Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Institutional Equities

This page has been intentionally left blank

Institutional Equities

Alcoholic Beverage Sector

Initi

atin

g C

over

age

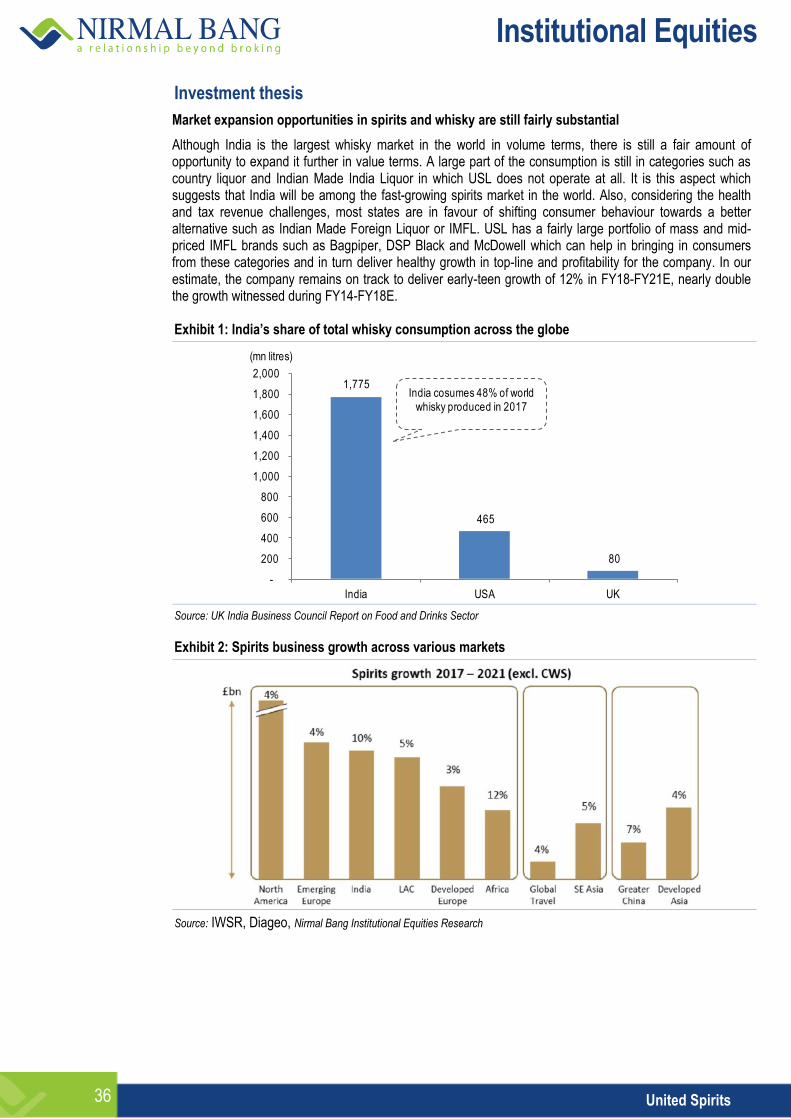

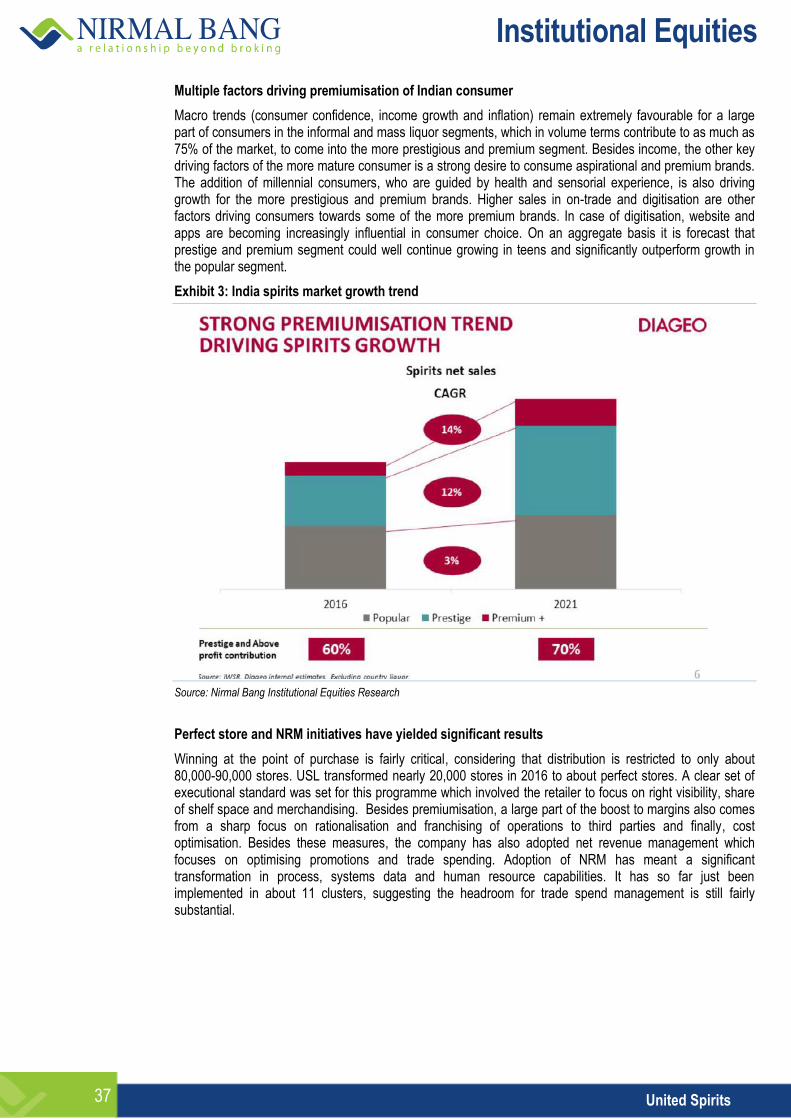

Good Food, Great Drinks India ranks among the most attractive alcoholic beverage markets in the world. Within the Indian consumer space too we expect alcoholic beverages to be the fastest-growing sub-sector during the period FY18-FY21E. We expect operating earnings to be in the vicinity of 22%, well ahead of its peers in food and personal care sectors. Several drivers such as demographics, increase in per capita spending on the back of lifestyle and premiumisation driven by improved affordability and continued innovation are driving substantial growth for the sector. Although regulation challenges are still fairly high, the responsible and sustainable strategy adopted by most companies is giving them adequate leverage with policy makers and we believe this aspect should not be a major impediment to earnings growth. We initiate coverage on the alcoholic beverage sector with a positive view and our key investment recommendations are United Breweries (UBL) and United Spirits (USL).

Robust fundamentals underpin the opportunity: Per capita consumption increase in the region of 2%-3%, which coupled with new consumer addition of a similar magnitude, should support attractive high single-digit volume growth. Although the current consumption in the country is skewed in favour of spirits, we expect beer to outpace industry growth considering that it is biased towards affluence and has a great appeal with women and youth.

Affordable luxury: Consumer evolution, lifestyles and continued increase in disposable income has resulted in most Indian consumers trading up significantly in the alcoholic beverage segment and we believe this momentum will only gain further strength with ‘less is more’ becoming a more prevalent theme. Several new innovation and product launches in the premium portfolio have also provided a further fillip to this trend, and we expect premiumisation to contribute as much as 30%-50% to annual growth of the industry.

Regulation challenges are modest: Apart from taxation, we do not envisage any major regulation challenges to the sector as most state governments appear to be much more progressive in their outlook towards alcohol purchase and consumption. If the distribution side gets a small fillip, as seen recently in Uttar Pradesh or UP, there could be significant uplift in growth rate. Governments are also mindful of price elasticity and some recent behaviour suggests that they will not be fairly disruptive in their approach.

Margin expansion likely to sustain: Despite price controls and stiff taxation challenges, most companies have managed to report margin gains over the past decade. Considering that the top-line outlook is considerably improved, we expect these trends to continue and sustain the current pace of annual expansion by 50bps-100 bps over FY18-FY21E.

Valuations attractive after consolidation: Despite reporting significantly improved earnings performance in the past 12 months, stocks of alcoholic beverages companies have largely moved sideways in line with sluggish markets. This consolidation has significantly improved their valuations and they are now trading in line or below historical valuation averages. Considering that growth will be significantly above historical averages and ahead of peers in the consumer space, we find the valuations to be attractive for the sector and have assigned Buy rating on United Breweries and United Spirits.

View: Positive

Vijay Chugh Research Analyst [email protected] +91-22-3926 8064

Company Rating Market cap

CMP (Rs)

Target price (Rs)

Up/ Down (%)

EPS (Rs) P/E (x) RoCE (%)

Rsbn US$bn FY19E FY20E FY21E FY19E FY20E FY21E FY19E FY20E FY21E

United Breweries Buy 329.2 4.6 1,237 1,525 23 22.3 27.6 33.3 55.4 44.9 37.2 28.2 29.4 29.8

United Spirits Buy 457.8 6.4 641 765 19 10.1 13.9 16.6 63.7 46.0 38.6 20.0 22.5 23.4

Source: Nirmal Bang Institutional Equities Research

13 December 2018

Institutional Equities

4 Alcoholic Beverage Sector

Table of Content

Indian alcoholic beverages could outpace food and tobacco sectors’ growth by about 300bps ………………………………………………………………………….…………………………………….…05

March of the premium Indian consumer continues…………………………………………………….....06

Digital is a key part of consumer outreach…………………………………………………..………….....07

Regulation headwinds for the industry have moderated……………………………………………….....08

Revenue growth for alcoholic beverages staging a comeback………………………………….……....10

Valuation and recommendation…………………………………………………………….……...…..…...12

Overall risks to our rating…………………………………………………………………….……...…..…...14

Companies

United Breweries …………………………….…………………………………………………...…….…….17

United Spirits ………………………………………………………………….……………….…..…....……35

Institutional Equities

5 Alcoholic Beverage Sector

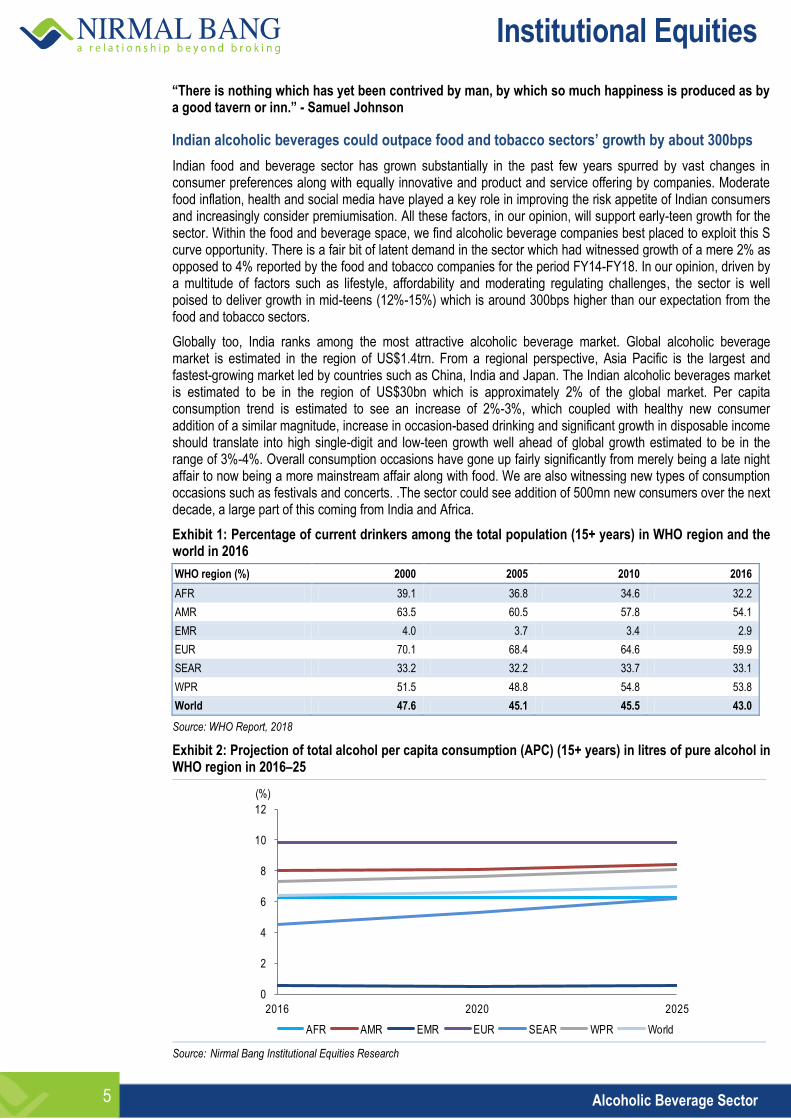

“There is nothing which has yet been contrived by man, by which so much happiness is produced as by a good tavern or inn.” - Samuel Johnson

Indian alcoholic beverages could outpace food and tobacco sectors’ growth by about 300bps

Indian food and beverage sector has grown substantially in the past few years spurred by vast changes in consumer preferences along with equally innovative and product and service offering by companies. Moderate food inflation, health and social media have played a key role in improving the risk appetite of Indian consumers and increasingly consider premiumisation. All these factors, in our opinion, will support early-teen growth for the sector. Within the food and beverage space, we find alcoholic beverage companies best placed to exploit this S curve opportunity. There is a fair bit of latent demand in the sector which had witnessed growth of a mere 2% as opposed to 4% reported by the food and tobacco companies for the period FY14-FY18. In our opinion, driven by a multitude of factors such as lifestyle, affordability and moderating regulating challenges, the sector is well poised to deliver growth in mid-teens (12%-15%) which is around 300bps higher than our expectation from the food and tobacco sectors.

Globally too, India ranks among the most attractive alcoholic beverage market. Global alcoholic beverage market is estimated in the region of US$1.4trn. From a regional perspective, Asia Pacific is the largest and fastest-growing market led by countries such as China, India and Japan. The Indian alcoholic beverages market is estimated to be in the region of US$30bn which is approximately 2% of the global market. Per capita consumption trend is estimated to see an increase of 2%-3%, which coupled with healthy new consumer addition of a similar magnitude, increase in occasion-based drinking and significant growth in disposable income should translate into high single-digit and low-teen growth well ahead of global growth estimated to be in the range of 3%-4%. Overall consumption occasions have gone up fairly significantly from merely being a late night affair to now being a more mainstream affair along with food. We are also witnessing new types of consumption occasions such as festivals and concerts. .The sector could see addition of 500mn new consumers over the next decade, a large part of this coming from India and Africa.

Exhibit 1: Percentage of current drinkers among the total population (15+ years) in WHO region and the world in 2016

WHO region (%) 2000 2005 2010 2016

AFR 39.1 36.8 34.6 32.2

AMR 63.5 60.5 57.8 54.1

EMR 4.0 3.7 3.4 2.9

EUR 70.1 68.4 64.6 59.9

SEAR 33.2 32.2 33.7 33.1

WPR 51.5 48.8 54.8 53.8

World 47.6 45.1 45.5 43.0

Source: WHO Report, 2018

Exhibit 2: Projection of total alcohol per capita consumption (APC) (15+ years) in litres of pure alcohol in WHO region in 2016–25

Source: Nirmal Bang Institutional Equities Research

0

2

4

6

8

10

12

2016 2020 2025

AFR AMR EMR EUR SEAR WPR World

(%)

Institutional Equities

6 Alcoholic Beverage Sector

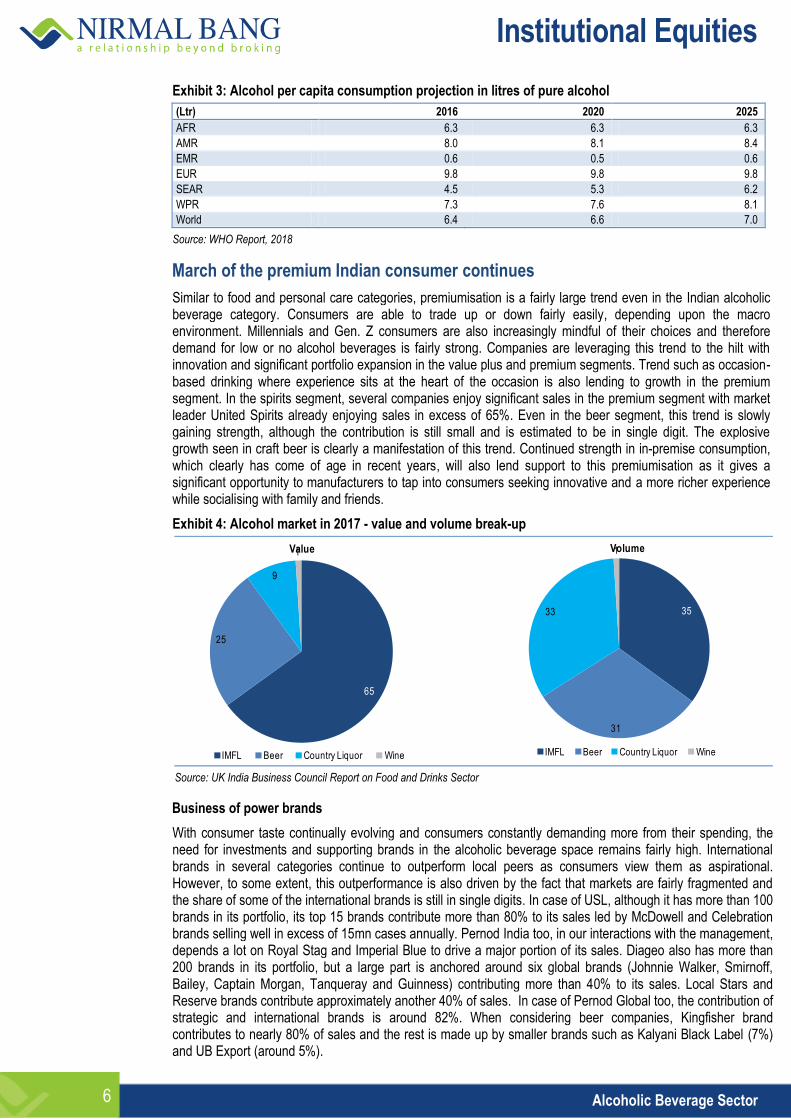

Exhibit 3: Alcohol per capita consumption projection in litres of pure alcohol

(Ltr) 2016 2020 2025

AFR 6.3 6.3 6.3

AMR 8.0 8.1 8.4

EMR 0.6 0.5 0.6

EUR 9.8 9.8 9.8

SEAR 4.5 5.3 6.2

WPR 7.3 7.6 8.1

World 6.4 6.6 7.0

Source: WHO Report, 2018

March of the premium Indian consumer continues

Similar to food and personal care categories, premiumisation is a fairly large trend even in the Indian alcoholic beverage category. Consumers are able to trade up or down fairly easily, depending upon the macro environment. Millennials and Gen. Z consumers are also increasingly mindful of their choices and therefore demand for low or no alcohol beverages is fairly strong. Companies are leveraging this trend to the hilt with innovation and significant portfolio expansion in the value plus and premium segments. Trend such as occasion-based drinking where experience sits at the heart of the occasion is also lending to growth in the premium segment. In the spirits segment, several companies enjoy significant sales in the premium segment with market leader United Spirits already enjoying sales in excess of 65%. Even in the beer segment, this trend is slowly gaining strength, although the contribution is still small and is estimated to be in single digit. The explosive growth seen in craft beer is clearly a manifestation of this trend. Continued strength in in-premise consumption, which clearly has come of age in recent years, will also lend support to this premiumisation as it gives a significant opportunity to manufacturers to tap into consumers seeking innovative and a more richer experience while socialising with family and friends.

Exhibit 4: Alcohol market in 2017 - value and volume break-up

Source: UK India Business Council Report on Food and Drinks Sector

Business of power brands

With consumer taste continually evolving and consumers constantly demanding more from their spending, the need for investments and supporting brands in the alcoholic beverage space remains fairly high. International brands in several categories continue to outperform local peers as consumers view them as aspirational. However, to some extent, this outperformance is also driven by the fact that markets are fairly fragmented and the share of some of the international brands is still in single digits. In case of USL, although it has more than 100 brands in its portfolio, its top 15 brands contribute more than 80% to its sales led by McDowell and Celebration brands selling well in excess of 15mn cases annually. Pernod India too, in our interactions with the management, depends a lot on Royal Stag and Imperial Blue to drive a major portion of its sales. Diageo also has more than 200 brands in its portfolio, but a large part is anchored around six global brands (Johnnie Walker, Smirnoff, Bailey, Captain Morgan, Tanqueray and Guinness) contributing more than 40% to its sales. Local Stars and Reserve brands contribute approximately another 40% of sales. In case of Pernod Global too, the contribution of strategic and international brands is around 82%. When considering beer companies, Kingfisher brand contributes to nearly 80% of sales and the rest is made up by smaller brands such as Kalyani Black Label (7%) and UB Export (around 5%).

65

25

9

1

IMFL Beer Country Liquor Wine

Value

35

31

33

1

IMFL Beer Country Liquor Wine

Volume

Institutional Equities

7 Alcoholic Beverage Sector

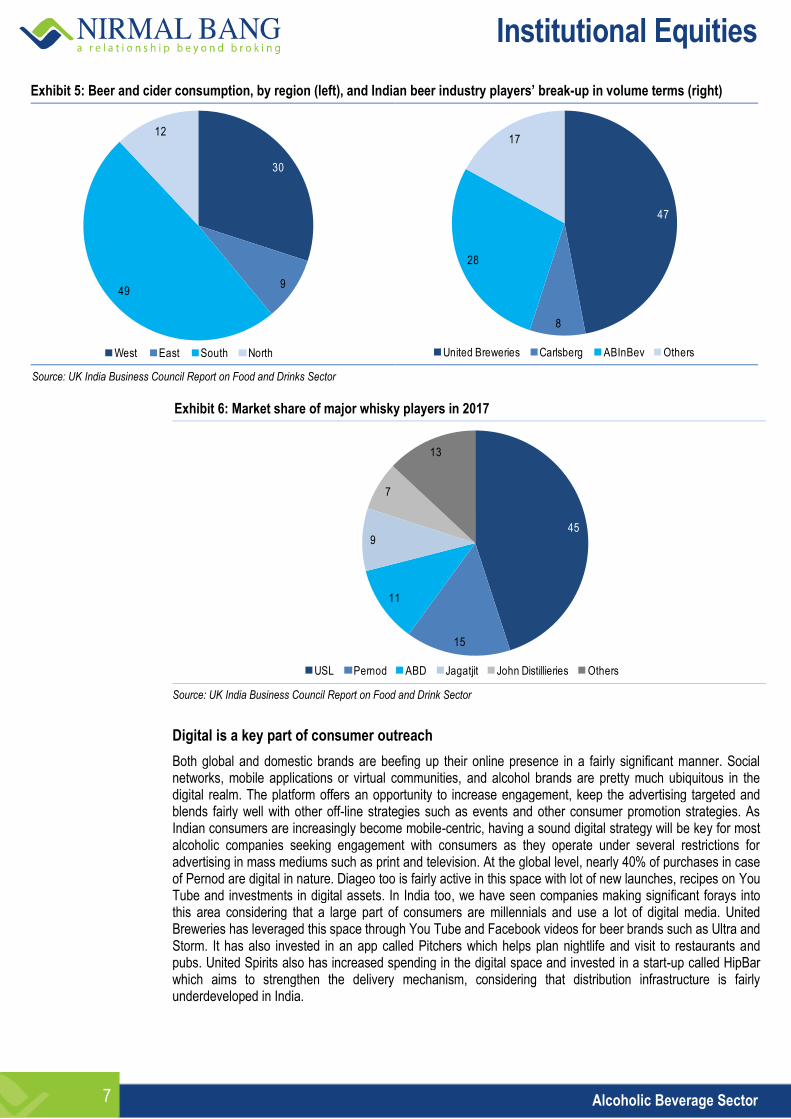

Exhibit 5: Beer and cider consumption, by region (left), and Indian beer industry players’ break-up in volume terms (right)

Source: UK India Business Council Report on Food and Drinks Sector

Exhibit 6: Market share of major whisky players in 2017

Source: UK India Business Council Report on Food and Drink Sector

Digital is a key part of consumer outreach

Both global and domestic brands are beefing up their online presence in a fairly significant manner. Social networks, mobile applications or virtual communities, and alcohol brands are pretty much ubiquitous in the digital realm. The platform offers an opportunity to increase engagement, keep the advertising targeted and blends fairly well with other off-line strategies such as events and other consumer promotion strategies. As Indian consumers are increasingly become mobile-centric, having a sound digital strategy will be key for most alcoholic companies seeking engagement with consumers as they operate under several restrictions for advertising in mass mediums such as print and television. At the global level, nearly 40% of purchases in case of Pernod are digital in nature. Diageo too is fairly active in this space with lot of new launches, recipes on You Tube and investments in digital assets. In India too, we have seen companies making significant forays into this area considering that a large part of consumers are millennials and use a lot of digital media. United Breweries has leveraged this space through You Tube and Facebook videos for beer brands such as Ultra and Storm. It has also invested in an app called Pitchers which helps plan nightlife and visit to restaurants and pubs. United Spirits also has increased spending in the digital space and invested in a start-up called HipBar which aims to strengthen the delivery mechanism, considering that distribution infrastructure is fairly underdeveloped in India.

30

949

12

West East South North

47

8

28

17

United Breweries Carlsberg ABInBev Others

45

15

11

9

7

13

USL Pernod ABD Jagatjit John Distillieries Others

Institutional Equities

8 Alcoholic Beverage Sector

Regulation headwinds for the industry have moderated

Although there are a myriad of regulations impacting production and sale of alcoholic beverages in India, the current trend does seem to suggest that regulation is looking to balance the interests of consumers, industry and other stakeholders. Many alcoholic beverage manufacturers are practicing responsibility and sustainability as a part of their strategy. As part of their CSR efforts, they are supporting road safety, responsible drinking and women empowerment in a significant manner. All these good corporate citizen efforts are providing enough leverage with policy makers and public health professionals. As opposed to the past, most alcoholic companies are in a fairly good position to shape the regulatory landscape. Prohibition risk, which ranks as the highest for the industry, has not so far been raised by politicians in the current election narrative except for Chhattisgarh where the Congress has stated that it may consider prohibition. The more accommodative stance by Kerala government after a sharp drop in tourist arrivals and more recently the changes made by Supreme Court to its highway liquor store ban order does indicate that multiple stakeholders needs to be balanced. In Uttar Pradesh, the government has taken several steps to end the erstwhile distribution monopoly and enable more free trade.

Pricing controls and taxation have been the other areas of significant challenge. Although pricing controls are unlikely to change, most states have been progressive in their attitude towards manufacturers and they received significant pricing support in FY18. Taxation challenges too have been acknowledge by states considering the price elasticity of products, especially in the mid and mass segments. On aggregate basis, we have seen the pace of expansion drop to around 3%. After raising taxes on beer significantly in December 2017, Maharashtra government acknowledged the impact it had on demand and took a fair bit of course correction in August 2018. Even on the taxation side, after a sharp increase in taxes in FY16, we have seen a fair bit of moderation in the taxation rate. In the past too we have observed that major excise duty revision usually take up to five years. As per our current estimates, the next major excise duty revision is not due until FY21. Premiumisation and improved affordability should also reduce the price elasticity witnessed after a steep taxation increase in the past.

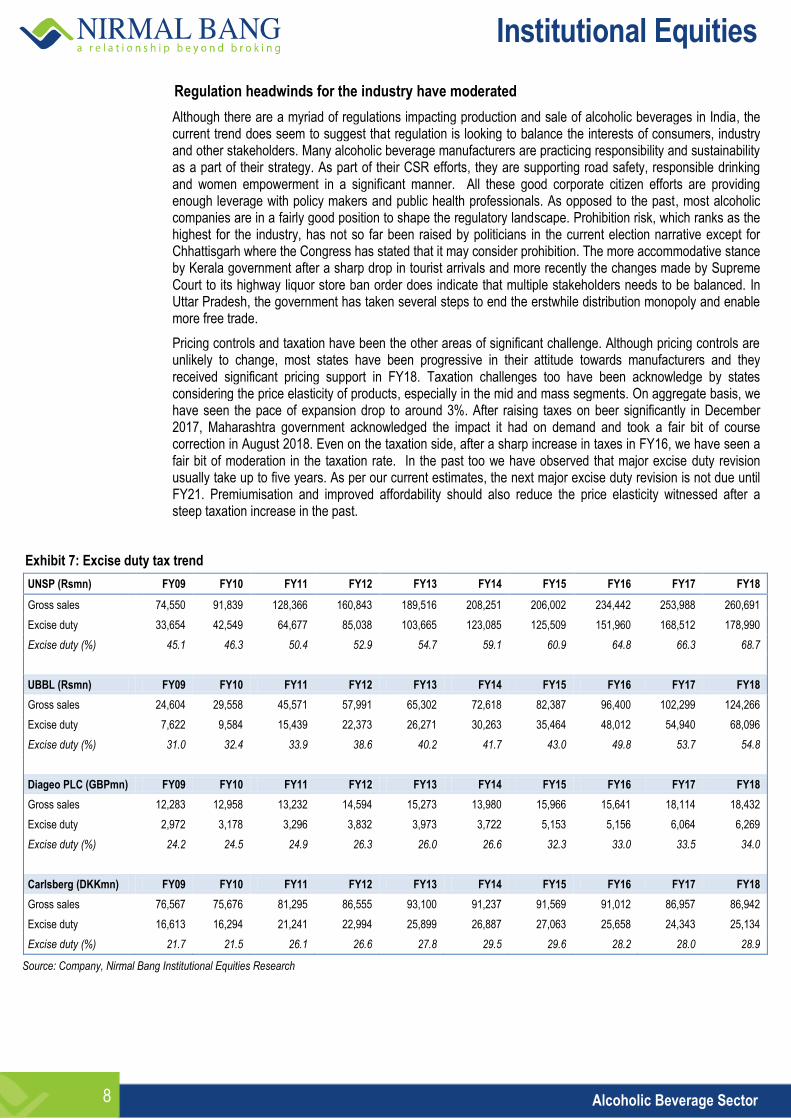

Exhibit 7: Excise duty tax trend

UNSP (Rsmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 74,550 91,839 128,366 160,843 189,516 208,251 206,002 234,442 253,988 260,691

Excise duty 33,654 42,549 64,677 85,038 103,665 123,085 125,509 151,960 168,512 178,990

Excise duty (%) 45.1 46.3 50.4 52.9 54.7 59.1 60.9 64.8 66.3 68.7

UBBL (Rsmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 24,604 29,558 45,571 57,991 65,302 72,618 82,387 96,400 102,299 124,266

Excise duty 7,622 9,584 15,439 22,373 26,271 30,263 35,464 48,012 54,940 68,096

Excise duty (%) 31.0 32.4 33.9 38.6 40.2 41.7 43.0 49.8 53.7 54.8

Diageo PLC (GBPmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 12,283 12,958 13,232 14,594 15,273 13,980 15,966 15,641 18,114 18,432

Excise duty 2,972 3,178 3,296 3,832 3,973 3,722 5,153 5,156 6,064 6,269

Excise duty (%) 24.2 24.5 24.9 26.3 26.0 26.6 32.3 33.0 33.5 34.0

Carlsberg (DKKmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 76,567 75,676 81,295 86,555 93,100 91,237 91,569 91,012 86,957 86,942

Excise duty 16,613 16,294 21,241 22,994 25,899 26,887 27,063 25,658 24,343 25,134

Excise duty (%) 21.7 21.5 26.1 26.6 27.8 29.5 29.6 28.2 28.0 28.9

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

9 Alcoholic Beverage Sector

Health and Premiumisation are key mega trends driving global alcoholic beverage markets

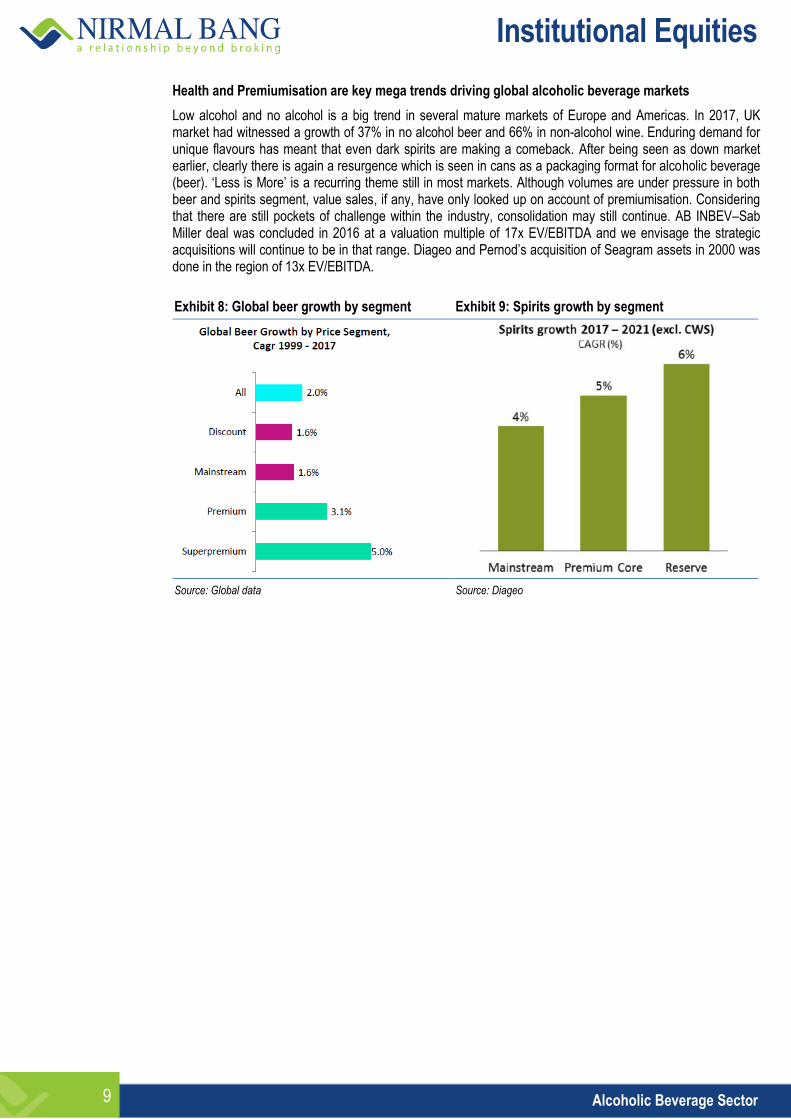

Low alcohol and no alcohol is a big trend in several mature markets of Europe and Americas. In 2017, UK market had witnessed a growth of 37% in no alcohol beer and 66% in non-alcohol wine. Enduring demand for unique flavours has meant that even dark spirits are making a comeback. After being seen as down market earlier, clearly there is again a resurgence which is seen in cans as a packaging format for alcoholic beverage (beer). ‘Less is More’ is a recurring theme still in most markets. Although volumes are under pressure in both beer and spirits segment, value sales, if any, have only looked up on account of premiumisation. Considering that there are still pockets of challenge within the industry, consolidation may still continue. AB INBEV–Sab Miller deal was concluded in 2016 at a valuation multiple of 17x EV/EBITDA and we envisage the strategic acquisitions will continue to be in that range. Diageo and Pernod’s acquisition of Seagram assets in 2000 was done in the region of 13x EV/EBITDA.

Exhibit 8: Global beer growth by segment Exhibit 9: Spirits growth by segment

Source: Global data Source: Diageo

Institutional Equities

10 Alcoholic Beverage Sector

Sector financials

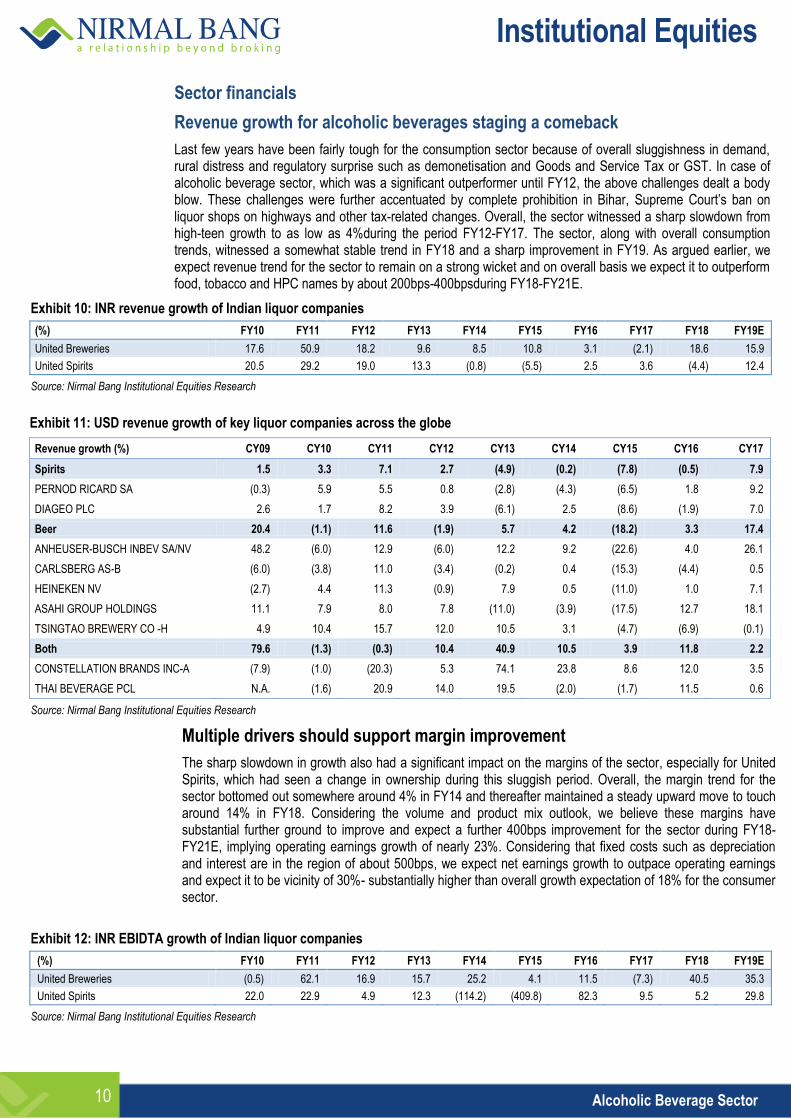

Revenue growth for alcoholic beverages staging a comeback

Last few years have been fairly tough for the consumption sector because of overall sluggishness in demand, rural distress and regulatory surprise such as demonetisation and Goods and Service Tax or GST. In case of alcoholic beverage sector, which was a significant outperformer until FY12, the above challenges dealt a body blow. These challenges were further accentuated by complete prohibition in Bihar, Supreme Court’s ban on liquor shops on highways and other tax-related changes. Overall, the sector witnessed a sharp slowdown from high-teen growth to as low as 4%during the period FY12-FY17. The sector, along with overall consumption trends, witnessed a somewhat stable trend in FY18 and a sharp improvement in FY19. As argued earlier, we expect revenue trend for the sector to remain on a strong wicket and on overall basis we expect it to outperform food, tobacco and HPC names by about 200bps-400bpsduring FY18-FY21E.

Exhibit 10: INR revenue growth of Indian liquor companies

(%) FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E

United Breweries 17.6 50.9 18.2 9.6 8.5 10.8 3.1 (2.1) 18.6 15.9

United Spirits 20.5 29.2 19.0 13.3 (0.8) (5.5) 2.5 3.6 (4.4) 12.4

Source: Nirmal Bang Institutional Equities Research

Exhibit 11: USD revenue growth of key liquor companies across the globe

Revenue growth (%) CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Spirits 1.5 3.3 7.1 2.7 (4.9) (0.2) (7.8) (0.5) 7.9

PERNOD RICARD SA (0.3) 5.9 5.5 0.8 (2.8) (4.3) (6.5) 1.8 9.2

DIAGEO PLC 2.6 1.7 8.2 3.9 (6.1) 2.5 (8.6) (1.9) 7.0

Beer 20.4 (1.1) 11.6 (1.9) 5.7 4.2 (18.2) 3.3 17.4

ANHEUSER-BUSCH INBEV SA/NV 48.2 (6.0) 12.9 (6.0) 12.2 9.2 (22.6) 4.0 26.1

CARLSBERG AS-B (6.0) (3.8) 11.0 (3.4) (0.2) 0.4 (15.3) (4.4) 0.5

HEINEKEN NV (2.7) 4.4 11.3 (0.9) 7.9 0.5 (11.0) 1.0 7.1

ASAHI GROUP HOLDINGS 11.1 7.9 8.0 7.8 (11.0) (3.9) (17.5) 12.7 18.1

TSINGTAO BREWERY CO -H 4.9 10.4 15.7 12.0 10.5 3.1 (4.7) (6.9) (0.1)

Both 79.6 (1.3) (0.3) 10.4 40.9 10.5 3.9 11.8 2.2

CONSTELLATION BRANDS INC-A (7.9) (1.0) (20.3) 5.3 74.1 23.8 8.6 12.0 3.5

THAI BEVERAGE PCL N.A. (1.6) 20.9 14.0 19.5 (2.0) (1.7) 11.5 0.6

Source: Nirmal Bang Institutional Equities Research

Multiple drivers should support margin improvement

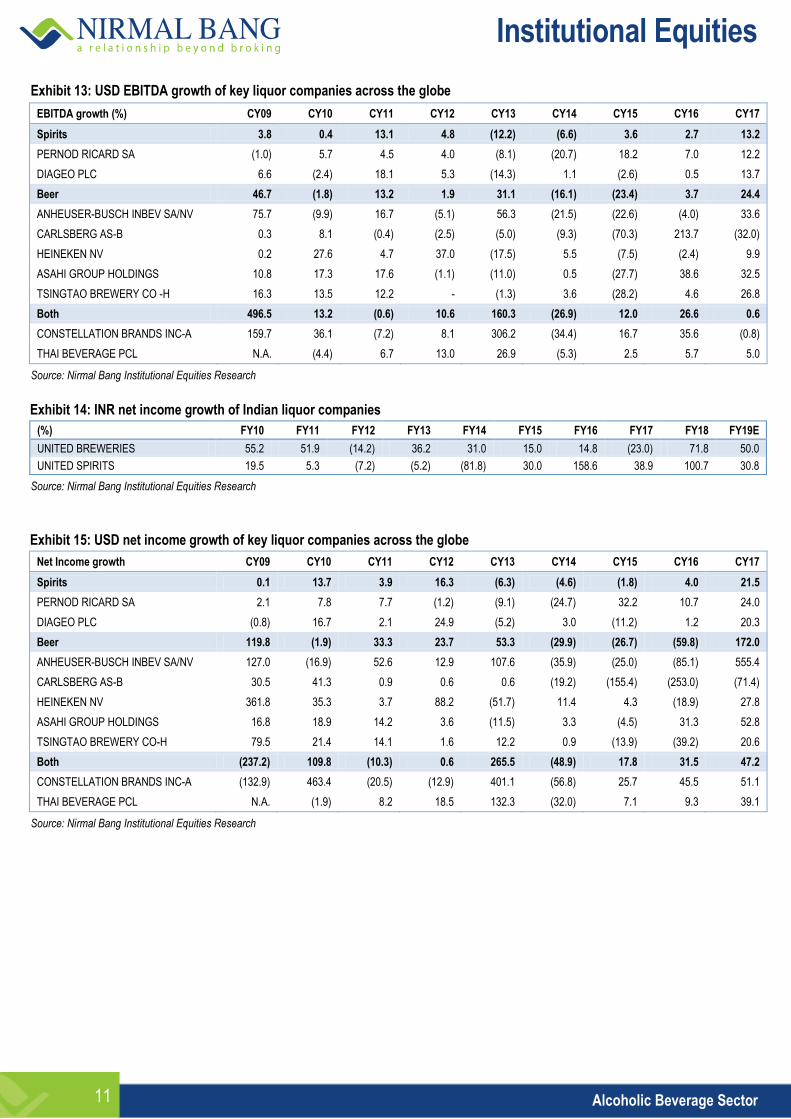

The sharp slowdown in growth also had a significant impact on the margins of the sector, especially for United Spirits, which had seen a change in ownership during this sluggish period. Overall, the margin trend for the sector bottomed out somewhere around 4% in FY14 and thereafter maintained a steady upward move to touch around 14% in FY18. Considering the volume and product mix outlook, we believe these margins have substantial further ground to improve and expect a further 400bps improvement for the sector during FY18-FY21E, implying operating earnings growth of nearly 23%. Considering that fixed costs such as depreciation and interest are in the region of about 500bps, we expect net earnings growth to outpace operating earnings and expect it to be vicinity of 30%- substantially higher than overall growth expectation of 18% for the consumer sector.

Exhibit 12: INR EBIDTA growth of Indian liquor companies

(%) FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E

United Breweries (0.5) 62.1 16.9 15.7 25.2 4.1 11.5 (7.3) 40.5 35.3

United Spirits 22.0 22.9 4.9 12.3 (114.2) (409.8) 82.3 9.5 5.2 29.8

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

11 Alcoholic Beverage Sector

Exhibit 13: USD EBITDA growth of key liquor companies across the globe

EBITDA growth (%) CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Spirits 3.8 0.4 13.1 4.8 (12.2) (6.6) 3.6 2.7 13.2

PERNOD RICARD SA (1.0) 5.7 4.5 4.0 (8.1) (20.7) 18.2 7.0 12.2

DIAGEO PLC 6.6 (2.4) 18.1 5.3 (14.3) 1.1 (2.6) 0.5 13.7

Beer 46.7 (1.8) 13.2 1.9 31.1 (16.1) (23.4) 3.7 24.4

ANHEUSER-BUSCH INBEV SA/NV 75.7 (9.9) 16.7 (5.1) 56.3 (21.5) (22.6) (4.0) 33.6

CARLSBERG AS-B 0.3 8.1 (0.4) (2.5) (5.0) (9.3) (70.3) 213.7 (32.0)

HEINEKEN NV 0.2 27.6 4.7 37.0 (17.5) 5.5 (7.5) (2.4) 9.9

ASAHI GROUP HOLDINGS 10.8 17.3 17.6 (1.1) (11.0) 0.5 (27.7) 38.6 32.5

TSINGTAO BREWERY CO -H 16.3 13.5 12.2 - (1.3) 3.6 (28.2) 4.6 26.8

Both 496.5 13.2 (0.6) 10.6 160.3 (26.9) 12.0 26.6 0.6

CONSTELLATION BRANDS INC-A 159.7 36.1 (7.2) 8.1 306.2 (34.4) 16.7 35.6 (0.8)

THAI BEVERAGE PCL N.A. (4.4) 6.7 13.0 26.9 (5.3) 2.5 5.7 5.0

Source: Nirmal Bang Institutional Equities Research

Exhibit 14: INR net income growth of Indian liquor companies

(%) FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E

UNITED BREWERIES 55.2 51.9 (14.2) 36.2 31.0 15.0 14.8 (23.0) 71.8 50.0

UNITED SPIRITS 19.5 5.3 (7.2) (5.2) (81.8) 30.0 158.6 38.9 100.7 30.8

Source: Nirmal Bang Institutional Equities Research

Exhibit 15: USD net income growth of key liquor companies across the globe

Net Income growth CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Spirits 0.1 13.7 3.9 16.3 (6.3) (4.6) (1.8) 4.0 21.5

PERNOD RICARD SA 2.1 7.8 7.7 (1.2) (9.1) (24.7) 32.2 10.7 24.0

DIAGEO PLC (0.8) 16.7 2.1 24.9 (5.2) 3.0 (11.2) 1.2 20.3

Beer 119.8 (1.9) 33.3 23.7 53.3 (29.9) (26.7) (59.8) 172.0

ANHEUSER-BUSCH INBEV SA/NV 127.0 (16.9) 52.6 12.9 107.6 (35.9) (25.0) (85.1) 555.4

CARLSBERG AS-B 30.5 41.3 0.9 0.6 0.6 (19.2) (155.4) (253.0) (71.4)

HEINEKEN NV 361.8 35.3 3.7 88.2 (51.7) 11.4 4.3 (18.9) 27.8

ASAHI GROUP HOLDINGS 16.8 18.9 14.2 3.6 (11.5) 3.3 (4.5) 31.3 52.8

TSINGTAO BREWERY CO-H 79.5 21.4 14.1 1.6 12.2 0.9 (13.9) (39.2) 20.6

Both (237.2) 109.8 (10.3) 0.6 265.5 (48.9) 17.8 31.5 47.2

CONSTELLATION BRANDS INC-A (132.9) 463.4 (20.5) (12.9) 401.1 (56.8) 25.7 45.5 51.1

THAI BEVERAGE PCL N.A. (1.9) 8.2 18.5 132.3 (32.0) 7.1 9.3 39.1

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

12 Alcoholic Beverage Sector

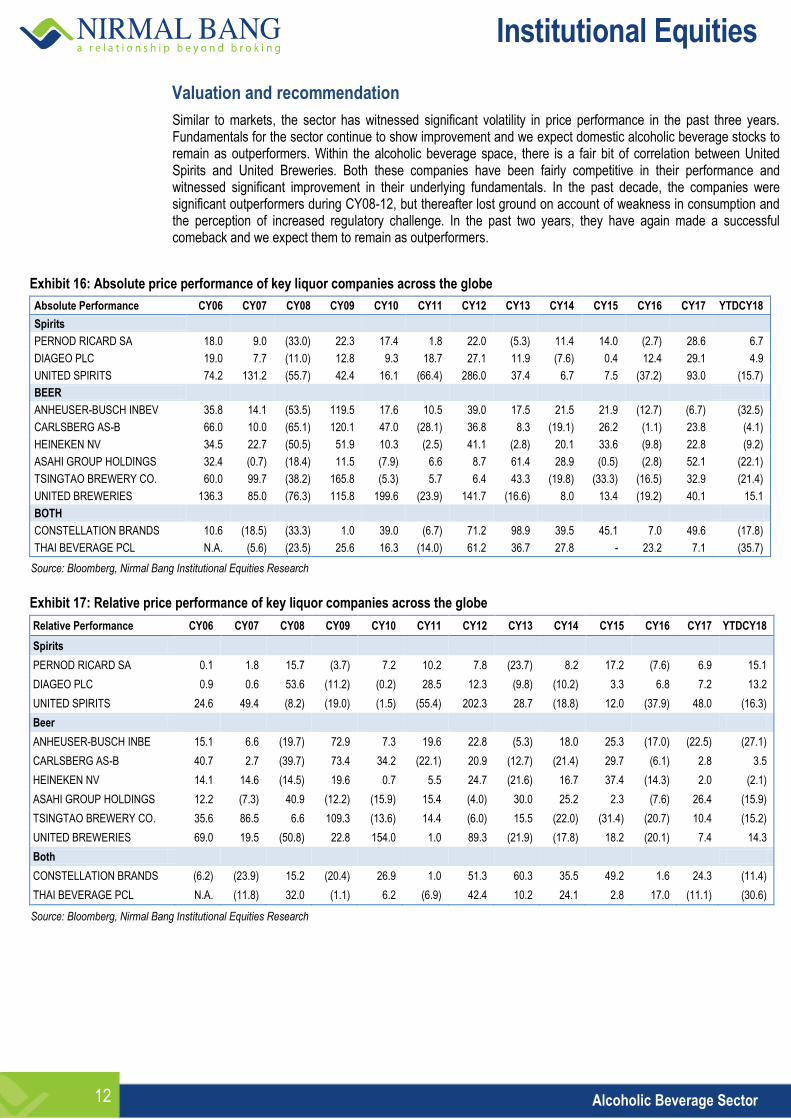

Valuation and recommendation

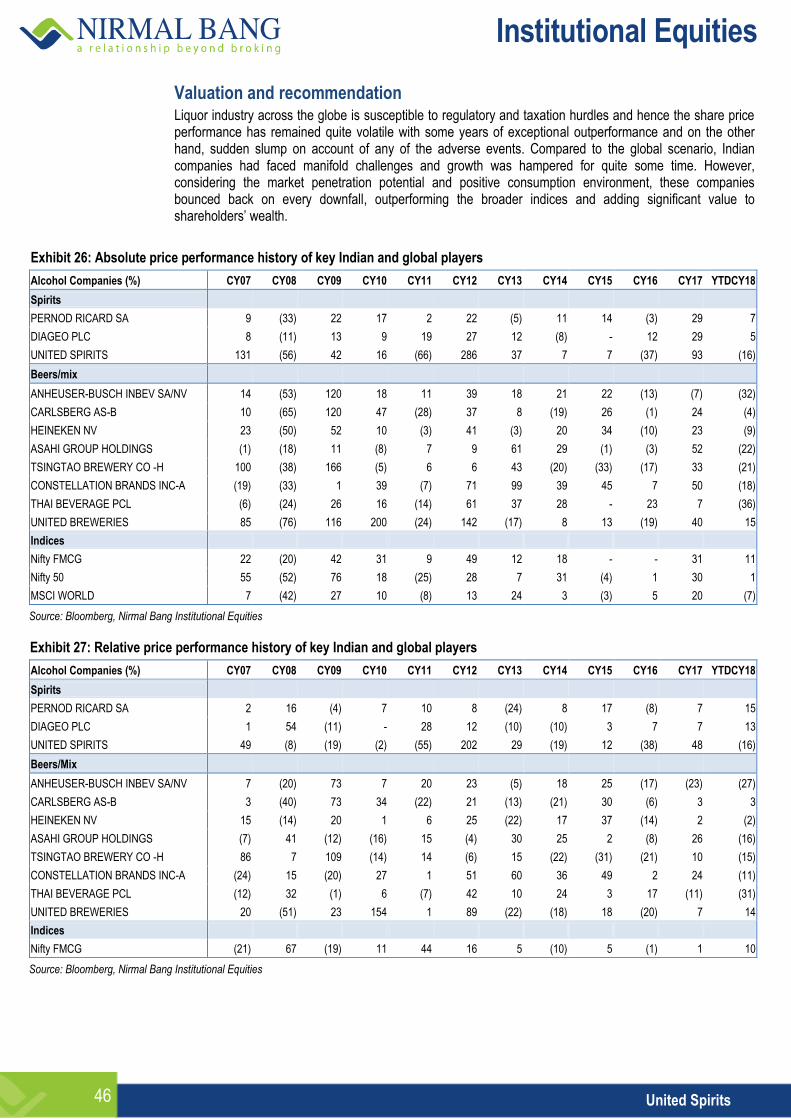

Similar to markets, the sector has witnessed significant volatility in price performance in the past three years. Fundamentals for the sector continue to show improvement and we expect domestic alcoholic beverage stocks to remain as outperformers. Within the alcoholic beverage space, there is a fair bit of correlation between United Spirits and United Breweries. Both these companies have been fairly competitive in their performance and witnessed significant improvement in their underlying fundamentals. In the past decade, the companies were significant outperformers during CY08-12, but thereafter lost ground on account of weakness in consumption and the perception of increased regulatory challenge. In the past two years, they have again made a successful comeback and we expect them to remain as outperformers.

Exhibit 16: Absolute price performance of key liquor companies across the globe

Absolute Performance CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 YTDCY18

Spirits

PERNOD RICARD SA 18.0 9.0 (33.0) 22.3 17.4 1.8 22.0 (5.3) 11.4 14.0 (2.7) 28.6 6.7

DIAGEO PLC 19.0 7.7 (11.0) 12.8 9.3 18.7 27.1 11.9 (7.6) 0.4 12.4 29.1 4.9

UNITED SPIRITS 74.2 131.2 (55.7) 42.4 16.1 (66.4) 286.0 37.4 6.7 7.5 (37.2) 93.0 (15.7)

BEER

ANHEUSER-BUSCH INBEV 35.8 14.1 (53.5) 119.5 17.6 10.5 39.0 17.5 21.5 21.9 (12.7) (6.7) (32.5)

CARLSBERG AS-B 66.0 10.0 (65.1) 120.1 47.0 (28.1) 36.8 8.3 (19.1) 26.2 (1.1) 23.8 (4.1)

HEINEKEN NV 34.5 22.7 (50.5) 51.9 10.3 (2.5) 41.1 (2.8) 20.1 33.6 (9.8) 22.8 (9.2)

ASAHI GROUP HOLDINGS 32.4 (0.7) (18.4) 11.5 (7.9) 6.6 8.7 61.4 28.9 (0.5) (2.8) 52.1 (22.1)

TSINGTAO BREWERY CO. 60.0 99.7 (38.2) 165.8 (5.3) 5.7 6.4 43.3 (19.8) (33.3) (16.5) 32.9 (21.4)

UNITED BREWERIES 136.3 85.0 (76.3) 115.8 199.6 (23.9) 141.7 (16.6) 8.0 13.4 (19.2) 40.1 15.1

BOTH

CONSTELLATION BRANDS 10.6 (18.5) (33.3) 1.0 39.0 (6.7) 71.2 98.9 39.5 45.1 7.0 49.6 (17.8)

THAI BEVERAGE PCL N.A. (5.6) (23.5) 25.6 16.3 (14.0) 61.2 36.7 27.8 - 23.2 7.1 (35.7)

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 17: Relative price performance of key liquor companies across the globe

Relative Performance CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 YTDCY18

Spirits

PERNOD RICARD SA 0.1 1.8 15.7 (3.7) 7.2 10.2 7.8 (23.7) 8.2 17.2 (7.6) 6.9 15.1

DIAGEO PLC 0.9 0.6 53.6 (11.2) (0.2) 28.5 12.3 (9.8) (10.2) 3.3 6.8 7.2 13.2

UNITED SPIRITS 24.6 49.4 (8.2) (19.0) (1.5) (55.4) 202.3 28.7 (18.8) 12.0 (37.9) 48.0 (16.3)

Beer

ANHEUSER-BUSCH INBE 15.1 6.6 (19.7) 72.9 7.3 19.6 22.8 (5.3) 18.0 25.3 (17.0) (22.5) (27.1)

CARLSBERG AS-B 40.7 2.7 (39.7) 73.4 34.2 (22.1) 20.9 (12.7) (21.4) 29.7 (6.1) 2.8 3.5

HEINEKEN NV 14.1 14.6 (14.5) 19.6 0.7 5.5 24.7 (21.6) 16.7 37.4 (14.3) 2.0 (2.1)

ASAHI GROUP HOLDINGS 12.2 (7.3) 40.9 (12.2) (15.9) 15.4 (4.0) 30.0 25.2 2.3 (7.6) 26.4 (15.9)

TSINGTAO BREWERY CO. 35.6 86.5 6.6 109.3 (13.6) 14.4 (6.0) 15.5 (22.0) (31.4) (20.7) 10.4 (15.2)

UNITED BREWERIES 69.0 19.5 (50.8) 22.8 154.0 1.0 89.3 (21.9) (17.8) 18.2 (20.1) 7.4 14.3

Both

CONSTELLATION BRANDS (6.2) (23.9) 15.2 (20.4) 26.9 1.0 51.3 60.3 35.5 49.2 1.6 24.3 (11.4)

THAI BEVERAGE PCL N.A. (11.8) 32.0 (1.1) 6.2 (6.9) 42.4 10.2 24.1 2.8 17.0 (11.1) (30.6)

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

13 Alcoholic Beverage Sector

Exhibit 18: Relative (Nifty) price performance of Indian FMCG players

Relative performance (%) CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 YTDCY18

Home and Personal care

DABUR INDIA (0.4) (24.7) 52.6 7.6 7.0 31.6 1.5 23.8 4.4 23.5 (2.5) (2.3) 15.7

COLGATE PALMOLIVE (INDIA) 3.2 (32.4) 107.2 (7.7) 11.9 51.1 23.9 (19.1) 0.4 13.6 (9.7) (5.5) (0.6)

HINDUSTAN UNILEVER (21.5) (36.2) 143.0 (39.8) 0.2 72.7 0.9 1.8 1.4 18.3 (7.0) 28.7 12.5

EMAMI INDIA 45.6 (20.3) 45.3 24.9 39.3 12.1 37.6 11.1 26.3 32.4 (7.6) 8.7 (33.2)

PROCTOR & GAMBLE HYGIENE (28.2) (41.0) 104.0 28.9 (9.2) 33.8 14.5 3.3 45.2 1.3 22.1 3.1 (3.2)

GILLETTE INDIA (16.1) 2.3 9.4 2.9 22.1 40.6 (1.6) (22.0) 21.4 47.8 (10.5) 22.2 (2.3)

MARICO 5.4 (18.3) 67.7 5.7 (1.6) 61.1 17.5 (4.7) 14.2 45.0 11.8 (3.7) (1.9)

GODREJ CONSUMER PROD (18.4) (41.3) 113.5 8.1 24.4 32.2 46.7 11.3 (13.7) 41.4 11.1 2.9 12.3

JYOTHI LABORATORIES - - (9.8) 32.0 31.3 (20.7) 57.9 9.3 4.3 25.8 4.8 (56.1) 1.3

F&B and Tobacco

NESTLE INDIA (13.2) (14.7) 100.9 (0.2) 26.9 42.4 (4.5) (0.8) (8.1) (4.9) 0.4 1.5 23.1

BRITANNIA INDUSTRIES (42.5) (13.0) 86.2 (27.7) 4.3 43.9 (12.9) 72.9 52.1 68.0 (5.5) 26.8 20.4

ITC (11.4) (23.1) 70.0 (16.9) 18.1 52.9 11.6 5.1 (12.8) (7.3) 7.3 (15.3) 6.8

GLAXOSMITHKLINECONSUMER (27.4) (15.7) 58.8 30.6 52.5 44.1 17.3 9.3 0.5 13.9 (24.2) 1.6 6.0

UNITED SPIRITS 24.6 49.4 (8.2) (19.0) (1.5) (55.4) 202.3 28.7 (18.8) 12.0 (37.0) 46.8 (28.6)

VST INDUSTRIES (41.9) (38.7) 16.2 43.3 0.9 128.5 41.0 (16.5) (16.7) (6.9) 37.5 3.6 (11.0)

UNITED BREWERIES (21.8) 24.6 (59.0) 73.2 (3.4) (15.5) 163.8 (23.5) 40.6 58.4 50.2 45.4 (36.3)

Others

TITAN CO. (24.3) 17.4 23.0 (12.6) 114.1 26.2 30.2 (24.4) 26.6 (5.2) (8.6) 104.1 (6.0)

JUBILANT FOODWORKS N.A. N.A. N.A. N.A. N.A. 60.0 33.7 (7.5) (17.6) 12.3 (44.2) 60.4 37.6

WESTLIFE DEVELOPMENT N.A. N.A. N.A. N.A. N.A. N.A. 605.0 853.4 (36.7) (20.1) (32.1) 54.5 0.6

ASIAN PAINTS (9.0) (3.5) 68.8 14.2 35.8 19.5 33.9 3.6 16.9 22.4 (2.1) 1.1 8.9

NIFTY FMCG INDEX (16.3) (21.0) 66.8 (19.4) 10.7 44.0 16.3 5.1 (10.0) 4.6 (0.2) 0.6 5.6

Source: Bloomberg, Nirmal Bang Institutional Equities Research

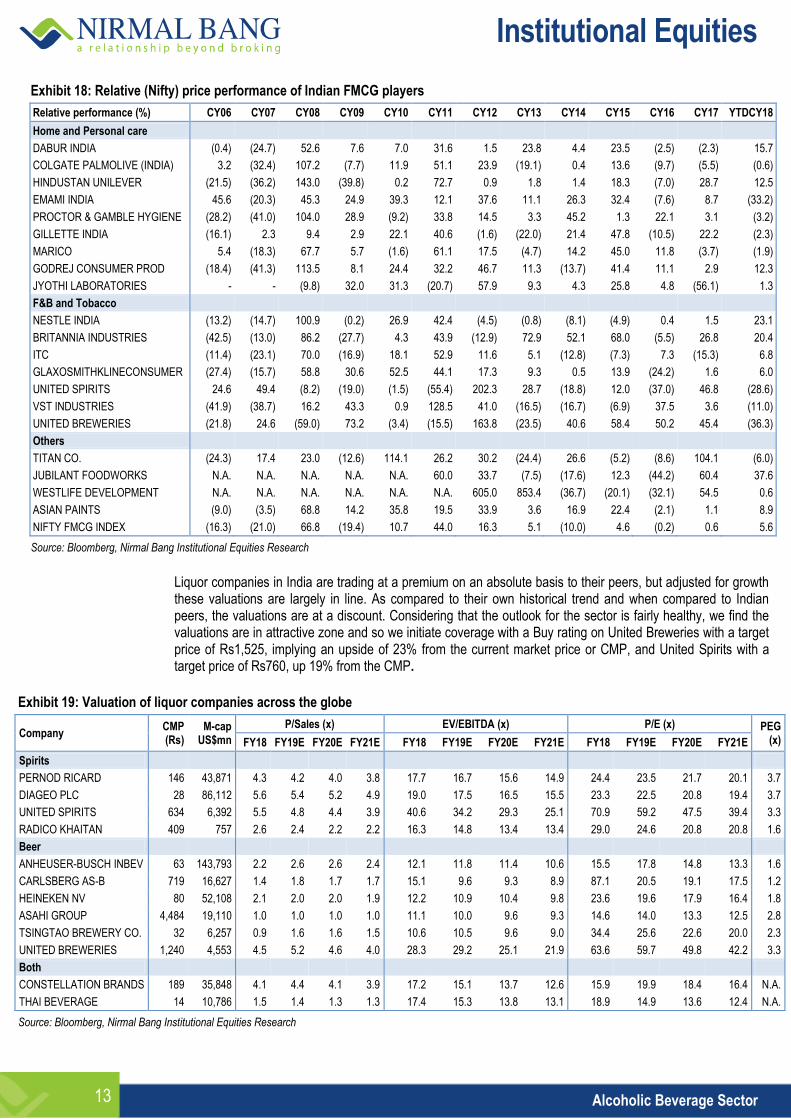

Liquor companies in India are trading at a premium on an absolute basis to their peers, but adjusted for growth these valuations are largely in line. As compared to their own historical trend and when compared to Indian peers, the valuations are at a discount. Considering that the outlook for the sector is fairly healthy, we find the valuations are in attractive zone and so we initiate coverage with a Buy rating on United Breweries with a target price of Rs1,525, implying an upside of 23% from the current market price or CMP, and United Spirits with a target price of Rs760, up 19% from the CMP.

Exhibit 19: Valuation of liquor companies across the globe

Company CMP (Rs)

M-cap US$mn

P/Sales (x) EV/EBITDA (x) P/E (x) PEG (x) FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E

Spirits

PERNOD RICARD 146 43,871 4.3 4.2 4.0 3.8 17.7 16.7 15.6 14.9 24.4 23.5 21.7 20.1 3.7

DIAGEO PLC 28 86,112 5.6 5.4 5.2 4.9 19.0 17.5 16.5 15.5 23.3 22.5 20.8 19.4 3.7

UNITED SPIRITS 634 6,392 5.5 4.8 4.4 3.9 40.6 34.2 29.3 25.1 70.9 59.2 47.5 39.4 3.3

RADICO KHAITAN 409 757 2.6 2.4 2.2 2.2 16.3 14.8 13.4 13.4 29.0 24.6 20.8 20.8 1.6

Beer

ANHEUSER-BUSCH INBEV 63 143,793 2.2 2.6 2.6 2.4 12.1 11.8 11.4 10.6 15.5 17.8 14.8 13.3 1.6

CARLSBERG AS-B 719 16,627 1.4 1.8 1.7 1.7 15.1 9.6 9.3 8.9 87.1 20.5 19.1 17.5 1.2

HEINEKEN NV 80 52,108 2.1 2.0 2.0 1.9 12.2 10.9 10.4 9.8 23.6 19.6 17.9 16.4 1.8

ASAHI GROUP 4,484 19,110 1.0 1.0 1.0 1.0 11.1 10.0 9.6 9.3 14.6 14.0 13.3 12.5 2.8

TSINGTAO BREWERY CO. 32 6,257 0.9 1.6 1.6 1.5 10.6 10.5 9.6 9.0 34.4 25.6 22.6 20.0 2.3

UNITED BREWERIES 1,240 4,553 4.5 5.2 4.6 4.0 28.3 29.2 25.1 21.9 63.6 59.7 49.8 42.2 3.3

Both

CONSTELLATION BRANDS 189 35,848 4.1 4.4 4.1 3.9 17.2 15.1 13.7 12.6 15.9 19.9 18.4 16.4 N.A.

THAI BEVERAGE 14 10,786 1.5 1.4 1.3 1.3 17.4 15.3 13.8 13.1 18.9 14.9 13.6 12.4 N.A.

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

14 Alcoholic Beverage Sector

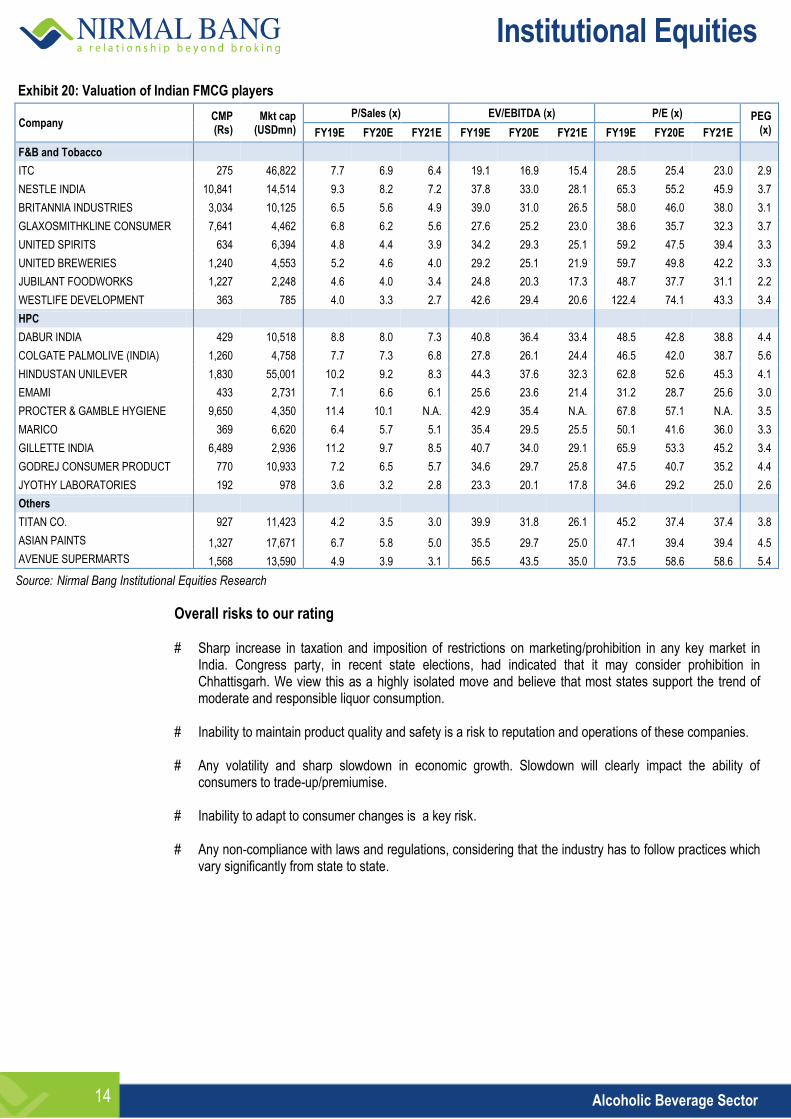

Exhibit 20: Valuation of Indian FMCG players

Company CMP (Rs)

Mkt cap (USDmn)

P/Sales (x) EV/EBITDA (x) P/E (x) PEG (x) FY19E FY20E FY21E FY19E FY20E FY21E FY19E FY20E FY21E

F&B and Tobacco

ITC 275 46,822 7.7 6.9 6.4 19.1 16.9 15.4 28.5 25.4 23.0 2.9

NESTLE INDIA 10,841 14,514 9.3 8.2 7.2 37.8 33.0 28.1 65.3 55.2 45.9 3.7

BRITANNIA INDUSTRIES 3,034 10,125 6.5 5.6 4.9 39.0 31.0 26.5 58.0 46.0 38.0 3.1

GLAXOSMITHKLINE CONSUMER 7,641 4,462 6.8 6.2 5.6 27.6 25.2 23.0 38.6 35.7 32.3 3.7

UNITED SPIRITS 634 6,394 4.8 4.4 3.9 34.2 29.3 25.1 59.2 47.5 39.4 3.3

UNITED BREWERIES 1,240 4,553 5.2 4.6 4.0 29.2 25.1 21.9 59.7 49.8 42.2 3.3

JUBILANT FOODWORKS 1,227 2,248 4.6 4.0 3.4 24.8 20.3 17.3 48.7 37.7 31.1 2.2

WESTLIFE DEVELOPMENT 363 785 4.0 3.3 2.7 42.6 29.4 20.6 122.4 74.1 43.3 3.4

HPC

DABUR INDIA 429 10,518 8.8 8.0 7.3 40.8 36.4 33.4 48.5 42.8 38.8 4.4

COLGATE PALMOLIVE (INDIA) 1,260 4,758 7.7 7.3 6.8 27.8 26.1 24.4 46.5 42.0 38.7 5.6

HINDUSTAN UNILEVER 1,830 55,001 10.2 9.2 8.3 44.3 37.6 32.3 62.8 52.6 45.3 4.1

EMAMI 433 2,731 7.1 6.6 6.1 25.6 23.6 21.4 31.2 28.7 25.6 3.0

PROCTER & GAMBLE HYGIENE 9,650 4,350 11.4 10.1 N.A. 42.9 35.4 N.A. 67.8 57.1 N.A. 3.5

MARICO 369 6,620 6.4 5.7 5.1 35.4 29.5 25.5 50.1 41.6 36.0 3.3

GILLETTE INDIA 6,489 2,936 11.2 9.7 8.5 40.7 34.0 29.1 65.9 53.3 45.2 3.4

GODREJ CONSUMER PRODUCT 770 10,933 7.2 6.5 5.7 34.6 29.7 25.8 47.5 40.7 35.2 4.4

JYOTHY LABORATORIES 192 978 3.6 3.2 2.8 23.3 20.1 17.8 34.6 29.2 25.0 2.6

Others

TITAN CO. 927 11,423 4.2 3.5 3.0 39.9 31.8 26.1 45.2 37.4 37.4 3.8

ASIAN PAINTS 1,327 17,671 6.7 5.8 5.0 35.5 29.7 25.0 47.1 39.4 39.4 4.5

AVENUE SUPERMARTS 1,568 13,590 4.9 3.9 3.1 56.5 43.5 35.0 73.5 58.6 58.6 5.4

Source: Nirmal Bang Institutional Equities Research

Overall risks to our rating # Sharp increase in taxation and imposition of restrictions on marketing/prohibition in any key market in

India. Congress party, in recent state elections, had indicated that it may consider prohibition in Chhattisgarh. We view this as a highly isolated move and believe that most states support the trend of moderate and responsible liquor consumption.

# Inability to maintain product quality and safety is a risk to reputation and operations of these companies. # Any volatility and sharp slowdown in economic growth. Slowdown will clearly impact the ability of

consumers to trade-up/premiumise. # Inability to adapt to consumer changes is a key risk. # Any non-compliance with laws and regulations, considering that the industry has to follow practices which

vary significantly from state to state.

Institutional Equities

15 Alcoholic Beverage Sector

CCoommppaannyy SSeeccttiioonn

Institutional Equities

16 Alcoholic Beverage Sector

This page has been intentionally left blank

Institutional Equities

Initi

atin

g C

over

age

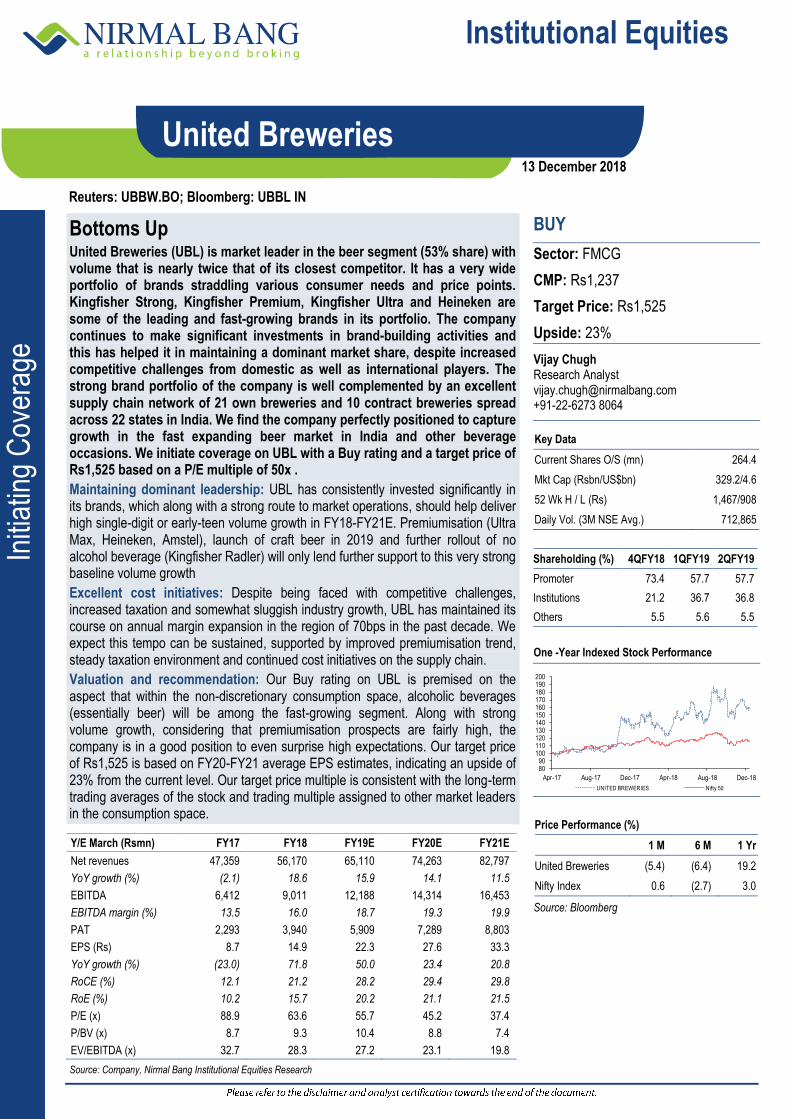

Reuters: UBBW.BO; Bloomberg: UBBL IN

United Breweries

Bottoms Up United Breweries (UBL) is market leader in the beer segment (53% share) with volume that is nearly twice that of its closest competitor. It has a very wide portfolio of brands straddling various consumer needs and price points. Kingfisher Strong, Kingfisher Premium, Kingfisher Ultra and Heineken are some of the leading and fast-growing brands in its portfolio. The company continues to make significant investments in brand-building activities and this has helped it in maintaining a dominant market share, despite increased competitive challenges from domestic as well as international players. The strong brand portfolio of the company is well complemented by an excellent supply chain network of 21 own breweries and 10 contract breweries spread across 22 states in India. We find the company perfectly positioned to capture growth in the fast expanding beer market in India and other beverage occasions. We initiate coverage on UBL with a Buy rating and a target price of Rs1,525 based on a P/E multiple of 50x .

Maintaining dominant leadership: UBL has consistently invested significantly in its brands, which along with a strong route to market operations, should help deliver high single-digit or early-teen volume growth in FY18-FY21E. Premiumisation (Ultra Max, Heineken, Amstel), launch of craft beer in 2019 and further rollout of no alcohol beverage (Kingfisher Radler) will only lend further support to this very strong baseline volume growth

Excellent cost initiatives: Despite being faced with competitive challenges, increased taxation and somewhat sluggish industry growth, UBL has maintained its course on annual margin expansion in the region of 70bps in the past decade. We expect this tempo can be sustained, supported by improved premiumisation trend, steady taxation environment and continued cost initiatives on the supply chain.

Valuation and recommendation: Our Buy rating on UBL is premised on the aspect that within the non-discretionary consumption space, alcoholic beverages (essentially beer) will be among the fast-growing segment. Along with strong volume growth, considering that premiumisation prospects are fairly high, the company is in a good position to even surprise high expectations. Our target price of Rs1,525 is based on FY20-FY21 average EPS estimates, indicating an upside of 23% from the current level. Our target price multiple is consistent with the long-term trading averages of the stock and trading multiple assigned to other market leaders in the consumption space.

BUY

Sector: FMCG

CMP: Rs1,237

Target Price: Rs1,525

Upside: 23%

Vijay Chugh Research Analyst [email protected] +91-22-6273 8064

Key Data

Current Shares O/S (mn) 264.4

Mkt Cap (Rsbn/US$bn) 329.2/4.6

52 Wk H / L (Rs) 1,467/908

Daily Vol. (3M NSE Avg.) 712,865

Shareholding (%) 4QFY18 1QFY19 2QFY19

Promoter 73.4 57.7 57.7

Institutions 21.2 36.7 36.8

Others 5.5 5.6 5.5

One -Year Indexed Stock Performance

8090

100110120130140150160170180190200

Apr-17 Aug-17 Dec-17 Apr-18 Aug-18 Dec-18

UNITED BREWERIES Nifty 50

Price Performance (%)

1 M 6 M 1 Yr

United Breweries (5.4) (6.4) 19.2

Nifty Index 0.6 (2.7) 3.0

Source: Bloomberg

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Net revenues 47,359 56,170 65,110 74,263 82,797

YoY growth (%) (2.1) 18.6 15.9 14.1 11.5

EBITDA 6,412 9,011 12,188 14,314 16,453

EBITDA margin (%) 13.5 16.0 18.7 19.3 19.9

PAT 2,293 3,940 5,909 7,289 8,803

EPS (Rs) 8.7 14.9 22.3 27.6 33.3

YoY growth (%) (23.0) 71.8 50.0 23.4 20.8

RoCE (%) 12.1 21.2 28.2 29.4 29.8

RoE (%) 10.2 15.7 20.2 21.1 21.5

P/E (x) 88.9 63.6 55.7 45.2 37.4

P/BV (x) 8.7 9.3 10.4 8.8 7.4

EV/EBITDA (x) 32.7 28.3 27.2 23.1 19.8

Source: Company, Nirmal Bang Institutional Equities Research

13 December 2018

Institutional Equities

United Breweries 18

Investment thesis

Beer has potential to become fast-growing category in the food and beverage space

Although Kingfisher and other beer brands have been in existence for a fairly long period in India, considering the pricing and regulation challenges the size of overall market is still fairly small from a regional and global pool perspective. The global beer market is estimated to be in excess of 2,000mn hecto litre and India’s contribution to the overall pool is fairly insignificant at around 1%. (China’s contribution is in excess of 25%). Urbanisation and emerging middle class consumer, in our opinion, will increasingly consider beer as a good alternate to spirits and other beverage choices and it is this aspect it will be the strongest driver of growth. Considering the low alcohol content, beer is also perceived to be more safe and healthier by most new and existing consumers of alcoholic beverages. This aspect too, in our opinion, is fairly important considering that consumer choices continue to evolve towards more premium and healthier options within the alcoholic beverage space. In the past three years, the market has seen expansion by 11% despite a myriad of regulation challenges, and as these challenges moderate and consumer confidence continues to hold up we expect growth to remain in early teens for the industry. We expect UBL with its wide portfolio and distribution capabilities to outperform.

Exhibit 1: Beer industry’s volume growth

225235

263 270280

294

337360

0

50

100

150

200

250

300

350

400

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

(mn cases)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 2: Strong product portfolio

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 19

Premiumisation pace to gather momentum

All segments in the alcoholic beverage category are rapidly premiumising and this is true even in case of beer. We believe the global premium pool is around 20% of the beer market and in India it is in mid single-digit. Although Fosters came into the beer market in late 90s and planted some seeds of premiumisation, it did not change the category dynamics much and preference remained strongly in favour of strong beer. The alcohol space, contrary to beers, continued to benefit from differentiation with single malt, blended scotch and white spirits taking over the scene. It was only in late 2010 with the entry of Micro Breweries and Stouts that the beer market started witnessing some differentiation. It was also around time that UBL launched its Kingfisher Ultra brand which, in our opinion, has topped 3mn cases in sales in 2018. Considering that craft beer has enjoyed acceptance in a fairly short period of time, it wouldn’t surprise us that beer - which is increasingly becoming a lifestyle drink - could witness premiumisation at a much faster pace than what was witnessed in the past. UBL is enjoying good growth momentum in its premium properties, Ultra Max and Heineken. The recent launch of Amstel as a premium beer in the strong beer segment and entry into craft beer somewhere in 4QFY19 and 1QFY20 will only give a further filip to UBL in the premium space. It is important to note that, contrary to popular perception, it is not small brewers but AB Inbev which is the largest craft beer brand now in the US.

Exhibit 3: Strong growth of premium brands despite regulatory hurdles

Source: Company, Nirmal Bang Institutional Equities Research

Innovation and brand investments should help improve market share

Despite competitive challenges from the likes of Carlsberg, Tuborg, Bira and other premium brands, Kingfisher has not only held its ground but expanded its market share by around 200bps in the past five years to around 52%. Kingfisher enjoys association with the most marquee sporting, fashion and music events such as IPL, Lakme Fashion Week etc. It also has been consistent with innovation and brand launches such as Kingfisher Ultra, Kingfisher Ultra Max, Kingfisher Buzz, Kingfisher Storm, Heineken and Amstel

Radler is an interesting opportunity from growth, diversification and risk perspective. Considering the health, lifestyle and regulation aspects, UBL has chosen to expand its presence in the non-alcoholic beverage space with the launch of Kingfisher Radler in Gujarat - a state that has enforced prohibition – and in Bengaluru. In several markets overseas, Radlers has great consumer appeal as it is an attractive option for those who do not consume alcohol. It also helps in expanding the drinking occasions to lunch time or sports events. It also has great appeal to women and could be used as a tool to induct new consumers into the beer category. In case of Heineken, low and zero alcohol beer contribute to as much as 6% of sales and is one of the fast-growing category within its portfolio.

Institutional Equities

United Breweries 20

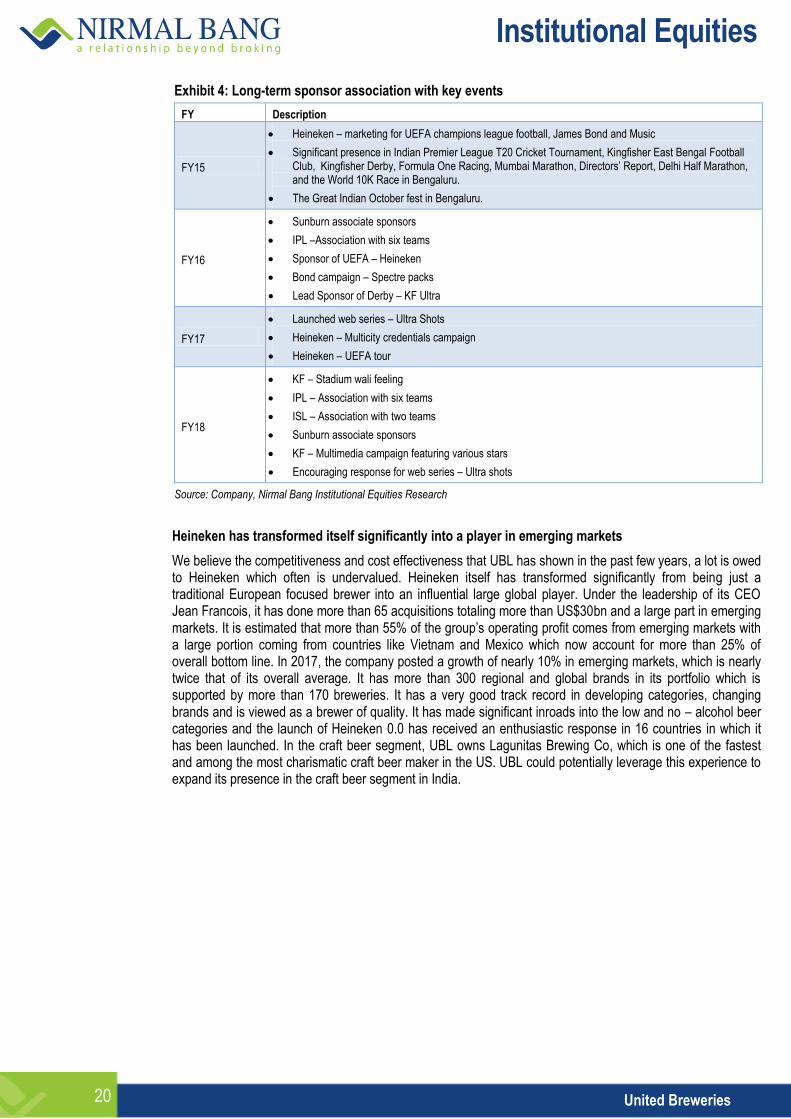

Exhibit 4: Long-term sponsor association with key events

FY Description

FY15

Heineken – marketing for UEFA champions league football, James Bond and Music

Significant presence in Indian Premier League T20 Cricket Tournament, Kingfisher East Bengal Football Club, Kingfisher Derby, Formula One Racing, Mumbai Marathon, Directors’ Report, Delhi Half Marathon, and the World 10K Race in Bengaluru.

The Great Indian October fest in Bengaluru.

FY16

Sunburn associate sponsors

IPL –Association with six teams

Sponsor of UEFA – Heineken

Bond campaign – Spectre packs

Lead Sponsor of Derby – KF Ultra

FY17

Launched web series – Ultra Shots

Heineken – Multicity credentials campaign

Heineken – UEFA tour

FY18

KF – Stadium wali feeling

IPL – Association with six teams

ISL – Association with two teams

Sunburn associate sponsors

KF – Multimedia campaign featuring various stars

Encouraging response for web series – Ultra shots

Source: Company, Nirmal Bang Institutional Equities Research

Heineken has transformed itself significantly into a player in emerging markets

We believe the competitiveness and cost effectiveness that UBL has shown in the past few years, a lot is owed to Heineken which often is undervalued. Heineken itself has transformed significantly from being just a traditional European focused brewer into an influential large global player. Under the leadership of its CEO Jean Francois, it has done more than 65 acquisitions totaling more than US$30bn and a large part in emerging markets. It is estimated that more than 55% of the group’s operating profit comes from emerging markets with a large portion coming from countries like Vietnam and Mexico which now account for more than 25% of overall bottom line. In 2017, the company posted a growth of nearly 10% in emerging markets, which is nearly twice that of its overall average. It has more than 300 regional and global brands in its portfolio which is supported by more than 170 breweries. It has a very good track record in developing categories, changing brands and is viewed as a brewer of quality. It has made significant inroads into the low and no – alcohol beer categories and the launch of Heineken 0.0 has received an enthusiastic response in 16 countries in which it has been launched. In the craft beer segment, UBL owns Lagunitas Brewing Co, which is one of the fastest and among the most charismatic craft beer maker in the US. UBL could potentially leverage this experience to expand its presence in the craft beer segment in India.

Institutional Equities

United Breweries 21

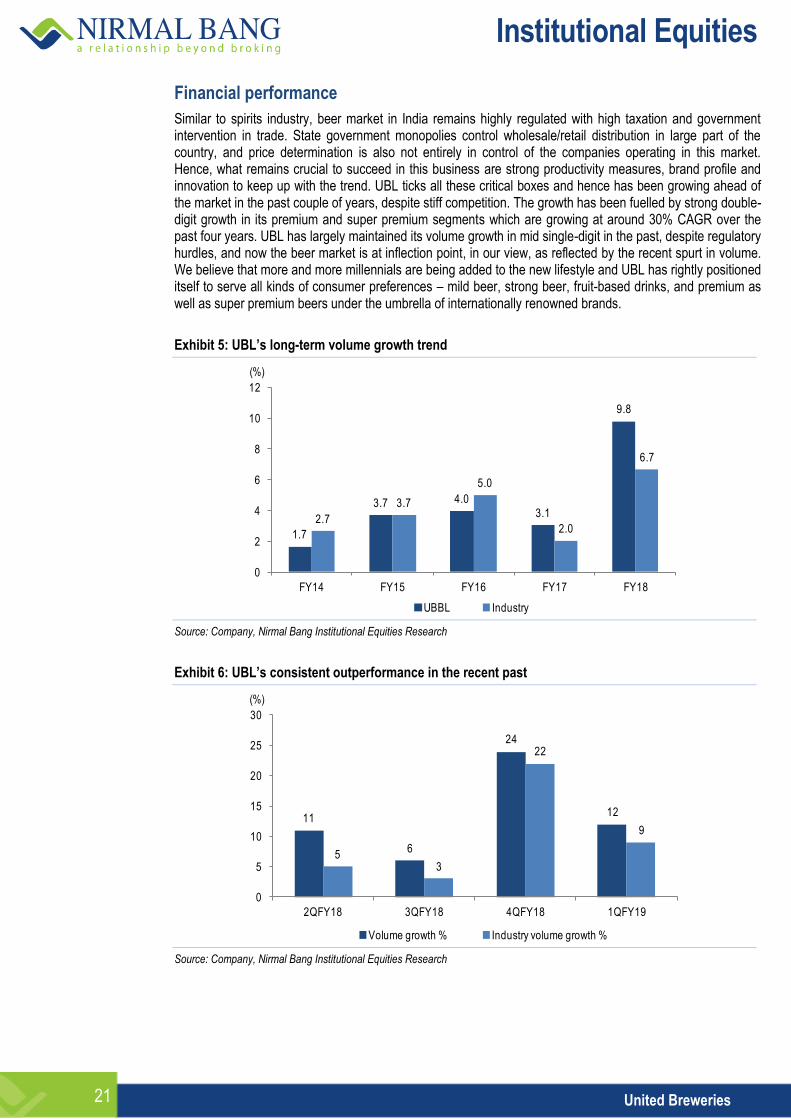

Financial performance

Similar to spirits industry, beer market in India remains highly regulated with high taxation and government intervention in trade. State government monopolies control wholesale/retail distribution in large part of the country, and price determination is also not entirely in control of the companies operating in this market. Hence, what remains crucial to succeed in this business are strong productivity measures, brand profile and innovation to keep up with the trend. UBL ticks all these critical boxes and hence has been growing ahead of the market in the past couple of years, despite stiff competition. The growth has been fuelled by strong double-digit growth in its premium and super premium segments which are growing at around 30% CAGR over the past four years. UBL has largely maintained its volume growth in mid single-digit in the past, despite regulatory hurdles, and now the beer market is at inflection point, in our view, as reflected by the recent spurt in volume. We believe that more and more millennials are being added to the new lifestyle and UBL has rightly positioned itself to serve all kinds of consumer preferences – mild beer, strong beer, fruit-based drinks, and premium as well as super premium beers under the umbrella of internationally renowned brands.

Exhibit 5: UBL’s long-term volume growth trend

1.7

3.7 4.0

3.1

9.8

2.7

3.7

5.0

2.0

6.7

0

2

4

6

8

10

12

FY14 FY15 FY16 FY17 FY18

UBBL Industry

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 6: UBL’s consistent outperformance in the recent past

11

6

24

12

53

22

9

0

5

10

15

20

25

30

2QFY18 3QFY18 4QFY18 1QFY19

Volume growth % Industry volume growth %

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 22

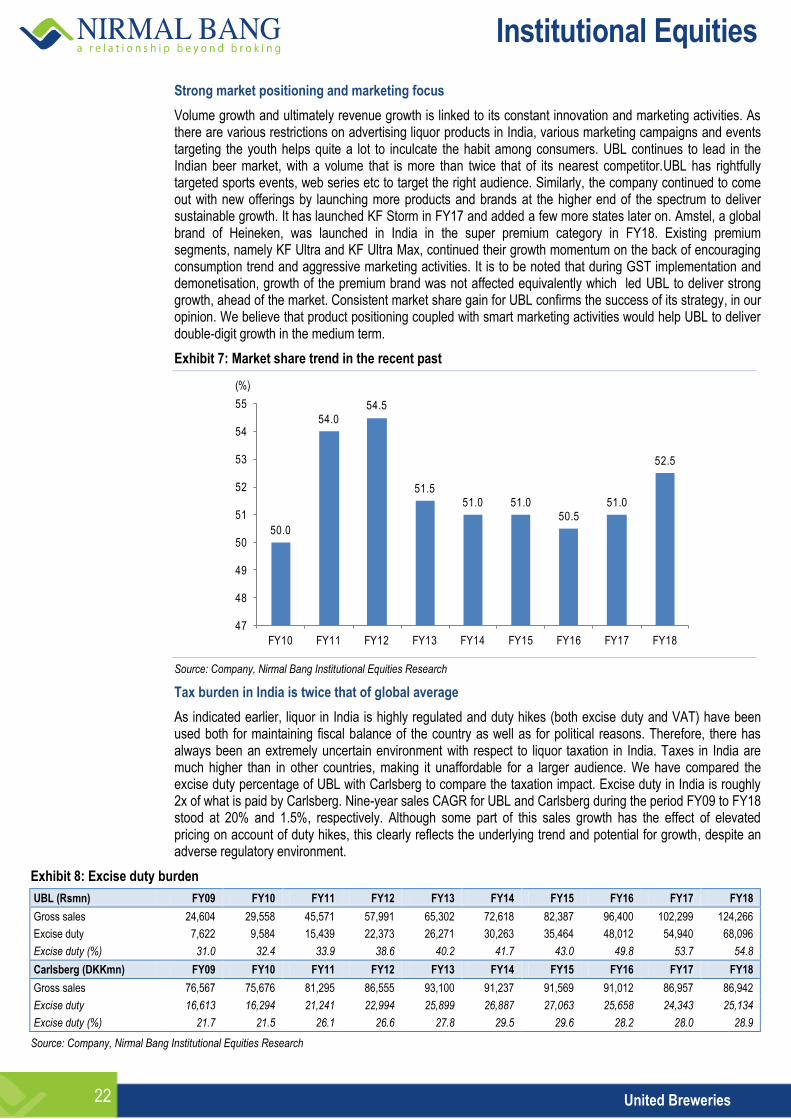

Strong market positioning and marketing focus

Volume growth and ultimately revenue growth is linked to its constant innovation and marketing activities. As there are various restrictions on advertising liquor products in India, various marketing campaigns and events targeting the youth helps quite a lot to inculcate the habit among consumers. UBL continues to lead in the Indian beer market, with a volume that is more than twice that of its nearest competitor.UBL has rightfully targeted sports events, web series etc to target the right audience. Similarly, the company continued to come out with new offerings by launching more products and brands at the higher end of the spectrum to deliver sustainable growth. It has launched KF Storm in FY17 and added a few more states later on. Amstel, a global brand of Heineken, was launched in India in the super premium category in FY18. Existing premium segments, namely KF Ultra and KF Ultra Max, continued their growth momentum on the back of encouraging consumption trend and aggressive marketing activities. It is to be noted that during GST implementation and demonetisation, growth of the premium brand was not affected equivalently which led UBL to deliver strong growth, ahead of the market. Consistent market share gain for UBL confirms the success of its strategy, in our opinion. We believe that product positioning coupled with smart marketing activities would help UBL to deliver double-digit growth in the medium term.

Exhibit 7: Market share trend in the recent past

50.0

54.054.5

51.551.0 51.0

50.551.0

52.5

47

48

49

50

51

52

53

54

55

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Tax burden in India is twice that of global average

As indicated earlier, liquor in India is highly regulated and duty hikes (both excise duty and VAT) have been used both for maintaining fiscal balance of the country as well as for political reasons. Therefore, there has always been an extremely uncertain environment with respect to liquor taxation in India. Taxes in India are much higher than in other countries, making it unaffordable for a larger audience. We have compared the excise duty percentage of UBL with Carlsberg to compare the taxation impact. Excise duty in India is roughly 2x of what is paid by Carlsberg. Nine-year sales CAGR for UBL and Carlsberg during the period FY09 to FY18 stood at 20% and 1.5%, respectively. Although some part of this sales growth has the effect of elevated pricing on account of duty hikes, this clearly reflects the underlying trend and potential for growth, despite an adverse regulatory environment.

Exhibit 8: Excise duty burden

UBL (Rsmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 24,604 29,558 45,571 57,991 65,302 72,618 82,387 96,400 102,299 124,266

Excise duty 7,622 9,584 15,439 22,373 26,271 30,263 35,464 48,012 54,940 68,096

Excise duty (%) 31.0 32.4 33.9 38.6 40.2 41.7 43.0 49.8 53.7 54.8

Carlsberg (DKKmn) FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Gross sales 76,567 75,676 81,295 86,555 93,100 91,237 91,569 91,012 86,957 86,942

Excise duty 16,613 16,294 21,241 22,994 25,899 26,887 27,063 25,658 24,343 25,134

Excise duty (%) 21.7 21.5 26.1 26.6 27.8 29.5 29.6 28.2 28.0 28.9

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 23

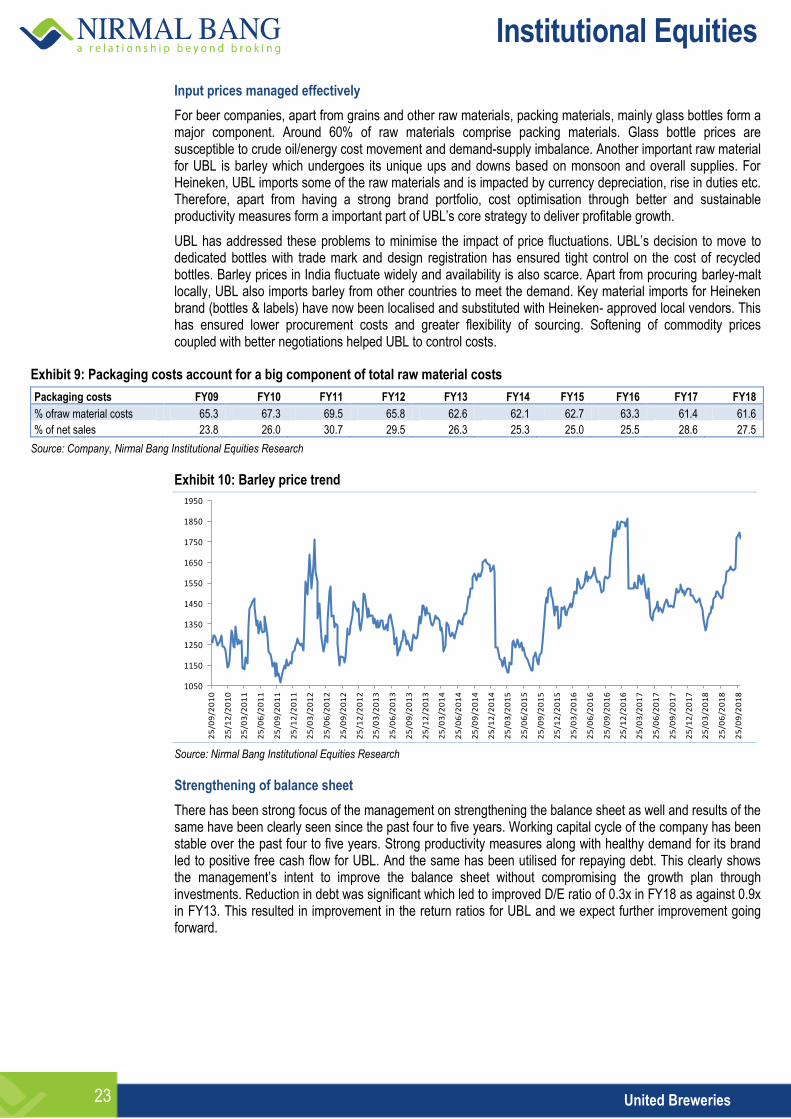

Input prices managed effectively

For beer companies, apart from grains and other raw materials, packing materials, mainly glass bottles form a major component. Around 60% of raw materials comprise packing materials. Glass bottle prices are susceptible to crude oil/energy cost movement and demand-supply imbalance. Another important raw material for UBL is barley which undergoes its unique ups and downs based on monsoon and overall supplies. For Heineken, UBL imports some of the raw materials and is impacted by currency depreciation, rise in duties etc. Therefore, apart from having a strong brand portfolio, cost optimisation through better and sustainable productivity measures form a important part of UBL’s core strategy to deliver profitable growth.

UBL has addressed these problems to minimise the impact of price fluctuations. UBL’s decision to move to dedicated bottles with trade mark and design registration has ensured tight control on the cost of recycled bottles. Barley prices in India fluctuate widely and availability is also scarce. Apart from procuring barley-malt locally, UBL also imports barley from other countries to meet the demand. Key material imports for Heineken brand (bottles & labels) have now been localised and substituted with Heineken- approved local vendors. This has ensured lower procurement costs and greater flexibility of sourcing. Softening of commodity prices coupled with better negotiations helped UBL to control costs.

Exhibit 9: Packaging costs account for a big component of total raw material costs

Packaging costs FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

% ofraw material costs 65.3 67.3 69.5 65.8 62.6 62.1 62.7 63.3 61.4 61.6

% of net sales 23.8 26.0 30.7 29.5 26.3 25.3 25.0 25.5 28.6 27.5

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 10: Barley price trend

1050

1150

1250

1350

1450

1550

1650

1750

1850

1950

25

/09

/20

10

25

/12

/20

10

25

/03

/20

11

25

/06

/20

11

25

/09

/20

11

25

/12

/20

11

25

/03

/20

12

25

/06

/20

12

25

/09

/20

12

25

/12

/20

12

25

/03

/20

13

25

/06

/20

13

25

/09

/20

13

25

/12

/20

13

25

/03

/20

14

25

/06

/20

14

25

/09

/20

14

25

/12

/20

14

25

/03

/20

15

25

/06

/20

15

25

/09

/20

15

25

/12

/20

15

25

/03

/20

16

25

/06

/20

16

25

/09

/20

16

25

/12

/20

16

25

/03

/20

17

25

/06

/20

17

25

/09

/20

17

25

/12

/20

17

25

/03

/20

18

25

/06

/20

18

25

/09

/20

18

Source: Nirmal Bang Institutional Equities Research

Strengthening of balance sheet

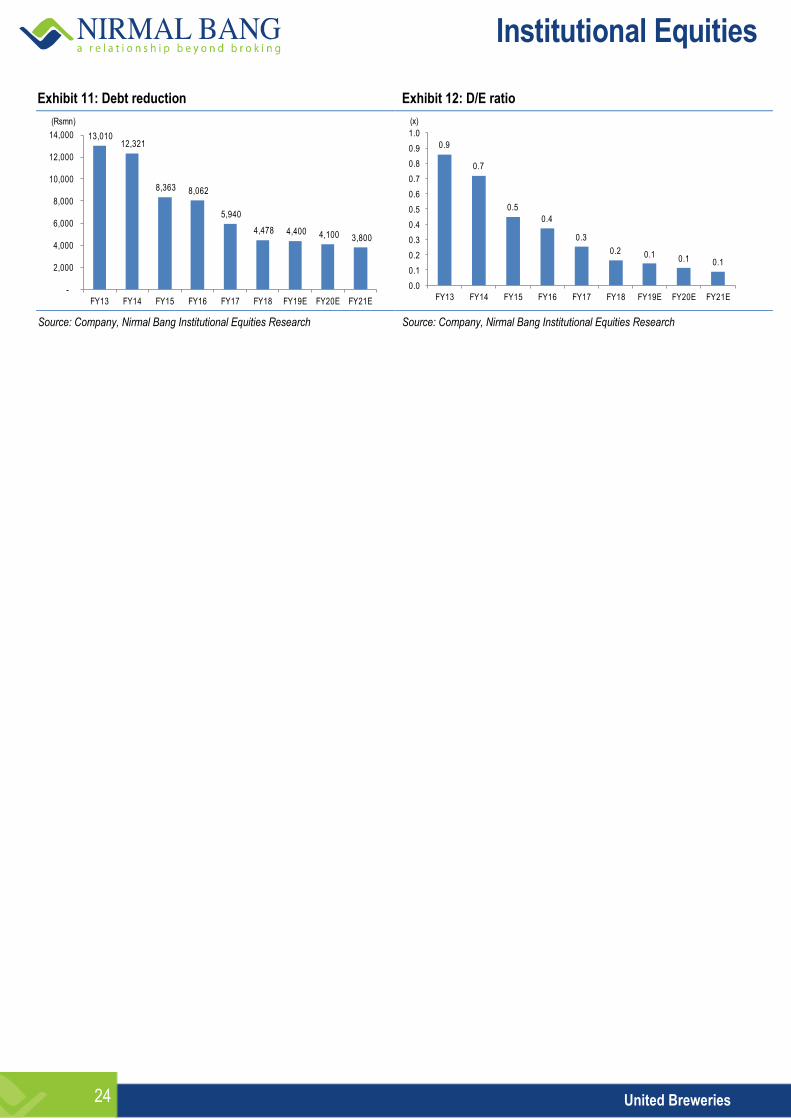

There has been strong focus of the management on strengthening the balance sheet as well and results of the same have been clearly seen since the past four to five years. Working capital cycle of the company has been stable over the past four to five years. Strong productivity measures along with healthy demand for its brand led to positive free cash flow for UBL. And the same has been utilised for repaying debt. This clearly shows the management’s intent to improve the balance sheet without compromising the growth plan through investments. Reduction in debt was significant which led to improved D/E ratio of 0.3x in FY18 as against 0.9x in FY13. This resulted in improvement in the return ratios for UBL and we expect further improvement going forward.

Institutional Equities

United Breweries 24

Exhibit 11: Debt reduction Exhibit 12: D/E ratio

13,010 12,321

8,363 8,062

5,940

4,478 4,400 4,100 3,800

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(Rsmn)

0.9

0.7

0.5

0.4

0.3

0.2 0.1 0.1 0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(x)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 25

Financial trends

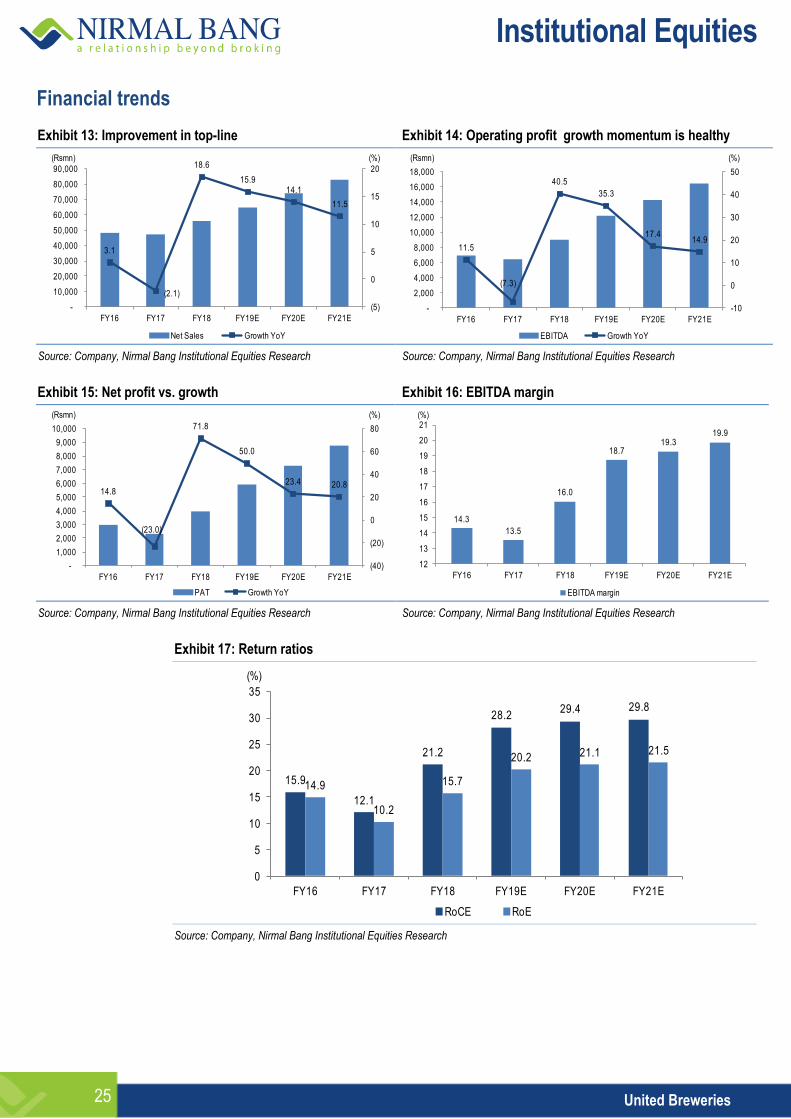

Exhibit 13: Improvement in top-line Exhibit 14: Operating profit growth momentum is healthy

3.1

(2.1)

18.6

15.9 14.1

11.5

(5)

0

5

10

15

20

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY16 FY17 FY18 FY19E FY20E FY21E

Net Sales Growth YoY

(Rsmn) (%)

11.5

(7.3)

40.5

35.3

17.4 14.9

-10

0

10

20

30

40

50

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FY16 FY17 FY18 FY19E FY20E FY21E

EBITDA Growth YoY

(Rsmn) (%)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 15: Net profit vs. growth Exhibit 16: EBITDA margin

14.8

(23.0)

71.8

50.0

23.4 20.8

(40)

(20)

0

20

40

60

80

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY16 FY17 FY18 FY19E FY20E FY21E

PAT Growth YoY

(Rsmn) (%)

14.3

13.5

16.0

18.719.3

19.9

12

13

14

15

16

17

18

19

20

21

FY16 FY17 FY18 FY19E FY20E FY21E

EBITDA margin

(%)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 17: Return ratios

15.9

12.1

21.2

28.229.4 29.8

14.9

10.2

15.7

20.2 21.1 21.5

0

5

10

15

20

25

30

35

FY16 FY17 FY18 FY19E FY20E FY21E

RoCE RoE

(%)

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 26

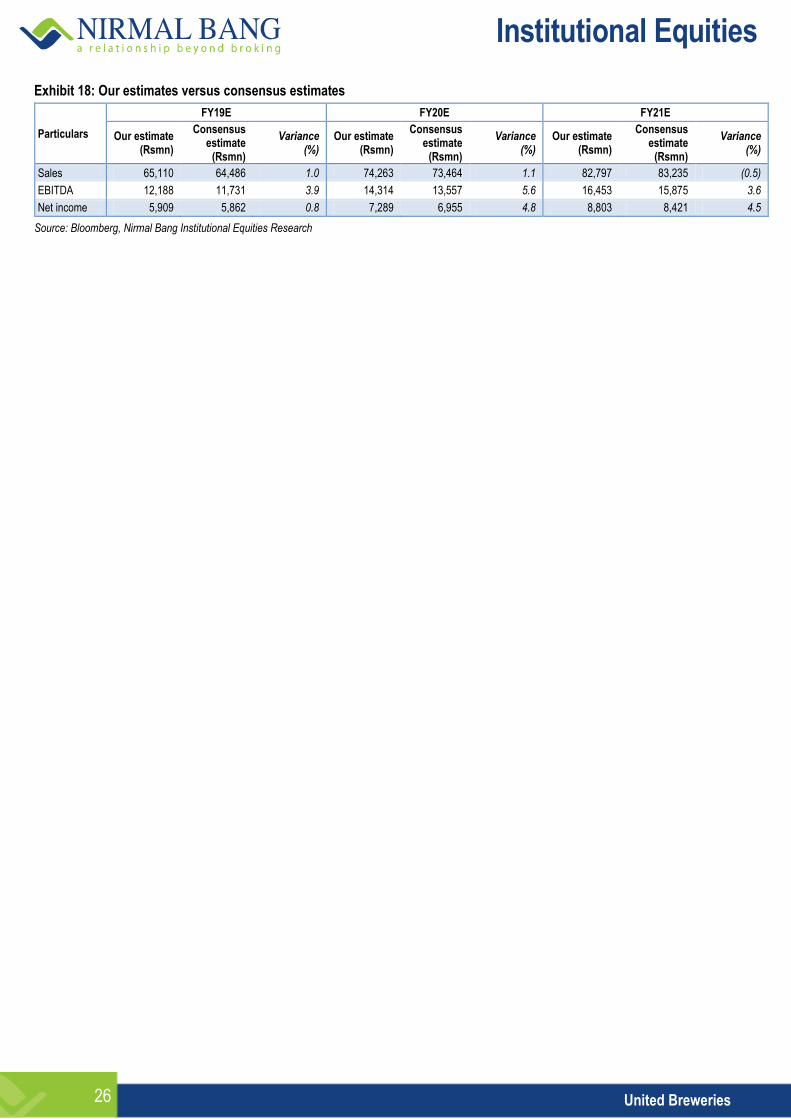

Exhibit 18: Our estimates versus consensus estimates

Particulars

FY19E FY20E FY21E

Our estimate (Rsmn)

Consensus estimate

(Rsmn)

Variance (%)

Our estimate (Rsmn)

Consensus estimate

(Rsmn)

Variance (%)

Our estimate (Rsmn)

Consensus estimate

(Rsmn)

Variance (%)

Sales 65,110 64,486 1.0 74,263 73,464 1.1 82,797 83,235 (0.5)

EBITDA 12,188 11,731 3.9 14,314 13,557 5.6 16,453 15,875 3.6

Net income 5,909 5,862 0.8 7,289 6,955 4.8 8,803 8,421 4.5

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 27

Valuation and recommendation Liquor industry across the globe is susceptible to regulatory and taxation hurdles and hence the share price performance remained quite volatile with some years of exceptional outperformance and on the other hand, sudden slump on account of any of the adverse events. Compared to the global scenario, Indian companies had faced manifold challenges and growth was hampered for quite some time. However, considering the penetration potential and positive consumption environment, these companies bounced back on every downfall, outperforming broader indices and adding significant value to shareholders’ wealth.

Exhibit 19: Absolute price performance history of key Indian and global players

Alcohol Companies (%) CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 YTDCY18

Spirits

PERNOD RICARD SA 9 (33) 22 17 2 22 (5) 11 14 (3) 29 7

DIAGEO PLC 8 (11) 13 9 19 27 12 (8) - 12 29 5

UNITED SPIRITS 131 (56) 42 16 (66) 286 37 7 7 (37) 93 (16)

Beers/Mix

ANHEUSER-BUSCH INBEV SA/NV 14 (53) 120 18 11 39 18 21 22 (13) (7) (32)

CARLSBERG AS-B 10 (65) 120 47 (28) 37 8 (19) 26 (1) 24 (4)

HEINEKEN NV 23 (50) 52 10 (3) 41 (3) 20 34 (10) 23 (9)

ASAHI GROUP HOLDINGS (1) (18) 11 (8) 7 9 61 29 (1) (3) 52 (22)

TSINGTAO BREWERY CO -H 100 (38) 166 (5) 6 6 43 (20) (33) (17) 33 (21)

CONSTELLATION BRANDS INC-A (19) (33) 1 39 (7) 71 99 39 45 7 50 (18)

THAI BEVERAGE PCL (6) (24) 26 16 (14) 61 37 28 - 23 7 (36)

UNITED BREWERIES L 85 (76) 116 200 (24) 142 (17) 8 13 (19) 40 15

Indices

Nifty FMCG 22 (20) 42 31 9 49 12 18 - - 31 11

Nifty 50 55 (52) 76 18 (25) 28 7 31 (4) 1 30 1

MSCI WORLD 7 (42) 27 10 (8) 13 24 3 (3) 5 20 (7)

Source: Bloomberg, Nirmal Bang Institutional Equities

Exhibit 20: Relative price performance history of key Indian and global players

Alcohol Companies (%) CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 YTDCY18

Spirits

PERNOD RICARD SA 2 16 (4) 7 10 8 (24) 8 17 (8) 7 15

DIAGEO PLC 1 54 (11) - 28 12 (10) (10) 3 7 7 13

UNITED SPIRITS 49 (8) (19) (2) (55) 202 29 (19) 12 (38) 48 (16)

Beers/Mix

ANHEUSER-BUSCH INBEV SA/NV 7 (20) 73 7 20 23 (5) 18 25 (17) (23) (27)

CARLSBERG AS-B 3 (40) 73 34 (22) 21 (13) (21) 30 (6) 3 3

HEINEKEN NV 15 (14) 20 1 6 25 (22) 17 37 (14) 2 (2)

ASAHI GROUP HOLDINGS (7) 41 (12) (16) 15 (4) 30 25 2 (8) 26 (16)

TSINGTAO BREWERY CO-H 86 7 109 (14) 14 (6) 15 (22) (31) (21) 10 (15)

CONSTELLATION BRANDS INC-A (24) 15 (20) 27 1 51 60 36 49 2 24 (11)

THAI BEVERAGE PCL (12) 32 (1) 6 (7) 42 10 24 3 17 (11) (31)

UNITED BREWERIES 20 (51) 23 154 1 89 (22) (18) 18 (20) 7 14

Indices

Nifty FMCG (21) 67 (19) 11 44 16 5 (10) 5 (1) 1 10

Source: Bloomberg, Nirmal Bang Institutional Equities

Institutional Equities

United Breweries 28

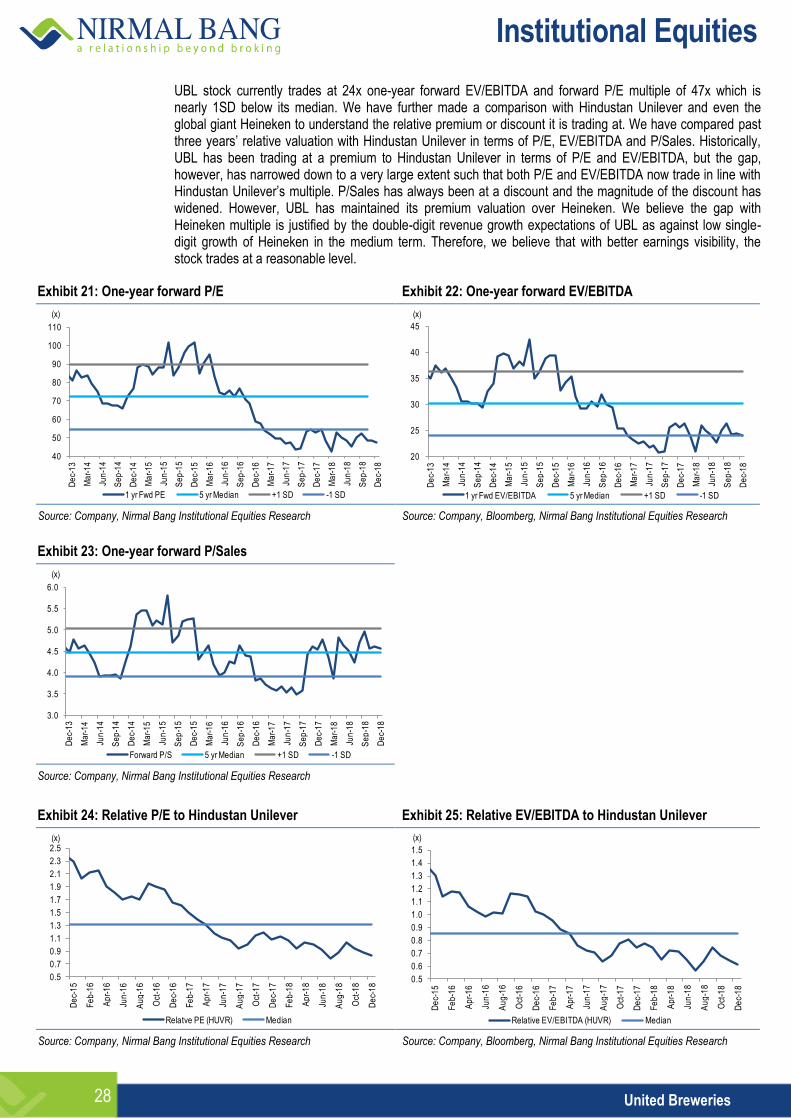

UBL stock currently trades at 24x one-year forward EV/EBITDA and forward P/E multiple of 47x which is nearly 1SD below its median. We have further made a comparison with Hindustan Unilever and even the global giant Heineken to understand the relative premium or discount it is trading at. We have compared past three years’ relative valuation with Hindustan Unilever in terms of P/E, EV/EBITDA and P/Sales. Historically, UBL has been trading at a premium to Hindustan Unilever in terms of P/E and EV/EBITDA, but the gap, however, has narrowed down to a very large extent such that both P/E and EV/EBITDA now trade in line with Hindustan Unilever’s multiple. P/Sales has always been at a discount and the magnitude of the discount has widened. However, UBL has maintained its premium valuation over Heineken. We believe the gap with Heineken multiple is justified by the double-digit revenue growth expectations of UBL as against low single-digit growth of Heineken in the medium term. Therefore, we believe that with better earnings visibility, the stock trades at a reasonable level.

Exhibit 21: One-year forward P/E Exhibit 22: One-year forward EV/EBITDA

40

50

60

70

80

90

100

110

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun

-18

Se

p-1

8

De

c-1

8

1 yr Fwd PE 5 yr Median +1 SD -1 SD

(x)

20

25

30

35

40

45

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun

-18

Se

p-1

8

De

c-1

8

1 yr Fwd EV/EBITDA 5 yr Median +1 SD -1 SD

(x)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 23: One-year forward P/Sales

3.0

3.5

4.0

4.5

5.0

5.5

6.0

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun

-18

Se

p-1

8

De

c-1

8

Forward P/S 5 yr Median +1 SD -1 SD

(x)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 24: Relative P/E to Hindustan Unilever Exhibit 25: Relative EV/EBITDA to Hindustan Unilever

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

Relatve PE (HUVR) Median

(x)

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

Relative EV/EBITDA (HUVR) Median

(x)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

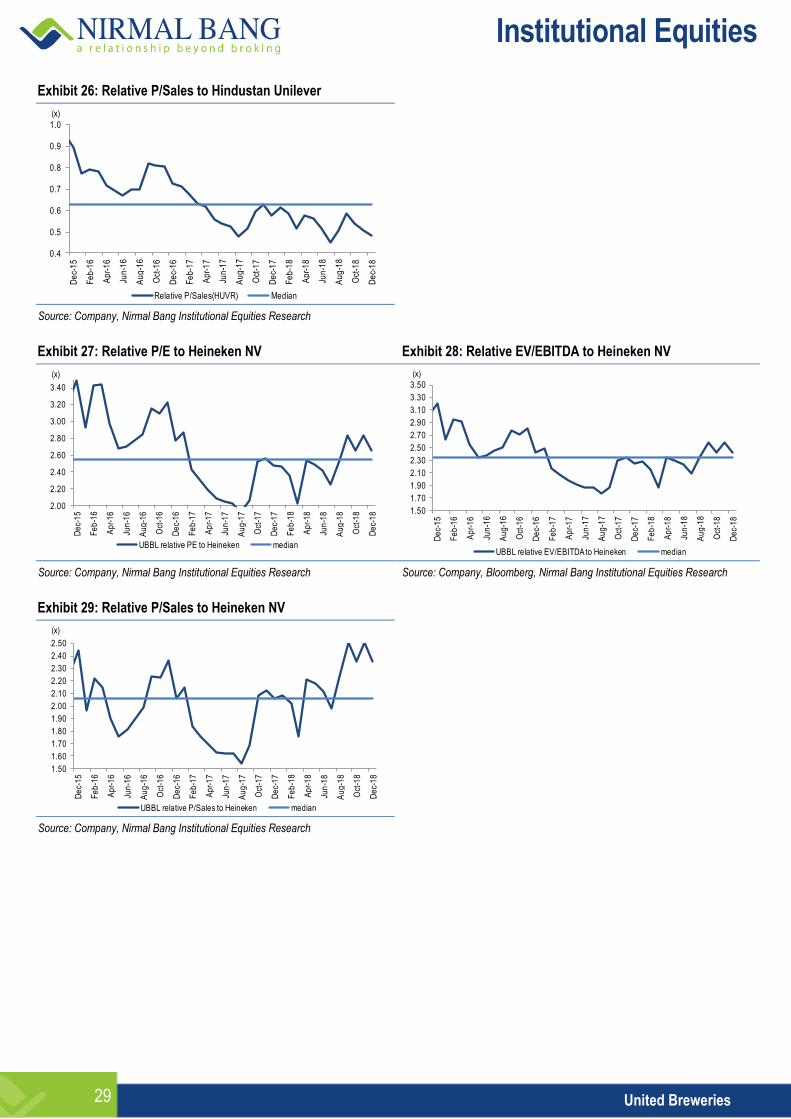

Institutional Equities

United Breweries 29

Exhibit 26: Relative P/Sales to Hindustan Unilever

0.4

0.5

0.6

0.7

0.8

0.9

1.0

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

Relative P/Sales(HUVR) Median

(x)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 27: Relative P/E to Heineken NV Exhibit 28: Relative EV/EBITDA to Heineken NV

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

UBBL relative PE to Heineken median

(x)

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

3.30

3.50

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

UBBL relative EV/EBITDA to Heineken median

(x)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 29: Relative P/Sales to Heineken NV

1.50

1.60

1.70

1.80

1.90

2.00

2.10

2.20

2.30

2.40

2.50

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

UBBL relative P/Sales to Heineken median

(x)

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 30

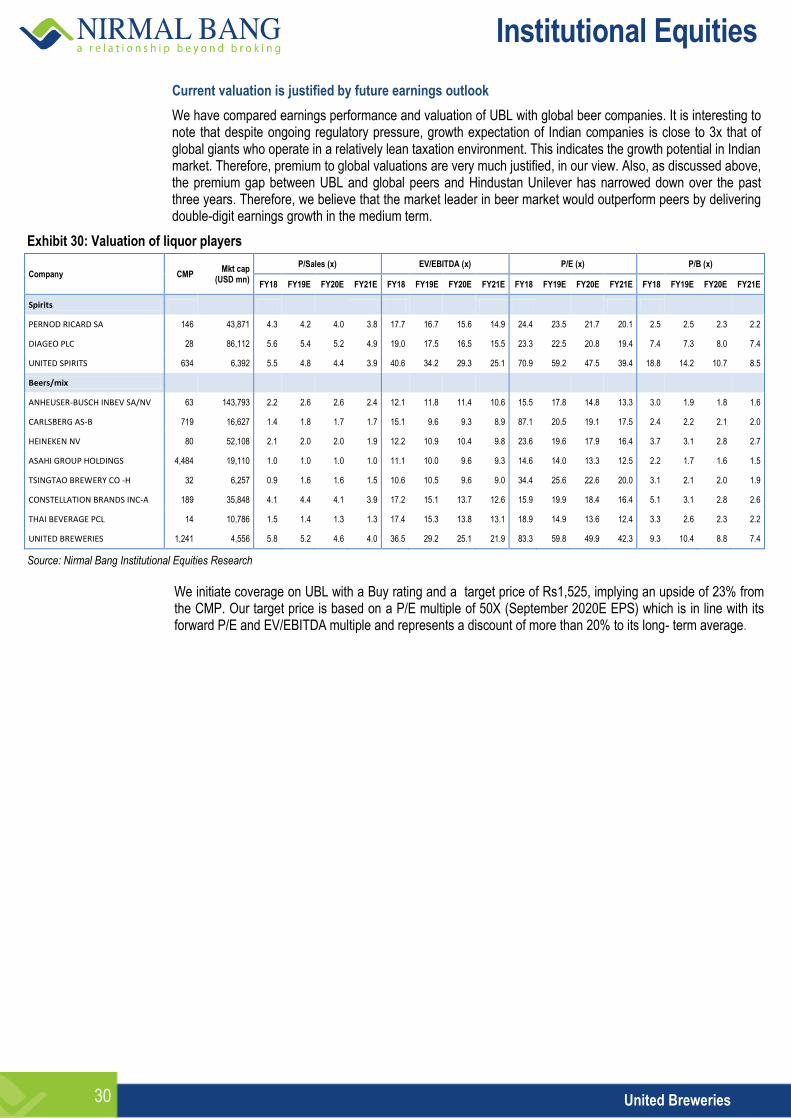

Current valuation is justified by future earnings outlook

We have compared earnings performance and valuation of UBL with global beer companies. It is interesting to note that despite ongoing regulatory pressure, growth expectation of Indian companies is close to 3x that of global giants who operate in a relatively lean taxation environment. This indicates the growth potential in Indian market. Therefore, premium to global valuations are very much justified, in our view. Also, as discussed above, the premium gap between UBL and global peers and Hindustan Unilever has narrowed down over the past three years. Therefore, we believe that the market leader in beer market would outperform peers by delivering double-digit earnings growth in the medium term.

Exhibit 30: Valuation of liquor players

Company CMP Mkt cap

(USD mn)

P/Sales (x) EV/EBITDA (x) P/E (x) P/B (x)

FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E

Spirits

PERNOD RICARD SA 146 43,871 4.3 4.2 4.0 3.8 17.7 16.7 15.6 14.9 24.4 23.5 21.7 20.1 2.5 2.5 2.3 2.2

DIAGEO PLC 28 86,112 5.6 5.4 5.2 4.9 19.0 17.5 16.5 15.5 23.3 22.5 20.8 19.4 7.4 7.3 8.0 7.4

UNITED SPIRITS 634 6,392 5.5 4.8 4.4 3.9 40.6 34.2 29.3 25.1 70.9 59.2 47.5 39.4 18.8 14.2 10.7 8.5

Beers/mix

ANHEUSER-BUSCH INBEV SA/NV 63 143,793 2.2 2.6 2.6 2.4 12.1 11.8 11.4 10.6 15.5 17.8 14.8 13.3 3.0 1.9 1.8 1.6

CARLSBERG AS-B 719 16,627 1.4 1.8 1.7 1.7 15.1 9.6 9.3 8.9 87.1 20.5 19.1 17.5 2.4 2.2 2.1 2.0

HEINEKEN NV 80 52,108 2.1 2.0 2.0 1.9 12.2 10.9 10.4 9.8 23.6 19.6 17.9 16.4 3.7 3.1 2.8 2.7

ASAHI GROUP HOLDINGS 4,484 19,110 1.0 1.0 1.0 1.0 11.1 10.0 9.6 9.3 14.6 14.0 13.3 12.5 2.2 1.7 1.6 1.5

TSINGTAO BREWERY CO -H 32 6,257 0.9 1.6 1.6 1.5 10.6 10.5 9.6 9.0 34.4 25.6 22.6 20.0 3.1 2.1 2.0 1.9

CONSTELLATION BRANDS INC-A 189 35,848 4.1 4.4 4.1 3.9 17.2 15.1 13.7 12.6 15.9 19.9 18.4 16.4 5.1 3.1 2.8 2.6

THAI BEVERAGE PCL 14 10,786 1.5 1.4 1.3 1.3 17.4 15.3 13.8 13.1 18.9 14.9 13.6 12.4 3.3 2.6 2.3 2.2

UNITED BREWERIES 1,241 4,556 5.8 5.2 4.6 4.0 36.5 29.2 25.1 21.9 83.3 59.8 49.9 42.3 9.3 10.4 8.8 7.4

Source: Nirmal Bang Institutional Equities Research

We initiate coverage on UBL with a Buy rating and a target price of Rs1,525, implying an upside of 23% from the CMP. Our target price is based on a P/E multiple of 50X (September 2020E EPS) which is in line with its forward P/E and EV/EBITDA multiple and represents a discount of more than 20% to its long- term average.

Institutional Equities

United Breweries 31

Risks

We are assuming that the liquor industry is at inflection point as the worst in terms of regulations and taxation is over and increasing millennial population would largely drive growth for premium category. However, any event or announcement hurting the consumer sentiment or plan could be detrimental to our earnings estimates.

We expect inflation to remain at a moderate level in the next couple of years, and any sharp increase thereafter could hurt discretionary spending of consumers and incremental growth could be impacted to a reasonable extent.

Although, we acknowledge the competition in the spirits market, aggressive strategy on account of the second-largest player or any other peer in terms of new brands or competitive pricing could lead to variation in our estimates.

We are banking on the changing lifestyle of the consumer, but any disruption caused to this trend on account of health awareness etc could lead to a different picture altogether.

Institutional Equities

United Breweries 32

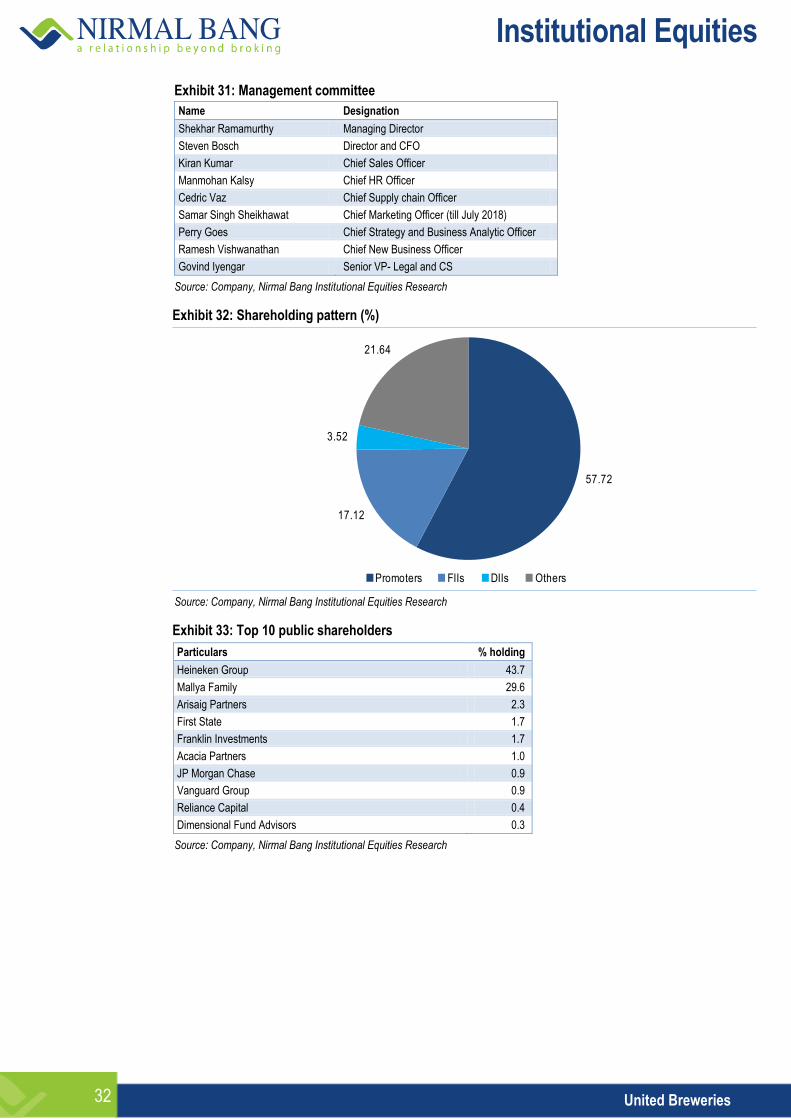

Exhibit 31: Management committee

Name Designation

Shekhar Ramamurthy Managing Director

Steven Bosch Director and CFO

Kiran Kumar Chief Sales Officer

Manmohan Kalsy Chief HR Officer

Cedric Vaz Chief Supply chain Officer

Samar Singh Sheikhawat Chief Marketing Officer (till July 2018)

Perry Goes Chief Strategy and Business Analytic Officer

Ramesh Vishwanathan Chief New Business Officer

Govind Iyengar Senior VP- Legal and CS

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 32: Shareholding pattern (%)

57.72

17.12

3.52

21.64

Promoters FIIs DIIs Others Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 33: Top 10 public shareholders

Particulars % holding

Heineken Group 43.7

Mallya Family 29.6

Arisaig Partners 2.3

First State 1.7

Franklin Investments 1.7

Acacia Partners 1.0

JP Morgan Chase 0.9

Vanguard Group 0.9

Reliance Capital 0.4

Dimensional Fund Advisors 0.3

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

United Breweries 33

Financials (consolidated)

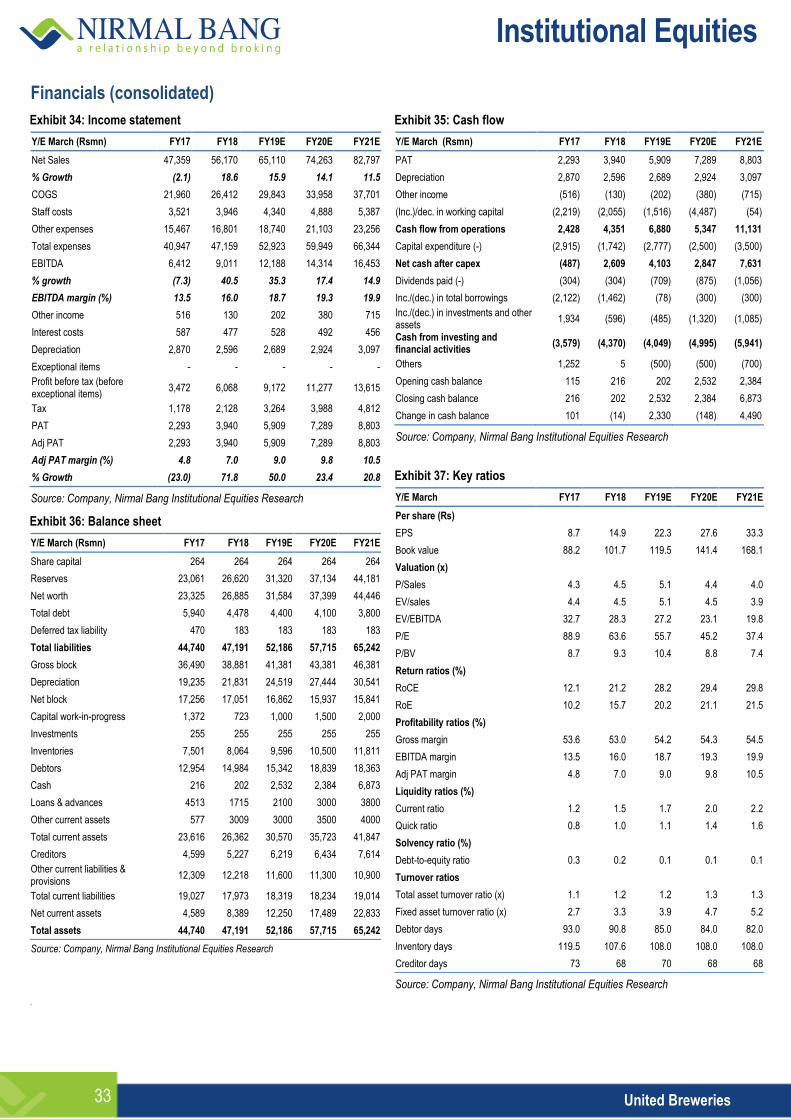

Exhibit 34: Income statement

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Net Sales 47,359 56,170 65,110 74,263 82,797

% Growth (2.1) 18.6 15.9 14.1 11.5

COGS 21,960 26,412 29,843 33,958 37,701

Staff costs 3,521 3,946 4,340 4,888 5,387

Other expenses 15,467 16,801 18,740 21,103 23,256

Total expenses 40,947 47,159 52,923 59,949 66,344

EBITDA 6,412 9,011 12,188 14,314 16,453

% growth (7.3) 40.5 35.3 17.4 14.9

EBITDA margin (%) 13.5 16.0 18.7 19.3 19.9

Other income 516 130 202 380 715

Interest costs 587 477 528 492 456

Depreciation 2,870 2,596 2,689 2,924 3,097

Exceptional items - - - - -

Profit before tax (before exceptional items)

3,472 6,068 9,172 11,277 13,615

Tax 1,178 2,128 3,264 3,988 4,812

PAT 2,293 3,940 5,909 7,289 8,803

Adj PAT 2,293 3,940 5,909 7,289 8,803

Adj PAT margin (%) 4.8 7.0 9.0 9.8 10.5

% Growth (23.0) 71.8 50.0 23.4 20.8

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 36: Balance sheet

Y/E March (Rsmn) FY17 FY18 FY19E FY20E FY21E

Share capital 264 264 264 264 264

Reserves 23,061 26,620 31,320 37,134 44,181

Net worth 23,325 26,885 31,584 37,399 44,446

Total debt 5,940 4,478 4,400 4,100 3,800

Deferred tax liability 470 183 183 183 183

Total liabilities 44,740 47,191 52,186 57,715 65,242

Gross block 36,490 38,881 41,381 43,381 46,381

Depreciation 19,235 21,831 24,519 27,444 30,541

Net block 17,256 17,051 16,862 15,937 15,841

Capital work-in-progress 1,372 723 1,000 1,500 2,000