Ambuja Cements Ltd. RESULT UPDATE July 25, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ambuja Cements Ltd.

RESULT UPDATE July 25, 2017

2 Page

Result Highlights:

•Total Sales stood at INR 32602 Mn as against our estimate of INR 32020 mn which was up by 12.4% Y-O-Y and 11.6% Q-O-Q. Volume growth stood at 5% Y-O-Y reaching 6.05 MT (est. 6.21 MT) as against 5.76 MT in Q2CY16 and 6.02 MT in Q1CY17. Realizations increased by 5.71% Y-O-Y and 10.67% Q-O-Q.

•EBIDTA stood at INR 6510 Mn which was up by 8.9% Y-O-Y and 65.2% Q-O-Q and EBIDTA margin stood at 19.9% as against 20.6% same quarter last year and 13.5% last quarter.

•PAT stood at INR 3922 Mn which was down by 13.2% Y-O-Y and up 59.1% Q-O-Q while PAT Margin stood at 12%. The net profit was down on Y-O-Y basis primarily on account of lower other income.

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Ambuja Cements Ltd. Strong realization boosts operating performance ! CMP

INR 268 Target

INR 282 Potential Upside

5.2% Market Cap (INR Mn)

531,756 Recommendation

ACCUMULATE Sector

Cement

SHARE PRICE PERFORMANCE

Shares outs (Mn) 1986

EquityCap (INR Mn) 3971

Mkt Cap (INR Mn) 531756

52 Wk H/L (INR) 282/191

Volume Avg (3m K) 3470.1

Face Value (INR) 2

Bloomberg Code ACEM IN

MARKET DATA

SENSEX 32228

NIFTY 9965

MARKET INFO

Revenues in-line with estimates:

During Q2CY17, revenues for Ambuja Cements Ltd (ACEM) stood at INR 32602 mn as against our estimate of INR 32020 mn which was up by 12.4% Y-O-Y and 11.6% Q-O-Q. Cement sales volumes for ACEM stood at 6.05 MT as against our estimate of 6.21 MT and grew by 5% Y-O-Y and ~1% Q-O-Q. Realizations increased sharply with a growth of 5.71% Y-O-Y and 10.67% Q-O-Q.

The company derives 40%/35%/20% of its volumes from North/West/East respectively. We expect demand to remain healthy in North and East primarily on account of off-take in affordable housing projects and higher infrastructure spend by Government. We believe the company will be one of the key beneficiary on account of strong and recognized brand.

We expect the cement volumes for the company to grow from 21.47 MT in CY16 to 25.47 MT in CY18 translating into 8.92% CAGR while we estimate total revenues to surge by 13.03% from INR 105381.5 mn in CY16 to INR 134621.5 mn in CY18.

Robust realizations boosts EBITDA/ton: EBITDA during the quarter stood at INR 6510 mn; up by 8.9% Y-O-Y and 65.2% Q-O-Q. EBITDA/ton stood at INR 1012 as against INR 955 in Q2CY16 and INR 606 in Q1CY17. The significant rise observed sequentially in EBITDA/ton was primarily on account of strong realization growth. Going ahead, we expect the operating efficiencies for the company to remain healthy on account of stability in cement prices on the back of improved demand and higher operating leverage. We estimate capacity utilizations for ACEM to increase from 72.41% in CY16 to 85.91% in CY18. We expect EBITDA/ton for the company to surge from INR 734 in CY16 to INR 984 by CY18 and EBITDA to grow at 24.93% CAGR from INR 16826.9 mn to INR 26262.43 mn over CY16-CY18.

Higher efficiencies; surge in FCFF to lead to better return ratios: Currently, the net cash and cash equivalents for the company stands at INR 31429 mn. We expect the free cash flow generation for the company to surge significantly on account of improvement in operating efficiencies and minimal capex plans. Consequently, we reckon an enhancement in return ratios with ROE increasing from 5.09% in CY16 to 8.06% by CY18 and ROCE surging from 7.17% to 11.97% in the same period. We believe that efficient deployment of capital in capacity addition or in efficiency improvement measures will act as re-rating trigger for the company.

Particulars Jun 17 Mar 17 Dec 16

Promoters 63.11 63.11 63.11

FIIs 16.75 18.21 18.38

DIIs 11.48 10.69 10.6

Others 8.67 8 7.91

Total 100 100 100

SHARE HOLDING PATTERN (%)

Volume CAGR expected between CY16 and CY18

8.92%

Revenue CAGR expected between CY16 and CY18

13%

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

70

85

100

115

Jul-1

6

Se

p-1

6

No

v-16

Jan

-17

Mar

-17

May

-17

Jul-1

7

Sensex Ambuja Cement

3 Page

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Valuation and Outlook:

The company marginally outperformed on the volume front with a growth of 5% Y-O-Y as against expected industry growth of 3% Y-O-Y while the significant improvement sequentially in operating efficiencies was primarily on account of strong realization growth. Going ahead, we expect the volumes to grow by 8.92% over CY16-CY18E factoring in pick up in affordable housing and infrastructure development projects. Further, we expect EBITDA to grow at 24.93% CAGR surging from INR 16826.9 mn to INR 26262.4 mn over CY16-CY18. With expected net cash and cash equivalents of INR 42895.7 mn by CY18, the company trades at an EV/ton of $185 and EV/EBITDA of 14x on CY18 basis (standalone value). We value Ambuja Cement Ltd on SOTP methodology (EV/EBITDA of 14x and EV/ton of $180 for standalone business on CY18E; 20% Holding company discount in ACC stake on CY18E) and arrive at a target price of INR 282 which is an upside of 5.2% from CMP of INR 268. We believe efficient capital deployment in capacity addition or efficiency improvement measures in standalone business and turnaround in ACC’s performance will lead to re-rating of the stock. We have an ACCUMULATE rating for the stock.

Particulars (in INR) CY14 CY15 CY16 CY17E CY18E

Realization/ton 4474.36 4303.31 4266.60 4437.27 4614.76

COGS cost/ton 384.10 379.74 347.69 354.12 348.14

Employee cost/ton 262.56 270.79 276.53 281.65 282.02

Power and fuel cost/ton 1022.67 943.01 853.27 948.06 992.46

Transportation and Handling cost/ton 1101.08 1152.82 1151.77 1170.25 1162.67

Other Expenses/ton 863.75 896.23 903.64 864.97 845.58

EBITDA/ton 840.19 660.71 733.71 818.22 983.88

Particulars (INR Mn) CY14 CY15 CY16 CY17E CY18E

Revenues 112375.60 107639.60 105381.50 117981.73 134621.47

EBITDA 19284.40 15314.70 16826.90 20172.87 26262.43

PAT 14963.60 8075.60 9700.90 12490.72 16396.70

EPS 9.66 5.20 4.89 6.29 8.26

P/E (x) 23.69 39.07 42.21 42.45 30.40

EV/EBITDA (x) 16.05 17.38 22.88 24.57 18.55

Source: Company, KRChoksey Research

Source: Company, KRChoksey Research

Key Financials

Operating metrics

Ambuja Cements Ltd.

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

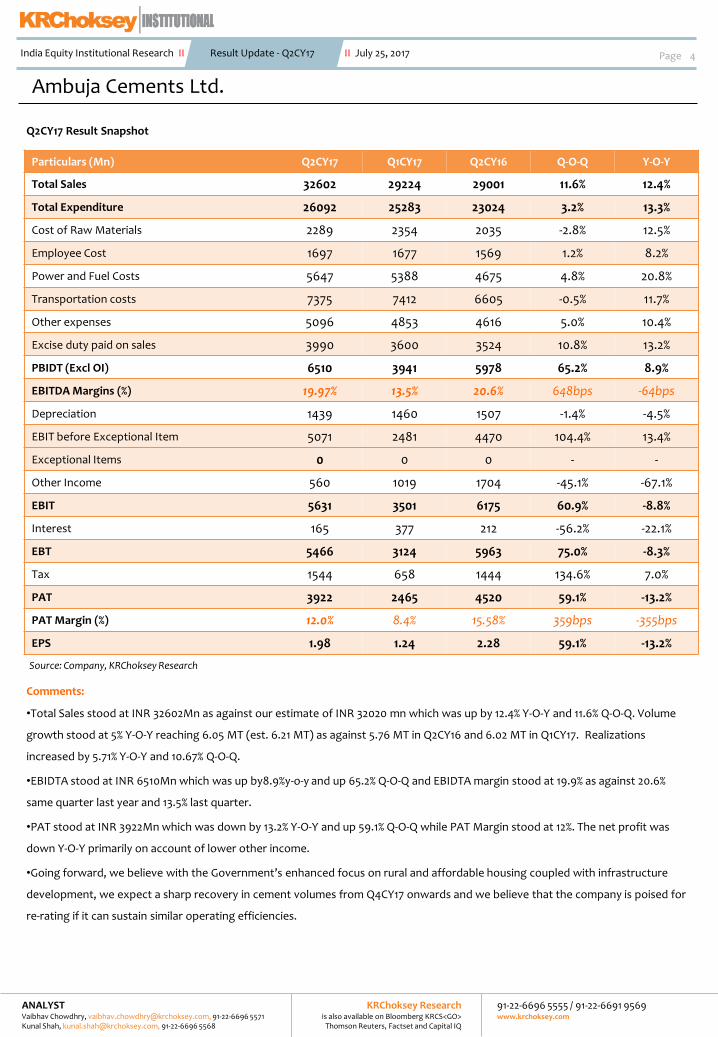

Q2CY17 Result Snapshot Comments:

•Total Sales stood at INR 32602Mn as against our estimate of INR 32020 mn which was up by 12.4% Y-O-Y and 11.6% Q-O-Q. Volume

growth stood at 5% Y-O-Y reaching 6.05 MT (est. 6.21 MT) as against 5.76 MT in Q2CY16 and 6.02 MT in Q1CY17. Realizations

increased by 5.71% Y-O-Y and 10.67% Q-O-Q.

•EBIDTA stood at INR 6510Mn which was up by8.9%y-o-y and up 65.2% Q-O-Q and EBIDTA margin stood at 19.9% as against 20.6%

same quarter last year and 13.5% last quarter.

•PAT stood at INR 3922Mn which was down by 13.2% Y-O-Y and up 59.1% Q-O-Q while PAT Margin stood at 12%. The net profit was

down Y-O-Y primarily on account of lower other income.

•Going forward, we believe with the Government’s enhanced focus on rural and affordable housing coupled with infrastructure

development, we expect a sharp recovery in cement volumes from Q4CY17 onwards and we believe that the company is poised for

re-rating if it can sustain similar operating efficiencies.

Particulars (Mn) Q2CY17 Q1CY17 Q2CY16 Q-O-Q Y-O-Y

Total Sales 32602 29224 29001 11.6% 12.4%

Total Expenditure 26092 25283 23024 3.2% 13.3%

Cost of Raw Materials 2289 2354 2035 -2.8% 12.5%

Employee Cost 1697 1677 1569 1.2% 8.2%

Power and Fuel Costs 5647 5388 4675 4.8% 20.8%

Transportation costs 7375 7412 6605 -0.5% 11.7%

Other expenses 5096 4853 4616 5.0% 10.4%

Excise duty paid on sales 3990 3600 3524 10.8% 13.2%

PBIDT (Excl OI) 6510 3941 5978 65.2% 8.9%

EBITDA Margins (%) 19.97% 13.5% 20.6% 648bps -64bps

Depreciation 1439 1460 1507 -1.4% -4.5%

EBIT before Exceptional Item 5071 2481 4470 104.4% 13.4%

Exceptional Items 0 0 0 - -

Other Income 560 1019 1704 -45.1% -67.1%

EBIT 5631 3501 6175 60.9% -8.8%

Interest 165 377 212 -56.2% -22.1%

EBT 5466 3124 5963 75.0% -8.3%

Tax 1544 658 1444 134.6% 7.0%

PAT 3922 2465 4520 59.1% -13.2%

PAT Margin (%) 12.0% 8.4% 15.58% 359bps -355bps

EPS 1.98 1.24 2.28 59.1% -13.2%

4 Page

Source: Company, KRChoksey Research

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

Ambuja Cements Ltd.

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Standalone Financials

Balance Sheet (INR Mn) CY14 CY15 CY16 CY17E CY18E

Equity Share Capital 3099.50 3103.80 3971.30 3971.30 3971.30 Reserves 97933.80 99964.90 186764.30 193009.66 199568.34 Net worth 101033.30 103068.70 190735.60 196980.96 203539.64 Total loans 291.50 327.40 368.10 368.10 368.10 Capital Employed 107633 109358 196433 202820 209464 Net block 69172.80 65061.50 62986.70 58936.50 57746.74 Current Investments 20670.00 21192.30 10650.20 10650.20 10650.20 Inventories 8883.90 8954.50 9375.40 10348.60 11176.49 Sundry debtors 2279.80 2863.60 3000.80 3232.38 3688.26 Sundry creditors 6184.90 6798.20 8969.80 9898.66 10933.52 Cash and bank 24581.20 28483.90 14128.70 24345.32 32613.56 Total Current assets 59952.10 65486.00 41089.50 52593.45 62644.66 Total Current liabilities 31375.40 32260.90 36109.70 37176.46 39393.76 Capital Deployed 107633 109358 196433 202820 209464

5 Page

Profit & Loss (INR Mn) CY14 CY15 CY16 CY17E CY18E

Total Sales 112375.60 107639.60 105381.5 117981.73 134621.47 COGS 8507.90 8267.00 7464.9 8211.39 8868.30 Employee Expenses 5815.80 5895.20 5937.2 6530.92 7184.01 Power and fuel 22652.20 20529.40 18319.6 21983.52 25281.05 Transportation cost 24388.90 25096.80 24728.4 27135.80 29616.72 Other Expenses 19132.00 19510.90 19401.2 20056.89 21539.43 Excise duty 12594.40 13025.60 12703.3 13890.34 15869.51 EBITDA 19284.40 15314.70 16826.9 20172.87 26262.43 D&A 5095.30 6256.60 8501.3 5850.00 6189.76 Other income 4289.80 3581.90 5762.3 5000.00 5000.00 EBIT 18478.90 12640.00 14087.9 19322.87 25072.68 Interest Expense 644.80 917.90 714.8 680.00 600.00 PBT 17834.10 11722.10 13373.1 18642.87 24472.68 Tax 2870.50 3646.50 3672.2 6152.15 8075.98 Effective tax rate 16.10% 31.11% 27.46% 33.00% 33.00% PAT 14963.60 8075.60 9700.9 12490.72 16396.70

Cash Flow (INR Mn) CY14 CY15 CY16 CY17E CY18E

PAT 14963.60 8075.60 9700.90 12490.72 16396.70 Depreciation & Amortization 5095.30 6256.60 8501.30 5850.00 6189.76 (Incr)/Decr in Working Capital 147.80 227.90 357.70 -78.94 519.81 Cash Flow from Operating 16752.70 15528.10 14153.90 18941.78 23706.26 (Incr)/ Decr in Gross PP&E -8234.10 -6213.80 -3910.50 -1799.80 -5000.00 Cash Flow from Investing -4600.90 -829.20 -34026.00 -1799.80 -5000.00 (Decr)/Incr in Debt 0.00 35.90 141.30 0.00 0.00 Dividend -6173.00 -7443.50 -5511.10 -6245.36 -9838.02 Finance costs -318.30 -389.30 -359.20 -680.00 -600.00 Cash Flow from Financing -7171.40 -8968.90 -6822.60 -6925.36 -10438.02 Incr/(Decr) in Balance Sheet Cash 4980.40 5730.00 -26694.70 10216.62 8268.24 Cash and cash equivalents at the Start of the Year 39606.60 44587.00 50317.00 14128.70 24345.32 Cash and cash equivalents at the End of the Year 44587.00 50317.00 23622.30 24345.32 32613.56

Source: Company, KRChoksey Research

Source: Company, KRChoksey Research

Source: Company, KRChoksey Research

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

Ambuja Cements Ltd.

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

6 Page

Source: Company, KRChoksey Research

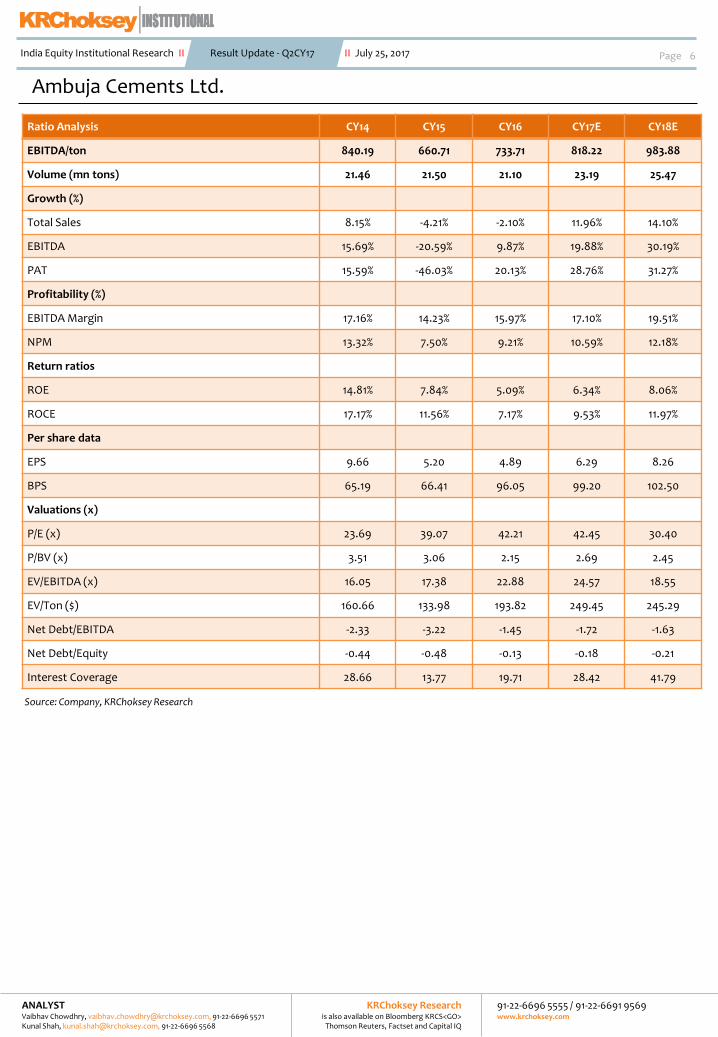

Ratio Analysis CY14 CY15 CY16 CY17E CY18E

EBITDA/ton 840.19 660.71 733.71 818.22 983.88

Volume (mn tons) 21.46 21.50 21.10 23.19 25.47

Growth (%)

Total Sales 8.15% -4.21% -2.10% 11.96% 14.10%

EBITDA 15.69% -20.59% 9.87% 19.88% 30.19%

PAT 15.59% -46.03% 20.13% 28.76% 31.27%

Profitability (%)

EBITDA Margin 17.16% 14.23% 15.97% 17.10% 19.51%

NPM 13.32% 7.50% 9.21% 10.59% 12.18%

Return ratios

ROE 14.81% 7.84% 5.09% 6.34% 8.06%

ROCE 17.17% 11.56% 7.17% 9.53% 11.97%

Per share data

EPS 9.66 5.20 4.89 6.29 8.26

BPS 65.19 66.41 96.05 99.20 102.50

Valuations (x)

P/E (x) 23.69 39.07 42.21 42.45 30.40

P/BV (x) 3.51 3.06 2.15 2.69 2.45

EV/EBITDA (x) 16.05 17.38 22.88 24.57 18.55

EV/Ton ($) 160.66 133.98 193.82 249.45 245.29

Net Debt/EBITDA -2.33 -3.22 -1.45 -1.72 -1.63

Net Debt/Equity -0.44 -0.48 -0.13 -0.18 -0.21

Interest Coverage 28.66 13.77 19.71 28.42 41.79

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

Ambuja Cements Ltd.

91-22-6696 5555 / 91-22-6691 9569 www.krchoksey.com

ANALYST Vaibhav Chowdhry, [email protected], 91-22-6696 5571 Kunal Shah, [email protected], 91-22-6696 5568

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Analyst Certification

We, Vaibhav Chowdhry (B.Com, MBA), research analyst, & Kunal Shah (BE), senior research associate, author and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect my views about the subject issuer(s) or securities. I also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & Conditions and other disclosures:

KRChoksey Shares and Securities Pvt. Ltd (hereinafter referred to as KRCSSPL) is a registered member of National Stock Exchange of India Limited, Bombay Stock Exchange Limited and MCX Stock Exchange Limited. KRCSSPL is a registered Research Entity vide SEBI Registration No. INH000001295 under SEBI (Research Analyst) Regulations, 2014.

We submit that no material disciplinary action has been taken on KRCSSPL and its associates (Group Companies) by any Regulatory Authority impacting Equity Research Analysis activities.

KRCSSPL prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analyst covers.

The information and opinions in this report have been prepared by KRCSSPL and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of KRCSSPL. While we would endeavor to update the information herein on a reasonable basis, KRCSSPL is not under any obligation to update the information. Also, there may be regulatory, compliance or other reasons that may prevent KRCSSPL from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or KRCSSPL policies, in circumstances where KRCSSPL might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. KRCSSPL will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. KRCSSPL accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. Our employees in sales and marketing team, dealers and other professionals may provide oral or written market commentary or trading strategies that reflect opinions that are contrary to the opinions expressed herein, .In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest.

Associates (Group Companies) of KRCSSPL might have received any commission/compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of brokerage services or specific transaction or for products and services other than brokerage services.

KRCSSPL or its Associates (Group Companies) have not managed or co-managed public offering of securities for the subject company in the past twelve months

KRCSSPL encourages the practice of giving independent opinion in research report preparation by the analyst and thus strives to minimize the conflict in preparation of research report. KRCSSPL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither KRCSSPL nor Research Analysts have any material conflict of interest at the time of publication of this report.

It is confirmed that, Vaibhav Chowdhry (B.Com, MBA), research analyst, & Kunal Shah (BE), senior research associate, of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific brokerage service transactions.

KRCSSPL or its associates (Group Companies) collectively or its research analyst do not hold any financial interest/beneficial ownership of more than 1% (at the end of the month immediately preceding the date of publication of the research report) in the company covered by Analyst, and has not been engaged in market making activity of the company covered by research analyst.

Since associates (Group Companies) of KRCSSPL are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report.

It is confirmed that, Vaibhav Chowdhry (B.Com, MBA), research analyst, & Kunal Shah (BE), senior research associate, do not serve as an officer, director or employee of the companies mentioned in the report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other

jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject KRCSSPL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

Please send your feedback to [email protected] Visit us at www.krchoksey.com

Kisan Ratilal Choksey Shares and Securities Pvt. Ltd Registered Office:

1102, Stock Exchange Tower, Dalal Street, Fort, Mumbai – 400 001. Phone: 91-22-6633 5000; Fax: 91-22-6633 8060.

Corporate Office: ABHISHEK, 5th Floor, Link Road, Andheri (W), Mumbai – 400 053.

Phone: 91-22-6696 5555; Fax: 91-22-6691 9576.

7 Page

Ambuja Cements Ltd.

India Equity Institutional Research II Result Update - Q2CY17 II July 25, 2017

Ambuja Cements Ltd

Date CMP (INR) TP (INR) Recommendation

25-Jul-17 268 282 ACCUMULATE

02-May-17 246 248 HOLD

Rating Legend

Our Rating Upside

Buy More than 15%

Accumulate 5% - 15%

Hold 0 – 5%

Reduce -5% – 0

Sell Less than -5%

Related Documents