TERMS OF USE Agricultural Foreign Trade Development 2012 Annual Report is a publication of the Bureau of Agricultural Statistics (BAS), Department of Agriculture. The BAS reserves exclusive right to reproduce this publication in whatever form. Should any portion of this publication be included in a report/article, the title of the publication and the BAS should be cited as the source of the data. The BAS will not be responsible for any information derived from the processing of data contained in this publication. ISSN-2012-0419 October 2013 Please direct technical inquiries to the Office of the Director Bureau of Agricultural Statistics Ben-Lor Building, 1184 Quezon Avenue Quezon City 1100 Philippines. Email: [email protected] Website: www.bas.gov.ph

Agri Foreign Trade2012

Dec 21, 2015

RP Agri Foreign Trade

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

TERMS OF USE Agricultural Foreign Trade Development 2012 Annual Report is a publication of the Bureau of Agricultural Statistics (BAS), Department of Agriculture. The BAS reserves exclusive right to reproduce this publication in whatever form. Should any portion of this publication be included in a report/article, the title of the publication and the BAS should be cited as the source of the data. The BAS will not be responsible for any information derived from the processing of data contained in this publication.

ISSN-2012-0419 October 2013

Please direct technical inquiries to the Office of the Director Bureau of Agricultural Statistics Ben-Lor Building, 1184 Quezon Avenue Quezon City 1100 Philippines. Email: [email protected] Website: www.bas.gov.ph

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

FOREWORD

The Agricultural Foreign Trade Development Report is an annual publication of the Bureau of Agricultural Statistics (BAS). This 23

rd edition presents a brief discussion

on the country’s overall agricultural trade performance in 2012. It summarizes the quarterly trade memos that are periodically provided to the Office of the Secretary, Department of Agriculture (DA). It features statistics on trade with the country’s trading partners, volume and value of top 10 agricultural exports and imports including the world prices of selected commodities. Data used in this report were sourced from the Foreign Trade Statistics of the National Statistics Office (NSO). The world price statistics were obtained from the Bangko Sentral ng Pilipinas (BSP) and the World Bank (WB). The BAS welcomes comments and suggestions from the data users and readers of this report.

ROMEO S. RECIDE Director

i 40

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

TABLE OF CONTENTS

Pages

FOREWORD ……………………………………………………………………………………………………. i TABLE OF CONTENTS ……………………………………………………………………………………… iii LIST OF TABLES ………………………………………………………………………………………………. iv LIST OF FIGURES …………………………………………………………………………………………….. vi HIGHLIGHTS ……………………………………………………………………………………………………. 1 OVERALL AGRICULTURAL TRADE …………………………………………………………….. 1 TOP AGRICULTURAL EXPORTS …………………………………………………………………. 2 TOP AGRICULTURAL IMPORTS …………………………………………………………………. 3 WORLD PRICES TRENDS …………………………………………………………………………… 4 STATISTICAL TABLES AND GRAPHS ………………………………………………………………….. 7

iii 38

0.00

0.50

1.00

1.50

2.00

2.50

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

Month

Figure 25 World Prices of Coconut Oil

January-December, 2011-2012

2012

2011

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

Month

Figure 29World Prices of Rice (5% broken) January- December, 2011-2012

2012

2011

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

Month

Figure 26 World Prices of Copra

January to December, 2011-2012

2012

2011

0.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

Month

Figure 27 World Prices of Sugar

January- December, 2011-2012

2012

2011

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

Month

Figure 30World Prices of Rice (25% broken)

January- December, 2011-2012

2012

2011

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

US

$/k

g

MonthFigure 28

World Prices of SoybeanJanuary - December, 2011-2012

2012

2011

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

LIST OF TABLES

Table No. Pages

1 SUMMARY OF PHILIPPINE AGRICULTURAL TRADE, 2010-2012 ….……… 9 1a PHILIPPINE AGRICULTURAL TRADE, BY QUARTER, 2011-2012 ………….. 10 2 AGRICULTURAL TRADE BALANCES WITH MAJOR TRADING PARTNERS OF THE PHILIPPINES, 2011-2012 ………………………………………………………. 11 3 QUANTITY AND VALUE OF PHILIPPINE AGRICULTURAL EXPORTS BY COMMODITY GROUP, 2011-2012 ………………….…………………………….. 12 4 TOP TEN PHILIPPINE AGRICULTURAL EXPORTS, 2011-2012 ………………. 14 4a VALUE OF TOP TEN AGRICULTURAL EXPORTS, BY QUARTER, 2011-2012 …………….……………………………………………………. 15 5 MAJOR MARKETS OF TOP TEN PHILIPPINE AGRICULTURAL EXPORTS, 2012 …………………………………………………………………………………. 16 6 QUANTITY AND VALUE OF PHILIPPINE AGRICULTURAL IMPORTS BY COMMODITY GROUP, 2011-2012 ………………………………………………… 20 7 TOP TEN AGRICULTURAL IMPORTS, 2011-2012 ………………………………… 21 7a VALUE OF TOP TEN AGRICULTURAL IMPORTS, BY QUARTER, 2011-2012 ………………………………………………………………….. 22 8 MAJOR SUPPLIERS OF TOP TEN PHILIPPINE AGRICULTURAL IMPORTS, 2012 ………………………………………………………………………………… 23

37 iv

Jan

ua

ry5

.23

05

.81

5(1

0.0

6)

2.1

32

2.2

29

(4.3

5)

0.9

45

8.9

20

(89

.41

)3

.50

45

.80

9(3

9.6

8)

Feb

rua

ry4

.94

26

.34

7(2

2.1

4)

2.2

47

2.4

11

(6.8

0)

1.0

68

10

.02

0(8

9.3

4)

3.7

79

5.5

81

(32

.29

)

Ma

rch

4.4

37

6.4

39

(31

.09

)2

.28

32

.60

4(1

2.3

3)

1.1

44

9.9

60

(88

.51

)3

.78

14

.83

9(2

1.8

6)

Ap

ril

4.2

21

6.6

17

(36

.21

)2

.24

42

.58

8(1

3.2

9)

1.0

30

10

.27

0(8

9.9

7)

3.6

65

4.9

71

(26

.27

)

Ma

y4

.07

16

.41

7(3

6.5

6)

2.3

56

2.6

89

(12

.38

)0

.95

31

0.1

10

(90

.57

)3

.37

64

.52

3(2

5.3

6)

Jun

e3

.71

96

.06

2(3

8.6

5)

2.3

30

2.6

00

(10

.38

)0

.95

49

.76

0(9

0.2

3)

2.8

63

4.5

25

(36

.73

)

July

4.1

99

5.9

09

(28

.94

)2

.36

02

.48

5(5

.03

)0

.96

59

.61

0(8

9.9

6)

2.8

93

4.5

62

(36

.58

)

Au

gust

3.8

54

5.9

62

(35

.36

)2

.34

82

.47

1(4

.98

)0

.95

19

.51

0(9

0.0

0)

2.5

95

4.6

18

(43

.81

)

Sep

tem

ber

3.9

46

6.0

60

(34

.88

)2

.31

42

.33

8(1

.03

)0

.96

59

.47

0(8

9.8

1)

2.7

63

4.5

16

(38

.82

)

Oct

ob

er3

.82

15

.46

3(3

0.0

6)

2.3

03

2.1

63

6.4

70

.95

69

.54

0(8

9.9

8)

2.9

54

4.0

85

(27

.69

)

No

vem

ber

3.5

25

5.4

03

(34

.76

)2

.15

32

.14

40

.42

0.9

34

9.5

60

(90

.23

)2

.80

03

.33

0(1

5.9

2)

Dec

emb

er3

.36

75

.21

9(3

5.4

9)

2.1

29

2.1

70

(1.8

9)

0.9

44

9.4

20

(89

.98

)2

.89

63

.34

7(1

3.4

7)

Co

ffee

In

tern

ati

on

al

Co

ffee

Org

an

iza

tio

n i

nd

ica

tor

pri

ce, o

ther

mil

d A

rab

ica

s, a

vera

ge N

ew Y

ork

an

d B

rem

en/H

am

bu

rg m

ark

ets,

ex-

do

ck

Co

ffee

In

tern

ati

on

al

Co

ffee

Org

an

iza

tio

n i

nd

ica

tor

pri

ce, R

ob

ust

as,

ave

rage

New

Yo

rk a

nd

Le

Ha

vre/

Ma

rsei

lles

ma

rket

s, e

x-d

ock

Ba

na

na

(C

entr

al

an

d S

ou

th A

mer

ica

n),

ma

jor

bra

nd

s, U

S im

po

rt p

rice

,fre

e o

n t

ruck

US

Go

lf p

ort

s

Ru

bb

er (

an

y o

rigi

n),

RSS

no

. 1, i

n b

ale

s, R

ub

ber

Tra

der

s A

sso

cia

tio

n, s

po

t, N

ew Y

ork

Sou

rce:

Ba

ng

ko S

entr

al n

g P

ilip

ina

s

Co

mm

od

ity

Pri

ce D

ata

, Wo

rld

Ba

nk

Tab

le 1

1. W

OR

LD P

RIC

ES O

F SE

LEC

TED

CO

MM

OD

ITIE

S, 2

011-

2012

… C

on

tin

ued

($ p

er k

g.)

Gro

wth

Rat

e

Ye

ar/M

on

thG

row

th

Rat

e

Gro

wth

Rat

e

Gro

wth

Rat

e

20

12

20

11

20

12

20

11

20

12

20

11

20

12

20

11

Co

ffe

e, A

rab

ica

Co

ffe

e, R

ob

ust

aB

anan

aR

ub

be

r

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

LIST OF TABLES

Table No. Pages

9 DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTS TO ASEAN MEMBER COUNTRIES, 2012 …………………….………………….…… 27 9a DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTS TO AUSTRALIA, JAPAN, AND USA, 2012 ……………………………………………. 28 9b DISTRIBUTION OF PHILIPPINE AGRICULTURAL EXPORTS TO EU MEMBER COUNTRIES, 2012 ……………………………………………………. 29 10 DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTS FROM ASEAN MEMBER COUNTRIES, 2012 ……………………………………….. 31 10a DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTS FROM AUSTRALIA, JAPAN, AND USA, 2012 ………………………………………. 32 10b DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTS FROM EU MEMBER COUNTRIES, 2012 ……………………………………………… 33 11 WORLD PRICES OF SELECTED COMMODITIES JANUARY-DECEMBER, 2011-2012 …………………………………………………….. 35

v 36

20

12

20

11

20

12

20

11

20

12

20

11

Jan

ua

ry0

.54

20

.51

74

.88

0.5

34

0.4

68

14

.20

0.5

16

0.4

05

27

.48

0.2

73

0.2

65

2.9

8

Feb

rua

ry0

.53

80

.52

42

.58

-0

.47

3-

0.5

18

0.4

21

23

.26

0.2

80

0.2

93

(4.5

7)

Ma

rch

0.5

48

0.4

93

11

.20

-0

.45

6-

0.5

27

0.4

08

29

.02

0.2

81

0.2

91

(3.3

7)

Ap

ril

0.5

48

0.4

84

13

.11

-0

.44

8-

0.5

33

0.4

09

30

.39

0.2

74

0.3

19

(14

.19

)

Ma

y0

.60

10

.48

12

4.7

4-

0.4

48

-0

.56

20

.42

13

3.3

80

.26

90

.30

8(1

2.5

4)

Jun

e0

.60

00

.51

41

6.7

8-

0.4

74

-0

.54

10

.42

82

6.6

00

.26

70

.31

1(1

3.9

4)

July

0.5

74

0.5

38

6.5

90

.55

50

.50

79

.51

0.5

19

0.4

49

15

.47

0.3

33

0.3

01

10

.74

Au

gust

0.5

68

0.5

66

0.3

20

.54

50

.53

42

.10

0.5

09

0.4

65

9.3

90

.33

20

.31

07

.03

Sep

tem

ber

0.5

63

0.5

99

(5.9

3)

0.5

44

0.5

56

(2.1

1)

0.5

12

0.5

14

(0.3

9)

0.3

21

0.2

95

8.6

4

Oct

ob

er0

.55

80

.59

9(6

.86

)0

.53

30

.56

0(4

.94

)0

.52

00

.48

96

.40

0.3

21

0.2

75

16

.89

No

vem

ber

0.5

59

0.6

15

(9.1

0)

0.5

30

0.5

84

(9.2

9)

0.5

23

0.5

50

(4.8

7)

0.3

22

0.2

74

17

.20

Dec

emb

er0

.55

70

.58

6(4

.92

)0

.53

00

.56

6(6

.28

)0

.52

00

.54

4(4

.34

)0

.30

90

.25

91

9.3

3

Ric

e (T

ha

i) 5

% b

roke

n, w

hit

e ri

ce (

WR

), M

ille

d, i

nd

ica

tive

pri

ce b

ase

d o

n

wee

kly

surv

eys

of

exp

ort

tra

nsa

ctio

ns,

go

vern

men

t st

an

da

rd, F

.O.B

. Ba

ngk

ok

Ric

e (T

ha

i) 2

5%

bro

ken

, WR

, mil

led

, in

dic

ati

ve s

urv

ey p

rice

, go

vern

men

t st

an

da

rds,

F.O

.B. B

an

gko

k

Ric

e A

1 S

pec

ial

, bro

ken

ker

nel

ob

tain

ed f

rom

th

e m

illi

ng

of

WR

15

%, 2

0%

, an

d 2

5%

, in

dic

ati

ve p

rice

, go

vern

men

t st

an

da

rd, F

.O.B

. Ba

ngk

ok

Ma

ize

(US)

, No

. 2, y

ello

w, F

.O.B

. US

Gu

lf P

ort

s

Sou

rce:

Ba

ng

ko S

entr

al n

g P

ilip

ina

s

Co

mm

od

ity

Pri

ce D

ata

, Wo

rld

Ba

nk

Gro

wth

Rat

e

Mai

ze (

corn

)

20

11

5%

Bro

ken

20

12

25

% B

roke

n

Tab

le 1

1. W

OR

LD P

RIC

ES O

F SE

LEC

TED

CO

MM

OD

ITIE

S, 2

011-

2012

… C

on

tin

ued

($ p

er k

g.)

Ric

e

Gro

wth

Rat

e

Ye

ar/M

on

thA

1 S

pe

cial

Gro

wth

Rat

e

Gro

wth

Rat

e

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

LIST OF FIGURES

Figure No. Pages

1 SHARE OF AGRICULTURAL AND NON-AGRICULTURAL EXPORTS TO TOTAL PHILIPPINE EXPORTS, 2012 ………………………………………………. 9 2 SHARE OF AGRICULTURAL AND NON-AGRICULTURAL IMPORTS TO TOTAL PHILIPPINE IMPORTS, 2012 ………………………………………………. 9 3 PHILIPPINE AGRICULTURAL EXPORTS, BY QUARTER, 2011-2012 ……... 10 4 PHILIPPINE AGRICULTURAL IMPORTS, BY QUARTER, 2011-2012 ……… 10 5 VALUE OF COCONUT OIL EXPORTS, BY QUARTER, 2011-2012 ………….. 18 6 VALUE OF FRESH BANANA EXPORTS, BY QUARTER, 2011-2012 ….…….. 18 7 VALUE OF TUNA EXPORTS, BY QUARTER, 2011-2012 ………….………….… 18 8 VALUE OF PINEAPPLE AND PINEAPPLE PRODUCT EXPORTS, BY QUARTER, 2011-2012 ………………………….………………………………………. 18 9 VALUE OF DESSICATED COCONUT EXPORTS, BY QUARTER, 2011-2012 ………………………….………………………………………. 18 10 VALUE OF SEAWEEDS AND CARAGEENAN EXPORTS, BY QUARTER, 2011-2012 ………………….………………………………………………. 18 11 VALUE OF TOBACCO MANUFACTURED EXPORTS, BY QUARTER, 2011-2012 ………………….………………………………………………. 19 12 VALUE OF COPRA OIL CAKE EXPORTS, BY QUARTER, 2011-2012 ………….………………………………………………………. 19 13 VALUE OF FERTILIZER MANUFACTURED EXPORTS, BY QUARTER, 2011-2012 …………………………………………………………………. 19

35 vi

WORLD PRICES

Jan

ua

ry1

.45

12

.03

8(2

8.8

0)

0.9

65

1.3

54

(28

.73

)0

.51

90

.65

3(2

0.4

4)

0.4

98

0.5

72

(12

.94

)

Feb

rua

ry1

.41

12

.25

6(3

7.4

6)

0.9

45

1.5

03

(37

.13

)0

.53

20

.65

0(1

8.1

5)

0.5

12

0.5

70

(10

.18

)

Ma

rch

1.3

38

1.9

25

(30

.49

)0

.88

81

.28

0(3

0.6

3)

0.5

31

0.5

79

(8.1

6)

0.5

43

0.5

53

(1.8

1)

Ap

ril

1.3

48

2.0

89

(35

.47

)0

.90

31

.42

1(3

6.4

5)

0.5

02

0.5

37

(6.5

9)

0.5

75

0.5

56

3.4

2

Ma

y1

.15

52

.09

7(4

4.9

2)

0.7

69

1.4

19

(45

.81

)0

.45

90

.48

4(5

.19

)0

.57

30

.55

63

.06

Jun

e1

.05

81

.80

3(4

1.3

2)

0.7

08

1.1

86

(40

.30

)0

.45

10

.55

6(1

8.8

0)

0.5

67

0.5

58

1.6

1

July

1.0

70

1.6

62

(35

.62

)0

.71

41

.12

1(3

6.3

1)

0.5

04

0.6

22

(18

.92

)0

.66

20

.55

91

8.4

3

Au

gust

1.0

01

1.4

54

(31

.16

)0

.65

60

.98

5(3

3.4

0)

0.4

60

0.6

12

(24

.76

)0

.68

40

.55

82

2.5

8

Sep

tem

ber

0.9

67

1.3

05

(25

.90

)0

.64

50

.86

7(2

5.6

1)

0.4

41

0.5

88

(25

.03

)0

.67

00

.54

32

3.3

9

Oct

ob

er0

.89

81

.20

8(2

5.6

6)

0.5

91

0.8

04

(26

.49

)0

.44

80

.56

1(2

0.1

9)

0.6

17

0.5

03

22

.66

No

vem

ber

0.8

48

1.4

79

(42

.66

)0

.57

70

.98

0(4

1.1

2)

0.4

26

0.5

30

(19

.47

)0

.58

90

.48

62

1.1

9

Dec

emb

er0

.78

51

.44

5(4

5.6

7)

0.5

26

0.9

68

(45

.66

)0

.42

60

.50

8(1

6.1

8)

0.6

07

0.4

74

28

.06

No

tes:

Co

con

ut

Oil

- (

Ph

ilip

pin

es/I

nd

on

esia

), b

ulk

,C.I

.F. R

ott

erd

am

Co

pra

- (

Ph

ilip

pin

es/I

nd

on

esia

), b

ulk

,C.I

.F. N

.W. E

uro

pe

Suga

r-In

tern

ati

on

al

Suga

r A

gree

men

t (I

SA)

F.O

.B. C

ari

bb

ean

Po

rt.

Soyb

ean

s (U

S), C

.I.F

. Ro

tter

da

m

Sou

rce:

Ba

ng

ko S

entr

al n

g P

ilip

ina

s

Co

mm

od

ity

Pri

ce D

ata

, Wo

rld

Ba

nk

Tab

le 1

1. W

OR

LD P

RIC

ES O

F SE

LEC

TED

CO

MM

OD

ITIE

S, 2

011-

2012

($ p

er k

g.)

Ye

ar/M

on

thG

row

th

Rat

e

20

12

Soyb

ean

s

Gro

wth

Rat

e

Gro

wth

Rat

e

20

11

20

12

20

11

Gro

wth

Rat

e

Co

con

ut

Oil

Co

pra

20

12

20

11

20

11

20

12

Suga

r

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

LIST OF FIGURES

Figure No. Pages

14 VALUE OF CENTRIFUGAL SUGAR EXPORTS, BY QUARTER, 2011-2012 ………………….………………………………………………. 19 15 VALUE OF WHEAT (INCLUDING SPELT) & MESLIN IMPORTS, BY QUARTER, 2011-2012 ……….……………………………………………………….… 25 16 VALUE OF SOYABEAN OIL CAKE/MEAL IMPORTS, BY QUARTER, 2011-2012 ………………………………………………….………………. 25 17 VALUE OF MILK & CREAM AND PRODUCTS IMPORTS BY QUARTER, 2011-2012 ……………………………………………….…………………. 25 18 VALUE OF RICE IMPORTS, BY QUARTER, 2011-2012 ……………………..….. 25 19 VALUE OF FERTILIZER MANUFACTURED IMPORTS, BY QUARTER, 2011-2012 ………………………………………………………………….. 25 20 VALUE OF MEAT OF UREA IMPORTS, BY QUARTER, 2011-2012 ………………………………………………………………….. 25 21 VALUE OF COFFEE IMPORTS, BY QUARTER, 2011-2012 ……….………..…. 26 22 VALUE OF BOVINE ANIMALS IMPORTS, BY QUARTER, 2011-2012 ……………………………………………………….…………. 26 23 VALUE OF TOBACCO UNMANUFACTURED, BY QUARTER, 2011-2012 ………………………………………………………………………………….….…. 26 24 VALUE OF MAIZE/CORN, BY QUARTER, 2011-2012 …………….…..………… 26 25 WORLD PRICES OF COCONUT OIL, JANUARY - DECEMBER, 2011-2012 ………………………………………………………………………………………… 38 26 WORLD PRICES OF COPRA, JANUARY- DECEMBER, 2011-2012 …………. 38

vii 34

Ital

yLa

tvia

Lith

uan

iaLu

xem

bo

urg

Mal

taN

eth

erl

and

Po

lan

dP

ort

uga

lSl

ova

ck

Re

pu

blic

Slo

ven

iaSp

ain

Swe

de

n

UK

Gre

at

Bri

tain

& N

.

Ire

lan

d

1.

Foo

d a

nd

Liv

e A

nim

als

62

.46

90

.00

13

.26

30

.00

11

07

.52

89

.55

70

.27

82

6.1

41

0.7

83

16

.39

64

41

.11

7

A.

Live

An

ima

ls (

No

.)0

.00

10

.00

10

.81

10

.23

82

.34

24

.74

7

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

0.0

52

13

.40

80

.03

97

.58

62

.36

97

1.7

59

C.

Da

iry

Pro

du

cts

an

d B

ird

s Eg

gs1

.59

01

2.9

80

9.2

41

0.1

52

1.7

05

0.4

76

0.7

37

66

.74

8

D.

Fish

an

d F

ish

Pre

pa

rati

on

s0

.08

90

.32

4

0

.08

60

.15

70

.82

42

.03

0

E. C

erea

ls a

nd

Cer

eals

Pre

pa

rati

on

s1

.53

61

.00

20

.00

40

.04

10

.04

00

.29

62

.93

92

2.2

15

F. V

eget

ab

les

an

d F

ruit

s3

.15

95

.17

30

.00

21

.55

00

.01

00

.51

12

6.0

82

G.

Suga

r a

nd

Su

gar

Pre

pa

rati

on

s0

.05

23

.26

32

.66

20

.22

20

.91

12

9.4

52

H.

Co

ffee

, Tea

, Co

coa

, Sp

ices

an

d

1.2

82

5.5

58

0.0

78

0.8

43

0.8

07

13

.21

1

Ma

nu

fact

ure

s th

ereo

f

I. F

eed

ing

Stu

ff f

or

An

ima

ls

(exc

lud

ing

un

mil

led

Cer

eals

)

J. M

isce

lla

neo

us

Edib

le P

rod

uct

s a

nd

1

.30

7

33

.73

2

0.0

98

4

.68

3

2.0

50

7

0.8

58

P

rep

ara

tio

ns

II.

Tob

acc

o a

nd

To

ba

cco

Ma

nu

fact

ure

s0

.03

0

0.0

35

0.0

68

0

.16

8

0.0

88

0

.04

5

16

.03

4

III.

Cru

de

Ma

teri

als

0.8

24

5.1

46

0.7

28

0.4

81

22

.62

9

A.

Oil

See

ds

an

d O

legi

no

us

Fru

its

a/

0.0

23

B.

Cru

de

Ru

bb

er0

.03

80

.78

40

.00

13

.47

2

C.

Cru

de

Fert

iliz

er0

.00

30

.07

7

D.

Cru

de

An

ima

l a

nd

Veg

s. M

ate

ria

ls0

.78

64

.36

00

.72

70

.48

11

9.0

56

IV.

An

ima

l a

nd

Veg

eta

ble

Oil

an

d F

ats

1.5

92

2.8

10

0.0

42

7.2

58

2.6

32

0.5

87

26

.93

9

A.

An

ima

l a

nd

Veg

eta

ble

Oil

s a

nd

Fa

ts0

.09

02

.69

30

.04

23

.48

70

.54

31

7.6

32

B.

Fixe

d V

eget

ab

le O

il a

nd

Fa

ts1

.50

30

.11

73

.77

12

.63

20

.04

49

.30

7

V.

Fert

iliz

er M

an

ufa

ctu

red

6.8

13

0.5

79

0.0

36

1.0

85

18

.66

6

VI.

Agr

icu

ltu

ral

Ch

emic

als

an

d M

ate

ria

ls3

.63

71

2.7

52

0.2

28

1.4

46

0.1

62

9.4

03

67

.10

6

VII

. A

gric

ult

ura

l M

ach

iner

y (N

o.)

11

.55

03

.16

10

.00

20

.04

20

.85

94

.47

62

.07

23

9.4

35

TOTA

L V

ALU

E O

F A

GR

ICU

LTU

RA

L IM

PO

RTS

80

.10

0.0

01

0.0

80

.00

0.0

01

32

.01

9.6

70

.55

0.0

00

.00

36

.64

8.1

43

0.0

76

31

.93

TOTA

L V

ALU

E O

F P

HIL

IPP

INE

IMP

OR

TS3

18

.06

0.0

61

2.1

11

.08

3.1

63

25

.05

18

.82

6.0

51

.78

2.9

32

71

.82

12

8.1

52

90

.36

1,3

79

.43

a/

les

s th

an

0.0

01

Tab

le 1

0b.

DIS

TRIB

UTI

ON

OF

PH

ILIP

PIN

E A

GR

ICU

LTU

RA

L IM

PO

RTS

FR

OM

EU

MEM

BER

CO

UN

TRIE

S, 2

012

(C.I

.F. V

alu

e in

Mil

lio

n U

S $)

Tota

l

Ph

ilip

pin

e

Agr

icu

ltu

ral

Imp

ort

s

fro

m E

U

EUR

OP

EAN

UN

ION

Ite

m

53

.40

13

1.8

76

0.0

94

13

4.0

14

9.1

17

2.9

05

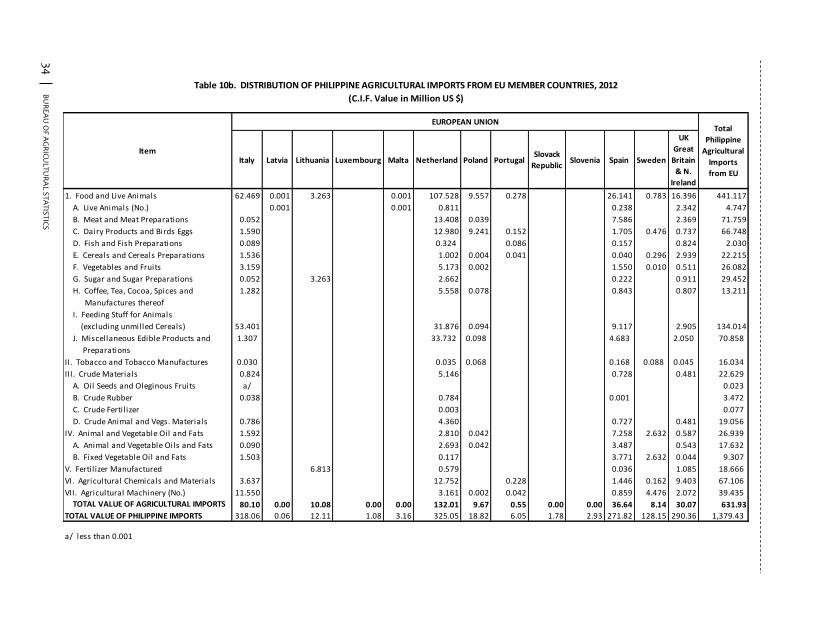

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

LIST OF FIGURES

Figure No. Pages

27 WORLD PRICES OF SUGAR, JANUARY - DECEMBER, 2011-2012 ……….. 38 28 WORLD PRICES OF SOYBEANS, JANUARY - DECEMBER, 2011-2012 …… 38 29 WORLD PRICES OF RICE (5% BROKEN), JANUARY- DECEMBER, 2011-2012 ………………………………………………………………………………………… 38 30 WORLD PRICES OF RICE (25% BROKEN), JANUARY- DECEMBER, 2011-2012 ………………………………………………………………………………………….. 38 31 WORLD PRICES OF RICE (A1 SPECIAL), JANUARY - DECEMBER, 2011-2012 ………………………………………………………………………………………… 39 32 WORLD PRICES OF MAIZE, JANUARY- DECEMBER, 2011-2012 ….….…… 39 33 WORLD PRICES OF COFFEE, ARABICA, JANUARY- DECEMBER, 2011-2012 ………………………………………………………………………………………… 39 34 WORLD PRICES OF COFFEE, ROBUSTA, JANUARY- DECEMBER, 2011-2012 ………………………………………………………………………………………… 39 35 WORLD PRICES OF BANANA, JANUARY- DECEMBER, 2011-2012 ………. 39 36 WORLD PRICES OF RUBBER, JANUARY- DECEMBER, 2011-2012 ……….. 39

33 viii A

ust

ria

Be

lgiu

mC

ypru

sC

zech

Re

pu

blic

De

nm

ark

Esto

nia

Fin

lan

dFr

ance

Ge

rman

yG

ree

ceH

un

gary

Ire

lan

d

1.

Foo

d a

nd

Liv

e A

nim

als

2.1

34

37

.94

20

.93

50

.54

31

6.6

27

0.0

00

1.2

66

84

.48

95

9.6

51

0.0

41

0.0

02

11

.07

1

A.

Live

An

ima

ls (

No

.)0

.03

0.0

06

0.0

40

.90

0.3

7

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

8.9

72

0.2

88

0.0

09

2.9

18

0.1

23

23

.36

61

1.2

33

1.3

94

C.

Da

iry

Pro

du

cts

an

d B

ird

s Eg

gs2

.45

60

.51

18

.07

80

.87

31

7.5

56

4.3

80

6.0

12

D.

Fish

an

d F

ish

Pre

pa

rati

on

s0

.03

00

.12

40

.24

20

.15

10

.00

2

E. C

erea

ls a

nd

Cer

eals

Pre

pa

rati

on

s5

.00

00

.00

31

.22

40

.03

39

.52

20

.57

6

F. V

eget

ab

les

an

d F

ruit

s0

.19

36

.71

70

.64

70

.45

70

.04

00

.88

56

.61

20

.03

40

.09

2

G.

Suga

r a

nd

Su

gar

Pre

pa

rati

on

s0

.05

83

.87

20

.01

40

.34

10

.11

51

4.7

58

3.1

35

0.0

50

H.

Co

ffee

, Tea

, Co

coa

, Sp

ices

an

d M

an

ufa

ctu

res

0.0

11

0.7

41

0.0

07

2.2

59

1.6

18

0.0

07

ther

eof

I.

Feed

ing

Stu

ff f

or

An

ima

ls

(ex

clu

din

g u

nm

ille

d C

erea

ls)

J. M

isce

lla

neo

us

Edib

le P

rod

uct

s a

nd

0

.05

0

3

.30

6

1

.12

7

0

.04

2

5

.66

5

1

5.3

36

3

.46

2

P

rep

ara

tio

ns

II.

Tob

acc

o a

nd

To

ba

cco

Ma

nu

fact

ure

s1

4.3

76

0

.10

9

0

.06

6

0

.40

7

0

.45

1

0

.19

0

III.

Cru

de

Ma

teri

als

0.2

87

0.1

09

2.8

12

4.4

73

7.7

64

0.0

05

A.

Oil

See

ds

an

d O

legi

no

us

Fru

its

0.0

23

B.

Cru

de

Ru

bb

er0

.10

90

.01

40

.47

02

.05

6

C.

Cru

de

Fert

iliz

er0

.07

40

.00

1

D.

Cru

de

An

ima

l a

nd

Veg

s. M

ate

ria

ls0

.21

32

.79

84

.00

35

.68

40

.00

5

IV.

An

ima

l a

nd

Veg

eta

ble

Oil

an

d F

ats

1.5

29

0.9

76

1.2

17

8.1

59

0.1

38

A.

An

ima

l a

nd

Veg

eta

ble

Oil

s a

nd

Fa

ts0

.86

20

.97

61

.21

47

.62

60

.09

9

B.

Fixe

d V

eget

ab

le O

il a

nd

Fa

ts0

.66

70

.00

20

.53

20

.03

9

V.

Fert

iliz

er M

an

ufa

ctu

red

5.4

45

0.0

07

0.0

83

4.6

18

VI.

Agr

icu

ltu

ral

Ch

emic

als

an

d M

ate

ria

ls0

.43

37

.41

11

.33

50

.00

21

1.1

62

18

.00

70

.77

20

.35

8

VII

. A

gric

ult

ura

l M

ach

iner

y (N

o.)

0.0

97

1.3

01

0.1

34

0.5

68

0.0

10

1.6

01

13

.55

60

.00

6

TOTA

L V

ALU

E O

F A

GR

ICU

LTU

RA

L IM

PO

RTS

2.6

66

8.2

90

.93

0.7

92

2.4

30

.00

1.2

81

03

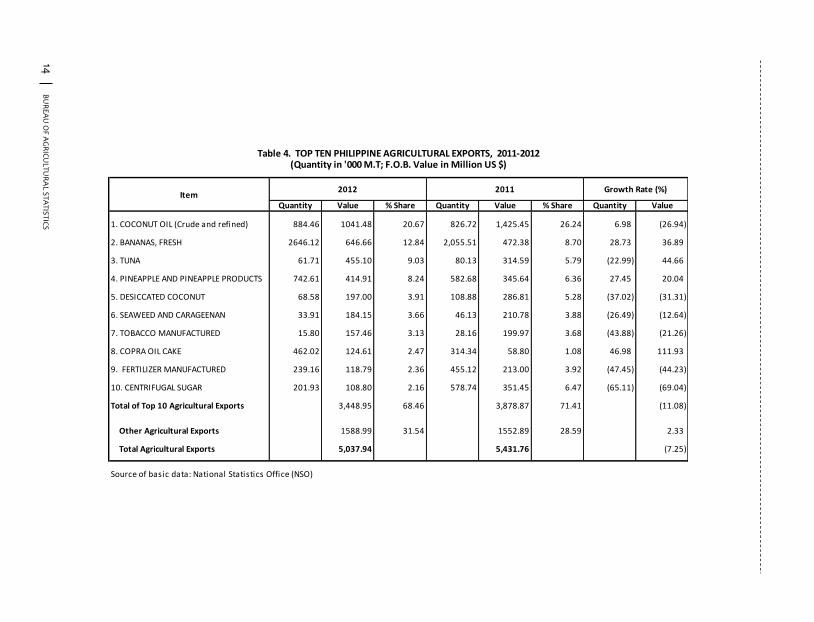

.09

11

2.1

60

.50

0.7

71

1.7

6

TOTA

L V

ALU

E O

F P

HIL

IPP

INE

IMP

OR

TS5

3.6

13

06

.49

1.3

97

6.8

57

6.5

30

.28

13

9.0

29

37

.27

15

54

.68

4.0

61

4.2

73

69

.98

a/

les

s th

an

0.0

01

EUR

OP

EAN

UN

ION

1.8

23

6.8

16

Tab

le 1

0b.

DIS

TRIB

UTI

ON

OF

PH

ILIP

PIN

E A

GR

ICU

LTU

RA

L IM

PO

RTS

FR

OM

EU

MEM

BER

CO

UN

TRIE

S, 2

012

(C.I

.F. V

alu

e in

Mil

lio

n U

S $)

Ite

m

2.3

07

0.0

40

9.3

38

16

.23

50

.06

2

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

OVERALL AGRICULTURAL TRADE SITUATION

1. The Philippine agricultural foreign trade performance weakened in 2012

compared to 2011, where the gap between our exports and imports further widened. Trade deficit grew by around 30 percent, from US$ 2,408.17 million in 2011 to US$ 3,130.39 million this year (Table 1).

While total exports registered increase in revenue, earnings from agricultural exports dropped from US$ 5,431.76 million in 2011 to US$ 5,037.94 million in 2012 or 7.25 percent.

The share of agricultural exports declined to 9.67 percent in 2012 from 11.24 percent in 2011.

Agricultural imports posted a 4.19 percent increase in expenditures from US$ 7,839.93 million in 2011 to US$ 8,168.33 million in 2012.

Agricultural imports shared 12.41 percent to total expenditures on imports amounting to US$ 65,839.34 million.

2. Trade with Japan and European Union (EU) both posted surpluses. However, the

movements were in opposite directions. Trade surplus with Japan exhibited an increasing rate while that with EU registered a decrease. Trade deficits were noted for the country’s other trading partners (Table 2).

Trade surplus with Japan grew by 11.92 percent above 2011 level. In 2012, Japan was the country’s top market for fresh banana; 2

nd top

importer of pineapple and pineapple products; and 3rd

leading market for coconut oil, tuna and centrifugal sugar. Value of agricultural exports to this country was US$ 691.85 million or 13.73 percent of our total agricultural exports revenue in 2012. On the other hand, the Philippines’ agricultural import from Japan was valued at US$ 116.17 million.

EU shared 18.10 percent of the country’s total export revenue. EU was a major market for Philippine coconut oil, tuna, desiccated coconut and seaweed & carrageenan. Agricultural trade surplus with EU was down by 38.92 percent to US$ 279.82 million in 2012 from US$ 458.08 million in 2011. While agricultural imports increased by about 4.0 percent, exports

1 32

Item

Total Philippine

Agricultural

Imports

Australia Japan USA

1. Food and Live Animals 6106.15 690.65 27.96 1681.87

A. Live Animals (No.) 29.47 18.00 0.00 4.02

B. Meat and Meat Preparations 492.49 98.94 0.22 112.16

C. Dairy Products and Birds Eggs 792.736 83.963 0.125 223.162

D. Fish and Fish Preparations 232.183 0.308 21.561 9.771

E. Cereals and Cereals Preparations 1758.683 451.374 0.723 545.157

F. Vegetables and Fruits 412.498 6.729 0.524 80.383

G. Sugar and Sugar Preparations 235.532 3.666 0.126 44.728

H. Coffee, Tea, Cocoa, Spices and Manufactures thereof 363.662 2.235 1.114 12.329

I. Feeding Stuff for Animals

(excluding unmilled Cereals) 1063.766 17.185 0.197 585.345

J. Miscellaneous Edible Products and Preparations 725.129 8.252 3.373 64.810

II. Tobacco and Tobacco Manufactures 165.954 0.087 0.035 1.488

III. Crude Materials 311.641 2.718 11.348 41.711

A. Oil Seeds and Oleginous Fruits 100.732 0.706 0.073 20.679

B. Crude Rubber 35.379 0.028 7.664 1.158

C. Crude Fertil izer 82.355 0.000 0.186 0.365

D. Crude Animal and Vegs. Materials 93.175 1.984 3.425 19.508

IV. Animal and Vegetable Oil and Fats 409.061 11.328 0.620 2.619

A. Animal and Vegetable Oils and Fats 291.756 10.917 0.583 2.168

B. Fixed Vegetable Oil and Fats 117.304 0.411 0.037 0.451

V. Fertil izer Manufactured 638.105 5.421 30.826 1.746

VI. Agricultural Chemicals and Materials 399.738 4.161 35.789 16.160

VII. Agricultural Machinery (No.) 137.683 5.289 9.588 19.753

TOTAL VALUE OF AGRICULTURAL IMPORTS 8168.331 719.657 116.167 1765.348

TOTAL VALUE OF PHILIPPINE IMPORTS 65,839.335 1,453.909 6,986.691 7,596.233

Table 10a. DISTRIBUTION OF PHILIPPINE AGRICULTURAL IMPORTS FROM AUSTRALIA, JAPAN and USA, 2012

(C.I.F. Value in Million US $)

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

38.92 percent to US$ 279.82 million in 2012 from US$ 458.08 million in 2011. While agricultural imports increased by about 4.0 percent, exports declined by about 14.50 percent.

Agricultural trade with ASEAN member-countries posted further trade deficit by 6.57 percent. Agricultural exports to ASEAN countries were down by 6.85 percent, but agricultural imports from the region moved up by 0.92 percent.

Trade deficit with Australia was sustained and further increased by 31.20 percent. Australia shared less than one (1) percent to our agricultural exports revenue at US$ 48.03 million and nearly nine (9) percent to our agricultural imports expenditures at US$ 719.66 million.

Agricultural trade with the United States of America (USA) posted biggest growth in deficit by 179.72 percent. Deficit grew to US$ 561.90 million from US$ 200.88 million in 2011. Exports decreased by 17.25 percent while imports by 6.66 percent. The USA shared about one fourth to our agricultural exports in 2012.

Trade with the rest of the world (ROW) sustained trade deficit though at very slow rate of 0.09 percent, that is, from US$ 1,401.88 million in 2011 to US$ 1,403.16 million in 2012.

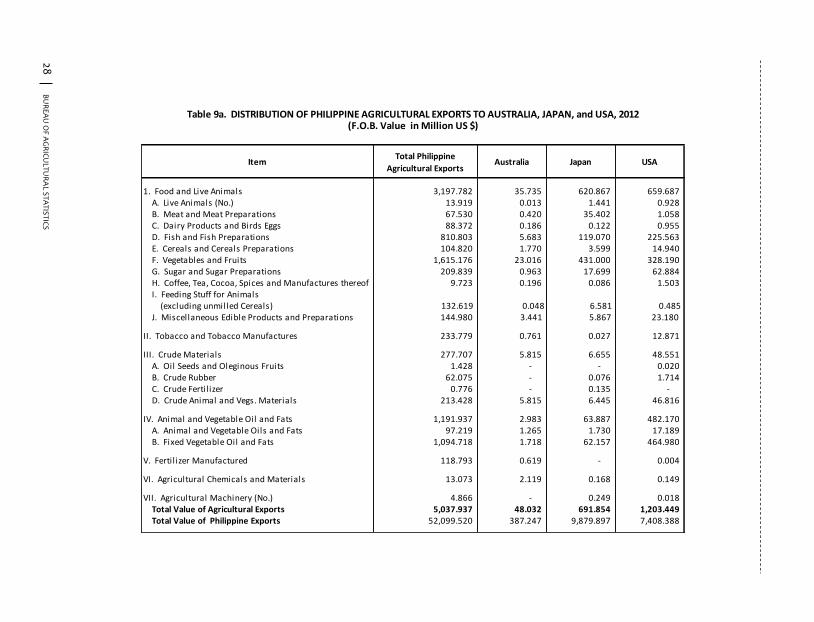

3. Top Agricultural Exports

Top agricultural exports shared 68.46 percent to total agricultural exports revenue at US$ 3,448.95 million or 11.08 percent lower than the 2011 earnings. Coconut oil recorded the biggest export revenue though at a decreasing rate. Export gainers in 2012 included fresh banana, tuna, pineapple and pineapple products and copra oil cake (Tables 4-6).

Coconut oil shared 20.67 percent to the Philippine top ten (10) export earnings. However, this was lower by 26.94 percent in revenue compared to 2011. Export earnings were down to US$ 1,041.48 million in 2012 from US$ 1,425.45 million in 2011. The highest export recorded was in the 2

nd quarter

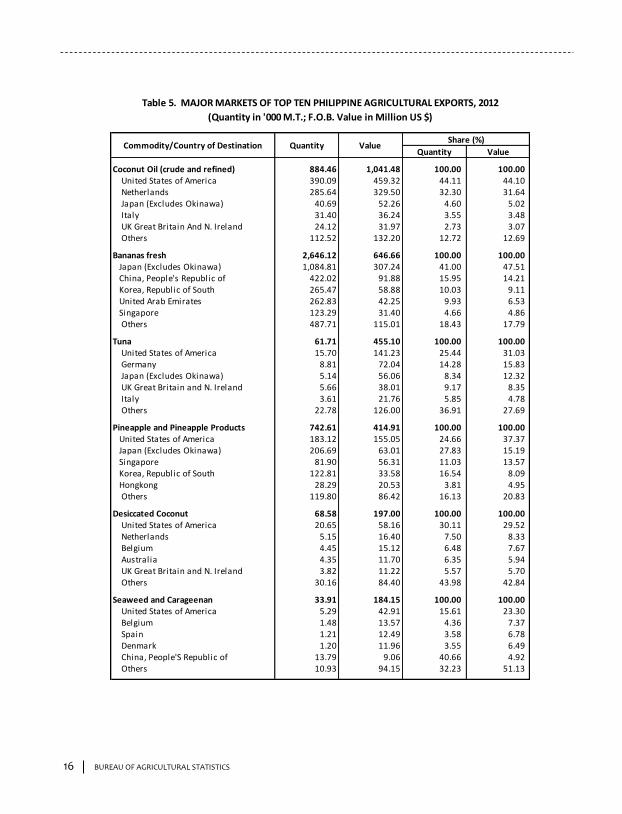

at US$ 294.39 million. Major markets were USA (44.10%); the Netherlands (31.64%); Japan (5.02%); Italy (3.48%); UK Great Britain and Northern Ireland (3.07%) and others (12.69%).

31 2

Bru

ne

iC

amb

od

iaIn

do

ne

sia

Lao

PD

RM

alay

sia

Mya

nm

arSa

bah

Sara

wak

Sin

gap

ore

Thai

lan

dV

ietn

am

1.

Foo

d a

nd

Liv

e A

nim

als

0.0

10

.06

30

2.2

51

63

.44

25

.47

0.0

01

86

.62

28

0.0

44

90

.72

14

48

.60

A.

Live

An

ima

ls (

No

.)-

-

-

-

-

-

-

0

.03

-

0.0

26

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

-

-

-

0

.02

-

-

0.5

7

1.3

1

0.0

8

1.9

87

C.

Da

iry

Pro

du

cts

an

d B

ird

s Eg

gs-

-

1

0.3

7

1

2.1

8

-

-

4.8

5

14

.35

4.3

0

46

.04

7

D.

Fish

an

d F

ish

Pre

pa

rati

on

s0

.01

-

6

.28

0

.38

0

.02

-

2

.22

1

.95

3

5.2

8

4

6.1

33

E. C

erea

ls a

nd

Cer

eals

Pre

pa

rati

on

s-

0.0

6

55

.20

4.6

1

14

.87

-

8.3

0

54

.24

36

5.7

3

5

02

.98

5

F. V

eget

ab

les

an

d F

ruit

s-

-

6

.78

1

.34

1

0.2

9

-

2

.34

1

2.7

8

8

.65

4

2.1

91

G.

Suga

r a

nd

Su

gar

Pre

pa

rati

on

s-

-

1

8.5

7

1

0.1

4

-

-

2.0

7

23

.07

7.4

9

61

.34

H.

Co

ffee

, Tea

, Co

coa

, Sp

ices

an

d

Ma

nu

fact

ure

s th

ereo

f

I. F

eed

ing

Stu

ff f

or

An

ima

ls-

-

5.8

2

1

.89

0.2

9

-

24

.16

35

.81

2.6

2

70

.59

(exc

lud

ing

un

mil

led

Cer

eals

)

J. M

isce

lla

neo

us

Edib

le P

rod

uct

s -

-

3

7.4

8

88

.31

-

-

12

1.1

8

1

14

.39

8.7

2

37

0.0

6

a

nd

Pre

pa

rati

on

s

II.

Tob

acc

o a

nd

To

ba

cco

Ma

nu

fact

ure

s-

-

1

.00

2

5.8

8

-

-

0.5

9

3.4

8

5.8

7

36

.82

III.

Cru

de

Ma

teri

als

0.0

00

.00

29

.49

1.8

10

.00

00

.00

2.5

07

.03

3.0

74

3.9

0

A.

Oil

See

ds

an

d O

legi

no

us

Fru

its

-

-

18

.71

0.0

1

-

-

0

.78

0

.10

1

.23

2

0.8

3

B.

Cru

de

Ru

bb

er-

-

0

.09

0

.95

-

-

0.1

6

3.4

5

0.1

3

4.7

8

C.

Cru

de

Fert

iliz

er-

-

0

.02

0

.20

-

-

1.2

5

0.1

6

1.2

4

2.8

6

D.

Cru

de

An

ima

l a

nd

Veg

s. M

ate

ria

ls-

-

1

0.6

6

0

.65

-

0.0

0

0

.32

3

.32

0

.47

1

5.4

2

IV.

An

ima

l a

nd

Veg

eta

ble

Oil

an

d F

ats

-

-

61

.44

25

3.0

9

-

-

22

.22

5.0

2

3.1

1

34

4.8

8

A.

An

ima

l a

nd

Veg

eta

ble

Oil

s a

nd

Fa

ts-

-

3

5.2

7

1

83

.98

-

-

1

3.0

1

4

.98

3

.05

2

40

.29

B.

Fixe

d V

eget

ab

le O

il a

nd

Fa

ts-

-

2

6.1

7

6

9.1

1

-

-

9.2

0

0.0

4

0.0

6

10

4.5

9

V.

Fert

iliz

er M

an

ufa

ctu

red

-

-

44

.43

55

.72

-

-

2

4.4

1

2

.72

5

5.9

8

1

83

.26

VI.

Agr

icu

ltu

ral

Ch

emic

als

an

d M

ate

ria

ls-

0.1

5

44

.91

14

.81

-

-

7

.83

4

8.2

8

1

3.5

9

1

29

.57

VII

. A

gric

ult

ura

l M

ach

iner

y (N

o.)

-

-

1.0

5

5.7

1

-

-

3

.59

8

.46

0

.98

1

9.7

9

TOTA

L V

ALU

E O

F A

GR

ICU

LTU

RA

L IM

PO

RTS

0.0

10

.20

48

4.5

80

.00

52

0.4

62

5.4

70

.00

0.0

02

47

.76

35

5.0

35

73

.30

22

06

.82

TOTA

L V

ALU

E O

F P

HIL

IPP

INE

IMP

OR

TS5

8.5

83

.01

2,9

64

.70

0

.05

2,5

42

.05

3

0.1

0

7

0.8

2

17

.86

4,6

56

.50

3

,65

9.0

6

1,0

59

.67

1

5,0

62

.40

Tota

l

Ph

ilip

pin

e

Agr

icu

ltu

ral

Imp

ort

s

fro

m A

SEA

N

16

1.7

6

4

4.5

7

-

-

-

2

2.1

2

5

7.8

5

2

0.9

3

Tab

le 1

0. D

ISTR

IBU

TIO

N O

F P

HIL

IPP

INE

AG

RIC

ULT

UR

AL

IMP

OR

TS F

RO

M A

SEA

N M

EMB

ER C

OU

NTR

IES,

201

2(C

.I.F

. Val

ue

in M

illi

on

US

$)

Ite

m

-

ASE

AN

30

7.2

4

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

Fresh Bananas which shared 12.84 percent to the total top agricultural commodities was the Philippines’ 2

nd top export commodity in 2012.

Export revenue grew by 36.89 percent, the highest of which was posted during the 4

th quarter of 2012. Japan shared 47.51 percent at

US$ 307.24 million of the total export earnings from this commodity. Other major markets were People’s Republic of China, South Korean Republic, United Arab Emirates and Singapore.

Tuna generated US$ 455.10 million earnings from exports to the USA (31.03%); Germany (15.83%); Japan (12.32%); UK Great Britain and N. Ireland (8.35%); Italy (4.78%) and others (27.69%).

Export revenues from pineapple and pineapple products increased by 20.04 percent. The US$ 414.91 million earnings were mostly shared by procurement from USA (37.37%); Japan (15.19 %) and Singapore (13.57%).

Best performer in 2012 was copra oil cake which moved up by 111.93% in revenue from US$ 58.80 million to US$ 124.61 million finding its way to the top 8 list.

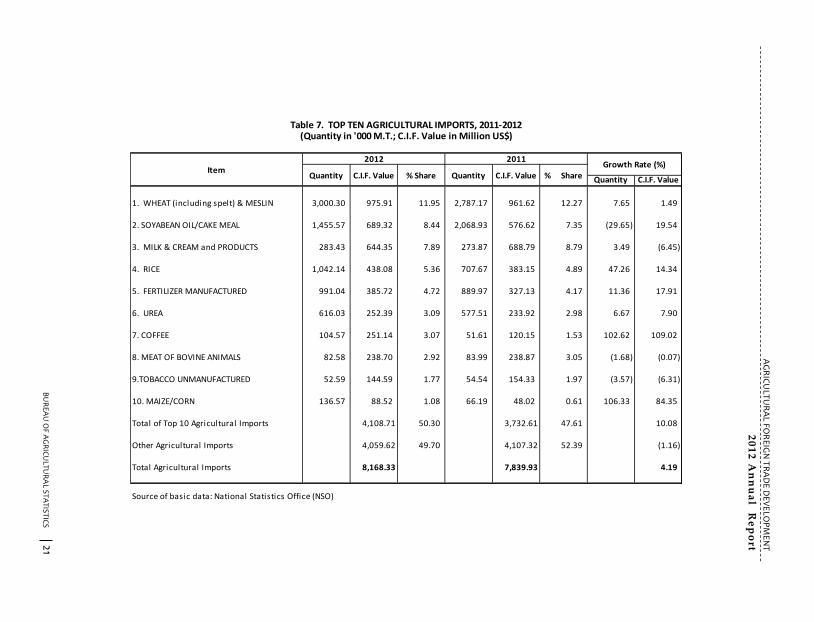

4. Top Agricultural Imports

The total value of top ten agricultural imports at US$ 4,108.71 million was about half (50.30%) of the country’s agricultural import expenditures at US$ 8,168.33 million in 2012. Except for milk & cream and products, meat of bovine animals and unmanufactured tobacco, expenditures for all of the top ten import commodities recorded increasing rate (Tables 7-8).

Wheat (including spelt) & Meslin had the largest share of nearly 12 percent to the total agricultural imports. The highest importation of wheat was recorded during the 3

rd quarter at US$ 295.44 million. More

than half (54.09 %) of our wheat imports were sourced from the USA; about 40.91 % from Australia while the rest came from India, Canada, Singapore and other countries.

3 30

Ital

yLa

tvia

Lith

uan

iaLu

xem

bo

urg

Mal

taN

eth

erl

and

Po

lan

dP

ort

uga

lSl

ova

ck

Re

pu

blic

Slo

ven

iaSp

ain

Swe

de

n

UK

Gre

at

Bri

tain

& N

.

Ire

lan

d

1.

Foo

d a

nd

Liv

e A

nim

als

29

.43

50

.08

60

.64

10

.00

00

.69

86

7.5

17

3.3

69

1.1

90

0.1

02

0.5

42

25

.40

44

.03

27

5.0

74

34

7.9

69

A.

Live

An

ima

ls (

No

.)0

.03

40

.12

00

.24

9

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

0.0

05

a/

0.0

22

C.

Da

iry

Pro

du

cts

an

d B

ird

s Eg

gsa

/0

.00

0

D.

Fish

an

d F

ish

Pre

pa

rati

on

s2

2.3

72

0.2

82

a/

0.5

58

14

.49

72

.26

10

.82

40

.06

70

.46

51

6.2

02

1.0

02

40

.84

61

91

.84

0

E. C

erea

ls a

nd

Cer

eals

Pre

pa

rati

on

s0

.56

60

.67

10

.00

40

.18

50

.00

31

.16

92

.96

9

F. V

eget

ab

les

an

d F

ruit

s4

.16

60

.08

60

.35

90

.13

64

3.1

07

1.1

08

0.2

89

0.0

35

0.0

77

8.0

84

2.9

68

27

.23

41

33

.26

7

G.

Suga

r a

nd

Su

gar

Pre

pa

rati

on

s0

.37

90

.00

40

.04

70

.06

80

.03

82

.70

83

.80

0

H.

Co

ffee

, Tea

, Co

coa

, Sp

ices

an

d

0.0

39

0.4

93

0.5

81

0.7

11

1.8

82

Ma

nu

fact

ure

s th

ereo

f

I. F

eed

ing

Stu

ff f

or

An

ima

ls

(exc

lud

ing

un

mil

led

Cer

eals

)

J. M

isce

lla

neo

us

Edib

le P

rod

uct

s a

nd

1

.91

21

.09

10

.07

30

.27

90

.02

12

.27

46

.35

1

P

rep

ara

tio

ns

II.

Tob

acc

o a

nd

To

ba

cco

Ma

nu

fact

ure

s0

.96

60

.49

60

.88

00

.67

51

.97

60

.06

00

.11

81

5.6

60

III.

Cru

de

Ma

teri

als

0.8

09

0.1

75

0.2

63

0.4

82

2.0

09

2.1

58

0.0

22

0.0

28

12

.55

70

.03

98

.85

16

9.6

74

A.

Oil

See

ds

an

d O

legi

no

us

Fru

its

0.0

00

B.

Cru

de

Ru

bb

er0

.03

4

C.

Cru

de

Fert

iliz

er0

.00

0

D.

Cru

de

An

ima

l a

nd

Veg

s. M

ate

ria

ls0

.80

90

.17

50

.26

30

.48

22

.00

92

.15

80

.02

20

.02

81

2.5

57

0.0

39

8.8

51

69

.64

0

IV.

An

ima

l a

nd

Veg

eta

ble

Oil

an

d F

ats

36

.24

20

.26

03

70

.93

8

a

/ 0

.01

3

2

0.9

36

0

.01

5

3

2.0

52

4

77

.25

7

A.

An

ima

l a

nd

Veg

eta

ble

Oil

s a

nd

Fa

ts0

.08

34

1.4

41

a/

0.2

71

0.0

81

44

.05

6

B.

Fixe

d V

eget

ab

le O

il a

nd

Fa

ts3

6.2

42

0.1

77

32

9.4

97

0.0

13

20

.66

50

.01

53

1.9

71

43

3.2

01

V.

Fert

iliz

er M

an

ufa

ctu

red

0.0

00

VI.

Agr

icu

ltu

ral

Ch

emic

als

an

d M

ate

ria

ls0

.42

80

.00

40

.14

10

.15

40

.01

61

.04

0

VII

. A

gric

ult

ura

l M

ach

iner

y (N

o.)

0.0

15

0.0

29

0.1

46

Tota

l Val

ue

of

Agr

icu

ltu

ral E

xpo

rts

67

.88

00

.52

11

.40

00

.00

01

.18

04

41

.34

96

.21

71

.35

30

.10

20

.58

36

1.0

27

4.1

75

11

6.1

11

91

1.7

46

Tota

l Val

ue

of

Ph

ilip

pin

e E

xpo

rts

21

8.6

02

1.1

32

4.1

32

5.3

22

30

.01

91

55

4.3

61

45

.63

91

5.6

84

4.7

94

2.1

05

10

9.3

28

84

.61

06

56

.58

35

91

0.1

46

a/

less

th

an

0.0

01

Tab

le 9

b.

DIS

TRIB

UTI

ON

OF

PH

ILIP

PIN

E A

GR

ICU

LTU

RA

L EX

PO

RTS

TO

EU

MEM

BER

CO

UN

TRIE

S, 2

012

(F.O

.B. V

alu

e in

'00

0 U

S $

) …

Con

tinu

ed

EUR

OP

EAN

UN

ION

7.5

89

0.0

12

Tota

l

Ph

ilip

pin

e

Agr

icu

ltu

ral

Exp

ort

s to

EU

7.5

77

Ite

m

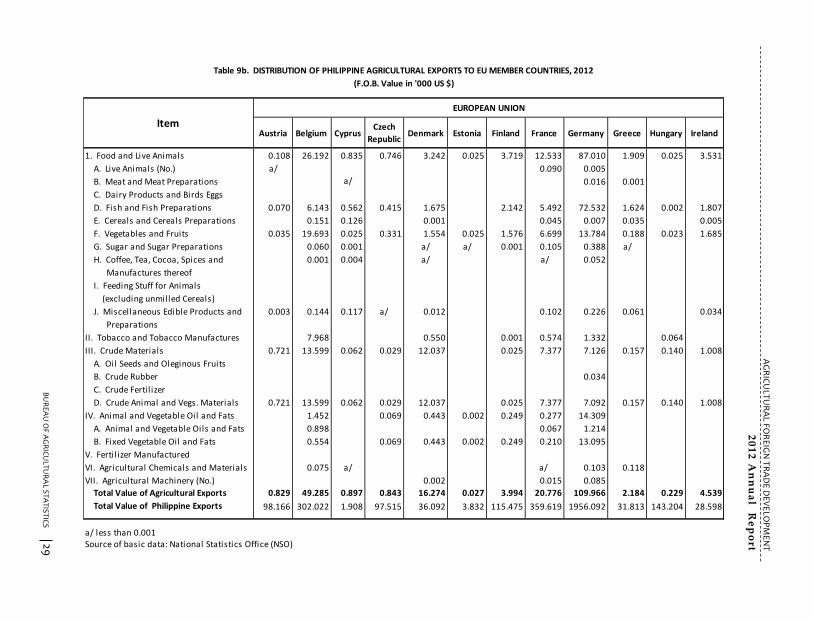

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

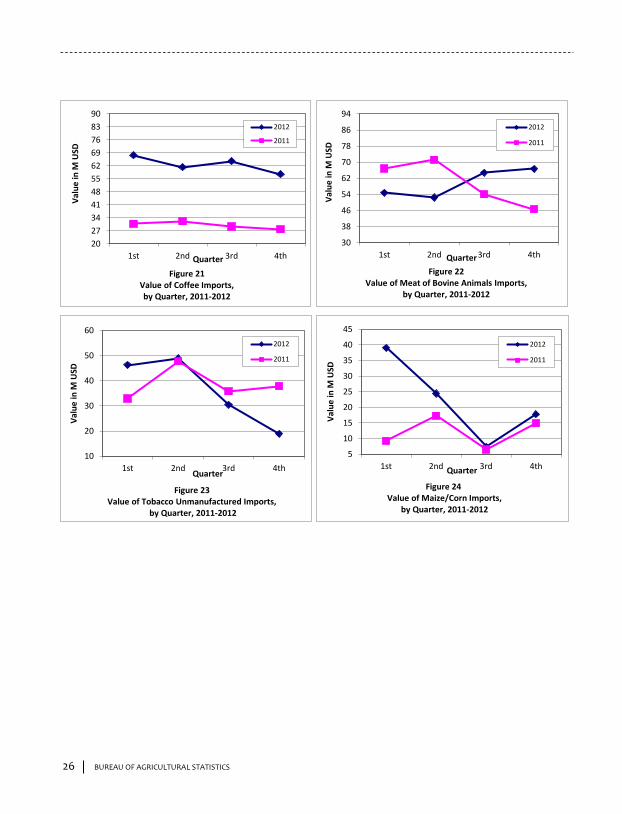

Coffee had the 7th

biggest agricultural import expenditure in 2012. From US$ 120.15 million in 2011, import expenditures increased to US$ 251.14 million or 109.02 percent growth. Most of our coffee imports came from Indonesia (56.19%); Vietnam (19.59%) and Malaysia (11.40%). Rice, the country’s 4

th top import commodity, recorded a 14.34 percent increase in

import expenditure from US$ 383.15 million in 2011 to US$ 438.08 million in 2012. Biggest importation in 2012 was recorded during the 3

rd quarter while the

least was posted in the 1st

quarter. Most of our rice imports (82.01%) were sourced from Vietnam; while the rest came from India, Pakistan, Myanmar, Thailand and other countries. Maize/corn importation grew by 84.35 percent at US$ 88.52 million in 2012 from US$ 48.02 million in 2011 moving to the 10

th top import commodity list of

2012. Heaviest importation was recorded during the first quarter at US$ 39.02 million while the least importation was during the third quarter at US$ 7.36 million. Corn was sourced largely from Thailand (35.04%), South Africa (25.54%) and Brazil (15.58%) and others.

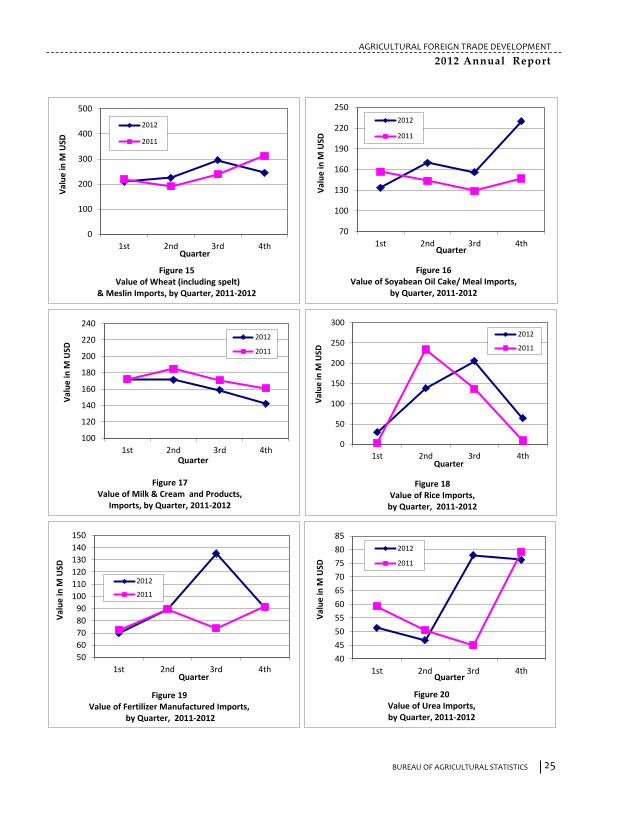

5. World Price Trends

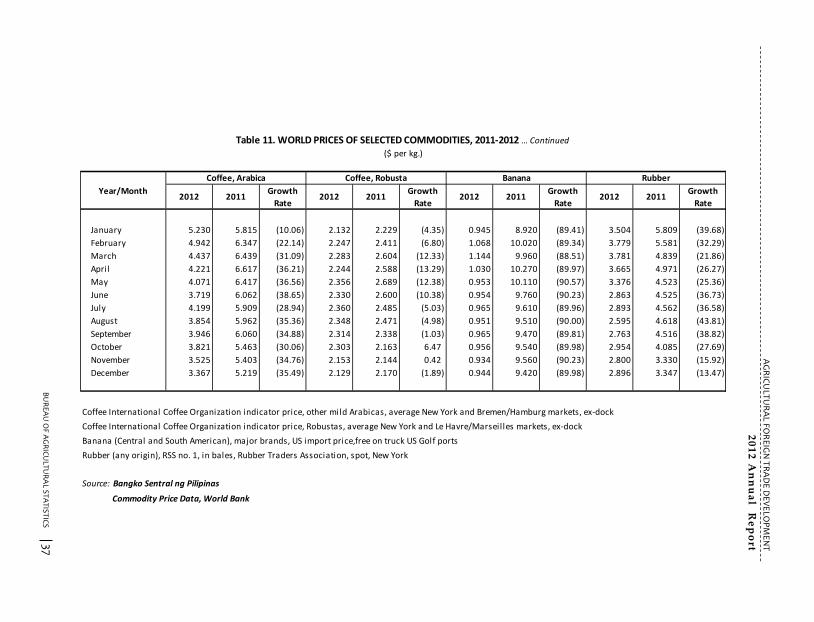

World prices were lower throughout 2012 for most of the monitored commodities - coconut oil, copra, sugar, maize, coffee, banana and rubber (Table 11).

Coconut oil and copra. Sustained downtrend in the prices of coconut oil and copra was noted from January to December of 2012. Price decreased by as much as 45% for both commodities. Price ranged from US$ 1.451/kg in January to US$ 0.785/kg in December for coconut oil. Prices of copra started at US$ 0.965/kg in January and were down to as low as US$ 0.526/kg in December. Sugar. Drop in the prices of sugar in the world market was observed through-out the year 2012. Highest price was posted in February at US $ 0.532/kg while the lowest price was during November and December at US$ 0.426/kg.

29 4 A

ust

ria

Be

lgiu

mC

ypru

sC

zech

Re

pu

blic

De

nm

ark

Esto

nia

Fin

lan

dFr

ance

Ge

rman

yG

ree

ceH

un

gary

Ire

lan

d

1.

Foo

d a

nd

Liv

e A

nim

als

0.1

08

26

.19

20

.83

50

.74

63

.24

20

.02

53

.71

91

2.5

33

87

.01

01

.90

90

.02

53

.53

1

A.

Live

An

ima

ls (

No

.)a

/0

.09

00

.00

5

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

a/

0.0

16

0.0

01

C.

Da

iry

Pro

du

cts

an

d B

ird

s Eg

gs

D.

Fish

an

d F

ish

Pre

pa

rati

on

s0

.07

06

.14

30

.56

20

.41

51

.67

52

.14

25

.49

27

2.5

32

1.6

24

0.0

02

1.8

07

E. C

erea

ls a

nd

Cer

eals

Pre

pa

rati

on

s0

.15

10

.12

60

.00

10

.04

50

.00

70

.03

50

.00

5

F. V

eget

ab

les

an

d F

ruit

s0

.03

51

9.6

93

0.0

25

0.3

31

1.5

54

0.0

25

1.5

76

6.6

99

13

.78

40

.18

80

.02

31

.68

5

G.

Suga

r a

nd

Su

gar

Pre

pa

rati

on

s0

.06

00

.00

1a

/a

/0

.00

10

.10

50

.38

8a

/

H.

Co

ffee

, Tea

, Co

coa

, Sp

ices

an

d

0.0

01

0.0

04

a/

a/

0.0

52

Ma

nu

fact

ure

s th

ereo

f

I. F

eed

ing

Stu

ff f

or

An

ima

ls

(exc

lud

ing

un

mil

led

Cer

eals

)

J. M

isce

lla

neo

us

Edib

le P

rod

uct

s a

nd

0

.00

30

.14

40

.11

7a

/ 0

.01

20

.10

20

.22

60

.06

10

.03

4

Pre

pa

rati

on

s

II.

Tob

acc

o a

nd

To

ba

cco

Ma

nu

fact

ure

s7

.96

80

.55

00

.00

10

.57

41

.33

20

.06

4

III.

Cru

de

Ma

teri

als

0.7

21

13

.59

90

.06

20

.02

91

2.0

37

0.0

25

7.3

77

7.1

26

0.1

57

0.1

40

1.0

08

A.

Oil

See

ds

an

d O

legi

no

us

Fru

its

B.

Cru

de

Ru

bb

er0

.03

4

C.

Cru

de

Fert

iliz

er

D.

Cru

de

An

ima

l a

nd

Veg

s. M

ate

ria

ls0

.72

11

3.5

99

0.0

62

0.0

29

12

.03

70

.02

57

.37

77

.09

20

.15

70

.14

01

.00

8

IV.

An

ima

l a

nd

Veg

eta

ble

Oil

an

d F

ats

1.4

52

0.0

69

0.4

43

0.0

02

0.2

49

0.2

77

14

.30

9

A.

An

ima

l a

nd

Veg

eta

ble

Oil

s a

nd

Fa

ts0

.89

80

.06

71

.21

4

B.

Fixe

d V

eget

ab

le O

il a

nd

Fa

ts0

.55

40

.06

90

.44

30

.00

20

.24

90

.21

01

3.0

95

V.

Fert

iliz

er M

an

ufa

ctu

red

VI.

Agr

icu

ltu

ral

Ch

emic

als

an

d M

ate

ria

ls0

.07

5a

/a

/ 0

.10

30

.11

8

VII

. A

gric

ult

ura

l M

ach

iner

y (N

o.)

0.0

02

0.0

15

0.0

85

Tota

l Val

ue

of

Agr

icu

ltu

ral E

xpo

rts

0.8

29

49

.28

50

.89

70

.84

31

6.2

74

0.0

27

3.9

94

20

.77

61

09

.96

62

.18

40

.22

94

.53

9

Tota

l Val

ue

of

Ph

ilip

pin

e E

xpo

rts

98

.16

63

02

.02

21

.90

89

7.5

15

36

.09

23

.83

21

15

.47

53

59

.61

91

95

6.0

92

31

.81

31

43

.20

42

8.5

98

a/

less

th

an

0.0

01

Sou

rce

of

ba

sic

da

ta: N

ati

on

al

Sta

tist

ics

Off

ice

(NSO

)

(F.O

.B. V

alu

e in

'00

0 U

S $

) EUR

OP

EAN

UN

ION

Tab

le 9

b.

DIS

TRIB

UTI

ON

OF

PH

ILIP

PIN

E A

GR

ICU

LTU

RA

L EX

PO

RTS

TO

EU

MEM

BER

CO

UN

TRIE

S, 2

01

2

Item

BUREAU OF AGRICULTURAL STATISTICS BUREAU OF AGRICULTURAL STATISTICS

AGRICULTURAL FOREIGN TRADE DEVELOPMENT

2012 Annual Report

Soybeans. Prices of soybeans were down from January to March and climbed up throughout the year at varied rates. Price peaked in August at US$ 0.684/kg.

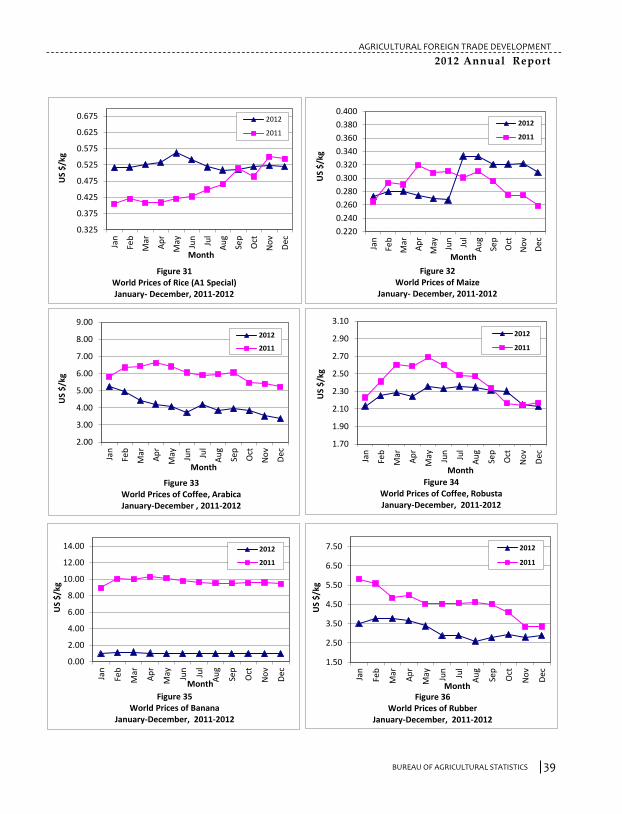

Rice. Uptrend in the international prices of rice 5% broken were recorded from January to August while downtrend from September to December of 2012. Price peaked in May at US$ 0.601/kg. Prices of rice 25% broken were decreasing at varied rates for most of the months except in January, July and August when price increases were posted. Highest price was recorded in July at US$ 0.555/kg. Prices of rice A1 Special moved up from January to August but slowed down in September, November and December. Price ranged from US$ 0.509/kg to US$ 0.562/kg. Maize (corn). In 2012, monthly fluctuations were observed in the prices of maize. Highest price was US$ 0.333/kg in July while lowest was US$ 0.267/kg in June. Coffee, Arabica. Coffee Arabica was relatively cheaper at the world market in 2012 compared to 2011. Price decreases were sustained throughout the year. Price ranged from US$ 3.367/kg, (December) to US$ 5.230/kg (January). Coffee, Robusta. Prices of Robusta Coffee were relatively lower in 2012; however prices were higher in October and November relative to 2011. Banana. Lower prices of banana were noted in the world market throughout 2012. Price cuts were from a low of 88.51 percent to a high of 90.23 percent compared to 2011. Prices ranged from US$ 0.934/kg to US$ 1.144 /kg. Rubber. Decreases were likewise noted on the world prices of rubber. Price ranged from US$ 2.595/kg to US$ 3.781/kg.

5 28

Ite

mTo

tal P

hili

pp

ine

Agr

icu

ltu

ral E

xpo

rts

Au

stra

liaJa

pan

USA

1.

Foo

d a

nd

Liv

e A

nim

als

3,1

97

.78

2

35

.73

5

6

20

.86

7

65

9.6

87

A

. Li

ve A

nim

als

(N

o.)

13

.91

9

0.0

13

1.4

41

0.9

28

B.

Mea

t a

nd

Mea

t P

rep

ara

tio

ns

67

.53

0

0.4

20

35

.40

2

1

.05

8

C

. D

air

y P

rod

uct

s a

nd

Bir

ds

Eggs

88

.37

2

0.1

86

0.1

22

0.9