Airport PPPs: Benefits, drivers, and success factors January 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Airport PPPs: Benefits, drivers, and success factors

January 22, 2015

Contents

1. WBG Overview

2. Airport PPPs

3. Lessons Learned & Getting PPPs Right

4. WBG Experience in Airports PPPs

2

1 – World Bank Group Overview

IBRD International Bank for

Reconstruction and Development

IDA International Development

Association

MIGA Multilateral Investment and Guarantee Agency

Est. 1945 Est. 1960

IFC International Finance

Corporation

Est. 1956 Est. 1988

Role:

Clients:

Products:

Shared Mission: To Promote Economic Development and Reduce Poverty

To promote institutional, legal and regulatory reform

To promote institutional, legal and regulatory reform

To promote private sector development

To reduce political investment risk

Governments of member countries with per capita income between $1,025 and $6,055.

Governments of poorest countries with per capita income of less than $1,025

Private companies and governments in member countries

Foreign investors in member countries

Technical assistance Loans Policy Advice

Technical assistance Interest Free Loans Policy Advice

Equity/Quasi-Equity Long-term Loans Risk Management Advisory Services

Political Risk Insurance

4

WBG partner of choice in PPPs

350

Global market knowledge and experience as both advisor and investor

projects since 1989

Objectivity & transparency in transactions

Neutral partner balancing objectives of government, consumers and investors

Only multilateral organization offering direct advisory services to governments globally

Social and environmental focus

Risk sharing and long-term commitment

Pioneering transactions in frontier markets & sectors

5

Full spectrum of support from upstream policy, advisory, public financing,

private financing (debt and equity), guarantees, PRI, and mobilization

2 - Airport PPPs

PPP Variants in Airports

7

Technical Assistance

Service Contract

Management Contract

Lease Contract

Concession Contract

3-5 yrs 5-15 yrs

1-3 yrs

25-30 yrs

Priv

ate

Sect

or In

volv

emen

t

Contract Duration

Siemens-LGW

Baggage Handling contract

ADP-Egyptian Regional Airports

/ Fraport-Cairo &

KAIA/KKIA airports

TAV-Izmir Airport

Concession Lease

TAV-Madinah Airport

/ GMR-Delhi

Airport

Vinci – ANA (Portuguese

Airports)

MAHB – Astana Airport

Full Divestiture

Airport PPPs benefit Governments

Construction Significant reduction in

project development risk with transfer of

construction risk to the private sector

Financing Access to private sector

financing, freeing government budgets for

social sectors

Efficiencies Introducing operational efficiencies with best in

class international practices

Public Sector Benefits

Revenues Potential for new revenue

streams for governments/airport

authorities

O&M Transfer of risks related to

Operations and Maintenance with clear KPIs and performance

incentives

8

Asset Transfer Airport and related

developments return to public sector ownership at the end of the concession

Airports are also attractive Assets for Private Sector

Strong growth Forecasted growth leading to potential for significant cash flow and improved

margins

Efficiencies Significant ability to

introduce operational efficiencies and improve

financial performance

Opportunities Opportunities to develop real estate, commercial and auxiliary activities

outside of the regulated perimeter

Attractive Assets for Private Sector

Exchange rate risk Low foreign exchange risks

as airports generate substantial revenues in

hard currency

Commercial Revenues

High potential for improving airport amenities

thereby increasing non- regulated revenues

9

Private Investment in Airports

10

• Private investment in airports is on the rise again

post the 2007-2010 period where sector activity waned due to lack of financing, traffic concerns, and gaps in valuation expectations.

• Fundraising for infrastructure deals has remained positive, and as of early 2014, there are 136 unlisted funds targeting $86bn in capital commitments.

• Investors are likely to look to emerging markets where expected returns are higher than in developed markets.

Source: Private Participation in Infrastructure Database (World Bank)

Source: Preqin, 2013 Infrastructure Raising and Deals 10

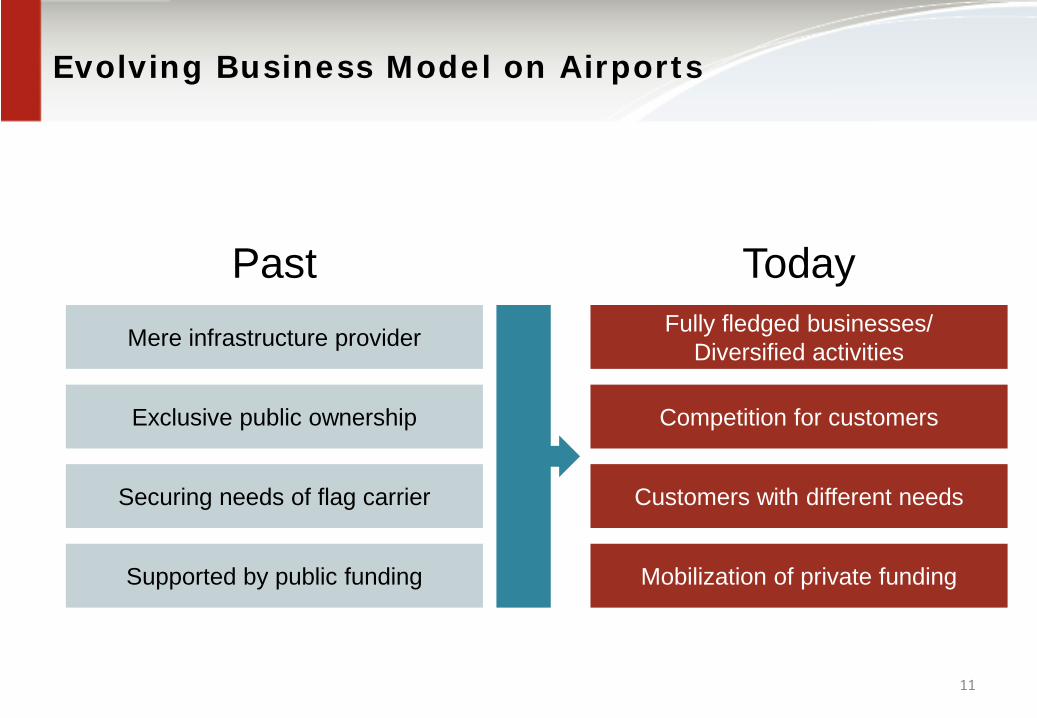

Evolving Business Model on Airports

Past Today Mere infrastructure provider

Exclusive public ownership

Securing needs of flag carrier

Supported by public funding

Fully fledged businesses/ Diversified activities

Competition for customers

Customers with different needs

Mobilization of private funding

11

Key Sector Players

12

• Traditional players - Infrastructure funds; - Construction firms (on

greenfield or brownfield expansion).

• New players

- Direct investments by pension funds with increasing focus on emerging markets;

- Sovereign wealth funds; - Private equity; - Operator / financial institution

consortiums; and, - Private equity (smaller airports

c. <5m pax).

Global financial crisis has led to an adjustment in mix of airport investors.

Key Air Traffic Drivers

13

09 27

Competition

Rise of LCCs or foreign

carriers can increase

affordability and route

options which drives

traffic

Hub Status

Small countries

with high air connectivity

due to airport hub

status boosts traffic

potential (eg: Sing.,

UAE)

Economic Health

Higher

personal income and growth of economy (ie: GDP)

Demographic Changes

Growing

population can raise

propensity to fly

Market Maturity

Increasing maturity

eventually leads to

saturation

Crises

Financial crisis or war / terrorism

dampens air traffic

Geography

Need for air transport higher in

island nations or

isolated regions with

big distances between

cities

Population Mix

Countries with high immigrant population see large visiting

friends and relative

(VFR) traffic (e.g: UAE)

What are the revenue streams?

Aeronautical Non-Aeronautical

Landing Fees

Terminal Area Air Navigation Fee

Aircraft Parking & Hangar Charges

Airport Noise Charge

Passenger Service Charge

Security Charge

Ground Handling Charges

En Route Air Navigation Fee

Night flight fees

Concession fees for Aviation Fuel & Oil

Concession fees for Commercial Activities

Revenues from Car Parking & Car Rentals

Rental of Airport Land, Space in Buildings &

Assorted Equipment

Fees charged for Airport Tours, Admissions

etc.

Other non-airport Revenues

Note: new charges can be envisaged in the case of projects with major expansion works to match revenue flow levels with private sector return requirements (subject to regulatory framework of country where airport is being developed)

14

Common Structuring Issues (1/3)

Issue Description

Contract Type Concession (BTO, BOT etc), Management contract, TSA; choice will depend on requirements leveled on private partner, government preference, accounting / regulatory issues etc.

Project Scope Full scope (all of airside and landside including commercial developments), only airside activities, limited to one terminal etc.

Investment obligations

Expansion / rehabilitation requirements placed on investor at the beginning of contract + future expansion requirements with appropriate trigger mechanisms

Contract Term Driven by concession type (ie: 15-25 years for concession, 3-5 years management contract, etc), and financial return requirements

Basis for bidding Weighting and defining components of technical and financial bid (ie: input vs. output based design, upfront fees vs. ongoing concession revenue sharing, pass/fail vs. scoring bids)

Regulatory regime

Regulated tariffs set by concession contract or through existing country wide regulatory framework

15

Common Structuring Issues (2/3)

Issue Description

Role of Grantor Define what role Grantor will play on project (eg: general facilitator, providing vacant enjoyment of land / site, security, ATC, etc.).

Exclusivity Specify any protection from existing airports or new airport developments with no compete clauses (eg: no new international airport within 200km radius)

Traffic risk Protection against traffic risk (ie: investor assumes 100% or protected below a certain traffic level)

Sponsor stability requirements

Define any minimal equity participations by individual investors at bid and lock in periods over contract term

Inflation Define tariff indexation level and frequency of adjustments

FX protection Potential requirement when local currency volatile and majority of financing is international (and / or bidders are international). Can be implemented through adjustments to aeronautical tariffs

16

Common Structuring Issues (3/3)

Issue Description

Performance Obligations

Define investor obligations throughout contract to adhere to service levels or standards (eg: IATA level C, minimum technical requirements) and penalties if breach occurs, through liquidated damages, performance bonds, and default clauses

Existing airport staff

Level of employment protection offered, requirements placed on investor to accept them over defined term and conditions

Governing law, arbitration

In most jurisdictions, international investors will have preference / requirement for non-local law and international arbitration

Termination Triggers and compensation levels for debt and equity on both grantor and investor sides needs to be defined

Conditions precedent

All conditions that need to be fulfilled by grantor and investor prior to financial close need to be clearly defined in the contract and monitored

17

Impact of PPP on Responsibilities

18

PRE-PPP PPP APPROACH

CAA / Govt

Airport Co*

Private Sector

CAA / Govt

Airport Co*

Private Sector

Revenues

-overflight / ATC -airport revenues** Payment to Govt / Airport Co + - + / + -

Capex / Staff / / Regulation Supervision Slot Coordination This allocation is one example amongst many and may vary from project to project depending on structure (eg: security staff provided by State or private operator, capex subsidies required, etc.)

* May be contained within CAA in certain countries ** Payment of operating costs also falls on private sector under concession model

3 – Lessons Learned & Getting PPPs Right

PPP = Preparation Preparation Preparation

20

• MUST prepare for the main stages of a PPP - Due Diligence; - Structuring; - Tendering; - Award / Closing; and - Implementation / Monitoring

• Each of the stages requires careful methodical preparation - short cuts are costly.

• Core to achieving a successful result is ensuring advisory team is highly experienced and

has all the required skill-sets (ie: financial, legal, technical, etc.) – even highly experienced global infrastructure investors do not rely solely on their in-house expertise to complete transactions.

• The following section illustrates issues that can arise and the important role advisors play in supporting clients to address these complexities.

Airport PPPs: some issues…

21

National security

Land acquisition

Environmental issues

Resettlement

Passengers vs. Cargo

Land value capture

Terminal design

Traffic Airside capex

Tourism Level of service

Domestic Competition

Exclusivity International Competition

Safety & Security

Customs

Immigration

Ground Handling

Retail concessions Fuel

Devaluation

Laws & Regulation

Concession fee

Subsidy

Zoning

Lenders Investors

Electricity

Water and Water Treatment

Sanitation

Ground transportation Road access

Lack of preparation leads to failure…

22

• Extensive analyses are ESSENTIAL (technical, commercial, financial, strategic) to test proposed structure with market and meet Govt’s objectives;

• Jump starting tender phase without preparation and structure is highly risky = almost guaranteed to fail.

• Structuring allows Govt’s to design a project based on their objectives, capabilities, risk appetite and market interest;

• Structuring reduces uncertainty for bidders and gets them to make proposals based on Govt’s needs, and at the highest value;

• Structuring reduces the temptation of accepting spontaneous offers, which may not provide best value for money for the Govt.

Preparation / Due Diligence: you can’t build a house from the roof up

Structuring: inadequate project structure raises risk profile for all

…as does weak framework, bankability…

23

Uncertainty or new framework raises project risk profile and lowers bid value.

Lack of government support / indecision leads to delays and conflict.

• Mismatch between risk / obligations and levels of return anticipated dilutes investor interest;

• Unrealistic demands set by public sector leads to failure in bids (eg: developing greenfield airport with no / weak traffic record).

Bankability: Fair & Appropriate Risk Allocation is Key

Commitment: Buy-In Critical At All Stages

Framework: Avoid Surprises

…and inadequate profiling of candidates along with absence of competition

24

• Competitive tension results in much better offers for public sector;

• Transparency from competitive tender improves credibility of process and public support.

• Pre qualification allows to retain the most appropriate profiles of candidates;

• Wrong candidate – inappropriate selection criteria is highly risky.

Partner Profile: Avoid Unqualified Candidates

Competition: Maximises Public Sector Gains

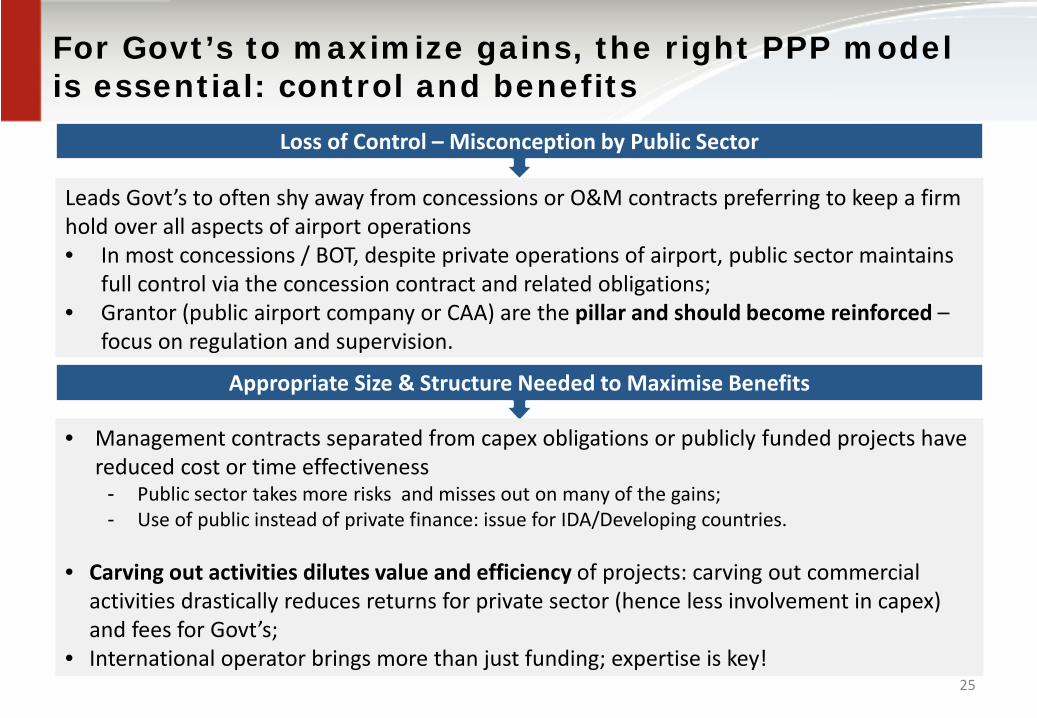

For Govt’s to maximize gains, the right PPP model is essential: control and benefits

25

Leads Govt’s to often shy away from concessions or O&M contracts preferring to keep a firm hold over all aspects of airport operations • In most concessions / BOT, despite private operations of airport, public sector maintains

full control via the concession contract and related obligations; • Grantor (public airport company or CAA) are the pillar and should become reinforced –

focus on regulation and supervision.

Loss of Control – Misconception by Public Sector

Appropriate Size & Structure Needed to Maximise Benefits

• Management contracts separated from capex obligations or publicly funded projects have reduced cost or time effectiveness - Public sector takes more risks and misses out on many of the gains; - Use of public instead of private finance: issue for IDA/Developing countries.

• Carving out activities dilutes value and efficiency of projects: carving out commercial

activities drastically reduces returns for private sector (hence less involvement in capex) and fees for Govt’s;

• International operator brings more than just funding; expertise is key!

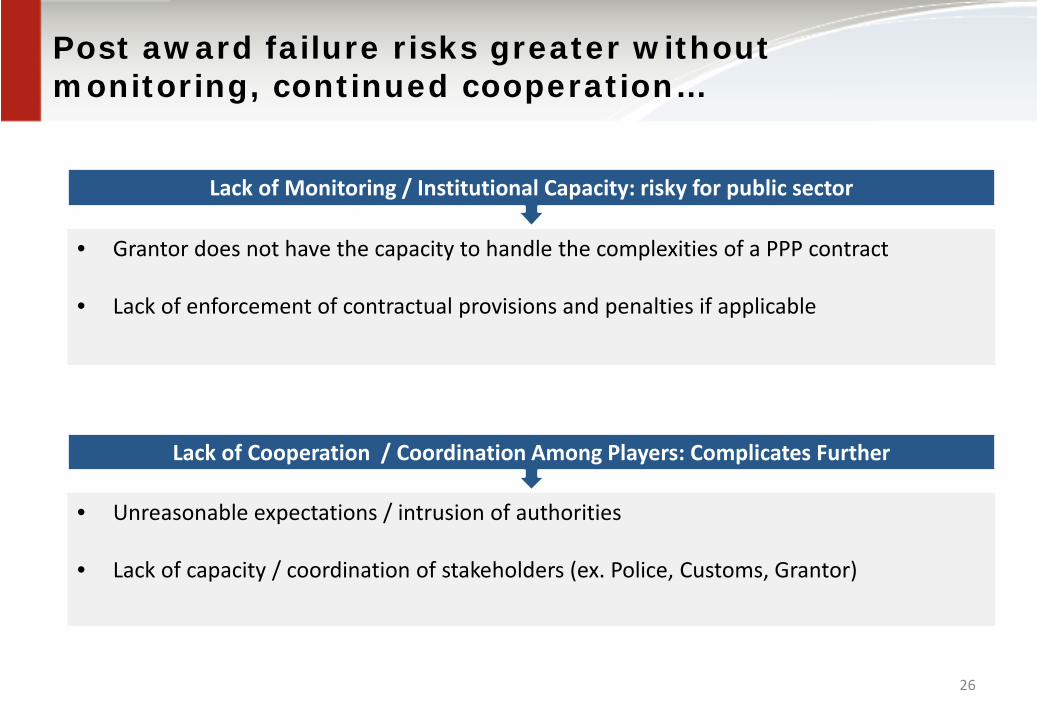

Post award failure risks greater without monitoring, continued cooperation…

26

• Unreasonable expectations / intrusion of authorities

• Lack of capacity / coordination of stakeholders (ex. Police, Customs, Grantor)

• Grantor does not have the capacity to handle the complexities of a PPP contract

• Lack of enforcement of contractual provisions and penalties if applicable

Lack of Monitoring / Institutional Capacity: risky for public sector

Lack of Cooperation / Coordination Among Players: Complicates Further

…or with poorly designed contracts containing inadequate provisions

27

• Lack of, or inadequate provisions on applicable laws, cure periods, step-in rights, etc.

• Lack of clarity on exit strategy

• Lack of clarity on obligations and contribution, guaranties

• Poorly conceived (or lack of) performance obligations and related penalties

• Lack of clarity on unforeseen events, force majeure, modification of plans or structure

Incomplete Contractual Provisions: Creates Sense of Unfairness

Inadequate dispute resolution mechanisms: Can Drag Disputes Longer

4 - WBG Experience: Investment and Advisory in Airports PPPs (Majority IFC)

Airport Credentials

29

Loan

Cambodia Airports ( Siem Reap and Phnom

Penh)

$27 ,500,000

IFC as Lender

Concession

Nnamdi Azikiwe International Airport,

Abuja, Nigeria

IFC mandated as Transaction Adviser

Concession

Prince Mohammad bin Abdulaziz Int’l Airport

in Madinah , Saudi Arabia

IFC mandated as Transaction Adviser

Loan

Tbilisi Airport in Georgia

$27,000,000

IFC as Lender

Equity Lima JCIAirport in Peru

$20,000,000

IFC as Investor

Loan Queen Alia Airport in

Jordan

$120,000,000 Loan

$160,000,000 Syndicated Loan

IFC Lender & Arranger

Loan Pulkovo Airport in

Russia

€ 70,000,000 Loan

€ 100,000,000 Syndicated Loan

IFC Lender & Arranger

Loan Montego Bay in Jamaica

$45,000,000 Loan

$45,000,000 Syndicated Loan

IFC Lender & Arranger

Loan TAV - Tunisia

€ 132,500,000 Loan

€ 257,500, 000 Syndicated Loan

IFC Lender & Arranger

Concession

Male International Airport in Maldives

IFC mandated as Transaction Adviser

Concession

Hajj Terminal at King Abdulaziz Int’l Airport

in Jeddah, Saudi Arabia

IF C mandated as Transaction Adviser

Concession

Queen Alia International Airport in Jordan

IFC mandated as Transaction Adviser

Related Documents

![HBO Divestiture Opportunity (DRAFT) September [8], 2009.](https://static.cupdf.com/doc/110x72/5a4d1b6a7f8b9ab0599b2a26/hbo-divestiture-opportunity-draft-september-8-2009.jpg)