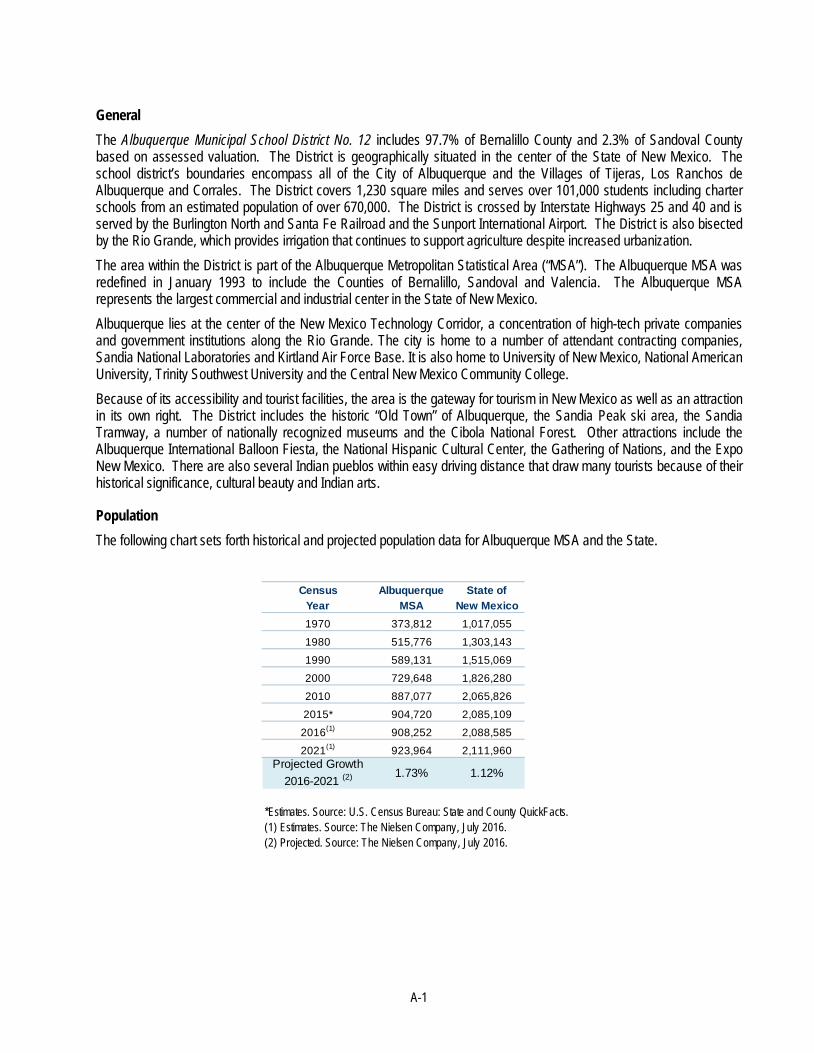

NOTICE ALBUQUERQUE MUNICIPAL SCHOOL DISTRICT NO. 12 Bernalillo and Sandoval Counties, New Mexico $15,000,000 1 - General Obligation Education Technology Notes, Series 2017 Preliminary Official Statement, subject to completion, dated December 1, 2016 The Preliminary Official Statement, dated December 1, 2016 (the “Preliminary Official Statement”) relating to the above-described Notes (the “Notes”) of the Albuquerque Municipal School District No. 12 (the “Issuer” or the “District”), has been posted on the internet as a matter of convenience. Paper copies of the Preliminary Official Statement are available from the Issuer by contacting the financial advisor, RBC Capital Markets, LLC, at (505) 872-5999. The posted version of the Preliminary Official Statement has been formatted in Adobe Portable Document Format (Adobe Acrobat 11.0). Although this format should replicate the Preliminary Official Statement available from the Issuer, its appearance may vary for a number of reasons, including electronic communication difficulties or particular user software or hardware. Using software other than Adobe Acrobat 11.0 may cause the Preliminary Official Statement that you view or print to differ in format from the Preliminary Official Statement. The Preliminary Official Statement and the information contained therein are subject to completion or amendment or other change without notice. Under no circumstances shall the Preliminary Official Statement constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Notes in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The District plans on issuing Series 2017 General Obligation School Building Bonds (the “Bonds”) in conjunction with the Notes. For purposes of Rule 15c2-12 promulgated by the Securities and Exchange Commission, the Preliminary Official Statement alone, and no other document or information on the internet, constitutes the “Official Statement “ that the Issuer has deemed “final” as of its date in respect of the Notes, except for certain pertinent information permitted to be omitted therefrom. No person has been authorized to give any information or to make any representations other than those contained in the Preliminary Official Statement in connection with the offer and sale of the Notes, and, if given or made, such information or representations must not be relied upon as having been authorized. The information and expressions of opinion in the Preliminary Official Statement are subject to change without notice and neither the delivery of the Official Statement nor any sale made thereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Issuer since the date of the Preliminary Official Statement. By choosing to proceed and view the electronic version of the Preliminary Official Statement, you acknowledge that you have read and understood this Notice. Preliminary Official Statement dated December 1, 2016 1 Preliminary, subject to change.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NOTICE

ALBUQUERQUE MUNICIPAL SCHOOL DISTRICT NO. 12 Bernalillo and Sandoval Counties, New Mexico

$15,000,0001 - General Obligation Education Technology Notes, Series 2017

Preliminary Official Statement, subject to completion,

dated December 1, 2016

The Preliminary Official Statement, dated December 1, 2016 (the “Preliminary Official Statement”) relating to the above-described Notes (the “Notes”) of the Albuquerque Municipal School District No. 12 (the “Issuer” or the “District”), has been posted on the internet as a matter of convenience. Paper copies of the Preliminary Official Statement are available from the Issuer by contacting the financial advisor, RBC Capital Markets, LLC, at (505) 872-5999. The posted version of the Preliminary Official Statement has been formatted in Adobe Portable Document Format (Adobe Acrobat 11.0). Although this format should replicate the Preliminary Official Statement available from the Issuer, its appearance may vary for a number of reasons, including electronic communication difficulties or particular user software or hardware. Using software other than Adobe Acrobat 11.0 may cause the Preliminary Official Statement that you view or print to differ in format from the Preliminary Official Statement.

The Preliminary Official Statement and the information contained therein are subject to completion or amendment or other change without notice. Under no circumstances shall the Preliminary Official Statement constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Notes in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The District plans on issuing Series 2017 General Obligation School Building Bonds (the “Bonds”) in conjunction with the Notes.

For purposes of Rule 15c2-12 promulgated by the Securities and Exchange Commission, the Preliminary Official Statement alone, and no other document or information on the internet, constitutes the “Official Statement “ that the Issuer has deemed “final” as of its date in respect of the Notes, except for certain pertinent information permitted to be omitted therefrom.

No person has been authorized to give any information or to make any representations other than those contained in the Preliminary Official Statement in connection with the offer and sale of the Notes, and, if given or made, such information or representations must not be relied upon as having been authorized. The information and expressions of opinion in the Preliminary Official Statement are subject to change without notice and neither the delivery of the Official Statement nor any sale made thereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Issuer since the date of the Preliminary Official Statement.

By choosing to proceed and view the electronic version of the Preliminary Official Statement, you acknowledge that you have read and understood this Notice. Preliminary Official Statement dated December 1, 2016

1 Preliminary, subject to change.

i

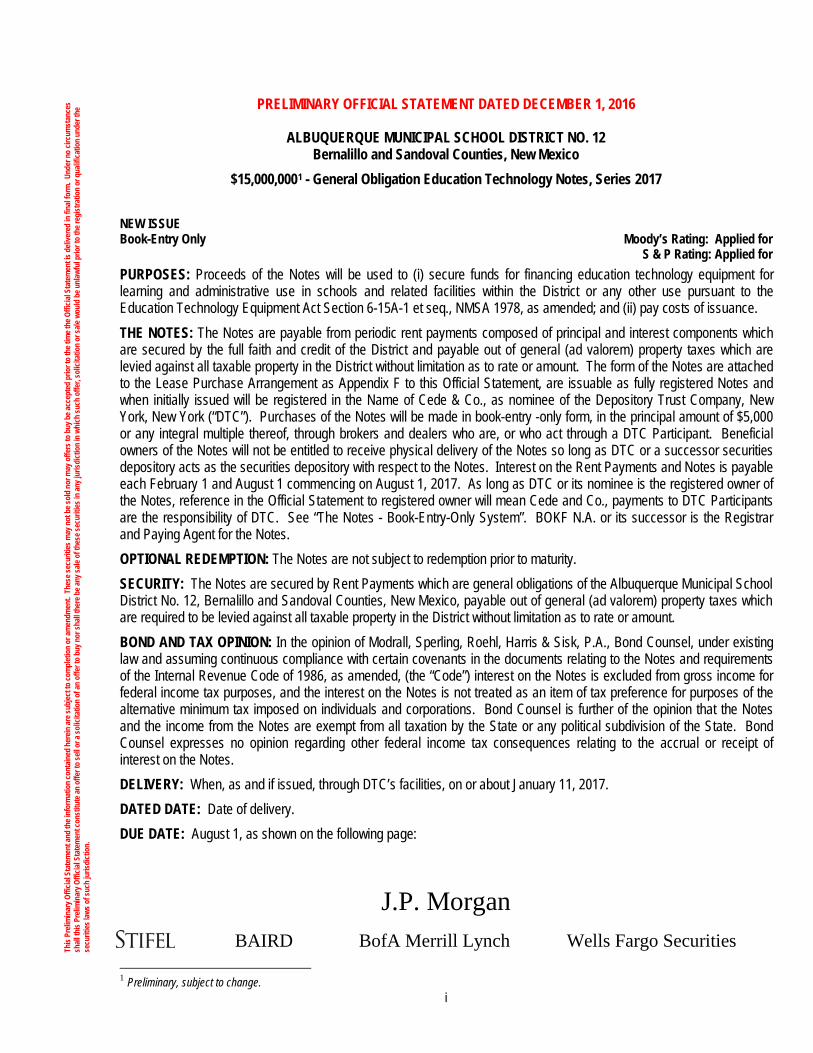

PRELIMINARY OFFICIAL STATEMENT DATED DECEMBER 1, 2016

ALBUQUERQUE MUNICIPAL SCHOOL DISTRICT NO. 12 Bernalillo and Sandoval Counties, New Mexico

$15,000,0001 - General Obligation Education Technology Notes, Series 2017 NEW ISSUE Book-Entry Only Moody’s Rating: Applied for S & P Rating: Applied for PURPOSES: Proceeds of the Notes will be used to (i) secure funds for financing education technology equipment for learning and administrative use in schools and related facilities within the District or any other use pursuant to the Education Technology Equipment Act Section 6-15A-1 et seq., NMSA 1978, as amended; and (ii) pay costs of issuance. THE NOTES: The Notes are payable from periodic rent payments composed of principal and interest components which are secured by the full faith and credit of the District and payable out of general (ad valorem) property taxes which are levied against all taxable property in the District without limitation as to rate or amount. The form of the Notes are attached to the Lease Purchase Arrangement as Appendix F to this Official Statement, are issuable as fully registered Notes and when initially issued will be registered in the Name of Cede & Co., as nominee of the Depository Trust Company, New York, New York (“DTC”). Purchases of the Notes will be made in book-entry -only form, in the principal amount of $5,000 or any integral multiple thereof, through brokers and dealers who are, or who act through a DTC Participant. Beneficial owners of the Notes will not be entitled to receive physical delivery of the Notes so long as DTC or a successor securities depository acts as the securities depository with respect to the Notes. Interest on the Rent Payments and Notes is payable each February 1 and August 1 commencing on August 1, 2017. As long as DTC or its nominee is the registered owner of the Notes, reference in the Official Statement to registered owner will mean Cede and Co., payments to DTC Participants are the responsibility of DTC. See “The Notes - Book-Entry-Only System”. BOKF N.A. or its successor is the Registrar and Paying Agent for the Notes. OPTIONAL REDEMPTION: The Notes are not subject to redemption prior to maturity. SECURITY: The Notes are secured by Rent Payments which are general obligations of the Albuquerque Municipal School District No. 12, Bernalillo and Sandoval Counties, New Mexico, payable out of general (ad valorem) property taxes which are required to be levied against all taxable property in the District without limitation as to rate or amount. BOND AND TAX OPINION: In the opinion of Modrall, Sperling, Roehl, Harris & Sisk, P.A., Bond Counsel, under existing law and assuming continuous compliance with certain covenants in the documents relating to the Notes and requirements of the Internal Revenue Code of 1986, as amended, (the “Code”) interest on the Notes is excluded from gross income for federal income tax purposes, and the interest on the Notes is not treated as an item of tax preference for purposes of the alternative minimum tax imposed on individuals and corporations. Bond Counsel is further of the opinion that the Notes and the income from the Notes are exempt from all taxation by the State or any political subdivision of the State. Bond Counsel expresses no opinion regarding other federal income tax consequences relating to the accrual or receipt of interest on the Notes. DELIVERY: When, as and if issued, through DTC’s facilities, on or about January 11, 2017. DATED DATE: Date of delivery. DUE DATE: August 1, as shown on the following page:

J.P. Morgan

BAIRD BofA Merrill Lynch Wells Fargo Securities

1 Preliminary, subject to change.

This

Preli

min

ary O

fficia

l Sta

tem

ent a

nd th

e inf

orm

atio

n co

ntain

ed h

erein

are s

ubjec

t to

com

plet

ion

or am

endm

ent.

The

se se

curit

ies m

ay n

ot b

e sol

d no

r may

offe

rs to

buy

be a

ccep

ted

prio

r to

the t

ime t

he O

fficia

l Sta

tem

ent i

s deli

vere

d in

fina

l for

m. U

nder

no

circu

mst

ance

s sh

all th

is Pr

elim

inar

y Offi

cial S

tate

men

t con

stitu

te an

offe

r to

sell o

r a so

licita

tion

of an

offe

r to

buy n

or sh

all th

ere b

e any

sale

of th

ese s

ecur

ities

in an

y jur

isdict

ion

in w

hich

such

offe

r, so

licita

tion

or sa

le wo

uld

be u

nlaw

ful p

rior t

o th

e reg

istra

tion

or q

ualif

icatio

n un

der t

he

secu

rities

laws

of s

uch

juris

dict

ion.

ii

Maturing Interest Yield or Cusip # Maturing Interest Yield or Cusip #(August 1) Principal Rate Price 013595 (August 1) Principal Rate Price 013595

2017 $150,000 2020 $3,750,0002018 3,750,000 2021 3,600,0002019 3,750,000

Preliminary, subject to change.

EDUCATION TECHNOLOGY NOTES, SERIES 2017(1)

iii

ISSUER

Albuquerque Municipal School District No. 12 Bernalillo County, New Mexico

P.O. Box 25704 (87125) 6400 Uptown Blvd. NE, 6 East

Albuquerque, New Mexico 87110 (505) 880-3661

(505) 830-0220 - Fax

BOARD OF EDUCATION President: Dr. David Peercy

Vice-President: Lorenzo Garcia Secretary: Steven Michael Quezada

Member: Dr. Analee Maestas Member: Peggy Muller-Aragón

Member: Barbara Petersen Member: Dr. Donald Duran

FINANCIAL ADVISOR RBC Capital Markets, LLC

6301 Uptown Blvd. NE, Suite 110 Albuquerque, New Mexico 87110

(505) 872-5999

PAYING AGENT/REGISTRAR/ESCROW AGENT

BOKF, N.A. 100 Sun Avenue NE, Suite 500

Albuquerque, New Mexico 87109 (505) 222-8447

UNDERWRITERS’ COUNSEL

Hogan Lovells US LLP One Tabor Center, Suite 1500

1200 Seventeenth Street Denver, Colorado 80202

(303) 899-7311

DISTRICT ADMINISTRATION

Superintendent: Raquel Reedy Chief Operations Officer: Scott Elder

Chief Financial Officer: Tami Coleman

BOND COUNSEL/ DISCLOSURE COUNSEL

Modrall, Sperling, Roehl, Harris & Sisk, P.A. 500 Fourth Street NW, Suite 1000 Albuquerque, New Mexico 87102

(505) 848-1800

SENIOR MANAGER

J.P. Morgan Securities LLC 1125 17th Street, Floor 02 Denver, Colorado 80202

CO-MANAGERS

Stifel, Nicolaus & Company, Incorporated 2325 East Camelback Road, Suite 750

Phoenix, Arizona 85016 (602) 794-4001

Robert W. Baird & Co. Inc. 210 University Blvd., Suite 460

Denver, Colorado 80206

BofA Merrill Lynch 333 S. Hope Street, Suite 2310 Los Angeles, California 90071

Wells Fargo Securities 1445 Ross Avenue, Suite 2314

Dallas, Texas 75202

iv

A Few Words About Official Statements

Official statements for municipal securities issues – like this one – contain the only “official” information about a particular issue of municipal securities. This Official Statement is not an offer to sell or solicitation of an offer to buy Notes in any jurisdiction where it is unlawful to make such offer, solicitation or sale and no unlawful offer, solicitation or sale of the Notes may occur through this Official Statement or otherwise. This Official Statement is not a contract and provides no investment advice. Investors should consult their advisors and legal counsel with their questions about this Official Statement, the Notes or anything else related to this issue.

MARKET STABILIZATION In connection with this Official Statement, the Underwriters may over-allot or effect transactions which stabilize and maintain the market price of the Notes at a level above that which might otherwise prevail in the open market. The Underwriters are not obligated to do this and are free to discontinue it at any time. The estimates, forecasts, projections and opinions in this Official Statement are not hard facts, and no one, including the District, guarantees them. The District and other reliable sources have provided information for this Official Statement, with the goal of providing disclosure to investors which meets legal requirements. Modrall, Sperling, Roehl, Harris & Sisk, P.A. Albuquerque, New Mexico is serving as special counsel for disclosure to the District, has assisted in the preparation of the Official Statement, has reviewed its contents, and has participated in conferences with representatives of the District, Financial Advisor, and the Underwriters to issue its disclosure counsel opinion. Such firm has no responsibility for the accuracy or completeness of any information furnished in connection with any offer or sale of the Notes in the Official Statement or otherwise. The legal fees to be paid to bond counsel and disclosure counsel for services rendered in connection with the issuance of the Notes is contingent upon the sale and delivery of such Notes and all legal fees will be paid from Note proceeds. Any part of this Official Statement may change at any time, without prior notice. Also, important information about the District and other relevant matters may change after the date of this Official Statement. All document summaries are just that – they are not complete or definitive, and they may omit relevant information. Such documents are qualified in their entirety by reference to the complete documents. Any investor who wishes to review the full text of documents may request them at no cost from the District or the Financial Advisor as follows:

District Albuquerque Municipal School District

P.O. Box 25704 (87125) 6400 Uptown Blvd. NE, 6E

Albuquerque, New Mexico 87110 Attn: Tami Coleman

Financial Advisor RBC Capital Markets, LLC

6301 Uptown Blvd. NE, Suite 110 Albuquerque, NM 87110

Attn: Paul J. Cassidy

iii

TABLE OF CONTENTS

Page Page

INTRODUCTION ................................................................. 1 THE ISSUER ...................................................................... 1 SECURITY ........................................................................ 1 LIMITED ROLE OF AUDITORS ................................................ 1 PLAN OF FINANCE .............................................................. 1 SELECTED DEBT RATIOS ..................................................... 2

THE NOTES ....................................................................... 2 GENERAL TERMS AND DESCRIPTION OF THE NOTES ................. 2 BOND REGISTRAR AND PAYING AGENT .................................. 2 OPTIONAL PRIOR REDEMPTION ............................................ 2 RECORD DATE .................................................................. 2 TRANSFERS AND EXCHANGES .............................................. 3

SECURITY AND REMEDIES ................................................ 3 LIMITATIONS OF REMEDIES .................................................. 3

SOURCES AND USES OF FUNDS ....................................... 3

DEBT AND OTHER FINANCIAL OBLIGATIONS ................... 4 OUTSTANDING DEBT .......................................................... 5 DEBT SERVICE REQUIREMENTS TO MATURITY ......................... 6 STATEMENT OF ESTIMATED DIRECT AND OVERLAPPING DEBT .... 7

TAX BASE.......................................................................... 8 ANALYSIS OF ASSESSED VALUATION ..................................... 8 HISTORY OF ASSESSED VALUATION....................................... 9 MAJOR TAXPAYERS ............................................................ 9 SCHOOL TAX RATES........................................................... 9 TAX RATES ..................................................................... 10 YIELD CONTROL LIMITATION .............................................. 11 DEVELOPMENTS LIMITING RESIDENTIAL PROPERTY TAX INCREASES ..................................................................... 11 TAX COLLECTIONS ........................................................... 12 INTEREST ON DELINQUENT TAXES ....................................... 12 PENALTY FOR DELINQUENT TAXES ...................................... 13 REMEDIES AVAILABLE FOR NON-PAYMENT OF TAXES ............. 13

THE DISTRICT.................................................................. 13 SCHOOL DISTRICT POWERS ............................................... 13 MANAGEMENT ................................................................. 14 INSURANCE .................................................................... 15 INTERGOVERNMENTAL AGREEMENTS ................................... 15 SCHOOL PROPERTY ......................................................... 15

STUDENT ENROLLMENT ..................................................... 15

FINANCES OF THE EDUCATIONAL PROGRAM ................ 16 DISTRICT BUDGET PROCESS .............................................. 16 SOURCES OF REVENUE FOR GENERAL FUND ......................... 16 STATE EQUALIZATION GUARANTEE ...................................... 17 STATEMENT OF NET POSITION ............................................ 19 STATEMENT OF ACTIVITIES ................................................ 20 BALANCE SHEET – GENERAL FUND ..................................... 21 STATEMENT OF REVENUES & EXPENDITURES & CHANGES IN FUND BALANCES – GENERAL FUND ............................................. 22 DEBT SERVICE FUNDS ...................................................... 22 CAPITAL PROJECTS FUNDS ................................................ 22 FIDUCIARY FUNDS ............................................................ 23 EMPLOYEES AND RETIREMENT PLAN ................................... 23 PENSION PLAN STATISTICS ................................................ 25

TAX MATTERS ................................................................. 26 INTERNAL REVENUE SERVICE AUDIT PROGRAM ..................... 26 ORIGINAL ISSUE DISCOUNT ................................................ 26 ORIGINAL ISSUE PREMIUM ................................................. 27

LITIGATION ...................................................................... 27 RECENT EVENTS ............................................................. 27

RATINGS .......................................................................... 28

THE FINANCIAL ADVISOR................................................ 28

LEGAL MATTERS............................................................. 29

CONTINUING DISCLOSURE UNDERTAKING .................... 29

DISCLOSURE CERTIFICATE ............................................ 30

ADDITIONAL MATTERS ................................................... 30

A LAST WORD ................................................................. 31 APPENDICES: A. ECONOMIC AND DEMOGRAPHIC INFORMATION

RELATING TO THE DISTRICT B. JUNE 30, 2015 AUDITED FINANCIAL STATEMENTS C. THE BOOK-ENTRY-ONLY SYSTEM D. FORM OF BOND COUNSEL OPINION E. CONTINUING DISCLOSURE UNDERTAKING F. LEASE PURCHASE ARRANGEMENT

1

Albuquerque Municipal School District No. 12 Bernalillo and Sandoval Counties, New Mexico $15,000,0001 - General Obligation Education Technology Notes, Series 2017

INTRODUCTION Thank you for your interest in learning more about the $15,000,000 Albuquerque Municipal School District No. 12, Bernalillo and Sandoval Counties, New Mexico, General Obligation Education Technology Notes, Series 2017 (the “Notes”). This Official Statement will tell you about the Notes, their security and the risks involved in an investment in the Notes. Although the District has approved this Official Statement, it does not intend it to substitute for competent investment advice, tailored for your situation. The Issuer The District is a political subdivision of the State of New Mexico (the "State") organized for the purpose of operating and maintaining an educational program for the school-age children residing within its boundaries. The District encompasses almost all of Bernalillo County and a portion of Sandoval County (the “Counties”). Both counties are centrally located in New Mexico. The District’s boundaries encompass all of the City of Albuquerque and the Villages of Tijeras, Los Ranchos and Corrales. The District's 2016 assessed valuation is $15,849,486,540. The District had an enrollment of 85,905 students for the 2016-17 school year based on the 40th day count. There are 54 charter schools operating within the District’s boundaries with 16,845 students attending in 2015-16 school year based on the 40th day count. See "THE DISTRICT." Security The Notes are payable from periodic rent payments which Lessor hereby assigns to the Paying Agent/Registrar composed of principal and interest components which are secured by the full faith and credit of the District and payable out of general (ad valorem) property taxes which are levied against all taxable property in the District without limitation as to rate or amount. The Lessor assigns the Rent Payments received from the Lessee to the Paying Agent/Registrar for payment to the owners of the Note. Neither the State nor Counties have any responsibility to pay the debt service on the Notes. Limited Role of Auditors This document presents information from District records and other sources including a portion of the audited financial statements of the District for the year ended June 30, 2015, contained in Appendix B. CliftonLarsonAllen, LLP, the District’s independent auditor, has not been engaged to perform and has not performed, since the date of the report included herein, any procedures on the financial statements addressed in that report. It also has not performed any procedures relating to this Official Statement. Plan of Finance Proceeds of the Notes will be used to (i) secure funds for financing education technology equipment for learning and administrative use in schools and related facilities within the District or any other use pursuant to the Education Technology Equipment Act Section 6-15A-1 et seq., NMSA 1978, as amended; and (ii) pay costs of issuance. In conjunction with the Notes, the District also expects to issue approximately $100,000,0001 of General Obligation School Building Bonds, Series 2017 (the “Bonds”). The proceeds of the Bonds will be used for the purposes of erecting, remodeling, making additions to and furnishing school buildings, purchasing and improving school grounds and purchasing computer software and hardware for student use in public school classrooms, providing matching funds for capital outlay projects funded pursuant to the Public School Capital Outlay Act, or any combination of those purposes within the District and paying costs of issuance associated with the Bonds. 1 Preliminary, subject to change.

2

Selected Debt Ratios 2016

2016 Assessed Valuation $15,849,486,540

2016 Actual Valuation (1) $58,241,501,394

District General Obligation Debt Outstanding (Including the Bonds & Notes) $623,630,000 (2)

District Net General Obligation Debt $614,797,140Estimated Direct & Overlapping G/O Debt $1,322,589,903

District Net Debt as a Percentage of Assessed Valuation 3.88% Estimated Actual Valuation 1.06%

Direct & Overlapping Debt as Percentage of Assessed Valuation 8.34% Estimated Actual Valuation 2.27%

Estimated Population 670,893

District Net Debt Per Capita $916.39Direct and Overlapping Debt Per Capita $1,971.39

(1) Actual valuation is computed by adding the exemptions to the assessed valuation and multiplying by three.

(2) Preliminary, subject to change.

THE NOTES New Mexico law enables the District to issue the General Obligation Education Technology Notes pursuant to Section 6-15A-1 et seq., NMSA, 1978.

General Terms and Description of the Notes The Notes will bear interest at the rates and mature in the amounts and on the dates shown on the inside front cover of this Official Statement. All Notes are fully registered in denominations of $5,000 or integral multiples thereof in conformance with the Constitution and laws of the State and pursuant to the Note Resolution. Notes payments are made to The Depository Trust Company (“DTC”), and DTC will then remit the payments to its participants for disbursement to the beneficial owners of the Notes. See “Book-Entry-Only System” in Appendix C.

Bond Registrar and Paying Agent BOKF, N.A. will serve as Registrar, Paying Agent and Escrow Agent for the Notes.

Optional Prior Redemption The Notes are not subject to optional redemption by the District prior to their stated maturity date.

Record Date The Record Date for the Notes with respect to any interest payment date is the 15th day of the month (whether or not a business day) immediately preceding the interest payment date. The person in whose name any Note is registered on any Record Date with respect to any interest payment date shall be entitled to receive the interest payable thereon on such interest payment date notwithstanding any transfer or exchange thereof subsequent to such Record Date and prior to such interest payment date.

3

Transfers and Exchanges Registered Note owners may surrender and transfer their Notes, in person or by duly authorized attorney, at the office of the Paying Agent and Registrar. They must complete an approved transfer form and pay any taxes or governmental charges which apply to the transfer. As explained below, while DTC is the securities depository for the Notes, it will be the sole registered owner of the Notes.

SECURITY AND REMEDIES The Notes are secured by Rent Payments which are general obligations of the District paid out of general (ad valorem) property taxes which are required to be levied against all taxable property in the District without limitation as to rate or amount. The District must use all of the property taxes collected for debt service, and any other legally available money, to pay the debt service on the Notes and other outstanding debt. Various New Mexico laws and constitutional provisions apply to the assessment and collection of ad valorem property taxes. There is no guarantee that there will not be any changes that would have a material effect on the District. Limitations of Remedies There is no provision for acceleration of maturity of the principal of the Notes in the event of a default in the payment of principal of or interest on the Notes. Consequently, remedies available to the owners of the Notes may need to be enforced from year to year. The enforceability of the rights and remedies of the owners of the Notes, and the obligations incurred by the District in issuing the Notes, are subject to the following: the federal bankruptcy code and applicable bankruptcy, insolvency, reorganization, moratorium, or similar laws relating to or affecting the enforcement of creditor's rights generally, now or hereafter in effect; usual equity principles that may limit the specific enforcement under State law of certain remedies; the exercise by the United States of America of the powers delegated to it by the federal Constitution; and the reasonable and necessary exercise, in certain exceptional situations, of the police power inherent in the sovereignty of the State and its governmental bodies in the interest of serving a significant and legitimate public purpose. Bankruptcy proceedings, or the exercise of powers by the federal or State government, if initiated, could subject the owners of the Notes to judicial discretion and interpretation of their rights in bankruptcy or otherwise, and consequently may entail risks of delay, limitation, or modification of their rights.

SOURCES AND USES OF FUNDS It is anticipated that the proceeds of the Notes will be applied as follows:

Series 2017 G/OEducation Technology Notes

Par amount

Premium

Total $0.00

Uses Project Fund

Costs of Issuance

Underwriters' Discount

Deposit to Debt Service Fund

Total $0.00

Sources

4

DEBT AND OTHER FINANCIAL OBLIGATIONS Article IX, Section 11 of the New Mexico Constitution limits the powers of a district to incur general obligation debt extending beyond the fiscal year. The district can incur such debt for the purpose of erecting, remodeling, making additions to and furnishing school buildings or purchasing or improving school grounds, to purchase computer software and hardware for student use in public schools, to provide matching funds for capital outlay projects funded pursuant to the Public School Capital Outlay Act, or any combination of these purposes but only after the proposition to create any such debt has been submitted to a vote of the qualified electors of the district, and a majority of those voting on the question vote in favor of creating the debt. The total indebtedness of the district may not exceed 6% of the assessed valuation of the taxable property within the district as shown by the last preceding general assessment. The district also may create a debt by entering into a lease-purchase arrangement to acquire education technology equipment without submitting the proposition to a vote of the qualified electors of the district, but any such debt is subject to the 6% debt limitation. The issuance of refunding bonds does not have to be submitted to a vote of the qualified electors of the district. The assessed valuation of taxable property within the District is $15,849,486,540 for tax year 2016, as approved by the State of New Mexico Taxation and Revenue Department, Property Tax Division. The maximum general obligation indebtedness of the District may not exceed 6% of the assessed valuation or $950,969,192. After the Notes are issued, the ratio of total outstanding general obligation (G/O) debt of the District to the 2016 assessed valuation will be no greater than 3.88% as summarized below:

2016 Assessed Valuation $15,849,486,5402016 Actual Valuation (1) $58,241,501,394

Total Bonded Debt Outstanding (Including the Bonds & Notes) $623,630,000 (3)

Less Estimated Debt Service Fund Balance (2) 8,832,860NET DEBT $614,797,140

Ratio of Estimated Net Debt to 2016 Assessed Valuation: 3.88%Ratio of Estimated Net Debt to 2016 Actual Valuation: 1.06%Per Capita Net Bonded Debt: $916.39Est. Population: 670,893

(1) Actual valuation is computed by adding the exemptions to the assessed valution and multiplying by three.

(2) As of 9/30/2016, the debt service cash balance for the Bonds and Notes was $13,054,652. The amount attributable to principal reduction is 68%.

(3) Preliminary, subject to change.

5

Outstanding Debt The District has issued debt (“Outstanding Debt”) in the past for various capital improvements and has never defaulted in the payment of any of its debt or other obligations. Listed below is the District's total general obligation debt outstanding including the Notes.

Original Amount Final PrincipalIssued Maturity Outstanding

Series 2004 QZAB $4,625,000 08/01/20 $4,625,000 (1)

Series 2006 QZAB 7,160,000 08/01/20 7,160,000 (1)

Series 2009A 124,700,000 08/01/22 73,600,000

Series 2009C - QSCBs 14,300,000 08/01/24 14,300,000

Series 2009D Ref 16,800,000 08/01/18 6,505,000

Series 2010A 85,410,000 08/01/21 46,750,000

Series 2010B - QSCBs 32,690,000 08/01/27 32,690,000

Series 2010C - BABs 31,900,000 08/01/24 31,900,000

Series 2012 Ref 39,670,000 08/01/21 25,045,000

Series 2012 - ETNs 13,000,000 08/01/17 1,950,000

Series 2013A 43,400,000 08/01/29 30,000,000

Series 2014 - ETNs 15,000,000 08/01/19 8,000,000

Series 2014A 75,000,000 08/01/29 65,500,000

Series 2014B Ref 94,305,000 08/01/23 94,305,000

Series 2015 70,000,000 08/01/30 66,300,000

Series 2017 100,000,000 08/01/33 100,000,000 (2)

Series 2017 - ETNs 15,000,000 08/01/21 15,000,000 (2)

$782,960,000 $623,630,000 (2)

(1) An irrevocable escrow account has been established to pay the principal in 2020 for the Series 2004 General Obligation Qualified Zone Academy Bonds ("QZABs") of $4,625,000 and Series 2006 QZABs of $7,160,000. The District makes semi-annual payments of $111,255 and $199,641, respectively, for the 2004 and 2006 QZABs.

(2) Preliminary, subject to change. Note: The District has a Lease Purchase Arrangement outstanding with the New Mexico Finance Authority (“NMFA”) in the amount of $2,447,266 for the purchase of a building facility occupied by DATA Charter School which receives annual appropriations. The District has entered into a sublease agreement with DATA Charter School whereby the proceeds from the sublease with DATA Charter School will be used by the District to pay the lease purchase payments to NMFA. This outstanding loan with NMFA is not considered general obligation debt.

6

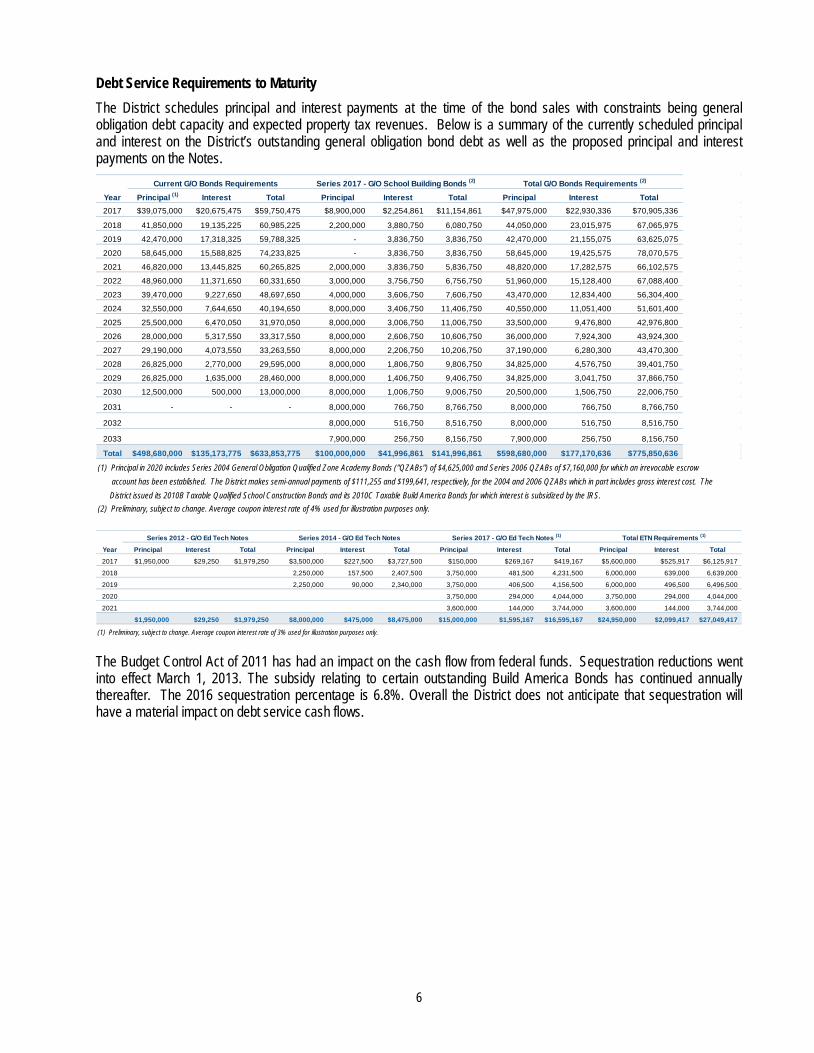

Debt Service Requirements to Maturity The District schedules principal and interest payments at the time of the bond sales with constraints being general obligation debt capacity and expected property tax revenues. Below is a summary of the currently scheduled principal and interest on the District’s outstanding general obligation bond debt as well as the proposed principal and interest payments on the Notes.

Year Principal (1) Interest Total Principal Interest Total Principal Interest Total2017 $39,075,000 $20,675,475 $59,750,475 $8,900,000 $2,254,861 $11,154,861 $47,975,000 $22,930,336 $70,905,336

2018 41,850,000 19,135,225 60,985,225 2,200,000 3,880,750 6,080,750 44,050,000 23,015,975 67,065,975

2019 42,470,000 17,318,325 59,788,325 - 3,836,750 3,836,750 42,470,000 21,155,075 63,625,075

2020 58,645,000 15,588,825 74,233,825 - 3,836,750 3,836,750 58,645,000 19,425,575 78,070,575

2021 46,820,000 13,445,825 60,265,825 2,000,000 3,836,750 5,836,750 48,820,000 17,282,575 66,102,575

2022 48,960,000 11,371,650 60,331,650 3,000,000 3,756,750 6,756,750 51,960,000 15,128,400 67,088,400

2023 39,470,000 9,227,650 48,697,650 4,000,000 3,606,750 7,606,750 43,470,000 12,834,400 56,304,400

2024 32,550,000 7,644,650 40,194,650 8,000,000 3,406,750 11,406,750 40,550,000 11,051,400 51,601,400

2025 25,500,000 6,470,050 31,970,050 8,000,000 3,006,750 11,006,750 33,500,000 9,476,800 42,976,800

2026 28,000,000 5,317,550 33,317,550 8,000,000 2,606,750 10,606,750 36,000,000 7,924,300 43,924,300

2027 29,190,000 4,073,550 33,263,550 8,000,000 2,206,750 10,206,750 37,190,000 6,280,300 43,470,300

2028 26,825,000 2,770,000 29,595,000 8,000,000 1,806,750 9,806,750 34,825,000 4,576,750 39,401,750

2029 26,825,000 1,635,000 28,460,000 8,000,000 1,406,750 9,406,750 34,825,000 3,041,750 37,866,750

2030 12,500,000 500,000 13,000,000 8,000,000 1,006,750 9,006,750 20,500,000 1,506,750 22,006,750

2031 - - - 8,000,000 766,750 8,766,750 8,000,000 766,750 8,766,750

2032 8,000,000 516,750 8,516,750 8,000,000 516,750 8,516,750

2033 7,900,000 256,750 8,156,750 7,900,000 256,750 8,156,750

Total $498,680,000 $135,173,775 $633,853,775 $100,000,000 $41,996,861 $141,996,861 $598,680,000 $177,170,636 $775,850,636

(1) Principal in 2020 includes Series 2004 General Obligation Qualified Zone Academy Bonds ("QZABs") of $4,625,000 and Series 2006 QZABs of $7,160,000 for which an irrevocable escrow account has been established. The District makes semi-annual payments of $111,255 and $199,641, respectively, for the 2004 and 2006 QZABs which in part includes gross interest cost. The District issued its 2010B Taxable Qualified School Construction Bonds and its 2010C Taxable Build America Bonds for which interest is subsidized by the IRS.(2) Preliminary, subject to change. Average coupon interest rate of 4% used for illustration purposes only.

Current G/O Bonds Requirements Total G/O Bonds Requirements (2)Series 2017 - G/O School Building Bonds (2)

Year Principal Interest Total Principal Interest Total Principal Interest Total Principal Interest Total

2017 $1,950,000 $29,250 $1,979,250 $3,500,000 $227,500 $3,727,500 $150,000 $269,167 $419,167 $5,600,000 $525,917 $6,125,917

2018 2,250,000 157,500 2,407,500 3,750,000 481,500 4,231,500 6,000,000 639,000 6,639,000

2019 2,250,000 90,000 2,340,000 3,750,000 406,500 4,156,500 6,000,000 496,500 6,496,500

2020 3,750,000 294,000 4,044,000 3,750,000 294,000 4,044,000

2021 3,600,000 144,000 3,744,000 3,600,000 144,000 3,744,000

$1,950,000 $29,250 $1,979,250 $8,000,000 $475,000 $8,475,000 $15,000,000 $1,595,167 $16,595,167 $24,950,000 $2,099,417 $27,049,417

(1) Preliminary, subject to change. Average coupon interest rate of 3% used for illustration purposes only.

Series 2012 - G/O Ed Tech Notes Series 2017 - G/O Ed Tech Notes (1) Total ETN Requirements (1)Series 2014 - G/O Ed Tech Notes

The Budget Control Act of 2011 has had an impact on the cash flow from federal funds. Sequestration reductions went into effect March 1, 2013. The subsidy relating to certain outstanding Build America Bonds has continued annually thereafter. The 2016 sequestration percentage is 6.8%. Overall the District does not anticipate that sequestration will have a material impact on debt service cash flows.

7

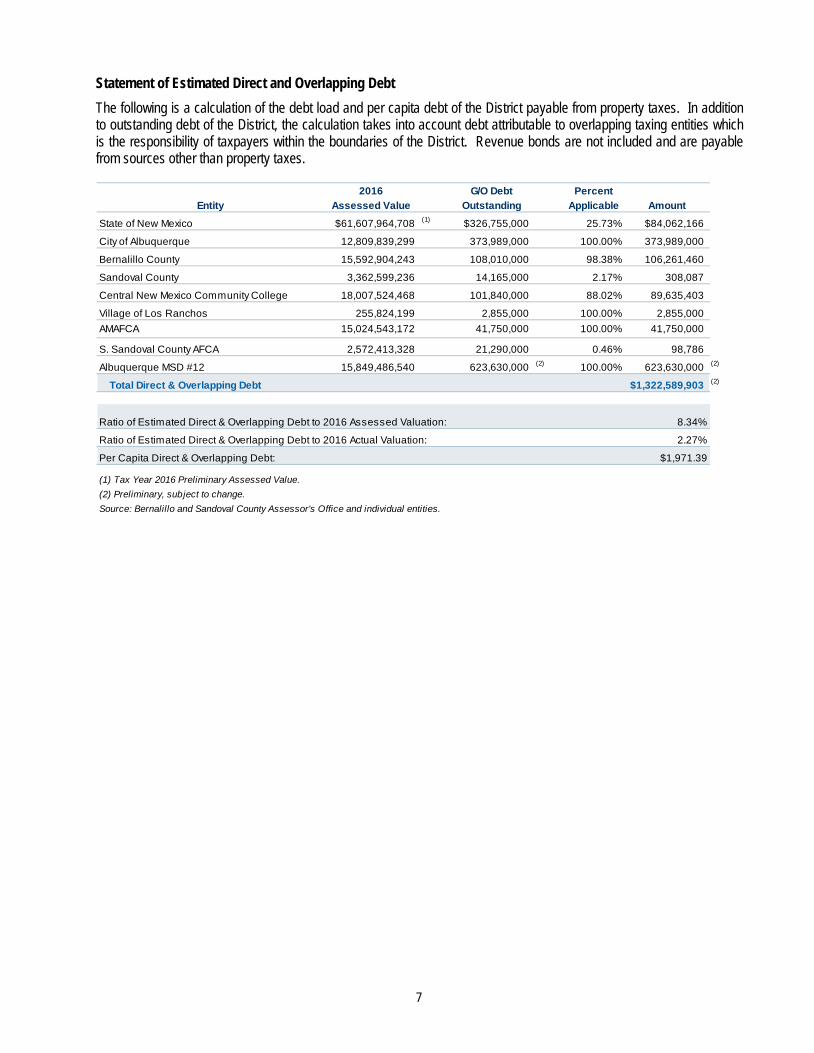

Statement of Estimated Direct and Overlapping Debt The following is a calculation of the debt load and per capita debt of the District payable from property taxes. In addition to outstanding debt of the District, the calculation takes into account debt attributable to overlapping taxing entities which is the responsibility of taxpayers within the boundaries of the District. Revenue bonds are not included and are payable from sources other than property taxes.

2016 G/O Debt Percent Entity Assessed Value Outstanding Applicable Amount

State of New Mexico $61,607,964,708 (1) $326,755,000 25.73% $84,062,166

City of Albuquerque 12,809,839,299 373,989,000 100.00% 373,989,000

Bernalillo County 15,592,904,243 108,010,000 98.38% 106,261,460

Sandoval County 3,362,599,236 14,165,000 2.17% 308,087

Central New Mexico Community College 18,007,524,468 101,840,000 88.02% 89,635,403

Village of Los Ranchos 255,824,199 2,855,000 100.00% 2,855,000 AMAFCA 15,024,543,172 41,750,000 100.00% 41,750,000

S. Sandoval County AFCA 2,572,413,328 21,290,000 0.46% 98,786

Albuquerque MSD #12 15,849,486,540 623,630,000 (2) 100.00% 623,630,000 (2)

Total Direct & Overlapping Debt $1,322,589,903 (2)

Ratio of Estimated Direct & Overlapping Debt to 2016 Assessed Valuation: 8.34%

Ratio of Estimated Direct & Overlapping Debt to 2016 Actual Valuation: 2.27%

Per Capita Direct & Overlapping Debt: $1,971.39

(1) Tax Year 2016 Preliminary Assessed Value.(2) Preliminary, subject to change.Source: Bernalillo and Sandoval County Assessor's Office and individual entities.

8

TAX BASE Analysis of Assessed Valuation Assessed Valuation of property within the District is calculated as follows: Of the total estimated actual valuation of all taxable property in the District, 33-1/3% is legally subject to ad valorem taxes. After deduction of certain personal exemptions, the 2016 assessed valuation is $15,849,486,540. The actual value of personal property within the District (see "Assessments" below) is determined by the County Assessor. The actual value of certain property within the District (see "Centrally Assessed" below) is determined by the State of New Mexico, Taxation and Revenue Department, Property Tax Division. The analysis of Assessed Valuation follows.

2012 2013 2014 2015 2016Assessments

Value of Land 5,906,813,865$ 5,952,979,105$ $5,998,412,077 6,074,923,232$ 6,096,679,421$ Improvements 11,130,654,783 11,309,860,160 11,586,717,135 11,879,356,387 12,310,560,860Personal Property 417,744,022 410,972,559 423,964,859 439,684,411 456,199,122Mobile Homes 48,209,149 48,070,176 47,500,004 45,914,324 46,375,126Livestock 1,005,793 1,048,857 1,001,787 1,689,431 1,292,204

Assessor's Total Valuation 17,504,427,612$ 17,722,930,857$ 18,057,595,862$ 18,441,567,785$ 18,911,106,733$

Less ExemptionsHead of Family 198,426,899$ 198,649,431$ $198,923,200 202,130,886$ 201,459,476$ Veterans 262,668,629 271,467,283 279,185,992 293,349,048 305,793,498 Other 2,898,393,631 2,967,147,829 2,970,475,406 3,057,255,810 3,057,094,284

Total Exemptions 3,359,489,159$ 3,437,264,543$ 3,448,584,598$ 3,552,735,744$ 3,564,347,258$

Assessors Net Valuation 14,144,938,453$ 14,285,666,314$ 14,609,011,264$ 14,888,832,041$ 15,346,759,475$

Centrally Assessed 501,031,823 471,532,736 486,445,306 485,801,905 502,727,065

Total Assessed Valuation 14,645,970,276$ 14,757,199,050$ 15,095,456,570$ 15,374,633,946$ 15,849,486,540$

2012 2013 2014 2015 2016Residential 10,734,595,776$ 10,933,360,182$ 11,248,957,181$ 11,545,459,995$ 12,007,217,036$ Non-Residential 3,911,374,500 3,823,838,868 3,846,499,389 3,829,173,951 3,842,269,504

Total 14,645,970,276$ 14,757,199,050$ 15,095,456,570$ 15,374,633,946$ 15,849,486,540$

Cross County Assessed Valuation2012 2013 2014 2015 2016

Bernalillo County 14,303,913,042$ 14,413,800,252$ 14,743,206,829$ 14,832,114,991$ 15,495,589,301$ Sandoval County (1)

342,057,234 343,398,798 352,249,741 542,518,955 353,897,239

Total 14,645,970,276$ 14,757,199,050$ 15,095,456,570$ 15,374,633,946$ 15,849,486,540$

(1) Portion of Corrales located in Sandoval County (2A-In Corrales & 2AC - Albuquerque/Corrales).

Source: Bernalillo and Sandoval Counties Assessor's Offices.

9

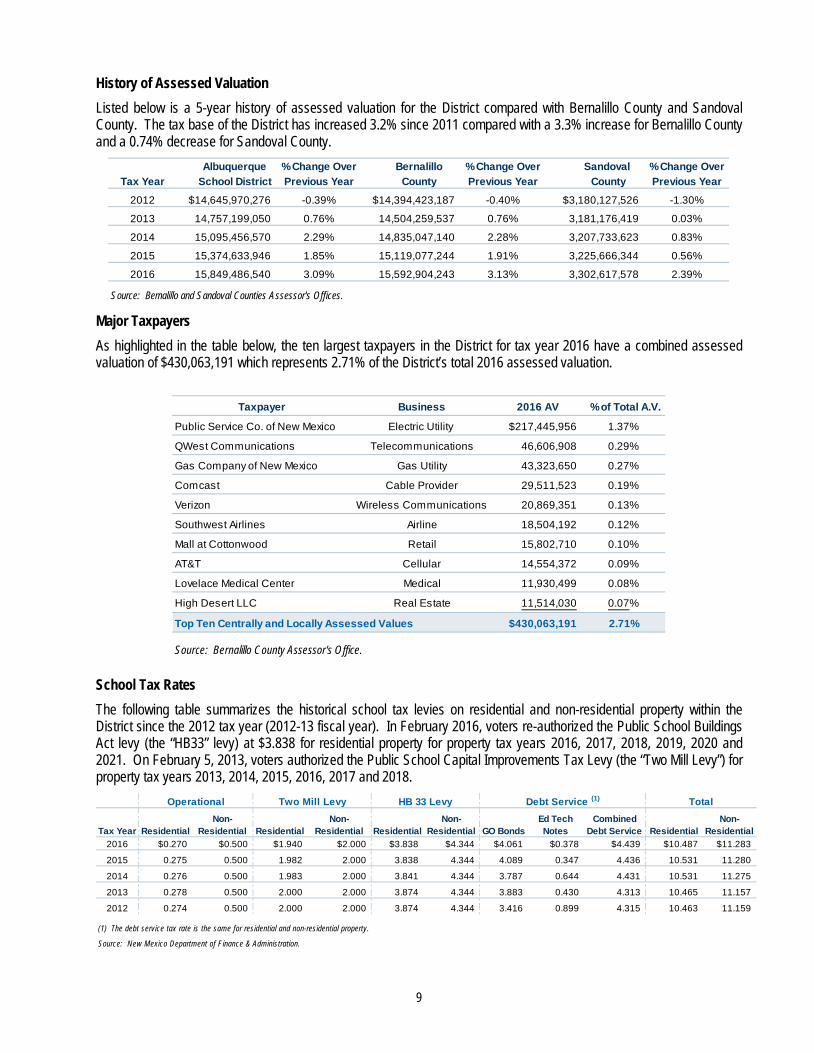

History of Assessed Valuation Listed below is a 5-year history of assessed valuation for the District compared with Bernalillo County and Sandoval County. The tax base of the District has increased 3.2% since 2011 compared with a 3.3% increase for Bernalillo County and a 0.74% decrease for Sandoval County.

Albuquerque % Change Over Bernalillo % Change Over Sandoval % Change OverTax Year School District Previous Year County Previous Year County Previous Year

2012 $14,645,970,276 -0.39% $14,394,423,187 -0.40% $3,180,127,526 -1.30%

2013 14,757,199,050 0.76% 14,504,259,537 0.76% 3,181,176,419 0.03%

2014 15,095,456,570 2.29% 14,835,047,140 2.28% 3,207,733,623 0.83%

2015 15,374,633,946 1.85% 15,119,077,244 1.91% 3,225,666,344 0.56%

2016 15,849,486,540 3.09% 15,592,904,243 3.13% 3,302,617,578 2.39%

Source: Bernalillo and Sandoval Counties Assessor's Offices. Major Taxpayers As highlighted in the table below, the ten largest taxpayers in the District for tax year 2016 have a combined assessed valuation of $430,063,191 which represents 2.71% of the District’s total 2016 assessed valuation.

Taxpayer Business 2016 AV % of Total A.V.

Public Service Co. of New Mexico Electric Utility $217,445,956 1.37%

QWest Communications Telecommunications 46,606,908 0.29%

Gas Company of New Mexico Gas Utility 43,323,650 0.27%

Comcast Cable Provider 29,511,523 0.19%

Verizon Wireless Communications 20,869,351 0.13%

Southwest Airlines Airline 18,504,192 0.12%

Mall at Cottonwood Retail 15,802,710 0.10%

AT&T Cellular 14,554,372 0.09%

Lovelace Medical Center Medical 11,930,499 0.08%

High Desert LLC Real Estate 11,514,030 0.07%

Top Ten Centrally and Locally Assessed Values $430,063,191 2.71%

Source: Bernalillo County Assessor's Office.

School Tax Rates The following table summarizes the historical school tax levies on residential and non-residential property within the District since the 2012 tax year (2012-13 fiscal year). In February 2016, voters re-authorized the Public School Buildings Act levy (the “HB33” levy) at $3.838 for residential property for property tax years 2016, 2017, 2018, 2019, 2020 and 2021. On February 5, 2013, voters authorized the Public School Capital Improvements Tax Levy (the “Two Mill Levy”) for property tax years 2013, 2014, 2015, 2016, 2017 and 2018.

Tax Year ResidentialNon-

Residential ResidentialNon-

Residential ResidentialNon-

Residential GO BondsEd Tech Notes

Combined Debt Service Residential

Non-Residential

2016 $0.270 $0.500 $1.940 $2.000 $3.838 $4.344 $4.061 $0.378 $4.439 $10.487 $11.283

2015 0.275 0.500 1.982 2.000 3.838 4.344 4.089 0.347 4.436 10.531 11.280

2014 0.276 0.500 1.983 2.000 3.841 4.344 3.787 0.644 4.431 10.531 11.275

2013 0.278 0.500 2.000 2.000 3.874 4.344 3.883 0.430 4.313 10.465 11.157

2012 0.274 0.500 2.000 2.000 3.874 4.344 3.416 0.899 4.315 10.463 11.159

(1) The debt service tax rate is the same for residential and non-residential property.

Source: New Mexico Department of Finance & Administration.

TotalDebt Service (1)Operational Two Mill Levy HB 33 Levy

10

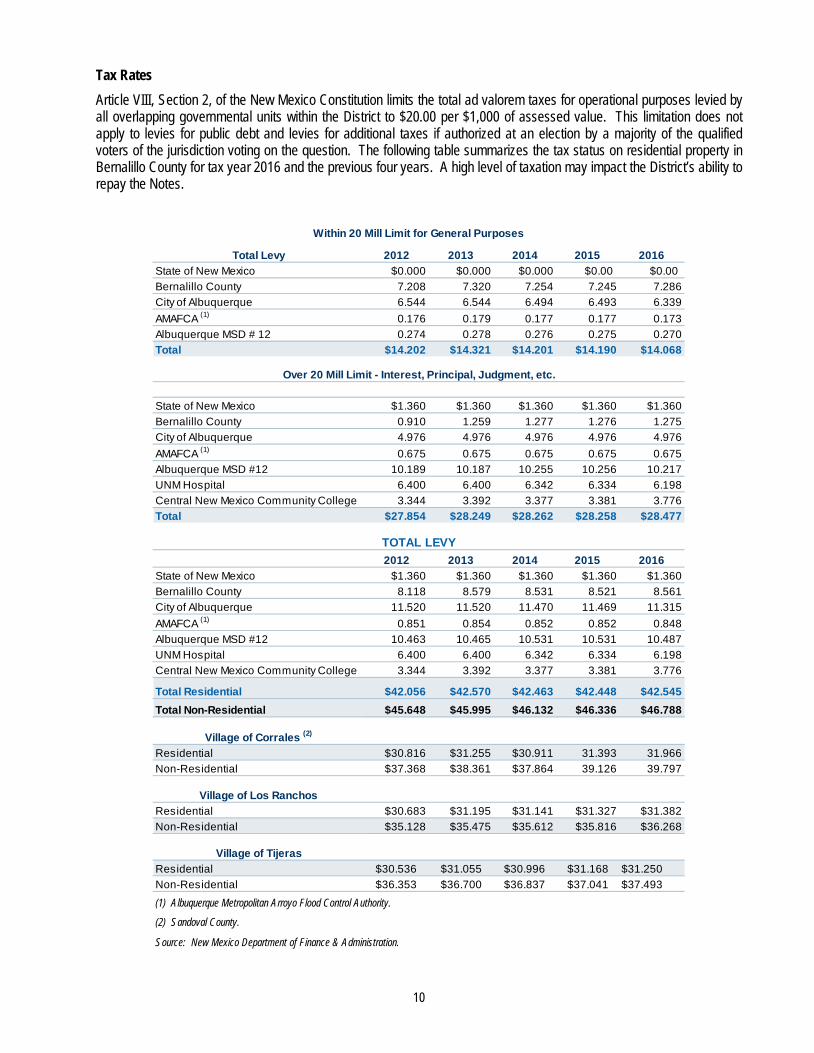

Tax Rates Article VIII, Section 2, of the New Mexico Constitution limits the total ad valorem taxes for operational purposes levied by all overlapping governmental units within the District to $20.00 per $1,000 of assessed value. This limitation does not apply to levies for public debt and levies for additional taxes if authorized at an election by a majority of the qualified voters of the jurisdiction voting on the question. The following table summarizes the tax status on residential property in Bernalillo County for tax year 2016 and the previous four years. A high level of taxation may impact the District’s ability to repay the Notes.

Total Levy 2012 2013 2014 2015 2016State of New Mexico $0.000 $0.000 $0.000 $0.00 $0.00Bernalillo County 7.208 7.320 7.254 7.245 7.286City of Albuquerque 6.544 6.544 6.494 6.493 6.339AMAFCA (1) 0.176 0.179 0.177 0.177 0.173Albuquerque MSD # 12 0.274 0.278 0.276 0.275 0.270Total $14.202 $14.321 $14.201 $14.190 $14.068

State of New Mexico $1.360 $1.360 $1.360 $1.360 $1.360Bernalillo County 0.910 1.259 1.277 1.276 1.275City of Albuquerque 4.976 4.976 4.976 4.976 4.976AMAFCA (1) 0.675 0.675 0.675 0.675 0.675Albuquerque MSD #12 10.189 10.187 10.255 10.256 10.217UNM Hospital 6.400 6.400 6.342 6.334 6.198Central New Mexico Community College 3.344 3.392 3.377 3.381 3.776Total $27.854 $28.249 $28.262 $28.258 $28.477

2012 2013 2014 2015 2016State of New Mexico $1.360 $1.360 $1.360 $1.360 $1.360Bernalillo County 8.118 8.579 8.531 8.521 8.561City of Albuquerque 11.520 11.520 11.470 11.469 11.315AMAFCA (1) 0.851 0.854 0.852 0.852 0.848Albuquerque MSD #12 10.463 10.465 10.531 10.531 10.487UNM Hospital 6.400 6.400 6.342 6.334 6.198Central New Mexico Community College 3.344 3.392 3.377 3.381 3.776

Total Residential $42.056 $42.570 $42.463 $42.448 $42.545Total Non-Residential $45.648 $45.995 $46.132 $46.336 $46.788

Village of Corrales (2)

Residential $30.816 $31.255 $30.911 31.393 31.966Non-Residential $37.368 $38.361 $37.864 39.126 39.797

Village of Los RanchosResidential $30.683 $31.195 $31.141 $31.327 $31.382Non-Residential $35.128 $35.475 $35.612 $35.816 $36.268

Village of TijerasResidential $30.536 $31.055 $30.996 $31.168 $31.250Non-Residential $36.353 $36.700 $36.837 $37.041 $37.493

(1) Albuquerque Metropolitan Arroyo Flood Control Authority.

(2) Sandoval County.

Source: New Mexico Department of Finance & Administration.

Within 20 Mill Limit for General Purposes

Over 20 Mill Limit - Interest, Principal, Judgment, etc.

TOTAL LEVY

11

Yield Control Limitation State law limits property tax increases from the prior property tax year. Specifically, no taxing entity may set a rate or impose a tax (excluding oil and gas production ad valorem and oil and gas production equipment ad valorem taxes) or assessment which will produce revenues which exceed the prior year's tax revenues from residential and non-residential property multiplied by a "growth control factor." The growth control factor is the percentage equal to the sum of (a) "percent change I" plus (b) the prior property tax year's total taxable property value plus "net new value", as defined by Statute, divided by such prior property tax year's total taxable property value, but if that percentage is less than 100%, then the growth control fact is (a) "percent change I" plus (b) 100%. "Percent change I" is based upon the annual implicit price deflator index for state and local government purchases of goods and services (as published in the United States Department of Commerce monthly publication entitled "Survey of Current Business," or any successor publication) and is a percent (not to exceed 5%) that is derived by dividing the increase in the prior calendar year (unless there was a decrease, in which case zero is used) by the index for such calendar year next preceding the prior calendar year. The growth control factor applies to authorized operating levies and to any capital improvements levies, but does not apply to levies for paying principal and interest on public general obligation debt, including the Notes.

Developments Limiting Residential Property Tax Increases In an effort to limit large annual increases in residential property taxes in some areas of the State (particularly the Santa Fe and Taos areas which have experienced large increases in residential property values in recent years), an amendment to the uniformity clause (Article VIII, Section 1) of the New Mexico Constitution was proposed during the 1997 Legislative Session. The amendment was submitted to voters of the State at the general election held on November 3, 1998 and was approved by a wide margin. The amendment directs the Legislature to provide for valuation of residential property in a manner that limits annual increases in valuation. The limitation may be applied to classes of residential property taxpayers based on occupancy, age or income. Further, the limitations may be authorized statewide or at the option of a local jurisdiction and may include conditions for applying the limitations. Bills implementing the constitutional amendment were enacted in 2001 and were codified as Sections 7-36-21.2 NMSA 1978 and 7-36-21.3 NMSA 1978. Section 7-36-21.2 NMSA 1978 establishes a statewide limitation on residential property valuation increases beginning in tax year 2001 (the “Statutory Valuation Cap on Residential Increases”). Annual valuation increases are limited to 3% over the prior year’s valuation or 6.1% over the valuation from two years prior. Subject to certain exceptions, these limitations do not apply:

1. To property that is being valued for the first time; 2. To physical improvements made to the property in the preceding year; 3. When the property is transferred to a person other than a spouse, or a child who occupies the property as his

principal residence and who qualifies for the head of household exemption on the property under the Property Tax Code;

4. When a change occurs in the zoning or use of the property; and 5. To property that is subject to the valuation limitations under Section 7-36-21.3 NMSA 1978.

On March 28, 2012, the New Mexico Court of Appeals upheld the constitutionality of a law capping residential valuation increases until a home changes ownership. The plaintiff appealed the case to the New Mexico Supreme Court which upheld the constitutionality of the law. The New Mexico Legislature has brought up the issue of the disparity in valuations in the past several years, but has not enacted any of the bills into law. To the extent that court or legislative action is taken or a further constitutional amendment is passed amending the valuation provisions, it could have a material impact on the valuation of residential property in the District.

12

Section 7-36-21.3 NMSA 1978 places a limitation on the increase in value for property taxation purposes for single-family dwellings occupied by low-income owners who are 65 years of age or older or who are disabled. The statute fixes the valuation of the property to the valuation in the year that the owner turned 65 or became disabled. The Section 7-36-21.3 limitation does not apply:

1. To property that is being valued for the first time; 2. To a change in valuation resulting from physical improvements made to the property in the preceding year; and 3. To a change in valuation resulting from a change in the zoning or permitted use of the property in the preceding

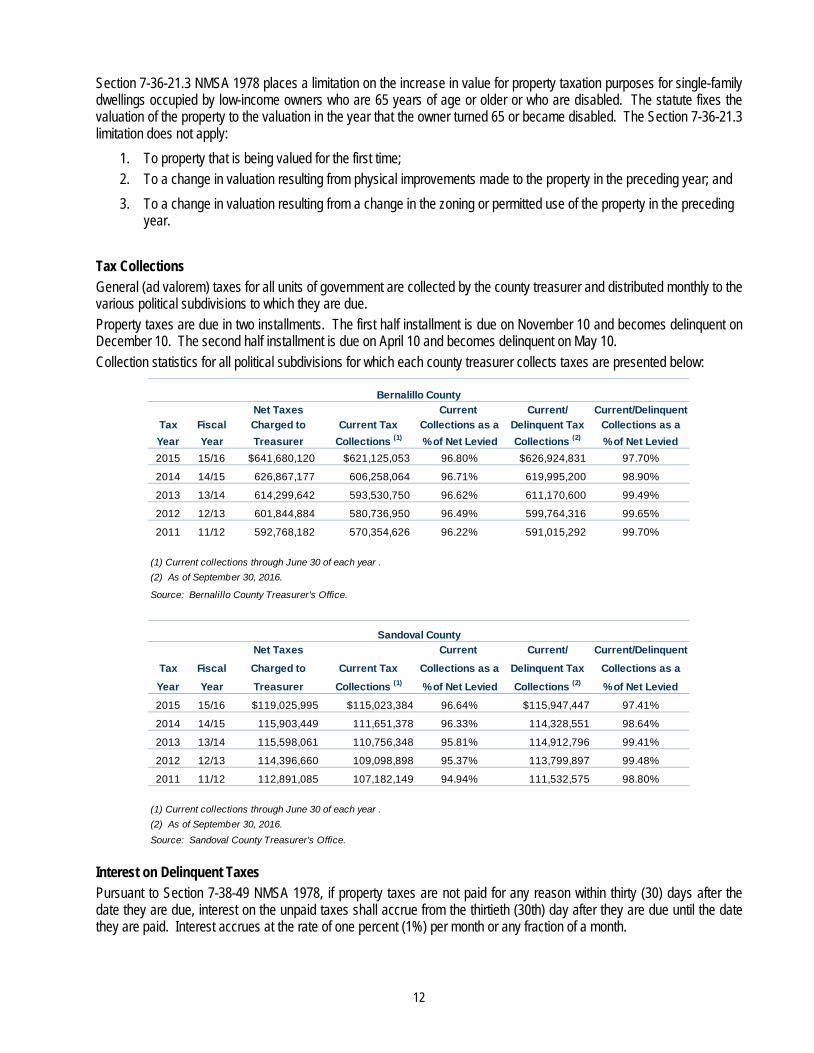

year. Tax Collections General (ad valorem) taxes for all units of government are collected by the county treasurer and distributed monthly to the various political subdivisions to which they are due. Property taxes are due in two installments. The first half installment is due on November 10 and becomes delinquent on December 10. The second half installment is due on April 10 and becomes delinquent on May 10. Collection statistics for all political subdivisions for which each county treasurer collects taxes are presented below:

Net Taxes Current Current/ Current/DelinquentTax Fiscal Charged to Current Tax Collections as a Delinquent Tax Collections as aYear Year Treasurer Collections (1) % of Net Levied Collections (2) % of Net Levied2015 15/16 $641,680,120 $621,125,053 96.80% $626,924,831 97.70%

2014 14/15 626,867,177 606,258,064 96.71% 619,995,200 98.90%

2013 13/14 614,299,642 593,530,750 96.62% 611,170,600 99.49%

2012 12/13 601,844,884 580,736,950 96.49% 599,764,316 99.65%

2011 11/12 592,768,182 570,354,626 96.22% 591,015,292 99.70%

(1) Current collections through June 30 of each year .

Source: Bernalillo County Treasurer's Office.

Net Taxes Current Current/ Current/Delinquent

Tax Fiscal Charged to Current Tax Collections as a Delinquent Tax Collections as a

Year Year Treasurer Collections (1) % of Net Levied Collections (2) % of Net Levied

2015 15/16 $119,025,995 $115,023,384 96.64% $115,947,447 97.41%

2014 14/15 115,903,449 111,651,378 96.33% 114,328,551 98.64%

2013 13/14 115,598,061 110,756,348 95.81% 114,912,796 99.41%

2012 12/13 114,396,660 109,098,898 95.37% 113,799,897 99.48%

2011 11/12 112,891,085 107,182,149 94.94% 111,532,575 98.80%

(1) Current collections through June 30 of each year .

Source: Sandoval County Treasurer's Office.

Bernalillo County

Sandoval County

(2) As of September 30, 2016.

(2) As of September 30, 2016.

Interest on Delinquent Taxes Pursuant to Section 7-38-49 NMSA 1978, if property taxes are not paid for any reason within thirty (30) days after the date they are due, interest on the unpaid taxes shall accrue from the thirtieth (30th) day after they are due until the date they are paid. Interest accrues at the rate of one percent (1%) per month or any fraction of a month.

13

Penalty for Delinquent Taxes Pursuant to Section 7-38-50 NMSA 1978, if property taxes become delinquent, a penalty of one percent (1%) of the delinquent tax for each month, or any portion of a month, they remain unpaid shall be imposed, but the total penalty shall not exceed five percent (5%) of the delinquent taxes. The minimum penalty imposed is $5.00. A county can suspend application of the minimum penalty requirement for any tax year. If property taxes become delinquent because of an intent to defraud by the property owner, fifty percent (50%) of the property tax due or fifty dollars ($50.00), whichever is greater, shall be added as a penalty.

Remedies Available for Non-Payment of Taxes Pursuant to Section 7-38-47 NMSA 1978, property taxes are the personal obligation of the person owning the property on the date on which the property was subject to valuation for property taxation purposes. A personal judgment may be rendered against the taxpayer for payment of taxes that are delinquent, together with any penalty and interest on the delinquent taxes. Taxes on real property are a lien against the real property. Pursuant to Section 7-38-65 NMSA 1978, delinquent taxes on real property may be collected by selling the real property on which taxes are delinquent. Pursuant to Section 7-38-53 NMSA 1978, delinquent property taxes on personal property may be collected by asserting a claim against the owner(s) of the personal property for which taxes are delinquent.

THE DISTRICT The District is a political subdivision of the State organized for the purpose of operating and maintaining an educational program for the school-age children residing within its boundaries. Currently the District operates and maintains a variety of facilities in meeting its obligation to provide an educational program within its boundaries that cover 1,230 square miles with an estimated population of 670,893. The Albuquerque Municipal School District No. 12 is the 34th largest school district in the country and the largest school district in the State with over 101,000 public school students in the area, including those who attend charter schools. The District operates 142 school sites - 89 elementary schools, 27 middle schools, two K through 8 schools, 13 high schools and 11 schools of choice. In addition, there are 22 District authorized charter schools and 32 State authorized charter schools for a total of 54 charter schools within the District. The District’s educational program also includes vocational, technical and occupational training. In addition, the District is responsible for the educational instruction of students in the following institutions: Bernalillo County Detention Center; Bernalillo County Juvenile Detention Center; Family School and Hogares Youth Home. The District employs 11,992 employees and is one of the largest employers in the Albuquerque MSA. School District Powers The District’s powers are subject to regulations adopted by the New Mexico Public Education Department (“PED”). Pursuant to an amendment to Article XII, Section 6 of the New Mexico Constitution, adopted at a special election held September 23, 2003, the Secretary of Education (the “Secretary”) is the governing authority and has control, management, and direction of all public schools pursuant to power provided by law. The Secretary further exercises supervision and authority over the PED. Generally, the powers of the Secretary and the PED include determining policy regarding operations of all public schools, designating courses of instruction, adopting regulations, determining qualifications for teachers, counselors and their assistants, and prescribing minimum educational standards. The Secretary may order the creation or consolidation of school districts.

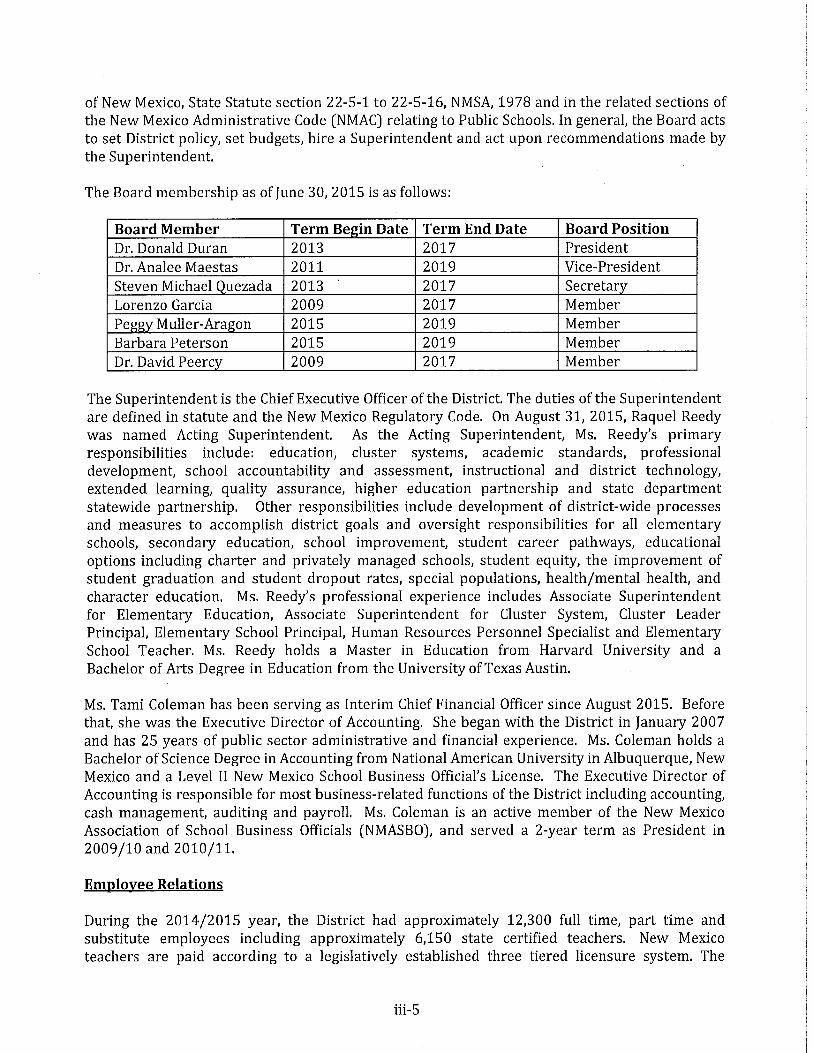

14

Management The District Board (the "Board"), subject to regulations of PED, develops educational policies for the District. The Board employs a superintendent of schools, delegates administrative and supervisory functions to the superintendent, fixes the superintendent’s salary, has the capacity to sue and be sued, contracts, leases, purchases and sells property for the District, acquires and disposes of all property, provides for the repair and maintenance of the District’s property, and adopts regulations pertaining to the administration of all powers or duties of the Board. Members serve without compensation for four-year terms of office and are elected in non-partisan elections held every two years on the first Tuesday in February. The current District Board Members are:

Dr. David Peercy, President Term expires March 1, 2017

Dr. Analee Maestas, Member Term expires March 1, 2019

Lorenzo Garcia, Vice President Term expires March 1, 2017

Peggy Muller-Aragón, Member Term expires March 1, 2019

Steven Michael Quezada, Secretary, Term expires March 1, 2017

Barbara Petersen, Member, Term expires March 1, 2019

Dr. Donald Duran, Member Term expires March 1, 2017

The Superintendent of Schools is selected by and serves at the discretion of the Board. All other staff members are selected by the Superintendent. The current Administrative Staff is: Raquel Reedy, Superintendent. The Superintendent is the Chief Executive Officer of the District. The duties of the Superintendent are defined in statute and the New Mexico Regulatory Code. On August 31, 2015, Raquel Reedy was named Acting Superintendent and on April 20, 2016, she was confirmed as the Superintendent. As the Superintendent, Ms. Reedy’s primary responsibilities include: academic standards, professional development, school accountability and assessment, instructional and District technology, extended learning, quality assurance, higher education partnership and state department statewide partnership. Other responsibilities include development of District-wide processes and measures to accomplish District goals and oversight responsibilities for all elementary schools, secondary education, school improvement, student career pathways, educational options including charter and privately managed schools, student equity, the improvement of student graduation and student dropout rates, special populations, health/mental health, and character education. Ms. Reedy’s professional experience includes Associate Superintendent for Elementary Education, Associate Superintendent for Cluster System, Cluster Leader Principal, Elementary School Principal, Human Resources Personnel Specialist and Elementary School Teacher. Ms. Reedy holds a Master in Education from Harvard University and a Bachelor of Arts Degree in Education from the University of Texas Austin. Scott Elder, Chief Operations Officer: Scott Elder was selected to serve as the Interim Chief Operations Officer for the Albuquerque Public Schools effective July 1, 2016. A 26-year APS veteran, Mr. Elder has been both a teacher and a principal. His experiences have been primarily in Title I schools, working with the most at-risk populations in the city. His schools have shown consistent growth and progress. Mr. Elder, utilizing School Improvement Grant funding and community resources, guided Highland High School to raise its graduation rate 17% in 4 years. He has run a highly rated alternative school and helped start APS’ Early College Academy. Mr. Elder holds Bachelor of Arts in Political Science and Spanish as well as a Master of Arts in Secondary Education. He is currently completing his Masters of Business Administration at the Anderson School at the University of New Mexico. Tami Coleman, Chief Financial Officer. In June 2016, Tami Coleman was named Chief Financial Officer after serving 10 months in the interim position. Ms. Coleman began with the District in January 2007 and has over 25 years of New Mexico public school administrative and financial experience. Ms. Coleman holds a Bachelor of Science Degree in Accounting from National American University in Albuquerque, New Mexico, and a Level II New Mexico School Business Official’s License. As the Chief Financial Officer, she is a member of the Superintendent’s Cabinet and Leadership teams. The Chief Financial Officer manages the finances of the District and oversees the business units which handle the financial activity of the school District. Ms. Coleman is an active member of the New Mexico Association of School Business Officials (NMASBO), and served a 2-year term as President in 2009/10 and 2010/11.

15

Insurance The District is registered with the State of New Mexico Insurance Commission (the “Commission”) as a self-insured entity for workers’ compensation, property and liability coverage. However, the District has purchased excess coverage policies that cover losses over $500,000, $250,000 and $350,000 for workers’ compensation, property and liability, respectively. In order to self-insure, the Commission requires that the District restrict its cash balance in an amount equal to the estimated workers’ compensation claim liability, excluding incurred but not reported claims. The District is self-insured for group health and offers other employee related benefits through several providers. The District is not responsible for charter school liability. Intergovernmental Agreements The District has entered into various joint powers agreements with other governmental entities in the State which permit all the governmental entities to jointly provide certain equipment purchases and other services cooperatively. School Property Currently, the District operates and maintains a variety of facilities in meeting its obligations to provide an educational program for the school-aged children residing within its boundaries. The District operates 142 school sites – 89 elementary schools, 27 middle schools, 13 high schools, 2 K-8 schools, and 11 schools of choice. The District owns vacant land held for future school sites. Student Enrollment The District’s student enrollment for the current and previous four years is detailed below. The District has experienced declines in enrollment over the last several years, but recently experienced a modest increase for the 2016-17 school year. Declines in enrollment are attributable to a variety of factors, including competition from District and State approved charter schools. There can be no assurances that the District will not continue to experience declines in enrollment.

2012-13 2013-14 2014-15 2015-16 2016-17*

Elementary School 46,441 45,587 45,509 43,232 43,738

Middle School 19,207 19,030 18,771 18,874 18,209 High School 23,954 23,938 24,049 22,579 23,958

Total 89,602 88,555 88,329 84,685 85,905 APS & State Authorized Charter Schools 12,527 12,726 15,456 16,845 N/A

Total Student in the APS Area 102,129 101,281 103,785 101,530 85,905

* Charter Enrollments for 2016-17 are not yet available.Source: Albuquerque Municipal School District No. 12.

16

FINANCES OF THE EDUCATIONAL PROGRAM

The basic format for the financial operation of the District is provided by the PED through the School Budget Planning Division which is directed by State law to supervise and control the preparation of all budgets of all school districts. The District receives revenue from a variety of local, State, and federal sources, the most important of which are described below. New Mexico's public school finance laws are subject to review and examination through the judicial process, and are subject to legislative changes as well. As a result, the District cannot anticipate with certainty all of the factors which may influence the financing of its future activities. There is no assurance that there will not be any change in, interpretation of, or addition to the applicable laws, provisions, and regulations which would have a material effect, directly or indirectly, on the affairs of the District. District Budget Process Each year, the school district budget process begins with the educational appropriations passed by the Legislature and signed into law by the Governor. The actual budget process follows specific steps set by the PED. • Pursuant to instruction by the PED, the District must submit an operating budget for the next school year to the PED.

If the District fails to submit a budget, the PED must prepare a District budget for the ensuing year. Upon written approval of the state superintendent [secretary], the date for the submission of the operating budget may be extended to a later date fixed by the state superintendent (Section 22-8-6).

• Before May 31 of each year, the District Board must hold a public hearing to fix the estimated budget for the next school year.

• Before June 20 of each year, the District must submit a balanced budget to the PED. • On or before July 1 of each year, the PED must approve and certify an approved operating budget for use by the

District Board. No school board, officer or employee of a school district may make an expenditure or incur any obligation for the expenditure of public funds unless that expenditure is made in accordance with an operating budget approved by the PED. This requirement, however, does not prohibit the transfer of funds between line items within a series of a budget. Final budgets may not be altered or amended after approval by the PED except upon the District’s request to the PED. An instance in which such requests will be approved include a change within the budget that does not increase the total amount of the budget. Additional budget items may also be approved if the District is to receive unanticipated revenues. Finally, if it becomes necessary to increase the District's budget by more than $1,000 for any reason other than those listed above, the PED may order a special public hearing to consider the requested increase. Formal budgetary integration is employed as a management control device during the year for the General Fund, Special Revenue Funds, and Debt Service Fund with appropriations lapsing at year end. Total expenditures of any function category may not exceed categorical appropriations. To conform with PED's requirements, budgets for all funds of the District are adopted on the cash basis of accounting except for state instructional material credit. State instructional material funds provide for free textbooks from the PED. As a result, budgets are not prepared in conformity with generally accepted accounting principles (GAAP), and budgetary comparisons are presented on the cash basis of accounting. Sources of Revenue for General Fund The General Fund is the primary operating fund of the District and accounts for all financial resources, except those required to be accounted for in other funds. The sources of revenue for the District's General Fund are: Local Revenues - Local revenues are a minor source of revenue to the District composed, in part, by a property tax annually levied on and against all of the taxable property within the District for operational purposes. The levy is limited by State law to a rate of 50 cents for each $1,000 of net taxable value of taxable property. Other sources of local revenues include interest income earned on the District's investments, rentals and sale of property. In fiscal year 2015, the District received $5,018,707 from local sources. Federal Revenues - Another minor source of annual revenue for the District's General Fund is derived from federal grant funds related to vocational, special education, and various other programs and P.L. 874 federal impact moneys paid to

17

the District in lieu of taxes on federal land located in the District. In fiscal year 2015, the District received $2,023,945 in federal revenues for its General Fund. State Revenues - The District's largest source of annual revenue is derived from the SEG payments described below. During fiscal year 2015, the District received $635,987,410 from state sources. Such payments represented approximately 98% of actual fiscal year 2015 General Fund revenues. State Equalization Guarantee The State Legislature enacted New Mexico’s current public school funding formula in 1974. Designed to distribute operational funds to local school districts in an objective manner, the funding formula is based upon the educational needs of individual students and costs of the programs designed to meet those needs. Program cost differentials are based upon nationwide data regarding the relative costs of various school programs, as well as data specific to New Mexico. The objectives of the formula are (1) to equalize educational opportunity statewide (by crediting certain local and federal support and then distributing state support in an objective manner) and (2) to retain local autonomy in actual use of funds by allowing funds to be used in local districts at the discretion of local policy making bodies. The formula is divided into three basic parts: 1. Educational program units that reflect the different costs of identified programs; 2. Training and experience units that attempt to provide additional funds so that districts may hire and retain better

educated and more experienced instructional staff; and 3. Size adjustment units that recognize local school and community needs, economies of scale, types of students,

marginal costs increases for growth in enrollment from one year to the next, and adjustments for the creation of new districts.

SEG payments are made monthly and prior to June 30 each fiscal year. The calculation of the distribution is also based on the local and federal revenues received from June 1 of the previous fiscal year through May 31 of the fiscal year for which the SEG payment is being computed. In the event that a district receives more SEG funds than its entitlement, the district must make a refund to the State’s general fund. Even though the current public school funding formula has been in place for more than three decades, some districts have indicated a concern about the fact that some districts receive less revenue per pupil compared to others. In response to these concerns, the Legislature, the Governor, and the State Board of Education authorized an independent, comprehensive study of the formula, that was conducted in 1996. In its principal finding the independent consultant concluded,“. . .When evaluated on the basis of generally accepted standards of equity, the New Mexico public school funding formula is a highly equitable formula. . . .[S]pending disparities are less than in other states and statistically insignificant.” Despite the acknowledged equity of the formula, the independent consultant pointed out a strong perception of unfairness in the so-called “density” factor and in the training and experience computations of some districts. As a result, the Legislature enacted the following changes to the funding formula: • Required that special education students be counted with regular students with “add-on” weights assigned depending

upon the severity of the disability; • Changed weights for special education ancillary services and included diagnosticians in ancillary services

computations; and • Repealed the so-called “density” factor and replaced it with an at-risk factor that is available to all school districts.

18

State Equalization Guarantee payments to the District for the current and previous four fiscal years are as follows: School Program Number of

Year Unit Value Program Units Amount2016 - 2017 $4,040.24 156,824.18 $629,702,140

2015 - 2016 4,027.75 156,956.25 632,180,552

2014 - 2015 4,005.75 159,344.16 612,562,319

2013 - 2014 3,817.55 161,840.66 614,087,079

2012 - 2013 3,673.54 161,693.72 590,190,332

Source: Albuquerque Municipal School District No. 12. PED receives Federal mineral-leasing funds from which it makes annual allocations to the District for purchasing instructional materials. In fiscal year 2015, the District received $6,116,138 for textbook purchases. The District is also reimbursed by the State for the costs of transporting pupils to and from school. These payments are based upon a formula consisting of the number of students per square mile that are transported. In fiscal year 2015, the District received $22,789,277 for transportation purposes.

19

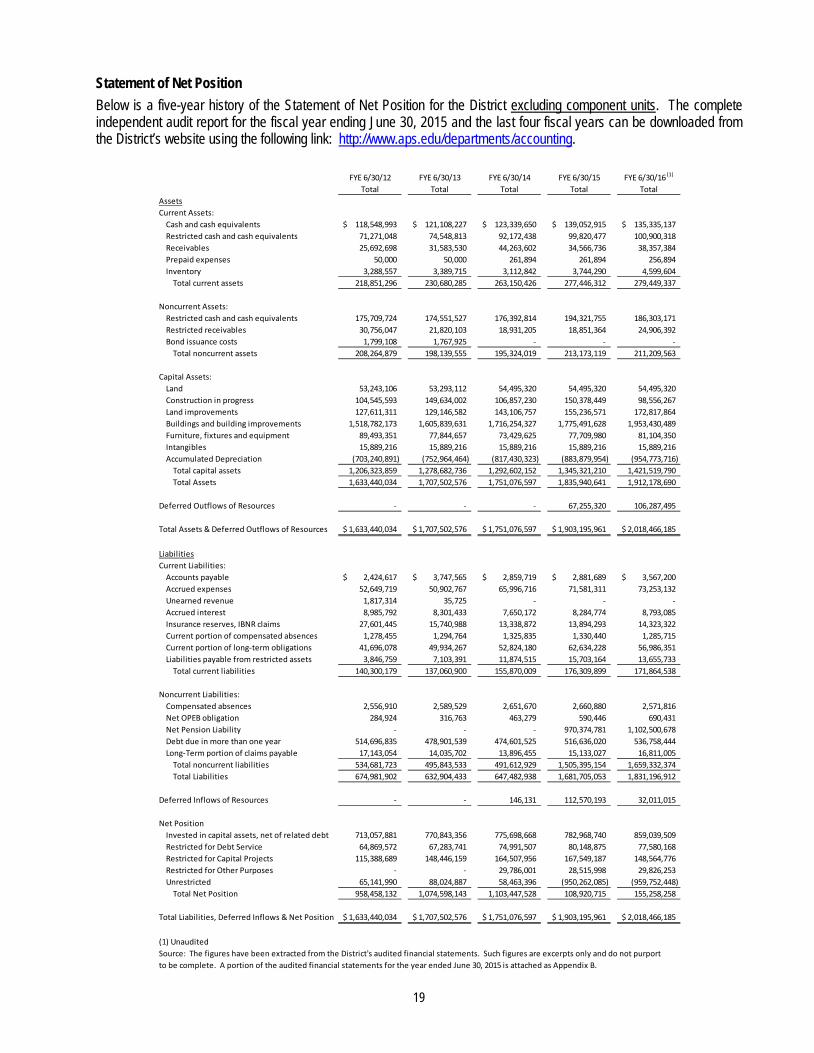

Statement of Net Position Below is a five-year history of the Statement of Net Position for the District excluding component units. The complete independent audit report for the fiscal year ending June 30, 2015 and the last four fiscal years can be downloaded from the District’s website using the following link: http://www.aps.edu/departments/accounting.

FYE 6/30/12 FYE 6/30/13 FYE 6/30/14 FYE 6/30/15 FYE 6/30/16 (1)

Total Total Total Total TotalAssetsCurrent Assets:

Cash and cash equivalents 118,548,993$ 121,108,227$ 123,339,650$ 139,052,915$ 135,335,137$ Restricted cash and cash equivalents 71,271,048 74,548,813 92,172,438 99,820,477 100,900,318 Receivables 25,692,698 31,583,530 44,263,602 34,566,736 38,357,384 Prepaid expenses 50,000 50,000 261,894 261,894 256,894 Inventory 3,288,557 3,389,715 3,112,842 3,744,290 4,599,604

Total current assets 218,851,296 230,680,285 263,150,426 277,446,312 279,449,337

Noncurrent Assets:Restricted cash and cash equivalents 175,709,724 174,551,527 176,392,814 194,321,755 186,303,171 Restricted receivables 30,756,047 21,820,103 18,931,205 18,851,364 24,906,392 Bond issuance costs 1,799,108 1,767,925 - - -

Total noncurrent assets 208,264,879 198,139,555 195,324,019 213,173,119 211,209,563