AKUNTANSI KEPERILAKUAN (BEHAVIORAL ACCOUNTING) Supriyadi Jurusan Akuntansi Fakultas Ekonomika dan Bisnis UNIVERSITAS GADJAH MADA

AKUNTANSI KEPERILAKUAN ( BEHAVIORAL ACCOUNTING )

Feb 08, 2016

AKUNTANSI KEPERILAKUAN ( BEHAVIORAL ACCOUNTING ). Supriyadi Jurusan Akuntansi Fakultas Ekonomika dan Bisnis UNIVERSITAS GADJAH MADA. a dalah suatu sistem yang berfungsi. Informasi keuangan yang. Apakah Akuntansi ?. Akuntansi. mengidentifikasi. mencatat. relevan. mengkomunikasikan. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AKUNTANSI KEPERILAKUAN(BEHAVIORAL ACCOUNTING)

SupriyadiJurusan Akuntansi

Fakultas Ekonomika dan BisnisUNIVERSITAS GADJAH MADA

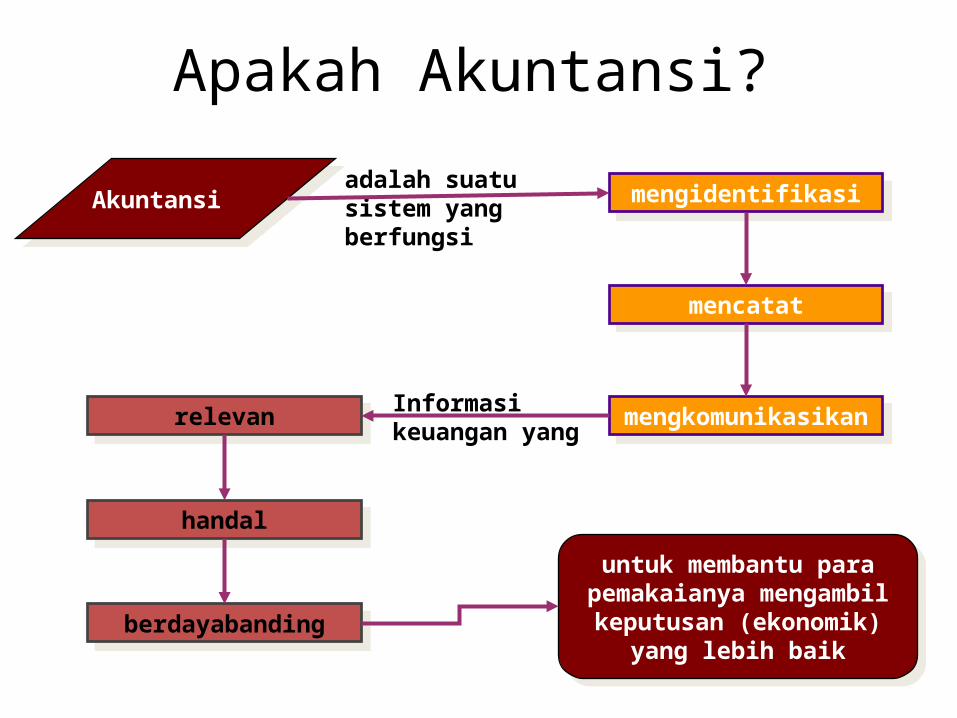

mengidentifikasi

mencatat

mengkomunikasikanrelevan

handal

berdayabanding

Apakah Akuntansi?

Akuntansiadalah suatu sistem yang berfungsi

Informasi keuangan yang

untuk membantu para pemakaianya mengambil

keputusan (ekonomik) yang lebih baik

Managemen

Bag. SDM

Kantor Pajak

SPI

Bapepam

Bag. Pemasaran

Bag. Keuangan

Investor

Kreditur

Siapa Pemakai Informasi Akuntansi?

Pelanggan

Pemakai Internal

Pemakai Eksternal

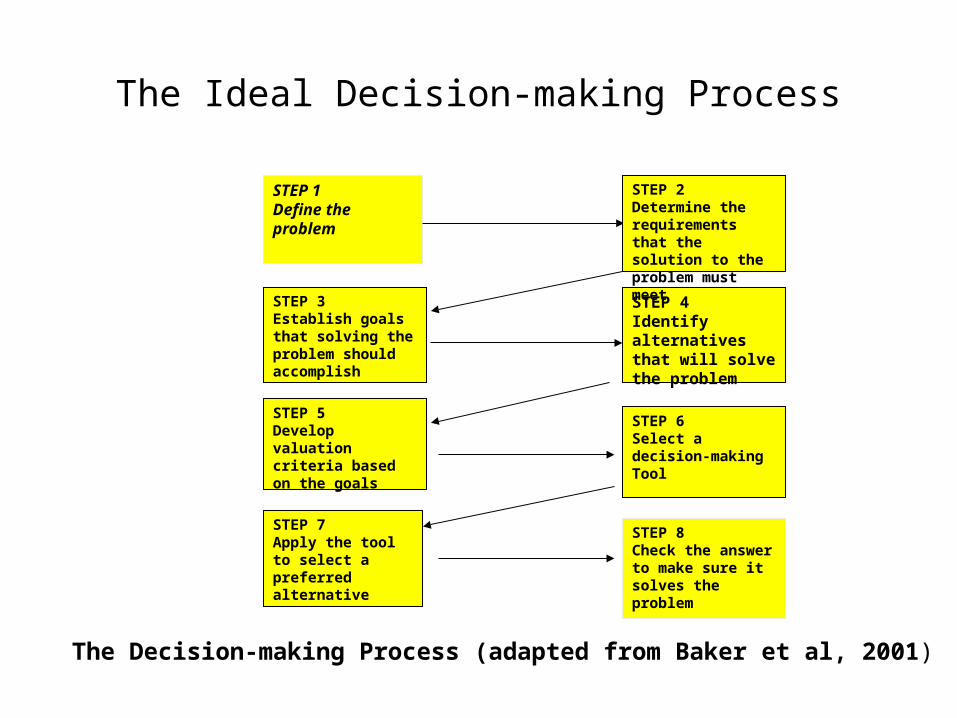

The Ideal Decision-making Process

STEP 1Define the problem

STEP 3Establish goals that solving the problem should accomplish

STEP 4Identify alternatives that will solve the problem

STEP 5Develop valuation criteria based on the goals

STEP 6Select a decision-making Tool

STEP 7Apply the tool to select apreferred alternative

STEP 8Check the answerto make sure itsolves the problem

The Decision-making Process (adapted from Baker et al, 2001)

STEP 2Determine the requirements that the solution to the problem must meet

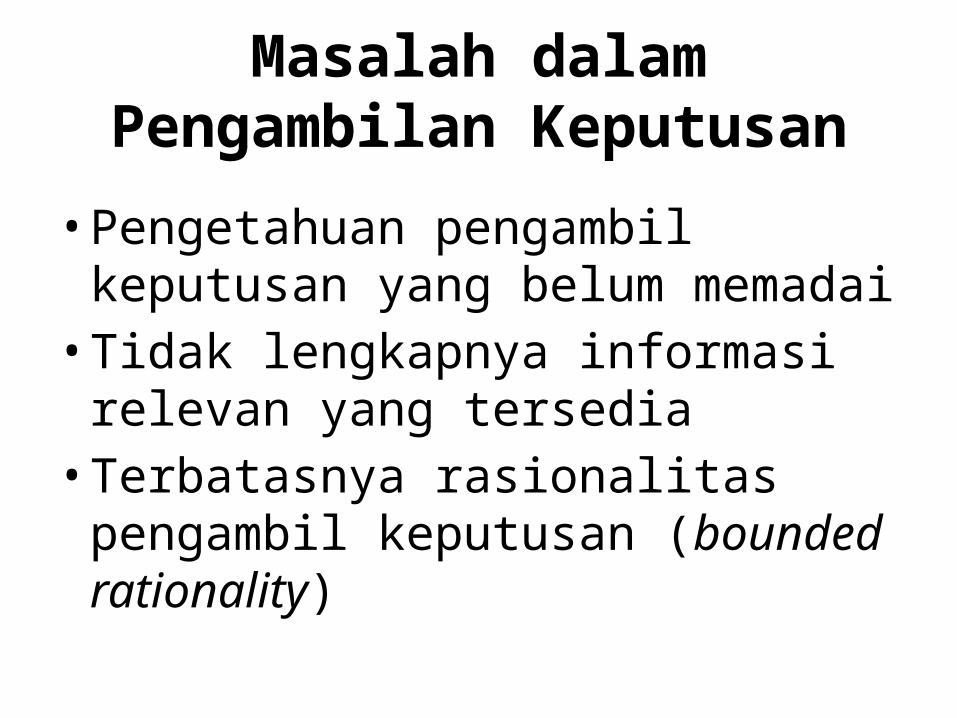

Masalah dalam Pengambilan Keputusan

• Pengetahuan pengambil keputusan yang belum memadai• Tidak lengkapnya informasi relevan

yang tersedia• Terbatasnya rasionalitas pengambil

keputusan (bounded rationality)

Apakah Kita Rasional?

• Bounded rationality: suatu kondisi bahwa dalam pengambilan keputusan, individu mempunyai keterbatasan informasi, kemampuan kognitif, dan waktu.

• Cognitive Bias: pola penyimpangan dalam pengambilan keputusan pada situasi tertentu karena distorsi persepsi, ketidakakuratan prediksi, interpretasi yang tidak logis, atau tidak rasional.

Heuristics

Bounded rationality Cognitive Bias Heuristics

Heuristics: individu menggunakan strategi (taktik) sederhana atau rules of thumb dalam pembuatan keputusan (Tversky

dan Kahneman, 1973)

Heuristics

• The Availability HeuristicsContoh: Manakah yang menyebabkan kematian

lebih banyak di AS: (a) Kanker perut, atau (b) Kecelakaan kendaraan

• The Representativeness HeuristicsContoh: Kasus kelahiran bayi di rumah sakit besar

dan kecil

• Anchoring and AdjustmentContoh: Kasus referent point

Akuntansi Keperilakuan

• Studi terkait dengan perilaku individu

• Studi perilaku individu dalam konteks akuntansi.

• Studi tentang perilaku individual akuntan atau non-akuntan karena pengaruh informasi dan atau fungsi akuntansi.

9

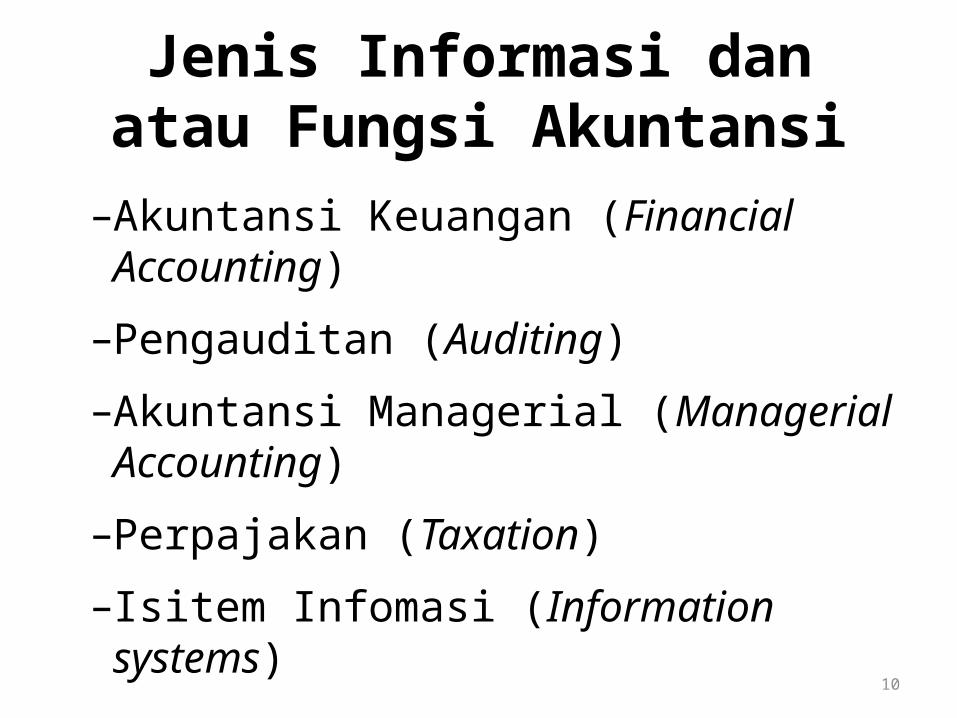

Jenis Informasi dan atau Fungsi Akuntansi

–Akuntansi Keuangan (Financial Accounting)

–Pengauditan (Auditing)

–Akuntansi Managerial (Managerial Accounting)

–Perpajakan (Taxation)

–Isitem Infomasi (Information systems)10

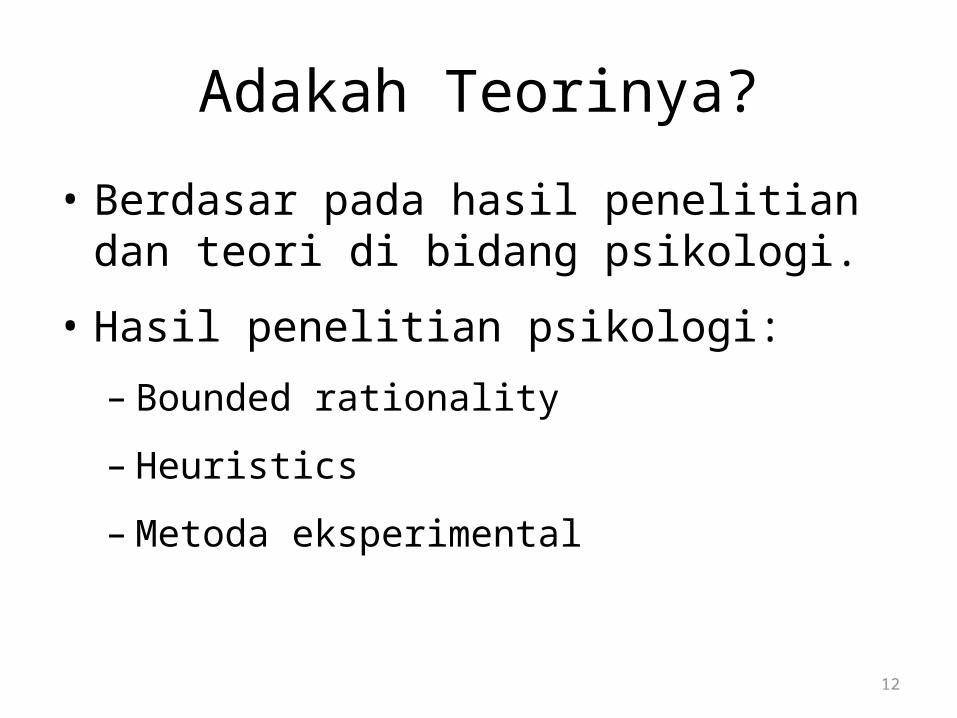

Adakah Teorinya?

• Berdasar pada hasil penelitian dan teori di bidang psikologi.

• Hasil penelitian psikologi:– Bounded rationality

– Heuristics

– Metoda eksperimental

12

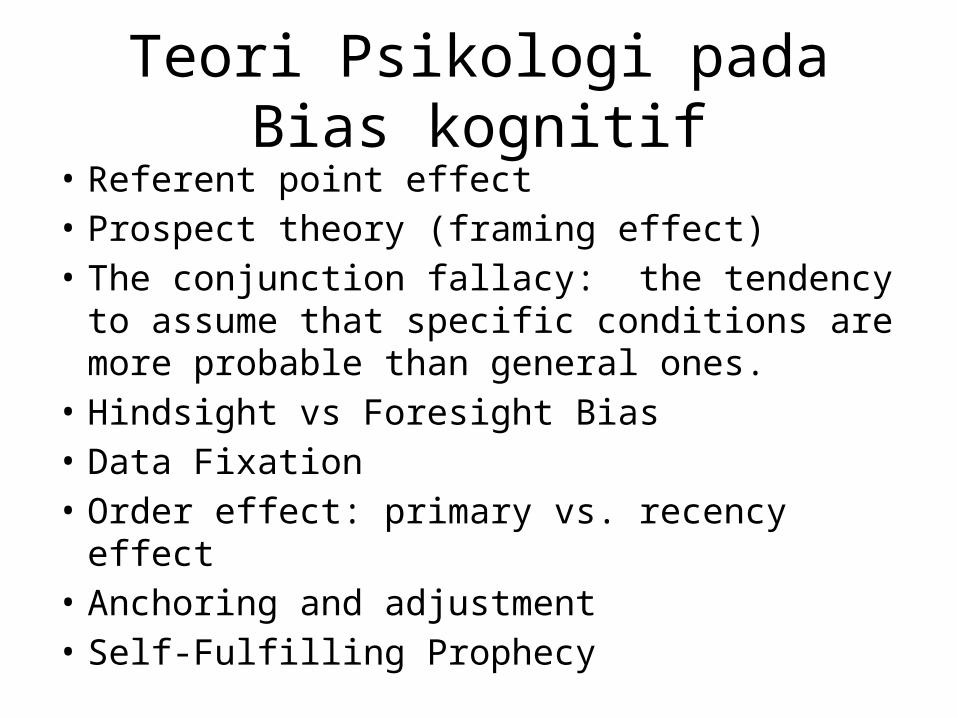

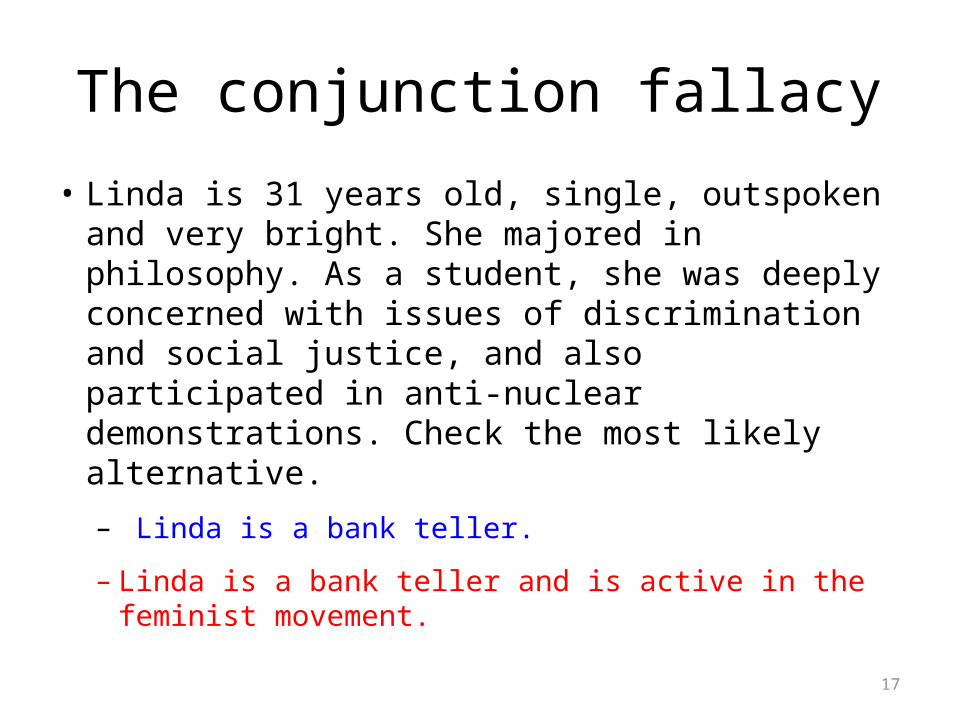

Teori Psikologi pada Bias kognitif• Referent point effect• Prospect theory (framing effect)• The conjunction fallacy: the tendency to

assume that specific conditions are more probable than general ones.

• Hindsight vs Foresight Bias• Data Fixation• Order effect: primary vs. recency effect• Anchoring and adjustment• Self-Fulfilling Prophecy

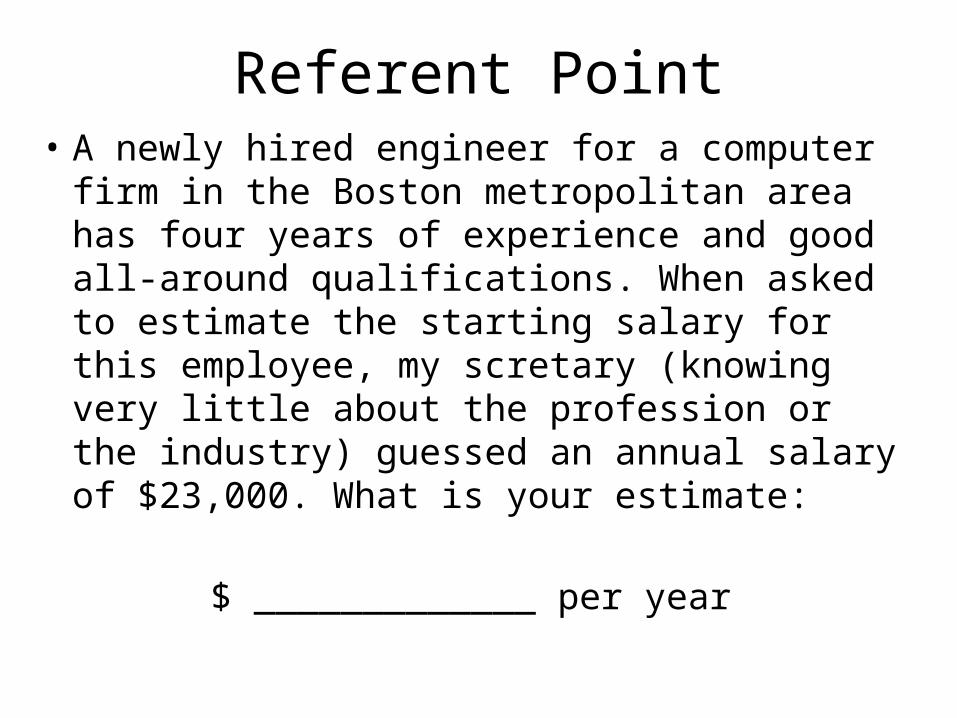

Referent Point• A newly hired engineer for a computer firm in

the Boston metropolitan area has four years of experience and good all-around qualifications. When asked to estimate the starting salary for this employee, my scretary (knowing very little about the profession or the industry) guessed an annual salary of $23,000. What is your estimate:

$ _____________ per year

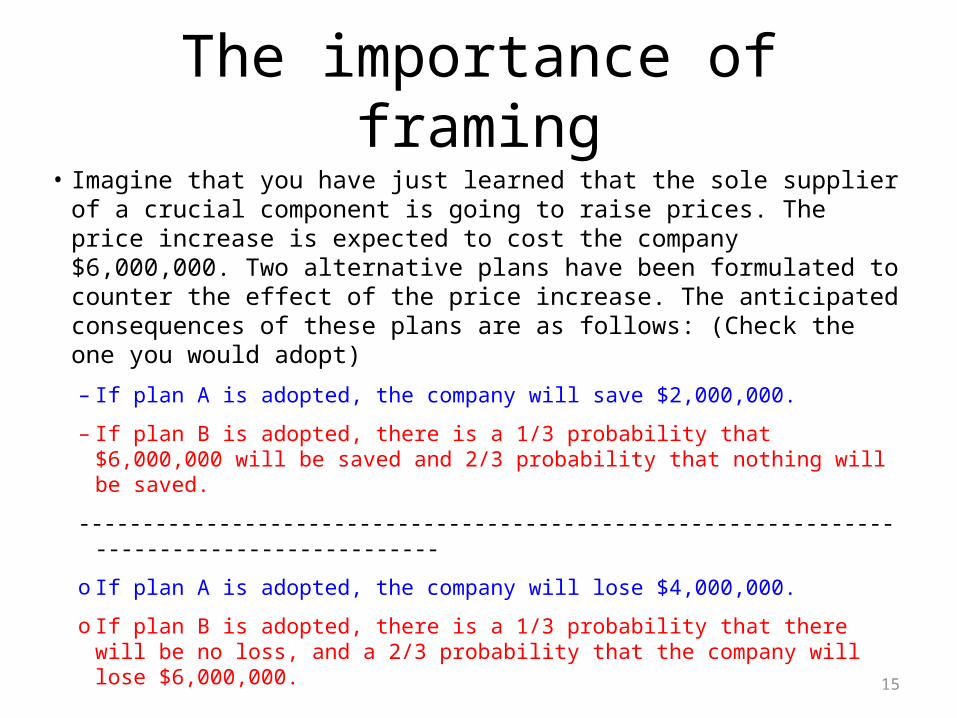

The importance of framing• Imagine that you have just learned that the sole supplier of a

crucial component is going to raise prices. The price increase is expected to cost the company $6,000,000. Two alternative plans have been formulated to counter the effect of the price increase. The anticipated consequences of these plans are as follows: (Check the one you would adopt)– If plan A is adopted, the company will save $2,000,000.

– If plan B is adopted, there is a 1/3 probability that $6,000,000 will be saved and 2/3 probability that nothing will be saved.

-------------------------------------------------------------------------------------------

o If plan A is adopted, the company will lose $4,000,000.

o If plan B is adopted, there is a 1/3 probability that there will be no loss, and a 2/3 probability that the company will lose $6,000,000.

15

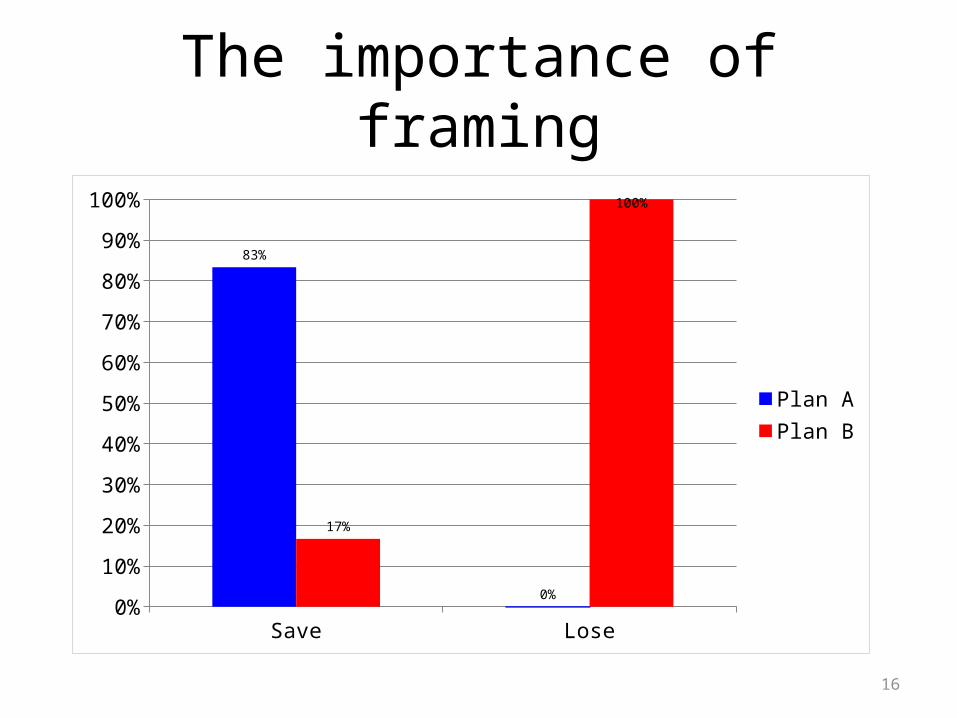

The importance of framing

16

Save Lose0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

83%

0%

17%

100%

Plan APlan B

The conjunction fallacy

• Linda is 31 years old, single, outspoken and very bright. She majored in philosophy. As a student, she was deeply concerned with issues of discrimination and social justice, and also participated in anti-nuclear demonstrations. Check the most likely alternative.– Linda is a bank teller.

– Linda is a bank teller and is active in the feminist movement.

17

The conjunction fallacy

18

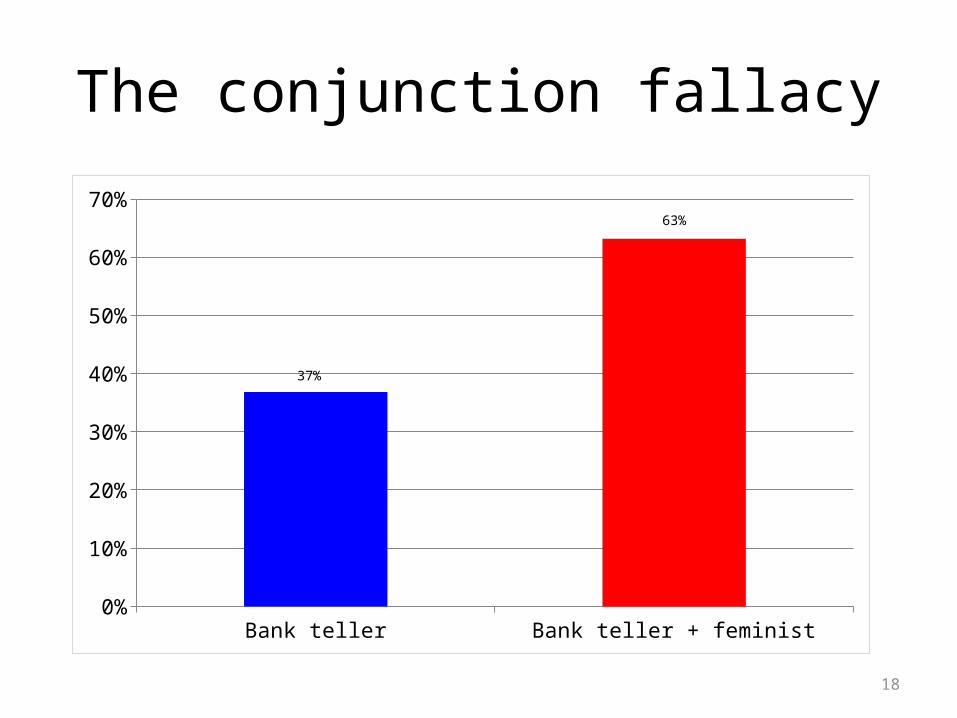

Bank teller Bank teller + feminist0%

10%

20%

30%

40%

50%

60%

70%

37%

63%

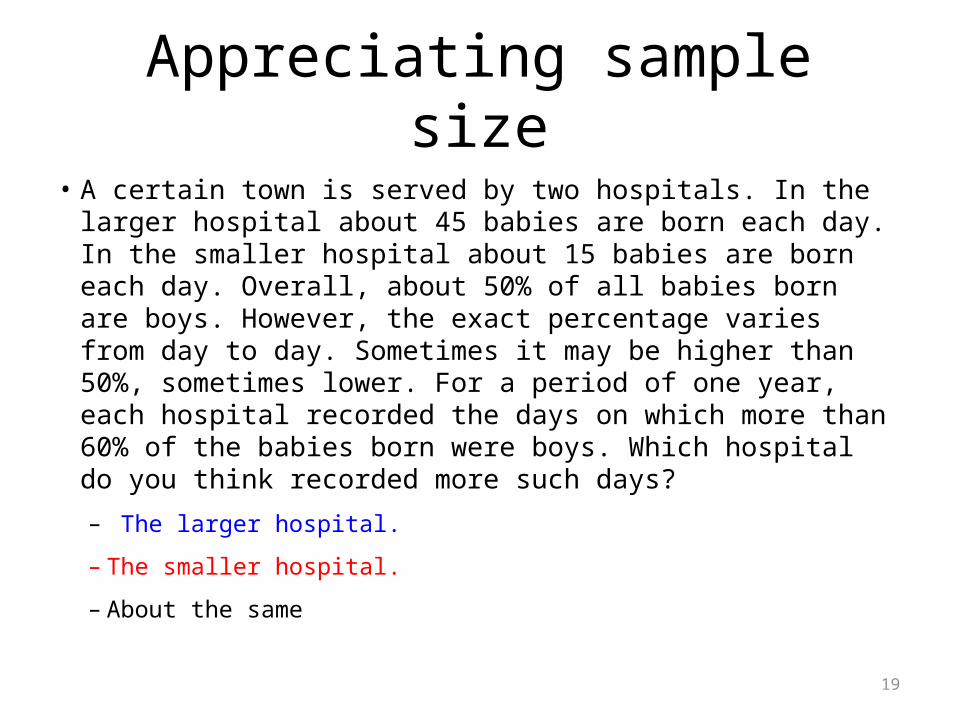

Appreciating sample size• A certain town is served by two hospitals. In the larger hospital

about 45 babies are born each day. In the smaller hospital about 15 babies are born each day. Overall, about 50% of all babies born are boys. However, the exact percentage varies from day to day. Sometimes it may be higher than 50%, sometimes lower. For a period of one year, each hospital recorded the days on which more than 60% of the babies born were boys. Which hospital do you think recorded more such days?– The larger hospital.

– The smaller hospital.

– About the same

19

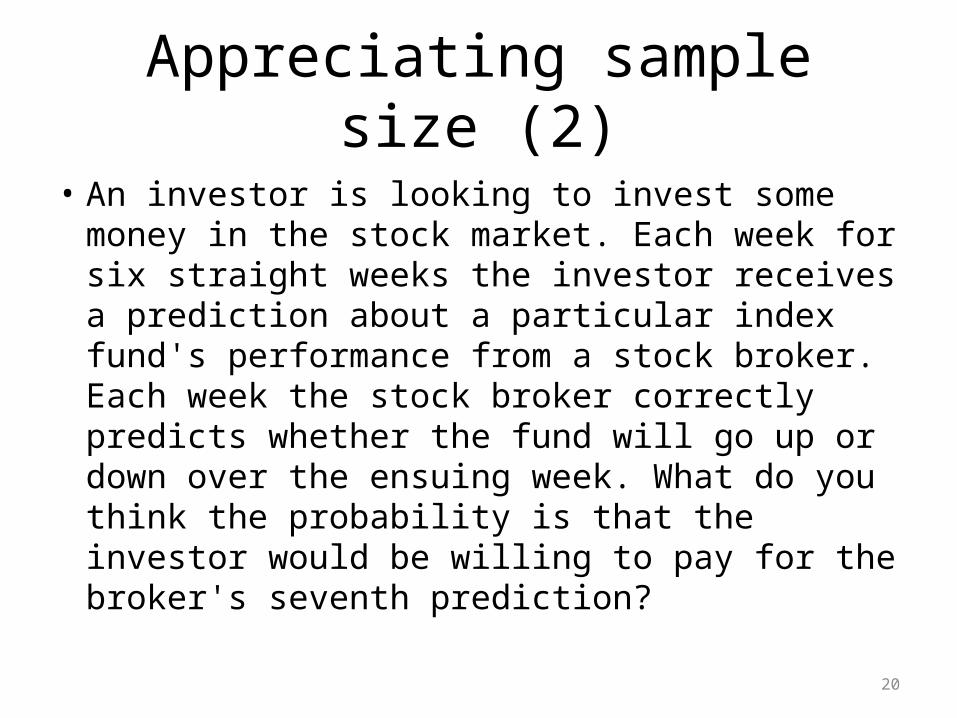

Appreciating sample size (2)

• An investor is looking to invest some money in the stock market. Each week for six straight weeks the investor receives a prediction about a particular index fund's performance from a stock broker. Each week the stock broker correctly predicts whether the fund will go up or down over the ensuing week. What do you think the probability is that the investor would be willing to pay for the broker's seventh prediction?

20

Terima kasih

Related Documents