DISSERTATION REPORT ON "RECRUITEMENT OF FINANACIAL ADVISOR FOR INCREASING PRODUCTIVITY” SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF THE DEGREE OF "MASTER OF BUSINESS ADMINISTRATION" UTTARAKHAND TECHNICAL UNIVERSITY SUBMITTED TO : SUBMITTED BY : TWEENA PANDEY MOHD DANISH (FACULTY MANAGEMENT ) MBA (UIM) Sem.- IV U.I.M.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISSERTATION REPORT

ON

"RECRUITEMENT OF FINANACIAL ADVISOR

FOR INCREASING PRODUCTIVITY”

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT

OF THE DEGREE OF

"MASTER OF BUSINESS ADMINISTRATION"

UTTARAKHAND TECHNICAL UNIVERSITY

SUBMITTED TO : SUBMITTED BY : TWEENA PANDEY MOHD DANISH (FACULTY MANAGEMENT ) MBA (UIM) Sem.-IVU.I.M.

(2009-2011)UTTARANCHAL INSTITUTE OF MANAGEMENT

DEHRADUNCERTIFICATE

I have the pleasure in certifying that

MOHD DANISH is a bonafide student of 4th

Semester of the Master's Degree of Business

Administration of Uttaranchal Institute of

Management, Dehradun.

He has completed his dissertation report

work entitled "RECRUITEMENT OF FINANCIAL ADVISORS

FOR INCREASING PRODUCTIVITY" under my guidance.

I certify that this is his original

effort and has not been copied from any other

source. This project has also not been

submitted in any other University for the

purpose of award of any degree.

This report fulfills the requirement of

the curriculum prescribed by Uttarakhand

Technical University, Dehradun for the said

course.

Signature :........................................

......

Name of the Guide :...............................

Date :.............................................

.........

DECLARATION

I hereby declare that Dissertation titled

"RECRUITMENT OF FINANCIAL ADVISORS FOR INCREASING

PRODUCTIVITY" is submitted as a requirement

for partial fulfillment of "Master of

Business Administration (MBA)" degree from

Uttaranchal Institute of Management,

Dehradun.

The empirical findings in the

dissertation are based on the basis of

primary date collected and prepared by me. I

have not copied anything from any source or

project submitted earlier.

(MOHD DANISH)

M.B.A. (Sem. -IV)

(Batch 2009-2011)

ACKNOWLEDGEMENT

The completion of the report “WITH SPECIAL REFERENCE TO

THEIR REQUIRMENT IN INSURANCE SECTOR” has given us immense

pleasure and knowledge. It is an incident of great pleasure

of submitting this report, obligations were heavy and many

during our report work.

It gives me immense pleasure to express my deep sense

of gratitude and appreciation to my external guide Ms.

TWEENA PANDEY whose constant encouragement and valuable

suggestion gave back bone support in completing this

project.

I take the opportunity to thanks to the faculty of MBA

department for motivating, encouraging, guiding and

supporting at every step & sparing their valuable time for

me.

Last but not the least I record my sincere thanks to

all beloved and respectable persons who directly or

indirectly helped me in the completion of this report

successfully and could find any separate mention.

Above all I praise “GOD” the most beneficial, the most

merciful that I have been able to complete my training

project successfully.

��T A B L E O F C O N T E N T S

��

1) Executive Summary

2) Company profile

About ICICI Bank About Prudential About ICICI Prudential…………………..17

2) Industry Profile……………………………… 19

Insurance Importance of Insurance Privatization of Insurance Need of Insurance Major Players of Life Insurance

3) Sectional Work Done in the Company

Products Offered Work Done at ICICI Prudential Learning Suggestions

4) Research Methodology

Primary Objective Limitations

5) Case Study

6) Swot Analyses

7) Recommendation

8) Conclusion

9) Bibliography

10)Synopsis

��

��

��E X E C U T I V E S U M M A R Y

��

Insurance is a legal contract that protects people from the

financial costs that result from Loss of life, loss of

health, lawsuits, or property damage. Insurance provides a

means for individuals and societies to cope with some of the

risks faced in everyday life. People purchase contracts of

insurance, called policies, from a variety of insurance

organizations.

� Insurance has been divided into two segments

Life Insurance

General Insurance

Life insurance is a contract for payment of a sum of money

to the person assured on the happening of the event insured

against. Usually the contract provides for the payment of an

amount on the date of maturity or at specified intervals or

at unfortunate death. The contract also provides for the

payment of premium periodically to the corporation by the

assured. General Insurance includes many areas of insurance

like marine, motor, engg. Health, fire etc. the contract

provides for the payment of an amount on the happening of

some contingency.

These types of contracts are annual in nature. ICICI and

prudential came together in 1993 to provide mutual fund

products in India and today are the largest private sector

mutual fund company in India.

ICICI prudential was amongst the first private sector

insurance companies to begin operations in December 2000

after receiving approval from Insurance Regulatory

Development Authority (IRDA). ICICI Prudential’s equity base

stands at Rs. 3.75 billion, with ICIC Bank and Prudential

plc holding 74% and 26% stake respectively. As of December

31, 2002, the company had issued nearly 230,000 policies

with a sum assured of over Rs. 6,500 crore and premium

income in excess of Rs. 340 crore. Today the company is the

#1 private life insurer in the country.

At ICICI prudential customer delight is their guiding

principles. Ensuring world class solution by offering

customized product with transparent benefits supported by

the best technology is their business philosophy benefits

supported by the best technology is their business

philosophy. According to Mr. Majid Khan unit manager, ICICI

PRU. The company has used innovative marketing as well as

pricing strategies and their premium chart would be much

lower than the other player in the market. Company has

launched various products in the market with most

competitive premium among all players

��

��

��C O M P A N Y P R O F I L E

��

Industrial Credit Investment Corporation of India (ICICI)

was formed in 1995 at the initiative of the World Bank, the

Government of India and representatives of Indian industry.

The principal objective was to create a development

financial institution for providing medium-term and long-

term project financing to Indian businesses. ICICI bank is

India’s second largest bank with total assets of about Rs. 1

trillion and a network of about 540 branches and offices and

over 1,000 ATMs. ICICI Bank offers a wide range of banking

products and financial services to corporate and retail

customers through a variety of delivery channels and through

its specialized subsidiaries and affiliates in the areas of

investment banking, life and non life insurance, venture

capital, asset management and information technology. ICIC

Bank’s equity shares are listed in India on stock exchanges

at Chennai, Delhi, Kolkata and Vadodara, the Stock Exchange,

Mumbai and the National Stock Exchange of India Limited and

its American Depositary Receipts (ADRs) are listed on the

New York Stock Exchange (NYSE). The Bank offers a broad

spectrum of financial services to individuals and companies

including deposit accounts, commercial banking, mortgagees,

car loans, personal loans, corporate and trade finance,

credit and debit cards and other banking services. In the

1990s, ICICI transformed its business from a development

financial institution offering only project finance to a

diversified financial services group offering a wide variety

of products and services, both directly and through a number

of subsidiaries and affiliates like ICICI Bank. In 1999,

ICICI become the first Indian company and the first bank or

financial institution from non-Japan Asia to be listed on

the NYSE.

ICICI prudential has one of the largest distribution

networks amongst private life insurers in India, having

commenced operations in 23 cities and towns in India. These

are:

Ahemdabad, Bangalore, Chandigarh, Chennai, Coimbatore,

Gurgaon, Hyderabad, Indore, Jaipur, Kochi, Kolkata, Lucknow,

Ludhiana, Madurai, Mangalore, Meeruit, Mumbai, Nagpur,

Nasik, Noida, New Delhi, Pune and Vadodara. The company has

the largest number of bancassurance tie-ups, having

agreements with ICICI Bank, Citibank, Allahabad Bank,

Federal Bank, South Indian Bank, Bank of India, Lord Krishna

Bank, and Punjab & Maharashtra Co-operative Bank, as well

as some corporate agents. It has also tied up with

organizations like Dhan for distribution of Salaam Zindagi,

a policy for the socially and economically underprivileged

sections of society.

� About Prudential

Established in 1848, prudential is a leading international

financial services company in the UK, with some US$276

billion funds under-management and more than 13 million

customers worldwide. Prudential has brought to market an

integrated range of financial services products that now

includes life assurance, pensions, mutual funds, banking,

investment management and general insurance. In Asia,

prudential is UK’s largest life insurance company with a

vast network of 22 life and manual fund operations in twelve

countries – China, Hong Kong, India, Indonesia, Japan,

Korea, Malaysia, the Philippines, Singapore, Taiwan,

Thailand and Vietnam. Since 1923, Prudential has championed

customer centric products and services supported by over

60,000 staff and agents across the region.

� About ICICI Prudential

ICICI and prudential came together in 1993 to provide mutual

fund products in India and today are the largest private

sector mutual fund company in India. ICICI prudential was

amongst the first private sector insurance companies to

begin operations in December 2000 after receiving approval

from Insurance Regulatory Development Authority (IRDA).

ICICI Prudential’s equity base stands at Rs. 3.75 billion,

with ICIC Bank and Prudential plc holding 74% and 26% stake

respectively. As of December 31, 2002, the company had

issued nearly 230,000 policies with a sum assured of over

Rs. 6,500 crore and premium income in excess of Rs. 340

crore. Today the company is the #1 private life insurer in

the country.

ICICI prudential has recruited and trained over 16,000

insurance agents to interface with and advise customers, and

has the highest number amongst private life insurers on the

renowned million-dollar round table (MDRT). Their latest

venture ICICI prudential life plans to take car eof the

insurance needs at various stages of life. ICICI prudential

life insurance company has mopped up a premium income of Rs.

75 crore for the year ended March 31, 2004 reflecting a 106

per cent growth over corresponding period last year. It has

sold 4.7 lacks policies during the year, against one lakh

policies sold in fiscal 2002. ICICI prudential has cornered

about 31 percent of the private sector insurance market,

which today accounts for 10 pe cent of incremental sales of

the entire industry. Average premium is Rs. 18000+ majority

of 1.2 lakh policies sold by ICICI prudential in last

quarter of fiscal 2004 were pension and unit-linked plan.

Pension products accounts 25 per cent of the sales giving

ICICI prudential an overall industry share of 25 percent

��

��

��I N D U S T R Y P R O F I L E

��

Insurance is a legal contract that protects people from the

financial costs that result from Loss of life, loss of

health, lawsuits, or property damage. Insurance provides a

means for individuals and societies to cope with some of the

risks faced in everyday life. People purchase contracts of

insurance, called policies, from a variety of insurance

organizations. Insurance is conceived as a method of sharing

of these losses, embodying the principle of co-operation

existed in the early civilization. There is evidence that

during the Aryan civilizations, loss of profits in industry

was insured by the village co-operative in India. Almost

everyone living in modern, industrialized countries buys

insurance, for instance, laws in most states require people

who own a car to buy insurance before driving it on public

roads. Lenders require anyone who finances the purchase of a

home or car with borrowed money to insure that property.

Business partners take out life insurance on each other to

make sure that business will succeed even if one of the

partners die.

� Insurance has been divided into two segments

Life Insurance

General Insurance

Life insurance is a contract for payment of a sum of money

to the person assured on the happening of the event insured

against. Usually the contract provides for the payment of an

amount on the date of maturity or at specified intervals or

at unfortunate death.

The contract also provides for the payment of premium

periodically to the corporation by the assured. General

Insurance includes many areas of insurance like marine,

motor, engg. Health, fire etc. the contract provides for the

payment of an amount on the happening of some contingency.

These types of contracts are annual in nature. Historians

believe that insurance first developed in summer and

Babylonia.

The merchants and traders of these societies transferred and

pooled their money to protect themselves and pirates. In the

18th Century BC, Babylonian king Samurai developed a code of

law, known as the code of specific rules governing the

practices of early risk sharing activities. Insurance also

developed during the 1700s in the North American colonies.

In 1730 Benjamin Frank contributed for the Insurance of

Houses from Loss by fire. Early development of insurance was

unorganized. It was mainly insuring commercial risks. The

insurance inhuman life started in England in 1583AD for term

Assurance for 12 months, which was issued for the first

time.

In 1705 amicable society started paying assurance on death a

tern carried on unto 1757.

In 1762 equitable society was the first co. to start charging

premium on scientific basis. In India the references to

insurance history relates to the East India Co. when some

policies where issued on the life of Bruisers in foreign

currency. In 1870- Bombay Mutual Insurance Limited

In 1874- Oriental Govt. Security life Assurance Co Limited

In 1896 – Bart Insurance Co. and 1897 empire of India.

In 1905 – no of insurance company life Hindustan co-op United

India, Bombay Life

National – Asian were set up during the above period. After

2nd world war several new companies were established, most

important being New India Assurance Co. others were Jupiter,

Lame, Andhra, Industrial Metropolitan and New Asiatic. After

1st World War the peace of Industrialization was accelerated

in India.

The Swedish movement had already gathered momentum and

nationalism in the twenties, Indian offices began to take

due share of the country’s business. It continuously

progressed and there seemed to be steady rise in the per

capita insurance in the country. The government started to

exercise control with the passing of insurance act 1912

there was a marked increase in the volume of insurance

business and other form of Business. More companies were

floated.

With a view to have a closer watch on the matter of

investment of funds and expenditure and general management

of business govt. enacted the insurance act in 1938 and also

the Dep’t of Insurance under the authority of the

superintendent of Insurance was established. This act was

further amended in 1950. Before nationalization there were

97 operating centers almost all urban.

There were 245 different insurance companies then.

Nationalization off the Insurance business in 19 Jan 1956.

LIC act of 1956 was passed by the parliament and received

presidential assent on 18th June 1956 and act come into

force on 1st July 1956-LIC came into existence on the 1st

September 1956.

� Importance of Insurance

Insurance benefit society by allowing individuals to share

the risks faced by many people. But it also serves many

other important economic and societal functions. Because

insurance is available and affordable, banks can make loans

with the assurance that the loan’s collateral is covered

against damage. This increased availability of credit helps

people buy homes and cars. Insurance also provides the

capital that communities need to quickly rebuild and recover

economically from natural disasters, such as floods or

earthquakes. Insurance itself has become a significant

economic force in most industrialized countries. Employers

buy insurance to cover their employees against work related

injuries and health problems. Businessmen also insure their

property, including technology used in production against

damage and theft. Because it makes business operations

safer; insurance encourages businesses to make economic

transactions, which benefit the economies of countries.

Insurance companies perform a type of monetary

redistribution they collect premium and eventually

redistribute that money as payments. Depending on the type

of insurance, redistribution can take place anywhere from a

few months to many decades. Because of this delay between

collections and paying out funds, insurance companies invest

their funds to bring in extra revenues. Such investments

help businesses and government finance their operations, and

few months from those investments deport the operations of

insurance companies. With these investments earnings,

insurance companies can keep rates much lower than would

otherwise be possible.

� Privatization of Insurance

The Indian insurance has finally opened up. The first movetowards liberalization came

with the Amphora Committee Report in 1993 which recommendedthe privatization of

insurance.

Indian stands to gain witty the following major advantages:

Better products with more reasonable and

affordable pricing

Quick servicing

Increased saving rate

Long-term funds for infrastructure development

will be available to the country

Large inflow of foreign capital

It is debated that the insurance business does not produce

profit in the first five year. Cross subsidization is a

feature of the Indian Market. Event the fire portfolio which

is considered profitable, cross subsidizes the other

department. Tariff reductions are likely to reduce further.

Insurer will have to institute proper claims management

process in order to extract proficiencies. The govt. is

soon to present the new model for taxing life insurance

companies at internationally competitive rates.

New entrants would be well advised to look ahead to the

stage where brand strength will be a competitive advantage

and sketch their alliances accordingly. Infect alliances

related to distribution rather than to product or technology

will prove most valuable in the long run. Brokers will come

into the market for first time and there is bound to be

intense competition as a result of this in the multi

channels of distribution.

� Need of Insurance

Since beginning of the world, man has always felt insecurity

for his assets and even life. There is uncertainty in every

aspect of life. It is an old saying that only death and tax

are certain, however even the time of death and rate jog tax

is not certain. Uncertainties expose our assets to losses

and consequently endless problems. A fire in a factory may

burn everything and owner’s only source of earning with

investment of huge capital is finished but insurance will

come to one’s rescue if insurance is taken, all the

operations can be started again. Insurance does not only

provide reimbursement at the time of loss but at the time

of taking the policy, insurer provides suggestive measures

to reduce the effect of hazards and losses. Earthquake,

flood, riot, strike, theft, explosion, fire, etc. are some

of the common dangers to our assets. Moreover life insurance

besides providing financial assistance to the insured,

these policies provide investment opportunities and even

pension plans at market interest rate.

� Opportunities in Insurance

In Indian market, the opportunity for insurance companies is

huge. The efforts of government companies have lacked

sincerity, as there is large untapped market even after 45

years of nationalization. According to sources, 30 cores

people of India can afford insurance however only 8 cores

of them have taken any insurance. Life insurance premium

collected in a year is only 2% of gross domestic product in

India with that of 12% in USA. Total non-life insurance

premium is a mere 0.6% of GDP which is almost negligible. On

the basis of this it can be sold that there is huge scope

for insurance in India. There is still much to achieve and

a big market to explore.

The latent demand foreseen in Indian market and the success

of liberalized market in emergent economies make this a

great opportunity. To avail this may international players

including the world leaders have set up their business in

India in last two years.

Prudential life insurance was first company to tie up with

an Indian company i.e. is ICICI and gets a license. Each

company requires 100 crores of capital to start their

business, which is a big amount to ensure the solvency of

company at all times. Other companies, which have come up,

are:

MAJOR PLAYERS OF LIFE INSURANCE IN INDIA

Life Insurance Corporation of India

ICICI prudential Life Insurance

HDFC Standard Life Insurance

Max New York Life Insurance

Birla Sun Life Insurance

Om Kotak Mahindra Life Insurance

Reliance Life Insurance

Allianz Bajaj Life Insurance

Ing Vyasa Life Insurance

SBI Life Insurance

Metlife Insurance

Sahara Life Insurance

Aviva Life Insurance

��

��

��S E C T I O N A L W O R K D O N E I N T H

E C O M P A N Y��

� Advisors recruitment for the company

Advisors are the base of any insurance company .For his

recruitments ,primarily we analyse his/her necessary,

qualification his personality and selling skill and than

experience. It s a challenging job to recruit the advisors

in competitive market.

� Products offered by the company through advisors

At ICICI prudential customer delight is their guiding

principles. Ensuring world class solution by offering

customized product with transparent benefits supported by

the best technology is their business philosophy benefits

supported by the best technology is their business

philosophy. According to Mr. Majid Khan unit manager, ICICI

PRU. The company has used innovative marketing as well as

pricing strategies and their premium chart would be much

lower than the other player in the market. Company has

launched various products in the market with most

competitive premium among all players.

PROJECTION PLAN

These are very good plan for those who want protection

(especially) for their family because happiness and security

for our family is all that we want. However, the

uncertainties of life often worry you. Unfortunate events

can make you are no longer around. Life insurance can help

ease many of those worries. It ensures that your loved ones

are adequately provided for and that their future is secure,

no matter what the uncertainty.

ICICI PRU offers you a choice of 3 level term products with insuranceprotection:

Life Guard Level Term Assurance Life Guard Level Term Assurance with Return of Premium Life Guard Single premium

��HOW THESE PLANS WORK

��Life Guard Level Term Assurance

What is Life Guard level term assurance policy? Thisplan provides financial protection to your familyin case of the unfortunate event of death.

How does the Life Guard Level Term Assurance policywork? You will have to pay a regular annualpremium for the term chosen and will be providedthe insurance cover on your life equal to the sumassured.

What benefit does this plan offer you? In case of death of the life assured during their term,

the sum assured under the plan will be paid to thebeneficiary. There are no maturity benefits.Hence, on survival till maturity, the policy willterminate without any returns.

How much you have to pay for this plan?

The following table gives you indicative premiums for

various age term combinations for a sum assured of

Rs. 10 Lakhs.

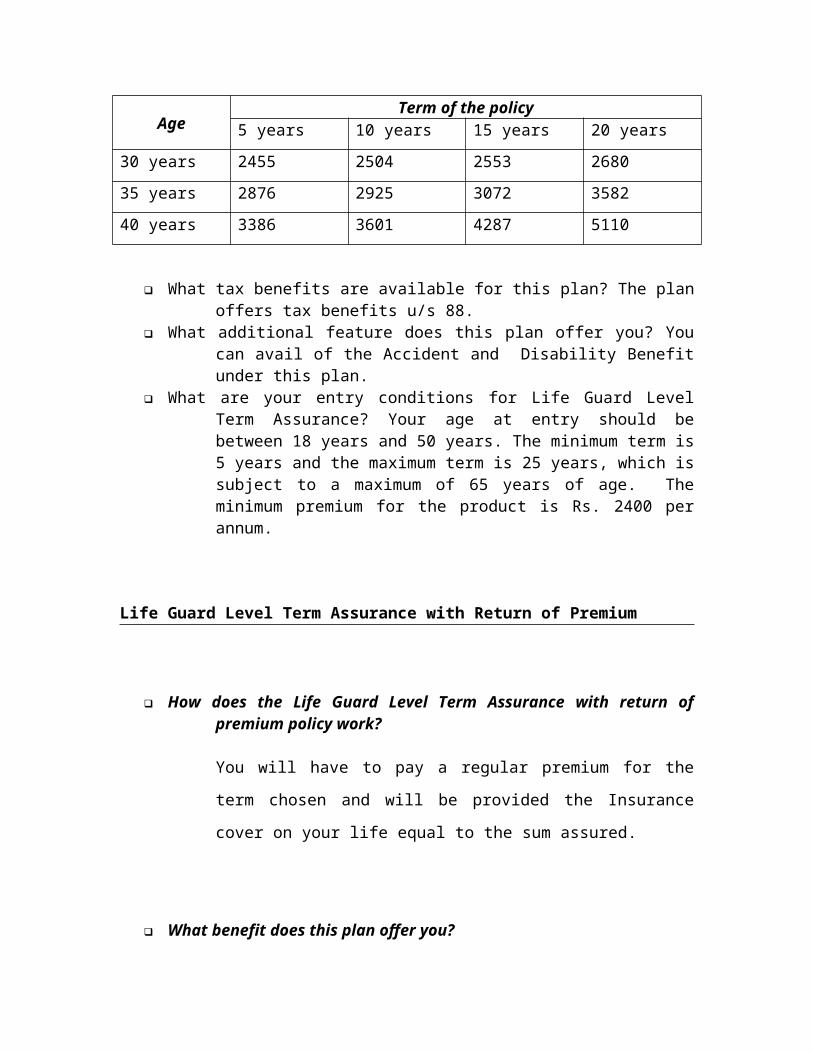

AgeTerm of the policy

5 years 10 years 15 years 20 years30 years 2455 2504 2553 268035 years 2876 2925 3072 358240 years 3386 3601 4287 5110

What tax benefits are available for this plan? The planoffers tax benefits u/s 88.

What additional feature does this plan offer you? Youcan avail of the Accident and Disability Benefitunder this plan.

What are your entry conditions for Life Guard LevelTerm Assurance? Your age at entry should bebetween 18 years and 50 years. The minimum term is5 years and the maximum term is 25 years, which issubject to a maximum of 65 years of age. Theminimum premium for the product is Rs. 2400 perannum.

Life Guard Level Term Assurance with Return of Premium

How does the Life Guard Level Term Assurance with return ofpremium policy work?

You will have to pay a regular premium for the

term chosen and will be provided the Insurance

cover on your life equal to the sum assured.

What benefit does this plan offer you?

In case of death of the life assured during the

term, the sum assured under the plan will be paid

to the beneficiary. On survival till maturity, all

the premiums paid, will be returned without

interest.

What tax benefits are available for this plan?

The plan offers tax benefits u/s 88.

What additional feature does this plan offer you?

You can avail of the accident and disabilitybenefit under this plan.

What are your entry conditions for Life Guard Level Term Assurancewith Return of premium?

Your age at entry should be between 18 years and

50 years. The minimum term is 5 years and the

maximum term is 25 years, which is subject to a

maximum of 65 years of age. The minimum premium

for the product is Rs. 2400 per annum.

Life Guard Single Premium

What is Life Guard Single Premium policy?

This is a single premium variant of the Level TermAssurance Plan.

How does the Life Guard Single Premium policy work?

You have to make a one-time premium payment,

depending upon the term and the sum assured chose

by you.

What benefit does this plan offer you?

In case of the death of the life assured during

the term, the sum assured under the plan will be

paid to beneficiary. There are no maturity

benefits at the end of the term.

What tax benefits are available for this plan?

The plan offers tax benefits u/s 88.

What are your entry conditions for Life Guard Single Premium?

Your age at entry should be between 18 years and

50 years. The minimum term is 5 year and the

maximum term is 15 years, which is subject to a

maximum of 65 years of age. The minimum sum

assured for the product is Rs. 2 lakhs.

Saving Plans

Most endowment policies are a good way of saving for the

future. A policy can be designed to make your savings grow

and have them available to you at the end of a fixed number

of years. Or, a policy could provide you with an income

every three or four years.

ICICI provides you three savings plans with insuranceprotection

Save ‘n’ Protect

Smart Kid

Cashbak

How these plans work

What is Smart Kid?

A plan which gives child the freedom to pursue their

dreams, the strength to face challenges, the guarantee to

live life to its fullest whatever be the uncertainty. As

parents, your biggest concern is that of securing the

future of your child. In today’s world, with ever

increasing competition, escalating cost of education and

uncertain financial markets, it is very important to plan

for your child’s future. It is a plan that provides

guaranteed benefits to your child along with the life

insurance cover. Smartkid is so designed that it provides

money at all the critical milestones in his/her life,

whatever be the uncertainties.

Who can purchase this policy?

Parents (between 20-60 years) with children in the age

group of 0-12 years can purchase this policy.

What should you buy smart kid?

Because smartkid ensures that you have total peace of

mind as far as your child’s future is concerned. In the

event of death of the Life assured Sum assured of the

plan is paid immediately – assists the family in meeting

the unforeseen expenses incurred because of the

unfortunate loss.

Waiver of premium – no future premia are payable, thereby

ensuring that your family is not burdened financially.

Thus, there will be no financial obstacle in realizing

the dream which the parent or child had.

What are the options for premium payment?

Mode of payment:: Monthly, half yearly and yearly.

What are the limits of Smart Kid?

Minimum premium: Rs. 8,000/- per year

Sum Assured: From Rs. 100,000/- to Rs.3,000,000/-

Maximum limit under Income Benefit Rider: Rs.1,000,000/-

Maximum limit under Accident & DisabilityBenefit Rider: Rs. 1,000,000/-

What tax benefits will you get?

The premium that you will be paying will be tax exempt

under section 88. Save ‘n’ Protect Being the head of the

family requires that you bear quite a few

responsibilities. Some of these include: being able to

fund your child’s higher education, your daughter’s

weeding, your own cozy nest and realize all your other

dreams. This is an ideal plan for those who want to

accumulate funds on a regular basis while enjoying

insurance protection.

What exactly does the Save ‘n’ protect do?

It is a fixed term policy that combines savings with life

cover. It is a fixed term plan in which you pay premium

regularly during the term. On the death of the life

assured, in the beneficiary will get the sum assured, the

guaranteed additions and the vested bonuses. Once the

policy matures, i.e. at the end of the term, you can get

the full sum assured and guaranteed additions as well as

the vested bonuses. In addition, you will get an

extended term insurance cover for five years after the

maturity date of the policy for 50% of the sum assured.

You will not have to pay any premium for the same.

Who can apply?

You can apply if you are in the age group of 0 to 60

years. The maximum cover ceasing age is 70 years. The

minimum sum assured you should apply for is Rs. 50,000

and the minimum term is 10 years. The minimum premium is

Rs. 4,8000 p.a.

Can I take a loan against my policy?

Yes, you can avail of a loan under the policy, to meet

your requirements. This will be dependent on the

surrender value your policy acquires. Interest is charged

on the amount of loan availed.

Can I discontinue my policy?

Your policy acquires a paid up value after premiums are

paid for three years. A guaranteed surrender value is

payable to you, if you decide to terminate the policy

after 3 years premiums are paid. However, the insurance

protection provided under this policy will also cease.

What are the add-on-cover?

Accident & Disability Benefit

Critical Illness Benefit

Major Surgical Assistance

What tax benefits will you get?

The premium that you will be paying will be tax exemptunder section 88.

Cash Bank

As an individual you have to be financially prepared for

various milestones in your life. If you are newly married,

you need to plan for a baby a few years from now. If you

have teenage children you need to plan for their university

education. What you need is a plan to meet your periodic

financial, requirement with the added benefit of insurance

protection.

What exactly does the CashBak do?

Sit is a three in one plan that combines savings,liquidity and protection through the following:

Fixed term of 15 or 20 years

Survival benefit payments at regularintervals

Premiums are payable throughout the term ofthe policy

On the death of the life assured, thebeneficiary will get the sum assured, theguaranteed additions and the vested bonuses.

Who can apply?

You can apply if you are 16 years old and no older than

55 years. The minimum sum assured you should apply for

Rs. 75,000. The minimum premium amount is Rs. 4,800 p.a.

Can I take a loan against my policy?

No loans are available under this policy.

Can I discontinue my policy?

Yes, you can discontinue your policy after premiums are

paid for three years. A guaranteed surrender value is

payable to you, if you decide to terminate the policy

after 3 years premiums are paid. However, the insurance

protection provided under this policy will also case.

What are the add-on cover?

Accident & Disability Benefit

Critical Illness Benefit

Major Surgical Assistance

Retirement Plans

When a person grows old both the physical capacity as well

as the financial capacity of that person become weak and at

some time inefficient and as a result what ever the standard

of living that the person maintained in his young get

deteriorated with span of time. It is not in the power

anybody to returned the physical strength back to the person

but with some retirement plans i.e. pension plans the

financial strength can be regained by the person in order to

maintain his present standard of living. These plans take

care of the inflation as well future requirement of a person

at his old age. At present ICICI Prudential offers four

types of retirement plans for the public. This plans gives a

safety and security o those people who aged and not

involving in any of financial activities and complete

depends on any monetary to sustain their living.

Forever Life

It is a comprehensive retirement solution that is developed

keeping in mind a persons’ various capabilities and needs,

with respect to one’s retirement planning. This is a plan

that ensures you to maintain your lifestyle for a lifetime.

So, whether you are 30 or 60 this is a just the right

retirement plan for a person. Ideally, this plan is suitable

for those peoples who are between 30-35 years of age to take

the maximum benefit of this plan. This gives a person a

longer period for your retirement plan. It is a deferred

annuity plan and it provides regular incomes for life after

a stipulated date.

The amount you receive depends on the premium you pay till

the stipulated date and the annuity option you choose. It

also offers life cover during the deferment phase.

The plan has two phases – The Deferment Period (Policy Term)

and the Annuity Period. Premiums are paid in the deferment

period till the time of vesting. From the vesting date

annuity is paid for the lifetime of the annuitant. The

premium depend upon the age of the person and also the term

of the product, which the deferment period.

The policy attains a value at the end of deferment period,

which is the total of the sum assured under the policy

guaranteed additions (@3.5% compounded for the first 4 years

of the policy) + vested bonuses (depending on the company’s

performance and are not guaranteed) this value is applied

to purchase annuity at the time of vesting.

This plan has two main benefits they are

Spouse Benefits

In case of the unfortunate event of death, the annuity

starts for the spouse. The annuity payable is determined on

the basis of your sum assured plus guaranteed additions plus

the vested bonuses if any at the time of the death. Your

spouse would have the option to either take the accumulated

value of the Sum Assured + Guaranteed Additions + Vested

Bonuses (if any) or opt for an annuity using a desired

portion of the accumulated value and take the rest as lump

sum.

Annuity Benefit

On the date of vesting (retirement), you start receiving a

regular income for life. This amount would depend upon the

annuity option chosen by you and the accumulated value as on

the vesting date. The annuity would also depend upon the

annuity rates offered by the company as on that date and are

not guaranteed. At vesting, you will have the option of

taking up to 25% of the aggregate of the sum assured,

guaranteed additions and vested bonuses (if any) as lump-

sum. The remaining will be used to provide with a regular

stream of income for life.

How this plan can give the customer the tax benefit?

Tax benefit u/s 80CCC the amount you invest is fully

deducted from income subject to the lump sum amount of Rs.1,

00,000

Is this plan is flexible? If yes then in what way?

Yes this plan is quite flexible and it is in the followingway:-

Choice of Retirement Date: You have the flexibility to postpone

the vesting from the originally chosen vesting date up to a

maximum of 70 year of your age. During the postponed period

your accumulated amount will earn interest as determined by

the company from time to time. There will be no life cover

or premium paid during this period. Open market option: This

option gives you the flexibility to buy a pension from any

other insurer of your choice, at the time of vesting. So you

have three freedom to take the best from the market.

Annuity Options: You have the flexibility to choose from fourdifferent annuity options.

Life Annuity : Annuity for Life annuity with return of

purchase price: Life annuity for the annuitant with the

return of the purchase price to the beneficiary. Life

annuity guaranteed for 5, 10, 15 years: Guaranteed annuity

is paid for the chosen term (5/10/15) and after that the

annuity continues if at that time annuitant is alive.

What additional benefit can be draw from this plan?

Critical Illness Benefit

Major Surgical Benefit

Accident and Disability Benefit

Life Link Pension This plan is a complete retirement

solution with total flexibility, total control that gives a

person the power to plan for your own retirement. It

provides regular income for your life from a date, which can

b chosen by you. The amount you receive would depend upon

the premiums you pay, the market value of your investment

and the option of the annuity chosen. It is a pension plan

that provides the benefit to you to invest your money in

market linked funds. During the deferment period when, a

part of the premium is used to pay for the initial charges

and the rest would be invested in the plan of your choice.

Entry into the plan will be based on the Unit Value

applicable on the date of issuance. Some benefits that are

offered by this plan to the customer are as follows: Death

benefit: you have the flexibility of choosing a zero death

benefit or a death benefit of 105% of the premium. In case

of the unfortunate event of death, the spouse would get the

higher of the death benefit (105% or 0% of the premium paid)

chosen by you or the value of your units as on that date.

Your spouse would have the option to either take the

higher of the death benefit or the value of units or opt for

an annuity. Annuity benefit on the date of vesting

(retirement), you start receiving a regular income for life.

This amount would depend upon the annuity option chosen by

you and the value of units as on the vesting date. The

annuity would also depend upon the annuity rates offered by

the company as on that date and are not guaranteed. At

vesting, you will have the option of taking up to 25% of the

value of units at the time of vesting as lump sum. The

remaining will be used to provide with a regular stream of

income for life.

Whether this plan is flexible or not? If yes then what else can acustomer draw from this plan apart from the above benefits?

Choice of retirement date: you have the flexibility to start

your pension whenever you want after a stipulated age. A

choice that lets you make the best of the market conditions

by timing the start of your pension.

CHOICE OF PLANS

You have the option to choose between our Growth plan,

Income plan or balanced plan. Maximize (growth) plan: This

plan offers you the benefit of long term capital

appreciation from a portfolio that is primarily invested in

equity and equity linked securities. Protector (Income)

plan: This plan offers you steady returns with a portfolio

that primarily invested in debt and debt related

securities. Balancer (balanced) Plan: This plan offers you

the flexibility of growth and steady returns with the

portfolio being invested in a mix of equity and fixed income

securities. Switch between funds:

During the deferment period you can switch between the

various plan options to take advantage of the prevailing

market conditions or with the change in your priorities.

You can do one free switch every year. Top-up of

investments: During the deferment period you have the option

of increasing your investment with top-ups (minimum amount

of Rs. 10,000).

Annuity Options: You have the flexibility to choose from fourdifferent annuity options.

Life Annuity: Annuity for Life.

Life Annuity with return or purchase price: Life annuity for the

annuitant with the return of the purchase price to the

beneficiary.

Life annuity guaranteed for 5, 10, 15 years: Guaranteed Annuity is

paid for the chosen

term (5/10/15) and after that the annuity continues if atthat time annuitant is alive.

Joint Life, last survivor with Return of purchase price: In this case the

annuity is first paid to the annuitant, after the death of

the annuitant the spouse starts getting a pension which is

equal in amount of the annuity paid to the annuitant. After

the death of the last survivor the purchase price is

returned back to the beneficiary.

Choice of retirement date: You have the flexibility to postpone

your vesting age upto a maximum of 70 years of age.

Open market option: This option gives you the flexibility to

buy a pension from any other insurer of your choice, at the

time of vesting. So you have the freedom to take the best

from the market.

What tax benefits are available with Life Link Pension?

Tax benefit u/s 80 C the amount of investment or the amount

of premium you pay is fully deducted from your income

subject to Rs.1,00,000

How much you have to pay?

The minimum premium in this plan is Rs. 25,000. What are

your entry conditions? You can apply for this plan if you

are between 18 and 62 years of age. You have the flexibility

of choosing the vesting age between 50 and 70 years of age.

Minimum term of the product is 3 years.

RETIREMENT PLANS

Joint Life, Last Survivor with Return of Purchase Price: In

this case the annuity is first paid to the annuitant, after

the death of the annuitant the spouse starts getting a

pension which is equal in amount of the annuity paid to the

annuitant. After the dearth of the last survivor the

purchase price is returned back to the beneficiary. Choice

of Retirement Date: You have the flexibility to postpone

your vesting age upto a maximum of 70 years of age. Open

Market Option: This option gives you the flexibility to buy

a pension from any other insurer of your choice, at the time

of vesting. So you have the freedom to take the best from

the market.

What tax benefits are available with Life Link Pension?

Tax benefit u/s 80CCC(1): Upto Rs. 10,000 deducted from

your taxable income.

How much you have to pay?

The minimum premium in this plan is Rs. 25,000.

What are your entry conditions?

You can apply for this plan if you are between 18 and 62

years of age. You have the flexibility of choosing the

vesting age between 50 and 70 years of age. Minimum term of

the product is 3 years.

RIDERS

Riders are the additional benefit that you can add on to

your policy. You can opt for riders when taking the basic

policy at a marginally incremental cost. No bonuses are paid

on the riders.

CRITICAL ILLNESS BENEFIT RIDER

A rider added to a life insurance policy to protect the

insured in the event of a critical illness. 9 medical

conditions are covered by this benefit. This ensures living

benefits payable to the insured for medical expenses prior

to death. This rider is available with Save’n’ Protect,

Cash Bak, Forever Life (Regular Premium Deferred Pension),

Life Time and Life Time pension. If the life Assured is

diagnosed to be suffering from a specified Critical Illness

after six months from the date of policy, the Sum assured

under this policy shall be paid together with guaranteed

additions and vestdonu.

CONDITIONS

When the policy is in force for the full sumassured

Any time before the expiry of the policy Before the age of 65 (which ever is earlier) On the payment of the Sum Assured together

with the bonuses and guaranteed additions ifany, allocated to the policy, the policyterminates

EXCLUSIONS

The critical illness shall not have been caused by the

existence of Acquired Immune Deficiency Syndrome or the

presence of any Human Immune deficiency Virus Infection in

the person of the Life Assured. Self inflicted injury. Drug

abuse

Failure to follow medical advice

War, whether declared or not and civil

commotion

Pregnancy

Breach of law

Aviation other than as a fare paying

passenger in a commercial licensed aircraft

(being a multi engine aircraft)

Hazardous sports/pastimes

The benefit shall not be payable in respect of any illness

other than those denied as Critical Illness, nor shall it

apply or be payable in respect of any of those said

illnesses the symptoms of which have occurred or which has

been diagnosed or for which the insured person received

treatment, during the first 6 months from the date of

policy. The maximum aggregate of critical Illness Benefit

granted by the Company under all the policies of the Life

Assured shall not exceed Rs. 10,00,000.

PREMIUM

The premium for this benefit is guaranteed for five years

only from the date of commencement of policy. The company

reserves the right to carry out a general review of the

experience from time to time and change the premium as a

result of such review. The company will give notice in

writing about the change and the Life Assured will have the

option not to pay any increased premium.

In such a case the benefit will be appropriately reduced

from the effective date of the change in premium and the

company will advise the Life Assured accordingly 80D. This

rider is available with Save’n protect, Cash Back Forever

Life (Regular Premium Deferred Pension), Life Time and Life

Time pension. The maximum sum assured under Major Surgical

Assistance Benefit granted by the Company under all the

policies of the Life Assured shall not exceed Rs. 10,00,000.

BENEFITS

Under this the life assured is paid

50% of sum assured in respect of majorprocedures

30% of sum assured in respect of intermediateprocedures

20% of sum assured in respect of minorprocedures this benefit is payable on morethan one occasion when the life assuredundergoes

surgery. However the total benefit payable incase of all the procedures is restricted to a

maximum of 50% of the sum assured.

CONDITIONS

The benefit would be available only for medically necessary

surgical procedures performed at a hospital as in patient

When the policy is in force for the full sum Assured Anytime

before the expiry of the policy or before the age of 65

(whichever is earlier)

EXCLUSIONS

The company shall not be liable to pay any sum under or in

terms of this benefit in the event of Preexisting injuries

or illnesses, treatment that is not taken from recognized

hospitals or doctors. No benefit will be payable in respect

of a claim which, in the opinion of our Chief Medical

officer, results directly or indirectly from a condition for

which the insured person has previously received

treatment, or which had previously been diagnosed, or

which he was aware of, at the commencement of the policy or

within the first 6 months from the date of policy.

HIV/AIDS

Congenital or hereditary diseases or physical

defects

Attempted suicide

Attempted suicide

Self inflicted injury, drug abuse

Injuries from natural disasters

War and civil commotion

Criminal acts

Taking part in flying activity other than as a passenger in

a commercially licensed aircraft, (being a multi – engine

aircraft) By engaging in hazardous sports/pastimes, i.e.

taking part in (or practicing for) boxing, caving, climbing,

horse racing, mountaineering, off piste skiing, pot holing,

power boat racing, underwater diving, yacet racing or any

race, trial or timed motor sport.

ACCIDENT BENEFIT

This benefit is payable in case of death that occurs as a result of anaccident. The death must occur:

When the policy is in force for the full sumassured

Any time before the expiry of the policy

Before the age of 65 (whichever is earlier)

BENEFITS

If you are covered under this benefit and if death occurs as

the result of an accident during the term of the policy,

your beneficiary shall receive an additional amount equal to

the accident cover under the rider. If the accidental death

occurs during the term of the policy, while you are

traveling as a fare paying passenger on an authorized public

mass transport namely bus or train, your beneficiary will

be entitled to twice the accident cover under the rider.

DISABILITY BENEFIT

This benefit is payable in case of disability that occurs as

a result of an accident. The maximum cover under this

benefit is Rs. 10,00,000. This is inclusive of all the

policies you may have taken with us. The disability must

occur.

When the policy is in force for the full Sum

Assured

Any time before the expiry of the policy

Before the age of 65 (whichever is earlier)

BENEFITS

If the Life Assured is totally and permanently disabled as a result of an

accident the following additional benefit paid:

10% of the Sum Assured every year for 10

years commencing from the first anniversary

of the disability date. Premiums under this

rider falling due on or after the disability

date shall be waived.

If there are any other benefits payable under

this rider then all such benefits shall cease

to be available on and after the disability

date

The dearth due to accident should not be

caused By attempted suicide or self inflicted

injuries while sane or insane, or whilst the

Life Assured is under the influence of any

narcotic substance or drug or intoxicating

liquor; or By engaging in aerial flights

(including parachuting and skydiving other

than as a fare paying passenger on a

licensed passenger carrying commercial

aircraft (being a multi engine aircraft)

operating on a regular scheduled route; or

By the Life assured committing any breach oflaw

Due to war, whether declared or not or civilcommotion

By engaging in hazardous sports/pastimes,

i.e. taking part in (or practicing for)

boxing, caving, climbing, horse racing, jet

skiing, martial arts, mountaineering, off

piste skiing, pot holing, power boat racing,

underwater diving, yact racing or any race,

trail of timed motor sport.

WORK DONE AT ICICI PRUENTIAL LIFE INSURANCE COMPANY

ICICI is a company known for its professionalism and survive

that gives value to the customer. Inside story of the

company & are above expectations. At ICICI prudential, my

training was related to marketing of the product of ICICI

prudential and also making agents for the company. I am

dividing my learning experience into two parts relating to

each of the above-mentioned parts.

Marketing or getting people’s perception at

the time of selling policies, about the new

private life insurance companies and also

about the products of ICICI prudential

available in the market.

Whenever I met a person and talked about

ICICI prudential the person told me that he

already has a life insurance policy from LIC.

In almost 100% cases I found such answers.

It’s a very tough job to break the monopoly

as well as the goodwill of LIC in the market,

after serving 47 years in the country with no

competition LIC has created an atmosphere

when people think that life insurance means

LIC, and to this perception, people often say

that I have my LIC instead of saying that I

have my life insurance policy.

At the time of selling the policy what I

found that the most preferred plan is money

back. The reason being availability of funds

after every five year which can be used for

further premium. Whenever I used my contracts

& met the persons for policy selling purpose

what I found that most of the people do not

have faith on private players, they have

doubts on the credibility and long stay of

private insurance companies.

But with good products & value added

services, ICICI prudential emerges as a

leader in the private sector. In the whole

period of my corporate training I met with so

many people and gave seven leads to the

company because of the time constraint. But

out of these seven leads I alone convert one

lead into a full flesh policy within training

period and rest of the leads were in the

pipelines, and the company’s agents were

working on these leads.

Practical experience at the time of making an agent:-

To convince a person to become an agent off any life

insurance company is a very tough job, because after opening

up of the insurance sector the agent force of LIC has

created a mess in the market, by paying the first premium of

client from their own pocket. This type of activities

demoralize people from becoming the agent of a life

insurance company. As data was not provided by the company

so my first target source was my friend circle for the

agent purpose. Out of nine leads of mine I made two agents

over there, and rest of people declined due to reasons

which are as follows:

According to them, it’s not a prestigious job

as they belong to good families (in terms of

money).

According to them LIC has a strong monopoly

in the insurance market and nobody is going

to break it, so it is a time wastage to

become an insurance agent for ICICI

prudential.

They thought that instead of spending their

time on ICICI prudential they should go for

LIC, which is more beneficial.

Since they are not ready to become an

insurance agent but when I explained about

the ICICI bank and about the prudential that

is the number one insurance company in U.K.

and has a good market goodwill with ethics,

two of them get agreed with me for becoming

the agent of ICICI prudential.

LEARNING’S

Based on the work done in the company major findings of the study have

been highlighted below….

Most of the people are satisfied with the

extent of their life insurance cover. They

are not interested in buying more life

insurance.

People do not consider life insurance as a

good savings because of low returns.

As life insurance is a long-term contract.

Maximum people do not have faith on Private

life insurance companies, they still prefer

LIC. Because of less advertising not many

people are aware about private life

insurance companies.

Most of the people do not know about broker,

corporate agents and banc assurance, they

rely on their agents only

The most preferred type of plan is money

back. The reason being availability of funds

after every five years, which can be used for

paying further premium, thus saving the

regular income.

Some people have no idea about what type of

cover they have.

Most of the people feel that life insurance

is essential but they think returns are low.

Some people have their doubts on the

credibility and long stay of private

insurance companies.

SUGGESTIONS

Advertising of the insurance product shouldstress on the need of security.

Insurance should be popularized as the meansof securing future rather than saving tax.

New entrants should come out with innovativeriders.

Policies should be issued quickly and withless formalities

Other service should also be improved.

Newspaper/Magazines and television are themost effective medium of advertising lifeinsurance.

Insurance agents should be well trained.

��

��

��R E S E A R C H M E T H O D O L O G Y

��

PRIMARY OBJECTIVES

To study the awareness amongst the people on

life insurance products.

To study the reasons for buying life

insurance products and classify the target

buyer in terms of income and age

To know the type of life cover most preferredby the public

To find out what policies ICICI prudential isproviding

To find out what are the benefits of each ofthe policy

To find out the working process of aninsurance agent

To find out how ICICI prudential recruits theagents.

To understand the functioning of an insurancecompany.

To know the origin and history of lifeinsurance companies

LIMITATIONS OF THE STUDY

It was difficult to get appointment from the

person whom I know because of their busy

schedule.

Since the project had to be completed within

eight weeks, it was too short a time to

convert the prospective buyers into

customers. Since the study involved a through

analysis of the insurance market and relative

study of various players offering the

similar products and that of similar, it

required a dedicated labor in term of both

time and effort. Since the curriculum did not

permit more time, the study had to be very

limited.

��

��

��C A S E S T U D Y

��

In spite of the vast potential, the retirement solutions

category remained virtually untapped by the Indian

Insurance players - until ICICI Prudential decided to build

and explore this hidden goldmine. The following case study

discusses how ICICI Prudential used smart marketing

strategy to exploit this opportunity to its advantage.

ICICI Prudential. Market Scenario With increasing life

expectancy on one hand and rising inflation and medical

costs on the other, the need for planning one’s retirement

was emerging as an important one. However, it was quite

surprising to know only 11 per cent of India’s total working

population was adequately covered for post-retirement life.

This was mainly due to low awareness of and attitudinal

barriers with respect to these issues among consumers.

OPPORTUNITIES

About 90 per cent of the working population in India was

without retirement cover. Of this, a sizeable portion

belonged to the age group of 30-40 yrs - a big market left

unexploited so far. Even the market leader LIC, which has

been in the country for decades, had failed to truly drive

growth of the retirement products category.

Proof being the mere 4.16 per cent contribution of pension

products to its entire portfolio (as of end 2002).

BARRIERS

The task of capturing the unexploited market however, turned

out to be an uphill one. The first barrier was low

awareness of the need for early retirement planning among

consumers. Add to it the consumer’s notion that planning for

retirement starts only in your 50s. The bigger issue

however, was the consumer’s perceptions and fears as far as

retirement was concerned. The word ‘retirement’ itself

brought to mind all the negatives associated with old age –

loss of independence (social, financial and physical),

causing ‘avoidance’ or deferment of decisions regarding the

same.

THE CHALLENGE

To re-position the traditional concept of retirement

planning and thus create relevance for it among the 30-40

yrs age group. To change behavior, inducing consumers to

invest in retirement planning early in life.

CAMPAIGN OBJECTIVES

Bring the concept of planning for retirement into the

consideration set of 30-40 year old working men/ women

thereby creating a new market 50 per cent of pensions

contributions to come from persons below 40 years Sales and

market share targets within six months post campaign (for

the period Sep 2002 to Mar 2003):

Sales target: INR 400 million

Share of total pensions market: 10 per cent

3.Contribution of pensions to portfolio: 20per cent

TARGET AUDIENCE

SEC A, B, 30-40 year old, chief wage earner, who: is at the

prime of his working life, with a higher disposable income

and majority of work life still at hand. Currently thinks

that retirement planning holds very low importance, as

compared to other needs of asset acquisition, child’s

education etc.

CREATIVESTRATEGY

Consumer Insight “Retirement is a long way off – why plan

for it now?”“Retirement means the end of all good things in

life” Creative strategy To a younger target group, for whom

retirement is synonymous with growing old, the strategy was

to offer a fresh perspective by mirroring the never say die

attitude of the 35 yr old. If age doesn’t stop him from

sharing in the joys of life now, why should it stop him

later? Proposition

ICICI Prudential Retirement solutions help you plan early

for retirement, ensuring that you will continue to live life

the way you always wanted to. The advertising message

“Retire from work – not life!”

OTHER COMMUNICATIONPROGRAMS

The laddered task of share gain through changing consumer

attitudes and behaviour, called for a multi-dimensional

communication strategy that went beyond traditional mass

media.

Retirement Solutions Seminars: Through a tie

up with The Times of India, full-page

educative advertorials were released in three

metros inviting consumers for a free seminar

on early retirement planning. Over 2000

consumers attended these seminars.

Direct Marketing Campaign: More than 15

databases were carefully chosen to accurately

target the 30-40 yr old. Customers

of/subscribers to ICICI Bank credit card

holders, Safety Bond holders, Money control

and Myiris are few of the databases that were

used.

Retirement Planner: An educative booklet in

the form of a planner was created explaining

why it made better sense to start planning

for retirement several years in advance. The

mode of distribution was an innovation in

Brand Equity (The Economic Times).

Retirement calculator: A user-friendly

calculator was designed to help customers

calculate the current savings required in

order to meet post-retirement expenses. This

was made available on the brand website and

used extensively as a needs analysis tool at

the time of sale.

MEDIASTRATEGY

The overriding objective of the media strategy was customer

interaction through various touch points using a 24-hour

cycle. So a multi media strategy was developed to contact

the target at every possible touch point.

TV: This was the main for reach, impact anddemonstrate the emotional pay off. For the first month oflaunch a high reach, high frequency plan was implemented,followed up with three months of sustained activity. Theactivity started with 40-second commercials and then movedto 20 and 30 seconds edits aimed at increasing frequency.

Print: Press reinforced the rational benefit of savingearly to cushion your retirement by

highlighting the product’s comprehensive features. Vehicleswere chosen based on the best cost per response i.e. thepublication which would generate the maximum no of callins.

Radio: The new FM channels launched in the previousyear were explored to reach

audiences out of home. The spots were aired so as to get themorning and evening office-

going traffic..

Outdoor: A high visibility-high impact outdoor strategy wasimplemented across 21 cities. Morning traffic sites werespecifically selected to target the office going consumer.

Internet: Used innovatively to seek responses via click-throughs. Financial sites and general interest sites werechosen considering the net is used both in office and at

home.

Direct Marketing: Mailers and brochures played the dual role ofeducating the

Consumer on the rationale behind planningearly for retirement and the advantages ofICICI Pru Retirement Solutions.

Public Relations: Was effectively used toeducate consumers on early retirement

Planning, making them more receptive towardsthe brand’s communication. Competitive

Media Spends: The combined spend of just the top 2 competitorsput to- gether amounted to Rs 16 crores approx.Comparatively the spends on the ICICI Pru campaign was Rs4.8crores.

MEDIA

Television

Newspaper

Consumer Magazine

Radio

Point-of-Purchase

Out-of-Home

Public Relations

Sales Promotion

Consumer Seminars

Evidence Of Results Overwhelming Response

To begin with, the campaign triggered a large number of

consumer response calls and e-mails (35000 calls and 3000

emails).The response rate for mailers sent out (Direct

Marketing) varied from five per cent to 7.5 per cent, far

higher than both domestic and international norms across

categories.

Changing Attitudes

The average age of a person investing in ICICI Pruretirement solutions dropped to 38.5

years.

Sales and Market Shares:

The success of the campaign was not limited to phone calls

alone. The campaign contributed greatly to the

organisation’s topline and bottomline as is evident form the

charts below: 1. Sales achieved for the period Sept ‘02 to

Mar ’03, were INR 740 million as compared to a target of INR

400 million. 2. Market share Gain: The brand increased its

share of pensions market to 23 per cent against target of 10

per cent for the period Sep 2002 to Mar 2003. The table

below which compares ICICI Pru’s share in the pensions

market with the overall life insurance category puts the

campaign’s success in perspective.

��

��

��S W O T A N A L Y S I S

��

Strengths

ICICI PRUDENTIAL belongs to the ICICI group which isone of the largest financialinstitutions in India, ever sinceit inception in 1986 the ICICIgroup has created numerous successstories in whatever business theylanded. It gives ICICI PRUDENTIALan advantage to enjoy the alreadyexisting goodwill of ICICI group.

The ICICI PRUDENTIAL is a joint venturing of prudential

a Uk based insurance company andICICI Bank. Prudential wasestablished more than 150 years agoand the company is listed on theLondon Stock Exchange with a marketcapitalization of approximately $6billion and is a member of theelite FTSE 100 index. In the 2003rankings of the World's 500 largestcorporations by Fortune magazine,Old Mutual climbed 87 places toposition number 366 and was alsolisted as the 14th largestinsurance company in the world. Thejoint venture enjoys the blend of

one of the most experienced andtrusted companies internationallyas well as nationally.

ICICI PRUDENTIAL has one of the lowest NonPerforming Assets (NPA’s) in theindustry, which is .16%. Itprovides the company a strongfinancial stability as well asdepicts whom cohesively the companymanages itself.

ICICI PRUDENTIAL has been rewarded with FAAA ratingby CRISIL and AAA rating by FITCH,this depicts the actual performanceof the organization in terms of itsefficiency. The company spends lesson marketing so it actually hasmore finances available to sustainthe growth of the company andprovide better returns to thecustomers.

ICICI PRUDENTIAL offers the most flexible andinnovative unique products such askcmp etc, which surely gives it acompetitive edge over thecompetitors. The distributionchannel is amazing with a widereach as the company has officesall over India in more than 60cities.

Weakness

The company doesn’t spend much on marketingand it actually may be a reason for not beinga market leader among the private players.

The company has yet to make any significantpresence in the rural sector, as the brandname is yet not famous in the rural India.

The company has a conservative approach andthey believe in steady and very safeprogress, which actually results them to bein a position where they are behind some ofthe more aggressive market players like ICICI

In India the rural market and middle classsociety still don’t have faith in privateinsurers and their genuinity.

Opportunities

The whole rural market is a kind of nichesegment for insurance business. The onlycompany which has some presence in ruralmarket is LIC. So, I is at par with all otherprivate companies and the its an equalcompetition for all, there is an opportunityto make a mark and be the first among theprivate insurers and capture the ruralmarket.

The ICICI being such a big name has anopportunity to grow its insurance businessusing the goodwill of the group companies andthey can even target the customers of eachcompany of their group to get insurance

through them by offering special incentivesor schemes ,such as providing medicalinsurances along with saving accounts intheir banks. etc.

The good showing at the stock markets andgrowing Indian economy enables the ICICIPRUDENTIAL to give better returns tocustomers, specially in unit link schemes.

The Indian mass is getting more aware aboutthe importance of the insurance so they arerelatively more receptive to insuranceschemes, therefore it gives a chance to

� ICICI PRUDENTIAL

The world trends in distribution channel for

selling insurance are changing, these days

55% insurance in Europe is sold through

banks. ICICI has its own bank spread all over

the nation, this can be used to make cross

selling possible.

� THREATS

The rural India and middle class India still

don’t have faith in private insurers.

The ICICI PRUDENTIAL is competing with

private companies which are spending huge

amounts on marketing, so to maintain a

competitive edge with these companies in

terms of acquiring market shares would be a

tough task.

��

��

��R E C O M M E N D A T I O N S

��

There is some of the recommendation we had come up with

while doing this project. It will help to make insurance

more important sector in today’s economy. The need of the

hour is to devise a comprehensive strategy that will help

the firms face the challenges of the future. The financial

services industry around the world over is undergoing a

major transformation. It is very important that trained

marketing professionals who are able to communicate specific

features of the policy should sell the policy.

From our study we could find out that people

are not aware about the policies and features

of insurance. Therefore ICICI are recommended

to shed light on policies and explain the

benefits, thus increasing the awareness.

The penetration of insurance in India is

around 22%. This indicates that a vast

majority of rural population is not covered.

The market player needs to explore this

untapped potential through their marketing

and sales network.

The returns of the policies are not properly

managed and never given in time. So, these

must be looked at.

Pricing of insurance products, as empirically

available in India, shows that pricing is not

in consonance with market realities. Life

Insurance premium is generally perceived, as

being too high while general insurance

(especially motor insurance) is priced too

low.

Some insurance products, which are not

available in India, should, be introduced in

market. There are areas for new product

development: Industry all risk policies,

Large projects risk cover, Risk beyond a

floor level, Extended public and product

liability cover

Insurance companies will also had to get

savvy in distribution. Enhanced marketing

thus will be crucial. Already many companies

have full operation capabilities over a 12-

hour period. Facilities such as customer

service center are already into 24-hour mode.

These will provide services such as motor

vehicle recovery. Technology will also play

an important role on the market. The lines of

distinction between banks insurance companies

and brokerages are getting blurred. The

future seems to belong to financial

supermarkets that will offer a host of

services and products to the consumer. In the

next millennium all these activities would

play a crucial role in the overall

development and maturity of the insurance

industry

��

��

��C O N C L U S I O N S

��

There has been tremendous change in the insurance history.

And with it there has been continuous growth in this sector

both in Indian as well as world context. The opening up of

the insurance sector has changed the whole look of the

industry. While the LIC in order to face the competition is

coming with new strategies.

New players like ICICI Pru are leading the sector due to

their strategic management and tailored made projects. From

our study also we conclude that though the awareness and

people opting for LIC plans are more as compare to ICICI

Pru but the later are gaining momentum in the market day by

day. The primary reasons for buying an insurance policy,

whether life or non-life is to protect us from vagaries of