Aerospace & Defense 2008 Outlook and Investment Themes July 8, 2008 Ken Herbert Vice President/Partner

Aerospace & Defense Analyst Briefing: 2008 Outlook and Investment Themes

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Aerospace & Defense

2008 Outlook and Investment Themes

July 8, 2008

Ken Herbert

Vice President/Partner

2www.frost.com

Agenda

• Industry Fundamentals

• Market Outlook

• Investment Themes and Proprietary Research

3www.frost.com

Main Focus Areas

Commercial Aviation & Services

Commercial Aviation & Services

Defense Technologies &

Services

Defense Technologies &

Services

Airborne Platforms & Avionics

Airborne Platforms & Avionics

Aircraft & Engine MRO

Aircraft & Engine MRO

Homeland SecurityHomeland SecurityC4ISRC4ISR

4www.frost.com

Agenda

• Industry Fundamentals

5www.frost.com

Key Issues Impacting Industry Today

1. Top line growth facing headwinds, Commercial aerospace and Defense

cycles peaking?

2. Changing administration and political uncertainty

3. Shifting defense procurement priorities

4. Aircraft OEMs shifting business model, pushing more risk onto suppliers,

geographic expansion

5. Secular Asian growth drives need for exposure across entire industry

6. PMA and MRO models evolving

7. Increasing industry consolidation, European firms building presence in US

defense market, Asian firms expanding globally

8. Maintaining earnings growth as cycles slow, managing costs and margins

9. Effective position in homeland security market to maximize opportunities

10. Business jet offset, how much more can it provide?

6www.frost.com

Industry Fundamentals: Commercial Aerospace

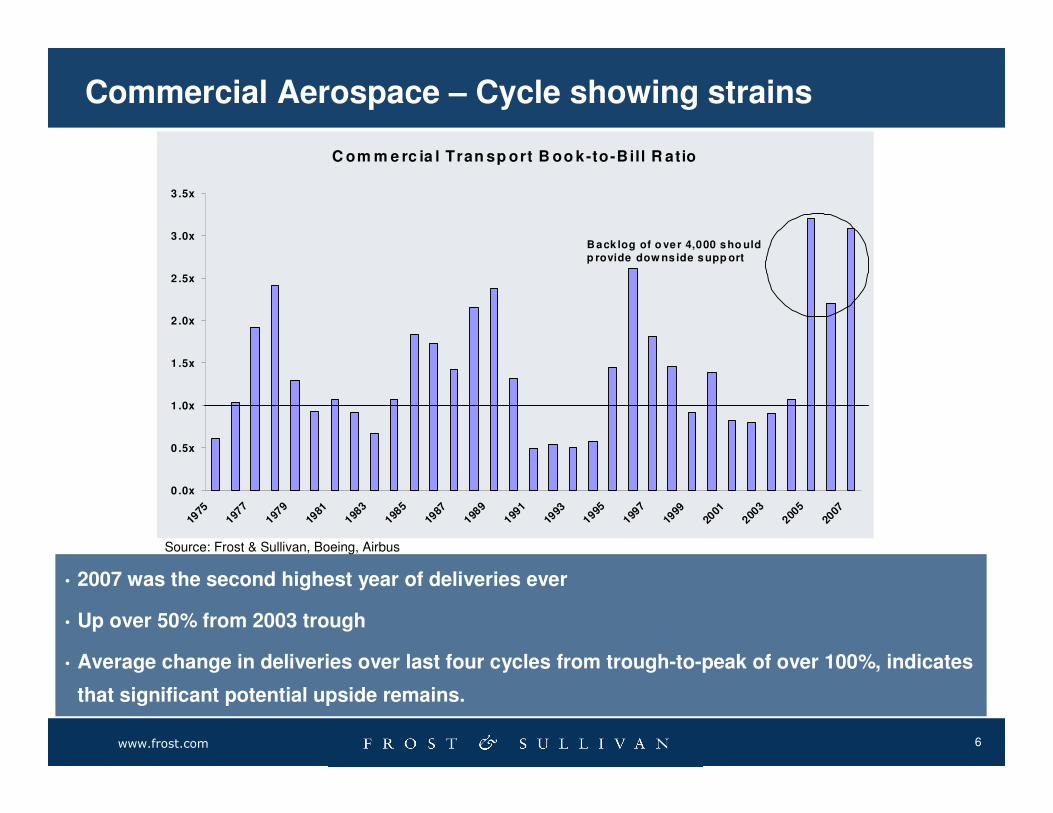

• 2007 was the second highest year of deliveries ever

• Up over 50% from 2003 trough

• Average change in deliveries over last four cycles from trough-to-peak of over 100%, indicates

that significant potential upside remains.

C om m e rc ia l Tran sp ort B oo k-to-Bill R atio

0 .0x

0 .5x

1 .0x

1 .5x

2 .0x

2 .5x

3 .0x

3 .5x

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

B ack log of o ver 4,000 sho uld p rovide dow ns ide supp ort

Commercial Aerospace – Cycle showing strains

Source: Frost & Sullivan, Boeing, Airbus

7www.frost.com

Industry Fundamentals: Commercial Aerospace

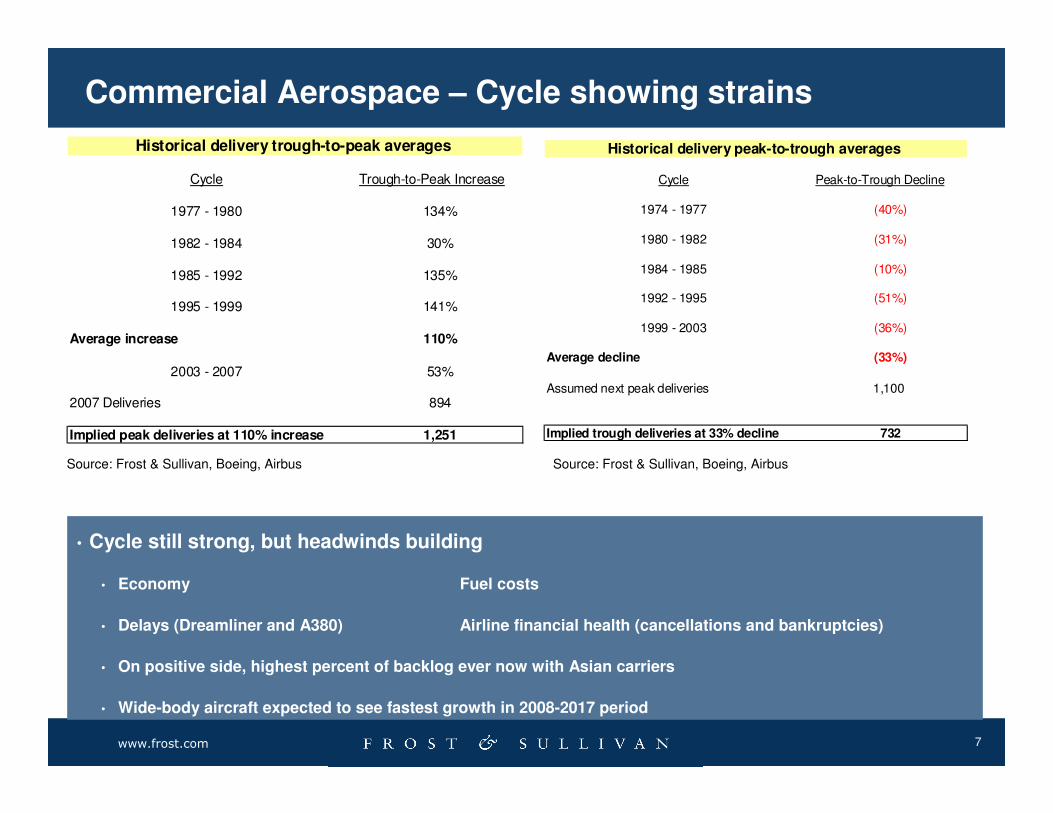

• Cycle still strong, but headwinds building

• Economy Fuel costs

• Delays (Dreamliner and A380) Airline financial health (cancellations and bankruptcies)

• On positive side, highest percent of backlog ever now with Asian carriers

• Wide-body aircraft expected to see fastest growth in 2008-2017 period

Commercial Aerospace – Cycle showing strains

Cycle Trough-to-Peak Increase

1977 - 1980 134%

1982 - 1984 30%

1985 - 1992 135%

1995 - 1999 141%

Average increase 110%

2003 - 2007 53%

2007 Deliveries 894

Implied peak deliveries at 110% increase 1,251

Historical delivery trough-to-peak averages

Cycle Peak-to-Trough Decline

1974 - 1977 (40%)

1980 - 1982 (31%)

1984 - 1985 (10%)

1992 - 1995 (51%)

1999 - 2003 (36%)

Average decline (33%)

Assumed next peak deliveries 1,100

Implied trough deliveries at 33% decline 732

Historical delivery peak-to-trough averages

Source: Frost & Sullivan, Boeing, Airbus Source: Frost & Sullivan, Boeing, Airbus

8www.frost.com

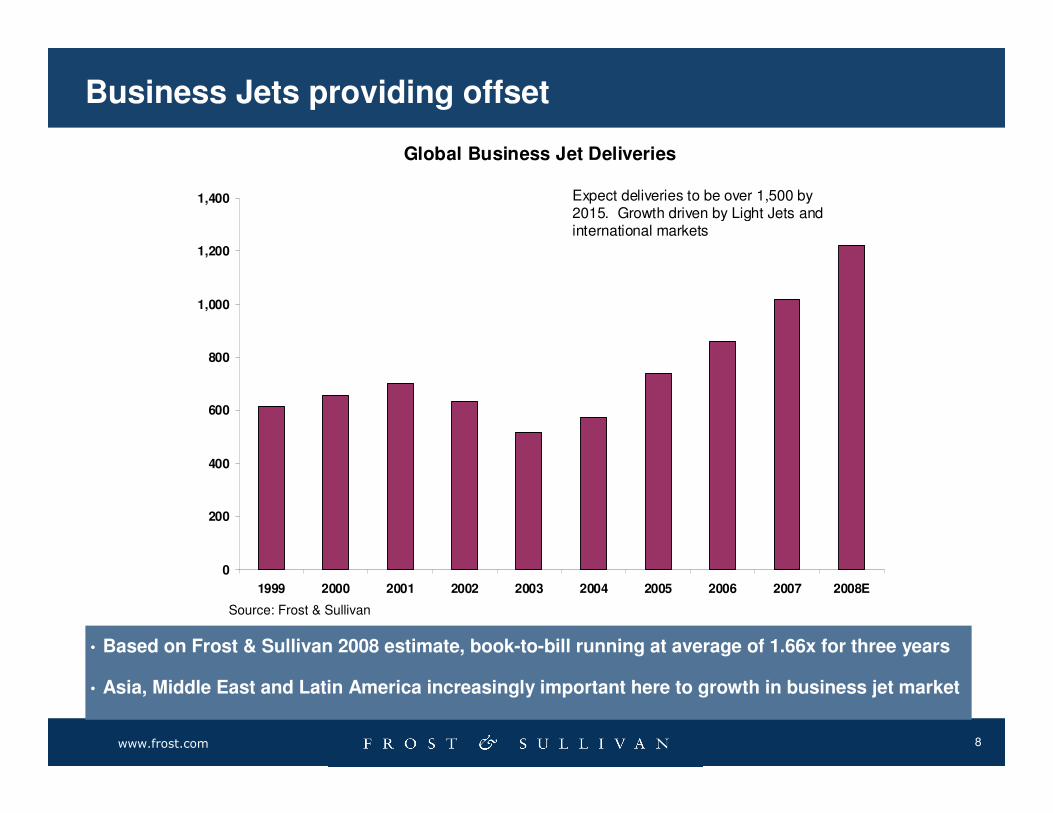

Business Jets providing offset

• Based on Frost & Sullivan 2008 estimate, book-to-bill running at average of 1.66x for three years

• Asia, Middle East and Latin America increasingly important here to growth in business jet market

Global Business Jet Deliveries

0

200

400

600

800

1,000

1,200

1,400

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008E

Expect deliveries to be over 1,500 by 2015. Growth driven by Light Jets and international markets

Source: Frost & Sullivan

9www.frost.com

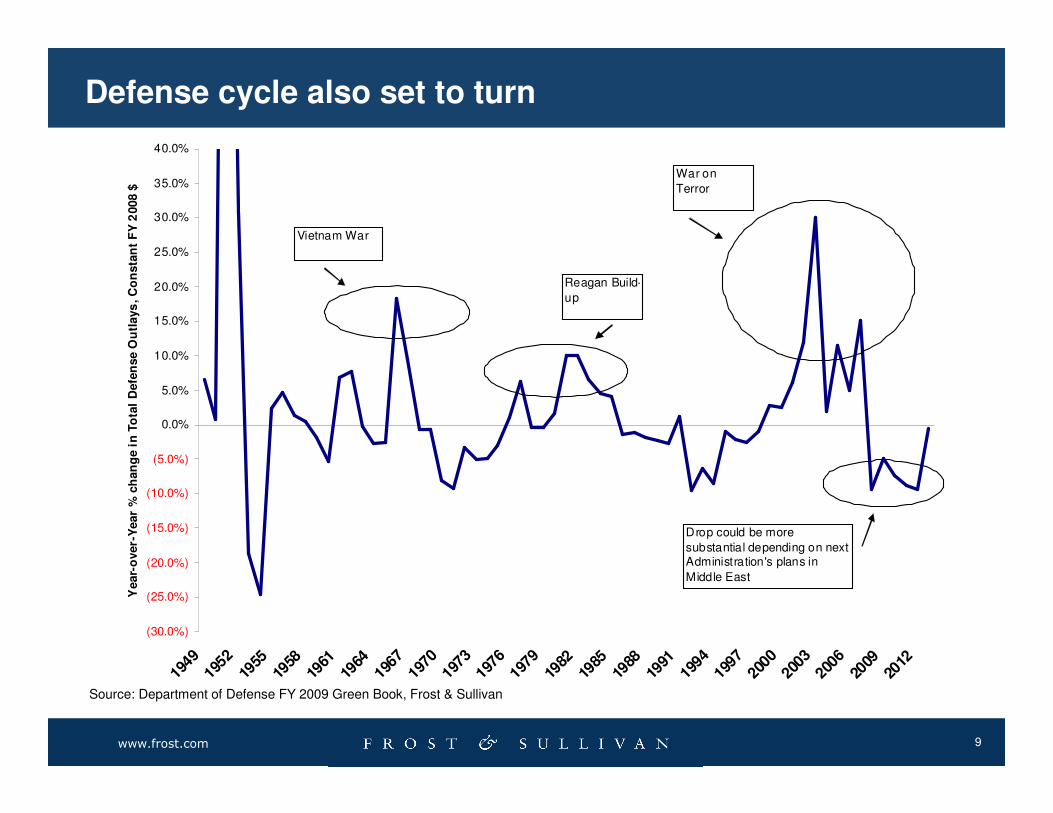

Defense cycle also set to turn

(30.0%)

(25.0%)

(20.0%)

(15.0%)

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Year-

over-

Year

% c

han

ge i

n T

ota

l D

efe

nse O

utl

ays

, C

on

sta

nt

FY

2008 $

Drop could be more

substantial depending on next Administration's plans in

Middle East

Vietnam War

Reagan Build-

up

War on

Terror

Source: Department of Defense FY 2009 Green Book, Frost & Sullivan

10www.frost.com

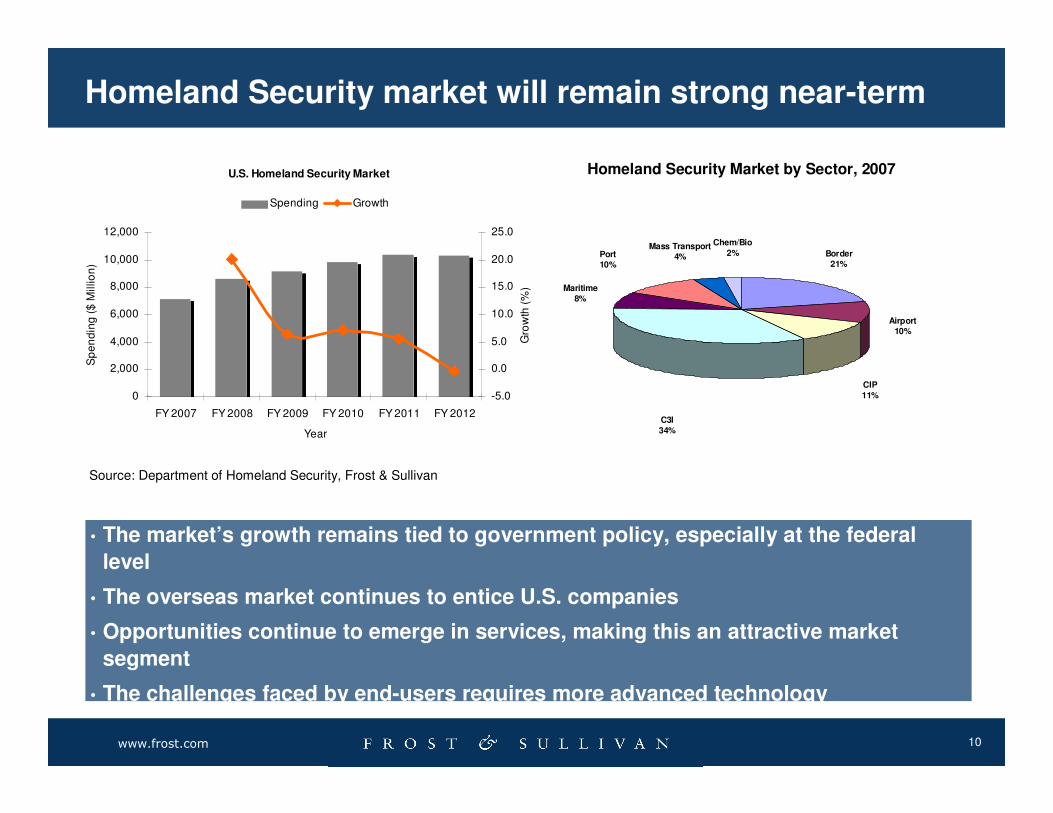

Homeland Security market will remain strong near-term

• The market’s growth remains tied to government policy, especially at the federal

level

• The overseas market continues to entice U.S. companies

• Opportunities continue to emerge in services, making this an attractive market

segment

• The challenges faced by end-users requires more advanced technology

U.S. Homeland Security Market

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Year

Sp

en

din

g (

$ M

illio

n)

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Gro

wth

(%

)

Spending Growth

Homeland Security Market by Sector, 2007

Mass Transport4%

Chem/Bio2%Port

10%

Maritime8%

C3I34%

CIP11%

Airport10%

Border21%

Source: Department of Homeland Security, Frost & Sullivan

11www.frost.com

Agenda

• Market Outlook

12www.frost.com

Frost & Sullivan Market Outlook

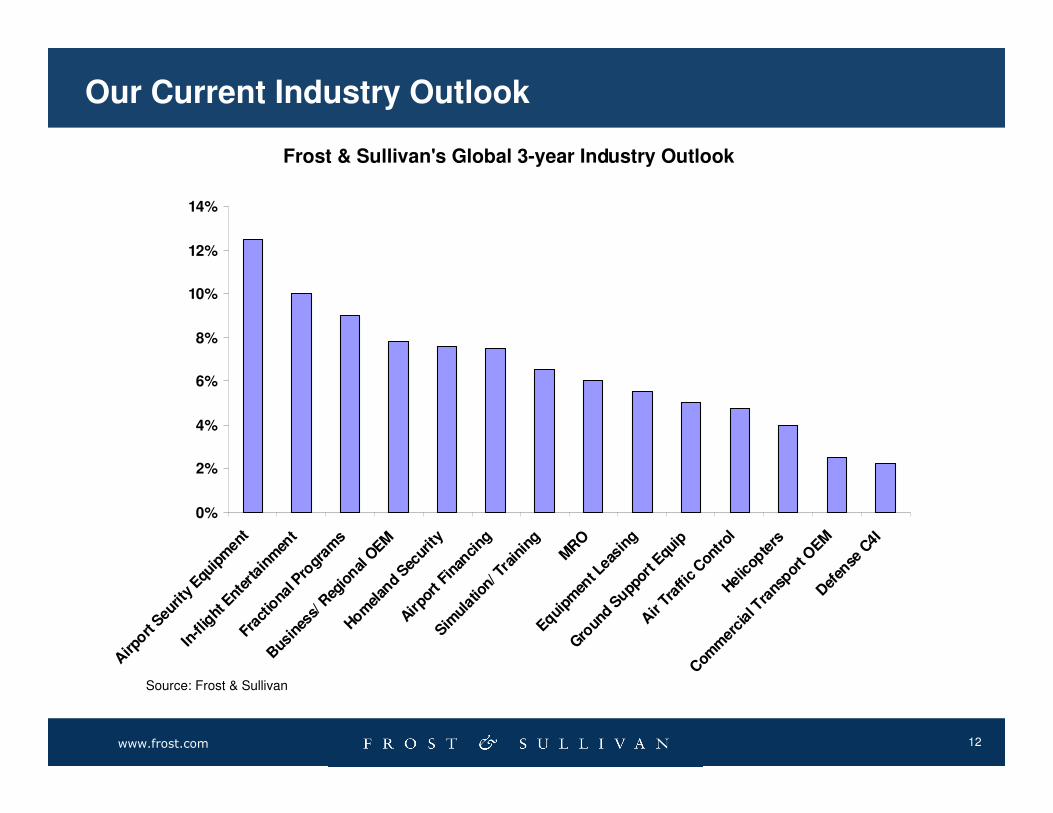

Our Current Industry Outlook

Frost & Sullivan's Global 3-year Industry Outlook

0%

2%

4%

6%

8%

10%

12%

14%

Airp

ort Seu

rity

Equip

men

t

In-fl

ight

Ent

erta

inm

ent

Frac

tiona

l Pro

gram

s

Bus

ines

s/ R

egio

nal O

EM

Homel

and

Secur

ity

Airpo

rt F

inan

cing

Simul

atio

n/ T

rain

ing

MR

O

Equipm

ent L

easi

ng

Gro

und

Suppor

t Equ

ip

Air

Traf

fic C

ontr

olHel

icop

ters

Com

mer

cial

Tra

nspor

t OEM

Def

ense

C4I

Source: Frost & Sullivan

13www.frost.com

Agenda

• Investment Themes

14www.frost.com

Agenda

• Secular Asian growth story will continue – opportunities across the

value chain

• Business jet risk to the upside

• Shifting DoD procurement trends creating opportunities

• Cost rationalization and cost structure shifting

• Evolving MRO and PMA business models

15www.frost.com

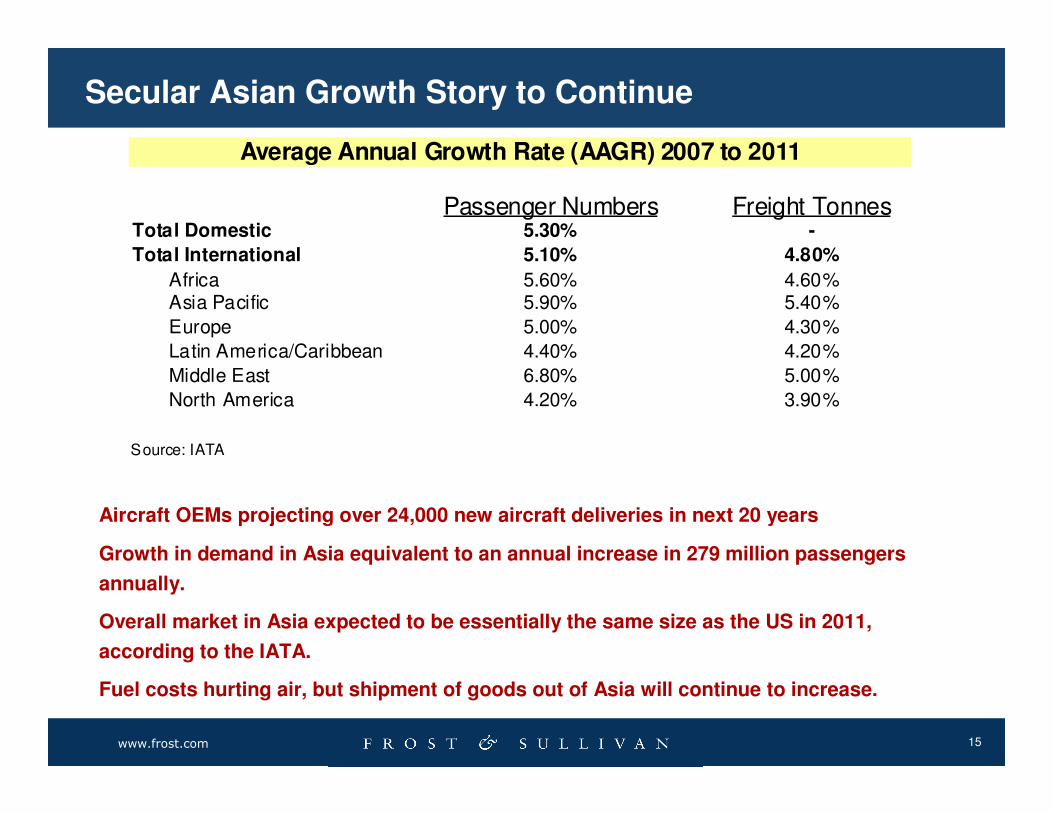

Industry Outlook : Commercial Aerospace

Passenger Numbers Freight TonnesTotal Domestic 5.30% -

Total International 5.10% 4.80%

Africa 5.60% 4.60%Asia Pacific 5.90% 5.40%

Europe 5.00% 4.30%

Latin America/Caribbean 4.40% 4.20%

Middle East 6.80% 5.00%

North America 4.20% 3.90%

Source: IATA

Average Annual Growth Rate (AAGR) 2007 to 2011

Aircraft OEMs projecting over 24,000 new aircraft deliveries in next 20 years

Growth in demand in Asia equivalent to an annual increase in 279 million passengers

annually.

Overall market in Asia expected to be essentially the same size as the US in 2011,

according to the IATA.

Fuel costs hurting air, but shipment of goods out of Asia will continue to increase.

Secular Asian Growth Story to Continue

16www.frost.com

Industry Fundamentals : Commercial Aerospace

Significant investment globally, but very focused in Asia Pacific region.

Coastal regions, such as in China, seeing significant activity

Also, many tier 2 airports planned for upgrade and modifications to support domestic

travel in Asian countries such as China and Indonesia

Asia Pacific Planned Airport Upgrades and New Construction

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010

Upgrades

New Construction

Secular Asian Growth Story to Continue

Air Passenger Shares Air Freight Shares

US Domestic 25% 1%

North America - Latin America 2% 5%Other within North America 3% 0%Europe - North America 2% 12%

Within Europe 24% 6%Europe - Asia Pacific 2% 18%

Within Asia Pacific 27% 26%Asia Pacif ic - North America 2% 13%Within Middle East 2% 1%

Others 6% 17%Within Latin America 5% 1%

Source: IATA

Estimates on 2011 Global Shares of Passengers and Freight

Source: Frost & Sullivan

17www.frost.com

Asia Pacific Aerospace service sector will provide significant opportunities

across spectrum of offerings

Gaps in availability of pilots, maintenance professionals, and cabin crew well understood.

Industry estimates are that at least 17,000 pilots annually need to be trained to keep pace

with optimistic delivery forecasts. These estimates exceed current capacity significantly.

China alone estimates it needs at least 18,000 pilots over the next 20 years.

While obvious opportunities can be played--simulation and training equipment and

hardware, certification programs, language and translation—seeing significant interest

from clients in other ways to benefit.

Secular Asian Growth Story to Continue

18www.frost.com

Business and Regional Jet Risk to the Upside

� Historically, the global business jet market was driven by corporate purchasing in the United

States. That market is currently pressured, resulting in some lowered expectations.

� Our current conservative estimates are that this market will grow by between 8% and 10%

through 2010.

� However, in 2007 over 50% of new business jet purchases are made outside of the US. This

has been driven by wealth creation and explosion of fractional jet model in Asia and Europe.

� Moreover, current expectations are that over 1,600 jets over 30 years of age will retire in the

next three to five years. This accounts for almost 20% of the future expected demand.

� However, there are an additional 1,800 jets that are over 25 years of age in service. We

believe that an acceleration of the replacement rate for these jets is likely. Newer jets are

much more fuel efficient. Moreover, the price of new jets is falling.

� If an additional 25% of the jets that are currently over 25 years old get retired early, the

industry growth can get closer to 15%.

Business Jet Market – Risks to the Upside

19www.frost.com

Business and Regional Jet Risk to the Upside

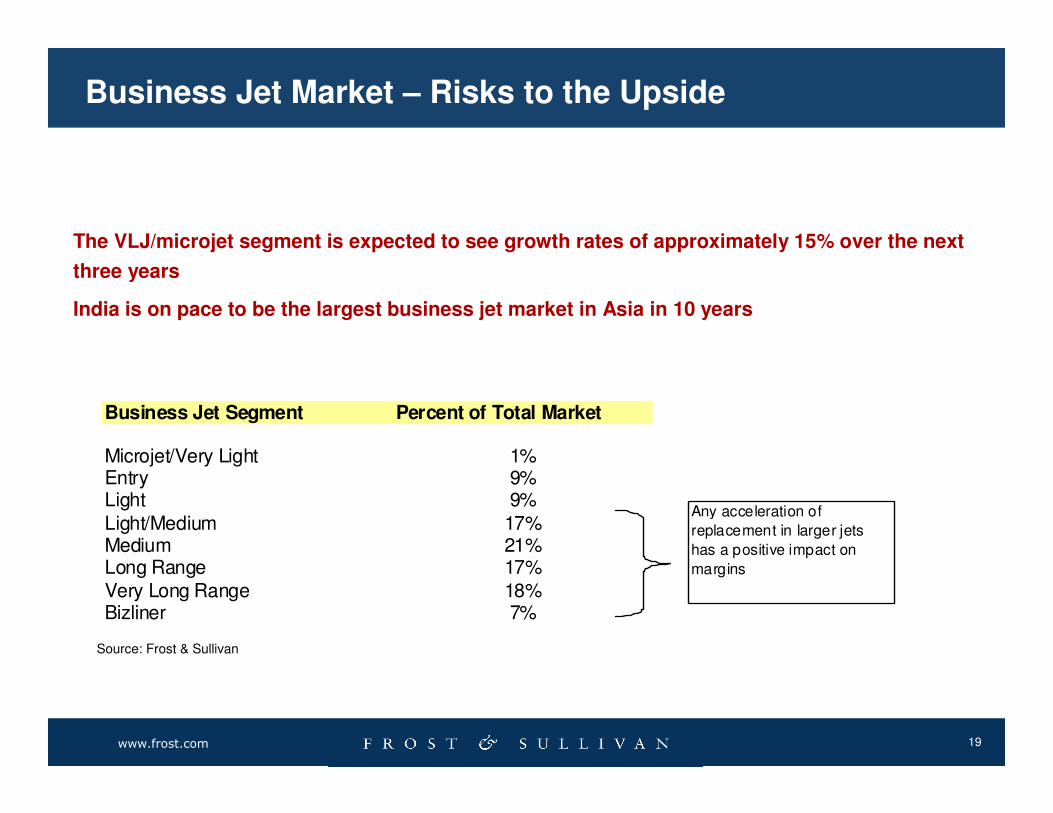

The VLJ/microjet segment is expected to see growth rates of approximately 15% over the next

three years

India is on pace to be the largest business jet market in Asia in 10 years

Business Jet Segment Percent of Total Market

Microjet/Very Light 1%Entry 9%Light 9%Light/Medium 17%Medium 21%Long Range 17%Very Long Range 18%Bizliner 7%

Any acceleration of

replacement in larger jets

has a positive impact on

margins

Business Jet Market – Risks to the Upside

Source: Frost & Sullivan

20www.frost.com

Shifting DoD Procurement Policies Creating Opportunities

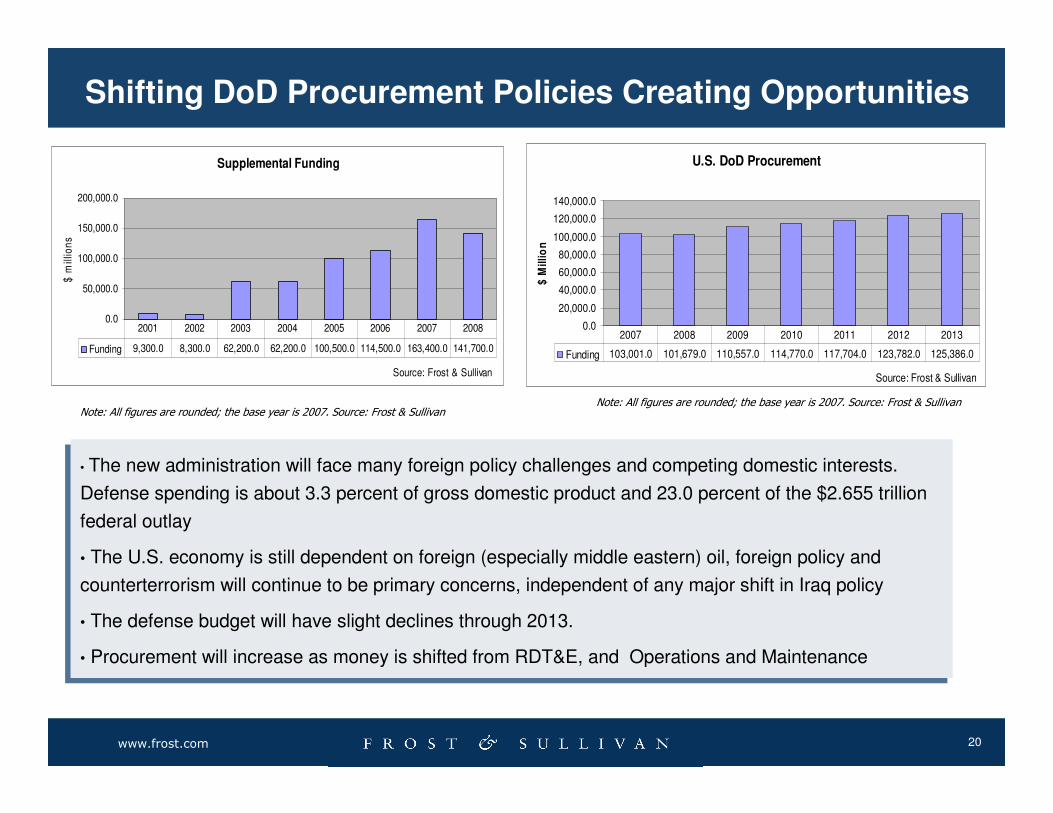

• The new administration will face many foreign policy challenges and competing domestic interests.

Defense spending is about 3.3 percent of gross domestic product and 23.0 percent of the $2.655 trillion

federal outlay

• The U.S. economy is still dependent on foreign (especially middle eastern) oil, foreign policy and

counterterrorism will continue to be primary concerns, independent of any major shift in Iraq policy

• The defense budget will have slight declines through 2013.

• Procurement will increase as money is shifted from RDT&E, and Operations and Maintenance

• The new administration will face many foreign policy challenges and competing domestic interests.

Defense spending is about 3.3 percent of gross domestic product and 23.0 percent of the $2.655 trillion

federal outlay

• The U.S. economy is still dependent on foreign (especially middle eastern) oil, foreign policy and

counterterrorism will continue to be primary concerns, independent of any major shift in Iraq policy

• The defense budget will have slight declines through 2013.

• Procurement will increase as money is shifted from RDT&E, and Operations and Maintenance

Note: All figures are rounded; the base year is 2007. Source: Frost & SullivanNote: All figures are rounded; the base year is 2007. Source: Frost & Sullivan

U.S. DoD Procurement

0.0

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

140,000.0

Source: Frost & Sullivan

$ M

illi

on

Funding 103,001.0 101,679.0 110,557.0 114,770.0 117,704.0 123,782.0 125,386.0

2007 2008 2009 2010 2011 2012 2013

Supplemental Funding

0.0

50,000.0

100,000.0

150,000.0

200,000.0

Source: Frost & Sullivan

$ m

illio

ns

Funding 9,300.0 8,300.0 62,200.0 62,200.0 100,500.0 114,500.0 163,400.0 141,700.0

2001 2002 2003 2004 2005 2006 2007 2008

21www.frost.com

C4ISR – Funding and Programs

• Key platforms drive strong revenue growth

• Need for high-quality global bandwidth

• Greater use of unmanned aerial vehicles and more sophisticated ISR

platforms

• Greater use of SATCOM and automated systems creates need for a

larger infrastructure

• "Long War" will lead to sustained spending on C4ISR systems

• Solving technical interoperability requires high levels of investment in

RDT&E Spending and increased use of COTS

• Ground Forces share of funding will increase over the next five years

•Immature programs will be cut or shelved and remaining program

management will be consolidated until the ground forces (and Air Force

tanker and transport) resets are complete

•The MDA makes up a large portion of joint funding along with space

programs administered by the Air Force, EW to defeat IEDs, Special

Operations Forces equipment, medical equipment, and fuel

•Final result: stable defense budgets with more joint programs for basic

equipment and fewer prime contracts

•DoD now utilizes Indefinite Delivery/Indefinite Quantity contracts 42% of

the time, increasing flexibility and responsiveness

•The adoption of net-centric warfare doctrine enabled by IP and SDR

technologies is an opportunity for commercial companies to enter the U.S.

Aerospace & Defense market

Note: All figures are rounded; the base year is 2007. Source: Frost & Sullivan

Note: All figures are rounded; the base year is 2007. Source: Frost & Sullivan

$-

$2,000,000.00

$4,000,000.00

$6,000,000.00

$8,000,000.00

$10,000,000.00

$12,000,000.00

$14,000,000.00

$16,000,000.00

$18,000,000.00

$20,000,000.00

2005 2006 2007 2008 (Est.)

Total RDT&E

Total Procurement

Total C4ISR

$-

$2,000,000.00

$4,000,000.00

$6,000,000.00

$8,000,000.00

$10,000,000.00

$12,000,000.00

$14,000,000.00

$16,000,000.00

$18,000,000.00

$20,000,000.00

ARMY AF NAVY Joint Total

2005

2006

2007

2008 (Est.)

22www.frost.com

LCT & REGIONAL BUSINESS

0

500

1000

1500

2000

2500

3000

3500

4000

A320

Fam

ily

B737

B787

ERJ

B777

DH

C-8

A350

CR

J

A330

ATR

A380

Superje

t

B747

AR

J

A340

No

. o

f d

eli

veri

es (

2008-2

017)

•The A320 and B737 families are expected to dominate aircraft deliveries over the next 10 years, with both Airbus and Boeing shifting production/assembly lines to APAC countries

• New aircraft programmes will increasingly become more popular, with the B787 becoming one of the most successful programme launches

• The vast majority of twin aisle aircraft will be delivered to Asian airlines, whilst narrow body aircraft deliveries will be equallydistributed between Asia and North America. North America will remain the key demand origin for regional aircraft

0

200

400

600

800

1000

1200

1400

Gulfs

trea

m

Cita

tion X

/XLS

/Sov.

Cita

tion 1

/2/3

/4

Falco

n

Hawke

rC

hallenger

Learj

etP

rem

ier O

ne

TBM 8

50

PC

-12

No

. o

f d

eli

veri

es (

2008-2

017)

•Gulfstream, Citation and Falcon jets will be the most popular business jet aircraft over the next 10 years, whilst manufacturers are for the first time looking for partnerships in growth regions

• India will soon join the Global Aerospace Industry to produce its first regional and business aircraft, with support from Western manufacturers

• Due to North America’s position as the largest demand originator for business aviation aircraft, there are lesser number of manufacturing/assembly partnerships in growth regions

A320 and B737 present most opportunities in the long term, as both Airbus and Boeing establish their supplier list for the new generation platforms, due to enter production by 2013-2014

Aircraft supplier base in transition

23www.frost.com

EADS Socata to relocate

manufacturing/assembly to India

HAL to produce fuselage for over

200 G150 a/c

HAL to manufacture

doors for Airbus / Enter

a $1 billion agreement with Boeing

for future work

Tata Motors entering commercial aviation

manufacturing under JV with Boeing

ERJ145 Assembly in China, in a

Embraer/Harbin JV

Mitsubishi and

Kawasaki producing wings and

fuselage for B787

Airbus A320 Assembly line in

China to ship over 300 units in next

10 years

Chinese AVIC component

manufacturing for

B747/B787

APAC will become a major outsourcing region for components and systems manufacturing

4300

230

920

0

580240

Russia/CIS

3200

5800

4500

6900

1330490

0780

Africa &

Middle

EastAPAC

3620

1980

Europe

7940

11600

North

America

920990

Latin

America

LCT & Regional A/C deliveries

LCT & Regional A/C production

Business A/C deliveries

Business A/C production

Boeing will keep aircraft assembly in the USA, but target more partnerships

with APAC manufacturers for components and

systems

Airbus will shift an increasing number of

assembly lines to APAC, as well as target

partnerships in the region on component and system

level

Honda, Mitsubishi and KAI

investing in the regional market by introducing

own jets

Sukhoi will deliver over 240 units of the Superjet

Hawker Beechcraft opened a new

manufacturing facility in Mexico, whilst Bombardier is looking to shift

Learjet at its existing facilities there

Embraer will be looking to

outsource to lower-cost regions – with Mexico being an obvious target

IAI to grow in business aviation

manufacturing, after

partnership with Gulfstream

on G150

Hinduja the next possible major entry in the aviation market, after Tata Motors

1270920

Aircraft supplier base in transition

24www.frost.com

Aircraft supplier base in transition

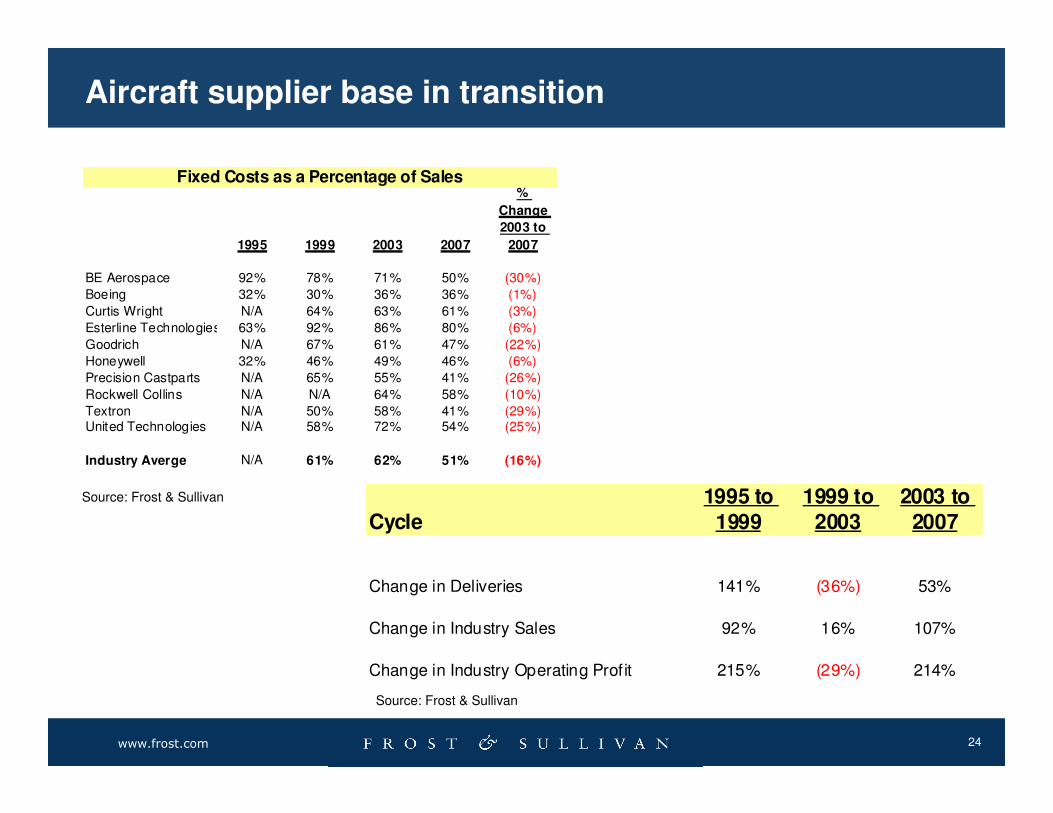

1995 1999 2003 2007

%

Change

2003 to

2007

BE Aerospace 92% 78% 71% 50% (30%)

Boeing 32% 30% 36% 36% (1%)

Curtis Wright N/A 64% 63% 61% (3%)

Esterline Technologies 63% 92% 86% 80% (6%)

Goodrich N/A 67% 61% 47% (22%)

Honeywell 32% 46% 49% 46% (6%)

Precision Castparts N/A 65% 55% 41% (26%)

Rockwell Collins N/A N/A 64% 58% (10%)

Textron N/A 50% 58% 41% (29%)United Technologies N/A 58% 72% 54% (25%)

Industry Averge N/A 61% 62% 51% (16%)

Fixed Costs as a Percentage of Sales

Cycle1995 to

19991999 to

20032003 to

2007

Change in Deliveries 141% (36%) 53%

Change in Industry Sales 92% 16% 107%

Change in Industry Operating Profit 215% (29%) 214%

Source: Frost & Sullivan

Source: Frost & Sullivan

25www.frost.com

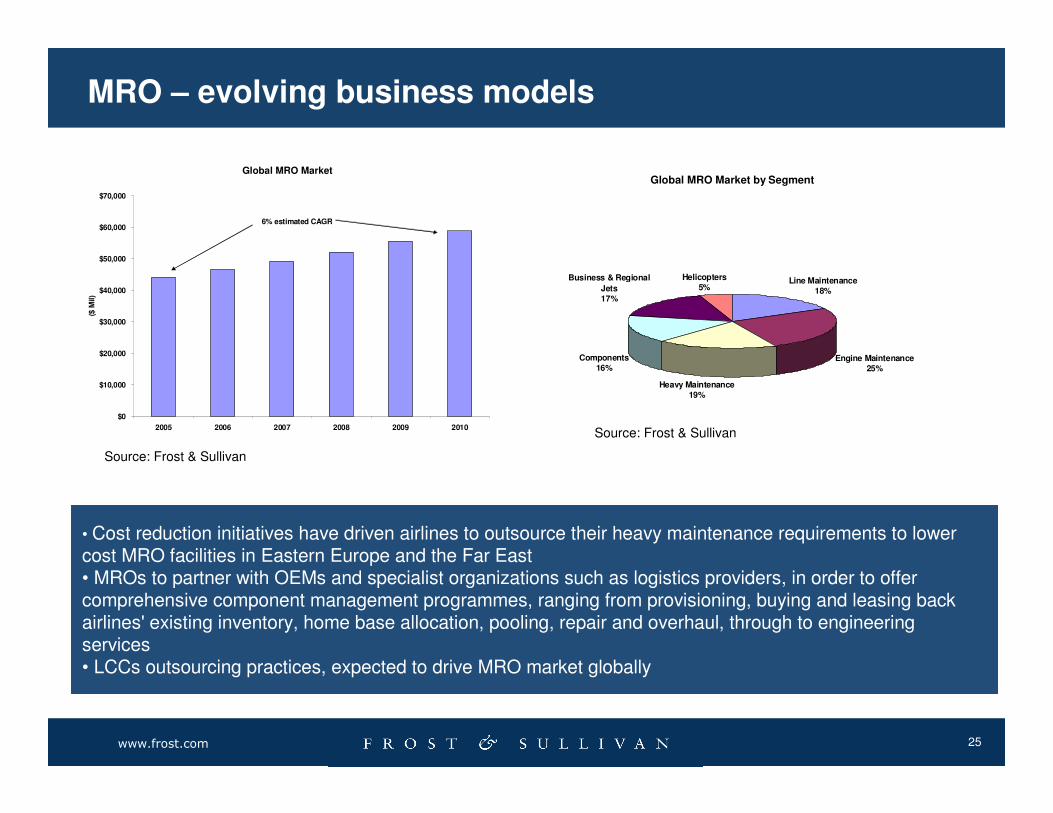

• Cost reduction initiatives have driven airlines to outsource their heavy maintenance requirements to lower cost MRO facilities in Eastern Europe and the Far East• MROs to partner with OEMs and specialist organizations such as logistics providers, in order to offer comprehensive component management programmes, ranging from provisioning, buying and leasing back airlines' existing inventory, home base allocation, pooling, repair and overhaul, through to engineering services• LCCs outsourcing practices, expected to drive MRO market globally

Global MRO Market

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

2005 2006 2007 2008 2009 2010

($ M

il)

6% estimated CAGR

Global MRO Market by Segment

Line Maintenance18%

Engine Maintenance25%

Heavy Maintenance19%

Components16%

Business & Regional

Jets17%

Helicopters5%

MRO – evolving business models

Source: Frost & Sullivan

Source: Frost & Sullivan

26www.frost.com

North America

• Remains the core market for all PMA suppliers, driven by straightforward approval procedures and clear cost reductions amongst airlines that have adopted PMA parts

• Market now represents approximately 55% of PMA suppliers’revenues, down from 90% in 1996

• American Airlines, Delta Air Lines, United Airlines and Air Canada represent largest PMA buyers

Africa

• Market not targeted by PMA suppliers, hence usage levels are marginal

• Bureaucracy, negative perception of PMAs and prevalence of lessors main barriers

Europe

• Second most important market for suppliers, approximately 30% of PMA revenues

• Lufthansa and Iberia remain pioneers in their level of acceptance of PMA parts

• Expected bilateral between FAA-EASA and EASA’s proactive involvement will further boost growth in the region

Asia Pacific

• Third biggest market for PMAs, with JAL, Cathay Pacific, China Airlines, Asiana are amongst the first to sign contracts with PMA suppliers

• Interest from many carriers and MRO organizations, particularly from China

• Main barriers to entry remain bureaucracy and relatively young fleets

Latin America

• Low usage / acceptance of PMA parts, due to bureaucracy and relative small size of airline-customers

• Varig is the only carrier with established PMA programme

Middle East

• Region new to PMA parts, with sporadic purchases

• Saudi Arabian Airlines, Gulf Air, GAMCO, Jordan Airmotive have shown interest

• Young fleets of region’s largest carriers and prevalence of lessors barriers to greater use

Source: Frost & Sullivan

PMA – Regional acceptance levels

27www.frost.com

What is the market telling us

YTD Stock Performance for leading Aerospace and Defense firms

(80%)

(60%)

(40%)

(20%)

0%

20%

40%

60%

AIR

BEAVTG

IDC

PSPRD

CO

GR

TXT

COL

PCP

TDG BAU

TXHO

NLL

LN

OC

CW CR

S&P 5

00ESLA

TK ITT

GD

RTNLM

TDO

VSA

ID

RS

28www.frost.com

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

29www.frost.com

For Additional Information

For additional information or to receive the audio file that

accompanies this analyst briefing please contact:

Stephanie Ochoa

Corporate Communications

North American

Analyst Briefing Coordinator

(210) 247-2421

Related Documents