WeiserMazars LLP is an independent member firm of Mazars Group. WEISERMAZARS LLP Alternative Financing Solutions to Grow Your Business Fred M. Kaplan, MBA, CBM - Director October 16, 2013 TRUE CLARITY IS NATURALLY RARE A mirror-like, or specular reflection occurs in nature only when the angle at which the incident of light touches a surface, equals the angle at which it is reflected.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WeiserMazars LLP is an independent member firm of Mazars Group.

W E I S E R M A Z A R S L L PAlternative Financing Solutions to Grow Your Business

Fred M. Kaplan, MBA, CBM - DirectorOctober 16, 2013

TRUE CLARITY IS NATURALLY RARE

A mirror-like, or specular reflection occurs in nature only when the angle at which the incident of light touches a surface, equals the angle at which it is reflected.

C R E D E N T I A L S

2

Drexel MBA in Finance Former Controller & CFO Former President of KFCG– Loan Brokers & Borrower Advocates

(Conventional, Govt. Guaranteed, Alternative)– Network of Over 100 Bank & Non-Bank Lenders

3

A L T E R N A T I V E F I N A N C E S O L U T I O N S

Government Guaranteed Loan Programs

Accounts Receivable Factoring

Purchase Order Financing

Unsecured Business Credit

Merchant Cash Advance

G O V E R N M E N T G U A R A N T E E D L O A N S

4

S B A P R O G R A M S

Available Loan Term 25 Years 20 Years

5

SBA 7(a) SBA 504

Eligible Business For Profit For Profit

Eligibility Criteria

Sales & Employee Limits By Industry Net Worth < $15 million,NIAT < $5.0 Million

Maximum Loan Amount $5 Million $5 million ($5.5 million for Mfg., Energy &

High Impact)

Loan Guarantee 75% / Maximum of $3.750 Million

Non-guaranteed First Mortgage to 50% of Costs; 40% CDC Second Mortgage

Interest Rates Negotiable to NYP + 2.75%or 1 Mo. LIBOR + 300bps + 2.75%

Negotiable First Mortgage; Fixed Below Market CDC Second Mortgage

Fees 2% - 3.75% of Guaranteed Portion Fees Approximately 3% of CDC Loan Amount

S B A P R O G R A M S

6

SBA 7(a) SBA 504

Collateral 100% Liquidated LTV or all available Collateral (Can be a collateral deficiency)

90% LTV(Some exceptions apply)

Prepayment Penalties

Loan Maturities > 15 Years(Year 1 = 5%, Year 2 = 3%, Year 3 = 1%)

10 Year Loans = 4 YRS20 YR Loans = 10 YRS

(Declining based on debenture rate)

S B A L O A N S : U S E O F P R O C E E D S

7

SBA 7(a) SBA 504

Acquisition of Real Estate P PLeasehold Improvements P P

Equipment P PRefinance Debt P PWorking capital P

Inventory P Business Acquisition P

Transaction Costs P P

C O N V E N T I O N A L V S . S B A 7 ( A )

8

Profitability Measured primarily by Net Interest Margin & Deposits

Measured primarily by Net Interest Margin (Retailed Portion of loan)/ Non interest feeIncome (Secondary Market Sale)/ Loan Servicing Income & Deposits

Conventional Loan SBA 7(a) Loan

Interest Rate Variable or Fixed Rate Primary Rate based on NYP or LIBOR

Term Maturity

FFM&E: 5-7 Year TermReal Estate: 5-10 Year Term with Balloon

Working Capital: Up to 10 Year TermFFM&E: Useful Life Up to 15 Year TermReal Estate: 25 Year Term with no Balloon

Amortization FFM&E: Typically fully amortizedReal Estate: 15- 25 years amortization

FFM&E & Real Estate: Fully Amortized (No Balloons)

Collateral Typically fully collateralized based on discounted collateral values

Absence of full collateral coverage based on discounted collateral value is acceptable. Loan guarantee covers collateral shortfall.

Covenants Typical for C&I and real estate Transactions Acceptable based on lender approval

Fees Varies based on loan type and competitive factors Agency Loan Guarantee Fee

S B A 7 ( A ) B E N E F I T S

9

•Longer Term Financing7 - 10 Years - Working Capital10 - 15 Years (Useful Life) - M&E25 Years - Real Estate•No Balloon Provisions•Reduction in Equity and Collateral Requirements•Consolidate Loan Components (Weighted-Average Term)

Lower Monthly PaymentsImproved Cash Flow

S B A 7 ( A ) L O A N P A Y M E N T C O M P A R I S O N

10

AmountConventional

- (3 Loans)Real Estate Loan $ 500,000 20Equipment Loan $ 350,000 3Working Capital $ 150,000 1Total $ 1,000,000 Rate 5.50%

SBA 7(a) - (1-Loan)

25 10 10

17.5 Blended Term Prime + 2.75%

Assumptions Loan Term - Years

Loan Payments Conventional Loan

Monthly PmtAnnual Debt

ServiceReal Estate Loan $ 3,439 $ 41,273 Equipment Loan $ 10,569 $ 126,823 WC - I/O $ 8,250 $ 99,000 WC - Principal Due at Maturity $ 150,000 Total - 3 Loans $ 22,258 $ 267,096

SBA 7(a) Loan

Monthly

Pmt

Annual Debt

Service

Total - 1 Loan $ 7,702 $ 92,429

Reduction in Annual Debt Service $(174,667) -65.4%

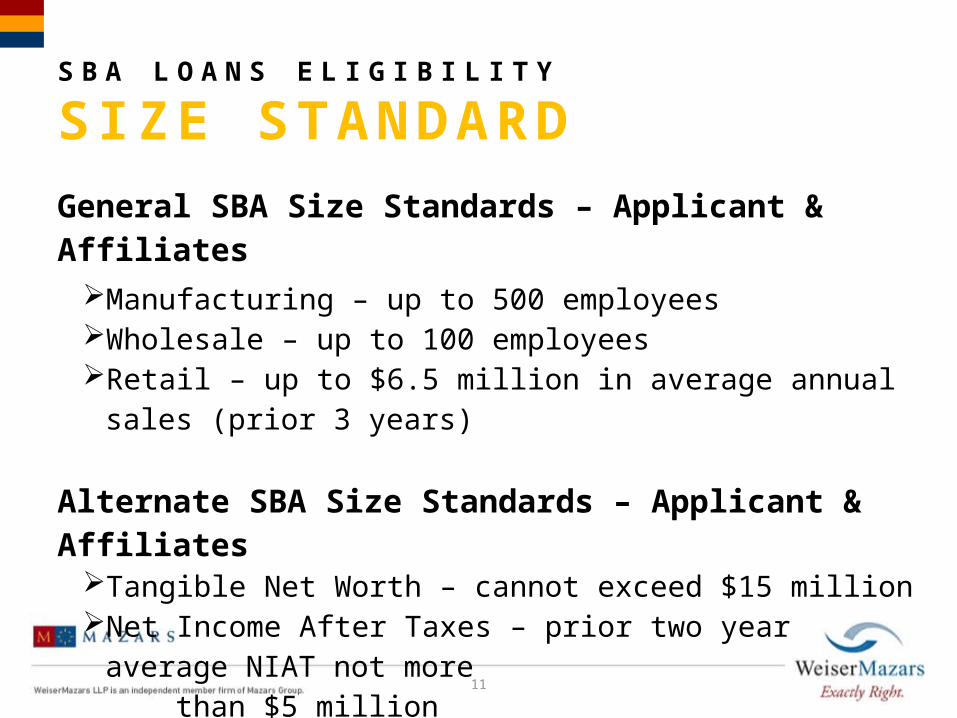

S B A L O A N S E L I G I B I L I T Y

S I Z E S TA N D A R D

11

General SBA Size Standards – Applicant & AffiliatesManufacturing – up to 500 employeesWholesale – up to 100 employeesRetail – up to $6.5 million in average annual sales (prior 3 years)

Alternate SBA Size Standards – Applicant & AffiliatesTangible Net Worth – cannot exceed $15 millionNet Income After Taxes – prior two year average NIAT not more

than $5 million

S B A L O A N S E L I G I B I L I T Y

G U A R A N T E E S & L I Q U I D I T Y

12

• The Personal Guaranty of all Principals with a 20% or greater ownership interest is required.• Personal Liquid Resources of all guarantors

based on the loan size: Loans < $250,000 – Maximum of 2x the loan amount

or $100,000; whichever is greater, Loans of $250,000 to $500,000 – Maximum of 1.5x

the loan amount or $500,000; whichever is greater, Loans > $500,000 – Maximum of 1x the loan amount

or $750,000, whichever is greater.

A C C O U N T S R E C E I V A B L E F I N A N C I N G

13

P U R P O S E O F A R F I N A N C I N G

14

• Offer credit terms to customers• Fund payroll, pay suppliers and vendors, rent, utilities

Finance the day-to-day operations of the company while waiting for business customers to pay their invoices

F A C T O R I N G

15

The discounted sale of accounts receivable to raise cash for daily expenses

Not credit driven

Simpler to use than a credit line

Finance day-to-day business expenses without

debt

Better than a

loan, for many

growing companies

F A C T O R I N G T E R M S

16

Advance Rate: % the Factor will initially advance for eligible invoices (70-90%)

Reserve: amount the factor will hold back until invoices are paid (inverse of Advance Rate)

Discount Rate: Factor’s fee (1.5% - 4.0%) Turn: Average days customers take to pay their invoices. Notification/Non-Notification: To inform or not to inform

customers Recourse/Non-Recourse: Whether the factor returns

uncollected invoices to the client (usually > 90 days)

T R A D I T I O N A L F A C T O R I N G ( N O N - R E C O U R S E )

17

Prior to shipping,/providing services, client seeks credit approval from Factor **

Client invoices customers (Account Debtors) for goods or services

Factor advances 70%-to 90% of invoice to client, most commonly 80%, in 24 hours

Factor collects the invoiced amount from the Account Debtor

Factor releases the reserve, less its fee for service (1.5 – 4.0% every 30 days)

D I S C O U N T F A C T O R I N G ( R E C O U R S E )

18

Client invoices customers (Account Debtors) for goods or services, sends copy to Factor

Factor advances 70%-to 90% of invoices, most commonly 80%, in 24 hours

Factor collects the invoiced amounts from the Account Debtors

Factor pays it’s client the balance not advanced from those invoices, less its fee for service (1.5 – 4.0% every 30 days)

Invoices not collected in 90 days are returned to the client for collection. The advance is reversed on the client’s account.

B A N K L I N E E X A M P L E

$200K AR$100K eligible (aged under 90 days)

$50K aged 1-30 @ 65% = 32,500$30K aged 31-60 @ 55% = 16,500$20K aged 61-90 @ 45% = 9,000Total =

58,000

Cost /month@ 0.5% (6% APR) = $290

19

F A C T O R I N G E X A M P L E

$200K AR$100K eligible (aged under 90

days)

$100K @ 80% = 80,000

Cost/month @ 2% fee = $1,600

20

W I T H F A C T O R I N G F A C I L I T Y …

No balance sheet debt Smaller, less expensive accounting function– No monthly reporting to lender– Factoring company reports to client every month, or in real

time. Factor becomes the company Credit & Collection Dept.– Client receives a complete professional commercial credit

team, which he/she could never afford to hire.

21

W I T H F A C T O R I N G F A C I L I T Y …

Allows business owner and staff to:– Concentrate on producing products and services– Getting and keeping customers– Without having to engage in administrative activities in

which they have no skills, no interest. Enables client company to greatly expand market

area and efforts, without having to worry about whether or not customers will pay.

Examples: Driller, Consultant

22

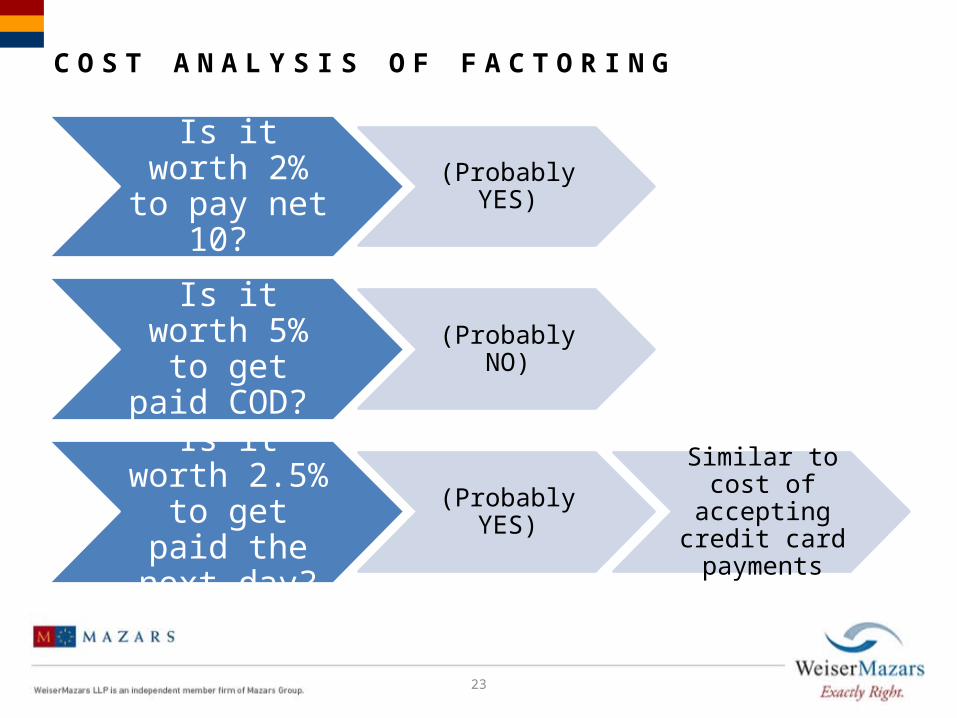

C O S T A N A L Y S I S O F F A C T O R I N G

23

Is it worth 2% to pay net 10?

(Probably YES)

Is it worth 5% to get paid

COD? (Probably NO)

Is it worth 2.5% to get paid the

next day?(Probably YES)

Similar to cost of accepting credit card payments

P U R C H A S E O R D E R F I N A N C I N G

24

P U R C H A S E O R D E R F I N A N C I N G

25

Company receives large order

PO funder advances funds to produce goods, accepting production risk

Merchandise shipped to customer, invoice cut by company

Factor purchases invoice, accepting collection risk, advances funds to company, takes out PO funder

Factor receives invoice payment from account debtor, remits reserve (less fee) to client

R E S U L T O F P O F I N A N C I N G

26

Customer gets to accept orders otherwise not possible

Company can grow beyond what a bank would allow and enable

PO Financing can be advanced as a Standby Letter of Credit for importing of merchandise

Examples: Bedding Manufacturer, Purchasing Agent

Q U A L I F I C A T I O N S

27

Must reflect a

reasonable profit

margin

May finance

purchase of finished goods or

WIP (more expensive)

Order will be shipped all at once.

This financing

not available for

inventory on shelf for future sale.

U N S E C U R E D B U S I N E S S L O A N

28

U N S E C U R E D B U S I N E S S L O A N

29

• Business Expansion• Pay bills• Purchase additional inventory• Buy out business partner• Purchase commercial equipment• Infusion of working capital• Examples: Startups, Medical device

manufacturer

Why:

U B L R E Q U I R E M E N T S

30

• 650 credit score on all three bureaus. Not just the middle score.

Quality Personal Credit

• Personal or Business credit reports

No Bankruptcy’s

• Late pays, Collections, Judgments, Liens

Business can not have had in the last 3 years:

U B L P A R A M E T E R S

31

Funding in 1 day to 4 weeks depending upon the transaction

Pricing ranges from Prime +2 to Prime +8

• Checkbook credit line, 2 to 7-year terms depending on credit and dollar amountIf two years TIB:

• Business Credit Cards at 0% first-year interestIf start-up:

W E I S E R M A Z A R S L L P

A full-service firm with national focus and international reach

Since 1921, WeiserMazars LLP has provided a unique combination of foresight and experience when fulfilling client needs in accounting, tax and advisory services. Whether on the local level or internationally, the firm guides clients through their day-to-day operations and works with them to ensure they have the right financial structure in place to meet their business goals. Our reputation for integrity and quality has been earned by providing our clients with proactive, value-added guidance at every stage of the business lifecycle. Defining features of our firm include:

Over 100 partners and more than 700 professionals in six U.S. offices located in New York, New York, Long Island, NY, Metropark, NJ, Philadelphia, PA, Chicago, IL and West Palm Beach, Florida

Named one of the top accounting firms in the country by Accounting Today in 2013

An integrated, customized approach – Our full service platform integrates accounting, auditing, tax and advisory services seamlessly to best address the critical issues our clients face

Focused industry training – our team members at all levels receive specialized industry training so that they are familiar with a client’s total business environment

We specialize in providing audit, consulting and transaction services to local, national and international financial organizations including insurance companies, banks, broker-dealers and real estate organizations.

International Capability

We are the independent U.S. member firm of Mazars Group, one of the world’s most prominent international accounting, audit, tax and advisory services organizations with:

Access to nearly 14,000 professionals in more than 70 countries on six continents International reach uncommon in firms with such an intense focus on coordinated, client-centric

service Expertise on global issues, cultures and techniques

32

Related Documents