Agenda item 9 Discussions on Topics for FAS Work Plan 2014-2016

Agenda item 9 Discussions on Topics for FAS Work Plan 2014-2016.

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Agenda item 9

Discussions on Topics for FAS Work Plan 2014-2016

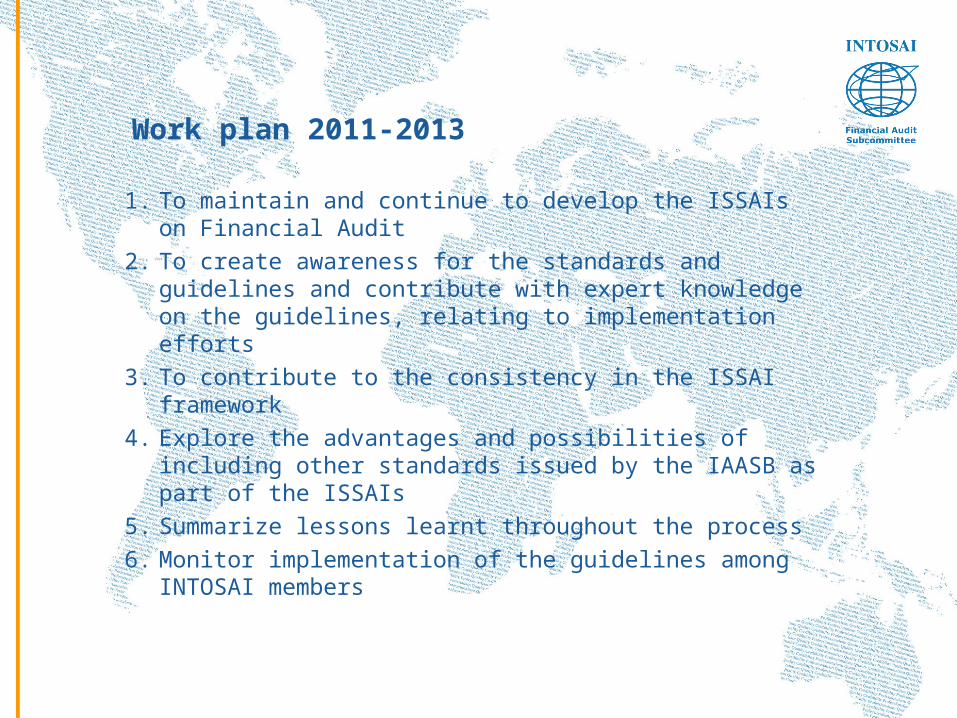

Work plan 2011-2013

1. To maintain and continue to develop the ISSAIs on Financial Audit

2. To create awareness for the standards and guidelines and contribute with expert knowledge on the guidelines, relating to implementation efforts

3. To contribute to the consistency in the ISSAI framework

4. Explore the advantages and possibilities of including other standards issued by the IAASB as part of the ISSAIs

5. Summarize lessons learnt throughout the process6. Monitor implementation of the guidelines among

INTOSAI members

1. To maintain and continue to develop the ISSAIs on Financial Audit

• Goal attended to, new PN 610 will be handled in this meeting. New PN 720 will be up next year.

• Goal considered relevant for coming period• New ISA projects• Need for clarifications of PNs due to

comments received during implementation• Other needs for development?

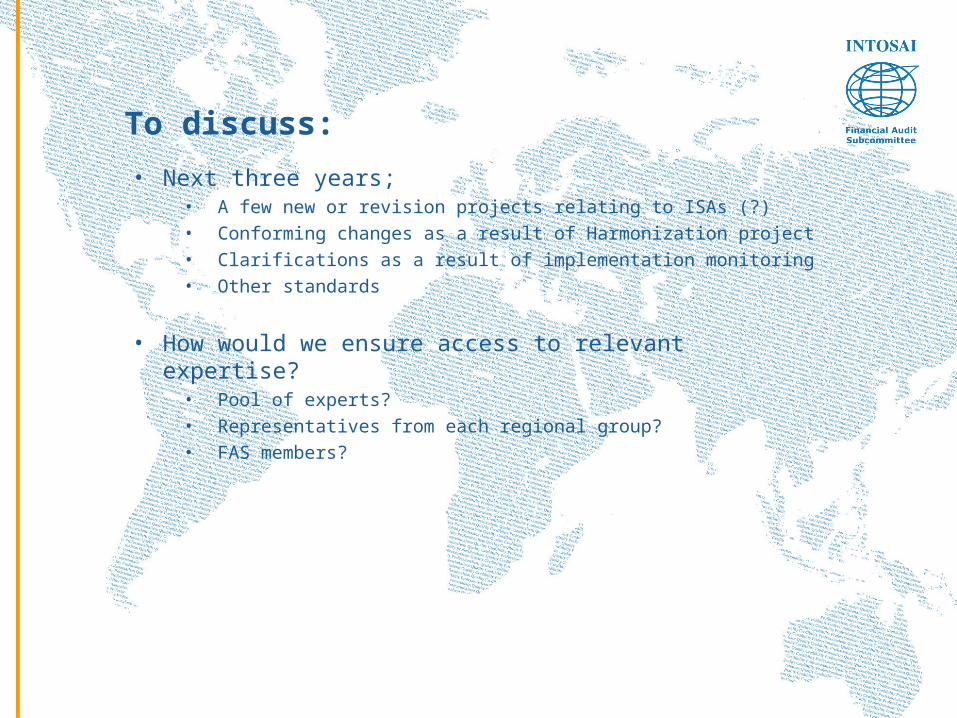

To discuss:

• Next three years;• A few new or revision projects relating to ISAs (?)• Conforming changes as a result of Harmonization project• Clarifications as a result of implementation monitoring• Other standards

• How would we ensure access to relevant expertise? • Pool of experts? • Representatives from each regional group? • FAS members?

2. To create awareness for the standards and guidelines and contribute with expert knowledge on the guidelines, relating to implementation efforts

• Activities so far: • INTOSAI Journal,• Key persons• Awareness raising material presented on

website• Awareness raising seminars and speeches

• Goal partly relevant for next period, especially expertise knowledge

• Support IDI?

To discuss:

• Who should be most efficient to approach? • Who should be involved?• What kind of presentation, awareness

raising, or training material do we need to develop?

• Need for more detailed implementation guidance?

3. To contribute to the consistency in the ISSAI framework • Goal attended to through participation in

Harmonization Project• May include the need for conforming

changes of existing guidelines• Such changes needs to be attended to

before 2013• Goal may be relevant if new PSC harmonization

initiatives are decided (ISSAI 30)

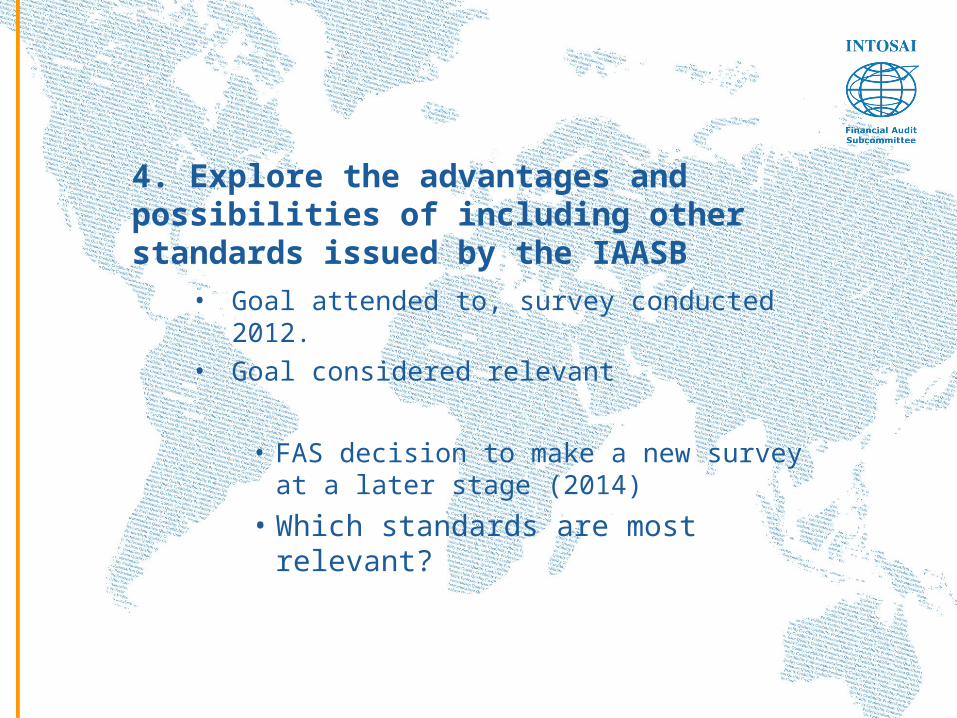

4. Explore the advantages and possibilities of including other standards issued by the IAASB

• Goal attended to, survey conducted 2012. • Goal considered relevant

• FAS decision to make a new survey at a later stage (2014)

• Which standards are most relevant?

Additional standards of possible relevance

International Standards on Review Engagements (ISREs)

ISRE 2400, Engagements to Review Financial StatementsISRE 2410, Review of Interim Financial Information Performed by the Independent Auditor of the Entity

International Standards on Assurance Engagements (ISAEs)

ISAE 3000, Assurance Engagements Other than Audits or Reviews of Historical Financial InformationISAE 3400, The Examination of Prospective Financial InformationISAE 3410, Assurance on a Greenhouse Gas StatementISAE 3420, Assurance on the Process to Compile Pro Forma Financial Information Included in a Prospectus

International Standards on Related Services (ISRSs)

ISRS 4400, Engagements to Perform Agreed-upon Procedures Regarding Financial InformationISRS 4410, Engagements to Compile Financial Statements

Other areas that might need guidance

• Guidance for SAIs with responsibilities related to fraud in an audit of financial statements?

• Guidance for SAIs with responsibilities related to environmental issues (sustainability reports) in an audit of financial statements?

• Guidance for SAIs with responsibilities to report on internal controls in an audit of financial statements?

• Guidance for Sais with responsibilities to perform Budget Execution Audits?

To discuss:

• How do we best approach the need for additional relevant IAASB standards (survey, public consultation paper, use of KP, regional groups)?

• If we launch a survey, how would such a survey be conducted (web-based, hearings)?

• Are there areas, in addition to possible IAASB assurance standards, we need to consider as part of the broader mandate for a financial audit in the public sector?

5. Summarize lesson learnt

• Carry out a review of lessons learnt by different actors relevant to FAS’ work.

• Draw conclusions on lessons learnt and share them with relevant stakeholders.

• FAS decision to replace this with “chairmans reflections”

6. Monitor implementation of the guidelines among INTOSAI members.

• Pre-implementation monitoring activities

• Post-implementation activities

Pre-implementation monitoring activities

• Main purpose is to identify those that have decided to implement and, if possible, receive early alerts on needs for clarifications

• Pre-implementation questions sent out to key persons;

• Has your organization decided to implement the ISSAIs for Financial Audit?• Yes, we will implement/have implemented the ISSAIs as the authoritative standard.• Yes, we will implement/have implemented the ISSAIs as guidance to support other

standards (if so, please specify which standards).• No, but we will implement/have implemented the ISAs as the authoritative standard• No, but we are considering implementing the ISSAIs for Financial Audit.• No, and we are not considering implementing the ISSAIs.

Pre-implementation monitoring activities

• If you have decided to implement the ISSAIs for Financial Audit, how will you go about the implementation process?

• We will implement/have implemented the ISSAIs all at once.• We will implement/have implemented the ISSAIs step by step.• We were already working in accordance with the ISAs and only require

minor adjustments to our current audit approach.

• Discussions:• Do we need to approach a larger number of

SAIs, and if so, how can we approach them?• Additional information needed?

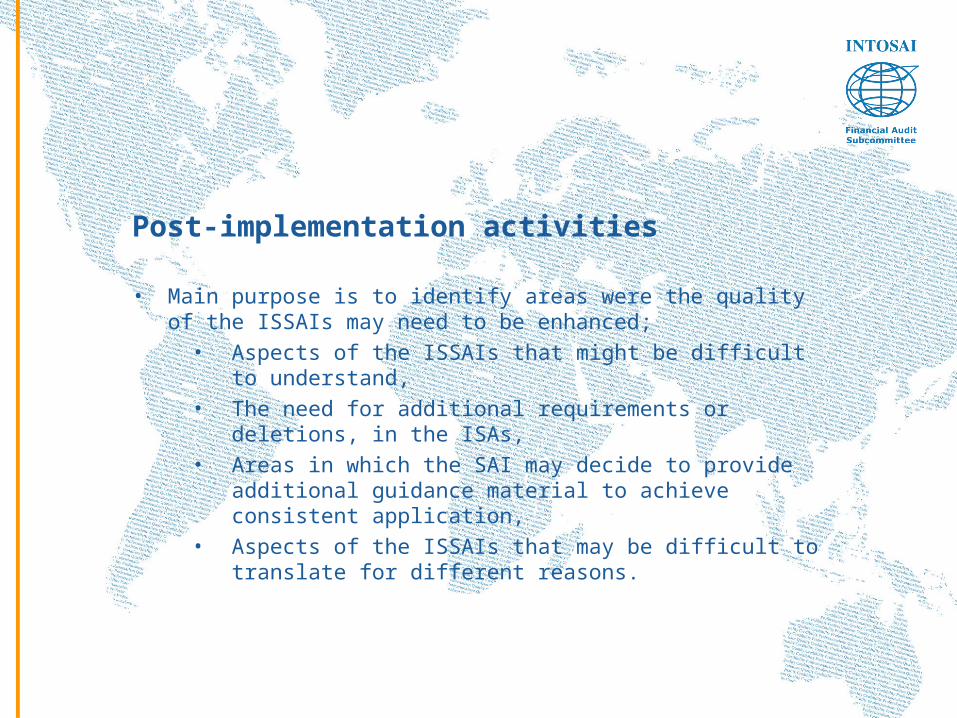

Post-implementation activities

• Main purpose is to identify areas were the quality of the ISSAIs may need to be enhanced;

• Aspects of the ISSAIs that might be difficult to understand,

• The need for additional requirements or deletions, in the ISAs,

• Areas in which the SAI may decide to provide additional guidance material to achieve consistent application,

• Aspects of the ISSAIs that may be difficult to translate for different reasons.

Post-implementation activities

• Will need a more comprehensive survey and best undertaken when a significant number of SAIs have implemented.

• To discuss:• How?• Timing?• Who?

Related Documents