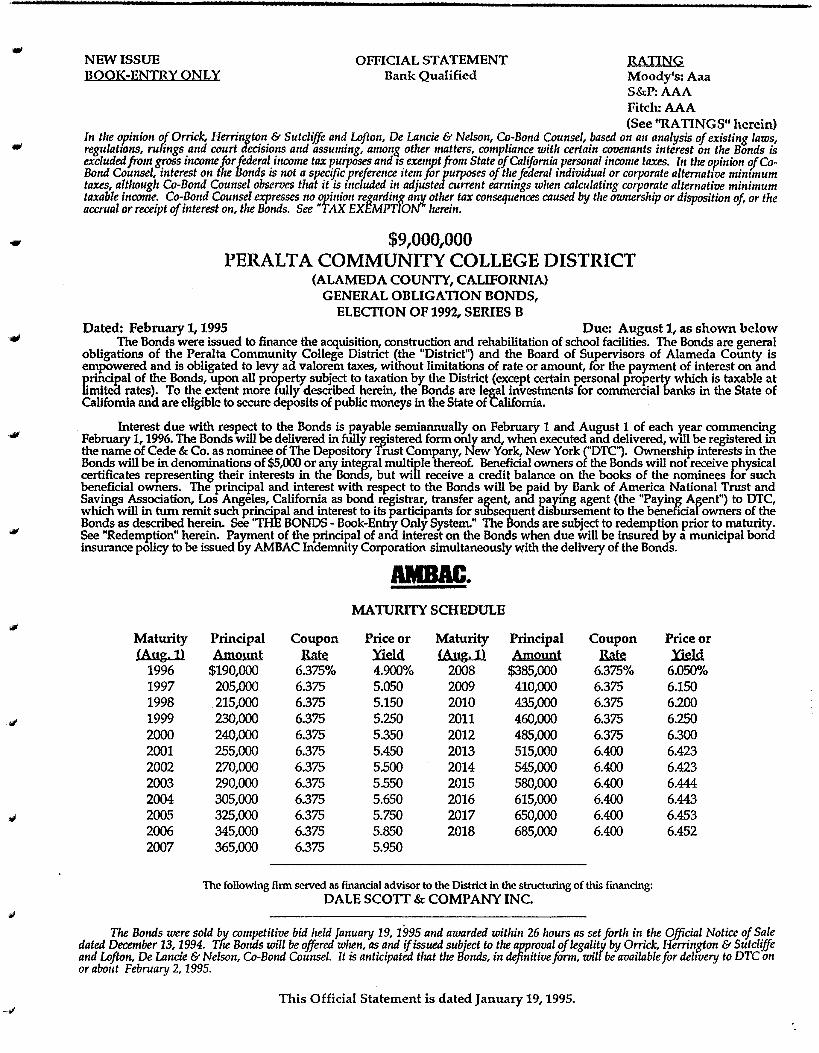

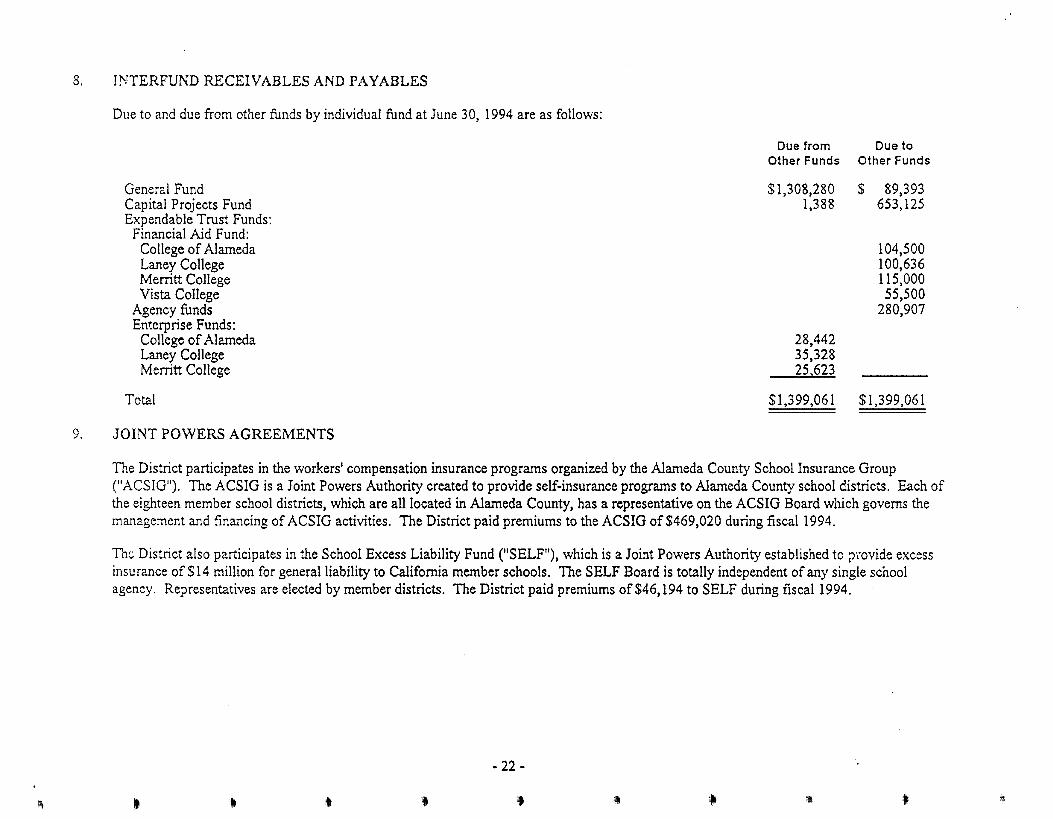

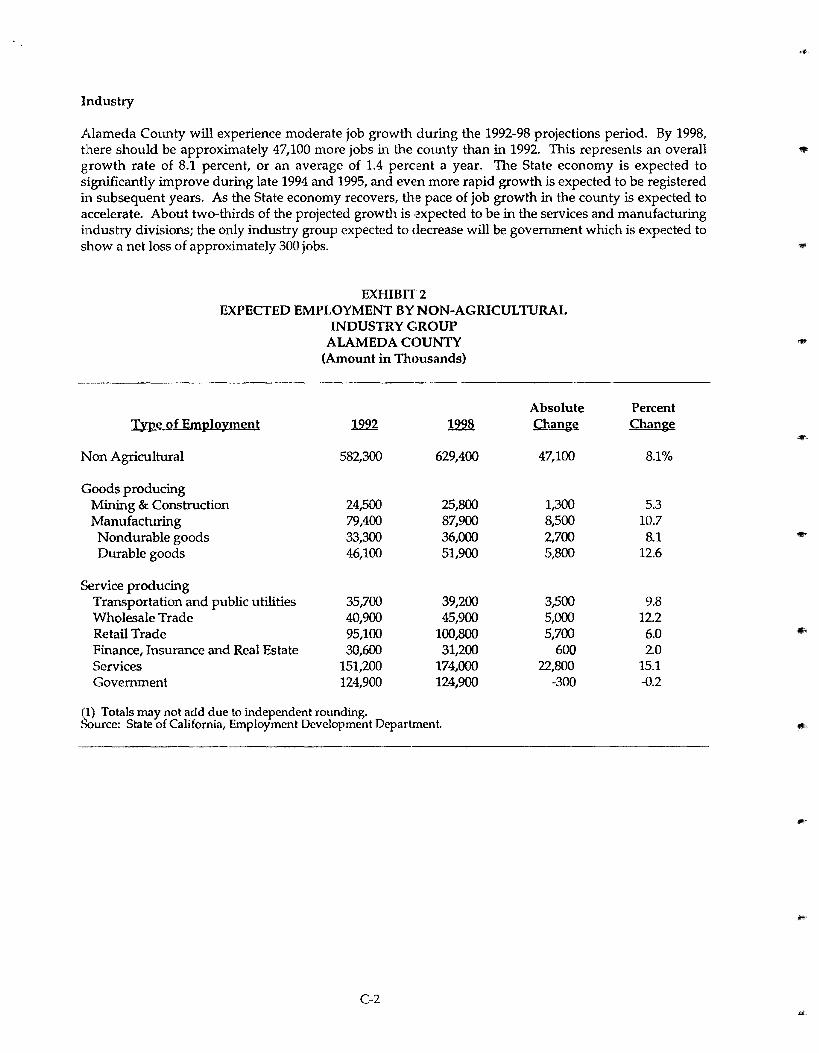

,-, ,,fll -.,., NEW ISSUE BOOK-ENTRY ONLY OFFICIAL STATEMENT Bank Qualified RATING Moody's: Aaa S&P:AAA Fitch: AAA (See "RATINGS" herein) In the opinion of Orrick, Herrington & Sutcliffe and Lofton, De Lancie & Nelson, Co-Bond Counsel, based on an analysis of existing laws, regulations, rufings and court aecisions and assuming, amon! other matters, compliance with certain covenants interest on the Bonds is excluded from ~oss income for federal income tax purposes and rs exenpt from State of California personal income taxes. In the opinion cf Co- Bond Counsel, interest on the lJonds is not a specific preference item Jor/urposes of the federal individual or corporate alternative minimum taxes, altlwugh Co-Bond Counsel observes tlrat it is included in adjuste current earnings wlten calculating corporate alternative minimum taxable income. Co-Bond Counsel expresses no opinion regarding any other tax consequences caused by the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See "TAX EXEMPTIONH herein. $9,000,000 PERALTA COMMUNITY COLLEGE DISTRICT (ALAMEDA COUNTY, CALIFORNIA) GENERAL OBLIGATION BONDS, ELECTION OF 1992, SERIES B Dated: February 1, 1995 Due: August 1, as shown below The Bonds were issued to finance the acquisition, construction and rehabilitation of school facilities. The Bonds are general obligations of the Peralta Community College District (the "District") and the Board of Supervisors of Alameda County is empowered and is obligated to levy aa valorem taxes, without limitations of rate or amount, for the payment of interest on and principal of the Bonds, upon all property subject to taxation by the District (except certain personal property which is taxable at limitea rates). To the extent more fully described herein, the Bonds are legal investments for commercial banks in the State of California and are eligible to secure deposits of public moneys in the State of California. Interest due with respect to the Bonds is Eayable semiannually on February 1 and Augt!St 1 of each r,ear commencing February 1, 1996. The Bonds will be delivered in fully registered form only and, when executed and delivered, will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ("DTC"). Ownership interests in the Bonds will be in denominations of $5,000 or any integral multiple Thereof. Beneficial owners of the Bonds will not receive physical certificates representing their interests in the Boncfs, but will receive a credit balance on the books of the nominees for such beneficial owners. The principal and interest with respect to the Bonds will be paid by Bank of America National Trust and Savings Association, Los Angeles, California as bond registrar, transfer agent, and paying agent (the "Paying Agent") to OTC, which will in turn remit such principal and interest to its participants for subsequent disbursement to the beneficia[ owners of the Bonds as described herein. See ''THE BONDS - Book-Entry: Only System." The Bonds are subject to redemption prior to maturity. See "Redemption" herein. Payment of the principal of and interest on the Bonds when due will be insured by a municipal bond insurance policy to be issued &y AMBAC Indemruty Corporation simultaneously with the delivery of the Bonds. AMBAC. MA TIJRITY SCHEDULE Maturity Principal Coupon Price or Maturity Principal Coupon Price or {Aug, l} Amf.mnt Tukl (A:ug. ll Am2:Y.nt Rab: 1996 $190,000 6.375% 4.900% 2008 $385,000 6.375% 6.050% 1997 205,000 6.375 5.050 2009 410,000 6.375 6.150 1998 215,000 6.375 5.150 2010 435,000 6.375 6.200 1999 230,000 6.375 5.250 2011 460,000 6.375 6.250 2000 240,000 6.375 5.350 2012 485,000 6.375 6.300 2001 255,000 6.375 5.450 2013 515,000 6.400 6.423 2002 270,000 6.375 5.500 2014 545,000 6.400 6.423 2003 290,000 6.375 5.550 2015 580,000 6.400 6.444 2004 305,000 6.375 5.650 2016 615,000 6.400 6.443 2005 325,000 6.375 5.750 2017 650,000 6.400 6.453 2006 345,000 6.375 5.850 2018 685,000 6.400 6.452 2007 365,000 6.375 5.950 The following firm setved as financial advisor to the District in the structuring of this financing: DALE SCOIT & COMPANY INC. The Bonds were sold by competitive bid held January 19, 1995 and awarded within 26 hours as set forth in the Official Notice of Sale dated December 13, 1994. The Bonds will be offered when, as and if issued subject to the approval of legalitv by Orrick, Herrington & Sutcliffe and Lofton, De Lancie & Nelson, Co-Bond Counsel. It is anticipated that the Bonds, in definitive form, wil[ be available for delivery to DTC on or about February 2, 1995. This Official Statement is dated January 19, 1995.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

,-,

,,fll

-.,.,

NEW ISSUE BOOK-ENTRY ONLY

OFFICIAL STATEMENT Bank Qualified

RATING Moody's: Aaa S&P:AAA Fitch: AAA (See "RATINGS" herein)

In the opinion of Orrick, Herrington & Sutcliffe and Lofton, De Lancie & Nelson, Co-Bond Counsel, based on an analysis of existing laws, regulations, rufings and court aecisions and assuming, amon! other matters, compliance with certain covenants interest on the Bonds is excluded from ~oss income for federal income tax purposes and rs exenpt from State of California personal income taxes. In the opinion cf CoBond Counsel, interest on the lJonds is not a specific preference item Jor/urposes of the federal individual or corporate alternative minimum taxes, altlwugh Co-Bond Counsel observes tlrat it is included in adjuste current earnings wlten calculating corporate alternative minimum taxable income. Co-Bond Counsel expresses no opinion regarding any other tax consequences caused by the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See "TAX EXEMPTIONH herein.

$9,000,000 PERALTA COMMUNITY COLLEGE DISTRICT

(ALAMEDA COUNTY, CALIFORNIA) GENERAL OBLIGATION BONDS,

ELECTION OF 1992, SERIES B Dated: February 1, 1995 Due: August 1, as shown below

The Bonds were issued to finance the acquisition, construction and rehabilitation of school facilities. The Bonds are general obligations of the Peralta Community College District (the "District") and the Board of Supervisors of Alameda County is empowered and is obligated to levy aa valorem taxes, without limitations of rate or amount, for the payment of interest on and principal of the Bonds, upon all property subject to taxation by the District (except certain personal property which is taxable at limitea rates). To the extent more fully described herein, the Bonds are legal investments for commercial banks in the State of California and are eligible to secure deposits of public moneys in the State of California.

Interest due with respect to the Bonds is Eayable semiannually on February 1 and Augt!St 1 of each r,ear commencing February 1, 1996. The Bonds will be delivered in fully registered form only and, when executed and delivered, will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ("DTC"). Ownership interests in the Bonds will be in denominations of $5,000 or any integral multiple Thereof. Beneficial owners of the Bonds will not receive physical certificates representing their interests in the Boncfs, but will receive a credit balance on the books of the nominees for such beneficial owners. The principal and interest with respect to the Bonds will be paid by Bank of America National Trust and Savings Association, Los Angeles, California as bond registrar, transfer agent, and paying agent (the "Paying Agent") to OTC, which will in turn remit such principal and interest to its participants for subsequent disbursement to the beneficia[ owners of the Bonds as described herein. See ''THE BONDS - Book-Entry: Only System." The Bonds are subject to redemption prior to maturity. See "Redemption" herein. Payment of the principal of and interest on the Bonds when due will be insured by a municipal bond insurance policy to be issued &y AMBAC Indemruty Corporation simultaneously with the delivery of the Bonds.

AMBAC. MA TIJRITY SCHEDULE

Maturity Principal Coupon Price or Maturity Principal Coupon Price or {Aug, l} Amf.mnt ~ Tukl (A:ug. ll Am2:Y.nt Rab: ~

1996 $190,000 6.375% 4.900% 2008 $385,000 6.375% 6.050% 1997 205,000 6.375 5.050 2009 410,000 6.375 6.150 1998 215,000 6.375 5.150 2010 435,000 6.375 6.200 1999 230,000 6.375 5.250 2011 460,000 6.375 6.250 2000 240,000 6.375 5.350 2012 485,000 6.375 6.300 2001 255,000 6.375 5.450 2013 515,000 6.400 6.423 2002 270,000 6.375 5.500 2014 545,000 6.400 6.423 2003 290,000 6.375 5.550 2015 580,000 6.400 6.444 2004 305,000 6.375 5.650 2016 615,000 6.400 6.443 2005 325,000 6.375 5.750 2017 650,000 6.400 6.453 2006 345,000 6.375 5.850 2018 685,000 6.400 6.452 2007 365,000 6.375 5.950

The following firm setved as financial advisor to the District in the structuring of this financing: DALE SCOIT & COMPANY INC.

The Bonds were sold by competitive bid held January 19, 1995 and awarded within 26 hours as set forth in the Official Notice of Sale dated December 13, 1994. The Bonds will be offered when, as and if issued subject to the approval of legalitv by Orrick, Herrington & Sutcliffe and Lofton, De Lancie & Nelson, Co-Bond Counsel. It is anticipated that the Bonds, in definitive form, wil[ be available for delivery to DTC on or about February 2, 1995.

This Official Statement is dated January 19, 1995.

No dealer, broker, salesperson or other person has been authorized by the District to give any information or to make any representations other than those contained herein and, if given or made, such other information or representation must not be relied upon as having been authorized by the District. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make an offer, solicitation or sale.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as representation of facts.

The information set forth herein has been obtained from sources believed to be reliable but it is not guaranteed as to accuracy or completeness, and is not to be construed as representation by Dale Scott & Company Inc. or Bank of America National Trust and Savings Association.

The District has, by resolution adopted on October 25, 1994, designated the Series B Bonds as "qualified tax-exempt obligations" pursuant to Section 265(b )(3) of the Code. Such section provides an exception to the prohibition against the ability of a "financial. institution" (as defined in the Internal Revenue Code of 1986) to deduct its interest expense allocable to tax-exempt interest.

WITH RESPECT TO THIS OFFERING, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE mATWHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANYTIME.

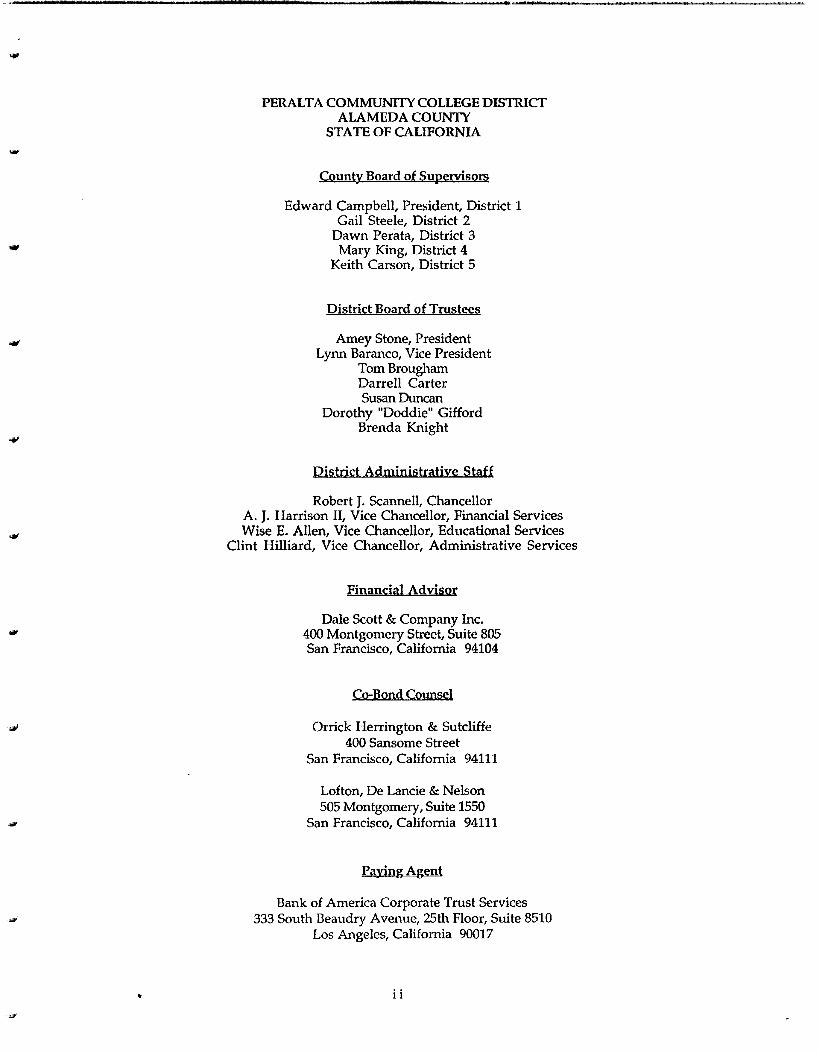

-PERALTA COMMUNITY COLLEGE DISTRICT

ALAMEDA COUNTY STATE OF CALIFORNIA

County Board of Supervisors

Edward Campbell, President, District 1 Gail Steele, District 2

Dawn Pera.ta, District 3 Mary King, District 4

Keith Carson, District 5

District Board of Trustees

Amey Stone, President Lynn Baranco, Vice President

Tom Brougham Darrell Carter Susan Duncan

Dorothy "Doddie" Gifford Brenda Knight

District Administrative Staff

Robert J. Scannell, Chancellor A. J. Harrison II, Vice Chancellor, Financial Services Wise E. Allen, Vice Chancellor, Educational Services

Clint Hilliard, Vice Chancellor, Administrative Services

Financial Advisor

Dale Scott & Company Inc. 400 Montgomery Street, Suite 805 San Francisco, California 94104

Co-Bond Counsel

Orrick Herrington & Sutcliffe 400 Sansome Street

San Francisco, California 94111

Lofton, De Lande & Nelson 505 Montgomery, Suite 1550

San Francisco, California 94111

Paying Agent

Bank of America Corporate Trust Services 333 South Beaudry A venue, 25th Floor, Suite 8510

Los Angeles, California 90017

i i

TABLE OF CONTENTS

INTRODUCTION .............................................................................................................. l

THE BONDS ..................................................................................................................... 1 Authority for Issuance ............................................................................................ 1 Terms of Sale ......................................................................................................... 1 Description of the Bonds .......................................................................................... 1 Book-Entry Only System ........................................................................................ 2 Interest .................................................................................................................. 3 Redemption ........................................................................................................... 3

Optional Redemption ................................................................................. 3 Notice of Redemption ................................................................................. 4

Payment ................................................................................................................ 4 • Legal Opinion ........................................................................................................ 4 Security ................................................................................................................. 5 Bond Insurance ....................................................................................................... 5 Purpose of the Issue ................................................................................................ 7 Annual Debt Service ................................................................................................ 8

THE DISTRICT .................................................................................................................. 9 General Information ............................................................................................... 9 Employee Relations ............................................................................................... 10 Pension Plans ......................................................................................................... 11

DISTRICT DEBT STRUCTURE ........................................................................................... 11 Short-Term Borrowing ............................................................................................ 11 Lease Obligations .................................................................................................. 11 Long-Term Borrowing ............................................................................................. 11 Property Tax Collection Procedures ......................................................................... 13 Unitary Taxation of Utility Property ..................................................................... 13 Tax Levies and Delinquencies ................................................................................. 14 The Teeter Plan ...................................................................................................... 14 County Pooled Investment ........................................................................................ 15 Top Ten Taxpayers ................................................................................................. 15 Historic Assessed Valuation ......................................................... " ......................... 16 Tax Rates ............................................................................................................... 16

DISTRICT FINANCIAL INFORMATION .......................................................................... 17 District Budget ...................................................................................................... 17 Accounting Practices ............................................................................................... 18

STATE OF CALIFORNIA FINANCES ................................................................................ 19 General. ................................................................................................................. 19 State Funding of Education ..................................................................................... 19 Proposition 98 and Proposition 111 .......................................................................... 20

LIMITATIONS ON TAX REVENUES ................................................................................. 22 Property Tax Rate Limitations - Article XIIIA ........................................................ 22 Legislation Implementing Article XIIIA ................................................................. 22 Appropriation Limitation - Article XIIIB ............................................................... 23 Proposition 62 ........................................................................................................ 23

iii

-

1111~

,ml'

-,1111.111

TAX EXEMPTION .............................................................................................................. 24

CERTAIN LEGAL MA TIERS .............................................................................................. 24 Legality for lnvestment .......................................................................................... 24 Interest Deduction for Financial Institutions ............................................................ 25 Absence of Litigation .............................................................................................. 25

RATINGS .................................................................... -...................................................... 25

MISCELLANEOUS ............................................................................................................ 26

APPENDIX A - EXCERPTS OF AUDITED FINANCIAL STATEMENTS OF THE DISTRICT FOR FISCAL YEAR 1993-94

APPENDIX B - FORM OF OPINION OF CO-BOND COUNSEL

APPENDIX C- COUNTY OF ALAMEDA

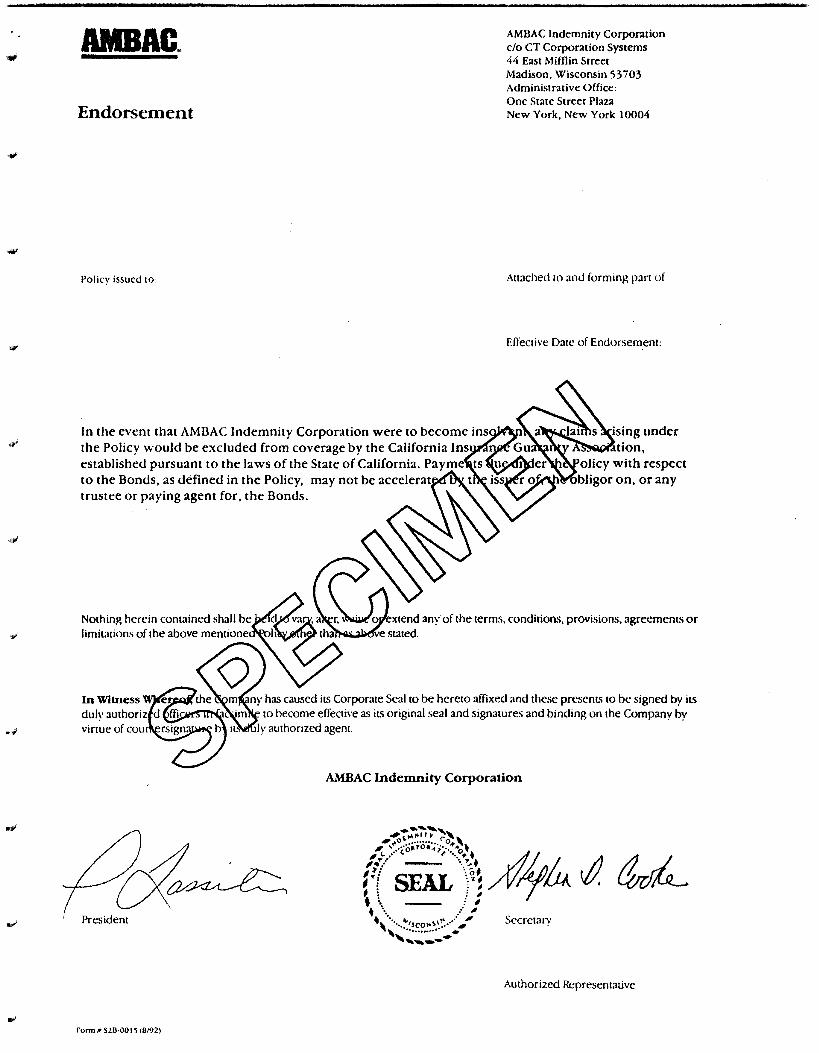

APPENDIX D- FORM OF BOND INSURANCE POLICY

iv

[THIS PAGE INTEl'ITTONALLY LEFf BLANK]

-

..

'""'

OFFICIAL STATEMENT

$ 9,000,000 PERALTA COMMUNITY COLLEGE DISTRICT

(ALAMEDA COUNTY, CALIFORNIA) GENERAL OBLIGATION BONDS,

ELECTION OF 1992, SERIES B

INTRODUCTION

The $9,000,000 principal amount of Peralta Community College District (the "District") General Obligation Bonds, Election of 1992, Series B (the "Bonds") represents the sale of a portion of the bonds approved by more than two-thirds of the voters casting ballots at an election held in the Peralta Community College District on November 3, 1992. The Bonds represent general obligations of the District to be issued under provisions of the State of California Education Code, and pursuant to a resolution of the Board of Supervisors of Alameda County adopted on December 13, 1994 (the "County Resolution"). Proceeds from the sale of the Bonds will be used to finance the acquisition, construction and rehabilitation of school facilities.

THE BONDS

Authority for Issuance

The $9,000,000 principal amount of bonds of the District are general obligation bonds to be issued under provisions of Title 1, Division 1, Part 10, Chapter 2 of the State of California Education Code, commencing with Section 15100, and pursuant to the County Resolution. The Bonds represent the second series of bonds authorized from $50,000,000 approved by District voters on November 3, 1992. In June, 1993, the District issued $9,000,000.

Terms of Sale

Bids for purchase of the Bonds were received at or before 9:00 a.m. (Pacific Time}, January 19, 1995 at the office of Dale Scott & Co., Inc., 400 Montgomery Street, Suite 805, San Francisco, CA 94104. The Bonds will be sold pursuant to the terms of sale contained in the Official Notice of Sale adopted by the Board of Supervisors of Alameda County on December 13, 1994.

Description of the Bonds

The Bonds will be dated February 1, 1995 and will be issued in registered form in denominations of $5,000 or any integral multiple thereof, provided that no Bond shall have principal maturing on more than one maturity date. The Bonds will be delivered in fully registered form only and, when executed and delivered, will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ("DTC"). Beneficial Owners (as defined herein) of the Bonds will not receive physical certificates representing their interests in the Bonds, but will receive a credit balance on the books of the nominees for such beneficial owners. The principal and interest with respect to the Bonds will be paid by Bank of America National Trust and Savings Association, Los Angeles, California as Paying Agent to DTC, which will in turn remit such principal and interest to its participants for subsequent disbursement to the Beneficial Owners of the Bonds as described herein. As long as Cede & Co. is the registered owner of the Bonds, principal and interest on the Bonds are payable by wire transfer with same-day funds transferred by the Paying Agent to Cede & Co., as nominee for

DTC, which will in turn remit such amounts to DTC Participants (as defined herein) for subsequent distribution to the Beneficial Owners.

As long as Cede & Co. is the registered owner of the :Bonds, as nominee of DTC, references herein to the registered owners shall mean Cede & Co. as aforesaid and shall not mean the Beneficial Owners of the Bonds. See "THE BONDS - Book - Entry Only System." The Bonds will mature on August 1, in the years and amounts as set forth on the cover.

Book-Entry Only System

The Depository Trust Company ("DTC"), New York, New York, will act as securities depository for the Bonds. The Bonds will be issued as fully-registered Bonds in the name of Cede & Co., DTC's partnership nominee. One fully-registered bond will be issued for each maturity in the aggregate principal amount of the Bonds, and will be deposited with DTC.

DTC is a limited-purpose trust company organized under the New York Banking Law, a "banking organization" within the meaning of the New York Banking Law, a member of the Federal Reserve System, a "clearing corporation" within the meaning of the New York Uniform Commercial Code, and a "clearing agency" registered pursuant to the provisions of Section 17 A of the Securities Exchange Act of 1934. DTC holds securities that its participants ("Participants") deposit with DTC. DTC also facilitates the settlement among Participants of securities transactions, such as transfers and pledges, in deposited securities through electronic computerized book-entry changes in Participant accounts, thereby eliminating the need for physical movem4mt of securities certificates. Direct Participants include securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is owned by a number of its Direct Participants and by the New York Stock Exchange, Inc., the American Stock Exchange, Inc., and the National Association of Securities Dealers Inc. Access to the OTC system is also available to others such as securities brokers and dealers, banks, and trust companies that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly ("Indirect Participants.") The Rules applicable to DTC and its Participants are on file with the Securities and Exchange Commission.

Purchases of Bonds under the DTC system must be made by or through Direct Participants, which will receive a credit for the Bonds on DTC's records. The ownership interest of each actual purchaser of each Bond ("Beneficial Owner") is in turn to be recordedl on the Direct and Indirect Participants' records. Beneficial Owners will not receive written confirmation from OTC of their purchase, but Beneficial Owners are expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Bonds are to be accomplished by entries made on the books of Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in Bonds, except in the event that use of the book-entry system for the Bonds is discontinued.

To facilitate subsequent transfers, all Bonds deposit,a?d by Participants with DTC are registered in the name of DTC's partnership nominee, Cede & Co. Th,e deposit of Bonds with DTC and their registration in the name of Cede & Co. effect no change in ben~ficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Bonds; DTC's records reflect only the identity of the Direct Participants to whose accounts such Bonds are credited, which may or may not be the Beneficial Owners. The Participants will remain responsible for keeping account of their holdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will

2

-

•

-

-

llll~

be governed by arrangements among them, subject to any statutory requirements as may be in effect from time to time.

Neither DTC nor Cede & Co. will consent or vote with respect to Bonds. Under its usual procedures, DTC mails an Omnibus Proxy to the issuer of the securities as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'s consenting or voting rights to those Direct Participants to whose accounts the Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy).

Principal and interest payments on the Bonds will be made to DTC. DTC's practice is to credit Direct Participant's accounts on the payable date in accordance with their respective holdings shown on DTC's records unless DTC has reason to believe that it will not receive payment on the payable date. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in "street name," and will be the responsibility of such Participant and not of DTC, the Paying Agent, or the District, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of principal and interest to DTC is the responsibility of the District or the Paying Agent, disbursement of such payments to Direct Participants shall be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners shall be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as securities depository with respect to the Bonds at any time by giving reasonable notice to the District or the Paying Agent. Under such circumstances, in the event that a successor securities depository is not obtained, physical certificates are required to be printed and delivered.

The District may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, certificates will be printed and delivered.

The foregoing description of DTC, the procedures and record keeping with respect to ownership of the Bonds, payment of principal of and interest on the Bonds to DTC Participants or Beneficial Owners, confirmation and transfer of ownership interest in such Bonds and other related transactions by and between DTC, the DTC Participants and the Beneficial Owners is based solely on information provided by DTC. Accordingly, no representations can be made by the District concerning these matters.

Interest

Interest on the Bonds at the rates specified in the schedule of maturities set forth above is payable on February 1, 1996 and semiannually thereafter on each August 1 and February 1.

Each Bond shall bear interest from the interest payment date next preceding the date of authentication thereof unless it is authenticated as of a day during the period from the fifteenth (15th) day of the month next preceding the month of any interest payment date to the interest payment date, inclusive, in which event it shall bear interest from such interest payment date, or unless it is authenticated on or before January 15, 1996 in which event it shall bear interest from February 1, 1995.

Redemption

Optional Redemption. The Bonds maturing on or after August 1, 2004 are subject to redemption prior to their respective stated maturity dates at the option of the District, from any source of available funds, as a whole on any date, or in part on any interest payment date, on or after August 1, 2003, of such maturities as may be specified by the District, by lot within any one maturity if less than all of the

3

Bonds of such maturity are redeemed at the following prices, expressed as a percentage of the principal amount to be redeemed, plus accrued interest thereon to the redemption date:

Redemption Dates

August 1, 2003 to July 31, 2004 August 1, 2004 to July 31, 2005 August 1, 2005 and thereafter

Redemption Price

102.0% 101.0 100.0

Notice of Redemption. Notice of redemption of the Bonds shall be mailed, postage prepaid, not less than thirty (30) or more than sixty (60) days prior to the redemption date (i) to the respective registered owners thereof at their address appearing on the bond registration books, (ii) to the Securities Depositories set forth in the County Resolution, and (iii) to one or more of the Information Services set forth in the County Resolution. Notice of redemption to the Securities Depositories and the Information Services shall be given by registered mail. Each notice of redemption shall, (a) state the date of such notice; (b) state the name of the Bond~: and the date of issue of the Bonds; (c) state the redemption date; (d) state the redemption price; (e) state the dates of maturity of the Bonds to be redeemed, and, if less than all of the Bonds of any such maturity are to be redeemed, the distinctive numbers of the Bonds of such maturity to be redeemed, and in the case of Bonds redeemed in part only, the respective portions of the principal amount thereof to be redeemed; (f) state the CUSIP number, if any, of each maturity of Bonds to be redeemed; (g) require that such Bonds be surrendered by the owners at the principal corporate trust office of the Paying Agent in Los Angeles, California, or at any other place or places designated by the Paying Agent; and (h) give notice that further interest on such Bonds will not accrue after the designated redemption date.

Neither the failure to receive such notice nor any defect in any notice so mailed shall affect the sufficiency of the proceedings for the redemption of such Bonds or the cessation of accrual of interest represented thereby from and after the redemption date.

Payment

Principal (or redemption price) is payable upon surrender of the Bonds in lawful money of the United States of America at the corporate trust office of Bank of America National Trust and Savings Association in Los Angeles, California. Interest on the Bonds shall be payable in like lawful money to the person whose name appears on the bond registration books of the Paying Agent as the registered owner thereof as of the close of business on the fifteenth (15th) day of the month immediately preceding an interest payment date, whether or not such day is a business day. Such interest shall be paid by check or draft mailed to such owner at such address as appears on such registration books of the Paying Agent, or upon written request of the owner of Bonds aggregating not less than $1,000,000 in principal amount, such request having been made before the fifteenth (15th) day of the month immediately preceding an interest payment date, by wire transfer in immediately available funds at an account maintained in the United States at such wire address as such owner shall specify in its written notice. However, as long as Bonds are held in book entry form only, principal and interest payments shall be made by the Paying Agent in immediately payable funds to DTC. The Bonds shall no longer be deemed to be outstanding and unpaid if the District shall have made adequate provision for the payment, in accordance with the Bonds and the County Resolution, of the principal and interest to become due thereon at maturity.

Legal Opinion

The legal opinion of Orrick Herrington & Sutcliffe and Lofton, De Lande & Nelson, both of San Francisco, California, Co-Bond Counsel to the District, approving the validity of the Bonds, will be

4

•

•

-

-

-

"'"

supplied to the original purchasers of the Bonds without cost. A copy of the legal opinion, certified by the official in whose office the original is filed, will accompany each Bond, without charge to the successful bidder.

Co-Bond Counsel has undertaken no responsibility for the accuracy, completeness or fairness of the Official Statement or other offering materials relating to the Bonds and expresses no opinion relating thereto.

Security

The Bonds are general obligations of the District, and the Board of Supervisors of Alameda County, California (the "County") has the power and is obligated to levy ad valorem taxes for payment of both principal and interest of the Bonds upon all property within the District subject to taxation by the District (except certain personal property which is taxable at limited rates), without limitation of rate or amount.

Bond Insurance

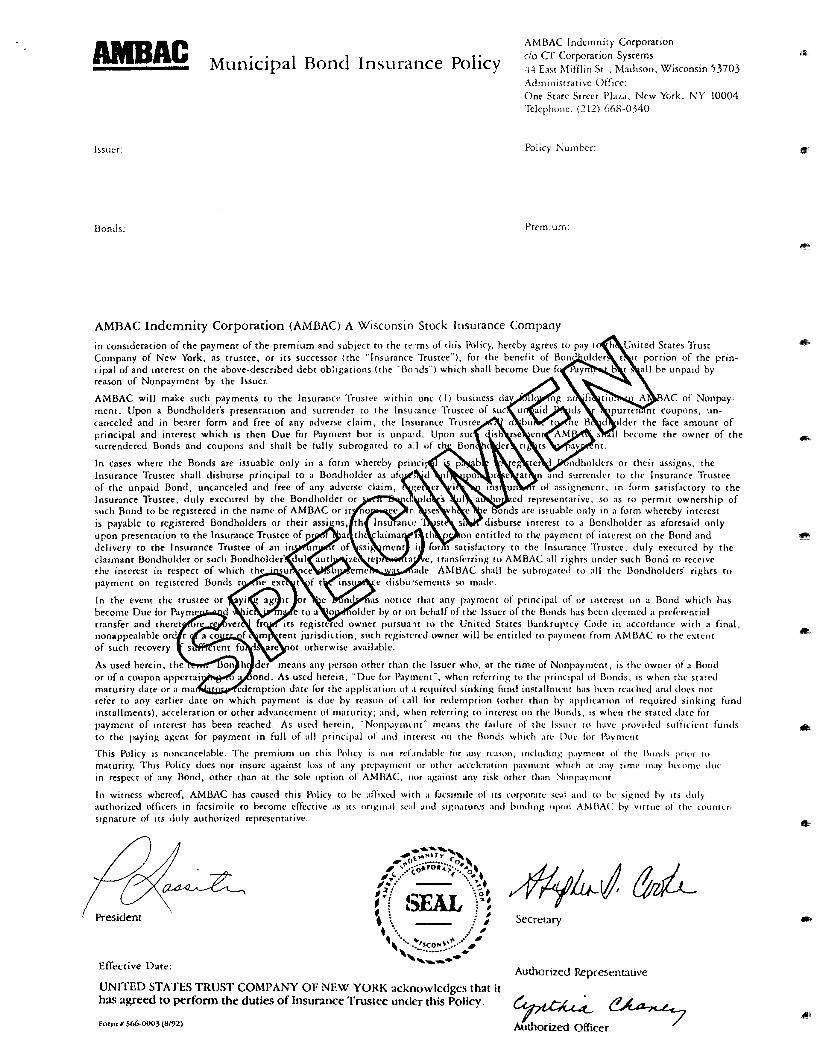

AMBAC Indemnity Corporation (" AMBAC Indemnity") has made a commitment to issue a municipal bond insurance policy (the "Municipal Bond Insurance Policy") relating to the Bonds effective as of the date of issuance of the Bonds. Under the terms of the Municipal Bond Insurance Policy, AMBAC Indemnity will pay to the United States Trust Company of New York, New York, New York or any successor thereto (the "Insurance Trustee") that portion of the principal of and interest on the Bonds which shall become Due for Payment but shall be unpaid by reason of Nonpayment by the Issuer (as such terms are defined in the Municipal Bond Insurance Policy). AMBAC Indemnity will make such payments to the Insurance Trustee on the later of the date on which such principal and interest becomes Due for Payment or within one business day following the date on which AMBAC Indemnity shall have received notice of Nonpayment from the Paying Agent. The insurance will extend for the term of the Bonds and, once issued, cannot be cancelled by AMBAC Indemnity.

The Municipal Bond Insurance Policy will insure payment only on stated maturity dates and on mandatory sinking fund installment dates, in the case of principal, and on stated dates for payment, in the case of interest. If the Bonds become subject to mandatory redemption and insufficient funds are available for redemption of all outstanding Bonds, AMBAC Indemnity will remain obligated to pay principal of and interest on outstanding Bonds on the originally scheduled interest and principal payment dates including mandatory sinking fund redemption dates. In the event of any acceleration of the principal of the Bonds, the insured payments will be made at such times and in such amounts as would have been made had there not been an acceleration.

In the event the Paying Agent has notice that any payment of principal of or interest on a Bond which has become Due for Payment and which is made to a Bondholder by or on behalf of the District has been deemed a preferential transfer and theretofore recovered from its registered owner pursuant to the United States Bankruptcy Code in accordance with a final, nonappealable order of a court of competent jurisdiction, such registered owner will be entitled to payment from AMBAC Indemnity to the extent of such recovery if sufficient funds are not otherwise available.

The Municipal Bond Insurance Policy does not insure any risk other than Nonpayment, as defined in the Policy. Specifically, the Municipal Bond Insurance Policy does not cover:

1. payment on acceleration, as a result of a call for redemption (other than mandatory sinking fund redemption) or as a result of any other advancement of maturity.

5

2. payment of any redemption, prepayment or acceleration premium.

3. nonpayment of principal or interest caused by the insolvency or negligence of any Trustee or Paying Agent, if any.

If it becomes necessary to call upon the Municipal Bond Insurance Policy, payment of principal requires surrender of Bonds to the Insurance Trustee together with an appropriate instrument of assignment so as to permit ownership of such Bonds to be registered in the name of AMBAC Indemnity to the extent of the payment under the Municipal Bond Insurance Policy. Payment of interest pursuant to the Municipal Bond Insurance Policy requires proof of Bondholder entitlement to interest payments and an appropriate assignment of the Bondholder's right to payment to AMBAC Indemnity.

Upon payment of the insurance benefits, AMBAC Indemnity will become the owner of the Bond, appurtenant coupon, if any, or right to payment of principal or interest on such Bond and will be fully subrogated to the surrendering Bondholder's rights to payment.

In the event that AMBAC Indemnity were to become insolvent, any claims arising under the Policy would be excluded from coverage by the California Insurance Guaranty Association, established pursuant to the laws of the State of California.

AMBAC Indemnity is a Wisconsin-domiciled stock insurance corporation regulated by the Office of the Commissioner of Insurance of the State of Wisconsin and licensed to do business in 50 states, the District of Columbia, and the Commonwealth of Puerto Rico, with admitted assets of approximately $2,150,000,000 (unaudited) and statutory capital o:f approximately $1,204,000,000 (unaudited) as of September 30, 1994. Statutory capital consists of AMBAC Indemnity's policyholders' surplus and statutory contingency reserve. AMBAC Indemnity is a wholly-owned subsidiary of AMBAC Inc., a 100% publicly-held company. Moody's Investor's Service, Inc., Standard & Poor's Corporation, and Fitch Investors Service, Inc. have each assigned a triple-A claims-paying ability rating to AMBAC Indemnity.

Copies of AMBAC Indemnity's financial statements prepared in accordance with statutory accounting standards are available from AMBAC Indemnity. The address of AMBAC Indemnity's administrative offices and its telephone number are One State Street Plaza, 17th Floor, New York, New York, 10004 and (212) 668-0340.

AMBAC Indemnity has entered into pro rata reinsurance agreements under which a percentage of the insurance underwritten pursuant to certain municipal bond insurance programs of AMBAC Indemnity has been and will be assumed by a number of foreign and domestic unaffiliated reinsurers.

AMBAC Indemnity has obtained a ruling from the Internal Revenue Service to the effect that the insuring of an obligation by AMBAC Indemnity will not affect the treatment for federal income tax purposes of interest on such obligation and that insurance proceeds representing maturing interest paid by AMBAC Indemnity under policy provisions substantially identical to those contained in its municipal bond insurance policy shall be treated for federal income tax purposes in the same manner as if such payments were made by the issuer of the Bonds.

AMBAC Indemnity makes no representation regarding the Bonds or the advisability of investing in the Bonds and makes no representation regarding, nor has it participated in the preparation of, the Official Statement other than the information suppli1:?d by AMBAC Indemnity and presented under the heading "The Bonds - Bond Insurance."

6 !!E"'

,,.,,

Purpose of the Issue

The District will use the proceeds of the Bonds in the following manner:

• Approximately $2.18 million will be used to rebuild exposed decks which also serve as roofs and to replace paving as necessary to mitigate safety hazards and comply with the American Disability Act (ADA).

• Approximately $1.0 million to provide and improve data and communication cable ways; provide conduit, pullboxes and control points for the wiring of all instructional spaces for voice, data and video.

• Approximately $5.2 million for the improvement of the general classroom, laboratory prototypes, library space and the children's center roof.

• Approximately $440,000 to provide minor real property improvements throughout the District, as prioritized within the campus proposals.

7

Annual Debt Service

Exhibit 1 below presents a schedule of the annual debt service for the Bonds which are the second series of general obligation bonds issued by the District. In June 1993, the District issued Series A in the amount of $9,000,000.

EXHIBIT1 ANNUAL DEBT SERVICE, SERIES B BONDS PERALTA COMMUNm· COLLEGE DISTRICT

Fiscal Year Ending Annual Debt Uune30) Principal Interest Service

1996 $ 0.00 $574,647.50 $574,647.50 1997 190,000.00 568,591.25 758,591.25 1998 205,000.00 556,000.63 761,000.63 1999 215,000.00 542,613.13 757,613.13 2000 230,000.00 528,428.75 758,428.75 2001 240,000.00 513,447.50 753,447.50 2002 255,000.00 497,669.37 752,669.37 2003 270,000.00 480,935.00 750,935.00 2004 290,000.00 463,085.00 753,085.00 2005 305,000.00 444,119.37 749,119.37 2006 325,000.00 424,038.13 749,038.13 2007 345,000.00 402,681.88 747,681.88 2008 365,000.00 380,050.63 745,050.63 2009 385,000.00 356,144.37 741,144.37 2010 410,000.00 330,803.75 740,803.75 2011 435,000.00 303,869.37 738,869.37 2012 460,000.00 275,341.25 735,341.25 2013 485,000.00 245,219.37 730,219.37 2014 515,000.00 213,280.00 728,280.00 2015 545,000.00 179,360.00 724,360.00 2016 580,000.00 143,360.00 723,360.00 2017 615,000.00 105,120.00 720,120.00 2018 650,000.00 64,640.00 714,640.00 2019 685,000.00 21,920.00 706,920.00

Total $9,000,000.00 $8,615,366.25 $17,615,366.25

8

.,

-

411

..,

''"'

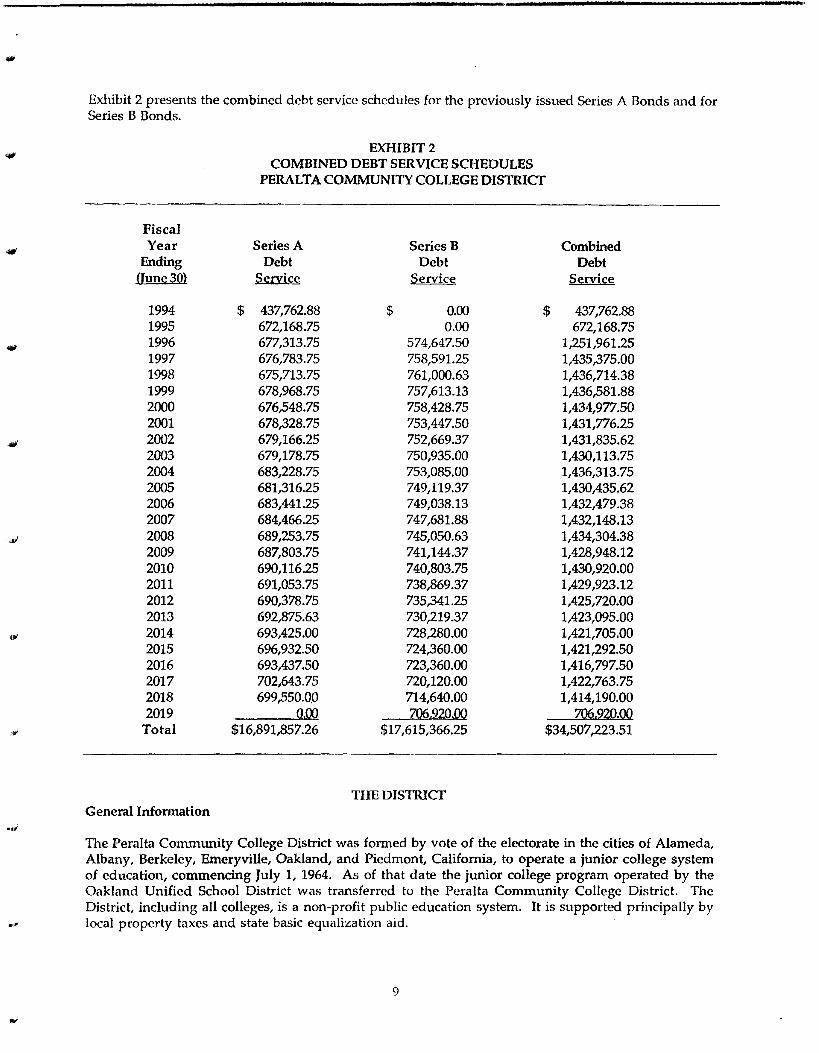

Exhibit 2 presents the combined debt service schedules for the previously issued Series A Bonds and for Series B Bonds.

EXHIBIT 2 COMBINED DEBT SERVICE SCHEDULES

PERALTA COMMUNITY COLLEGE DISTRICT

Fiscal Year Series A Series B Combined

Ending Debt Debt Debt (June30) Service Service Service

1994 $ 437,762.88 $ 0.00 $ 437,762.88 1995 672,168.75 0.00 672,168.75 1996 677,313.75 574,647.50 1,251,961.25 1997 676,783.75 758,591.25 1,435,375.00 1998 675,713.75 761,000.63 1,436,714.38 1999 678,968.75 757,613.13 1,436,581.88 2000 676,548.75 758,428.75 1,434,977.50 2001 678,328.75 753,447.50 1,431,776.25 2002 679,166.25 752,669.37 1,431,835.62 2003 679,178.75 750,935.00 1,430,113.75 2004 683,228.75 753,085.00 1,436,313.75 2005 681,316.25 749,119.37 1,430,435.62 2006 683,441.25 749,038.13 1,432,479.38 2007 684,466.25 747,681.88 1,432,148.13 2008 689,253.75 745,050.63 1,434,304.38 2009 687,803.75 741,144.37 1,428,948.12 2010 690,116.25 740,803.75 1,430,920.00 2011 691,053.75 738,869.37 1,429,923.12 2012 690,378.75 735,341.25 1,425,720.00 2013 692,875.63 730,219.37 1,423,095.00 2014 693,425.00 728,280.00 1,421,705.00 2015 696,932.50 724,360.00 1,421,292.50 2016 693,437.50 723,360.00 1,416,797.50 2017 702,643.75 720,120.00 1,422,763.75 2018 699,550.0.0 714,640.00 1,414,190.00 2019 Q.00 706.920.00 706920.00

Total $16,891,857.26 $17,615,366.25 $34,507,223.51

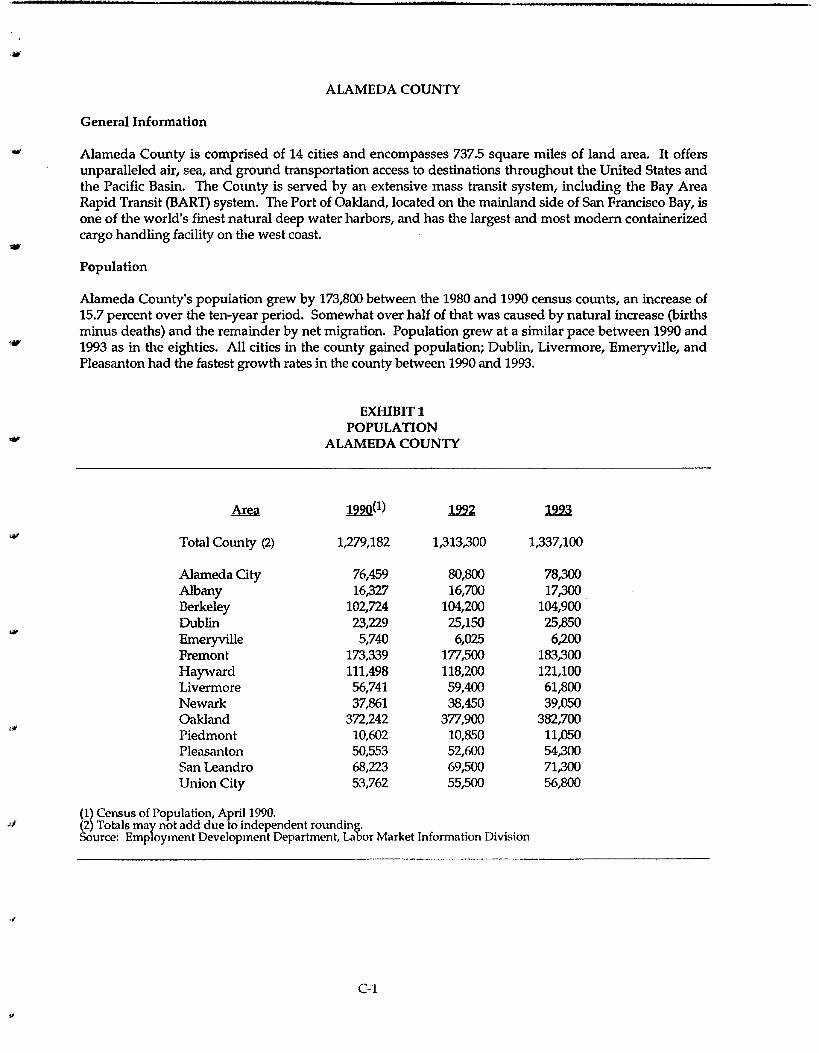

THE DISTRICT General Information

The Peralta Community College District was formed by vote of the electorate in the cities of Alameda, Albany, Berkeley, Emeryville, Oakland, and Piedmont, California, to operate a junior college system of education, commencing July 1, 1964. As of that date the junior college program operated by the Oakland Unified School District was transferred to the Peralta Community College District. The District, including all colleges, is a non-profit public education system. It is supported principally by

.,.. local property taxes and state basic equalization aid.

9

The District covers approximately 78 square miles, and is traversed by Interstate Highways 80, 580 and 880. The District contains an international airport and a deep water port.

The District plants consist of four colleges and the District Administrative Center (DAC). With the exception of the DAC, all of the buildings were built in the early 1970s. The DAC was constructed in 1980. The District is comprised of approximately 30 structures.

The District maintains the College of Alameda, Laney College, Merritt College and Vista Community College. Total full-time equivalent students (FTES) for the 1994-95 academic year is estimated to be 15,710. The District expects attendance to remain stable over the next five to seven years.

The District is governed by a Board of Trustees consisting of seven members and one student. Members are elected to four-year terms in alternating slots. Elections are held every two years. The student trustee is elected yearly by the student body at large.

EXHrnIT 3 FULL-TIME EQUIV A.LENT STUDENTS

PERALTA COMMUNm( COLLEGE DISTRICT

Fiscal Year

1986-87 1987-88 1988-89 1989-90 1990-91 (1)

1991-92 1992-93 1993-94 1994-95 (2)

1995-96 (2)

1996-97 <2>

Full-Time Equivalent Students

14,201 13,786 14,143 14,361 16,682 17,081 16,449 15,710 '15,710 15,867 16,025

(1) In 1990-91 the system was converted from ADA to FfES (Full-Time Equivalent Student). (2) Projection.

Employee Relations

Peralta Community College District employees are represented by three unions. The Peralta Federation of Teachers represents teachers, and the AFL/CIO Local 790 & International Union of Operating Engineers and Local 39 represent classifo!d employees. All three unions are under contracts that expired June 30, 1994. The provisions of the a~~reements that expired will remain in full force and effect until amended by negotiation. In the opinion of management, employee relations are amicable.

10

-

-

Pension Plans

The District participates in the State of California Teacher's Retirement System ("STRS"). This plan covers basically all full-time certificated employees. The District's contribution to STRS for fiscal year 1993-94 was $1,955,344 and for fiscal year 1994-95 $1,767,160 is budgeted.

The District also participates in the State of California Public Employees' Retirement System ("PERS"). This plan covers all classified personnel who are employed four or more hours per day. The District's contribution to PERS for fiscal year 1993-94 was $876,101 and for fiscal year 1994-95 $1,116,210 is budgeted. Both STRS and PERS are operated on a statewide basis.

DISTRICT DEBT STRUCTURE

Short-Term Borrowing

The District has no outstanding short-term debt.

Lease Obligations

The District currently has leases outstanding for a variety of educational equipment including a telephone system and duplicating equipment.

Lease payments through the end of these leases are shown in Exhibit 4.

Long-Term Borrowing

EXHIBIT4 PERALTA COMMUNTIY COLLEGE DISTRICT

OUTSTANDING LEASE OBLIGATIONS

Xe.il Payment

1994-95 $902,301 1995-96 756,221 1996-97 597,731 1997-98 430,266 1998-99 263,710 1999-00 100,364

The District has never defaulted on the payment of principal or interest on any of its indebtedness.

The District will have $32,000,000 of authorized but unissued long-term debt after the issuance of the Bonds. Series A in the amount of $9,000,000 was issued in June 1993.

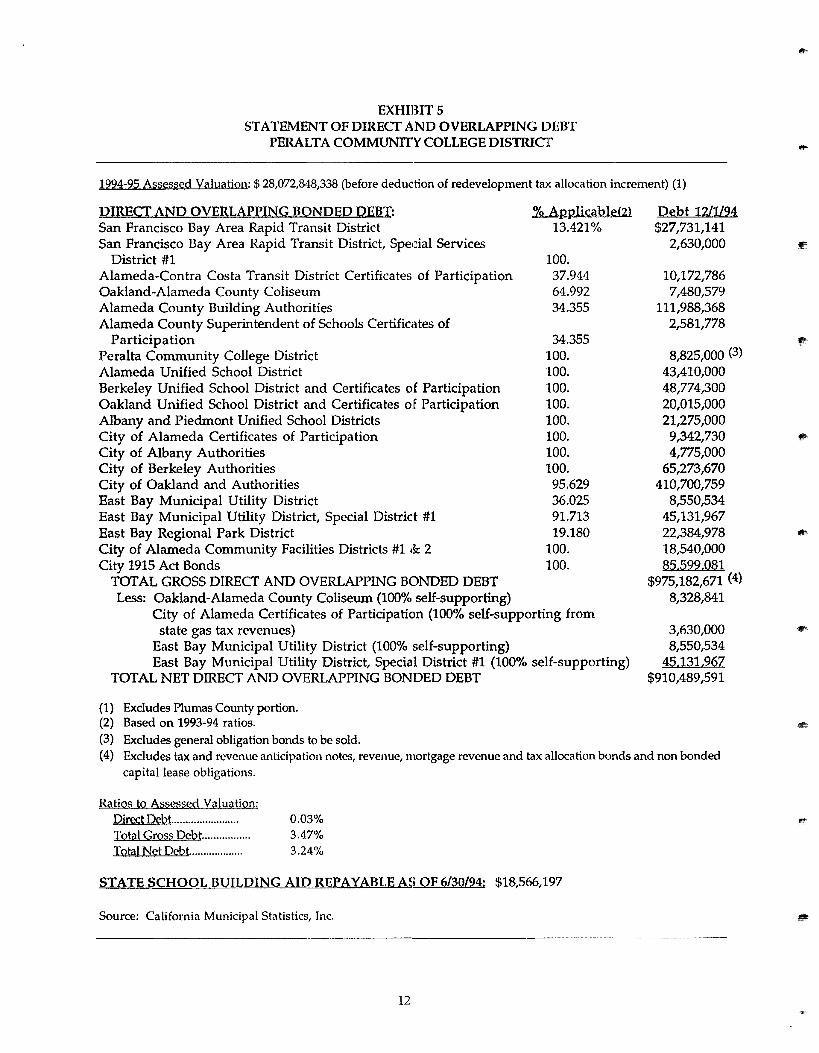

Contained within the District's boundaries are numerous overlapping local agencies providing public services. These local agencies have outstanding bonds issued in the form of general obligation, lease revenue and special assessment. The direct and overlapping debt of the District is shown in Exhibit 5. Self-supporting revenue bonds, tax allocation bonds and non-bonded capital lease obligations are excluded from the debt statement.

11

EXHIBIT 5 STATEMENT OF DIRECT AND OVERLAPPING DEBT

PERALTA COMMUNITY COLLEGE DISTRICT

1994-95 Assessed Valuation:$ 28,072,848,338 (before deduction of redevelopment tax allocation increment) (1)

DIRECT AND OVERLAPPING BONDED DEBT: San Francisco Bay Area Rapid Transit District San Francisco Bay Area Rapid Transit District, Spedal Services

District #1 Alameda-Contra Costa Transit District Certificates of Participation Oakland-Alameda County Coliseum Alameda County Building Authorities Alameda County Superintendent of Schools Certificates of

Participation Peralta Community College District Alameda Unified School District Berkeley Unified School District and Certificates of Participation Oakland Unified School District and Certificates of Participation Albany and Piedmont Unified School Districts City of Alameda Certificates of Participation City of Albany Authorities City of Berkeley Authorities City of Oakland and Authorities East Bay Municipal Utility District East Bay Municipal Utility District, Special District #1 East Bay Regional Park District City of Alameda Community Facilities Districts #1 ck 2 City 1915 Act Bonds

TOTAL GROSS DIRECT AND OVERLAPPING BONDED DEBT Less: Oakland-Alameda County Coliseum (100% self-supporting)

% Applicable(2) 13.421%

100. 37.944 64.992 34.355

34.355 100. 100. 100. 100. 100. 100. 100. 100. 95.629 36.025 91.713 19.180

100. 100.

City of Alameda Certificates of Participation (100% self-supporting from state gas tax revenues)

East Bay Municipal Utility District (100% self-supporting) East Bay Municipal Utility District, Special District #1 (100% self-supporting)

TOTAL NET DIRECT AND OVERLAPPING BONDED DEBT

(1) Excludes Plumas County portion. (2) Based on 1993-94 ratios.

(3) Excludes general obligation bonds to be sold.

Debt 12/1/94 $27,731,141

2,630,000

10,172,786 7,480,579

111,988,368 2,581,778

8,825,000 (3)

43,410,000 48,774,300 20,015,000 21,275,000

9,342,730 4,775,000

65,273,670 410,700,759

8,550,534 45,131,967 22,384,978 18,540,000 85.599.081

$975,182,671 (4)

8,328,841

3,630,000 8,550,534

45.131.967 $910,489,591

(4) Excludes tax and revenue anticipation notes, revenue, mortgage revenue and tax allocation bonds and non bonded capital lease obligations.

Ratios to Assessed Valuation: Direct Debt... .................... . Total Gross Debt ................ . Total Net Debt.. ............... ..

0.03% 3.47% 3.24%

STATE SCHOOL BUILDING AID REPAYABLE AS OF 6/30/94: $18,566,197

Source: California Municipal Statistics, Inc.

12

-----------------------------1·"~-···"'"" _______ .. ____ '"lliW"""-"''"""'""""""""""'"""'"'"'""'""""'-l#HlilttlU1"illillllllialitllll1fl•!illl>"

1111'

Property Tax Collection Procedures

In California, property which is subject to ad valorem taxes is classified as "secured" or "unsecured." The "secured roll" is that part of the assessment roll containing state-assessed public utilities' property and property, the taxes on which are a lien on real property sufficient, in the opinion of the county assessor, to secure payment of the taxes. A tax levied on unsecured property does not become a lien against such unsecured property, but may become a lien on certain other property owned by the taxpayer. Every tax which becomes a lien on secured property has priority over all other liens arising pursuant to State law on such secured property, regardless of the time of the creation of the other liens. Secured and unsecured property are entered separately on the assessment roll maintained by the county assessor. The method of collecting delinquent taxes is substantially different for the two classifications of property.

Property taxes on the secured roll are due in two installments, on November 1 and February 1 of each fiscal year. If unpaid, such taxes become delinquent after December 10 and April 10, respectively, and a 10% penalty attaches to any delinquent payment. In addition property on the secured roll with respect to which taxes are delinquent is sent to collections on or about June 30 of the fiscal year. Such property may thereafter be redeemed by payment of the delinquent taxes and a delinquency penalty, plus a redemption penalty of 1-1 /2% per month to the time of redemption. If taxes are unpaid for a period of five years or more, the property is deeded to the State and then is subject to sale by the county tax collector.

Historically, property taxes are levied for each fiscal year on taxable real and personal property situated in the taxing jurisdiction as of the preceding March 1. A bill enacted in 1983, SB 813 (Statutes of 1983, Chapter 498), however, provided for the supplemental assessment and taxation of property as of the occurrence of a change of ownership or completion of new construction. Thus, this legislation eliminated delays in the realization of increased property taxes from new assessments. As amended, SB 813 provided increased revenue to taxing jurisdictions to the extent that supplemental assessments of new construction or changes of ownership occur subsequent to the March 1 lien date.

Property taxes on the unsecured roll are due on the March 1 lien date and become delinquent, if unpaid on the following August 31. A ten percent (10%) penalty is also attached to delinquent taxes in respect of property on the unsecured roll, and further, an additional penalty of 1-1/2% per month accrues with respect to such taxes beginning the first day of the third month following the delinquency date. The taxing authority has four ways of collecting unsecured personal property taxes: (1) a civil action against the taxpayer; (2) filing a certificate in the office of the county clerk specifying certain facts in order to obtain a judgment lien on certain property of the taxpayer; (3) filing a certificate of delinquency for record in the county recorder's office, in order to obtain a lien on certain property of the taxpayer; and (4) seizure and sale of personal property, improvements or possessory interests belonging or assessed to the assessee. The exclusive means of enforcing the payment of delinquent taxes in respect of property on the secured roll is the sale of the property securing the taxes to the State for the amount of taxes which are delinquent.

Unitary Taxation of Utility Property

Historically, property of regulated public utilities has been assessed for local tax purposes by the State Board of Equalization on a geographical basis in basically the same manner as other taxable property in any taxing jurisdiction.

In 1987, the State Legislature enacted Chapter 921 amending Section 98.9 and various other sections of the Revenue and Taxation Code. The changes call for the establishment in each county of one countywide tax rate area with the assessed value of all unitary and operating non-unitary utility property being assigned to this tax rate area.

13

The result is a single assessed valuation figure for all utility property owned by each utility within the county without any breakdown for individual taxing jurisdictions.

All of this property is then subjected to a tax at a rate equal to the sum of the following two rates:

1. A rate determined by dividing the county's total ad valorem tax levies for the secured roll for the prior year, exclusive of levies for debt serv:ice, by the county's total ad valorem secured roll assessed value for the prior year.

2. A rate determined by dividing the county's total ad valorem tax levies for the secured roll for the prior year for debt service only by the county's total ad valorem secured roll assessed value for the prior year.

The foregoing process results in the creation of two pools of money, pool 1 being available for general tax purposes and pool 2 for debt service purposes, each pool being then allocated to the various taxing jurisdictions in the county by a statutory formula.

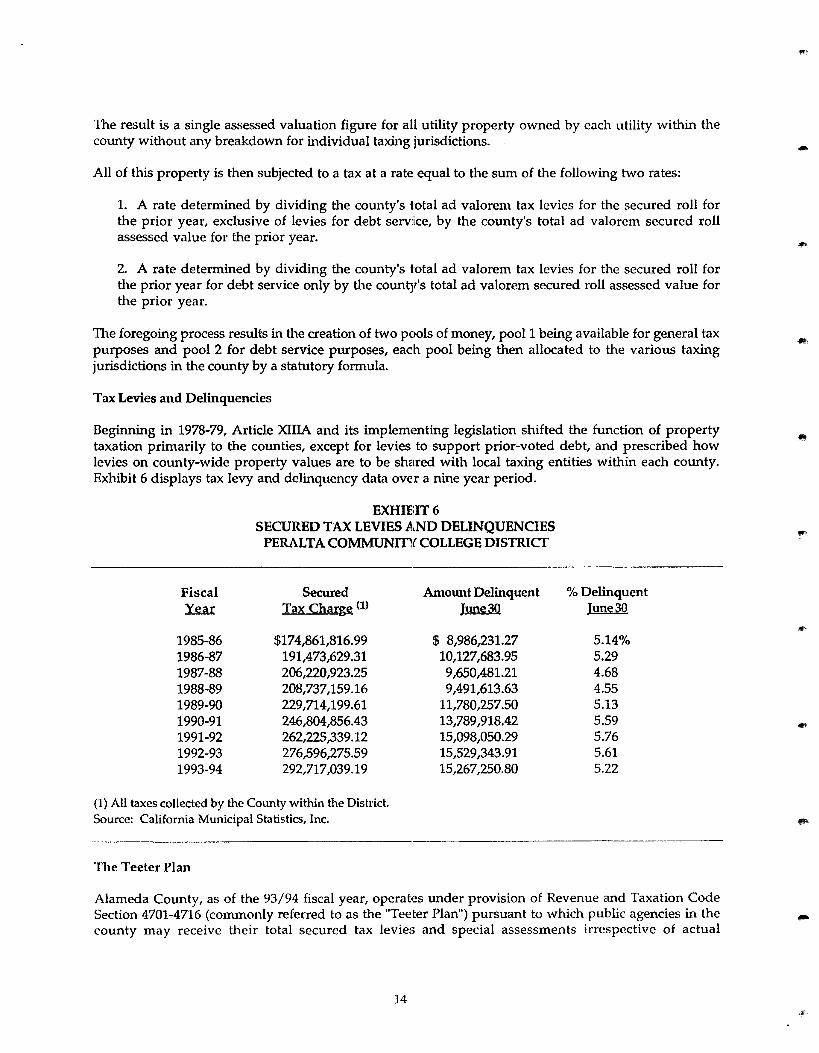

Tax Levies and Delinquencies

Beginning in 1978-79, Article XIIIA and its implementing legislation shifted the function of property taxation primarily to the counties, except for levies to support prior-voted debt, and prescribed how levies on county-wide property values are to be shared with local taxing entities within each county. Exhibit 6 displays tax levy and delinquency data over a nine year period.

Fiscal Year

1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 1991-92 1992-93 1993-94

EXHIE:IT6 SECURED TAX LEVIES AND DELINQUENCIES

PERALTA COMMUNm( COLLEGE DISTRICT

Secured Tax Charge <1>

$174,861,816.99 191,473,629.31 206,220,923.25 208,737,159.16 229,714,199.61 246,804,856.43 262,225,339.12 276,596,275.59 292,717,039.19

Amount Delinquent ~

$ 8,986,231.27 10,127,683.95 9,650,481.21 9,491,613.63

11,780,257.50 13,789 ,918.42 15,098,050.29 15,529,343.91 15 ,267 ,250.80

(1) All taxes collected by the County within the District. Source: California Municipal Statistics, Inc.

The Teeter Plan

% Delinquent ~

5.14% 5.29 4.68 4.55 5.13 5.59 5.76 5.61 5.22

Alameda County, as of the 93/94 fiscal year, operates under provision of Revenue and Taxation Code Section 4701-4716 (commonly referred to as the "Teeter Plan") pursuant to which public agencies in the county may receive their total secured tax levies and special assessments irrespective of actual

14

·-

,.-

-

''"""

collections and delinquencies. Pursuant to said provisions, the county establishes a delinquency reserve and assumes responsibility for all secured delinquencies.

Because of the method of tax collection, the District is assured of 100 percent collection of its total secured tax levies. This method of tax collection and distribution is, however, subject to future discontinuance if demanded by the participating entities.

CotUtty Pooled Inveshnent

As required by state law, the District deposits all of its general fund revenues with the County of Alameda's Pooled Investment Fund. Regarding the Pooled Investment Fund, the County's investment policy states that "The investments of the County shall be diversified and undertaken in a manner which seeks to ensure preservation of capital in the overall portfolio. The investment portfolio shall be designed to attain a market-average rate of return, taking into account investment risk constraints and cash-flow characteristics and requirements of the County's operations."

The County Pooled Investment Fund has an average maturity life of approximately 21 months, as of December 1994. The District has no reason to believe that the general fund revenues or any other District funds on deposit with Alameda County are at risk.

Top Ten Taxpayers

Exhibit 7 lists the top ten property taxpayers within the District for fiscal year 1994-95.

EXHIBIT7 1993-94 TOP TEN TAXPAYERS

PERALTA COMMUNITY COLLEGE DIS1RICT

Alameda Real Estate Investments Kaiser Foundation Health Plan Cutter Laboratories Inc. 1111 Associates Clorox Company Lake Merritt Plaza Kaiser Center Inc. Webster Street Partners, Ltd. Ordway Associates Owens Illinois Glass Container

Property Description

Commercial Office Buildings Commercial Office Buildings Pharmaceutical Manufacturer Commercial Office Buildings Commercial Office Buildings Commercial Office Buildings Commercial Office Buildings Commercial Office Buildings Commercial Office Buildings Heavy Industrial

(1) Total 1994-95 Local Secured Assessed Valuation: $25,821,676,169. Source: California Municipal Statistics, Inc.

15

1994-95 Assessed Valuation

$171,523,630 140,842,797 126,628,784 117,300,000 85,540,797 84,789,495 79,289,427 61,119,142 60,705,300 59,343,935

%of Total

0.66% 0.55 0.49 0.45 0.33 0.33 0.31 0.24 0.24 0.23

Historic Assessed Valuation

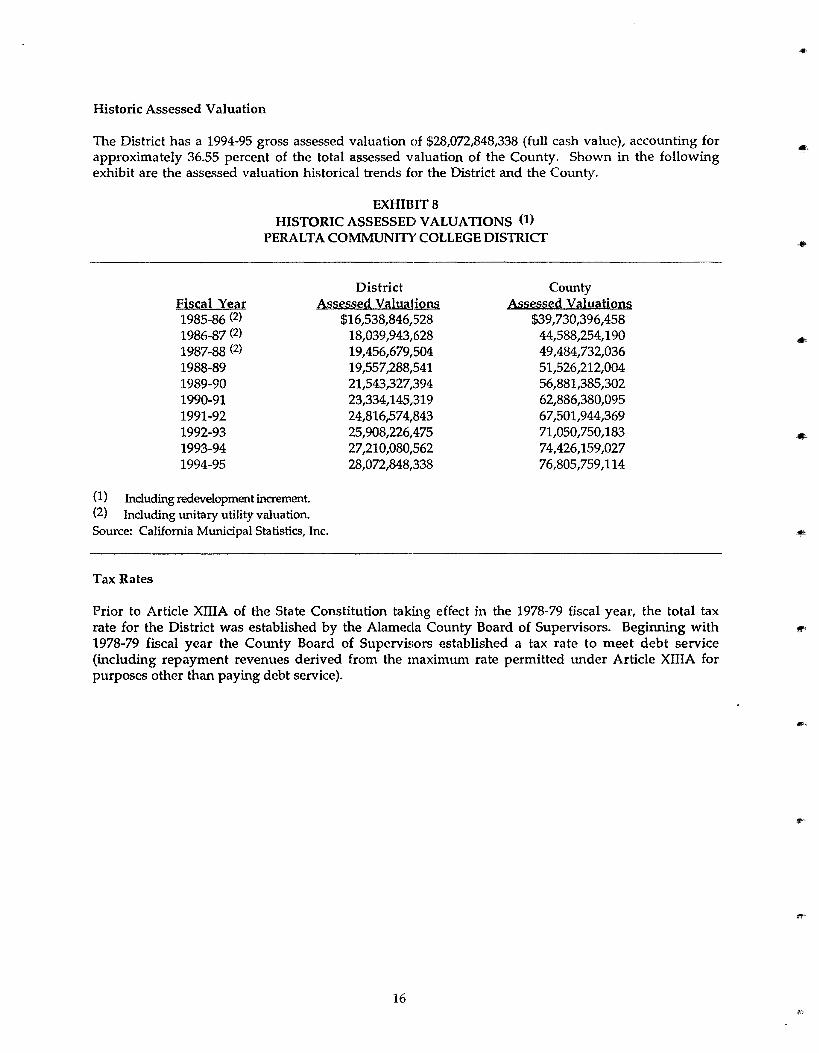

The District has a 1994-95 gross assessed valuation of $28,072,848,338 (full cash value), accounting for approximately 36.55 percent of the total assessed valuation of the County. Shown in the following exhibit are the assessed valuation historical trends for the District and the County.

EXHIBIT 8 HISTORIC ASSESSED VALUATIONS (1)

PERALTA COMMUNm' COLLEGE DISTRICT

Fiscal Year 1985-86 <2>

1986-87 (2)

1987-88 (2)

1988-89 1989-90 1990-91 1991-92 1992-93 1993-94 1994-95

{l) Including redevelopment increment.

District Assessed Valuations

$16,538,846,528 18,039 ,943,628 19,456,679,504 19,557,288,541 21,543,327,394 23,334,145,319 24,816,574,843 25,908,226,475 27,210,080,562 28,072,848,338

(2) Including unitary utility valuation. Source: California Municipal Statistics, Inc.

Tax Rates

County Assessed Valuations

$39,730,396,458 44,588,254, l 90 49 ,484,732,036 51,526,212,004 56,881,385,302 62,886,380,095 67,501,944,369 71,050,750,183 74,426,159,027 76,805,759,114

Prior to Article XIIIA of the State Constitution taking effect in the 1978-79 fiscal year, the total tax rate for the District was established by the Alameda County Board of Supervisors. Beginning with 1978-79 fiscal year the County Board of Supervif;ors established a tax rate to meet debt service (including repayment revenues derived from the maximum rate permitted under Article XIIIA for purposes other than paying debt service).

16

•

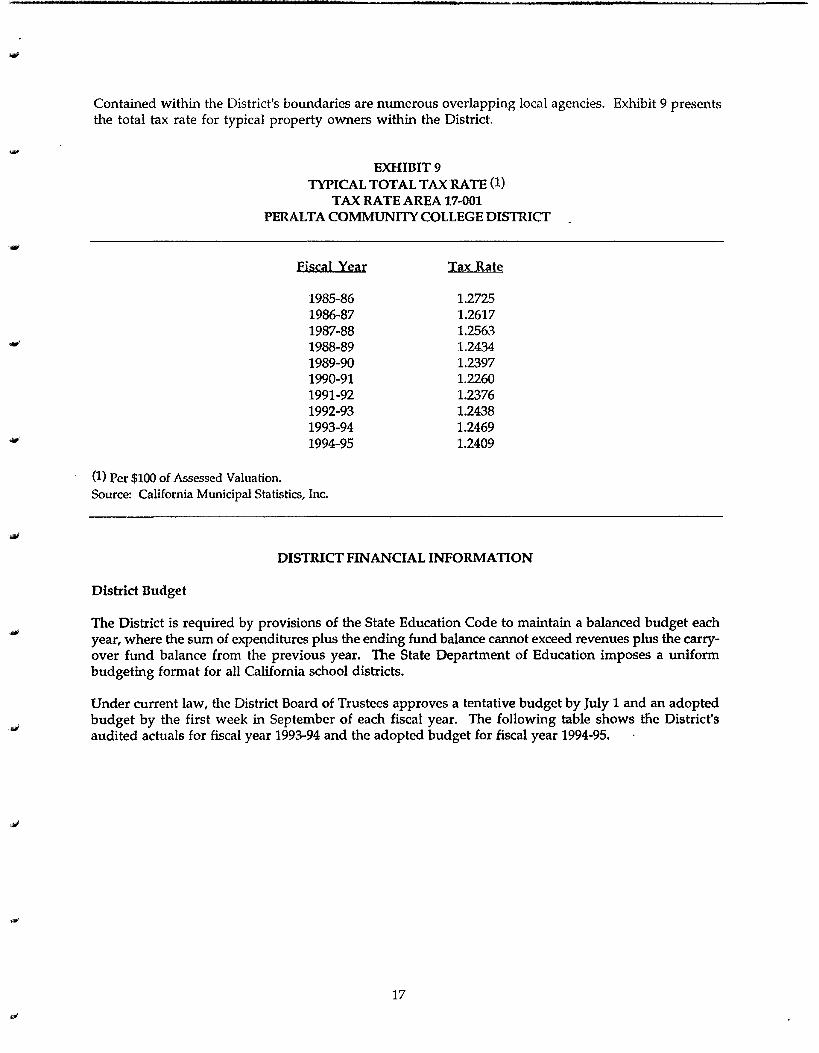

-Contained within the District's boundaries are numerous overlapping local agencies. Exhibit 9 presents the total tax rate for typical property owners within the District.

EXHIBIT9 TYPICAL TOTAL TAX RATE (1)

TAX RATE AREA 17-001 PERALTA COMMUNITY COLLEGE DISTRICT

Fiscal Year

1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 1991-92 1992-93 1993-94 1994-95

Tax Rate

1.2725 1.2617 1.2563 1.2434 1.2397 1.2260 1.2376 1.2438 1.2469 1.2409

(1) Per $100 of Assessed Valuation. Source: California Municipal Statistics, Inc.

DISTRICT FINANCIAL INFORMATION

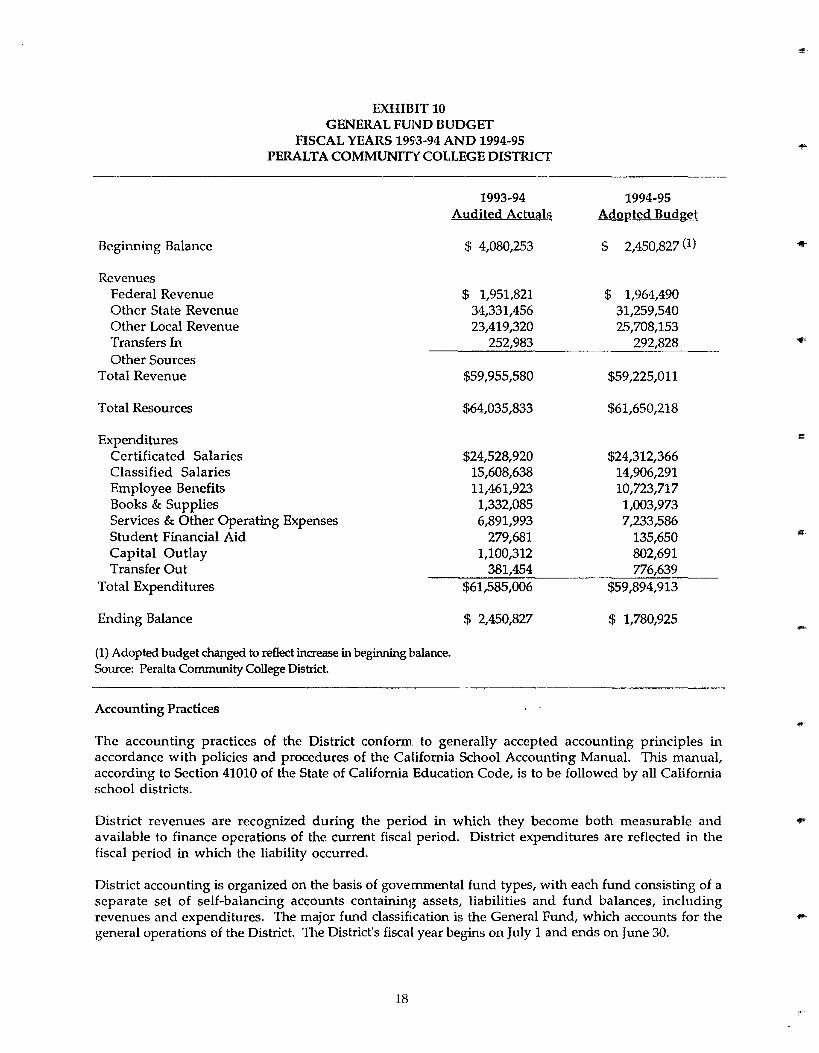

District Budget

The District is required by provisions of the State Education Code to maintain a balanced budget each year, where the sum of expenditures plus the ending fund balance cannot exceed revenues plus the carryover fund balance from the previous year. The State Department of Education imposes a uniform budgeting format for all California school districts.

Under current law, the District Board of Trustees approves a tentative budget by July 1 and an adopted budget by the first week in September of each fiscal year. The following table shows t:li.e District's audited actuals for fiscal year 1993-94 and the adopted budget for fiscal year 1994-95.

17

Beginning Balance

Revenues Federal Revenue Other State Revenue Other Local Revenue Transfers In Other Sources

Total Revenue

Total Resources

Expenditures Certificated Salaries Classified Salaries Employee Benefits Books & Supplies

EXHIBITlO GENERAL FUND BUDGET

FISCAL YEARS 1993-94 AND 1994-95 PERALTA COMMUNITk' COLLEGE DISTRICT

1993-94 Audited Actual!?

$ 4,080,253

$ 1,951,821 34,331,456 23,419,320

252,983

$59,955,580

$64,035,833

$24,528,920 15,608,638 11,461,923 1,332,085

Services & Other Operating Expenses 6,891,993 Student Financial Aid Capital Outlay Transfer Out

Total Expenditures

Ending Balance

(1) Adopted budget ch~ged to reflect increase in beginning balance. Source: Peralta Community College District.

Accounting Practices

279,681 1,100,312

381,454 $61,585,006

$ 2,450,827

1994-95 Adopted Budget

$ 2,450,827 (1)

$ 1,964,490 31,259,540 25,708,153

292,828

$59,225,011

$61,650,218

$24,312,366 14,906,291 10,723,717 1,003,973 7,233,586

135,650 802,691 776,639

$59 ,894,913

$ 1,780,925

The accounting practices of the District conform to generally accepted accounting principles in accordance with policies and procedures of the California School Accounting Manual. This manual, according to Section 41010 of the State of California Education Code, is to be followed by all California school districts.

District revenues are recognized during the period in which they become both measurable and available to finance operations of the current fiscal period. District expenditures are reflected in the fiscal period in which the liability occurred.

District accounting is organized on the basis of governmental fund types, with each fund consisting of a separate set of self-balancing accounts containing assets, liabilities and fund balances, including revenues and expenditures. The major fund classification is the General Fund, which accounts for the general operations of the District. The District's fiscal year begins on July 1 and ends on June 30.

18

•

--

-

d1Jlli'1

.,..,

The District's independent auditors are currently Deloitte & Touche and Clarence White of California. Excerpts from the audited financial statements for the year ended June 30, 1994 are included as Appendix A hereto.

STATE OF CALIFORNIA FINANCES

General

The State of California (the "State") requires that from all State revenues there shall first be set apart the moneys to be applied for support of the public school system and public institutions of higher education. California school districts receive a significant portion of their funding from State appropriations. As a result, decreases in State revenues may significantly affect appropriations made by the legislature to school districts.

The 1994-95 State budget totals $57 billion. The budget includes $40.9 billion in general fund spending.

State Funding of Education

Annual State apportionments of basic and equalization aid to school districts for general purposes are computed up to a revenue limit per unit of average daily attendance ("ADA"). Such apportionments will, in general, amount to the difference between the District's revenue limit and the District's local property tax allocation. Revenue limit calculations are adjusted annually in accordance with a number of factors designed primarily to provide cost of living increases and to equalize revenues among all of the same type of California school districts. In November 1988, California voters approved an amendment to the California Constitution which guarantees primary and secondary education and the community college system a certain percentage of the state general fund budget for the 1988-89 budget year and subsequent budget years.

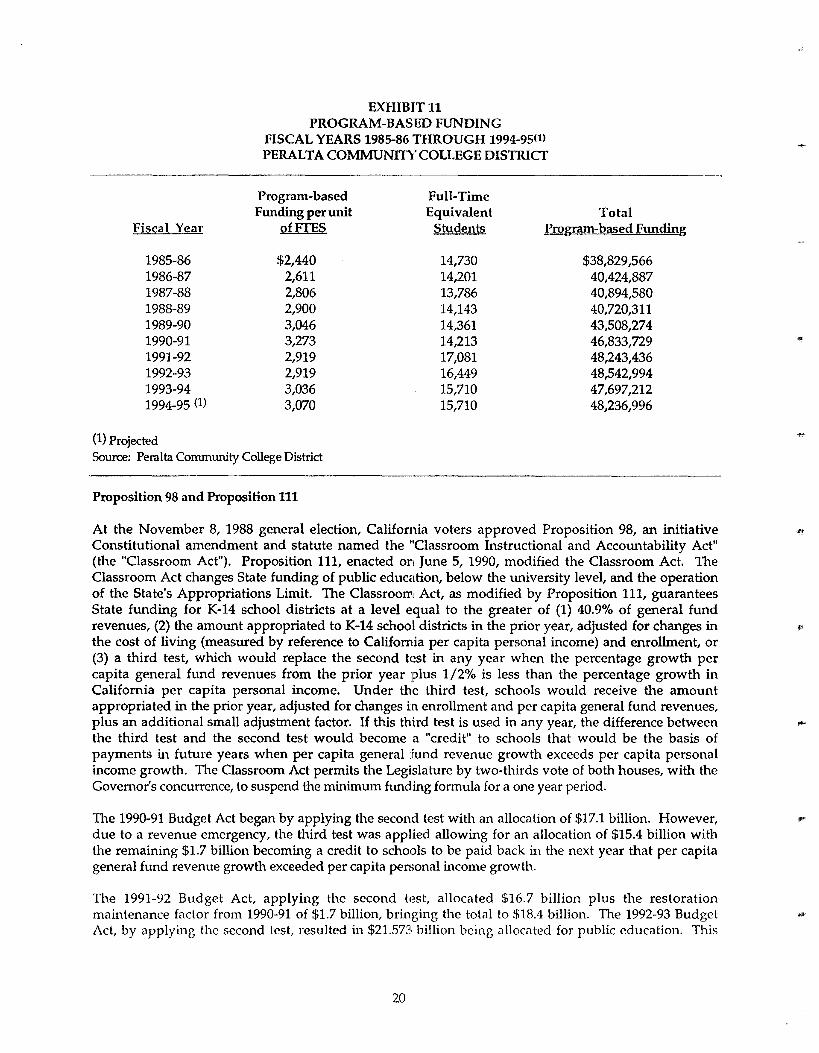

Exhibit 11 shows the District's program-based funding per unit of full-time equivalent students for 1994-95 and the past nine years. In the 1991-92 fiscal year the community college workload measure was changed from average daily attendance (ADA) to full-time equivalent students (FIBS), pursuant to program-based funding regulations. Program-based funding (PBF) is a formula which applies funding standards to several variables common to all educational institutions. PBF replaces the revenue limit approach that uses a single rate per ADA.

19

Fiscal Year

1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 1991-92 1992-93 1993-94 1994-95 (1)

(1) Projected

EXHIBITll PROGRAM-BASED FUNDING

FISCAL YEARS 1985-86 THROUGH 1994-95(1) PERALTA COMMUNID' COLLEGE DISTIUCT

Program-based Funding per unit

ofFfES

Full-Time Equivalent

Students Total

Program-based Funding

$2,440 2,611 2,806 2,900 3,046 3,273 2,919 2,919 3,036 3,070

14,730 14,201 13,786 14,143 14,361 14,213 17,081 16,449 15,710 15,710

$38,829 ,566 40,424,887 40,894,580 40,720,311 43,508,274 46,833,729 48,243,436 48,542,994 47,697,212 48,236,996

Source: Peralta Community College District

Proposition 98 and Proposition 111

At the November 8, 1988 general election, California voters approved Proposition 98, an initiative Constitutional amendment and statute named the "Classroom Instructional and Accountability Act" (the "Classroom Act"). Proposition 111, enacted on June 5, 1990, modified the Classroom Act. The Classroom Act changes State funding of public education, below the university level, and the operation of the State's Appropriations Limit. The Classroom Act, as modified by Proposition 111, guarantees State funding for K-14 school districts at a level equal to the greater of (1) 40.9% of general fund revenues, (2) the amount appropriated to K-14 school districts in the prior year, adjusted for changes in the cost of living (measured by reference to California per capita personal income) and enrollment, or (3) a third test, which would replace the second test in any year when the percentage growth per capita general fund revenues from the prior year plus 1/2% is less than the percentage growth in California per capita personal income. Under the third test, schools would receive the amount appropriated in the prior year, adjusted for changes it1 enrollment and per capita general fund revenues, plus an additional small adjustment factor. If this third test is used in any year, the difference between the third test and the second test would become a "credit" to schools that would be the basis of payments in future years when per capita general Jfund revenue growth exceeds per capita personal income growth. The Classroom Act permits the Legislature by two-thirds vote of both houses, with the Governor's concurrence, to suspend the minimum funding formula for a one year period.

The 1990-91 Budget Act began by applying the second test with an allocation of $17.1 billion. However, due to a revenue emergency, the third test was applied allowing for an allocation of $15.4 billion with the remaining $1.7 billion becoming a credit to schools to be paid back in the next year that per capita general fund revenue growth exceeded per capita personal income growth.

The 1991-92 Budget Act, applying the second test, allocated $16.7 billion plus the restoration maintenance factor from 1990-91 of $1.7 billion, bringing the total to $18.4 billion. The 1992-93 Budget Act, by applying the second test, resulted in $21.573 billion being allocated for public education. This

20

,,w

,d

,,llif

''""

_,..,

includes a 1991-92 over-appropriation of $1.83 billion that was applied against the 1992-93 guarantee and, a loan of $766 million for K-12 that was to be paid back in installments in the first years that the current years K-12 funding is greater than the prior years K-12 funding, not to exceed 50% of the funded revenue limit cost of living adjustment and, a loan of $241 million for community college districts that was to be paid back in two equal installments over the next two years. The result was a per pupil allocation of $4,185.00, the same as 1991-92.

The third test, with an additional clause prohibiting schools from receiving cuts deeper than any other state agencies, was used for 1993-94. The allocation to K-12 public education in the 1993-94 budget was $13.87 billion. The budget allowed for per-pupil funding to remain the same as the previous year and, as in past years, included a loan of approximately $609 million for K-12 schools to be paid back in the same manner as described above. The allocation to community colleges was $1.05 billion and included a loan of $178 million to be paid back in future years.

The 1994-95 budget provides $24.9 billion ($14.4 billion General Fund) in Proposition 98 funding for K-14 programs. This exceeds the amount provided in 1993-94 by $532 million. On a cash basis, the funding level for K-12 schools was $4,225 per pupil in 1993-94, slightly more than the $4,217 level provided in the 1993 budget package. (This resulted from a lower than expected number of K-12 students statewide.) The 1994-95 funding level for K-12 schools is $4,199 per pupil and represents a reduction in overall level of funding from 1993-94. The 1994-95 budget, however, effectively provides the same budgeted level of funding for classroom needs of $4,217 per pupil due to a $100 million reduction in contributions to the Public Employees Retirement System (PERS). The 1994 Budget Act also provides the community colleges $115 million more from Proposition 98 sources than colleges received during 1993-94.

Changes made during the 1992-93 State Budget adoption process require county auditors to increase the amount of property taxes transferred from local governments to school and community college districts. Increasing the amount of property taxes allocated to schools and community colleges reduces the amount that must be provided from the state General Fund under Proposition 98. As a result , the first test for 1992-93 was calculated at 37.391 % of general fund revenues instead of 40.9%. Due to the $2.6 billion transfer from cities, counties, and special districts to K-12 schools, the first test was calculated at approximately 33% for the 1993-94 budget year. Technical problems in the 1993 legislation that increased the property tax shifts had resulted in a smaller than expected transfer to schools and community colleges, and consequently required the state to provide additional funds in order to achieve the desired level of K-14 appropriations.

Since the Classroom Act is unclear in some details, there can be no assurance that the Legislature or a court might not interpret the Classroom Act to require a different percentage of general fm1d revenues to be allocated to K-14 districts, or to apply the relevant percentage to the State's budgets in a different way than is proposed in the Governor's Budget. In any event, the Governor and other fiscal observers expect the Classroom Act to place increasing pressure on the State's budget over future years, potentially reducing resources available for other State programs, especially to the extent the Article XIIIB spending limit would restrain the State's ability to fund such other programs by raising taxes.

The Classroom Act also changes how tax revenues in excess of the State Appropriations Limit are distributed. Any excess State tax revenues up to a specified amount would, instead of being returned to taxpayers, be transferred to K-14 districts. Any such transfer to K-14 districts would be excluded from the State Appropriations Limit for K-14 districts and the K-14 districts' State Appropriations Limit for the next year would automatically be increased by the amount of such transfer. These additional moneys would enter the base funding calculation for K-14 districts for subsequent years, creating further pressure on other portions of the State budget, particularly if revenues decline in a year following an Article XIIIB surplus.

21

Under the Classroom Act as amended by Proposition 111, any excess of the aggregate tax revenues received over the consecutive two year period in which the State Appropriations Limit is tested above the combined Appropriations Limits for those two years is divided equally between transfers to districts and refunds to taxpayers.

LIMITATIONS ONT AX REVENUES

Property Tax Rate Limitations - Article XIIIA

On June 6, 1978, the California voters added Article XIIIA to the California Constitution which limits the amount of any ad valorem taxes on real property to one percent (1%) of its full cash value. Additional ad valorem property taxes may be levied to pay debt service on indebtedness approved prior to July 1, 1978. On June 3, 1986, an amendment to Article XIIIA was approved by California voters. This amendment allows for additional ad valorem p:roperty taxes to be levied on bonded indebtedness, for the acquisition or improvement of real property, which has been approved on or after July 1, 1978, by two-thirds of the voters voting on such indebtedness. Article XIIIA defines full cash value to mean "the county assessor's valuation of real property as shown on the 1975-76 tax bill under full cash value, or thereafter, the appraised value of real property when purchased, newly constructed or a change in ownership has occurred after the 1975 assessment period." This cash value may be increased at a rate not to exceed two percent (2%) per year to account for inflation. The California Supreme Court upheld the validity of Article XIIIA, in general, in the case of Amador Valley Joint Union High School District v. State Board of Equalization (1978), 22 Cal 3rd 208. Article XIIIA has subsequently been amended to permit reduction of the "full cash value" base in the event of declining property values caused by damage, destruction or the other factors, to provide that there would be no increase in the "full cash value" base in the event of reconstruction of property damaged or destroyed in a disaster and in various other minor or technical ways.

The California Supreme Court and U.S. Supreme Court have upheld the constitutionality of Article XIIIA to the California Constitution.

Legislation Implementing Article XIIIA

Legislation has been enacted and amended a number of times since 1978 to implement Article XIIIA. Under current law, local agencies are no longer pem1itted to levy directly any ad valorem property tax. The 1 % property tax is automatically levied annually by the county and distributed according to a formula among taxing agencies. The formula apportions the tax roughly in proportion to the relative shares of taxes levied prior to 1978. Any special tax to pay voter-approved indebtedness is levied in addition to the basic 1 % property tax.

Increases of assessed valuation resulting from reapprnisals of property due to new construction, change in ownership or from the 2% annual adjustment are allocated among the various jurisdictions in the "taxing area" based upon their respective "situs." Any such allocation made to a local agency continues as part of its allocation in future years.