International Research Journal of Finance and Economics ISSN 1450-2887 Issue 40 (2010) © EuroJournals Publishing, Inc. 2010 http://www.eurojournals.com/finance.htm An Empirical Investigation of the Demutualization Impact on Market Performance of Stock Exchanges Arwa Morsy Doctoral Program, Department of Accounting, Finance and Economics Maastricht School of Management, The Netherlands E-mail: [email protected] ; [email protected] Kami Rwegasira Professor and Head of Department of Accounting, Finance and Economics Maastricht School of Management, The Netherlands E-mail: [email protected] Abstract Prior studies in the literature on the impact of demutualization on the performance of stock exchanges focused on only a few market measures. Some used very small sample sizes. And others only examined the stock exchanges’ performance relative to other listed firms in their market and to other initial public offerings. Consequently the issue has remained controversial and open to debate. In this study, we test whether or not the demutualization program resulted in better market performance using a wider range of market measures and larger sample sizes drawn from demutualized stock exchanges that are members of the World Federation of Exchanges and have undergone the demutualization program over the 1993-2004 period. By employing a matched-pairs methodology to examine 16 market measures in the pre and post demutualization periods, we find empirical persuasive evidence that suggests that the demutualization programs do not improve the market performance of the equity and bonds markets of demutualized stock exchanges. We find that demutualization resulted in significant improvement in only seven out of the sixteen market measures used test for change in performance. This result was noted in the total number of listed companies, number of transactions, domestic market capitalization, capital raised by domestic companies, total value of share trading, turnover velocity of domestic shares, and value of bonds listed. The research hypothesis that demutualization improves stock exchange market performance is not however supported in the remaining market measures; market capitalization of newly listed shares, new capital raised by IPOs, number of bonds issuers, number of bonds listed, average value of transactions, capital raised by bonds, value of bonds trading and market concentration of the 5 percent largest companies. Keywords: Demutualization, stock exchanges, market performance, capital markets, financial markets JEL Classification Codes: G10, G15, G39 1. Introduction Prior to 1990s, stock exchanges all over the world used to operate as mutual organizations. Early 1990s, stock exchanges started to undertake major organizational and operational changes. One of the most noted changes was the trend toward demutualization. Demutualization is the process of

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 40 (2010) © EuroJournals Publishing, Inc. 2010 http://www.eurojournals.com/finance.htm

An Empirical Investigation of the Demutualization Impact on

Market Performance of Stock Exchanges

Arwa Morsy Doctoral Program, Department of Accounting, Finance and Economics

Maastricht School of Management, The Netherlands E-mail: [email protected] ; [email protected]

Kami Rwegasira

Professor and Head of Department of Accounting, Finance and Economics Maastricht School of Management, The Netherlands

E-mail: [email protected]

Abstract

Prior studies in the literature on the impact of demutualization on the performance of stock exchanges focused on only a few market measures. Some used very small sample sizes. And others only examined the stock exchanges’ performance relative to other listed firms in their market and to other initial public offerings. Consequently the issue has remained controversial and open to debate. In this study, we test whether or not the demutualization program resulted in better market performance using a wider range of market measures and larger sample sizes drawn from demutualized stock exchanges that are members of the World Federation of Exchanges and have undergone the demutualization program over the 1993-2004 period. By employing a matched-pairs methodology to examine 16 market measures in the pre and post demutualization periods, we find empirical persuasive evidence that suggests that the demutualization programs do not improve the market performance of the equity and bonds markets of demutualized stock exchanges. We find that demutualization resulted in significant improvement in only seven out of the sixteen market measures used test for change in performance. This result was noted in the total number of listed companies, number of transactions, domestic market capitalization, capital raised by domestic companies, total value of share trading, turnover velocity of domestic shares, and value of bonds listed. The research hypothesis that demutualization improves stock exchange market performance is not however supported in the remaining market measures; market capitalization of newly listed shares, new capital raised by IPOs, number of bonds issuers, number of bonds listed, average value of transactions, capital raised by bonds, value of bonds trading and market concentration of the 5 percent largest companies.

Keywords: Demutualization, stock exchanges, market performance, capital markets, financial markets

JEL Classification Codes: G10, G15, G39 1. Introduction Prior to 1990s, stock exchanges all over the world used to operate as mutual organizations. Early 1990s, stock exchanges started to undertake major organizational and operational changes. One of the most noted changes was the trend toward demutualization. Demutualization is the process of

International Research Journal of Finance and Economics - Issue 40 (2010) 39

transforming the organization from a mutually owned structure to profit, investor-owned corporation. Under a mutual governance structure, members; or broker dealers with ‘seats’ on the exchange are also owners of the stock exchange with all voting rights related to this ownership. Transforming the organization into a demutualized structure means that trading and ownership can be separated. A demutualized stock exchange is a limited liability company that is owned by its shareholders – who provide capital to the exchange and receive profits but need not carry out trading on the exchange (Aggrarwal, 2002). The remarkable change in the ownership and organizational structure of the demutualized stock exchanges was mainly motivated by some intense global competition and advances in technology. Decisions to demutualization are based in essence on the recognition that the old member-owned organizational structure fails to provide the flexibility and the financing needed to compete in the global competitive environment. Demutualized stock exchanges are driven by profit-seeking investors who want to produce better financed organizations with greater ability to respond quickly to the fast changing market place. Some of the typical sources of revenues such as, listing fees, membership fees become less important. For the demutualized exchanges, transaction fees and new products and services are more important sources to expand their revenue (Ibid.).

The trend of demutualization started in 1993 with the Stockholm Stock Exchange, which was the first stock exchange to demutualize. This was followed by Helsinki (1995), Copenhagen (1996) and Amsterdam (1997). This was followed by several other major stock exchanges such as ASX, TSX, the Singapore Stock Exchange and the Hong Kong Exchanges and Clearing Limited (“HKEx”). ASX was one of the first exchanges to do an Initial Public Offering (IPO) and list its shares on its own market place. TSX, which demutualized in 2000, became in 2002 a public company through listing its shares on its exchange. In Asia-Pacific, Singapore Exchange Limited (“SGX”) was the first stock exchange to demutualize in December 1999. End of 2000, SGX’s shares were listed on its own market place, after the merger process of the Stock Exchange of Singapore (“SES”) and the Singapore International Monetary Exchange (“SIMEX”). In 2000, HKEx was also created as a result of the merger and demutualization of Stock Exchange of Hong Kong Limited (“SEHK”) and the Hong Kong Futures Exchange Limited (“HKFE”) and the Hong Kong Securities Clearing Company Limited (“HKSCC”). Mid 2000, HKEx shares were listed on its own marketplace, following the merger. In 2000, Tokyo Stock Exchange; one of the largest exchanges in the world completed its demutualization. In 2006, the New York Stock Exchange (NYSE), comprising 30.46% of world market capitalisation, converted its governance structure via a backdoor listing facilitated by its merger with Archipelago Holdings, a rival electronic exchange. The demutualization of the Bourse de Montréal, Chicago Board Options Exchange (CBOE), Chicago Board of Trade (CBOT), Chicago Mercantile Exchange (CME) and the Sydney Futures Exchange (SFE) shows that this process also takes place amongst derivatives and commodity exchanges (Hughes and Zargar, 2006).

Despite this international trend, stock exchange demutualization continues to generate debate amongst academics, business people and policy makers on the impact of such conversion; from the mutualized to demutualized organizational form. Proponents to demutualization argue that demutualization and self-listing can greatly free up the ability of stock exchanges to engage in many commercial activities. One example is the Australian Stock Exchange. Few months after its demutualization, it announced a merger proposal (unsuccessfully) with the Sydney Futures Exchange. Within a year, the exchange formed a strategic alliance with NASDAQ, created a joint venture with Perpetual Trustees in 2000, created an operational trading link with both North America and Singapore in 2001, launched a futures market in 2002, and by 2003 had entered memorandums of understanding (MOUs) with the Philippines, Thailand, Singapore, Tokyo, Hong Kong, Shanghai and Shenzhen exchanges. A similar trend was also noted in many other demutualized stock exchanges such as Deutsche Borse, London Stock Exchange, and Singapore Stock exchange (Worthington and Higgs 2005/06). Demutualization can also help the stock exchange to modernize its technology, obtain a governance structure that is more flexible in responding to industry and market conditions, avoid concentration of ownership power in a particular group of stock exchange participants and ensure

40 International Research Journal of Finance and Economics - Issue 40 (2010)

financial decision-making by ensuring that resources are allocated to business initiatives and ventures that enhance shareholder value (Lee, 2002).

Opponents to demutualization argue that the above mentioned benefits of demutualization may in reality not materialize or may be obtainable with a mutual governance structure for a securities exchange. Thus, any cost-saving that a demutualized stock exchange with direct investor access might result in is low in comparison to the benefits that can be obtained from the presence of brokers, with ownership interests in the exchange. From their point of view, in many developing countries, the creation of any financial institution is extremely hard, and the creation of investors is even harder than the creation of the brokers (Ibid.). In addition, the change in the governance structure raises concerns regarding the ability of the demutualized stock exchange to develop and enforce appropriate listing and disclosure standards, surveillance and discipline, financial and operational compliance, and fair and equitable treatment of customers. There is also a question on whether or not the demutualized stock exchange will perform better (Steil, 2002). A related issue addressed by Worthington and Higgs (2006) is whether the act of demutualization and/or listing has allowed new risky business activities that did not take place when the stock exchange was mutual and that may be of concern to regulators.

The impact of demutualization on the market performance of stock exchanges is not clear yet. Earlier literature that looked at the demutualization trend did not focus on the impact, largely because the trend of demutualization was very recent at the time of writing these studies. Subsequent studies on the impact of demutualization focused on very few measures. Some of them used very small sample sizes and others also analyzed the impact on only demutualized stock exchanges that were completely transformed into publicly listed companies. Therefore, until today, there is little empirical evidence on the impact of demutualization on market performance. We deal with the shortcomings in the prior literature and investigate the impact of demutualization on the market performance of stock exchanges through analyzing a wide variety of market measures in the pre and post demutualization periods. Performance changes are tested on a matched pair basis in order to examine whether stock exchanges performed better after demutualization. 2. Previous Empirical Literature In general, empirical literature on the demutualization of stock exchanges is scarce. There are few academic studies that explain the impact of governance change on the exchange itself. Though there are many theoretical (non-empirical) studies that agree that demutualization should be a natural move to improve exchanges competitiveness in a changing business environment, it is still unclear in reality (empirically) how different demutualization affect the stock exchange performance. Following is a review of the existing empirical literature on the impact of demutualization on the performance of exchanges.

There are three studies that use input-output ratios and use data development analysis and stochastic frontier analysis to assess the efficiency of exchanges (Schmiedel 2001, 2002 and Serifsoy, 2005). Schmiedal 2001, 2002 employed frontier efficiency methods in order to derive relative efficiency values of an exchange. In his two papers he employed two different methods of frontier analysis. While Schmiedel (2001) employs a parametric stochastic frontier model to evaluate the cost efficiency of European stock exchanges, he applies a non-parametric method in the second paper (Schmiedel, 2002). Schmiedel's findings on stock exchange governance are not clear, however. Schmiedal’s first paper, which controls for demutualized exchanges within the regression, displays a positive impact of demutualization on cost efficiency, whereas his second paper indicates that the mean of productivity gains is higher for mutual exchanges.

Serifsoy (2005) also conducted an efficiency analysis that focuses on the exchange governance and uses more recent data than that used by Schmiedel. Similar to Schmiedel (2002), he also employed a non-parametric approach to calculate relative efficiency scores. However, he used a broader set of output variables. Serifsoy (2005) calculates in a first step individual efficiency and productivity values via the Data Envelopment Analysis (DEA). In a second step, Serifsoy (2005) regresses the derived

International Research Journal of Finance and Economics - Issue 40 (2010) 41

values against variables that - amongst others - form the institutional arrangement of the exchanges in order to determine efficiency and productivity differences between mutual, demutualized but customer-owned exchanges and publicly listed exchanges. This step allows understanding whether there is a significant impact of different governance structures on the impact on the performance of stock exchanges. Serifsoy (2005) concludes that demutualized exchanges exhibit higher technical efficiency than mutual ones. However, demutualized exchanges perform relatively poor as far as productivity growth is concerned. There is no evidence that publicly listed exchanges achieves higher efficiency and productivity values than demutualized exchanges with a customer-dominated structure (Serifsoy, 2005).

Another strand of literature assesses the development of liquidity following demutualization. This can be seen in Krishnamurti et al (2003), Mendiola and O’Hara (2004) and Treptow (2006). Krishnamurti, Sequeira & Fangjian (2003) show that the organization structure of a stock exchange matters through comparing two major stock exchanges in India; the mutualized - Bombay Stock Exchange (BSE) and the demutualized National Stock Exchange (NSE). These two exchanges adopt similar trading systems, trade essentially identical stocks and follow same trading hours, but they have different organizational structures. Krishnamurti et al. used trading data for 40 stocks listed on two Indian exchanges in the 1990s and found out that the demutualized National Stock Exchange is able to pass on lower trading costs to investors than BSE. Using the Hasbrouck (1993)1 measure of market quality, they show that NSE provides a better market quality than BSE.

Mendiola and O’Hara (2004) also examined the liquidity issue following the exchange’s demutualization. They used the illiquidity ratio, or the extent to which daily volume move daily prices. In order to study whether liquidity provision has improved after the exchange equitization, Mendiola and O’Hara (2004) collected daily volume and price change data for a sample of stocks trading on each of the exchanges in the sample. The sample was selected to represent the market for each exchange, and it included about 80-120 stocks for each market – except Athens Stock exchange, where only 14 stocks comprised the most of the trading). Mendiola and O’Hara (2004) then calculated the illiquidity ratio for each stock on a daily basis one year before and one year after each exchange’s listing or IPO date. The overall illiquidity ratio is then calculated as the average across the stocks. Mendiola and O’Hara (2004) provided evidence that liquidity production is improving after the exchange conversion. They found out that illiquidity is reduced for four of the seven firms in the sample in the first year after conversion. They also show that this improvement continues into the second year for most of the sample exchanges. They conclude that in general, the liquidity data is supportive of enhanced exchange performance, but is not definitive.

Treptow (2006) also presented a detailed analysis on the consequences of demutualization of securities exchange on liquidity. In order to capture the demutualization impact on liquidity, Treptow (2006) examined securities that are listed on two markets simultaneously. He used a quasi-experimental framework, as all securities are listed in primary markets that demutualized during the study period. All securities share the NYSE (which was not yet demutualized at the time of conducting the study), as a common second trading venue. The data consists of various liquidity measures for 156 dually listed equity issues on the New York Stock Exchange and 12 non-U.S. exchanges, and spans across a ten-year period. Treptow (2006) found out that demutualization brings significant beneficial effects on demutualizing exchange’s liquidity. In comparison to pre demutualization levels, turnover and resiliency increase, while spreads tighten. He also concluded that the liquidity gap between a demutualized and an undemutualized exchange increases due to the transformation.

1 Hasbrouck (1993) measures transaction costs in stock markets based on decomposition of a non-stationary time series

into a random-walk component and a residual stationary component. When applied to stock transaction prices, the random-walk component is identified as the efficient price with the stationary component (termed the pricing error) representing the difference between efficient price and actual transaction price. Dispersion of the pricing error that results from this division, measures how closely actual transaction prices follow a random walk and, therefore, constitutes an appropriate measure for transaction costs (Krishnamurti et al., 2003).

42 International Research Journal of Finance and Economics - Issue 40 (2010)

Several empirical studies have also assessed the development of other variables in the post demutualization period. Hazarika (2005) studied the impact of demutualization on trading volumes and costs; considering two different reasons for the conversion of stock exchanges. She highlighted the role of competition as a motivation for demutualization and thus studied the impact of demutualization in two different situations; in which competition plays very different roles.

In order to examine how increasing competition and demutualization had an impact on the exchange’s order flow and trading costs, she analyzed London Stock Exchange (LSE), by documenting the impact of increasing competition on exchange’s volume and testing if the introduction of ‘residual claimant’ helped LSE regain order-flow. She further conducted a time-series analysis of trading costs as LSE faced competition and responded to it. Hazarika also studied another stock exchange that demutualized for reasons other than competition. She examined the case of Borsa Italiana (BI) which was privatized by the Government in spite of members’ resistance. The results highlighted the important role that competition plays in stock exchange markets. In the case of Borsa Italiana; which demutualized for reasons other than competition, the stock exchange captures the entire order flow and eliminates the little competition which is out there. Additionally, the owners of the demutualized stock exchange have no incentives to lower trading costs. This suggests that a demutualization with no competition actually leads to more or complete dominance by the primary exchange, making the introduction of potential competition even more difficult in the future. The results indicate that introducing a ‘residual claimant’ in the governance structure of stock exchanges is definitely better for the exchange. Demutualization leads to an increase in the order flow. This impact is not however clear for investors. The impact of demutualization differs according to whether the exchange is subject to competitive forces. Where the stock exchange demutualizes in a competitive environment, investors are better off, as trading costs continue to decline post-demutualization. On the contrary, a demutualized stock exchange with no competitive environment could make investors worse off.

Finally, Worthington and Higgs (2006), analyzed market risk in four demutualized and self-listed stock exchanges; the Australian Stock Exchange, the Deutsche Borse, the London Stock Exchange and the Singapore Stock Exchange. They use a bivariate MA-GARCH model to estimate time-varying betas for each stock exchange from listing date until 7 June 2005. The series involves different sampling periods given the varying self-listing dates. The end date for all series is 7 June 2005 with the ASX starting on 14 October 1998, DEB on 5 February 2001, LSE on 22 July 2001 and SGX on 22 November 2000. The sample periods at the time of study represent the longest series of data possible. The raw data employed in the study are the daily prices of the four stock exchange companies and the daily market value-weighted equity indices for Australia, Germany, the United Kingdom and Singapore. The company data were obtained from Bloomberg and the market indices from Morgan Stanley Capital International (MSCI). They used MSCI market indices instead of, the Australian All Ordinaries, Germany’s DAX, the United Kingdom’s FTSE100 and Singapore’s Straits Times, because of their consistency in depth, breadth and construction. Daily company and MSCI index returns provide the respective asset and market portfolio data. While the results indicate significant beta volatility, unit root tests show the betas to be mean-reverting. These findings are used to suggest that despite concerns that demutualized and self-listed stock exchanges entail new market risks that need regulatory intervention, the betas of the stock exchange companies have not changed significantly since listing. However, market risk does vary considerable across the exchanges. 3. How does this study fit in literature? There are several limitations to the above-mentioned studies. Early work on the impact of demutualization represented in Schmiedel’s paper did not focus on differences in exchanges governance, largely because the trend of demutualization was very recent at the time of writing these studies. Subsequent works on the impact of demutualization focused on certain indicators; such as efficiency (Serifsoy, 2005), liquidity (Kishnamurti et al, 2003; and Treptow, 2006), trading volume and

International Research Journal of Finance and Economics - Issue 40 (2010) 43

costs for two exchanges that demutualized in two different situations; in which competition played very different roles (Hazarika, 2005), and market risk (Worthington and Higgs, 2006).

Studies by Krishnamuti et al.(2003) and Hazarika (2005) only examine two stock exchanges; which is not enough to yield robust conclusions. Further, Krishnamurti et al (2003) also focus on the post-demutualization period only. Their findings cannot be explicitly related to the demutualization event as it only provides a comparative analysis between two stock exchanges in India with different ownership structures. Further, the exchange considered as demutualized by Krishnamurti et al (2003); National Stock Exchange of India, does not meet the general criteria that describe an exchange as demutualized. Although NSE is considered a for-profit exchange, the ownership of its shares is not totally separated from membership and its shares can not be traded freely. NSE is controlled by a small number of banks and insurance companies.

The analysis of Mendiola and O’Hara (2004) covers wider varieties of measures. Mendiola and O’Hara study liquidity, and risk-based measures of performance. In addition, they study five general accounting measures of performance: the return on assets, the return on equity, profitability, asset turnover and financial leverage. However, there are several limitations to Mendiola and O’Hara’s study. First, it is restricted to exchanges that have been completely transformed into publicly listed companies. Second, the sample size is small. Out of the universe of traded exchanges, the research focuses on eight stock exchanges. The research excludes some traded stock exchanges due to lack of information on trading volume, unavailability of data due to recent conversion of the stock exchange or when the stock exchange (such as Stockholm Exchange) is not listed separately, but instead trades as part of its parent company (OM). Third, there is a problem of having a control group of stock exchanges because almost all of the large stock exchanges are part of the sample. This problem makes it impossible to apply comparisons across all stock exchanges because it is only the smaller stock exchanges that are still member-owned (at time of carrying out the study). Fourth, the study is applied to traded stock exchanges and since prior conversion stock exchanges do not have traded stock, it is impossible to tell the market performance in the absence of conversion. Finally, most of the conversions happened in the last three years of applying the study. It was noted that this period witnessed difficulty for asset markets world-wide (Mendiola and O’Hara, 2004).

This study deals with most of the above-mentioned limitations. The impact of demutualization on market performance is captured through analyzing several market measures in the pre and post demutualization periods. The study is more comprehensive as it uses wide variety of market measures extracted from literature to study market performance. Larger sample sizes are used in this study (between 11-20 stock exchanges in each sample). Stock exchanges used in the analysis are varied; they include large and small stock exchanges and include those of developed and emerging economies. The study has also applied a control analysis to study whether or not there are factors other than demutualization that might have an impact on the performance of stock exchanges. Depending on the availability of data, we study demutualized stock exchanges; that are members of the World Federation of Exchanges (WFE)2. The following sections discuss the data and research methodology and present an analysis of results. 3. Hypothesis Testing Given the previous studies presented above, it appears that there are strong reasons to suggest that market performance should improve following the stock exchange demutualization. We are testing a

2 According to the World Federation of Exchanges, demutualized stock exchanges include those exchanges registered as

private, limited companies but which are not listed. The demutualization of an exchange is a process by which a non-profit member-owned organization is transformed into a for-profit shareholder corporation. Ownership is somewhat more open. Private, limited companies are bourses registered as private companies, generally with a paid-up share capital. Intermediaries are almost always the sole owners of the exchange, and their ownership and intermediation rights and activities are strongly linked. Publicly listed exchanges include those stock exchanges that go public when its shares are listed on an exchange and are freely negotiable among investors (WFE Cost and Revenue Survey, Sept. 2006).

44 International Research Journal of Finance and Economics - Issue 40 (2010)

hypothesis that demutualization leads to better market performance of the equity and bonds markets of demutualized stock exchanges.

Recast in a testable form, the research major hypothesis is posited as given below: H1: Demutualization leads to better market performance of the equity and bonds markets of

demutualized stock exchanges. And because market performance of the equity and bonds markets can be measured in terms of

several market indicators, minor hypotheses can be stated as follows: H2: Total number of listed companies after demutualization > total number of listed companies

before demutualization. H3: Number of transactions in equity shares after demutualization > number of transactions in

equity shares before demutualization. H4: Domestic market capitalization after demutualization > domestic market capitalization

before demutualization. H5: Market capitalization of newly listed shares after demutualization > market capitalization

of newly listed shares before demutualization. H6: New capital listed by shares after demutualization > new capital listed by shares before

demutualization. H7: New capital listed by IPOs after demutualization > new capital listed by IPOs before

demutualization. H8: Number of bonds issues after demutualization > number of bonds issues before

demutualization. H9: Number of bonds listed after demutualization > number of bonds listed before

demutualization. H10: Number of new bonds listed after demutualization > number of new bonds listed before

demutualization. H11: Average value of transactions after demutualization > average value of transactions

before demutualization. H12: Total value of share trading after demutualization > total value of share trading before

demutualization. H13: Turnover velocity of domestic shares after demutualization > turnover velocity of

domestic shares before demutualization H14: Values of bonds listed after demutualization > value of bonds listed before

demutualization. H15: Capital raised by bonds after demutualization > capital raised by bonds before

demutualization. H16: Value of bonds trading after demutualization > value of bonds trading before

demutualization. H17: Market concentration of the 5 percent largest companies after demutualization > market

concentration of the 5 percent largest companies before demutualization. 4. Scope of the Research The data set for this study was obtained by analyzing demutualized stock exchanges that are members of the World Federation of Exchanges – that had been demutualized by year 2004 and have at least two years of both pre – and post demutualization data. As seen in the appendix, by end of 2004, the World Federation of Exchanges reported 26 demutualized stock exchanges3. Of these 26 demutualized stock 3 These include demutualized but not publicly listed exchanges and stock exchanges that demutualized and later become

publicly listed companies: Bolsa Mexicana de Valores, BME Spanish Exchanges, Bolsa de Valores de Colombia, Bourse de Montreal, Borsa Italiana, Budapest Stock Exchange Ltd., Bursa Malaysia, Copenhagen Stock Exchange, National Stock Exchange of India Limited, Oslo Borse, Taiwan Stock Exchange Corporation, Tokyo Stock Exchange, Wiener Borse, Athens Stock Exchange, Australian Stock Exchange, Bolsa de Comercio de Santiago, Bolsa de Valores de Lima,

International Research Journal of Finance and Economics - Issue 40 (2010) 45

exchanges, there were 13 stock exchanges that are also publicly listed exchanges. We add to this list OMX Helsinki Stock Exchange, which demutualized in 1995 and become part of OMX in 2003. The sample chosen to study each of the market measures depends on the availability of data in WFE statistics. For merged stock exchanges (Euronext and OMX), demutualization happened before the merger. Therefore it was better to study the impact of demutualization for these stock exchanges prior merger. Stock exchanges like Euronext Amesterdam, OMX Stockholm, OMX Copenhagen, OMX Helsinki stock exchanges were included in the analysis in their prior-merger form. The nature of availability of data allowed studying these cases before merger (OMX and Euronext) - with exception to ‘domestic market capitalization indicator’4. Pre and post – demutualization data were obtained from the World Federation of Exchanges. 5. Research Method 5.1. Research Method Used to Test the Hypotheses

The study employs a matched pair’s methodology in order to compare the pre - and post-demutualization performance measures of the exchanges. In order to investigate the impact of demutualization, the study calculates the mean of each variable for each of the market indicators, for at least two years before demutualization and the average two years after the demutualization. For all exchanges, the year of demutualization (year 0) includes both the member and cooperative (de-mutual) ownership phases of the exchange. Year 0 is thus excluded from the mean calculations.

The study then tests the null hypothesis for each of the market indicators that the difference in the two averages before and after demutualization is equal to, or less than zero. Under the null hypothesis, these test statistics follow a Student t-distribution if the sample is normally distributed. Given the fact that some variables are not normally distributed, an alternative technique is the non-parametric Wilcoxon signed-rank test will be employed. This procedure tests whether the median difference in variable values between the pre and post-demutualization samples is zero or less than zero. Conclusions are based on the standardized test statistic Z.

The condition for any stock exchange to be included in the sample is that at least two observations be available for each window; two before demutualization and two after demutualization.

In addition to the Wilcoxon test, the study also uses a proportion test to verify whether the proportion (p) of stock exchanges experiencing changes in a given direction is greater than what would be expected by chance (typically testing whether p = 0.05). Given the wide variance in countries and exchanges; finding that a large proportion of stock exchanges changed performance in the same direction may be at least as useful as a finding concerning the median change in performance.

The study uses common market measures for the size and liquidity of equity and bonds markets to measure change of performance post demutualization. Pre-demutualization data and post-demutualization data are typically obtained from the database of the World Federation of Exchanges.

Though the above mentioned methodology has not been used so far to measure the impact of the demutualization program on the performance of exchanges, the methodology has been used extensively in literature to study the impact of transferring a similar type of ownership structure of enterprises; the privatization program. There are varied literature studies that compare the performance of the privatized firms in the pre and post privatization period. Studies that measure the performance of privatized firms in the pre and post privatization period follow a very common approach; called MNR approach reference to the first study published using this methodology for Megginson et al, (1994). Examples of other studies that follow this approach5 include those of: Boubakri and Cosset (1998), D’Souza and Megginson (1999), Verbrugge et al (2000), Boubakri and Cosset (1999), Dewenter and

Deutsche Borse AG, Euronext, Hong Kong Exchanges and Clearing, London Stock Exchange, OMX Stockholm Stock Exchange, Osaka Securities Exchange, Philippine Stock Exchange, Singapore Exchange and, TSX Group (WFE Cost and Revenue Survey 2004).

4 Where data was only available for Euronext 5 In non transition economies (Megginson and Netter (2001))

46 International Research Journal of Finance and Economics - Issue 40 (2010)

Malatesta (2000), and Boardman, Laurin and Vining (2000). We follow the above mentioned approach to compare the market performance of demutualized stock exchanges in the pre and post demutualization period. We examine the market size and liquidity for the equity and bonds markets and market concentration – for the equity market. We had to eliminate the analysis of the derivative markets, because of the lack of reliable and consistent data across the exchanges. We use 16 market measures to test whether demutualization results in better market performance of stock exchanges, and we follow the definitions of the World Federation of Exchanges listed below6. 5.2. Market Measures

5.2.1. Market Size 5.2.1.1. Equity Market

• Domestic market capitalization: The market capitalization of a stock exchange is the total number of issued shares of domestic companies, including their several classes, multiplied by their respective prices at a given time. This figure reflects the comprehensive value of the market at that time. The market capitalization figures include shares of domestic companies, shares of foreign companies which are exclusively listed on an exchange; i.e. the foreign company is not quoted on any other exchange, common and preferred shares of domestic companies .The market capitalization figures exclude investment funds; rights, warrants, ETFs, convertible instruments, options, futures, foreign listed shares other than exclusively listed ones, and companies whose only business goal is to hold shares of other listed companies (WFE).

• Market capitalization of newly listed domestic shares: The market capitalization of newly listed domestic shares is the total number of new shares issued multiplied by their value on the first day of quotation (WFE).

• Total Number of listed companies: Number of companies which have shares listed on a specific exchange, split into domestic and foreign, excluding investment funds and unit trusts. A company with several classes of shares is counted just once (WFE).

• Number of trades in equity shares: The number of trades represents the actual number of transactions which have occurred during the period on the relevant Exchange. The number is single counted (i.e., includes one side of the transaction only) (WFE).

• Investment flows – new capital raised by shares: This is the amount of new capital raised through the sale of new shares issued by a new issuer (company) through an Initial Public Offering (IPO), capital increases by already listed companies (reserved to previous shareholders), and SPOs (new shareholders subscribe the shares) (WFE).

• Investment flows – new capital raised by shares / IPOs: The amount of Initial Public Offerings (IPO) represents the amount of money raised by shares issued by domestic companies entering the market (WFE).

6 Since raw data are obtained from WFE database.

International Research Journal of Finance and Economics - Issue 40 (2010) 47

5.2.1.2. Bonds Market • Number of bond issuers:

The total number of bond issuers represents the number of organizations which issued the fixed-income instruments listed on the exchange. These issuers are broken down into domestic private, public, and foreign entities. Domestic private bonds include corporate bonds, bonds issued by domestic banks and financial institutions. Domestic public bonds include government bonds and bills, state-related institutions whose instruments are guaranteed by the state, and municipal bonds. Foreign bonds listed on the exchange are issued by non-resident institutions: foreign governments, banks, financial institutions, supranational organizations (European Investment Bank (EIB), The European Bank for Reconstruction and Development (EBRD), World Bank …). They also include eurobonds (bonds issued under a law of a state different from the one of the issuer and placed in a foreign country inside the euro zone). An issuer may list bonds with different maturities, but the total number of issuers is unchanged (WFE).

• Number of bonds listed: Represents the number of bonds listed by the different categories of issuers, and split into domestic public bonds, domestic private bonds, and foreign bonds. A single issuer may list many securities with different maturities (WFE).

• Number of new bonds listed: This is the number of new bonds listed during a given year issued by the different categories of issuers, and split into domestic public bonds, domestic private bonds, and foreign bonds (WFE).

5.2.2. Liquidity 5.2.2.1. Equity Market

• Value of share trading: The value of share trading is the total number of shares traded multiplied by their respective matching prices. WFE distinguishes trading value of domestic and foreign shares, as well as investment funds. Investment funds are excluded from market capitalization to avoid double counting, but included in share trading to reflect the exchange’s entire share transaction business. Figures are single counted (only one side of the transaction is considered) (WFE).

• Average Value of Trades: The average value of trades during a given year is calculated by dividing the total value of share trading divided by the total number of trades in equity shares (WFE).

• Turnover velocity of domestic shares: The turnover velocity is the ratio between the turnover of domestic shares and their market capitalization. The value is annualized by multiplying the monthly moving average by 12, according to the following formula: (Monthly Domestic Share Turnover / Month-end Domestic Market Capitalization) * 12 Only domestic shares are used in order to be consistent. WFE calculates Turnover velocity in 2 steps:

o Step 1: calculate for each month the annualized ratio between the domestic share turnover and the domestic market capitalization, multiplied by 12;

o Step 2: add together, using a moving average methodology, the percentage ratios obtained in step 1, divided by 12.

5.2.2.2. Bonds Market

• Value of bonds listed: Data represent the number of bonds listed multiplied by their price at year-end.

• Value of bond trading:

48 International Research Journal of Finance and Economics - Issue 40 (2010)

The value of bonds trading value is the total number of bonds traded multiplied by their respective matching prices. The table indicates the value of bond trading split into domestic private, domestic public and foreign bonds. As WFE does for the value of share turnover, the value of bond trading is broken down into electronic order book trades and negotiated deals. Figures are single counted (WFE).

• Investment flows – new capital raised by bonds This represents the amount of capital raised through the sale of bonds issued by a new or existing issuer during the reporting period (WFE).

5.2.3. Market Concentration In some countries a few companies dominate the market (Ibid. p.8). To measure the degree of market concentration in equity market, the study considers market concentration of the 5 percent most capitalized and most traded companies. This information is given in percentage. 5.2.4. Control Analysis In addition, to better understand the magnitude of observed initial and aftermath market performance for the demutualized stock exchanges, we conduct several panel regressions to identify the significance of selected exogenous variables (independent variables) which are the size of the stock exchange, its growth, leverage and age on return on assets and return on equity for the stock exchange (dependent variable).

These explanatory variables other than demutualization might play an important role in determining the financial and market performance for the exchange. The study will estimate the following simple regressions to examine the effect of other factors than demutualization on the stock exchange ROA and ROE after demutualization. This will help to control for the effects of these factors.

У = α + β1 χ1 (1) У = α + β2 χ2 (2) У = α + β3 χ3 (3) У = α + β4 χ4 (4) Where, У = ROA or ROE for the stock exchange χ1 = Size of the stock exchange Size is commonly identified by the market value of equity and the book value of assets. The

study calculates the average market value of equity and average book value of assets respectively and then takes the natural logarithm of these average values. The natural logarithm is used to scale down the high values of the size measures and is used by most researchers.

χ2 = Growth The research considers the growth in assets. Growth in assets = (assets of the current year /

assets of the previous year) - 1. Growth of the stock exchange can also be measured in terms of growth of transactions. Growth in assets is however a better measure for the growth of the exchange.

χ3 = Leverage Leverage measures how much of the firm’s total assets are financed by debt or equity. The

most commonly leverage measures used are the debt / equity ratio and the debt / asset ratio. The study calculates leverage as Debt / Equity.

χ4 = Age of the stock exchange Age of the stock exchange is the number of years since the stock exchange was founded. In each regression analysis, we examine: • R2; which – as a percentage represents the percentage of the variation in the outcome that

can be explained by the model (Field 2003). • The F-test. This test is based on the ratio of the improvement due to the model and the

difference between the model and the observed data. F = MSM / MSR. If the model is

International Research Journal of Finance and Economics - Issue 40 (2010) 49

good, then we expect the improvement in prediction due to the model to be large7 (greater than 1 at least) (Ibid.).

• Beta value: provides the change in the outcome associated with a unit change in the predictor

• The t-statistic tests the null hypothesis that the value of ß is zero: therefore, if it is significant we accept the hypothesis that ß value is significantly different from zero (Ibid.).

• If the t-statistic is very large, then it is unlikely to have occurred by chance. As a general rule, if this observed significance is less than 0.05, then the result reflects a genuine effect (Ibid.).

6. Empirical Results We present in this section the empirical findings of the performance changes in variables described in the section 5. The analysis is based on the results of the Wilcoxon signed-rank and the proportion tests. The analysis considers various samples of demutualized stock exchanges8. Performance change results are presented for each sample. Two techniques are employed to test for the significant changes in performance of demutualized stock exchanges. The Wilcoxon signed-rank test is employed to test for the significant changes in median values. The proportion test is employed to determine whether the proportion of demutualized stock exchanges experiencing changes in a given direction is greater than what would be expected by chance. The mean (median) value of each variable is provided for the pre- and post-demutualization period, the mean (median) change for each variable after versus before demutualization, Z statistics with their significance levels, and the number of useable stock exchanges. The percentage of demutualized stock exchanges that changed as predicted with Z statistics and their significance levels are provided. For the Wilcoxon signed-rank test, the results are listed under the null hypothesis that the median change is less than or equal zero and the alternative hypothesis that the median change is greater than zero. This is valid for all variables except for market concentration variable; where the null hypothesis is that the median is greater than or equal zero and the alternative hypothesis is that median is less than zero. The results of changes in performance for the whole sample for each variable are presented in table 1.

7 Mean Squares for the model (MSM) will be large, and the difference between the model and the observed data to be small

(so, the residual mean squares (MSR) will be small) 8 Depending on the availability of data for demutualized stock exchanges in WFE’s database

50 International Research Journal of Finance and Economics - Issue 40 (2010)

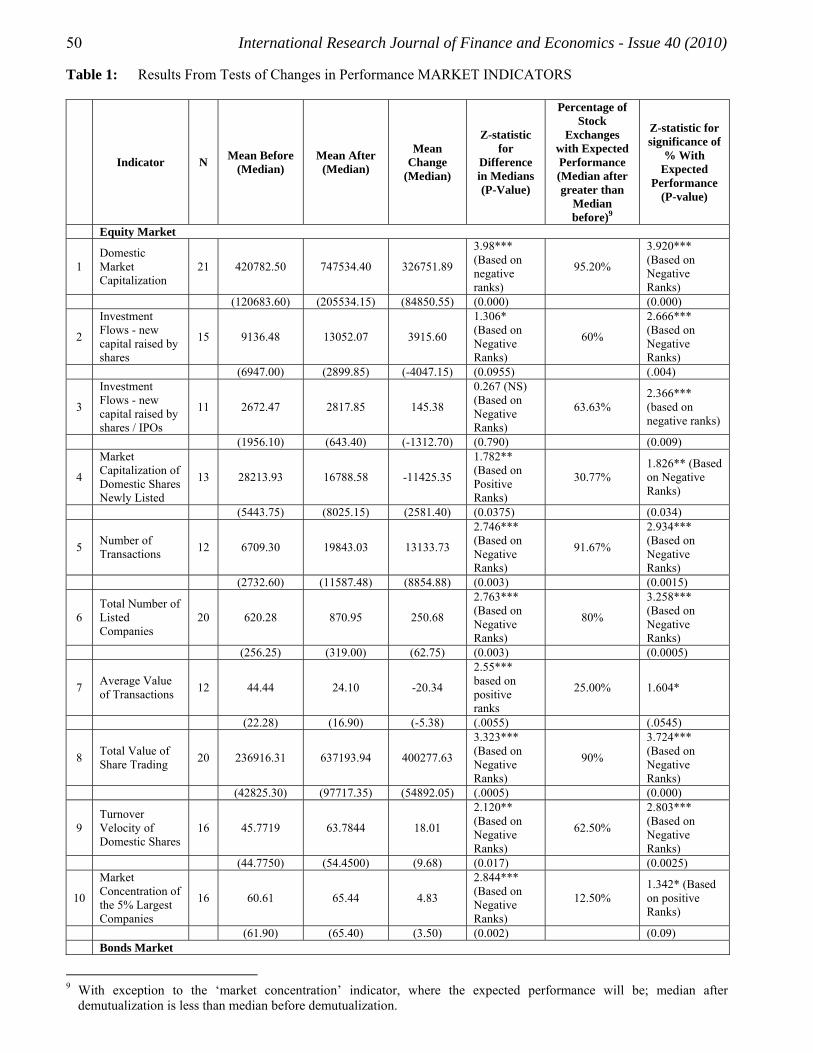

Table 1: Results From Tests of Changes in Performance MARKET INDICATORS

Indicator N Mean Before (Median)

Mean After (Median)

Mean Change

(Median)

Z-statistic for

Difference in Medians (P-Value)

Percentage of Stock

Exchanges with Expected Performance (Median after greater than

Median before)9

Z-statistic for significance of

% With Expected

Performance (P-value)

Equity Market

1 Domestic Market Capitalization

21 420782.50 747534.40 326751.89

3.98*** (Based on negative ranks)

95.20%

3.920*** (Based on Negative Ranks)

(120683.60) (205534.15) (84850.55) (0.000) (0.000)

2

Investment Flows - new capital raised by shares

15 9136.48 13052.07 3915.60

1.306* (Based on Negative Ranks)

60%

2.666*** (Based on Negative Ranks)

(6947.00) (2899.85) (-4047.15) (0.0955) (.004)

3

Investment Flows - new capital raised by shares / IPOs

11 2672.47 2817.85 145.38

0.267 (NS) (Based on Negative Ranks)

63.63% 2.366*** (based on negative ranks)

(1956.10) (643.40) (-1312.70) (0.790) (0.009)

4

Market Capitalization of Domestic Shares Newly Listed

13 28213.93 16788.58 -11425.35

1.782** (Based on Positive Ranks)

30.77% 1.826** (Based on Negative Ranks)

(5443.75) (8025.15) (2581.40) (0.0375) (0.034)

5 Number of Transactions 12 6709.30 19843.03 13133.73

2.746*** (Based on Negative Ranks)

91.67%

2.934*** (Based on Negative Ranks)

(2732.60) (11587.48) (8854.88) (0.003) (0.0015)

6 Total Number of Listed Companies

20 620.28 870.95 250.68

2.763*** (Based on Negative Ranks)

80%

3.258*** (Based on Negative Ranks)

(256.25) (319.00) (62.75) (0.003) (0.0005)

7 Average Value of Transactions 12 44.44 24.10 -20.34

2.55*** based on positive ranks

25.00% 1.604*

(22.28) (16.90) (-5.38) (.0055) (.0545)

8 Total Value of Share Trading 20 236916.31 637193.94 400277.63

3.323*** (Based on Negative Ranks)

90%

3.724*** (Based on Negative Ranks)

(42825.30) (97717.35) (54892.05) (.0005) (0.000)

9 Turnover Velocity of Domestic Shares

16 45.7719 63.7844 18.01

2.120** (Based on Negative Ranks)

62.50%

2.803*** (Based on Negative Ranks)

(44.7750) (54.4500) (9.68) (0.017) (0.0025)

10

Market Concentration of the 5% Largest Companies

16 60.61 65.44 4.83

2.844*** (Based on Negative Ranks)

12.50% 1.342* (Based on positive Ranks)

(61.90) (65.40) (3.50) (0.002) (0.09) Bonds Market

9 With exception to the ‘market concentration’ indicator, where the expected performance will be; median after

demutualization is less than median before demutualization.

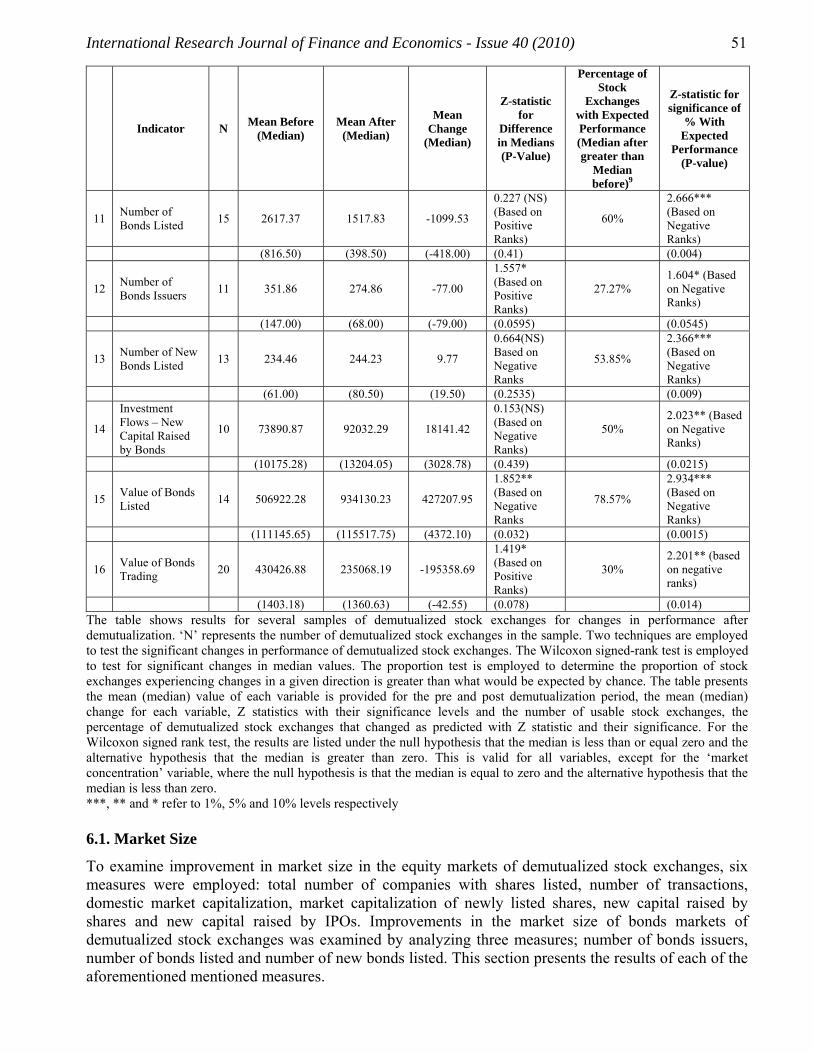

International Research Journal of Finance and Economics - Issue 40 (2010) 51

Indicator N Mean Before (Median)

Mean After (Median)

Mean Change

(Median)

Z-statistic for

Difference in Medians (P-Value)

Percentage of Stock

Exchanges with Expected Performance (Median after greater than

Median before)9

Z-statistic for significance of

% With Expected

Performance (P-value)

11 Number of Bonds Listed 15 2617.37 1517.83 -1099.53

0.227 (NS) (Based on Positive Ranks)

60%

2.666*** (Based on Negative Ranks)

(816.50) (398.50) (-418.00) (0.41) (0.004)

12 Number of Bonds Issuers 11 351.86 274.86 -77.00

1.557* (Based on Positive Ranks)

27.27% 1.604* (Based on Negative Ranks)

(147.00) (68.00) (-79.00) (0.0595) (0.0545)

13 Number of New Bonds Listed 13 234.46 244.23 9.77

0.664(NS) Based on Negative Ranks

53.85%

2.366*** (Based on Negative Ranks)

(61.00) (80.50) (19.50) (0.2535) (0.009)

14

Investment Flows – New Capital Raised by Bonds

10 73890.87 92032.29 18141.42

0.153(NS) (Based on Negative Ranks)

50% 2.023** (Based on Negative Ranks)

(10175.28) (13204.05) (3028.78) (0.439) (0.0215)

15 Value of Bonds Listed 14 506922.28 934130.23 427207.95

1.852** (Based on Negative Ranks

78.57%

2.934*** (Based on Negative Ranks)

(111145.65) (115517.75) (4372.10) (0.032) (0.0015)

16 Value of Bonds Trading 20 430426.88 235068.19 -195358.69

1.419* (Based on Positive Ranks)

30% 2.201** (based on negative ranks)

(1403.18) (1360.63) (-42.55) (0.078) (0.014) The table shows results for several samples of demutualized stock exchanges for changes in performance after demutualization. ‘N’ represents the number of demutualized stock exchanges in the sample. Two techniques are employed to test the significant changes in performance of demutualized stock exchanges. The Wilcoxon signed-rank test is employed to test for significant changes in median values. The proportion test is employed to determine the proportion of stock exchanges experiencing changes in a given direction is greater than what would be expected by chance. The table presents the mean (median) value of each variable is provided for the pre and post demutualization period, the mean (median) change for each variable, Z statistics with their significance levels and the number of usable stock exchanges, the percentage of demutualized stock exchanges that changed as predicted with Z statistic and their significance. For the Wilcoxon signed rank test, the results are listed under the null hypothesis that the median is less than or equal zero and the alternative hypothesis that the median is greater than zero. This is valid for all variables, except for the ‘market concentration’ variable, where the null hypothesis is that the median is equal to zero and the alternative hypothesis that the median is less than zero. ***, ** and * refer to 1%, 5% and 10% levels respectively 6.1. Market Size

To examine improvement in market size in the equity markets of demutualized stock exchanges, six measures were employed: total number of companies with shares listed, number of transactions, domestic market capitalization, market capitalization of newly listed shares, new capital raised by shares and new capital raised by IPOs. Improvements in the market size of bonds markets of demutualized stock exchanges was examined by analyzing three measures; number of bonds issuers, number of bonds listed and number of new bonds listed. This section presents the results of each of the aforementioned mentioned measures.

52 International Research Journal of Finance and Economics - Issue 40 (2010)

6.1.1. Equity Market 6.1.1.1. Results of H2 on Total Number of Listed Companies: Data on the total number of listed companies come from World Federation of Exchanges annual reports and represents number of companies which have shares listed on a specific exchange, split into domestic and foreign, excluding investment funds and unit trusts. A company with several classes of shares is counted just once. A company is considered foreign when it is incorporated in a country other than that where the exchange is located (WFE Annual Report 2007).

The results of the wilcoxon signed rank test and the proportion tests for a sample of 20 demutualized stock exchanges show that total number of listed companies had significantly improved in the post demutualization period. Both the statistical tests (the Z statistic for difference in medians of the whole sample and the Z statistic for significance of the percentage with expected performance) pass the critical value of significance at one percent level. The increase in total number of listed companies is equally significant at one percent level for 70% of the sample demutualized stock exchanges under study. 6.1.1.2. Results of H3 on Number of Transactions in Equity Shares Table 1 shows that the number of transactions improves significantly after demutualization. The mean (median) for a sample of 12 demutualized stock exchanges jump from 6709.3 (2732.6) to 19843.03 (11587.48). Both statistical tests pass the critical values of significance at one percent level. The increase in the number of transactions is equally significant for 91.67 percent of the sample stock exchanges. 6.1.1.3. Results of H4 on Domestic Market Capitalization Domestic market capitalization of a stock exchange represents the total number of issued shares of domestic companies, including their several classes, multiplied by their respective prices at a given time. This figure reflects the comprehensive value of the market at that time (WFE). Domestic market capitalization is an indication of the size and performance of stock markets, and therefore the importance of private investor capital in the economy. Table 1 shows that domestic market capitalization increases after demutualization, and that this improvement is significant at the one percent level under both statistical measures. The mean & (median) increase from 420782.5 (120683.6) in the pre-demutualization period to 747534.4 (205534.15) in the post-demutualization period, and 95.2 % of the stock exchanges in the sample changed as predicted and increased after demutualization. 6.1.1.4. Results of H5 on Market Capitalization of Newly Listed Shares In contrast to the results of domestic market capitalization, market capitalization of domestic shares newly listed for a whole sample of 13 demutualized stock exchanges, has significantly decreased in the after demutualization period; at five percent level. Only about one third of the whole sample has the post-demutualization market capitalization of newly listed shares higher than the pre-demutualization level; with five percent significance level. 6.1.1.5. Results of H6 on New Capital Raised by Shares A sample of 15 demutualized stock exchanges were examined for changes in this measure. Both the wilcoxon and the proportion tests show that new capital raised by shares, increases significantly after the demutualization period; at ten percent level. About 60% of the sample has changed as predicted by the research hypothesis. The increase in this percentage changed is significant at one percent level. 6.1.1.6. Results of H7 on New Capital Raised by IPOs Though median change results for the new capital raised by IPOs is higher in the post-demutualization period; it is not significant.

International Research Journal of Finance and Economics - Issue 40 (2010) 53

6.1.2. Bonds Market 6.1.2.1. Results of H8 on Number of Bonds Issuers The total number of bonds issuers represents the number of organizations which issued the bonds instruments listed on the exchange. These issuers are broken down into domestic private, public, and foreign entities. In general, stock exchanges expect an increase in the number of bonds issuers following demutualization. Therefore, we make our prediction and we examine it by testing whether the number of bonds issuers increased after demutualization. Results show that for a sample of 11 demutualized stock exchanges, there is a decrease in the number of bonds issuers of 77 (79); from 351.86 (147.00) to 274.86 (68.00). The proportion test indicates that this decline is significant at 10 percent. Only 27.27 percent of the demutualized stock exchanges in the sample changed as predicted and showed an increase in the number of bonds issuers; at 10 percent significance level. 6.1.2.2. Results of H9 on Number of Bonds Listed By examining changes in the number of bonds listed for a sample of 15 stock exchanges, we find that for the sample, both the mean and the median values decrease in the post demutualization period; from 2617.37 (816.5) to 1517.83 (398.5). The wilcoxon and proportion tests both show that this decrease is not significant at any of the required levels. About 60% of the sample have changed as predicted and experienced an increase in medians. 6.1.2.3. Results on H10 on Number of New Bonds Listed We also study whether or not the number of new bonds listed during a given year issued by the different categories of issuers has increased. Both the mean and median values increase after demutualization; from 234.46 (61) to 244 (80.5). However, this increase is not significant at any of the required probability levels. About 54 percent of the whole sample has changed as predicted by the research hypothesis; at one percent level. 6.2. Liquidity

6.2.1. Equity Market 6.2.1.1. Results on H11 on Average Value of Transactions The average value of trades during a given year is calculated by dividing the total value of share trading by the total number of trades in equity shares. Results of a sample of 12 stock exchanges tell that both the mean and median changes decrease in the post demutualization period. Both the wilcoxon and proportion tests support this change and indicate its significance at one percent level. Only 25% of the sample have changed as predicted and showed significant increase in the after demutualization period (only at 10 percent level). 6.2.1.2. Results on H12 on Total Value of Share Trading The value of share trading defined as the total number of shares traded multiplied by their respective matching prices has increased significantly after demutualization. Both the wilcoxon and the proportion tests for the whole sample and for the percentage with expected performance show this increase at one percent level (table 1). 6.2.1.3. Results on H13 on Turnover Velocity of Domestic Shares The turnover velocity is as the ratio between the turnover of domestic shares and their market capitalization. WFE annualizes this value by multiplying the monthly moving average by 12, according to the following formula: (Monthly Domestic Share Turnover / Month-end Domestic Market Capitalization) * 12. We find that this indicator increase significantly after demutualization. Both the wilcoxon and the proportion tests show this increase at 5 percent level. The median values of 62.5 percent of the sample demutualized stock exchanges have increased significantly in the post – demutualization period.

54 International Research Journal of Finance and Economics - Issue 40 (2010)

6.2.2. Bonds Market 6.2.2.1. Results of H14 on Value of Bonds Listed Value of bonds listed represent the number of bonds listed multiplied by their price at year-end. From table 1, we find that this indicator improves significantly after demutualization. Both the mean and median values of a sample of 14 demutualized stock exchanges increased significantly in the post demutualization period. The wilcoxon and proportion tests show this increase at 5 percent significance level. The increase in the value of bonds listed is equally significant at one percent level for 78.57 percent of the sample stock exchanges. 6.2.2.2. Results of H15 on - Investment Flows – Capital Raised by Bonds Both the mean and median values of a sample of 10 demutualized stock exchanges increase in the post-demutualization period. However, the wilcoxon and proportion tests show that this increase is not significant at any of the required probability levels. 50 percent of the sample increased in the post demutualization period as predicted by the research hypothesis (median after demutualization is greater than median before demutualization) and this increase is significant at five percent level.

6.2.2.3. Results on H16 on Value of Bonds Trading The bond trading value is the total number of bonds traded multiplied by their respective matching prices. This includes domestic private, domestic public and foreign bonds. Results of the wilcoxon and proportion tests of a complete sample of 20 demutualized stock exchanges show that there is a significant decrease in the value of bonds trading; at one percent level. Only 30 percent of the sample has changed as predicted and has the median values the values of bonds trading increased after demutualization; at five percent level. 6.3. Market Concentration

6.3.1. Results on H17 on Market Concentration of the 5 percent largest companies In order to measure the degree of market concentration, the study considers market concentration of the 5 percent most capitalized and most traded companies. Most of the stock exchanges in the sample have exhibited a highly significant increase in market concentration in the post demutualization period; at one percent level. 6.4. Results on the Major Research Hypothesis (H1) on the Impact of Demutualization on the Market Performance of the Equity and Bonds Markets of Demutualized Stock Exchanges Our findings indicate that about 43.75% of the market measures have significantly improved after demutualization. The research hypothesis is supported in the case of H2, H3, H4, H6, H12, H13 and H14; related to total number of listed companies, number of transactions in equity shares, domestic market capitalization, new capital raised by shares, total value of share trading, turnover velocity of domestic shares and value of bonds listed. The results of the remaining market measures doe not support their research hypothesis. Therefore, our evidence suggests that stock exchange demutualization does not appear to improve the market performance of the bonds and equity markets of demutualized stock exchanges. 6.5. Results of the Control Analysis

We run several regressions to figure out the significance of selected exogenous variables (independent variables) which are the size of the stock exchange, its growth, leverage and age on return on assets and return on equity for the stock exchange (dependent variables). We found out that for all regressions of the four independent variables that were conducted on return on assets (ROA) and return on equity (ROE), the p-values are so large, which make us conclude that the results do not reflect genuine effect. The regression models result in bad predictions of ROA and ROE.

International Research Journal of Finance and Economics - Issue 40 (2010) 55

6.6. Limitations

The findings of this study need to be read and interpreted with an understanding of the following caveats:

a. To guarantee the consistency and availability of the data, the analysis is limited to demutualized stock exchanges that are members of the World Federation of Exchanges (WFE). Data are derived from WFE database and annual reports.

b. Because data were driven from WFE, we stick to WFE definition of demutualized exchanges and we include those stock exchanges that are classified as demutualized by WFE10.

c. Because the methodology of the study needs 2-3 years in the after demutualization period, and because we want to exclude year 2008 from the analysis due to the international financial crisis that affected the performance of stock exchanges, we analyze those stock exchanges that demutualized in or before 2004. As of 2004, there were a total of 26 demutualized stock exchanges that are members of WFE.

d. For merged stock exchanges (Euronext and OMX), demutualization happened before the merger. Therefore it was better to study demutualized stock exchanges prior merger. Stock exchanges like Euronext Amesterdam, OMX Stockholm, OMX Copenhagen, OMX Helsinki stock exchanges were included in the analysis in their prior-merger form. The nature of availability of data allowed studying these cases before merger (OMX and Euronext) - with exception to ‘domestic market capitalization indicator’11.

7. Conclusion This study analyzes and evaluates the market performance of demutualized stock exchanges that demutualized between 1993 and 2004. We examine whether or not their market performance improved after implementing the demutualization program. We focus on market size and liquidity for the equity and bonds market in addition to market concentration of the 5 % largest companies in the equity market.

Market size of equity markets that have undergone the demutualization program has been measured in terms of six measures; total number of companies with shares listed, number of transactions, domestic market capitalization, market capitalization of newly listed shares, new capital raised by shares and new capital raised by IPOs. Results are mixed and exhibit different change in performance for the samples of demutualized stock exchanges.

We find that four out of the six measures show high significance for improvement after demutualization and support the research hypothesis. Three indicators; total number of listed companies, number of transactions and domestic market capitalization have significantly improved after demutualization at 1 percent level. The fourth indicator; new capital raised by shares has also increased after demutualization, but at 10 percent level.

The remaining two indicators used to test market size of equity markets do not support the research hypothesis. Market capitalization of domestic shares newly listed, exhibits a significant decrease (at 5 percent level) in the post-demutualization period. And, though new capital raised by shares exhibits improvement after demutualization; this improvement is not significant at any of the required significance levels12.

In terms of the percentage of firms that changed as predicted by the research hypothesis and their significance levels. For all the six measures of market size of the equity market , the Z statistic of the percentage with expected performance pass the critical values of significance at 1 and 5%. The

10 We add to this list OMX Helsinki Stock Exchange, which demutualized in 1995 and become part of OMX in 2003. 11 Where data was only available for Euronext 12 1, 5 and 10 percent levels

56 International Research Journal of Finance and Economics - Issue 40 (2010)

increase in all the six measures is significant as low as 30.77 percent and as high as 95.20 percent of the sample stock exchanges.

For improvements in size of the demutualized bonds markets; we use three measures: number of bonds listed, number of new bonds listed and, number of bonds issuers. Results show that the number of bonds listed and the number of bonds issuers decrease in the post-demutualization period. Though this decline is insignificant in the case of number of bonds listed, it is significant for the number of bonds issuers at 10 percent. The median value of the number of new bonds listed increases in the post-demutualization period, but this increase is not significant for the whole sample at any of the required probability levels.

As for the impact of the post demutualization structure on the liquidity of stock exchange, we employed three measures for liquidity change in the equity market: value of share trading, average value of transactions and turnover velocity of domestic shares. Results are mixed. We note a high significant improvement; at one percent level for two of these indicators; total value of share trading and turnover velocity of domestic shares. On the contrary, average value of transactions has decreased significantly after demutualization; at one percent level.

In the bonds market, three measures were employed to study changes in liquidity; value of bonds listed, value of bonds trading and new capital raised by bonds. It is evident that value of bonds listed increased significantly after demutualization; at 5 percent level. The new capital raised by bonds also increased, but this increase is not significant at any of the required probability levels. Against these results, value of bonds trading significantly decreased after demutualization at 10 percent probability level.

We also find out that market concentration of the 5% largest companies increases significantly after demutualization; at one percent level; A fact that leads us to fail to reject the null hypothesis.

Our findings indicate that only about 43.75% of the market measures have significantly improved after demutualization. The research hypothesis is only supported in the case of H2, H3, H4, H6, H12, H13 and H14; related to total number of listed companies, number of transactions in equity shares, domestic market capitalization, new capital raised by shares, total value of share trading, turnover velocity of domestic shares and value of bonds listed. The results of the remaining market measures doe not support their research hypothesis. Our evidence suggests that stock exchange demutualization does not appear to improve the market performance of the bonds and equity markets of demutualized stock exchanges. We recommend that this study be replicated after couple of years. From a broader perspective, we note that there are several market measures that improved after demutualization, but their improvement is not significant. With longer time periods under investigation, the impact of demutualization will be clearer.

International Research Journal of Finance and Economics - Issue 40 (2010) 57

References [1] Aggarwal, R., 2002. “Demutualization and Corporate Governance of Stock Exchanges”,

Journal of Applied Corporate Finance, Vol.15, No.1, pp.105 -113. [2] Boubakri, N. and J-C. Cosset, 1998. “The Financial and Operating Performance of Newly

Privatized Firms: Evidence from Developing Countries”, Journal of Finance, Vol. 53, pp.1081-1110.

[3] Boubakri, N. and J-C. Cosset, 1999. “Does Privatization Meet the Expectations? Evidence from African Countries”, Working Paper, Monteral: Ecole des HEC.

[4] Boardman, A., C., Laurin and A., Vining, 2000. “Privatization in Canada: Operating, Financial and Stock Price Performance with International Comparisons”, Working Paper, University of British Columbia, Vancouver.

[5] Elliott, J., 2002. “Demutualization of Securities Exchanges: A Regulatory Perspective”, IMF Working Paper, WP/02/119, International Monetary Fund.

[6] D’Souza, J., W., Megginson, 1999. “The Financial and Operating Performance of Newly Privatized Firms in the 1990s”, Journal of Finance, Vol., pp. 54, 1397.

[7] Dewenter, K. and P., Malatesta, 2000. “State-owned and privately-owned firms: An empirical analysis of profitability, leverage, and labour intensity”, American Economic Review.

[8] Field, A., 2003. Discovering Statistics Using SPSS for Windows (London: Sage Publications Ltd.)

[9] Hazarika, S., 2005. “Governance Change in Stock Exchanges”, Working Paper, Baruch College, City University, New York.

[10] Hughes, P. and E. Zargar, 2006. “Exchange Demutualization”, Blake, Cassels and Graydon LLP.

[11] International Organization for Securities Commissions, 2000. IOSCO Discussion Paper on Stock Exchange Demutualization.

[12] IOMA/IOCA. Annual Meeting, Chicago 10-13 April 2005. In Annual Report and Statistics 2005, World Federation of Exchanges (WFE), 15-16.

[13] Krishnamurti, C., J. Sequeira and F. Fangjian, 2003. “Stock Exchange Governance and Market Quality”, Journal of Banking and Finance, Vol. 27, No. 9, 1859-1878

[14] Lee, R., 2002. “The Future of Securities Exchanges”, Working Paper – the Wharton Financial Institutions Centre at Wharton School.

[15] Lucy, J., 2004. “Market demutualization and privatisation: The Australian experience”, International Organization of Securities Commission (IOSCO), Amman 2004 Annual Conference.

[16] Megginson, W. and J., Netter, 2001. “From State to Market: A Survey of Empirical Studies on Privatization”, Journal of Economic Literature, Vol. 39, issue 2321-2390.

[17] Megginson, W., R. Nash and M., Randenborgh, 1994. “The Financial and Operating Performance of Newly Privatized firms: An International Empirical Analysis”, Journal of Finance, Vol. XLIX, No. 2, 403-452.

[18] Mendiola, A. and M., O’Hara, 2004. “Taking stock in stock markets: the changing governance of exchanges”, Working Paper, Cornell University.

[19] Schmiedel, H., 2001. “Technological Development and concentration of stock exchanges in Europe”, Bank of Finland Discussion Paper, 21.

[20] Schmiedal, H., 2002. “Total Factor Productivity Growth in European Stock Exchanges: A non-parametric Frontier Approach”, Discussion Paper II, Bank of Finland.

[21] Serifsoy, B., 2005. “Demutualization, outsider ownership and stock exchange performance: empirical evidence”. Goethe University Frankfurt Working Paper Series: Finance & Accounting.

[22] Steil, B., 2002. “Changes in the Ownership Structure of Securities Exchanges: Causes and Consequences”, Brookings-Wharton Papers on Financial Services, 61-91.

58 International Research Journal of Finance and Economics - Issue 40 (2010)

[23] Treptow, F. 2006. The Economics of Demutualization: An Empirical Analysis of the Securities Exchange Industry (Wiesbaden: Deutscher Universitaets-Verlag).

[24] Verbrugge, J., W. Megginson and W. Owens, 1999. “State Ownership and the Financial Performance of Privatized Banks: An Empirical Analysis”, Conference Proceedings of a Policy Research Workshop Held at the World Bank, March 15-16, 1999, Dallas: Federal Research Bank of Dallas.

[25] World Federation of Exchanges (WFE), Annual Report and Statistics 2005. [26] World Federation of Exchanges (WFE), Annual Report and Statistics 2007. [27] World Federation of Exchanges, World Federation of Exchanges Cost and Revenue Survey