PowerPoint Presentation by LuAnn Bean Professor of Accounting Florida Institute of Technology Allocating Costs To Responsibility Centers CHAPTER 13 © 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use. Managerial Accounting 11E Maher/Stickney/Weil

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PowerPoint Presentation by

LuAnn BeanProfessor of AccountingFlorida Institute of Technology

Allocating Costs To Responsibility

Centers

CHAPTER 13

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in

part, except for use as permitted in a license distributed with a certain product or service or

otherwise on a password-protected website for classroom use.

Managerial Accounting 11E

Maher/Stickney/Weil

CHAPTER GOALChapter 13 discusses concepts and methods

of assigning indirect costs such as overhead, to departments. Additionally, service department cost allocation and joint-process cost allocation are explained.

☼ ☼

DIRECT COST: Definition

Is one that firms can identify specifically with, or trace

directly to a particular product, department, or process.

LO 1

INDIRECT COST: Definition

Results from joint use of a facility or service by several

products, departments, or processes.

LO 1

What are common costs?

Common costs are indirect costs that cannot be

identified by a cost object.

LO 1MANAGERS WANT TO KNOW!

Why allocate indirect costs to products?

Full product costs should be known, including

allocated indirect costs, for pricing and planning

decisions.

LO 1MANAGERS WANT TO KNOW!

SERVICE DEPARTMENT

Service department costs, a source of indirect costs, should be charged to users because:¯These costs should be covered by the

contribution margin of revenue-generating departments

¯User departments must be aware of what costs their department must cover

¯User departments should not treat service departments as if they are free

LO 2

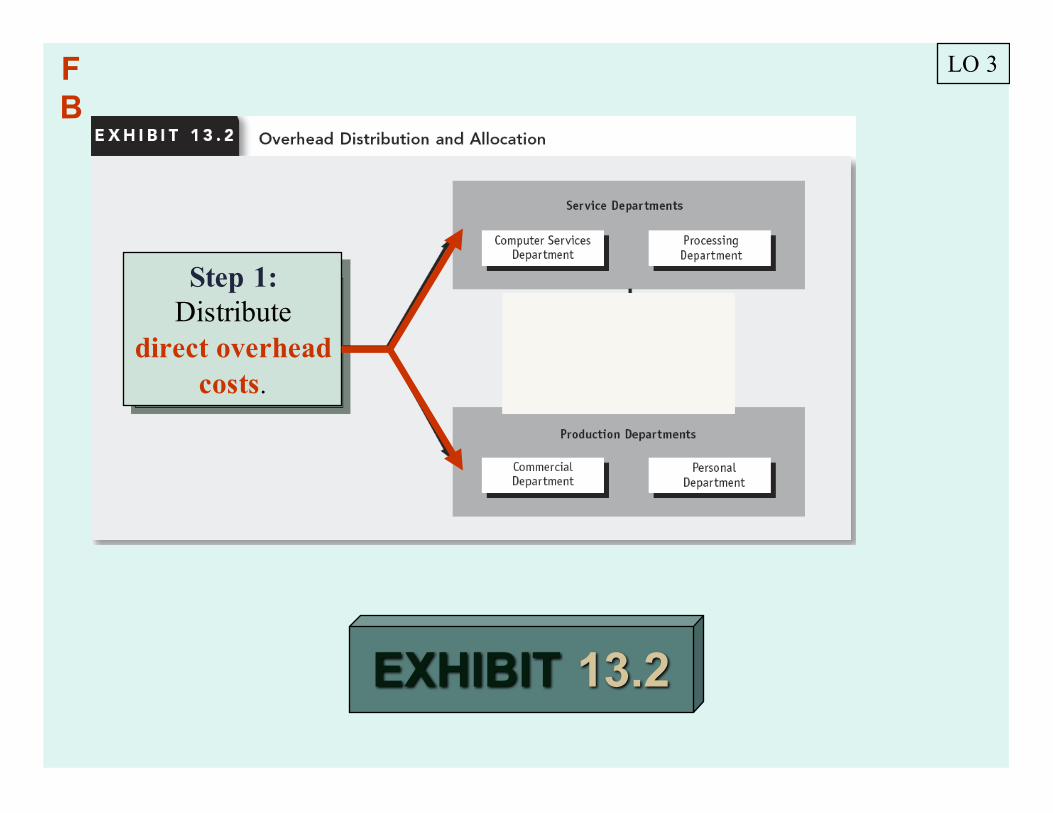

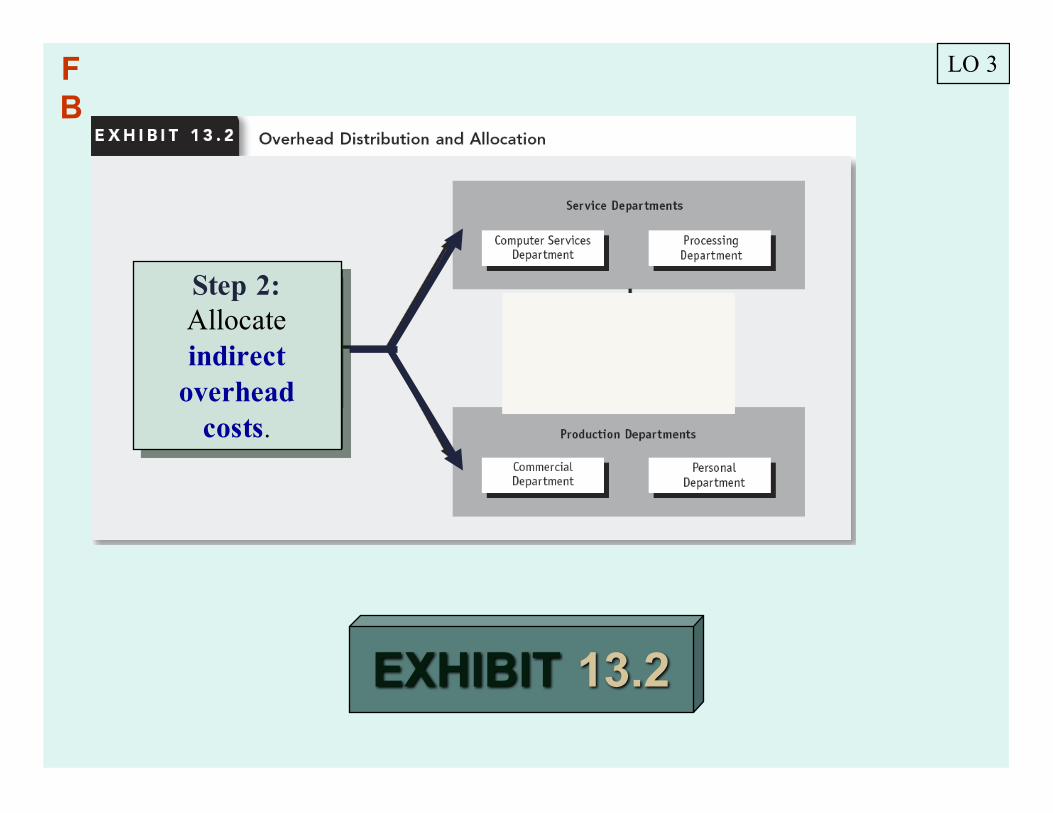

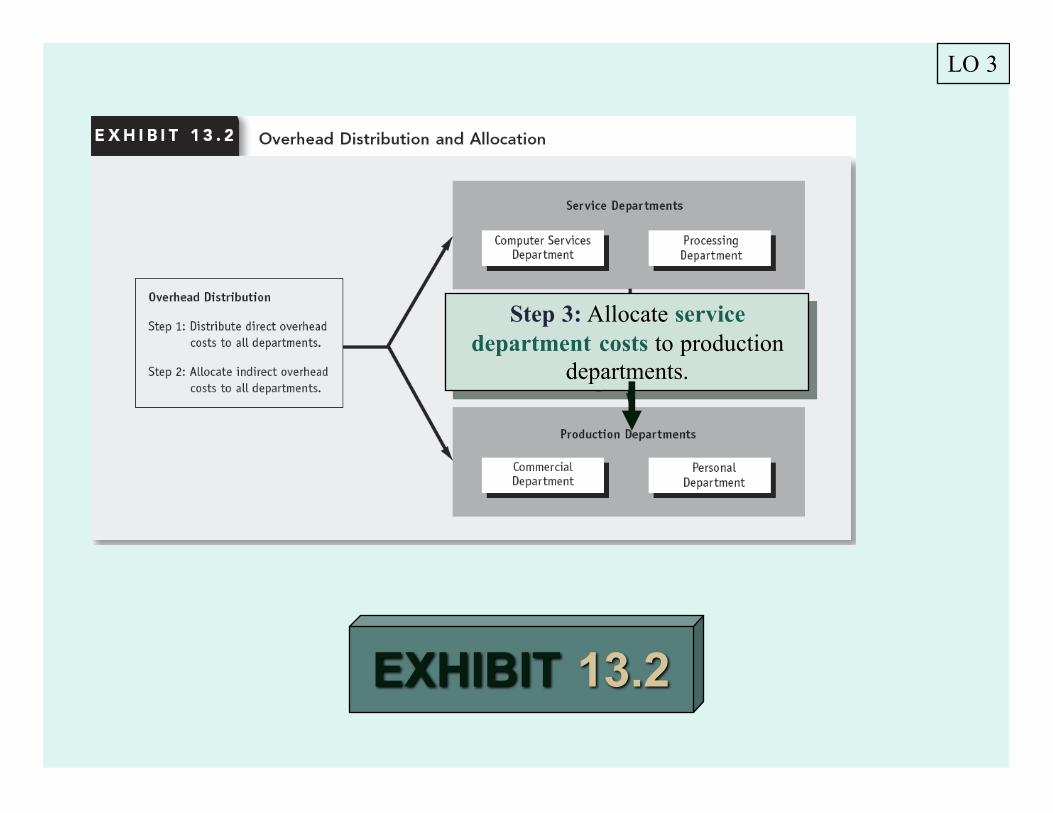

COST ALLOCATION

The cost allocation process has three steps:1) Assign direct costs to departments2) Allocate indirect costs to departments3) Allocate service department costs to

production departments

LO 3

EXAMPLE: First Bank

First Bank (FB) has 4 departments. Productiondepartments are the Commercial Department and the Personal Department. Servicedepartments are Computer Services and Processing.

Indirect costs are allocated to each department. Service department costs are allocated to

production departments in order to properly price their products.

LO 3

Continued

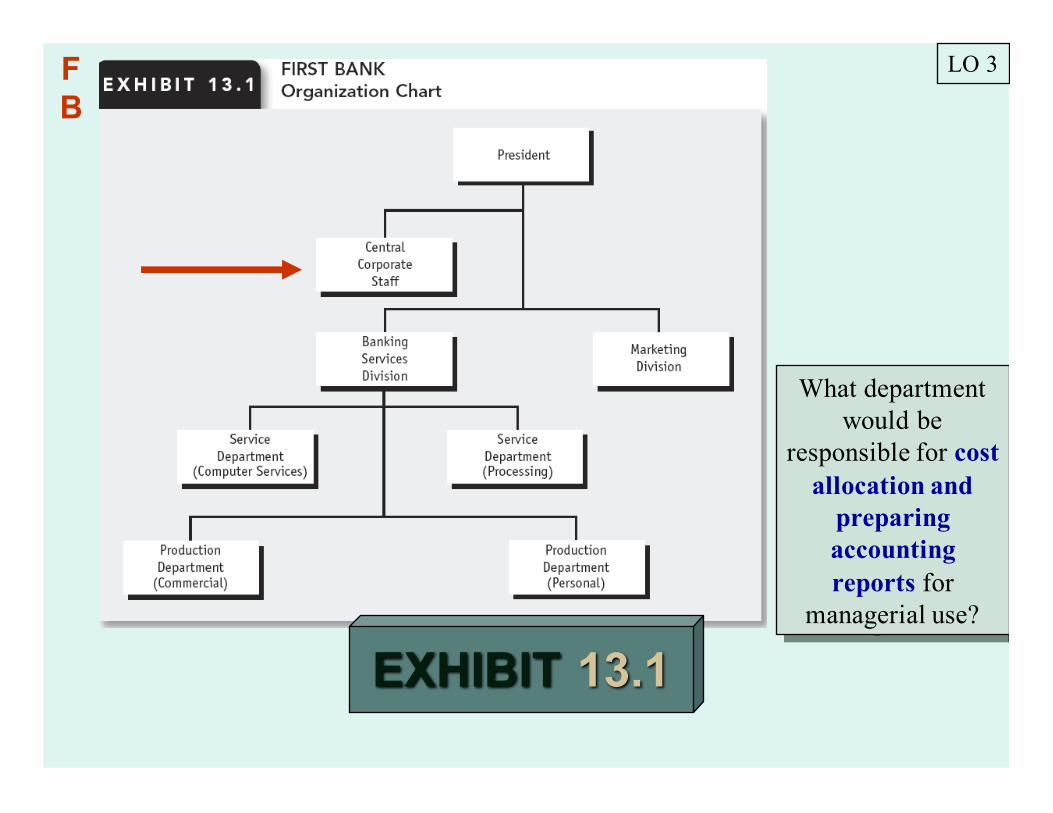

FB

EXHIBIT 13.1

LO 3

What department would be

responsible for cost allocation and

preparing accounting reports for

managerial use?

FB

EXHIBIT 13.2

LO 3

Step 1:Distribute

direct overhead costs.

FB

EXHIBIT 13.2

LO 3

Step 2:Allocate indirect

overhead costs.

FB

ALLOCATION

First Bank has four indirect costs: security, property taxes, rent and utilities and miscellaneous. When allocating indirect costs, First Bank must select a cost driver for each indirect cost, although miscellaneous costs may not have a cost driver.

LO 3FB

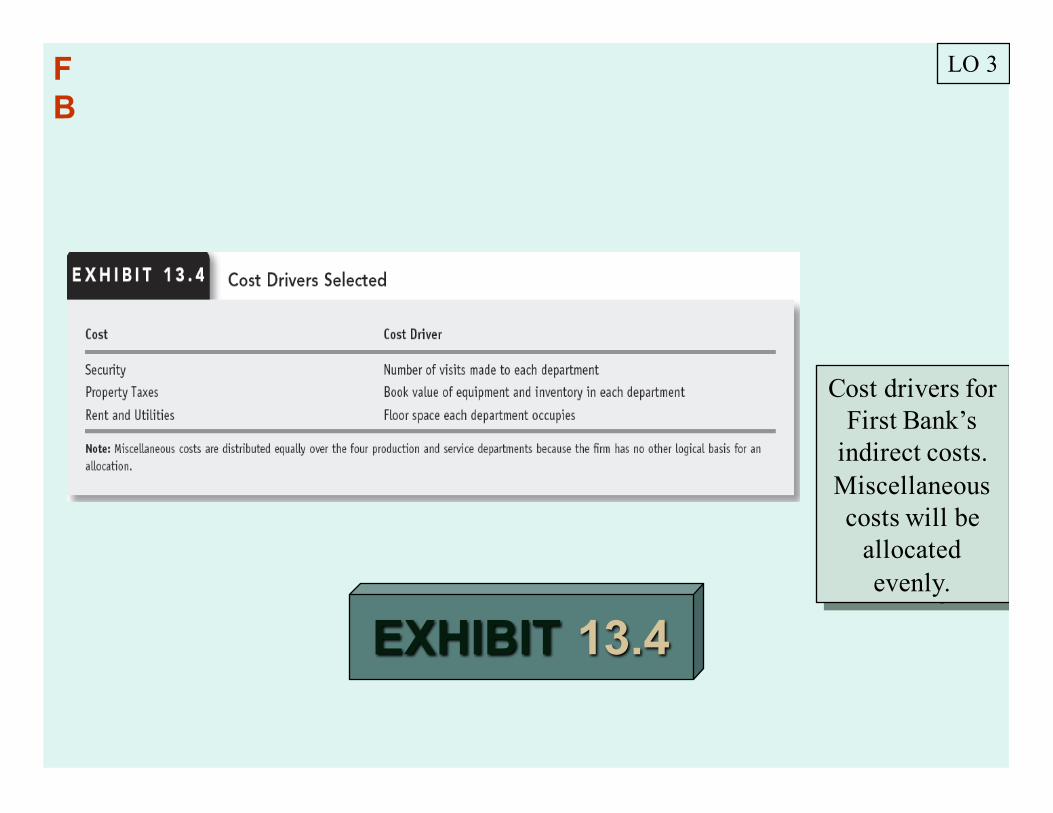

EXHIBIT 13.4

LO 3

Cost drivers for First Bank’s

indirect costs. Miscellaneous costs will be

allocated evenly.

FB

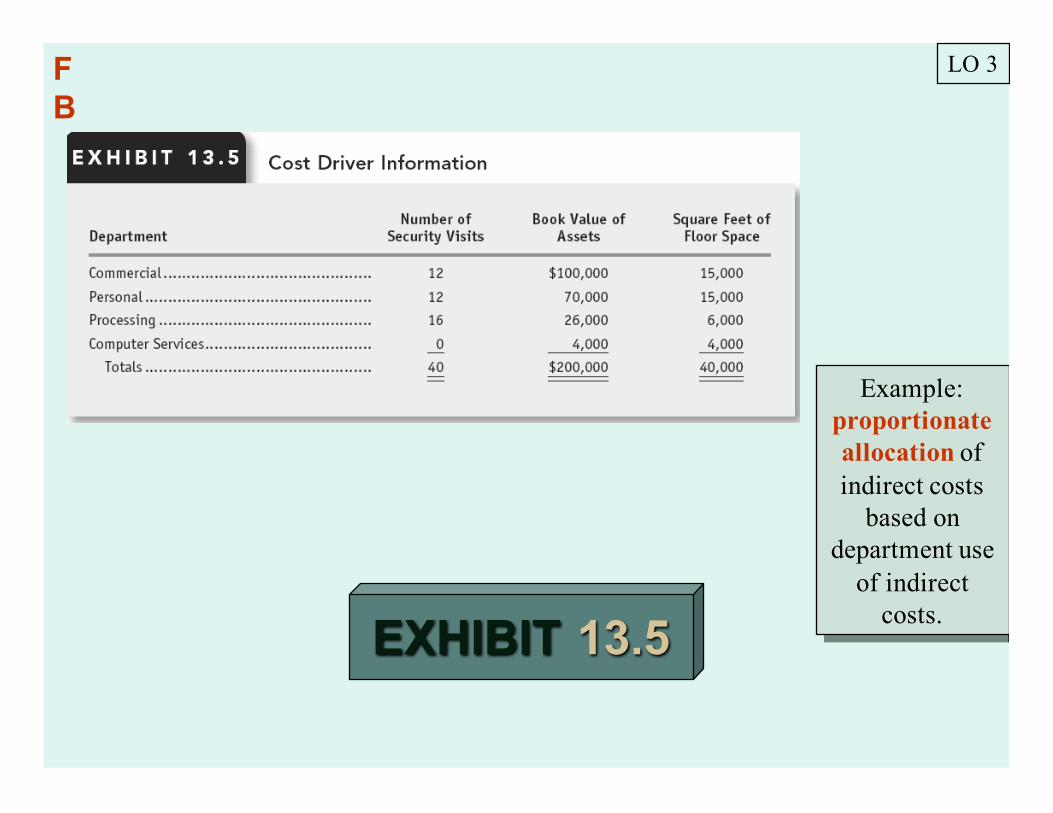

EXHIBIT 13.5

LO 3

Example: proportionate allocation of indirect costs

based on department use

of indirect costs.

FB

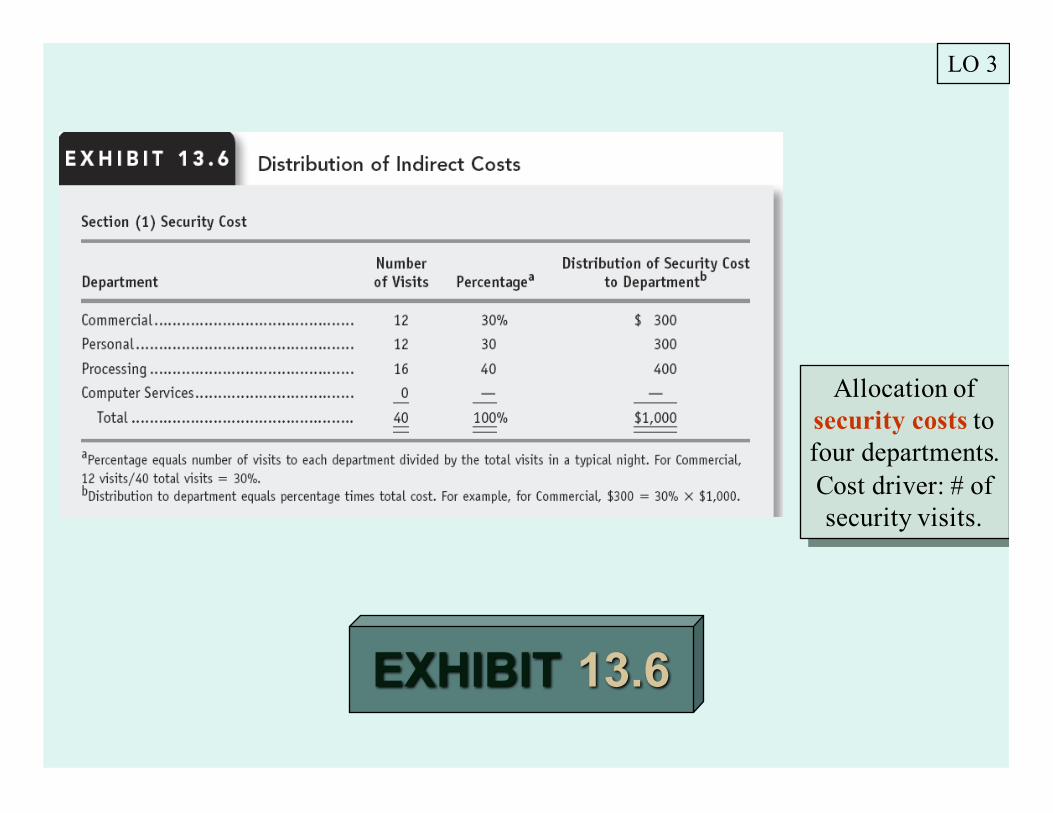

EXHIBIT 13.6

LO 3

Allocation of security costs to four departments. Cost driver: # of security visits.

EXHIBIT 13.6

LO 3

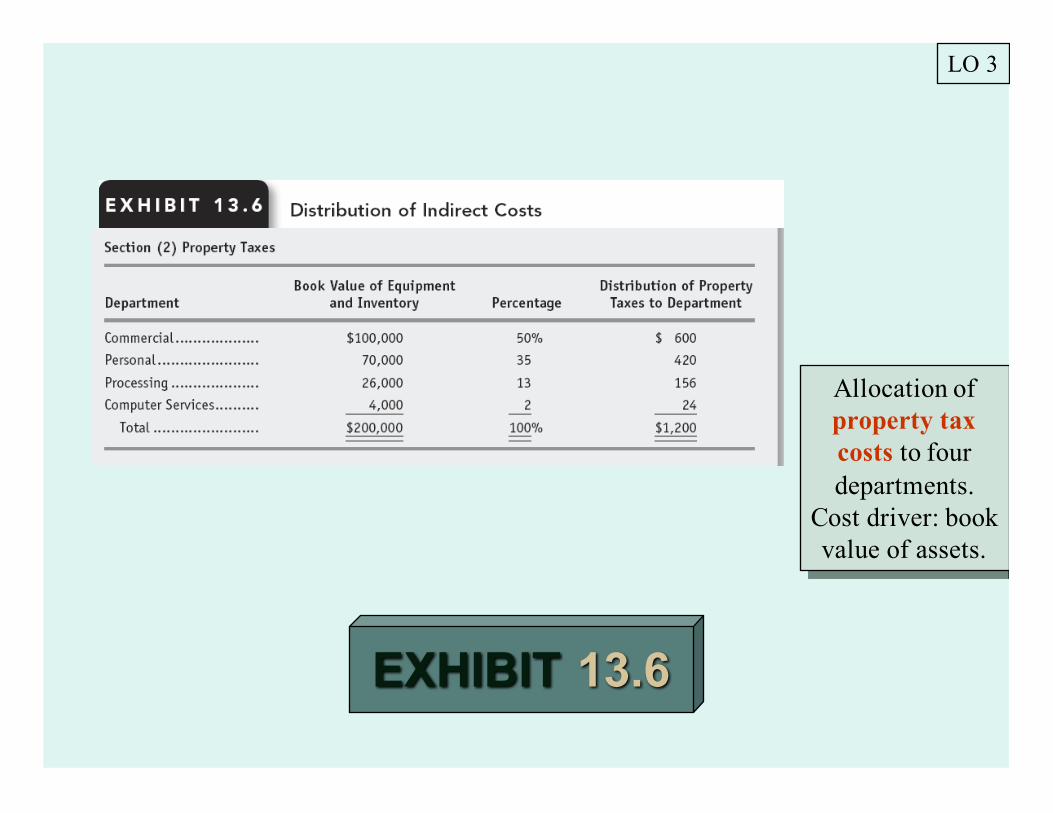

Allocation of property tax costs to four departments.

Cost driver: book value of assets.

EXHIBIT 13.6

LO 3

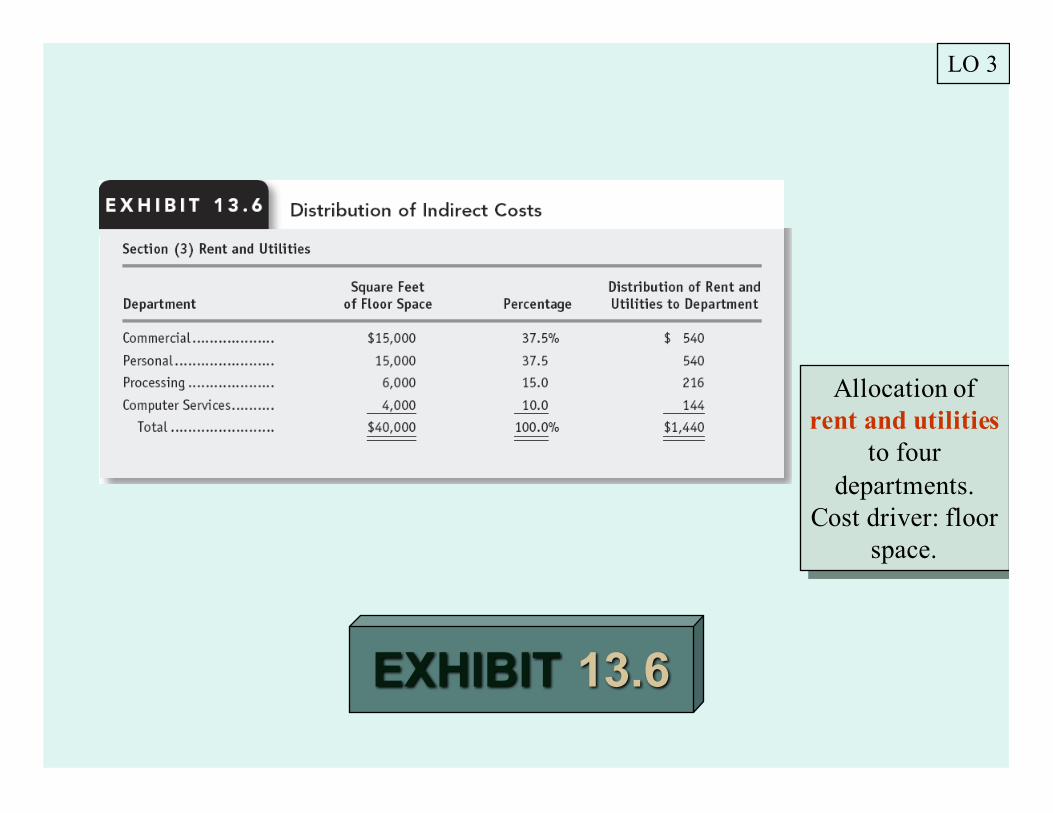

Allocation of rent and utilities

to four departments.

Cost driver: floor space.

EXHIBIT 13.2

LO 3

Step 3: Allocate service department costs to production

departments.

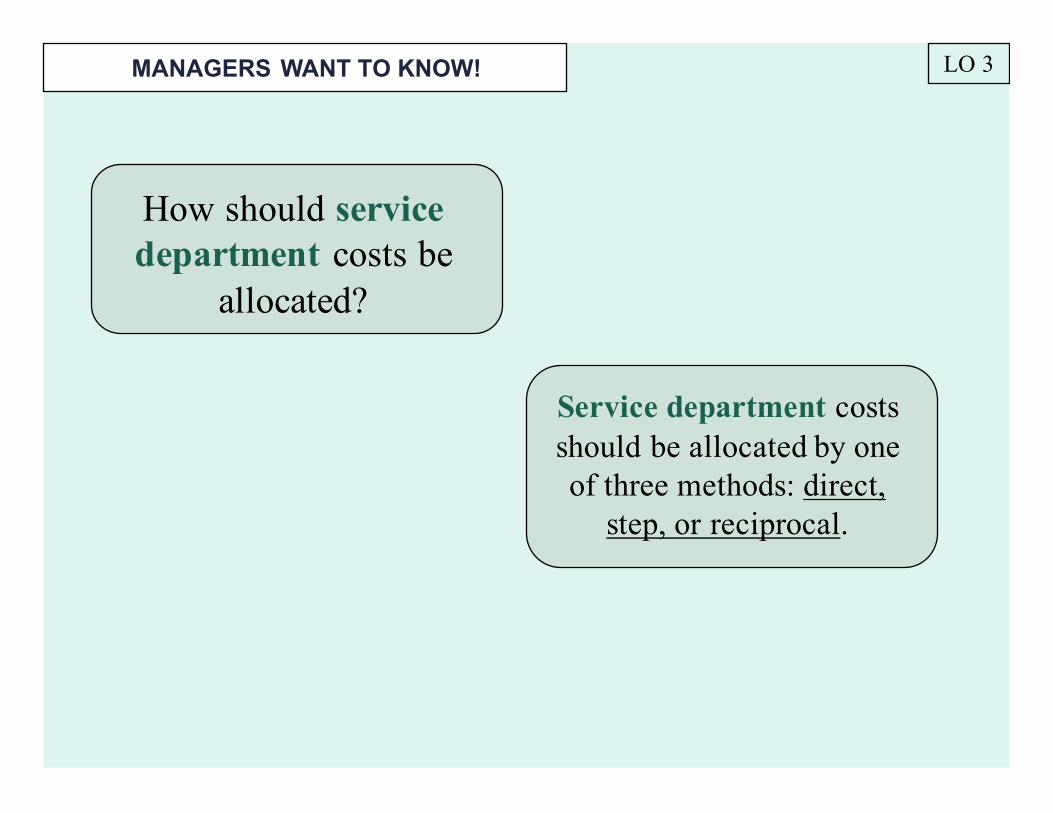

How should service department costs be

allocated?

Service department costs should be allocated by one of three methods: direct,

step, or reciprocal.

LO 3MANAGERS WANT TO KNOW!

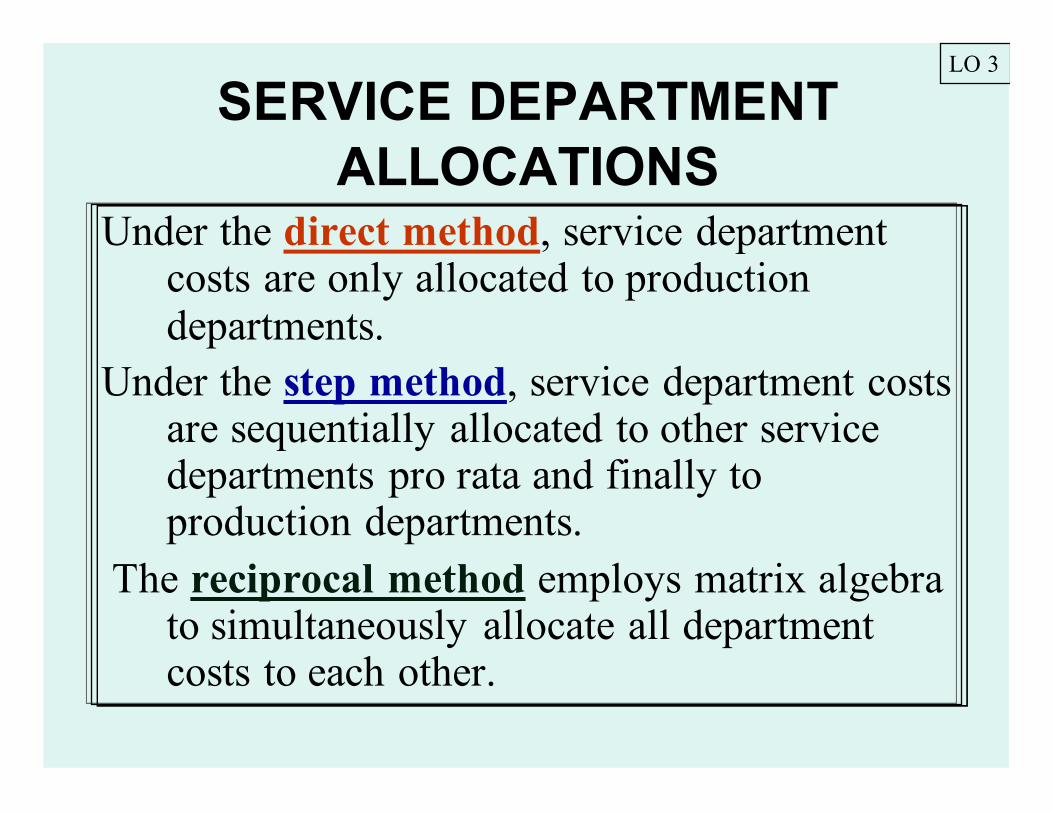

SERVICE DEPARTMENT ALLOCATIONS

Under the direct method, service department costs are only allocated to production departments.

Under the step method, service department costs are sequentially allocated to other service departments pro rata and finally to production departments.

The reciprocal method employs matrix algebra to simultaneously allocate all department costs to each other.

LO 3

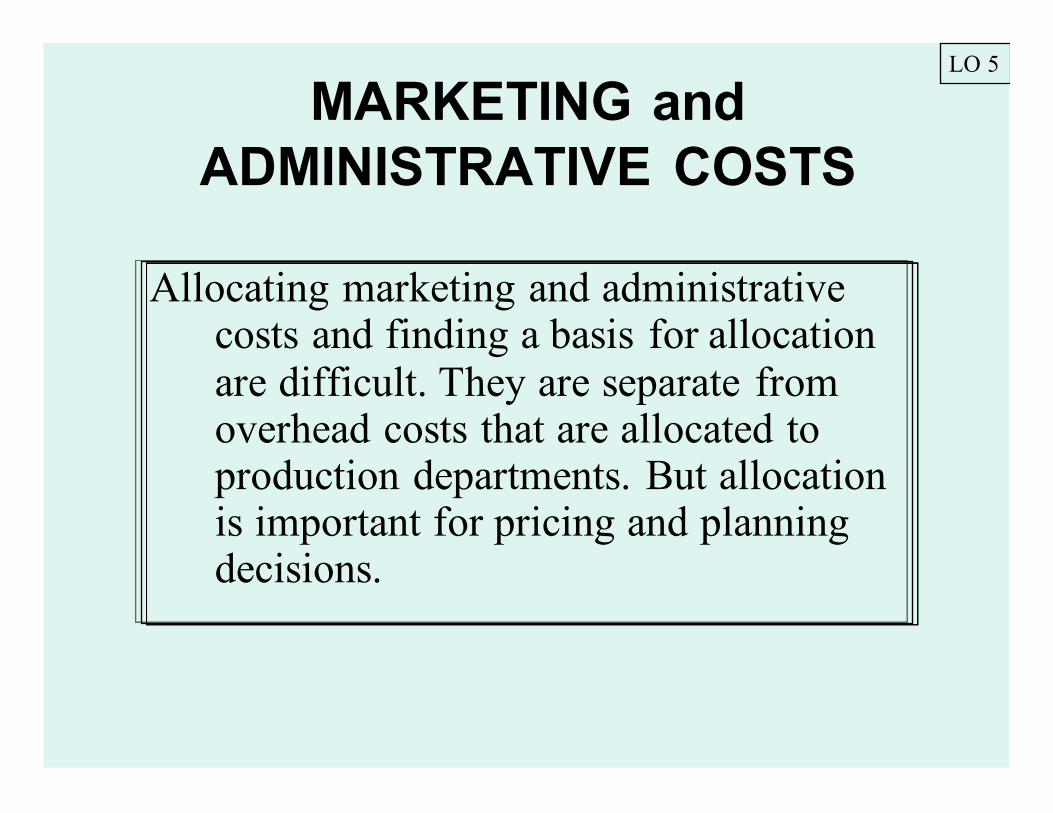

MARKETING and ADMINISTRATIVE COSTS

Allocating marketing and administrative costs and finding a basis for allocation are difficult. They are separate from overhead costs that are allocated to production departments. But allocation is important for pricing and planning decisions.

LO 5

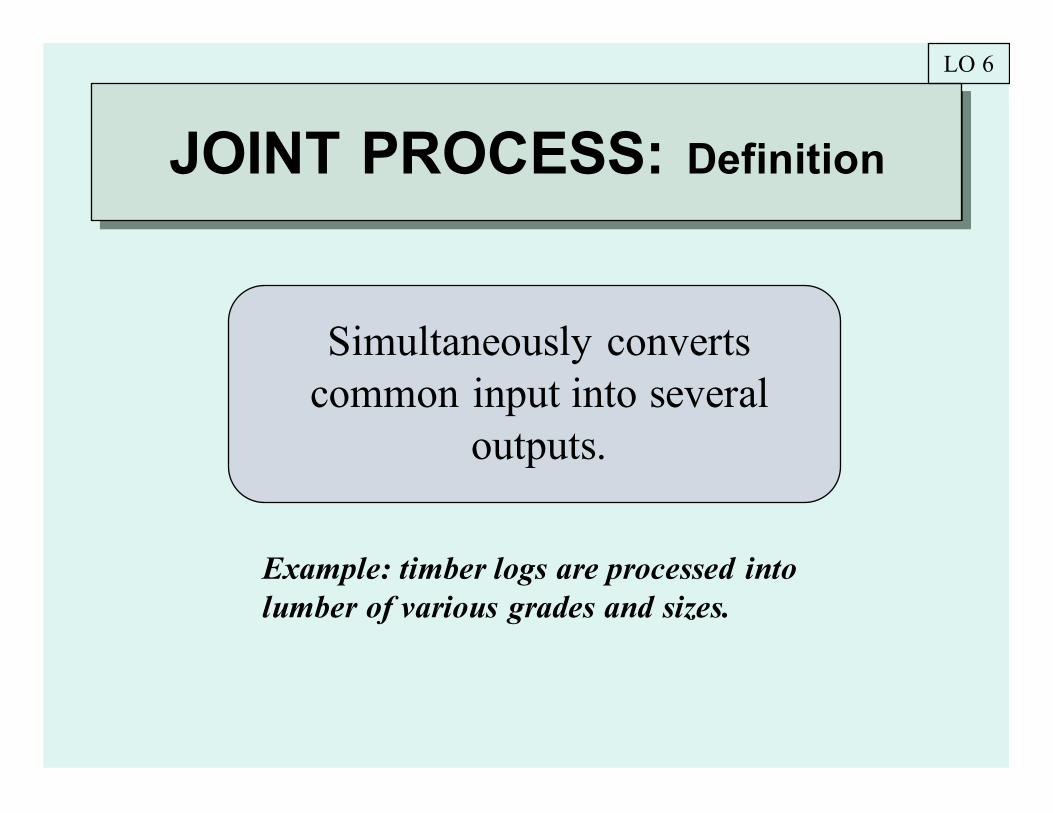

JOINT PROCESS: Definition

Simultaneously converts common input into several

outputs.

Example: timber logs are processed into lumber of various grades and sizes.

LO 6

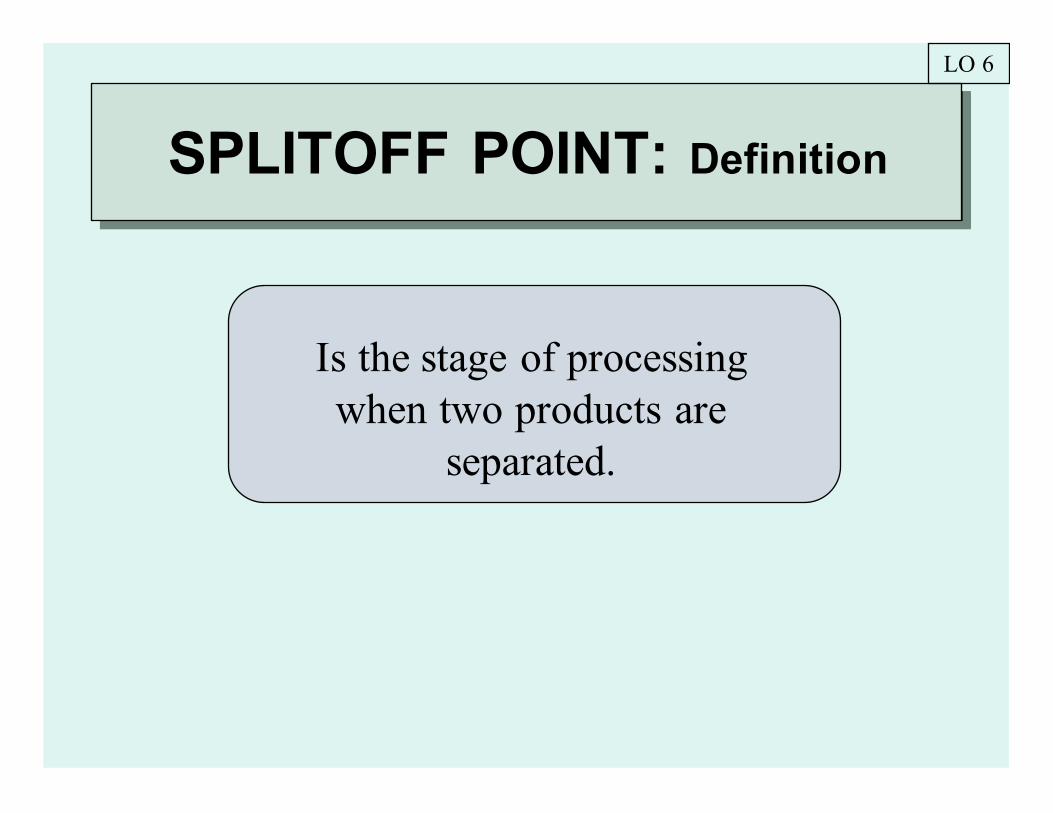

SPLITOFF POINT: Definition

Is the stage of processing when two products are

separated.

LO 6

The NRV method implies a matching of input costs with revenues generated by

each output.

LO 6

The physical quantities method is used whenoutput product prices are highly volatileor when significant processing occurs

between split off and the 1st point of marketability.

ALLOCATING JOINT-PROCESS COSTS

Organizations allocate joint costs for many reasons:¯Measuring performance¯Determining and responding to regulatory

rate changes¯Estimating casualty losses¯Resolving contractual interests and

obligations¯Financial and tax reporting

LO 7

27

End of CHAPTER 13

Related Documents