Strat. Change 24: 85–97 (2015) Published online in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/jsc.1999 RESEARCH ARTICLE Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change: Briefings in Entrepreneurial Finance Strategic Change DOI: 10.1002/jsc.1999 Behavioral Microfinance: Evidence from a Field Experiment in Cairo 1 Hayyan Alia Burgundy School of Business, Dijon, France Guillermo Mateu Burgundy School of Business, Dijon, France Angela Sutan Burgundy School of Business, Dijon, France Understanding the behavior of the poor has long been an important focus of microfinance (MF) research. On the one hand, several studies have been con- ducted to understand the financial decisions of MF clients related to the construc- tion of trustworthiness and social collateral (which replaces financial collateral in MF loans). On the other hand, the natural counterpart of trustworthiness (i.e., risk taking) has been another main point of focus when evaluating MF clients’ behavior. Yet, most of these studies remain observational, use standard surveys about behavior, or make use of financial information only — as found in many qualitative impact assessments and econometric studies. erefore, the usual biases when reporting stated behavior, in particular about items that are difficult to rationalize (such as trustworthiness and risk taking), are difficult to capture. Only recently have experimental games become popular in MF to gain deeper insights into MF clients and reduce these biases. Overall, the financial decisions of MF clients seem complex to MF practitio- ners, who increasingly question the needs and wants of poor MF clients, especially after the recent crises in the MF industry. Two of the most documented difficulties that MF institutions (MFIs) usually face are the adverse selection problem and the absence of financial collateral provided by the borrower (Giné et al., 2010). In other words, MFIs serve clients without credit history, and are therefore unable to predict their willingness or ability to repay the loan. Moreover, these clients live in social neighborhoods where no one around has financial reserves to cover a Microfinance clients reveal safer financial behaviors compared with non-microfinance clients. The self-esteem of microfinance clients is higher compared with non-microfinance clients. MFIs should investigate in detail the structure of the social neighborhood prior to client selection. 1 JEL classification codes: B41, C14, D03, G02, I30. E xperimental incentive-compatible techniques bring unbiased evidence from the field about what is unique in the behavior of microfinance clients.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Strat. Change 24: 85–97 (2015)Published online in Wiley Online Library(wileyonlinelibrary.com) DOI: 10.1002/jsc.1999 RESEARCH ARTICLE

Copyright © 2015 John Wiley & Sons, Ltd.Strategic Change: Briefi ngs in Entrepreneurial Finance

Strategic Change DOI: 10.1002/jsc.1999

Behavioral Microfi nance: Evidence from a Field

Experiment in C airo 1

Hayyan Alia Burgundy School of Business , Dijon , France

Guillermo Mateu Burgundy School of Business , Dijon , France

Angela Sutan Burgundy School of Business , Dijon , France

Understanding the behavior of the poor has long been an important focus of microfi nance (MF) research. On the one hand, several studies have been con-ducted to understand the fi nancial decisions of MF clients related to the construc-tion of trustworthiness and social collateral (which replaces fi nancial collateral in MF loans). On the other hand, the natural counterpart of trustworthiness (i.e., risk taking) has been another main point of focus when evaluating MF clients ’ behavior. Yet, most of these studies remain observational, use standard surveys about behavior, or make use of fi nancial information only — as found in many qualitative impact assessments and econometric studies. Th erefore, the usual biases when reporting stated behavior, in particular about items that are diffi cult to rationalize (such as trustworthiness and risk taking), are diffi cult to capture. Only recently have experimental games become popular in MF to gain deeper insights into MF clients and reduce these biases.

Overall, the fi nancial decisions of MF clients seem complex to MF practitio-ners, who increasingly question the needs and wants of poor MF clients, especially after the recent crises in the MF industry. Two of the most documented diffi culties that MF institutions (MFIs) usually face are the adverse selection problem and the absence of fi nancial collateral provided by the borrower ( Giné et al ., 2010 ). In other words, MFIs serve clients without credit history, and are therefore unable to predict their willingness or ability to repay the loan. Moreover, these clients live in social neighborhoods where no one around has fi nancial reserves to cover a

Microfi nance clients reveal safer

fi nancial behaviors compared with

non-microfi nance clients.

The self-esteem of microfi nance

clients is higher compared with

non-microfi nance clients.

MFIs should investigate in detail

the structure of the social

neighborhood prior to client

selection.

1 JEL classifi cation codes: B41, C14, D03, G02, I30.

Experimental incentive-compatible techniques bring unbiased evidence from the

fi eld about what is unique in the behavior of microfi nance clients.

86 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

based mechanisms in MF through implementing a series of ten MF games in framed fi eld experiments. Th e study helped to explain the tendency of many MFIs toward individual-lending contracts. More recently, Kolstad and Wiig ( 2013 ) elaborated more on the group-lending model but from the angle of the individual characteristics of the borrowers. Cassar et al . ( 2007 ) used MF and trust games in fi eld experiments to measure the infl uence of social capital on the behavior of clients in the group-lending model. Other examples of MF papers using experimental games to study group lending and joint liability mecha-nisms are found in the studies of Kono ( 2006 ), Abbink et al . ( 2006 ), Werner ( 2010 ), Carpenter and Williams ( 2010 ), McIntosh et al . ( 2013 ), and Fischer ( 2013 ).

In this article, we aim to shed light on two aspects of behavioral MF. By comparing MF clients with non-clients, we endeavor to fi nd whether MF clients ’ behavior is diff erent from that of non-clients. To our knowledge, only one previous research paper used, at the same time, MF clients and non-clients as participants in experimental games: Becchetti and Conzo ( 2011 ) used an investment game to test the creditworthiness of MF clients compared with non-clients in Argentina. Th ey considered creditwor-thiness and trustworthiness as synonyms, and thus the investment game they used was based on a standard two-player trust game ( Berg et al ., 1995 ). Th eir fi ndings show that MF clients have higher creditworthiness compared with non-clients, as they were receiving from the trustors (and expected to give back) signifi cantly more than the non-client participants. Supported by their fi ndings, Bec-chetti and Conzo ( 2011 ) suggest the use of their invest-ment game in microfi nance impact evaluation studies. Our study explores further the trustworthiness of MF clients, and treats the risk-aversion aspect in addition.

Th e remainder of this article is organized as follows: the fi rst section describes the sample and procedures; the following section presents the two studies on trustworthi-ness and risk aversion, the results of the games imple-mented in each study, and the recommendations built on these results; a fi nal section concludes.

possible future loss. Th erefore, it is of high importance to comprehend how MF clients deal with the trust and risk elements during the lending process. Because of the speci-fi city of the MF clients, studying their fi nancial behavior is a key factor for success in this industry.

Experimental games are an eff ective tool to study decision making (for an extensive review of the most celebrated experimental games, see Roth and Kagel, 1995 ). Karlan ( 2005 ) discussed and confi rmed the valid-ity of using experimental games for predicting the fi nan-cial decisions of MF clients. Measuring trustworthiness and risk aversion is possible by implementing diff erent games. First, measures of trustworthiness can be obtained through the trust game ( Berg et al ., 1995 ), by measuring the trust in others. Th e trust game also provides an effi -cient tool to study network structure and hierarchy. Self-esteem games measure self-trust through evaluating the basic self-confi dences that leads MF clients to borrow money. Th is measurement can be done by psychological and experimental means ( Blascovich and Tomaka, 1991 ). Second, risk choices are usually addressed with a variety of individual lottery choices. Besides lottery-based games, the public goods game provides further explanation of the bearing of investment risks by the participant in collective investing activities. Th e sustainability of the social col-lateral can usually be measured in games such as public goods ( Fehr and Gächter, 2000 ). In this article, we attempt to implement framed fi eld experiments (following the characterization of Harrison and List, 2004 ) to shed light on these two dimensions (trust and risk aversion) of MF clients ’ decision making. Experimentally, we provide dif-ferent measures for each of the mentioned dimensions. In addition, we use a control group of non-MF clients as a reference point.

In reviewing the literature on the use of experimental games in MF research, we fi nd that most of the studies have focused on researching the mechanisms of the group-lending and joint-liability model. Without purporting to be exhaustive, the most comprehensive work in the fi eld is that of Giné et al . ( 2010 ). Th e authors studied group-

Behavioral Microfi nance 87

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

Study 1

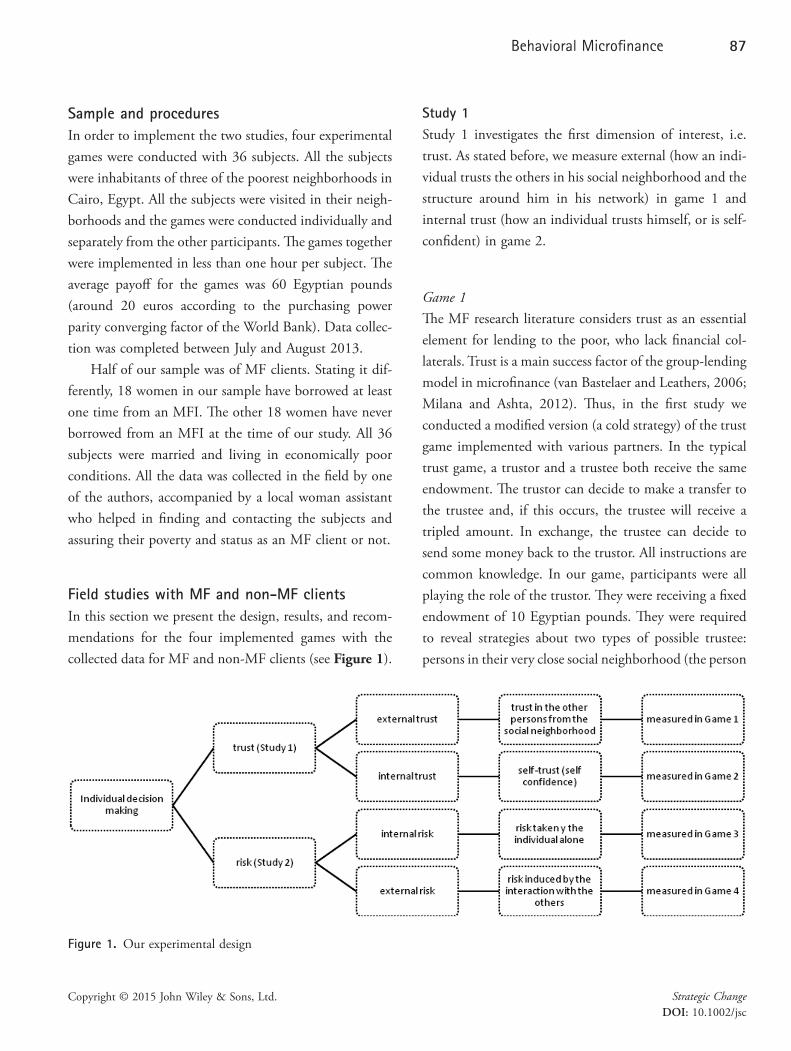

Study 1 investigates the fi rst dimension of interest, i.e. trust. As stated before, we measure external (how an indi-vidual trusts the others in his social neighborhood and the structure around him in his network) in game 1 and internal trust (how an individual trusts himself, or is self-confi dent) in game 2.

Game 1 Th e MF research literature considers trust as an essential element for lending to the poor, who lack fi nancial col-laterals. Trust is a main success factor of the group-lending model in microfi nance ( van Bastelaer and Leathers, 2006 ; Milana and Ashta, 2012 ). Th us, in the fi rst study we conducted a modifi ed version (a cold strategy) of the trust game implemented with various partners. In the typical trust game, a trustor and a trustee both receive the same endowment. Th e trustor can decide to make a transfer to the trustee and, if this occurs, the trustee will receive a tripled amount. In exchange, the trustee can decide to send some money back to the trustor. All instructions are common knowledge. In our game, participants were all playing the role of the trustor. Th ey were receiving a fi xed endowment of 10 Egyptian pounds. Th ey were required to reveal strategies about two types of possible trustee: persons in their very close social neighborhood (the person

Sample and procedures

In order to implement the two studies, four experimental games were conducted with 36 subjects. All the subjects were inhabitants of three of the poorest neighborhoods in Cairo, Egypt. All the subjects were visited in their neigh-borhoods and the games were conducted individually and separately from the other participants. Th e games together were implemented in less than one hour per subject. Th e average payoff for the games was 60 Egyptian pounds (around 20 euros according to the purchasing power parity converging factor of the World Bank). Data collec-tion was completed between July and August 2013.

Half of our sample was of MF clients. Stating it dif-ferently, 18 women in our sample have borrowed at least one time from an MFI. Th e other 18 women have never borrowed from an MFI at the time of our study. All 36 subjects were married and living in economically poor conditions. All the data was collected in the fi eld by one of the authors, accompanied by a local woman assistant who helped in fi nding and contacting the subjects and assuring their poverty and status as an MF client or not.

Field studies with MF and non-MF clients

In this section we present the design, results, and recom-mendations for the four implemented games with the collected data for MF and non-MF clients (see Figure 1 ).

Figure 1. Our experimental design

88 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

values of the Give and the Expect values. We classify the data into MF clients and non-MF clients. We analyze the possible diff erences observed in both groups (clients and non-clients) to explain the diff erences in trusting behav-ior. To do that, we implemented non-parametrical tests to show that no signifi cant diff erences were observed in the variables Give and Expect between clients and non-clients. Table 1 contains the values for the tests. Th erefore, appar-ently, no diff erence exists in the structure and hierarchy of the trust of MF clients and non-clients. We have to look deeper in this direction, and our analysis allows us to present our second result.

Result 2: MF clients have a stable structure of their social neighborhood, compared with non-clients, for which the structure of the social neighborhood modulates overall trust.

Going deeper into the analysis, we created the variable Ratio-close as the result of the ratio Expect by Give ( Expect / Give ) in the scenario called Close , and we defi ned Ratio-others as the ratio of Expect by Give ( Expect / Give ) in the scenario Other . Th ese variables are the returns on

they most care about, their spouse, their best friend) and unknown persons (therefore, in total, they were facing four scenarios). Strategies were to be constructed in two dimensions: the amount sent to the trustee (hereafter denoted Give ) and the expected amount to be sent back by the trustee (hereafter denoted Expect ). Th ey were informed that one of them would be randomly selected to implement the real trust game. Th is variant of the trust game was meant to reveal the structure and hierarchy of the social neighborhood of the individual, by means of the ranking performed on their Give and Expect strategies.

Result 1: MF clients trust and expect reciprocity from their social neighborhood as much non-MF clients.

In addition to the two variables of interest Give and Expect defi ned previously, we take into consider-ation four possible scenarios to measure the decision of subjects (1 = Important person ; 2 = Spouse ; 3 = Friend ; 4 = Other ). According to these four scenarios, we can introduce a distinction according to the position in the social neighborhood (or the personal identity) of the dif-ferent scenarios. We argue that the three fi rst scenarios ( Important person , Spouse , and Friend ) refer to close sce-narios (people situated in a close position to the trustor in the social neighborhood), while the fourth scenario ( Other ) refers to an anonymous situation where the prox-imity with the person is reduced. To replicate this sugges-tion in the analysis, we create the variable Close as the average of the fi rst three variables. In this sense, this dis-tinction allows us to measure diff erent behaviors accord-ing to the identity and proximity of the subject in the four scenarios. Note that the variable Give goes from 0 to 10, while Expect is from 0 to 40; that is, three times the maximum giving (30) plus 10 pounds of personal endowment.

Table 1 presents the results from the trust game according to the four diff erent scenarios and to the vari-able Close . Th e variables in columns refer to the average

Table 1. Trust game across scenarios

Average Clients Non-clients

(std. dev.) ( n = 18) ( n = 18)

Scenarios Give Expect Give Expect

Important person 6.94 14.86 5.80 15.13(2.50) (12.26) (2.88) (11.77)

Spouse 3.55 9.88 4.22 6.94(4.07) (13.33) (3.47) (11.64)

Friend 5.25 13.47 5.55 9.72(3.10) (13.03) (1.61) (8.98)

Other 2.72 a 3.47 b 4.16 a 5.48 b (2.83) (13.03) (3.53) (5.95)

Close 5.25 c 12.74 d 5.19 c 10.60 d (2.02) (7.69) (1.49) (6.16)

Source : Mann–Whitney test ( p -values): a (0.2058), b (0.7733), c (0.8841), d (0.3745).

Behavioral Microfi nance 89

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

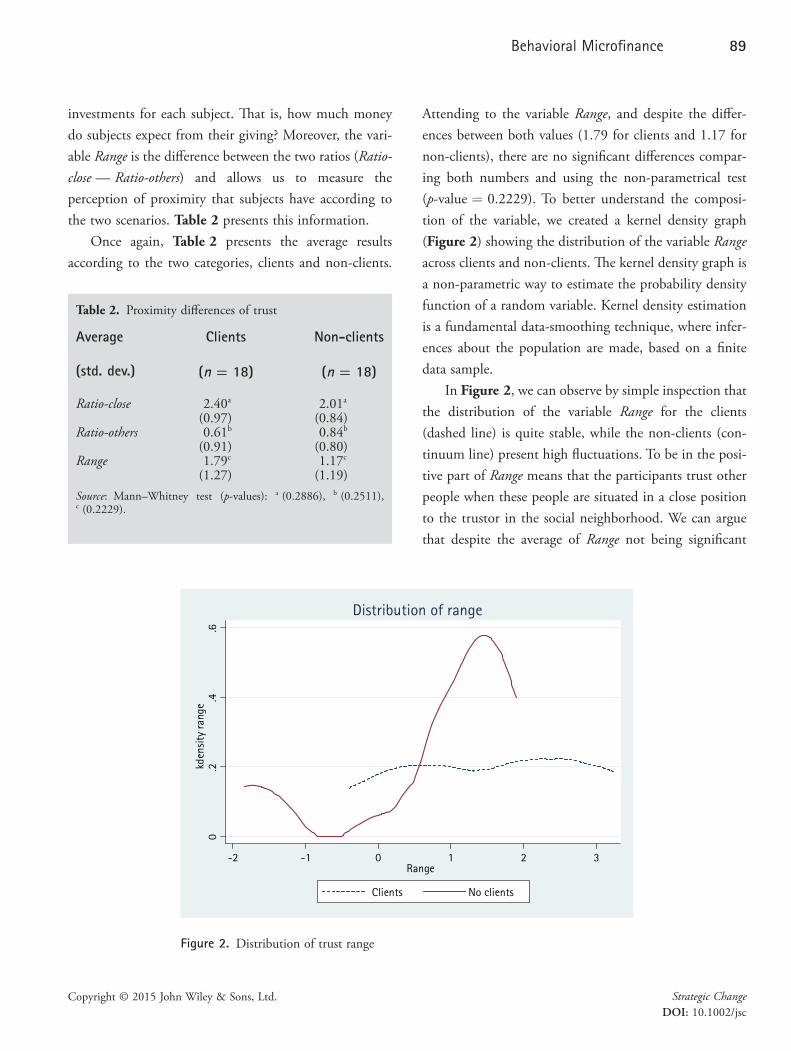

Attending to the variable Range , and despite the diff er-ences between both values (1.79 for clients and 1.17 for non-clients), there are no signifi cant diff erences compar-ing both numbers and using the non-parametrical test ( p -value = 0.2229). To better understand the composi-tion of the variable, we created a kernel density graph ( Figure 2 ) showing the distribution of the variable Range across clients and non-clients. Th e kernel density graph is a non-parametric way to estimate the probability density function of a random variable. Kernel density estimation is a fundamental data-smoothing technique, where infer-ences about the population are made, based on a fi nite data sample.

In Figure 2 , we can observe by simple inspection that the distribution of the variable Range for the clients (dashed line) is quite stable, while the non-clients (con-tinuum line) present high fl uctuations. To be in the posi-tive part of Range means that the participants trust other people when these people are situated in a close position to the trustor in the social neighborhood. We can argue that despite the average of Range not being signifi cant

investments for each subject. Th at is, how much money do subjects expect from their giving? Moreover, the vari-able Range is the diff erence between the two ratios ( Ratio-close — Ratio-others ) and allows us to measure the perception of proximity that subjects have according to the two scenarios. Table 2 presents this information.

Once again, Table 2 presents the average results according to the two categories, clients and non-clients.

Table 2. Proximity diff erences of trust

Average Clients Non-clients

(std. dev.) ( n = 18) ( n = 18)

Ratio-close 2.40 a 2.01 a (0.97) (0.84)

Ratio-others 0.61 b 0.84 b (0.91) (0.80)

Range 1.79 c 1.17 c (1.27) (1.19)

Source : Mann–Whitney test ( p -values): a (0.2886), b (0.2511), c (0.2229).

0.2

.4.6

kden

sity

range

-2 -1 0 1 2 3Range

Clients No clients

Distribution of range

Figure 2. Distribution of trust range

90 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

fi nance institution in India), Basargekar ( 2009 ) has shown that although the AMM ’ s services didn ’ t lead to a signifi -cant economic empowerment of its clients, those clients experienced a signifi cant positive change in regard to their self-esteem and leadership skills. Despite our study not being on the impact of microfi nance intervention in the lives of poor women, such a signifi cant diff erence between borrowers and non-borrowers can possibly be explained by the microfi nance variable. More research is required to support this reasoning, which can help practitioners understand better the need to focus more on pre/post credit scoring of their clients.

As we can see in Table 3 , the average amounts from both categories diff er, presenting an average (on a scale from 0 to 100) of 81.66 for clients and 57.77 for non-clients. Th ese diff erent variables — through clients and non-clients — are tested non-parametrically and show a signifi cant diff erence between groups ( p -value = 0.0322).

Recommendations from Study 1 Result 1 and Result 2 mean that MF clients modulated the structure of their social neighborhood to be continu-ous around them: clearly, this means that they evolve in a social neighborhood in which they can count as much on close partners as on partners from larger social circles. Th is can be interpreted in two ways: either MF clients have acquired the ability to select their overall social neighborhood, and therefore anyone in this social neigh-borhood can act as social collateral, or there are victims

between clients and non-clients, there are signifi cant fl uc-tuations when we observe the variable distribution. Focus-ing on the non-clients ’ line, we observe a quite low density in the negative part of the variable, while it shows a posi-tive trend in the positive part (from 0 to 2).

Finally, the third and unexpected result from our fi rst game is that the husband receives the lower amount of investment among the people in the Close scenarios. Indeed, as we note, Spouse is only given 3.55 Egyptians pounds over 10. Th is unexpected result arose from the relatively low amount individuals both give and expect from their spouses. Indeed, as compared with other values from the close social neighborhood, the spouse reveals the lowest amount.

Result 3: Th e spouse (and by extension the family) is not the optimal collateral to be selected from the social neighborhood.

Game 2 Th is game, denoted the expertise game, was a scenario meant to reveal overconfi dence attributes — that is, beliefs of participants (self-confi dence) in their abilities to give expert advice about opportunities to succeed in a market, as a proxy for internal trust. Such self-images are consid-ered to have important signaling eff ects to the other part-ners of the business, given the fact that the MF clients evolve in an uncertain environment. In our scenario, they were simply asked to indicate their level of expertise com-pared with expert advice in a vignette scenario.

Th e purpose of this game is to analyze the level of self-esteem of subjects when they have to compare them-selves against others. Th e basic result, presented in Table 3 , summarizes the average answers in two categories.

Result 4: MFI clients are over-confi dent in their abilities to give expert advice.

Th is result supports the fi ndings in microfi nance impact research. For example, in an impact analysis study of Annapurna Mahila Mandal (AMM) (an urban micro-

Table 3. Expertise

Clients No clients

( n = 18) ( n = 18)

Expertise level 81.66 a 57.77 a (29.55) (32.63)

Source : Mann–Whitney test ( p -value): a (0.0332).

Behavioral Microfi nance 91

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

edge, even with our limited sample, this is the fi rst attempt to measure the structure of social neighborhoods using trust games and the fi rst provision of detailed information about the role of each category of partners from the social neighborhood. It indicates a way for MFI to select the optimal social collateral for MF loans.

Th e Spouse result ( Result 3 ) can hide a double inter-pretation: either family is built on tradition and not on trust, therefore individuals do not consider their spouse as the most important person in their lives; or, unlike traditional entrepreneurial activities documented in devel-oped countries, poor individuals from Cairo are able to separate ‘professional’ and ‘private’ activities. More research should be conducted in this direction to enforce the intu-ition. Indeed, Afrin et al . ( 2010 ) highlight the following interesting points in their study of the factors behind the development of entrepreneurship of rural female MF clients: (1) rural women are encouraged to participate in entrepreneurial activities when other family members practice such activities; (2) women are encouraged when their work is recognized by their husband in the fi rst place, then by other family members, and fi nally by others. In other words, lack of family support is a main factor aff ecting the entrepreneurship of female MF clients. Th us, our Result 3 shows evidence that supports the latter point. Considering the poor relationship between the par-ticipants and their husbands (for the majority of women in our sample), depending on the family for social col-lateral is logically not the best option, as the women are not only discouraged, but also abandoned, by their husbands.

Recommendation 2: Practitioners should consider peers for forming groups instead of family members in the group-lending model.

As for the explanation of diff erences between client and non-client subjects, it could be that MF clients have increased their level of self-esteem after receiving the micro loan. Th is idea is already connected with the theory

of trust illusion (i.e., over-confi dence in their surrounding individuals). In both cases, this stands for a positive role of the MFIs: they strengthen the social neighborhood or, at least, enforce positive expectations about norms in society. In time, both cases are theoretically known to lead to a development of trustworthy behavior in society. It is worth clarifying here that, in the MF literature, social interactions that aff ect the fi nancial behavior of MF clients are referred to using the terms ‘social capital’ and ‘social collateral.’ According to Postelnicu et al . ( 2013 ), social capital refers to the social ties between the microfi nance borrowers inside their groups. Social collateral refers to internal and external social ties that aff ect the behavior of MF clients. Such ties interest MFIs as they help in predict-ing the repayment performance of loans in the group-lending model ( Postelnicu et al ., 2013 ).

At the opposite end, non-MFI clients reveal a stan-dard structure of the social neighborhood: they trust and expect more from close relations, and less from individuals from their social periphery.

Recommendation 1: MFIs that use the group-lending model should investigate in detail the structure of the group prior to lending.

Understanding the social neighborhood of the MF clients is a key factor in the microfi nance industry. Th ose clients have special needs and live in special circumstances (compared with routine bankable borrowers). Owing to this particularity, MF practitioners are increasingly con-sidering the social neighborhood/capital of their clients, especially after social crises that compromised the reputa-tion of microfi nance recently — such as the 2010 crisis in Andhra Pradesh. Th is latter crisis has highlighted the fact that an infusion of debt cannot resolve (and on the contrary, could magnify) deeper-rooted social problems in the community where microfi nance intervenes ( Mader, 2013 ). All together, these fi rst results present interesting insights about the structure of the social neighborhood for MFI clients compared with non-clients. To our knowl-

92 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

times. 2 In each scenario, subjects have to choose whether they want to play the game with high risk ( Risk2 ), with low risk ( Risk1 ), or with no risk ( Risk0 ). In this sense, each variable represents a continuum value from 0 to 2 accord-ing to the subjects ’ decisions. Additionally, we have created the variable AvgRisk as the average of the fi rst three vari-ables ( Risk0 , Risk1 , and Risk2 ). Additionally, we have created a range variable called Risk-Range to observe the impact of time and experience in the risk preferences, defi ned as Risk2 — Risk0 .

Generally speaking, we observe large numbers for non-clients in all four fi rst cases. However, the non-parametric tests (Mann–Whitney) show there are diff er-ences only in the case of Risk2 and AvgRisk (at 5% and 10%, respectively). Values of the tests are included below the table. According to these results, we can assume that the risk perception of MF clients increases with time (and experience). Th is corroborates previous fi ndings surveyed in Giné et al . ( 2010 ) about an internalization of respon-sible behavior when individuals become MFI clients.

of contingencies of self-worth, and is documented in the literature.

Recommendation 3: More research should help in identifying reasons for such an increased self-esteem other than social attention and socially acquired rank.

Study 2

Th is study refers to the natural counterpart of trust (i.e., risk) and captures in Game 3 the internal risk and in Game 4 the external risk.

Game 3 According to Churchill ( 2002 ), the conception of risk management and the understanding of risk by the micro-fi nance clients was always an important issue in behavioral microfi nance. Th e use of microloans by microfi nance clients is, in many cases in practice, dedicated to fulfi lling the need for fi nancial cushions to face any future risks. Th erefore, Game 3 was a simple game meant to quantify risk. Participants received an endowment of one pound. Th ey were required to choose between three options: status quo (no risk lottery, hereafter called Risk0 ) or buy a ticket at their endowment cost to play a high ( Risk2 ) or low ( Risk1 ) risk lottery (both with expected values equal to the cost of the ticket). Th e lottery was to be played sequentially three times (to measure the relationship with increased time). Our results here show clearly the aversion to risk that refl ects clear understanding (of the microfi -nance clients in our sample) of the cost of credit, which is very expensive when used as a safety net.

Result 5: MFI clients are more risk averse than non-clients, and risk aversion increases with time.

To enforce this result, data is presented in Table 4 — as in the previous tables, separating the sample into columns (clients and non-clients). Table 4 presents the average risk decisions through three diff erent scenarios ( Risk0 , Risk1 , and Risk2 ) as we repeat exactly the same game three

Table 4. Risk preferences

Average Clients Non-clients

(std. dev.) ( n = 18) ( n = 18)

Risk0 0.94 a 1.05 a (0.53) (0.63)

Risk1 1.33 b 1.5 b (0.59) (0.51)

Risk2 1.11 c 1.5 c (0.47) (0.51)

AvgRisk 1.12 d 1.35 d (0.39) (0.37)

Risk-Range 0.16 e 0.44 e (0.69) (0.70)

Source : Mann–Whitney test ( p -values): a (0.5692), b (0.4159), c (0.0272), d (0.0874), e (0.2406).

2 Note that nobody knew the game was going to be repeated three times.

Behavioral Microfi nance 93

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

in case they were off ered the possibility of punishing small contributors, if they would take this opportunity to punish.

Result 6: MF clients sustain as much as non-clients the provision of public goods.

In the public-good scenario, subjects have to decide on two questions. Actually, we collected the variables Con-tribution [0–10] and Punishment [0 = no; 1 = yes]. Th e amount of money participants want to invest in the public good shows an average result of 6.22 pounds for clients and 6.11 pounds for non-clients. Th ese results provide no diff erence between the two groups. In terms of punish-ment, over 50% of subjects in both groups said that they would punish others according to the described scenario.

To show more information about this last game, we run several regressions in Table 5 to know which kind of variables are aff ecting the decision to contribute to the public good in relation to the previous results. In this sense, we divided the sample into two categories (clients and non-clients) to observe the diff erences in both groups — as in the previous methodology. Regression (1)

Game 4 Microfi nance research (at least, consumer research in microfi nance) does not particularly study the ‘public goods’ issue. Chowdhury et al . ( 2004 ) is one of only a few examples to elaborate on the social impact of microfi -nance and its contribution to the development of public goods. However, their focus was on MFIs rather than on clients ’ contributions to public goods. Nilsson ( 2008 ) highlights the contribution of MF clients in the creation of public goods indirectly by being involved in the formal economy through their micro-enterprises (and paying taxes that enable the government to provide public goods).

Th us, the last game was a variant of a cold-strategy public-goods game played in groups of four, meant to measure the sustainability of the social neighborhood. In a fi rst step, participants received an endowment of ten pounds and had at their disposal two possibilities: keep the money in a private account or invest the money in a public account. Th e experimenter would multiply the money in the public account by two and divide it by four, equally redistributing it, indiff erent to individual contri-butions. Th e money not invested in the public account is considered as money kept for the private account, thus for the participant. In the second step, they were asked,

Table 5. Linear regression explaining the contribution to the public good

(1) (2) (3) (4) (5)

All Clients Non-clients Clients Non-clients

Punishment − 0.346 1.918 − 2.447 0.389 − 2.514 * (0.884) (1.183) (1.400) (1.260) (1.204)

Ratio-close 1.161 ** 1.753 ** 1.263(0.484) (0.623) (0.845)

Ratio-others 1.157 ** 0.500 2.188 ** (0.498) (0.707) (0.761)

Constant 2.944 ** 1.055 4.925 ** 5.722 *** 5.654 *** (1.415) (1.935) (2.014) (1.034) (1.103)

Observations 36 18 18 18 18 R -squared 0.285 0.347 0.266 0.034 0.456 Standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

94 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

individuals enroll in MFI loans (because they know the extra risk related to the entrepreneurial project will be covered inside the social neighborhood). If this is not the case, they avoid undertaking the extra risk corresponding to the entrepreneurial project. Th is constitutes an amazing invisible regulating hand (because overall, it keeps the risk constant over the society) that needs further investigation. Th us, provision of public goods is highly dependent on the stability of the social neighborhood.

Recommendation 4: When microfi nance projects aim to increase the contribution of the poor in public goods, poor entrepreneurs are easier to convince (to be part of the formal economy) when they can experience the provision of the public goods directly on the local level rather than on the national level.

Recommendation 5: Micro-insurance products are important to consider in microfi nance. Micro-insurance fi ts with the needs of risk-averse microfi nance clients.

Conclusion

Th e fi ndings of the four games implemented in our article show that overall, MF clients seem to have a higher valu-ation of money and better self-esteem compared with non-client participants. Figure 3 recapitulates all the fi ndings from the four games.

Based on the results of Game 1 and Game 4, MF subjects are shown to be more stable in their fi nancial investment decisions when they involve strangers. Only non-MF subjects ’ tendency to invest in strangers aff ects their contributions to public goods, which is not the case for MF subjects. In this sense, MF subjects seem to dis-tinguish clearly between close and non-close people in their fi nancial investment decisions. Game 3 shows, with statistical signifi cance, that MF subjects have higher risk aversion compared with non-MF subjects. Finally, Game 2 shows that self-esteem (from an entrepreneurial experi-ence point of view) is statistically diff erent between clients and non-clients.

is formed by the whole data of the sample, and in other regressions the sample is divided into clients and non-clients. We use explanatory variables such us Punishment , Ratio-close , and Ratio-others ( Ratio-close and Ratio-others were already explained in Study 1).

Identifying the eff ect of explanatory variables in the contribution to the public good, the variable Punishment has no signifi cant eff ect except in regression (5), showing a negative and marginal eff ect. Indeed, the most interest-ing results behind the data are the behavioral patterns we have obtained for the variables Ratio-close and Ratio-others . Concretely, we fi nd the variable Ratio-close positive and signifi cantly related for the whole data and for the clients sample. In this sense, clients trusting in ‘close people’ increase their contributions (at 5%). Additionally, we observe the variable Ratio-others to be positive and signifi cantly correlated with the contribution to the public good for the whole data (regression 1) and for the non-clients sample (regression 5). We support the idea that non-clients trusting in ‘other people’ increase their contributions at 5% too. Th is identifi ed pattern across clients and non-clients allows us to identify a diff erent behavior across MF and non-MF clients. Indeed, while MF clients contribute more to the public good in the presence of positive expectations about the stability of their social neighborhood, non-clients contribute more when interacting with strangers. Th is means that when-ever uncertainty about expected behavior is reduced, the public goods in general will be provided with more contributions.

Recommendations from Study 2 For MF clients, uncertainty is reduced inside their close social neighborhood (from whom they expect a lot). At the opposite end, for non-clients, uncertainty is unexpect-edly reduced outside the close social neighborhood. Th is means that the public good will be provided, relying on social norms only. Th is enforces the intuition of self-selection for participants in MFI projects: only when aware of a strong and sustainable social neighborhood will

Behavioral Microfi nance 95

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

MFIs improve their social performance by excluding bor-rowers with less potential.

Acknowledgments

Th e authors thank the Burgundy Regional Council ( PARI10 ) for co-funding this project, Arvind Ashta, the Banque Populaire Chair in Microfi nance, and LESSAC for all the scientifi c support they provided. Th e authors thank also Aff at Shabbana for valuable support provided in the fi eld research. Th e authors take sole responsibility for what is written in this article. Note: An important obstacle that prevented us from forming a bigger sample was the unstable political situation in Egypt at the time of this research, an issue that made mobility in Cairo very diffi cult — especially in the poor areas.

It should be taken into consideration that all the participants were selected from very poor neighborhoods, with the only criterion of being a microfi nance client or not. In addition, being a microfi nance client in our sample does not imply that the client is an entrepreneur. Th is criterion was not used in our selection and does not apply to many of our MF subjects. Taking into account these two considerations, our statistically signifi cant results call for future research focusing on whether the intervention of microfi nance in the lives of the poor might alter their fi nancial behavior toward better, fi nancially rational deci-sions. Qualitative impact evaluation studies need to answer this important question. MFIs might need to rethink the credit-scoring strategies they use in this case. If microfi nance has an impact on the behavioral fi nance of clients, then less strict scoring-based decisions can help

Figure 3. Summary of fi ndings and contributions

96 Hayyan Alia, Guillermo Mateu, and Angela Sutan

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

References

Abbink K , Irlenbusch B , Renner E . 2006 . Group size and social ties in microfi nance institutions . Economic Inquiry 44 ( 4 ): 614 – 628 .

Afrin S , Islam N , Ahmed SU . 2010 . Microcredit and rural women entrepreneurship development in Bangladesh: A multivariate model . Journal of Business & Management 16 ( 1 ): 9 – 36 .

Basargekar P. 2009 . Microcredit and a macro leap: An impact analysis of Annapurna Mahila Mandal (AMM), an urban microfi nance institution in India . Th e Icfai University Journal of Financial Economics VII ( 3&4 ): 105 – 120 .

Becchetti L , Conzo P . 2011 . Enhancing capabilities through credit access: Creditworthiness as a signal of trustworthiness under asymmetric information . Journal of Public Economics 95 ( 3/4 ): 265 – 278 .

Berg J , Dickhaut J , McCabe K. 1995 . Trust, reciprocity, and social history . Games and Economic Behavior 10 ( 1 ): 122 – 142 .

Blascovich J , Tomaka J . 1991 . Measures of self-esteem . Mea-sures of Personality and Social Psychological Attitudes 1 : 115 – 160 .

Carpenter JP , Williams T . 2010 . Moral hazard, peer monitoring, and microcredit: Field experimental evidence from Paraguay . FRB of Boston Working Paper, No. 10.

Cassar A , Crowley L , Wydick B . 2007 . Th e eff ect of social capital on group loan repayment: Evidence from fi eld experi-ments . Economic Journal 117 ( 517 ): F85 – F106 .

Chowdhury M , Mosley P , Simanowitz A . 2004 . Introduction . Journal of International Development 16 : 291 – 300 .

Churchill C. 2002 . Trying to understand the demand for microinsurance . Journal of International Development 14 : 381 – 387 .

Fehr E , Gächter S . 2000 . Cooperation and punishment in public goods experiments . Th e American Economic Review 90 ( 4 ): 980 – 994 .

Fischer G. 2013 . Contract structure, risk-sharing, and invest-ment choice . Econometrica 81 ( 3 ): 883 – 939 .

Giné X , Jakiela P , Karlan D , Morduch J . 2010 . Microfi nance games . American Economic Journal: Applied Economics 2 ( 3 ): 60 – 95 .

Harrison G , List JA . 2004 . Field experiments . Journal of Eco-nomic Literature 42 : 1009 – 1055 .

Karlan DS. 2005 . Using experimental economics to measure social capital and predict fi nancial decisions . American Eco-nomic Review 95 (5): 1688 – 1699 .

Kolstad I , Wiig A . 2013 . Does an educated mind take the broader view? A fi eld experiment on in-group favouritism among microcredit clients . Journal of Socio-Economics 45 : 10 – 17 .

Kono H . 2006 . Is group lending a good enforcement scheme for achieving high repayment rates? Evidence from fi eld exper-iments in Vietnam. Institute of Developing Economies, Japan External Trade Organization(JETRO), IDE Discussion Papers No. 61.

Mader P. 2013 . Rise and fall of microfi nance in India: Th e Andhra Pradesh crisis in perspective . Strategic Change 22 : 47 – 66 .

McIntosh C , Sadoulet E , Buck S , Rosada T. 2013 . Reputation in a public goods game: Taking the design of credit bureaus to the lab . Journal of Economic Behavior & Organization 95 : 270 – 285 .

Milana C , Ashta A . 2012 . Developing microfi nance: A survey of the literature . Strategic Change 21 : 299 – 330 .

Nilsson A. 2008 . Overview of fi nancial systems for slum upgrading and housing . Housing Finance International 23 ( 2 ): 19 – 25 .

Postelnicu L , Hermes N , Szafarz A . 2013 . Defi ning social col-lateral in microfi nance group lending . Working Papers CEB No 13-050.

Roth AE , Kagel JH . 1995 . Th e Handbook of Experimental Eco-nomics (Vol. 1 ). Princeton University Press : Princeton, NJ .

van Bastelaer T , Leathers H. 2006 . Trust in lending: Social capital and joint liability seed loans in Southern Zambia . World Development 34 ( 10 ): 1788 – 1807 .

Werner P. 2010 . Th e dynamics of cooperation in group lending — a microfi nance experiment . University of Cologne.

Behavioral Microfi nance 97

Copyright © 2015 John Wiley & Sons, Ltd. Strategic Change DOI: 10.1002/jsc

BIOGRAPHICAL NOTES

Hayyan Alia is a PhD student at CRESE, University of Franche-Comté, Besançon, France.

Also, a teaching associate in the Finance, Law, and Control Department and a research associate at the Banque Populaire Chair in Microfi nance, Burgundy School of Business, Dijon, France.

Correspondence to:

Hayyan Alia

The Banque Populaire Chair in Microfi nance

Burgundy School of Business

29 Rue Sambin

21000 Dijon, France

email: [email protected]

Guillermo Mateu is associate professor in the Finance, Law, and Control Department and a research fellow at LESSAC (Laboratory for Experimentation in Social Sciences and Behavioral Analysis), Burgundy School of Business, Dijon, France.

Angela Sutan is a professor in Experimental Economics in the Department of Organization Management and Entrepreneurship and the head of LESSAC (Laboratory for Experimentation in Social Sciences and Behavioral Analysis), Burgundy School of Business, Dijon, France. She is also an associate research fellow at LAMETA, Montpellier, France.

Related Documents