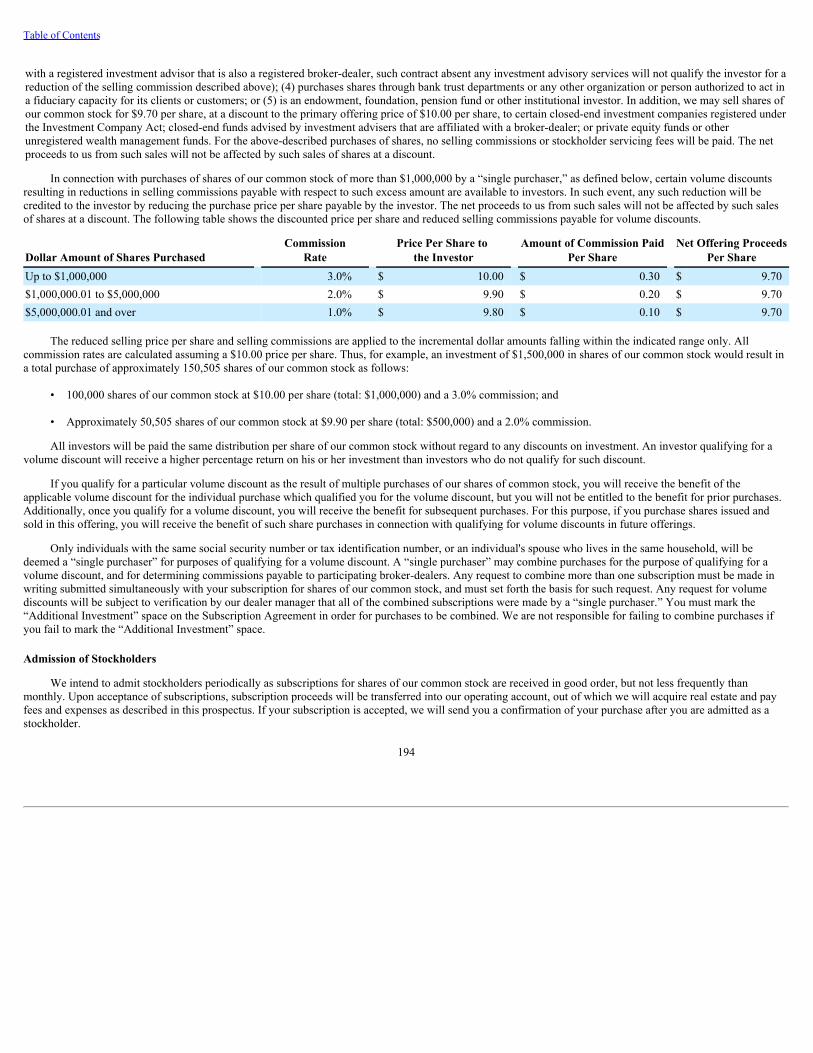

AMERICAN HEALTHCARE REIT, INC. FORM 424B3 (Prospectus filed pursuant to Rule 424(b)(3)) Filed 02/17/16 Address 18191 VON KARMAN AVENUE SUITE 300 IRVINE, CA, 92612 Telephone 949-270-9200 CIK 0001632970 SIC Code 6798 - Real Estate Investment Trusts Industry Specialized REITs Sector Financials Fiscal Year 12/31 http://www.edgar-online.com © Copyright 2022, EDGAR Online, a division of Donnelley Financial Solutions. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, a division of Donnelley Financial Solutions, Terms of Use.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AMERICAN HEALTHCARE REIT, INC.

FORM 424B3(Prospectus filed pursuant to Rule 424(b)(3))

Filed 02/17/16

Address 18191 VON KARMAN AVENUE

SUITE 300IRVINE, CA, 92612

Telephone 949-270-9200CIK 0001632970

SIC Code 6798 - Real Estate Investment TrustsIndustry Specialized REITs

Sector FinancialsFiscal Year 12/31

http://www.edgar-online.com© Copyright 2022, EDGAR Online, a division of Donnelley Financial Solutions. All Rights Reserved.

Distribution and use of this document restricted under EDGAR Online, a division of Donnelley Financial Solutions, Terms of Use.

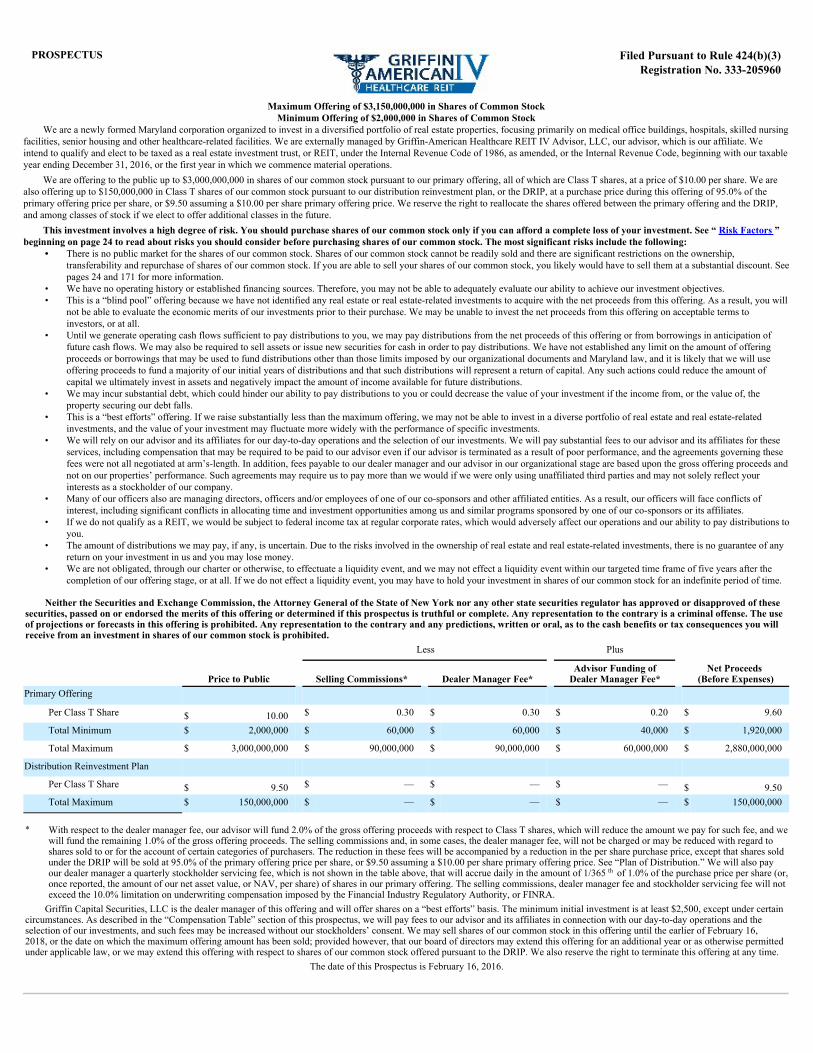

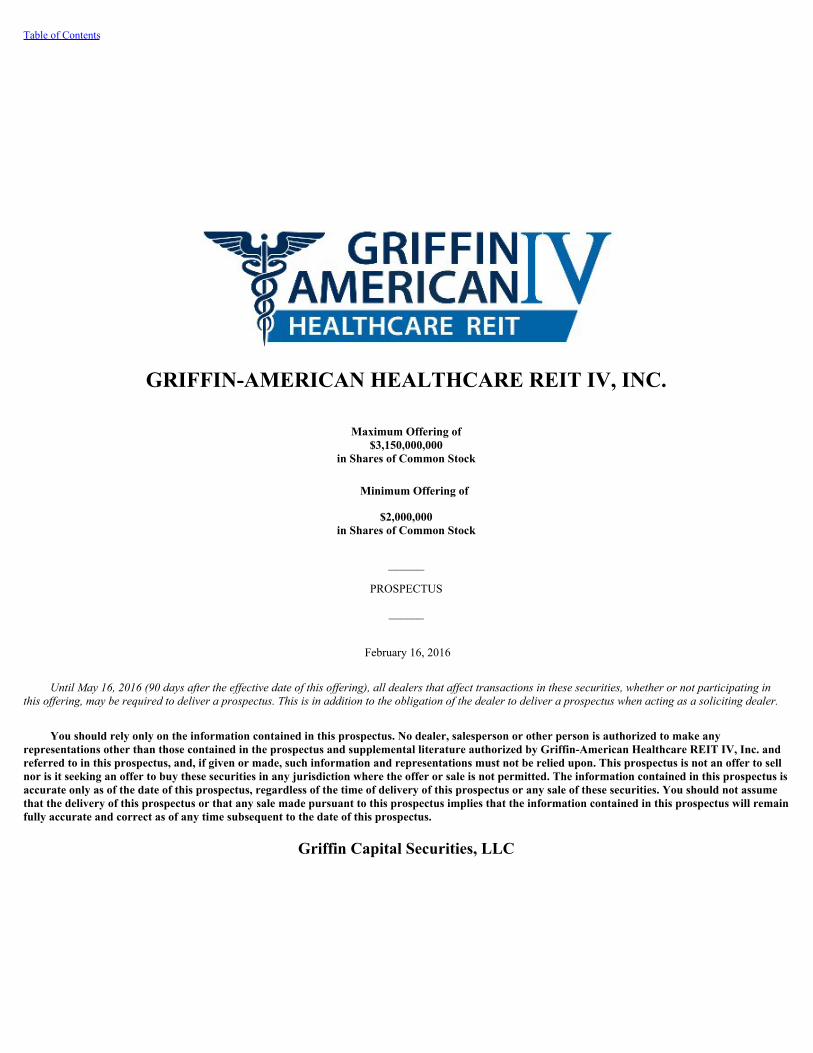

PROSPECTUS Filed Pursuant to Rule 424(b)(3)Registration No. 333-205960

Maximum Offering of $3,150,000,000 in Shares of Common StockMinimum Offering of $2,000,000 in Shares of Common Stock

We are a newly formed Maryland corporation organized to invest in a diversified portfolio of real estate properties, focusing primarily on medical office buildings, hospitals, skilled nursingfacilities, senior housing and other healthcare-related facilities. We are externally managed by Griffin-American Healthcare REIT IV Advisor, LLC, our advisor, which is our affiliate. Weintend to qualify and elect to be taxed as a real estate investment trust, or REIT, under the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, beginning with our taxableyear ending December 31, 2016, or the first year in which we commence material operations.

We are offering to the public up to $3,000,000,000 in shares of our common stock pursuant to our primary offering, all of which are Class T shares, at a price of $10.00 per share. We arealso offering up to $150,000,000 in Class T shares of our common stock pursuant to our distribution reinvestment plan, or the DRIP, at a purchase price during this offering of 95.0% of theprimary offering price per share, or $9.50 assuming a $10.00 per share primary offering price. We reserve the right to reallocate the shares offered between the primary offering and the DRIP,and among classes of stock if we elect to offer additional classes in the future.

This investment involves a high degree of risk. You should purchase shares of our common stock only if you can afford a complete loss of your investment. See “ Risk Factors ”beginning on page 24 to read about risks you should consider before purchasing shares of our common stock. The most significant risks include the following:

• There is no public market for the shares of our common stock. Shares of our common stock cannot be readily sold and there are significant restrictions on the ownership,transferability and repurchase of shares of our common stock. If you are able to sell your shares of our common stock, you likely would have to sell them at a substantial discount. Seepages 24 and 171 for more information.

• We have no operating history or established financing sources. Therefore, you may not be able to adequately evaluate our ability to achieve our investment objectives.• This is a “blind pool” offering because we have not identified any real estate or real estate-related investments to acquire with the net proceeds from this offering. As a result, you will

not be able to evaluate the economic merits of our investments prior to their purchase. We may be unable to invest the net proceeds from this offering on acceptable terms toinvestors, or at all.

• Until we generate operating cash flows sufficient to pay distributions to you, we may pay distributions from the net proceeds of this offering or from borrowings in anticipation offuture cash flows. We may also be required to sell assets or issue new securities for cash in order to pay distributions. We have not established any limit on the amount of offeringproceeds or borrowings that may be used to fund distributions other than those limits imposed by our organizational documents and Maryland law, and it is likely that we will useoffering proceeds to fund a majority of our initial years of distributions and that such distributions will represent a return of capital. Any such actions could reduce the amount ofcapital we ultimately invest in assets and negatively impact the amount of income available for future distributions.

• We may incur substantial debt, which could hinder our ability to pay distributions to you or could decrease the value of your investment if the income from, or the value of, theproperty securing our debt falls.

• This is a “best efforts” offering. If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio of real estate and real estate-relatedinvestments, and the value of your investment may fluctuate more widely with the performance of specific investments.

• We will rely on our advisor and its affiliates for our day-to-day operations and the selection of our investments. We will pay substantial fees to our advisor and its affiliates for theseservices, including compensation that may be required to be paid to our advisor even if our advisor is terminated as a result of poor performance, and the agreements governing thesefees were not all negotiated at arm’s-length. In addition, fees payable to our dealer manager and our advisor in our organizational stage are based upon the gross offering proceeds andnot on our properties’ performance. Such agreements may require us to pay more than we would if we were only using unaffiliated third parties and may not solely reflect yourinterests as a stockholder of our company.

• Many of our officers also are managing directors, officers and/or employees of one of our co-sponsors and other affiliated entities. As a result, our officers will face conflicts ofinterest, including significant conflicts in allocating time and investment opportunities among us and similar programs sponsored by one of our co-sponsors or its affiliates.

• If we do not qualify as a REIT, we would be subject to federal income tax at regular corporate rates, which would adversely affect our operations and our ability to pay distributions toyou.

• The amount of distributions we may pay, if any, is uncertain. Due to the risks involved in the ownership of real estate and real estate-related investments, there is no guarantee of anyreturn on your investment in us and you may lose money.

• We are not obligated, through our charter or otherwise, to effectuate a liquidity event, and we may not effect a liquidity event within our targeted time frame of five years after thecompletion of our offering stage, or at all. If we do not effect a liquidity event, you may have to hold your investment in shares of our common stock for an indefinite period of time.

Neither the Securities and Exchange Commission, the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of thesesecurities, passed on or endorsed the merits of this offering or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. The useof projections or forecasts in this offering is prohibited. Any representation to the contrary and any predictions, written or oral, as to the cash benefits or tax consequences you willreceive from an investment in shares of our common stock is prohibited. Less Plus

Price to Public Selling Commissions* Dealer Manager Fee* Advisor Funding of

Dealer Manager Fee* Net Proceeds

(Before Expenses)Primary Offering

Per Class T Share $ 10.00 $ 0.30 $ 0.30 $ 0.20 $ 9.60

Total Minimum $ 2,000,000 $ 60,000 $ 60,000 $ 40,000 $ 1,920,000

Total Maximum $ 3,000,000,000 $ 90,000,000 $ 90,000,000 $ 60,000,000 $ 2,880,000,000

Distribution Reinvestment Plan Per Class T Share $ 9.50 $ — $ — $ — $ 9.50Total Maximum $ 150,000,000 $ — $ — $ — $ 150,000,000

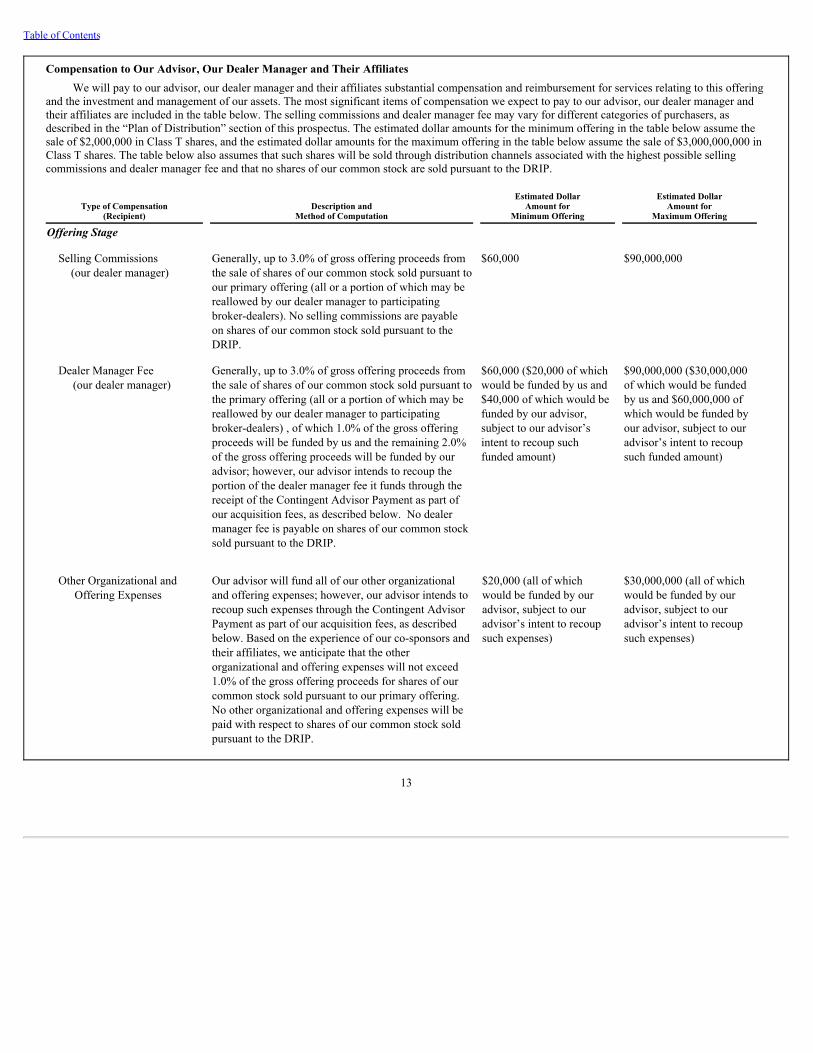

* With respect to the dealer manager fee, our advisor will fund 2.0% of the gross offering proceeds with respect to Class T shares, which will reduce the amount we pay for such fee, and wewill fund the remaining 1.0% of the gross offering proceeds. The selling commissions and, in some cases, the dealer manager fee, will not be charged or may be reduced with regard toshares sold to or for the account of certain categories of purchasers. The reduction in these fees will be accompanied by a reduction in the per share purchase price, except that shares soldunder the DRIP will be sold at 95.0% of the primary offering price per share, or $9.50 assuming a $10.00 per share primary offering price. See “Plan of Distribution.” We will also payour dealer manager a quarterly stockholder servicing fee, which is not shown in the table above, that will accrue daily in the amount of 1/365 th of 1.0% of the purchase price per share (or,once reported, the amount of our net asset value, or NAV, per share) of shares in our primary offering. The selling commissions, dealer manager fee and stockholder servicing fee will notexceed the 10.0% limitation on underwriting compensation imposed by the Financial Industry Regulatory Authority, or FINRA.

Griffin Capital Securities, LLC is the dealer manager of this offering and will offer shares on a “best efforts” basis. The minimum initial investment is at least $2,500, except under certaincircumstances. As described in the “Compensation Table” section of this prospectus, we will pay fees to our advisor and its affiliates in connection with our day-to-day operations and theselection of our investments, and such fees may be increased without our stockholders’ consent. We may sell shares of our common stock in this offering until the earlier of February 16,2018, or the date on which the maximum offering amount has been sold; provided however, that our board of directors may extend this offering for an additional year or as otherwise permittedunder applicable law, or we may extend this offering with respect to shares of our common stock offered pursuant to the DRIP. We also reserve the right to terminate this offering at any time.

The date of this Prospectus is February 16, 2016.

Table of Contents

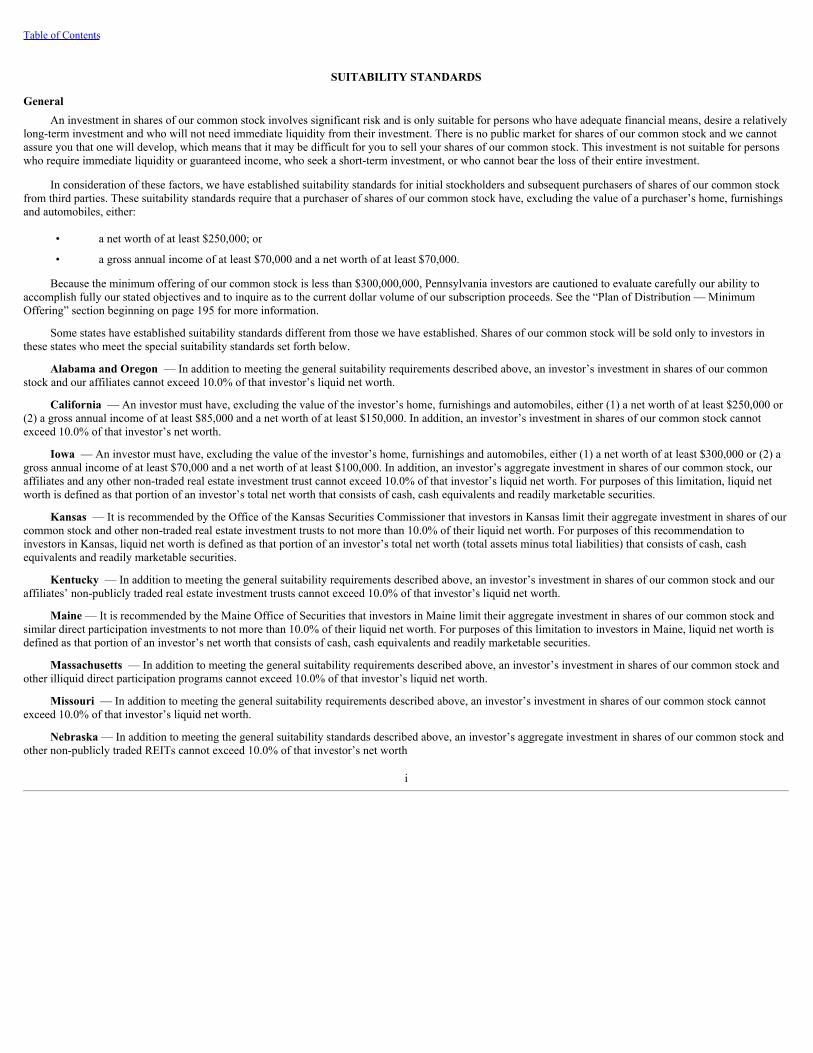

SUITABILITY STANDARDS

GeneralAn investment in shares of our common stock involves significant risk and is only suitable for persons who have adequate financial means, desire a relatively

long-term investment and who will not need immediate liquidity from their investment. There is no public market for shares of our common stock and we cannotassure you that one will develop, which means that it may be difficult for you to sell your shares of our common stock. This investment is not suitable for personswho require immediate liquidity or guaranteed income, who seek a short-term investment, or who cannot bear the loss of their entire investment.

In consideration of these factors, we have established suitability standards for initial stockholders and subsequent purchasers of shares of our common stockfrom third parties. These suitability standards require that a purchaser of shares of our common stock have, excluding the value of a purchaser’s home, furnishingsand automobiles, either:

• a net worth of at least $250,000; or

• a gross annual income of at least $70,000 and a net worth of at least $70,000.

Because the minimum offering of our common stock is less than $300,000,000, Pennsylvania investors are cautioned to evaluate carefully our ability toaccomplish fully our stated objectives and to inquire as to the current dollar volume of our subscription proceeds. See the “Plan of Distribution — MinimumOffering” section beginning on page 195 for more information.

Some states have established suitability standards different from those we have established. Shares of our common stock will be sold only to investors inthese states who meet the special suitability standards set forth below.

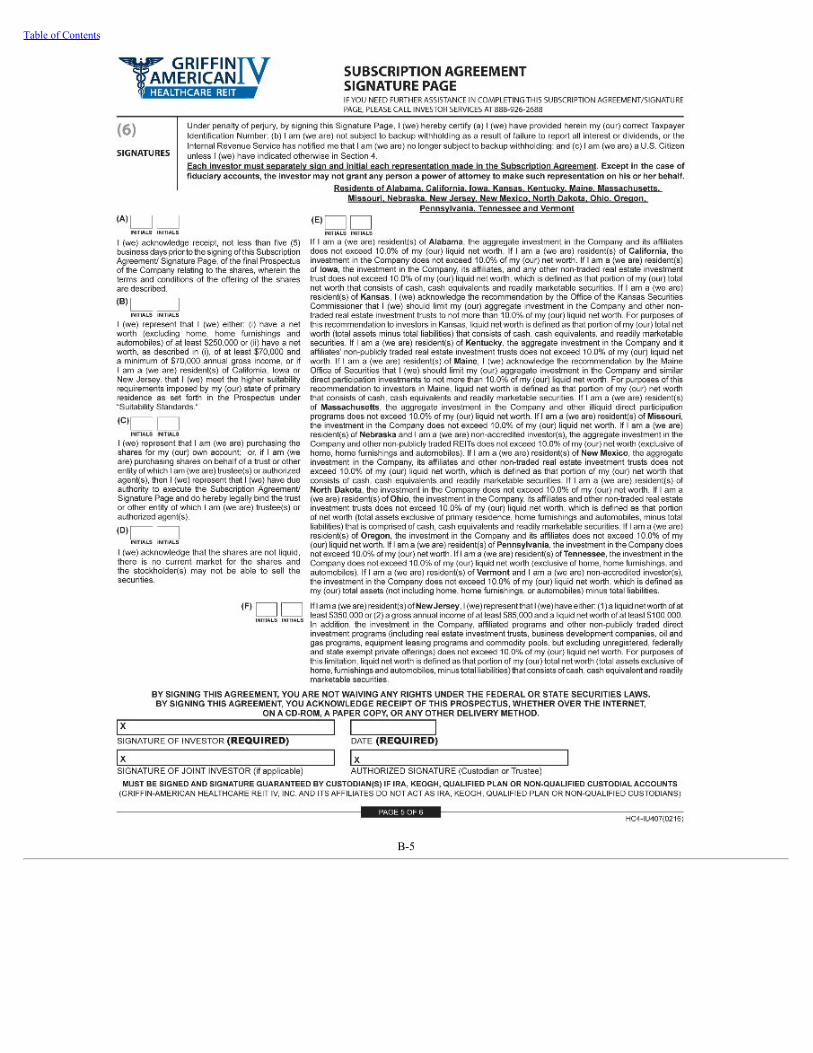

Alabama and Oregon — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our commonstock and our affiliates cannot exceed 10.0% of that investor’s liquid net worth.

California — An investor must have, excluding the value of the investor’s home, furnishings and automobiles, either (1) a net worth of at least $250,000 or(2) a gross annual income of at least $85,000 and a net worth of at least $150,000. In addition, an investor’s investment in shares of our common stock cannotexceed 10.0% of that investor’s net worth.

Iowa — An investor must have, excluding the value of the investor’s home, furnishings and automobiles, either (1) a net worth of at least $300,000 or (2) agross annual income of at least $70,000 and a net worth of at least $100,000. In addition, an investor’s aggregate investment in shares of our common stock, ouraffiliates and any other non-traded real estate investment trust cannot exceed 10.0% of that investor’s liquid net worth. For purposes of this limitation, liquid networth is defined as that portion of an investor’s total net worth that consists of cash, cash equivalents and readily marketable securities.

Kansas — It is recommended by the Office of the Kansas Securities Commissioner that investors in Kansas limit their aggregate investment in shares of ourcommon stock and other non-traded real estate investment trusts to not more than 10.0% of their liquid net worth. For purposes of this recommendation toinvestors in Kansas, liquid net worth is defined as that portion of an investor’s total net worth (total assets minus total liabilities) that consists of cash, cashequivalents and readily marketable securities.

Kentucky — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock and ouraffiliates’ non-publicly traded real estate investment trusts cannot exceed 10.0% of that investor’s liquid net worth.

Maine — It is recommended by the Maine Office of Securities that investors in Maine limit their aggregate investment in shares of our common stock andsimilar direct participation investments to not more than 10.0% of their liquid net worth. For purposes of this limitation to investors in Maine, liquid net worth isdefined as that portion of an investor’s net worth that consists of cash, cash equivalents and readily marketable securities.

Massachusetts — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock andother illiquid direct participation programs cannot exceed 10.0% of that investor’s liquid net worth.

Missouri — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock cannotexceed 10.0% of that investor’s liquid net worth.

Nebraska — In addition to meeting the general suitability standards described above, an investor’s aggregate investment in shares of our common stock andother non-publicly traded REITs cannot exceed 10.0% of that investor’s net worth

i

Table of Contents

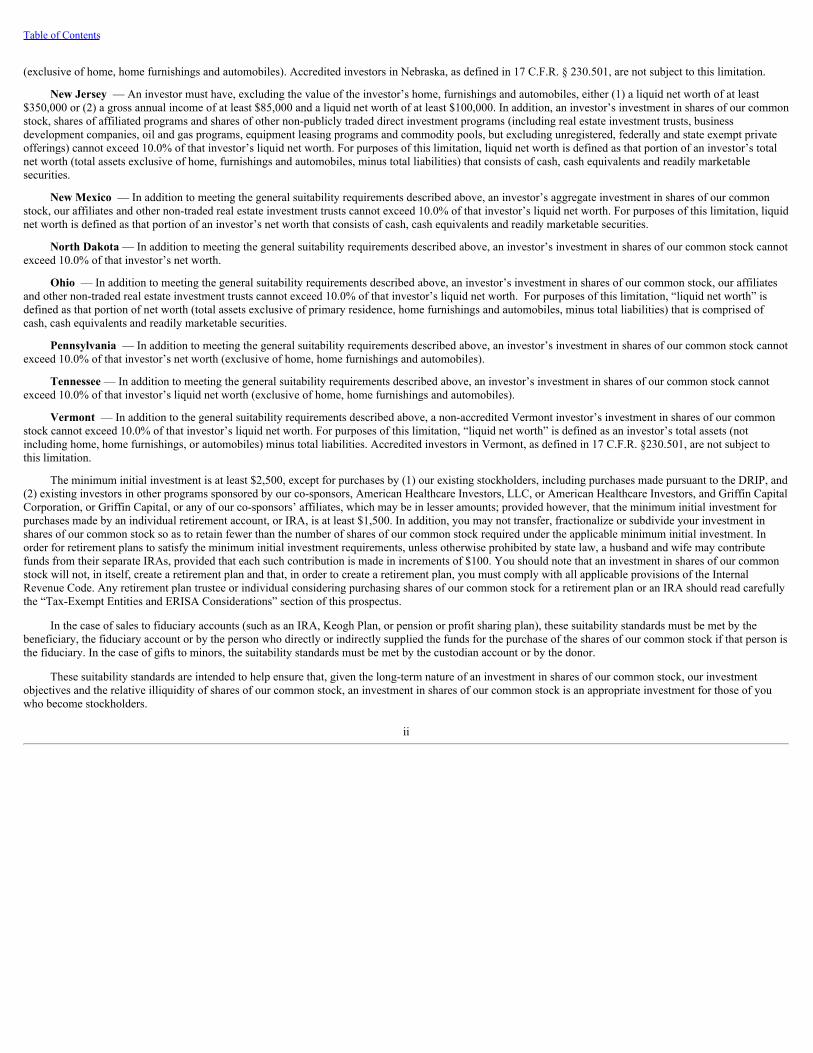

(exclusive of home, home furnishings and automobiles). Accredited investors in Nebraska, as defined in 17 C.F.R. § 230.501, are not subject to this limitation.

New Jersey — An investor must have, excluding the value of the investor’s home, furnishings and automobiles, either (1) a liquid net worth of at least$350,000 or (2) a gross annual income of at least $85,000 and a liquid net worth of at least $100,000. In addition, an investor’s investment in shares of our commonstock, shares of affiliated programs and shares of other non-publicly traded direct investment programs (including real estate investment trusts, businessdevelopment companies, oil and gas programs, equipment leasing programs and commodity pools, but excluding unregistered, federally and state exempt privateofferings) cannot exceed 10.0% of that investor’s liquid net worth. For purposes of this limitation, liquid net worth is defined as that portion of an investor’s totalnet worth (total assets exclusive of home, furnishings and automobiles, minus total liabilities) that consists of cash, cash equivalents and readily marketablesecurities.

New Mexico — In addition to meeting the general suitability requirements described above, an investor’s aggregate investment in shares of our commonstock, our affiliates and other non-traded real estate investment trusts cannot exceed 10.0% of that investor’s liquid net worth. For purposes of this limitation, liquidnet worth is defined as that portion of an investor’s net worth that consists of cash, cash equivalents and readily marketable securities.

North Dakota — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock cannotexceed 10.0% of that investor’s net worth.

Ohio — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock, our affiliatesand other non-traded real estate investment trusts cannot exceed 10.0% of that investor’s liquid net worth. For purposes of this limitation, “liquid net worth” isdefined as that portion of net worth (total assets exclusive of primary residence, home furnishings and automobiles, minus total liabilities) that is comprised ofcash, cash equivalents and readily marketable securities.

Pennsylvania — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock cannotexceed 10.0% of that investor’s net worth (exclusive of home, home furnishings and automobiles).

Tennessee — In addition to meeting the general suitability requirements described above, an investor’s investment in shares of our common stock cannotexceed 10.0% of that investor’s liquid net worth (exclusive of home, home furnishings and automobiles).

Vermont — In addition to the general suitability requirements described above, a non-accredited Vermont investor’s investment in shares of our commonstock cannot exceed 10.0% of that investor’s liquid net worth. For purposes of this limitation, “liquid net worth” is defined as an investor’s total assets (notincluding home, home furnishings, or automobiles) minus total liabilities. Accredited investors in Vermont, as defined in 17 C.F.R. §230.501, are not subject tothis limitation.

The minimum initial investment is at least $2,500, except for purchases by (1) our existing stockholders, including purchases made pursuant to the DRIP, and(2) existing investors in other programs sponsored by our co-sponsors, American Healthcare Investors, LLC, or American Healthcare Investors, and Griffin CapitalCorporation, or Griffin Capital, or any of our co-sponsors’ affiliates, which may be in lesser amounts; provided however, that the minimum initial investment forpurchases made by an individual retirement account, or IRA, is at least $1,500. In addition, you may not transfer, fractionalize or subdivide your investment inshares of our common stock so as to retain fewer than the number of shares of our common stock required under the applicable minimum initial investment. Inorder for retirement plans to satisfy the minimum initial investment requirements, unless otherwise prohibited by state law, a husband and wife may contributefunds from their separate IRAs, provided that each such contribution is made in increments of $100. You should note that an investment in shares of our commonstock will not, in itself, create a retirement plan and that, in order to create a retirement plan, you must comply with all applicable provisions of the InternalRevenue Code. Any retirement plan trustee or individual considering purchasing shares of our common stock for a retirement plan or an IRA should read carefullythe “Tax-Exempt Entities and ERISA Considerations” section of this prospectus.

In the case of sales to fiduciary accounts (such as an IRA, Keogh Plan, or pension or profit sharing plan), these suitability standards must be met by thebeneficiary, the fiduciary account or by the person who directly or indirectly supplied the funds for the purchase of the shares of our common stock if that person isthe fiduciary. In the case of gifts to minors, the suitability standards must be met by the custodian account or by the donor.

These suitability standards are intended to help ensure that, given the long-term nature of an investment in shares of our common stock, our investmentobjectives and the relative illiquidity of shares of our common stock, an investment in shares of our common stock is an appropriate investment for those of youwho become stockholders.

ii

Table of Contents

Each of the participating broker-dealers, authorized registered representatives or any other person selling shares of our common stock on our behalf, and ourco-sponsors, are required to:

• make every reasonable effort to determine that the purchase of shares of our common stock is a suitable and appropriate investment for eachinvestor based on information provided by such investor to the broker-dealer, including such investor’s age, investment objectives, income, networth, financial situation and other investments held by such investor; and

• maintain, for at least six years, records of the information used to determine that an investment in shares of our common stock is suitable andappropriate for each investor.

In making this determination, your participating broker-dealer, authorized registered representative or other person selling shares of our common stock on ourbehalf will, based on a review of the information provided by you, consider whether you:

• meet the minimum income and net worth standards established in your state;

• can reasonably benefit from an investment in shares of our common stock based on your overall investment objectives and portfolio structure;

• are able to bear the economic risk of the investment based on your overall financial situation; and

• have an apparent understanding of:

• the fundamental risks of an investment in shares of our common stock;

• the risk that you may lose your entire investment;

• the lack of liquidity of shares of our common stock;

• the restrictions on transferability of shares of our common stock;

• the background and qualifications of our advisor; and

• the tax consequences of an investment in shares of our common stock.

In addition, by signing the Subscription Agreement, you represent and warrant to us that you have received a copy of this prospectus and that you meet thenet worth and annual gross income requirements described above. These representations and warranties help us to ensure that you are fully informed about aninvestment in our company and that we adhere to our suitability standards. In the event you or another stockholder or a regulatory authority attempted to hold ourcompany liable because stockholders did not receive copies of this prospectus or because we failed to adhere to each state’s investor suitability requirements, wewill assert these representations and warranties made by you in any proceeding in which such potential liability is disputed in an attempt to avoid any such liability.By making these representations, you will not waive any rights that you may have under federal or state securities laws.

Restrictions Imposed by the USA PATRIOT Act and Related ActsIn accordance with the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001, or the

USA PATRIOT Act, the securities offered hereby may not be offered, sold, transferred or delivered, directly or indirectly, to any “unacceptable investor,” whichmeans anyone who is acting, directly or indirectly:

• in contravention of any United States of America, or U.S., or international laws and regulations, including without limitation any anti-moneylaundering or anti-terrorist financing sanction, regulation, or law promulgated by the Office of Foreign Assets Control of the United StatesDepartment of the Treasury, or OFAC, or any other U.S. governmental entity (such sanctions, regulations and laws, together with any supplementor amendment thereto, are referred to herein as the U.S. Sanctions Laws), such that the offer, sale or delivery, directly or indirectly, wouldcontravene such U.S. Sanctions Laws; or

• on behalf of terrorists or terrorist organizations, including those persons or entities that are included on the List of Specially Designated Nationalsand Blocked Persons maintained by OFAC, as such list may be amended from time to time, or any other lists of similar import as to any non-U.S.country, individual, or entity.

iii

Table of Contents

HOW TO SUBSCRIBE

Investors who meet the suitability standards described herein may subscribe for shares of our common stock as follows:

• Review this entire prospectus and any appendices and supplements accompanying this prospectus.

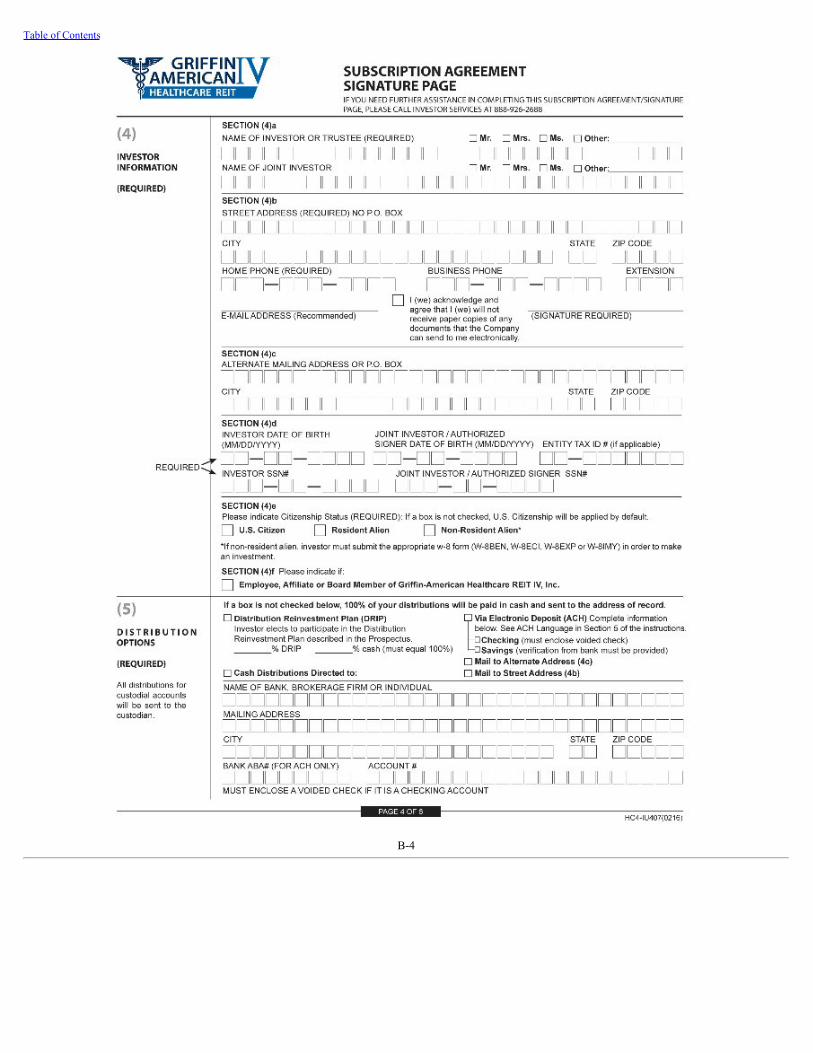

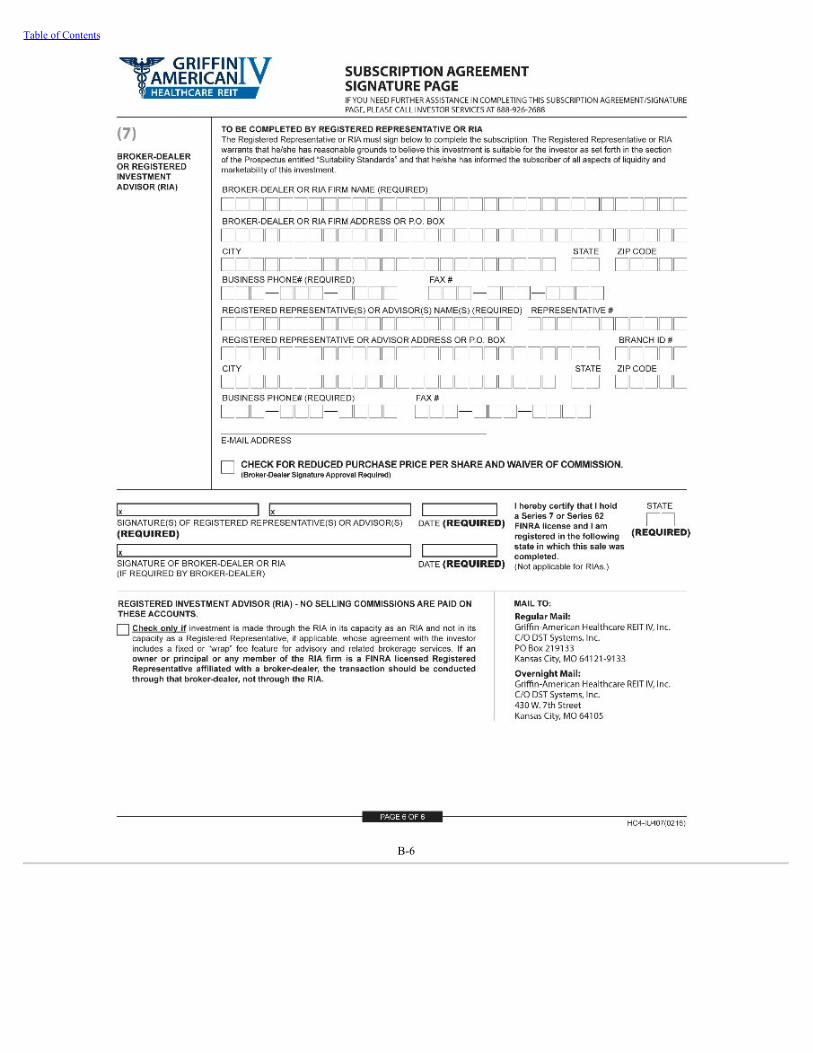

• Complete the execution copy of the Subscription Agreement. A specimen copy of the Subscription Agreement is included in this prospectus asExhibit B.

• Deliver the full purchase price of the shares of our common stock being subscribed for in the form of checks, drafts, wire, Automated ClearingHouse (ACH) or money orders, along with a completed, executed Subscription Agreement to your participating broker-dealer.

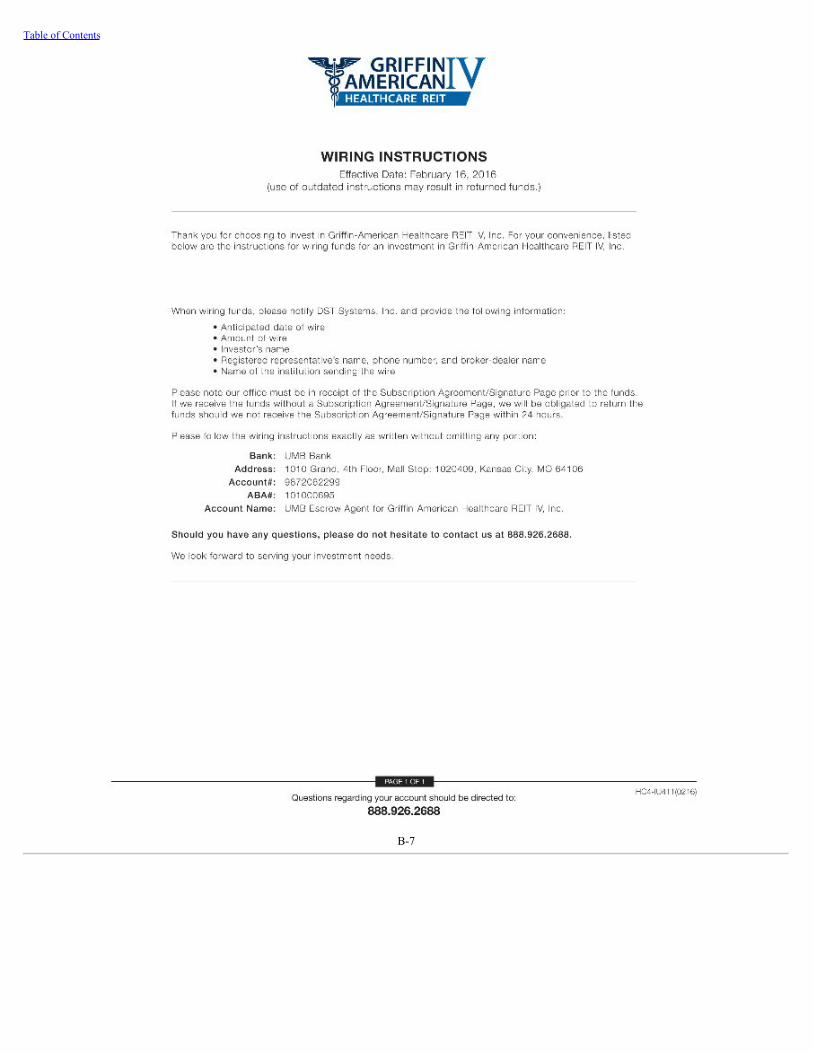

• Until such time as we have raised the minimum offering amount (or, for Ohio, Washington and Pennsylvania investors, we have raised a total of$10,000,000, $20,000,000 and $150,000,000, respectively), you should make your form(s) of payment payable to “UMB Bank Escrow Agent forGriffin-American Healthcare REIT IV, Inc.” After we have raised $2,000,000, we will notify our dealer manager and participating broker-dealersand after that you should make your form(s) of payment payable to “Griffin-American Healthcare REIT IV, Inc.,” except that (i) Ohio investorsshould continue to make their form(s) of payment payable to “UMB Bank Escrow Agent for Griffin-American Healthcare REIT IV, Inc.” until wehave received and accepted subscriptions for $10,000,000, at which point form(s) of payment should be made payable to “Griffin-AmericanHealthcare REIT IV, Inc.”; (ii) Washington investors should continue to make their form(s) of payment payable to “UMB Bank Escrow Agent forGriffin-American Healthcare REIT IV, Inc.” until we have received and accepted subscriptions for $20,000,000, at which point form(s) of paymentshould be made payable to “Griffin-American Healthcare REIT IV, Inc.”; and (iii) Pennsylvania investors should continue to make their form(s) ofpayment payable to “UMB Bank Escrow Agent for Griffin-American Healthcare REIT IV, Inc.” until we have received and accepted subscriptionsfor $150,000,000, at which point form(s) of payment should be made payable to “Griffin-American Healthcare REIT IV, Inc.”

By executing the Subscription Agreement and paying the total purchase price for the shares of our common stock subscribed for, each investor attests that heor she meets the minimum income and net worth standards we have established.

Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription, in whole or in part. An approved custodian ortrustee must process and forward to us subscriptions made through IRAs, Keogh plans, 401(k) plans and other tax-deferred plans. See the “Suitability Standards”and the “Plan of Distribution — Subscription Process” sections of this prospectus for additional details on how you can subscribe for shares of our common stock.

IMPORTANT NOTE ABOUT THIS PROSPECTUS

As used in this prospectus, the term “co-sponsors” refers to American Healthcare Investors, LLC and Griffin Capital Corporation, collectively; the terms“advisor” and “Griffin-American Advisor” refer to Griffin-American Healthcare REIT IV Advisor, LLC, an affiliate of our co-sponsors. As used in thisprospectus, the terms “our operating partnership” and “Healthcare REIT IV OP” refer to Griffin-American Healthcare REIT IV Holdings, LP, of which Griffin-American Healthcare REIT IV, Inc. is the sole general partner. The words “we,” “us” or “our” refer to Griffin-American Healthcare REIT IV, Inc. and ouroperating partnership, taken together, unless the context requires otherwise.

iv

TABLE OF CONTENTS

PageSUITABILITY STANDARDS iHOW TO SUBSCRIBE ivIMPORTANT NOTE ABOUT THIS PROSPECTUS ivQUESTIONS AND ANSWERS ABOUT THIS OFFERING 1PROSPECTUS SUMMARY 6RISK FACTORS 24CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS 60ESTIMATED USE OF PROCEEDS 61MANAGEMENT OF OUR COMPANY 64INVESTMENT OBJECTIVES, STRATEGY AND CRITERIA 83COMPENSATION TABLE 104SECURITY OWNERSHIP 113CONFLICTS OF INTEREST 114PRIOR PERFORMANCE SUMMARY 118MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS 135FEDERAL INCOME TAX CONSIDERATIONS 146TAX-EXEMPT ENTITIES AND ERISA CONSIDERATIONS 163DESCRIPTION OF CAPITAL STOCK 169DISTRIBUTION REINVESTMENT PLAN 177SHARE REPURCHASE PLAN 178CERTAIN PROVISIONS OF MARYLAND LAW AND OF OUR CHARTER AND BYLAWS 181THE OPERATING PARTNERSHIP AGREEMENT 184PLAN OF DISTRIBUTION 191REPORTS TO STOCKHOLDERS 197SUPPLEMENTAL SALES MATERIAL 197LEGAL MATTERS 197EXPERTS 197ELECTRONIC DELIVERY OF DOCUMENTS 198WHERE YOU CAN FIND ADDITIONAL INFORMATION 198

INDEX TO FINANCIAL STATEMENTS F-1EXHIBIT A: PRIOR PERFORMANCE TABLES A-1EXHIBIT B: FORM OF SUBSCRIPTION AGREEMENT B-1EXHIBIT C: DISTRIBUTION REINVESTMENT PLAN C-1EXHIBIT D: SHARE REPURCHASE PLAN D-1

v

Table of Contents

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

Set forth below are some of the more frequently asked questions and answers relating to our structure, our management, our business and an offering of thistype.

Q: What is a real estate investment trust, or REIT?

A: In general, a REIT is a company that:

• combines the capital of many investors to acquire or provide financing for real estate;

• pays annual distributions to investors of at least 90.0% of its taxable income (computed without regard to the dividends paid deduction and excluding netcapital gain);

• avoids the “double taxation” treatment of income that would normally result from investments in a corporation because a REIT is not generally subject tofederal corporate income taxes on net income that it distributes to stockholders; and

• enables individual investors to invest in a large-scale diversified real estate portfolio through the purchase of shares in the REIT.

Q: What is Griffin-American Healthcare REIT IV, Inc.?

A: Griffin-American Healthcare REIT IV, Inc. is a newly formed Maryland corporation that intends to qualify and elect to be taxed as a REIT for federal incometax purposes beginning with the taxable year ending December 31, 2016, or the first year in which we commence material operations. We do not have anyemployees and are externally managed by our advisor, Griffin-American Healthcare REIT IV Advisor, LLC, which we refer to as Griffin-American Advisoror our advisor.

Q: Who is your advisor and what is its relationship to Griffin-American Healthcare REIT IV, Inc.?

A: Our advisor is Griffin-American Healthcare REIT IV Advisor, LLC. Our advisor is jointly owned by our co-sponsors, American Healthcare Investors andGriffin Capital. American Healthcare Investors is the managing member and owns 75.0% of our advisor.

Q: What are some of the most significant risks relating to an investment in Griffin-American Healthcare REIT IV, Inc.?

A: An investment in our common stock is subject to a number of risks. Listed below are some of the most significant risks relating to your investment.

• There is no public market for the shares of our common stock. Shares of our common stock cannot be readily sold and there are significant restrictions onthe ownership, transferability and repurchase of shares of our common stock. If you are able to sell your shares of our common stock, you likely wouldhave to sell them at a substantial discount.

• We have no operating history or established financing sources. Therefore, you may not be able to adequately evaluate our ability to achieve ourinvestment objectives.

• This is a “blind pool” offering because we have not identified any real estate or real estate-related investments to acquire with the net proceeds from thisoffering. As a result, you will not be able to evaluate the economic merits of our investments prior to their purchase. We may be unable to invest the netproceeds from this offering on acceptable terms to investors, or at all.

• Until we generate operating cash flows sufficient to pay distributions to you, we may pay distributions from the net proceeds of this offering or fromborrowings in anticipation of future cash flows. We may also be required to sell assets or issue new securities for cash in order to pay distributions. Wehave not established any limit on the amount of offering proceeds or borrowings that may be used to fund distributions other than those limits imposed byour organizational documents and Maryland law, and it is likely that we will use offering proceeds to

1

Table of Contents

fund a majority of our initial years of distributions and that such distributions will represent a return of capital. We may also be required to sell assets orissue new securities for cash in order to pay distributions. Any such actions could reduce the amount of capital we ultimately invest in assets andnegatively impact the amount of income available for future distributions.

• We may incur substantial debt, which could hinder our ability to pay distributions to you or could decrease the value of your investment if the incomefrom, or the value of, the property securing our debt falls.

• This is a “best efforts” offering. If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio of real estateand real estate-related investments, and the value of your investment may fluctuate more widely with the performance of specific investments.

• We will rely on our advisor and its affiliates for our day-to-day operations and the selection of our investments. We will pay substantial fees to ouradvisor and its affiliates for these services, and the agreements governing these fees were not all negotiated at arm’s-length. In addition, fees payable toour dealer manager and our advisor in our organizational stage will be based upon the gross offering proceeds and not on our properties’ performance.Such agreements may require us to pay more than we would if we were only using unaffiliated third parties and may not solely reflect your interests as astockholder of our company.

• Our advisor may be entitled to receive significant compensation in the event of our liquidation or in connection with a termination of the advisoryagreement, even if such termination is the result of poor performance by our advisor.

• Many of our officers also are managing directors, officers and/or employees of one of our co-sponsors and other affiliated entities. As a result, our officerswill face conflicts of interest, including significant conflicts in allocating time and investment opportunities among us and similar programs sponsored byone of our co-sponsors or its affiliates.

• If we do not qualify as a REIT, we would be subject to federal income tax at regular corporate rates, which would adversely affect our operations and ourability to pay distributions to you.

• The amount of distributions we may pay, if any, is uncertain. Due to the risks involved in the ownership of real estate and real estate-related investments,there is no guarantee of any return on your investment in us and you may lose money.

• This is a fixed price offering. The fixed offering price was arbitrarily determined by our board of directors and may not accurately represent the currentvalue of our assets at any particular time.

• We are not obligated, through our charter or otherwise, to effectuate a liquidity event, and we may not effect a liquidity event within our targeted timeframe of five years after the completion of our offering stage, or at all. If we do not effect a liquidity event, you may have to hold your investment inshares of our common stock for an indefinite period of time.

• The healthcare industry is heavily regulated, and new laws or regulations, changes to existing laws or regulations, loss of licensure or failure to obtainlicensure could result in the inability of our tenants to make lease payments to us.

• Our board of directors may change our investment objectives without seeking your approval.

Q: How will you structure the ownership and operation of your assets?

A: We will own substantially all of our assets and conduct our operations through an operating partnership, Griffin-American Healthcare REIT IV Holdings, LP,which was organized in Delaware on January 23, 2015. We are the sole general partner of Griffin-American Healthcare REIT IV Holdings, LP, which werefer to as either Healthcare REIT IV OP or our operating partnership. Because we will conduct substantially all of our operations through an operatingpartnership, we are organized in what is referred to as an “UPREIT” structure.

2

Table of Contents

Q: What is an “UPREIT”?

A: UPREIT stands for Umbrella Partnership Real Estate Investment Trust. We use the UPREIT structure because a contribution of property directly to us isgenerally a taxable transaction to the contributing property owner. In this structure, a contributor of a property who desires to defer taxable gain on thetransfer of his or her property may transfer the property to the partnership in exchange for limited partnership units and defer taxation of gain until thecontributor later exchanges his or her limited partnership units, normally on a one-for-one basis, for shares of common stock of the REIT. We believe thatusing an UPREIT structure gives us an opportunity to acquire desired properties from persons who may not otherwise sell their properties because ofunfavorable tax results.

Q: What will you do with the money raised in this offering?

A: We intend to use the net proceeds from this offering to acquire a diversified portfolio of real estate properties, focusing primarily on medical office buildings,hospitals, skilled nursing facilities, senior housing and other healthcare-related facilities. We may also originate and acquire secured loans and other realestate-related investments on an infrequent and opportunistic basis. We generally will seek investments that produce current income. The diversification ofour portfolio will depend upon the amount of proceeds we receive in this offering. We estimate that 91.9% of the gross offering proceeds will be used topurchase real estate and real estate-related investments, pay down debt or to fund distributions if our cash flows from operations are insufficient, and theremaining 8.1% will be used to pay the costs of this offering, including selling commissions and the dealer manager fee, and to pay fees to our advisor for itsservices in connection with the selection and acquisition of properties. In addition, we will pay fees from our cash flows from operations, including thestockholder servicing fee, as described in the “Compensation Table” section of this prospectus. If our cash flows from operations are not sufficient to pay thestockholder servicing fee, we will pay the stockholder servicing fee through borrowings in anticipation of future cash flows. Until we invest all the proceedsof this offering in our targeted investments, we may invest in short-term, highly liquid or other authorized investments. Such short-term investments will notearn significant returns, and we cannot guarantee how long it will take to fully invest all the net proceeds from this offering in targeted investments. Becausewe have not acquired or identified any investment opportunities, this offering is considered a “blind pool.”

Q: What kind of offering is this?

A: Through Griffin Capital Securities, LLC, which we refer to as Griffin Securities or our dealer manager, we are offering a maximum of $3,000,000,000 inshares of our common stock in our primary offering, all of which are Class T shares, at a price of $10.00 per share. These shares are being offered on a “bestefforts” basis. We are also offering $150,000,000 in shares of our common stock pursuant to the DRIP to those stockholders who elect to participate in suchplan, as described in this prospectus, at a price of 95.0% of the primary offering price per share, or $9.50 assuming a $10.00 per share primary offering price.We reserve the right to reallocate the shares of common stock we are offering between our primary offering and the DRIP, and among classes of stock if weelect to offer additional classes in the future.

Q: How does a “best efforts” offering work?

A: When securities are offered to the public on a “best efforts” basis, the broker-dealers participating in the offering are only required to use their best efforts tosell the securities and have no firm commitment or obligation to purchase any of the securities. Because this is a “best efforts” offering, we cannot guaranteethat any specific number of shares of our common stock will be sold. We intend to admit stockholders periodically as subscriptions for shares of our commonstock are received, but not less frequently than monthly.

Q: How long will this offering last?

A: We may sell shares of our common stock in this offering until the earlier of the date on which the maximum offering amount has been sold or February 16,2018; provided however, that our board of directors may extend this offering for an additional year or as otherwise permitted under applicable law, or wemay extend this offering with respect to shares of our common stock offered pursuant to the DRIP. We also reserve the right to terminate this offering at anytime.

Q: Who can buy shares of Griffin-American Healthcare REIT IV common stock?

3

Table of Contents

A: Generally, you can buy shares of our common stock pursuant to this prospectus provided that you have either (1) a net worth of at least $250,000, or (2) agross annual income of at least $70,000 and a net worth of at least $70,000. For this purpose, net worth does not include your home, home furnishings orpersonal automobiles. However, these minimum levels are higher in certain states, so you should carefully read the more detailed description under“Suitability Standards” beginning on page i of this prospectus.

Q: For whom is an investment in shares of our common stock appropriate?

A: An investment in shares of our common stock may be appropriate for you if you meet the minimum suitability standards mentioned above, seek to diversifyyour personal portfolio with a real estate-based investment, seek to receive current income, seek to preserve capital, wish to obtain the benefits of potentiallong-term capital appreciation and are able to hold your investment for a time period consistent with our liquidity plans. On the other hand, we cautionpersons who require immediate liquidity or guaranteed income, or who seek a short-term investment, that an investment in shares of our common stock willnot meet those needs.

Q: May I make an investment through my IRA, SEP plan or other tax-deferred account?

A: Yes. You may make an investment through your IRA, simplified employee pension, or SEP, plan or other tax-deferred account. In making these investmentdecisions, you should consider, at a minimum: (1) whether the investment is in accordance with the documents and instruments governing your IRA, SEPplan or other tax-deferred account; (2) whether the investment satisfies the fiduciary requirements associated with your IRA, SEP plan or other tax-deferredaccount; (3) whether the investment will generate unrelated business taxable income, or UBTI, to your IRA, SEP plan or other tax-deferred account;(4) whether there is sufficient liquidity for such investment under your IRA, SEP plan or other tax-deferred account; (5) the need to value the assets of yourIRA, SEP plan or other tax-deferred account annually or more frequently; and (6) whether the investment would constitute a prohibited transaction underapplicable law. You should also consider any investment restrictions imposed by the Employee Retirement Income Security Act of 1974, as amended, orERISA, and the Internal Revenue Code. See the “Federal Income Tax Considerations” and “Tax-Exempt Entities and ERISA Considerations” sections of thisprospectus for additional information.

Q: Is there any minimum investment required?

A: Yes. The minimum initial investment is at least $2,500, except for purchases by (1) our existing stockholders, including purchases made pursuant to theDRIP, and (2) existing investors in other programs sponsored by our co-sponsors, or any of our co-sponsors’ affiliates, which may be in lesser amounts;provided however, that the minimum initial investment for purchases made by an IRA is at least $1,500.

Q: How do I subscribe for shares of Griffin-American Healthcare REIT IV common stock?

A: You must meet the suitability standards described in the “Suitability Standards” section of this prospectus in order to purchase shares of our common stock inthis offering. If you would like to purchase shares of our common stock, please proceed as directed in the “How to Subscribe” section of this prospectus.

Q: If I buy shares of common stock, will I receive distributions and how often?

A: Provided we have sufficient available cash flow, we expect to pay distributions on a monthly basis to our stockholders. Our distribution policy will be set byour board of directors and is subject to change based on available cash flow. Once our board of directors authorizes distributions, we expect that suchdistributions will have a daily record date so your distribution benefits will begin to accrue immediately upon becoming a stockholder. However, we cannotguarantee the amount of distributions we will pay, if any.

Q: Will the distributions I receive be taxable as ordinary income?

A: If you are a taxable stockholder, distributions that you receive, including distributions that are reinvested pursuant to the DRIP, generally will be taxed asordinary income to the extent they are from our current or accumulated earnings and profits, unless we have designated all or a portion of the distribution as acapital gain distribution. In such case, such designated portion of the distribution will be treated as a capital gain. To the extent that we pay a distribution inexcess of our current and accumulated earnings and profits, the distribution will be treated first as a tax-free return of capital, reducing the tax basis in yourshares of our common stock, and the amount of each

4

Table of Contents

distribution in excess of your tax basis in your shares of our common stock will be taxable as a gain realized from the sale of your shares of our commonstock.

For example, because depreciation expense reduces taxable income but does not reduce cash available for distribution, if our distributions exceed our currentand accumulated earnings and profits, the portion of such distributions to you exceeding our current and accumulated earnings and profits (to the extent ofyour positive basis in your shares of our common stock) will be considered a return of capital to you for tax purposes. These amounts will not be subject toincome tax immediately but will instead reduce the tax basis of your investment, in effect, deferring a portion of your income tax until you sell your shares ofour common stock or we liquidate, assuming we do not pay any future distributions in excess of our current and accumulated earnings and profits at a timethat your tax basis in your shares of our common stock is zero. If you are a tax-exempt entity, distributions from us generally will not constitute UBTI, unlessyou have borrowed to acquire or carry your stock or have used the shares of our common stock in a trade or business. There are exceptions to this rule forcertain types of tax-exempt entities. Because each investor’s tax considerations are different, especially the treatment of tax-exempt entities, we suggest thatyou consult with your tax advisor. See the “Federal Income Tax Considerations — Taxation of Taxable U.S. Stockholders,” the “Federal Income TaxConsiderations — Taxation of Tax-Exempt Stockholders” and the “Distribution Reinvestment Plan” sections of this prospectus.

Q: May I reinvest my distributions?

A: Yes. See the “Distribution Reinvestment Plan” section of this prospectus for more information regarding the DRIP.

Q: If I buy shares of common stock in this offering, how may I later sell them?

A: At the time you purchase shares of our common stock, they will not be listed for trading on any national securities exchange. As a result, if you wish to sellyour shares of our common stock, you may not be able to do so promptly or at all, or you may only be able to sell them at a substantial discount from theprice you paid. In general, however, you may sell your shares of our common stock to any buyer that meets the applicable suitability standards unless suchsale would cause the buyer to own more than 9.9% of the value of shares of our then outstanding capital stock (which includes common stock and anypreferred stock we may issue) or more than 9.9% of the value or number of shares, whichever is more restrictive, of our then outstanding common stock. Seethe “Suitability Standards” and the “Description of Capital Stock — Restrictions on Ownership and Transfer” sections of this prospectus. We have adopted ashare repurchase plan, or our share repurchase plan, as discussed under the “Share Repurchase Plan” section of this prospectus, which may provide limitedliquidity for some of our stockholders.

Q: Will I be notified of how my investment is doing?

A: Yes. You will receive periodic updates on the performance of your investment with us, including:

• four quarterly investment statements, which will generally include a summary of the amount you have invested, the monthly distributions paid and theamount of distributions reinvested pursuant to the DRIP, as applicable;

• an annual report after the end of each year; and

• an annual Internal Revenue Service, or IRS, Form 1099, if applicable, after the end of each year.

Q: When will I get my detailed tax information?

A: Your Form 1099-DIV tax information will be mailed by January 31 of each year.

Q: Who can help answer my questions?

A: If you have any questions regarding this offering or if you would like additional copies of this prospectus, you should contact your registered representativeor:

Griffin Capital Securities, LLC18191 Von Karman Avenue, Suite 300Irvine, California 92612Telephone: (949) 270-9300

5

Table of Contents

PROSPECTUS SUMMARY

This prospectus summary highlights material information contained elsewhere in this prospectus. Because it is a summary, it may not contain all ofthe information that is important to your decision whether to invest in shares of our common stock. To understand this offering fully, you should read theentire prospectus carefully, including the “Risk Factors” section.

Griffin-American Healthcare REIT IV, Inc.We were formed as a Maryland corporation on January 23, 2015. We intend to provide investors the potential for income and growth through

investment in a diversified portfolio of real estate properties, focusing primarily on medical office buildings, hospitals, skilled nursing facilities, seniorhousing and other healthcare-related facilities. We also may originate and acquire secured loans and other real estate-related investments on an infrequentand opportunistic basis. We generally will seek investments that produce current income. We intend to qualify and elect to be taxed as a REIT under theInternal Revenue Code beginning with our taxable year ending December 31, 2016, or the first year in which we commence material operations.

Our headquarters are located at 18191 Von Karman Avenue, Suite 300, Irvine, California 92612 and our telephone number is (949) 270-9200. Weintend to maintain a website at www.healthcarereitiv.com where you can find additional information about us. The contents of that website are notincorporated by reference in, or otherwise a part of, this prospectus.

Summary Risk FactorsAn investment in our common stock is subject to a number of risks. Listed below are some of the most significant risks relating to your investment.• There is no public market for the shares of our common stock. Shares of our common stock cannot be readily sold and there are significant

restrictions on the ownership, transferability and repurchase of shares of our common stock. If you are able to sell your shares of our commonstock, you likely would have to sell them at a substantial discount.

• We have no operating history or established financing sources. Therefore, you may not be able to adequately evaluate our ability to achieve ourinvestment objectives.

• This is a “blind pool” offering because we have not identified any real estate or real estate-related investments to acquire with the net proceedsfrom this offering. As a result, you will not be able to evaluate the economic merits of our investments prior to their purchase. We may beunable to invest the net proceeds from this offering on acceptable terms to investors, or at all.

• Until we generate operating cash flows sufficient to pay distributions to you, we may pay distributions from the net proceeds of this offering orfrom borrowings in anticipation of future cash flows. We may also be required to sell assets or issue new securities for cash in order to paydistributions. We have not established any limit on the amount of offering proceeds or borrowings that may be used to fund distributions otherthan those limits imposed by our organizational documents and Maryland law, and it is likely that we will use offering proceeds to fund amajority of our initial years of distributions and that such distributions will represent a return of capital. We may also be required to sell assets orissue new securities for cash in order to pay distributions. Any such actions could reduce the amount of capital we ultimately invest in assets andnegatively impact the amount of income available for future distributions.

• We may incur substantial debt, which could hinder our ability to pay distributions to you or could decrease the value of your investment if theincome from, or the value of, the property securing our debt falls.

• This is a “best efforts” offering. If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio ofreal estate and real estate-related investments, and the value of your investment may fluctuate more widely with the performance of specificinvestments.

• We will rely on our advisor and its affiliates for our day-to-day operations and the selection of our investments. We will pay substantial fees toour advisor and its affiliates for these services, and the agreements governing these fees were not all negotiated at arm’s-length. In addition, feespayable to our dealer manager and our advisor in our organizational stage will be based upon the gross offering proceeds and not on ourproperties’ performance. Such agreements may require us to pay more than we would if we were only using unaffiliated third parties and maynot solely reflect your interests as a stockholder of our company.

• Our advisor may be entitled to receive significant compensation in the event of our liquidation or in connection with a termination of theadvisory agreement, even if such termination is the result of poor performance by our advisor.

6

Table of Contents

• Many of our officers also are managing directors, officers and/or employees of one of our co-sponsors and other affiliated entities. As a result,our officers will face conflicts of interest, including significant conflicts in allocating time and investment opportunities among us and similarprograms sponsored by one of our co-sponsors or its affiliates.

• If we do not qualify as a REIT, we would be subject to federal income tax at regular corporate rates, which would adversely affect ouroperations and our ability to pay distributions to you.

• The amount of distributions we may pay, if any, is uncertain. Due to the risks involved in the ownership of real estate and real estate-relatedinvestments, there is no guarantee of any return on your investment in us and you may lose money.

• This is a fixed price offering. The fixed offering price was arbitrarily determined by our board of directors and may not accurately represent thecurrent value of our assets at any particular time.

• We are not obligated, through our charter or otherwise, to effectuate a liquidity event, and we may not effect a liquidity event within our targetedtime frame of five years after the completion of our offering stage, or at all. If we do not effect a liquidity event, you may have to hold yourinvestment in shares of our common stock for an indefinite period of time.

• The healthcare industry is heavily regulated, and new laws or regulations, changes to existing laws or regulations, loss of licensure or failure toobtain licensure could result in the inability of our tenants to make lease payments to us.

• Our board of directors may change our investment objectives without seeking your approval.

Investment ObjectivesOur investment objectives are:• to preserve, protect and return your capital contributions;• to pay regular cash distributions; and• to realize growth in the value of our investments upon our ultimate sale of such investments.

See the “Investment Objectives, Strategy and Criteria” section of this prospectus for a more complete description of our business and objectives.

Description of InvestmentsWe generally will seek to acquire a diversified portfolio of real estate properties, focusing primarily on medical office buildings, hospitals, skilled

nursing facilities, senior housing and other healthcare-related facilities, such as long-term acute care centers, surgery centers, memory care facilities,specialty medical and diagnostic service facilities, laboratories and research facilities, pharmaceutical and medical supply manufacturing facilities andoffices leased to tenants in healthcare-related industries. We generally will seek investments that produce current income. We may acquire propertieseither alone or jointly with another party. We also may originate or acquire secured loans and other real estate-related investments on an infrequent andopportunistic basis. Our real estate-related investments may include mortgage, mezzanine, bridge and other loans, common and preferred stock of, orother interests in, public or private unaffiliated real estate companies, commercial mortgage-backed securities, and certain other securities, includingcollateralized debt obligations and foreign securities.

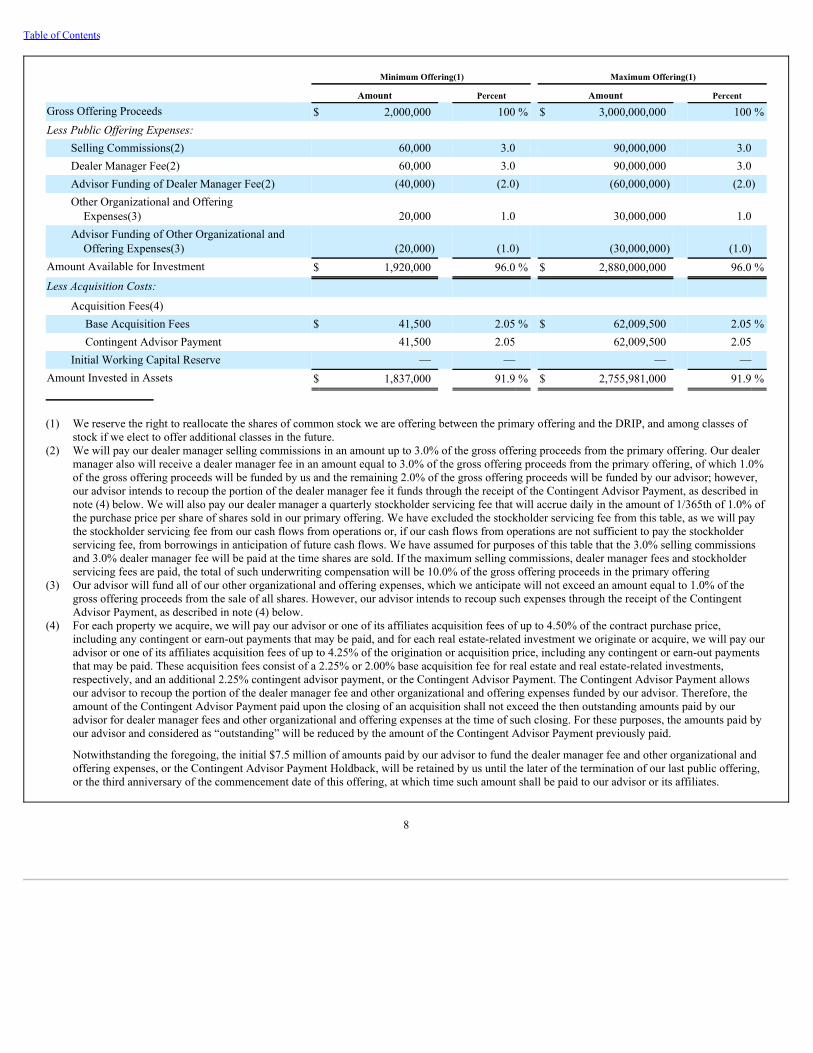

Estimated Use of Proceeds Depending primarily on the number of shares of our common stock we sell pursuant to this offering and assuming no shares are reallocated from

the DRIP to our primary offering and the maximum primary offering amount of $3,000,000,000 is raised in the manner described in the “Estimated Useof Proceeds” section of this prospectus, we estimate that approximately 91.9% of the gross offering proceeds will be used to purchase real estate and realestate-related investments, pay down debt or to fund distributions if our cash flows from operations are insufficient. We have not established any limit onthe amount of offering proceeds that may be used to fund distributions other than those limits imposed by our organizational documents and Marylandlaw, and it is likely that we will use offering proceeds to fund a majority of our initial distributions. We expect that the remaining 8.1% will be used topay the costs of this offering, including selling commissions and the dealer manager fee, and to pay fees to our advisor for its services in connection withthe selection and acquisition of properties. We will not pay selling commissions, a dealer manager fee or other organizational and offering expenses withrespect to shares of our common stock sold pursuant to the DRIP; therefore, a greater percentage of the proceeds to us from such sales will be used topurchase real estate and real estate-related investments, and to fund our share repurchase plan.

7

Table of Contents

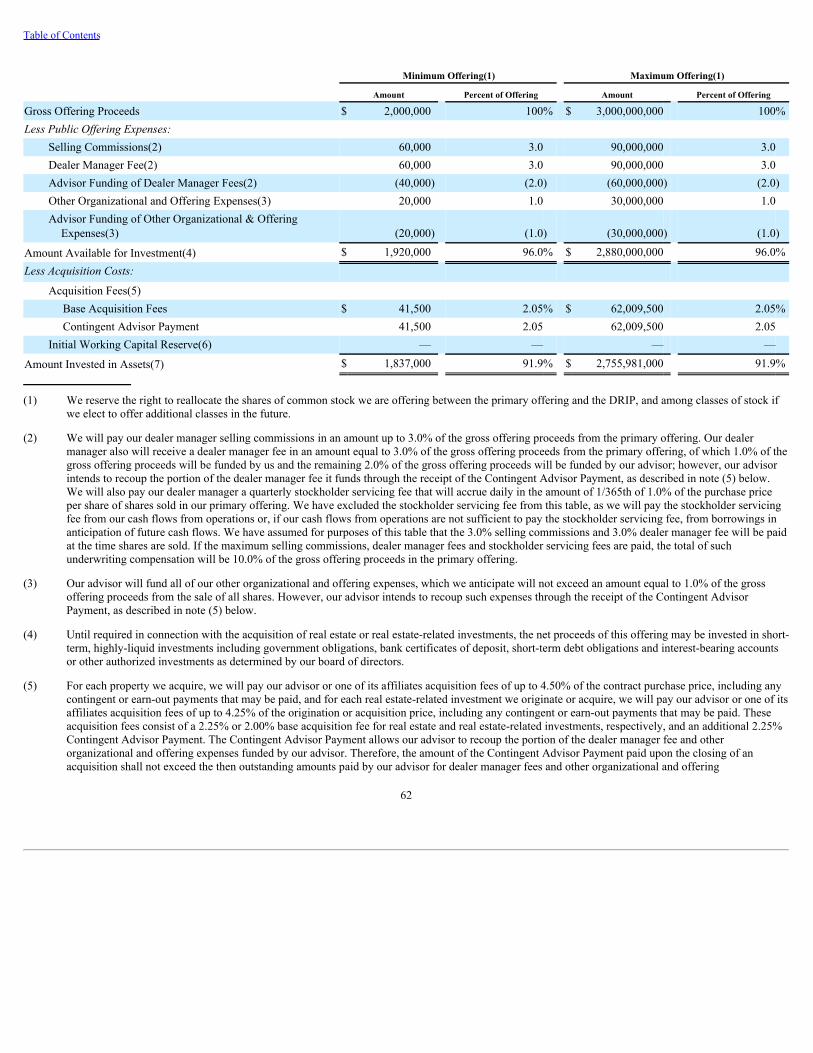

Minimum Offering(1) Maximum Offering(1)

Amount Percent Amount Percent

Gross Offering Proceeds $ 2,000,000 100 % $ 3,000,000,000 100 %Less Public Offering Expenses:

Selling Commissions(2) 60,000 3.0 90,000,000 3.0Dealer Manager Fee(2) 60,000 3.0 90,000,000 3.0Advisor Funding of Dealer Manager Fee(2) (40,000) (2.0) (60,000,000) (2.0)Other Organizational and Offering

Expenses(3) 20,000 1.0 30,000,000 1.0Advisor Funding of Other Organizational and

Offering Expenses(3) (20,000) (1.0) (30,000,000) (1.0)Amount Available for Investment $ 1,920,000 96.0 % $ 2,880,000,000 96.0 %Less Acquisition Costs:

Acquisition Fees(4) Base Acquisition Fees $ 41,500 2.05 % $ 62,009,500 2.05 %Contingent Advisor Payment 41,500 2.05 62,009,500 2.05

Initial Working Capital Reserve — — — —Amount Invested in Assets $ 1,837,000 91.9 % $ 2,755,981,000 91.9 %

(1) We reserve the right to reallocate the shares of common stock we are offering between the primary offering and the DRIP, and among classes of

stock if we elect to offer additional classes in the future.(2) We will pay our dealer manager selling commissions in an amount up to 3.0% of the gross offering proceeds from the primary offering. Our dealer

manager also will receive a dealer manager fee in an amount equal to 3.0% of the gross offering proceeds from the primary offering, of which 1.0%of the gross offering proceeds will be funded by us and the remaining 2.0% of the gross offering proceeds will be funded by our advisor; however,our advisor intends to recoup the portion of the dealer manager fee it funds through the receipt of the Contingent Advisor Payment, as described innote (4) below. We will also pay our dealer manager a quarterly stockholder servicing fee that will accrue daily in the amount of 1/365th of 1.0% ofthe purchase price per share of shares sold in our primary offering. We have excluded the stockholder servicing fee from this table, as we will paythe stockholder servicing fee from our cash flows from operations or, if our cash flows from operations are not sufficient to pay the stockholderservicing fee, from borrowings in anticipation of future cash flows. We have assumed for purposes of this table that the 3.0% selling commissionsand 3.0% dealer manager fee will be paid at the time shares are sold. If the maximum selling commissions, dealer manager fees and stockholderservicing fees are paid, the total of such underwriting compensation will be 10.0% of the gross offering proceeds in the primary offering

(3) Our advisor will fund all of our other organizational and offering expenses, which we anticipate will not exceed an amount equal to 1.0% of thegross offering proceeds from the sale of all shares. However, our advisor intends to recoup such expenses through the receipt of the ContingentAdvisor Payment, as described in note (4) below.

(4) For each property we acquire, we will pay our advisor or one of its affiliates acquisition fees of up to 4.50% of the contract purchase price,including any contingent or earn-out payments that may be paid, and for each real estate-related investment we originate or acquire, we will pay ouradvisor or one of its affiliates acquisition fees of up to 4.25% of the origination or acquisition price, including any contingent or earn-out paymentsthat may be paid. These acquisition fees consist of a 2.25% or 2.00% base acquisition fee for real estate and real estate-related investments,respectively, and an additional 2.25% contingent advisor payment, or the Contingent Advisor Payment. The Contingent Advisor Payment allowsour advisor to recoup the portion of the dealer manager fee and other organizational and offering expenses funded by our advisor. Therefore, theamount of the Contingent Advisor Payment paid upon the closing of an acquisition shall not exceed the then outstanding amounts paid by ouradvisor for dealer manager fees and other organizational and offering expenses at the time of such closing. For these purposes, the amounts paid byour advisor and considered as “outstanding” will be reduced by the amount of the Contingent Advisor Payment previously paid.

Notwithstanding the foregoing, the initial $7.5 million of amounts paid by our advisor to fund the dealer manager fee and other organizational andoffering expenses, or the Contingent Advisor Payment Holdback, will be retained by us until the later of the termination of our last public offering,or the third anniversary of the commencement date of this offering, at which time such amount shall be paid to our advisor or its affiliates.

8

Table of Contents

For purposes of this table, the 2.25% base acquisition fee and the 2.25% Contingent Advisor Payment are applied against the amount invested inassets shown in the table. However, the percentages that appear in this table are stated as a percentage of the gross offering proceeds shown in thetable. As a result, the base acquisition fee and the Contingent Advisor Payment stated in the table each represent approximately 2.05% of the grossoffering proceeds shown in the table.

Acquisition fees may be paid in connection with the purchase, development or construction of real properties, or the making of or investing in loansor other real estate-related investments. Acquisition fees do not include acquisition expenses, which may be paid from offering proceeds. Forpurposes of this table, we have assumed that (a) no real estate-related investments are originated or acquired and (b) no debt is incurred in respect ofany property acquisitions. However, as disclosed throughout this prospectus, we expect to use leverage, which results in higher fees paid to ouradvisor and its affiliates. Assuming, in addition to our other assumptions, a maximum leverage of 50.0% of our assets, the maximum acquisitionfees (including the Contingent Advisor Payment) would be approximately $214,768,000. Furthermore, under our charter, we have a limitation onborrowing that precludes us from borrowing in excess of 300% of our net assets without the approval of a majority of our independent directors.Generally speaking, the preceding calculation is expected to approximate 75.0% of the aggregate cost of our real estate and real estate-relatedinvestments before depreciation, amortization, bad debt and other similar non-cash reserves. Assuming, in addition to our other assumptions, amaximum leverage of 75.0% of the aggregate cost of our real estate and real estate-related investments before depreciation, amortization, bad debtand other similar non-cash reserves, the maximum acquisition fees (including the Contingent Advisor Payment) would be approximately$341,516,000. These assumptions may change due to different factors including changes in the allocation of shares of our common stock betweenthe primary offering and the DRIP, the extent to which proceeds from the DRIP are used to repurchase shares of our common stock pursuant to ourshare repurchase plan and the extent to which we make real estate-related investments. To the extent that we issue new shares of our common stockoutside of this offering or interests in our operating partnership in order to acquire real properties, then the acquisition fees and amounts invested inreal properties will exceed the amount stated above.

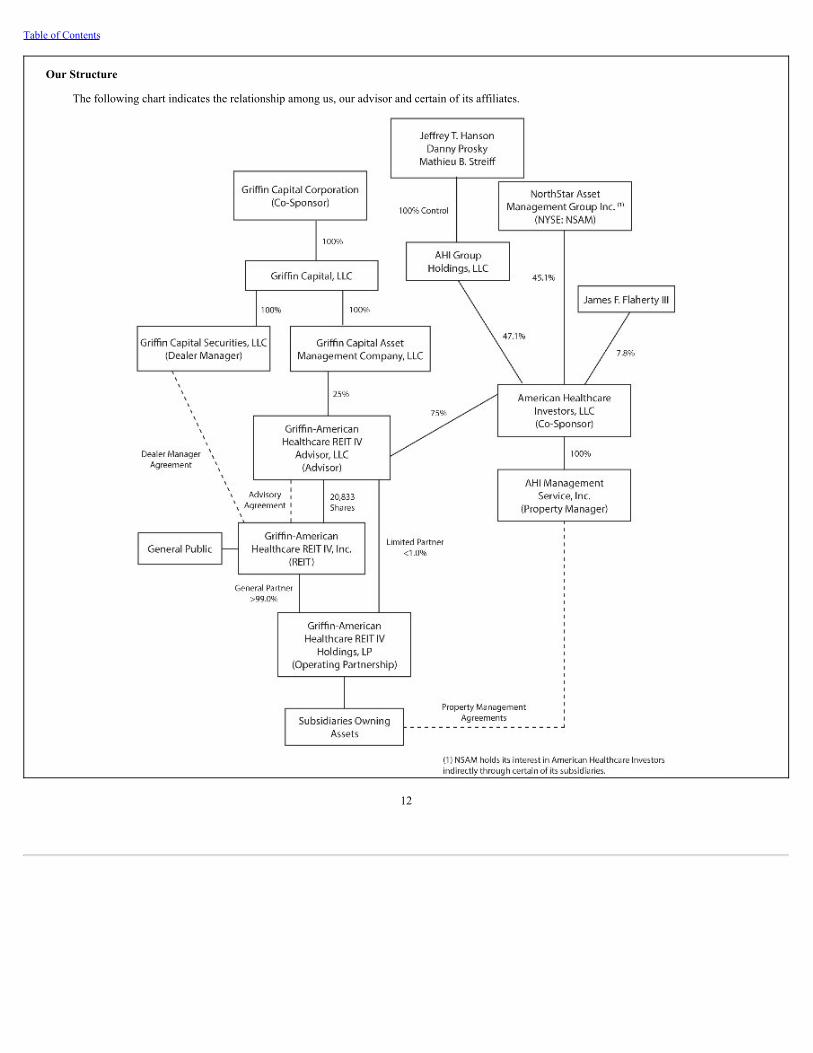

Our AdvisorWe are advised by Griffin-American Advisor. Our advisor is a subsidiary of and jointly owned by our co-sponsors, American Healthcare Investors

and Griffin Capital. Our advisor, which was formed in Delaware on January 23, 2015, is responsible for supervising and managing our day-to-dayoperations.

Our advisor will use its best efforts, subject to the oversight and review of our board of directors, to, among other things, research, identify, reviewand make investments in and dispositions of properties and securities on our behalf consistent with our investment policies and objectives. Our advisorwill perform its duties and responsibilities under an advisory agreement, or the advisory agreement, as our fiduciary. All of our officers are managingdirectors or employees of American Healthcare Investors or its affiliates.

Our Co-SponsorsAmerican Healthcare Investors

American Healthcare Investors, the managing member and 75.0% owner of our advisor, is an investment management firm formed in October 2014that specializes in the acquisition and management of healthcare-related real estate. American Healthcare Investors is 47.1% owned by AHI GroupHoldings, LLC (formerly known as American Healthcare Investors LLC), or AHI Group Holdings, an investment management firm formed in August2011 that has specialized in the acquisition and management of healthcare-related real estate and founded by Jeffrey T. Hanson, our Chief ExecutiveOfficer and Chairman of our Board of Directors; Danny Prosky, our President, Chief Operating Officer and Interim Chief Financial Officer; and MathieuB. Streiff, our Executive Vice President and General Counsel. Nationally recognized real estate executives, Messrs. Hanson, Prosky and Streiff havedirectly overseen in excess of $23.0 billion in combined acquisition and disposition transactions, more than $13.0 billion of which has been healthcare-related. NorthStar Asset Management Group Inc. (NYSE: NSAM), or NSAM, indirectly owns approximately 45.1% of American Healthcare Investorsand Mr. James F. Flaherty III, one of NSAM’s partners and the former Chairman and Chief Executive Officer of HCP, Inc., a publicly-traded healthcareREIT, owns approximately 7.8% of American Healthcare Investors. NSAM and its affiliates serve as the advisor and/or sponsor to other investmentvehicles that invest in healthcare real estate and healthcare real estate-related assets, as well as other assets.

American Healthcare Investors manages a 29 million-square-foot portfolio of healthcare real estate valued at approximately $8.0 billion, based onaggregate purchase price, on behalf of multiple investment programs that include thousands of individual and institutional investors. As of February 1,2016, this international portfolio includes approximately

9

Table of Contents

590 buildings comprised of medical office buildings, hospitals, senior housing, skilled nursing facilities and integrated senior care campuses locatedthroughout the United States and the United Kingdom.

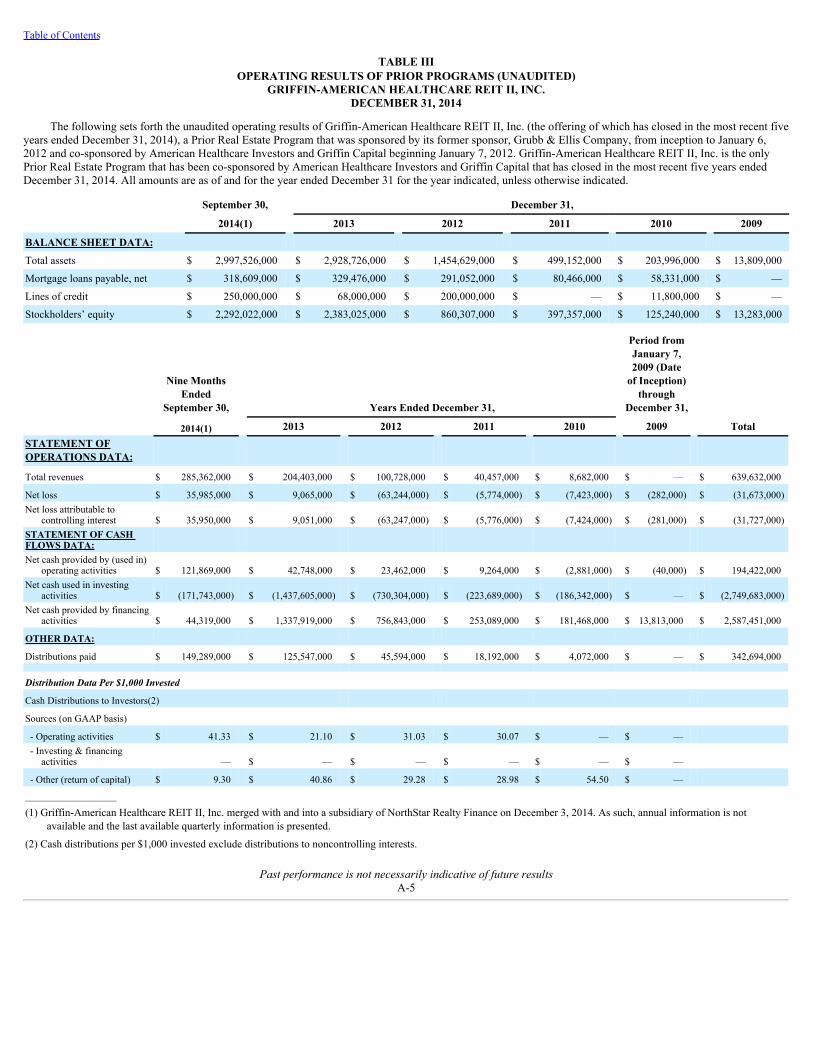

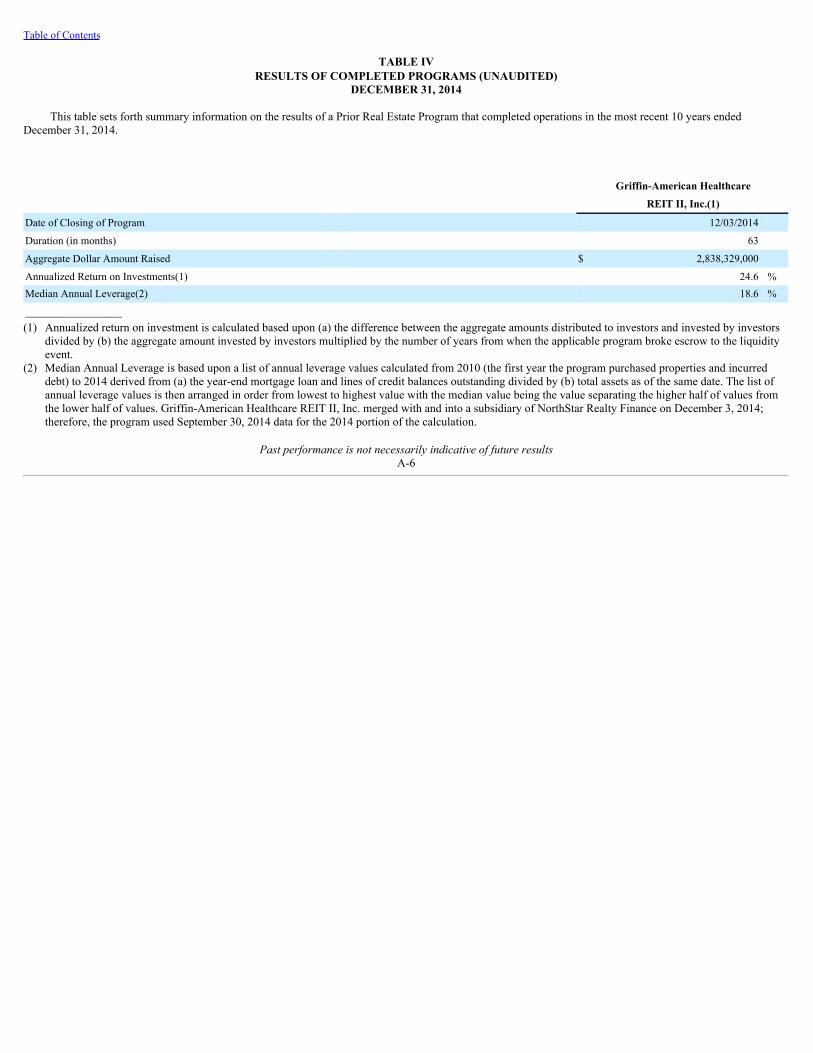

Included in this managed portfolio are properties owned by Griffin-American Healthcare REIT III, Inc., or GA Healthcare REIT III, a publicly-registered, non-traded REIT co-sponsored by American Healthcare Investors. GA Healthcare REIT III is the only other real estate program currentlysponsored by American Healthcare Investors, although American Healthcare Investors previously served as the co-sponsor of Griffin-AmericanHealthcare REIT II, Inc., or GA Healthcare REIT II, a publicly-registered, non-traded REIT that was acquired by NorthStar Realty Finance Corp., orNorthStar Realty Finance, a diversified commercial real estate company that is organized as a publicly-traded REIT listed on the NYSE and is externallymanaged by affiliates of NSAM, pursuant to a merger with GA Healthcare REIT II in December 2014 for approximately $4 billion in a combination ofcommon stock and cash. Prior to the completion of the merger, GA Healthcare REIT II had completed 77 acquisitions comprising approximately 11.6million square feet of GLA for an aggregate contract purchase price of approximately $3 billion.

Griffin CapitalGriffin Capital is a privately-owned real estate company with a 21-year track record sponsoring real estate investment vehicles and managing

institutional capital. Led by senior executives, each with more than two decades of real estate experience who have collectively closed more than 650transactions representing over $22.0 billion in transaction value, Griffin Capital and its affiliates have acquired or constructed approximately 53.6 millionsquare feet of space since 1995. As of February 1, 2016, Griffin Capital and its affiliates own, manage, sponsor and/or co-sponsor a portfolio consistingof approximately 36.6 (1) million square feet of space located in 29 states and 0.1 million square feet located in the United Kingdom, representingapproximately $6.3 (1) billion in asset value, based on purchase price, including GA Healthcare REIT III. Griffin Capital also is the sponsor of GriffinCapital Essential Asset REIT, Inc., or GC REIT, and Griffin Capital Essential Asset REIT II, Inc., or GC REIT II, each of which is a publicly-registered,non-traded REIT, and is the co-sponsor of GA Healthcare REIT III. Griffin Capital is also the sponsor of Griffin-Benefit Street Partners BDC Corp., orGB-BDC, a non-diversified, closed-end management investment company that intends to elect to be regulated as a business development company, orBDC, under the Investment Company Act, and Griffin Institutional Access Real Estate Fund, or GIREX, a non-diversified, closed-end managementinvestment company that is operated as an interval fund under the Investment Company Act. Griffin Securities serves as the dealer manager for GC REITII, GB-BDC and our company, and as the exclusive wholesale marketing agent for GIREX. Griffin Securities also previously served as the dealermanager for GA Healthcare REIT II and GA Healthcare REIT III. Griffin Capital, through its indirect wholly-owned subsidiary, Griffin Capital AssetManagement Company, LLC, indirectly owns 25.0% of our advisor.

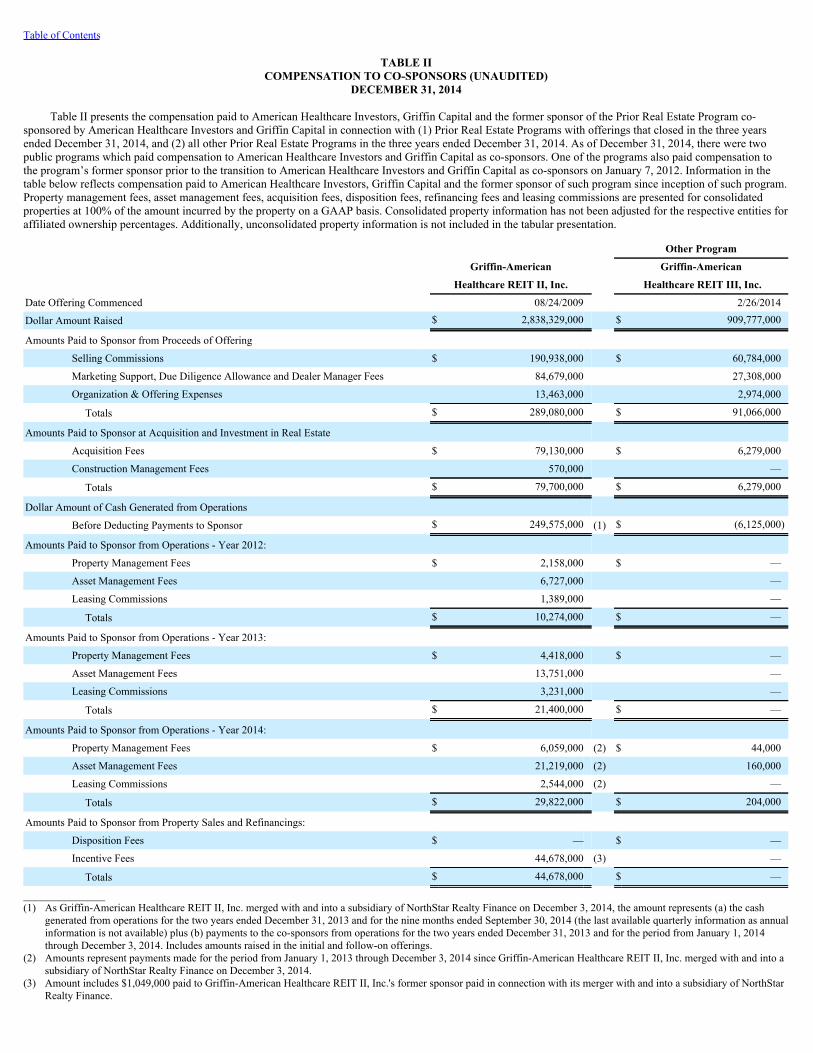

Please see the “Management of Our Company — Our Co-Sponsors” section beginning on page 73 and the “Prior Performance Summary” sectionbeginning on page 118 for a description of the programs sponsored by American Healthcare Investors and Griffin Capital and a discussion of the materialadverse business developments experienced by such programs.

Our Dealer ManagerGriffin Securities, an affiliate of Griffin Capital, serves as our dealer manager for this offering.

Our Board of Directors and Executive OfficersWe operate under the direction of our board of directors, the members of which are accountable to us and our stockholders as fiduciaries. The board

of directors is responsible for the management and control of our affairs. Our board of directors consists of five members, two of which are designated byAHI Group Holdings (one of such designees is independent of our co-sponsors, our advisor or any of their affiliates), two of which are designated byNSAM (one of such designees is independent of our co-sponsors, our advisor or any of their affiliates), and one of which (who is independent of our co-sponsors, our advisor or any of their affiliates) is mutually agreed upon by AHI Group Holdings and NSAM. Currently, we have five directors, Jeffrey T.Hanson, Ronald J. Lieberman, Brian J. Flornes, Dianne Hurley and Wilbur J. Smith III. Messrs. Hanson and Smith have been designated by AHI GroupHoldings, Mr. Lieberman and Ms. Hurley have been designated by NSAM and Mr. Flornes has been mutually agreed upon by AHI Group Holdings andNSAM. Ms. Hurley and Messrs. Flornes and Smith are each independent of our co-sponsors, our advisor, or any of their affiliates. Our charter requiresthat a majority of our directors be independent of our co-sponsors, our advisor, or any of their affiliates except for a period of up to 60 days after thedeath, removal or resignation of an independent director pending the election of such independent________(1) Includes the property information related to a joint venture with affiliates of Digital Realty Trust, L.P. and a joint venture in which GA HealthcareREIT III holds a majority interest.

10

Table of Contents

director’s successor. Our charter also provides that our independent directors are responsible for reviewing the performance of our advisor and mustapprove certain matters set forth in our charter. Our directors will be elected annually by our stockholders. We have five executive officers, includingMr. Hanson, our Chief Executive Officer, Mr. Prosky, our President, Chief Operating Officer and Interim Chief Financial Officer, Mathieu B. Streiff, ourExecutive Vice President and General Counsel, Stefan K.L. Oh, our Executive Vice President of Acquisitions, and Cora Lo, our Assistant GeneralCounsel and Secretary. Mr. Hanson, Mr. Prosky, Mr. Streiff, Mr. Oh and Ms. Lo are all employees of American Healthcare Investors.

For more information regarding our directors and executive officers, see the “Management of Our Company — Directors and Executive Officers”section of this prospectus.

Our Operating PartnershipWe intend to own all of our assets through our operating partnership, Griffin-American Healthcare REIT IV Holdings, LP, or its subsidiaries. We

are the sole general partner of our operating partnership and our advisor is a limited partner of our operating partnership. Our advisor has certainsubordinated distribution rights in addition to its rights as a limited partner in the event certain performance-based conditions are satisfied. See“— Compensation to Our Advisor, Our Dealer Manager and Their Affiliates” below for a summary description of our advisor’s subordinated distributionrights.

Conflicts of InterestOur officers are also managing directors, officers and/or employees of our advisor, one of our co-sponsors, and/or other affiliated entities and they

may become involved in advising and investing in other real estate entities, including other REITs, which may give rise to conflicts of interest. As aresult, such persons may experience conflicts between their fiduciary obligations to us and their fiduciary obligations to, and pecuniary interests in, ourco-sponsors and their affiliated entities.