TAYLOR COLLISON LTD. www.taylorcollison.com.au ABN 53008172450 AFSL 247083 1 CAMPBELL RAWSON [email protected] +61 415 146 725 www.taylorcollison.com.au Aerometrex Limited (AMX) Initiating Coverage - Outperform Our View AMX operates in an industry where having leading technology is crucial to success. In all operating areas, AMX is the leader or equal leader in aerial image capture and processing with regards to technological capability. Limited access to capital has meant this capability has to date, not led to the corresponding leadership in market share and revenue. Following an IPO 12-months ago, AMX has invested heavily in more technology, people and marketing with the effects only now beginning to flow through the P&L. FY21 will likely see minimal EBITDA growth due to continued investment however we forecast 76% growth for FY22 as recent initiatives take hold and believe FY22 will be a sustainable earnings baseline. Trading on 10.8x our FY22E EV/EBITDA forecast we expect to see multiple expansion as earnings traction increases through 2H21 and the market begins to price in FY22. Furthermore, we expect AMX to take market share in the subscription-revenue space from Nearmap which trades on an 47x FY22E EV/EBITDA multiple. We believe AMX’s 77% discount to Nearmap is too steep given the growth outlook and the industry leading nature of AMX’s assets. Long-Term Attractions • AMX has industry leading capture and processing technology across all divisions. The design of its own cameras and processing tools now allows AMX to maintain significant IP and produce higher quality imagery than competitors. This is highlighted in 3D where no competitor globally is producing imagery to the same detail (2cm resolution). • AMX has a first mover advantage in 3D modelling having begun 3D operations in 2012 and only in recent years has it become more widely utilised in many industries. This provides a significant competitive advantage with most competitors years behind in development. AMX has recently begun operations in the USA where we estimate the market to be worth ~$500m. • AMX has a difficult to replicate personnel base with most operational staff being experts in their field. Specialised operators are attracted to AMX based on the technological leadership prevalent in the business model. This has led to significant levels of expertise and we expect this experience to keep AMX at the forefront of industry innovation. • The Australian aerial photography and LiDAR market is worth $150m (excluding 3D). AMX has a realistic opportunity to capture 50% of this through increased awareness of its services, driven by leading technology. We see the following as the biggest risks to AMX’s future earnings • AMX is currently in a heavy investment phase with a focus on building out its MetroMap image base and growing 3D revenue in the USA. Despite superior technology and early signs of traction, there remains execution risk in the USA. Additionally, $5-$6m p.a. will be spent on image capture to build out the MetroMap platform and once again, despite strong growth rates to date, there is a risk subscription-based revenue may not grow to cover this cost as the near-monopoly incumbent, Nearmap (NEA), could alter pricing or strategy. • Whilst employee expertise is one of the biggest assets, it also provides key- man risk. We note this is particularly evident in 3D where the capture of images is fundamental to produce high quality models. Few in the market have this expertise. Many employees are subject to confidentiality agreements and all are well incentivised by salary and share options with 80% currently owning AMX shares. 26 November 2020 Recommendation: Outperform Summary (AUD) Market Capitalisation $112m Share price $1.19 52 week low $0.70 52 week high $2.60 Share price graph (AUD) Key Financials (AUD) FY20A FY21E FY22E Revenue 20.1 23.6 29.1 Trading EBITDA 4.6 4.8 8.4 EBITDA Margin 22.9% 20.2% 28.7% NPAT Adj. (0.3) 0.0 2.6 EPS Adj. (0.3) 0.0 2.7 PE Ratio NA NA 43.3 EV/EBITDA 19.5 19.3 10.8 EV/EBIT 794 NA 24.5 Dividend 0.0 0.0 0.0 Div yield 0% 0% 0%

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 1

CAMPBELL RAWSON

+61 415 146 725

www.taylorcollison.com.au

Aerometrex Limited (AMX)

Initiating Coverage - Outperform

Our View

AMX operates in an industry where having leading technology is crucial to

success. In all operating areas, AMX is the leader or equal leader in aerial image

capture and processing with regards to technological capability. Limited access to

capital has meant this capability has to date, not led to the corresponding

leadership in market share and revenue. Following an IPO 12-months ago, AMX

has invested heavily in more technology, people and marketing with the effects

only now beginning to flow through the P&L. FY21 will likely see minimal EBITDA

growth due to continued investment however we forecast 76% growth for FY22

as recent initiatives take hold and believe FY22 will be a sustainable earnings

baseline. Trading on 10.8x our FY22E EV/EBITDA forecast we expect to see

multiple expansion as earnings traction increases through 2H21 and the market

begins to price in FY22. Furthermore, we expect AMX to take market share in the

subscription-revenue space from Nearmap which trades on an 47x FY22E

EV/EBITDA multiple. We believe AMX’s 77% discount to Nearmap is too steep

given the growth outlook and the industry leading nature of AMX’s assets.

Long-Term Attractions

• AMX has industry leading capture and processing technology across all

divisions. The design of its own cameras and processing tools now allows

AMX to maintain significant IP and produce higher quality imagery than

competitors. This is highlighted in 3D where no competitor globally is

producing imagery to the same detail (2cm resolution).

• AMX has a first mover advantage in 3D modelling having begun 3D

operations in 2012 and only in recent years has it become more widely

utilised in many industries. This provides a significant competitive advantage

with most competitors years behind in development. AMX has recently begun

operations in the USA where we estimate the market to be worth ~$500m.

• AMX has a difficult to replicate personnel base with most operational staff

being experts in their field. Specialised operators are attracted to AMX based

on the technological leadership prevalent in the business model. This has led

to significant levels of expertise and we expect this experience to keep AMX

at the forefront of industry innovation.

• The Australian aerial photography and LiDAR market is worth $150m

(excluding 3D). AMX has a realistic opportunity to capture 50% of this through

increased awareness of its services, driven by leading technology.

We see the following as the biggest risks to AMX’s future earnings

• AMX is currently in a heavy investment phase with a focus on building out its

MetroMap image base and growing 3D revenue in the USA. Despite superior

technology and early signs of traction, there remains execution risk in the

USA. Additionally, $5-$6m p.a. will be spent on image capture to build out the

MetroMap platform and once again, despite strong growth rates to date, there

is a risk subscription-based revenue may not grow to cover this cost as the

near-monopoly incumbent, Nearmap (NEA), could alter pricing or strategy.

• Whilst employee expertise is one of the biggest assets, it also provides key-

man risk. We note this is particularly evident in 3D where the capture of

images is fundamental to produce high quality models. Few in the market

have this expertise. Many employees are subject to confidentiality

agreements and all are well incentivised by salary and share options with

80% currently owning AMX shares.

26 November 2020

Recommendation: Outperform

Summary (AUD)

Market Capitalisation $112m

Share price $1.19

52 week low $0.70

52 week high $2.60

Share price graph (AUD)

Key Financials (AUD)

FY20A FY21E FY22E

Revenue 20.1 23.6 29.1

Trading EBITDA 4.6 4.8 8.4

EBITDA Margin 22.9% 20.2% 28.7%

NPAT Adj. (0.3) 0.0 2.6

EPS Adj. (0.3) 0.0 2.7

PE Ratio NA NA 43.3

EV/EBITDA 19.5 19.3 10.8

EV/EBIT 794 NA 24.5

Dividend 0.0 0.0 0.0

Div yield 0% 0% 0%

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 2

Aerometrex Limited (AMX)

26 November 2020

Aerometrex Limited (AMX) - Summary of Forecasts AMX 1.19

PROFIT & LOSS SUMMARY (A$m) BALANCE SHEET SUMMARY

Year end June FY19A FY20A FY21E FY22E Year end June FY19A FY20A FY21E FY22E

Revenue 16.1 20.1 23.6 29.1 Cash 5.1 22.2 20.2 21.4

Statutory EBITDA 5.0 3.9 4.8 8.4 Receivables 2.8 2.5 3.1 3.8

Trading EBITDA 5.0 4.6 4.8 8.4 Inventories 0.0 0.0 0.0 0.0

Dep'n/Other Amort'n (2.0) (3.8) (4.8) (4.7) Other 1.4 1.0 1.0 1.0

EBIT 3.1 0.1 0.0 3.7 Total Current Assets 9.2 25.8 24.3 26.2

Net Interest (0.2) (0.2) 0.0 0.0 Deferred Tax Assets 0.3 1.4 1.4 1.4

Pre-Tax Profit 2.9 (0.1) 0.0 3.7 Goodwill 0.0 0.0 0.0 0.0

Tax Expense (0.3) (0.2) (0.0) (1.1) Property Plant & Equip 9.8 16.4 18.2 20.0

Tax rate -10% 232% 30% 30% Intangibles 3.1 6.6 7.9 9.6

NPAT Adj. 2.6 (0.3) 0.0 2.6 Other 0.0 0.0 0.0 0.0

Reported NPAT 2.6 (0.3) 0.0 2.6 Total Non-Current Assets 13.3 24.4 27.6 30.9

TOTAL ASSETS 22.5 50.1 51.9 57.1

Margins on Sales Revenue Accounts Payable 1.1 4.3 4.9 6.1

Operating EBITDA 31.3% 22.9% 20.2% 28.7% Contract liabilities 0.5 1.3 2.1 3.2

EBIT 19.0% 0.6% 0.0% 12.7% Current tax liabilities 0.3 0.0 0.0 0.0

NPAT Adj. 16.0% -1.3% 0.1% 8.9% Employee benefits 0.9 1.3 1.3 1.3

Borrowings 0.0 0.0 0.0 0.0

Change on pcp Other 8.5 1.2 1.2 1.2

Total Revenue 19.2% 20.3% 14.1% 18.9% Total Current Liab 11.3 8.0 9.5 11.8

Operating EBITDA 22.4% -8.7% 3.5% 75.9% Borrowings 0.0 0.0 0.0 0.0

Other financial liabilities 3.1 2.7 2.5 2.2

PER SHARE DATA Employee benefits 0.1 0.2 0.2 0.2

Year end June FY19A FY20A FY21E FY22E Deferred tax liabilities 1.1 1.6 1.6 1.6

EPS Adj. (c) 4.3 (0.3) 0.0 2.7 Total Non-Current Liab 4.3 4.5 4.2 4.0

Growth (pcp) 36.9% 107.7% -105.2% 15932.8% TOTAL LIABILITIES 15.6 12.5 13.7 15.7

Dividend (c) 0.0 0.0 0.0 0.0 TOTAL EQUITY 6.9 37.6 38.2 41.4

Franking 100% 100% 100% 100%

Gross CF per Share (c) 8.6 28.1 (2.1) 1.2 CASH FLOW SUMMARY

Year end June FY19A FY20A FY21E FY22E

KEY RATIOS EBIT (excl Abs/Extr) 3.1 0.1 0.0 3.7

Year end June FY19A FY20A FY21E FY22E Add: D&A 2.0 3.8 4.8 4.7

Net Debt/(Cash) : Equity (%) -73% -59% -53% -51% Change in Pay. 0.6 3.2 0.7 1.2

EBIT Interest cover (x) 16.0 0.3 0.0 18.5 Less: Tax paid (0.3) (0.2) (0.0) (1.1)

Current ratio (x) 0.8 3.2 2.6 2.2 Net Interest (0.2) (0.2) 0.0 0.0

ROE (%) 40.8% -1.2% 0.0% 6.5% Change in Rec. (0.1) (0.2) 0.6 0.7

Dividend Payout Ratio (%) 0.0% 0.0% 0.0% 0.0% Gross Cashflows 5.4 9.5 6.0 9.1

Capex (2.6) (5.3) (4.0) (4.0)

VALUATION MULTIPLES Free Cashflows 1.2 (0.1) (2.0) 1.1

Year end June FY19A FY20A FY21E FY22E Dividends Paid (0.7) 0.0 0.0 0.0

PER (x) 27.9 (361.0) 6,943.7 43.3 Contingent consideration paid (1.6) (4.3) (4.0) (4.0)

Dividend Yield (%) 0.0% 0.0% 0.0% 0.0% Net Cashflows 5.2 22.7 (2.0) 1.1

FCF Yield (%) 1.7% -0.1% -1.8% 1.0%

EV/EBITDA (x) 21.2 19.5 19.3 10.8

EV/EBIT (x) 35.0 794.3 127152.8 24.5

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 3

Aerometrex Limited (AMX)

26 November 2020

Aerometrex Limited

Aerometrex (AMX) is an established professional aerial mapping company with specialist expertise in aerial imaging,

photogrammetry, light detection and ranging surveys (LiDAR), 3D modelling and subscription services. Technology is at the core

of the business model with AMX’s innovation creating proprietary capabilities and driving market share growth. AMX is one of the

aerial surveying industry pioneers having been the first to adopt many new practices to provide higher quality imaging to

customers. This process has cultivated a significant competitive advantage in some of its markets as the investment required by

competitors will take many years to match AMX’s quality of product and service.

Company History

Aerometrex was founded in Queensland in 1980 and relocated to South Australia in 2000. From 2000 the business took on a

clearer growth path with technological advancement at the forefront.

At this time, now Chief Operating Officer, David Byrne, started with Aerometrex in the role of chief photogrammetrist and

production manager of the company’s mapping operations. Prior to being COO, David’s influence as Chief Technical Officer and

head of R&D saw his team develop several camera advancements and is a key reason AMX has a technology advantage in the

current market.

In 2011, AMX was purchased by management and was the catalyst for increased ownership by staff. Mark Deuter had been with

the company since 2005 in the role of General Manager and following the buyout was promoted to Managing Director/CEO, a role

which he still holds. Mark had overseen the introduction of digital aerial camera technology and established AMX’s aerial

operations whilst also implementing the strategic growth path. This included the release of AMX’s first 3D modelling service in

2012 which still remains without a viable competitor at the level of detail and quality provided by AMX. Mark’s background in

geography, computer science and 30+ years experience with ultra detailed surveys and airborne data processing remain an ideal

fit for the growth of AMX.

Revenue has been generated primarily in Australia but major projects have been completed in the USA, Europe, Africa, the Middle

East, SE Asia, PNG and New Zealand. Many of the overseas projects have been driven by AMX’s reputation and leading

technology. After developing the 3D modelling service in 2012, client software systems were slow to catch up to be able to

accurately present the imagery. With adequate software now prevalent, the technology has widespread acceptance in urban

planning, architecture, property development, real estate, engineering, construction, telecommunications and even computer

game developers. The market opportunity and growth in demand led AMX to set up a USA office in February 2020 with limited

fixed costs.

In 2015, AMX acquired aerial LiDAR surveying firm Atlass Australia and in the following two years invested in new sensors and

aircraft to support growth across all operating divisions. This acquisition and investment has seen LiDAR revenue grow from

$1.7m in FY17 to $8.9m in FY20.

Although project revenue continues to have a strong growth profile, recently, AMX has increased its focus on MetroMap. MetroMap

was established in 2018 and is AMX’s subscription-based imagery business and is growing AMX’s recurring revenue under a

Data as a Service (DaaS) model. This product requires upfront investment by AMX to capture imagery of much of Australia but

then provides multiple users with access to the information. Demand for this product is increasing and AMX expects to take

meaningful market share from the near-monopoly player, Nearmap.

AMX listed on the ASX on 10 December 2019 by raising $25m through the issue of 25m shares at $1.00. This was in addition to

existing shares of 60.2m and 9.2m convertible notes converted to shares through the offer. Following the listing, AMX was 58%

owned by management and employees who have a 12-month escrow period.

Following listing, AMX have established the USA office, won significant contracts in Australia and acquired customers and content

through the acquisition of competitor, Spookfish Australia.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 4

Aerometrex Limited (AMX)

26 November 2020

Business Overview & Analysis

AMX’s Market

The aerial surveying industry in Australia is an important contributor to the development of cities and society as well as the use of natural resources and management of the environment. Geospatial technology underpins many key institutions such as security of land tenure and local government asset management. It also provides the information needed to plan and cost major engineering and infrastructure projects. Aerial imagery, LiDAR and 3D modelling are data sources for planning and have become prevalent in industry, providing the base mapping data for many types of thematic information. The role of aerial survey information in Australia has progressed from wholly government-owned and managed operations, to private contractors vying for government contracts and private sector work, and now, to subscription-based models based entirely on private enterprise and offering pre-packaged datasets for broad consumption.

Revenue Streams

AMX revenue is generated in two distinct ways:

1. AMX operates a project aerial survey service model whereby aerial surveying is completed at the request of a client over a specific area. Historically this has been AMX’s core revenue stream and is the basis of its reputation.

2. AMX operates a Data as a Service (DaaS) model which leverages existing imagery and provides customers with access to a web-based application (MetroMap) under a subscription model. Whilst existing imagery is plentiful, to provide a comprehensive and up-to-date portfolio of imagery, this model requires AMX to fly aerial surveys for its own purposes and ownership as well as negotiating shared IP rights on data generated for project work.

The majority of revenue continues to be derived by project work however the subscription service is a significant focus for management as it increases recurring revenue and reduces operating earnings risk.

AMX operates four divisions:

1. Aerial Imagery/Photomapping – Project based

2. LiDAR – Light Detection and Ranging Surveys – Project based with potential for imagery to be subscription based

3. 3D modelling – Project based with potential for imagery to be subscription based

4. MetroMap – DaaS

Most recently, Covid-19 has delayed the decision-making process of some clients but it has also improved access to airspace allowing AMX to fly surveys for its own purpose. We expect longer term for the remote working thematic to increase demand for AMX’s services as companies don’t need people ‘on the ground’ as often.

0

1

2

3

4

5

6

7

8

9

10

Aerial Photomapping LiDAR 3D MetroMap

$ m

illio

ns

AMX Revenue

FY17 FY18 FY19 FY20

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 5

Aerometrex Limited (AMX)

26 November 2020

1. Aerial Imagery/Photomapping

Background

This area is AMX’s historic business which provides it with an archive of digital aerial imagery dating back to 2002 with access rights (through acquisition) to data sets back to 1943.

AMX generates revenue in this area through contracts with a broad range of customers across many industries, including:

• Government

• Mining

• Engineering/Infrastructure

• Internet – eg Google

• Environmental

• Urban planning

• Oil & Gas

Aerial image – 5cm resolution (Source: AMX FY20 result presentation)

These contracts are project based and AMX targets an operating margin of 30%. Imagery purposes include the likes of measurement of land/buildings, environmental monitoring and transport corridor analysis. Superior technology in the capture and processing of images is what drives the high standard of AMX’s capability and has enabled a wide range of industries to utilise aerial imagery.

After years of utilising only commercial technology, AMX’s tech team now design its own camera (MetroCam) used for aerial photography. The AMX built cameras produce an image resolution of 5cm pixels which we understand to be a level of detail that is equal to or better than the rest of the industry.

At a cost of <$1m each, the cameras are cheaper than commercial cameras ($1.5m) and are built in the USA. As the cameras are self-manufactured, four-year warranties are applied which removes the need for servicing contracts that are required with commercial cameras – this reduces the R&M expense. The cameras have a 5-7year useful life (balance of wear and technological change) and AMX currently have one of these cameras in use with another due to arrive in December.

Commercial cameras are still currently utilised with four of these in use for all aerial imagery with the exception of LiDAR which utilises different technology.

The technology focus continues after capture as refined computer algorithms help speed up processing and create increased storage capacity. Importantly, every pixel of each image is re-distorted to a “measurable accuracy”. This ensures the dimensions of the image are exact and can be utilised sufficiently. For example, engineering firms use the data to digitally measure structures or insurance companies use the imagery to determine the condition of a site prior to an event occurring.

Whilst AMX have a competitive advantage in image capture, the real focus and competitive advantage lies in the processing. AMX’s team are experts in the field and the R&D team continue to heavily invest in processing adaptations to improve the product/service provided. Over time, we expect camera technological advancements to become more difficult to obtain as useful resolution can only get so refined. In the long-term, competitors may catch up to AMX on the image capture front but we believe the processing, data set production and information gathering tools that AMX continues to develop will ensure a long-term competitive advantage.

Aerial Imagery Market

The aerial imagery market encompasses all capture and processing of images taken from the air by any mode. This includes planes, helicopters, drones and satellites. Research on the aerial imagery market is completed by various market research and advisory firms. Estimates vary as shown below.

Prescient and Strategic Intelligence $1.4bn 2016 13.4% 2017-2023

Fortune Business Insights $1.44bn 2017 14.2% 2018-2025 $4.1bn @ end 2025

Allied Market Research $1.25bn 2015 12.9% 2016-2022 $2.8bn @ 2022

Global Market Insights $1.7bn 2017 >12% 2018-2024 $4.0bn @ 2024

Future Estimated

Market Size and yearResearch Firm

CAGR

EstimateTime Period

Market Size Estimate

(USD)

Estimate

Date

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 6

Aerometrex Limited (AMX)

26 November 2020

Key Points from research reports:

- Asia-Pacific was estimated to make up >20% of the market.

- All of the advisory firms believe North America to have the largest share of the global market with 45-50%. They also expect the region to experience the fastest growth rate over the estimated time frames.

- Urban planning expected to be the greatest driver of growth with estimates of >16%. Military and defence is a close second with CAGR estimates of 15%+, particularly in the USA.

AMX believes that these factors will continue to drive growth in aerial imaging, particularly within Australia:

• Technology improvements – sensor technology improvements such as the very large-format digital cameras and high-sampling LiDAR sensors are continually evolving and appearing in the markets. These drive improved quality images and provides greater scope for end use practices.

• Improvements in analytical and artificial intelligence-based information extraction – this has been evident in recent years, resulting in easier extraction of value-added information from aerial imagery and LiDAR data sets. The ability to provide industry-specific information to customers will serve to broaden the demand for these products.

• Emergence of 3D mapping – a strong trend towards 3D mapping, which is expected to become the standard base map product of the future as the industry evolves and technology improves.

• Urbanisation and planning – aerial imagery and LiDAR data products have become important tools for engineers and planners. As metropolitan areas continue to expand and densify, the importance of high-resolution data to document, manage and provide services to facilitate growth are essential.

• Environmental management – with an increasingly environmental-conscious society, environmental management of forests, reefs, wetlands, coasts and parks is creating further demand for aerial imagery.

Our View – Aerial Imagery

Within Australia, AMX splits the addressable aerial imagery market in two:

1. Project revenue - $15-$20m

2. Subscription revenue - $80m

Although aerial imagery is the terminology for the capture of all images utilised by AMX. In this instance revenue for the aerial imagery division is focused solely on the project revenues. Project revenue will always exist as certain geographies or clients will require imagery to be fully private. For example, images of defence force land or land on a prospective mining site. Much of this business is repeat and meaningful portions are deemed annuity-style but we do not expect meaningful long-term growth in project revenue as many customers are transitioning to the subscription model.

We have forecast small declines in revenue for this division over the next two years as customers are transitioned to the subscription model. We highlight this is a shift of revenue to another division, not a reflection of lost business. Despite not expecting significant market growth, we do anticipate AMX to maintain 30%+ market share of this space in the long-term. We note visibility is ~4-6 months in project revenues.

We outline our view on the subscription-based market under our MetroMap analysis further below. Source: AMX FY20 presentation

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 7

Aerometrex Limited (AMX)

26 November 2020

2. LiDAR – Light Detection and Ranging

Background

In 2015, AMX acquired aerial LiDAR capability through the purchase of LiDAR surveying firm Atlass Australia. Since then AMX has greatly diversified the business as it was historically almost exclusively working in the coal mining industry. It is currently servicing many industries including agriculture, environment, forestry, infrastructure/engineering, transport, mining, surveying and mapping, urban planning, renewable energy, and water resources.

LiDAR image (Source: AMX FY20 result presentation)

Key points on LiDAR technology:

• LiDAR is an advanced aerial surveying technique which utilises active laser pulses generated by the sensor to measure the distance of aircraft to ground. The absolute position of the aircraft is determined by sophisticated airborne GPS and inertial measurement systems, so the subtraction of the distance to ground from the aircraft height gives the height of the terrain.

• The sensors can sample up to a million light pulses per second, and create a very detailed, high-sampled model of the terrain surface in XY and Z coordinates. This creates a sample of anywhere from 8-60 different points within each square metre.

• LiDAR can be used for a wide variety of applications including creation of Digital Terrain Models (DTMs) and Digital Surface Models (DSMs), measurement of mining stockpile volumes, sampling of tree heights, measurement of buildings in urban areas, monitoring major construction and infrastructure projects involving mass movements of overburden, and other applications.

• The laser pulses are of sufficient number and strength to penetrate to the ground through moderate to dense canopy vegetation, allowing the terrain level or features to be mapped even under forests and woodland canopies. This is particularly helpful in such disciplines as archaeology and forestry.

Similar to aerial imagery, AMX conducts LiDAR projects with a goal of achieving a 30%+ operating margin.

Projects undertaken to date have been mapping projects commissioned both by governments at various levels and major private companies. Elevation and topographic products derived from aerial LiDAR surveys have been utilised by industries including agriculture, infrastructure, engineering, transport, forestry, mining, renewable energy and water resources. Further applications can be found in bushfire prediction and analysis, climate change management and coastal erosion.

LiDAR is a rapid growth area for AMX and investments over the last few years include the purchase of four state-of-the-art LiDAR sensors at a cost of approximately $1 million each. The return on investments in LiDAR can be seen with revenue up from $1.7m in FY17 to $8.9m in FY20.

Most recently, AMX’s R&D team have developed a new pre-emptive firefighting tool as an advancement of uses for the existing LiDAR technology. The product analyses LiDAR images of bushfire prone areas and provides a full depth, 3D view of fuel loads. The penetrating power of LiDAR technology delivers a far more accurate image of vegetation and is more sensitive to vegetation structure and density than other satellite or radar technology. This tool is the first of its kind and was developed in conjunction with government and is available for emergency authorities for this bushfire season in order to minimise the risk of catastrophic fires.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 8

Aerometrex Limited (AMX)

26 November 2020

Our View – LiDAR

AMX believe the LiDAR market in Australia is worth $50-$60m and is growing at 10%+ as the technology uses become more widespread.

We understand the incumbent in this market, AAM Group, to have 60-70% market share. With a revenue CAGR of 51% over the last three years, AMX’s investment in new technology and planes is ensuring market share is being taken. We understand the incumbent may be falling behind on technology investments and therefore impacting customer relationships. As such, we believe a long-term market share of 50% for AMX is a realistic proposition (currently ~20%).

Similar to aerial imagery, LiDAR image capture technology can be purchased by any company however the investment in application development to better use the data is what continues to drive AMX’s growth and customer adoption of the technology.

AMX are in the early phases of converting LiDAR derived data products to the subscription model under the MetroMap platform, therefore increasing the operating margin and breadth of customer. We expect to see continued strong growth from the LiDAR division through FY21 and FY22 as the market awareness of the data applications continues to grow, the focus on our environment increases for various levels of government and as AMX takes market share.

3. 3D Modelling

Background

AMX has developed its own 3D modelling service, which is a revolutionary implementation of the “massive multi-ray matching” photogrammetric method. It offers 3D models of the highest resolution (2cm pixel) and absolute accuracy (5cm in XY & Z) derived from aerial platforms and has attracted worldwide attention via AMX’s YouTube channel and social media.

AMX also offers a lower-resolution 3D product for larger areas, at 7.5cm pixel size. This product is offered for sale for metropolitan and suburban areas through its MetroMap platform. This 3D product resolution is superior to other offerings in the Australian market, which are generally at 15cm or even 50cm resolution. The worldwide attention has led to increased revenue and we anticipate growth to continue as a result of the reputation and market leading capability.

3D data can be viewed in many viewing systems, ranging from projection onto flat computer screens in a web browser interface, to 3D TVs, holographic technology or fully immersive Virtual Reality (VR) systems. AMX caters for most known data formats, software systems and hardware viewing systems in delivering its 3D data products.

Despite having the technology since 2012, 3D modelling for high-value capital projects as well as high-value investment centres (such as capital city CBDs) has only become mainstream in the last few years, thanks in part to the improved nature of software to view the product.

The process of obtaining the images is slightly different to aerial imagery and LiDAR due to helicopters being used to make navigation easier around city scapes. The camera costs are significantly lower at ~$100k and are much smaller in size and therefore easier to transport from project to project.

Whilst a lower setup cost compared with other aerial imagery is less of a barrier to entry, AMX believe the skill set required to accurately capture images is difficult to master and their staff are industry leading in this regard.

3D Modelling Market

The market for 3D modelled data has gradually expanded to include urban planning, architecture, property development, real estate, heritage documentation, engineering and construction and telecommunications (wireless and 5G network analysis). In addition to the geospatial user market there has been strong interest from industries as diverse as computer games, movie production, cemeteries, event management and advertising agencies.

As with other forms of geospatial data, the global market for 3D imagery is seen to be rapidly growing. As a relatively new technology, market data is difficult to come by. Having been a 3D pioneer by starting in 2012, AMX has created a substantial lead on the rest of the market with how the imagery is processed and applied. Management believe it will be very difficult for competitors to catch up over the next decade given the significant protected IP built up already.

AMX sees 3D modelled data as the future of mapping and believes that it will eventually replace 2D mapping as the default mapping system for all applications. There is a very high potential for expansion of the 3D modelling service in the large US market, and for generating 3D model subscription services for capital cities. Similarly, strong growth for 3D modelling services is expected in Europe over the next five years. AMX have setup a small office in Denver, Colorado to grow its US business and can service the West Coast and Midwest from this location. As Denver is the North American “hub” for geospatial science, AMX are well placed to attract the best talent.

We estimate both the USA and European markets to be currently worth ~$500m each. Within Australia we estimate the market to be worth ~$80-$100m on the assumption that 2D mapping is gradually being replaced by 3D.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 9

Aerometrex Limited (AMX)

26 November 2020

Our View – 3D Modelling

Australia was a somewhat early adopter of the 3D modelling technology and as such competition is greater here than overseas. Despite this, AMX has global industry leading technology and capability in this area with no competitor generating the same accuracy or resolution of image. AMX believes that accurate imagery is vital to derive accurate 3D models and that expertise in image capture is difficult to replace in the current 3D market. We understand employees in AMX’s USA operation in particular are experts in this space and despite being well incentivised, we note this creates a level of “key-man risk”.

From projects completed to date and the current demand pipeline, we believe the opportunity is global and expect growth to be focused on the USA as this market is playing catch up to Australia and therefore provides AMX with an opportunity to obtain significant market share. Notably, 3D is less capital intensive than other aerial imagery and we estimate operating margin for 3D projects to be 40%+. There is scope for further margin improvement should AMX transfer more 3D imagery to its MetroMap platform.

We believe the execution and “key-man” risk is far outweighed by the opportunity that exists in the USA and we see a pathway where 3D modelling becomes the core part of AMX’s business over the next decade. Sales processes remain in the early stages and we anticipate the investment phase to continue through 1H22 followed by profitability (in the USA) from early CY22. In the interim, we expect 3D earnings growth to continue in Australia as 2D imagery transitions and the application of data sets through AMX’s technology expands further.

4. MetroMap

Background

Established in 2018, MetroMap is an online imagery web-serving application, offering AMX’s imagery to a subscriber base. MetroMap is the high growth area of the business which benefits from the experience and history of AMX’s aerial imagery prowess.

MetroMap offers its subscribers four captures per annum for each major capital city, in addition to rural and regional city captures once p.a. This capture ensures up-to-date images and is at AMX’s own cost of $5-$6m p.a. irrespective of the number of subscribers. The capture is completed primarily by its own proprietary technology, MetroCam, as well as commercial cameras when required.

The platform is designed to allow subscribers to utilise imagery in any captured area of Australia in any way they like. This allows AMX to offer the same captured image to multiple customers for varied use to generate greater revenue per image. This provides customers with a better value proposition as they can access new imagery without additional project costs each time.

A by-product of aerial imagery terrain corrections, Digital Surface Models (DSM’s), are a depiction of the terrain surface including buildings, vegetation and surface features. These products are for applications involving line-of-sight calculation, such as telecommunications and security. MetroMap offers high-quality, accurate DSMs as part of its suite of geospatial data types.

In addition to standard natural colour imagery, MetroMap offers near-infra-red (nIR) imagery coverages for several cities. nIR imagery is useful for all applications involving vegetation vigour as the nIR spectral band is sensitive to plant chlorophyll. These applications include management of parks and gardens, irrigation systems, agriculture and horticulture, as well as bushfire burn severity.

The MetroMap web browser interface incorporates 3D viewing capability as well as 2D imagery capability.

Acquisition

In May 2020, AMX acquired the Australian arm of global company, Spookfish (owned by EagleView Technologies). The acquisition was of aerial imagery contracts and provides AMX with 250 additional clients, an extensive historic image library and ~$1m in recurring revenue. The cost of acquisition was $750k upfront with an additional $750k to be paid upon a certain number of customers renewing their contracts in 2021. The instant client capture for MetroMap will pay for itself after one year assuming all the clients renew.

Our View – MetroMap

AMX has recently captured 75% of the Australian population in three months. Every capital city and 49 regional cities and towns provides customers with the most up-to-date imagery at a 5cm pixel size – more detailed than any competitor. AMX have also secured Suncorp, PSMA Australia and numerous other engineering firms, architects, urban planners and surveying firms as customers for MetroMap in 1Q21. The total contracts are worth $1.0m for FY21 and highlight the traction the service is gaining.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 10

Aerometrex Limited (AMX)

26 November 2020

Outlined below is the run rate of annual MetroMap subscriptions. We note some of the growth can be attributed to the acquisition of Spookfish and the transition of existing aerial imagery project customers. However, the majority of growth is organic and underpinned by new corporate customers. We expect this growth to continue with the market now recognising the quality of product and we anticipate MetroMap being profitable on an operating level from FY22.

AMX believe the subscription-based market to be worth ~$80m currently and growing at global industry rates (10-15% p.a.). The end game for this market in Australia is dependent on the ability for AMX and competitors to add various 3D and LiDAR products to the platform. We estimate long-term this market could reach $200-$250m p.a.

Irrespective of size, a duopoly is likely with Nearmap the key competitor in this space. Given customer traction growth and AMX’s capture and processing technological advantage, we expect market share gains to continue. Undoubtedly we expect Nearmap to defend its position in the market however we see 40%+ share for AMX to be plausible longer-term.

Crucially, recurring subscription revenue reduces operating risk and removes a heavy reliance on project revenues. On current growth rates we anticipate MetroMap revenue of ~$30m in five years.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 11

Aerometrex Limited (AMX)

26 November 2020

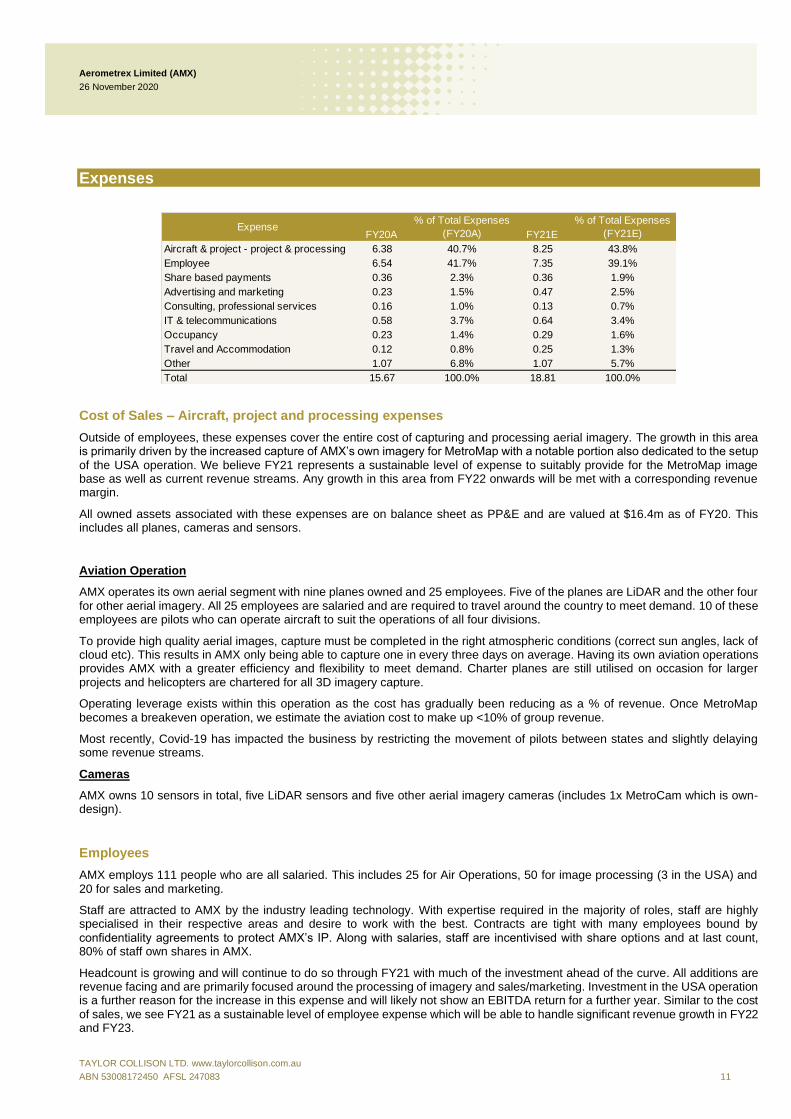

Expenses

Cost of Sales – Aircraft, project and processing expenses

Outside of employees, these expenses cover the entire cost of capturing and processing aerial imagery. The growth in this area is primarily driven by the increased capture of AMX’s own imagery for MetroMap with a notable portion also dedicated to the setup of the USA operation. We believe FY21 represents a sustainable level of expense to suitably provide for the MetroMap image base as well as current revenue streams. Any growth in this area from FY22 onwards will be met with a corresponding revenue margin.

All owned assets associated with these expenses are on balance sheet as PP&E and are valued at $16.4m as of FY20. This includes all planes, cameras and sensors.

Aviation Operation

AMX operates its own aerial segment with nine planes owned and 25 employees. Five of the planes are LiDAR and the other four for other aerial imagery. All 25 employees are salaried and are required to travel around the country to meet demand. 10 of these employees are pilots who can operate aircraft to suit the operations of all four divisions.

To provide high quality aerial images, capture must be completed in the right atmospheric conditions (correct sun angles, lack of cloud etc). This results in AMX only being able to capture one in every three days on average. Having its own aviation operations provides AMX with a greater efficiency and flexibility to meet demand. Charter planes are still utilised on occasion for larger projects and helicopters are chartered for all 3D imagery capture.

Operating leverage exists within this operation as the cost has gradually been reducing as a % of revenue. Once MetroMap becomes a breakeven operation, we estimate the aviation cost to make up <10% of group revenue.

Most recently, Covid-19 has impacted the business by restricting the movement of pilots between states and slightly delaying some revenue streams.

Cameras

AMX owns 10 sensors in total, five LiDAR sensors and five other aerial imagery cameras (includes 1x MetroCam which is own-design).

Employees

AMX employs 111 people who are all salaried. This includes 25 for Air Operations, 50 for image processing (3 in the USA) and 20 for sales and marketing.

Staff are attracted to AMX by the industry leading technology. With expertise required in the majority of roles, staff are highly specialised in their respective areas and desire to work with the best. Contracts are tight with many employees bound by confidentiality agreements to protect AMX’s IP. Along with salaries, staff are incentivised with share options and at last count, 80% of staff own shares in AMX.

Headcount is growing and will continue to do so through FY21 with much of the investment ahead of the curve. All additions are revenue facing and are primarily focused around the processing of imagery and sales/marketing. Investment in the USA operation is a further reason for the increase in this expense and will likely not show an EBITDA return for a further year. Similar to the cost of sales, we see FY21 as a sustainable level of employee expense which will be able to handle significant revenue growth in FY22 and FY23.

FY20A FY21E

Aircraft & project - project & processing 6.38 40.7% 8.25 43.8%

Employee 6.54 41.7% 7.35 39.1%

Share based payments 0.36 2.3% 0.36 1.9%

Advertising and marketing 0.23 1.5% 0.47 2.5%

Consulting, professional services 0.16 1.0% 0.13 0.7%

IT & telecommunications 0.58 3.7% 0.64 3.4%

Occupancy 0.23 1.4% 0.29 1.6%

Travel and Accommodation 0.12 0.8% 0.25 1.3%

Other 1.07 6.8% 1.07 5.7%

Total 15.67 100.0% 18.81 100.0%

Expense% of Total Expenses

(FY20A)

% of Total Expenses

(FY21E)

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 12

Aerometrex Limited (AMX)

26 November 2020

Sales and Marketing

A significant step up in advertising is occurring to build awareness of AMX’s services, capability and the MetroMap platform. Prior to listing, capital constraints restricted AMX from investing heavily in this area and investment is now increasing rapidly to help revenue catch up with market position. We expect this expense to grow proportionate to revenue over the next two years.

R&D

AMX invest heavily in R&D as technology is what delivers much of its competitive advantage and industry leadership. Most of the R&D is focused on image processing tools and providing data sets from images. A prime example is the recent LiDAR tool developed by the AMX team to help identify heavy fuel loads in vegetation to try and prevent catastrophic bushfires. This was an industry first and was developed in conjunction with government. The majority of R&D is expensed and most of this is captured in employee cost as it is labour intensive.

Competition & Competing Technologies

Aerial imagery and mapping

Project aerial surveys is a competitive landscape in Australia, in which much work is tendered by government agencies or large corporations and strong value-for-money cases must be made to win work. AMX’s policy is to pursue quality, accuracy, resolution and service as key company objectives. This has seen AMX continue to build market share. AMX meets the standard accuracy specifications for aerial imagery on government-related work and for engineering projects. AMX’s analysis of the market suggests many competitors do not meet the required standards which, along with its own quality delivery, underpins AMX’s market share.

LiDAR

In recent times, AMX has seen a contraction of survey providers in the LiDAR market, with a down-grading of some competitors’ capacities. We assume as AMX are taking share in this space that the incumbent, AAM Group, may be one of those competitors. LiDAR technology is rapidly advancing and investment in the latest sensor technology has placed AMX in a strong position in this market.

3D Modelling

AMX has no known competitor providing 2cm 3D models from unrestricted aerial platforms. This is a niche speciality that AMX has made its own by continuing to innovate and refine its methodologies and applications. AMX’s large metropolitan 3D coverages at 7.5cm pixel size and 5cm pixel size are also class-leading for this data type.

MetroMap

The subscription market for aerial imagery services is more fragmented, enabling strong sales performance outside regulated Government procurement channels to drive rapid growth. The rise of MetroMap has created an effective competitor to the existing near-monopoly (held by Nearmap) in this market and we expect AMX to continue growing corporate customers to the point where a fairly even duopoly exists.

Competing Technologies

Drones With the benefit of considerable experience using both drones and conventional aircraft, AMX does not believe that drone imagery is the aerial imagery technology of the future. A drone is simply a platform for a sensor and must be compared against larger scale solutions to form a view on cost-effectiveness. There has been rapid growth in the number, sophistication and type of drones available in the market, but there are serious scale limitations with the technology and drone operations are tightly regulated. There are specific instances in which a drone platform may be cheaper, i.e. for very small areas which require very frequent capture updates. However, the decision of which technology to use should always be based on product quality, accuracy, safety and cost-effectiveness. Satellite Satellite imagery is useful for continental-scale imagery captures at relatively very low resolution. The highest resolution imagery captured by satellites is in the order of 30cm pixel size, which is the coarsest resolution captured by aerial imagery platforms. There is an increasing demand for image resolution in the 2cm to 20cm range and the physical limitations of satellites do not allow imaging at these resolutions.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 13

Aerometrex Limited (AMX)

26 November 2020

AMX Competitive Advantage

AMX believes its competitive advantage lies in the quality of product/service delivered which is an outcome of best practice at every step. This includes leveraging the best available commercial equipment as well as own development and using the technology in the right way to obtain higher quality data.

AMX utilises the highest level of available technology for image capture and whilst this is an advantage over some competitors, the real advantage lies in the extraction of information from the imagery.

The ability to extract industry-specific information from aerial imagery is a rapidly developing area and substantial research is being conducted world-wide to use artificial intelligence (AI) methods to supplement existing extraction methods (classification, digitising, modelling). AMX is already using these systems internally with the use of commercially available AI software, but is also in discussions with key specialist providers in this area. Spatial accuracy of input data is critical to the usefulness of derived data products and this is a key distinction for the development of AMX products.

Furthermore, AMX has first mover advantage in the 3D space having begun operating in 2012. With the most refined technology globally, resulting in the highest resolution available, and with long R&D times, competitors will struggle to keep up as AMX continues to invest and attracts customers in a rapidly growing market.

Finally, a long operating history with a highly experienced workforce is a key strength. Senior executives and Board members are qualified in specialist areas such as photogrammetry, mapping/GIS, aviation, 3D modelling and LiDAR. AMX’s people are a very strong asset and the assemblage of skills and experience would be very difficult to replicate by new entrants to the market.

Growth Strategy

AMX’s strategy is to continue to grow both the imagery/geospatial data subscription services (MetroMap) and aerial survey project services with a focus on 3D modelling and LiDAR. The increase in available capital from the IPO will help fund increased investment in marketing and sales which we expect to translate to increased revenue and a wider customer base.

MetroMap

With a significant portion of Australia now captured by AMX, the platform is set to increase annuity revenue by attracting new customers. A wide range of data types can be sold through MetroMap and aerial imagery is an ideal base to derive value-added information products using AI and other classification and interpretation tools. Wherever possible, AMX intends that IP rights on imagery and 3D models collected for project requirements will be retained so those products can be used within MetroMap. This strategy allows the lowest cost base for MetroMap collections and enables multiple sales of the same data.

LiDAR

Investment in the latest technology has driven a 51% CAGR over the last three years and this growth is expected to continue strongly. This will be driven by geographic expansion within Australia as well as capturing more market share and the development of value-added products from LiDAR data (such as the recent bushfire technology). AMX intends to continue to invest strongly in its LiDAR business by increased sales and marketing efforts, by obtaining more resources, such as aircraft and sensors, and by building LiDAR data and products into its subscription model where there are strong resale opportunities.

3D

AMX believes that its 3D modelling service will have strong growth potential in Australia as well as internationally. As described further above, with global industry leading technology, AMX is poised to grow quickly in the vast USA market as competitors with inferior technology are likely to find it difficult to compete. AMX’s strategy is to build relationships with large companies and local/state governments to build a core earnings base with recurring revenue potential.

AMX has multiple sales strategies for tackling the United States market, involving direct project sales as well as developing sales channel partner relationships and subscription models. In Europe, success from major project tenders in France and Germany have delivered notable recognition in the market and this service can be scaled up to meet international demand relatively easily.

Acquisition Opportunities

The recent acquisition of Spookfish’s Australian operations is a prime example of AMX’s target. The purchase provided AMX with

a number of new clients through customer contracts and rights to an image library. This provided AMX with quick scale to help

absorb the setup costs of MetroMap whilst also taking out a competitor. Furthermore, the seller (EagleView technologies) is a

competitor in other sectors but has provided AMX with a potential global relationship to further growth of other technologies.

With industry leading technology, a network of capture infrastructure and extensive personnel expertise and experience, it is

unlikely AMX will look to purchase a competitor’s entire business. With its own R&D team delivering much of the industries new

technology, we see it likely that any acquisition would be focused around customer acquisition only.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 14

Aerometrex Limited (AMX)

26 November 2020

Peer Group Analysis & Valuation

Comparisons are difficult to make as a number of AMX’s competitors/peers are either large US/European businesses that are now divisions of global information behemoths or; too small to be listed; or privately owned. Internationally some of the closest peers include:

• Blom ASA

• EagleView Technologies

• Kucera International

• Quantum Spatial

As AMX’s international focus is currently on 3D, the companies above are peers in aerial imagery, LiDAR and/or subscription based services that operate in the USA and Europe.

In order to make financial comparisons, we have included information below on two international listed companies:

1. Fugro NV – a Dutch listed aerial imaging business with operations throughout Europe. 2. TGS Nopec Geophysical Company – a global 2D and 3D imaging and data analytics business focused entirely on

subsurface information for the global energy industry.

We note the TGS share price has halved this year as exposure to less O&G exploration has impacted on sentiment. We also note that although EV/EBITDA multiples provide the fairest comparison, these businesses all operate with a significant library of IP and the resultant amortisation varies drastically between companies. For example on a PE basis, TGS trades at a premium to AMX compared with a discount on an EV/EBITDA basis. We further note that as Australia is a global leading player in this area, the market is likely to place higher value on local stocks given the industry leading technology that exists here vs. overseas.

The clearest comparison is made with direct competitor, Nearmap. Nearmap is the only Australian competitor/peer that is listed and currently holds the near-monopoly position of the subscription-based market in Australia. We believe this market position is a key driver of the extreme valuation and anticipate the valuation multiple to decline as AMX takes market share with its MetroMap platform.

AMX is currently still investing to prepare for future revenue streams and therefore we believe FY21 is not a fair comparison with the established Nearmap operations. We believe FY22 (FY+2) EBITDA is more representative of AMX’s business and note that we expect a longer-term EBITDA margin of 30%.

Given Nearmap’s size, market position in Australia and growth overseas, a trading discount for AMX is appropriate however we believe the discount is too great and does not reflect the industry leading technology and growth options at AMX’s disposal. We understand it is still early in AMX’s foray into the USA and subscription-based revenue streams but think a discount in the region of 30-40% is more appropriate at this juncture.

We expect the valuation gap to close in part by Nearmaps valuation compressing as AMX takes market share. Therefore, below we have applied various discounts to Nearmaps current valuation to provide an appropriate base for comparison.

Mkt Cap

AUD

TGS TGS.OSE Norway $2.09bn 76.2% 4.2 80.1% 4.0

Fugro NV FUR.AMS Holland $677m 9.4% 7.3 11.0% 6.1

Nearmap NEA.ASX Australia $1.18bn 12.8% 73.3 16.3% 47.1

Aerometrex AMX.ASX Australia $112m 20.2% 19.2 28.7% 10.6

Median 16.5% 13.3 22.5% 8.4

AMX Discount to NearMap -74% -77%

Source: Factset Estimates November '20

FY+2 Consensus

Estimates

Providers of Imagery/Analytics

EBITDA

margin

EBITDA

margin

EV/EBITDA

(x)

EV/EBITDA

(x) Stock Code LocationCompany

FY+1 Consensus

Estimates

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 15

Aerometrex Limited (AMX)

26 November 2020

If we assume a 20% pullback in NEA’s FY22 valuation and apply a 40% discount from there for AMX, we come to a multiple of 22.6x EV/EBITDA, which as seen on our valuation matrix below, is implying a share price of ~$2.20. We feel over the next six months this would be a more representative view of the growth options and market dynamic between AMX and Nearmap.

With investment in image capture, equipment and headcount to continue in FY21 and a diluted underlying earnings trend, we expect the share price to climb during 2H21 as earnings traction from MetroMap continues and the market begins to price in FY22 earnings.

Valuation Matrix

Above we provide the implied share prices at various EV/EBITDA multiples and varying levels of EBITDA. For each multiple and EBITDA combination we use our FY22E cash and debt levels. The current share price, our current trading EBITDA forecast and the implied multiple are in bold.

Nearmap (NEA) 47.1 5% 44.7 30% 31.3 40% 26.8

10% 42.4 30% 29.7 40% 25.4

15% 40.0 30% 28.0 40% 24.0

20% 37.7 30% 26.4 40% 22.6

25% 35.3 30% 24.7 40% 21.2

30% 33.0 30% 23.1 40% 19.8

AMX

Discount

AMX Implied

Fair FY22

Multiple

Implied NEA

multiple

AMX

Discount

AMX Implied

Fair FY22

Multiple

Company

FY22

EV/EBITDA

multiple (x)

Multiple discount to

reflect expected

market share losses

8 10 10.8 12 14 16 18 20 22 24 26 28 30

4 $0.57 $0.65 $0.69 $0.74 $0.82 $0.91 $0.99 $1.08 $1.16 $1.25 $1.33 $1.42 $1.50

5 $0.65 $0.76 $0.80 $0.87 $0.97 $1.08 $1.18 $1.29 $1.39 $1.50 $1.61 $1.71 $1.82

6 $0.74 $0.87 $0.92 $0.99 $1.12 $1.25 $1.37 $1.50 $1.63 $1.75 $1.88 $2.01 $2.14

7 $0.82 $0.97 $1.03 $1.12 $1.27 $1.42 $1.56 $1.71 $1.86 $2.01 $2.16 $2.31 $2.45

8 $0.91 $1.08 $1.14 $1.25 $1.42 $1.59 $1.75 $1.92 $2.09 $2.26 $2.43 $2.60 $2.77

8.4 $0.94 $1.12 $1.19 $1.29 $1.47 $1.65 $1.82 $2.00 $2.18 $2.36 $2.53 $2.71 $2.89

9 $0.99 $1.18 $1.26 $1.37 $1.56 $1.75 $1.95 $2.14 $2.33 $2.52 $2.71 $2.90 $3.09

10 $1.08 $1.29 $1.37 $1.50 $1.71 $1.92 $2.14 $2.35 $2.56 $2.77 $2.98 $3.20 $3.41

11 $1.16 $1.39 $1.49 $1.63 $1.86 $2.09 $2.33 $2.56 $2.79 $3.03 $3.26 $3.49 $3.73

12 $1.25 $1.50 $1.60 $1.75 $2.01 $2.26 $2.52 $2.77 $3.03 $3.28 $3.53 $3.79 $4.04

13 $1.33 $1.61 $1.72 $1.88 $2.16 $2.43 $2.71 $2.98 $3.26 $3.53 $3.81 $4.09 $4.36

14 $1.42 $1.71 $1.83 $2.01 $2.31 $2.60 $2.90 $3.20 $3.49 $3.79 $4.09 $4.38 $4.68

FY

22

E T

rad

ing

EB

ITD

A (

$m

)

FY22 EV/EBITDA Multiple (x)

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 16

Aerometrex Limited (AMX)

26 November 2020

Financial Forecasts

AMX has a total of $6.7m in debt facilities available which is primarily used for funding capital purchases. No debt is currently

outstanding.

FY21 Forecasts

We forecast revenue growth of 17% primarily driven by an increase in LiDAR and MetroMap subscription revenue. With a step up

in aircraft and capture costs to ensure near country-wide coverage of Australia for the MetroMap platform, we forecast EBITDA

growth of only 3%. An increase in employee and occupancy costs will also impact EBITDA as the investment in the USA operation

continues.

NPAT is broadly flat yoy as the increase in image capture creates an increase in amortisation. Images are written off over two

years and this will level our from FY21 onwards.

FY22 Forecasts

We believe FY22 will be a sustainable earnings baseline for AMX as the initial investments required for MetroMap and 3D modelling in the USA will have been absorbed and revenue will be flowing through to offset those costs. We forecast 23% revenue growth driven by 20% growth in LiDAR, 25% in 3D and 125% in MetroMap subscriptions. With more consistent expenses vs pcp, this translates to EBITDA of $8.4m, 76% growth and a 29% EBITDA margin. NPAT of $2.6m may give management consideration of bringing in dividends however we note reinvestment in growth remains the current focus.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 17

Aerometrex Limited (AMX)

26 November 2020

Share Register

In addition to the 94.4m shares on issue, there are 4.5m options also outstanding. 60.2m of the shares are voluntarily escrowed

until 10/12/20. This amounts to 64% of the float.

We note that 58% of shares are held by staff or executives and ~80% of total staff currently hold shares in the business.

Top 20 Shareholders - as at 30/6/20 Shares % Held

199 Investment Pty 12,113,824 12.8%

Mark Deuter & Lynette Deuter 11,400,865 12.1%

DAIJ Pty 8,583,850 9.1%

Scott Tomlinson 8,362,230 8.9%

Beata Serafin & Wojciech Misiara 6,660,999 7.1%

National Nominees 5,129,105 5.4%

Mrs Margaret Darley 4,935,566 5.2%

Todd Dunow & Jane Swinton 3,425,181 3.6%

Citicorp Nominees 2,735,265 2.9%

HSBC Custody Nominees 1,626,691 1.7%

JP Morgan Nominees 1,101,381 1.2%

Warren Darley & Margaret Darley 1,083,427 1.1%

Merrill Lynch Nominees 976,548 1.0%

National Nominees 722,857 0.8%

Nathan Michael 649,388 0.7%

Katalin Garami & Peter Pap 568,088 0.6%

Alberto Zaniolo & Joanna Dziolak 473,407 0.5%

Jeremy Pollard 421,330 0.4%

Fabrice Marre 252,798 0.3%

BNP Paribas Nominees 250,000 0.3%

Total 71,472,800 76%

Substantial Shareholders - as at 30/6/20 Shares % Held

Matthew White 12,113,824 12.8%

Mark Deuter 11,400,865 12.1%

David Byrne 8,583,850 9.1%

Scott Tomlinson 8,362,230 8.9%

Perennial Value 7,268,855 7.7%

Beata Serafin & Wojciech Misiara 6,660,999 7.1%

Margaret Darley 4,935,566 5.2%

Total Shares on Issue 94,400,000 63%

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 18

Aerometrex Limited (AMX)

26 November 2020

Board of Directors

Mark Lindh Chairman & Non-Executive Director

Mark is a founder and co-principal of Adelaide Equity Partners, an investment house established in 2006. Prior to that, he was executive director of Rundle Capital Partners which was a division of Washington H Soul Pattinson. Mark is a corporate advisor with significant experience in advising predominantly listed companies encompassing a range of industries including technology, energy, resources, infrastructure and utilities. He has acted as the principal corporate and financial advisor to a number of Australian corporate success stories and has extensive experience in Australian equity and debt markets and advising clients on capital raisings, mergers and acquisitions and investor relations. Mark was appointed to the board in May 2019 and has been Chair since October 2019. Mark currently is also a director of ASX listed Advanced Braking Technology Ltd.

Mark Deuter Managing Director

Mark joined Aerometrex in 2005 under the previous ownership as Aerometrex’s General Manager, overseeing the expansion of Aerometrex as it introduced digital aerial camera technology. He established Aerometrex’s aerial operations and managed the human resources, sales and marketing functions. He also set strategic directions for Aerometrex’s growth in Australia. On the change of ownership via a management buy-out in 2011, Mark was appointed Managing Director and Chairman of the Board (2011 to Feb 2019). Under his direction, Aerometrex has experienced a period of sustained growth and corporate innovation. Prior to joining Aerometrex, Mark ‘s career spanned 28 years working across airborne geophysics data processing, cartography, aerial surveying, photogrammetry, aerial photography and topographic mapping for various private and government institutions.

Matthew White Non-Executive Director

Matthew was appointed as Financial Controller of Aerometrex in 2008 and then Finance Director of the company in 2011 after guiding the company through the management buyout process that occurred in that year. He has been instrumental in all financial strategies and decisions of the company during the current successful growth period. Matthew has over 27 years experience as an accountant, business and tax advisor. He has over 12 years experience as a registered mortgage broker and over 3 years experience as a financial planner. Matthew is the founder and sole director of Business Initiatives Pty Ltd, an Adelaide based Chartered Accountancy firm. The firm offers a holistic approach to clients’ financial needs, offering a wide range of services with a strong focus on continuous business improvement and wealth creation. Matthew works in a client advisory role for small to medium sized businesses.

Dr Peter Foster Independent Non-Executive Director

Peter has extensive business experience across a variety of industries. He is a creative entrepreneur with wide-ranging experience in developing innovative technologies for global markets, having founded and grown numerous technology and commercial ventures. Peter has extensive experience with the invention and intellectual property protection process and holds over 40 international patents in optics and precision electronics. He has also held senior scientific positions with a local medical laser manufacturer and with the Department of Metallic Materials, University of Bayreuth, Germany, and has delivered intensive courses on startups and technology commercialisation for the University of Adelaide. Peter holds several private company directorships across a diverse range of industries including VivoSense, a San Diego based pharmaceutical services company and leads its commercial advisory board whose members are located across the US.

David Byrne Executive Director & Chief Operating Officer

David joined Aerometrex in 2000 as Aerometrex’s Chief Photogrammetrist. He has been largely responsible for Aerometrex’s successful technical programme, he has managed and overseen its IT infrastructure, research and development and led the production team establishing high technical standards which underpin the quality and accuracy that Aerometrex is renowned for. David was appointed as COO in June 2020. David has published several technical papers and has represented Aerometrex at major Australian Spatial Science conferences on many occasions. He is a member of the Surveying and Spatial Sciences Institute and served on the National Remote Sensing and Photogrammetry Committee for three years. He was awarded Spatial Professional of the Year at the SA Spatial Excellence Awards in 2013.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 19

Aerometrex Limited (AMX)

26 November 2020

Key Management Personnel

Chris Mahar CFO

Chris has 30 years of experience across commerce and business advisory services. Prior to joining Aerometrex, Chris was a Commercial Finance Manager for Navitas Ltd (ASX: NVT), a global education company which until July 2019 was listed on the ASX prior to being purchased by a private equity firm.

Todd Dunow National Sales Manager

Todd has 25 years experience across many aspects of the aerial survey industry. Todd has led the sales and business development team for the last 9 years. Todd has been with AMX since 2001.

Beata Serafin Chief People Officer

Beata has 14 years experience across various disciplines of aerial imagery and has spent the last three years leading the company's HR function. Beata has been with AMX since 2003.

Tol Mofflin Head of Aviation/Chief Pilot

Tol has over 20 years and more than 6,500 hours of international aviation experience including 18 years within management roles.

Ralph Lante GM - LiDAR

Ralph has had a 40-year career in the geospatial sciences. He has worked for the South Australian and Northern Territory Governments in key aerial imagery roles and was centrally involved in a major GIS program in the Philippines. He also previously worked for SAAB Systems as well as Aerometrex during the period 2001- 2007. Ralph re-joined Aerometrex in 2016 as General Manager, LiDAR operations. Ralph was appointed in 2015.

Rick Cassidy President – US Operations

Rick has over 30 years experience across IT and engineering roles. For the last 10 years Rick has been working in the geospatial industry as VP, SVP and President responsible for leading the global and regional sales, operations and delivery teams.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 20

Aerometrex Limited (AMX)

26 November 2020

Key Risks

Reliance on Key Personnel Aerometrex currently employ or engage as consultants a number of key management and personnel and Aerometrex’s future depends on retaining and attracting suitable qualified personnel. Aside from technology, AMX’s competitive advantage lies in the skills and IP of flying and photography staff. The way in which images are captured enables AMX to produce higher a quality product than competitors and these skills are inherent in certain staff members. These staff members are well incentivised and we see losing some of these employees as one of the biggest risks to AMX’s operating earnings – particularly in the 3D space. There is no guarantee that Aerometrex will be able to attract and retain suitable qualified personnel, and a failure to do so could materially adversely affect the business, operating results and financial prospects. Technology and product development The success of Aerometrex is dependent on the technology and products offered and used by Aerometrex being suitable for Aerometrex to undertake the projects and opportunities available in a viable and cost-effective manner. Factors which may create risk include data storage costs, cost of production and the functioning of image processing software and computing resources. Suppliers and customers Aerometrex depends on continued relationships with its current suppliers and clients. There can be no guarantee that Aerometrex’s supplier and client relationships will continue or will continue to be successful. Aerometrex’s contracts with suppliers and clients, as with all other contracts, allow for termination. Further, there is a risk that new agreements formed with clients in the future may be less favourable to Aerometrex, such as key terms and pricing, due to unanticipated changes in the market. Competition Aerometrex competes with other geospatial mapping companies. Some of these companies have greater financial and other resources than Aerometrex and as a result may be in a better position to compete for future business opportunities. There is no assurance that Aerometrex can compete effectively with these companies. International operations Aerometrex intends to increase its investment into the expansion of its international operations. There is a risk that this investment may not be profitable or succeed long-term, due to poor execution or external factors beyond Aerometrex’s control. Aviation operations Aerometrex conducts aviation operations under its Air Operator Certificate (AOC). All aviation activity involves a degree of risk and is managed by rigorous attention to aviation safety standards. It is a key element of Aerometrex’s risk management procedures to understand the nature and full dimensions of the inherent risks to its aviation operations and how best to mitigate them. Operational assets and equipment Aerometrex’s proposed activities will be subject to numerous operational risks, many of which are beyond Aerometrex’s control. Aerometrex’s operations may be curtailed, delayed or cancelled as a result of factors such as mechanical difficulties, shortages in or increases in the costs of consumables, spare parts, plant and equipment, external services failure (such including energy and water supply), industrial disputes and action, difficulties in commissioning and operating plant and equipment, IT system failures, mechanical failure or plant breakdown, and compliance with governmental requirements. Further, Aerometrex has a number of assets and equipment that are crucial to Aerometrex’s operations and would result in serious but temporary disruption to Aerometrex’s ability to deliver its products, particularly in the area or aerial surveying. The occurrence of any one or a combination of these events may have a materially adverse effect on Aerometrex’s performance and the value of its assets. Other risks Other risks that are specific to Aerometrex, and are therefore relevant to an investment in Aerometrex, include risks in relation to insurance, demand for services, contractors, potential acquisitions, growth, counterparties, intellectual property, technical failure, operational failure, disputes, litigation, non-payment, currency exchange rates, debt and interest rates, financial performance, legal compliance and project management.

TAYLOR COLLISON LTD. www.taylorcollison.com.au

ABN 53008172450 AFSL 247083 21

Aerometrex Limited (AMX)

26 November 2020

Disclaimer

The following Warning, Disclaimer and Disclosure relate to all material presented in this document and should be read before making any investment decision.

Warning (General Advice Only): Past performance is not a reliable indicator of future performance. This report is a private communication to clients and intending clients and is not intended for public circulation or publication or for the use of any third party, without the approval of Taylor Collison Limited ABN 53 008 172 450 (“Taylor Collison”), an Australian Financial Services Licensee and Participant of the ASX Group. TC Corporate Pty Ltd ABN 31 075 963 352 (“TC Corporate”) is a wholly owned subsidiary of Taylor Collison Limited. While the report is based on information from sources that Taylor Collison considers reliable, its accuracy and completeness cannot be guaranteed. This report does not take into account specific investment needs or other considerations, which may be pertinent to individual investors, and for this reason clients should contact Taylor Collison to discuss their individual needs before acting on this report. Those acting upon such information and recommendations without

contacting one of our advisors do so entirely at their own risk.

This report may contain “forward-looking statements”. The words “expect”, “should”, “could”, “may”, “predict”, “plan” and other similar expressions are intended to identify forward-looking statements. Indications of and guidance on, future earnings and financial position and performance are also forward-looking statements. Forward-looking statements, opinions and estimates provided in this report are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions.

Any opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice and Taylor Collison assumes no obligation to update this document after it has been issued. Except for any liability which by law cannot be excluded, Taylor Collison, its directors, employees and agents disclaim all liability (whether in negligence or otherwise) for any error, inaccuracy in, or omission from the information contained in this document or any loss or damage suffered by the recipient or any other person directly or indirectly through

relying upon the information.