Altria Inc. The Fund @ Sprott Equity Research Sell, Current: $52.50, Price Target: $44.64 March 11, 2015 Spyridoula Maria Karasavva BIBCandidate 2017 Global Financial Management and Systems Equity Analyst [email protected] http://fund.ssb.carleton.ca Kyle Stolys BCom Candidate 2016 Finance Sector Manager [email protected] Updated Investment Thesis 5-Year Performance Source: Bloomberg Decline in cigarette volume The cigarette industry has been experiencing a long term 3-4% annual decline. Despite a rising market share in Marlboro, Altria’s cigarette shipment volume has been following industry’s lead and has been declining around 3% yoy. Well-run low maintenance business with very skilled Management Strengthening Taxes and Litigation pressure Dividend yield Altria’s CAPEX on average equals around 3-4% of the company’s Cash from Operations. Altria also manages to operate efficiently using negative working capital while increases its profitability. New government proposals for excise tax increases focusing on cigarettes but also including machine made large cigars, pipe tobacco and chewable tobacco-derived nicotine products as well as the so far unregulated e-cigarettes. Altria has a long history of paying substantial dividends and increasing them at a high rate. Current yield is 3.70%, which is actually quite low compared the historical yield for the stock. However, high levels of debt and stagnant forecasted EPS growth creates concerns as to whether the impressive growth rate in dividends can be sustained. Stronger U.S. consumer Increases in employment gains result in higher consumer spending and a potential shift from discount to more premium products. Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Altria Inc.

The Fund @ Sprott Equity Research

Sell, Current: $52.50, Price Target: $44.64 March 11, 2015

Spyridoula Maria Karasavva BIBCandidate 2017 Global Financial Management and Systems Equity Analyst [email protected] http://fund.ssb.carleton.ca

Kyle Stolys BCom Candidate 2016 Finance Sector Manager [email protected]

Updated Investment Thesis

5-Year Performance

Source: Bloomberg

Decline in cigarette volume

The cigarette industry has been experiencing a long term 3-4% annual decline. Despite a rising market share in Marlboro, Altria’s cigarette shipment volume has been following industry’s lead and has been declining around 3% yoy.

Well-run low maintenance business with very skilled Management

Strengthening Taxes and Litigation pressure

Dividend yield

Altria’s CAPEX on average equals around 3-4% of the company’s Cash from Operations.

Altria also manages to operate efficiently using negative working capital while increases its

profitability.

New government proposals for excise tax increases focusing on cigarettes but also including machine made large cigars, pipe tobacco and chewable tobacco-derived nicotine

products as well as the so far unregulated e-cigarettes.

Altria has a long history of paying substantial dividends and increasing them at a high rate.

Current yield is 3.70%, which is actually quite low compared the historical yield for the

stock. However, high levels of debt and stagnant forecasted EPS growth creates concerns

as to whether the impressive growth rate in dividends can be sustained.

Stronger U.S. consumer

Increases in employment gains result in higher consumer spending and a potential shift

from discount to more premium products.

Page 1

The Fund @ Sprott | Equity Research

Page 2

Company Overview Altria Inc (MO) is a holding company which is currently the largest tobacco and

smokeless tobacco manufacturer in the United States. The company currently has 49.8%

of the US tobacco market through its subsidiary Philip Morris USA. Philip Morris USA

sells Marlboro, Virginia Slims, and discount brands such as Basic. Philip Morris

International (NYSE:PM) used to be also an Altria subsidiary until it was spun off in

2008. Apart from tobacco, other subsidiaries of the company include US Smokeless

Tobacco Co. (various smokeless tobacco products such as chewing tobacco), NuMark (e-

cigarettes), Michelle Wine Estates (Wine) and Philip Morris Capital Corporation

(Financial, primarily leasing). In addition, the company has a minority stake (27%) in

SABMiller Plc., a multinational brewing and beverage company based in UK with $91

billion in market cap. SABMiller was formed in 2002 when MO announced an agreement

with SAB to merge Miller Brewing Company into South African Breweries. MO received

430,000,000 shares or 36% of economic interest in SABMiller.

Industry Dynamics Declining Cigarette Sales Volume

USA faces significant governmental and private sector actions, including efforts aimed at

reducing the incidence of tobacco use and efforts seeking to hold PM USA responsible for

the adverse health effects associated with both smoking and exposure to environmental

tobacco smoke. These actions, combined with the diminishing social acceptance of

smoking, have resulted in a 3 to 4% average annual decrease in cigarette industry volume,

and we expect that these factors will continue to reduce cigarette consumption levels.

Consolidation and Restructuring

Tobacco companies have been able to overcome the industry decline and produce strong

cash flows by constantly consolidating operations and restructuring themselves to

eliminate unnecessary costs. As an industry who is limited to a small marketing and

promotion footprint by law, much of their business model tends to be cost driven. This

focus of restructuring operations and maximizing efficiencies has led to solid margins and

consistent cash flow.

Source: Bloomberg, Student Estimates Source: Bloomberg

20,000

21,000

22,000

23,000

24,000

25,000

26,000

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

Smokeable products Non Smokeable products Wine all other

Figure 1: Revenue Breakdown by Product Figure 2: Market Share Breakdown

Marlboro, 44%

Other Premium,

3%

Discount, 4%

Non-Altria, 50%

Growth/Regulation in E-cigarettes

E-cigs have exploded in growth in part due to minimal regulation as well as being an

affordable alternative to traditional tobacco products. While they are not a tobacco product

specifically, they are a nicotine delivery device and many of the major players in the

tobacco industry have taken investment in to the substitute product. Some estimations

believe that e-cigs could pass traditional cigarettes in usage by 2023. While this seems

certainly possible at the current pace, there is a great likelihood of future regulation that

could slow down e-cigarettes’ growth.

Ban on Menthols

When legislation passed in 2009 to eliminate flavored cigarettes from the US marketplace,

one flavor was permitted to stay, menthol. Menthol cigarettes are a more palatable

alternative to traditional cigarettes and have been gaining sizable market share during the

cigarette consumption decline of the last half century. As of 2014 menthol cigarettes

amounted for 28% to 30% of the US cigarette market share. The EU has already

committed to banning the sale of menthols but the FDA has delayed making a judgment

upon them. The concern many hold is that menthol cigarettes are what younger

generations get hooked on first due to their milder nature. A ban on menthols would be

extremely detrimental to tobacco sales if there was no alternative readily available for

adoption.

Taxes and Litigation

Federal, state and local excise taxes have increased substantially over the past decade, far

outpacing the rate of inflation. The President’s 2015 Budget proposes significant tax

increases for all tobacco products, including machine made large cigars, pipe tobacco and

chewable tobacco-derived nicotine products and the so far unregulated e-cigs. The

proposed budget would increase the FET by $0.94 per pack raising the total FET to $1.95

per pack. On a brighter side, as of October 2015 the fed government along with 22 states

adopted a weight-based tax methodology for smokeless tobacco. This will result in lower

excise tax expenses for Altria as the ad valorem method which was being used until now

resulted in more tax being paid on premium products than was paid on lower-priced

products of equal weight.

The Fund @ Sprott | Equity Research

Source: Bloomberg Industries U.S. E-Cigarette Model

Page 3

Figure 3: Projected Cigarette/E-Cigarette Growth

Growth & Risk Analysis Growth Outlook

Employment rates are continuing to increase. In 2015 we expect employment gains to

average 260,000 per month — about 3.1 million for the year. These gains will fuel

consumer and business confidence and lead to rising wages and consumer spending. Altria

could take advantage of the strengthening US economy by applying further cigarette pack

price increases. In addition, US adult consumers could shift towards more premium

brands. This would be very beneficial for Altria, as the company has very strong premium

brand portfolios in all of its segments. However, as the unemployment rate nears its full

employment level of around 5%, this consumer shift from discount to premium products

becomes less frequent and less substantial.

Major Risks

The biggest issue is the market decline of their most significant product line, cigarettes.

Furthermore, there is the concern that further government action, such as excise tax hikes

or more widespread and stringent smoking bans, could exacerbate the erosion of volume

of cigarettes sold by Altria. According to Bloomberg, the price elasticity of demand for

cigarettes appear to have risen from historical 0.4 to 0.7 in recent years, which means a

price hike due to taxes will have a more adverse impact.

Market dynamics could shift during 2015 upon completion of Reynolds American Inc.'s

acquisition of Lorillard Inc. In Fitch's estimation, Reynolds American's share of the U.S.

market will climb to one-third overall, from around 27% currently; gaining ground on

Altria that controls one-half of the marketplace. Imperial Tobacco's cigarette share will

jump to approximately 10% (from 3% presently) with acquired value brands Salem,

Winston, Maverick, and Kool.

Litigation is another area of concern, as the company has a disclosure note in its financial

statements that refers to contingent liabilities which may arise as a result of adverse results

on lawsuits against Altria. Other risk factors include rise in tobacco leaf prices,

competitive pressures and shifting consumer preferences .

The Fund @ Sprott | Equity Research

Source: Gallup Source: Gallup

Page 4

Figure 4: Consumer Spending by Annual

Household Income, Dec 2013 to Dec 2014

Figure 5: Self-Reported US Daily Consumer

Spending

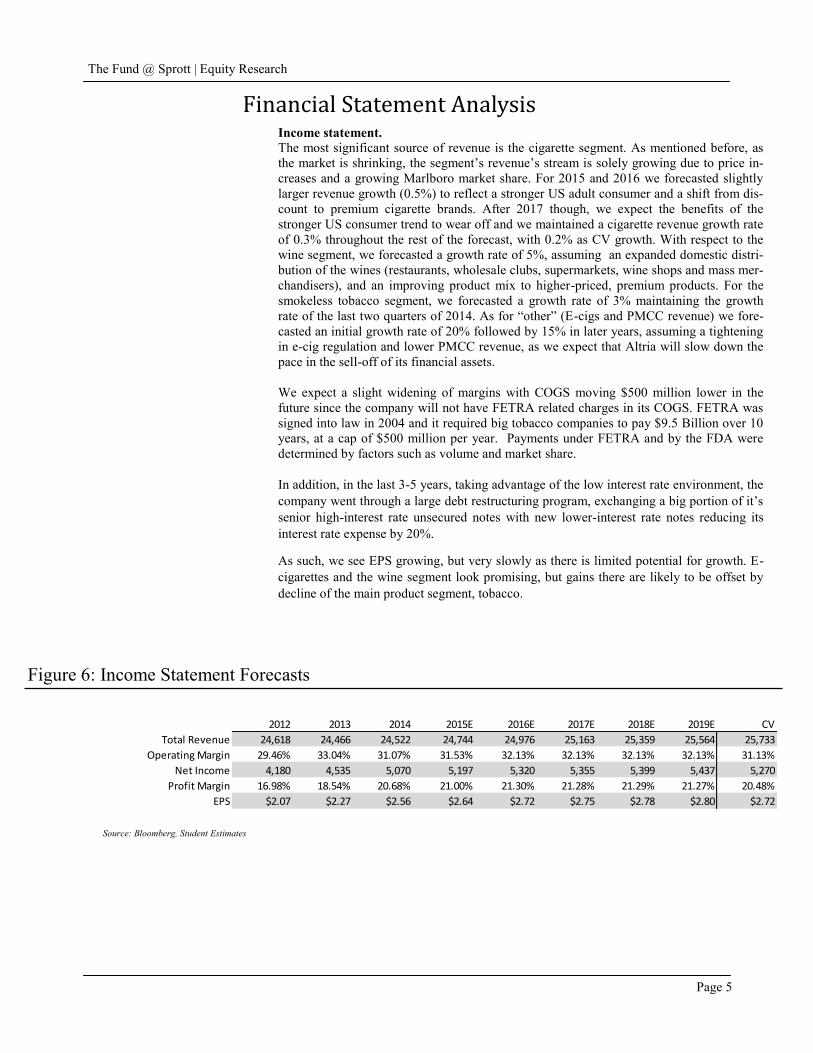

Income statement.

The most significant source of revenue is the cigarette segment. As mentioned before, as

the market is shrinking, the segment’s revenue’s stream is solely growing due to price in-

creases and a growing Marlboro market share. For 2015 and 2016 we forecasted slightly

larger revenue growth (0.5%) to reflect a stronger US adult consumer and a shift from dis-

count to premium cigarette brands. After 2017 though, we expect the benefits of the

stronger US consumer trend to wear off and we maintained a cigarette revenue growth rate

of 0.3% throughout the rest of the forecast, with 0.2% as CV growth. With respect to the

wine segment, we forecasted a growth rate of 5%, assuming an expanded domestic distri-

bution of the wines (restaurants, wholesale clubs, supermarkets, wine shops and mass mer-

chandisers), and an improving product mix to higher-priced, premium products. For the

smokeless tobacco segment, we forecasted a growth rate of 3% maintaining the growth

rate of the last two quarters of 2014. As for “other” (E-cigs and PMCC revenue) we fore-

casted an initial growth rate of 20% followed by 15% in later years, assuming a tightening

in e-cig regulation and lower PMCC revenue, as we expect that Altria will slow down the

pace in the sell-off of its financial assets.

We expect a slight widening of margins with COGS moving $500 million lower in the

future since the company will not have FETRA related charges in its COGS. FETRA was

signed into law in 2004 and it required big tobacco companies to pay $9.5 Billion over 10

years, at a cap of $500 million per year. Payments under FETRA and by the FDA were

determined by factors such as volume and market share.

In addition, in the last 3-5 years, taking advantage of the low interest rate environment, the

company went through a large debt restructuring program, exchanging a big portion of it’s

senior high-interest rate unsecured notes with new lower-interest rate notes reducing its

interest rate expense by 20%.

As such, we see EPS growing, but very slowly as there is limited potential for growth. E-

cigarettes and the wine segment look promising, but gains there are likely to be offset by

decline of the main product segment, tobacco.

Financial Statement Analysis

Source: Bloomberg, Student Estimates

The Fund @ Sprott | Equity Research

Page 5

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Total Revenue 24,618 24,466 24,522 24,744 24,976 25,163 25,359 25,564 25,733

Operating Margin 29.46% 33.04% 31.07% 31.53% 32.13% 32.13% 32.13% 32.13% 31.13%

Net Income 4,180 4,535 5,070 5,197 5,320 5,355 5,399 5,437 5,270

Profit Margin 16.98% 18.54% 20.68% 21.00% 21.30% 21.28% 21.29% 21.27% 20.48%

EPS $2.07 $2.27 $2.56 $2.64 $2.72 $2.75 $2.78 $2.80 $2.72

Figure 6: Income Statement Forecasts

Source: Bloomberg, Student Estimates

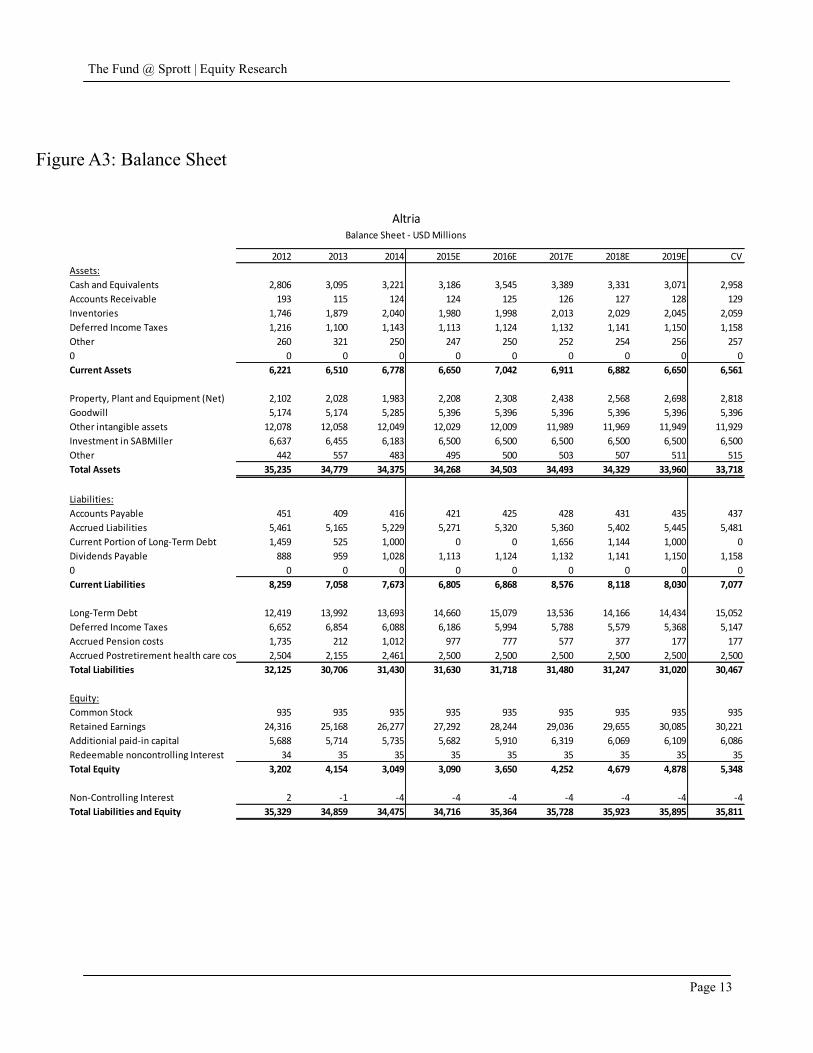

Balance Sheet

Altria has an average five-year debt ratio of 0.90 and a BBB+ Credit Rating. As men-

tioned previously in the Income Statement section, the company has made serious efforts

in exchanging its high interest rate senior unsecured notes with newer low interest rate

notes. As a result, we assume that Altria’s future debt ratio will remain the same into the

future as they continue to optimize operations and maximize shareholder value. With re-

spect to the interest coverage ratio, it has been increasing by 24% on average for the last 3

years, reflecting Altria’s lower interest expenses due to the debt restructuring. We assume

the interest coverage ratio to remain stable in future years.

The company has been operating and increasing EPS while having negative working capi-

tal for the last 2 years. It covers its working capital needs mainly through its cash from

operations and/or short term borrowings under its commercial paper program.

With respect to Current Assets, we expect them to amount for a larger percent of the com-

pany’s revenues in the future, mainly driven by higher cash balances.

Source: Bloomberg, Student Estimates Source: Bloomberg, Student Estimates

The Fund @ Sprott | Equity Research

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Current Assets 6,221 6,510 6,778 7,162 7,907 7,954 7,904 7,436 8,436

Current Liabilities 8,259 7,058 7,673 6,805 6,868 8,576 8,118 8,030 7,077

Pension Liabilities 6,652 6,854 6,088 6,186 5,994 5,788 5,579 5,368 5,147

Long-Term Debt 12,419 13,992 13,693 14,660 15,079 13,536 14,166 14,434 15,052

Total Equity 3,202 4,154 3,049 3,129 3,596 3,960 3,968 3,549 4,921

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

CV

Current Ratio Quick Ratio Cash Ratio

82%

83%

84%

85%

86%

87%

88%

89%

90%

91%

92%

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

CV

Debt Ratio (%)

Figure 7: Balance Sheet Forecasts

Figure 8: Current Ratio, Quick Ratio, Cash Ratio Figure 9: Debt Ratio

Page 6

Cash Flow Statement.

In our cash flow forecast we assumed depreciation to increase by 6.5% in 2015 due to the

new USSTC manufacturing facility. For the rest of our forecast we assumed a 5% annual

decline in depreciation as the company uses a straight line depreciation method and is in

decline. However, depreciation is not very relevant to our forecast as Altria is not capital

intensive.

CAPEX on average equals 3-4% of Altria’s Cash from Operations. For 2015 we forecast-

ed a $60 million increase in CAPEX due to USSTC’s new manufacturing facility. For the

rest of the forecast, after examining Altria’s CAPEX for each business segment, we as-

sumed that CAPEX will average at $130 mill. Specifically, CAPEX related to the smokea-

bles segment will remain flat, while CAPEX related to the wine and e-cigarette segments

will grow. With respect to the non-smokeables segment we expect CAPEX to decrease in

the future, upon the completion of USSTC’s 2015 large investment in a non-smokeables’

manufacturing facility.

In April 2014, Nu Mark acquired the e-vapor business of Green Smoke, Inc. and its affili-

ates (“Green Smoke”) for a total purchase price of up to approximately $130 million. The

acquisition enhances Nu Mark’s competitive position by adding e-vapor experience,

broadening product offerings and strengthening supply chain capabilities. We do not fore-

cast any further acquisitions in the future.

In 2015 Altria will conclude its current $1 billion share buyback program. For the follow-

ing years we forecasted additional share buybacks as we assume that the company will use

its lower COGS to further reward its shareholders. In order to forecast issuance of new

debt, we used a 4 year average of Altria’s Total Debt/EBIT ratio. We assumed the total

debt to EBIT ratio to remain at 1.88 and forecasted new debt additions as a result. Divi-

dends paid is expected to grow steadily, albeit at a lower rate and we believe that the com-

pany in long term will maintain a 80% OCFS Payout Ratio - as forecasted.

The Fund @ Sprott | Equity Research

Source: Bloomberg, Student Estimates

Page 7

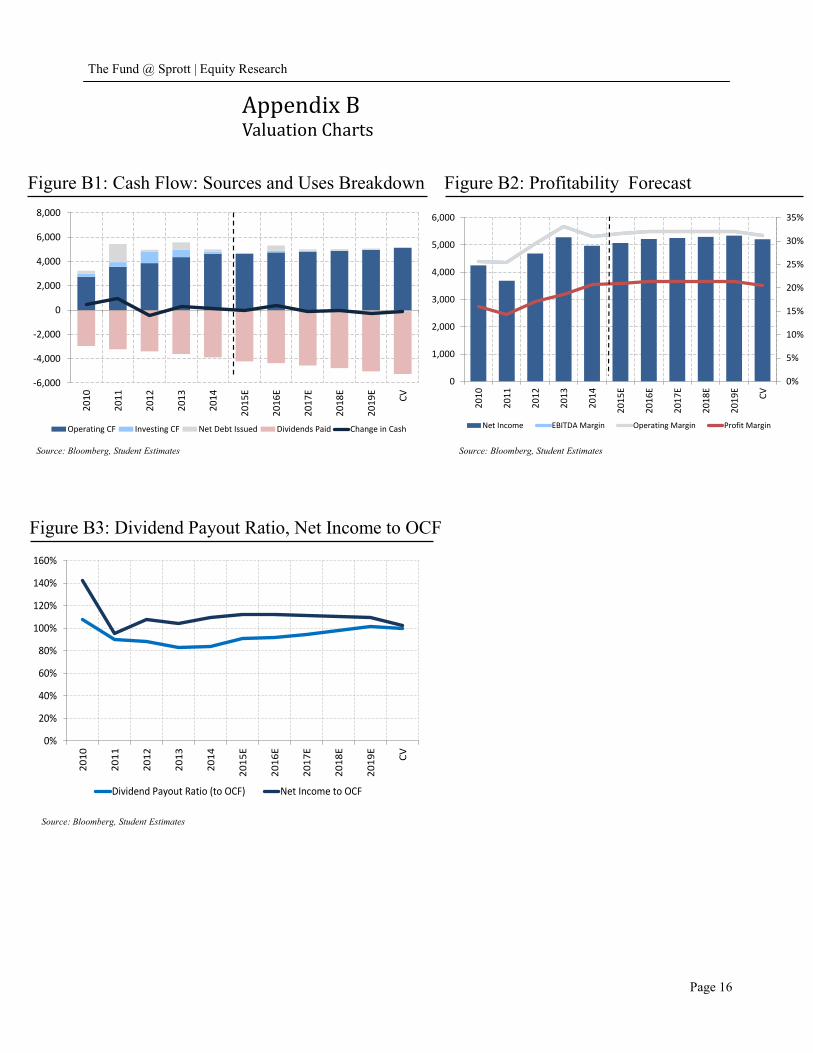

Cash Flow: Sources and Uses Breakdown

Source: Bloomberg, Student Estimates

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Cash from Operations 3,865 4,355 4,643 5,133 5,229 5,258 5,280 5,307 5,449

Cash from Investing 920 602 177 75 150 70 20 (30) (120)

Cash from Financing (5,209) (4,668) (4,694) (4,731) (4,667) (5,307) (5,376) (5,774) (4,352)

Net Change in Cash (424) 289 126 477 712 20 (77) (497) 977

Ending Cash Balance 2,806 3,095 3,221 3,698 4,410 4,431 4,354 3,857 4,834

Figure 10: Cash Flow Statement Forecast

The Fund @ Sprott | Equity Research

Page 8

Valuation Altria has approximately 27% of the economic and voting interest of SABMiller plc

(“SABMiller”), which Altria accounts for under the equity method of accounting as

Altria's stake in SABMiller is less than 50%, and the company does not exercise control

over SABMiller. Altria is not allowed to fully consolidate SABMiller onto its balance

sheet, or to mark the stake up to its current value and can only record the book value of its

SABMiller holding on its balance sheet. Altria’s holding in SABMiller is currently

booked at $6.2 billion on the balance sheet. However, the current market value of the

holding is $25B. Altria has held SAB Miller stock for over a decade and would owe

massive capital gains taxes if sold today. Management has said they do not plan on selling

the stock for this reason and will continue to collect dividends from SAB Miller over the

long term.

In order to capture this value we have done two valuations, a DDM since many investors

are attracted to the high yield Altria offers as well as a modified DCF model. We have

altered our DCF to include the dividends Altria receives from their SAB Miller

investment. We have done this since these dividends are a recurring income for the

company and we do not expect Altria to sell the holding. Dividends have grown at a rate

of 8.5% over the last 5 years and we do not believe a material decrease in this growth rate

will occur. We forecast 7% growth in dividend income over the next 5 years.

2 stage DCF Model Assumptions recap: When discounting the company’s cash flows we used Bloomberg’s WACC of 7.1% to be more conservative as our self-calculated WACC of 6.06% was significantly lower. For a terminal growth rate we used 1%. With respect to debt issuances, we expect Altria to issue further debt in the future so as to cover its needs in cash. In addition, we expect Management to use its future COGS savings to continue rewarding shareholders through share-buybacks. As for CAPEX, we forecasted higher CAPEX for 2015 due to the manufacturing of the new USSTC facility. For the rest of the forecasted period we assumed lower CAPEX related to the smokeables and the non-smokeables segments and higher CAPEX related to the wine and the e-cigarettes segments. According to our 2-stage DCF Model Altria is 26.1% overvalued.

Figure 11: DCF Valuation

Source: Bloomberg, Student Estimates

2015E 2016E 2017E 2018E 2019E CV

EBIT (1 - Tax Rate) 5,071 5,216 5,255 5,296 5,339 5,207

Add: Depreciation Expense 200 220 209 199 189 179

Add: Div's from SAB Miller 488 522 559 598 640 684

Less: Capital Expenditures -225 -100 -130 -130 -130 -120

Less: Change in Non-Cash WC -139 -21 -17 -18 -18 0

FCFF per Year 5,395 5,837 5,876 5,945 6,018 5,950

FCFF Discounted 4,496 5,450 5,123 4,839 4,574 74,139

PV - Future Cash Flows 98,620 Assumptions: WACC 7.10%

Excess Cash 3,186 Ke 7.90%

MV of Debt 13,950 Kd 1.80%

Shares Outstanding 1,968 CV Growth Rate 1.00%

DCF Value Per Share $44.64

Figure 12: DDM Valuation

2015E 2016E 2017E 2018E 2019E CV

Ops Cash Flow per Share $2.35 $2.43 $2.47 $2.51 $2.55 $2.72

YoY Growth 0.02% 3.38% 1.88% 1.51% 1.65% 6.53%

Dividends per Share $2.13 $2.30 $2.48 $2.68 $2.89 $2.12

YoY Growth 8.00% 8.00% 8.00% 8.00% 8.00% -26.73%

PV of Cash Flow $2.13 $2.13 $2.13 $2.13 $2.13 $31.89

Total PV per Share $42.54 Assumptions: Ke 7.90%

CV Dividend Growth 3.00%

DDM Model

Assumptions Recap: We used Bloomberg’s cost of equity of 7.9% instead of our self-calculated

cost of equity of 6.72% for the same reasons as in the DCF Model. We assumed terminal dividend

growth to be 3%. In addition, we assume that the company will grow at a rate of 1% and that

through share buybacks it will manage to grow its dividends by 3%.

Our DDM Model found Altria 12.7% overvalued.

Source: Bloomberg, Student Estimates

The Fund @ Sprott | Equity Research

Page 9

Investment Positives

Altria has a leading market share in an industry with inelastic product demand.

Strong growth in the e-cigarette and wine segments.

The company has a long history of paying large dividends and increasing them at a

high rate. Current dividend yield is 3.70%

A strengthening US economy and a decreasing unemployment rate could have a

positive impact on Altria as they could lead consumers to shift from discount to

premium products while also creating price increase opportunities for the company.

Due to its experienced management, Altria manages to operate efficiently and

increase its EPS even while having negative working capital.

As a mature business with a leading market share in two out of the four segments it

operates in, Altria has no need for high levels of CAPEX.

As a result of substantial debt restructurings the company’s interest rate has lowered

dramatically but is still high at a weighted average of 5.43%.

Investment Negatives

Minimal yoy growth in Altria’s key segment, cigarettes.

New pressures from the US government for FET tax increases related to all tobacco

products, even e-cigarettes.

Altria is overleveraged compared to its peers which could lead to future problems.

Dividend yield has been declining since 2003 reflecting the company’s high levels

of debt and poor growth prospects.

Upon completion of Lorillard's acquisition, Reynolds is expected to gain around 5%

market share on Altria.

Conclusion

Investment Recommendation

Sell, Target Price $44.64

In conclusion, Altria’s growth prospects are grim as the cigarette industry is declining,

the regulatory environment is tightening and competition is strengthening. We are confi-

dent in the future operations of Altria but at today’s current stock price ($52.50) Altria

is significantly overvalued using multiple valuation methods. Therefore we recommend

selling our position in Altria.

The Fund @ Sprott | Equity Research

Disclaimer This report was written by a student currently enrolled in a program at the Sprott School of Business. The purpose of this report is to demonstrate the investment analysis

skills of Sprott students. The analyst is not a registered investment advisor, broker or an officially licensed financial professional. The investment opinion contained in

this report does not represent an offer or solicitation to buy or sell any securities. This report is written solely for the consideration of this student managed investment

fund and should not be used by individuals to make personal investment decisions. Unless otherwise noted, facts and figures included in this report are from publicly

available sources. We cannot guarantee that the information in this report is 100 percent accurate, although we believe it to be from reliable sources. Information

contained in this report is only believed to be accurate as of the day it was published, and it is subject to change without notice. It cannot be guaranteed that the faculty or

students do not have an investment position in the securities mentioned in this report.

Page 10

The Fund @ Sprott | Equity Research

Page 11

Appendix A Pro-forma Financial Statements

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Revenues 24,618 24,466 24,522 24,744 24,976 25,163 25,359 25,564 25,733

Expenses:

Cost of Goods Sold/Production 7,937 7,206 7,785 7,441 7,510 7,567 7,626 7,687 7,738

Excise Taxes 7,118 6,803 6,577 6,928 6,993 7,046 7,101 7,158 7,463

Marketing, administration and research costs 2,301 2,340 2,539 2,573 2,448 2,466 2,485 2,505 2,522

Other operating expense -52 22 2 0 0 0 0 0 0

other 0 0 0 0 0 0 0 0 0

EBITDA 7,253 8,084 7,620 7,802 8,024 8,085 8,148 8,213 8,010

Depreciation Expense 0 0 0 0 0 0 0 0 0

EBIT 7,253 8,084 7,620 7,802 8,024 8,085 8,148 8,213 8,010

Interest Expense (Income) 1,126 1,049 808 796 829 836 842 849 903

EBT (Before Other Items) 6,127 7,035 6,812 7,006 7,195 7,249 7,306 7,364 7,107

Non-Operating Items

0 0 0 0 0 0 0 0 0 0

loss on early extinguishment of debt -874 -1,084 -44 -10 -10 -10 0 0 0

Equity In Earnings of Affiliate/Joint Ventures (SABMiller)1,224 991 1,006 1,000 1,000 1,000 1,000 1,000 1,000

EBT (After Other Items) 6,477 6,942 7,774 7,996 8,185 8,239 8,306 8,364 8,107

Income Tax Expense 2,294 2,407 2,704 2,798 2,865 2,884 2,907 2,928 2,838

Non-Controlling Interest 2 3 3 0 0 0 0 0 0

Net Income 4,180 4,535 5,070 5,197 5,320 5,355 5,399 5,437 5,270

Common Shares Outstanding 2,024 1,999 1,978 1,968 1,958 1,948 1,943 1,939 1,939

Exercisable/Convertible Shares 0 0 0 0 0 0 0 0 0

Basic Earnings Per Share $2.07 $2.27 $2.56 $2.64 $2.72 $2.75 $2.78 $2.80 $2.72

Diluted Earnings Per Share $2.07 $2.27 $2.56 $2.64 $2.72 $2.75 $2.78 $2.80 $2.72

AltriaIncome Statement - USD Millions

Figure A1: Income Statement

The Fund @ Sprott | Equity Research

Page 12

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Revenues 100% 100% 100% 100% 100% 100% 100% 100% 100%

Expenses:

Cost of Goods Sold/Production 32% 29% 32% 30% 30% 30% 30% 30% 30%

Excise Taxes 29% 28% 27% 28% 28% 28% 28% 28% 29%

Marketing, administration and research costs 9% 10% 10% 10% 10% 10% 10% 10% 10%

Other operating expense 0% 0% 0% 0% 0% 0% 0% 0% 0%

other 0% 0% 0% 0% 0% 0% 0% 0% 0%

EBITDA 29% 33% 31% 32% 32% 32% 32% 32% 31%

Depreciation Expense 0% 0% 0% 0% 0% 0% 0% 0% 0%

EBIT 29% 33% 31% 32% 32% 32% 32% 32% 31%

Interest Expense (Income) 5% 4% 3% 3% 3% 3% 3% 3% 4%

EBT (Before Other Items) 25% 29% 28% 28% 29% 29% 29% 29% 28%

Non-Operating Items

0 0% 0% 0% 0% 0% 0% 0% 0% 0%

loss on early extinguishment of debt -4% -4% 0% 0% 0% 0% 0% 0% 0%

Equity In Earnings of Affiliate/Joint Ventures (SABMiller)5% 4% 4% 4% 4% 4% 4% 4% 4%

EBT (After Other Items) 26% 28% 32% 32% 33% 33% 33% 33% 32%

Income Tax Expense 9% 10% 11% 11% 11% 11% 11% 11% 11%

Non-Controlling Interest 0% 0% 0% 0% 0% 0% 0% 0% 0%

Net Income 17% 19% 21% 21% 21% 21% 21% 21% 20%

AltriaCommon Size Income Statement

Figure A2: Common Size Income Statement

The Fund @ Sprott | Equity Research

Page 13

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Assets:

Cash and Equivalents 2,806 3,095 3,221 3,186 3,545 3,389 3,331 3,071 2,958

Accounts Receivable 193 115 124 124 125 126 127 128 129

Inventories 1,746 1,879 2,040 1,980 1,998 2,013 2,029 2,045 2,059

Deferred Income Taxes 1,216 1,100 1,143 1,113 1,124 1,132 1,141 1,150 1,158

Other 260 321 250 247 250 252 254 256 257

0 0 0 0 0 0 0 0 0 0

Current Assets 6,221 6,510 6,778 6,650 7,042 6,911 6,882 6,650 6,561

Property, Plant and Equipment (Net) 2,102 2,028 1,983 2,208 2,308 2,438 2,568 2,698 2,818

Goodwill 5,174 5,174 5,285 5,396 5,396 5,396 5,396 5,396 5,396

Other intangible assets 12,078 12,058 12,049 12,029 12,009 11,989 11,969 11,949 11,929

Investment in SABMiller 6,637 6,455 6,183 6,500 6,500 6,500 6,500 6,500 6,500

Other 442 557 483 495 500 503 507 511 515

Total Assets 35,235 34,779 34,375 34,268 34,503 34,493 34,329 33,960 33,718

Liabilities:

Accounts Payable 451 409 416 421 425 428 431 435 437

Accrued Liabilities 5,461 5,165 5,229 5,271 5,320 5,360 5,402 5,445 5,481

Current Portion of Long-Term Debt 1,459 525 1,000 0 0 1,656 1,144 1,000 0

Dividends Payable 888 959 1,028 1,113 1,124 1,132 1,141 1,150 1,158

0 0 0 0 0 0 0 0 0 0

Current Liabilities 8,259 7,058 7,673 6,805 6,868 8,576 8,118 8,030 7,077

Long-Term Debt 12,419 13,992 13,693 14,660 15,079 13,536 14,166 14,434 15,052

Deferred Income Taxes 6,652 6,854 6,088 6,186 5,994 5,788 5,579 5,368 5,147

Accrued Pension costs 1,735 212 1,012 977 777 577 377 177 177

Accrued Postretirement health care costs 2,504 2,155 2,461 2,500 2,500 2,500 2,500 2,500 2,500

Total Liabilities 32,125 30,706 31,430 31,630 31,718 31,480 31,247 31,020 30,467

Equity:

Common Stock 935 935 935 935 935 935 935 935 935

Retained Earnings 24,316 25,168 26,277 27,292 28,244 29,036 29,655 30,085 30,221

Additionial paid-in capital 5,688 5,714 5,735 5,682 5,910 6,319 6,069 6,109 6,086

Redeemable noncontrolling Interest 34 35 35 35 35 35 35 35 35

Total Equity 3,202 4,154 3,049 3,090 3,650 4,252 4,679 4,878 5,348

Non-Controlling Interest 2 -1 -4 -4 -4 -4 -4 -4 -4

Total Liabilities and Equity 35,329 34,859 34,475 34,716 35,364 35,728 35,923 35,895 35,811

Balance Sheet - USD Millions

Altria

Figure A3: Balance Sheet

The Fund @ Sprott | Equity Research

Page 14

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Assets:

Cash and Equivalents 8% 9% 9% 9% 10% 10% 10% 9% 9%

Accounts Receivable 1% 0% 0% 0% 0% 0% 0% 0% 0%

Inventories 5% 5% 6% 6% 6% 6% 6% 6% 6%

Deferred Income Taxes 3% 3% 3% 3% 3% 3% 3% 3% 3%

Other 1% 1% 1% 1% 1% 1% 1% 1% 1%

0 0% 0% 0% 0% 0% 0% 0% 0% 0%

Current Assets 18% 19% 20% 19% 20% 20% 20% 20% 19%

Property, Plant and Equipment (Net) 6% 6% 6% 6% 7% 7% 7% 8% 8%

Goodwill 15% 15% 15% 16% 16% 16% 16% 16% 16%

Other intangible assets 34% 35% 35% 35% 35% 35% 35% 35% 35%

Investment in SABMiller 19% 19% 18% 19% 19% 19% 19% 19% 19%

Other 1% 2% 1% 1% 1% 1% 1% 2% 2%

Total Assets 100% 100% 100% 100% 100% 100% 100% 100% 100%

Liabilities:

Accounts Payable 1% 1% 1% 1% 1% 1% 1% 1% 1%

Accrued Liabilities 15% 15% 15% 15% 15% 16% 16% 16% 16%

Current Portion of Long-Term Debt 4% 2% 3% 0% 0% 5% 3% 3% 0%

Dividends Payable 3% 3% 3% 3% 3% 3% 3% 3% 3%

0 0% 0% 0% 0% 0% 0% 0% 0% 0%

Current Liabilities 23% 20% 22% 20% 20% 25% 24% 24% 21%

Long-Term Debt 35% 40% 40% 43% 44% 39% 41% 43% 45%

Deferred Income Taxes 19% 20% 18% 18% 17% 17% 16% 16% 15%

Accrued Pension costs 5% 1% 3% 3% 2% 2% 1% 1% 1%

Accrued Postretirement health care costs 7% 6% 7% 7% 7% 7% 7% 7% 7%

Total Liabilities 91% 88% 91% 92% 92% 91% 91% 91% 90%

Equity:

Common Stock 3% 3% 3% 3% 3% 3% 3% 3% 3%

Retained Earnings 69% 72% 76% 80% 82% 84% 86% 89% 90%

Additionial paid-in capital 16% 16% 17% 17% 17% 18% 18% 18% 18%

Redeemable noncontrolling Interest 0% 0% 0% 0% 0% 0% 0% 0% 0%

Total Equity 9% 12% 9% 9% 11% 12% 14% 14% 16%

Non-Controlling Interest 0% 0% 0% 0% 0% 0% 0% 0% 0%

Total Liabilities and Equity 100% 100% 100% 101% 102% 104% 105% 106% 106%

Common Size Balance Sheet

Altria

Figure A4: Common Size Balance Sheet

2012 2013 2014 2015E 2016E 2017E 2018E 2019E CV

Cash From Operating ActivitiesNet Income 4,183 4,535 5,070 5,197 5,320 5,355 5,399 5,437 5,270

Add (Deduct) Non-Cash Items:

Add: Depreciation Expense 205 192 188 200 220 209 199 189 179

Change in Non Cash Working Capital 1,194 -558 -194 -139 -21 -17 -18 -18 0

Deferred income tax benefit -929 -86 -129 -100 -100 -100 -100 -100 0

earnings from equity investment in venture joints (SABMiller)-1,224 -991 -1,006 -1,000 -1,000 -1,000 -1,000 -1,000 -1,000

dividends from SABMiller 402 439 456 488 522 559 598 640 684

Loss on early extinguishment of debt 874 1,084 44 10 10 10 0 0 0

Cash From Operations 3,865 4,355 4,643 4,621 4,752 4,816 4,877 4,947 5,133

Cash From Investing ActivitiesCapital Expenditures / Acquisitions -124 -131 -163 -225 -100 -130 -130 -130 -120

Asset Sales 0 0 0 0 0 0 0 0 00 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

Investments in finance assets 0 0 0 0 0 0 0 0 0

Proceeds from finance assets 1,049 716 369 300 250 200 150 100 0

other -5 17 73 0 0 0 0 0 0

Cash From Investing 920 602 177 75 150 70 20 -30 -120

Cash From Financing ActivitiesAdditions of Long-Term Debt 2,787 4,179 999 967 419 113 1,774 1,267 0

Reductions of Long-Term Debt -2,600 -3,559 -825 -1,000 0 0 -1,656 -1,144 0

Additions of Short-Term Debt 0 0 0 0 0 0 0 0 0

Reductions of Short-Term Debt 0 0 0 0 0 0 0 0 0

Net Debt Additions (Reductions) 187 620 174 -33 419 113 118 123 0

Issuance of Common Shares 0 0 0 0 0 0 0 0 0

Redemption of Common Shares -1,116 -600 -939 -518 -600 -600 -300 -300 0

Cash Dividends Paid -3,400 -3,612 -3,892 -4,182 -4,368 -4,563 -4,780 -5,007 -5,133

other 6 17 14 14 14 14 14 14 14

finance fees and debt issuance costs -22 -39 -7 -7 -7 -7 -7 -7 -7

Cash From Financing -5,209 -4,668 -4,694 -4,731 -4,542 -5,043 -4,955 -5,177 -5,126

Foreign Exchange Rate Gain (Loss) 0 0 0 0 0 0 0 0 0

Net Change in Cash -424 289 126 -35 359 -156 -57 -260 -113

Cash Balance, Beginning 3,230 2,806 3,095 3,221 3,186 3,545 3,389 3,331 3,071

Cash Balance, Ending 2,806 3,095 3,221 3,186 3,545 3,389 3,331 3,071 2,958

AltriaCash Flow Statement - USD Millions

The Fund @ Sprott | Equity Research

Page 15

Figure A5: Cash Flow Statement

The Fund @ Sprott | Equity Research

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

CV

Operating CF Investing CF Net Debt Issued Dividends Paid Change in Cash

0%

5%

10%

15%

20%

25%

30%

35%

0

1,000

2,000

3,000

4,000

5,000

6,000

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

CV

Net Income EBITDA Margin Operating Margin Profit Margin

0%

20%

40%

60%

80%

100%

120%

140%

160%

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

CV

Dividend Payout Ratio (to OCF) Net Income to OCF

Page 16

Appendix B Valuation Charts

Figure B1: Cash Flow: Sources and Uses Breakdown Figure B2: Profitability Forecast

Figure B3: Dividend Payout Ratio, Net Income to OCF

Source: Bloomberg, Student Estimates

Source: Bloomberg, Student Estimates Source: Bloomberg, Student Estimates

Related Documents