Alvarion Markets, Positioning and Offering

Alvarion Markets, Positioning and Offering. Proprietary Information. 2 Outline Alvarion Market – “The 3 pillars” Market trends Who are we ? Where are.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Alvarion Markets, Positioning and Offering

Proprietary Information.

2

Outline

• Alvarion Market – “The 3 pillars”• Market trends• Who are we ? • Where are we coming from ?• Alvarion Offering and Positioning • Road Map• New Alvarion - Marketing rebound• Wavion who?

Proprietary Information.

3

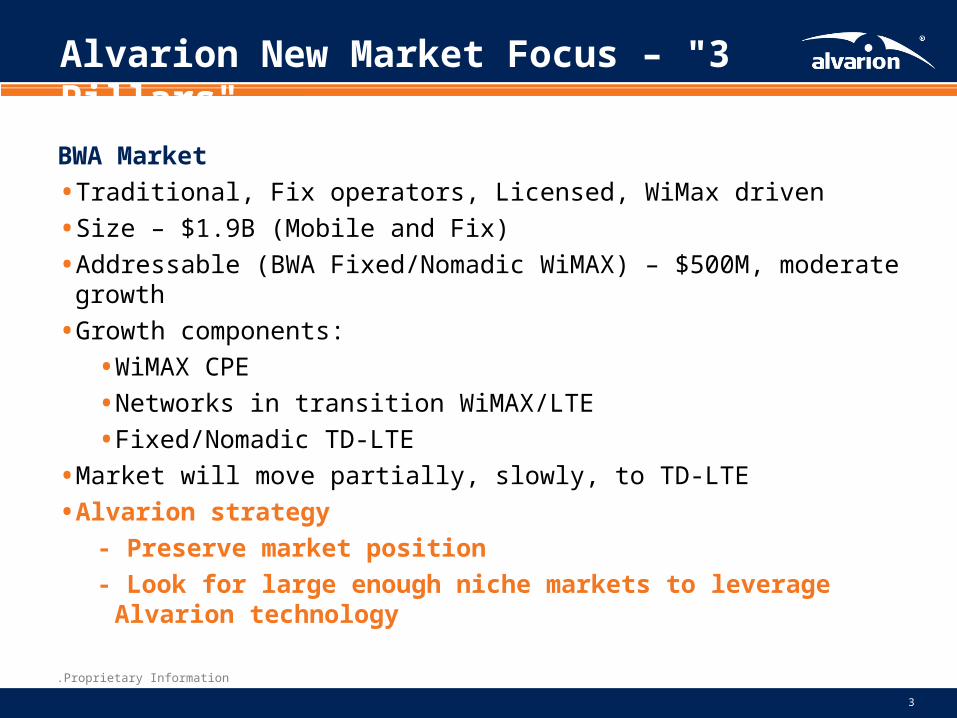

Alvarion New Market Focus – "3 Pillars"

BWA Market

• Traditional, Fix operators, Licensed, WiMax driven

• Size – $1.9B (Mobile and Fix)

• Addressable (BWA Fixed/Nomadic WiMAX) – $500M, moderate growth

• Growth components:

• WiMAX CPE

• Networks in transition WiMAX/LTE

• Fixed/Nomadic TD-LTE

• Market will move partially, slowly, to TD-LTE

• Alvarion strategy

- Preserve market position

- Look for large enough niche markets to leverage Alvarion technology

Proprietary Information.

4

Alvarion New Market Focus – "3 Pillars"

5GHz Private networks (Enterprise, Verticals) market

• Typical topologies: PtP, PtMP - WiFi, WiMAX, Proprietary

• “Close garden” solution

• Size - $800M, CAGR - 13%

• Alvarion Strategy - Rebound and grow

Carrier grade WiFi market

• New, Mobile Carriers

• Traditional, Enterprise

• Open system, mobile WiFi device driven

• Size - $500M, CAGR - 40%

• Alvarion Strategy - Grow and lead

Proprietary Information.

5

Wireless Broadband Market

• Smartphones and tablets are driving exploding data and video traffic

• Operators’ usage of Wi-Fi for data offloading and backhauling, in order to reduce cost, improve QoS, and enable service expansion

• Technology choice (Wi-Fi, 4G/LTE, Femto) driven by capacity, availability & cost

• “White Space” initiative and unlicensed spectrum will use Wi-Fi and LTE

Wi-Fi4G/LTE

Unlicensed Spectrum/bands (2.4, 5 GHz)Licensed bands (700MHz, 1.8, 2.1, 2.3, 2.5, 3.5 GHz)

Focused on fixed & mobile applicationsFocused on country- wide mobile applications

Lowest cost last mile solution (matured, small BS, CPE volume, consolidated standard) consumer electronics

Medium to high cost (non-mature, large BS, expensive CPE) 2-3 years for mass market

Expanding to “White Space” – “Wi-Fi on Steroids”

Frequency & bandwidth allocation delays, diversified

Wi-Fi and LTE are complementary solutions for carriers

Proprietary Information.

6

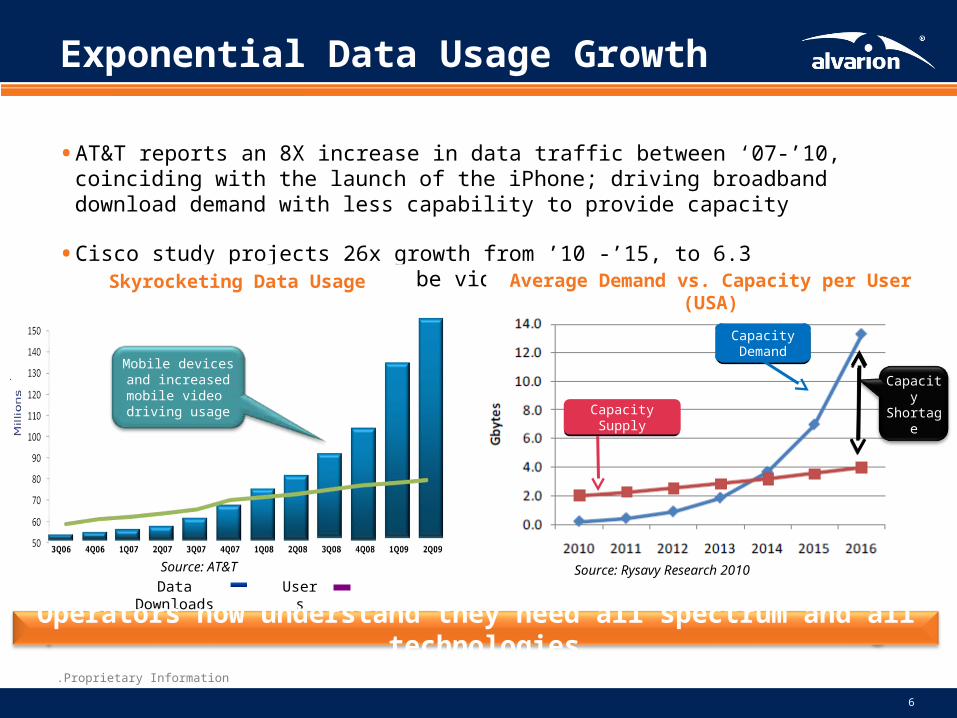

Source: AT&TData Downloads Users

Mobile devices and increased mobile

video driving usage

Capacity DemandCapacity Demand

Capacity SupplyCapacity Supply

Capacity Shortage

Source: Rysavy Research 2010

Operators now understand they need all spectrum and all technologies

Exponential Data Usage Growth

• AT&T reports an 8X increase in data traffic between ‘07-’10, coinciding with the launch of the iPhone; driving broadband download demand with less capability to provide capacity

• Cisco study projects 26x growth from ’10 -’15, to 6.3 exabytes/month; 2/3rds will be video

Skyrocketing Data Usage Average Demand vs. Capacity per User (USA)

Proprietary Information.

7

Where Are We Coming From ?

• 2 decades of wireless experience

• One of the largest fix wireless focused R&D organization

• One of the largest outdoor fix wireless installed base

• Large customer base

• Larger partners base

• WiMAX, WiMAX, … many technology building blocks (OFDMA, MIMO, etc.) are part of LTE

Proprietary Information.

8

Who Are We?

• Broadband Wireless Solutions provider

• Strong two market pillars – Carriers, Enterprise

• Multiple technologies – WiMAX, WiFi, DAS

• Value creator – Connectivity, Coverage, Capacity

• Company in transition

• From the Elephant track to leading in large niche markets

• In turn-around: From declining to stabilizing to rebounding

Providers of optimized broadband wireless solutions to address connectivity, capacity and coverage

challenges of public and private networks

Proprietary Information.

9

New Alvarion - Launch

• Reposition the company: New strategy and messages

• Multiple technologies and solutions

• Serving both Public and Private networks

• New product launches after 2 years with no product “news”

• Profitable company after few years with losses • New branding to serve the above

• Launch in the Sales kick off

Proprietary Information.

10

Alvarion Multi-Technology Solution Portfolio

Market /Solution

MobileCarriers

BWA Operators/WISPs

Enterprise/ VerticalMarkets

4G RAN)Licensed &

Unlicensed spectrum(

PrimarySecondary

- Close Garden 5GHz - Carrier-Grade WiFi2.4GHz and 5GHz

Primary)cellular offload(

Primary)access, backhaul(

Primary)access; backhaul(

Intelligent DASPrimarySecondary

Unique combination of complementary solutions optimized fora variety of networks, applications, topologies, and environments

Proprietary Information.

11

Public SafetySmart City

Industries & Business & Utility

Private Networks

Private NetworksPrivate Networks

WISPsFixed Access

4G Broadband Urban & Rural

4G Wireless Access

4G Wireless Access

4G Small Cell Backhaul

DAS

In-Building Capacity & Coverage

DAS

Metro WiFi

Carrier WiFi

Carrier WiFi

Products and Solutions

3G Data Offload

WBSn

Breeze Ultra

BreezeMAX Extreme

Breeze Access VL

BreezeNet B

BreezeCell BreezeMAX 4Motion

WALKair

Breeze Compact

WBSn

Proprietary Information.

12

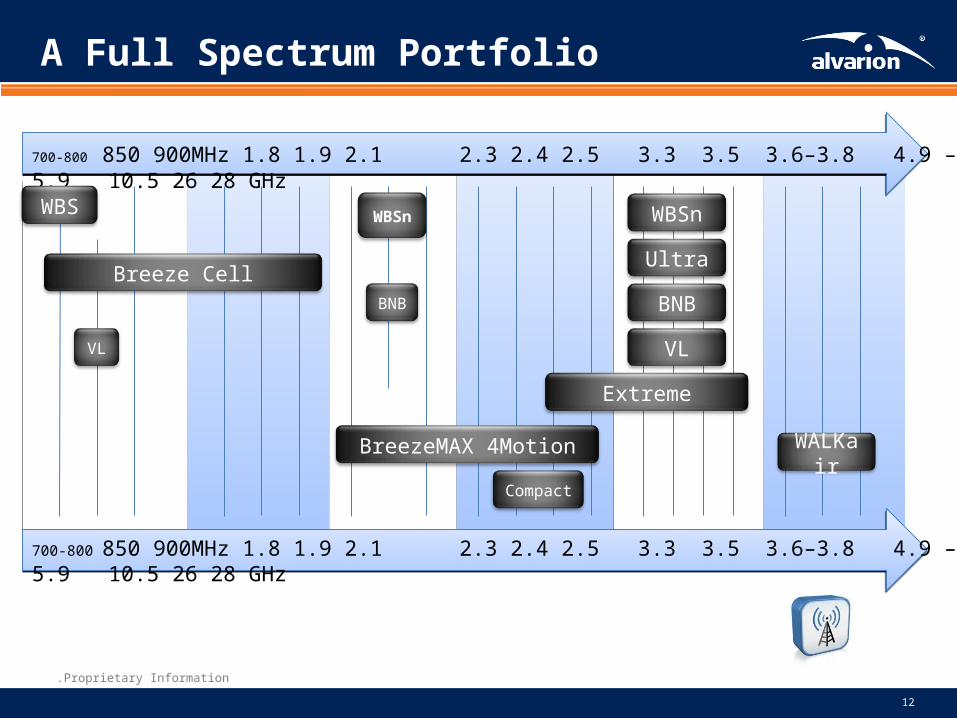

A Full Spectrum Portfolio

700-800 850 900MHz 1.8 1.9 2.1 2.3 2.4 2.5 3.3 3.5 3.6–3.8 4.9 – 5.8 5.9 10.5 26 28 GHz

WALKair

Breeze Cell

BreezeMAX 4Motion

Compact

WBSn

Ultra

BNB

VL

Extreme

700-800 850 900MHz 1.8 1.9 2.1 2.3 2.4 2.5 3.3 3.5 3.6–3.8 4.9 – 5.8 5.9 10.5 26 28 GHz

BNB

WBSn

VL

WBS

Proprietary Information.

13

Alvarion Product Plan 2012

• New products launch in all three market pillars • Compact

• Ultra

• WBSn

• Major product milestones• Extreme 2.0

• WALKair 5000

• LTE Trial, Phase 2

• NMS, Uplift and Wavion products

• DAS, Strategic customer and partner

Proprietary Information.

14

Carrier Wi-Fi• WBSn-2400-S • WBSn-2400-O

• WBSn-2450-S• WBSn-2450-O• WBSn-2450-SO/OS

• WBSn-2400-E • AlvariStar

DAS .. BreezeCell v2.0

Private

Networks

Extreme v1.8 Ultra PtP Ultra PtMP

Extreme v2.0

4G

Wireless

Access

4Motion v3.5

WALKair 5000

Compact 3.5GHz

BMAX Pro 6000

LTE Demo II

Compact 2.5G *

Portfolio Roadmap - 2012

H2’11 H1’12 H2’12

Proprietary Information.

15

Why New Branding?

• Reflect the new Alvarion strategy and messages

• Reposition Alvarion as a key provider of broadband solutions to private and public networks

• Reflect the merger of Alvarion and Wavion – “One Company – New Brand”

• Connect to our customers’ business and lifestyle

• Give Alvarion a modernized and refreshed look

Proprietary Information.

16

How Do We “Look”

Proprietary Information.

17

COO Organization Structure

Proprietary Information.

18

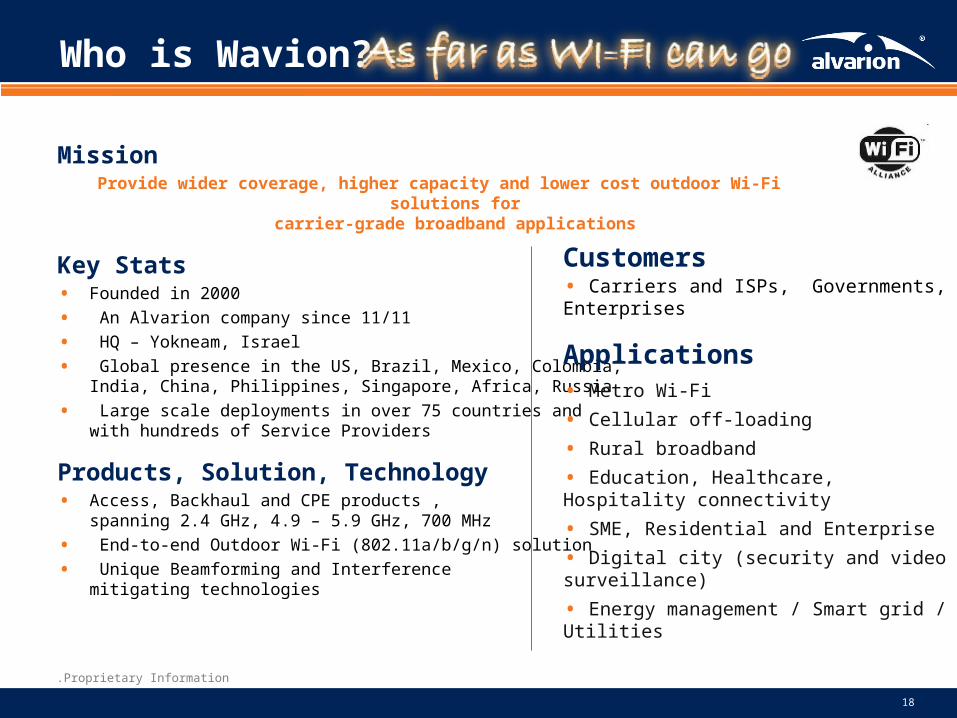

Who is Wavion?

MissionProvide wider coverage, higher capacity and lower cost outdoor Wi-Fi solutions for

carrier-grade broadband applications

Key Stats• Founded in 2000

• An Alvarion company since 11/11

• HQ – Yokneam, Israel

• Global presence in the US, Brazil, Mexico, Colombia,India, China, Philippines, Singapore, Africa, Russia

• Large scale deployments in over 75 countries andwith hundreds of Service Providers

Products, Solution, Technology• Access, Backhaul and CPE products ,

spanning 2.4 GHz, 4.9 – 5.9 GHz, 700 MHz

• End-to-end Outdoor Wi-Fi (802.11a/b/g/n) solution

• Unique Beamforming and Interferencemitigating technologies

Customers• Carriers and ISPs, Governments, Enterprises

Applications• Metro Wi-Fi

• Cellular off-loading

• Rural broadband

• Education, Healthcare, Hospitality connectivity

• SME, Residential and Enterprise

• Digital city (security and video surveillance)

• Energy management / Smart grid / Utilities

Proprietary Information.

19

Wi-Fi Market Trends

• Growing number of Wi-Fi devices

• Consolidation of Wi-Fi in Cellular handheld devices

• Start of Wi-Fi consolidation in the core cellular network (handoffs, mobility, roaming)

• Most of outdoor Wi-Fi market is still in traditional applications and developing countries

• Carriers growing interest in Wi-Fi

• Outdoor is noisier

2011 was the transition year to “Outdoor 11.n”

Proprietary Information.

20

Demand for Carrier Grade Wi-Fi

In Developed Countries

• 3G data offloading due to high penetration of smartphones and tablets

• Broadband extension to rural communities

In Developing Countries

• Low cost broadband access for Metro and Rural

• Residential and SME, mostly desk-top users

• Synergies with existing cellular infrastructure

Large carriers require licensed and unlicensed (Wi-Fi) frequencies to fully meet capacity needs

• Active deployments in US, Korea, Japan, EU etc.

• RFPs from Multinational carriers – Bharti, Telefonica, Vodafone, T-Mobile etc.

New Carrier Grade Wi-Fi Market is Ramping up

Proprietary Information.

21

ISPs, Government, Verticals

Growth in traditional unlicensed markets –mass market technology and devices

• ISPs

• Government

• Vertical markets

• Education

• Campuses

• Healthcare

• Hospitality connectivity

• Digital city(Security and Video Surveillance)

• Energy Management / Smart Grid / Utilities

Proprietary Information.

22

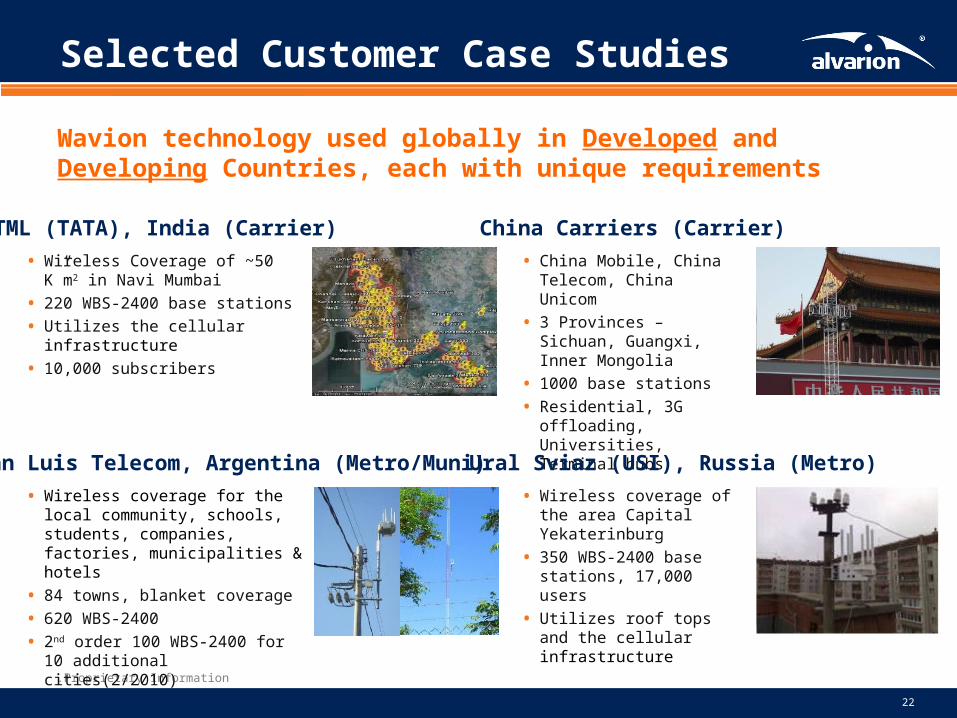

Wavion technology used globally in Developed and Developing Countries, each with unique requirements

Selected Customer Case Studies

TTML (TATA), India (Carrier)

• Wireless Coverage of ~50 K”m2 in Navi Mumbai

• 220 WBS-2400 base stations

• Utilizes the cellular infrastructure

• 10,000 subscribers

China Carriers (Carrier)

• China Mobile, China Telecom, China Unicom

• 3 Provinces – Sichuan, Guangxi, Inner Mongolia

• 1000 base stations

• Residential, 3G offloading, Universities, Terminal hubs

San Luis Telecom, Argentina (Metro/Muni)

• Wireless coverage for the local community, schools, students, companies, factories, municipalities & hotels

• 84 towns, blanket coverage

• 620 WBS-2400

• 2nd order 100 WBS-2400 for 10 additional cities(2/2010)

Ural Sviaz (USI), Russia (Metro)

• Wireless coverage of the area Capital Yekaterinburg

• 350 WBS-2400 base stations, 17,000 users

• Utilizes roof tops and the cellular infrastructure

Proprietary Information.

23

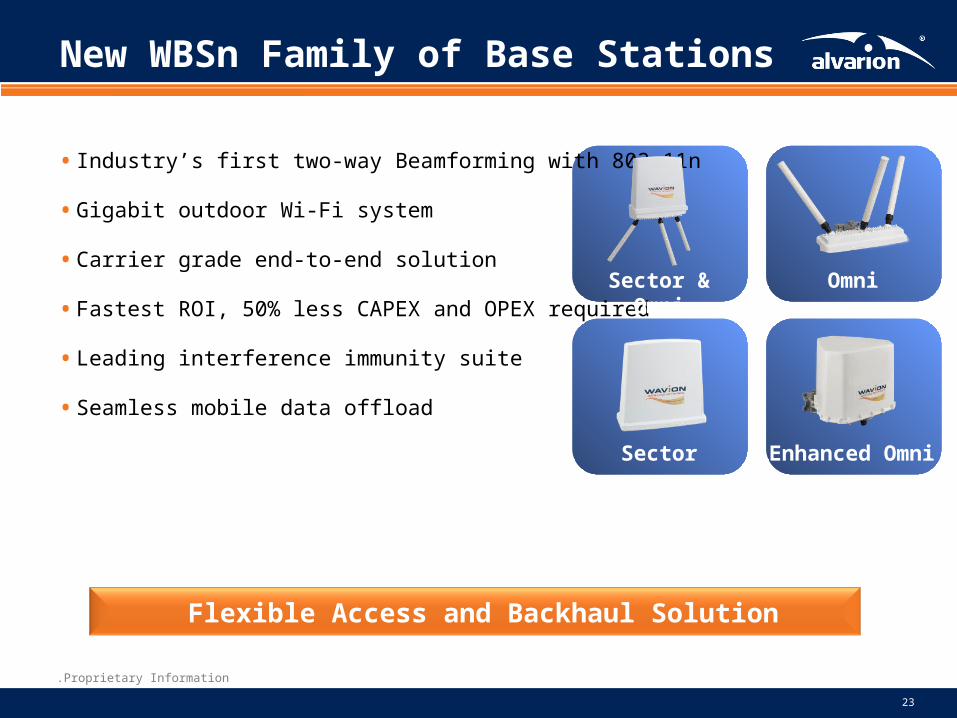

• Industry’s first two-way Beamforming with 802.11n

• Gigabit outdoor Wi-Fi system

• Carrier grade end-to-end solution

• Fastest ROI, 50% less CAPEX and OPEX required

• Leading interference immunity suite

• Seamless mobile data offload

Omni

New WBSn Family of Base Stations

Flexible Access and Backhaul Solution

Sector & Omni

Enhanced OmniSector

Proprietary Information.

24

Wavion offers end-to-end carrier grade wireless networks for a variety of applications, based on its Omni-direction and Sector Base Stations

•Carrier grade Wi-Fi solution

•One-stop-shop for projectexecution

•Wide product range

•Access, backhaul, CPEs,NMS, service provisioning,billing

•Fully managed

•Open standards

•Layer 3 – 4 routing, QOS, AAA, etc.

WBSn - E2E Wi-Fi Network Solution

CPEAccess Network

Bridging & Backhauling

Core Network

Indoor CPEs

Integrated backhaul Self forming Self healing

Portable Wi-Fi clients

Multiple configurations, 2.4

and 5 GHz dual band

Point-to-point linksWavion Service-Pro

WavioNet NMS

Outdoor CPEs

USB CPEs

Proprietary Information.

25

NOC

IP core

Cellular Data Network

Internet GW

WAN

HLR

• Beamforming 802.11n• Carrier grade • SIM authentication• Local break-out and full BH• Future: HS2.0, LBS, roaming

Wavion’s Mobile Data Offload

Proprietary Information.

26

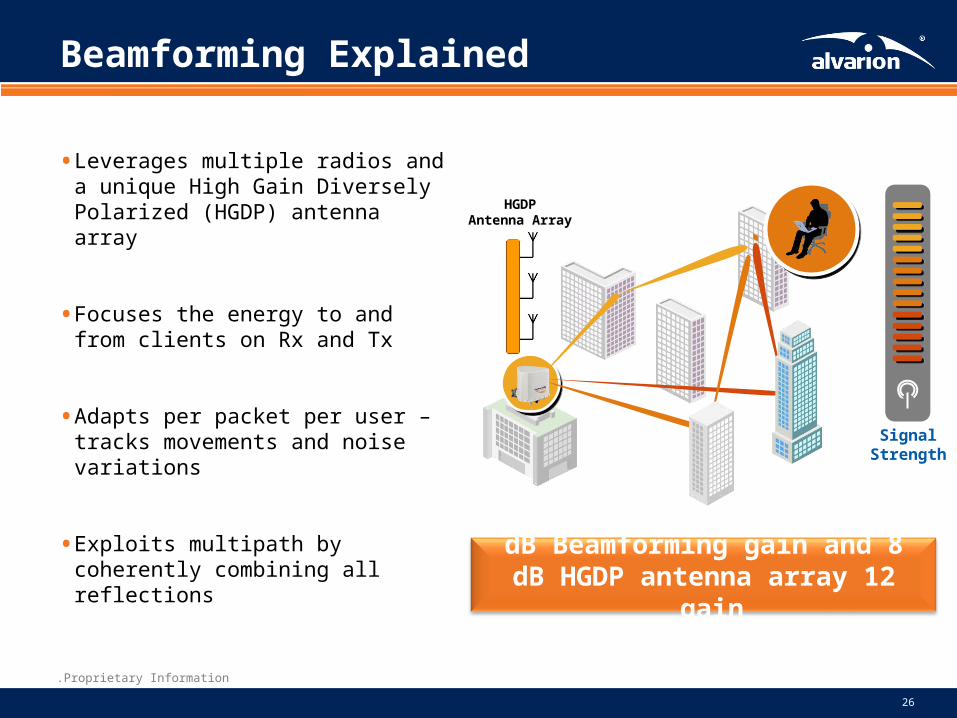

SignalStrength

HGDPAntenna Array

8 dB Beamforming gain and12 dB HGDP antenna array gain

Beamforming Explained

• Leverages multiple radios and a unique High Gain Diversely Polarized (HGDP) antenna array

• Focuses the energy to and from clients on Rx and Tx

• Adapts per packet per user – tracks movements and noise variations

• Exploits multipath by coherently combining all reflections

Proprietary Information.

27

Typical Deployment Scenarios

As Far As Wi-Fi Can GO

Proprietary Information.

28

Unlicensed BWA Market & Positioning

Low-End WISPs

High-End WISPs

Ca

mp

us

Sa

fe C

ity

Air

po

rts

Se

a p

ort

s

Min

es

Oil

& g

as

Ho

tels

Ma

lls

SP

G

Access Service

3G Offload

Ubi

quiti

Ubi

quiti

Mik

roT

ikM

ikro

Tik

Alv

ario

n +

Wav

ion

A

lvar

ion

+ W

avio

n

Ruc

kus

Ruc

kus

Mot

orol

aM

otor

ola

Rad

win

, T

ropo

s,

Fire

tide,

Sky

pilo

t

Rad

win

, T

ropo

s,

Fire

tide,

Sky

pilo

t

Alta

i, B

elA

irA

ltai,

Bel

Air

$$$perAccount

Dire

ctD

istr

ibu

tion

G r o w t h

Cis

coC

isco

Proprietary Information.

29

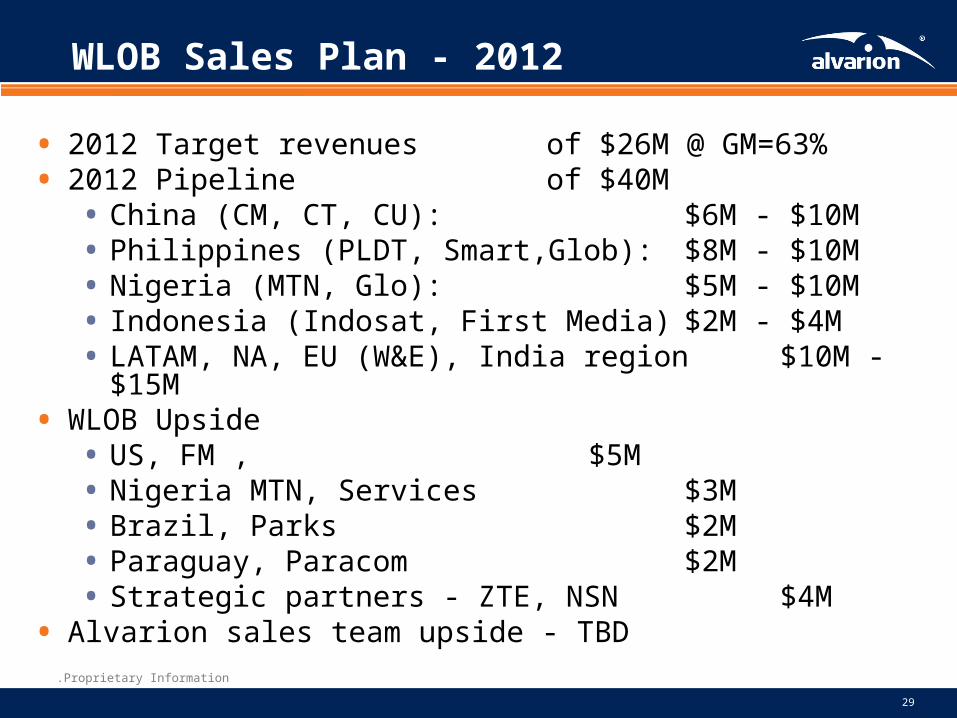

WLOB Sales Plan - 2012

• 2012 Target revenues of $26M @ GM=63%• 2012 Pipeline of $40M

• China (CM, CT, CU): $6M - $10M• Philippines (PLDT, Smart,Glob): $8M - $10M• Nigeria (MTN, Glo): $5M - $10M• Indonesia (Indosat, First Media) $2M - $4M• LATAM, NA, EU (W&E), India region $10M - $15M

• WLOB Upside• US, FM , $5M• Nigeria MTN, Services $3M • Brazil, Parks $2M• Paraguay, Paracom $2M• Strategic partners - ZTE, NSN $4M

• Alvarion sales team upside - TBD

Proprietary Information.

30

WLOB Sales Plan - 2012 #2

• Strategic Partners • OEM with ZTE • Ericsson / NSN / ALU – achieve homologation, at least one • Production in Brazil • ODM for WiFi Indoor strategy - WCPEn / WBSn-I

• Market Penetration• Asia - Indonesia, Thailand, Vietnam, Japan, Australia • Africa – Another Cellular group and large distributors • Western Europe • Eastern Europe - Serbia, Poland, Romania, Bulgaria, Hungary

• New Markets• 5.x Access and Backhaul – “Open garden”• Large scale indoor offering and GTM• Cable market, product, GTM - TBD• 700 MHz market – Sign new agreement with FM

Proprietary Information.

31

Sales Synergies in Process

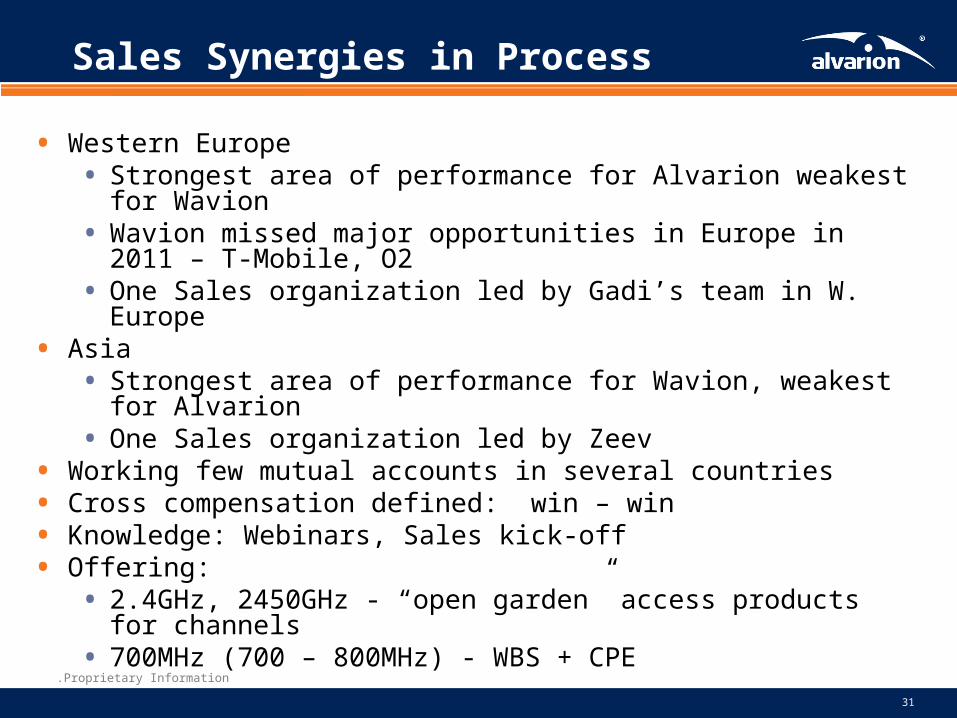

• Western Europe • Strongest area of performance for Alvarion weakest for Wavion • Wavion missed major opportunities in Europe in 2011 – T-Mobile, O2• One Sales organization led by Gadi’s team in W. Europe

• Asia • Strongest area of performance for Wavion, weakest for Alvarion • One Sales organization led by Zeev

• Working few mutual accounts in several countries• Cross compensation defined: win – win • Knowledge: Webinars, Sales kick-off• Offering:

• 2.4GHz, 2450GHz - “open garden” access products for channels• 700MHz (700 – 800MHz) - WBS + CPE

Proprietary Information.

32

Summary

• Wider technology, wider offering, wider addressable market

• New comer to a strong growth market, well positioned to succeed in this market

• Sizeable company for a growing market

• Strong synergies between Alvarion - Wavion

• Good news to the market - new strategy, new products, new markets

• Streamlined organization

2012 should be a turning point – It’s execution time!

Related Documents