RISK MANAGEMENT UPDATE Q2 2012 ALTRIUS CAPITAL MANAGEMENT, INC. | 855-ALTRIUS | WWW.ALTRIUS.US GLOBAL PERSPECTIVES WITH A VALUE FOCUS. PROVIDING TOTAL RETURN TO INVESTORS.

Altrius Town Hall Webinar 06/14/12

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

R I S K M A N A G E M E N T U P DA T E

Q2 2012

ALTRIUS CAPITAL MANAGEMENT INC | 855-ALTRIUS | WWWALTRIUSUS

GLOBAL PERSPECTIVES WITH A VALUE FOCUS PROVIDING TOTAL RETURN TO INVESTORS

Q2 2012

Altrius Team

2

James RussoChief Investment Strategist

Portfolio Manager

Allison CowardSenior Client Advisor

Analyst

Tara Hughes CPASenior Client Advisor

Analyst

Zachary SmithAnalyst

Team Portfolio Manager

Loriann HarkerClient Services Manager

Director Performance Accounting

Nathan ByrdAnalyst

Team Portfolio Manager

Rita SmithClient Services Manager

Director Operations Compliance

Investment Committee

Blue Team

Red Team

Q2 2012

Strategies

3

Q2 2012

Mobile Technology

4

Q2 2012

Executive Summary

5

Rising event risk probability ndash during the second quarter of 2012 various macroeconomic factors have increased the downside risks to global growth and investment returns in the near term

Heightened volatility ndash market volatility has spiked given the degree ofuncertainty and the inadequacy of policy response

Strategic risk management response ndash in Q1 and April we implemented several tactical portfolio shifts in an attempt to mitigate market volatility

Opportunity in crisis ndash negative headlines and pervasive gloomy sentiment haveenabled us to acquire distressed assets and improve portfolio returns and income

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

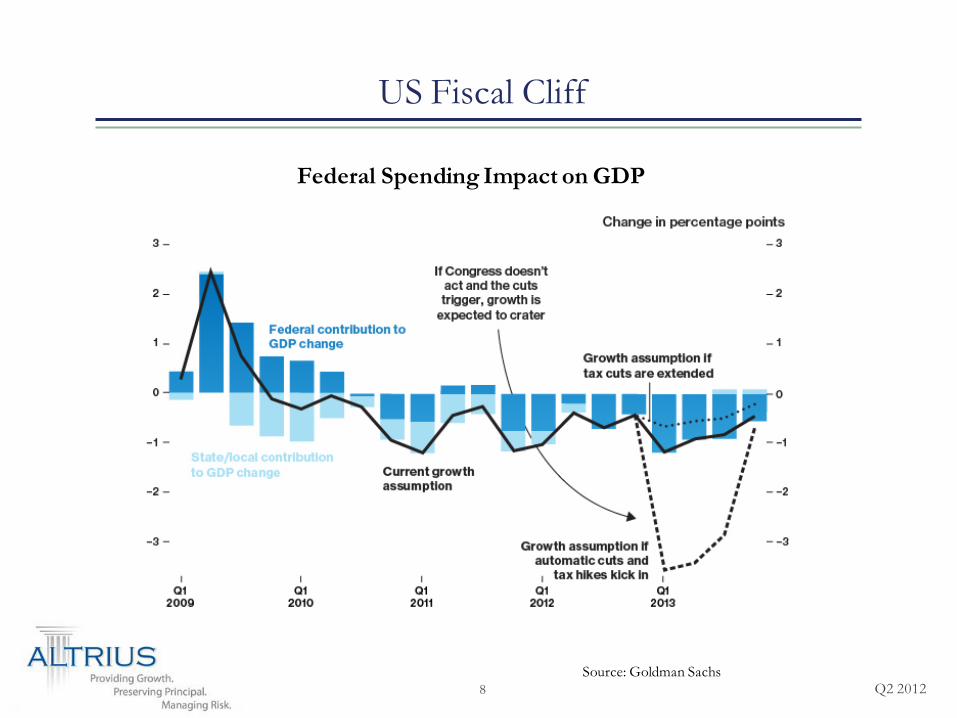

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

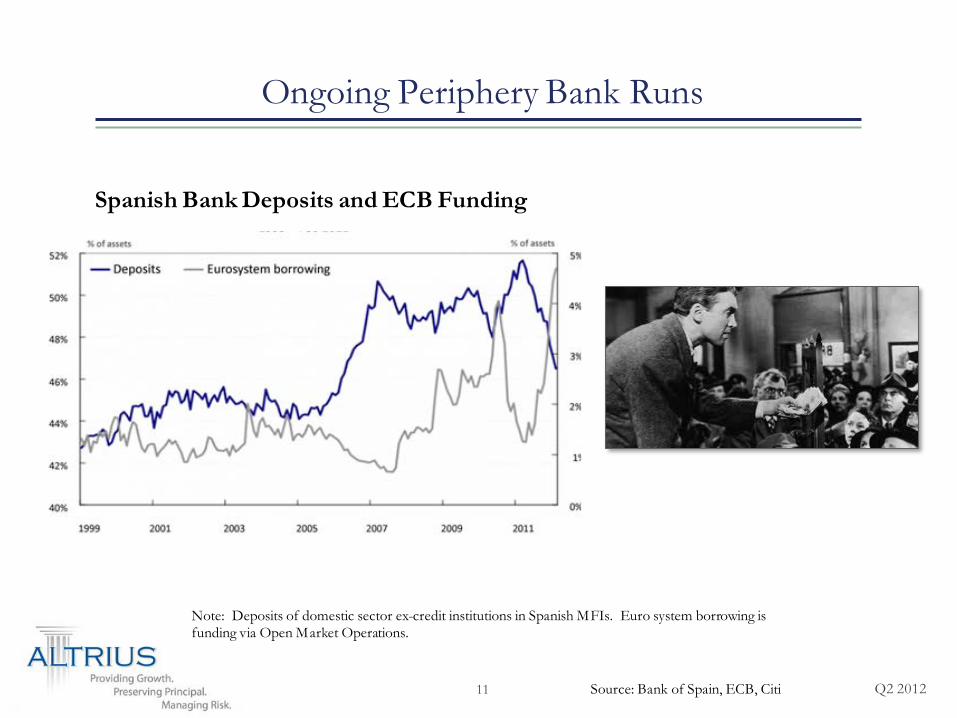

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

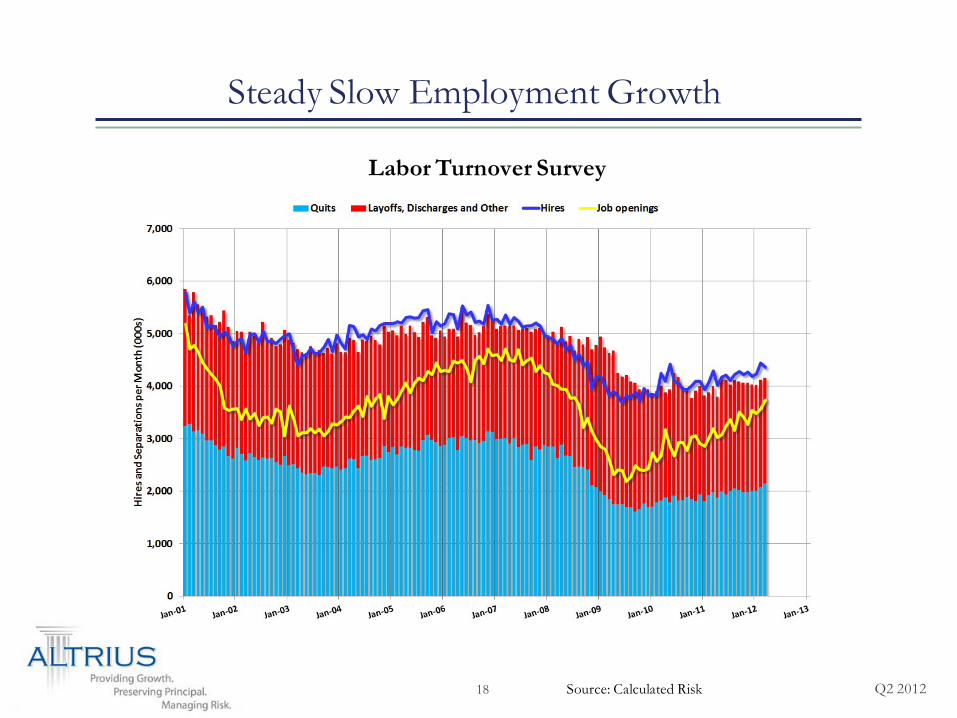

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

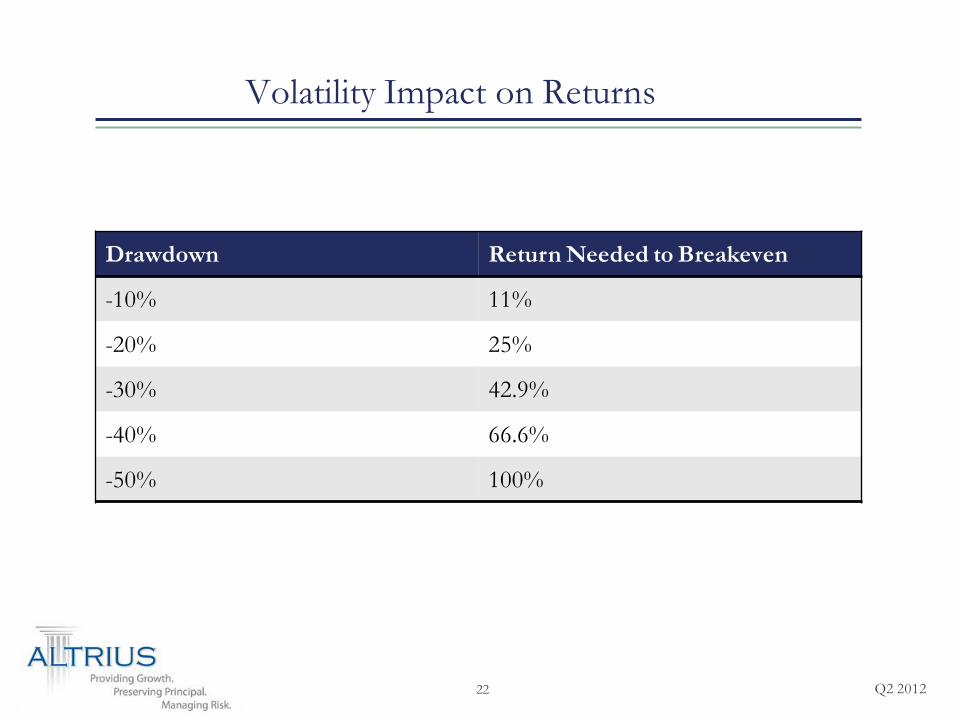

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

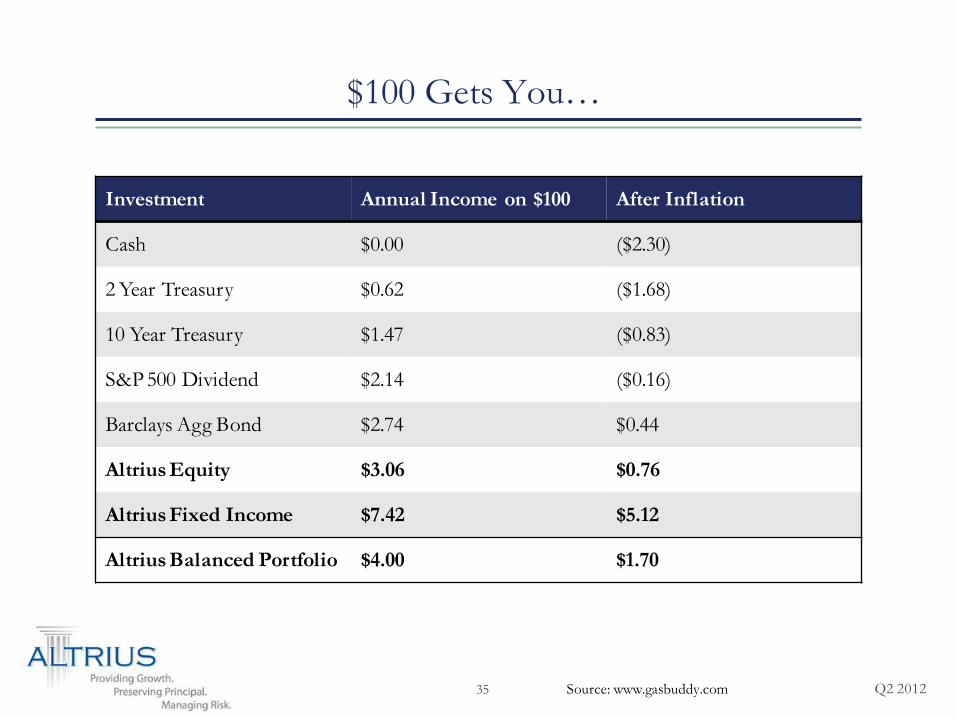

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Altrius Team

2

James RussoChief Investment Strategist

Portfolio Manager

Allison CowardSenior Client Advisor

Analyst

Tara Hughes CPASenior Client Advisor

Analyst

Zachary SmithAnalyst

Team Portfolio Manager

Loriann HarkerClient Services Manager

Director Performance Accounting

Nathan ByrdAnalyst

Team Portfolio Manager

Rita SmithClient Services Manager

Director Operations Compliance

Investment Committee

Blue Team

Red Team

Q2 2012

Strategies

3

Q2 2012

Mobile Technology

4

Q2 2012

Executive Summary

5

Rising event risk probability ndash during the second quarter of 2012 various macroeconomic factors have increased the downside risks to global growth and investment returns in the near term

Heightened volatility ndash market volatility has spiked given the degree ofuncertainty and the inadequacy of policy response

Strategic risk management response ndash in Q1 and April we implemented several tactical portfolio shifts in an attempt to mitigate market volatility

Opportunity in crisis ndash negative headlines and pervasive gloomy sentiment haveenabled us to acquire distressed assets and improve portfolio returns and income

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Strategies

3

Q2 2012

Mobile Technology

4

Q2 2012

Executive Summary

5

Rising event risk probability ndash during the second quarter of 2012 various macroeconomic factors have increased the downside risks to global growth and investment returns in the near term

Heightened volatility ndash market volatility has spiked given the degree ofuncertainty and the inadequacy of policy response

Strategic risk management response ndash in Q1 and April we implemented several tactical portfolio shifts in an attempt to mitigate market volatility

Opportunity in crisis ndash negative headlines and pervasive gloomy sentiment haveenabled us to acquire distressed assets and improve portfolio returns and income

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Mobile Technology

4

Q2 2012

Executive Summary

5

Rising event risk probability ndash during the second quarter of 2012 various macroeconomic factors have increased the downside risks to global growth and investment returns in the near term

Heightened volatility ndash market volatility has spiked given the degree ofuncertainty and the inadequacy of policy response

Strategic risk management response ndash in Q1 and April we implemented several tactical portfolio shifts in an attempt to mitigate market volatility

Opportunity in crisis ndash negative headlines and pervasive gloomy sentiment haveenabled us to acquire distressed assets and improve portfolio returns and income

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Executive Summary

5

Rising event risk probability ndash during the second quarter of 2012 various macroeconomic factors have increased the downside risks to global growth and investment returns in the near term

Heightened volatility ndash market volatility has spiked given the degree ofuncertainty and the inadequacy of policy response

Strategic risk management response ndash in Q1 and April we implemented several tactical portfolio shifts in an attempt to mitigate market volatility

Opportunity in crisis ndash negative headlines and pervasive gloomy sentiment haveenabled us to acquire distressed assets and improve portfolio returns and income

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Event Risks

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

Primary Global Risks

7

Source Risk to Global Growth

United States ldquoFiscal cliffrdquo hit of 5 to GDP at year-end

Europe Disorderly unwinding of the Euro bank runs etc

Emerging Markets Slowdown in China affecting other countries

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion

- Slide Number 37

- Contact Information

-

Q2 2012

US Fiscal Cliff

8Source Goldman Sachs

Federal Spending Impact on GDP

Q2 2012

Debt Ceiling Debate Hurts the Economy

9

Index of Economic Policy Uncertainty Debt Ceiling Impasse 2011

Source VoxEUorg

Note Index of policy-related economic uncertainty Weights 12 News-based 16 tax expirations 16 CPI disagreement 16 expenditures disagreement after each index normalized to have a standard-deviation of 1 News query run Feb 3 2011 Index normalized mean 100 from 1985-2009

Q2 2012

Euro is Structurally Unsound

10Source JP Morgan OECD

Euro Zone Current Account Balances

Q2 2012

Ongoing Periphery Bank Runs

11 Source Bank of Spain ECB Citi

Note Deposits of domestic sector ex-credit institutions in Spanish MFIs Euro system borrowing is funding via Open Market Operations

Spanish Bank Deposits and ECB Funding

Q2 2012

History Repeats

12 Source Essays in Persuasion Reinhart and Rogoff

Ultimately and probably soon there must be a readjustment of the balance of exports and imports America must buymore and sell less This is the only alternative to her making to Europe an annual present Either American pricesmust rise faster than European (which will be the case if the Federal Reserve Board allows the gold influx to produce itsnatural consequences) or failing this the same result must be brought about by a further depreciation of the Europeanexchanges until Europe by inability to buy has reduced her purchases to articles of necessity

-John M Keynes 1921

0

50

100

150

200

250

300

350

Germany France UK Italy Spain US

Publ

ic D

ebt

GD

P

1921 1924 1929

Country Public Debt Post-WWI

Q2 2012

Key Upcoming Euro Zone Dates

13

Date Event

Sunday June 17th Election in Greece to determine ruling party

Monday June 18th Independent Spanish bank stress tests by the ldquoBig 4rdquo

Monday June 18th Start of 2 day G20 summit meeting

Thursday June 21st Meeting of Euro Zone finance ministers

Thursday June 28th Start of 2 day European summit in Brussels

Saturday June 30th Greece required to enact new austerity measures

Q2 2012

Chinarsquos Unsustainable Economic Model

14

Residential Housing Bubbles

Source HSBC

Hou

sing

Val

ue M

ultip

le o

f GD

P

Q2 2012

China Slowing

15 Source Markit HSBC

China Manufacturing PMI

Q2 2012

Economic Overview

Q2 2012

The ldquoPlow Horse Economyrdquo

17 Source Calculated Risk

Percent US Job Losses in Post-WWII Recessions

Q2 2012

Steady Slow Employment Growth

18 Source Calculated Risk

Labor Turnover Survey

Q2 2012

Significant US Market Outperformance

19 Source Bespoke Invest

SampP 500 vs MSCI World Index

Q2 2012

Gas Prices Falling

20 Source wwwgasbuddycom

Average US Retail Gasoline Price

Q2 2012

The Importance of Managing Volatility

Q2 2012

Volatility Impact on Returns

22

Drawdown Return Needed to Breakeven

-10 11

-20 25

-30 429

-40 666

-50 100

Q2 2012

Low-Volatility Relative Performance

23

Contrary to CAPM efficient market claims high risk is often not associated with high reward

Empirical Returns by Volatility QuintileVa

lue o

f $1

Inve

sted

in 19

68

Source Benchmarks as Limits to Arbitrage Understanding the Low Volatility Anomaly Financial Analyst Journal Volume 67 2011

Q2 2012

Altrius Commitment to Risk-Adjusted Returns

24

Altrius has maintained a consistent focus on risk management while also achieving strong returns

Source Brockhouse Cooper analytics as of 12312011

Altrius 5yr RiskReturn vs Brockhouse Cooper LC Value Mandate

Ann

ualiz

ed R

etur

n (

)

Standard Deviation ()

Altrius LC Dividend Income

Russell 1000 Value

Altrius LC Dividend

Russell1000 Value

5yr Return 207 -264

StdDev 1991 2277

Beta 086 100

5yr Jensenrsquos Alpha 398 000

TrackingError 470 NA

Jensenrsquos Alpha is the average difference betweenthe return of the manager and the return of apassive strategy of equal market risk

Q2 2012

Altriusrsquo Tactical Response in Q1 and April

Q2 2012

Actions Taken in Q1 and April

26

Reduced portfolio Beta ndash during the market run-up in the first quarter we sold several more volatile stocks such as BAC and replaced them with healthcare and defense which have historically been less volatile

Added short position ndash purchased a position in a triple-short ETF intended to provide ballast to the rest of the portfolio

Increased fixed income allocation ndash reduced equity exposure and purchased bonds and preferred stocks with the proceeds

Defensive fund position ndash raised cash inside the Altrius Small Cap Value Fundin order to offset the volatility of the asset class

Q2 2012

Subsequent Market Decline

27 Source Doug Short

Q2 2012

Opportunity in Crisis

Q2 2012

Durable Business

29

Q2 2012

Example Stock ConAgra Foods

30

Business Consumer foods Chef Boyardee Egg Beaters Healthy Choice Snack Pack Garden Frost David Seeds etc

Dividend yield 39

PriceEarnings 13x (trailing twelve months)

Q2 2012

Stock Investment Criteria

31

Criteria Explanation

Durable business Simple time-tested business model with proven above-average profitability over market cycles

Above-average dividend Dividends are a critical source of long-run returns and high-dividend stocks have been show to outperform

Value price We avoid high flyers and limit ourselves to buying when assets are on sale relative to the broader market

International presence Where possible we invest in multinational companies with global brand recognition and overseas growth potential

Q2 2012

Non-Durable Businesses

32

Q2 2012

Example Stock HampR Block

33

Business Tax preparation service provider

Dividend yield 53

PriceEarnings 14x (trailing twelve months)

Q2 2012

Fixed Income Opportunities

34

Q2 2012

$100 Gets Youhellip

35 Source wwwgasbuddycom

Investment Annual Income on $100 After Inflation

Cash $000 ($230)

2 Year Treasury $062 ($168)

10 Year Treasury $147 ($083)

SampP 500 Dividend $214 ($016)

Barclays Agg Bond $274 $044

Altrius Equity $306 $076

Altrius Fixed Income $742 $512

Altrius Balanced Portfolio $400 $170

Q2 2012

Conclusion

36

We expect near term volatility primarily from political catalysts

Our focus is on managing risk rather than on outperforming an index

We have implemented several changes to mitigate potential drawdowns

Our long term outlook remains optimistic and we are finding investment opportunities in the crisis

Q2 2012

Questions

Q2 2012

Contact Information

38

Toll Free 855-ALTRIUSEmail Address infoaltrius-capitalcom

Altrius Capital Management434 Fayetteville StreetSuite 2110Raleigh NC 27601Phone 919-746-7977

Altrius Capital Management1323 Commerce DriveNew Bern NC 28562Phone 252-638-7598Fax 252-635-6739

Worldwide

Raleigh

New Bern

- Slide Number 1

- Altrius Team

- Strategies

- Mobile Technology

- Executive Summary

- Slide Number 6

- Primary Global Risks

- US Fiscal Cliff

- Debt Ceiling Debate Hurts the Economy

- Euro is Structurally Unsound

- Ongoing Periphery Bank Runs

- History Repeats

- Key Upcoming Euro Zone Dates

- Chinarsquos Unsustainable Economic Model

- China Slowing

- Slide Number 16

- The ldquoPlow Horse Economyrdquo

- Steady Slow Employment Growth

- Significant US Market Outperformance

- Gas Prices Falling

- Slide Number 21

- Volatility Impact on Returns

- Low-Volatility Relative Performance

- Altrius Commitment to Risk-Adjusted Returns

- Slide Number 25

- Actions Taken in Q1 and April

- Subsequent Market Decline

- Slide Number 28

- Durable Business

- Example Stock ConAgra Foods

- Stock Investment Criteria

- Non-Durable Businesses

- Example Stock HampR Block

- Fixed Income Opportunities

- $100 Gets Youhellip

- Conclusion