Sector Report Construction & Infrastructure kpmg.com/africa

Africa Construction and Infrastructure 2015 KPMG

Aug 12, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sector Report

Construction &Infrastructure

kpmg.com/africa

The series has the following reports:

• Banking in Africa

• Private Equity in Africa

• Insurance in Africa

• Power in Africa

• Healthcare in Africa

• Oil and Gas in Africa

• Manufacturing in Africa

• Fast-Moving Consumer Goods in Africa

• Luxury Goods in Africa

• The African Consumer and Retail

• White Goods in Africa

• Agriculture in Africa

Table of ContentsIntroduction 1

Emerging trends that will change the world of infrastructure –

The African Context 2

Building Time and Costs 3

Countries with Significant Construction / Infrastructure Opportunities 4

Angola 5

Ethiopia 6

Ghana 6

Ivory Coast 7

Kenya 7

Mozambique 8

Namibia 8

Nigeria 9

Company Focus: Dangote Cement 9

South Africa 11

Tanzania 12

Uganda 12

Zambia 13

Recent Infrastructure Developments 14

Final Thoughts 15

Key Infrastructure Indicators 16

Sources of Information 17

Contact Details 17

1 | Construction & Infrastructure

Introduction

African Development Bank (AfDB) President Donald Kareruka said during September 2014 that sustainable economic growth on the African continent is dependent on three factors: regional integration, the development of institutions (e.g. property rights and rule of law), as well as infrastructure. What is the effect of insufficient infrastructure on the African economy? The Infrastructure Consortium of Africa (ICA), for example, believes that 40 billion potential work hours are lost each year owing to people being unable to open a tap in their homes for water and instead needing to fetch water from another source. From the perspective of land transport, roads account for 80% of goods and 90% of passenger transport on the continent.

However, a minority of Africa’s roads are paved, and less than half of rural Africans have access to an all-season road. Land transport is considered so important to the continent that the African Union (AU) signed an agreement with China during January 2015 aimed at increasing direct road and railway transport between major African cities. The memorandum of understanding is the first continent-wide deal between China and the AU and the “document of the century” is the “most substantive project the AU has ever signed with a partner,” according to AU Commission Chairperson Nkosazana Dlamini-Zuma. China is already heavily invested in African transport projects, and around a quarter of the Asian giant’s investment on the continent is in the area of transport.

There are many approximations on the amount of infrastructure investment that the continent needs: a rough estimate is US$100bn per annum of which only half currently has financing. African governments have historically relied on donor aid and external borrowing to finance their fiscal deficits. At the same time, many states have financed infrastructure spending out of their fiscal budgets, resulting in fixed capital growth being dependent on available government finances. Contemporary financing options include:

• Domestic capital markets (where available and developed enough);

• Eurobonds sold on the international market;

• Public-Private Partnerships (PPPs);

• Private equity investment funds;

• Sovereign Wealth Funds (SWFs);

• Shari’ah-compliant Sukuk debt;

• Funding from multilateral organisations; and

• Dedicated infrastructure bonds.

Private equity, for example, is playing an increasing role in Africa’s infrastructure landscape, according to the South African Venture Capital and Private Equity Association (SAVCA). “Infrastructure gives private equity investors access to the strong African growth story, an exceptional theme in a structurally low-growth world,” commented SAVCA CEO Erika van der Merwe. The organisation added that international investors would like to buy into the Africa growth story but that this will not materialise without the rollout of sufficient infrastructure. “The multiplier effects created by infrastructural investments are powerful tools for uplifting people and growing economies – and make infrastructure-focused private equity funds an ideal vehicle for fulfilling an impact investing mandate,” commented SAVCA Chairman Emile du Toit. Infrastructure investment and private equity are ideal partners, with both focused on long-term success rather than short-term gains.

Construction & Infrastructure | 2

Emerging trends that will change the world of Infrastructure – The African Context

• A January 2015 special edition of KPMG’s FORESIGHT publication discussed ‘10 Emerging Trends for 2015: Trends that will change the world of infrastructure over the next 5 years’. Below are some comments from an African perspective related to these 10 factors:

• Governments take action to unclog the pipeline – National and local governments have become more interventionist in the area of infrastructure financing due to a desire to accelerate public service delivery. The majority of Eurobonds issued by African sovereigns (e.g. Kenya, Rwanda and Zambia) over the past four years have been specifically sold to raise funds towards infrastructure spending. This was, until recently, not a traditional avenue on the continent for funding infrastructure.

• Political and regulatory risks rise up the agenda – The Arab Spring that swept North Africa during 2011-12 caught many onlookers by surprise. Unlike the open conflict seen in many of Africa’s troubled states, the simmering tensions in Egypt and Libya were for too long seen as non-threatening to national stability. The aftermath of the political changes inspired by the Jasmine Revolution has forced stakeholders in many African countries to consider more acutely the underlying and sometimes not-so-visible political challenges in Africa.

• Market reforms: status quo is not fit for purpose – The deregulation of several large public utility sectors has widened the scope for investment in delivering previously monopolised private goods. The Nigerian electricity industry, for example, has been unbundled into generation and distribution companies and a single transmission company – the state holds the transmission rights while generation and distribution are fully privatised.

• The shifting role of multilaterals and development banks – Regional development banks have a role to play in shaping infrastructure markets from the planning stages to the ribbon cutting ceremony. The BRICS (Brazil, Russia, India, China and South Africa) grouping launched its New Development Bank (NDB) during July 2014 as a vehicle to support infrastructure investment and promote sustainable economic development in countries with financial constraints not catered for by e.g. the World Bank and International Monetary Fund (IMF).

• Big complexities start to impede big projects – Moving megaprojects from the drawing board to the ground is challenging for a multitude of reasons with skills challenges at the project management level a key issue. While global construction firms have internationally experienced project managers at their disposal their on-the-ground knowledge of African conditions might be limited. Even in South Africa, with its construction giants venturing ever deeper north into the continent, skills development remains a pressing concern.

• Striking the right balance between necessity and opportunity – More and more countries are introducing infrastructure-specific development plans though with varying focus points – some are too concerned with economic infrastructure compared to social infrastructure. The World Bank has pledged US$1.2bn to members of the five-nation East African Community (EAC) towards improving inland waterways and sea port facilities as part of an effort to boost regional integration. In a 2015-25 strategy paper, the bloc stated that it needs as much as US$100bn over the next decade to develop roads, ports, railways, transmission lines and oil & gas infrastructure.

• Striving for better asset performance – The privatisation (or part sale) of state assets as attractive for governments with troubled service delivery records as the sale of public holdings could see a cash injection for the fiscus and also see public entities perform better with the involvement of private enterprise. Botswana, for example, launched a broad privatisation drive in 2000, and most recently the Botswana Telecommunications Corporation Limited (BTCL) was set be floated on the local stock market during H1 of 2015.

• Resource scarcity drives investment – The management of scarce resources such as water is receiving reinvigorated attention due to the greater awareness of climate change globally. Investment in water infrastructure is gaining interest in not only arid nations but also those states with more abundant resources that could be commoditised into export revenues (in Lesotho, for example). Elsewhere, innovative technology is being used to reduce water usage in e.g. household toilets.

• Infrastructure players go global – Infrastructure development in a globalised world has become a multinational affair, attracting interest from global developers. In Africa, cross-national interest is booming, and not only from the previously dominant South African companies. Of the continent’s 10 largest listed companies involved in construction and building materials only one – Pretoria Portland Cement (PPC) – is from South Africa. Other major cross-national players include Nigeria’s Dangote Cement, Lafarge operations in Morocco and Zambia, and Egypt’s Suez Cement.

• Cities sharpen their focus on urban mobility – Increased mobility in urban areas supports the flow of goods, capital and people, and for the world’s poor offers a crucial link to access employment, social services and education. Half of Africans will in the near future live in cities where the number of available vehicle seats is way below the global average. Innovative solutions already implemented on the continent include inner-city water transport in Lagos, Nigeria and urban planning towards increased walkability of cities in Ethiopia and Kenya.

3 | Construction & Infrastructure

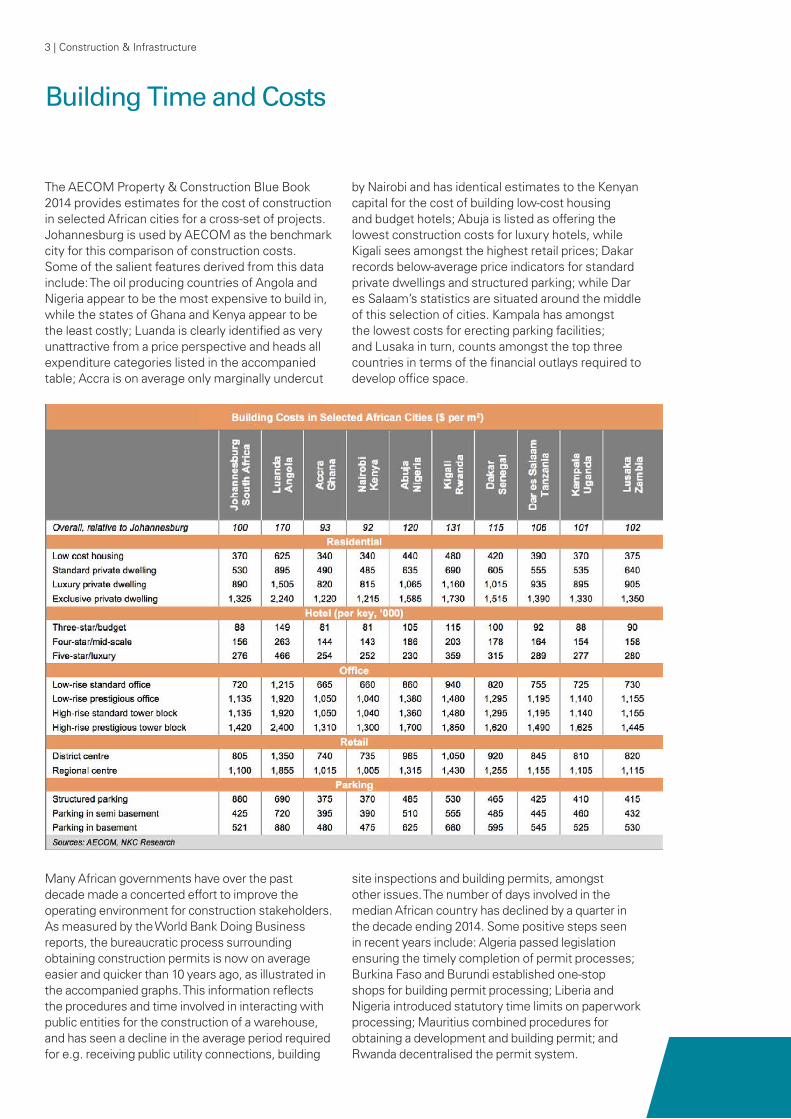

Building Time and Costs

The AECOM Property & Construction Blue Book 2014 provides estimates for the cost of construction in selected African cities for a cross-set of projects. Johannesburg is used by AECOM as the benchmark city for this comparison of construction costs. Some of the salient features derived from this data include: The oil producing countries of Angola and Nigeria appear to be the most expensive to build in, while the states of Ghana and Kenya appear to be the least costly; Luanda is clearly identified as very unattractive from a price perspective and heads all expenditure categories listed in the accompanied table; Accra is on average only marginally undercut

by Nairobi and has identical estimates to the Kenyan capital for the cost of building low-cost housing and budget hotels; Abuja is listed as offering the lowest construction costs for luxury hotels, while Kigali sees amongst the highest retail prices; Dakar records below-average price indicators for standard private dwellings and structured parking; while Dar es Salaam’s statistics are situated around the middle of this selection of cities. Kampala has amongst the lowest costs for erecting parking facilities; and Lusaka in turn, counts amongst the top three countries in terms of the financial outlays required to develop office space.

Many African governments have over the past decade made a concerted effort to improve the operating environment for construction stakeholders. As measured by the World Bank Doing Business reports, the bureaucratic process surrounding obtaining construction permits is now on average easier and quicker than 10 years ago, as illustrated in the accompanied graphs. This information reflects the procedures and time involved in interacting with public entities for the construction of a warehouse, and has seen a decline in the average period required for e.g. receiving public utility connections, building

site inspections and building permits, amongst other issues. The number of days involved in the median African country has declined by a quarter in the decade ending 2014. Some positive steps seen in recent years include: Algeria passed legislation ensuring the timely completion of permit processes; Burkina Faso and Burundi established one-stop shops for building permit processing; Liberia and Nigeria introduced statutory time limits on paperwork processing; Mauritius combined procedures for obtaining a development and building permit; and Rwanda decentralised the permit system.

Construction & Infrastructure | 4

The 2014 edition of the KPMG Infrastructure 100: World Markets report – a document showcasing one hundred projects that embody the spirit of infrastructure, development and private finance – included seven projects on the Africa continent (excluding South Africa).

These are i) the 3,218 km, US$13bn Nigeria High Speeds Rail, ii) 2,935 km Mombasa-Kigali Railway and iii) 100 MW KivuWatt power plant project in Rwanda, iv) the 525 m cable-supported Jinja Bridge in Uganda, and v) the offshore Kudu Gas Field in Namibia, as well as vi) the US$20bn Trans-Saharan Natural Gas Project from Nigeria to Algeria, and vii) the North-South Africa Corridor across the continent.

The following paragraphs take a closer look at selected construction and infrastructure trends in some of Africa’s bustling building sites. The 13 economies included in this document are seen as opportunities for investment and profit in the construction sector or linked to infrastructure development. The selected countries are: Angola, Egypt, Ethiopia, Ghana, Ivory Coast, Kenya, Mozambique, Namibia, Nigeria, South Africa, Tanzania, Uganda and Zambia. The combined value of their capital stock equalled almost US$265bn during 2013, or 57.5% of the continent’s infrastructure stock.

Countries With Significant Construction/ Infrastructure Opportunities

5 | Construction & Infrastructure

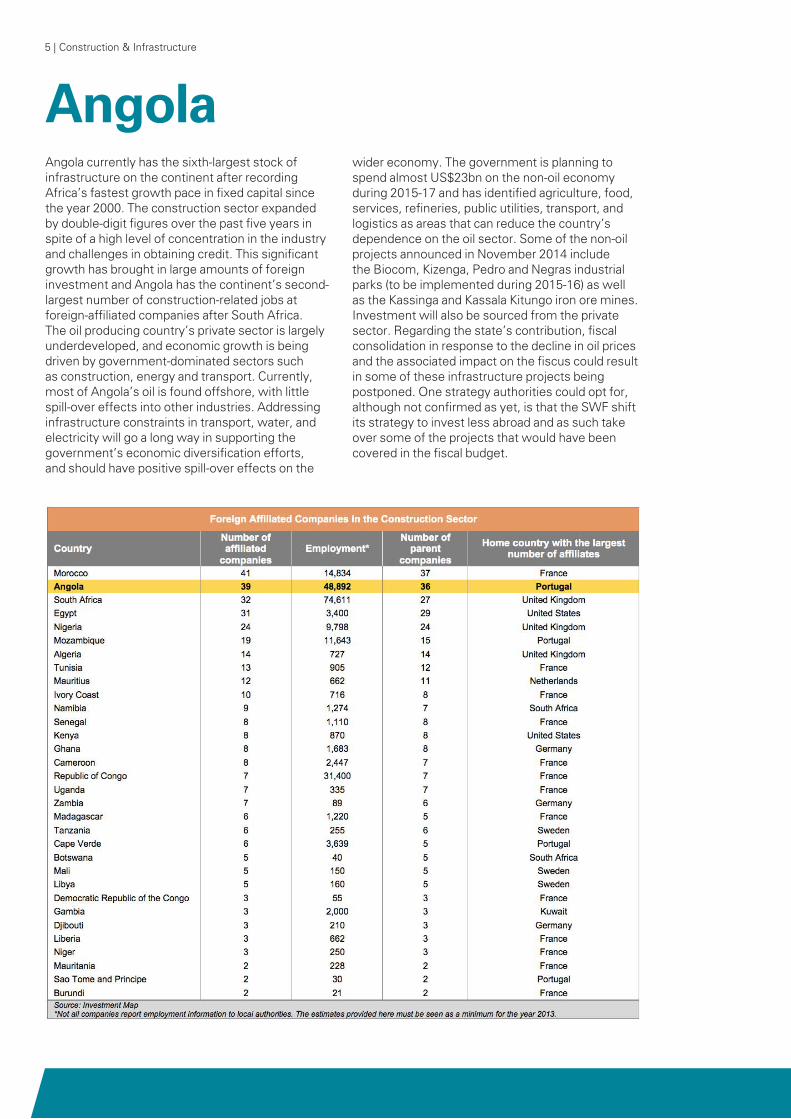

AngolaAngola currently has the sixth-largest stock of infrastructure on the continent after recording Africa’s fastest growth pace in fixed capital since the year 2000. The construction sector expanded by double-digit figures over the past five years in spite of a high level of concentration in the industry and challenges in obtaining credit. This significant growth has brought in large amounts of foreign investment and Angola has the continent’s second-largest number of construction-related jobs at foreign-affiliated companies after South Africa. The oil producing country’s private sector is largely underdeveloped, and economic growth is being driven by government-dominated sectors such as construction, energy and transport. Currently, most of Angola’s oil is found offshore, with little spill-over effects into other industries. Addressing infrastructure constraints in transport, water, and electricity will go a long way in supporting the government’s economic diversification efforts, and should have positive spill-over effects on the

wider economy. The government is planning to spend almost US$23bn on the non-oil economy during 2015-17 and has identified agriculture, food, services, refineries, public utilities, transport, and logistics as areas that can reduce the country’s dependence on the oil sector. Some of the non-oil projects announced in November 2014 include the Biocom, Kizenga, Pedro and Negras industrial parks (to be implemented during 2015-16) as well as the Kassinga and Kassala Kitungo iron ore mines. Investment will also be sourced from the private sector. Regarding the state’s contribution, fiscal consolidation in response to the decline in oil prices and the associated impact on the fiscus could result in some of these infrastructure projects being postponed. One strategy authorities could opt for, although not confirmed as yet, is that the SWF shift its strategy to invest less abroad and as such take over some of the projects that would have been covered in the fiscal budget.

7 | Construction & Infrastructure

EthiopiaThe nominal value of Ethiopia’s infrastructure increased three-fold from 2007 to 2013 and is now the seventh-largest on the continent. The country’s development strategy is currently still guided by the Growth and Transformation Plan (GTP) 2010-15. At its core, the GTP is a public-sector led investment strategy, with a particular focus on raising agricultural output and productivity, promoting industrialisation, and investing heavily in infrastructure. Ethiopia’s investment-led development strategy has delivered robust GDP growth and progress toward Millennium Development Goals (MDGs). In addition, development has been widespread, resulting in a remarkable reduction in poverty. Regional integration holds significant potential to support

growth in East Africa, as smaller economies benefit from larger regional markets, and countries take advantage of comparative advantages in the larger East African economy. Ethiopia’s ability to supply the region with electricity will be a key factor in supporting regional integration, allowing the country to take advantage of its demographic and natural resource advantages. From an installed capacity of only 2,300 MW at present, the Ethiopian Electric and Power Corporation (EEPCo) is planning to boost its generating abilities to 37,000 MW by 2037. Eventually, it is hoping to export in excess of 4,000 MW of hydroelectric power to nine of its East African neighbours. The country has the potential to source up to 45,000 MW from hydropower alone

GhanaThe shopping scene in the Great Accra Metropolitan Area (GAMA, the eleventh-largest metropolitan area in Africa) has changed significantly in the wake of oil being discovered in the country during 2007 and exported from late 2010. This helped the Ghanaian economy to grow by an average of 8.7% p.a. over the past five years while private consumption expenditure expanded by a mean of 7.5% p.a. The country’s growing middle class has attracted many international brands to its retail centres and is seeing a westernisation of shopping trends. However, the increase in shopping malls and the formalisation of the retail market has so far failed to keep pace with shoppers’ demands, and retail space is in short supply. The 27,500 m2 first phase of the West Hills Mall in Accra was opened in October 2014 with the 12,000 m2 second phase under construction. The 14,000 m2 Achimota Retail Centre is expected

to be completed by October 2014 and the 27,500 m2 Kumasi City Mall is set to open during H1 of 2016. A total of 250,000 m2 in space will be under development over the next three years. Looking further ahead, Ghana has an immense window of opportunity to benefit from favourable demographic shifts over the next 25 years. The working-age population (as a percentage of the total) is forecast by the United Nations to increase from 57.5% in 2010 to 64.8% in 2040 due to an expected drop in the country’s fertility rate. At the same time, income distribution dynamics will improve notably: the share of Ghanaians in the low income bracket is expected to fall from 60% at present to just 20% by 2030, while an emerging middle class and a small upper middle income group are also expected to emerge, accounting for 20% and 10% of the population, respectively, in 15 years from now.

Construction & Infrastructure | 8

Ivory CoastAbidjan successfully launched a US$750m, 10-year Eurobond issuance during July 2014 – the country’s first venture into the international debt market since defaulting on its first Eurobond payments some three years earlier. The Eurobond was issued with the intent of making a big contribution towards upgrading the cocoa-producing country’s physical infrastructure as part of its US$23bn National Development Plan. A second Eurobond (a 13-year note worth US$1bn) was offered to the market in March 2015 to bolster government finances and promote economic development. The purpose of the Eurobond and a planned debut US$350m sukuk bond during 2015 is to help finance the fiscal budget which is focused on employment creation and infrastructure development. The country already has some of the most developed and busiest port

infrastructure on the continent, ranked amongst the top 25% of countries by the World Economic Forum (WEF), and the government is on a drive to further increase its capacity to serve the trade needs of landlocked neighbours. China EximBank announced in December 2014 that it has made US$875m worth of financing available towards the construction of a second container terminal at the Port of Abidjan – already the largest harbour in West Africa – and construction is set to start during Q2 of 2015. With this project and other transport sector developments in mind, Business Monitor International (BMI) projects the local construction sector to grow by an average of 9% p.a. during 2015-19. French companies (e.g. Bouygues and Bollore) are players in the local construction sector.

KenyaThe standard-gauge railway that is currently under construction in Kenya has the potential to raise the country’s economic growth rate by 1.5 percentage points annually when finished. The railway line, which is expected to be completed before the end of 2017, will support growth by increasing national and international trade. The first phase of the scheme involves construction of a 472 km railway line from the coastal town of Mombasa to Nairobi. The next phase will be a 505 km railway line from Nairobi to Malaba on the Kenya-Uganda border. In order to generate funding for such projects, Kenya has in recent years sold dedicated infrastructure bonds: during October 2014, the country sold US$117m worth of 12-year bonds. From a regional perspective, integration efforts within the EAC received a significant boost in November 2014 when the World Bank pledged to provide support

for infrastructure investment across the region. The multilateral organisation stated that it will loan the EAC some US$1.2bn to improve inland waterways and ports in Kenya and Tanzania, as part of efforts to boost integration in the region. More specifically, the funds will be used to revive inland waterways on Lake Tanganyika and Lake Victoria, and improve handling capacity and efficiency at the Mombasa and Dar es Salaam ports. The EAC, which comprises Kenya, Tanzania, Uganda, Rwanda and Burundi is undertaking a substantial infrastructure investment programme while also deepening policy integration and reducing barriers to trade. In a recent 2015-25 strategy paper, the bloc stated that it needs at least US$68bn, and possibly up to US$100bn, over the next decade to develop roads, ports, railways, transmission lines and oil & gas infrastructure.

9 | Construction & Infrastructure

MozambiqueThe US Energy Information Administration (EIA) currently estimates Mozambique’s proven natural gas reserves at 100 trillion cubic feet (Tcf), which is the third-largest on the continent after Nigeria and Algeria. The lead developers of the country’s offshore reserves are the US’s Anadarko and Italy’s Eni who expect to start liquefied natural gas (LNG) exports from the Rovuma Basin by 2019 (at the earliest). Mozambican authorities are accumulating debt at an increasing pace in order to finance infrastructure projects, while the private sector is set to accumulate external financing aggressively in order to finance the vast imports needed to develop the natural gas sector. In addition, Mozambique could see up to US$20bn in net FDI during 2014-18 of which 80% will go towards the development of

the gas industry. The country’s overall infrastructure stock has doubled in value since 2008 as international gas companies upgraded and expanded the country’s infrastructure footprint. (Mozambique needs to import most of its capital and consumption requirements related to extractive industries.) Significant development is expected around the Palma area in the Cabo Delgado province. Empresa Nacional de Hidrocarbonetos EP (ENH, the state petroleum company) is planning an 18,000 hectare development adjacent to Anadarko and Eni’s planned LNG facilities that will feature residential, energy-intensive industrial, retail, agricultural and tourism components. This could see 250,000 people migrate to the area.

NamibiaNamibia’s infrastructure is of a high quality both in an African and global context. The country’s industrial sector has historically been dominated by mining and manufacturing though in recent years the construction industry has been buoyed by several large-scale infrastructural initiatives, such as the Port of Walvis Bay expansion project, the building of the Neckartal Dam, the government’s mass housing scheme, as well as developments at the Husab uranium mine, Otjikoto gold mine and Tschudi copper mine. (The various large-scale infrastructural projects currently underway in the country will continue to add pressure on the trade deficit due to the imports of building materials and certain high-value parts and components.) Amongst Namibia’s largest projects, construction of the Southern Africa Development Community (SADC) Gateway Port

(some 5 km north of Walvis Bay) will commence during H1 of 2015. This is part of Windhoek’s N$223bn infrastructure development plan which will also include an expansion of the country’s other harbour at Luderitz. Namibia is positioning itself to play an even greater role as logistics hub for the Southern African region, in particular landlocked countries like the Botswana, the Democratic Republic of the Congo (DRC), Malawi, Zambia and Zimbabwe. This drive will include private financiers and international construction companies – South African enterprises such as Aveng and Murray & Roberts have subsidiaries in the country. It is expected that the construction sector will remain one of the main drivers of Namibia’s economic growth over the medium term.

11 | Construction & Infrastructure

NigeriaFrom a political risk perspective, the effectiveness of state structures in Africa’s largest economy are under pressure from infrastructure challenges as well as corruption. Despite being the continent’s biggest hydrocarbon producer, Nigeria is blighted by persistent electricity outages, which force businesses and individuals who can afford them to rely on diesel generators. The country’s current peak power generation is around 4,000 MW compared to peak demand near 13,000 MW. Indeed, Nigeria’s net electricity generation per capita is amongst the lowest in the world, with around half of the population not having access to electricity. The government is hoping to connect 1.5 million Nigerians per year to the electricity grid in order to have 75% of citizens connected by the year 2020. The country’s power sector is currently on an expansion drive after being unbundled into

generation and distribution companies and a single transmission company. Nigeria holds the largest natural gas reserves in Africa, but presently still has limited infrastructure in place to take advantage of this massive energy resource. (At present, natural gas that is associated with oil production is mostly flared.) In March 2011, President Goodluck Jonathan formally launched the federal government’s Gas Revolution Master Plan, an ambitious programme designed to mark the beginning of the end of gas flaring in the country. The overall strategy is to attract US$25bn worth of investment into developing the country’s gas infrastructure and to create about 600,000 new jobs. The Nigerian National Petroleum Corporation (NNPC) expects to see US$16bn investment into gas-to-power, gas-based industrialisation and gas export activities over the next four years.

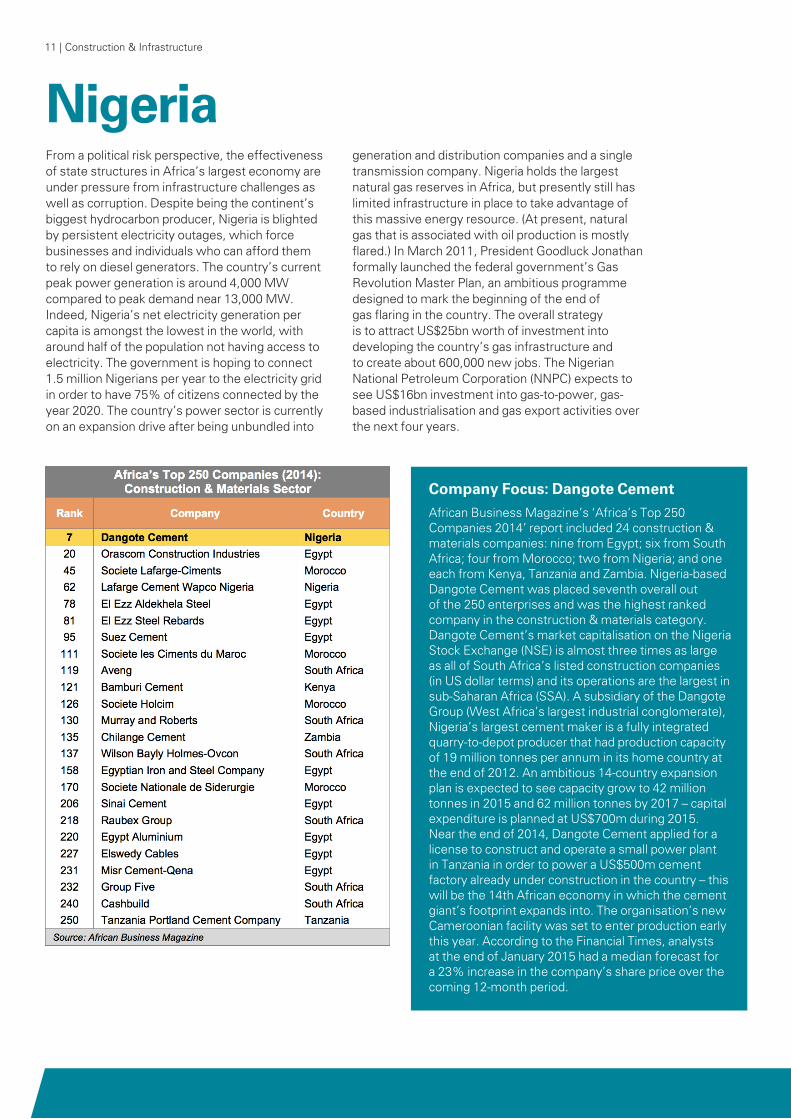

Company Focus: Dangote Cement

African Business Magazine’s ‘Africa’s Top 250 Companies 2014’ report included 24 construction & materials companies: nine from Egypt; six from South Africa; four from Morocco; two from Nigeria; and one each from Kenya, Tanzania and Zambia. Nigeria-based Dangote Cement was placed seventh overall out of the 250 enterprises and was the highest ranked company in the construction & materials category. Dangote Cement’s market capitalisation on the Nigeria Stock Exchange (NSE) is almost three times as large as all of South Africa’s listed construction companies (in US dollar terms) and its operations are the largest in sub-Saharan Africa (SSA). A subsidiary of the Dangote Group (West Africa’s largest industrial conglomerate), Nigeria’s largest cement maker is a fully integrated quarry-to-depot producer that had production capacity of 19 million tonnes per annum in its home country at the end of 2012. An ambitious 14-country expansion plan is expected to see capacity grow to 42 million tonnes in 2015 and 62 million tonnes by 2017 – capital expenditure is planned at US$700m during 2015. Near the end of 2014, Dangote Cement applied for a license to construct and operate a small power plant in Tanzania in order to power a US$500m cement factory already under construction in the country – this will be the 14th African economy in which the cement giant’s footprint expands into. The organisation’s new Cameroonian facility was set to enter production early this year. According to the Financial Times, analysts at the end of January 2015 had a median forecast for a 23% increase in the company’s share price over the coming 12-month period.

Construction & Infrastructure | 12

13 | Construction & Infrastructure

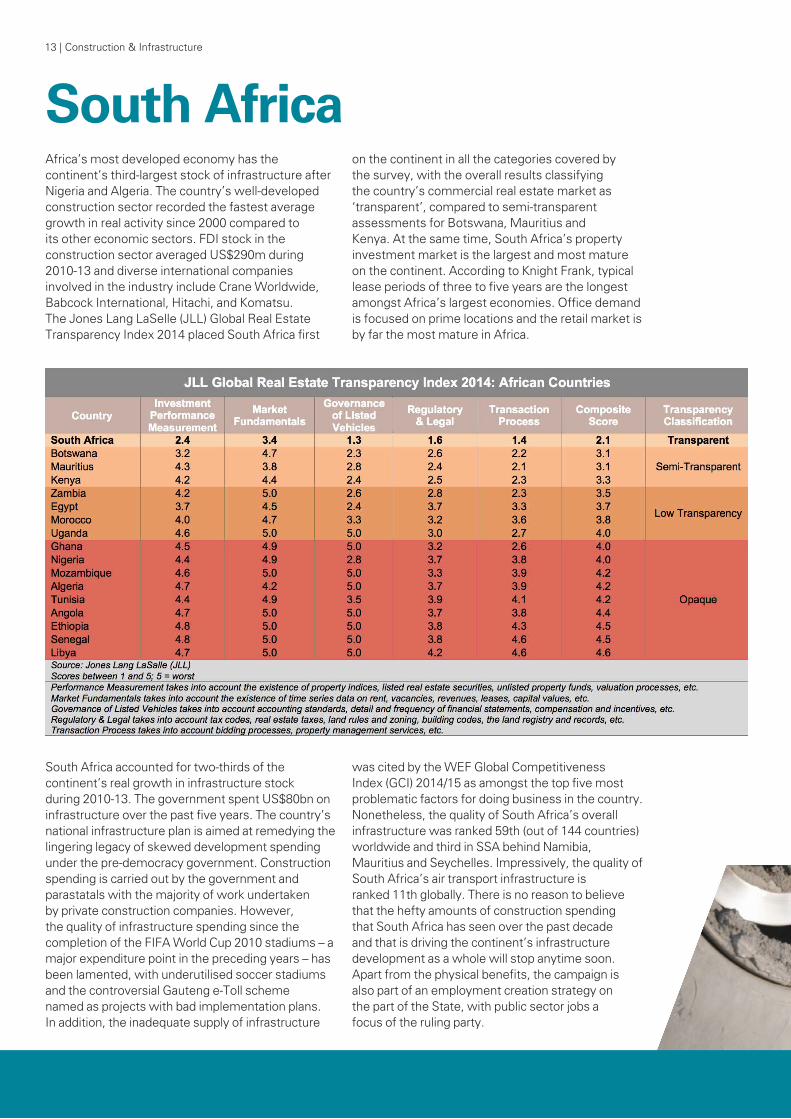

South AfricaAfrica’s most developed economy has the continent’s third-largest stock of infrastructure after Nigeria and Algeria. The country’s well-developed construction sector recorded the fastest average growth in real activity since 2000 compared to its other economic sectors. FDI stock in the construction sector averaged US$290m during 2010-13 and diverse international companies involved in the industry include Crane Worldwide, Babcock International, Hitachi, and Komatsu. The Jones Lang LaSelle (JLL) Global Real Estate Transparency Index 2014 placed South Africa first

on the continent in all the categories covered by the survey, with the overall results classifying the country’s commercial real estate market as ‘transparent’, compared to semi-transparent assessments for Botswana, Mauritius and Kenya. At the same time, South Africa’s property investment market is the largest and most mature on the continent. According to Knight Frank, typical lease periods of three to five years are the longest amongst Africa’s largest economies. Office demand is focused on prime locations and the retail market is by far the most mature in Africa.

South Africa accounted for two-thirds of the continent’s real growth in infrastructure stock during 2010-13. The government spent US$80bn on infrastructure over the past five years. The country’s national infrastructure plan is aimed at remedying the lingering legacy of skewed development spending under the pre-democracy government. Construction spending is carried out by the government and parastatals with the majority of work undertaken by private construction companies. However, the quality of infrastructure spending since the completion of the FIFA World Cup 2010 stadiums – a major expenditure point in the preceding years – has been lamented, with underutilised soccer stadiums and the controversial Gauteng e-Toll scheme named as projects with bad implementation plans. In addition, the inadequate supply of infrastructure

was cited by the WEF Global Competitiveness Index (GCI) 2014/15 as amongst the top five most problematic factors for doing business in the country. Nonetheless, the quality of South Africa’s overall infrastructure was ranked 59th (out of 144 countries) worldwide and third in SSA behind Namibia, Mauritius and Seychelles. Impressively, the quality of South Africa’s air transport infrastructure is ranked 11th globally. There is no reason to believe that the hefty amounts of construction spending that South Africa has seen over the past decade and that is driving the continent’s infrastructure development as a whole will stop anytime soon. Apart from the physical benefits, the campaign is also part of an employment creation strategy on the part of the State, with public sector jobs a focus of the ruling party.

Construction & Infrastructure | 14

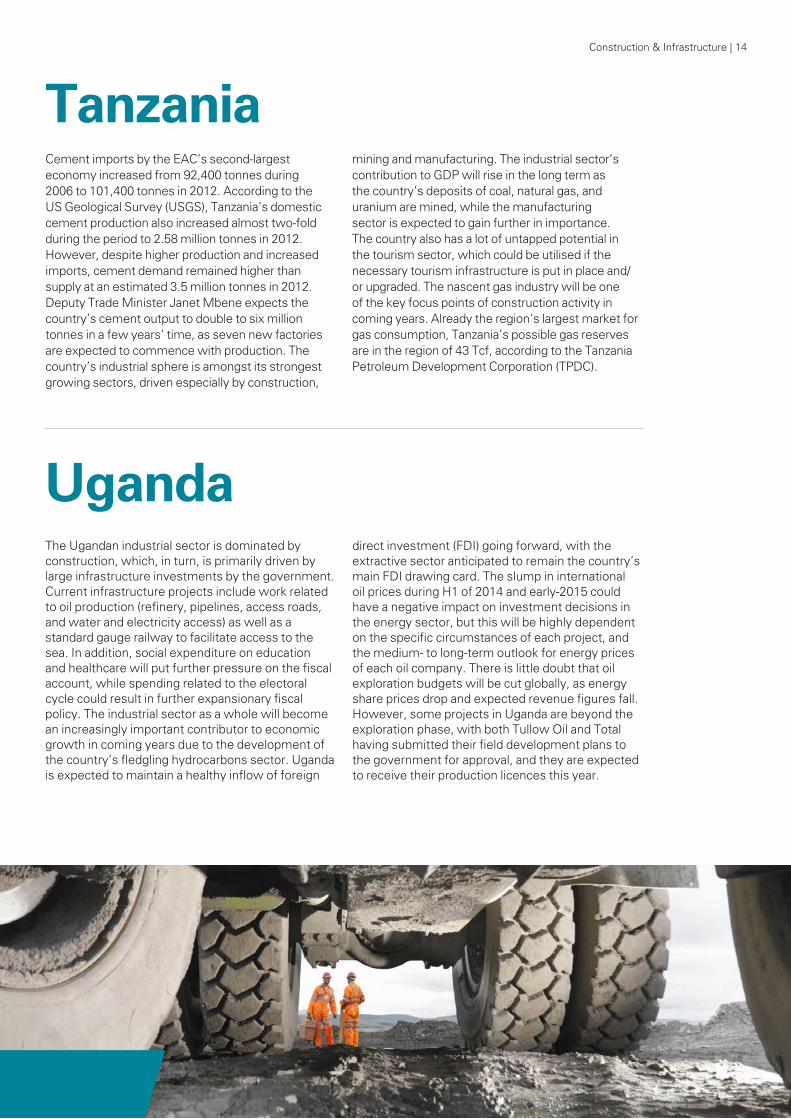

TanzaniaCement imports by the EAC’s second-largest economy increased from 92,400 tonnes during 2006 to 101,400 tonnes in 2012. According to the US Geological Survey (USGS), Tanzania’s domestic cement production also increased almost two-fold during the period to 2.58 million tonnes in 2012. However, despite higher production and increased imports, cement demand remained higher than supply at an estimated 3.5 million tonnes in 2012. Deputy Trade Minister Janet Mbene expects the country’s cement output to double to six million tonnes in a few years’ time, as seven new factories are expected to commence with production. The country’s industrial sphere is amongst its strongest growing sectors, driven especially by construction,

mining and manufacturing. The industrial sector’s contribution to GDP will rise in the long term as the country’s deposits of coal, natural gas, and uranium are mined, while the manufacturing sector is expected to gain further in importance. The country also has a lot of untapped potential in the tourism sector, which could be utilised if the necessary tourism infrastructure is put in place and/or upgraded. The nascent gas industry will be one of the key focus points of construction activity in coming years. Already the region’s largest market for gas consumption, Tanzania’s possible gas reserves are in the region of 43 Tcf, according to the Tanzania Petroleum Development Corporation (TPDC).

UgandaThe Ugandan industrial sector is dominated by construction, which, in turn, is primarily driven by large infrastructure investments by the government. Current infrastructure projects include work related to oil production (refinery, pipelines, access roads, and water and electricity access) as well as a standard gauge railway to facilitate access to the sea. In addition, social expenditure on education and healthcare will put further pressure on the fiscal account, while spending related to the electoral cycle could result in further expansionary fiscal policy. The industrial sector as a whole will become an increasingly important contributor to economic growth in coming years due to the development of the country’s fledgling hydrocarbons sector. Uganda is expected to maintain a healthy inflow of foreign

direct investment (FDI) going forward, with the extractive sector anticipated to remain the country’s main FDI drawing card. The slump in international oil prices during H1 of 2014 and early-2015 could have a negative impact on investment decisions in the energy sector, but this will be highly dependent on the specific circumstances of each project, and the medium- to long-term outlook for energy prices of each oil company. There is little doubt that oil exploration budgets will be cut globally, as energy share prices drop and expected revenue figures fall. However, some projects in Uganda are beyond the exploration phase, with both Tullow Oil and Total having submitted their field development plans to the government for approval, and they are expected to receive their production licences this year.

15 | Construction & Infrastructure

ZambiaThe rapid expansion seen in the mining sector since the turn of the century and resultant increase in downstream activities have boosted the industrial sector’s contribution to Zambia’s economic activity to 26% of GDP. Robust performance by the construction sector (accounting for about an eighth of GDP) has been underpinned by large-scale mining investments and developments, the domestic production of cement, as well as strong infrastructure spending by the government. Zambia has a structural fiscal deficit due to the high pressure on fixed capital formation in order to address the gaping transport and power infrastructure shortfall. Infrastructure-related projects account for 60% of the World Bank’s portfolio in Zambia and the average life of a project is 3.8 years. Geographically,

Zambia is favourably located as a regional hub and entry point into the SADC and close to the fast-growing EAC region, a position which could only firm up with the completion of the country’s ambitious road, rail and freight transport and power infrastructural programme. The outlook for the construction sector remains robust, and favourably positioned to take advantage of the prolonged energy (and to a lesser extent, base metal) slump. The industrial sector is forecast to continue growing in coming years on the back of on-going mining-related investment, although downside risk pertaining to proposed changes in the mining fiscal regime and current opacity in the political arena are expected to introduce short-term impediments.

Construction & Infrastructure | 16

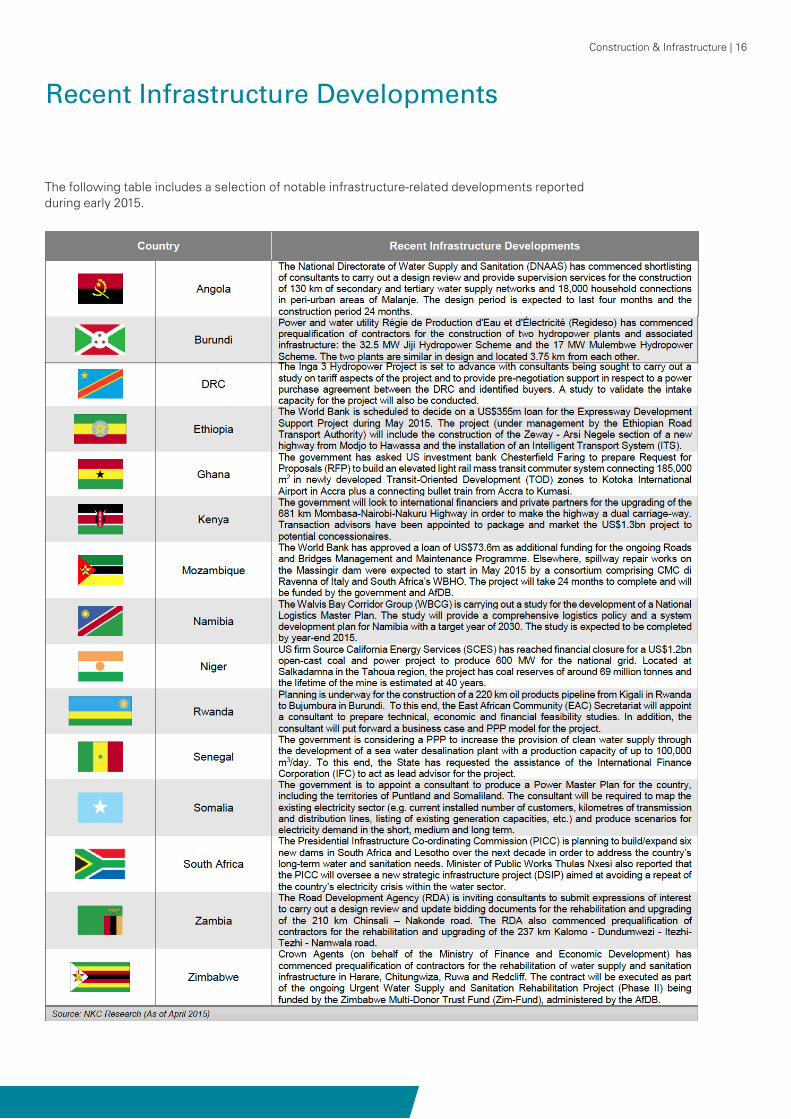

Recent Infrastructure Developments

The following table includes a selection of notable infrastructure-related developments reported during early 2015.

17 | Construction & Infrastructure

Final Thoughts

Africa’s largest, most vibrant and fastest growing economies are offering significant opportunities for companies in the construction business and with interests in infrastructure development. However, these countries are far from homogenous, and present diverse bureaucratic requirements, construction costs, levels of industry transparency, foreign involvement, and financial market development. Africa’s construction and infrastructure landscape is certainly full of challenges – as are many other sectors.

The continent is said to have a significant handicap in terms of economic development potential due to its infrastructure deficit. Even when excluding profit and loss considerations, the infrastructure issue is at heart also a humanitarian and socio-economic issue. In the case of some 40 billion potential work hours lost each year to African people being unable

to open a tap in their homes for water, the issue of infrastructure expands into areas of health and education as well.

However, with the rapid expansion in infrastructure seen over the past decade, the growing interest in non-African companies in partaking in this immense growth, as well as the evident positive outlook for construction in many African states, the opportunities presented by the continent cannot be ignored. This document incorporates an overview of several countries’ current activities surrounding oil and gas, shipping, electricity, retail, ports and railway. Africa is evidently firmly on the radar of major construction multinational companies with hundreds of large projects already underway on the continent. These initiatives are no longer limited to mineral resources, as many still believe, and have diversified into other sectors.

Key Infrastructure Indicators

Construction & Infrastructure | 18

Construction & Infrastructure | 20

Access Capital AECOM African Business Magazine African Business Review AllAfrica.com Andrew Maggs Consulting Bloomberg Broll Business Day Business Monitor International (BMI) Dangote Group DHL Engineering News Financial Mail Financial Times Global Cement Government of South Africa

Sources of InformationHow We Made It In Africa Infrastructure Consortium of Africa (ICA) International Monetary Fund (IMF) KPMG McKinsey & Company NKC African Economics Organisation for Economic Cooperation and Development (OECD) Reuters Suez Canal Authority The Africa Report The Oxford Business Group Trade Map United Nations US Geological Survey (USGS) USAID World Bank World Economic Forum (WEF)

© 2015 KPMG Africa Limited, a Cayman Islands company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. MC13429.

kpmg.com/social media kpmg.com/app

Seyi BickerstethChairman KPMG AfricaT: +234(1)4620045, 2805984 E: [email protected]

Bryan LeithCOO KPMG AfricaT: +27116476245 E: [email protected]

Benson MwesigwaAfrica High Growth MarketsKPMG AfricaT: +27609621364 E: [email protected]

Molabowale AdeyemoAfrica High Growth MarketsKPMG AfricaT: +27714417378 E: [email protected]

Gavin MaillePartner & Sector Leader Industrial,Automotive and ConstructionKPMG in South AfricaT: +27832537165 E: [email protected]

Klaus FindtHead, Infrastructure and Major Projects Group AfricaT: +27832899650E: [email protected] Kunle ElebutePartner & Head, Advisory ServicesKPMG in NigeriaT: +2348034020970 E: [email protected]

Sheel GillDirector, Transactions & RestructuringEast AfricaT: +254725650283 E: [email protected]

Contact details

KPMG Africa

21 | Construction & Infrastructure

Related Documents