African Tax Administration Paper 18 Who can make Ugandan taxpayers more compliant? Ronald Waiswa, Doris Akol and Milly Nalukwago Isingoma July 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

African Tax Administration Paper 18

Who can make Ugandan taxpayers morecompliant?Ronald Waiswa, Doris Akol and Milly Nalukwago Isingoma

July 2020

ICTD African Tax Administration Paper 18 Who can make Ugandan taxpayers more compliant? Ronald Waiswa, Doris Akol and Milly Nalukwago Isingoma July 2020

2

Who can make Ugandan taxpayers more compliant? Ronald Waiswa, Doris Akol and Milly Nalukwago Isingoma ICTD African Tax Administration Paper 18 First published by the Institute of Development Studies in July 2020 © Institute of Development Studies 2020 ISBN: 978-1-78118-665-7

This is an Open Access paper distributed under the terms of the Creative Commons Attribution Non Commercial 4.0 International license, which permits downloading and sharing provided the original authors and source are credited – but the work is not used for commercial purposes. http://creativecommons.org/licenses/by-nc/4.0/legalcode Available from: The International Centre for Tax and Development at the Institute of Development Studies, Brighton BN1 9RE, UK Tel: +44 (0) 1273 606261 Email: [email protected] Web: www.ictd.ac/publication Twitter: @ICTDTax Facebook: www.facebook.com/ICTDtax IDS is a charitable company limited by guarantee and registered in England Charity Registration Number 306371 Charitable Company Number 877338

3

Who can make Ugandan taxpayers more compliant? Ronald Waiswa, Doris Akol and Milly Nalukwago Isingoma Summary The rate of occurrence of tax evasion is higher in Uganda than in the rest of East Africa. Where the taxpayer has latitude to decide whether or not to be compliant, as in the case of income taxes, Ugandans seem to be less compliant than other East Africans. Uganda collects less in domestic taxes than other countries in the region. For revenue, the Ugandan government depends more on customs duties, on taxes that are difficult to dodge, notably Withholding Tax, and on taxes where there are in-built incentives to comply, such as Value Added Tax (VAT). The framework for improving tax compliance consists of three broad channels: making it easier for taxpayers to comply (facilitation), enforcement and increasing trust (in the government, in its spending practices, and in the tax collection agency itself). Using this framework, we discuss the measures that have been adopted by the Uganda Revenue Authority (URA) and the Government of Uganda, the successes achieved and the gaps that remain. The URA is best placed for facilitation. It also plays a major role in enforcement, although its efforts may be either supported or undermined by the government and politicians. The URA can do little to increase trust in the government in general; that is principally a job for the government. The URA can mainly make itself more trustworthy in the eyes of taxpayers by being transparent and minimising corruption. We find that URA has been successful in facilitating tax compliance, although there are opportunities for improvements on its current initiatives. The URA’s enforcement actions are, however, weak and limited. To a large extent, they have been undermined by the government and politicians. Enforcement has also been weak, due to internal URA factors, such as the understaffing of the enforcement team and the fact that the URA does not take enforcement action as often on small taxpayers. Lastly, very little has been done to build taxpayer morale. There are widespread concerns over the poor use of tax money, missing or poor government services and some sections of society being shielded from paying their share, because of their connections or roles in government. The URA is also not highly trusted and corruption is still a major problem among tax collectors. To build trust in the government, the URA is undertaking some of the tasks of justifying tax collection that would normally be undertaken by another part of government. There is a lot of scope for both the government and URA to gain more trust from the taxpayer. Improving tax compliance in Uganda will require the government (in the sense of the executive) and the URA to work more together. The government should give more support to URA activities, desist from protecting non-compliant taxpayers and be accountable to the public for the revenues collected. The URA needs to improve its trust-building initiatives and address some internal weaknesses. Keywords: tax compliance, tax reforms, revenue administration, political interference, facilitation, enforcement, trust. Ronald Waiswa is a supervisor for Research and Policy Analysis at Uganda Revenue Authority’s Research, Planning and Development Division. He also heads research and

4

training at Lida Africa. He has collaborated with ICTD on a number of research projects in Uganda and Ethiopia on issues, including taxing wealthy individuals and public sector agencies. Doris Akol is a Ugandan lawyer and administrator. At time of writing this paper, she was the Commissioner General of Uganda Revenue Authority. She has over 23 years’ experience in tax administration. Prior to becoming Commissioner General, she served as the Commissioner for Legal Services and Board Affairs. Milly Nalukwago Isingoma is the Assistant Commissioner for Research, Planning and Development at the URA. She is also the URA head of Delegation to the East African Revenue Authorities Technical Committee and a member of ICTD’s Centre Advisory Group.

5

Contents Summary 3 Acknowledgements 7 Acronyms 7 Introduction 8 1 Framework for improving tax compliance 10 2 Facilitation 10 2.1 Automation of tax services 11 2.2 Taxpayer education 12 2.3 Creating tax offices in all major towns across the country and 44 OSS 14 2.4 Staff motivation 15 3 Enforcement 15 3.1 Understaffing of the enforcement team 17 3.2 Little attention given to small taxpayers 18 4 Creating trust in the government and the URA 19 4.1 Creating trust in the government 20 4.1.1 Poor government spending practices 20 4.1.2 Unfair taxation where some are not paying their share because of 23 their connections to or role in government 4.1.3 Publishing government works: My Taxes Work publication and video 24 4.1.4 Because of You campaigns 24 4.1.5 Taxpayer Appreciation Days (TPAD) 25 4.2 Creating trust in the URA 26 4.2.1 Press briefs 27 4.2.2 Corporate Social Responsibility (CSR) 27 4.2.3 Open Minds Forum (OMF) 28 5 Summary and conclusion 29 References 31 Appendices 34 Appendix 1 Table A1 Respondents (taxpayers) characteristics 34 Appendix 2 Table A2 the URA Corporate Social Responsibility over time 35 Tables and Figures Table 0.1 Tax to GDP ratios over time 8 Table 0.2 Comparative income tax performance indicators 8 Figure 0.1 Domestic tax and customs contribution to tax revenue in 2017/18 9 Table 2.1 Taxpayer opinions on the tax system (electronic systems) 12 Table 2.2 Ability to use e-tax for the following business processes 12 Figure 2.1 Tax education annual budget allocations 13 Table 2.3 Tax education activities from FY2017/18–FY2018/19 13 Table 2.4 Which URA tax education programmes are you aware of? 14 Table 2.5 Taxpayer opinions on the tax system 15 Figure 4.1 Reactions to the URA’s letter appreciating taxpayers for a revenue 21

6

surplus in 2018/19

Table 4.1 Taxpayers’ views on how taxes are used 22 Figure 4.2 Staff opinions on the fairness of the tax system 23 Figure 4.3 ‘The tax system only benefits the rich and those connected to them 24 and is not fair to ordinary people’ Table 4.2 Taxpayers’ opinions on the effectiveness of the government works 24 publication Figure 4.4 Taxpayers’ opinions on the effectiveness of the TPAD 26 Table 4.3 Taxpayer opinions on the tax system 26 Figure 4.5 Taxpayers’ opinions on the effectiveness of press briefs 27 Table 4.4 Taxpayers’ opinions on the effectiveness of the URA initiatives 29

7

Acknowledgements We are greatly indebted to Professor Mick Moore who made a significant contribution to this paper. He guided us, supervised the whole process and sent us constant reminders to complete the paper. We also thank Susan Nakato for her useful comments on earlier drafts of this paper. We thank our colleagues in the Research and Modelling unit at URA who contributed to this research in various respects, and all those who participated in this research through interviews.

Acronyms ASYCUDA Automated System for Customs Data ATAF African Tax Administration Forum CAO Chief Administrative Officer CIT Corporate Income tax CSR Corporate Social Responsibility DCU Debt Collection Unit E-hub Localised name for URA data warehouse E-tax Domestic taxpayer management system used by the URA FIRs Federal Inland Revenue Services Forex Foreign Exchange Market FY Fiscal year IMF International Monetary Fund ITA Income Tax Act KCCA Kampala Capital City Authority LC5 Local Council V LG Local government MoFPED Ministry of Finance Planning and Economic Development NIN National Identification Number OECD Organisation for Economic Co-operation and Development OMF Open Minds Forum OSS One stop centre shop PAYE Pay As You Earn PIT Personal Income tax PSO Public Sector Tax Office RDC Resident District Commissioner SME Small and medium-sized enterprises TADAT Tax Administration Diagnostic Assessment Tool TIN Tax Identification Number TPAD Taxpayer Appreciation Days TREP Taxpayer Register Expansion Program TSS Taxpayer Service Strategy URA Uganda Revenue Authority URSB Uganda Registration Services Bureau VAT Value Added Tax

8

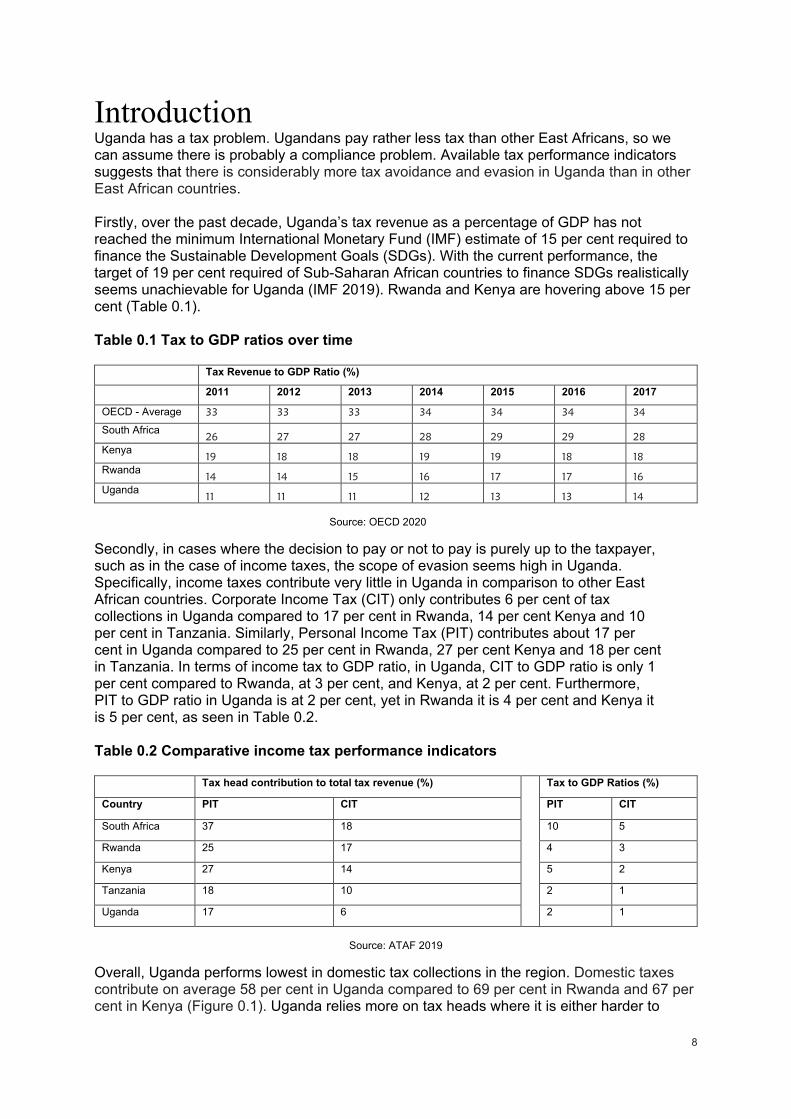

Introduction Uganda has a tax problem. Ugandans pay rather less tax than other East Africans, so we can assume there is probably a compliance problem. Available tax performance indicators suggests that there is considerably more tax avoidance and evasion in Uganda than in other East African countries. Firstly, over the past decade, Uganda’s tax revenue as a percentage of GDP has not reached the minimum International Monetary Fund (IMF) estimate of 15 per cent required to finance the Sustainable Development Goals (SDGs). With the current performance, the target of 19 per cent required of Sub-Saharan African countries to finance SDGs realistically seems unachievable for Uganda (IMF 2019). Rwanda and Kenya are hovering above 15 per cent (Table 0.1). Table 0.1 Tax to GDP ratios over time

Tax Revenue to GDP Ratio (%)

2011 2012 2013 2014 2015 2016 2017

OECD - Average 33 33 33 34 34 34 34 South Africa

26 27 27 28 29 29 28 Kenya

19 18 18 19 19 18 18 Rwanda

14 14 15 16 17 17 16 Uganda

11 11 11 12 13 13 14

Source: OECD 2020

Secondly, in cases where the decision to pay or not to pay is purely up to the taxpayer, such as in the case of income taxes, the scope of evasion seems high in Uganda. Specifically, income taxes contribute very little in Uganda in comparison to other East African countries. Corporate Income Tax (CIT) only contributes 6 per cent of tax collections in Uganda compared to 17 per cent in Rwanda, 14 per cent Kenya and 10 per cent in Tanzania. Similarly, Personal Income Tax (PIT) contributes about 17 per cent in Uganda compared to 25 per cent in Rwanda, 27 per cent Kenya and 18 per cent in Tanzania. In terms of income tax to GDP ratio, in Uganda, CIT to GDP ratio is only 1 per cent compared to Rwanda, at 3 per cent, and Kenya, at 2 per cent. Furthermore, PIT to GDP ratio in Uganda is at 2 per cent, yet in Rwanda it is 4 per cent and Kenya it is 5 per cent, as seen in Table 0.2. Table 0.2 Comparative income tax performance indicators

Tax head contribution to total tax revenue (%)

Tax to GDP Ratios (%)

Country PIT CIT PIT CIT

South Africa 37 18 10 5

Rwanda 25 17 4 3

Kenya 27 14 5 2

Tanzania 18 10 2 1

Uganda 17 6 2 1

Source: ATAF 2019

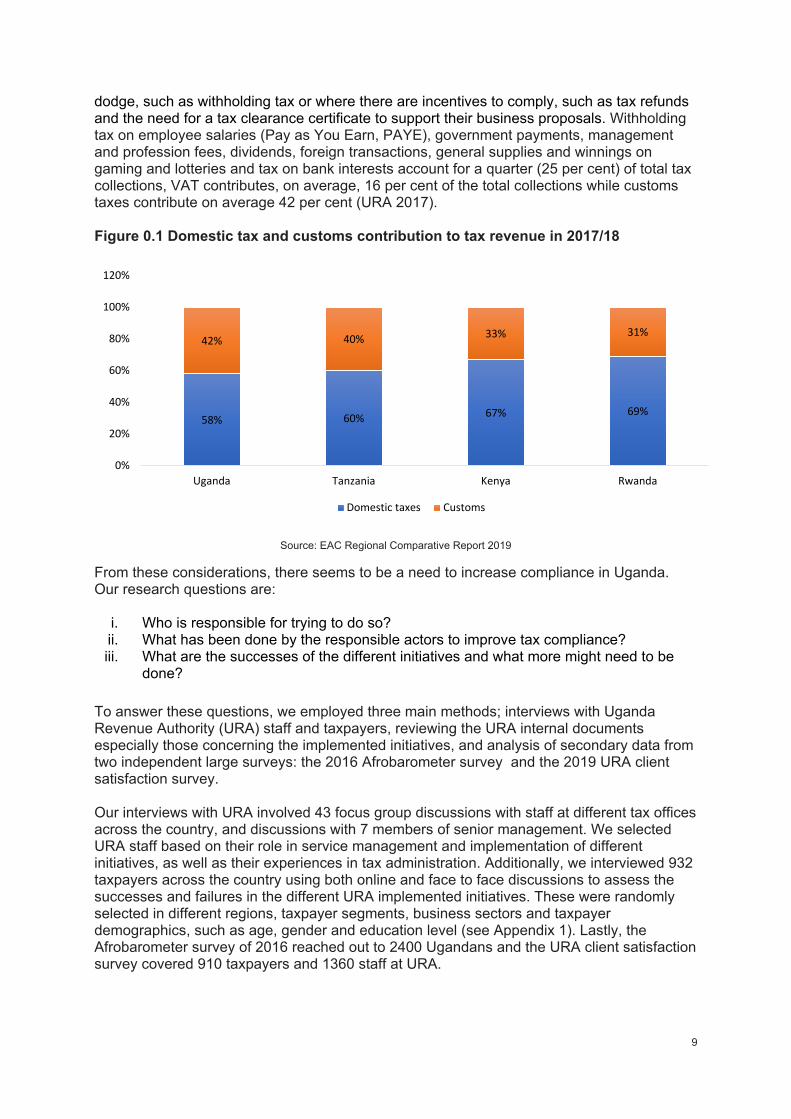

Overall, Uganda performs lowest in domestic tax collections in the region. Domestic taxes contribute on average 58 per cent in Uganda compared to 69 per cent in Rwanda and 67 per cent in Kenya (Figure 0.1). Uganda relies more on tax heads where it is either harder to

9

dodge, such as withholding tax or where there are incentives to comply, such as tax refunds and the need for a tax clearance certificate to support their business proposals. Withholding tax on employee salaries (Pay as You Earn, PAYE), government payments, management and profession fees, dividends, foreign transactions, general supplies and winnings on gaming and lotteries and tax on bank interests account for a quarter (25 per cent) of total tax collections, VAT contributes, on average, 16 per cent of the total collections while customs taxes contribute on average 42 per cent (URA 2017). Figure 0.1 Domestic tax and customs contribution to tax revenue in 2017/18

Source: EAC Regional Comparative Report 2019 From these considerations, there seems to be a need to increase compliance in Uganda. Our research questions are:

i. Who is responsible for trying to do so? ii. What has been done by the responsible actors to improve tax compliance? iii. What are the successes of the different initiatives and what more might need to be

done? To answer these questions, we employed three main methods; interviews with Uganda Revenue Authority (URA) staff and taxpayers, reviewing the URA internal documents especially those concerning the implemented initiatives, and analysis of secondary data from two independent large surveys: the 2016 Afrobarometer survey and the 2019 URA client satisfaction survey. Our interviews with URA involved 43 focus group discussions with staff at different tax offices across the country, and discussions with 7 members of senior management. We selected URA staff based on their role in service management and implementation of different initiatives, as well as their experiences in tax administration. Additionally, we interviewed 932 taxpayers across the country using both online and face to face discussions to assess the successes and failures in the different URA implemented initiatives. These were randomly selected in different regions, taxpayer segments, business sectors and taxpayer demographics, such as age, gender and education level (see Appendix 1). Lastly, the Afrobarometer survey of 2016 reached out to 2400 Ugandans and the URA client satisfaction survey covered 910 taxpayers and 1360 staff at URA.

58% 60% 67% 69%

42% 40% 33% 31%

0%

20%

40%

60%

80%

100%

120%

Uganda Tanzania Kenya Rwanda

Domestic taxes Customs

10

1 Framework for Improving Tax Compliance Broadly, there are three ways of increasing tax compliance:

i. facilitation, ii. enforcement, and iii. creating trust in the government and its tax and spending practices, so that people

are more willing to pay, as well as creating trust in the tax collection agency (Prichard, Custers, Dom, Davenport and Roscitt 2019)

There are two main sets of actors that can execute these methods: the tax collection agency and the government (meaning the central executive and Ministry of Finance). The tax collection agency has the greatest degree of control in relation to facilitation. It also plays a major role in enforcement, although its efforts may either be supported or undermined by the government and politicians. The tax collection agency plays the lowest potential role in creating trust in the government generally; that is basically a job for government. The role of the tax collection agency in creating public trust lies in ensuring that the public trusts its work where it can be seen, that it is a transparent agency and that its staff are not corrupt. In the next three sections, we discuss each of these terms in detail, what the URA and/or the government have been doing in terms of these methods, the successes realised and what more needs to be done and by whom.

2 Facilitation Facilitation recognises the role of the tax collection agency as a provider of services and information that should make compliance “as easy as possible”. It also involves making tax administrations “customer friendly”, with taxpayers treated as clients rather than potential criminals. Facilitation can be done in three broad ways:

i. Teaching taxpayers about tax laws and tax systems. Not all non-compliance is deliberate. Some taxpayers just don’t know how to comply (Kangave, Nakato, Waiswa and Lumala 2016; Okello 2014). By training them, they are equipped to be able to navigate complex tax systems and therefore more likely to comply. In Rwanda, for instance, a tax training for newly registered taxpayers increased the attendees’ probability to declare by 27 per cent compared to those who did not attend. It also had a significant and relatively large impact on nil-filing and tax amounts (Mascagni, Santoro and Mukama 2019). Aside from improving the likelihood of tax compliance, tax trainings reduce taxpayer vulnerability caused by expensive tax agents and corrupt tax officials. Similarly, informed taxpayers are able to take advantage of the tax benefits available to them, such as allowable deductions, hence protecting them from paying more than they should (ibid). Aondo and Sile (2018) examine 142 Small and Medium-sized Enterprises (SMEs) operating within the township of Nakuru in Kenya, concentrating within the manufacturing, trade and services sectors. They found that SME owners with greater knowledge of tax laws and policies tend to pay taxes at lower rates, as they are able to take advantage of the available allowable deductions.

11

ii. Simplifying the process of complying. Specific mechanisms include: (a) providing simplified but sufficient information about tax laws and tax systems; (b) simplifying tax systems and related reporting requirements; (c) simplifying tax laws and regulations such as presumptive tax regimes for small businesses; (d) offering free support and advice to taxpayers; (e) providing simple methods for making tax payments, including online, at banks and via SMS; and (f) reducing interactions between taxpayers and tax collectors, hence reducing on unnecessary delays and risks of abuse of the taxpayers, (Prichard et al. 2019).

iii. Reducing the scope of harassment and abuse by tax officials, especially at the point

of making tax payments. This can be achieved through increased staff monitoring, reducing face to face contact with tax officials, reducing officials’ discretion, as well as motivating tax collectors through pay increases, performance contracts etc. to the extent that they can offer a friendly service to taxpayers, (ibid).

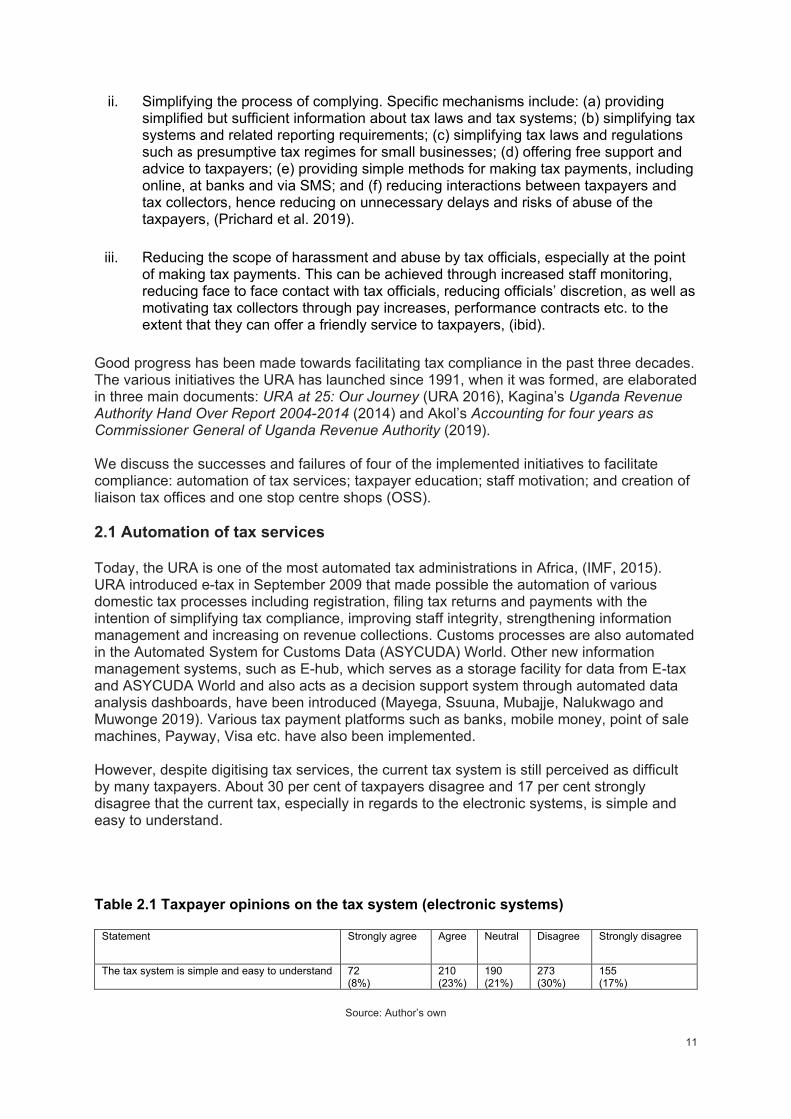

Good progress has been made towards facilitating tax compliance in the past three decades. The various initiatives the URA has launched since 1991, when it was formed, are elaborated in three main documents: URA at 25: Our Journey (URA 2016), Kagina’s Uganda Revenue Authority Hand Over Report 2004-2014 (2014) and Akol’s Accounting for four years as Commissioner General of Uganda Revenue Authority (2019). We discuss the successes and failures of four of the implemented initiatives to facilitate compliance: automation of tax services; taxpayer education; staff motivation; and creation of liaison tax offices and one stop centre shops (OSS). 2.1 Automation of tax services Today, the URA is one of the most automated tax administrations in Africa, (IMF, 2015). URA introduced e-tax in September 2009 that made possible the automation of various domestic tax processes including registration, filing tax returns and payments with the intention of simplifying tax compliance, improving staff integrity, strengthening information management and increasing on revenue collections. Customs processes are also automated in the Automated System for Customs Data (ASYCUDA) World. Other new information management systems, such as E-hub, which serves as a storage facility for data from E-tax and ASYCUDA World and also acts as a decision support system through automated data analysis dashboards, have been introduced (Mayega, Ssuuna, Mubajje, Nalukwago and Muwonge 2019). Various tax payment platforms such as banks, mobile money, point of sale machines, Payway, Visa etc. have also been implemented. However, despite digitising tax services, the current tax system is still perceived as difficult by many taxpayers. About 30 per cent of taxpayers disagree and 17 per cent strongly disagree that the current tax, especially in regards to the electronic systems, is simple and easy to understand. Table 2.1 Taxpayer opinions on the tax system (electronic systems)

Statement Strongly agree Agree Neutral Disagree Strongly disagree

The tax system is simple and easy to understand

72 (8%)

210 (23%)

190 (21%)

273 (30%)

155 (17%)

Source: Author’s own

12

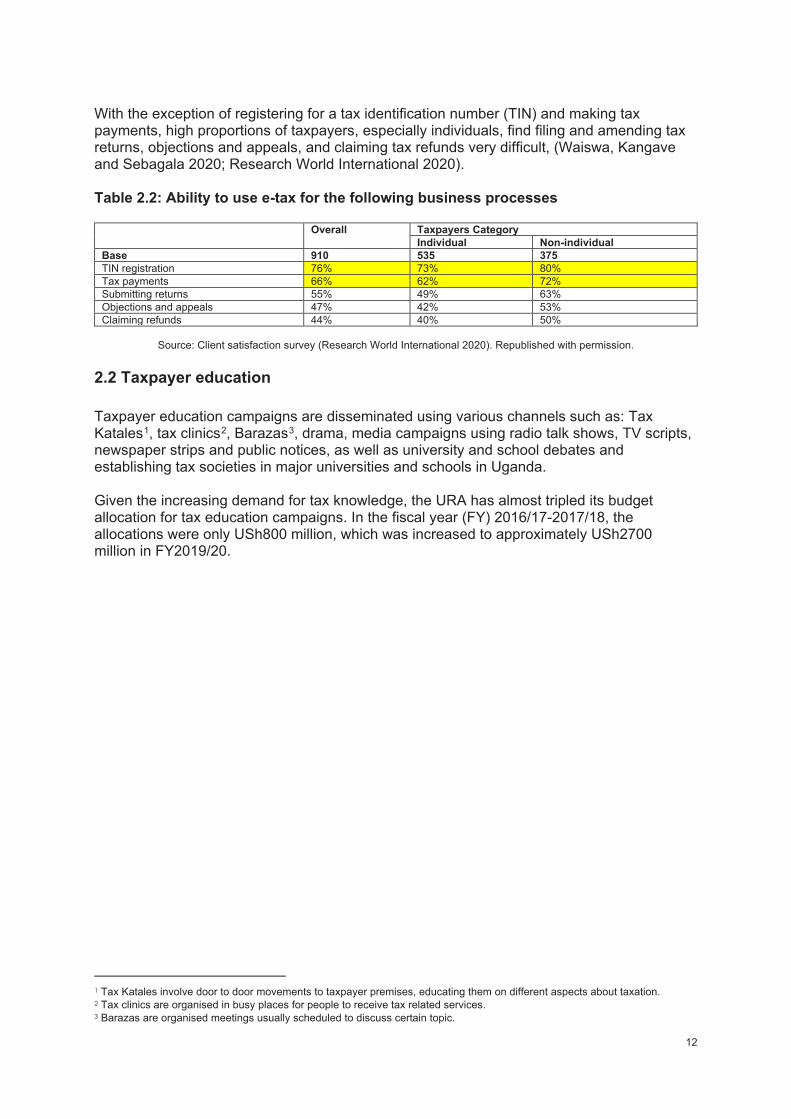

With the exception of registering for a tax identification number (TIN) and making tax payments, high proportions of taxpayers, especially individuals, find filing and amending tax returns, objections and appeals, and claiming tax refunds very difficult, (Waiswa, Kangave and Sebagala 2020; Research World International 2020). Table 2.2: Ability to use e-tax for the following business processes

Overall Taxpayers Category Individual Non-individual

Base 910 535 375 TIN registration 76% 73% 80% Tax payments 66% 62% 72% Submitting returns 55% 49% 63% Objections and appeals 47% 42% 53% Claiming refunds 44% 40% 50%

Source: Client satisfaction survey (Research World International 2020). Republished with permission.

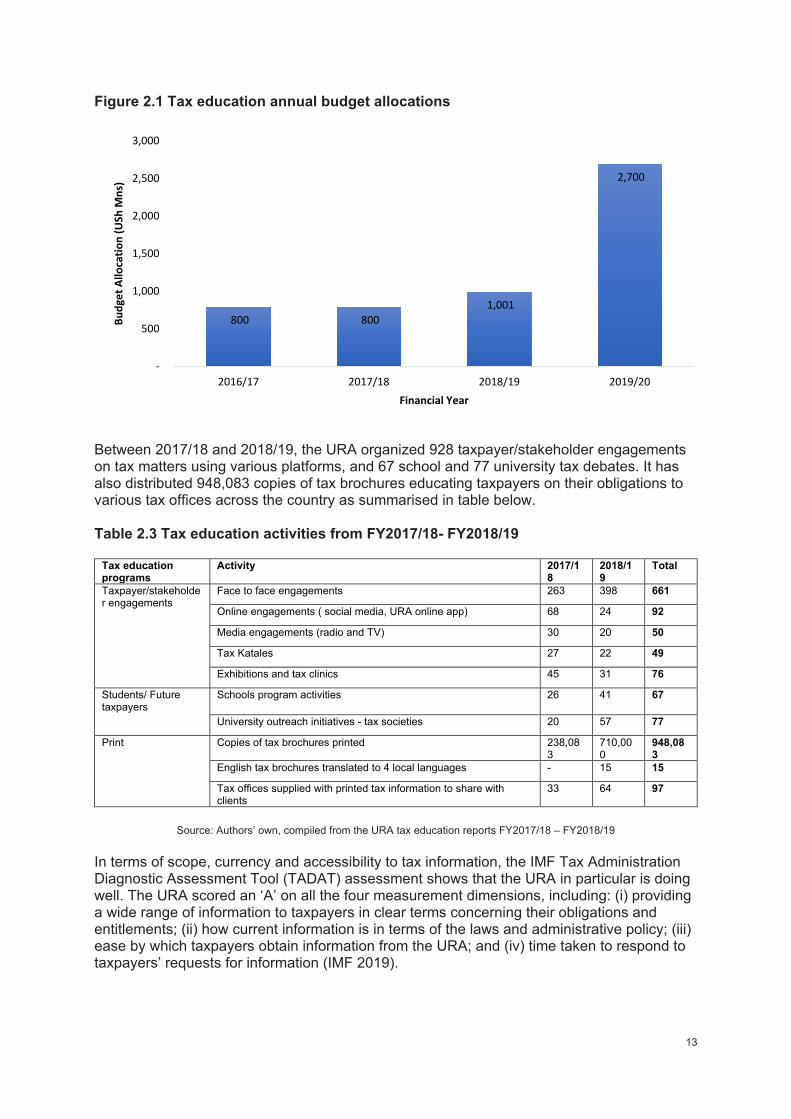

2.2 Taxpayer education Taxpayer education campaigns are disseminated using various channels such as: Tax Katales1, tax clinics2, Barazas3, drama, media campaigns using radio talk shows, TV scripts, newspaper strips and public notices, as well as university and school debates and establishing tax societies in major universities and schools in Uganda. Given the increasing demand for tax knowledge, the URA has almost tripled its budget allocation for tax education campaigns. In the fiscal year (FY) 2016/17-2017/18, the allocations were only USh800 million, which was increased to approximately USh2700 million in FY2019/20.

1 Tax Katales involve door to door movements to taxpayer premises, educating them on different aspects about taxation. 2 Tax clinics are organised in busy places for people to receive tax related services. 3 Barazas are organised meetings usually scheduled to discuss certain topic.

13

Figure 2.1 Tax education annual budget allocations

Between 2017/18 and 2018/19, the URA organized 928 taxpayer/stakeholder engagements on tax matters using various platforms, and 67 school and 77 university tax debates. It has also distributed 948,083 copies of tax brochures educating taxpayers on their obligations to various tax offices across the country as summarised in table below. Table 2.3 Tax education activities from FY2017/18- FY2018/19

Tax education programs

Activity 2017/18

2018/19

Total

Taxpayer/stakeholder engagements

Face to face engagements 263 398 661

Online engagements ( social media, URA online app) 68 24 92

Media engagements (radio and TV) 30 20 50

Tax Katales 27 22 49

Exhibitions and tax clinics 45 31 76

Students/ Future taxpayers

Schools program activities 26 41 67

University outreach initiatives - tax societies 20 57 77

Print Copies of tax brochures printed 238,083

710,000

948,083

English tax brochures translated to 4 local languages - 15 15

Tax offices supplied with printed tax information to share with clients

33 64 97

Source: Authors’ own, compiled from the URA tax education reports FY2017/18 – FY2018/19

In terms of scope, currency and accessibility to tax information, the IMF Tax Administration Diagnostic Assessment Tool (TADAT) assessment shows that the URA in particular is doing well. The URA scored an ‘A’ on all the four measurement dimensions, including: (i) providing a wide range of information to taxpayers in clear terms concerning their obligations and entitlements; (ii) how current information is in terms of the laws and administrative policy; (iii) ease by which taxpayers obtain information from the URA; and (iv) time taken to respond to taxpayers’ requests for information (IMF 2019).

800 800 1,001

2,700

-

500

1,000

1,500

2,000

2,500

3,000

2016/17 2017/18 2018/19 2019/20

Budg

et A

lloca

tion

(USh

Mns

)

Financial Year

14

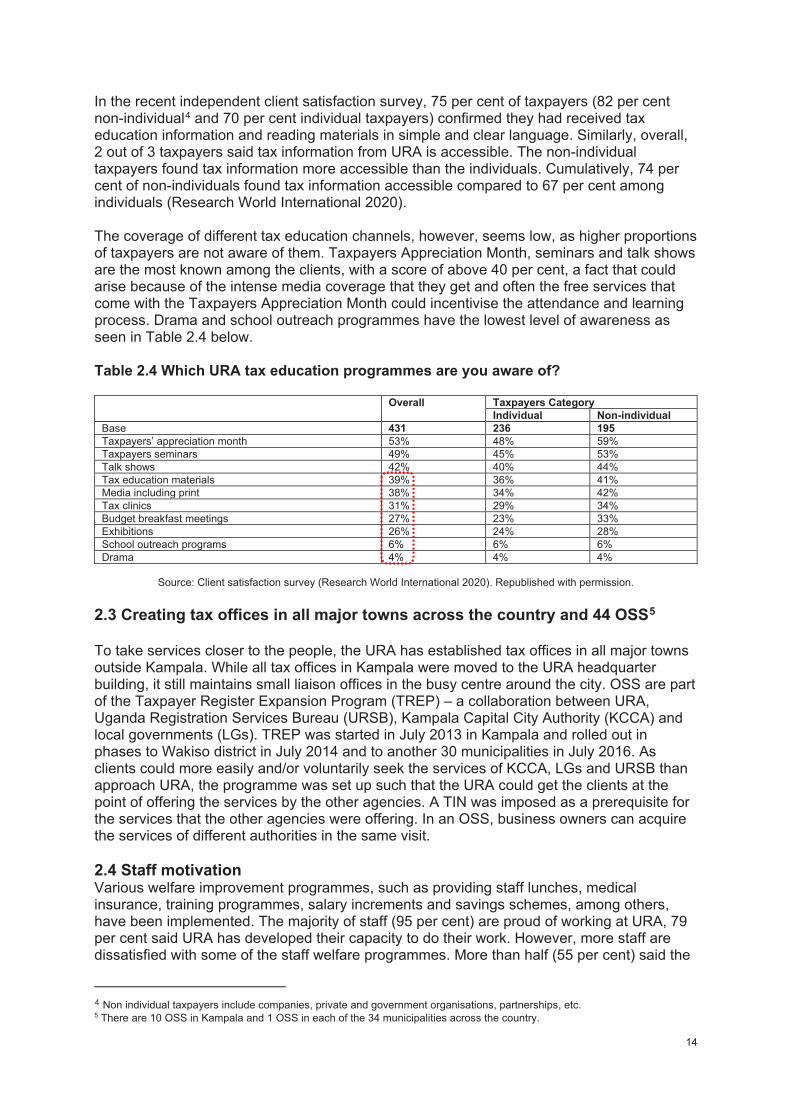

In the recent independent client satisfaction survey, 75 per cent of taxpayers (82 per cent non-individual4 and 70 per cent individual taxpayers) confirmed they had received tax education information and reading materials in simple and clear language. Similarly, overall, 2 out of 3 taxpayers said tax information from URA is accessible. The non-individual taxpayers found tax information more accessible than the individuals. Cumulatively, 74 per cent of non-individuals found tax information accessible compared to 67 per cent among individuals (Research World International 2020). The coverage of different tax education channels, however, seems low, as higher proportions of taxpayers are not aware of them. Taxpayers Appreciation Month, seminars and talk shows are the most known among the clients, with a score of above 40 per cent, a fact that could arise because of the intense media coverage that they get and often the free services that come with the Taxpayers Appreciation Month could incentivise the attendance and learning process. Drama and school outreach programmes have the lowest level of awareness as seen in Table 2.4 below. Table 2.4 Which URA tax education programmes are you aware of?

Overall Taxpayers Category Individual Non-individual

Base 431 236 195 Taxpayers’ appreciation month 53% 48% 59% Taxpayers seminars 49% 45% 53% Talk shows 42% 40% 44% Tax education materials 39% 36% 41% Media including print 38% 34% 42% Tax clinics 31% 29% 34% Budget breakfast meetings 27% 23% 33% Exhibitions 26% 24% 28% School outreach programs 6% 6% 6% Drama 4% 4% 4%

Source: Client satisfaction survey (Research World International 2020). Republished with permission.

2.3 Creating tax offices in all major towns across the country and 44 OSS5 To take services closer to the people, the URA has established tax offices in all major towns outside Kampala. While all tax offices in Kampala were moved to the URA headquarter building, it still maintains small liaison offices in the busy centre around the city. OSS are part of the Taxpayer Register Expansion Program (TREP) – a collaboration between URA, Uganda Registration Services Bureau (URSB), Kampala Capital City Authority (KCCA) and local governments (LGs). TREP was started in July 2013 in Kampala and rolled out in phases to Wakiso district in July 2014 and to another 30 municipalities in July 2016. As clients could more easily and/or voluntarily seek the services of KCCA, LGs and URSB than approach URA, the programme was set up such that the URA could get the clients at the point of offering the services by the other agencies. A TIN was imposed as a prerequisite for the services that the other agencies were offering. In an OSS, business owners can acquire the services of different authorities in the same visit. 2.4 Staff motivation Various welfare improvement programmes, such as providing staff lunches, medical insurance, training programmes, salary increments and savings schemes, among others, have been implemented. The majority of staff (95 per cent) are proud of working at URA, 79 per cent said URA has developed their capacity to do their work. However, more staff are dissatisfied with some of the staff welfare programmes. More than half (55 per cent) said the

4 Non individual taxpayers include companies, private and government organisations, partnerships, etc. 5 There are 10 OSS in Kampala and 1 OSS in each of the 34 municipalities across the country.

15

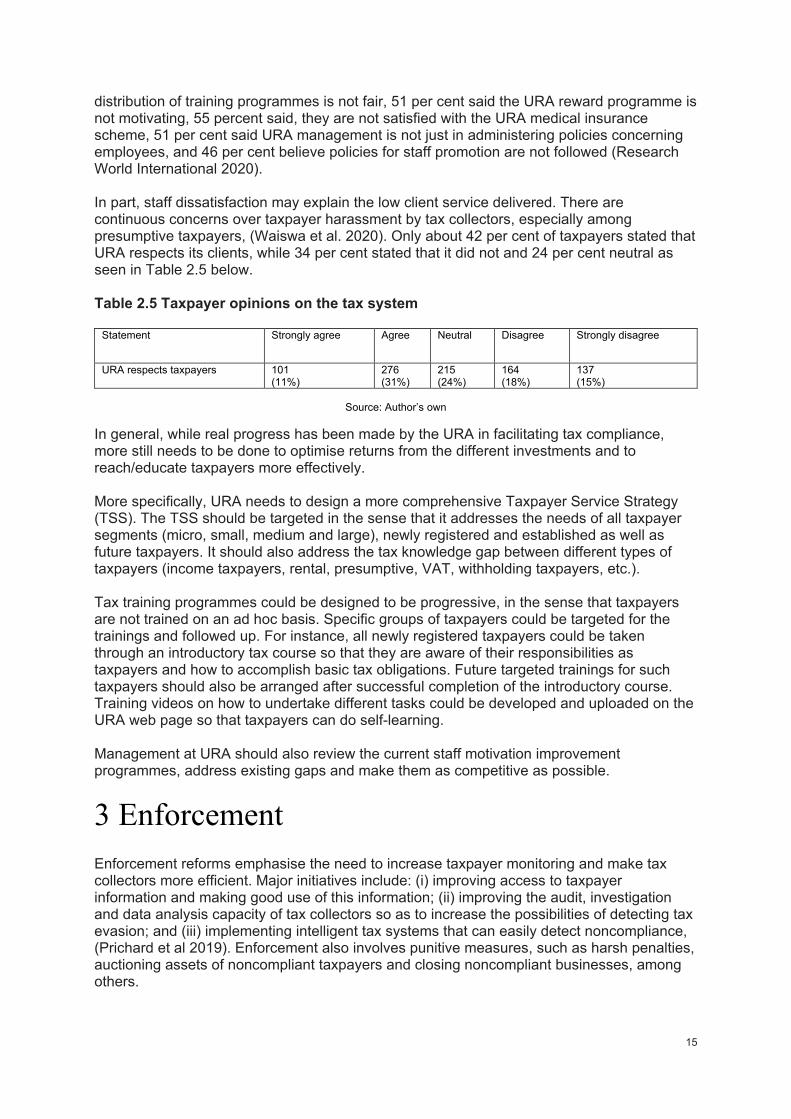

distribution of training programmes is not fair, 51 per cent said the URA reward programme is not motivating, 55 percent said, they are not satisfied with the URA medical insurance scheme, 51 per cent said URA management is not just in administering policies concerning employees, and 46 per cent believe policies for staff promotion are not followed (Research World International 2020). In part, staff dissatisfaction may explain the low client service delivered. There are continuous concerns over taxpayer harassment by tax collectors, especially among presumptive taxpayers, (Waiswa et al. 2020). Only about 42 per cent of taxpayers stated that URA respects its clients, while 34 per cent stated that it did not and 24 per cent neutral as seen in Table 2.5 below. Table 2.5 Taxpayer opinions on the tax system

Statement Strongly agree Agree Neutral Disagree Strongly disagree

URA respects taxpayers 101 (11%)

276 (31%)

215 (24%)

164 (18%)

137 (15%)

Source: Author’s own

In general, while real progress has been made by the URA in facilitating tax compliance, more still needs to be done to optimise returns from the different investments and to reach/educate taxpayers more effectively. More specifically, URA needs to design a more comprehensive Taxpayer Service Strategy (TSS). The TSS should be targeted in the sense that it addresses the needs of all taxpayer segments (micro, small, medium and large), newly registered and established as well as future taxpayers. It should also address the tax knowledge gap between different types of taxpayers (income taxpayers, rental, presumptive, VAT, withholding taxpayers, etc.). Tax training programmes could be designed to be progressive, in the sense that taxpayers are not trained on an ad hoc basis. Specific groups of taxpayers could be targeted for the trainings and followed up. For instance, all newly registered taxpayers could be taken through an introductory tax course so that they are aware of their responsibilities as taxpayers and how to accomplish basic tax obligations. Future targeted trainings for such taxpayers should also be arranged after successful completion of the introductory course. Training videos on how to undertake different tasks could be developed and uploaded on the URA web page so that taxpayers can do self-learning. Management at URA should also review the current staff motivation improvement programmes, address existing gaps and make them as competitive as possible.

3 Enforcement Enforcement reforms emphasise the need to increase taxpayer monitoring and make tax collectors more efficient. Major initiatives include: (i) improving access to taxpayer information and making good use of this information; (ii) improving the audit, investigation and data analysis capacity of tax collectors so as to increase the possibilities of detecting tax evasion; and (iii) implementing intelligent tax systems that can easily detect noncompliance, (Prichard et al 2019). Enforcement also involves punitive measures, such as harsh penalties, auctioning assets of noncompliant taxpayers and closing noncompliant businesses, among others.

16

Compared to facilitating compliance, where real progress has been made by the URA, tax enforcement actions are limited and weak. Current efforts have targeted only a few taxpayers. In the period 2014/15 to 2017/18, the URA only completed 9308 domestic tax audits, 1034 customs audits, 334 fraud investigations, 279 prosecution and litigation cases, and 27,054 seizure notices (Akol 2019). With the current taxpayer register standing at over 1.5 million taxpayers and, given the high levels of non-compliance among Ugandan taxpayers, enforcement progress has been slow. For instance, over 86 per cent of individuals supposed to file an income tax return do not file. Similarly, for non-individual taxpayers, about 44 per cent do not file while more than half (53 per cent) of those that submit their tax return file nil. More than half of Uganda’s taxpayers were classified as inactive, that is to say that they did not perform any transactions with URA for two consecutive years (Mayega et al 2019). These statistics (see also the Introduction to this paper) suggest that noncompliance in Uganda is widespread and therefore calls for more enforcement actions. While internally URA has registered real success in integrating its tax systems through the implementation of a data warehouse (E-hub system) that integrates domestic tax system (E-tax) with customs system (ASYCUDA World) and offers an easy platform to perform analysis on taxpayers, very little success has been achieved in integrating URA systems with those of external stakeholders. Presently, URA systems are not integrated with any external systems, including systems of other government agencies, making access to and use of taxpayer information in these institutions difficult. Besides the low levels of automation, especially in government entities and the use of different technologies, the URA’s access to third party information has been undermined by high ranking government officials, politicians and private sector players. For instance, one important source of taxpayer information is commercial banks. Despite Section 131 of the Income Tax Act (ITA) that gives URA unqualified access to taxpayer information, covering that in custody of banks, URA’s efforts to access detailed bank information have failed. It can only access bank information on an individual taxpayer and when it is in possession of an agency notice, not the entire bank databases. Furthermore, the Central Bank sometimes interfere with the process of accessing information by protecting commercial banks. Banks too sometimes collude with their customers to hide information from the URA and sometimes delay to respond to URA’s requests, (Kangave et al 2016). In 2017, the URA proposed to introduce a requirement for financial institutions, microfinance institutions, Foreign Exchange Market (Forex) exchange bureaus and money transferring institutions to report any transaction exceeding 1,000 currency points (equivalent to USh20 million or US$5333) to the URA on a monthly basis. Parliament rejected this proposal. The following year, 2018, the Commissioner for Domestic Taxes issued a letter to all commercial banks in Uganda, asking them to provide bank information on all account holders for the period 1 January 2016 to 31 December 2017. It requested account holders’ identification details, including the account name, TIN, National Identification Number (NIN), address, telephone number and email addresses, as well as the total cash deposits and withdrawals in the respective accounts for the period. The letter cited income tax provisions that gives URA unqualified access to this information. URA’s request received massive protests among the banking population and politicians. Banks through their umbrella association (Uganda Bankers Association) defied URA orders, asking URA to wait until their regulator body (Bank of Uganda) gives them the permission to share such information. In their reply, they cited the Bank of Uganda’s financial consumer protection guidelines that compel financial institutions to safeguard information relating to customer’s accounts. In a cabinet meeting chaired by the President, it was agreed that URA desists. Accordingly, URA was instructed to drop its intentions of demanding people’s accounts information and advised to continue requesting information on a case by case basis. (The East African 2018).

17

Similarly, the URA enforcement actions to recover unpaid taxes have received the same measure of resistance characterised by protests and political interferences. Tax officials in upcountry stations cited that one of the major challenges they face in enforcing on presumptive taxpayers is resistance from local leaders:

One time we enforced and traders demonstrated. The RDC (Resident District Commissioner) wrote to us to halt all our enforcement activities. The RDC had told them that the only tax they had to pay was trading licences When a 1 per cent withholding tax was introduced in 2017 on agricultural supplies, sugarcane growers attacked URA officials that had gone to sensitise them about the tax, milk dealers protested by pouring milk in the road, (Response from a URA staff).

The following year, the tax was abolished. Tax enforcements have also been undermined by weaknesses that are internal to URA itself, such as understaffing of the enforcement team and lack of attention paid to “small” taxpayers. 3.1 Understaffing of the enforcement team Tax officers in domestic taxes department are not allowed to enforce. The mandate to enforce using punitive measures, such as pursuing the recovery of outstanding taxes/debts using all available means within the legal provisions such as closing businesses and litigation among others is for the Debt Collection Unit (DCU) under the Legal Services and Board Affairs Department at the URA headquarters. However, URA only employs 12 staff in the DCU including one manager, two supervisors, eight officers and one office assistant. This is only 0.5 per cent of its staff employed in enforcing debt collection. It also employs only 10.8 per cent of its staff in audit, investigations, and verification functions. In Organisation for Economic Co-Operation and Development (OECD) countries, on average, 10 per cent of staff are deployed in enforcing debt collection and 30 per cent of staff in audit, investigations, and verification functions (OECD 2019). Indeed, our discussions with upcountry compliance officers indicated that DCU is very thin on ground.

We still have weak enforcement because we cannot enforce on our own. This is the mandate of DCU but it’s thin on the ground. You cannot call DCU to come and close a shop that has not paid 100,000 shillings. DCU rarely comes. This time we insisted on them and they visited our area twice and we have noticed more compliance. The only periods when we hit targets is when we moved with a police person and instructed him to close shops that had not paid. We enforced illegally but it worked. Response from upcountry URA staff

The shortage in human resources is not unique to the enforcement functions. URA is generally understaffed. The ratio of tax collectors to labour force in Uganda was estimated at 1: 6214 and that of tax collectors to population was 1: 17,368. In South Africa, the ratio of tax collectors to labour force was only 1: 1803, while that of tax collectors to population was 1: 4671, (MoFPED 2019). In 2017, a study of 21 tax authorities conducted by the African Tax Administration Forum (ATAF) indicated that URA was the fourth most understaffed tax authority (after Nigeria’s Federal Inland Revenue Services (FIRs), the Burundi Revenue Authority and the Rwanda Revenue Authority), with a labour force to tax administrator ratio being over 6000:1. Almost all the other tax authorities had a ratio of less than 4000:1. Similarly, besides FIRS and the Tanzania Revenue Authority, URA has a high taxpayer to

18

tax administrator ratio of over 300:1. Most of the other countries had a ratio of less than 100:1 (Africa Tax Administration Forum 2017). (Not all those in the active labour force are taxpayers). While staffing is clearly a challenge for the URA, the URA tax collectors are more efficient than those in most African countries. Revenue productivity per URA staff member is above average for the 34 African countries studied in 2019 (Africa Tax Administration Forum 2019). However, there is still a strong case for increasing its human resources in enforcement functions, given the high level of non-compliance among Ugandan taxpayers. 3.2 Little attention given to small taxpayers To meet revenue targets, coupled with the limited available resources, tax collectors have a tendency to target taxpayers that have the potential to pay significant amounts. This, however, creates stress on taxpayers who are continuously targeted, while making those not monitored more non-compliant, yet they need to be groomed into responsible taxpayers for the future. In our discussions with staff in charge of ensuring completeness, correctness and reliability of tax returns, they said that the focus on small taxpayers is very little:

We are not even in it. How can I chase for taxpayers of 50,000 shillings when I have other taxpayers that have large amounts? We have very little focus on such taxpayers. We do not even have the resources. It’s about prioritising. (Response from URA staff)

Going forward, more efforts are needed in strengthening the enforcement of tax compliance in Uganda. More specifically:

i. The executive as well as the local leaders/politicians need to be committed to fully supporting tax collection. They should not protect the non-compliant. Where taxing a particular income is justifiable by tax laws and the principles of taxation, such as fairness and efficiency, are honoured by the URA, political leaders should cease to interfere with URA’s actions. In a comparative study of tax administration reforms between Uganda and Georgia, it was found that the two countries implemented somewhat similar reforms but Georgia achieved far more success than Uganda because of differences in the level of commitment by political leaders in supporting revenue mobilisation, (Magumba 2019). There are cases where URA has succeeded in dealing with difficult taxpayers, simply because of support from high ranking government officials. For instance, we know that government entities in most African countries are bad taxpayers. The URA has successfully taxed government entities to a large extent, because of support from high ranking government officials. Within the first year of operationalising a specialised Public Sector Tax Office (PSO), revenue collections from government organisations increased by 194 per cent when compared to the previous year. The PSO became the second largest contributor to domestic tax collection in Uganda, after the Large Taxpayers’ Office (Saka, Waiswa and Kangave, 2018).

ii. The URA needs to engage local government leaders and the leaders of the business

communities in different parts of the country in the taxation of small taxpayers in general. Firstly, by teaching them about the income tax obligations of small business traders. Some of them do not know that these businesses are liable for income tax. They are only aware of the obligation to pay trading licence. Second, by involving them to sensitise the local business community on taxes and third, by notifying them about URA intentions to enforce prior to doing it. These measures are particularly reported to have been successful in the Kigezi region:

19

Originally, we had big resistance. We had to engage the RDC, CAO [Chief Administrative Officer] and LC5 [Local Council V] Chairperson6 on the income tax that small businesses had to pay. After explaining to them, they explained to the traders. Local leaders were not aware that these people had to pay income tax apart from trading licence. Since then we have never had any such resistance RDC even gave us airtime on radio to announce our plan to enforce.

(Interview with URA staff)

iii. Internally, the URA needs to scale up its enforcement actions. Firstly, by expanding

its enforcement team in terms of staffing and secondly, by making a deliberate effort to enforce on all categories of taxpayers small, medium or large.

iv. Lastly, there is need for deliberate action by the government to automate and

integrate all its systems with those of the URA. This will facilitate real time access to taxpayer information in other government systems. Private institutions should also be required to record sufficient details on their clients that can facilitate tax compliance enforcements. Such information could, for instance, include a NIN and a TIN. Similarly, the executive should openly instruct all institutions (public and private) to grant the URA real time access to taxpayer information, including that in custody of banks and government payment systems.

4 Creating trust in the government and the URA Building trust as part of the reform strategies underscores the importance of tax morale in enhancing tax compliance. Tax morale is the intrinsic motivation or willingness to pay taxes, (Torgler, Schaffne, and Macintyre, 2007). It shows through the voluntary readiness and willingness of taxpayers to comply with their tax obligations. Building trust addresses the role of ethics, social norms and views about the fairness, equity, reciprocity and accountability of tax systems in enhancing tax compliance. This suggests that taxpayers are more likely to comply if they perceive that:

• The tax systems are justly administered. Here, taxpayers understand the tax system, are treated well by the tax collectors, penalties are given fairly and there are available remedies in cases of abuse of their rights.

• Tax burdens are equitably distributed and everyone pays their share. In this case, tax policies and enforcements are designed and implemented such that taxpayers in similar economic circumstances pay similar taxes (horizontal equity) and in case taxpayers are economically different in terms of wealth, tax rules are progressive, where the wealthy individuals pay more, as a share of income, than the less wealthy and in the case of firms, there is relative balance of effective tax burdens across differently-sized firms (vertical equity).

• Tax revenues are translated into reciprocal publicly provided goods and services that taxpayers are satisfied with.

• The government is accountable to taxpayers (Prichard et al. 2019).

6 LC5 Chairperson refers to the political head of a district.

20

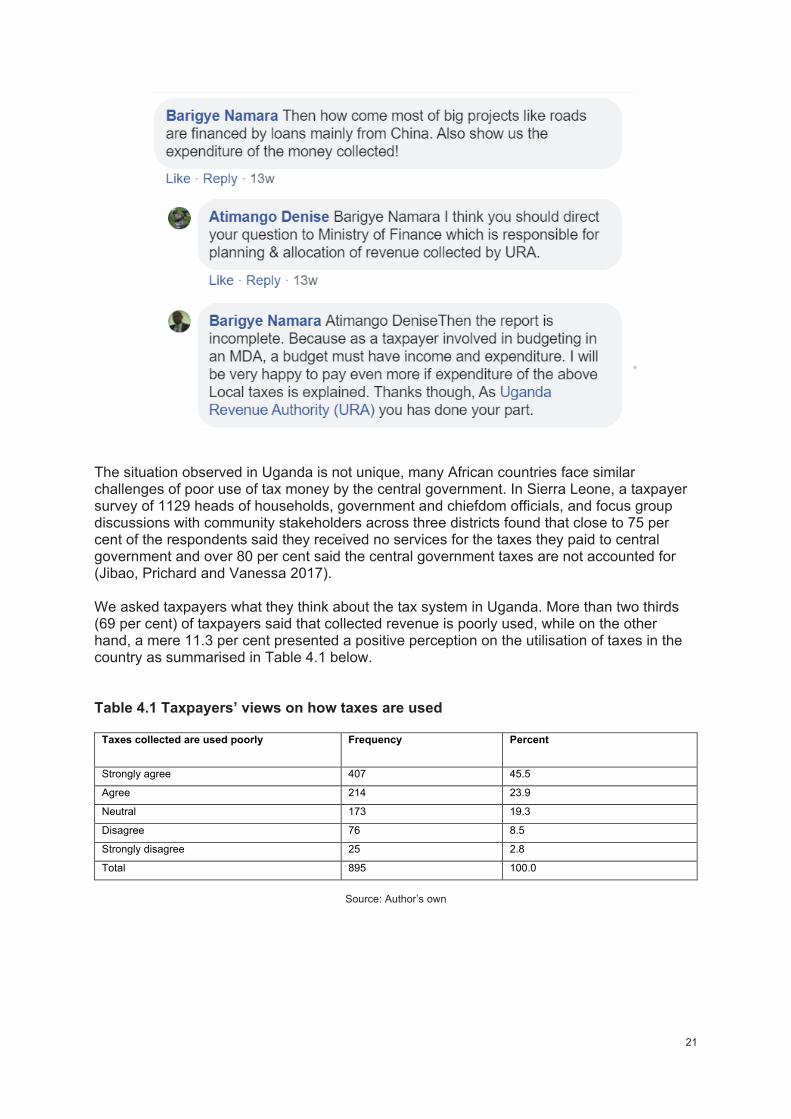

However, for most African governments, this is a bit of a stretch. If it takes all this to persuade taxpayers to comply voluntarily, then they will just force the money out of them. 4.1 Creating trust in the government The primary role of the government in increasing tax compliance lies in creating public trust in tax governance where citizens perceive that revenues are translated into quality goods and services, and that government accounts properly for the revenue collected. Ross (2004), for example, argued that taxpayers are agreeable to any form of tax that is proportionate to the government services. Torgler, Schaffne and Macintyre (2007) expand this notion to the quality of political institutions, accountability, control of corruption and trust in the judicial and parliamentary systems. Using data from 55 countries, the OECD found that satisfaction with public expenditures and services such as health, education, water and sanitation, especially in Africa, Latin America and Asia influences tax morale. It was also found that citizens are more likely to perceive tax obligations more favourably when their government is seen to be acting in a trustworthy manner (OECD 2013). Uganda is performing very poorly in terms of creating public trust. There seems to be two major concerns: (i) poor government spending practices and (ii) the perception that some sections of society are not paying their share because of their connections to or roles in the government. 4.1.1 Poor government spending practices There is quite a lot of evidence from interviews conducted that the (lack of) trust in government’s spending practices is a major issue. There is a general perception that: (i) taxes are poorly utilised; (ii) the services meant to be provided by government are either missing or of poor quality or even, at times, illegally offered at a fee by officials; and (iii) that a big portion of government revenue is used to fund the “wrong things”. Complaints about a huge “non-working” parliament, cabinet ministers and presidential advisors are common in many circles. Government works are not visible by the general public. Its mistakes, such as corruption scandals, poor quality of its services, and “sharing” of taxpayers’ money among government officials, especially by members of parliament, among others, seem to be more marketed by the media rather than its good works. The visible works such as roads, bridges and dams are always portrayed to be funded by either loans or grants from development partners, such as the European Union, World Bank etc. While it’s true that the government is using the money to spend on many things, such as paying the salaries of public servants, improving security and many others, the public does not seem to relate these more to tax spending. They need to see infrastructures labelled “funded by the government of Uganda” and good quality basic services, such as quality education, health services, water and sanitation provided. There are several complaints of lack of medicines, patients not being tended to if they haven’t paid in government hospitals, poor performance of students in government schools as compared to private schools and bad roads, among others. Under such circumstances, the public cannot appreciate the value of paying taxes. Figure 4.1 below shows some reactions to a letter posted by URA on its Facebook page, appreciating taxpayers for having enabled it to surpass its 2018/19 revenue target. Figure 4.1 Reactions to the URA’s letter appreciating taxpayers for a revenue surplus in 2018/19

21

The situation observed in Uganda is not unique, many African countries face similar challenges of poor use of tax money by the central government. In Sierra Leone, a taxpayer survey of 1129 heads of households, government and chiefdom officials, and focus group discussions with community stakeholders across three districts found that close to 75 per cent of the respondents said they received no services for the taxes they paid to central government and over 80 per cent said the central government taxes are not accounted for (Jibao, Prichard and Vanessa 2017). We asked taxpayers what they think about the tax system in Uganda. More than two thirds (69 per cent) of taxpayers said that collected revenue is poorly used, while on the other hand, a mere 11.3 per cent presented a positive perception on the utilisation of taxes in the country as summarised in Table 4.1 below. Table 4.1 Taxpayers’ views on how taxes are used

Taxes collected are used poorly Frequency Percent

Strongly agree 407 45.5

Agree 214 23.9

Neutral 173 19.3

Disagree 76 8.5

Strongly disagree 25 2.8

Total 895 100.0

Source: Author’s own

22

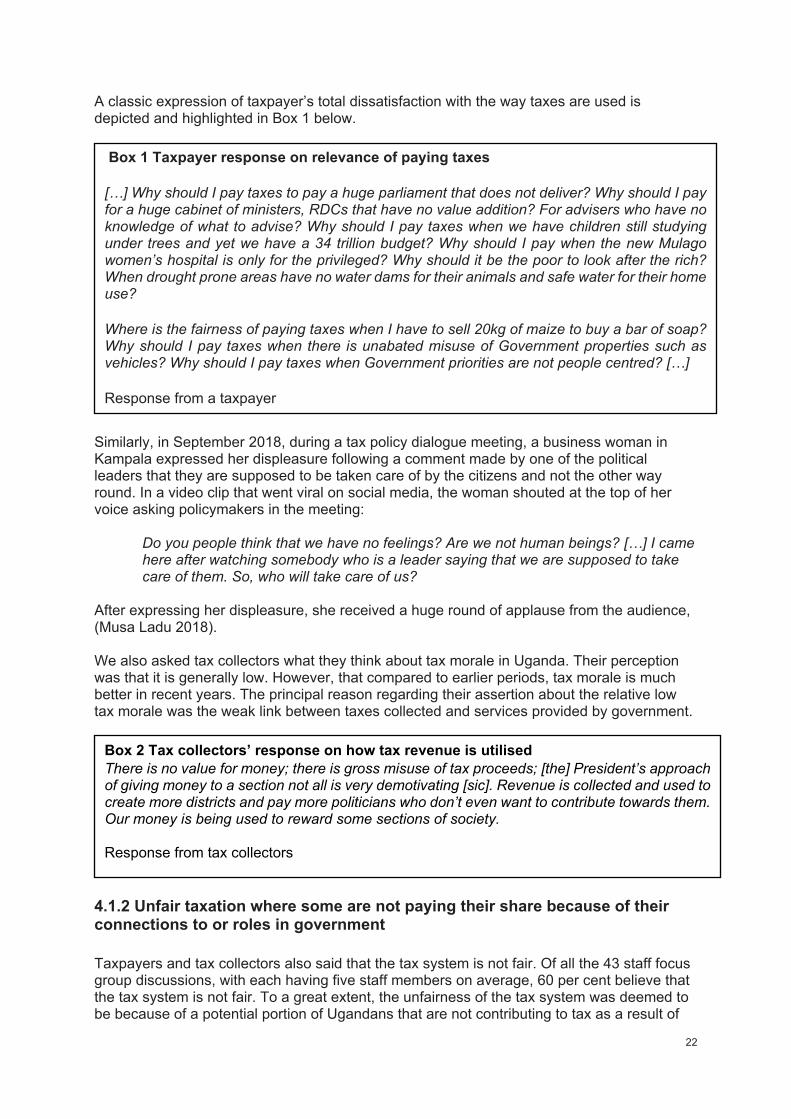

A classic expression of taxpayer’s total dissatisfaction with the way taxes are used is depicted and highlighted in Box 1 below.

Similarly, in September 2018, during a tax policy dialogue meeting, a business woman in Kampala expressed her displeasure following a comment made by one of the political leaders that they are supposed to be taken care of by the citizens and not the other way round. In a video clip that went viral on social media, the woman shouted at the top of her voice asking policymakers in the meeting:

Do you people think that we have no feelings? Are we not human beings? […] I came here after watching somebody who is a leader saying that we are supposed to take care of them. So, who will take care of us?

After expressing her displeasure, she received a huge round of applause from the audience, (Musa Ladu 2018). We also asked tax collectors what they think about tax morale in Uganda. Their perception was that it is generally low. However, that compared to earlier periods, tax morale is much better in recent years. The principal reason regarding their assertion about the relative low tax morale was the weak link between taxes collected and services provided by government.

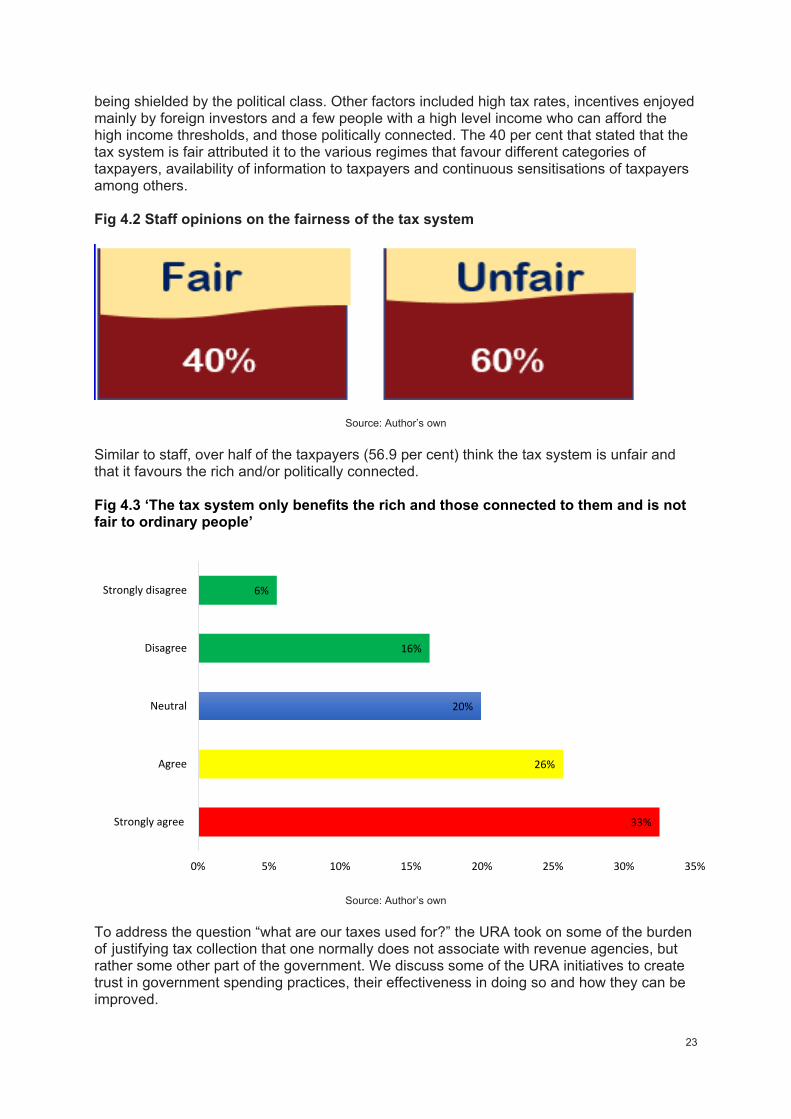

4.1.2 Unfair taxation where some are not paying their share because of their connections to or roles in government Taxpayers and tax collectors also said that the tax system is not fair. Of all the 43 staff focus group discussions, with each having five staff members on average, 60 per cent believe that the tax system is not fair. To a great extent, the unfairness of the tax system was deemed to be because of a potential portion of Ugandans that are not contributing to tax as a result of

Box 1 Taxpayer response on relevance of paying taxes

[…] Why should I pay taxes to pay a huge parliament that does not deliver? Why should I pay for a huge cabinet of ministers, RDCs that have no value addition? For advisers who have no knowledge of what to advise? Why should I pay taxes when we have children still studying under trees and yet we have a 34 trillion budget? Why should I pay when the new Mulago women’s hospital is only for the privileged? Why should it be the poor to look after the rich? When drought prone areas have no water dams for their animals and safe water for their home use?

Where is the fairness of paying taxes when I have to sell 20kg of maize to buy a bar of soap? Why should I pay taxes when there is unabated misuse of Government properties such as vehicles? Why should I pay taxes when Government priorities are not people centred? […]

Response from a taxpayer

Box 2 Tax collectors’ response on how tax revenue is utilised There is no value for money; there is gross misuse of tax proceeds; [the] President’s approach of giving money to a section not all is very demotivating [sic]. Revenue is collected and used to create more districts and pay more politicians who don’t even want to contribute towards them. Our money is being used to reward some sections of society. Response from tax collectors

23

being shielded by the political class. Other factors included high tax rates, incentives enjoyed mainly by foreign investors and a few people with a high level income who can afford the high income thresholds, and those politically connected. The 40 per cent that stated that the tax system is fair attributed it to the various regimes that favour different categories of taxpayers, availability of information to taxpayers and continuous sensitisations of taxpayers among others. Fig 4.2 Staff opinions on the fairness of the tax system

Source: Author’s own Similar to staff, over half of the taxpayers (56.9 per cent) think the tax system is unfair and that it favours the rich and/or politically connected. Fig 4.3 ‘The tax system only benefits the rich and those connected to them and is not fair to ordinary people’

Source: Author’s own To address the question “what are our taxes used for?” the URA took on some of the burden of justifying tax collection that one normally does not associate with revenue agencies, but rather some other part of the government. We discuss some of the URA initiatives to create trust in government spending practices, their effectiveness in doing so and how they can be improved.

33%

26%

20%

16%

6%

0% 5% 10% 15% 20% 25% 30% 35%

Strongly agree

Agree

Neutral

Disagree

Strongly disagree

24

4.1.3 Publishing government works: My Taxes Work publication and video My Taxes Work document publishes what the government has done with the taxes collected. The inaugural copy was published in 2017 with over 10,000 copies distributed to different stakeholders including taxpayers. It provides pictorial evidence on government works such as roads, health centres constructed, among others, in that particular year. These are also summarised in a video clip that is shared in seminars or workshops organised by the URA for taxpayers on the different taxpayer engagements. This initiative, however, is generally ineffective. Most taxpayers and URA staff are not aware of it. There are insufficient copies distributed both in Kampala and upcountry tax offices. To improve the effectiveness of the publication, staff suggest that: (i) copies should be made available in different tax offices across the country and (ii) an e-copy also be made available on the URA web portal for ease of access by taxpayers. Table 4.2 Taxpayers’ opinions on the effectiveness of the government works publication Initiative Not effective (%)

Moderately effective (%)

Effective (%)

Number of respondents

Government Works publication 47.1% 35.3% 17.6% 836

Source: Author’s own 4.1.4 Because of You campaigns These campaigns are intended to inform taxpayers that it is because of them that the government has been able to deliver different services. Different government works that have been funded using taxpayers’ money are publicised using different media platforms such as television, radios, billboards and print. 4.1.5 Taxpayer Appreciation Days (TPAD) The National Taxpayer Appreciation Fair is an annual series of taxpayer appreciation activities within all five regions of Uganda. It is geared towards building strong relationships with the private sector and giving broad accountability for what taxes have done for the people of Uganda. It started in 2005/06 as a one day ceremony in Kampala where the URA would recognise the most compliant taxpayers. In 2014/15, it was spread out to the four regions of Uganda and lasted a whole month, but with the final appreciation day held in Kampala. The final appreciation day is characterised by the URA partnering with different government agencies to offer free services to the public. All government ministries and authorities showcase their businesses and educate the general public about what their taxes have done and in which communities. Its fundamental objective is to encourage taxpayer compliance through driving tax accountability. The most complaint taxpayers with significant revenue contribution and growth are identified and rewarded at an exclusive event held in Kampala. This process also involves regional awards of taxpayers in different taxpayer categories (small, medium, large, individuals, non-individuals and the public sector taxpayers). According to staff, TPADs are a very good initiative and clients who are appreciated are greatly encouraged to continue complying. However, they cited a number of weaknesses including:

i. It rewards very few taxpayers, which can demotivate other compliant or fairly compliant taxpayers. In the financial year 2016/17 for example, only eight regional taxpayers under the Vantage award were rewarded. Of these, five were government

25

entities – specifically district local government and only thee private sector taxpayers, (Saka et al., 2019).

ii. Staff also stated that the appreciation in form of a letter/certificate of appreciation is

not enough.

iii. The process leaves out taxpayers in rural areas. Engagements are only held around city centres and there are no formal processes to facilitate participation of taxpayers from rural areas.

iv. The final appreciation day that involves provision of free services from different

government agencies is only held in Kampala. The free services are therefore not accessible to those who can’t travel from their different districts to Kampala.

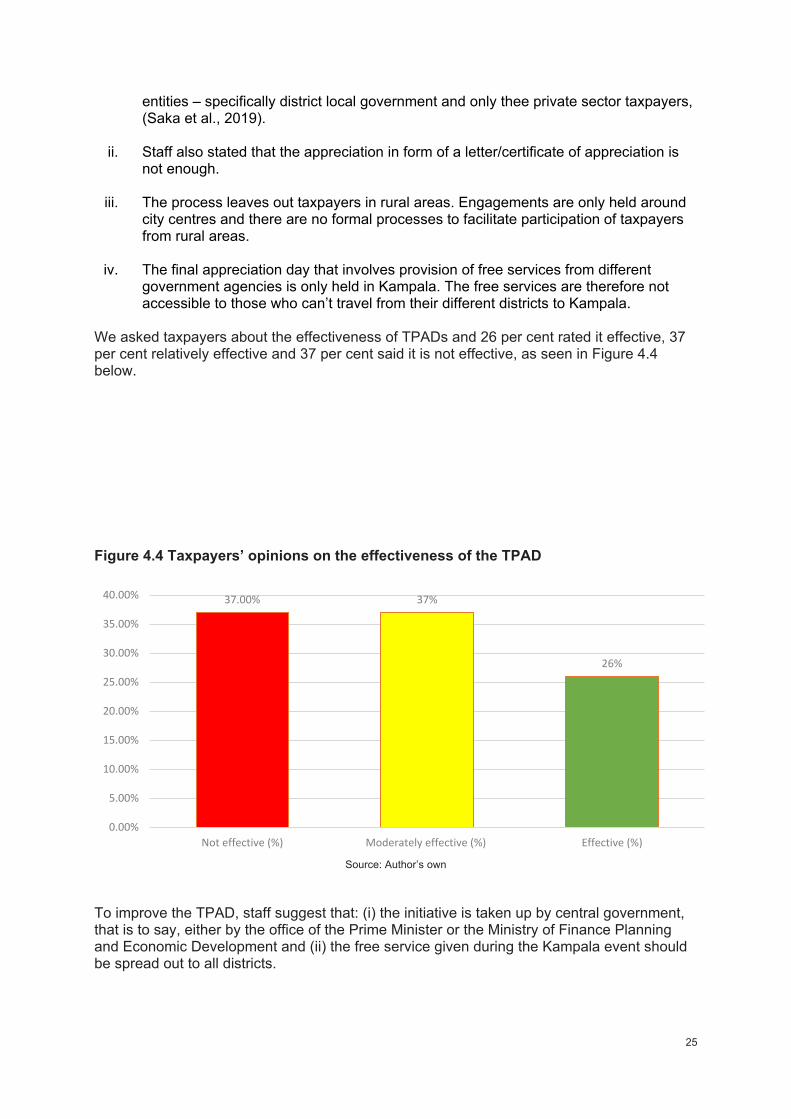

We asked taxpayers about the effectiveness of TPADs and 26 per cent rated it effective, 37 per cent relatively effective and 37 per cent said it is not effective, as seen in Figure 4.4 below. Figure 4.4 Taxpayers’ opinions on the effectiveness of the TPAD

Source: Author’s own

To improve the TPAD, staff suggest that: (i) the initiative is taken up by central government, that is to say, either by the office of the Prime Minister or the Ministry of Finance Planning and Economic Development and (ii) the free service given during the Kampala event should be spread out to all districts.

37.00% 37%

26%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Not effective (%) Moderately effective (%) Effective (%)

26

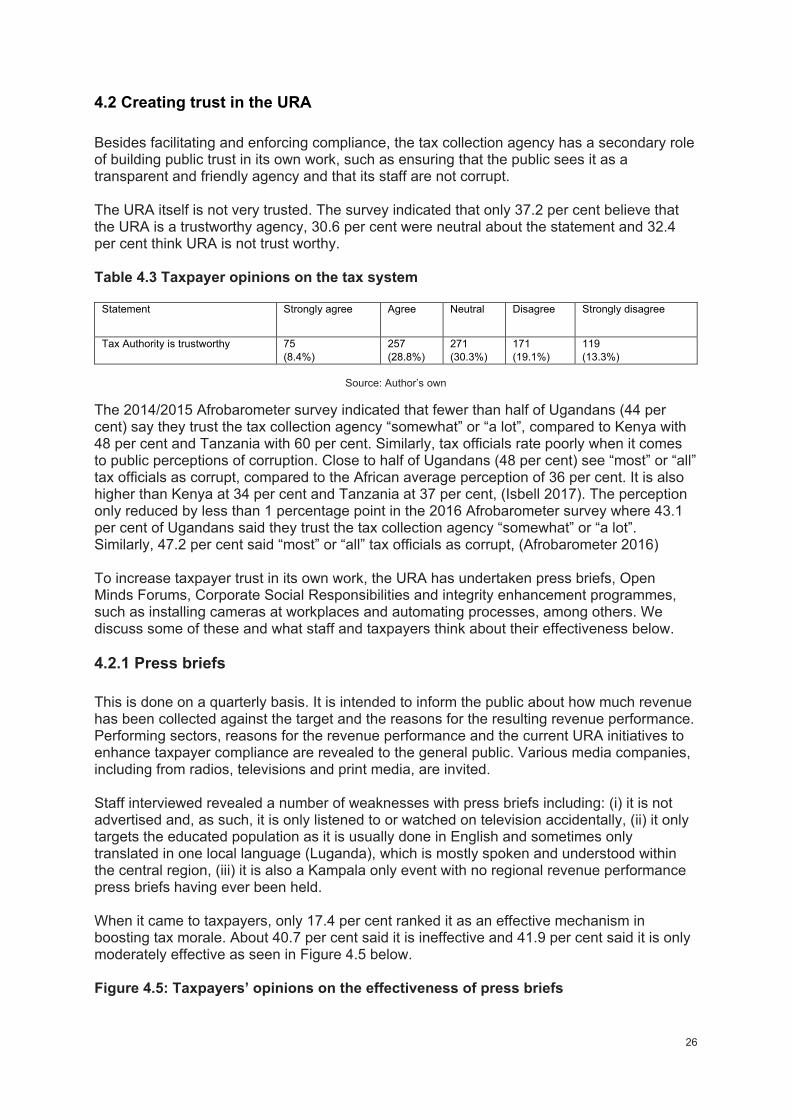

4.2 Creating trust in the URA Besides facilitating and enforcing compliance, the tax collection agency has a secondary role of building public trust in its own work, such as ensuring that the public sees it as a transparent and friendly agency and that its staff are not corrupt. The URA itself is not very trusted. The survey indicated that only 37.2 per cent believe that the URA is a trustworthy agency, 30.6 per cent were neutral about the statement and 32.4 per cent think URA is not trust worthy. Table 4.3 Taxpayer opinions on the tax system

Statement Strongly agree Agree Neutral Disagree Strongly disagree

Tax Authority is trustworthy 75 (8.4%)

257 (28.8%)

271 (30.3%)

171 (19.1%)

119 (13.3%)

Source: Author’s own

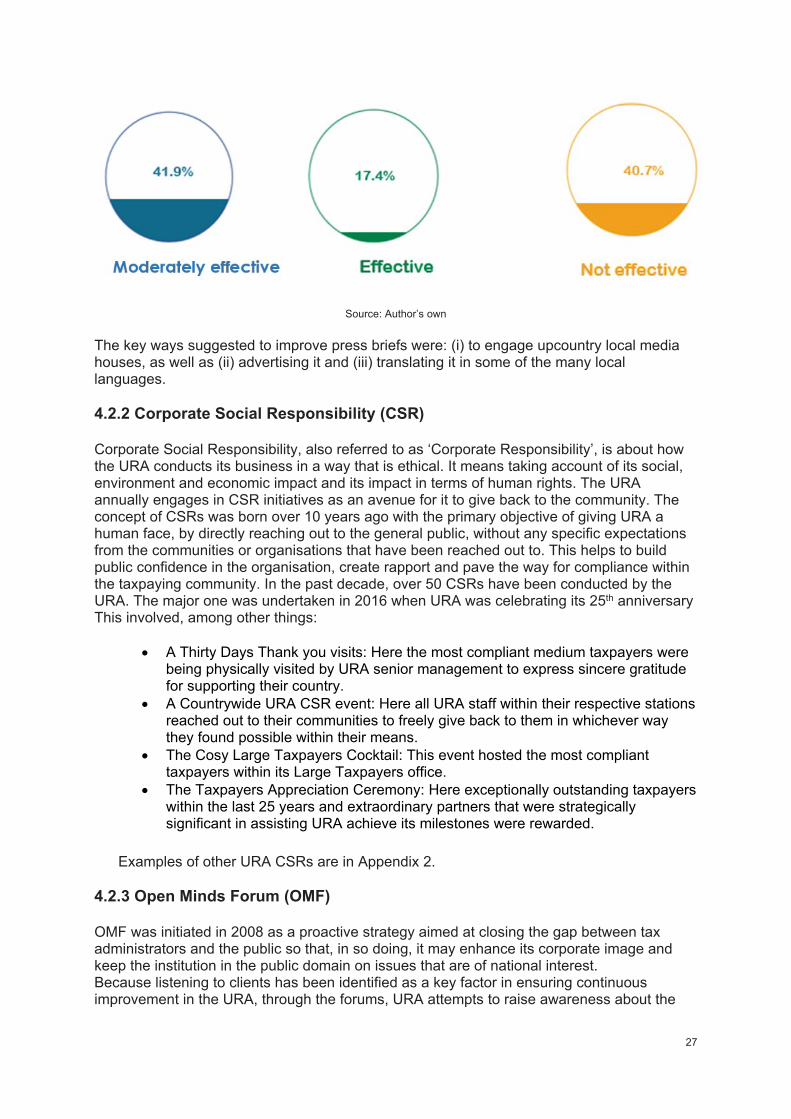

The 2014/2015 Afrobarometer survey indicated that fewer than half of Ugandans (44 per cent) say they trust the tax collection agency “somewhat” or “a lot”, compared to Kenya with 48 per cent and Tanzania with 60 per cent. Similarly, tax officials rate poorly when it comes to public perceptions of corruption. Close to half of Ugandans (48 per cent) see “most” or “all” tax officials as corrupt, compared to the African average perception of 36 per cent. It is also higher than Kenya at 34 per cent and Tanzania at 37 per cent, (Isbell 2017). The perception only reduced by less than 1 percentage point in the 2016 Afrobarometer survey where 43.1 per cent of Ugandans said they trust the tax collection agency “somewhat” or “a lot”. Similarly, 47.2 per cent said “most” or “all” tax officials as corrupt, (Afrobarometer 2016) To increase taxpayer trust in its own work, the URA has undertaken press briefs, Open Minds Forums, Corporate Social Responsibilities and integrity enhancement programmes, such as installing cameras at workplaces and automating processes, among others. We discuss some of these and what staff and taxpayers think about their effectiveness below. 4.2.1 Press briefs This is done on a quarterly basis. It is intended to inform the public about how much revenue has been collected against the target and the reasons for the resulting revenue performance. Performing sectors, reasons for the revenue performance and the current URA initiatives to enhance taxpayer compliance are revealed to the general public. Various media companies, including from radios, televisions and print media, are invited. Staff interviewed revealed a number of weaknesses with press briefs including: (i) it is not advertised and, as such, it is only listened to or watched on television accidentally, (ii) it only targets the educated population as it is usually done in English and sometimes only translated in one local language (Luganda), which is mostly spoken and understood within the central region, (iii) it is also a Kampala only event with no regional revenue performance press briefs having ever been held. When it came to taxpayers, only 17.4 per cent ranked it as an effective mechanism in boosting tax morale. About 40.7 per cent said it is ineffective and 41.9 per cent said it is only moderately effective as seen in Figure 4.5 below. Figure 4.5: Taxpayers’ opinions on the effectiveness of press briefs

27

Source: Author’s own The key ways suggested to improve press briefs were: (i) to engage upcountry local media houses, as well as (ii) advertising it and (iii) translating it in some of the many local languages. 4.2.2 Corporate Social Responsibility (CSR) Corporate Social Responsibility, also referred to as ‘Corporate Responsibility’, is about how the URA conducts its business in a way that is ethical. It means taking account of its social, environment and economic impact and its impact in terms of human rights. The URA annually engages in CSR initiatives as an avenue for it to give back to the community. The concept of CSRs was born over 10 years ago with the primary objective of giving URA a human face, by directly reaching out to the general public, without any specific expectations from the communities or organisations that have been reached out to. This helps to build public confidence in the organisation, create rapport and pave the way for compliance within the taxpaying community. In the past decade, over 50 CSRs have been conducted by the URA. The major one was undertaken in 2016 when URA was celebrating its 25th anniversary This involved, among other things:

• A Thirty Days Thank you visits: Here the most compliant medium taxpayers were being physically visited by URA senior management to express sincere gratitude for supporting their country.

• A Countrywide URA CSR event: Here all URA staff within their respective stations reached out to their communities to freely give back to them in whichever way they found possible within their means.

• The Cosy Large Taxpayers Cocktail: This event hosted the most compliant taxpayers within its Large Taxpayers office.

• The Taxpayers Appreciation Ceremony: Here exceptionally outstanding taxpayers within the last 25 years and extraordinary partners that were strategically significant in assisting URA achieve its milestones were rewarded.

Examples of other URA CSRs are in Appendix 2.

4.2.3 Open Minds Forum (OMF) OMF was initiated in 2008 as a proactive strategy aimed at closing the gap between tax administrators and the public so that, in so doing, it may enhance its corporate image and keep the institution in the public domain on issues that are of national interest. Because listening to clients has been identified as a key factor in ensuring continuous improvement in the URA, through the forums, URA attempts to raise awareness about the

28

challenges affecting the country or region and provides the public with a platform for discussion and an opportunity to freely offer solutions to these issues. The forum takes the form of a public debate on topical issues or presentations and dialogue by renowned local and international speakers who discuss a given topic. The programme exists for the purpose of presentation and explanation of ideas through dialogue. It provides an opportunity for public participation in policy formulation and development. According to staff, OMF is an informative platform that brings together policymakers and the public to discuss matters of national importance. It also provides a feedback mechanism for taxpayers to openly raise and receive answers to their complaints about the tax system. However, similar to other initiatives, it’s a Kampala only event and targets the educated only. To improve it, staff suggest that: (i) it should be regionalised and (ii) frequency of occurrence should be increased from the current once a year event. On the side of taxpayers, only 20 per cent said it is an effective measure for improving taxpayer morale, 40.7 per cent said it can only moderately improve tax morale and 39.3 per cent stated that’s it is not effective, as seen in Table 4.4. Table 4.4 Taxpayers’ opinions on the effectiveness of URA initiatives

Not effective (%)

Moderately effective (%)

Effective (%)

Number of respondents

Tax education campaigns 30.6% 43.3% 26.1 865 Open Minds Forum 39.3% 40.7% 20.0% 839 Simplified payment platforms (the URA app, using mobile money, etc.)

19.3% 37% 43.7% 855

Source: Author’s own

Going forward, to improve public trust in the government and URA, there is need for a deliberate effort by the government to properly account for collected tax revenue. Better ways to appreciate compliant taxpayers need to be devised. More specifically, we suggest:

i. The designation of a national accountability day. Just as there is a national budget reading day, we suggest that Ministry of Finance designates a day to only give accountability for public resources. This can mimic the URA taxpayer appreciation day but scaled up across the country.

ii. The URA government works publication and campaigns can be taken up as an initiative by the central government and then communicated annually using various communication channels.

iii. Better mechanisms of rewarding taxpayers’, e.g. rebates to the most compliant taxpayers in addition to the taxpayers’ visits and thank you letters need to be considered. Another thing to consider is to offer some free services, such as renewal of driving permits, passports and verification of documents, among others, to taxpayers who comply with taxes. The non-compliant would then contribute to national revenue by paying these fees.

iv. Spread the current URA initiatives to various parts of the country. Taxpayer appreciation and, accountability events can for example be held at different districts where URA has a tax office.

29

5 Summary and Conclusion Ugandans seem more noncompliant than other East Africans, especially in regards to income taxes. In this paper, we have discussed the three broad ways of improving tax compliance (facilitation, enforcement and creating trust in the government and its spending practices, as well as trust in the tax collection agency itself). We have also discussed what the two main actors (URA and government) responsible for working on these variables have done in the past, the successes achieved and the gaps that remain. We conclude that the URA has done well in facilitating tax compliance in Uganda although there are opportunities for improvements on its current initiatives. The URA enforcement actions are, however, still weak and limited. It has targeted a few taxpayers generally; the number of taxpayers that are subjected to the different compliance improvement initiatives, such as audits, inspections, enforcement actions, etc. are few in comparison to the taxpayer register. To a large extent, enforcement actions have been undermined by the government and politicians. Enforcements have also been weak because of weaknesses internal to the URA such as understaffing of the enforcement team and little attention paid to “small” taxpayers. Lastly, very little has been done in building taxpayer morale to pay taxes. There are widespread concerns over poor usage of tax money, missing or poor government services, and some sections of society being shielded from paying their share because of their connections to or roles in government. Generally, the government has not played its role in improving tax compliance in Uganda. In the end, we find that the URA is doing some of the job of justifying tax collection that one does not normally associate with revenue agencies, but rather another government department. Its initiatives are, however, very limited in terms of coverage. They are largely Kampala based and in cases where they have been taken upcountry, they are only held in major regional town centres. The measures are also more focused on the elite groups. The tax collection agency is also not trusted that much and corruption is still a major problem among tax collectors. Going forward, improving tax compliance in Uganda will require the government (in the sense of the presidential office or indeed the president himself) and the URA working together. The government should have total support for URA activities and should desist from protecting non-compliant taxpayers, as well as being accountable to the public for the collected revenues. The URA on the other hand, needs to address the gaps in its current initiatives, as well as closely address its internal weaknesses.

30

References Afrobarometer (2016) Merged Round 6 data (36 countries) (2016),

http://afrobarometer.org/data/merged-round-6-data-36-countries-2016 (accessed on 22 October 2019)

Akol, D. (2019) Accounting for four years leadership as Commissioner General of Uganda

Revenue Authority. Kampala: Uganda Revenue Authority, https://www.ura.go.ug/readMore.do?contentId=999000000001559&type=TIMELINE (accessed on 1 July 2020)

Aondo, R. M. and Sile, I. (2018) ‘Effect of taxpayers knowledge and tax compliance amongst

SMEs in Nakuru County Kenya’, European Journal of Business and Strategic Management 3.6: 13-26

ATAF (2017) African Tax Outlook, Pretoria: Africa Tax Administration Forum ATAF (2019) African Tax Outlook, Pretoria: Africa Tax Administration Forum IMF (2015) TADAT Performance Assessment Report for Uganda, Washington, D.C.:

International Monetary Fund IMF (2019) TADAT Performance Assessment Report Uganda. Washington, D.C.:

International Monetary Fund Isbell, T. (2017) Tax Compliance: Africans Affirm Civic Duty but Lack Trust in Tax

Department, Afrobarometer Policy Paper No.43, https://afrobarometer.org/sites/default/files/publications/Policy%20papers/ab_r6_policypaperno43_tax_compliance_in_africa-afrobarometer.pdf (accessed on 30 October 2019)

Jibao, S., Prichard, W. and Van den Boogaard, V. (2017) Informal Taxation in Post Conflict

Sierra Leone: Taxpayers’ Experiences and Perceptions, ICTD Working Paper 66, Brighton: Institute of Development Studies

Kagina, A. (2014) Uganda Revenue Authority Hand Over Report 2004-2014, Kampala:

Uganda Revenue Authority Kangave, J., Nakato S., Waiswa, R., Lumala, P. Z. and Nalukwago, M. I. (2018). What Can

We Learn from the Uganda Revenue Authority’s Approach to Taxing High Net Worth Individuals?, ICTD Working Paper 72, Brighton: IDS

Magumba, M. (2019) Tax Administration Reforms: Lessons from Georgia and Uganda, ICTD

African Tax Administration Paper 5, Brighton: IDS Mascagni, G., Santoro, F. and Mukama, D. (2019) Teach to comply? Evidence from a

Taxpayer Education Program in Rwanda, ICTD Working Paper 91, Brighton: IDS Mayega, J., Ssuuna, R., Mubajje, M., Nalukwago, M. I. and Muwonge, L. (2019). How clean

is our taxpayer Register? Data Management in Uganda Revenue Authority, ICTD, African Tax Administration Paper 12, Brighton: IDS

31

Musa Ladu, I. (2018) ‘Woman storms “high level” policy meeting on tax over remarks made by Museveni representative’, Daily Monitor, https://www.monitor.co.ug/News/National/Woman-attacks-Museveni-representative-policy-meeting-tax/688334-4748320-4c6rk8z/index.html (accessed on 1 July 2020)

MoFPED (2019) Domestic Revenue Mobilisation Strategy 2019/20-2023/24, Kampala:

Ministry of Finance, Planning and Economic Development OECD (2013) What drives tax morale? Organisation for Economic Co-operation and

Development OECD (2019) Tax Administration 2019: Comparative information on OECD and other

Advanced and Emerging Economies, Paris: Organisation for Economic Co-operation and Development

OECD (2020), Revenue Statistics: Comparative Tables, OECD Tax Statistics (database),

https://doi.org/10.1787/data-00262-en (accessed on 17 June 2020) Okello, A. (2014) Managing Income Tax Compliance through Self-Assessment, IMF Working

Paper, Washington, D.C.: International Monetary Fund Prichard, W., Custers, A., Dom, R., Davenport, S. and Roscitt, M. (2019) Innovations in Tax

Compliance: Conceptual Framework, Policy Research Working Paper, Washington D.C.: The World Bank

Research World International (2020) County Wide the URA Client Satisfaction Survey,

Kampala: Uganda Revenue Authority Ross, M. L. (2004) ‘Does Taxation Lead to Representation?’, British Journal of Political

Science, 34.2: 229-249 Saka, H., Waiswa, R. and Kangave, J. (2018) Taxing Government: The Case of the Uganda

Revenue Authority's Public Sector Office, ICTD Working Paper 84, Brighton: IDS The East African (2018) ‘Cabinet blocks the URA from accessing bank customers’ details’,

10 April, https://www.theeastafrican.co.ke/business/Uganda-blocks-the URA-from-accessing-bank-customers-details/2560-4380734-format-sitemap-t5offk/index.html (accessed 1 July 2020)

Torgler, B., Schaffne, M. and Macintyre, A. (2007), Tax Compliance, Tax Morale and

Governance Quality, International Center for Public Policy Working Paper Series, at AYSPS, GSU Paper 0727, Atlanta: International Center for Public Policy, Andrew Young School of Policy Studies, Georgia State University

URA (2015) Annual Monitoring and Evaluation Report, Uganda Revenue Authority URA (2016) the URA at 25: Our Journey, Kampala: Uganda Revenue Authority, https://the

URA.go.ug/readMore.do?contentId=999000000001557&type=TIMELINE (accessed 1 July 2020)

URA (2017) Revenue tables, Kampala: Uganda Revenue Authority URA (2019) Annual Revenue Report, Kampala: Uganda Revenue Authority

32

Waiswa, R., Kangave, J. and Sebagala, N. (2020) ‘Does Gender Matter in Tax Compliance? The Case of the URA’s Individual Taxpayers’, Forthcoming IDS Working paper, Brighton: IDS

33

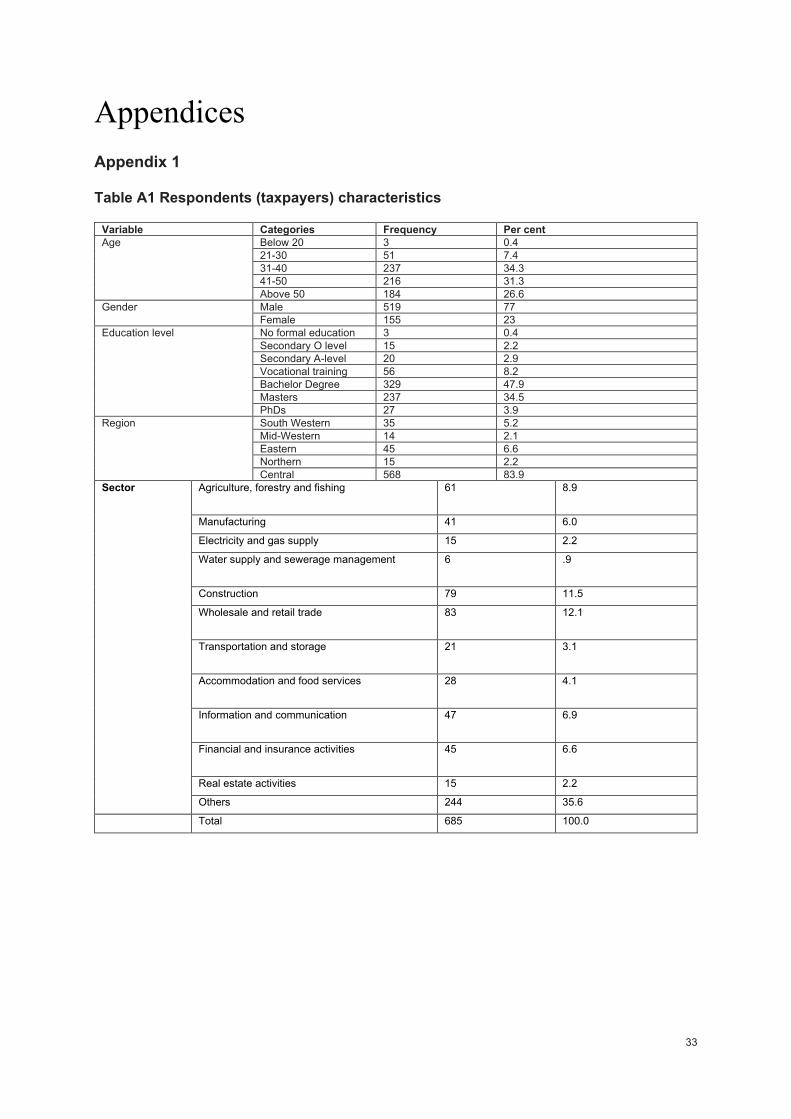

Appendices Appendix 1 Table A1 Respondents (taxpayers) characteristics

Variable Categories Frequency Per cent Age Below 20 3 0.4

21-30 51 7.4 31-40 237 34.3 41-50 216 31.3 Above 50 184 26.6

Gender Male 519 77 Female 155 23

Education level No formal education 3 0.4 Secondary O level 15 2.2 Secondary A-level 20 2.9 Vocational training 56 8.2 Bachelor Degree 329 47.9 Masters 237 34.5 PhDs 27 3.9

Region South Western 35 5.2 Mid-Western 14 2.1 Eastern 45 6.6 Northern 15 2.2 Central 568 83.9

Sector Agriculture, forestry and fishing 61 8.9

Manufacturing 41 6.0

Electricity and gas supply 15 2.2

Water supply and sewerage management 6 .9

Construction 79 11.5

Wholesale and retail trade 83 12.1

Transportation and storage 21 3.1

Accommodation and food services 28 4.1

Information and communication 47 6.9

Financial and insurance activities 45 6.6

Real estate activities 15 2.2

Others 244 35.6

Total 685 100.0

34

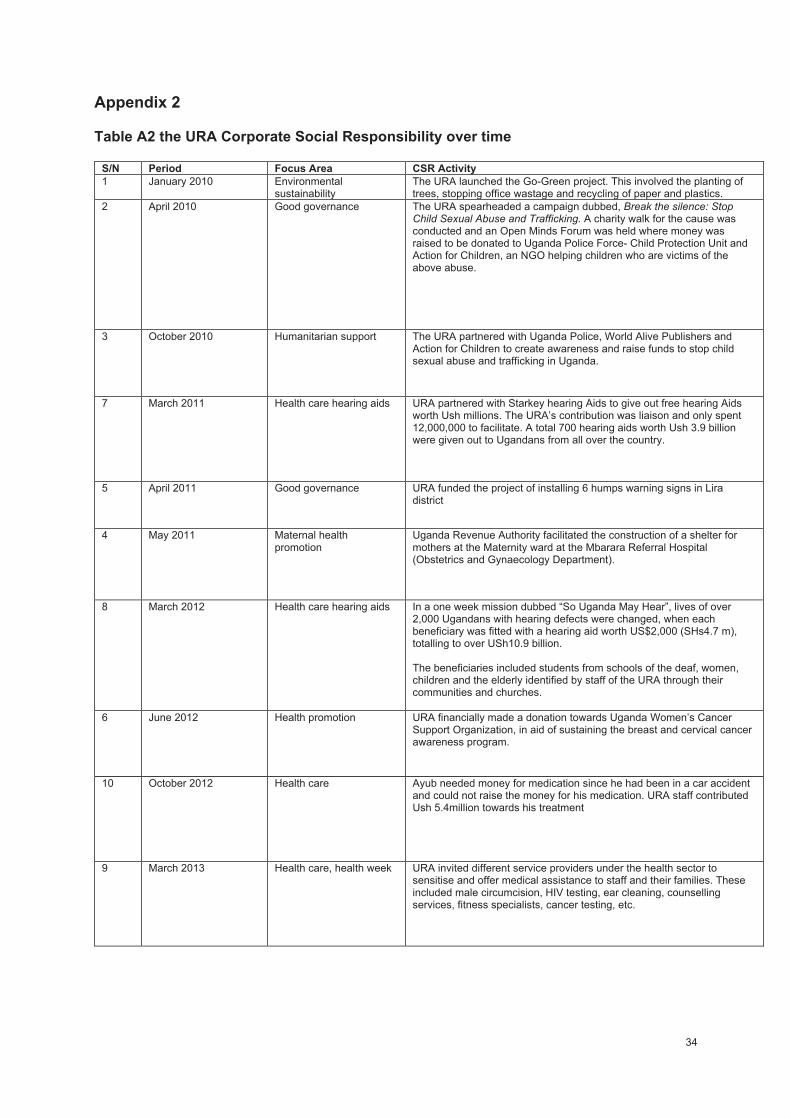

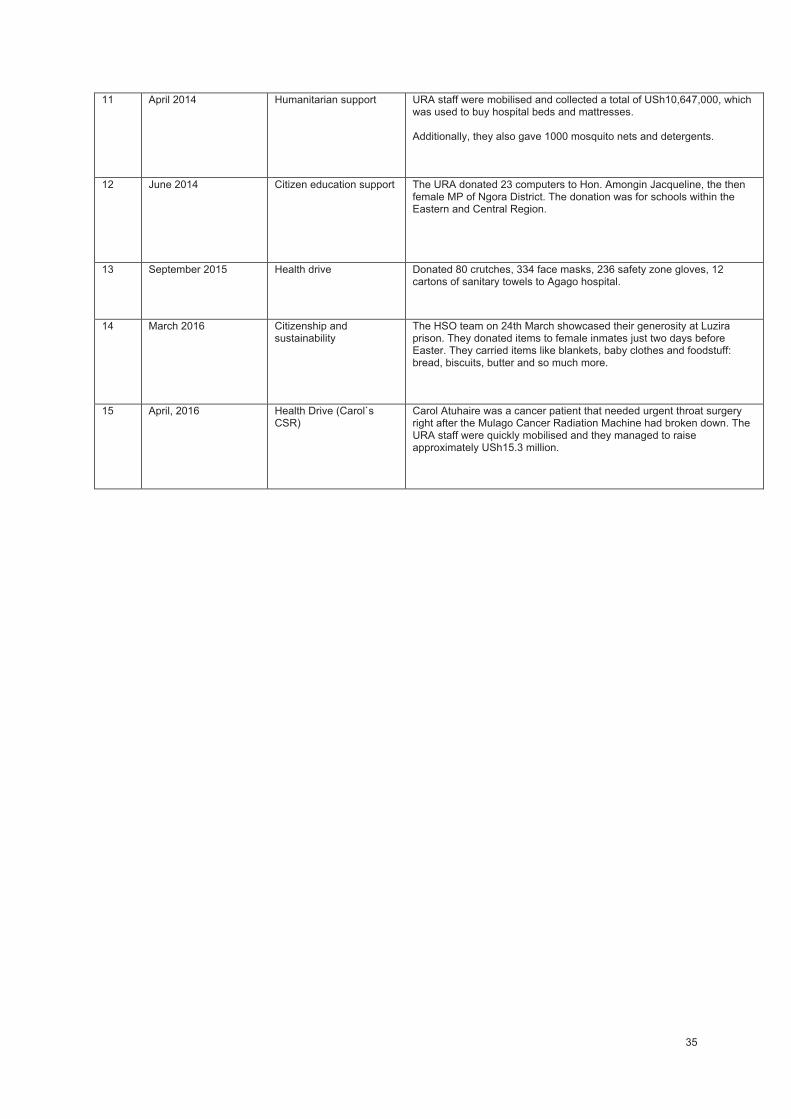

Appendix 2 Table A2 the URA Corporate Social Responsibility over time

S/N Period Focus Area CSR Activity 1 January 2010 Environmental

sustainability The URA launched the Go-Green project. This involved the planting of trees, stopping office wastage and recycling of paper and plastics.

2 April 2010 Good governance The URA spearheaded a campaign dubbed, Break the silence: Stop Child Sexual Abuse and Trafficking. A charity walk for the cause was conducted and an Open Minds Forum was held where money was raised to be donated to Uganda Police Force- Child Protection Unit and Action for Children, an NGO helping children who are victims of the above abuse.

3 October 2010 Humanitarian support The URA partnered with Uganda Police, World Alive Publishers and Action for Children to create awareness and raise funds to stop child sexual abuse and trafficking in Uganda.

7 March 2011 Health care hearing aids URA partnered with Starkey hearing Aids to give out free hearing Aids worth Ush millions. The URA’s contribution was liaison and only spent 12,000,000 to facilitate. A total 700 hearing aids worth Ush 3.9 billion were given out to Ugandans from all over the country.

5 April 2011 Good governance URA funded the project of installing 6 humps warning signs in Lira district

4 May 2011 Maternal health promotion

Uganda Revenue Authority facilitated the construction of a shelter for mothers at the Maternity ward at the Mbarara Referral Hospital (Obstetrics and Gynaecology Department).