16 December 2014 Credit Research Credit Flash – Euro High Yield UniCredit Research page 1 See last pages for disclaimer. Altice - initiation of coverage with buy ■ Altice is currently undergoing a period of rapid growth, which is largely driven by the company’s M&A-based expansion model. Altice’s business strategy is to acquire underperforming cable/telecom assets and then to raise their margins by generating synergies. Altice’s operating units tend to show much higher rates of EBITDA growth than revenue growth. This business model is similar to that of Liberty Global’s (LGI) levered equity growth model. However, LGI is at a different stage of its corporate development, with USD 18mn (EUR 14bn) in sales LTM 9M14 compared to Altice’s EUR 2.6bn. However, this is set to change with Numericable’s consolidation of SFR and the acquisition of Portugal Telecom, which should bring Altice’s fully consolidated revenues closer to EUR 13bn as of 2015 and EUR 16bn with Portugal Telecom. ■ Altice is expected to acquire Portugal Telecom in 2015. Its EUR 7.4bn offer has been accepted by Oi and now only requires approval from regulators and Portugal Telecom shareholders. Altice has also expressed interest in Bouygues Telecom, which we estimate could cost around EUR 7.0bn. These aggressive M&A targets for 2015-16, which were being contemplated even before the SFR deal was completed, reveal the difference between Altice and LGI: Altice’s acquisitions have been transformational, while LGI’s are incremental. The execution risks and rising leverage ratios inherent in these transactions are a major reason behind the difference in Altice’s current ratings ((P)B1 CWN/B+n) and LGI’s (Ba3s/BB-s). Furthermore, we see a high likelihood of a one- notch rating downgrade from S&P and Moody’s as a result of the additional leverage from the Portugal Telecom acquisition. ■ Altice’s main areas of activity are characterized by solid market shares with improving operating margins. Altice tends to position itself as the No. 2 cable/telecom provider in its main markets. Over the long term, this should result in strong free cash flow generation and contribute to deleveraging. However, over the medium term, we expect the company’s credit profile to become more highly leveraged, although within the limits of its covenants (RCF maintenance covenant: 4.5x). ■ ALTICE and ATCNA bonds trade at spreads closer to CEE peers (CBLCSY and ADRBID) than to Western European cable names. This is due to a one-to-two notch rating differential between Altice and its peers as well as to Altice’s much more aggressive M&A strategy, which entails greater uncertainty and execution risk. However, since the financing details of the Portugal Telecom acquisition have now been basically clarified and since Moody’s and S&P have already put the company on watch for a downgrade, we believe that most of the negative event risk has already been priced in. This can be seen in the sudden rise in ALTICE and ATCNA bonds spreads in recent months. In addition, current CDS curves reveal a high degree of skepticism toward Altice that we think is excessive considering current leverage and rating levels relative to peers, such as LGI. We currently see the main event risk for the company as a potential Bouygues transaction. However, we also believe that this transaction has potential for meaningful synergies and is likely to be financed with a significant equity component, which should provide some downside protection to bond prices at current levels. Recommendation Initiation with buy Major bond issues Mat Cpn Z-spread ALTICE 12/15/2019 8 580/523 ALTICE 1/15/2022 6.5 605/600 ALTICE 5/15/2022 7.25 693/676 ALTICE 6/15/2023 9 704/698 CDS-Spreads CDS CDS 1Y 133 CDS 3Y 346 CDS 5Y 479 CDS 7Y 558 CDS 10Y 580 Ratings L-T S-T Outlook Moody's (P)B1 Watch Neg. S&P B+ Negative Company web site http://www.altice.net Financial Calendar 2015 4Q14 results around 18 March ALTICE VS. CABLE PEERS Source: Bloomberg, UniCredit Research Author Jonathan Schroer, CFA (UniCredit Bank) +49 89 378-13212 [email protected] Bloomberg UCGR Internet www.research.unicredit.eu UPCB 7.625% 1/20 UPCB 6.375% 7/20 UPCB 8.375% 8/20 UPCB 6.75% 3/23 UPCB 6.375% 9/22 (SUB) UNITY 9.5% 3/21 UNITY 5.5% 9/22 UNITY 5.125% 1/23 UNITY 5.625% 4/23 UNITY 5.75% 1/23 UNITY 6.25% 1/29 TNETBB 6.375% 11/20 TNETBB 6.625% 2/21 TNETBB 6.25% 8/22 TNETBB 6.75% 8/24 NUMFP 5.375% 5/22 NUMFP 5.625% 5/24 ALTICE 7.25% 5/22 ALTICE 6.5% 1/22 ALTICE 9% 6/23 ALTICE 8% 12/19 (SUB) CBLCSY 7.5% 11/20 ADRBID 7.875% 11/20 0 100 200 300 400 500 600 700 800 0 1 2 3 4 5 6 7 bp mDur

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

16 December 2014 Credit Research

Credit Flash – Euro High Yield

UniCredit Research page 1 See last pages for disclaimer.

Altice - initiation of coverage with buy ■ Altice is currently undergoing a period of rapid growth, which is largely

driven by the company’s M&A-based expansion model. Altice’s business strategy is to acquire underperforming cable/telecom assets and then to raise their margins by generating synergies. Altice’s operating units tend to show much higher rates of EBITDA growth than revenue growth. This business model is similar to that of Liberty Global’s (LGI) levered equity growth model. However, LGI is at a different stage of its corporate development, with USD 18mn (EUR 14bn) in sales LTM 9M14 compared to Altice’s EUR 2.6bn. However, this is set to change with Numericable’s consolidation of SFR and the acquisition of Portugal Telecom, which should bring Altice’s fully consolidated revenues closer to EUR 13bn as of 2015 and EUR 16bn with Portugal Telecom.

■ Altice is expected to acquire Portugal Telecom in 2015. Its EUR 7.4bn offer has been accepted by Oi and now only requires approval from regulators and Portugal Telecom shareholders. Altice has also expressed interest in Bouygues Telecom, which we estimate could cost around EUR 7.0bn. These aggressive M&A targets for 2015-16, which were being contemplated even before the SFR deal was completed, reveal the difference between Altice and LGI: Altice’s acquisitions have been transformational, while LGI’s are incremental. The execution risks and rising leverage ratios inherent in these transactions are a major reason behind the difference in Altice’s current ratings ((P)B1 CWN/B+n) and LGI’s (Ba3s/BB-s). Furthermore, we see a high likelihood of a one-notch rating downgrade from S&P and Moody’s as a result of the additional leverage from the Portugal Telecom acquisition.

■ Altice’s main areas of activity are characterized by solid market shares with improving operating margins. Altice tends to position itself as the No. 2 cable/telecom provider in its main markets. Over the long term, this should result in strong free cash flow generation and contribute to deleveraging. However, over the medium term, we expect the company’s credit profile to become more highly leveraged, although within the limits of its covenants (RCF maintenance covenant: 4.5x).

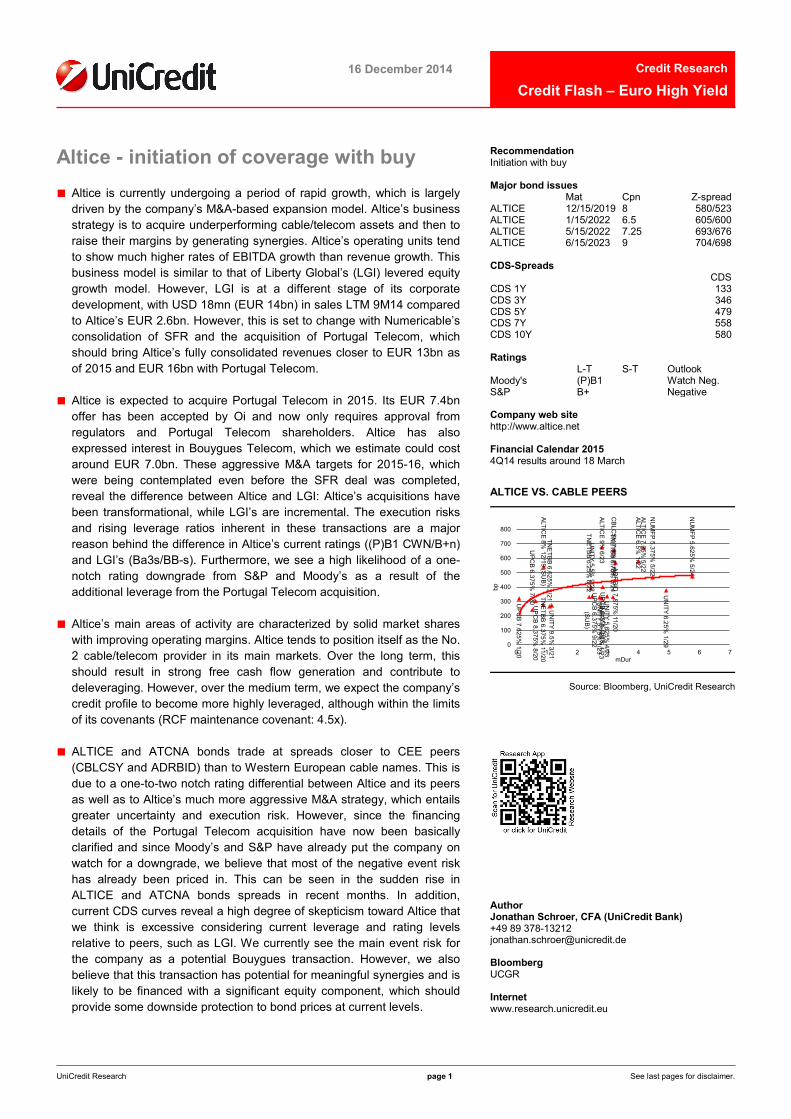

■ ALTICE and ATCNA bonds trade at spreads closer to CEE peers (CBLCSY and ADRBID) than to Western European cable names. This is due to a one-to-two notch rating differential between Altice and its peers as well as to Altice’s much more aggressive M&A strategy, which entails greater uncertainty and execution risk. However, since the financing details of the Portugal Telecom acquisition have now been basically clarified and since Moody’s and S&P have already put the company on watch for a downgrade, we believe that most of the negative event risk has already been priced in. This can be seen in the sudden rise in ALTICE and ATCNA bonds spreads in recent months. In addition, current CDS curves reveal a high degree of skepticism toward Altice that we think is excessive considering current leverage and rating levels relative to peers, such as LGI. We currently see the main event risk for the company as a potential Bouygues transaction. However, we also believe that this transaction has potential for meaningful synergies and is likely to be financed with a significant equity component, which should provide some downside protection to bond prices at current levels.

Recommendation Initiation with buy Major bond issues Mat Cpn Z-spread ALTICE 12/15/2019 8 580/523 ALTICE 1/15/2022 6.5 605/600 ALTICE 5/15/2022 7.25 693/676 ALTICE 6/15/2023 9 704/698 CDS-Spreads CDS CDS 1Y 133 CDS 3Y 346 CDS 5Y 479 CDS 7Y 558 CDS 10Y 580 Ratings L-T S-T Outlook Moody's (P)B1 Watch Neg. S&P B+ Negative Company web site http://www.altice.net Financial Calendar 2015 4Q14 results around 18 March

ALTICE VS. CABLE PEERS

Source: Bloomberg, UniCredit Research

Author Jonathan Schroer, CFA (UniCredit Bank) +49 89 378-13212 [email protected] Bloomberg UCGR Internet www.research.unicredit.eu

UP

CB

7.625% 1/20

UP

CB

6.375% 7/20

UP

CB

8.375% 8/20

UP

CB

6.75% 3/23

UP

CB

6.375% 9/22

(SU

B)

UN

ITY 9.5% 3/21

UN

ITY 5.5% 9/22

UN

ITY 5.125% 1/23

UN

ITY 5.625% 4/23

UN

ITY 5.75% 1/23

UN

ITY 6.25% 1/29

TNE

TBB

6.375% 11/20

TNE

TBB

6.625% 2/21

TNE

TBB

6.25% 8/22

TNE

TBB

6.75% 8/24

NU

MFP 5.375%

5/22

NU

MFP 5.625%

5/24

ALTIC

E 7.25%

5/22A

LTICE

6.5% 1/22

ALTIC

E 9%

6/23

ALTIC

E 8%

12/19 (SU

B)

CB

LCS

Y 7.5% 11/20 AD

RB

ID 7.875%

11/20

0

100

200

300

400

500

600

700

800

0 1 2 3 4 5 6 7

bp

mDur

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 2 See last pages for disclaimer.

Key Credit Points Group overview The Altice Group is a multinational cable and telecoms company that has evolved

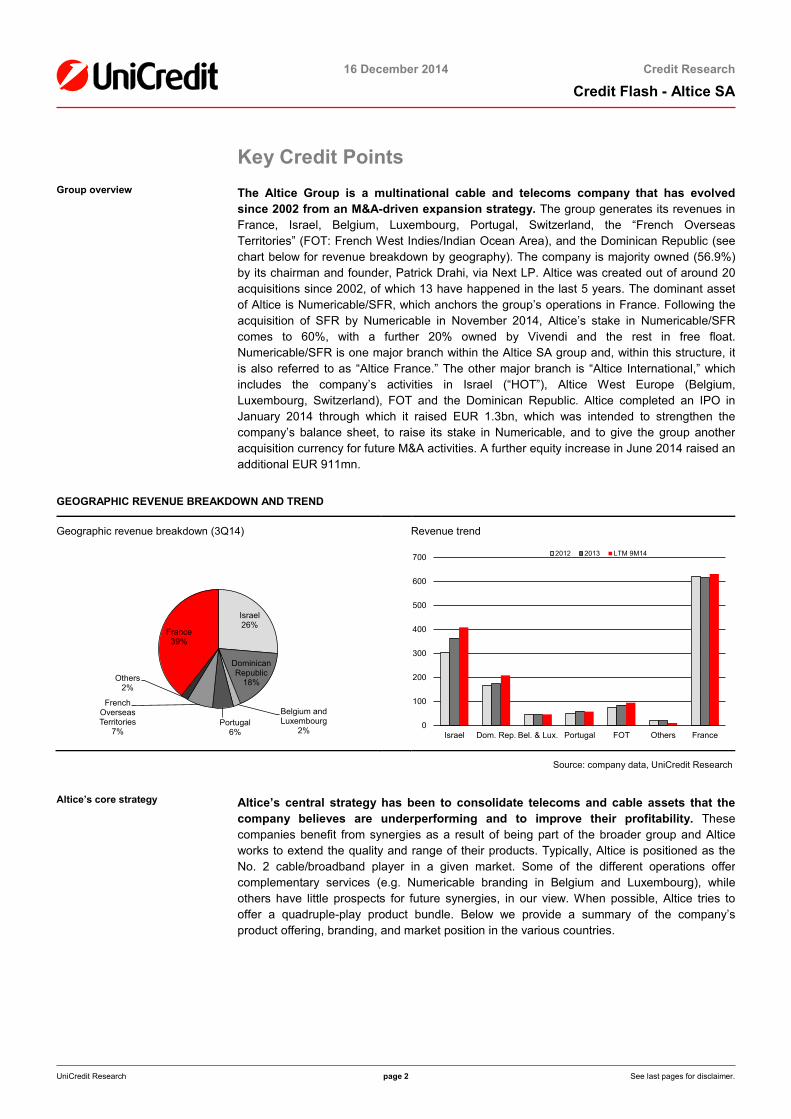

since 2002 from an M&A-driven expansion strategy. The group generates its revenues in France, Israel, Belgium, Luxembourg, Portugal, Switzerland, the “French Overseas Territories” (FOT: French West Indies/Indian Ocean Area), and the Dominican Republic (see chart below for revenue breakdown by geography). The company is majority owned (56.9%) by its chairman and founder, Patrick Drahi, via Next LP. Altice was created out of around 20 acquisitions since 2002, of which 13 have happened in the last 5 years. The dominant asset of Altice is Numericable/SFR, which anchors the group’s operations in France. Following the acquisition of SFR by Numericable in November 2014, Altice’s stake in Numericable/SFR comes to 60%, with a further 20% owned by Vivendi and the rest in free float. Numericable/SFR is one major branch within the Altice SA group and, within this structure, it is also referred to as “Altice France.” The other major branch is “Altice International,” which includes the company’s activities in Israel (“HOT”), Altice West Europe (Belgium, Luxembourg, Switzerland), FOT and the Dominican Republic. Altice completed an IPO in January 2014 through which it raised EUR 1.3bn, which was intended to strengthen the company’s balance sheet, to raise its stake in Numericable, and to give the group another acquisition currency for future M&A activities. A further equity increase in June 2014 raised an additional EUR 911mn.

GEOGRAPHIC REVENUE BREAKDOWN AND TREND

Geographic revenue breakdown (3Q14) Revenue trend

Source: company data, UniCredit Research

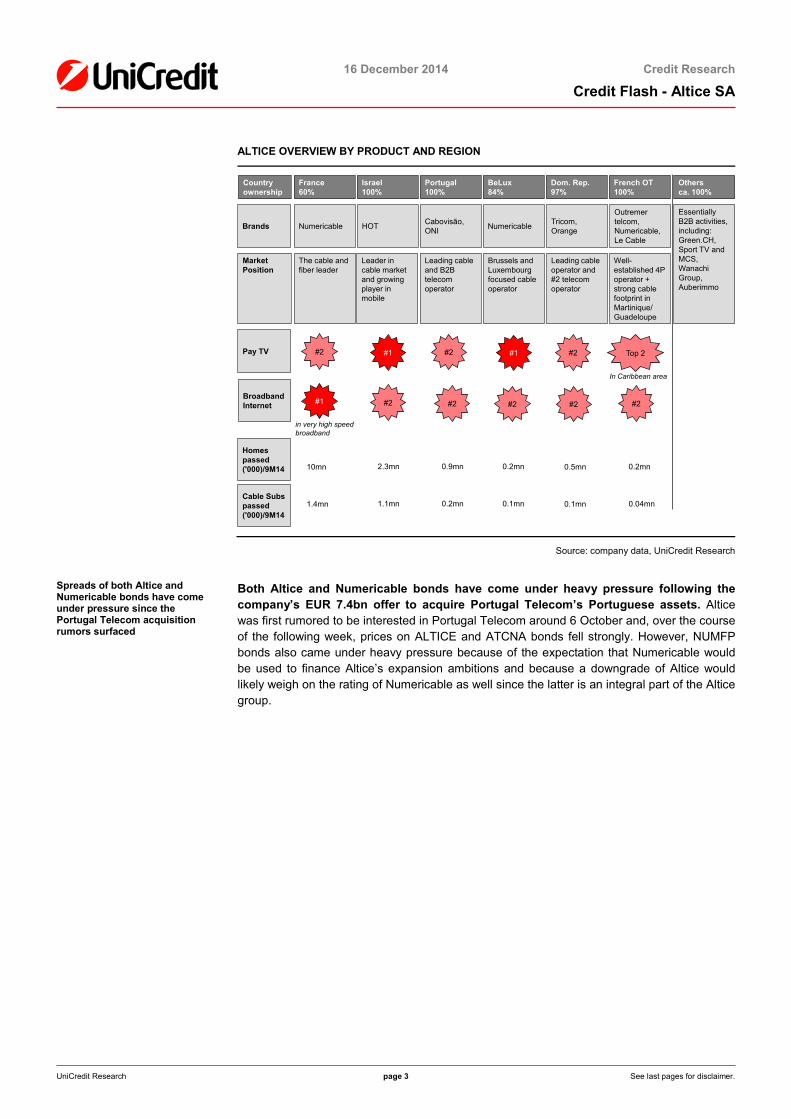

Altice’s core strategy Altice’s central strategy has been to consolidate telecoms and cable assets that the company believes are underperforming and to improve their profitability. These companies benefit from synergies as a result of being part of the broader group and Altice works to extend the quality and range of their products. Typically, Altice is positioned as the No. 2 cable/broadband player in a given market. Some of the different operations offer complementary services (e.g. Numericable branding in Belgium and Luxembourg), while others have little prospects for future synergies, in our view. When possible, Altice tries to offer a quadruple-play product bundle. Below we provide a summary of the company’s product offering, branding, and market position in the various countries.

Israel26%

Dominican Republic

18%

Belgium and Luxembourg

2%Portugal

6%

French Overseas Territories

7%

Others2%

France39%

0

100

200

300

400

500

600

700

Israel Dom. Rep. Bel. & Lux. Portugal FOT Others France

2012 2013 LTM 9M14

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 3 See last pages for disclaimer.

ALTICE OVERVIEW BY PRODUCT AND REGION

Source: company data, UniCredit Research

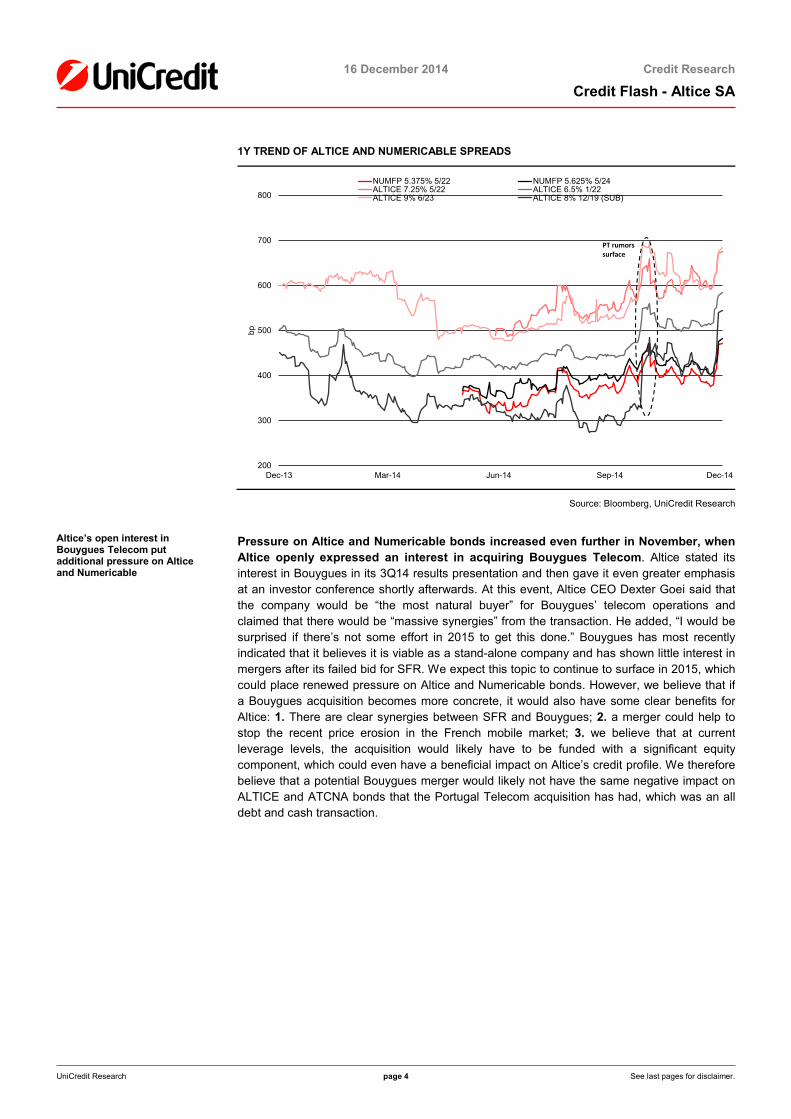

Spreads of both Altice and Numericable bonds have come under pressure since the Portugal Telecom acquisition rumors surfaced

Both Altice and Numericable bonds have come under heavy pressure following the company’s EUR 7.4bn offer to acquire Portugal Telecom’s Portuguese assets. Altice was first rumored to be interested in Portugal Telecom around 6 October and, over the course of the following week, prices on ALTICE and ATCNA bonds fell strongly. However, NUMFP bonds also came under heavy pressure because of the expectation that Numericable would be used to finance Altice’s expansion ambitions and because a downgrade of Altice would likely weigh on the rating of Numericable as well since the latter is an integral part of the Altice group.

Dom. Rep.97%

Others ca. 100%

French OT100%

France60%

BeLux84%

Israel100%

Portugal100%

Brands Numericable HOT Cabovisão, ONI Numericable Tricom,

Orange

Outremertelcom, Numericable, Le Cable

Country ownership

The cable and fiber leader

Leader in cable market and growing player in mobile

Leading cable and B2B telecom operator

Brussels and Luxembourg focused cable operator

Leading cable operator and #2 telecom operator

Well-established 4P operator + strong cable footprint in Martinique/Guadeloupe

Essentially B2B activities, including: Green.CH, Sport TV and MCS, WanachiGroup, Auberimmo

Pay TV

Broadband Internet

Homes passed ('000)/9M14

Cable Subs passed ('000)/9M14

#2 #2

#2 #2#2#2#2

#2#1 #1

#1

Top 2

In Caribbean area

in very high speed broadband

10mn 2.3mn 0.9mn 0.2mn 0.5mn 0.2mn

1.4mn 1.1mn 0.2mn 0.1mn 0.1mn 0.04mn

Market Position

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 4 See last pages for disclaimer.

1Y TREND OF ALTICE AND NUMERICABLE SPREADS

Source: Bloomberg, UniCredit Research

Altice’s open interest in Bouygues Telecom put additional pressure on Altice and Numericable

Pressure on Altice and Numericable bonds increased even further in November, when Altice openly expressed an interest in acquiring Bouygues Telecom. Altice stated its interest in Bouygues in its 3Q14 results presentation and then gave it even greater emphasis at an investor conference shortly afterwards. At this event, Altice CEO Dexter Goei said that the company would be “the most natural buyer” for Bouygues’ telecom operations and claimed that there would be “massive synergies” from the transaction. He added, “I would be surprised if there’s not some effort in 2015 to get this done.” Bouygues has most recently indicated that it believes it is viable as a stand-alone company and has shown little interest in mergers after its failed bid for SFR. We expect this topic to continue to surface in 2015, which could place renewed pressure on Altice and Numericable bonds. However, we believe that if a Bouygues acquisition becomes more concrete, it would also have some clear benefits for Altice: 1. There are clear synergies between SFR and Bouygues; 2. a merger could help to stop the recent price erosion in the French mobile market; 3. we believe that at current leverage levels, the acquisition would likely have to be funded with a significant equity component, which could even have a beneficial impact on Altice’s credit profile. We therefore believe that a potential Bouygues merger would likely not have the same negative impact on ALTICE and ATCNA bonds that the Portugal Telecom acquisition has had, which was an all debt and cash transaction.

200

300

400

500

600

700

800

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

bp

NUMFP 5.375% 5/22 NUMFP 5.625% 5/24ALTICE 7.25% 5/22 ALTICE 6.5% 1/22ALTICE 9% 6/23 ALTICE 8% 12/19 (SUB)

PT rumors surface

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 5 See last pages for disclaimer.

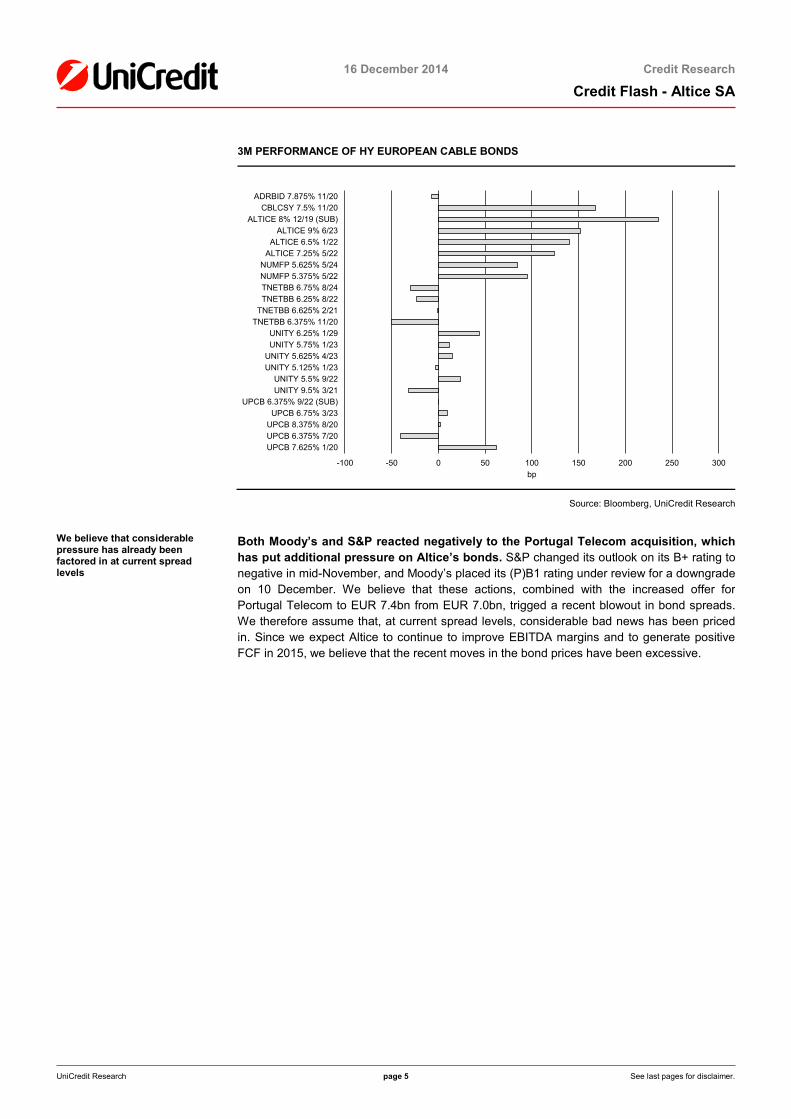

3M PERFORMANCE OF HY EUROPEAN CABLE BONDS

Source: Bloomberg, UniCredit Research

We believe that considerable pressure has already been factored in at current spread levels

Both Moody’s and S&P reacted negatively to the Portugal Telecom acquisition, which has put additional pressure on Altice’s bonds. S&P changed its outlook on its B+ rating to negative in mid-November, and Moody’s placed its (P)B1 rating under review for a downgrade on 10 December. We believe that these actions, combined with the increased offer for Portugal Telecom to EUR 7.4bn from EUR 7.0bn, trigged a recent blowout in bond spreads. We therefore assume that, at current spread levels, considerable bad news has been priced in. Since we expect Altice to continue to improve EBITDA margins and to generate positive FCF in 2015, we believe that the recent moves in the bond prices have been excessive.

-100 -50 0 50 100 150 200 250 300

UPCB 7.625% 1/20UPCB 6.375% 7/20UPCB 8.375% 8/20

UPCB 6.75% 3/23UPCB 6.375% 9/22 (SUB)

UNITY 9.5% 3/21UNITY 5.5% 9/22

UNITY 5.125% 1/23UNITY 5.625% 4/23

UNITY 5.75% 1/23UNITY 6.25% 1/29

TNETBB 6.375% 11/20TNETBB 6.625% 2/21

TNETBB 6.25% 8/22TNETBB 6.75% 8/24NUMFP 5.375% 5/22NUMFP 5.625% 5/24

ALTICE 7.25% 5/22ALTICE 6.5% 1/22

ALTICE 9% 6/23ALTICE 8% 12/19 (SUB)

CBLCSY 7.5% 11/20ADRBID 7.875% 11/20

bp

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 6 See last pages for disclaimer.

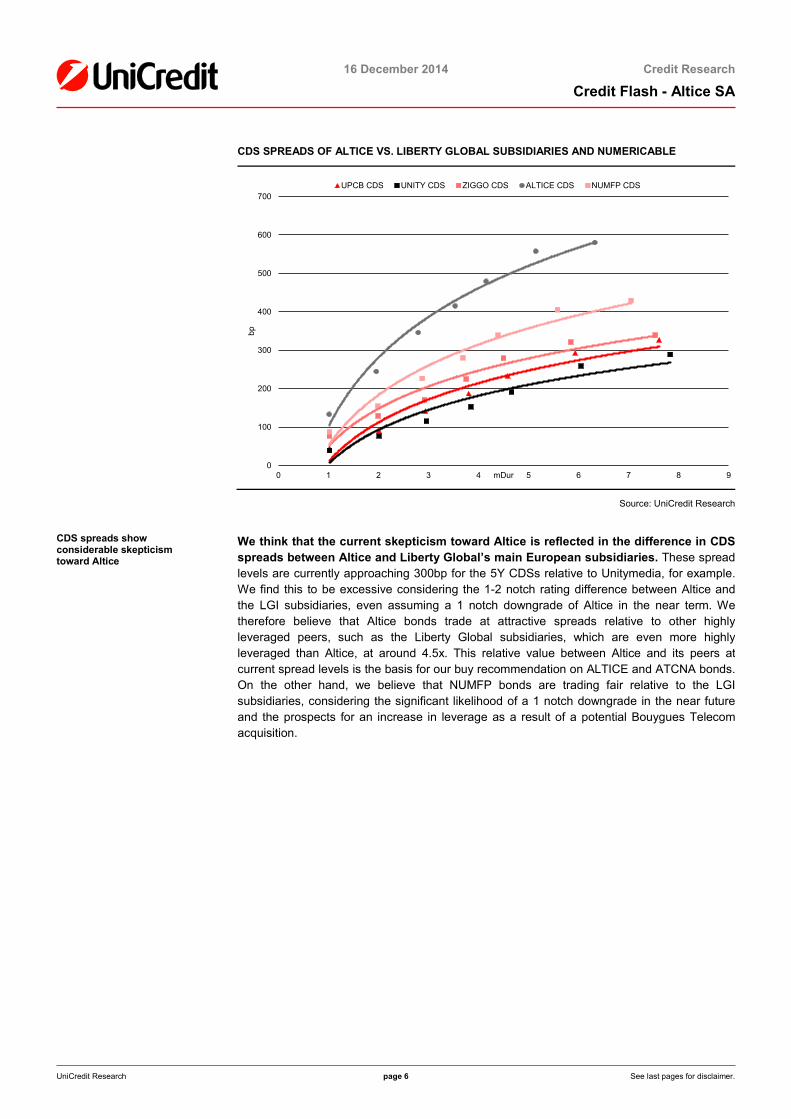

CDS SPREADS OF ALTICE VS. LIBERTY GLOBAL SUBSIDIARIES AND NUMERICABLE

Source: UniCredit Research

CDS spreads show considerable skepticism toward Altice

We think that the current skepticism toward Altice is reflected in the difference in CDS spreads between Altice and Liberty Global’s main European subsidiaries. These spread levels are currently approaching 300bp for the 5Y CDSs relative to Unitymedia, for example. We find this to be excessive considering the 1-2 notch rating difference between Altice and the LGI subsidiaries, even assuming a 1 notch downgrade of Altice in the near term. We therefore believe that Altice bonds trade at attractive spreads relative to other highly leveraged peers, such as the Liberty Global subsidiaries, which are even more highly leveraged than Altice, at around 4.5x. This relative value between Altice and its peers at current spread levels is the basis for our buy recommendation on ALTICE and ATCNA bonds. On the other hand, we believe that NUMFP bonds are trading fair relative to the LGI subsidiaries, considering the significant likelihood of a 1 notch downgrade in the near future and the prospects for an increase in leverage as a result of a potential Bouygues Telecom acquisition.

0

100

200

300

400

500

600

700

0 1 2 3 4 5 6 7 8 9

bp

mDur

UPCB CDS UNITY CDS ZIGGO CDS ALTICE CDS NUMFP CDS

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 7 See last pages for disclaimer.

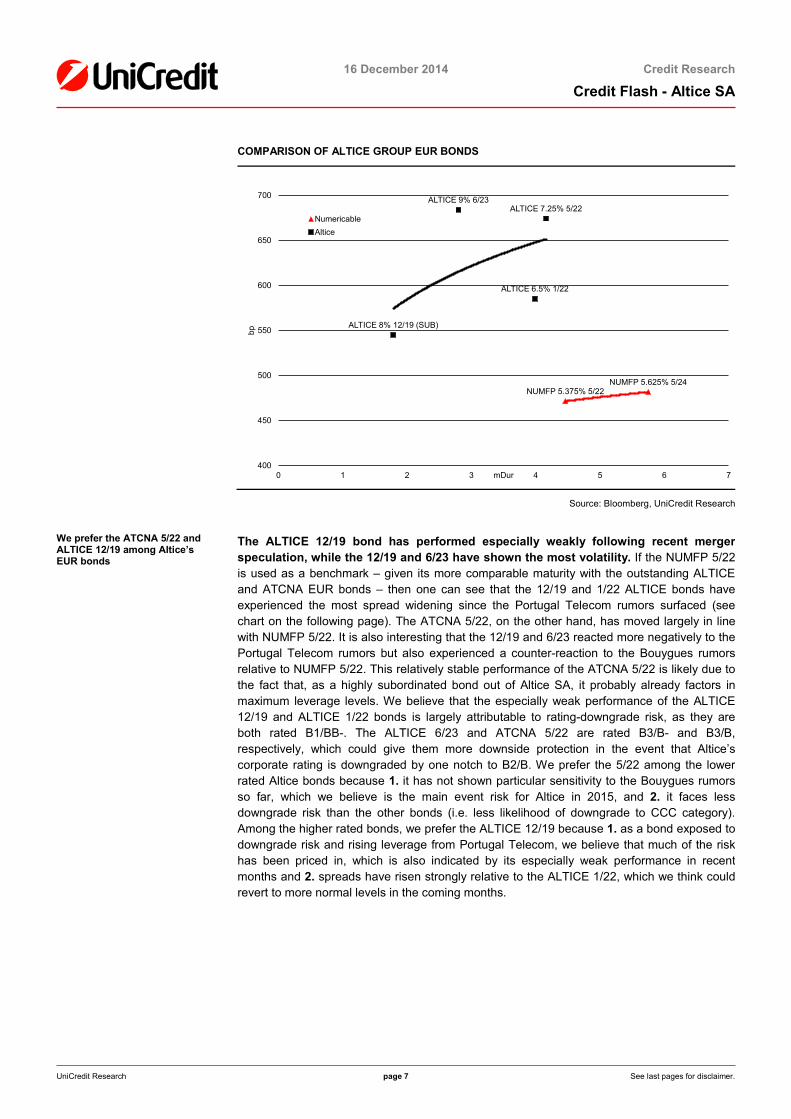

COMPARISON OF ALTICE GROUP EUR BONDS

Source: Bloomberg, UniCredit Research

We prefer the ATCNA 5/22 and ALTICE 12/19 among Altice’s EUR bonds

The ALTICE 12/19 bond has performed especially weakly following recent merger speculation, while the 12/19 and 6/23 have shown the most volatility. If the NUMFP 5/22 is used as a benchmark – given its more comparable maturity with the outstanding ALTICE and ATCNA EUR bonds – then one can see that the 12/19 and 1/22 ALTICE bonds have experienced the most spread widening since the Portugal Telecom rumors surfaced (see chart on the following page). The ATCNA 5/22, on the other hand, has moved largely in line with NUMFP 5/22. It is also interesting that the 12/19 and 6/23 reacted more negatively to the Portugal Telecom rumors but also experienced a counter-reaction to the Bouygues rumors relative to NUMFP 5/22. This relatively stable performance of the ATCNA 5/22 is likely due to the fact that, as a highly subordinated bond out of Altice SA, it probably already factors in maximum leverage levels. We believe that the especially weak performance of the ALTICE 12/19 and ALTICE 1/22 bonds is largely attributable to rating-downgrade risk, as they are both rated B1/BB-. The ALTICE 6/23 and ATCNA 5/22 are rated B3/B- and B3/B, respectively, which could give them more downside protection in the event that Altice’s corporate rating is downgraded by one notch to B2/B. We prefer the 5/22 among the lower rated Altice bonds because 1. it has not shown particular sensitivity to the Bouygues rumors so far, which we believe is the main event risk for Altice in 2015, and 2. it faces less downgrade risk than the other bonds (i.e. less likelihood of downgrade to CCC category). Among the higher rated bonds, we prefer the ALTICE 12/19 because 1. as a bond exposed to downgrade risk and rising leverage from Portugal Telecom, we believe that much of the risk has been priced in, which is also indicated by its especially weak performance in recent months and 2. spreads have risen strongly relative to the ALTICE 1/22, which we think could revert to more normal levels in the coming months.

NUMFP 5.375% 5/22NUMFP 5.625% 5/24

ALTICE 7.25% 5/22

ALTICE 6.5% 1/22

ALTICE 9% 6/23

ALTICE 8% 12/19 (SUB)

400

450

500

550

600

650

700

0 1 2 3 4 5 6 7

bp

mDur

NumericableAltice

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 8 See last pages for disclaimer.

SPREAD DIFFERENTIAL OF ALTICE BONDS VS. NUMFP 5/22

Source: Bloomberg, UniCredit Research

-150

-100

-50

0

50

100

150

200

250

300

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

ATCNA 5/22 Altice 1/22 Altice 6/23 Altice 12/19

PT rumorssurface

Bouyguesrumors

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 9 See last pages for disclaimer.

Altice Group Overview

Altice France The importance of France has risen considerably with Numericable’s acquisition of SFR

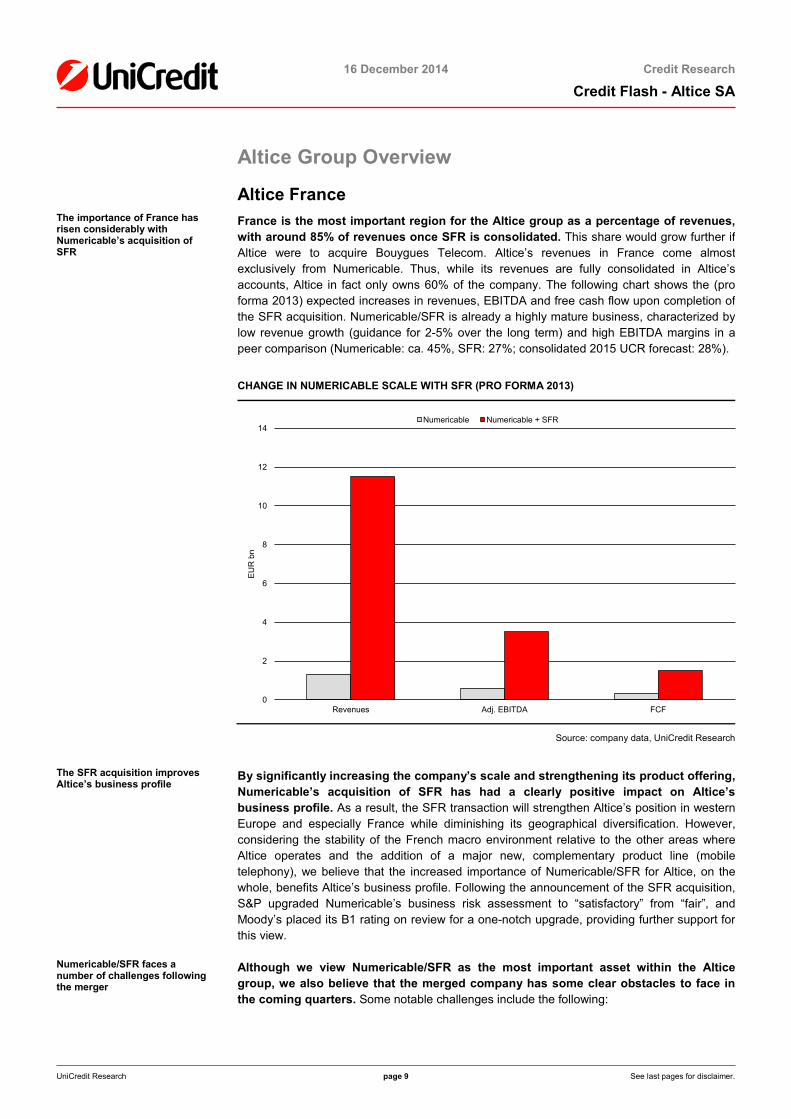

France is the most important region for the Altice group as a percentage of revenues, with around 85% of revenues once SFR is consolidated. This share would grow further if Altice were to acquire Bouygues Telecom. Altice’s revenues in France come almost exclusively from Numericable. Thus, while its revenues are fully consolidated in Altice’s accounts, Altice in fact only owns 60% of the company. The following chart shows the (pro forma 2013) expected increases in revenues, EBITDA and free cash flow upon completion of the SFR acquisition. Numericable/SFR is already a highly mature business, characterized by low revenue growth (guidance for 2-5% over the long term) and high EBITDA margins in a peer comparison (Numericable: ca. 45%, SFR: 27%; consolidated 2015 UCR forecast: 28%).

CHANGE IN NUMERICABLE SCALE WITH SFR (PRO FORMA 2013)

Source: company data, UniCredit Research

The SFR acquisition improves Altice’s business profile

By significantly increasing the company’s scale and strengthening its product offering, Numericable’s acquisition of SFR has had a clearly positive impact on Altice’s business profile. As a result, the SFR transaction will strengthen Altice’s position in western Europe and especially France while diminishing its geographical diversification. However, considering the stability of the French macro environment relative to the other areas where Altice operates and the addition of a major new, complementary product line (mobile telephony), we believe that the increased importance of Numericable/SFR for Altice, on the whole, benefits Altice’s business profile. Following the announcement of the SFR acquisition, S&P upgraded Numericable’s business risk assessment to “satisfactory” from “fair”, and Moody’s placed its B1 rating on review for a one-notch upgrade, providing further support for this view.

Numericable/SFR faces a number of challenges following the merger

Although we view Numericable/SFR as the most important asset within the Altice group, we also believe that the merged company has some clear obstacles to face in the coming quarters. Some notable challenges include the following:

0

2

4

6

8

10

12

14

Revenues Adj. EBITDA FCF

EU

R b

n

Numericable Numericable + SFR

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 10 See last pages for disclaimer.

■ Difficult growth prospects in a highly saturated market: Numericable is currently the sole cable operator in France and has the leading fiber network in the country, with 10mn homes passed. The merged company will be the market leader in ultra-high speed broadband, with a 55% market share, and will be No. 2 in total broadband, with a 25% market share. One of the goals behind the Numericable/SFR merger is to cross-sell cable products to SFR’s larger customer base (SFR subscribers 21.4mn vs. Numericable’s 1.1mn). However, given the already high market penetration of Numericable, we do not expect cable revenue growth to significantly accelerate above the 2-3% level seen so far in 2014. In addition, growth in consumer spending is likely to remain depressed in Western Europe for the foreseeable future, based on the near-term macro outlook, which would also weigh on discretionary spending, such as pay-tv.

■ Targets for synergies look ambitious and are likely to absorb Numericable management’s attention for the coming years: Numericable is targeting EBITDA synergies of EUR 730mn by 2017 and capex synergies of EUR 375mn. In order to reach these goals, Numericable has planned a range of actions, including cross-selling, making marketing more efficient, optimizing data transfers between networks and fiber deployment, together with reducing overlapping procurement and IT structures. While there are clearly synergies that can be gained from the two distinct companies’ operating in the same region, the fact that Numericable and SFR offer complementary rather than overlapping products makes these targets look ambitious, in our view. Over the longer term, Numericable is targeting an increase in the EBITDA margin from around 30% (pro forma) today to 40%, which we think would require more synergies than the EUR 730mn sought by 2017.

■ SFR’s performance has weakened noticeably in 2014, and we believe it will require additional investments to regain momentum. Through 9M14, revenues were down 2.9% to EUR 7.4bn from EUR 7.6bn in the prior-year period, and EBITDA plunged 19.2% to EUR 1.8bn from EUR 2.2bn as of 9M13. The weak performance was driven by an ongoing erosion of revenues in the company’s core retail segment to EUR 4.8bn from EUR 5.2bn (-6.3%). As a result, we believe that any capex synergies at Numericable/SFR are likely to be slow to appear.

Future M&A risk is substantial for Altice France

We think that Altice’s interest in acquiring Bouygues Telecom stems in large part from SFR’s revenue decline, which came about as a result of a price war among French mobile carriers. In addition to the potential to generate synergies, an SFR/Bouygues combination might help ease this downward price spiral by consolidating the French mobile market among three players (SFR/Bouygues, Orange and Illiad). Bouygues has said that it is preparing for four-way competition in the French marketplace but has also indicated that it would listen to an offer from Altice. Based on Bouygues Telecom’s 2013-14 EBITDA of around EUR 700-900mn (EUR 700mn LTM9M14, EUR 900mn in 2013) and a multiple of around 7.5x (Numericable paid 6.5x for SFR, offered 7.4x for Portugal Telecom pre-synergies), we see a potential acquisition price of up to EUR 7.0bn, which involves a higher multiple due to significantly greater synergy potential than with the previous two acquisitions. If Bouygues’s EBITDA of around EUR 900mn were added to Numericable’s EBITDA following the completion of the SFR takeover, then consolidated pro forma EBITDA could come to around EUR 4.4bn (based on pro forma 2013 or with synergies of EUR 300mn for SFR and EUR 200mn for Bouygues based on 2014 figures). However, this transaction is unlikely to be completed before 2016, when the company could potentially generate an additional EUR 300mn in synergies from SFR (i.e. total EBITDA of EUR 4.7bn). This would give Numericable capacity of around EUR 18.8bn in debt before exceeding its 4.0x net debt/EBITDA covenant in the current bond documentation. With current debt at Numericable of around EUR 11.8bn, this amounts to additional debt capacity of up to EUR 7.0bn, meaning that the transaction may barely fit under current Numericable covenants. However, it is unlikely to fit under Altice SA’s 4.0x incurrence covenant or, more importantly, the 4.5x maintenance covenant on the RCF.

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 11 See last pages for disclaimer.

We therefore believe that Altice would likely have to include an equity component to fund the transaction. The company has kept this option open for “transformational” acquisitions. As a result, we believe that a potential Bouygues acquisition would be unlikely to have the same negative effects on Altice bonds that the Portugal Telecom acquisition has had due to the potential synergies involved between SFR and Bouygues as well as the likelihood of an equity component in the financing.

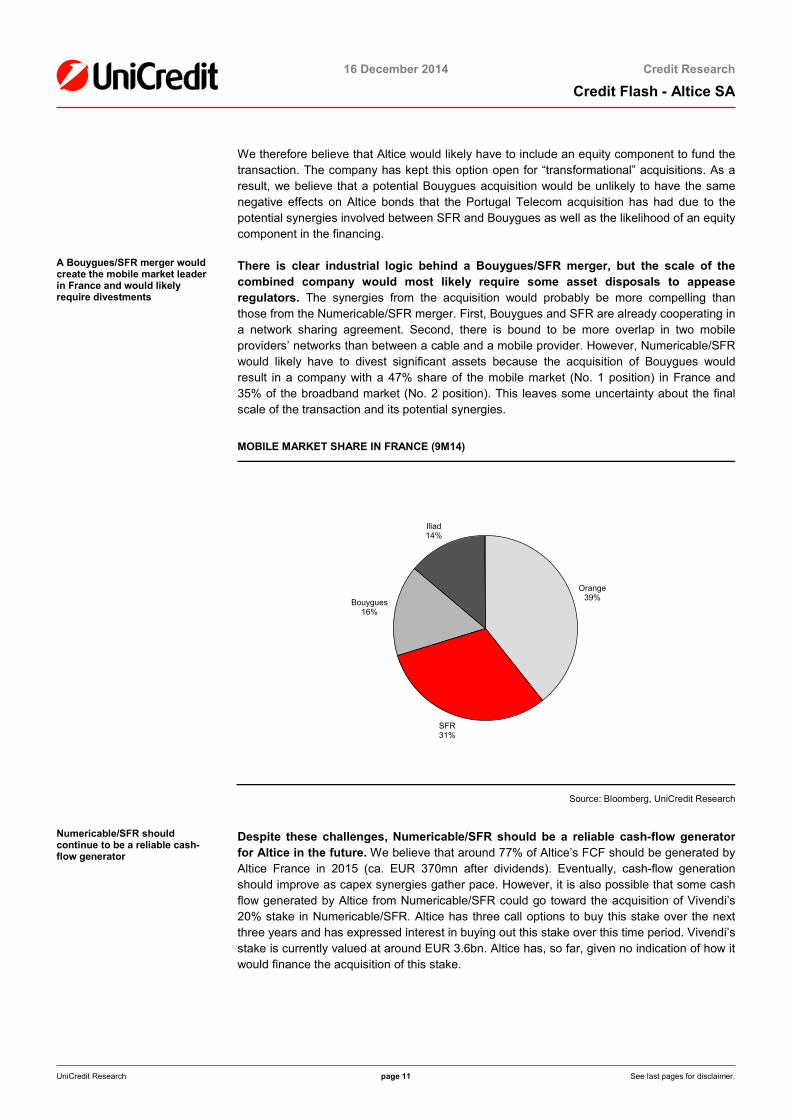

A Bouygues/SFR merger would create the mobile market leader in France and would likely require divestments

There is clear industrial logic behind a Bouygues/SFR merger, but the scale of the combined company would most likely require some asset disposals to appease regulators. The synergies from the acquisition would probably be more compelling than those from the Numericable/SFR merger. First, Bouygues and SFR are already cooperating in a network sharing agreement. Second, there is bound to be more overlap in two mobile providers’ networks than between a cable and a mobile provider. However, Numericable/SFR would likely have to divest significant assets because the acquisition of Bouygues would result in a company with a 47% share of the mobile market (No. 1 position) in France and 35% of the broadband market (No. 2 position). This leaves some uncertainty about the final scale of the transaction and its potential synergies.

MOBILE MARKET SHARE IN FRANCE (9M14)

Source: Bloomberg, UniCredit Research

Numericable/SFR should continue to be a reliable cash-flow generator

Despite these challenges, Numericable/SFR should be a reliable cash-flow generator for Altice in the future. We believe that around 77% of Altice’s FCF should be generated by Altice France in 2015 (ca. EUR 370mn after dividends). Eventually, cash-flow generation should improve as capex synergies gather pace. However, it is also possible that some cash flow generated by Altice from Numericable/SFR could go toward the acquisition of Vivendi’s 20% stake in Numericable/SFR. Altice has three call options to buy this stake over the next three years and has expressed interest in buying out this stake over this time period. Vivendi’s stake is currently valued at around EUR 3.6bn. Altice has, so far, given no indication of how it would finance the acquisition of this stake.

Orange39%

SFR31%

Bouygues16%

Iliad14%

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 12 See last pages for disclaimer.

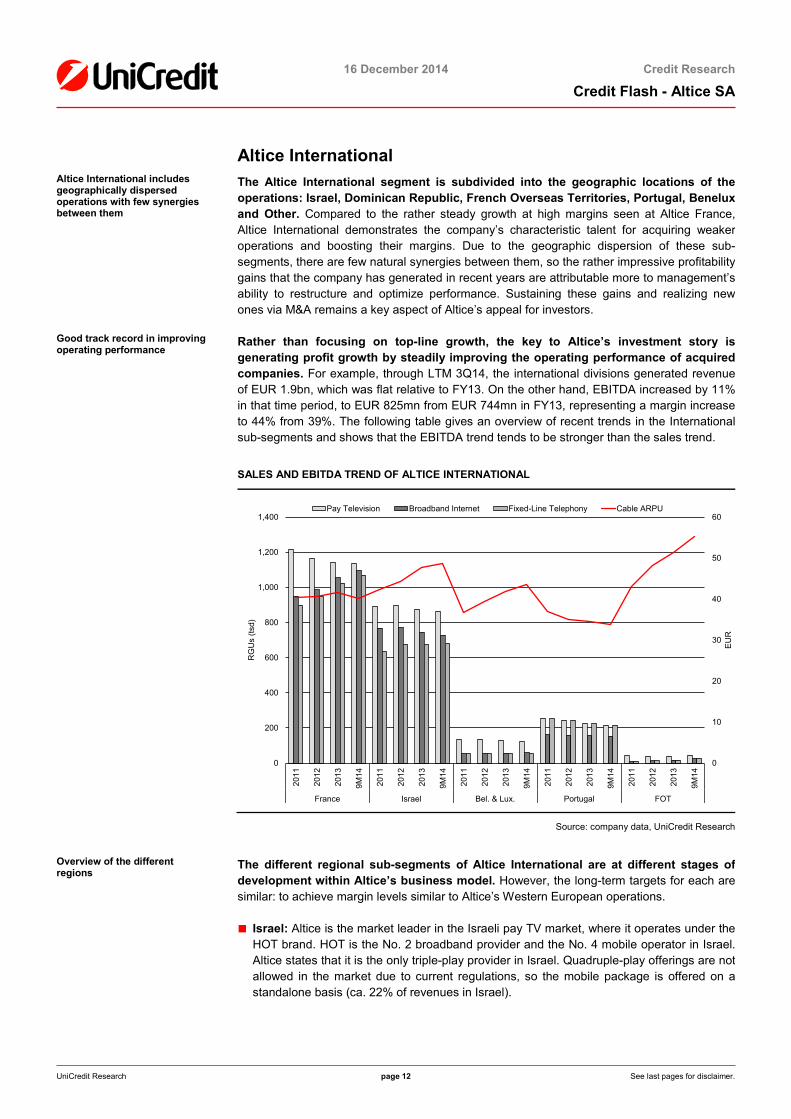

Altice International Altice International includes geographically dispersed operations with few synergies between them

The Altice International segment is subdivided into the geographic locations of the operations: Israel, Dominican Republic, French Overseas Territories, Portugal, Benelux and Other. Compared to the rather steady growth at high margins seen at Altice France, Altice International demonstrates the company’s characteristic talent for acquiring weaker operations and boosting their margins. Due to the geographic dispersion of these sub-segments, there are few natural synergies between them, so the rather impressive profitability gains that the company has generated in recent years are attributable more to management’s ability to restructure and optimize performance. Sustaining these gains and realizing new ones via M&A remains a key aspect of Altice’s appeal for investors.

Good track record in improving operating performance

Rather than focusing on top-line growth, the key to Altice’s investment story is generating profit growth by steadily improving the operating performance of acquired companies. For example, through LTM 3Q14, the international divisions generated revenue of EUR 1.9bn, which was flat relative to FY13. On the other hand, EBITDA increased by 11% in that time period, to EUR 825mn from EUR 744mn in FY13, representing a margin increase to 44% from 39%. The following table gives an overview of recent trends in the International sub-segments and shows that the EBITDA trend tends to be stronger than the sales trend.

SALES AND EBITDA TREND OF ALTICE INTERNATIONAL

Source: company data, UniCredit Research

Overview of the different regions

The different regional sub-segments of Altice International are at different stages of development within Altice’s business model. However, the long-term targets for each are similar: to achieve margin levels similar to Altice’s Western European operations.

■ Israel: Altice is the market leader in the Israeli pay TV market, where it operates under the HOT brand. HOT is the No. 2 broadband provider and the No. 4 mobile operator in Israel. Altice states that it is the only triple-play provider in Israel. Quadruple-play offerings are not allowed in the market due to current regulations, so the mobile package is offered on a standalone basis (ca. 22% of revenues in Israel).

0

10

20

30

40

50

60

0

200

400

600

800

1,000

1,200

1,400

2011

2012

2013

9M14

2011

2012

2013

9M14

2011

2012

2013

9M14

2011

2012

2013

9M14

2011

2012

2013

9M14

France Israel Bel. & Lux. Portugal FOT

EU

R

RG

Us

(tsd)

Pay Television Broadband Internet Fixed-Line Telephony Cable ARPU

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 13 See last pages for disclaimer.

Altice’s Israeli business has matured considerably in recent years and is now approaching a revenue level that is comparable with that of Numericable (before SFR). Despite a contracting top line (-1% as of LTM 3Q14 vs. FY13), the division continues to generate strong EBITDA growth (+12%). EBITDA margins have now reached a very high level of 47% (LTM 3Q14, +6pp vs. FY13). Therefore, we expect to see a stabilization of results here going forward which will more resemble the French operations than those in more dynamically growing markets.

■ Belgium and Luxembourg: With EBITDA margins of around 65%, this region is Altice’s most profitable. However, this market has also seen virtually no revenue growth in recent years. The company’s regional focus is mostly concentrated in the area around Luxembourg, where it is the market leader for pay TV and broadband, which it offers under the Numericable brand. However, Altice’s presence in the region is limited, with around 110,000 cable customers and 231,000 RGUs. Altice also offers mobile services via an MVNO under the Coditel brand (3,000 subscribers). Despite the highly developed nature of this market, Altice has still been able to raise the EBITDA margin here in recent years, from 61% in 2011.

■ Portugal: Despite a declining top line and difficult macro environment, Altice has managed solid EBITDA growth in this market in recent years. Portugal is a relatively small market for Altice at present and operates under the Cabelvisão brand. The Portuguese business is divided nearly evenly into B2C (51% of revenues through 9M14) and B2B (49%) offerings. In B2C, the company is the third-largest national provider (after ZON and Portugal Telecom); in B2B, it ranks second. The company recently acquired the B2B business and operates under the ONI brand. Competitive pressure is rising in Portugal as ZON has begun to offer quadruple-play bundles. Altice’s EBITDA margin has improved substantially in recent years, from 20% in 2012 to 28% as of LTM 3Q14, although this shows that there is more room before Altice reaches the levels of its most productive operations. We see the smaller scale and rising competitive pressure in this market as the major reasons behind Altice’s interest in acquiring the Portugal Telecom assets, which is discussed in a separate section below.

■ French Overseas Territories (FOT): Altice offers direct-to-home (DTH) and DSL products within the French West Indies and Indian Ocean area. It operates mainly under the Numericable and Outremer brands in the region. Altice has committed to sell the Outremer mobile business, although it will continue to offer its triple-play bundled Outremer product. The FOT market has a low subscriber base relative to Altice’s other regions but features very high average revenues per user (ARPUs). This region also has been experiencing higher top-line growth than most of Altice’s other markets (CAGR: 12% since 2012), with margins that are approaching the upper levels of the margins of Altice’s subsidiaries (EBITDA margin: 43% as of LTM 3Q14).

■ Dominican Republic: Altice acquired Orange Dominicana (ODO) and Triccom in late 2013. ODO is a mobile telephony and wireless broadband provider and is currently the second largest residential mobile operator and the third largest wireless broadband provider in the Dominican Republic. Tricom is active in pay-tv, broadband and fixed-line telephony, which it provides via its cable and DSL network. Altice is therefore able to offer a quadruple-play product in this region. The Dominican Republic has become an important contributor to Altice, with 14% of total revenues (pre-SFR) and EBITDA margins of 46% as of LTM 3Q14, which is near the group average of 45% in that time period.

■ Other: The Other segment includes Altice’s smaller businesses, mostly in the Swiss market. Altice provides B2B services under the green.ch and Green Datacenter brands. It also offers the sports TV channels Ma Chaîne Sport and Sportv. This segment is quite small, with a 2% share of revenues and EBITDA margins significantly below the group average (14% LTM 3Q14).

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 14 See last pages for disclaimer.

The acquisition of Portugal Telecom should significantly alter Altice group’s composition

The most concrete acquisition on the horizon is Altice’s offer for Portugal Telecom. On 9 December, Altice signed a definitive EUR 7.4bn offer to acquire the Portuguese assets of Portugal Telecom from Oi S.A. (EUR 5.6bn in cash, EUR 500mn earn-out provision, EUR 1.0bn pension liability, ca. EUR 300mn PPA). This transaction will considerably strengthen Altice’s Portuguese assets, giving it a 57% (assuming no required divestments by the regulator) market share of the Portuguese broadband market and making it the market leader in most segments of the Portuguese telecom market. However, it will also put significant pressure on the company’s credit metrics. Upon completion, Portugal will become Altice’s second-biggest market behind France (2013 pro forma Altice France: sales of EUR 11.5bn, EBITDA of 3.5bn; Altice Portugal + Portugal Telecom: EUR 2.6bn in sales, EUR 1.0bn in EBITDA). However, in some ways, the acquisition of Portugal Telecom would be atypical for Altice, in that Portugal Telecom is already operating at margins that are near the Altice group average (EBITDA margin: 41%, Altice group: 45% LTM 3Q14). Altice has said that it believes it can generate further synergies with the merger, but we believe that these will likely be lower than those of past acquisitions since Portugal Telecom is already operating fairly efficiently. Considering Portugal Telecom’s EBITDA of around EUR 1.0bn, the acquisition would result in a rise in Altice International’s leverage from 3.8x currently to above 4.0x, even if EUR 200mn in synergies are added. Given the 4.0x covenant at the Altice International level, we therefore expect that some debt will have to be issued out of Altice SA.

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 15 See last pages for disclaimer.

Credit Profile Outlook Altice’s credit profile should be driven primarily by M&A, secondarily by operating improvements

We expect that Altice’s credit profile will continue to be driven first by M&A activity and second by ongoing operational improvements from synergies generated by the acquired companies. While the latter can help offset pressure from the former, we think that M&A pressures will dominate in the near term. We believe that, only if Altice is successful with both mergers, would we likely see a pause (or at least a slowdown) in Altice’s M&A activity due to the scale of the companies that need to be integrated and the fact that Altice would emerge as one of the largest telecommunications providers in Europe. If the Bouygues transaction fails, then we would expect only short-term relief for Altice bonds, as the company will probably begin the search for new acquisition targets. In any case, we see high acquisition activity and high leverage as being part of Altice’s business model for the foreseeable future and we would assume leverage levels near current covenants for all Altice bonds. However, as stated before, We expect Altice’s leverage to remain below the levels of Liberty Global’s subsidiaries.

A Bouygues acquisition would likely require an equity component

We believe that an acquisition of both Bouygues and Portugal Telecom is feasible for Altice but would likely require some equity component. There is a net leverage maintenance covenant for the RCF at Altice SA of 4.5x. We think that, including synergies with the acquisition of Portugal Telecom, Altice SA’s leverage would rise above the 4.0x incurrence covenant, although there are certain baskets the company could use to fit under the covenants. If Altice were to complete both transactions, we believe that an all debt-and-cash acquisition of Bouygues would likely not be feasible under current covenants at the SA level. In particular, the expected proximity to the RCF maintenance covenant following the Portugal Telecom transaction further supports our expectation that an acquisition of Bouygues would need to be partially equity funded.

Rating trend is currently negative

We think there is a strong chance that Altice’s acquisition ambitions will cause its rating to be notched down by one in the near term to B2/B. S&P changed its outlook on Altice group to negative after the Portugal Telecom offer, and Moody’s placed its (P)B1 rating on review for a possible downgrade. This contrasts with the SFR transaction, which was initially seen as credit positive by the agencies. We believe that, regardless of the outcome of the various acquisition scenarios, it is only a matter of time before Altice raises its leverage close to the limits set by its covenants. We therefore expect Altice’s ratings to settle at the B level for the foreseeable future. However, we think that a move below this is unlikely, considering the group’s ongoing, solid liquidity profile; expected interest coverage of around 4.0x; and the covenant constraints (target for downgrade to B2/B at S&P: group gross leverage of above 6.0x).

Forecasts for 2015: we expect positive FCF generation

Although Altice’s scale will change dramatically with the SFR acquisition alone, we expect organic growth to be subdued through 2015. We are forecasting organic revenue growth of 1.5% in 2015 for Altice International and a basically flat trend for Altice France. However, as always, we believe that Altice can continue to generate disproportionately higher gains in EBITDA growth, thanks in large part to the synergies generated from recent acquisitions. Since SFR’s margins are significantly below those of Altice’s core cable business, we also expect a significant decline in the group’s operating margins as of 2015. We have factored in EUR 300mn in EBITDA synergies in 2015 for SFR (Altice’s guidance: EUR 730mn by 2017) because we expect all Altice subsidiaries to be under massive pressure to generate cost savings in the coming quarters and because we expect that Altice can find some “low-hanging fruit” at SFR in the first year. We have not factored in any capex synergies in the first year of integration (guidance: EUR 375mn by 2017) because we expect that SFR will need to undertake some investments to improve its competitive positioning in the first year and avoid any market-share losses.

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 16 See last pages for disclaimer.

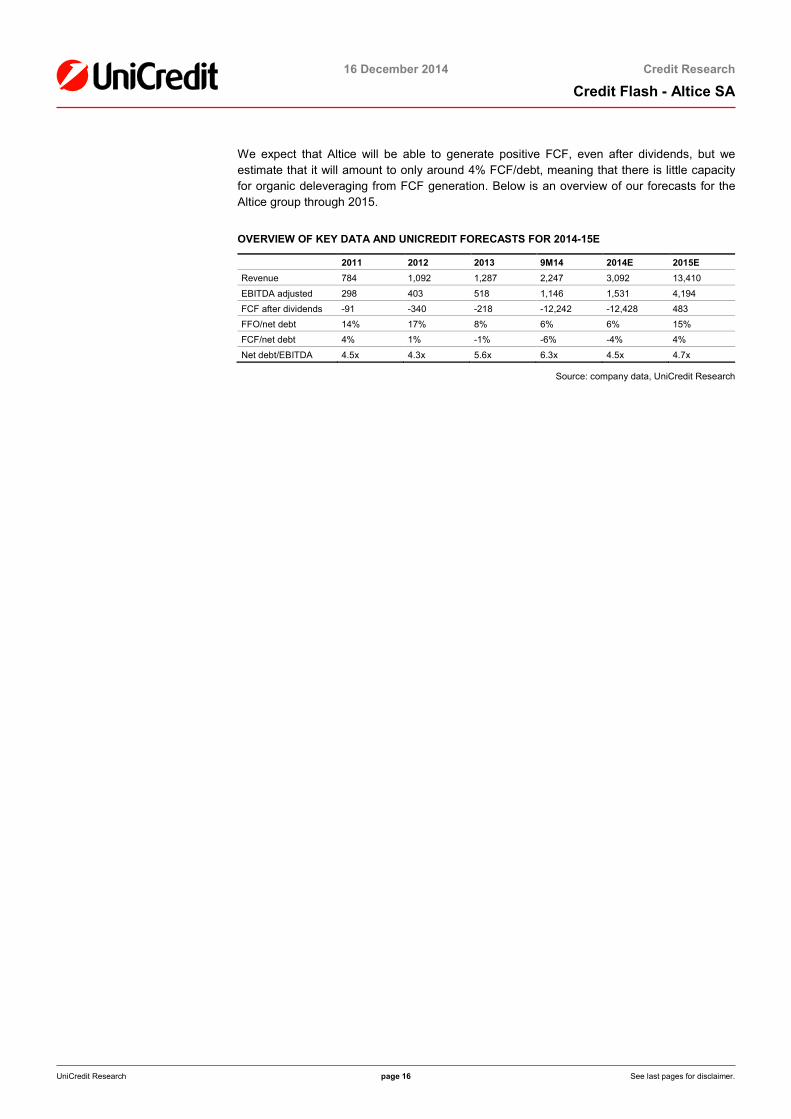

We expect that Altice will be able to generate positive FCF, even after dividends, but we estimate that it will amount to only around 4% FCF/debt, meaning that there is little capacity for organic deleveraging from FCF generation. Below is an overview of our forecasts for the Altice group through 2015.

OVERVIEW OF KEY DATA AND UNICREDIT FORECASTS FOR 2014-15E

2011 2012 2013 9M14 2014E 2015E Revenue 784 1,092 1,287 2,247 3,092 13,410

EBITDA adjusted 298 403 518 1,146 1,531 4,194 FCF after dividends -91 -340 -218 -12,242 -12,428 483 FFO/net debt 14% 17% 8% 6% 6% 15% FCF/net debt 4% 1% -1% -6% -4% 4%

Net debt/EBITDA 4.5x 4.3x 5.6x 6.3x 4.5x 4.7x

Source: company data, UniCredit Research

<date>

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 17 See last pages for disclaimer.

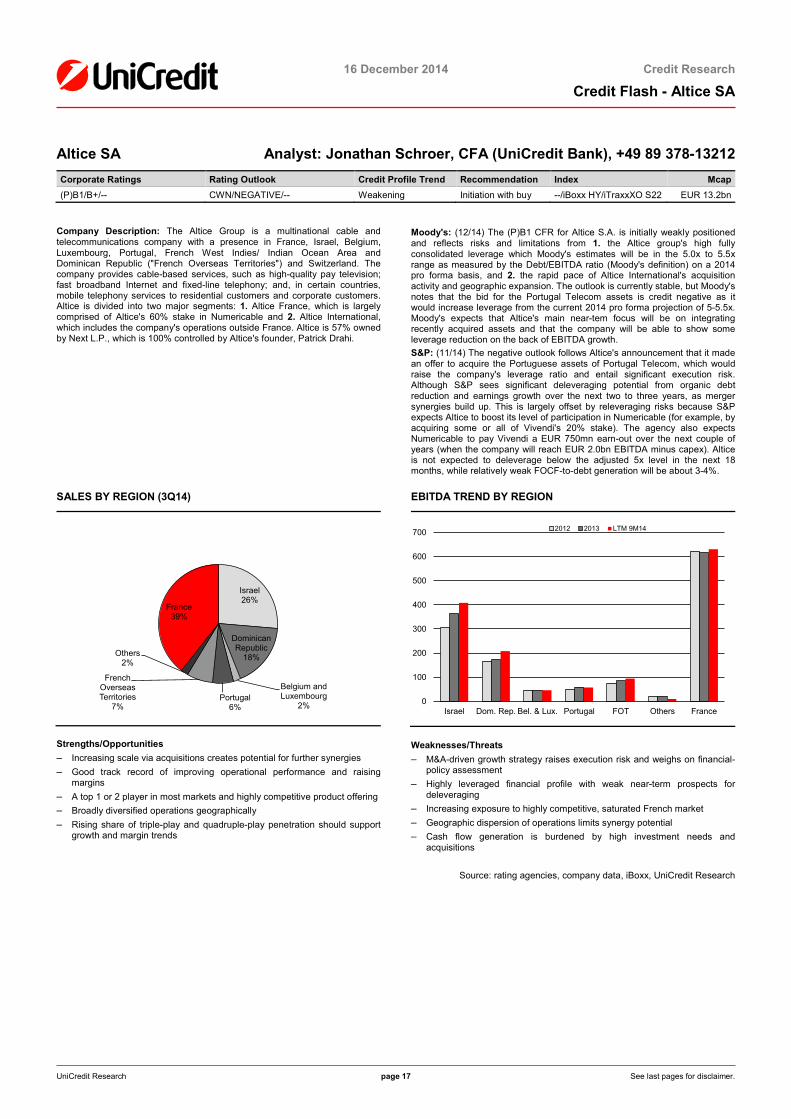

Altice SA Analyst: Jonathan Schroer, CFA (UniCredit Bank), +49 89 378-13212 Corporate Ratings Rating Outlook Credit Profile Trend Recommendation Index Mcap (P)B1/B+/-- CWN/NEGATIVE/-- Weakening Initiation with buy --/iBoxx HY/iTraxxXO S22 EUR 13.2bn

Company Description: The Altice Group is a multinational cable and telecommunications company with a presence in France, Israel, Belgium, Luxembourg, Portugal, French West Indies/ Indian Ocean Area and Dominican Republic ("French Overseas Territories") and Switzerland. The company provides cable-based services, such as high-quality pay television; fast broadband Internet and fixed-line telephony; and, in certain countries, mobile telephony services to residential customers and corporate customers. Altice is divided into two major segments: 1. Altice France, which is largely comprised of Altice's 60% stake in Numericable and 2. Altice International, which includes the company's operations outside France. Altice is 57% owned by Next L.P., which is 100% controlled by Altice's founder, Patrick Drahi.

Moody's: (12/14) The (P)B1 CFR for Altice S.A. is initially weakly positioned and reflects risks and limitations from 1. the Altice group's high fully consolidated leverage which Moody's estimates will be in the 5.0x to 5.5x range as measured by the Debt/EBITDA ratio (Moody's definition) on a 2014 pro forma basis, and 2. the rapid pace of Altice International's acquisition activity and geographic expansion. The outlook is currently stable, but Moody's notes that the bid for the Portugal Telecom assets is credit negative as it would increase leverage from the current 2014 pro forma projection of 5-5.5x. Moody's expects that Altice's main near-tem focus will be on integrating recently acquired assets and that the company will be able to show some leverage reduction on the back of EBITDA growth. S&P: (11/14) The negative outlook follows Altice's announcement that it made an offer to acquire the Portuguese assets of Portugal Telecom, which would raise the company's leverage ratio and entail significant execution risk. Although S&P sees significant deleveraging potential from organic debt reduction and earnings growth over the next two to three years, as merger synergies build up. This is largely offset by releveraging risks because S&P expects Altice to boost its level of participation in Numericable (for example, by acquiring some or all of Vivendi's 20% stake). The agency also expects Numericable to pay Vivendi a EUR 750mn earn-out over the next couple of years (when the company will reach EUR 2.0bn EBITDA minus capex). Altice is not expected to deleverage below the adjusted 5x level in the next 18 months, while relatively weak FOCF-to-debt generation will be about 3-4%.

SALES BY REGION (3Q14)

EBITDA TREND BY REGION

Strengths/Opportunities – Increasing scale via acquisitions creates potential for further synergies – Good track record of improving operational performance and raising

margins – A top 1 or 2 player in most markets and highly competitive product offering – Broadly diversified operations geographically – Rising share of triple-play and quadruple-play penetration should support

growth and margin trends

Weaknesses/Threats – M&A-driven growth strategy raises execution risk and weighs on financial-

policy assessment – Highly leveraged financial profile with weak near-term prospects for

deleveraging – Increasing exposure to highly competitive, saturated French market – Geographic dispersion of operations limits synergy potential – Cash flow generation is burdened by high investment needs and

acquisitions

Source: rating agencies, company data, iBoxx, UniCredit Research

Israel26%

Dominican Republic

18%

Belgium and Luxembourg

2%Portugal

6%

French Overseas Territories

7%

Others2%

France39%

0

100

200

300

400

500

600

700

Israel Dom. Rep. Bel. & Lux. Portugal FOT Others France

2012 2013 LTM 9M14

UniCredit Research page 18 See last pages for disclaimer.

16 December 2014 Credit Research

Credit Flash - Altice SA

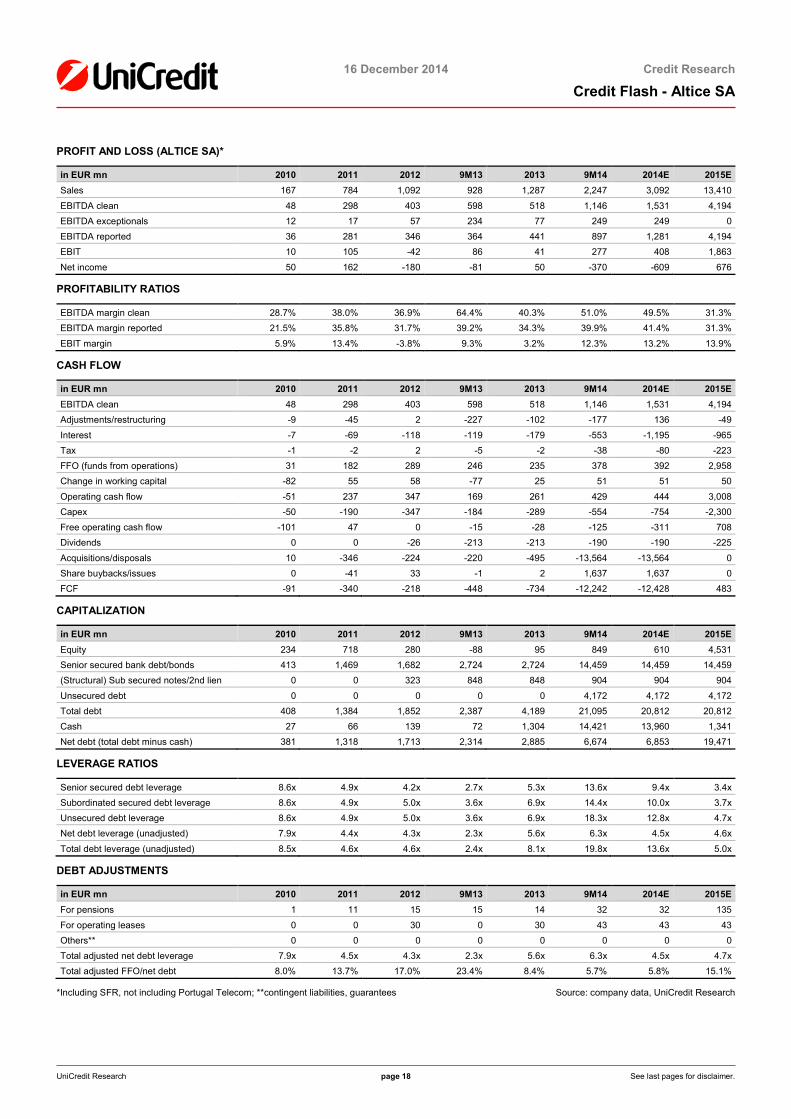

PROFIT AND LOSS (ALTICE SA)*

in EUR mn 2010 2011 2012 9M13 2013 9M14 2014E 2015E Sales 167 784 1,092 928 1,287 2,247 3,092 13,410

EBITDA clean 48 298 403 598 518 1,146 1,531 4,194 EBITDA exceptionals 12 17 57 234 77 249 249 0 EBITDA reported 36 281 346 364 441 897 1,281 4,194 EBIT 10 105 -42 86 41 277 408 1,863

Net income 50 162 -180 -81 50 -370 -609 676

PROFITABILITY RATIOS

EBITDA margin clean 28.7% 38.0% 36.9% 64.4% 40.3% 51.0% 49.5% 31.3% EBITDA margin reported 21.5% 35.8% 31.7% 39.2% 34.3% 39.9% 41.4% 31.3%

EBIT margin 5.9% 13.4% -3.8% 9.3% 3.2% 12.3% 13.2% 13.9%

CASH FLOW

in EUR mn 2010 2011 2012 9M13 2013 9M14 2014E 2015E EBITDA clean 48 298 403 598 518 1,146 1,531 4,194 Adjustments/restructuring -9 -45 2 -227 -102 -177 136 -49

Interest -7 -69 -118 -119 -179 -553 -1,195 -965 Tax -1 -2 2 -5 -2 -38 -80 -223 FFO (funds from operations) 31 182 289 246 235 378 392 2,958 Change in working capital -82 55 58 -77 25 51 51 50

Operating cash flow -51 237 347 169 261 429 444 3,008 Capex -50 -190 -347 -184 -289 -554 -754 -2,300 Free operating cash flow -101 47 0 -15 -28 -125 -311 708 Dividends 0 0 -26 -213 -213 -190 -190 -225

Acquisitions/disposals 10 -346 -224 -220 -495 -13,564 -13,564 0 Share buybacks/issues 0 -41 33 -1 2 1,637 1,637 0 FCF -91 -340 -218 -448 -734 -12,242 -12,428 483

CAPITALIZATION

in EUR mn 2010 2011 2012 9M13 2013 9M14 2014E 2015E Equity 234 718 280 -88 95 849 610 4,531 Senior secured bank debt/bonds 413 1,469 1,682 2,724 2,724 14,459 14,459 14,459 (Structural) Sub secured notes/2nd lien 0 0 323 848 848 904 904 904

Unsecured debt 0 0 0 0 0 4,172 4,172 4,172 Total debt 408 1,384 1,852 2,387 4,189 21,095 20,812 20,812 Cash 27 66 139 72 1,304 14,421 13,960 1,341 Net debt (total debt minus cash) 381 1,318 1,713 2,314 2,885 6,674 6,853 19,471

LEVERAGE RATIOS

Senior secured debt leverage 8.6x 4.9x 4.2x 2.7x 5.3x 13.6x 9.4x 3.4x Subordinated secured debt leverage 8.6x 4.9x 5.0x 3.6x 6.9x 14.4x 10.0x 3.7x Unsecured debt leverage 8.6x 4.9x 5.0x 3.6x 6.9x 18.3x 12.8x 4.7x Net debt leverage (unadjusted) 7.9x 4.4x 4.3x 2.3x 5.6x 6.3x 4.5x 4.6x

Total debt leverage (unadjusted) 8.5x 4.6x 4.6x 2.4x 8.1x 19.8x 13.6x 5.0x

DEBT ADJUSTMENTS

in EUR mn 2010 2011 2012 9M13 2013 9M14 2014E 2015E For pensions 1 11 15 15 14 32 32 135

For operating leases 0 0 30 0 30 43 43 43 Others** 0 0 0 0 0 0 0 0 Total adjusted net debt leverage 7.9x 4.5x 4.3x 2.3x 5.6x 6.3x 4.5x 4.7x Total adjusted FFO/net debt 8.0% 13.7% 17.0% 23.4% 8.4% 5.7% 5.8% 15.1%

*Including SFR, not including Portugal Telecom; **contingent liabilities, guarantees Source: company data, UniCredit Research

UniCredit Research page 19 See last pages for disclaimer.

16 December 2014 Credit Research

Credit Flash - Altice SA

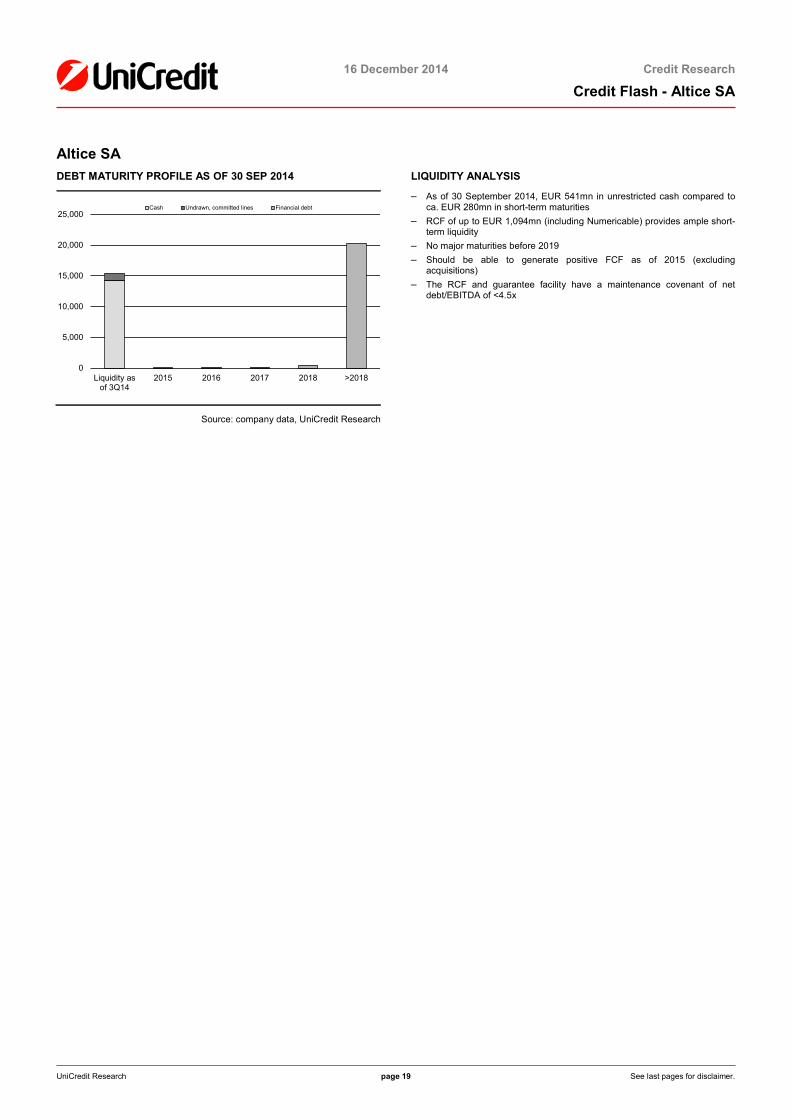

Altice SA DEBT MATURITY PROFILE AS OF 30 SEP 2014

Source: company data, UniCredit Research

LIQUIDITY ANALYSIS

– As of 30 September 2014, EUR 541mn in unrestricted cash compared to ca. EUR 280mn in short-term maturities

– RCF of up to EUR 1,094mn (including Numericable) provides ample short-term liquidity

– No major maturities before 2019 – Should be able to generate positive FCF as of 2015 (excluding

acquisitions) – The RCF and guarantee facility have a maintenance covenant of net

debt/EBITDA of <4.5x

0

5,000

10,000

15,000

20,000

25,000

Liquidity asof 3Q14

2015 2016 2017 2018 >2018

Cash Undrawn, committed lines Financial debt

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 20 See last pages for disclaimer.

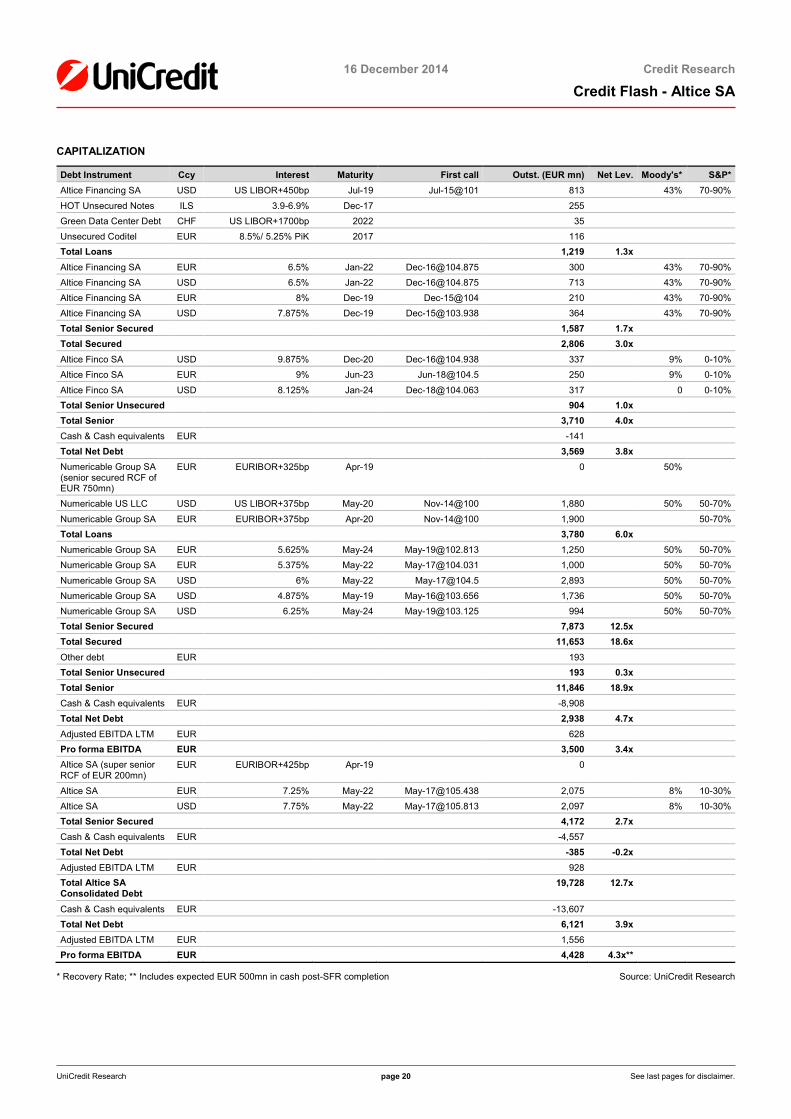

CAPITALIZATION

Debt Instrument Ccy Interest Maturity First call Outst. (EUR mn) Net Lev. Moody's* S&P* Altice Financing SA USD US LIBOR+450bp Jul-19 Jul-15@101 813 43% 70-90%

HOT Unsecured Notes ILS 3.9-6.9% Dec-17 255 Green Data Center Debt CHF US LIBOR+1700bp 2022 35 Unsecured Coditel EUR 8.5%/ 5.25% PiK 2017 116 Total Loans 1,219 1.3x Altice Financing SA EUR 6.5% Jan-22 [email protected] 300 43% 70-90% Altice Financing SA USD 6.5% Jan-22 [email protected] 713 43% 70-90% Altice Financing SA EUR 8% Dec-19 Dec-15@104 210 43% 70-90% Altice Financing SA USD 7.875% Dec-19 [email protected] 364 43% 70-90% Total Senior Secured 1,587 1.7x Total Secured 2,806 3.0x Altice Finco SA USD 9.875% Dec-20 [email protected] 337 9% 0-10% Altice Finco SA EUR 9% Jun-23 [email protected] 250 9% 0-10%

Altice Finco SA USD 8.125% Jan-24 [email protected] 317 0 0-10% Total Senior Unsecured 904 1.0x Total Senior 3,710 4.0x Cash & Cash equivalents EUR -141 Total Net Debt 3,569 3.8x Numericable Group SA (senior secured RCF of EUR 750mn)

EUR EURIBOR+325bp Apr-19 0 50%

Numericable US LLC USD US LIBOR+375bp May-20 Nov-14@100 1,880 50% 50-70%

Numericable Group SA EUR EURIBOR+375bp Apr-20 Nov-14@100 1,900 50-70% Total Loans 3,780 6.0x Numericable Group SA EUR 5.625% May-24 [email protected] 1,250 50% 50-70% Numericable Group SA EUR 5.375% May-22 [email protected] 1,000 50% 50-70%

Numericable Group SA USD 6% May-22 [email protected] 2,893 50% 50-70% Numericable Group SA USD 4.875% May-19 [email protected] 1,736 50% 50-70% Numericable Group SA USD 6.25% May-24 [email protected] 994 50% 50-70% Total Senior Secured 7,873 12.5x Total Secured 11,653 18.6x Other debt EUR 193 Total Senior Unsecured 193 0.3x Total Senior 11,846 18.9x Cash & Cash equivalents EUR -8,908 Total Net Debt 2,938 4.7x Adjusted EBITDA LTM EUR 628 Pro forma EBITDA EUR 3,500 3.4x Altice SA (super senior RCF of EUR 200mn)

EUR EURIBOR+425bp Apr-19 0

Altice SA EUR 7.25% May-22 [email protected] 2,075 8% 10-30% Altice SA USD 7.75% May-22 [email protected] 2,097 8% 10-30% Total Senior Secured 4,172 2.7x Cash & Cash equivalents EUR -4,557 Total Net Debt -385 -0.2x Adjusted EBITDA LTM EUR 928 Total Altice SA Consolidated Debt

19,728 12.7x

Cash & Cash equivalents EUR -13,607 Total Net Debt 6,121 3.9x Adjusted EBITDA LTM EUR 1,556 Pro forma EBITDA EUR 4,428 4.3x**

* Recovery Rate; ** Includes expected EUR 500mn in cash post-SFR completion Source: UniCredit Research

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 21 See last pages for disclaimer.

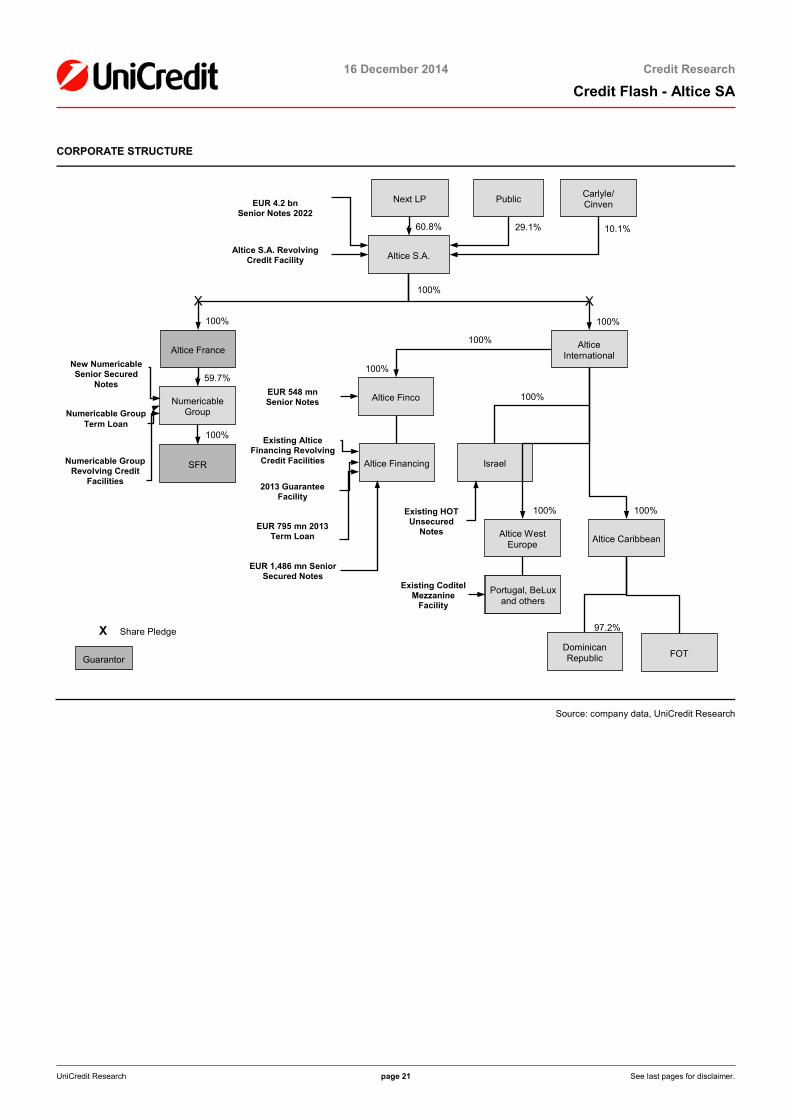

X X

CORPORATE STRUCTURE

Source: company data, UniCredit Research

Public Next LP Carlyle/ Cinven

Altice S.A.

Altice International

Altice Finco

Altice Financing Israel

Altice West Europe Altice Caribbean

Dominican Republic

FOT

Altice France

Numericable Group

SFR

Portugal, BeLux and others

EUR 4.2 bn Senior Notes 2022

Altice S.A. Revolving Credit Facility

EUR 548 mn Senior Notes

Existing Altice Financing Revolving

Credit Facilities

EUR 1,486 mn Senior Secured Notes

2013 Guarantee Facility

EUR 795 mn 2013 Term Loan

Existing HOT Unsecured

Notes

Existing Coditel Mezzanine

Facility

New Numericable Senior Secured

Notes

Numericable Group Term Loan

Numericable Group Revolving Credit

Facilities

60.8% 29.1% 10.1%

100%

100% 100%

59.7%

100%

100%

100%

100%

100% 100%

97.2%

Guarantor

X Share Pledge

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 22 See last pages for disclaimer.

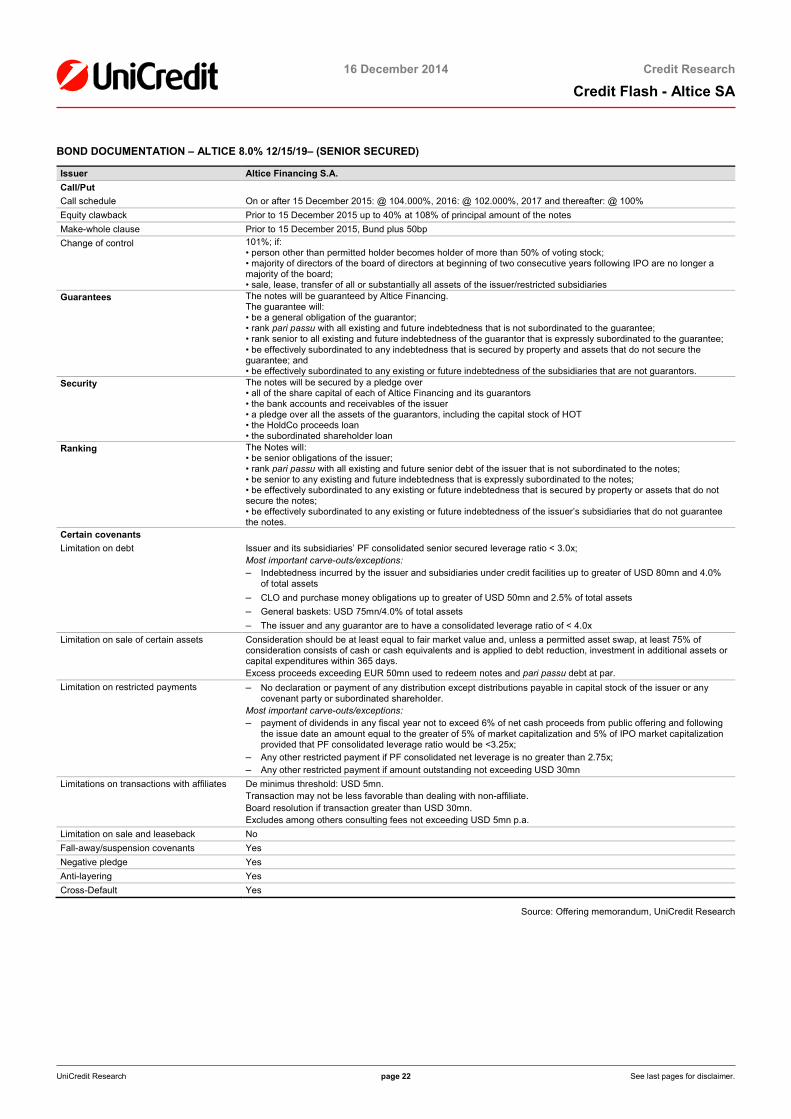

BOND DOCUMENTATION – ALTICE 8.0% 12/15/19– (SENIOR SECURED)

Issuer Altice Financing S.A. Call/Put Call schedule On or after 15 December 2015: @ 104.000%, 2016: @ 102.000%, 2017 and thereafter: @ 100% Equity clawback Prior to 15 December 2015 up to 40% at 108% of principal amount of the notes Make-whole clause Prior to 15 December 2015, Bund plus 50bp Change of control 101%; if:

• person other than permitted holder becomes holder of more than 50% of voting stock; • majority of directors of the board of directors at beginning of two consecutive years following IPO are no longer a majority of the board; • sale, lease, transfer of all or substantially all assets of the issuer/restricted subsidiaries

Guarantees The notes will be guaranteed by Altice Financing. The guarantee will: • be a general obligation of the guarantor; • rank pari passu with all existing and future indebtedness that is not subordinated to the guarantee; • rank senior to all existing and future indebtedness of the guarantor that is expressly subordinated to the guarantee; • be effectively subordinated to any indebtedness that is secured by property and assets that do not secure the guarantee; and • be effectively subordinated to any existing or future indebtedness of the subsidiaries that are not guarantors.

Security The notes will be secured by a pledge over • all of the share capital of each of Altice Financing and its guarantors • the bank accounts and receivables of the issuer • a pledge over all the assets of the guarantors, including the capital stock of HOT • the HoldCo proceeds loan • the subordinated shareholder loan

Ranking The Notes will: • be senior obligations of the issuer; • rank pari passu with all existing and future senior debt of the issuer that is not subordinated to the notes; • be senior to any existing and future indebtedness that is expressly subordinated to the notes; • be effectively subordinated to any existing or future indebtedness that is secured by property or assets that do not secure the notes; • be effectively subordinated to any existing or future indebtedness of the issuer’s subsidiaries that do not guarantee the notes.

Certain covenants Limitation on debt Issuer and its subsidiaries’ PF consolidated senior secured leverage ratio < 3.0x;

Most important carve-outs/exceptions: – Indebtedness incurred by the issuer and subsidiaries under credit facilities up to greater of USD 80mn and 4.0%

of total assets – CLO and purchase money obligations up to greater of USD 50mn and 2.5% of total assets – General baskets: USD 75mn/4.0% of total assets – The issuer and any guarantor are to have a consolidated leverage ratio of < 4.0x

Limitation on sale of certain assets Consideration should be at least equal to fair market value and, unless a permitted asset swap, at least 75% of consideration consists of cash or cash equivalents and is applied to debt reduction, investment in additional assets or capital expenditures within 365 days. Excess proceeds exceeding EUR 50mn used to redeem notes and pari passu debt at par.

Limitation on restricted payments – No declaration or payment of any distribution except distributions payable in capital stock of the issuer or any covenant party or subordinated shareholder.

Most important carve-outs/exceptions: – payment of dividends in any fiscal year not to exceed 6% of net cash proceeds from public offering and following

the issue date an amount equal to the greater of 5% of market capitalization and 5% of IPO market capitalization provided that PF consolidated leverage ratio would be <3.25x;

– Any other restricted payment if PF consolidated net leverage is no greater than 2.75x; – Any other restricted payment if amount outstanding not exceeding USD 30mn

Limitations on transactions with affiliates De minimus threshold: USD 5mn. Transaction may not be less favorable than dealing with non-affiliate. Board resolution if transaction greater than USD 30mn. Excludes among others consulting fees not exceeding USD 5mn p.a.

Limitation on sale and leaseback No Fall-away/suspension covenants Yes Negative pledge Yes Anti-layering Yes Cross-Default Yes

Source: Offering memorandum, UniCredit Research

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 23 See last pages for disclaimer.

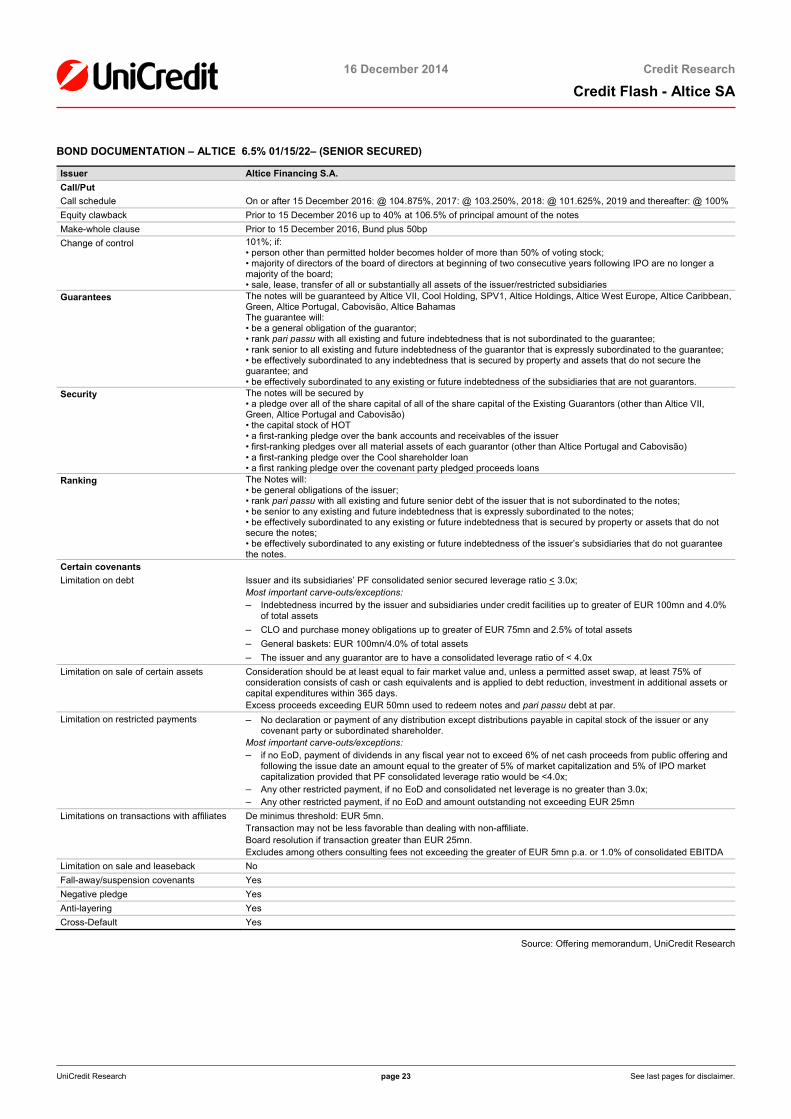

BOND DOCUMENTATION – ALTICE 6.5% 01/15/22– (SENIOR SECURED)

Issuer Altice Financing S.A. Call/Put Call schedule On or after 15 December 2016: @ 104.875%, 2017: @ 103.250%, 2018: @ 101.625%, 2019 and thereafter: @ 100% Equity clawback Prior to 15 December 2016 up to 40% at 106.5% of principal amount of the notes Make-whole clause Prior to 15 December 2016, Bund plus 50bp Change of control 101%; if:

• person other than permitted holder becomes holder of more than 50% of voting stock; • majority of directors of the board of directors at beginning of two consecutive years following IPO are no longer a majority of the board; • sale, lease, transfer of all or substantially all assets of the issuer/restricted subsidiaries

Guarantees The notes will be guaranteed by Altice VII, Cool Holding, SPV1, Altice Holdings, Altice West Europe, Altice Caribbean, Green, Altice Portugal, Cabovisão, Altice Bahamas The guarantee will: • be a general obligation of the guarantor; • rank pari passu with all existing and future indebtedness that is not subordinated to the guarantee; • rank senior to all existing and future indebtedness of the guarantor that is expressly subordinated to the guarantee; • be effectively subordinated to any indebtedness that is secured by property and assets that do not secure the guarantee; and • be effectively subordinated to any existing or future indebtedness of the subsidiaries that are not guarantors.

Security The notes will be secured by • a pledge over all of the share capital of all of the share capital of the Existing Guarantors (other than Altice VII, Green, Altice Portugal and Cabovisão) • the capital stock of HOT • a first-ranking pledge over the bank accounts and receivables of the issuer • first-ranking pledges over all material assets of each guarantor (other than Altice Portugal and Cabovisão) • a first-ranking pledge over the Cool shareholder loan • a first ranking pledge over the covenant party pledged proceeds loans

Ranking The Notes will: • be general obligations of the issuer; • rank pari passu with all existing and future senior debt of the issuer that is not subordinated to the notes; • be senior to any existing and future indebtedness that is expressly subordinated to the notes; • be effectively subordinated to any existing or future indebtedness that is secured by property or assets that do not secure the notes; • be effectively subordinated to any existing or future indebtedness of the issuer’s subsidiaries that do not guarantee the notes.

Certain covenants Limitation on debt Issuer and its subsidiaries’ PF consolidated senior secured leverage ratio < 3.0x;

Most important carve-outs/exceptions: – Indebtedness incurred by the issuer and subsidiaries under credit facilities up to greater of EUR 100mn and 4.0%

of total assets – CLO and purchase money obligations up to greater of EUR 75mn and 2.5% of total assets – General baskets: EUR 100mn/4.0% of total assets – The issuer and any guarantor are to have a consolidated leverage ratio of < 4.0x

Limitation on sale of certain assets Consideration should be at least equal to fair market value and, unless a permitted asset swap, at least 75% of consideration consists of cash or cash equivalents and is applied to debt reduction, investment in additional assets or capital expenditures within 365 days. Excess proceeds exceeding EUR 50mn used to redeem notes and pari passu debt at par.

Limitation on restricted payments – No declaration or payment of any distribution except distributions payable in capital stock of the issuer or any covenant party or subordinated shareholder.

Most important carve-outs/exceptions: – if no EoD, payment of dividends in any fiscal year not to exceed 6% of net cash proceeds from public offering and

following the issue date an amount equal to the greater of 5% of market capitalization and 5% of IPO market capitalization provided that PF consolidated leverage ratio would be <4.0x;

– Any other restricted payment, if no EoD and consolidated net leverage is no greater than 3.0x; – Any other restricted payment, if no EoD and amount outstanding not exceeding EUR 25mn

Limitations on transactions with affiliates De minimus threshold: EUR 5mn. Transaction may not be less favorable than dealing with non-affiliate. Board resolution if transaction greater than EUR 25mn. Excludes among others consulting fees not exceeding the greater of EUR 5mn p.a. or 1.0% of consolidated EBITDA

Limitation on sale and leaseback No Fall-away/suspension covenants Yes Negative pledge Yes Anti-layering Yes Cross-Default Yes

Source: Offering memorandum, UniCredit Research

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 24 See last pages for disclaimer.

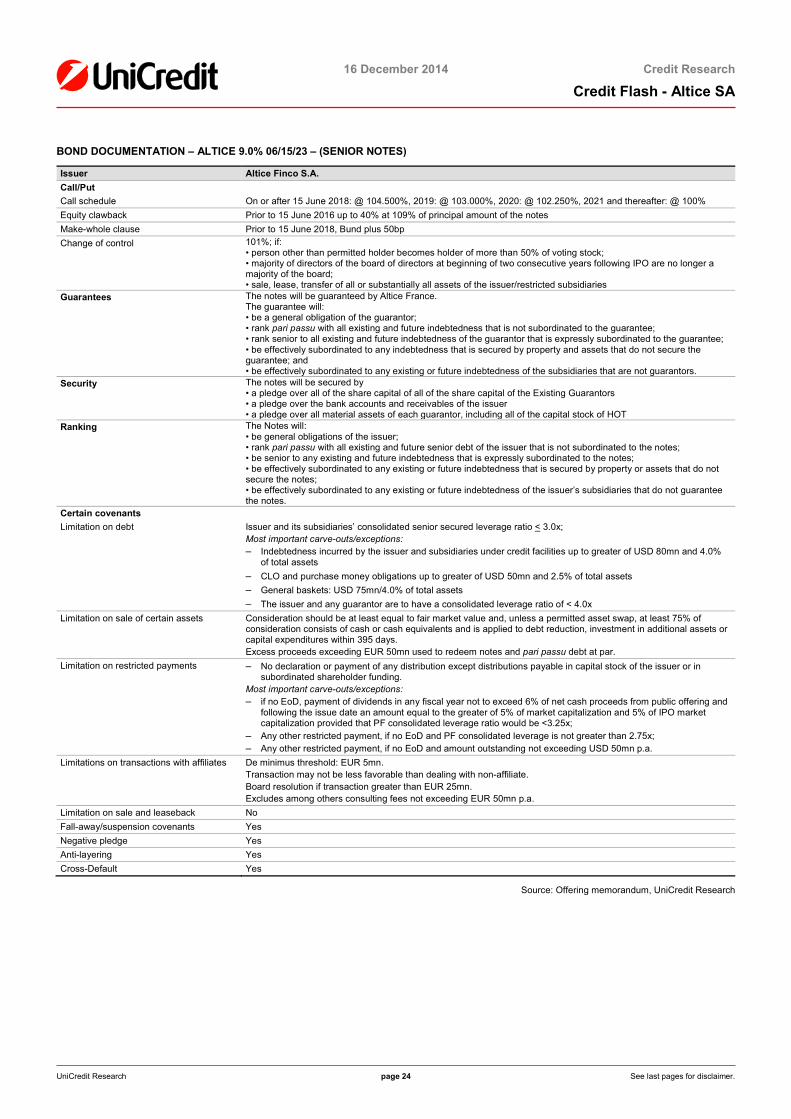

BOND DOCUMENTATION – ALTICE 9.0% 06/15/23 – (SENIOR NOTES)

Issuer Altice Finco S.A. Call/Put Call schedule On or after 15 June 2018: @ 104.500%, 2019: @ 103.000%, 2020: @ 102.250%, 2021 and thereafter: @ 100% Equity clawback Prior to 15 June 2016 up to 40% at 109% of principal amount of the notes Make-whole clause Prior to 15 June 2018, Bund plus 50bp Change of control 101%; if:

• person other than permitted holder becomes holder of more than 50% of voting stock; • majority of directors of the board of directors at beginning of two consecutive years following IPO are no longer a majority of the board; • sale, lease, transfer of all or substantially all assets of the issuer/restricted subsidiaries

Guarantees The notes will be guaranteed by Altice France. The guarantee will: • be a general obligation of the guarantor; • rank pari passu with all existing and future indebtedness that is not subordinated to the guarantee; • rank senior to all existing and future indebtedness of the guarantor that is expressly subordinated to the guarantee; • be effectively subordinated to any indebtedness that is secured by property and assets that do not secure the guarantee; and • be effectively subordinated to any existing or future indebtedness of the subsidiaries that are not guarantors.

Security The notes will be secured by • a pledge over all of the share capital of all of the share capital of the Existing Guarantors • a pledge over the bank accounts and receivables of the issuer • a pledge over all material assets of each guarantor, including all of the capital stock of HOT

Ranking The Notes will: • be general obligations of the issuer; • rank pari passu with all existing and future senior debt of the issuer that is not subordinated to the notes; • be senior to any existing and future indebtedness that is expressly subordinated to the notes; • be effectively subordinated to any existing or future indebtedness that is secured by property or assets that do not secure the notes; • be effectively subordinated to any existing or future indebtedness of the issuer’s subsidiaries that do not guarantee the notes.

Certain covenants Limitation on debt Issuer and its subsidiaries’ consolidated senior secured leverage ratio < 3.0x;

Most important carve-outs/exceptions: – Indebtedness incurred by the issuer and subsidiaries under credit facilities up to greater of USD 80mn and 4.0%

of total assets – CLO and purchase money obligations up to greater of USD 50mn and 2.5% of total assets – General baskets: USD 75mn/4.0% of total assets – The issuer and any guarantor are to have a consolidated leverage ratio of < 4.0x

Limitation on sale of certain assets Consideration should be at least equal to fair market value and, unless a permitted asset swap, at least 75% of consideration consists of cash or cash equivalents and is applied to debt reduction, investment in additional assets or capital expenditures within 395 days. Excess proceeds exceeding EUR 50mn used to redeem notes and pari passu debt at par.

Limitation on restricted payments – No declaration or payment of any distribution except distributions payable in capital stock of the issuer or in subordinated shareholder funding.

Most important carve-outs/exceptions: – if no EoD, payment of dividends in any fiscal year not to exceed 6% of net cash proceeds from public offering and

following the issue date an amount equal to the greater of 5% of market capitalization and 5% of IPO market capitalization provided that PF consolidated leverage ratio would be <3.25x;

– Any other restricted payment, if no EoD and PF consolidated leverage is not greater than 2.75x; – Any other restricted payment, if no EoD and amount outstanding not exceeding USD 50mn p.a.

Limitations on transactions with affiliates De minimus threshold: EUR 5mn. Transaction may not be less favorable than dealing with non-affiliate. Board resolution if transaction greater than EUR 25mn. Excludes among others consulting fees not exceeding EUR 50mn p.a.

Limitation on sale and leaseback No Fall-away/suspension covenants Yes Negative pledge Yes Anti-layering Yes Cross-Default Yes

Source: Offering memorandum, UniCredit Research

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 25 See last pages for disclaimer.

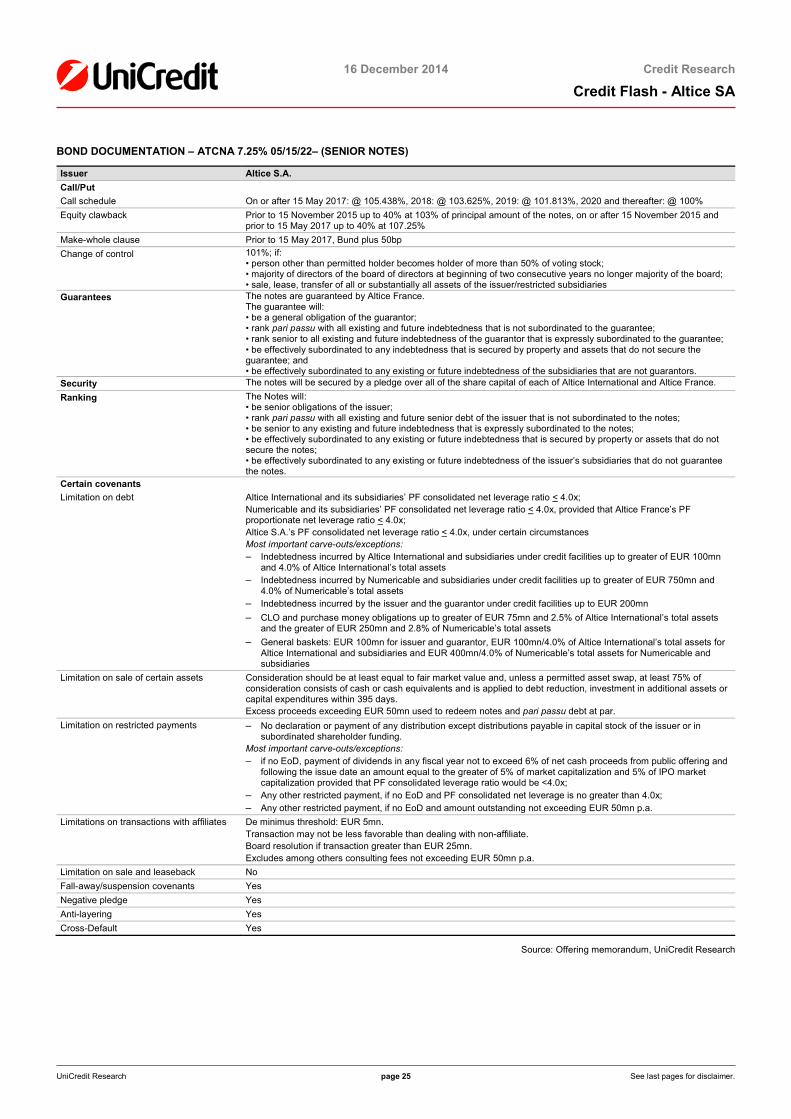

BOND DOCUMENTATION – ATCNA 7.25% 05/15/22– (SENIOR NOTES)

Issuer Altice S.A. Call/Put Call schedule On or after 15 May 2017: @ 105.438%, 2018: @ 103.625%, 2019: @ 101.813%, 2020 and thereafter: @ 100% Equity clawback Prior to 15 November 2015 up to 40% at 103% of principal amount of the notes, on or after 15 November 2015 and

prior to 15 May 2017 up to 40% at 107.25% Make-whole clause Prior to 15 May 2017, Bund plus 50bp Change of control 101%; if:

• person other than permitted holder becomes holder of more than 50% of voting stock; • majority of directors of the board of directors at beginning of two consecutive years no longer majority of the board; • sale, lease, transfer of all or substantially all assets of the issuer/restricted subsidiaries

Guarantees The notes are guaranteed by Altice France. The guarantee will: • be a general obligation of the guarantor; • rank pari passu with all existing and future indebtedness that is not subordinated to the guarantee; • rank senior to all existing and future indebtedness of the guarantor that is expressly subordinated to the guarantee; • be effectively subordinated to any indebtedness that is secured by property and assets that do not secure the guarantee; and • be effectively subordinated to any existing or future indebtedness of the subsidiaries that are not guarantors.

Security The notes will be secured by a pledge over all of the share capital of each of Altice International and Altice France. Ranking The Notes will:

• be senior obligations of the issuer; • rank pari passu with all existing and future senior debt of the issuer that is not subordinated to the notes; • be senior to any existing and future indebtedness that is expressly subordinated to the notes; • be effectively subordinated to any existing or future indebtedness that is secured by property or assets that do not secure the notes; • be effectively subordinated to any existing or future indebtedness of the issuer’s subsidiaries that do not guarantee the notes.

Certain covenants Limitation on debt Altice International and its subsidiaries’ PF consolidated net leverage ratio < 4.0x;

Numericable and its subsidiaries’ PF consolidated net leverage ratio < 4.0x, provided that Altice France’s PF proportionate net leverage ratio < 4.0x; Altice S.A.’s PF consolidated net leverage ratio < 4.0x, under certain circumstances Most important carve-outs/exceptions: – Indebtedness incurred by Altice International and subsidiaries under credit facilities up to greater of EUR 100mn

and 4.0% of Altice International’s total assets – Indebtedness incurred by Numericable and subsidiaries under credit facilities up to greater of EUR 750mn and

4.0% of Numericable’s total assets – Indebtedness incurred by the issuer and the guarantor under credit facilities up to EUR 200mn – CLO and purchase money obligations up to greater of EUR 75mn and 2.5% of Altice International’s total assets

and the greater of EUR 250mn and 2.8% of Numericable’s total assets – General baskets: EUR 100mn for issuer and guarantor, EUR 100mn/4.0% of Altice International’s total assets for

Altice International and subsidiaries and EUR 400mn/4.0% of Numericable’s total assets for Numericable and subsidiaries

Limitation on sale of certain assets Consideration should be at least equal to fair market value and, unless a permitted asset swap, at least 75% of consideration consists of cash or cash equivalents and is applied to debt reduction, investment in additional assets or capital expenditures within 395 days. Excess proceeds exceeding EUR 50mn used to redeem notes and pari passu debt at par.

Limitation on restricted payments – No declaration or payment of any distribution except distributions payable in capital stock of the issuer or in subordinated shareholder funding.

Most important carve-outs/exceptions: – if no EoD, payment of dividends in any fiscal year not to exceed 6% of net cash proceeds from public offering and

following the issue date an amount equal to the greater of 5% of market capitalization and 5% of IPO market capitalization provided that PF consolidated leverage ratio would be <4.0x;

– Any other restricted payment, if no EoD and PF consolidated net leverage is no greater than 4.0x; – Any other restricted payment, if no EoD and amount outstanding not exceeding EUR 50mn p.a.

Limitations on transactions with affiliates De minimus threshold: EUR 5mn. Transaction may not be less favorable than dealing with non-affiliate. Board resolution if transaction greater than EUR 25mn. Excludes among others consulting fees not exceeding EUR 50mn p.a.

Limitation on sale and leaseback No Fall-away/suspension covenants Yes Negative pledge Yes Anti-layering Yes Cross-Default Yes

Source: Offering memorandum, UniCredit Research

16 December 2014 Credit Research

Credit Flash - Altice SA

UniCredit Research page 26