The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. FEBRUARY 2014 AMISLAMIC BANK BERHAD Financial Institution Ratings Proposed RM3 billion Subordinated Sukuk Murabahah Programme RM2 billion Subordinated Sukuk Musharakah Programme (2011/2026) RM3 billion Senior Sukuk Musharakah Programme (2010/2040)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the security’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings.

FEBRUARY 2014

AMISLAMIC BANK BERHAD

Financial Institution Ratings

Proposed RM3 billion Subordinated Sukuk Murabahah

Programme

RM2 billion Subordinated Sukuk Musharakah Programme

(2011/2026)

RM3 billion Senior Sukuk Musharakah Programme

(2010/2040)

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the security’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings.

CREDIT RATING RATIONALE

FINANCIAL INSTITUTION RATINGS

FEBRUARY 2014

AMISLAMIC BANK BERHAD

– Initial Rating and Rating Update

Summary

RAM Ratings has assigned a final AA3/Stable rating to AmIslamic Bank Berhad’s

(the Bank) proposed RM3 billion Subordinated Sukuk Murabahah Programme

(the Proposed Sukuk Programme). At the same time, we have reaffirmed

AmIslamic’s financial institution ratings at AA2/Stable/P1. The long-term ratings of

the Bank’s RM2 billion Subordinated Sukuk Musharakah Programme

(2011/2026) and RM3 billion Senior Sukuk Musharakah Programme (2010/2040)

have also been reaffirmed at AA3/Stable and AA2/Stable, respectively.

The financial institution ratings of AmIslamic reflect its strategic importance as

AMMB Holdings Berhad’s (AmBank Group, rated AA3/Stable/P1) Islamic banking

arm and the Bank’s highly integrated operations with its sister bank, AmBank (M)

Berhad (AmBank, rated AA2/Stable/P1) under a universal-banking platform.

AmIslamic leverages on AmBank’s risk-management systems, infrastructure,

extensive branch network and channels.

AmIslamic remains focused on automobile financing, which makes up the lion's

share of the Bank's financing portfolio. The Bank’s gross impaired-financing (GIF)

ratio showed an uptick as at end-September 2013, mainly due to the impairment

of a lumpy credit and the seasoning impact on its automobile financing portfolio

following rapid growth. However, we note that its GIF ratio of 1.5% compares

favourably with the industry average of 2.0%. The Bank’s credit-cost ratio has

been also easing in the last few years, supported by strong recoveries; this ratio

came up to an annualised 0.7% in 1H FY Mar 2014.

On the funding front, AmIslamic remains exposed to depositor-concentration risk.

We, however, draw comfort from the expected liquidity support from AmBank

Group if the need arises. As at end-September 2013, AmIslamic's common-

equity tier-1 and total capital ratios stood at a healthy 10.0% and 15.1%,

respectively.

For more details, please refer to RAM’s rating rationale on AmIslamic published

Analysts: Cheryl Yong (603) 7628 1072 [email protected] Gladys Chua (603) 7628 1049 [email protected]

Principal Activity: Islamic banking Financial Institution Ratings: AA2/Stable/P1 [Reaffirmed] Instruments: (i) Proposed RM3 billion

Subordinated Sukuk Murabahah Programme

(ii) RM2 billion Subordinated Sukuk Musharakah Programme (2011/2026)

(iii) RM3 billion Senior Sukuk Musharakah Programme (2010/2040)

Issue Ratings: (i) AA3/Stable [Assigned] (ii) AA3/Stable [Reaffirmed] (iii) AA2/Stable [Reaffirmed] Islamic Contracts: (i) Murabahah (via a

Tawarruq arrangement) (ii) Musharakah (iii) Musharakah Maturity Dates: (i) 30 years from first

issuance (ii) 30 September 2026 (iii) 20 September 2040 Lead Arranger: AmInvestment Bank Berhad

Last Rating Action: 12 February 2014

AmIslamic Bank Berhad 2

on 29 November 2013.

Rating Approach

The sukuk to be issued under the Proposed Sukuk Programme are Basel III-

compliant and will receive Tier 2 regulatory capital treatment. In addition to a

subordinated ranking in the priority of claims in the event of bankruptcy or

liquidation, the sukuk also have a non-viability loss-absorption feature that may

cause the outstanding principal and any other amounts owed to be written-off

following the occurrence of a non-viability event.

Compared to existing Basel II subordinated debts issued by Malaysian banks,

the inclusion of the additional non-viability term would not necessitate additional

downward notching adjustments from RAM’s current approach to rating Basel II

Tier 2 capital instruments. RAM views the likelihood of a bank being non-viable

as sufficiently reflected in its long-term financial institution rating. Our view takes

into account RAM’s interpretation of circumstances that will constitute a non-

viability event, as articulated by Bank Negara Malaysia (BNM) in its Capital

Adequacy Framework for Islamic Banks on Capital Components. For further

details on our rating approach, please refer to our methodology paper, Rating

Bank Securities (published in November 2013), available at www.ram.com.my.

The sukuk to be issued under the Proposed Sukuk Programme are rated one

notch below AmIslamic’s long-term financial institution rating, reflecting the lower

ranking in the priority of claims upon bankruptcy or liquidation, relative to senior

unsecured creditors.

Proposed Subordinated Sukuk Programme

The Proposed Sukuk Programme will have a programme limit of RM3 billion and

tenure of 30 years from the date of the first issuance. Each issuance of the

Proposed Sukuk Programme may have tenure of at least 5 years from the issue

date subject to the call option which allow the Bank to redeem the securities on

any periodic profit payment date after a minimum period of 5 years from the date

of the tranche issuance. The Proposed Sukuk Programme applies the underlying

Shariah contract of Murabahah.

The sukuk to be issued under the Proposed Sukuk Programme will have a non-

viability loss-absorption feature which will be activated upon the occurrence of a

non-viability event. A non-viability event is the earlier of the following:

(i) BNM and Malaysia Deposit Insurance Corporation (PIDM) notify

AmIslamic writing that BNM and PIDM are of the opinion that a write-off

is necessary, without which AmIslamic would cease to be viable; or

AmIslamic Bank Berhad 3

(ii) BNM and PIDM publicly announce that a decision has been made by

BNM, PIDM, or any federal or state government in Malaysia, to provide

capital injections or equivalent support to AmIslamic, without which

AmIslamic would cease to be viable.

Upon the occurrence of a non-viability event, BNM shall have the option to

require the entire outstanding principal (or such portion thereof) and all other

amounts owing under the Proposed Sukuk Programme to be written off. This

write-off will not constitute an event of default or trigger cross-default clauses.

AmIslamic Bank Berhad 4

Corporate Information – AmIslamic Bank Berhad

Date of Incorporation:

14 April 1994

Commencement of Business:

1 May 2006 (as an Islamic banking subsidiary)

Major Shareholders (as at 30 September 2013):

AMMB Holdings Berhad

100%

Directors:

Tan Sri Azman Hashim (Chairman) Tun Mohammed Hanif Omar Tan Sri Datuk Clifford Francis Herbert Dato’ Larry Gan Nyap Liou @ Gan Nyap Liow Loh Chen Peng Chin Yuen Yin Cheah Tek Kuang Ashok Ramamurthy

Auditor:

Ernst & Young

Listing:

Not Listed

Key Management:

Ashok Ramamurthy Datuk Mohamed Azmi Mahmood Paul Lewis Dato’ James Lim Cheng Poh Kok Tuck Cheong Pushparani Rajadurai Mandy Simpson Nigel Denby Ross Neil Foden Datuk Mahdi Murad Tan Chin Aun

Group Managing Director Deputy Group Managing Director Managing Director, Retail Banking Managing Director, Business Banking Managing Director, Investment Banking Managing Director, Corporate & Institutional Banking Chief Financial Officer Chief Risk Officer Chief Operations Officer Chief Executive Officer of AmIslamic Bank Berhad Senior General Manager, Transaction Banking

Capital History:

Year Remarks Amount (RM million)

Cumulative Total (RM million)

2005 Balance brought forward (from the former commercial bank)

- 761.72

2005 Capital-reduction exercise pursuant to the business merger of AmBank (M) Berhad (formerly known as AmFinance Berhad) and AmIslamic Bank Berhad (formerly known as AmBank Berhad)

(608.68) 153.04

2006 Issuance of new ordinary shares 250.00 403.04

2011 Issuance of new ordinary shares 25.00 428.04

2013 Issuance of new ordinary share 34.88 462.92

AmIslamic Bank Berhad 5

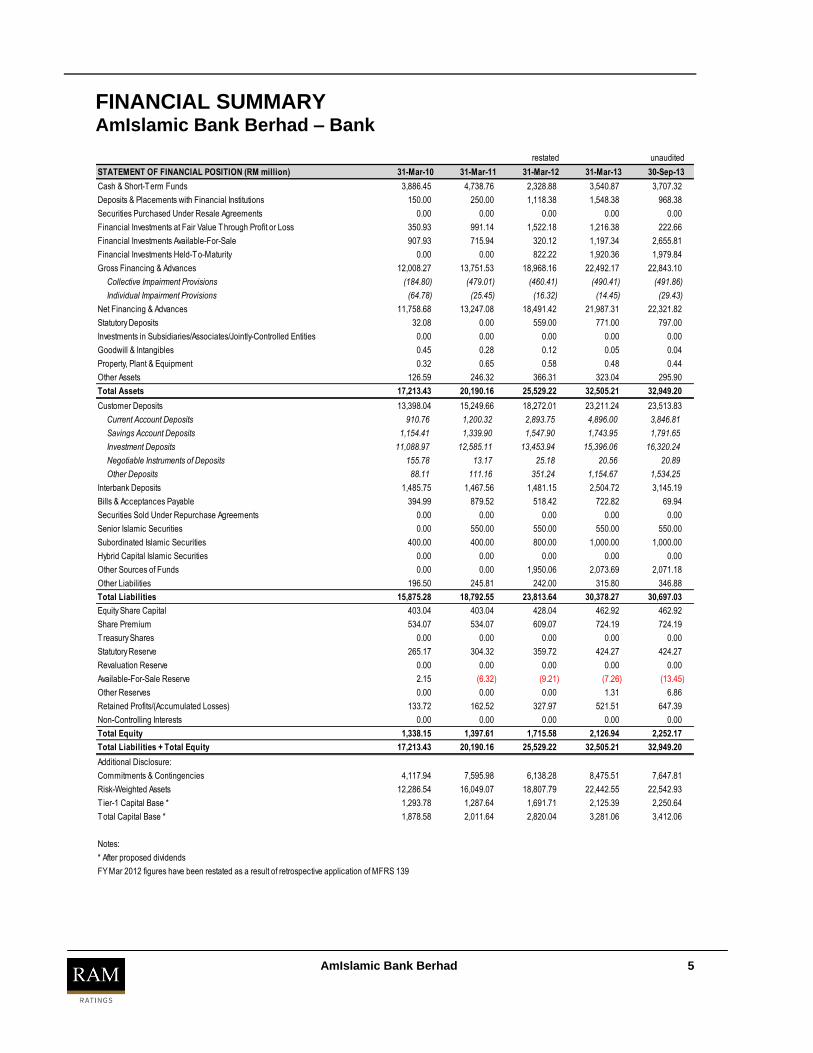

restated unaudited

STATEMENT OF FINANCIAL POSITION (RM million) 31-Mar-10 31-Mar-11 31-Mar-12 31-Mar-13 30-Sep-13

Cash & Short-Term Funds 3,886.45 4,738.76 2,328.88 3,540.87 3,707.32

Deposits & Placements with Financial Institutions 150.00 250.00 1,118.38 1,548.38 968.38

Securities Purchased Under Resale Agreements 0.00 0.00 0.00 0.00 0.00

Financial Investments at Fair Value Through Profit or Loss 350.93 991.14 1,522.18 1,216.38 222.66

Financial Investments Available-For-Sale 907.93 715.94 320.12 1,197.34 2,655.81

Financial Investments Held-To-Maturity 0.00 0.00 822.22 1,920.36 1,979.84

Gross Financing & Advances 12,008.27 13,751.53 18,968.16 22,492.17 22,843.10

Collective Impairment Provisions (184.80) (479.01) (460.41) (490.41) (491.86)

Individual Impairment Provisions (64.78) (25.45) (16.32) (14.45) (29.43)

Net Financing & Advances 11,758.68 13,247.08 18,491.42 21,987.31 22,321.82

Statutory Deposits 32.08 0.00 559.00 771.00 797.00

Investments in Subsidiaries/Associates/Jointly-Controlled Entities 0.00 0.00 0.00 0.00 0.00

Goodwill & Intangibles 0.45 0.28 0.12 0.05 0.04

Property, Plant & Equipment 0.32 0.65 0.58 0.48 0.44

Other Assets 126.59 246.32 366.31 323.04 295.90

Total Assets 17,213.43 20,190.16 25,529.22 32,505.21 32,949.20

Customer Deposits 13,398.04 15,249.66 18,272.01 23,211.24 23,513.83

Current Account Deposits 910.76 1,200.32 2,893.75 4,896.00 3,846.81

Savings Account Deposits 1,154.41 1,339.90 1,547.90 1,743.95 1,791.65

Investment Deposits 11,088.97 12,585.11 13,453.94 15,396.06 16,320.24

Negotiable Instruments of Deposits 155.78 13.17 25.18 20.56 20.89

Other Deposits 88.11 111.16 351.24 1,154.67 1,534.25

Interbank Deposits 1,485.75 1,467.56 1,481.15 2,504.72 3,145.19

Bills & Acceptances Payable 394.99 879.52 518.42 722.82 69.94

Securities Sold Under Repurchase Agreements 0.00 0.00 0.00 0.00 0.00

Senior Islamic Securities 0.00 550.00 550.00 550.00 550.00

Subordinated Islamic Securities 400.00 400.00 800.00 1,000.00 1,000.00

Hybrid Capital Islamic Securities 0.00 0.00 0.00 0.00 0.00

Other Sources of Funds 0.00 0.00 1,950.06 2,073.69 2,071.18

Other Liabilities 196.50 245.81 242.00 315.80 346.88

Total Liabilities 15,875.28 18,792.55 23,813.64 30,378.27 30,697.03

Equity Share Capital 403.04 403.04 428.04 462.92 462.92

Share Premium 534.07 534.07 609.07 724.19 724.19

Treasury Shares 0.00 0.00 0.00 0.00 0.00

Statutory Reserve 265.17 304.32 359.72 424.27 424.27

Revaluation Reserve 0.00 0.00 0.00 0.00 0.00

Available-For-Sale Reserve 2.15 (6.32) (9.21) (7.26) (13.45)

Other Reserves 0.00 0.00 0.00 1.31 6.86

Retained Profits/(Accumulated Losses) 133.72 162.52 327.97 521.51 647.39

Non-Controlling Interests 0.00 0.00 0.00 0.00 0.00

Total Equity 1,338.15 1,397.61 1,715.58 2,126.94 2,252.17

Total Liabilities + Total Equity 17,213.43 20,190.16 25,529.22 32,505.21 32,949.20

Additional Disclosure:

Commitments & Contingencies 4,117.94 7,595.98 6,138.28 8,475.51 7,647.81

Risk-Weighted Assets 12,286.54 16,049.07 18,807.79 22,442.55 22,542.93

T ier-1 Capital Base * 1,293.78 1,287.64 1,691.71 2,125.39 2,250.64

Total Capital Base * 1,878.58 2,011.64 2,820.04 3,281.06 3,412.06

Notes:

* After proposed dividends

FY Mar 2012 figures have been restated as a result of retrospective application of MFRS 139

FINANCIAL SUMMARY AmIslamic Bank Berhad – Bank

AmIslamic Bank Berhad 6

restated unaudited

STATEMENT OF COMPREHENSIVE INCOME (RM million) 31-Mar-10 31-Mar-11 31-Mar-12 31-Mar-13 30-Sep-13

6 months

Financing Income 980.04 1,104.59 1,308.46 1,560.04 826.39

Financing Expense (335.34) (439.77) (636.47) (816.01) (443.75)

Net Financing Income 644.70 664.82 671.99 744.03 382.65

Fee Income 46.12 62.07 59.49 78.04 31.35

Investment Income 6.87 12.94 32.30 14.23 10.86

Other Income (0.02) 0.01 0.02 (13.14) (0.39)

Gross Income 697.66 739.84 763.80 823.15 424.46

Personnel Expenses (6.52) (9.41) (9.93) (11.76) (5.40)

Other Operating Expenses (252.73) (271.44) (291.05) (342.69) (174.47)

Operating Income before Impairment Charges 438.41 458.98 462.82 468.70 244.59

Net Impairment Charges on Financing (90.30) (247.79) (163.21) (136.09) (73.75)

Net Impairment Charges on Financial Investments (4.22) 4.22 0.00 0.00 0.00

Net Impairment Charges on Commitments, Contingencies & Other Assets 12.71 (6.28) (0.13) (0.70) 0.69

Operating Income after Impairment Charges 356.61 209.13 299.48 331.92 171.53

Non-Recurring Items 0.00 0.00 0.00 0.00 0.00

Share of Associates/Jointly-Controlled Entities Profits/(Losses) 0.00 0.00 0.00 0.00 0.00

Pre-Tax Profit/(Loss) 356.61 209.13 299.48 331.92 171.53

Taxation & Zakat (95.27) (52.54) (80.40) (73.73) (40.06)

Net Profit/(Loss) 261.35 156.59 219.08 258.19 131.48

Gain/(Loss) on Available-For-Sale Financial Investments (9.00) (4.04) (3.85) 2.61 (8.26)

Changes in Cash Flow & Net Investment Hedges 0.00 0.00 0.00 0.00 0.00

Foreign Currency Translation Differences 0.00 0.00 0.00 0.00 0.00

Share of Other Comprehensive Income/(Loss) of Associates/Jointly-Controlled Entities 0.00 0.00 0.00 0.00 0.00

Income Tax Relating to Other Comprehensive Income/(Loss) 2.25 1.01 0.96 (0.65) 2.06

Other Components of Comprehensive Income/(Loss) 0.00 0.00 0.00 0.00 0.00

Total Comprehensive Income/(Loss) 254.60 153.56 216.19 260.15 125.28

Additional Disclosure:

Net Profit/(Loss) Attributable to Non-Controlling Interests 0.00 0.00 0.00 0.00 0.00

Dividends - Ordinary Shares & Preference Shares 200.00 39.90 0.00 0.00 0.00

FY Mar 2012 figures have been restated as a result of retrospective application of MFRS 139

FINANCIAL SUMMARY AmIslamic Bank Berhad – Bank

AmIslamic Bank Berhad 7

restated unaudited

KEY RATIOS 31-Mar-10 31-Mar-11 31-Mar-12 31-Mar-13 30-Sep-13

PROFITABILITY (%)

Net Financing Margin 4.18% 3.59% 3.02% 2.66% 2.42% *

Non-Financing Income to Gross Income 7.59% 10.14% 12.02% 9.61% 9.85%

Cost to Income 37.16% 37.96% 39.41% 43.06% 42.38%

Return on Assets 2.28% 1.12% 1.31% 1.14% 1.05% *

Return on Risk-Weighted Assets 3.14% 1.48% 1.72% 1.61% 1.53% *

Return on Equity 27.20% 15.29% 19.24% 17.28% 15.67% *

ASSET QUALITY (%)

Gross Impaired Financing Ratio 1.48% 2.09% 1.25% 1.19% 1.49%

Net Newly Classified Impaired Financing Ratio 0.68% 1.58% 0.86% 1.02% 1.52% *

Financing Credit Cost Ratio 0.78% 1.79% 0.95% 0.66% 0.65% *

Impairment Charge Ratio 0.75% 1.59% 0.84% 0.56% 0.54% *

Gross Impaired Financing Coverage Ratio 136.96% 157.44% 200.54% 188.07% 152.65%

LIQUIDITY & FUNDING (%)

Liquid Asset Ratio 32.58% 35.72% 23.18% 24.54% 26.00%

Interbank Deposits to Total Profit Bearing Funds 9.48% 7.91% 6.28% 8.33% 10.36%

Customer Deposits to Total Profit Bearing Funds 85.45% 82.22% 77.52% 77.21% 77.48%

CASA Deposits to Total Deposits 15.41% 16.66% 24.31% 28.61% 23.98%

Financing to Deposits Ratio 87.76% 86.87% 101.20% 94.73% 94.93%

CAPITALISATION (%)

Internal Rate of Capital Generation 4.68% 8.53% 14.07% 13.44% 6.00%

Common Equity T ier-1 Capital Ratio NA NA NA 9.47% ^ 9.98% ^

Tier-1 Capital Ratio 10.53% 8.02% 8.99% 9.47% ^ 9.98% ^

Total Capital Ratio 15.29% 12.53% 14.99% 14.62% ^ 15.14% ^

Notes:

* annualised

NA = Not Available / Not Applicable

FY Mar 2012 figures have been restated as a result of retrospective application of MFRS 139

^ The capital components of these ratios are computed in accordance with Bank Negara Malaysia's latest Capital Adequacy Framework , based on Basel III standards

FINANCIAL RATIOS AmIslamic Bank Berhad – Bank

AmIslamic Bank Berhad 8

KEY RATIOS FORMULAE

PROFITABILITY (%)

Net Financing Margin Net Finance Income / Average Profit Earning Assets

Non-Financing Income to Gross Income Non-Finance Income / Gross Income

Cost to Income (Personnel Expenses + Other Operating Expenses) / Gross Income

Return on Assets Pre-Tax Profit/(Loss) / Average Total Assets

Return on Risk-Weighted Assets Pre-Tax Profit/(Loss) / Average Total Risk-Weighted Assets

Return on Equity Pre-Tax Profit/(Loss) / Average Total Equity

Non-Finance Income Fee Income + Investment Income + Other Income

Profit Earning Assets Cash & Short-Term Funds + Deposits & Placements with Financial Institutions

+ Securities Purchased Under Resale Agreements + Total Financial Investments

+ Net Financing & Advances

Total Financial Investments Financial Investments at Fair Value Through Profit or Loss + Financial Investments Available-For-Sale

+ Financial Investments Held-To-Maturity

ASSET QUALITY (%)

Gross Impaired Financing Ratio Total Impaired Financing / Gross Financing & Advances

Net Newly Classified Impaired Financing Ratio Net Newly Classified Impaired Financing / Average Gross Financing & Advances

Financing Credit Cost Ratio Net Impairment Charges on Financing / Average Gross Financing & Advances

Impairment Charge Ratio (Net Impairment Charges on Financing + Net Impairment Charges on Financial Investments) /

(Average Gross Financing & Advances + Average Total Financial Investments)

Gross Impaired Financing Coverage Ratio Total Provisions / Gross Impaired Financing

Total Provisions Collective Impairment Provisions + Individual Impairment Provisions

Net Newly Classified Impaired Financing Newly Classified Impaired Financing - Recoveries on Impaired Financing

- Impaired Financing Reclassified As Performing

LIQUIDITY & FUNDING (%)

Liquid Asset Ratio Liquid Assets / (Customer Deposits + Short-Term Funds)

Interbank Deposits to Total Profit Bearing Funds Interbank Deposits / Profit Bearing Funds

Customer Deposits to Total Profit Bearing Funds Customer Deposits / Profit Bearing Funds

CASA Deposits to Total Deposits (Current Account + Savings Account Deposits) / Customer Deposits

Financing to Deposits Ratio Net Financing & Advances / Customer Deposits

Liquid Assets Cash & Short-Term Funds + Deposits & Placements with Financial Institutions

+ Securities Purchased Under Resale Agreements

+ Quoted Financial Investments (excluding Financial Investments Held-To-Maturity)

Short-Term Funds Interbank Deposits + Bills & Acceptances Payable + Securities Sold Under Repurchase Agreements

Profit Bearing Funds Financial Institutions + Quoted Securities (Excluding Financial Investments Held-To-Maturity)Customer Deposits + Interbank Deposits + Bills & Acceptances Payable

+ Securities Sold Under Repurchase Agreements + Total Borrowings

Total Borrowings Senior Islamic Securities + Subordinated Islamic Securities

Hybrid Capital Islamic Securities + Other Borrowings

CAPITALISATION (%)

Internal Rate of Capital Generation (Net Profit/(Loss) - Dividends) / Average Total Equity

Common Equity T ier-1 Capital Ratio Common Equity T ier-1 Capital / Total Risk-Weighted Assets

T ier-1 Capital Ratio T ier-1 Capital / Total Risk-Weighted Assets

Total Capital Ratio Total Capital / Total Risk-Weighted Assets

Common Equity T ier-1 Capital Ordinary Shares + Share Premium + Retained Earnings + Non-Controlling Interests + Applicable Reserves

± Applicable Regulatory Adjustments

T ier-1 Capital Common Equity T ier-1 Capital + Additional T ier-1 Capital Instruments ± Applicable Regulatory Adjustments

T ier-2 Capital T ier-2 Capital Instruments ± Applicable Regulatory Adjustments

Total Capital T ier-1 Capital + T ier-2 Capital

FINANCIAL RATIOS AmIslamic Bank Berhad – Bank

AmIslamic Bank Berhad 9

CREDIT RATING DEFINITIONS

Financial Institution Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A financial institution rated AAA has a superior capacity to meet its financial obligations. This is the highest long-term FIRassigned by RAM Ratings.

A financial institution rated AA has a strong capacity to meet its financial obligations. The financial institution is resilientagainst adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated A has an adequate capacity to meet its financial obligations. The financial institution is moresusceptible to adverse changes in circumstances, economic conditions and/or operating environments than those in

higher-rated categories.

A financial institution rated BBB has a moderate capacity to meet its financial obligations. The financial institution is morelikely to be weakened by adverse changes in circumstances, economic conditions and/or operating environments than

those in higher-rated categories. This is the lowest investment-grade category.

A financial institution rated BB has a weak capacity to meet its financial obligations. The financial institution is highlyvulnerable to adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated B has a very weak capacity to meet its financial obligations. The financial institution has alimited ability to withstand adverse changes in circumstances, economic conditions and/oroperating environments.

A financial institution rated C has a high likelihood of defaulting on its financial obligations. The financial institution ishighly dependent on favourable changes in circumstances, economic conditions and/or operating environments, the lack

of which would likely result in it defaultingon its financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

A financial institution rated P1 has a strong capacity to meet its short-term financial obligations. This is the highest short-term FIR assigned by RAM Ratings.

A financial institution rated P2 has an adequate capacity to meet its short-term financial obligations. The financialinstitution is more susceptible to the effectsof deteriorating circumstances than thosein the highest-rated category.

A financial institution rated P3 has a moderate capacity to meet its short-term financial obligations. The financialinstitution is more likely to be weakened by the effects of deteriorating circumstances than those in higher-rated

categories. This is the lowest investment-grade category.

A financial institution rated NP has a doubtful capacity to meet its short-term financial obligations. The financial institutionfaces major uncertainties that could compromise its capacity for payment of financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that thefinancial institution ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3

indicates that the financial institution ranks at the lower end of its generic rating category.

A Financial Institution Rating ("FIR") is RAM Ratings' current opinion on the overall capacity of a financial institution to meetits financial obligations. The opinion is not specific to any particular financial obligation, as it does not take into account theexpressed terms and conditions of any specific financial obligation.

AmIslamic Bank Berhad 10

CREDIT RATING DEFINITIONS

Issue Ratings - Debt-Based Sukuk

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A sukuk rated AAA has superior safety for payment of financial obligations. This is the highest long-term Issue Ratingassigned by RAM Ratings to a debt-based sukuk.

A sukuk rated AA has high safety for payment of financial obligations. The issuer is resilient against adverse changes incircumstances, economic conditions and/or operating environments.

A sukuk rated A has adequate safety for payment of financial obligations. The issuer is more susceptible to adversechanges in circumstances, economic conditions and/or operating environments than those in higher-rated categories.

A sukuk rated BBB has moderate safety for payment of financial obligations. The issuer is more likely to be weakened byadverse changes in circumstances, economic conditions and/or operating environments than those in higher-rated

categories. This is the lowest investment-grade category.

A sukuk rated BB has low safety for payment of financial obligations. The issuer is highly vulnerable to adverse changesin circumstances, economic conditions and/oroperating environments.

A sukuk rated B has very low safety for payment of financial obligations. The issuer has a limited ability to withstandadverse changes in circumstances, economic conditions and/oroperating environments.

A sukuk rated C has a high likelihood of default. The issuer is highly dependent on favourable changes in circumstances,economic conditions and/or operating environments, the lack of which would likely result in it defaulting on a particular

sukuk.

A sukuk rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular sukuk.

A sukuk rated P1 has high safety for payment of financial obligations in the short term. This is the highest short-termIssue Rating assigned by RAM Ratings to a debt-based sukuk.

A sukuk rated P2 has adequate safety for payment of financial obligations in the short term. The issuer is moresusceptible to the effects of deteriorating circumstances than those in the highest-rated category.

A sukuk rated P3 has moderate safety for payment of financial obligations in the short term. The issuer is more likely tobe weakened by the effects of deteriorating circumstances than those in higher-rated categories. This is the lowest

investment-grade category.

A sukuk rated NP has doubtful safety for payment of financial obligations in the short term. The issuer faces majoruncertainties that could compromise its capacity for payment of a particularsukuk.

A sukuk rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular sukuk.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that theissue ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3 indicates that the

issue ranks at the lower end of its generic rating category. In addition, RAM Ratings applies the suffixes (bg) or (s) to ratings which havebeen enhanced by a bank guarantee or other supports, respectively.

An Issue Rating for a debt-based sukuk is RAM Ratings' current opinion on the creditworthiness of a particular debt-basedsukuk. It reflects the overall capacity and willingness of an issuer to meet the financial obligations on a particular debt-based sukuk on a full and timely basis, taking into account its expressed terms and conditions. RAM Ratings’ sukuk ratingsare, however, not a measure of compliance with Shariah principles or the role, formation, practices, legitimacy andsoundness of the Shariah advisors’ recommendations and decisions.

AmIslamic Bank Berhad 11

CREDIT RATING DEFINITIONS

Issue Ratings - Partnership-Based Sukuk

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A sukuk rated AAA has superior safety for payment of capital and expected returns. This is the highest long-term IssueRating assigned by RAM Ratings to a partnership-based sukuk.

A sukuk rated AA has high safety for payment of capital and expected returns. The issuer is resilient against adversechanges in circumstances, economic conditions and/or operating environments.

A sukuk rated A has adequate safety for payment of capital and expected returns. The issuer is more susceptible toadverse changes in circumstances, economic conditions and/or operating environments than those in higher-rated

categories.

A sukuk rated BBB has moderate safety for payment of capital and expected returns. The issuer is more likely to beweakened by adverse changes in circumstances, economic conditions and/or operating environments than those in

higher-rated categories. This is the lowest investment-grade category.

A sukuk rated BB has low safety for payment of capital and expected returns. The issuer is highly vulnerable to adversechanges in circumstances, economic conditions and/or operating environments.

A sukuk rated B has very low safety for payment of capital and expected returns. The issuer has a limited ability towithstand adverse changes in circumstances, economic conditions and/oroperating environments.

A sukuk rated C has a high likelihood of not meeting the payment of capital and expected returns. The issuer is highlydependent on favourable changes in circumstances, economic conditions and/or operating environments, the lack of

which would likely result in it not fulfilling the terms of the investment contract.

A sukuk rated D is either currently not meeting or will not meet the payment of capital and expected returns. The D ratingmay also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to the issuer that could

jeopardise the fulfilment of the investment contract's terms.

A sukuk rated P1 has high safety for payment of capital and expected returns in the short term. This is the highest short-term Issue Rating assigned by RAM Ratings a partnership-based sukuk.

A sukuk rated P2 has adequate safety for payment of capital and expected returns in the short term. The issuer is moresusceptible to the effects of deteriorating circumstances than those in the highest-rated category.

A sukuk rated P3 has moderate safety for payment of capital and expected returns in the short term. The issuer is morelikely to be weakened by the effects of deteriorating circumstances than those in higher-rated categories. This is the

lowest investment-grade category.

A sukuk rated NP has doubtful safety for payment of capital and expected returns in the short term. The issuer facesmajor uncertainties that could compromise its capacity for fulfiling the terms of the investment contract.

A sukuk rated D is either currently not meeting or will not meet the payment of capital and expected returns. The D ratingmay also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to the issuer that could

jeopardise the fulfilment of the investment contract's terms.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that theissue ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3 indicates that the

issue ranks at the lower end of its generic rating category. In addition, RAM Ratings applies the suffixes (bg) or (s) to ratings which havebeen enhanced by a bank guarantee or other supports, respectively.

An Issue Rating for a partnership-based sukuk is RAM Ratings' current opinion on the creditworthiness of a particularpartnership-based sukuk. It reflects the overall capacity and willingness of an issuer to meet the payment of capital andexpected returns on a full and timely basis, taking into account the expressed terms and conditions of the investmentcontract. RAM Ratings’ sukuk ratings are, however, not a measure of compliance with Shariah principles or the role,formation,practices, legitimacy and soundness of the Shariah advisors’ recommendations and decisions.

AmIslamic Bank Berhad 12

RAM Ratings receives compensation for its rating services, normally paid by the issuers of such securities or the rated entity, and sometimes

third parties participating in marketing the securities, insurers, guarantors, other obligors, underwriters, etc. The receipt of this compensation has

no influence on RAM Ratings’ credit opinions or other analytical processes. In all instances, RAM Ratings is committed to preserving the

objectivity, integrity and independence of its ratings. Rating fees are communicated to clients prior to the issuance of rating opinions. While RAM

Ratings reserves the right to disseminate the ratings, it receives no payment for doing so, except for subscriptions to its publications.

RAM Ratings, its rating committee members and the analysts involved in the rating exercise have not encountered and/or are not aware of any

conflict of interest relating to the rating exercise. RAM Ratings will adequately disclose all related information in the report if there are such

instances.

Published by RAM Rating Services Berhad

Reproduction or transmission in any form is prohibited except by

permission from RAM Rating Services Berhad.

Copyright 2014 by RAM Rating Services Berhad

RAM Rating Services Berhad

Suite 20.01, Level 20

The Gardens South Tower

Mid Valley City, Lingkaran Syed Putra

59200 Kuala Lumpur

Tel: (603) 7628 1000 / (603) 2299 1000 Fax: (603) 7620 8251

E-mail: [email protected] Website: http://www.ram.com.my

Related Documents