1 PowerPoint PowerPoint Presentation by Presentation by Gail B. Wright Gail B. Wright Professor Emeritus of Professor Emeritus of Accounting Accounting Bryant University Bryant University © Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star Logo, and South-Western are trademarks used herein under license. MANAGEMENT ACCOUNTING 8 th EDITION BY HANSEN & MOWEN 15 QUALITY COSTS AND PRODUCTIVITY STUDENT EDITION

Akuntansi Manajemen Edisi 8 oleh Hansen & Mowen Bab 15

May 29, 2015

Akuntansi Manajemen Edisi 8 oleh Hansen & Mowen Bab 15 Quality Costs And Productivity

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

PowerPointPowerPoint Presentation by Presentation by

Gail B. WrightGail B. WrightProfessor Emeritus of AccountingProfessor Emeritus of AccountingBryant UniversityBryant University

© Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star Logo, and

South-Western are trademarks used herein under license.

MANAGEMENT ACCOUNTING

8th EDITION

BY

HANSEN & MOWEN

15 QUALITY COSTS AND PRODUCTIVITY

STUDENT EDITION

2

1. Identify & describe the 4 types of quality costs.

2. Prepare a quality cost report; differentiate between acceptable quality level & total quality control.

3. Tell why quality cost information is needed & show how it is used.

4. Explain what productivity is; calculate the impact of productivity changes on profits.

LEARNING OBJECTIVESLEARNING OBJECTIVES

3

WEIGHING COSTS & BENEFITS

Managers need to know what quality costs are & how they change over timeCosts of quality

Studies suggest that cost of quality production might be as much as 20% – 30% of sales

Benefits of qualityCompetitive dimension

LO 1

4

DIMENSIONS OF QUALITY: 1

Performance: how consistently a product functions

Aesthetics : appearance of tangible products, facilities, communication materials

Serviceability: ease of maintaining, repairing product

Features of quality design: characteristics that differentiate between similar products

LO 1

Continued

Aesthetics

5

DIMENSIONS OF QUALITY: 2

Reliability: probability that product, service will perform intended function for specified length of time

Durability: length of time a product functionsQuality of conformance : measure of how a

product meets its specificationsFitness for use: suitability of product for

advertised functions

LO 1

Quality of conformance

6

DEFECTIVE PRODUCT: Definition

DEFECTIVE PRODUCT: Definition

Is one that does not conform to specifications. Zero defects is

the goal.

LO 1

7

What are costs of quality?

Costs of quality exist because poor quality does or may exist:

• Control activities to prevent, detect poor quality.

• Failure activities are responses to poor quality.

LO 1

Failure activities

8

CATEGORIES OF QUALITY COSTS

1. Prevention costs: incurred to prevent poor quality

2. Appraisal costs : incurred to determine whether products, services conform to requirements, customer needs

3. Internal failure costs: incurred when non-conformance is discovered & product, service re-worked, scrapped, etc.

4. External failure costs: incurred when products fail to conform after delivery and recalled

LO 1

Appraisal costs

9

CLASSIFYING QUALITY COSTS

ObservableCosts available in accounting records

HiddenSignificantNot directly available in accounting recordsEstimated

Multiplier methodMarket researchTaguchi quality loss function

LO 1

10

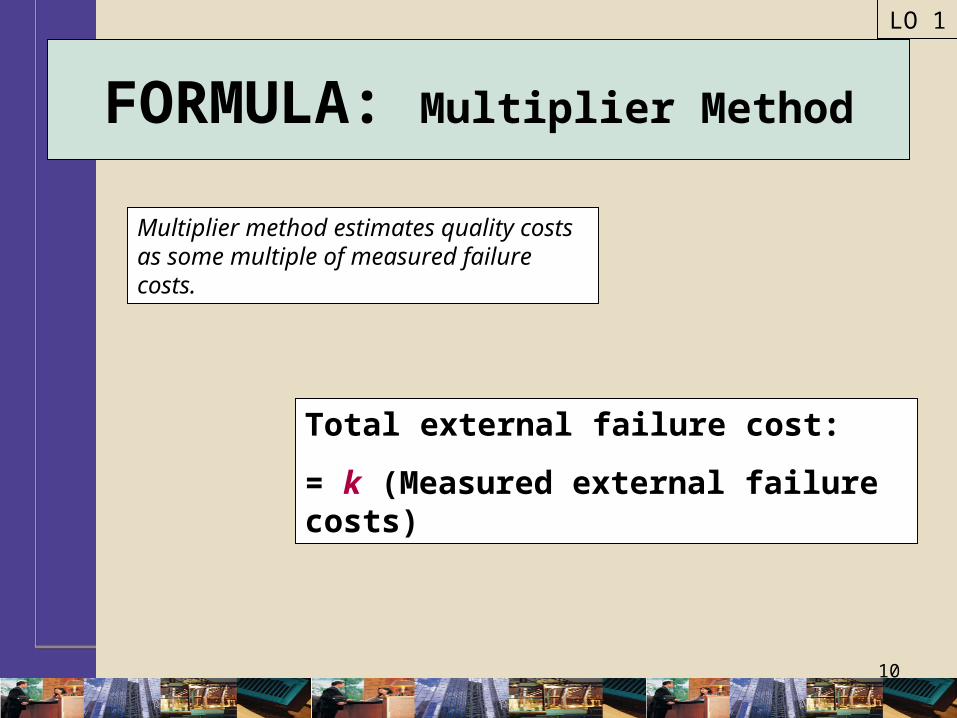

FORMULA: Multiplier Method

Multiplier method estimates quality costs as some multiple of measured failure costs.

LO 1

Total external failure cost:

= k (Measured external failure costs)

11

How does market research estimate hidden quality

costs?

Market research uses customer surveys & interviews of sales staff to project future profit

losses.

LO 1

12

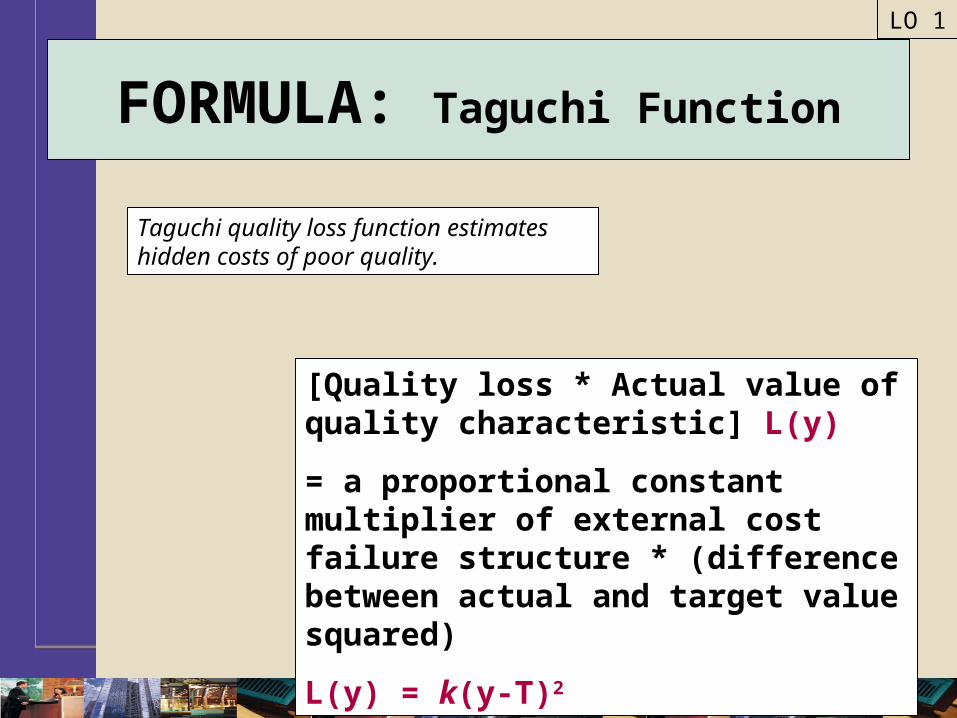

What assumption does the Taguchi quality loss

function make?

Taguchi quality loss function assumes that variations from

target value of quality characteristic causes hidden quality costs regardless of

specification limits.

LO 1

13

FORMULA: Taguchi Function

Taguchi quality loss function estimates hidden costs of poor quality.

LO 1

[Quality loss * Actual value of quality characteristic] L(y)

= a proportional constant multiplier of external cost failure structure * (difference between actual and target value squared)

L(y) = k(y-T)2

14

ACCEPTABLE QUALITY LEVEL (AQL): Definition

ACCEPTABLE QUALITY LEVEL (AQL): Definition

Is the optimal balance between control costs &

failure costs.

LO 2

15

Is there a problem with the ACL (traditional) view of

quality?

AQL encouraged lower quality levels by accepting production of a given number of defective

units.

LO 2

16

ZERO DEFECTS MODEL: Definition

ZERO DEFECTS MODEL: Definition

Claims that it is cost beneficial to reduce non-conforming units to zero.

LO 2

17

Is there a problem with the zero defects model?

Zero defects model understates quality costs & the potential for savings from efforts to improve

quality.

LO 2

understates

18

REDUCING QUALITY COSTS

Take direct attack on failure costs to drive them to zero

Invest in “right” prevention activities to bring about improvement

Reduce appraisal costs according to results achieved

Continuously evaluate, redirect prevention efforts to gain further improvement

LO 2

19

What is the strategy for reducing costs based on?

The strategy is based on the premise that a) there is a root cause for each failure, b) causes are preventable,

and c) prevention is always cheaper.

LO 2

20

ABM & OPTIMAL QUALITY COSTS

ABM classifies costs as value-added & non-value-added and recommends non-value-added costs be eliminated.

Value-added quality costs Prevention activities, when performed

efficiently

Non-value-added quality costs Appraisal costs Failure costs (both internal & external)

LO 2

21

TQC COMPONENT GRAPH

LO 2

EXHIBITEXHIBIT 15-815-8

Over time, quality costs shift from non-value-added to value-added (prevention) costs.

22

What are principal objectives of reporting

quality costs?

Principal objectives are to improve & facilitate a)

managerial planning, b) control, and c) decision making.

LO 3

23

TOTAL PRODUCTIVE EFFICIENCY

When concerned with productive efficiency, 2 conditions must be satisfied:

Technical efficiency: For any mix of inputs that will produce a given output, no more of any 1 input is used than necessary to produce the output

Input trade-off efficiency: Given the mixes that satisfy the first condition, the least costly mix is chosen.

LO 4

24

PARTIAL MEASURES: AnalysisPARTIAL MEASURES: Analysis

LO 4

Conclusions that can be drawn about partial measures:

Existence of trade-offs mandates total measure of productivity for assessing merits of productivity decisions

Because of possibility of trade-offs, financial productivity must be measured

Conclusions that can be drawn about partial measures:

Existence of trade-offs mandates total measure of productivity for assessing merits of productivity decisions

Because of possibility of trade-offs, financial productivity must be measured

25

TOTAL PRODUCTIVITY MEASUREMENT: Definition

TOTAL PRODUCTIVITY MEASUREMENT: Definition

Is measuring productivity for all inputs simultaneously.

LO 4

26

PROFIT-LINKED PRODUCTIVITY MEASUREMENT: Definition

PROFIT-LINKED PRODUCTIVITY MEASUREMENT: Definition

Is measuring the amount of profit change attributable to

productivity change.

LO 4

27

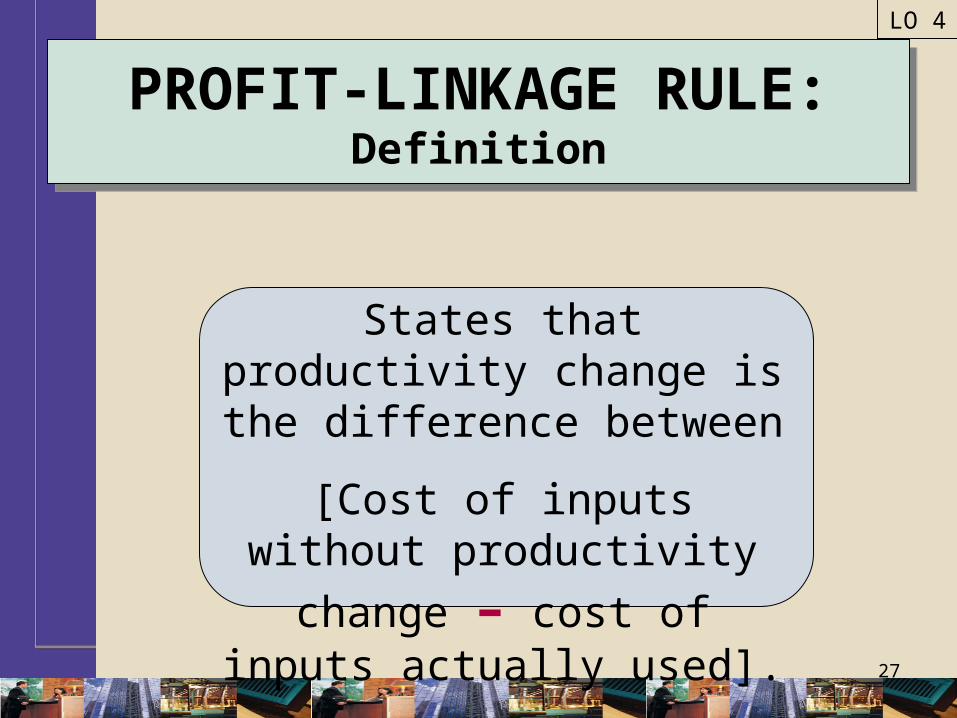

PROFIT-LINKAGE RULE: Definition

PROFIT-LINKAGE RULE: Definition

States that productivity change is the difference between

[Cost of inputs without

productivity change – cost of inputs actually used].

LO 4

28

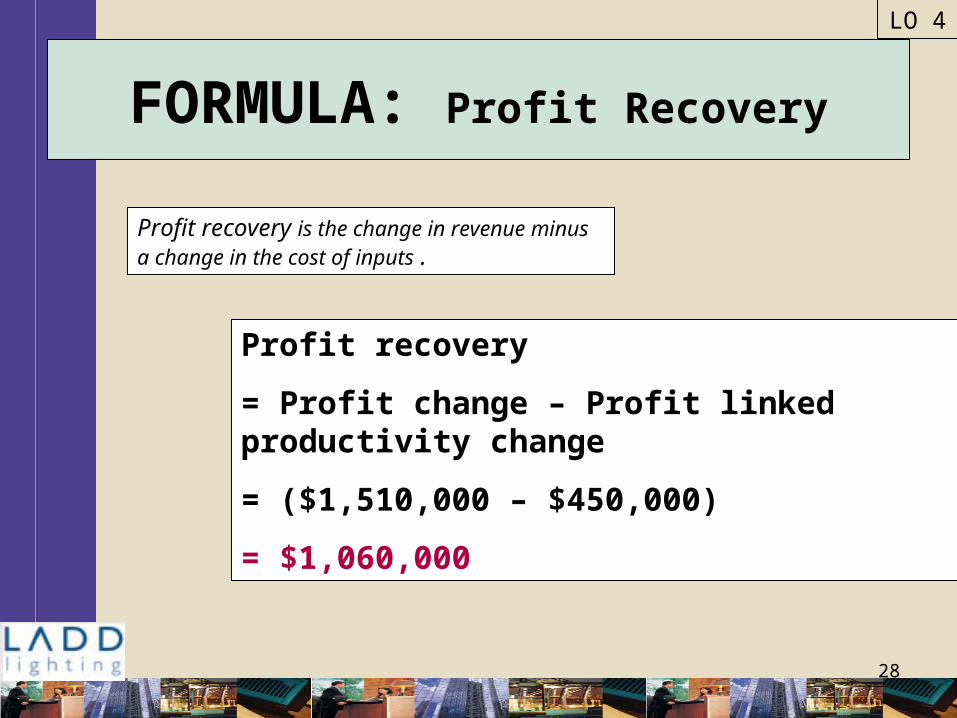

FORMULA: Profit Recovery

Profit recovery is the change in revenue minus a change in the cost of inputs .

LO 4

Profit recovery

= Profit change – Profit linked productivity change

= ($1,510,000 – $450,000)

= $1,060,000

29

THE ENDTHE END

CHAPTER 15

Related Documents