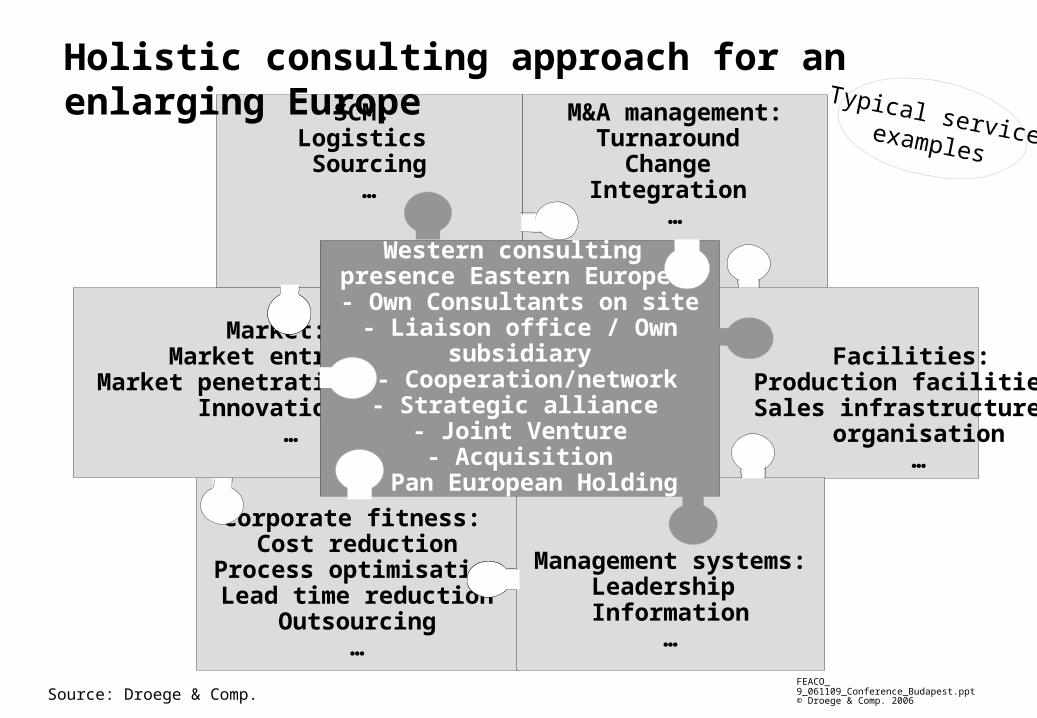

M&A management:Turnaround

Change Integration

…

Corporate fitness:

Cost reductionProcess optimisationLead time reduction

Outsourcing…

Market: Market entry Market penetration Innovation …

Facilities:

Production facilities Sales infrastructure/

organisation …

SCM: Logistics Sourcing

…

Management systems:Leadership Information

…

Western consulting presence Eastern Europe: - Own Consultants on site

- Liaison office / Own subsidiary - Cooperation/network

- Strategic alliance

- Joint Venture- Acquisition

- Pan European Holding

Holistic consulting approach for an enlarging Europe

Source: Droege & Comp.

Typical serviceexamples

FEACO_10_061109_Conference_Budapest.ppt© Droege & Comp. 2006

Foreign direct investments: Chances for consulting

Quelle: FEACO, Droege & Comp.

high

med

ium

low

low medium highManagement/consulting resources

Fin

anci

al r

eso

urc

es

Bul-garia

Czech Republic

Hun-gary

Po-land

Ro-mania

Russia

1.8

8.8Examples

Bn € 5.46.1

5.2

11.7

2001 2002 2003 2004 2005 2006

Bn €

29.4

47.6**

Green field

Joint Venture

Licence production

Sales subsidiary

Subcontracting

Export

Seed cornacquisition, M&A

Source: WIIW; Droege & Comp.

33.325.9

46.454.8

*Central, Eastern and South Eastern Europe**Forecast

Market entry/penetration Foreign direct investments Eastern Europe*

FEACO_11_061109_Conference_Budapest.ppt© Droege & Comp. 2006

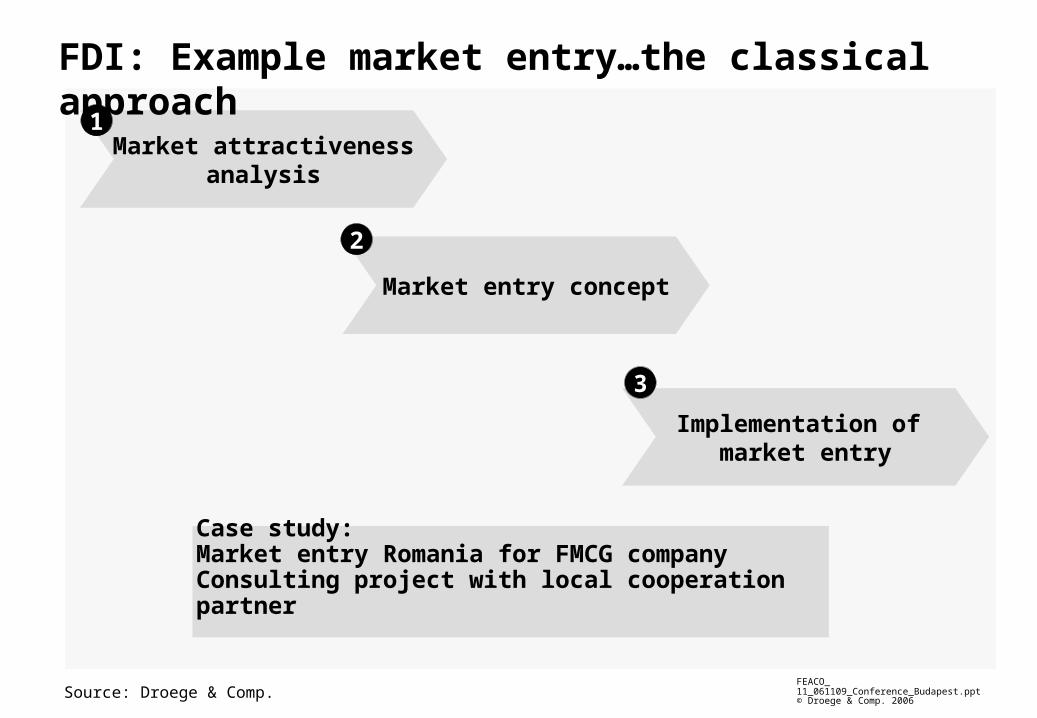

Market entry concept

2

Market attractivenessanalysis

FDI: Example market entry…the classical approach

1

Implementation of market entry

3

Source: Droege & Comp.

Case study:Market entry Romania for FMCG companyConsulting project with local cooperation partner

FEACO_12_061109_Conference_Budapest.ppt© Droege & Comp. 2006

Case study: Market entry Romania

•Client

Medium-sized market leader FMCG food (branded sausages)

•Major problems

Barriers to growth in current markets (domestic and EU export markets)

Customers get increasingly involved in Eastern Europe

Source: Droege & Comp.

Initial situationInitial situation

FEACO_13_061109_Conference_Budapest.ppt© Droege & Comp. 2006

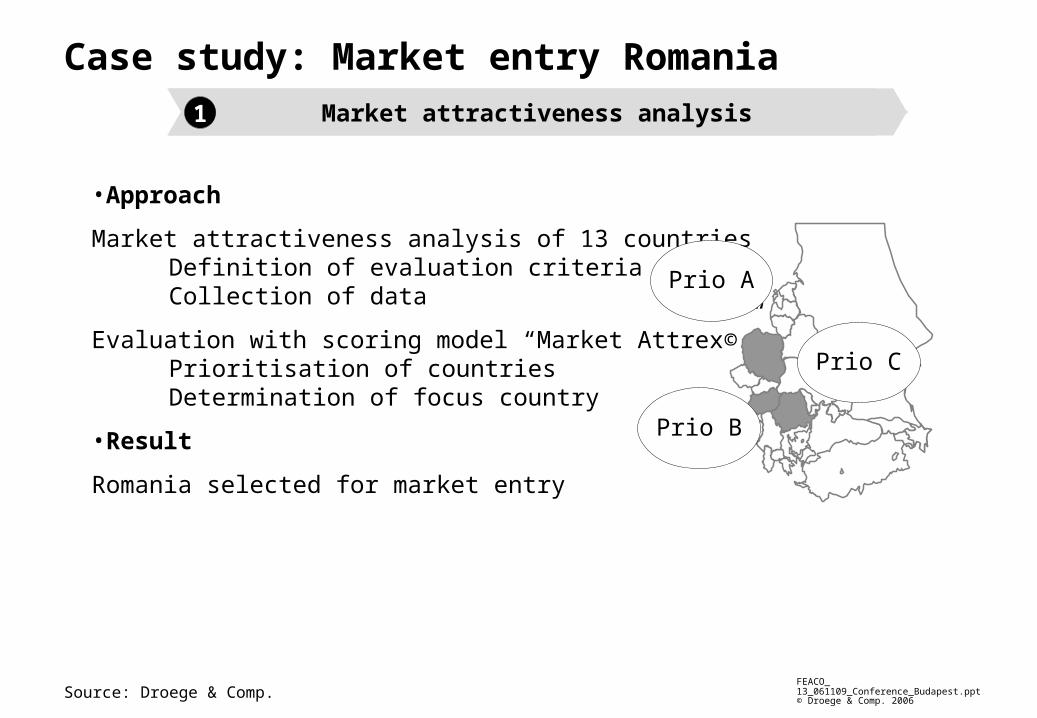

Case study: Market entry Romania

•Approach

Market attractiveness analysis of 13 countriesDefinition of evaluation criteriaCollection of data

Evaluation with scoring model “Market Attrex©”Prioritisation of countriesDetermination of focus country

•Result

Romania selected for market entry

Source: Droege & Comp.

Market attactiveness analysis

Prio A

Prio B

Prio C

1 Market attractiveness analysis1

FEACO_14_061109_Conference_Budapest.ppt© Droege & Comp. 2006

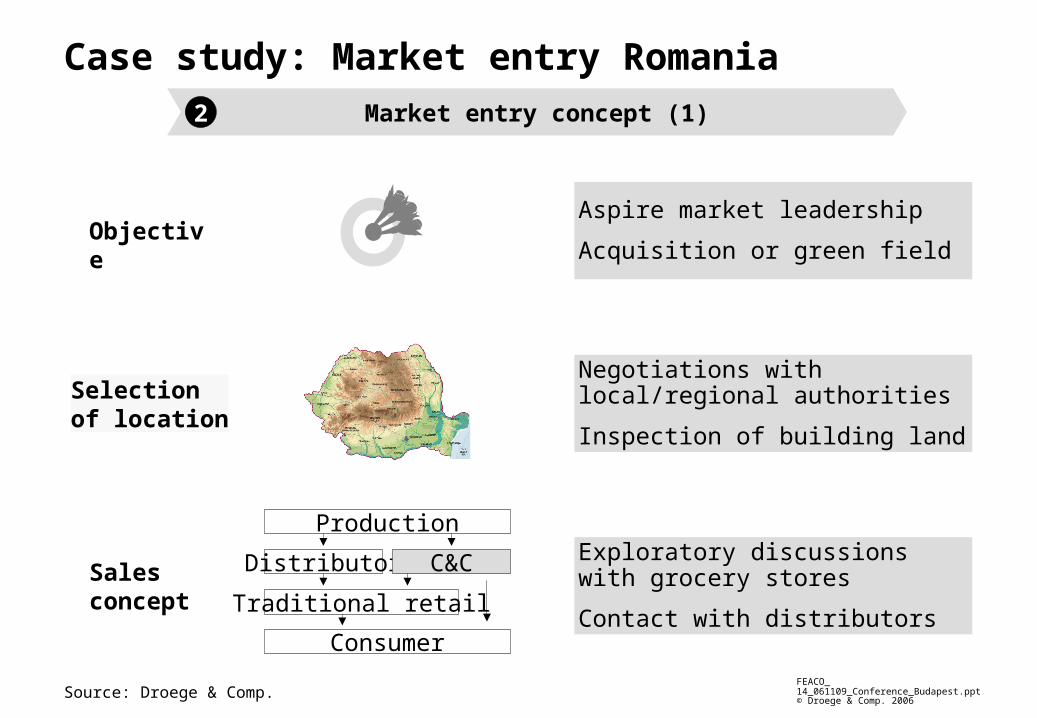

Case study: Market entry RomaniaMarket entry concept (1)

Selectionof location

Negotiations with local/regional authorities

Inspection of building land

Aspire market leadership

Acquisition or green field

Source: Droege & Comp.

Sales concept

Consumer

Production

Distributor C&C

Traditional retail

Objective

Exploratory discussions with grocery stores

Contact with distributors

2

FEACO_15_061109_Conference_Budapest.ppt© Droege & Comp. 2006

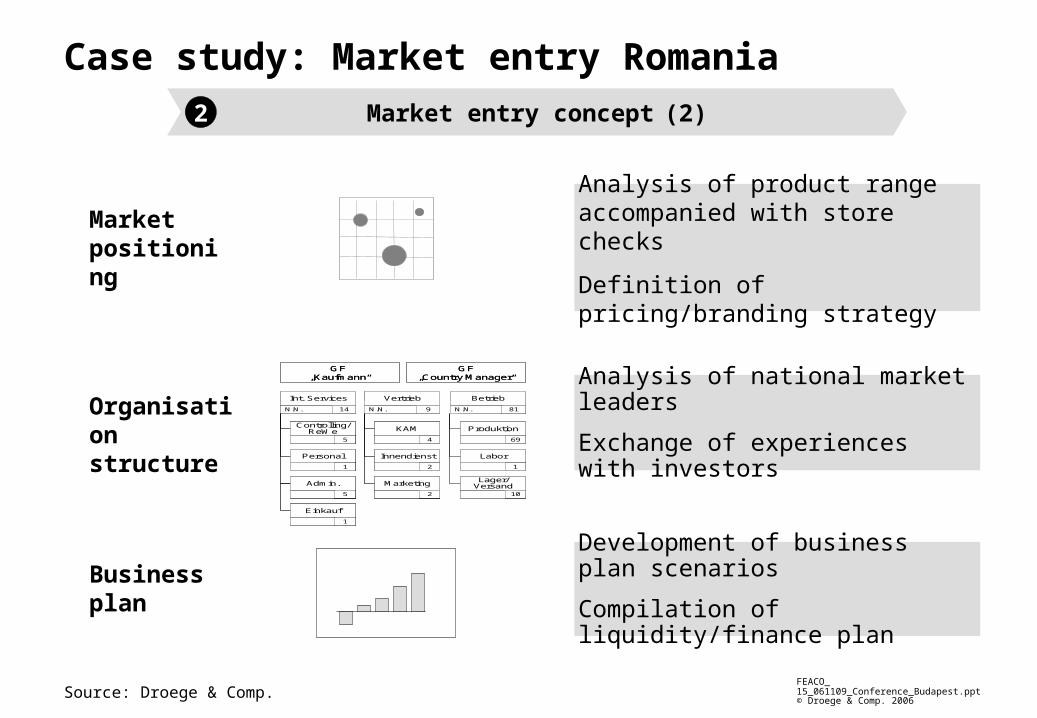

Case study: Market entry RomaniaMarket entry concept (2)

Marketpositioning

Businessplan

Development of business plan scenarios

Compilation of liquidity/finance plan

Analysis of national market leaders

Exchange of experiences with investors

Analysis of product range accompanied with store checks

Definition of pricing/branding strategy

Source: Droege & Comp.

Organisation structure Produktion

69

Labor

1

N.N.

Betrieb

81

Lager/Versand

10

N.N.

Vertrieb

9

KAM

4

Innendienst

2

Marketing

2

N.N.

Int. Services

14

Controlling/ReWe

5

Personal

1

Admin.

5

Einkauf

1

GF „Kaufmann“

GF„Country Manager“

Produktion

69

Labor

1

N.N.

Betrieb

81

Lager/Versand

10

N.N.

Vertrieb

9

KAM

4

Innendienst

2

Marketing

2

N.N.

Vertrieb

9

KAM

4

Innendienst

2

Marketing

2

N.N.

Int. Services

14

Controlling/ReWe

5

Personal

1

Admin.

5

Einkauf

1

N.N.

Int. Services

14

Controlling/ReWe

5

Personal

1

Admin.

5

Einkauf

1

GF „Kaufmann“

GF„Country Manager“

2

FEACO_16_061109_Conference_Budapest.ppt© Droege & Comp. 2006

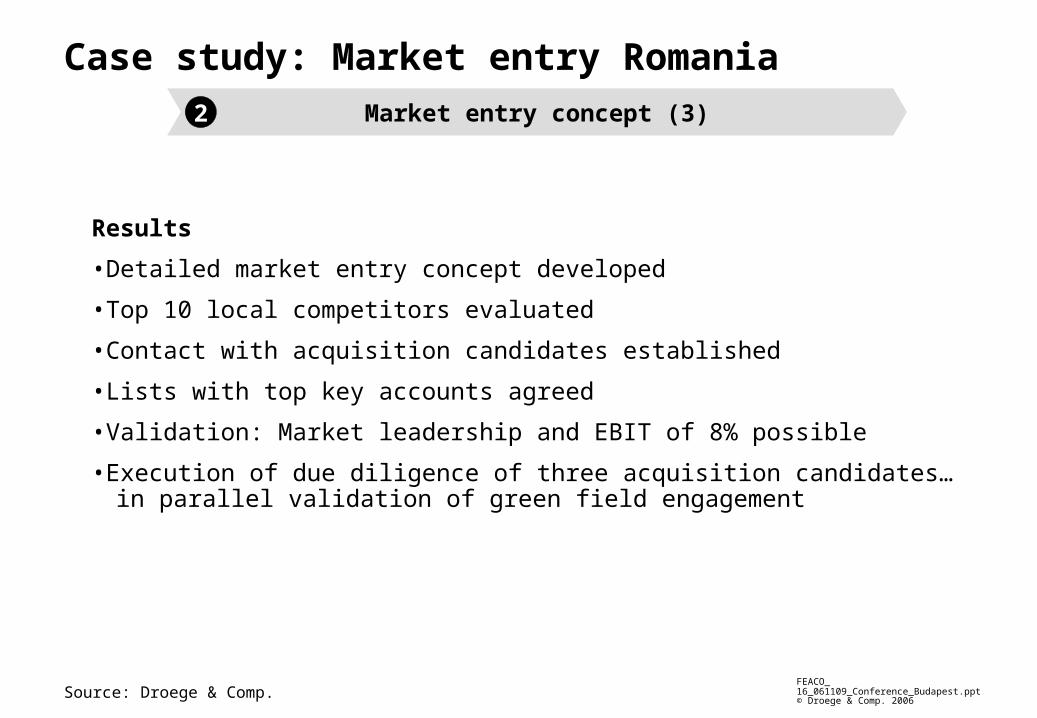

Case study: Market entry Romania

Results

•Detailed market entry concept developed

•Top 10 local competitors evaluated

•Contact with acquisition candidates established

•Lists with top key accounts agreed

•Validation: Market leadership and EBIT of 8% possible

•Execution of due diligence of three acquisition candidates… in parallel validation of green field engagement

Market entry concept (3)

Source: Droege & Comp.

2

FEACO_17_061109_Conference_Budapest.ppt© Droege & Comp. 2006

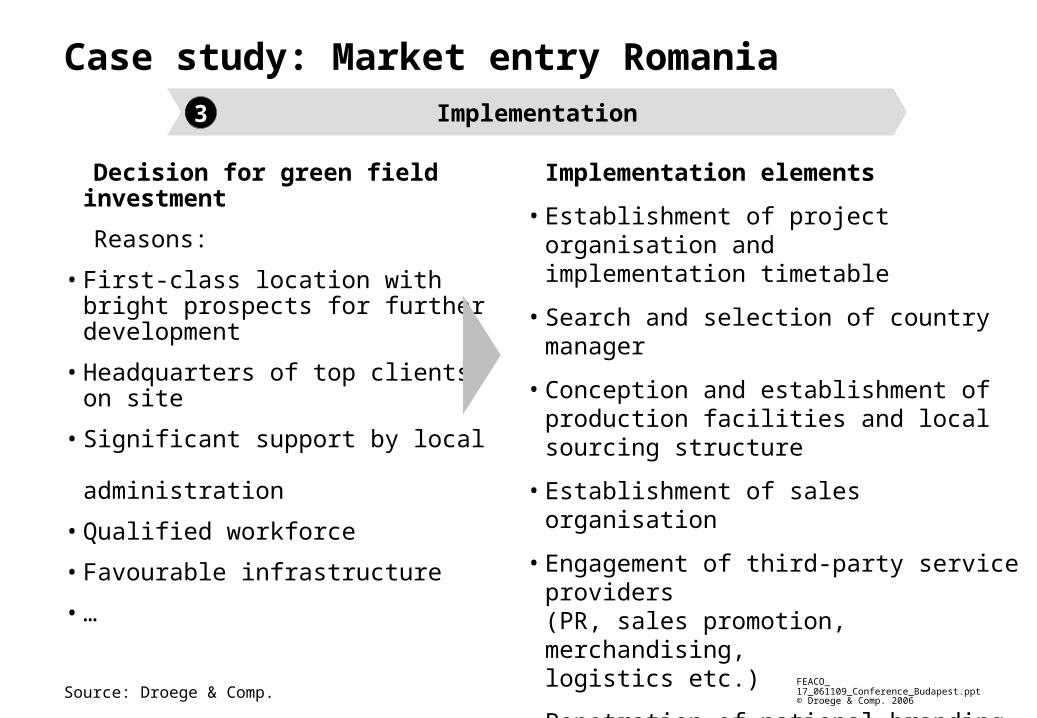

Case study: Market entry Romania

Decision for green field investment

Reasons:

• First-class location with bright prospects for further development

• Headquarters of top clients on site

• Significant support by local administration

• Qualified workforce

• Favourable infrastructure

• …

Implementation

Source: Droege & Comp.

Implementation elements

• Establishment of project organisation andimplementation timetable

• Search and selection of country manager

• Conception and establishment of production facilities and local sourcing structure

• Establishment of sales organisation

• Engagement of third-party service providers (PR, sales promotion, merchandising, logistics etc.)

• Penetration of national branding strategy (premium and standard)

• Development of assortment

• …

3

FEACO_18_061109_Conference_Budapest.ppt© Droege & Comp. 2006

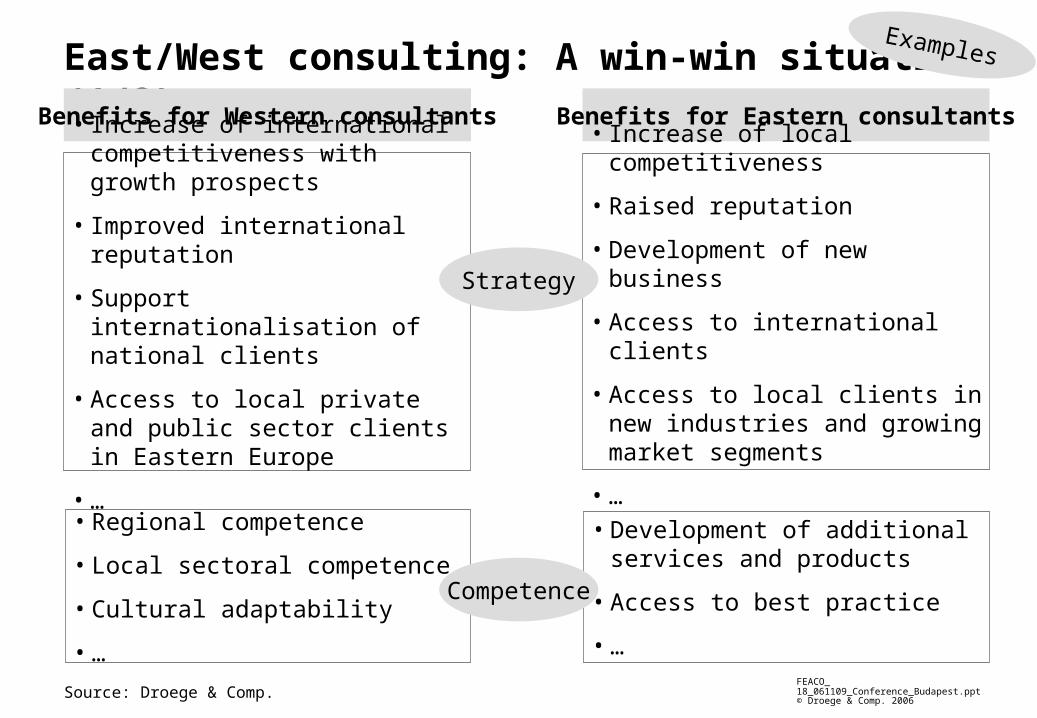

East/West consulting: A win-win situation (1/2)Examples

Benefits for Western consultants Benefits for Eastern consultants

Source: Droege & Comp.

• Increase of international competitiveness with growth prospects

• Improved international reputation

• Support internationalisation of national clients

• Access to local private and public sector clients in Eastern Europe

• …

• Increase of local competitiveness

• Raised reputation

• Development of new business

• Access to international clients

• Access to local clients in new industries and growing market segments

• …

Strategy

• Regional competence

• Local sectoral competence

• Cultural adaptability

• …

• Development of additional services and products

• Access to best practice

• …

Competence

FEACO_19_061109_Conference_Budapest.ppt© Droege & Comp. 2006

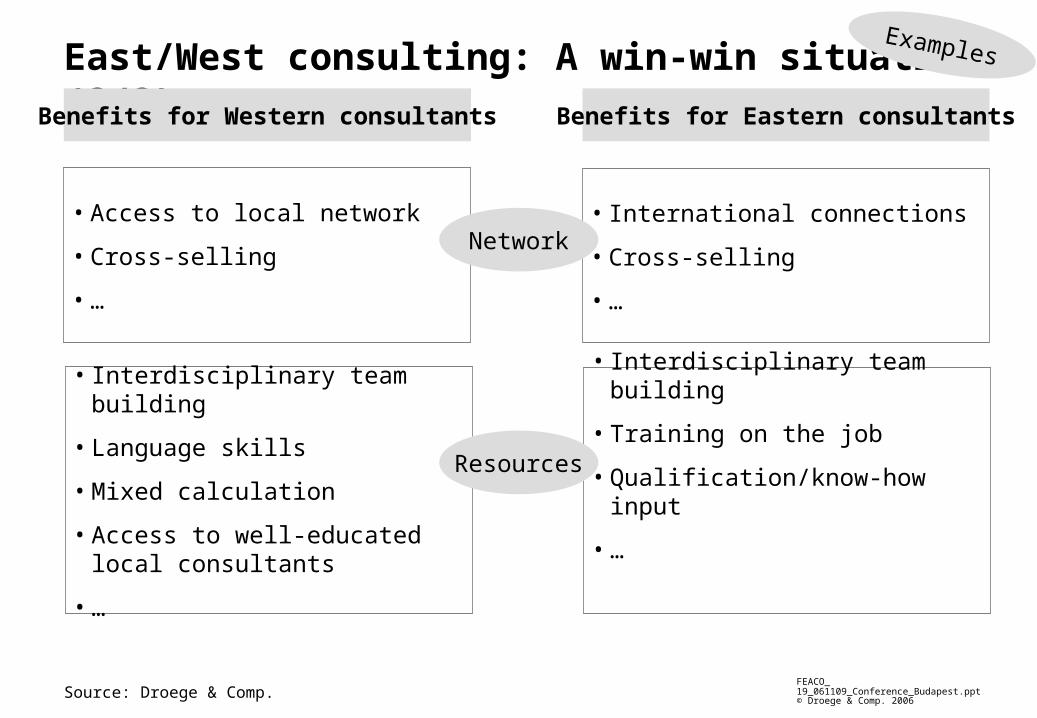

East/West consulting: A win-win situation (2/2)Examples

Benefits for Western consultants Benefits for Eastern consultants

Source: Droege & Comp.

• Access to local network

• Cross-selling

• …

• International connections

• Cross-selling

• …

Network

• Interdisciplinary team building

• Language skills

• Mixed calculation

• Access to well-educated local consultants

• …

• Interdisciplinary team building

• Training on the job

• Qualification/know-how input

• …

Resources

Related Documents