1.1 INTRODUCTION Business decisions may be based upon “intuition” or upon an intelligent analysis of factual data. There is no formula for analysis. Much depends on the purpose of analysis, the nature of analysis and exclusiveness of significant conclusions. There are three basic steps in the analysis of business problem; 1. Breakdown the figure into classification so that one can compare the past of the whole to each other and 2. Compare with significant outside factors and thus determine their relationship 3. This permits one to determine the reason for relat5ionship thus making possible understanding of essential nature of the situation and findings of solution to the problems involved in the situation. From the above view point the researcher of this project makes an attempt in analyzing the capital structure planning by breaking down the figures into classifications to compare the parts of the whole to each other. This project taken up to strengthen the academic of the project Cost of Capital Analysis The impact of changes in the capital structure on the cost of capital analysis and the profitability is analyzed as capital structure decisions are not taken in isolation. They are largely influenced by their twin factors of minimizing the cost of capital and maximizing the returns. Thus the cost of capital is 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1.1 INTRODUCTION

Business decisions may be based upon “intuition” or upon an intelligent analysis of

factual data. There is no formula for analysis. Much depends on the purpose of analysis, the

nature of analysis and exclusiveness of significant conclusions.

There are three basic steps in the analysis of business problem;

1. Breakdown the figure into classification so that one can compare the past of the whole to

each other and

2. Compare with significant outside factors and thus determine their relationship

3. This permits one to determine the reason for relat5ionship thus making possible

understanding of essential nature of the situation and findings of solution to the problems

involved in the situation.

From the above view point the researcher of this project makes an attempt in analyzing

the capital structure planning by breaking down the figures into classifications to compare the

parts of the whole to each other. This project taken up to strengthen the academic of the project

Cost of Capital Analysis

The impact of changes in the capital structure on the cost of capital analysis and the

profitability is analyzed as capital structure decisions are not taken in isolation. They are largely

influenced by their twin factors of minimizing the cost of capital and maximizing the returns.

Thus the cost of capital is the combination of various specific costs which are discussed below.

Cost of Equity

Equity capital like other sources of funds does not certainly involve a cost of the firm. It

may be recalled that the objectives of the financial management is to maximize the shareholders

wealth and maximization of market price of shares in the operational substitute for wealth

maximization. When equity shareholders invest their funds, they also except returns in the form

of dividends.

The market value of shares is a function of the returns that the shareholders except and

get. Thus in order to evaluate the capital structure of the firm it is necessary to know the cost of

capital of the company.

1

Cost of Debt

Cost of debt describes about the cost of raising finance from long term funds or

outsider’s fund. Thus an optimum amount of dent in the capital structure of the firm may reduce

its costs. However over utilization of debt may increase the interest payments of the company.

Debt of a firm is predominated figure in the capital structure and so there lays the

essentiality to calculate the cost of debt to derive at optimum capital structure.

Weighted Average Cost of Capital

Weighted average cost of capital is the composition of specific cost of capital lays cost

of equity and cost of debt. The overall cost of capital helps the company to analyze the overall

efficiency of the company. It describes the overall cost of capital of the company. Thus it is a

technique to measure the capital structure of the company.

Capital Structure

Given the objectives of the firm to maximize the value of its equity shares, the firm

should select the best mix of the equity and debt capital structure refers to the composition of

long term sources of funds such as debentures, long term debt, preference share capital and

equity including reserves and surplus. Optimum or balanced capital structure means an ideal

combination of borrowed and owned capital that may attain the marginal goal (i.e.) maximizing

the value of shareholders.

The choice of amount of debt and equity is made after comparison of certain

characteristics of each kind of security of internal factors related to the firms operations and

external factors that affect the firm. Thus the capital structure of the company may be a

combination of debt and equity leads to the maximum value of the firm.

Objective of Capital Structure

In context of the optimum capital structure, the firm may be faced with the problem of

mixing the equity securities and debt securities.

1. Payment of high interest.

2. Higher control of equity shareholders.

Thus optimum capital structure is decided on the basis of two danger points.

2

Tools and Techniques of Capital Structure

Companies do not plan their capital structure may prospect in short run but ultimately

they will face series problem in f\raising funds to meet their additional financial requirements in

future.

Whenever the financial manager considers the question of capital structure, it is always

the question of capital structure (i.e.) to decide the proportion of ownership funds and borrowed

funds. So the study was made to analyze the capital structure of the company using various

tools.

Ratio Analysis

One approach to analyze the capital structure of the firm is to make the comparison of

the ratios of the firm. Comparison is helpful as it is acts as a red signal to the management that

there may be something wrong with the capital structure of the company.

Ratio shows the significant relationship between figures shown in the Balance Sheet, in

Profit and Loss account or in any other part of accounting organization. Ratios are the best guide

for execution of basic managerial function like planning, forecasting and controlling.

3

1.2 INDUSTRY PROFILE

Milk is considered as a complete and ideal food and it contains most of the proximate

principles of a well balanced diet. India is the world’s largest milk producer and in set to

become the world’s largest food factory. Indian dairy industry embarked on recent innovation

technology by having a wide ranging impact on the growth of the industry.

This revolution is contributing to the productive utilization of growing milk surplus. It’s

important for healthy, active people to eat right. A glass of Milma milk three times a day gives

you more vitamin sand minerals than any other popular health drink and ensures that you get

sufficient proteins to help in providing the building blocks that constructs and repairs muscle.

Milma milk also helps to meet your calcium requirement. Dairy products are the richest source

of important nutrients like vitamin D which helps to use calcium effectively.

Calcium Counts for Young and Old

Calcium is one of the most important nutrients in Milma’s pasteurized milk. Calcium,

one of the most abundant minerals in the human body, is frequently found lacking in the daily

diet. Calcium is important not only for building and maintain strong bones but also for

regulating the heart beat and proper functioning of the nerves. With calcium playing such a

clerical role in maintain your health, you cannot afford a deficiency. Milma’s low far or fat free

milk give the same amount of calcium and other nutrients, minus fat. Pregnant women need

calcium for the growth of the baby.

The Fresh and Glowing Fresher

A well-nourished boy is more component to meet the mental and physical demands of

college life. Skipped meals and unhealthy eating habits can short change essential nutrients of

our body. Healthy eating not only made us look and feel good, but also make our body and for

the future.

Increasing our daily milk consumption will not help us on the calcium front, but also

help balance our diet and keep it nutrients rich. Consumption of three glass of Milma milk

everyday for the strong bones, good looks and a sharp mind.

4

The Power Drink for Teenagers

Milk is a vital drink throughout life and more so when it needs the teenagers in growing.

The 15% of the human grows during the teenage period. So that calcium is very much needed in

teenage for the growth. The essential growth nutrients like protein, potassium and calcium is

essential for all humans for their growth. Milma milk is the power drink for active young boys

and girls.

Kerala Co-Operative Milk Marketing Federation (KCMMF), popularly called Milma

was established in April, 1980 with its head office at Thiruvananthapuram for the successful

implementation of Operation Flood (a dairy programme launched in 1970 under the aegis of

National Dairy Development Board (NDDB).

TRCMPU

TRCMPU is carrying out various input activities in its milk shed and a details of the activities

carried out by the Regional Union in the Financial year 2011-2012 are given below.

Union has distributed Rs. 4.00 crores as price incentive to the societies and Rs. 3.5 crores as

summer incentive to the farmers.

In the financial year total numbers of 465 first aid centers are functioning in four districts and

29336 numbers of cases were attended.

Total number of de-centralized vetenary units are 30 and 29681 cases had been attended.

Total number of production enhancement camp (Gosamvardhini) conducted is 244 and total

number of cases attended is 12013.

50% subsidy on cattle insurance premium.

Total; A.I centers functioning under union is 26 and the total number of A.I performed is

9211.

Under100P scheme, 65 hectors of land was cultivated under fodder development programme

in Pathanamthitta District.

Under 100P-CMP Programme, various projects are implemented with the financial assistance

to the tune of Rs. 10.06 crores from the Govt. of Indi. 52 bulk coolers were installed with a total

capacity of 19600 liters.

5

Schemes for Milk Production Enhancement

Rs, 137.68 lakhs were spending for calf adoption scheme.

Insurance subsidy for new mini Dairy units was given for an amount of Rs. 3.15lakhs.

Cattle feed subsidy for a new mini dairy units was given for Rs. 37.39 lakhs.

Rs. 3.22 lakhs was spending for fodder cultivation schemes.

Rs.2.57 lakhs was spending for de-warming.

Under Benevolent fund scheme financial assistance to depend of deceased farmers and

scholarship for higher education are given Rs.25.64 lakhs spend during 2011-2012.

De-centralized vetenary units for providing vetenary service at doorstep of farmers and free

medicine Rs.51.14 lakhs during 2011-2012.

Future Plan

Maximization of women participation in Dairy sector.

10% growth rate in income through Dairying for the farmers.

Reaping on corporative identity through mnemonic symbol.

Enhance processing capacity.

Plan to launch new products.

Introducing of new brands.

Export of products.

Plans to custom pack products such as cheese, tera fino and fruit drinks.

Building of brand equity.

Restructuring of district system.

Benchmarking performance to international Quality Standards.

Introducing of bulk milk coolers at society for improvement of bacterial quality.

Quality awareness training.

1.3 COMPANY PROFILE

6

Brief Introduction of Milma

Kerala Co-Operative Milk Marketing Federation (KCMMF) popularly called Milma was

established in April 1980 with its head office Thiruvananthapuram for the successful

implementation of Operation Flood (a dairy development programme launched in 1970 under

the aegis of National Dairy Development Board (NDDB)).

The name Milma represents;

2100 primary milk co-operative societies.

5.24 lakhs farmer member.

Three Regional Cooperative milk producers union.

Eleven diaries.

Fourteen milk chilling centers.

Two cattle fed plant 10 MT per day capacity of 500 MT per day.

One milk powder plant 10MT per day capacity.

A well established training centre.

More than 4000 retail outlets.

Over 18000 people working either directly or indirectly for the functioning of Milma.

Apart from these, Milma servers millions of consumer’s day in and day out.

Mission

To channelize marketable surplus milk from rural areas to urban deficit areas to maximize the

returns to the producer and provide quality milk products to consumers.

To carryout activities for promoting production procurement processing and marketing of

milk and milk products for economic development of farming community.

To build a viable dairy in the state.

To provide a constant market and stable price to the farmers for the products.

The motto of co-operation “of the people, by the people and for the people” in the

foundation of the three tier system followed by the organization. At the village level Milma have

village milk co-operative societies- the local milk producers as its members. These village co-

operative units at the regional level and from co-operative milk producers unions. These unions

are federated at the level a form- State federation namely Kerala Co-operative Milk Marketing

Federation.

7

Milma- the Farmer’s Organization

Milma is an organization for the farmers. Farmers are the producer of the raw materials

that the milk. The shareholders in the organization and the chairman and the Board of Directors

are elected among them.

The farmers are the members of the Anand pattern co-operative societies (APCOS). The

President of the APCOS forms the general body of the Regional milk unions which federated to

form KCMMF

Milma’s Associates

Chief associates are;

National Dairy Development Board (NDDB)

NDDB under Dr. Varghese Kurian’s guidance set up KCMMF at 1980. Ever since then

there has been a close co-operation between NDDB and Federation.

Amul

The dairy co-operative of Gujarat has been the inspiration for the development of the

vast network of co-operative in Kerala.

Government of Kerala

The phenomenal success of the Dairy co-operative in Kerala could not have been

achieved without foundation of animal husbandry activities, led by the Animal Husbandry

Department, Kerala.

MILMA have 3 Regional Co-operative Unions;

1. Thiruvananthapuram Regional Co-operative Milk Producers Union Ltd.

2. Ernakulam Regional Co-operative Milk Producers Union Ltd.

3. Malabar Regional Co-operative Milk Producers Union Ltd.

Thiruvanthapuram Regional Co-operative Milk Producers Union Ltd (TRCMPU) is one

of the Regional Co-operative Milk Producers Union in Kerala state, and is the oldest one among

the three. The TRMPU includes the four southern district of Kerala.

a) Thiruvanthapuram

8

b) Kollam

c) Alleppy

d) Pathanamthitta

2678 primary milk co-operative societies now functioning as on31.03.2013.

8.31 lakhs farmer members.

Three regional co-operative milk producers union.

Thirteen diaries capable of handling 12 lakhs liters of milk per day.

Ten milk chilling centers.

Two cattle feed plants with cumulative capacity of 600 MT per day.

One milk powder plant of 10 MT per day capacity.

A well established training centre.

5200 retail outlets.

Over 32000 people working either directly or indirectly for the functioning of Milma.

Apart from these the company serves millions of consumers day-in and day- out.

1.4 PRODUCT PROFILE

Product and service details

9

Milma pasteurized having two kinds;

o Toned milk

o Double Toned milk

Toned Milk

Toned milk is considered common milk in which the colour of the package is blue which

contains 3.5% fat and 8.5% of SNF. This milk mainly focused on domestic consumer and is

available in 500 ml packet. Milma gives 4% of commission of sale of each packet of milk. The

price of the toned milk is Rs. 17.50.

Double Toned Milk

This milk contains high fat content of about 4.5% fat and 9% SNF. The price of the

double toned milk is Rs. 16. Both the above milk can be stored for 2 days under cool condition

below 7 degree Celsius.

Sambharam

Sambharam (Butter milk) is a favorite beverage in Kerala. Milma sambharam is only

product of its kind in the market and it is very popular throughout the state is comes in 200ml

packet. It is seasonal product mainly for summer season and is very demand in summer. In

future Milma is planning to launch 500ml packet of sambharam price is at Rs. 20.

Curd

It is a fermented product prepared from pasteurized skim milk using curd culture from

National Dairy Regional Institute (NDRI) is delicious tasty, free cholesterol and is available in

500ml packet. The market price of curd is Rs.20.

Ghee

Milma ghee is available in 500ml, 100ml 50ml and 1 liter. Ghee is the only exporting

product of Milma. The market price of the Milma ghee is as follows;

500ml – Rs.210

100ml – Rs.44

200ml – Rs.86

10

50ml – Rs.23

1 Liter- Rs.400

Peda

An indigenous product manufactured by evaporating water content from whiles some

cow’s milk and sweetened with cane sugar. It is nutritious and delicious sweet bite for children

and in 10 piece box which costs Rs.60. milma peda is produced in Pathanamthitta Dairy.

Milma Sip Up

It is made from pasteurized skim milk sweetened and flavored which is available in 25ml

polythene tube, which flavored by vanilla, strawberry, pineapple served in chilled condition. It

is good for health and is nutritious substance to all other sip ups. The market price of the sip up

is Rs.3.

Ice Cream

Milma ice cream is available in average of lip smacking flavours. Vanilla, chocolate,

pineapple, strawberry and pista. The only ice cream and Kerala manufactured in a dairy is

Milma ice cream and hence this is fresher than any other ice cream produced in the

Thiruvananthapuram dairy. The market price of ice cream is Rs.105, for standard flavour like

chocolate and butterscotch are Rs. 125, 135.

Cattle Feed

Balanced cattle feed is the major input to the dairy farmers of the state federation. There

is a high level of acceptance for this product in the market. The cattle feed is distributed to the

farmers at a reasonable price through different agencies.

Milma Instant Dairy Whitener

Milma has a plant in Allapuzha for the milk powder production from milk. The market

price of 500gm of milk powder is Rs. 175 and for 200gmis Rs.65.

Palada Mix

Palada mix is a product of Kozhikod dairy. The market price of Palada mix of 250gm is

RS.60.

11

Mango Drink

Thiruvananthapuram dairy is producing the mango drink. The market price of the mango

drink is Rs.50 per liter.

Milma Butter

Milma butter is produced in Thiruvanthapuram dairy. The market price of milma butter

is Rs.35 for 100gm. The product can be stored up to 6 months from the manufacturing date

under regeneration condition.

Low Fat Panner

Thiruvanthapuram dairy is producing the low fat panner. The market price of low fat

panner is Rs.28 for 100gm.

Milma Chocolick

Milma chocolik is a chocolate produced in the Ernakulam Dairy. The market price is

Rs.14 for Chocó bar and Rs.12 for mango bar.

Milma Plus

Milma plus is satirized from skimmed flavoured milk which is good energy drink

producer in the Allapuzha and Kollam Dairy. Milma plus is the flavours like chocolate,

strawberry pineapple, mango and pista. The market price of milma plus is Rs.20 for 200ml.

1.5 DEPARTMENT PROFILE

Human Resource Department

12

In Pathanamtitta Dairy the human resource management is headed by the assistant

manager, the dairy had a total strength of 120 workers out of which 80 are permanent and 35 are

temporary. Temporary employees are appointed for a period of 6 months usually they include

stenographers, typist etc...

Marketing Department

Marketing department of any organization has a key role to play the profile and

development. The marketing department in Pathanamthitta dairy is headed by an assistant

manager. Under he comes marketing officer, senior assistant officers etc...

Production Department

Production department is concerned with the process which combines and transfers

various resources into value added product or service. It is the core department of the company.

An organization’s wealth is to successfully utilize the resource available in the organization that

is men, material, money and machine. The importance of production department is the

processing of the milk and its other by-products. The production department is headed by the

assistant manager.

Finance and Accounting Department

Finance is considered as the life blood of business organization. Finance management

is one of the important areas of the management as the effectiveness of the business enterprise is

based on finance. The Pathanamthitta dairy the finance department is headed by the assistant

manager. The structure of the department is shown below;

Assistant Manager

Junior Superintendent

13

Senior Assistant

Junior Assistant

Quality Control Department

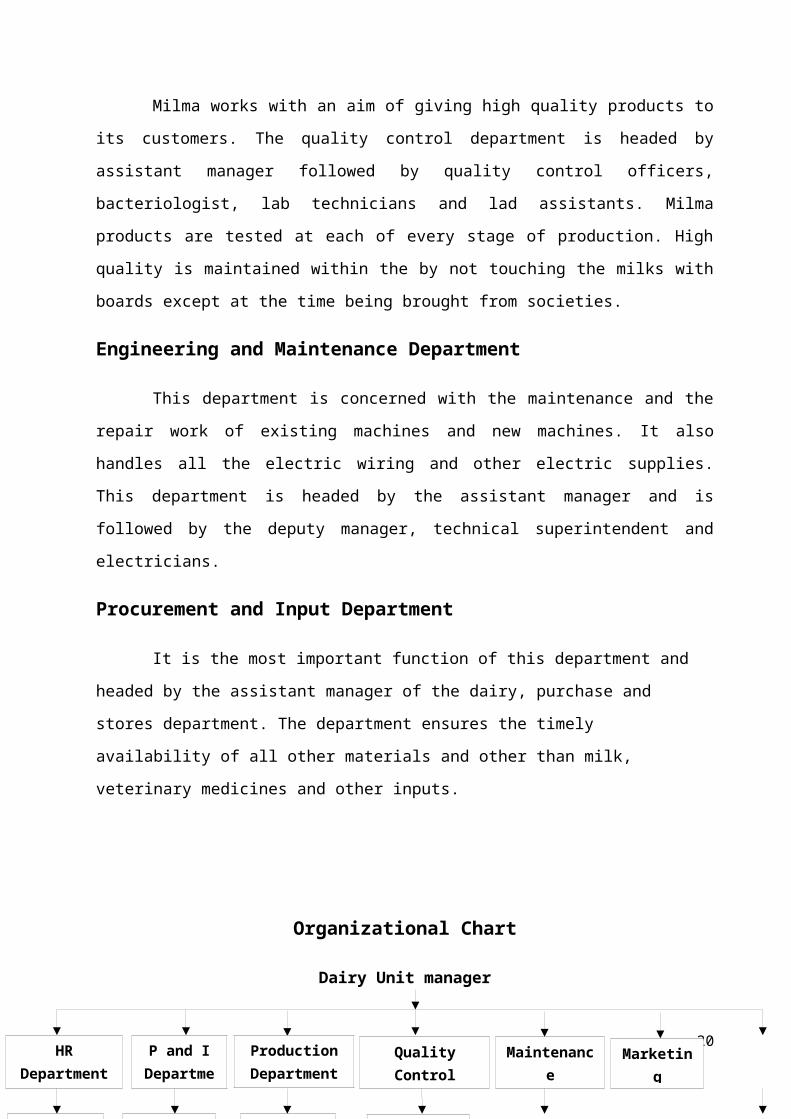

Milma works with an aim of giving high quality products to its customers. The quality

control department is headed by assistant manager followed by quality control officers,

bacteriologist, lab technicians and lad assistants. Milma products are tested at each of every

stage of production. High quality is maintained within the by not touching the milks with boards

except at the time being brought from societies.

Engineering and Maintenance Department

This department is concerned with the maintenance and the repair work of existing

machines and new machines. It also handles all the electric wiring and other electric supplies.

This department is headed by the assistant manager and is followed by the deputy manager,

technical superintendent and electricians.

Procurement and Input Department

It is the most important function of this department and headed by the assistant

manager of the dairy, purchase and stores department. The department ensures the timely

availability of all other materials and other than milk, veterinary medicines and other inputs.

Organizational Chart

Dairy Unit manager

14

HR Department

P and I Department

Production Department

Quality Control Department

Maintenance Department

Marketing Departmen

t

Finance Manager

Assistant Manager

Assistant Manager

Assistant Manager

Assistant Manager

1.6 NEED OF THE STUDY

This study helps to find out the Cost of Capital of Milma Dairy, Pathanamthitta.

Covers comparison and analysis of the performance of the concern and to point out the threat.

15

Assistant manager

Assistant Manager

Assistant Manager

Deputy Manager

Technical Supervisor

Marketing Officer

Assistant Marketing

Officer

Field Officer

Junior Superinte

ndent

Senior Assistant

Junior Assistant

1.7 OBJECTIVES OF THE STUDY

To examine the capital structure of the company.

To evaluate the cost of capital analysis in the Milma dairy.

To measure the profitability of the firm.

To study the leverage analysis in the reference of annual report.

16

To give suggestion on the basis of the above analysis, for an effective financial decisions

making.

SCOPE AND LIMITATIONS OF THE STUDY

1.8 Scope of the Study

The study helps to find out the strength and weakness of the concern in its management of

Cost of Capital and also the reason for the variation in profitability.

17

It gives the management an overall idea about its past performance and this is in turn will

help them to take corrective measures if they are not satisfied with their past performance.

1.9 Limitations of the Study

The availability of information and data limited by the time factor.

The study is based on the data obtained from the annual reports of the company.

The analysis of various ratios is done only for a period of 5 years.

Hence conclusion made may not be complete.

2. REVIEW OF LITERATURE

Brander and Lewis (1986)1

1 Brander and Lewis (1986) , Financial Management by M.Y Khan & P.K Jain, Tata McGraw

Hill Publishing Co. Ltd, 1997

18

Provide the theoretical framework that links capital structure and market structure.

Contrary to the project maximization objective postulated in industrial organization literature,

these theories like the corporate finance theory, assumes that the firm’s objective is to maximize

the wealth of the shareholders and show that the market structure affects the capital structure by

influencing the competitive behaviour and strategies of the firm. Firms in the oligopolistic

market will follow the strategy of maximizing their output for improving profitability in

favourable economic condition. In unfavorable economic conditions, they would take a cut in

production and reduce their profitability.

Jensen and Mocking2

Argue that the shareholder’s lender’s conflict results into risk shifting and wealth

appropriation in favour of shareholders as they take on risky investment projects (assets

substitution). Hence, shareholders and managers as their agents are prompted on to take on more

borrowing to finance. Risky project venders would receive interest and principal if project

succeed and shareholders would appropriate the residual income finance corporate theory that

justifies the use of high debt is the tax-shield theory.

Modigliani and Miller (1963)3

Profitability firms borrow more to save taxes since interest cost are tax deductible. The

output maximization by oligopoly firms is supposed to increase their profitability. Hence, both

the Agency Cost theory and tax-shield theory would predict a positive relationship between

capital structure and market structure. Capital structure increases the chances of financial

distress and bankruptcy. Firms face cost of financial distress when they are unable to service

debt. They will have high debt ratios if these costs are zero or trivial.

Scott(1976) Kim(1990)4

2 Jensen and Mocking (1986) , Principles of Management Accounting by Dr. S.N Maheswari,

Sultan Chand & Sons, 1995.

3 Modigliani and Miller (1963) , Financial Management by I.M Pandey, Vikas Publishing House Pvt Ltd, 19954 Scott(1976) Kim(1990) , Financial Management by M.Y Khan & P.K Jain, Tata McGraw Hill

Publishing Co. Ltd, 1997

19

Since cost of financial distress are trivial and high levered firm can actually go

bankrupt, firms with high probability of bankrupt will have low debt ratio. The chances of

bankruptcy for firms with large reserve funds will be relatively less but, unleveled firms with

high profitability and large reserve funds would have great competitive advantage. These firms

with deep purse may not survive but they would also gain by driving their rival firms into

bankrupt.

Bolton and Scharfstein (1990)5

These firms follow a policy of aggressive production and predatory price cuts to

eliminate their rivals by forcing them into financial distress. Their strategy pays them off

particularly when external funding is not available to the firms of the target predatory price

behaviour. The implication of this model is that the unleveled firm with deep purses (high

profitability and reserve funds) would have incentive to increase output to drive the competitors

into bankruptcy. Empirically, we can predict a negative relationship between capital structure

and market structure.

Myres (1977)6

Provide a model under which debt causes under-investment (asset substitution). Firms

reject those profitable, low risk investment projects that have the possibility of passing on

benefits from shareholders to lenders. Further, internal financing is cheaper than external

financing due to asymmetric information. Higher debt makes higher output costly for a levered

firm. There are a few empirical studies that have investigated the issues of capital structure and

market structure using the data of the U.S firms.

Chevalien (1993)7

5 Bolton and Scharfstein , Financial Management by Prasanna Chandra, Tata McGraw Hill

Publishing Co. Ltd, 1995.

6 Myres (1977) , Cost and Management Accounting by S.N Maheswari, Sultan Chand & Sons, 19967 Chevalien (1993) , Cost Accounting by Jain & Narang, Kalyani Publishing, New Delhi, 1997.

20

Provide evidence in support of a negative relationship between capital structure and

market structure. This result is consistent with the bankruptcy cost or the asymmetric

information / pecking order hypothesis.

3. RESEARCH METHODOLOGY

Research

Research is common pestilence refers to search for knowledge. Once can also define

research as a scientific and systematic search for a pertinent information on a specific topic. In

fact, research is an art of scientific investigation. Redman and Mary define research as a

“systematic effort to gain new knowledge”.

21

Research is an academic activity and as such the term should be used in a technical

sense. According to Clifford Woody, “research comprises defining redefining problems,

formulation of hypothesis, collecting, organizing and evaluating data, making deductions and

research conclusion and at last carefully testing the conclusion to determine whether they fit the

formulating hypothesis”.

Research Design

A research design is the arrangement of condition for collection and analysis of data in

a means that aims relevance to the research purpose with economy in procedure. In this study

the analytical research is followed.

Sources of Data Collection

In this study secondary data is the main source.

Primary Data

The primary data are those data which are collected for the first time by the researcher.

Secondary Data

The secondary data are those data which have already been collected someone else and

which have already been passed through the statistical process. In this study secondary data is

the main source. Thus the data was collected through;

Annual Reports

Books

Website of Milma Dairy

Internet

Tools used for Analysis

1) Ratios

2) Leverage Analysis

3) Capital Structure and Cost of Capital

4) Trend Analysis

Area of study

22

Milma dairy , Pathanamthitta , kerala

Period of study

The period of study is from 2009 to 2013.

4. DATA ANALYSIS AND INTERPRETATION

4.1 Ratio

4.1.1 Debt Equity Ratio

This financing of the total assets of the business concern is done by owner’s

equity (also known as internal equity) as well as outsider’s debt (also known as outsider’s

equity). How much fund has been provided by the owner’s and how much by the outsiders in

the acquisition of the total assets is a very significant factor affecting the long term solvency

position of the concern.

23

Table Showing Debt Equity Ratio

Year Long Term Debt Shareholder’s Fund Ratio

2008-2009 3314097.2 3567417.08 .929

2009-2010 2614008.3 4752742.35 .55

2010-2011 41829512.05 5980284.19 6.99

2011-2012 41859512.05 5980284.19 6.99

2012-2013 1885645 6280250 .300

Interpretation

The debt equity ratio was 3.29 in the year 2008-2009. It indicates long term debt is high

compare than shareholder fund but it was decreased during the next year. The lower proportion

of debt provides a higher margin of safety for them.

Graph 1

24

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

7

8

Ratio

Ratio

4.1.2 Interest Coverage Ratio

Apart from EBIT-EPS analysis, the ability of the firm to use debt from the profitability point

of view can also be judged in terms of coverage ratio namely;

Interest Coverage = Earnings before I and T / Fixed Interest Charges

25

Table Showing Interest Coverage Ratio

Year EBIT Interest Ratio

2008-2009 5435117.60 323242 16.81

2009-2010 6060665.58 699996.00 8.66

2010-2011 10710115.35 699996.00 15.30

2011-2012 3775818.47 699996.00 6.39

2012-2013 14891082 700000 21.27

Interpretation

The above table indicates that interest covered by earning was 7.81 times on an average.

Even though there has been a small fall in the ratio during the year 2010 and 2011 when

compared 2012. The ratio went up 10.04 times in the year 2012-2013. This was due to high

increase in the earning before interest and taxes.

Graph 2

26

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

5

10

15

20

25

Ratio

Ratio

4.1.3 Debtors Turnover Ratio

Debtor’s turnover ratio measures the number of times the receivables are rotated in terms of

sales. This ratio also indicates the efficiency of credit collection and efficiency of credit policy.

The ratio is helpful in determining the operational efficiency of a business concern and the

27

efficiency of credit policy. It is important to maintain reasonable quantitative relationship

between receivables and sales.

Debtor’s Turnover Ratio = Sales / Debtors

Table Showing Debtors Turnover Ratio

Year Sales Debtors Times

2008-2009 115570571.80 2889264.30 40

2009-2010 139266692.88 3027536.80 46

2010-2011 168393118.14 2629747.795 64.03

2011-2012 139266692.88 2629747.795 52.96

2012-2013 252541100.5 4194870.23 66.20

Interpretation

It is shown in the table that there is an increasing ratio of debtor’s turnover ratio from the

year 2009-2011, but the small variation in the year 2012 was due to the change in organization

strategy.

Graph 3

28

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

10

20

30

40

50

60

70

Times

Times

4.1.4 Debtors Collection Period

Debtor’s collection period indicates the financial strength of the organization because

it facilitates a comfortable working capital. The higher the turnover ratio and shorter the

collection period, better the trade credit management. Debtor’s collection period measures the

29

quality of debtors. Since it measures the rapidity or lowness with which money is collected from

them.

Debtors Collection Period = 365 Days / Debtor’s Turnover

Table Showing Debtors Collection Period

Year Days of Year Debtor’s Turnover Days

2008-2009 365 40 9

2009-2010 365 46 8

2010-2011 365 64.03 6

2011-2012 365 52.96 7

2012-2013 365 66.20 5

Interpretation

In the year 2008-2009, the debtor’s collection period is 9 days. It indicates too liberal and

insufficient credit collection performance. In the subsequent years company has taken measures

and decreased collection period. It shows good sign for the company.

Graph 4

30

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

7

8

9

10

Days

Days

4.1.5 Profitability Ratio

A company should earn profit to survive and grow over a long period of time. Profits

are essential, but it would be wrong to assume that every action initiated by management of a

company should be aimed at maximizing profits. The profitability ratios are calculated;

31

I. Gross Profit RatioII. Net Profit Ratio

III. Current Ratio

I. Gross Profit Ratio

Gross profit ratio is the relationship between Gross Profit and sales. This ratio can be

obtained the degree to which the selling price of the goods per unit may decline without

resulting in loses from operation to the firm. It is expressed in percentage data.

Gross Profit Ratio = Gross Profit / Net Sales * 100

II. Net Profit Ratio

Net profit ratio is the relationship between net profit and net sales. It is calculated after

excluding non-operating expenses. It is used to measure the efficiency and overall profitability

of the organization. This ratio helps in determining the efficiency with which affairs of the

business are being managed.

Net Profit Ratio = Net Profit / Sales* 100

III. Current Ratio

Current Ratio = Current Assets / Current Liabilities

Table Showing Gross Profit Ratio

32

Year Gross Profit Sales Ratio

2008-2009 3526118.86 344446633.69 1.024

2009-2010 8291413.38 412094161.81 2.012

2010-2011 4730881.83 493670662.22 .958

2011-2012 18286413.36 422094161.81 4.332

2012-2013 164961078 21423516.62 7.70

Interpretation

In 2008-2009 Gross Profit Ratio is average. This shows that opening stock is over valued.

But from 2009-2010 the ratio increases when compared to the previous years, this proved that

the selling price of the goods sold has gone up without corresponding increases in the costs.

Graph 5

33

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

7

8

9

Ratio

Ratio

Table Showing Net Profit Ratio

34

Year Profit after Sales Sales Ratio

2008-2009 -3435117.60 344446633.69 -1.578

2009-2010 -6060665.58 412094161.81 -1.470

2010-2011 -10710115.37 493670662.22 -2.169

2011-2012 3775818.47 422094161.81 0895

2012-2013 33849156.26 21423516.62 1.58

Interpretation

In 2008-2009 Net profit ratio is low. It indicates lack of improvement in the operational

efficiency of the business. From the year 2012-2013 the ratio is increased which shows that the

good profitability condition of the business.

Graph 6

35

2008-2009 2009-2010 2010-2011 2011-2012 2012-2013

-200

0

200

400

600

800

1000

Ratio

Ratio

Table Showing Current Ratio

36

Year Current Assets Current Liabilities Current Ratio

2008-2009 102458078.38 108869852.32 .941

2009-2010 218954815.6 238225938.85 .919

2010-2011 10156426.31 401442464.05 .253

2011-2012 25570689.92 401424664.05 .637

2012-2013 24147041 45101080.5 .535

Interpretation

The Current Ratio indicates that there is a fluctuation in each year, which represents there is

adequate for the day to day transaction.

Graph 7

37

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Current Ratio

Current Ratio

4.2 Leverage Analysis

38

4.2.1 Degree of Financial Leverage

Financial leverage affects the earning per share. When the economic conditions are good and

the firm’s EBIT is increasing, its EPS increases faster with more debt in the capital structure.

DFL = % Change in EPS / % Change in EBIT

Table Showing Degree of Financial Leverage

Interpretation

The above table shows that the EBIT of the company has increased in the year 2011-2012.

The decline in the year 2012-2013 was due to increase in the interest payments. On an average

the financial leverage was 1.21% times which implies that one percent change in EBIT will lead

to 1.07% change in EPS.

Graph 8

39

Year EBIT EPS Ratio

2008-2009 13672 11188 1.22

2009-2010 17608 15566 1.13

2010-2011 22244 20230 1.09

2011-2012 25999 23056 1.12

2012-2013 34674 32132 1.07

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130.95

1

1.05

1.1

1.15

1.2

1.25

Ratio

Ratio

4.2.2 Operating Leverage

Operating Leverage can be defined more precisely in terms of the way given

change in volume or value of sales, affects portfolio degree of Operating Leverage.

40

Degree of Operating Leverage (DOL) is defined as the percentage change n the Operating

Profit that results from a percentage change in units sold.

Operating Leverage can also be calculated by the formula.

DOL = Contribution / EBIT

Table Showing Operating Leverage

Year Contribution EBIT Ratio

2008-2009 42042 13672 3.07

2009-2010 51548 17608 2.92

2010-2011 55807 22244 2.50

2011-2012 59304 25999 2.28

2012-2013 62433 34674 1.80

Interpretation

The above table indicates the Operating Leverages for 5 years that is from 2009-2013. The

leverage was 2.04% times on an average. The leverage was increased in the year 2008-2009 and

lowest in the year 2012-2013.

Graph 9

41

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.5

1

1.5

2

2.5

3

3.5

Ratio

Ratio

4.2.3 Combined Leverage

The Degree of Financial Leverage and Operating Leverage can be combined to see the

effect of total leverage of EPS associate with a given change in sales. The degree of Combined

Leverage (DOL) is given by the formula.

42

Degree of Combined Leverage = Operating Leverage * Financial Leverage

Degree of Financial leverage constitutes a double edged sword. They have tremendous

acceleration effect on EPS and EBIT.

Table Showing Combined Leverage

Year Financial Leverage Operating Leverage Combined Leverage

2008-2009 1.22 3.07 3.74

2009-2010 1.13 2.92 3.29

2010-2011 1.09 2.50 2.72

2011-2012 1.12 2.28 2.46

2012-2013 1.07 1.80 1.92

Interpretation

The table shows Combined Leverage for five years (2009-2013) Combined Leverage was

higher in the year 2008-2009 amounts to 3.74 percent which explain that 2 percent change in

sales would lead to 2 percentage changes in Earnings per Share. The Combined Leverage was

3.74% on an average. This leverage was due to the existence of Financial Leverage of the

company.

Graph 10

43

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.5

1

1.5

2

2.5

3

3.5

4

Combined Leverage

Combined Leverage

Table showing sources of funds during the year 2008-2009

Particulars Amount (in lakhs) Percentage

44

Share Capital 4439 7%

Reserves and Surplus 28306 48%

Secured Loans 17267 29%

Unsecured Loans 7434 13%

Deferred Tax Liability 1744 3%

Total 59189 100%

Interpretation

From the above table of the total funds employed of Rs.59189 lakhs. Funds 7% raise through

share capital 48% of the raise using reserves and surplus, 29% of the source from secured loans

and 13% funds from unsecured loans and 3% of the funds are raised by deferred tax liability

further it is inferred that majority of the funds has been used in the form of reserves and surplus.

Graph 11

45

Share Capital Reserves and Surplus Secured Loans Unsecured Loans Deferred Tax Liability0%

10%

20%

30%

40%

50%

60%

Percentage

Percentage

Table showing sources of funds during the year 2009-2010

Particulars Amount (in lakhs) Percentage

46

Share Capital 4439 6%

Reserves and Surplus 39178 55%

Secured Loans 18811 26%

Unsecured Loans 6978 10%

Deferred Tax Liability 2471 3%

Total 71877 100%

Interpretation

From the above table of the total funds employed of Rs. 71877 lakhs funds 6% raise

through share capital 55% of the funds are raise through Reserves and Surplus, 26% of the

source from Secured loans and 3% of the fund are raised by Deferred Tax Liability further it is

inferred that majority of the funds has been used in the form of Reserves and Surplus.

Graph 12

47

Share Capital Reserves and Surplus

Secured Loans Unsecured Loans

Deferred Tax Liability

0%

10%

20%

30%

40%

50%

60%

Percentage

Percentage

Table Showing Sources of Funds during the year 2010-2011

Particulars Amount (in lakhs) Percentage

48

Share Capital 4439 6%

Reserves and Surplus 50685 68%

Secured Loans 11676 16%

Unsecured Loans 5865 8%

Deferred Tax Liability 1818 2%

Total 74483 100%

Interpretation

From the above table of the total funds employed of Rs.74483 lakhs. Funds 6%

of funds are raised through Share Capital 68% of the raise using Reserves and Surplus, 16% of

the sources from Secured Loans and 8% funds from Unsecured and 2% of the funds are raised

by Deferred Tax Liability further it is inferred that majority of the funds has been used in the

form of Reserves and Surplus.

Graph 13

49

Share Capital Reserves and Surplus Secured Loans Unsecured Loans Deferred Tax Liability0%

10%

20%

30%

40%

50%

60%

70%

80%

Percentage

Percentage

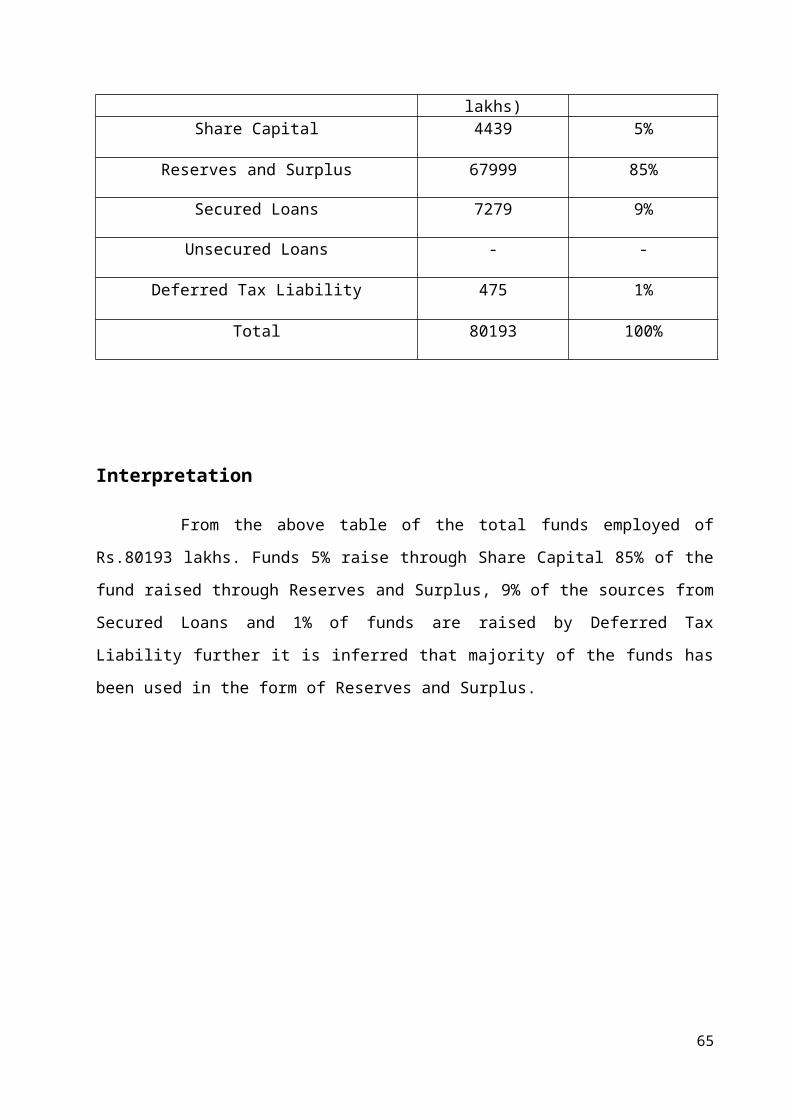

Table Showing Sources of Funds during the year 2011-2012

50

Particulars Amount (in lakhs) Percentage

Share Capital 4439 5%

Reserves and Surplus 67999 85%

Secured Loans 7279 9%

Unsecured Loans - -

Deferred Tax Liability 475 1%

Total 80193 100%

Interpretation

From the above table of the total funds employed of Rs.80193 lakhs. Funds 5%

raise through Share Capital 85% of the fund raised through Reserves and Surplus, 9% of the

sources from Secured Loans and 1% of funds are raised by Deferred Tax Liability further it is

inferred that majority of the funds has been used in the form of Reserves and Surplus.

Graph 14

51

Table Showing Sources of Funds during the year 2012-2013

52

Share Capital Reserves and Surplus Secured Loans Unsecured Loans Deferred Tax Liability0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Percentage

Percentage

Particulars Amount (in lakhs) Percentage

Share Capital 4439 6%

Reserves and Surplus 47142 62.5%

Secured Loans 16054 21%

Unsecured Loans 2637 3.5%

Deferred Tax Liability 5255 7%

Total 75527 100%

Interpretation

From the above table of the total funds employed of Rs.75527 lakhs. Funds 6%

raise through Share Capital 62.5% of the fund raised through Reserves and Surplus, 21% of the

sources from Secured Loans,3.5% of funds was raised through from Unsecured Loans and 7%

of funds are raised by Deferred Tax Liability further it is inferred that majority of the funds has

been used in the form of Reserves and Surplus.

Graph 15

53

Share Capital Reserves and Surplus Secured Loans Unsecured Loans Deferred Tax Liability0%

10%

20%

30%

40%

50%

60%

70%

Percentage

Percentage

4.4 Cost of Capital

In order to run and manage a company funds are needed, right from the promotional stage

up to end, finance play a vital role in a company’s life, if the funds are adequate the business

suffers and if the funds are not properly managed, it is therefore, necessary that correct estimates

54

of the current and further need of capital be made to have an optimum Capital Structure, which

shall help the organization to run the work smoothly and without any stress.

Overall Cost of Capital

KO= EBIT / V

EBIT – Earning before Interest and Tax

V = S + B

Value of the Firm = Value of Equity + Value of Debt

Table Showing Net Income Approach during the year 2008-2009

Particulars Amount (RS. In Lakhs)

Value Share (S) 23257

Market Value of the bond(B) 29168

Value of the Firm (V=S+B) 52425

Earnings before interest and Tax 13672

Overall Cost of Capital 0.26%

Interpretation

From the above table, Value of the Firm is Rs.52425; the overall Cost of Capital is 0.26%.

Graph 16

55

Value Sh

are (S)

Market V

alue o

f the b

ond(B)

Value o

f the Fi

rm (V=S+B)

Earnings b

efore i

nterest a

nd Tax

Overall C

ost of Capital

0100002000030000400005000060000

Amount (RS. In Lakhs)

Amount (RS. In Lakhs)

Table Showing Net Income Approach during the year 2009-2010

56

Particulars Amount (RS. In Lakhs)

Value Share (S) 32744

Market Value of the bond(B) 26445

Value of the Firm (V=S+B) 59189

Earnings before interest and Tax 17608

Overall Cost of Capital 0.29%

Interpretation

From the above table, Value of the Firm is Rs.59189; the overall Cost of Capital is 0.29%.

Graph 17

57

Value Sh

are (S)

Market V

alue o

f the b

ond(B)

Value o

f the Fi

rm (V=S+B)

Earnings b

efore i

nterest a

nd Tax

Overall C

ost of Capital

0

10000

20000

30000

40000

50000

60000

70000

3274426445

59189

17608

0.0029

Amount (RS. In Lakhs)

Table Showing Net Income Approach during the year 2010-2011

58

Particulars Amount (RS. In Lakhs)

Value Share (S) 43617

Market Value of the bond(B) 28260

Value of the Firm (V=S+B) 71877

Earnings before interest and Tax 22244

Overall Cost of Capital 0.30%

Interpretation

From the above table, Value of the Firm is Rs.71877; the overall Cost of Capital is 0.30%.

Graph 18

59

Value S

hare (S)

Market V

alue o

f the b

ond(B)

Value o

f the F

irm (V=S+

B)

Earnings b

efore i

nterest

and Ta

x

Overall

Cost of Capital

01000020000300004000050000600007000080000

43617

28260

71877

22244

0.00300000000000001

Amount (RS. In Lakhs)

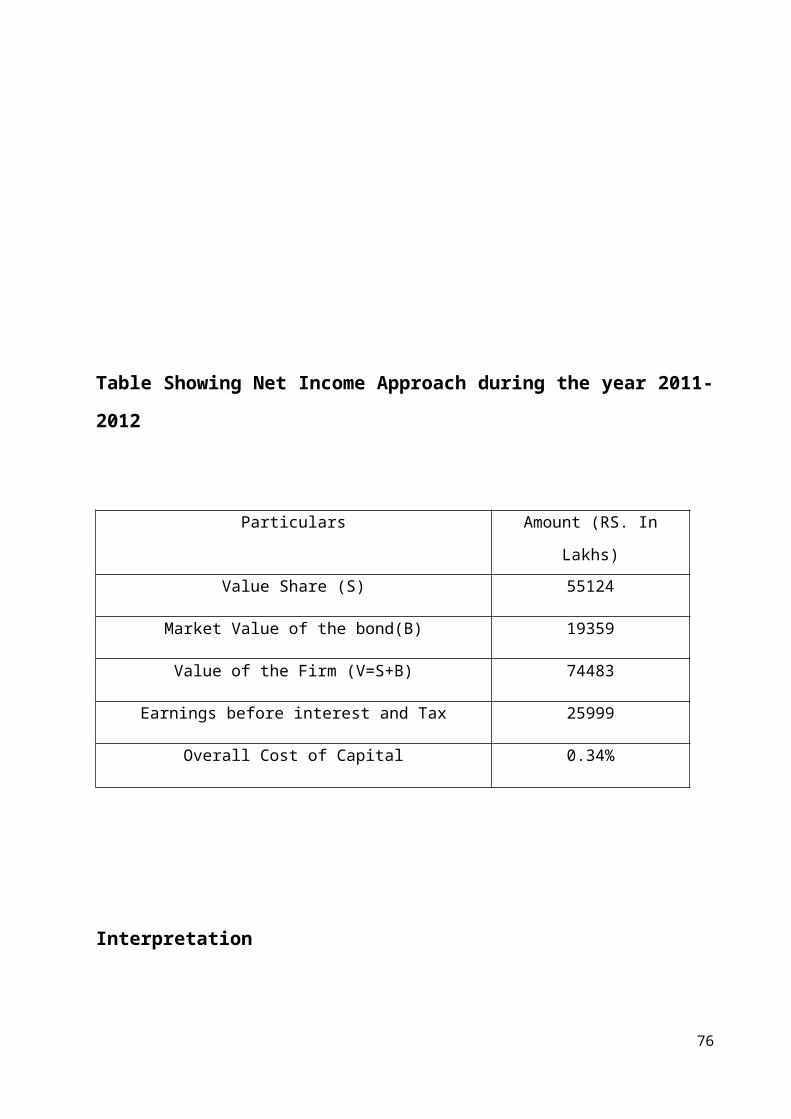

Table Showing Net Income Approach during the year 2011-2012

60

Particulars Amount (RS. In Lakhs)

Value Share (S) 55124

Market Value of the bond(B) 19359

Value of the Firm (V=S+B) 74483

Earnings before interest and Tax 25999

Overall Cost of Capital 0.34%

Interpretation

From the above table, Value of the Firm is Rs.74483; the overall Cost of Capital is 0.34%.

Graph 19

61

Value S

hare (S

)

Market

Value o

f the b

ond(B)

Value o

f the F

irm (V

=S+B)

Earnings

before

interest

and Ta

x

Overall

Cost of C

apita

l0

1000020000300004000050000600007000080000

55124

19359

74483

25999

0.00340000000000002

Amount (RS. In Lakhs)

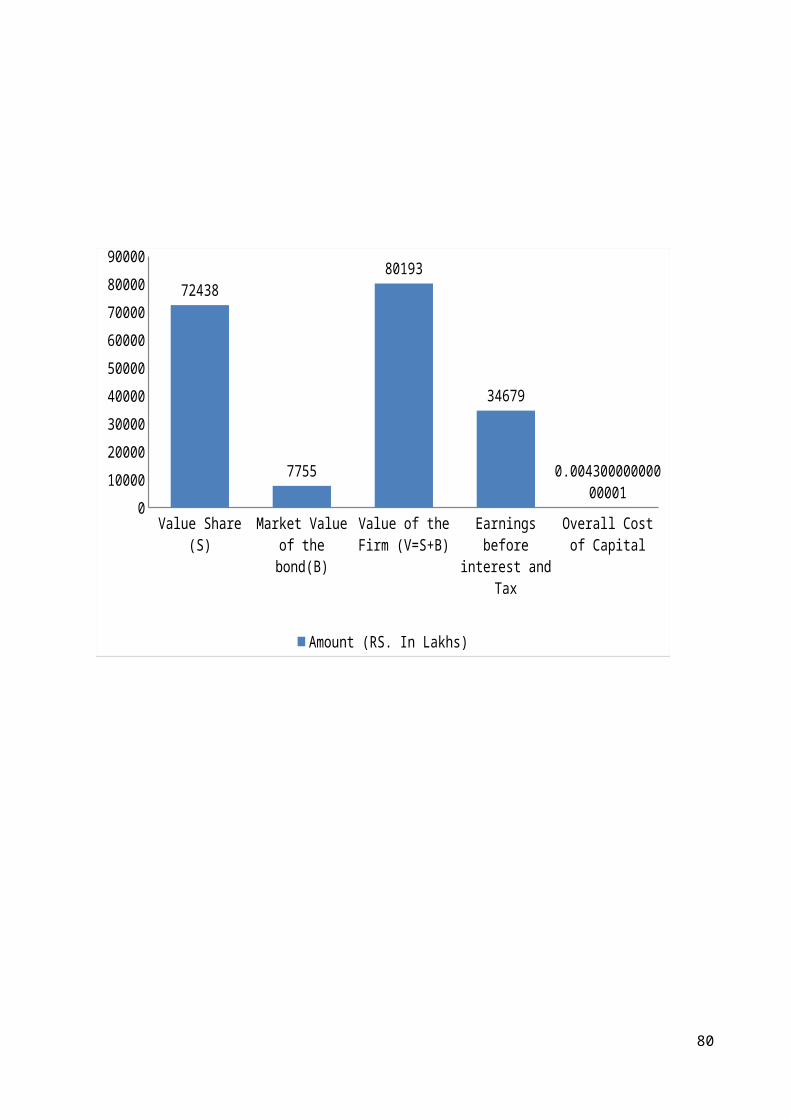

Table Showing Net Income Approach during the year 2012-2013

62

Particulars Amount (RS. In Lakhs)

Value Share (S) 72438

Market Value of the bond(B) 7755

Value of the Firm (V=S+B) 80193

Earnings before interest and Tax 34679

Overall Cost of Capital 0.43%

Interpretation

From the above table, Value of the Firm is Rs.80193; the overall Cost of Capital is 0.43%.

Graph 20

63

Value S

hare (S)

Market V

alue o

f the b

ond(B)

Value o

f the F

irm (V=S+

B)

Earnings b

efore i

nterest

and Ta

x

Overall

Cost of Capital

0100002000030000400005000060000700008000090000

72438

7755

80193

34679

0.00430000000000001

Amount (RS. In Lakhs)

Table Showing Net Operating Income Approach during the year 2009-2013

64

Year Cost of Capital Value of the Firm

2009 0.26% 52425

2010 0.29% 59189

2011 0.30% 71877

2012 0.34% 74483

2013 0.43% 80193

Interpretation

From the above table showing that the overall Cost of Capital is very low 0.26% in the year

2009 and value of the firm were Rs. 52425. But it started growing and reached 0.43% and

Rs.80193.

Graph 21.1

65

2009 2010 2011 2012 20130.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

0.50%

Cost of Capital

Cost of Capital

Graph 21.2

66

2009 2010 2011 2012 2013

5242559189

71877 7448380193

Value of the FirmValue of the Firm

4.4 Trend Analysis

67

Trend Analysis of sales = Sales of the Year / Total Sales * 100

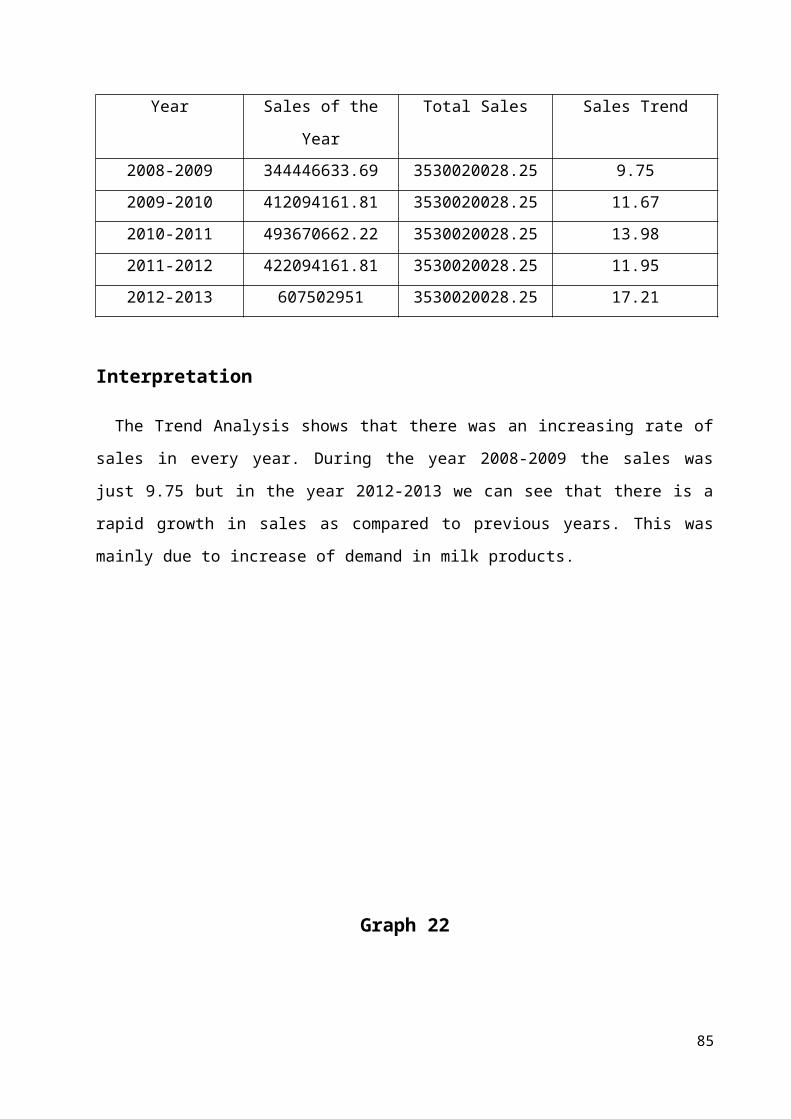

Table showing Trend Analysis in Sales

Year Sales of the Year Total Sales Sales Trend

2008-2009 344446633.69 3530020028.25 9.75

2009-2010 412094161.81 3530020028.25 11.67

2010-2011 493670662.22 3530020028.25 13.98

2011-2012 422094161.81 3530020028.25 11.95

2012-2013 607502951 3530020028.25 17.21

Interpretation

The Trend Analysis shows that there was an increasing rate of sales in every year. During the

year 2008-2009 the sales was just 9.75 but in the year 2012-2013 we can see that there is a rapid

growth in sales as compared to previous years. This was mainly due to increase of demand in

milk products.

Graph 22

68

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

2

4

6

8

10

12

14

16

18

20

Sales Trend

Sales Trend

5. FINDINGS, SUGGESTIONS AND CONCLUSION

69

5.1 Findings

Debt Equity Ratio indicates the average position of the firm. It shows .929% in the year 2009

and in the year 2013 it shows .30% low level.

Interest Coverage Ratio in the year 2009 was 16.81% and 2012 shows the low level of 6.39%

and it shows high level in 2013 of 21.27%.

Debtor’s Turnover Ratio indicates the increasing year to year. It shows 66.20% in the year

2013 which shows the good position of the firm.

The Gross Profit Ratio is increasing year to year. The highest ratio is 7.70% during the year

2013. The lowest ratio is .958% during the year 2011.

The Net Profit Ratio is high in the year 2013 at 1.58%. In 2011 Net Profit declined at -

2.169% and in the year 2009, 2012 the ratio is very low at -1.578% and -1.470% respectively.

The Degrees of Financial Leverage in the year 2009 were increased to 1.22%. In the 2013 it

shows decreasing of 1.07%.

The Operating Leverage indicates increase in the year 2009 with 3.07% and in the year 2013

it shows decreasing of 1.80% which indicates low position of the firm.

The Combined Leverage shows the highest in the year 2009 at 3.74%. But in the year 2013 it

decreased to 1.92%.

The sources of funds are increasing year by year. The highest source of funds during the year

2012 was 80193 and lowest in the year 2009 of 59189.

Net Income Approach shows the low rate of .26% during the year 2009. But in the year 2013

it shows 0.43% which indicates the good position of the firm.

5.2 Suggestions

In order to overcome the problems of Long term Solvency, Profitability and Leverage

position, Cost of Capital is suggested to follow.

70

The company’s current financial position is not so good, so they have to take much care

about decision regarding capital.

Motivating the employees in the organization is beneficial to the company.

The financial leverage is low, so it must be increased in future.

The sources of funds increasable it must be increasing in future.

Through reducing the Cost of Capital, the company can gain a lot.

5.3 Conclusion

Capital Structure is the key indicator to determine the position of an organization. It

can reduce the loss of wastage through effectively controlling Cost of Capital. In this study of

71

Milma Dairy it found that they are concentrating on the Cost of Capital analysis and maintaining

it.

The employees can be rewarded and they motivated and they may work truthfully for

the organization. So the Capital Structure may be normally increased by their effective work.

Profits are essential, but it would be wrong to assume that every action initiated by the

management of the company should be aimed at maximization of profits. It enhances the

goodwill of the company; stakeholders evaluate the performance of the company on the basis of

the profits. So that the Capital Structure and Cost of Capital analysis is necessary.

The thing is that, the company is giving more importance to the welfare of employees,

the company is basically a service oriented industry, and in such a way they are providing

quality goods and services rather than making profits.

APPENDIX

TRCMPU

72

Final Audit 2008-2009

Manufacturing and Trading Account for the year ended 31-2-2009

Sl.

No

Particulars Amount Sl.

No

Particulars amount

1. Purchase &

Consumption

106945938.29 1. Sales – Milk &

Products

228626306.29

2. Consumption of other

materials

210374.67 2. Sales by Transfer 15570571.80

3. Stock transfer in 207272568.17 3. Other Sales 249755.60

4. Freight / Carriage

Taxes & insurance

5076085.38

5. Wages & Allowance 4510831.38

6. Manufacturing

expenses

10341557.61

7. Procurement & Input

Charges

687048.12

8 Selling Expenses 5876111.19

Total 340920514.83 Total 344446633.69

Gross Profit 3526118.86

Grand Total 344446633.69 Grand Total 344446633.69

TRCMPU LTD

Final Audit 2009-2010

Manufacturing and Trading Account for the year ended 31-3-2010

73

Sl.

No

Particulars Amount Sl.

No

Particulars Amount

1. Raw Material

Consumed

119973693.59 1. Sales – Milk &

Products

272449735.91

2. Consumption of other

materials

346136.29 2. Sales by Transfer 139266692.88

3. Stock transfer in 251299833.27 3. Other Sales 377733.02

4. Freight / Carriage

Taxes & insurance

6250179.82

5. Wages & Allowance 6290760.88

6. Manufacturing

expenses

10816213.61

7. Procurement & Input

Charges

1838389.74

8 Selling Expenses 6914674.25

9. Taxes & Insurance 72867.00

Total 403802748.45 Total 412094161.81

Gross Profit 8291413.38

Grand Total 412094161.81 Grand Total 412094161.81

TRCMPU LTD

Final Audit 2010-2011

Manufacturing & Trading Account for the year ended 31-3-2011

74

Sl.

No

Particulars Amount Sl.

No

Particulars Amount

1. Raw Material

Consumed

151139165.10 1. Sales – Milk &

Products

324973460.97

2. Consumption of other

materials

229560.39 2. Sales by Transfer 168393118.14

3. Stock transfer in 295497727.96 3. Other Sales 1015730.63

4. Freight / Carriage

Taxes & insurance

7375030.39

5. Wages & Allowance 5536543.65

6. Manufacturing

expenses

11326195.57

7. Procurement & Input

Charges

9748261.62

8 Selling Expenses 9056296.93

9. Taxes & Insurance 46729.00

Total 489955511.02 Total 494686392.85

Gross Profit 4730881.83

Grand Total 494686392.85 Grand Total 494686392.85

TRCMPU LTD

Final Audit 2011-2012

Manufacturing and Trading Account for the year ended 31-3-2012

75

Sl.

No

Particulars Amount Sl.

No

Particulars Amount

1. Raw Material

Consumed

119976193.59 1. Sales – Milk &

Products

282449735.91

2. Consumption of other

materials

348636.29 2. Sales by Transfer 139266692.88

3. Stock transfer in 251299833.27 3. Other Sales 377733.02

4. Freight / Carriage

Taxes & insurance

6250179.82

5. Wages & Allowance 6290760.88

6. Manufacturing

expenses

10816213.61

7. Procurement & Input

Charges

1838389.74

8 Selling Expenses 6914674.25

9. Taxes & Insurance 72867.00

Total 403807748.45 Total 422094161

Gross Profit 18286413.36

Grand Total 422094161.81 Grand Total 422094161

TRCMPU LTD

Final Audit 2012-2013

Manufacturing and Trading Account for the year ended 31-3-2013

76

Sl.

No

Particulars Amount Sl.

No

Particulars Amount

1. Raw Material

Consumed

125368473.5 1. Sales – Milk &

Products

354561850.5

2. Consumption of other

materials

385544.5 2. Sales by Transfer 252541100.5

3. Stock transfer in 282545584.75 3. Other Sales 4000000.00

4. Freight / Carriage

Taxes & insurance

6250179.25

5. Wages & Allowance 6980000.00

6. Manufacturing

expenses

11500000.80

7. Procurement & Input

Charges

2512415.50

8 Selling Expenses 6914674.70

9. Taxes & Insurance 85000.00

Total 442541873.00 Total 607502951.00

Gross Profit 164961078.00

Grand Total 607502951.00 Grand Total 607502951.00

TRCMPU LTD

Final Audit 2008-2009

Profit & Loss Account for the year ended 31-3-2009

77

Sl.

No.

Particulars Amount Sl.

No.

Particulars Amount

1. Salaries and other

benefits

3854412.16 1. Gross Profit b/d 3526118.86

2. Administrative

Expenses

564541.18 Miscellaneous Income 169130.25

3. Miscellaneous

Expenses

3918442.40

4. Depreciation & other

services

469722.97

5. Interest on

Borrowings

323242.00

Total 9130366 Total 3698249.11

Net Loss 5435117.60

Grand Total 9130366.71 Grand Total 9130366.71

TRCMPU LTD

Final Audit 2009-2010

Profit & Loss Account for the year ended 31-3-2010

78

Sl.

No

.

Particulars Amount Sl.

No

.

Particulars Amount

1. Salaries and other

benefits

7376868 1. Gross Profit b/d 8449929.31

2. Administrative

Expenses

619513.88 Miscellaneous Income 196699.39

3. Miscellaneous

Expenses

4825591.06

4. Depreciation & other

services

1185325.27

5. Interest on

Borrowings

-

Total 14707294.28 Total 8646628.70

Net Loss 6060665.58

Grand Total 14707294.28 Grand Total 14707294.28

TRCMPU LTD

Final Audit 2010-2011

Profit & Loss Account for the year ended 31-3-2011

79

Sl.

No.

Particulars Amount Sl.

No.

Particulars Amount

1. Salaries and other

benefits

6891506.23 1. Gross Profit b/d 4730881.33

2. Administrative

Expenses

972056.37 Miscellaneous Income 171694.46

3. Miscellaneous

Expenses

5821591.22

4. Depreciation & other

services

1227541.84

5. Interest on Borrowings 699996.00

Total 15612691.66 Total 492576.29

Net Loss 10710115.37

Grand Total 15612691.66 Grand Total 15612691.66

TRCMPU LTD

Final Audit 2011-2012

Profit & Loss Account for the year ended 31-3-2012

80

Sl.

No.

Particulars Amount Sl.

No.

Particulars Amount

1. Salaries and other

benefits

7376868 1. Gross Profit b/d 18286413.36

2. Administrative

Expenses

619513.88 Miscellaneous Income 196699.39

3. Miscellaneous

Expenses

4825591.06

4. Depreciation & other

services

1185325.27

5. Interest on

Borrowings

699996.00

Total 14707294.28 Total 18483112.75

Net Profit 3775818.47

Grand Total 18483112.75 Grand Total 18483112.75

TRCMPU LTD

Final Audit 2012-2013

Profit & Loss Account for the year ended 31-3-2013

81

Sl.

No.

Particulars Amount Sl.

No.

Particulars Amount

1. Salaries and other

benefits

8850250.00 1. Gross Profit b/d 164961078.00

2. Administrative

Expenses

700000.50 2. Miscellaneous Income 300000.00

3. Miscellaneous

Expenses

5200000.00

4. Depreciation & other

services

200000.50

5. Interest on Borrowings 700000.00

Total 15650251.0 Total 165261078.00

Net Profit 149610827.00

Grand Total 165261078.00 Grand Total 165261078.00

TRCMPU LTD

Final Audit 2008-2009

Balance Sheet as on 31-3-2009

82

At the

begin

ning

of the

year

Particulars At the end of

the year 31-3-

2009

At the

begin

ning

of the

year

Particulars At the end of

the year 31-3-

2009

0 Borrowings 3314097.00 0 Cash in Hand 56414.59

0 Adjusting heads due

by

1106042.36 0 Cash at Bank 218779.65

0 Inter unit accounts

due by

107763809.96 0 Adjusting Head due

to

285291.86

0 Funds, Reserves &

Provisions

3567417.08 0 Inter unit Accounts

due to

100185695.48

0 Closing Stock 1711896.80

Fixed Assets 7858170.42

Net Loss 5435117.60

115751366.40 115751366.40

TRCMPU LTD

Final Audit 2009-2010

Balance Sheet as on 31-3-2010

83

Previous

year 31-3-

2008

Particulars At the end

of the year

31-3-2010

Previous

year 31-3-

2008

Particulars At the end

of the year

31-3-2010

3314097.00 Borrowings 2631944 56414.59 Cash in Hand 54702.22

1106042.36 Adjusting heads

due by

5585998.93 218779.65 Cash at Bank 942364.15

107763809.

96

Inter unit

accounts due by

232639939.

92

285291.86 Adjusting Head

due to

1357410.28

3567417.08 Funds, Reserves

& Provisions

4752742.35 100185695.

48

Inter unit

Accounts due to

1357410.28

1711896.80 Closing Stock 214375813.

62

5435117.60 Fixed Assets 2224525.33

Net Loss 6060665.58

Loss of the year 5435117.60

245610625.

20

245610625.

20

TRCMPU LTD

Final Audit 2010-2011

Balance Sheet as on 31-3-2011

84

Previous

year 31-3-

2009

Particulars At the end

of the year

31-3-2011

Previous

year 31-3-

2009

Particulars At the end

of the year

31-3-2011

2631944 Borrowings 1687048.00 54702.22 Cash in Hand 23368.71

5585998.93 Adjusting heads

due by

3325480.33 942364.15 Cash at Bank 3237268.65

232639939.

92

Inter unit

accounts due by

5980284.19 1357410.28 Adjusting Head

due to

3877485.31

4752742.35 Funds, Reserves

& Provisions

36816983.7

2

1357410.28 Inter unit

Accounts due to

483796.06

214375813.

62

Closing Stock 2534507.58

2224525.33 Fixed Assets 15304809.4

2

6060665.58 Net Loss 10710115.3

7

5435117.60 Loss of the year 11638445.1

4

47809796.2

4

47809796.2

4

TRCMPU LTD

Final Audit 2011-2012

Balance Sheet as on 31-3-2012

85

Previous

year 31-3-

2011

Particulars At the end

of the year

31-3-2012

Previous

year 31-3-

2011

Particulars At the end

of the year

31-3-2012

1687048.00 Borrowings 1687048.00 54702.22 Cash in Hand 23368.71

3325480.33 Adjusting heads

due by

3325480.33 942364.15 Cash at Bank 18651532.2

6

5980284.19 Inter unit

accounts due by

36816983.7

2

1357410.28 Adjusting Head

due to

3877485.31

36816983.7

2

Funds, Reserves

& Provisions

5980284.19 1357410.28 Inter unit

Accounts due to

483796.06

Net Profit 3775818.47 214375813.

62

Closing Stock 2534507.58

2224525.33 Fixed Assets 15304809.4

2

5435117.60 Loss of the year 10710115.3

7

51585614.7

1

51585614.7

1

TRCMPU LTD

Final Audit 2012-2013

Balance Sheet as on 31-3-2013

86

Previous

year 31-3-

2012

Particulars At the end

of the year

31-3-2013

Previous

year 31-3-

2012

Particulars At the end

of the year

31-3-2013

1687048.00 Borrowings 1885645 23368.71 Cash in Hand 25000

3325480.33 Adjusting heads

due by

3520465.5 18651532.2

6

Cash at Bank 19025550

36816983.7

2

Inter unit

accounts due by

41580615 3877485.31 Adjusting Head

due to

4512255.15

5980284.19 Funds, Reserves

& Provisions

6280250 483796.06 Inter unit

Accounts due to

584235.85

3775818.47 Net Profit 149610827 2534507.58 Closing Stock 2815350.5

15304809.4

2

Fixed Assets 175915411

202877802.

5

202877802.

5

6.BIBLIOGRAPHY

Financial Management by M.Y Khan & P.K Jain, Tata McGraw Hill Publishing Co. Ltd,

1997.

Principles of Management Accounting by Dr. S.N Maheswari, Sultan Chand & Sons, 1995.

87

Financial Management by I.M Pandey, Vikas Publishing House Pvt Ltd, 1995.

Financial Management by Prasanna Chandra, Tata McGraw Hill Publishing Co. Ltd, 1995.

Cost and Management Accounting by S.N Maheswari, Sultan Chand & Sons, 1996.

Cost Accounting by Jain & Narang, Kalyani Publishing, New Delhi, 1997.

Websites

http//www.google.com

http//www.wikipedia.com

88