Adverse Selection as a Policy Instrument: Unraveling Climate Change * Steve Cicala Tufts University David H´ emous University of Zurich Morten Olsen University of Copenhagen Click here for the latest version. December 3, 2021 Abstract This paper applies principles of adverse selection to overcome obstacles that prevent the implementation of Pigouvian policies to internalize externalities. Focusing on negative exter- nalities from production (such as pollution), we evaluate settings in which aggregate emissions are known, but individual contributions are unobserved by the government. We propose giving firms the option to pay a tax on their voluntarily and verifiably disclosed emissions, or pay an output tax based on the average rate of emissions among the undisclosed firms. The certifica- tion of relatively clean firms raises the output-based tax, setting off a process of unraveling in favor of disclosure. We derive sufficient statistics formulas to calculate the welfare of such a program relative to mandatory output or emissions taxes. We find that our mechanism would deliver significant gains over output-based taxation in two empirical applications: methane emissions from oil and gas fields, and carbon emissions from imported steel. * We are grateful to Thom Covert, Meredith Fowlie, Michael Greenstone, Suzi Kerr, Gib Metcalf, Mark Omara, Mar Reguant, James Sallee, Joseph Shapiro, Andrei Shleifer, Allison Stashko, Bob Topel and seminar participants at Tufts, Universit¨ at Bern, the Environmental Defense Fund, UC San Diego, the Midwest EnergyFest, Yale, Harvard, the Utah Winter Business Economics Conference, UC Santa Barbara, UC Berkeley, and the University of Chicago for helpful comments. Iv´ an Higuera-Mendieta provided excellent research assistance. Cicala gratefully acknowledges funding from the 1896 Energy and Climate Fund at the University of Chicago, and along with Olsen thanks the University of Zurich for hospitality. All errors remain our own. e-mail: [email protected], [email protected], [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Adverse Selection as a Policy Instrument:

Unraveling Climate Change∗

Steve Cicala

Tufts University

David Hemous

University of Zurich

Morten Olsen

University of Copenhagen

Click here for the latest version.

December 3, 2021

Abstract

This paper applies principles of adverse selection to overcome obstacles that prevent theimplementation of Pigouvian policies to internalize externalities. Focusing on negative exter-nalities from production (such as pollution), we evaluate settings in which aggregate emissionsare known, but individual contributions are unobserved by the government. We propose givingfirms the option to pay a tax on their voluntarily and verifiably disclosed emissions, or pay anoutput tax based on the average rate of emissions among the undisclosed firms. The certifica-tion of relatively clean firms raises the output-based tax, setting off a process of unraveling infavor of disclosure. We derive sufficient statistics formulas to calculate the welfare of such aprogram relative to mandatory output or emissions taxes. We find that our mechanism woulddeliver significant gains over output-based taxation in two empirical applications: methaneemissions from oil and gas fields, and carbon emissions from imported steel.

∗We are grateful to Thom Covert, Meredith Fowlie, Michael Greenstone, Suzi Kerr, Gib Metcalf, Mark Omara,Mar Reguant, James Sallee, Joseph Shapiro, Andrei Shleifer, Allison Stashko, Bob Topel and seminar participants atTufts, Universitat Bern, the Environmental Defense Fund, UC San Diego, the Midwest EnergyFest, Yale, Harvard,the Utah Winter Business Economics Conference, UC Santa Barbara, UC Berkeley, and the University of Chicagofor helpful comments. Ivan Higuera-Mendieta provided excellent research assistance. Cicala gratefully acknowledgesfunding from the 1896 Energy and Climate Fund at the University of Chicago, and along with Olsen thanks theUniversity of Zurich for hospitality. All errors remain our own. e-mail: [email protected], [email protected],[email protected]

1 Introduction

Uninternalized externalities abound. In spite of the simplicity of economists’ advice when

the magnitude of the harm is known, the obstacles to correcting such market failures are

myriad: political opposition, excessive implementation costs, the presence of havens induced

by competing jurisdictions, among others. In this paper we show the extent to which such

obstacles may be overcome in situations in which damage is caused by heterogenous agents.

We apply results from the literature on mechanism design under asymmetric information as

a policy lever to encourage program participation and voluntary revelation of harm.

We consider situations in which the aggregate level of harm (such as pollution or traffic

congestion) is known by the government, but the exact contributions of specific agents is not.

In such settings it is impossible to levy Pigouvian taxes due to the unobserved sources of

harm. The optimal uniform fee (such as an output tax on producers rather than an emissions

tax) falls short of the first best since the fee does not depend on one’s contribution to the

problem. It also fails to incentivize abatement to reduce damage (Cropper and Oates (1992);

Schmutzler and Goulder (1997); Fullerton et al. (2000); Farrokhi and Lashkaripour (2021)).

We propose creating the option to certify one’s damage, upon which a Pigouvian tax

will be levied, combined with an output-based fee that tracks the average rate of damage

among those choosing not to participate in the certification program.1 This encourages those

who inflict relatively little damage to certify, thus raising the output-based fee paid by non-

participants. This sets off an unraveling in favor of program participation as increasingly

damage-intensive agents seek to separate themselves from the tail of the distribution that

becomes concentrated by adverse selection.

We first develop a closed-economy model in which production is heterogenously associated

with an externality and derive the distance of an optimally-set output tax from the first-best

Pigouvian policy. We approximate with this distance with a sufficient statistics formula that

depends on marginal damages, the slope of the supply curve, variance of emissions, and

monitoring costs. We show how the option to reveal one’s emissions yields welfare objects

that are a linear combination of the outcomes under output and emissions taxes, with weights

equal to the relative variance of emissions under each policy. We also show that, under certain

conditions, the policy maker can achieve the same outcome by only knowing the mean of the

emissions distribution. This is achieved through an algorithm that encourages the gradual

unravelling of the emissions distribution, converging to an equilibrium in which the policy

1This can be calculated because the overall level of harm is observed, and subtracting the contribution ofcertified agents reveals the average contribution among those who remain uncertified.

1

maker has full information on the emissions distribution. We extend the analysis to allow

firms to abate and show that there is a natural complementarity between the two; only

through certification is it worthwhile for firms to abate.

As an empirical application of the closed-economy model, we use our mechanism to

internalize the cost of methane emissions from oil and gas production in the Permian basin

in Texas and New Mexico. The Permian is the source of 30% of U.S. oil production and

10% of natural gas (Administration (2019)). While royalty adders have been proposed to

address the climate externality of embodied carbon in these fuels on federal land (Prest and

Stock (2021)), methane emissions are a thornier problem. Methane is a potent greenhouse

gas that either leaks from the supply chain or is intentionally vented into the atmosphere

in an unmonitored fashion. Alvarez et al. (2018) estimate about 13 million tons of methane

leak from the oil and gas sector annually, for a social cost of about $20B. Nearly 60% of those

emissions occur during production, and in 2018 about 2.7 million metric tons were released

from the Permian basin, for a social cost of $4B (Zhang et al. (2020)). However, emissions

rates across wells are highly heterogeneous (Robertson et al. (2020)). We find that while

a royalty adder levied on production would reduces emissions by about 4%, a tax levied

directly on pollution would reduce emissions by 80%, before abatement. We find that our

sufficient statistics approximations deliver answers that closely follow more data-intensive,

bottom-up calculations. A voluntary emissions tax paired with a rolling output tax would

deliver identical outcomes as a emissions mandatory tax, with about $3B/year in benefits,

even with significant costs of emissions certification. The opt-in policy actually exceeds the

welfare of mandatory taxation as certification costs grow by allowing firms to economize on

the regulatory burden.

We then extend our model to an international setting, focusing on the constraints of

unilateral climate policy. Because greenhouse gases are global pollutants, it is natural that

research on climate policy has focused on international environmental agreements between

sovereign nations who regulate their respective producers.2 Such agreements must overcome

the unilateral incentive to shirk (Barrett (1994)), possibly by punishing countries outside

of the agreement (Nordhaus (2015)). Dynamic considerations also come into play as costly

investments in clean technology create hold-up problems in future negotiations due to their

complementarity with abatement (Beccherle and Tirole (2011); Harstad (2012); Battaglini

and Harstad (2016)). Governments are the key decisionmakers in this paradigm, and only

policies that are individually rational from each country’s perspective are feasible.

2See Chan et al. (2018) for a review.

2

The absence of strong, binding international agreements raises the question of how emis-

sions might be reduced through unilateral policy. The ability of unilateral carbon taxation to

reduce emissions is reduced (and possibly reversed) when production can profitably move to

unregulated jurisdictions, a problem known as ‘leakage’ (Bohm (1993); Copeland and Taylor

(1995); Aldy and Stavins (2012); HA c©mous (2016); Fowlie (2009); Fowlie et al. (2016)).

This prospect strengthens the incentive to shirk on international commitments by simulta-

neously reducing the effectiveness of the tax and increasing the benefits of becoming a haven.

Trade policy in the form of a “Border Carbon Adjustment” (BCA) has been considered the

primary instrument to mitigate the competitive disadvantage caused by taxing one’s own

emissions (Copeland (1996); Metcalf and Weisbach (2009); Elliott et al. (2010, 2013); Larch

and Wanner (2017), see Condon and Ignaciuk (2013) for a literature review). BCAs levy

tariffs based on the average carbon content of production in the country of origin so that

foreign producers (on average) cannot undercut domestic firms. Under such a policy foreign

producers remain effectively outside the reach of the government, as their tax burden is unre-

lated to firm-specific emissions. They face no individual incentives to abate their emissions,

and any pollution reductions depend on price elasticities of demand and supply.3

The goal of our approach in the international setting is to approximate the emissions

reductions that might be achieved with a widely-adopted price on carbon, but without re-

quiring the legally-binding international agreements that have proven elusive to date. To do

so, we focus on the direct interactions between a government and firms whose disclosures of

emissions are voluntary. International sovereignty may restrict what governments can man-

date of foreign firms, but does not foreclose the possibility of creating incentives to shape

their behavior. We do this by providing firms with the option to certify their emissions, and

basing the default rate on the average emissions of uncertified firms. This recasts the problem

of jurisdiction into one of screening, in which clean firms wish to separate themselves from

more intensive polluters (Spence (1973); Stiglitz (1975)). This separation causes the uncer-

tified mean to rise, setting off a process of unraveling that encourages further certification

(Akerlof (1970)).

We show the conditions under which the unraveling mechanism is preferable to a unilat-

eral domestic carbon tax, or a tax combined with a BCA. As an empirical application, we

consider the case of international trade in steel, an energy-intensive, trade-exposed sector

3Markusen (1975) and Hoel (1996) derive the optimal tariff in the presence of transboundary pollution.As highlighted by Keen and Kotsogiannis (2014) and Balistreri, Kaffine and Yonezawa (2019), an optimalenvironmental tariff generally differs from the BCA formula (even if a BCA were able to distinguish betweenthe carbon contents of different imports and even in the absence of terms of trade effects).

3

that is central to environmental trade policy (Miller and Boak (2021)). We consider trade

policy between the OECD and Brazil, a major steel exporter. Using the sufficient statis-

tics formulas we develop, we estimate that an optimally-implemented certification program

would achieve nearly 75% of the welfare gains of a universal carbon tax. However, we also

find that unrestricted access to such a program would create significant ‘backfilling’ wherein

the the dirtiest firms would expand their output to serve the untaxed foreign market. This

reduces the welfare benefits of certification, making the unrestricted program slightly inferior

to a standard border carbon adjustment. This example highlights the countervailing forces

that limit a government’s ability to reduce externalities outside of its jurisdiction, while also

presenting a mechanism to productively expand its reach.

The combination of optional disclosure and a rolling default creates a policy that mimics

the strategy that has been applied in private markets to ensure quality (Jovanovic (1982);

Grossman (1981); Milgrom and Roberts (1986); Milgrom (2008). See Dranove and Jin (2010)

for a review). In these settings firms voluntarily provide warranties or submit to audits in

order to separate themselves from low-quality producers. Even relatively lower-quality firms

become willing to make such disclosures to separate themselves from the absolute worst

offenders when consumers update their beliefs regarding those who decline to disclose (Jin

and Leslie (2003); Jin (2005); Lewis (2011)). It has also been used by firms to improve risk

selection for credit (Einav et al. (2012)), improve safety (Viscusi (1978); Hubbard (2000);

Jin and Vasserman (2019)), and has been suggested to encourage more efficient electricity

consumption (Borenstein (2005, 2013)) and fisheries management (Holzer (2015)). To our

knowledge this is the first paper to apply these principles to overcome obstacles to the

implementation of Pigouvian policies.

The use of screening mechanisms in public policy has been successfully applied to im-

prove the targeting of recipients of public benefits (Alatas et al. (2016); Finkelstein and

Notowidigdo (2019); Deshpande and Li (2019)). In such settings the government creates

hurdles so uptake is limited to those who value benefits more than the ordeal of enrollment.

These policies typically do not entail unraveling as the government is is free to choose the

magnitude of the enrollment ordeal so that the optimal point of separation is achieved im-

mediately (Kleven and Kopczuk (2011); Besley and Coate (1992); Nichols and Zeckhauser

(1982); Nichols et al. (1971)): The costs or benefits of non-participation are not program-

matically adjusted with the extent of participation. In our setting this would be analogous to

the government choosing its preferred carbon content of uncertified imports, which is likely

4

to run afoul of strategic trade considerations.4

There is a long tradition of regulation under asymmetric information in the mechanism

design literature (Baron and Myerson (1982); Laffont and Tirole (1993)). In the pollution

context, the regulator seeks to elicit information on abatement costs (Kwerel (1977); Roberts

and Spence (1976); Dasgupta et al. (1980); Baron (1985); Laffont (1994)) and must design

a policy schedule that elicits truthful revelation. In these settings, as in the context of

non-point source pollution, the lack of verifiability is the key constraint on the regulator

(Segerson (1988); Xepapadeas (1991); Laffont (1994); Xepapadeas (1995), among others.

For a review see Xepapadeas (2011)). While emissions remain unobserved at uncertified

firms, our focus on an optional, verifiable revelation of emissions converts the problem into

a traditional point-source setting in which firms face incentives to abate. Recent work on

voluntary environmental regulation notes the improved enforcement targeting for uncertified

firms, but does not unravel non-participation with changing in audit probabilities (Foster

and Gutierrez (2013, 2016)).

Organizationally, the paper separates the analysis between domestic and international

settings. In each setting we develop a theoretical model, and then apply the results from the

model to an empirical setting. The final section concludes.

2 Unraveling in the Domestic Case

To focus on the central issue of disclosure, we first consider a simplified setting of a closed

economy in which firms differ only in their emission rates. Throughout this section we focus

on a simple partial equilibrium model with an externality, though our approach would also

apply to a broader class of models. The government knows the full distribution of emis-

sions, but not those of individual firms unless they choose to certify. We take as given that

mandatory certification is not possible and characterize the welfare benefits of an optional

certification program.

First, we derive “sufficient statistics” in the sense of approximations to changes in wel-

fare that can be expressed through simple objects such as emissions variances and supply

elasticities. We begin by solving a benchmark model for any level of certification, and then

derive the optimal level of certification. We then weaken the information available to the

regulator and show the program may be implemented knowing only the first moment of the

4At the extreme, the government could simply prohibit imports from firms whose emissions are uncertified.This is not without precedent—the U.S. Food and Drug Administration mandates access for inspectors atfacilities abroad for any firm wishing to sell food or pharmaceuticals in the US (Federal Food, Drug andCosmetic Act, Section 807 (b) as amended by Section 306 of the FDA Food Safety Modernization Act). Thebasis of the jurisdiction problem we address is that such mandates are infeasible with respect to emissions.

5

emissions distribution. We conclude the section with a series of extensions to the benchmark

model: allowing for abatement, heterogeneous productivity, and adjustments that only occur

through entry and exit. These extensions yield minor adjustments to the exact expressions

of the benchmark model, but share a common fundamental structure.

2.1 Baseline model

We consider a closed economy and focus on a specific industry that produces a homogeneous

polluting good under perfect competition. A representative agent has preferences over this

good, represented by the following quasi-linear utility function:

U = C0 + u(C)− vG,

where C is total consumption of the polluting good and C0 is the consumption of an outside

good. The price of the outside good is normalized to 1. G denotes emissions from the

production of good C. The marginal social cost of emissions is v. The outside good does not

pollute.

The polluting good is produced by an (exogenous) mass 1 of firms who operate under

perfect competition. Firms have the same strictly convex cost function c(q) but vary in the

extent to which they pollute. The emissions rate per unit produced is denoted by e and

follows the cdf Ψ(e), with full support and corresponding pdf of ψ(e) > 0, on the domain

[e, e] where e ≥ 0 and e may be infinite. Though the overall distribution of emissions, Ψ,

and the production of each firm is observable, the emissions of an individual firm are private

information (unless the firm is certified as described below).

2.2 Equilibrium with an output tax or emission tax

In the following, we distinguish between a tax on emissions and one on output. First, consider

an output tax, t, which can be implemented even when individual emissions are not observed.

Let the market price be p and solve the firm’s problem in a decentralized equilibrium to get:

p = c′(q) + t. (1)

This defines a supply function q = s(p − t). With a mass 1 of firms this is also total

production, Q. The resulting profit function follows as π(p− t) = (p− t)s(p− t)−c(s(p− t)).The supply curve is upward-sloping by the convexity of the cost function and the profit

function is increasing in p − t. Utility maximization gives: u′(C) = p which together with

Q(p− t) = s(p− t) and C = Q defines an equilibrium price, p, and quantity, Q. Emissions

6

are given by:

G =

∫ e

e

s(p− t)eψ(e)de = s(p− t)E(e) (2)

Next, and in anticipation of the discussion of certification below, we solve for a setup in

which emissions are observable and taxed at τ . This gives an individual supply function of

s(p− τe) and aggregate supply and emissions of:

Q =

∫ e

e

s(p− τe)ψ(e)de = E [s(p− τe)] and G = E [es(p− τe)] (3)

The social planner would set t = vE(e) when emissions are not observed and τ = v when

emissions are observable. In the following, we solve for an equilibrium in which firms can

certify and be taxed based on their individual emissions.

2.3 Equilibrium with certification

We now introduce voluntary certification of emissions, in which a firm can choose between

two tax settings. If the firm chooses to (verifiably) reveal its level of emissions, e, it is

taxed at τe (where we do not necessarily impose that τ equals the social cost of carbon,

v). If the firm chooses not to reveal its level of emissions, it is taxed at the mean level of

emissions of the firms who do not certify t = τE(e|R), where R denotes the set of firms

who have not certified. We will keep this relationship between τ and t as an assumption

throughout most of the paper. We consider it a natural starting point since our interest lies

with the reallocation of taxes based on better information of underlying emissions and not

with changing the overall tax rates. Second, when the price of certification is set optimally

as in Section 2.4, t = τE(e|R) is in fact optimal.

When presenting this choice to firms, the policy maker must calculate R ex ante based on

knowledge of the distribution of emissions, Ψ(e). Here we assume that the policy maker can

do that. The total cost to a firm of certification equals the technical cost of certification, in

the form of a third-party expert, an objective monitoring system etc., F > 0 and a potential

additional tax/subsidy that the government might impose, f ≶ 0. In an equilibrium in which

some firms certify, and others do not, an indifferent firm with emissions level e is defined by:

π(p− τ e)− (F + f) = π(p− t). (4)

Since the left-hand side is decreasing in e, all firms with e < e certify and firms with e > e

do not. Consequently f is a tool to determine e. The resulting tax rate on output for firms

7

who do not certify is:

t = τE[e|e > e],

and where importantly, ∂t/∂e > 0, that is the rate at which uncertified firms are taxed is

increasing in the number of certified firms.

To facilitate the discussion below, we introduce ε, which is equal to the emissions rate at

which a firm is effectively taxed:

ε =

e

E(e|e > e)

if e ≤ e

if e > e,(5)

where E(ε) = E(e). Production by firms who do not certify is s(p − τE(e|e > e)) and for

those who do certify it is s(p− τe) such that total production i

Q =

∫ e

e

s(p− τe)ψ(e)de+ (1−Ψ(e))s(p− τE(e|e > e)) = E(s(p− τε)),

with corresponding emissions of:

G = E [εs(p− τε)] . (6)

The equilibrium price follows from market clearing, C = Q, and utility maximization,

u′(C) = p. We consider sufficient conditions for this equilibrium to be unique in Appendix

A. These include i) E[e|e > e] − e is decreasing in e and ii) s(· ) is weakly convex or τ is

small. The condition on E[e|e > e] is satisfied for most frequently used distributions and

below we will rely on first order approximations in which case ii) is satisfied.

For any variable x we let xV denote its value with certification and xU its value under

the output tax without certification. Comparing equations (6) and (2) gives the difference

in emissions between the two tax systems:

Lemma 1. The difference between emissions under voluntary certification, GV , and the

output tax, GU , is given by:

GV −GU = Cov[ε, s(pV − τε

)]+ E (e)

{E[s(pV − τε

)]− s

(pU − τE (e)

)}, (7)

where pV and pU are the equilibrium prices under certification and the output tax, respectively.

The effect of certification on emissions is generally ambiguous. However, emissions decline

8

when s is weakly convex and es(pV − τe) is concave in e. This is satisfied for linear supply

or small τ .

The equation in Lemma 1 consists of two terms. First, a reduction in emissions from a

reallocation effect: certification allows the reallocation of production from firms with high

emissions to those with low emissions. This is captured by the negative covariance term. The

second term combines two effects: i) a classical rebound effect as certified firms are taxed at a

lower rate and increase production and with it emissions and ii) a price effect in that possible

increases in the equilibrium price could further increase production. The condititions in the

lemma rule out these severe cases of rebound. They are automatically satisfied for linear

supply or small τ , in which case certification lowers total emissions: certification lowers the

tax rate for some firms and raises it for others, keeping the average tax rate constant at

τE(ε) = τE(e). With linear supply curves, total production and hence the market-clearing

price is unaffected by certification (when all firms remain in operation). With a reallocation

towards less polluting firms, but no change in aggregate production, total emissions must

decline.5

The following proposition gives the difference in welfare between the two settings for a

given tax rate, τ :

Proposition 1. The difference between social welfare with certification and the output tax

is given by:

W V −WU = E(π(pV − τε

))− π

(pV − τE (e)

)︸ ︷︷ ︸reallocation effect

+

∫ pV

pU(s (p− τE (e))−D (p)) dp︸ ︷︷ ︸

price effect

− (v − τ)(GV −GU

)︸ ︷︷ ︸untaxed emissions effect

− FΨ (e) . (8)

Where

a) The “reallocation effect” and the “price effect” are always weakly positive.

b) The “untaxed emissions effect” is zero for v = τ , and otherwise depends on whether

rising (falling) emissions are over (under) taxed relative to Pigouvian levels.

5Alternatively, consider a convex supply function, which implies that for a given price, total supply mustincrease with certification, so that the equilibrium price declines (pV < pU ). As a result, es(pV − τe) <es(pU − τe). In addition, when es(pV − τe) is concave in e an application of Jensen’s inequality ensures thatoverall emissions decline.

9

c) W V −WU + FΨ(e) is of ambiguous sign but when v ≥ τ it is positive when supply

curves are linear or for small τ .

Proof. Proof in Appendix 1.

The first term in equation (8) is a reallocation effect and captures the increase in profits

from a reallocation of production from firms with higher taxes to those with lower. ε is the

effective level of emission taxation under certification such that E[π(pV −τε)]−π(pV −τE(e))

is the average gain for firms. This effect is always positive.

Next, consider the untaxed emissions effect which captures the welfare effects of changing

emissions. These are zero when emissions are taxed at the Pigovian level, τ = v, whereas if

taxes are lower than this, there are net welfare gains from emissions reductions, which will

occur depending on the conditions of Lemma 1. That is, if τ < v, and the rebound effect

is not too strong, the untaxed emissions effect will be positive. FΨ(e) captures the fraction

Ψ(e) of firms and the F resources required to certify them.

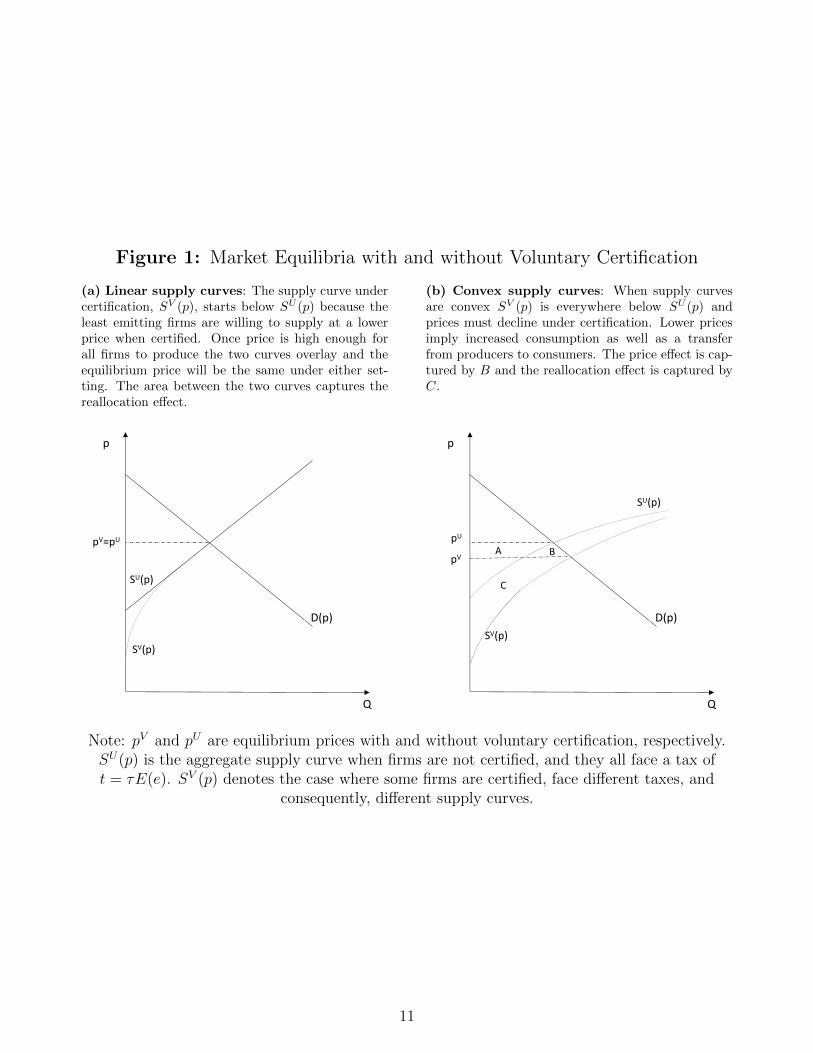

Figure 1 illustrates how reallocation and price effects depend on the concavity of the

supply function. SV (p) always intersects the y-axis lower than the SU(p) curve because

firms with low emissions face lower taxes. For sufficiently low prices, the number of firms

producing is increasing along SV (p). When the price is high enough for all firms to produce,

the two curves overlap when supply curves are linear, as in Panel (a). In this region, the

positive supply effect for firms with lower taxes is exactly matched by the negative effect for

firms facing a higher tax. Total quantities are unchanged and there is no price effect. The

reallocation effect is measured by the increase in producer surplus, represented by the area

between SV (p) and SU(p).

When supply curves are not linear, the price need not remain constant. Panel b considers

the case of convex supply curves.6 Convexity implies that the firms that face lower taxes

will increase their production by more than the firms who face higher taxes will reduce their

production. Consequently, the supply curve will be to the right. Again, the reallocation

effect is captured by the area between the curves (C), whereas the price effect is captured

by B. The area A is just a reallocation from producers to consumers and does not feature

in aggregate welfare changes.

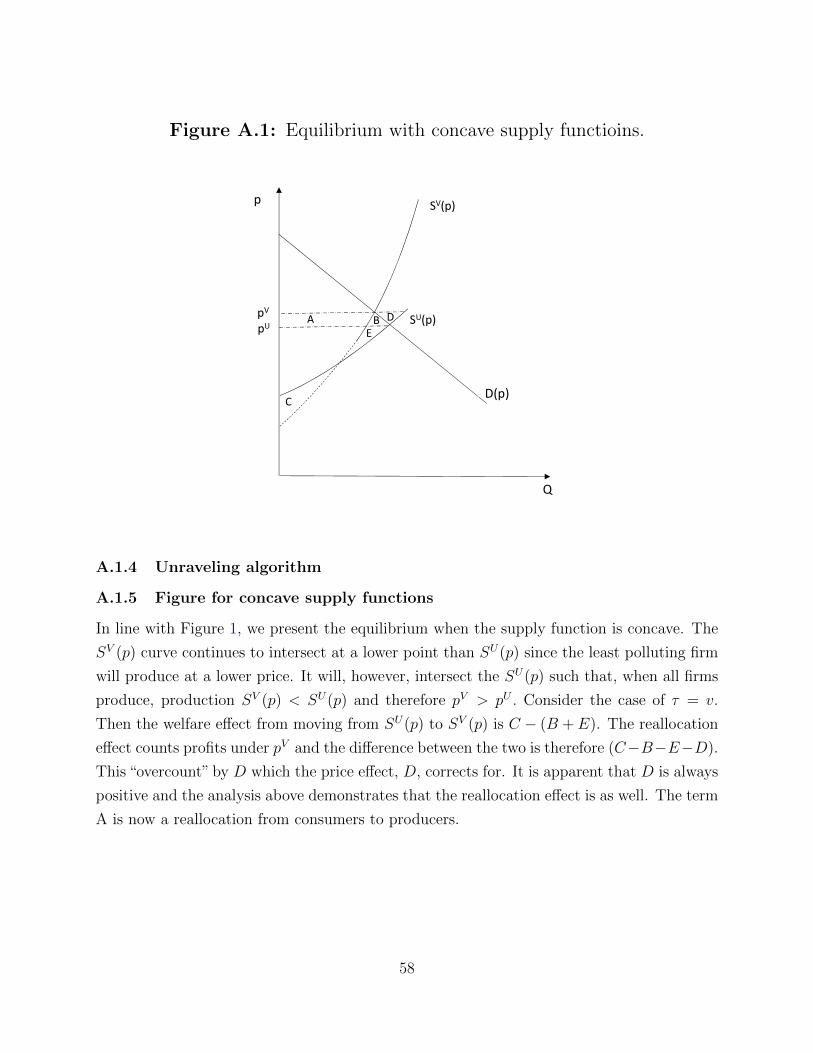

6Section A.1.5 in the Appendix considers the opposite case in which supply is concave and the priceincreases. Proposition 1 still holds, but the allocation of welfare between producers and consumers is different.

10

Figure 1: Market Equilibria with and without Voluntary Certification

(a) Linear supply curves: The supply curve undercertification, SV (p), starts below SU (p) because theleast emitting firms are willing to supply at a lowerprice when certified. Once price is high enough forall firms to produce the two curves overlay and theequilibrium price will be the same under either set-ting. The area between the two curves captures thereallocation effect.

D(p)

SU(p)

SV(p)

p

Q

pV=pU

(b) Convex supply curves: When supply curvesare convex SV (p) is everywhere below SU (p) andprices must decline under certification. Lower pricesimply increased consumption as well as a transferfrom producers to consumers. The price effect is cap-tured by B and the reallocation effect is captured byC.

SU(p)

SV(p)

pU

pVA B

C

D(p)

Q

p

Note: pV and pU are equilibrium prices with and without voluntary certification, respectively.SU(p) is the aggregate supply curve when firms are not certified, and they all face a tax oft = τE(e). SV (p) denotes the case where some firms are certified, face different taxes, and

consequently, different supply curves.

11

As can be intuited from Panel b, the price effect is of a higher order than the other terms.

Our goal is to establish “sufficient statistics” for changes in emissions and welfare that can be

easily evaluated using readily available data. In this pursuit, and with little loss of generality,

we will consider first-order approximations in τ in much of the analysis to come. This implies

that the price effect is zero and the reallocation effects and untaxed emission effects are both

positive (for τ ≤ v).

Corollary 1 considers such approximations. We assume that taxes, τ , and the social costs

of emissions, v, are small relative to prices. We then conduct Taylor expansions around τ = 0

(where v is of the same order).

Corollary 1. The expression W V −WU in Proposition 1 can be written as:

W V −WU =(v − τ

2

)s′ (p0)V ar (ε) τ − FΨ (e) + o

(τ 2), (9)

with a difference in emissions of:

GV −GU = −s′ (p0) τV ar (ε) + o(τ),

where p0 is the price when τ = 0. It holds that:

a) V ar(ε) = 0 if e = e and ∂V ar(ε)/∂e > 0.

b) W V −WU + FΨ(e) is positive if τ < 2v (to a second order).

c) GV −GU is negative (to a first order).7

d) These expressions hold exactly when supply curves are linear.

Proof. Appendix A.1.2.

Corollary 1 demonstrates that there is no price effect at first order and the primary

driver of the welfare consequences of certification come from the shift in production from

more to less polluting firms. With a constant production but a shift towards firms with

fewer emissions, total emissions are sure to decline. Even if average emissions were already

taxed efficiently, τ = v, total welfare increases because production is reallocated towards less

polluting firms. The size of this reallocation depends on the supply response, s′(p0), and the

variance of the taxed emissions rate, V ar(ε). When τ = v the entire welfare benefit from the

certification program accrues to firms (at first order). This result, however, depends on the

7When τ > v emissions are taxed excessively. The costs of doing so are quadratic in the deviations fromthe optimal tax, implying a quadratic distortion of increasingly high taxes on the dirtier firms. When τ > 2vthis effect dominates and causes negative welfare effects.

12

assumption of an exogenous unit mass of firms. Appendix A.1.6 demonstrates that if we allow

for endogenous entry of firms, all additional effects are of higher order and the expressions

of Corollary 1 remain unchanged, but the entire welfare benefit accrues to consumers.8

A natural question to ask is how far welfare of the voluntary certification in Proposition

1 is from the welfare that would be obtained if firm emission rates were known and taxable

(without necessarily imposing τ = v) (Jacobsen et al., 2020). Labeling such an equilibrium

with W FI for “full information” we find (at second order)

W V =V ar (ε)

V ar (e)W FI +WU

(1− V ar (ε)

V ar (e)

)− FΨ (e) + o(τ 2). (10)

By construction V ar(ε) ≤ V ar(e) so welfare under voluntary certification (gross of cer-

tification costs) is a weighted average of welfare with no certification, WU , and with full

information, W FI . The weight reflects the relative variance of the effectively-taxed emission

rate, ε, and the actual emission rates, e. This means that greater benefits of voluntary certi-

fication accrue as a larger share of the variance of emissions certify. Having additional firms

certify is only beneficial insofar as they represent a higher share of the emissions variance.

2.4 Optimal policy

In the following, we solve for the optimal combination of the three available policy tools: the

emissions tax on certified firms, τ , the output tax on uncertified firms, t, and the subsidy/tax

on certification, f . Appendix A.1.3 shows that these are

τ = v,

t = vE(e|e > e),

f = vE (e− e|e > e) s (p− vE (e|e > e)) > 0. (11)

The condition τ = v and t = vE(e|e > e) recover the standard Pigovian result that

emissions ought to be taxed at their (expected) social cost. Equation (11) shows that cer-

tification is excessive when τ and t are set optimally, and should be taxed. To see why, we

employ the first order condition with respect to f . This can equivalently be written wrt. to

8Specifically, we specify a free entry condition that E(π(ε)) = FE , where a slight abuse of notationpermits us to let π(ε) denote the profits of a firm with emissions rate ε. In this case, the mass of firms N isendogenous. The expressions in Corollary 1 take this into account by replacing s′(p0) with N0s

′(p0) whereN0 is the mass of firms under p0.

13

e as:

π (p− ve)− π (p− vE (e|e > e))− vE (e− e|e > e) s (p− vE (e|e > e))− F = 0. (12)

Increased certification implies higher profits for the marginal firm, e, captured by the first

two terms in the expression. In addition, the quantity tax on uncertified firms goes up, which

has a negative effect on profits for the uncertified firms. The third captures this whereas

the fourth term captures the social cost of certification, F. As τ = v emissions are taxed

correctly, and there is no marginal gain from changes to emissions. Comparing equation

(12) with the indifference condition of when firms certify (equation 4) we get Equation (11).

Since the certifying firms do not internalize the costs they impose on still non-certified firms,

the optimal policy requires a tax.

These considerations relate to the size of F and f . Corollary 1 does not specify the order

of F and f . Consider f = 0 (no tax or subsidy on certification). The gains from certification

are first order, so if F is first order, some firms will certify. Since welfare gains are second

order, equation (9) then delivers negative welfare benefits. If F is second order, almost all

firms certify. Neither of these is efficient, as just discussed. An f > 0 of first order according

to equation (11) ensures the optimal certification.

2.5 An “Unraveling” Algorithm

Having solved for the decentralized equilibrium and the social planner’s allocation, we take

a step back and assess the informational requirements needed to implement such a policy.

Whereas equation (9) gives an intuitive result of the welfare gains based on statistics that

are relatively easily obtained — such as the variance of emission rates and supply elasticities

— the implementation requires complete information on the distribution of e, which is rarely

available. We show the conditions under which a given “algorithm” can achieve a comparable

outcome without complete information on the distribution of e.

We assume that neither firms nor the government knows the distribution of emissions

rates, but they do observe the average emissions rate (through aggregated accounts or changes

in ambient pollution, for example). We further assume for this section that e <∞. Initially,

certification is not available and the government imposes an output tax t0 = τE(e). We

assume that the government introduces certification which allows firms to pay the emission

tax τ at some certification cost F . Since the government does not know the distribution Ψ(e),

it cannot predict the eventual threshold e and therefore cannot implement the equilibrium

described above by immediately announcing a new output tax τE (e|e > e).

14

Consider instead an iterative process where the government allows firms to certify at

increasing levels of emissions rates. That is, the government asks if firms with emissions

rate e want to certify and only those firms are allowed to do so. If they do, the level of

certification increases and the procedure starts again. The government continuously adjusts

the output tax as the emissions distribution is revealed. We show that we obtain a Nash

equilibrium when firms decide on certification as if they were the last ones to certify with

the information available at that point in time.

Assume that all firms with an emissions rate below e have certified and consider the

decision facing a firm with emissions rate e. The firm will certify if:

g (e) ≡ π (p (e)− τ e)− π (p (e)− τE (e|e > e))− F ≥ 0,

where p (e) is the price that would prevail on markets should the certification stop here and

the threshold be e = e. Since the distribution up to e has been revealed publicly and since

E (e) is known, both the government and the firm can compute E (e|e > e). Assuming that

g (e) > 0, then at least some firms will certify. Furthermore, with a bounded distribution,

g (e) = −F so not all firms will certify as long as F > 0. As firms decide sequentially to

certify, the process will continue up to the smallest emissions rate for which g switches sign,

which we denote e (which also corresponds to a laissez-faire equilibrium when the government

knows the full distribution ψ).

This leads to a Nash equilibrium because for firms with a lower emissions rate, e < e,

π (p (e)− τ e)− π (p (e)− τE (e|e > e))− F > g (e) = 0,

so that none of these firms would benefit from deviating from certification at the equilibrium.

Since g becomes negative just after e, firms with emission rate e + de, decide not to certify

and would indeed be worse off otherwise. Firms with a higher emission rate e > e, will not

certify either. Hence, even if the government does not know the distribution of Ψ(e) it can

implement an algorithm where the optimal certification decisions of firms gradually reveal

the shape of the distribution up until e.

The analysis can be straightforwardly extended to the social optimum if the government

continuously adjusts the certification tax f = τ (E (e|e > e)− e) s (p(e)− τE (e|e > e)) with

the information available.

15

2.6 Extensions

The following sections add two dimensions of flexibility to the baseline model: abatement

and heterogeneous productivity (Appendix A.1.6 allows for free entry). The extensions fit

easily in the framework presented so far, and we present them with a focus on the added

terms to emissions and welfare. The full explicit expressions are given in Appendix A.1.6.

Abatement

We keep the same structure as above but allow firms to spend b(a) per unit produced to

reduce their per-unit emissions by a. We require: b′(a) > 0 and b′′(a) > 0 for a > 0. For

simplicity, we further add b′(0) = b(0) = 0. Pre-abatement emissions are still distributed

according to Ψ(e), and a certified firm i pays an emission tax on e(i)− a(i) instead of e(i).

We continue to define ε in equation (5) as the pre-abatement emissions rate for certified

firms and the conditional mean of emissions for uncertified firms. Abatement investments

are not observable and non-certified firms consequently have no economic incentive to abate.

Hence, in an equilibrium without certification, no abatement takes place. Certified firms, in

contrast, do abate a strictly positive amount. They solve the problem:

maxq,apq − c(q)− τ(e− a)q − b(a)q

which leads to a common abatement level, a∗, among all firms that certify of a∗ = b′−1(τ).

We let A(τ) ≡ τa∗(τ) − b(a∗(τ)) > 0 denote the savings per unit of production due to

abatement. If e < a some firms sequester emissions. Individual supply functions of certified

firms with emissions rate e takes the form:

q = s (p− τe+ A(τ)) ,

such that supply is higher under abatement. The expression for changes in total emissions

with abatement takes the structure of Lemma 1 but adds two additional terms:

−a∗Ψ(e)E[s(pV − τe+ A(τ)

)|e < e

]+Ψ(e)E

{e[s(pV − τe+ A(τ)

)− s

(pV − τe

)]|e ≤ e

},

(13)

where (with slight misuse of notation) pV now represents the equilibrium price under cer-

tification with abatement. The first term in expression (13) is the direct impact of a mass

of Ψ(e) certifying and thereby abating their emissions by a∗. At the same time certification

lowers their tax burden, which yields a supply response analogous to a rebound effect on the

16

quantity produced. This additional effect pulls in the direction of higher emissions. If s is

convex and es(pV − τe) is increasing and weakly concave in e, then emissions must decline.

If τ is small emissions must decline as well.

Similarly, we can establish a result on welfare analogous to that of Proposition 1. Em-

bedded in equation (13) are the additional negative effects on emissions which increases the

positive untaxed emissions effect when v > τ . In addition, we get:

Ψ (e)(E(π(pV − τe+ A(τ)

)− π

(pV − τe

)|e ≤ e

)).

This captures the increase in profits to firms that receive a higher net price after abatement.

This benefit accrues only to the share of firms Ψ(e) that certify. For given price pV , profit

maximization ensures that this term is positive.

Finally, we continue our analysis using Taylor expansions and derive the following corol-

lary to Proposition 1:

Corollary 2. To a second-order approximation, the difference in social welfare when moving

to voluntary certification from an output tax in the presence of abatement is

W V −WU = τ(v − τ

2

)(s′(p0)V ar(ε) +

s(p0)Ψ (e)

b′′(0)

)− FΨ (e) + o

(τ 2),

where W V −WU+FΨ(e) is positive.

Corollary 2 takes advantage of the fact that to a first order e remains unchanged with

abatement and consequently we can add a single term to equation (9) from Corollary 1. b′′(0)

captures the curvature in the abatement costs. By assumption, it is always profitable to do

some abatement and a low curvature of the abatement function (b′′(0)), implies that, to a

first order, the optimal abatement level will be higher. Abatement benefits are proportional

to total production by the firms that abate: s (p0) Ψ(e). For this effect to be positive requires

τ < 2v (the reasoning is analogous to that of footnote 7).9

9Analogously to equation (10), to a first order, we can write welfare under certification with abatement asa weighted average of welfare without certification, WU , and welfare with full information under abatement,WFIA as:

WV = WFIAω + (1− ω)WU − FΨ(e) + o(τ2),

where ω =(V ar (ε) + s(p0)

s′(p0)b′′(0)Ψ (e)

)/(V ar (e) + s(p0)

s′(p0)b′′(0)

). Welfare under certification (gross of certi-

fication costs) continues to be a weighted average of the welfare with complete information and with no

information, but with the added term, s(p0)s′(p0)b′′(0)

Ψ(e) which captures (to a first order) the amount of abate-

ment done with certification.

17

Heterogeneous Productivity

In the following we again preclude abatement, but we allow firms to differ in their level of

productivity. In particular, firm i has costs of production of c(q)/ϕi, where c(q) has the

same properties as the cost function in Section 2 but ϕi > 0 differs across firms. We let

Ψ(e, ϕ) denote the joint distribution and allow unrestricted covariance between e and ϕ. We

consider supply functions with constant elasticity such that a firm i that certifies produces

qi = s0 [ϕi(p− τei)]α and the uncertified firms produce qu = s0 [ϕi(p− t)]α, where t is τ

times total emissions of uncertified firms divided by total production by uncertified firms.

This is also the optimal quantity tax rate under no certification.10

In this setup, firms differ both in their productivity and their emissions. Therefore, the

cut-off e of Section 2 is replaced by a cut-off function e(ϕ) which depends positively on

productivity.11 To a first order, the expressions for the change in emissions and welfare of

Corollary 2 take the same form, except V ar(ε) is replaced by the output-weighted variance

of emissions:˜V ar(ε) =

∫ϕ

∫ε

(ε− E(ε))2ψ(ϕ, ε)dεdϕ,

where ψ(ϕ, ε) = ϕαψ(ϕ, ε)/(∫

ϕ

∫εϕαψ(ϕ, ε)dεdϕ

)is a density distribution rescaled by out-

put (proportional to ϕα at price p0) such that E(ε) equals the average emissions per unit

without certification:

E(ε) =

∫ϕ

∫ε

εψ(ϕ, ε)dεdϕ = GU/SU

Intuitively, the reallocation effect is still the driving force behind our results, though firms’

emissions are now weighted by their size.

2.7 Adjustments along the extensive margin

The model presented above considered reallocation on the intensive margin. For complete-

ness, we consider situations in which the only margin of adjustment is whether to produce

or not. To focus on the supply side we consider an exogenous price p such that consumer

welfare (excluding emissions) is constant.12

10Although our approach could also be used with other supply functions, the analysis becomes morecomplicated, in particular because t is no longer the optimal quantity tax.

11Specifically, equation 4 is replaced by: 1ϕπ(ϕ(p − τ e(ϕ))) − (F + f) = 1

ϕπ(ϕ(p − t)) where π() is as

previously defined. This defines e(ϕ) where the cut-off emission rate depends positively on productivitybecause production increases with productivity whereas the certification cost, F + f , does not.

12This implies that we deviate from our assumption of a closed economy. Section 3 focuses explicitly on aninternational case, and here we do not explicitly model alternative consumers or suppliers. This approach is

18

Consider a mass 1 of potential firms each characterized by potential production q, entry

costs c and emissions, e. These are distributed according to Ψ(c, q, e) with a corresponding

pdf of ψ. The domain is [c, c] × [q, q] × [e, e] with weakly positive lower bounds and finite

upper bounds and Ψ has support everywhere. It will further be convenient to define the

unconditional distribution of e, ψe(e), and the two conditional distributions ψc(c|e, q) and

ψq(q|e). In the following we present only results and keep derivations in Appendix A.2.

Firms face a uniform price of p. In laissez-faire, a firm i produces if its individual draw

satisfies pqi ≥ ci. When a uniform quantity tax is imposed, this condition becomes (p−t)qi ≥ci.

Total production and emissions are then given by:

S(p− t) =

∫q1(p−t)q≥cdΨ(c, q, e), (14)

G(p− t) =

∫eq1(p−t)q≥cdΨ(c, q, e),

where 1(p−t)q≥c is the indicator function and it is understood that when not otherwise specified

integrals are over the full support of (c, q, e).

The slope of the aggregate supply curve is:

S ′(p− t) =

∫e

ψe(e)

∫q

q2ψc((p− t)q|e, q)ψq(q|e)dqde. (15)

The slope of the aggregate emission curve, G′(p − t), follows the same formula with eq2

instead of q2. Price or tax changes only affect production by firms on the margin of entry so

that ψc is only evaluated where c = (p − t)q. The “q2” reflects the fact that potential firms

with greater output are also more sensitive to per-unit price or tax changes. It will prove

useful to define

ψe(e) ≡(ψe(e)

∫q

q2ψc(pq|e, q)ψq(q|e)dq)/ (S ′(p)) ,

as the “sensitivity and size”-corrected distribution on e. ψe is the distribution of e scaling by

the size of firms (one q), their sensitivity to tax or price changes (the other q), evaluated at

t = 0 for the marginal firms (c = pq). Using this, the change in emissions (at t = 0) from

exact if i) demand is perfectly elastic at p, ii) there are no externalities associated with production elsewhereor iii) the externalities elsewhere are corrected by a Pigovian tax.

19

price changes is:

G′(p) = Eψe(e)× S′(p),

where Eψe simply denotes the expectation with respect to ψe. One can demonstrate that

(to a first order) the optimal uniform quantity tax is t∗ = vG′(p)/S ′(p) = vEψe(e), average

emissions weighted by q2 along the relevant margin of adjustment (where pq = c) and not

total emissions divided by total supply as was the case for the model on the intensive margin.

The difference arises because i) only firms on the margin of pq = c adjust to marginal price

changes and ii) larger firms are more important for changes to emissions and also more

sensitive to tax changes.

2.7.1 Equilibrium with certification

We set up a certification system along the same lines as for the intensive-margin case. We

assume that the certification cost F is second-order in τ . Firms with e ≤ e certify whereas

those with e > e do not.13 A firm that certifies will pay τe in emission tax and those that

do not will pay according to the average emissions of active non-certified firms:

t = τE (eq|e ≥ e, (p− t)q ≥ c)

E (q|e ≥ e, (p− t)q ≥ c)= τ

∫eq1e>e1(p−t)q≥cdΨ(c, q, e)∫q1e>e1(p−t)q≥cdΨ(c, q, e)

. (16)

This implies that total supply is given by:

S(p, τ, t) =

∫q(1e≤e1(p−τe)q≥c+F + 1e>e1(p−t)q≥c

)dΨ(c, q, e),

where corresponding expressions for total costs C(p, τ, t) and emissions G(p, τ, t) follow the

structure of S(p, τ, t) but replace q with c and eq, respectively. The total mass of firms who

certify is given by M =∫

1e≤e1(p−τe)q≥c+FdΨ(c, q, e). We proceed along the same lines as for

Corrollary 1 to arrive at the following result:

Proposition 2. Consider τ = v. The difference in welfare and emissions between certifica-

tion and no certification is given by:

W V −WU =v2

2S ′(p)×

13In the intensive margin case, it was immaterial whether we chose an exogenous e or a tax f to incentivizethe same level of certification. Here a tax, f , however, will affect both the margins of certification and ofentry and these two setups will not be equivalent. Therefore, we define e as the maximum emission rate thatthe government permits to certify. With F being second order in τ , the constraint binds and e = e.

20

[V arψe(ε) +

(G′(p)

S ′(p)− G(p)

S(p)

)2

−(

1− Ψe(e))(

Eψe(e|e > e)− E (eq|e ≥ e, pq ≥ c)

E (q|e ≥ e, pq ≥ c)

)2]−FM+o

(τ 2),

(17)

where G(p) and S(p) are evaluated at t = τ = 0 and Ψe(e) =∫ eeψe(e)de is the (sensitivity and

size-)corrected mass of firms with e ≤ e. ε is given by ε = e if e ≤ e and ε = Eψe(e|e > e)

otherwise.

Change in emissions is given by:

GV −GU = −τS ′(p)×[V arψe(ε) +

(G′(p)

S ′(p)− G(p)

S(p)

)Eψe(e) + (1− Ψe(e))

(G(p)

S(p)Eψe(e|e > e)− G′(p)

S ′(p)Eψe(e)

)]+o(τ).

(18)

Proof. See Appendix A.2.

Consider first the change in welfare which replicates the structure of welfare gains under

the intensive margin. As in the model with an intensive margin, the first term captures the

reallocation effect of moving from an optimally set uniform tax to an individual tax. However,

as discussed above, t = G(p)/S(p) in equation (16) is not set optimally. The change in welfare

is therefore best thought of as a two-step change: First moving to an optimal uniform tax

of G′(p)/S ′(p) (captured by the second term) and thereafter to the certification program

(captured by the first). The last term captures the fact that the uncertified firms do not pay

the optimal output tax. Naturally, if the uniform tax were already set to G′(p)/S ′(p) only

the reallocation (the first) term would appear.

The change in emissions share similar intuitions. The second term captures the change in

taxation rate for certified firms when moving from a uniform tax of G(p)/S(p) to G′(p)/S ′(p)

and the third term is a “correction”-term for the fact that uncertified firms are not taxed

according to individual emissions.

2.8 Domestic Empirical Application: Methane Emissions in the Permian Basin

A carbon-based economy has dizzying array of emissions sources for potential regulation.

One way to economize on enforcement costs while maximizing coverage is to focus attention

on fuel extraction rather than points of emission (Metcalf and Weisbach (2009)). The close

measurement of fuel production for royalties charges creates a point of taxation with minimal

21

additional regulatory cost. Taxation at the point of extraction also ensures the price of carbon

is reflected throughout the supply chain. Recent studies have evaluated the effects of pricing

coal as a ‘royalty adder’ above existing royalty rates in the Federal Coal Program (Gillingham

et al. (2016); Gerarden et al. (2020)) and oil and gas leasing more broadly (Prest and Stock

(2021)).

In this section we build on these royalty adder proposals to account for unmonitored

methane emissions from oil and gas fields. Methane (CH4) is a powerful greenhouse gas,

with an estimated social cost of $1500/metric ton (on Social Cost of Greenhouse Gases

(2021)), compared to $51/metric ton for carbon dioxide. It is the primary compound in

natural gas, and is released into the atmosphere during production from natural gas wells

due to faulty equipment, or from safety valves to relieve pressure. Methane is created when

longer hydrocarbon chains break down under heat and pressure underground. As a result,

wells drilled to recover oil also co-produce methane to varying degrees. In places without

sufficient infrastructure to deliver methane from oil wells to market, it is a waste product.

Best practices in such settings entail flaring the methane in situ, which converts the gas into

less-harmful carbon dioxide.14

We focus our analysis on the Permian Basin of west Texas and southeast New Mexico,

whose oil-rich shales yield nearly one-third of U.S. oil and 10% of natural gas production

(Administration (2019)). Poorly operated or malfunctioning flares, direct venting, and leaks

from these oil and gas fields are responsible for significant methane emissions. These are

recently estimated to be 2.7 million metric tons (Tg) per year based on the analysis of

satellite data (Zhang et al. (2020)), for a social cost of about $4B/year. Zhang et al. (2020)

calculate these emissions to have roughly similar global warming potential as CO2 emissions

from the entire U.S. residential sector.

The main regulatory challenge for internalizing methane emissions is that exact sources

are currently unobserved and enormously heterogeneous across leases. A random ground-

based sample of oil and gas wells in the Permian found that 70% of emissions came from

15% of the measured sites, while nearly one third of measurements were below detectible

levels (Robertson et al. (2020)). An output-based royalty adder that accounts for average

methane emissions falls short of an actual emissions tax according to the results of Section

2: there is too little output from clean leases and too much from polluting sources due to

14In North Dakota’s oil-rich Bakken Shale, for example, approximately one third of natural gas was flaredin the mid 2010’s, making the sparsely-populated oil fields prominently visible at night from space (Cicala(2015)). The state adopted regulations to reduce flaring, and recent work has found a drop of about 20%through 2016 (Lade and Rudik (2020)).

22

the lack of emissions-targeting.

We seek to answer the following questions: What are the differences in emissions and

welfare between an output-based tax and an emissions tax? How might adverse selection push

outcomes under an output-based tax with voluntary emissions taxation closer to those of a

fully mandatory emissions tax? To answer these questions we combine the complete annual

production data from New Mexico and Texas with emissions estimates from a stratified

random sample of wells (Robertson et al. (2020)). We use this sample to simulate the

distribution of lease-level emissions per barrel of oil equivalent (BOE) for 2019 in the Permian

Basin.

With the variance of emissions in hand, we require only the social cost of pollution

($1500/t) and the slope of the supply curve to approximate the emissions and welfare changes

due to voluntary certification according to Corollary 1. For this last number we use an

elasticity of supply of 0.89 from Newell et al. (2019),15 while limiting production to zero

for the share of leases whose emissions fees would exceed revenue.16 Output prices per

BOE are constructed by weighing spot market prices for fuels from the Energy Information

Administration by the site-level share of production from oil, gas, or natural gas liquids,

respectively. Further details on data construction and summary statistics are provided in

the Data Appendix.

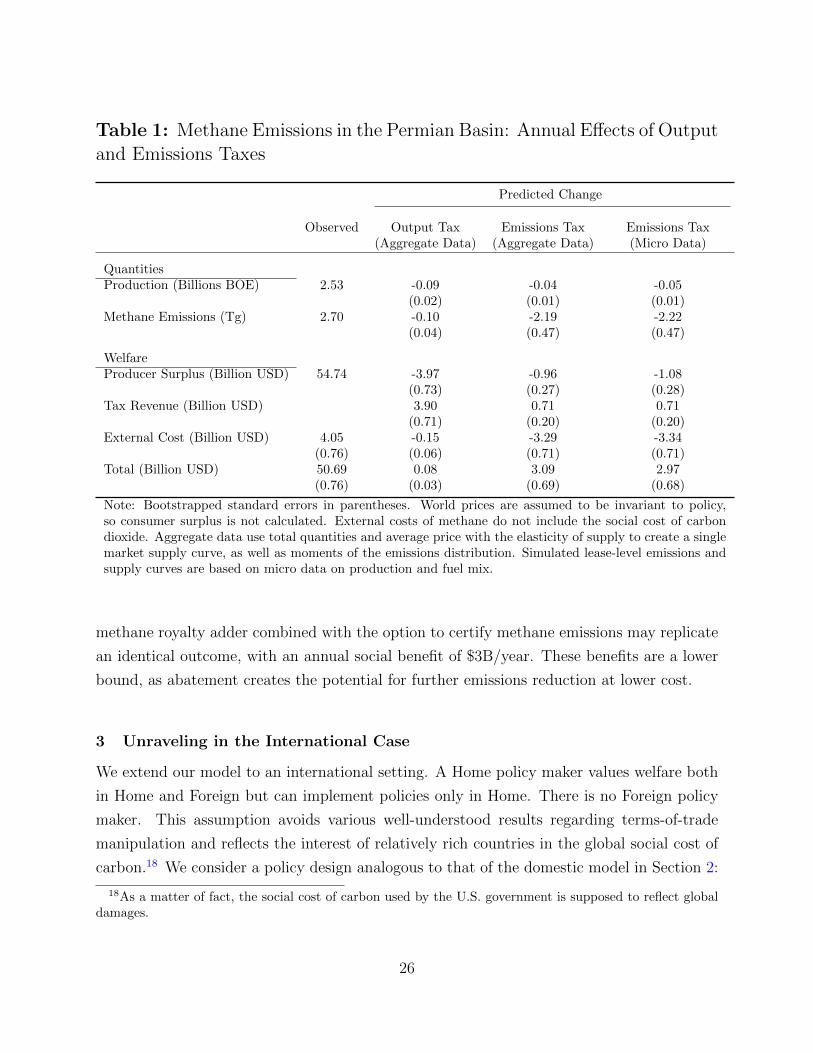

The first column of Table 1 presents quantity and welfare calculations based on observed

outcomes in 2019. We calculate standard errors for objects involving emissions by bootstrap-

ping from the estimates of Zhang et al. (2020) and Robertson et al. (2020). Details of the

procedure are provided in Appendix B. For each bootstrap sample’s estimates of emissions,

we calculate the corresponding quantities and welfare measures. The table reports the means

and standard deviations across 1,000 iterations. When calculating welfare, we assume that

world prices are unchanged, and therefore do not calculate consumer surplus.

To test our approximations, we calculate quantity and welfare changes two different

ways—using aggregate statistics and micro data. The second column applies a uniform tax

per barrel to the aggregate supply function to calculate outcomes. Section 2.1 derives the

difference between output and emissions taxes as a function of market aggregates, allowing

15This is the drilling elasticity based on Anderson et al. (2018), not the short-term change in productionfrom existing wells, whose marginal costs are essentially ignorable. We are interested in the long-term supplyresponse to our program. In steady state, the production elasticity is equal to the drilling elasticity (Hausmanand Kellogg (2015)). Anderson et al. (2018); Newell and Prest (2019) find similar elasticity estimates.

16Corollary 1 assumes that all agents remain active. In Appendix A we derive the corresponding expressionswhen firms have the option to shut down. We assume that leases whose tax bill exceeds revenue will shut in(i.e. pause production), and apply the expressions that account for shutting in.

23

heterogeneity only with respect to emissions rates. We use the empirical analogs of equation

(9) with an adjustment for shut-ins (i.e. zero output), plus the second column to arrive

at the third column, which estimates how outcomes are affected by a mandatory methane

tax. With a mandatory methane tax, we assume certification is costless and compliance is

complete.

Applying aggregate statistics to Corollary (1) is sufficient to approximate the effects of

policy. In the fourth column we show how these approximations compare to a bottom-up

calculation from lease-level data.17 For each bootstrap sample we use linear supply curves,

and each lease’s emissions intensity to calculate production decisions, emissions, producer

surplus, and tax revenues.

We estimate that methane leaks from the Permian basin in 2019 had a social cost of

about $4B, which is about 7% of producer surplus. An optimal output tax based on average

emissions per barrel would be about $1.60, or a 3% tax on oil and an 11% tax on natural gas.

An output tax of this magnitude reduces output by a relatively small amount, and its poor

targeting of the externality means that it is not particularly effective at reducing emissions.

The tax revenue and reduced externality costs exceed the lost producer surplus by about

$80M.

Even without allowing firms to abate their emissions, taxing the externality directly yields

significant welfare improvements. Rather than scaling back output with a uniformly-applied

tax, targeting those with relatively higher emissions causes about 1% of output to shut-in.

This zero bound means that the reduction in output is less under an emissions tax than an

output tax—even though we are using linear supply curves. Emissions fall by nearly 80%,

producer surplus losses are about one quarter of those under an output tax, and net welfare

is about $3B higher per year. These results are essentially unchanged in the fourth column.

Estimates based on calculations using market aggregates and applying Corollary (1) closely

track those from bottom-up lease-level calculations of the effects of an emissions tax.

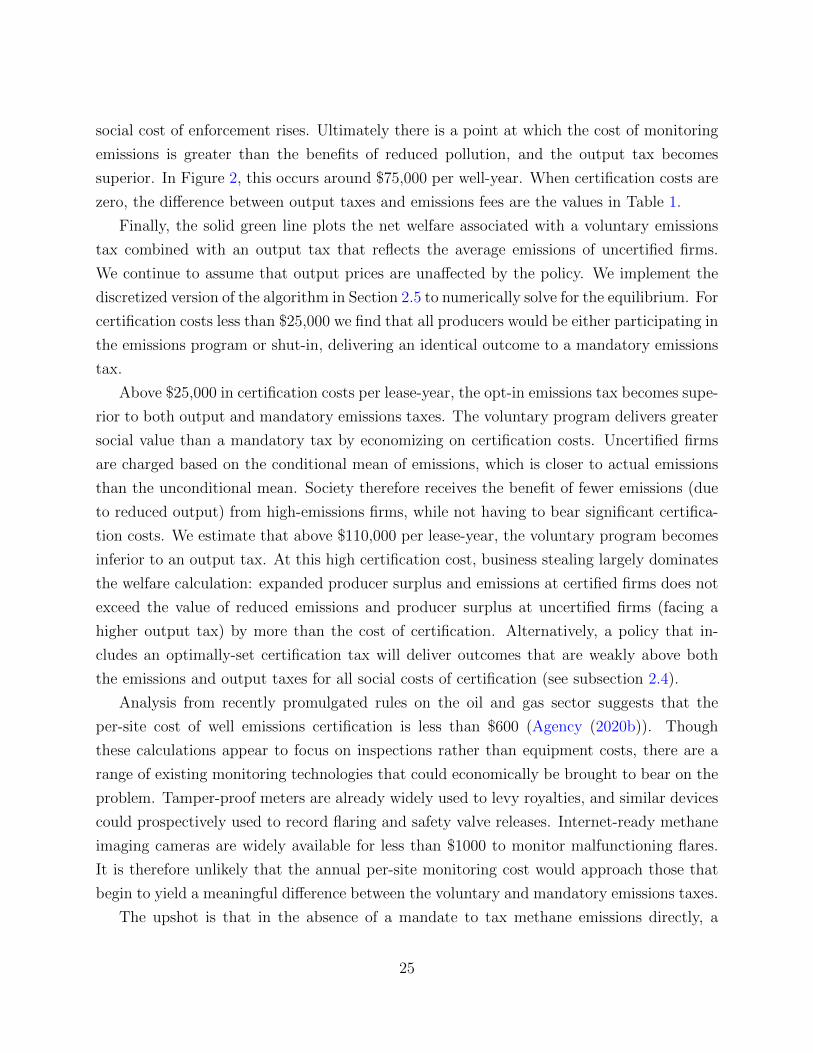

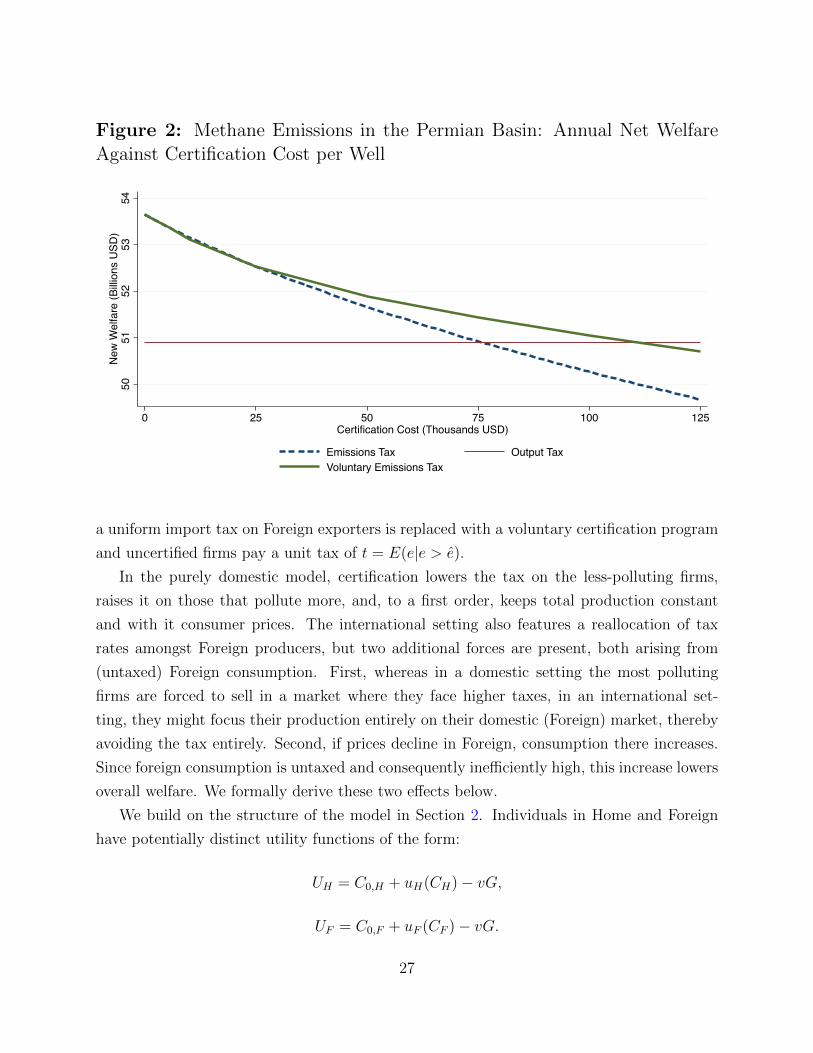

Figure 2 plots net welfare of three prospective policies as a function of the cost per well

of monitoring methane emissions, or “certification costs.” First, an output tax piggy-backs

on the royalty model of metering output, so no additional regulatory costs are involved. The

net welfare of an output tax is therefore flat with respect to certification costs. The second

prospective policy is a mandatory emissions fee with costly certification. This is depicted as

a dashed blue line in Figure 2. Such a policy loses ground relative to an output tax as the

17Emissions may come from an individual well or equipment at a ‘site’ shared across multiple wells. Sinceproduction and emissions are measured at the lease level, we refer to our unit of measurement as a lease.

24

social cost of enforcement rises. Ultimately there is a point at which the cost of monitoring

emissions is greater than the benefits of reduced pollution, and the output tax becomes

superior. In Figure 2, this occurs around $75,000 per well-year. When certification costs are

zero, the difference between output taxes and emissions fees are the values in Table 1.

Finally, the solid green line plots the net welfare associated with a voluntary emissions

tax combined with an output tax that reflects the average emissions of uncertified firms.

We continue to assume that output prices are unaffected by the policy. We implement the

discretized version of the algorithm in Section 2.5 to numerically solve for the equilibrium. For

certification costs less than $25,000 we find that all producers would be either participating in

the emissions program or shut-in, delivering an identical outcome to a mandatory emissions

tax.

Above $25,000 in certification costs per lease-year, the opt-in emissions tax becomes supe-

rior to both output and mandatory emissions taxes. The voluntary program delivers greater

social value than a mandatory tax by economizing on certification costs. Uncertified firms

are charged based on the conditional mean of emissions, which is closer to actual emissions

than the unconditional mean. Society therefore receives the benefit of fewer emissions (due

to reduced output) from high-emissions firms, while not having to bear significant certifica-

tion costs. We estimate that above $110,000 per lease-year, the voluntary program becomes

inferior to an output tax. At this high certification cost, business stealing largely dominates

the welfare calculation: expanded producer surplus and emissions at certified firms does not

exceed the value of reduced emissions and producer surplus at uncertified firms (facing a

higher output tax) by more than the cost of certification. Alternatively, a policy that in-

cludes an optimally-set certification tax will deliver outcomes that are weakly above both

the emissions and output taxes for all social costs of certification (see subsection 2.4).

Analysis from recently promulgated rules on the oil and gas sector suggests that the

per-site cost of well emissions certification is less than $600 (Agency (2020b)). Though

these calculations appear to focus on inspections rather than equipment costs, there are a

range of existing monitoring technologies that could economically be brought to bear on the

problem. Tamper-proof meters are already widely used to levy royalties, and similar devices

could prospectively used to record flaring and safety valve releases. Internet-ready methane

imaging cameras are widely available for less than $1000 to monitor malfunctioning flares.

It is therefore unlikely that the annual per-site monitoring cost would approach those that

begin to yield a meaningful difference between the voluntary and mandatory emissions taxes.

The upshot is that in the absence of a mandate to tax methane emissions directly, a

25

Table 1: Methane Emissions in the Permian Basin: Annual Effects of Outputand Emissions Taxes

Predicted Change

Observed Output Tax Emissions Tax Emissions Tax(Aggregate Data) (Aggregate Data) (Micro Data)

QuantitiesProduction (Billions BOE) 2.53 -0.09 -0.04 -0.05

(0.02) (0.01) (0.01)Methane Emissions (Tg) 2.70 -0.10 -2.19 -2.22

(0.04) (0.47) (0.47)

WelfareProducer Surplus (Billion USD) 54.74 -3.97 -0.96 -1.08

(0.73) (0.27) (0.28)Tax Revenue (Billion USD) 3.90 0.71 0.71

(0.71) (0.20) (0.20)External Cost (Billion USD) 4.05 -0.15 -3.29 -3.34

(0.76) (0.06) (0.71) (0.71)Total (Billion USD) 50.69 0.08 3.09 2.97

(0.76) (0.03) (0.69) (0.68)

Note: Bootstrapped standard errors in parentheses. World prices are assumed to be invariant to policy,so consumer surplus is not calculated. External costs of methane do not include the social cost of carbondioxide. Aggregate data use total quantities and average price with the elasticity of supply to create a singlemarket supply curve, as well as moments of the emissions distribution. Simulated lease-level emissions andsupply curves are based on micro data on production and fuel mix.

methane royalty adder combined with the option to certify methane emissions may replicate

an identical outcome, with an annual social benefit of $3B/year. These benefits are a lower

bound, as abatement creates the potential for further emissions reduction at lower cost.

3 Unraveling in the International Case

We extend our model to an international setting. A Home policy maker values welfare both

in Home and Foreign but can implement policies only in Home. There is no Foreign policy

maker. This assumption avoids various well-understood results regarding terms-of-trade

manipulation and reflects the interest of relatively rich countries in the global social cost of

carbon.18 We consider a policy design analogous to that of the domestic model in Section 2:

18As a matter of fact, the social cost of carbon used by the U.S. government is supposed to reflect globaldamages.

26

Figure 2: Methane Emissions in the Permian Basin: Annual Net WelfareAgainst Certification Cost per Well

5051

5253

54Ne

w W

elfa

re (B

illion

s US

D)

0 25 50 75 100 125Certification Cost (Thousands USD)

Emissions Tax Output TaxVoluntary Emissions Tax

a uniform import tax on Foreign exporters is replaced with a voluntary certification program

and uncertified firms pay a unit tax of t = E(e|e > e).

In the purely domestic model, certification lowers the tax on the less-polluting firms,

raises it on those that pollute more, and, to a first order, keeps total production constant

and with it consumer prices. The international setting also features a reallocation of tax

rates amongst Foreign producers, but two additional forces are present, both arising from

(untaxed) Foreign consumption. First, whereas in a domestic setting the most polluting

firms are forced to sell in a market where they face higher taxes, in an international set-

ting, they might focus their production entirely on their domestic (Foreign) market, thereby

avoiding the tax entirely. Second, if prices decline in Foreign, consumption there increases.

Since foreign consumption is untaxed and consequently inefficiently high, this increase lowers

overall welfare. We formally derive these two effects below.

We build on the structure of the model in Section 2. Individuals in Home and Foreign

have potentially distinct utility functions of the form:

UH = C0,H + uH(CH)− vG,

UF = C0,F + uF (CF )− vG.

27

These result in demand functions for Home, DH(p), and foreign, DF (p). Consumers in

both countries experience the same negative disutility, v, from global emissions, G. It costs

κ units of the outside good to transport the polluting good between Home and Foreign. It is

free to ship the outside good. The outside good, C0, is produced emissions-free, competitively

and one-for-one with labor. Labor is the only factor of production, and we choose the stock

in both Home and Foreign such that the outside sector is active in both countries. We

normalize the price to 1 in the outside good sector such that wages in both countries equal

1. The identical wages play no role in what follows.

The polluting good is produced competitively by a continuum of mass 1 of firms in Home

and a mass of 1 in Foreign. The emissions per unit produced in Home are distributed

according to ΨH(e) with ΨF (e) describing the Foreign distribution. Within each country,

firms differ only in their emissions and share a common cost function. To focus on the

international aspect and with little impact on the analysis to follow, we assume that all

emissions in Home are observable and emissions are taxed at τH . Firms can abate as described

in Section 2.6, and a Home firm will have a supply curve of sH(p − τHe + AH(τH)), where

AH(τH) ≡ τHaH(τH) − b(aH(τH)) is the net gain in price from abatement and aH(τH) =

b′−1(τH) is the level of abatement (and AF (τF ), analogously for Foreign). To streamline the

presentation, the main text will be devoted to comparing a tax policy analogous to that of

the domestic setting: Firms can choose to certify and be taxed according to emissions and

non-certified firms pay an output tax according to average emissions of uncertified firms.

Other comparisons exist, in particular allowing the output tax t to be set optimally. We will

discuss alternatives towards the end of this section and explore the optimal output tax in

Appendix A.3.3.

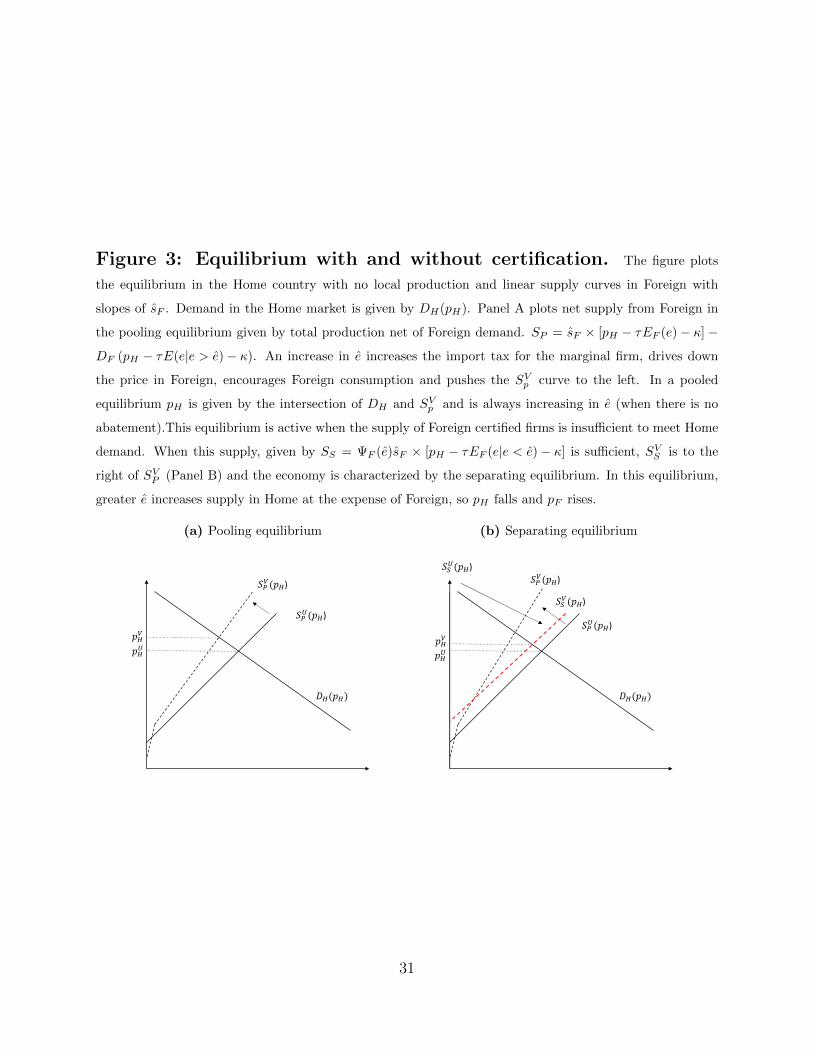

3.1 Equilibrium

Since the setting with no certification is a special case of the equilibrium with certification

(where no firm chooses to certify) we will solve for the general case. Consider an equilibrium

in which Home firms are all taxed at the emission rate of τH and certified Foreign firms pay an

emission tax of τF . There exists a cutoff e such that all Foreign firms with e ≤ e are certified

and all other Foreign firms pay a common output tariff on exports of τFEF (e|e > e) where

EF is the expectation operator over ΨF . In what follows, we take e as a policy parameter

determined either by an indifference condition such as equation (4) or by only permitting

firms below some predetermined level e to certify.

There are two subclasses of equilibria. In a pooled equilibrium, uncertified firms are

28

indifferent between selling domestically and exporting and continue to export to Home. In a

separating equilibrium uncertified firms only sell in the Foreign market. In either case, their

production can be evaluated at the foreign price denoted pF . If we define ρ as the difference

in net price between selling in Foreign and Home for an uncertified firm we have:

ρ ≡ pF − (pH − τFEF (e|e > e)− κ), (19)

where ρ = 0 in the pooled equilibrium and ρ ≥ 0 in the separating equilibrium.

The world market clearing condition for the polluting good is:

DH(pH) +DF (pF ) = (20)

EH [sH(pH − τHe+ AH)] + ΨF (e)EF [sF (pH − τF e− κ+ AF )|e < e] + (1−ΨF (e))sF (pF ).

The first line constitutes world demand as a function of the two consumer prices pH and

pF . The first term on the second line is Home production where emissions are always taxed

at τH and all firms abate. Hence, the second term of the second line is the production by

certified Foreign firms who face an emission tax of τF , transportation costs κ, abate at level

aF , and sell in the Home market at price pH . The equilibrium is characterized by the two

endogenous variables (pH , pF ). Equation (20) contributes one equilibrium equation. In the

pooled equilibrium equation (19) binds which adds the second equation of the equilibrium.

In such an equilibrium, equation (19) directly gives that the difference in consumer prices,

pH − pF , is increasing in e: the marginal exporter is more polluting and consequently faces

a higher import tariff which creates a higher price gap. Foreign prices must decline, but if

abatement is strong enough it is possible for prices in Home to decline as well (see details in