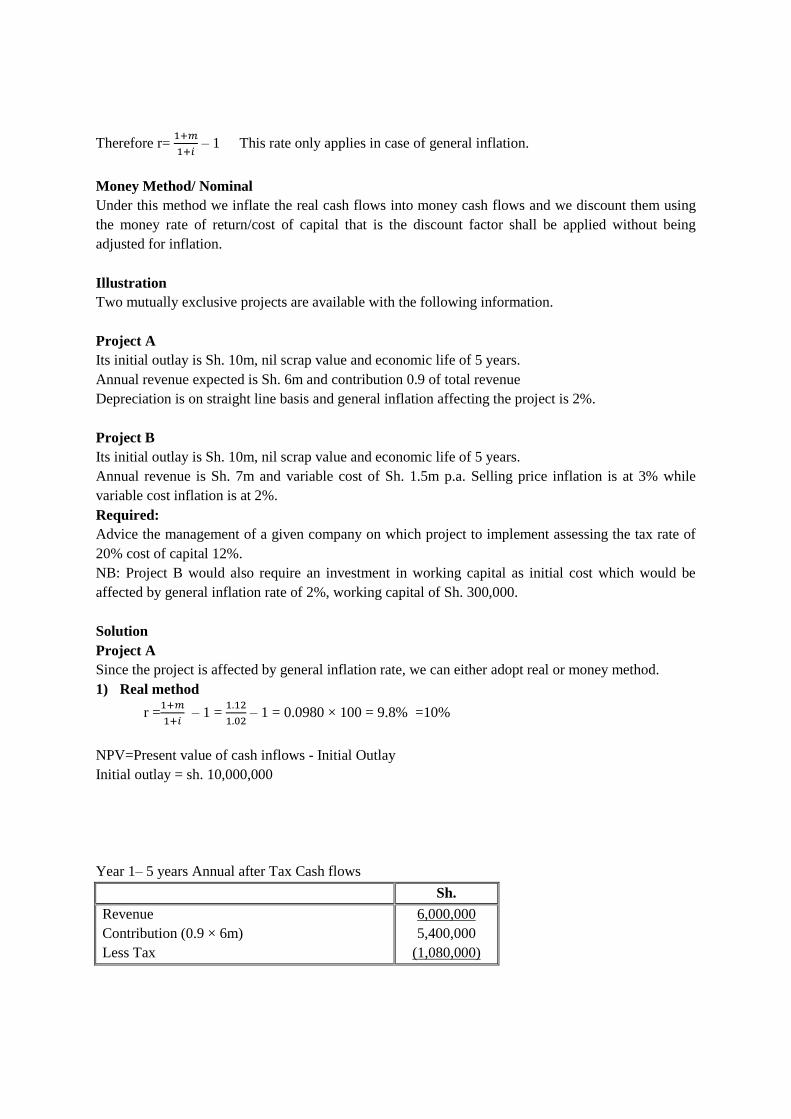

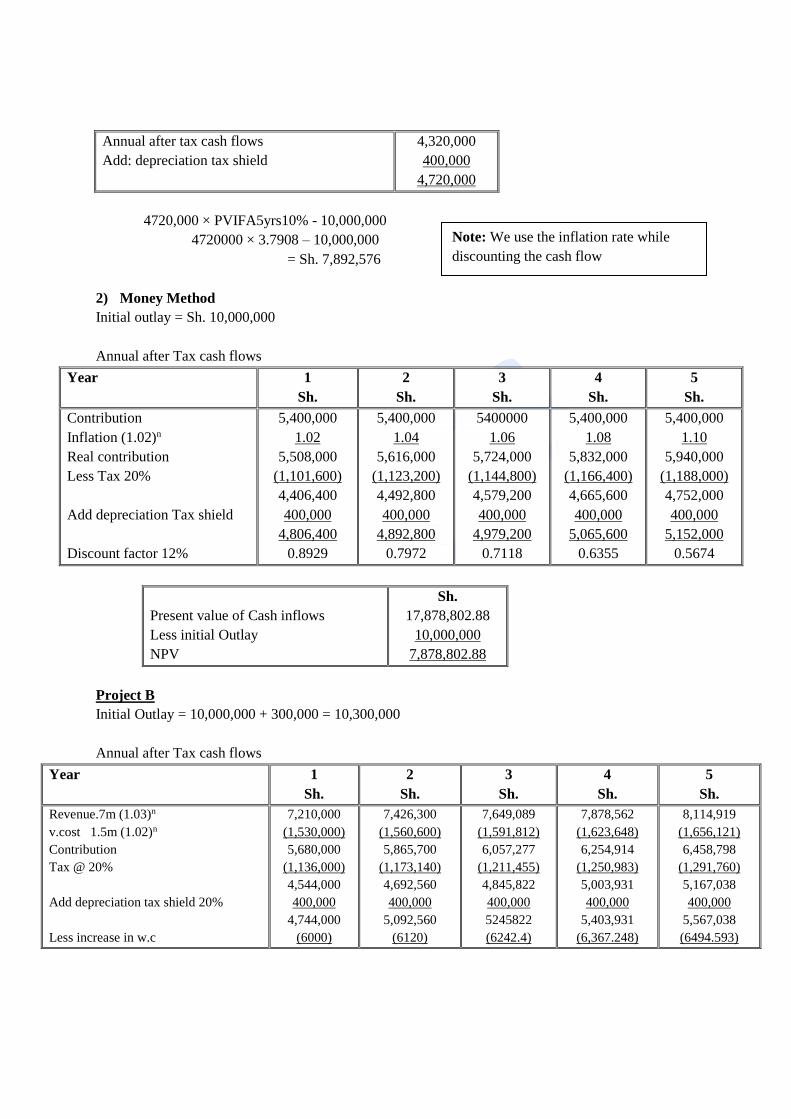

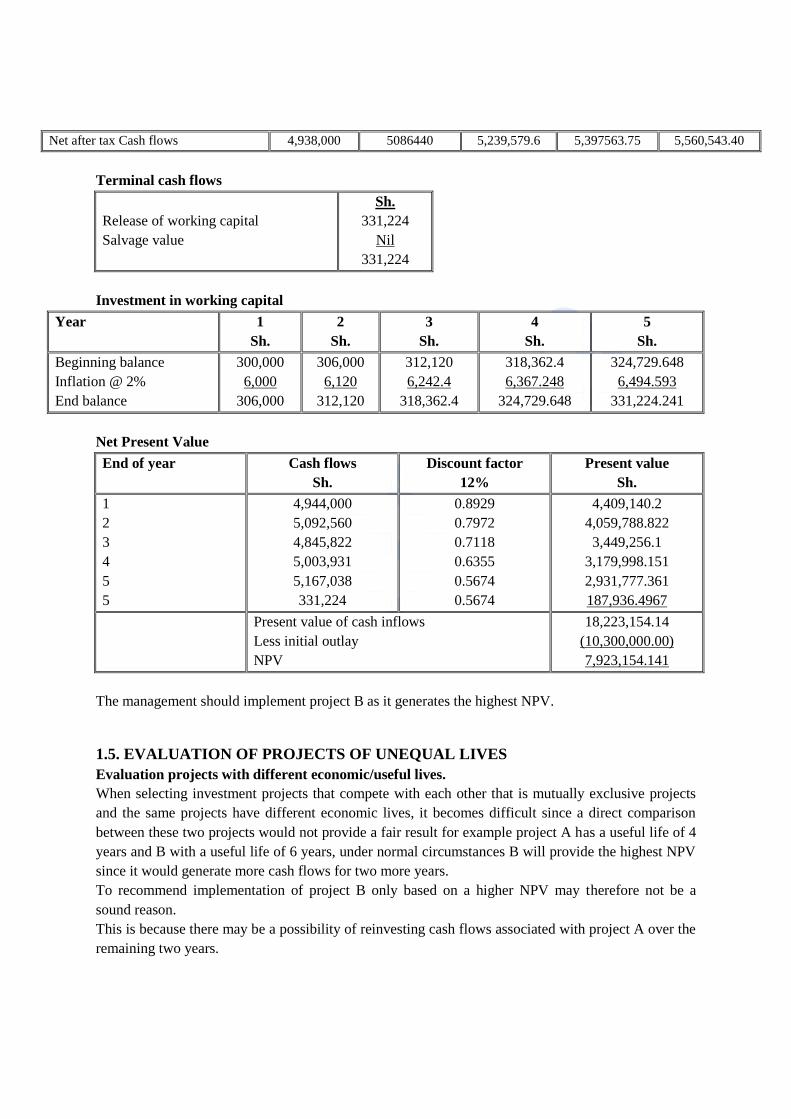

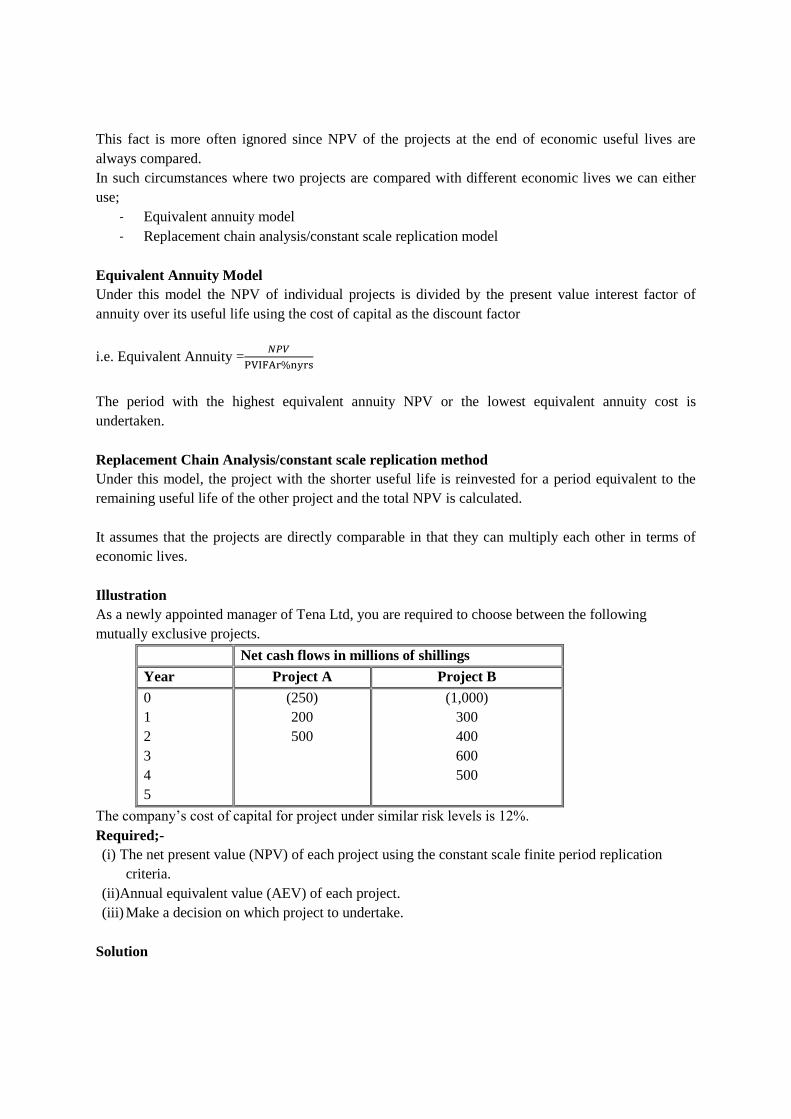

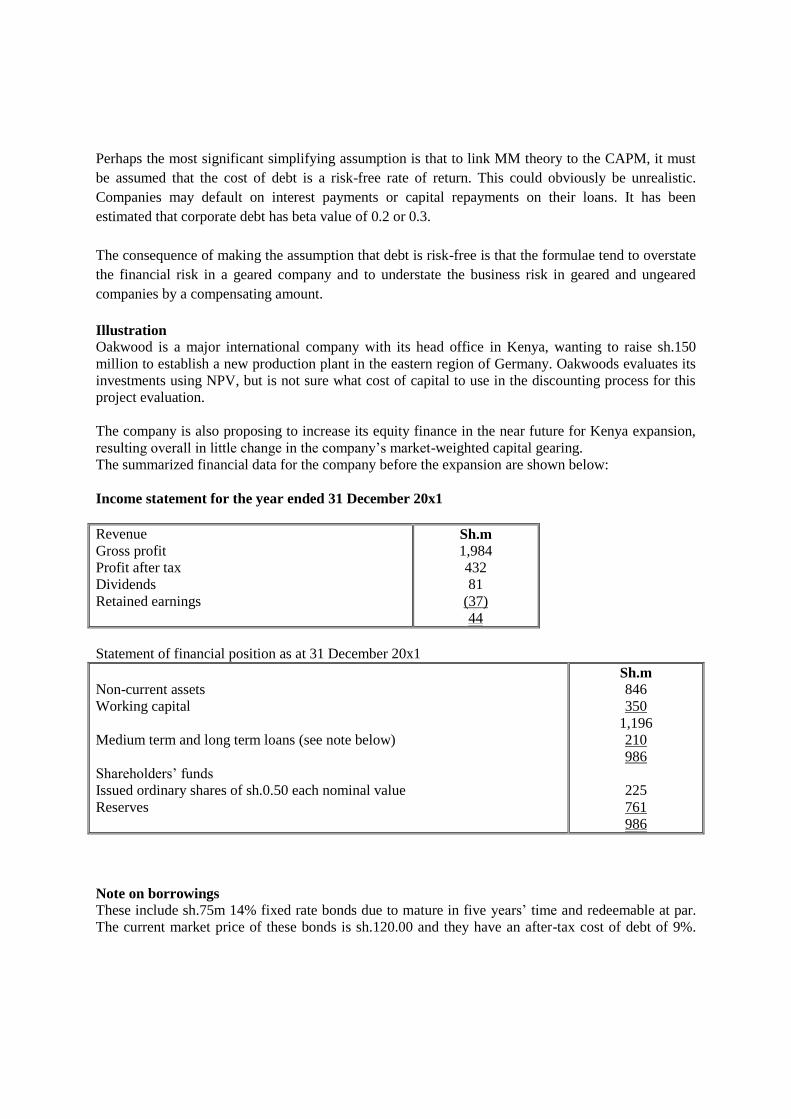

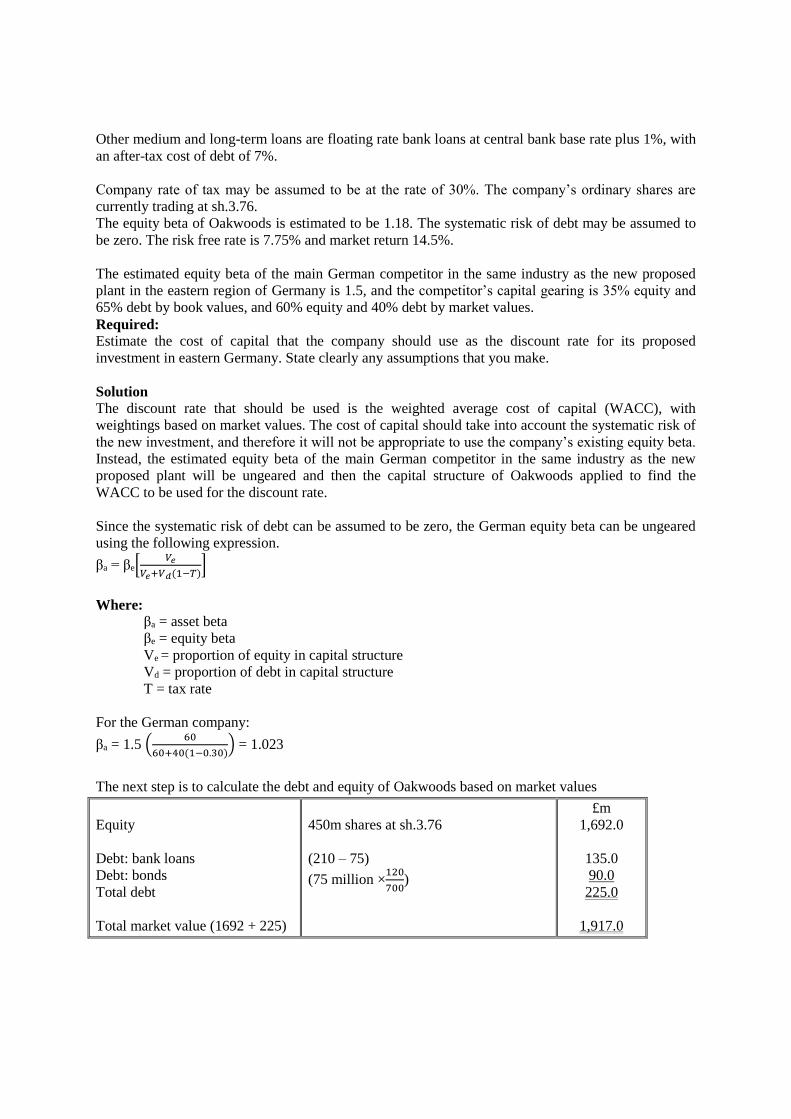

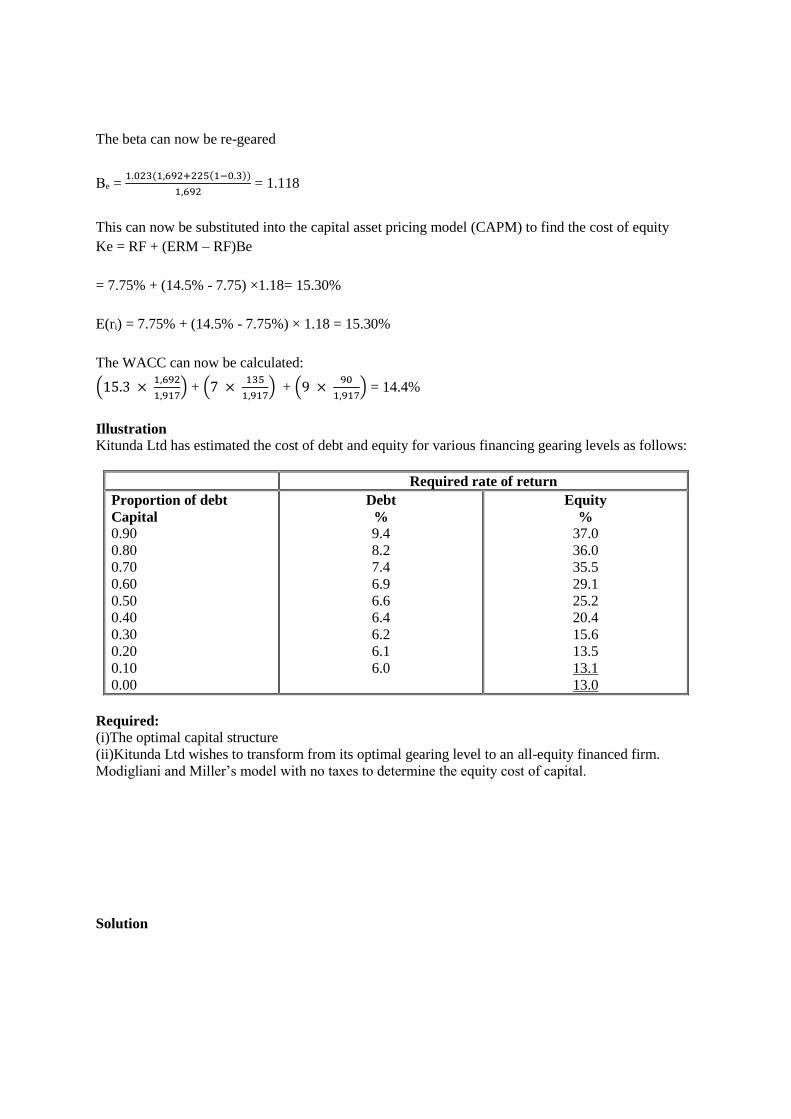

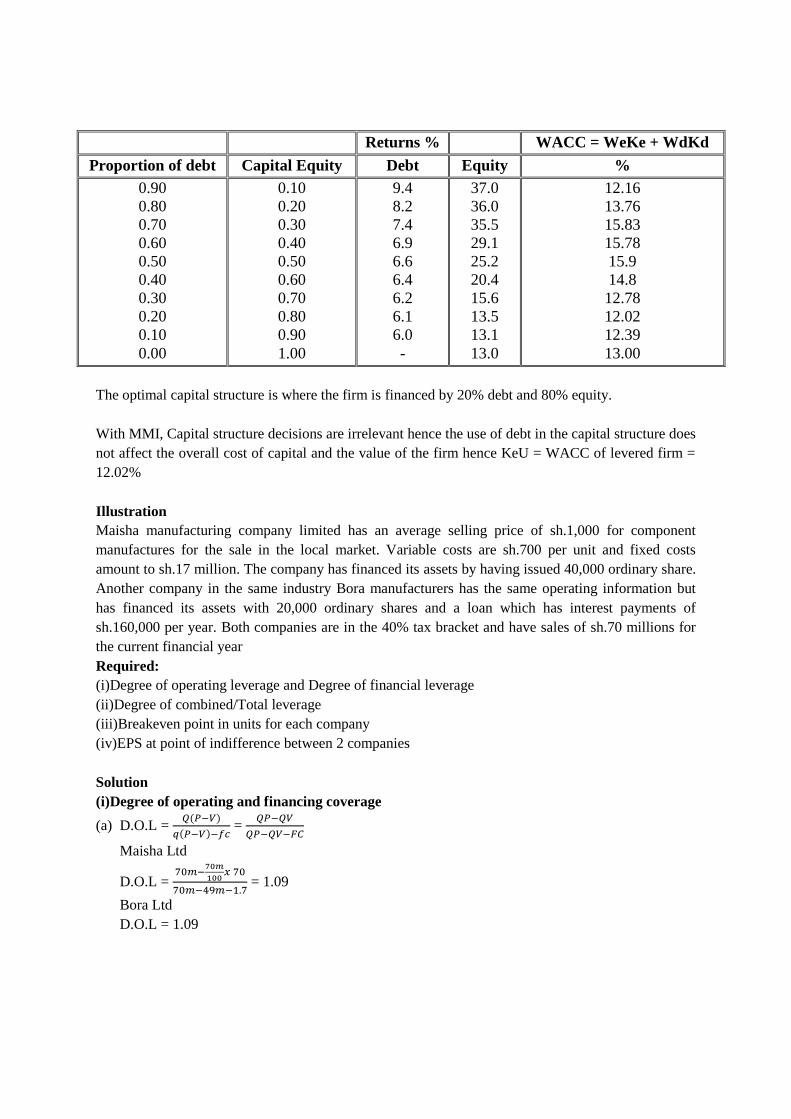

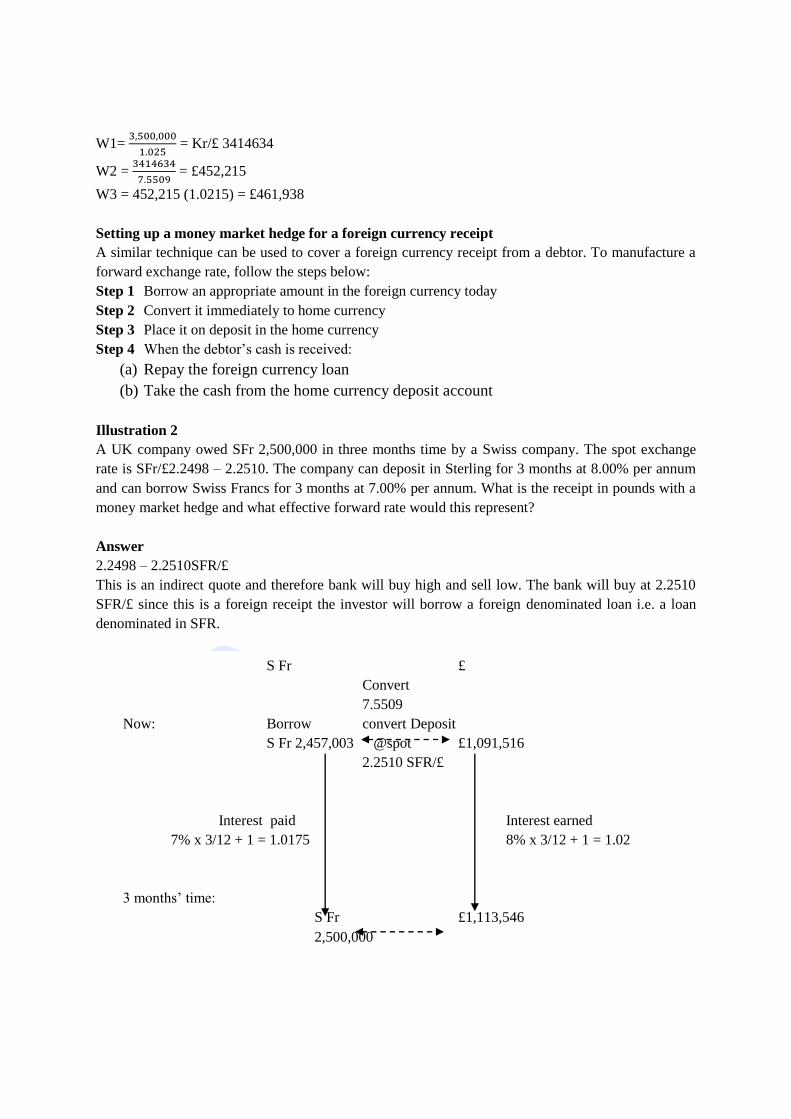

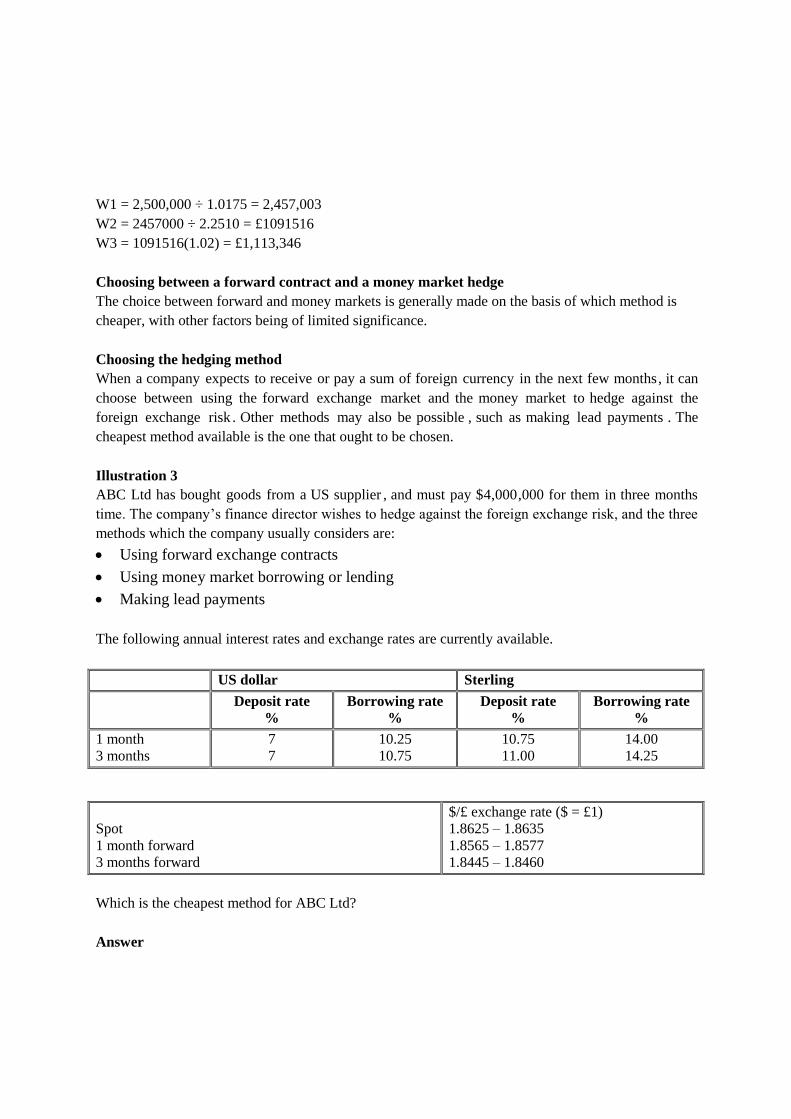

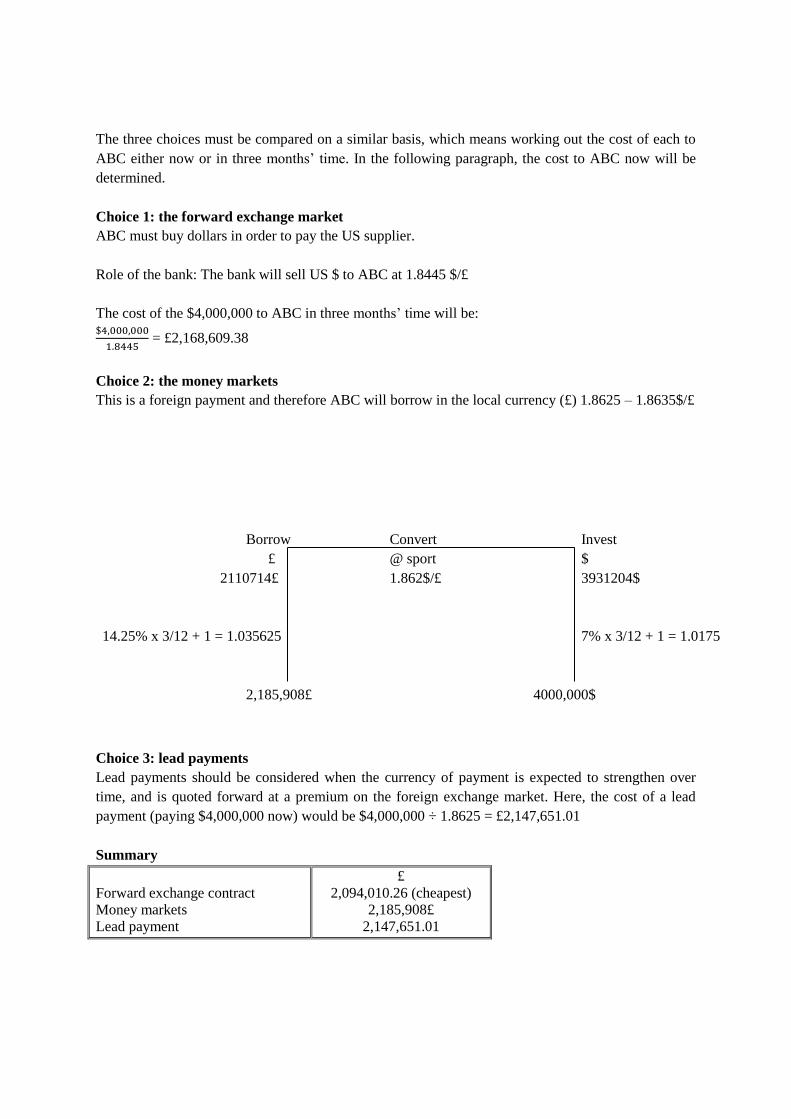

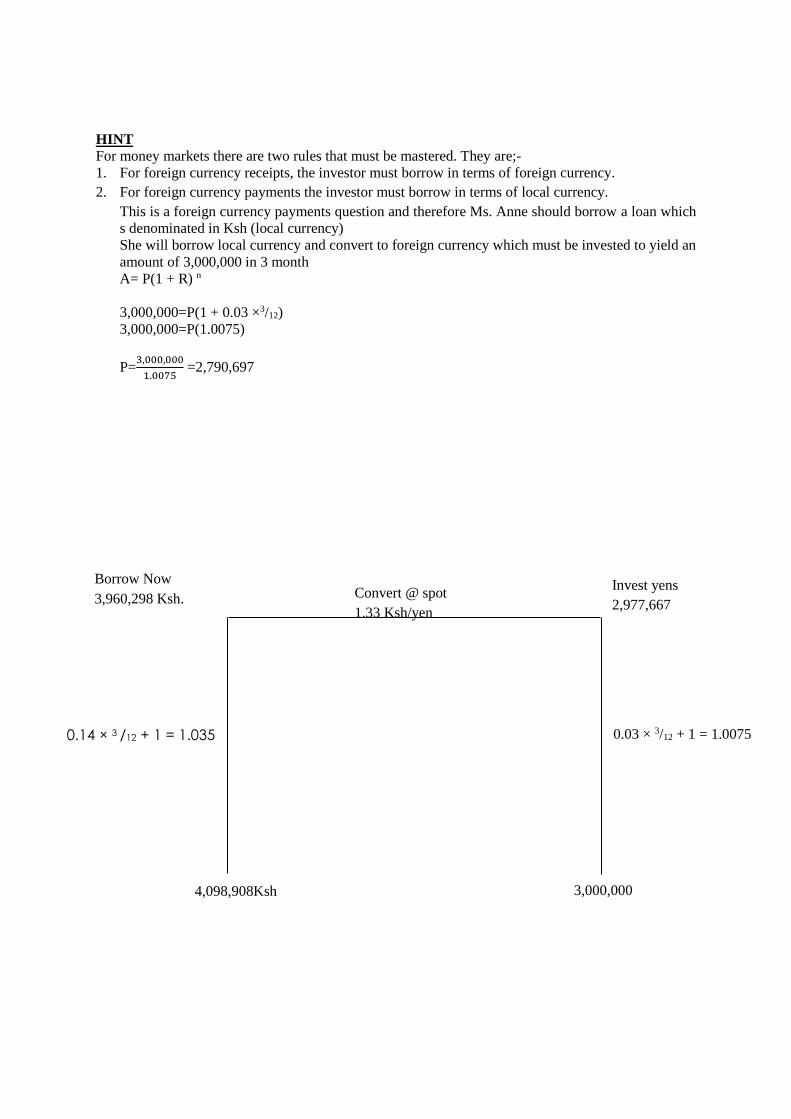

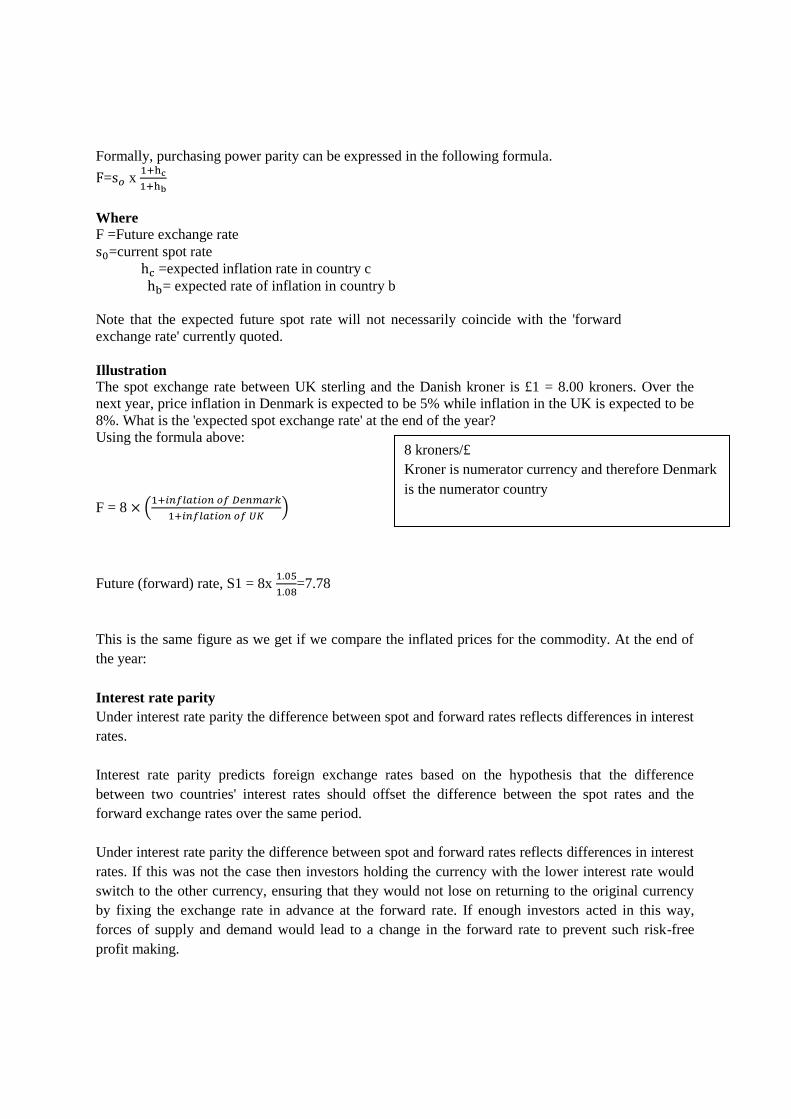

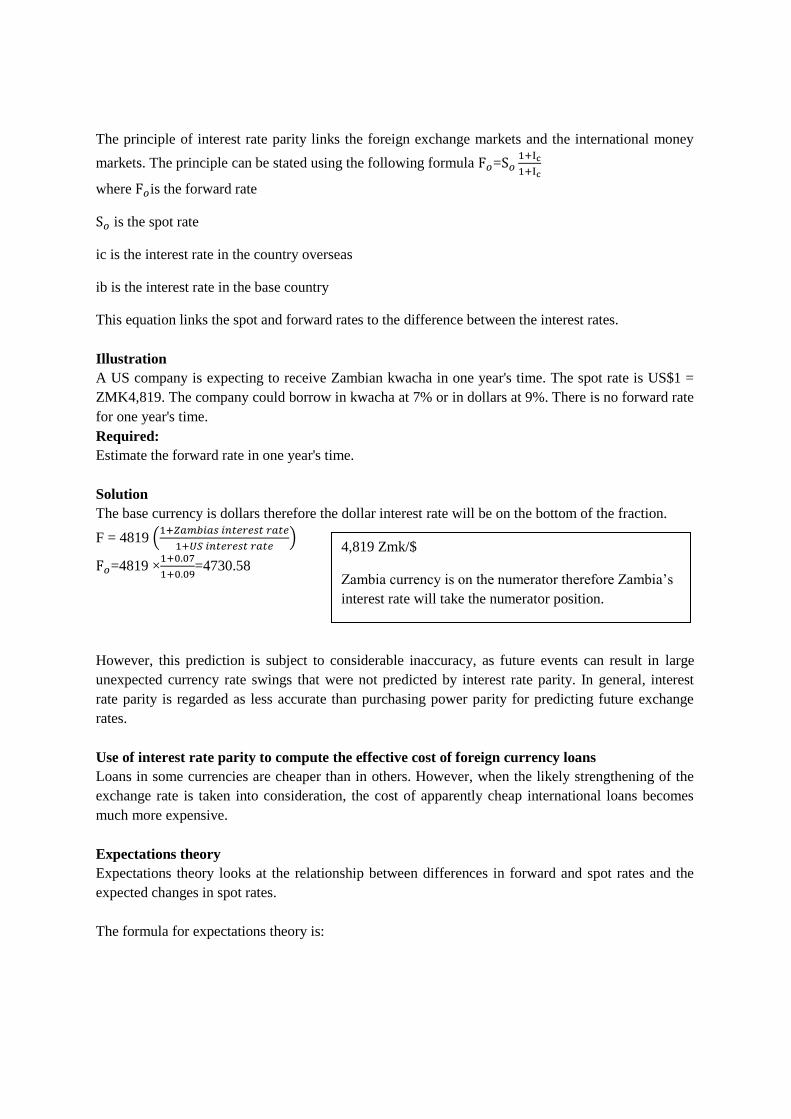

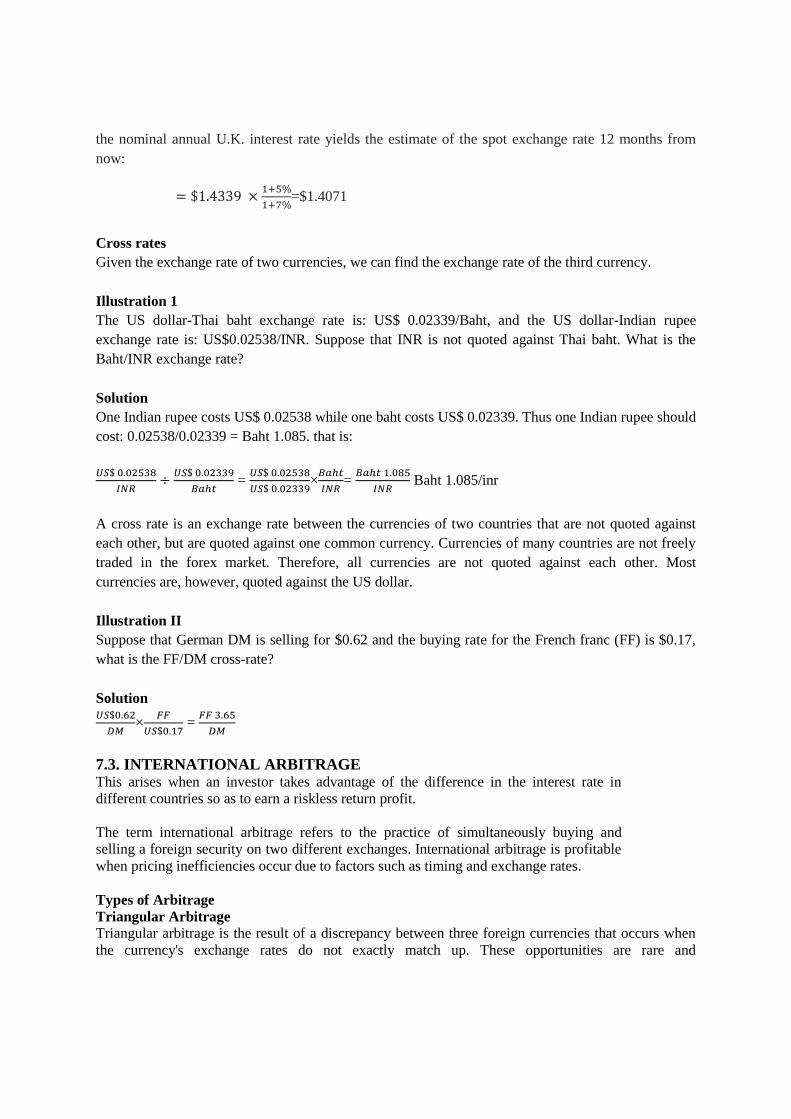

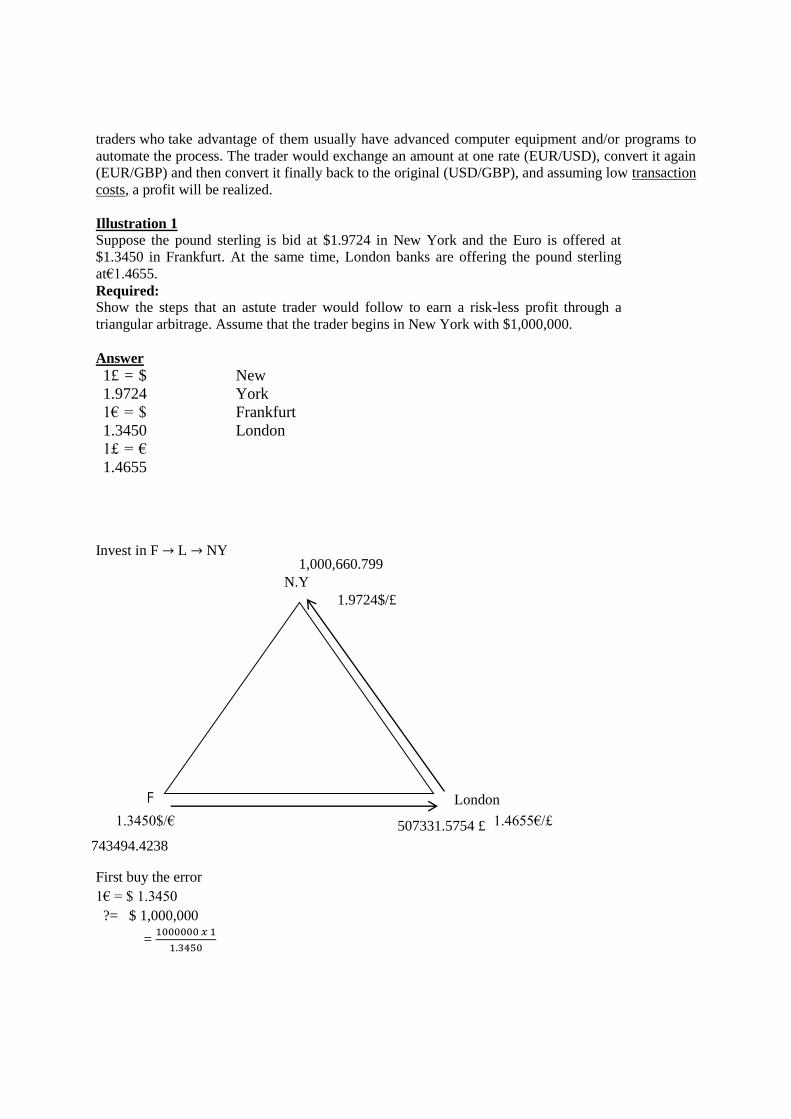

CPA CERTIFIED PUBLIC ACCOUNTANTS PART III SECTION 5 ADVANCED FINANCIAL MANAGEMENT STUDY TEXT Revised on: July 2019 KASNEB JULY 2018 SYLLABUS Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CPA

CERTIFIED PUBLIC ACCOUNTANTS

PART III

SECTION 5

ADVANCED FINANCIAL MANAGEMENT

STUDY TEXT

Revised on: July 2019

KASNEB JULY 2018 SYLLABUS

Page 1

SYLLABUS PAPER NO.15 ADVANCED FINANCIAL MANAGEMENT

GENERAL OBJECTIVE This paper is intended to equip the candidate with knowledge, skills and attitudes that will enable

him/her to apply advanced financial management techniques in an organisation.

15.0LEARNING OUTCOMES A candidate who passes this paper should be able to:

- Evaluate advanced capital budgeting decisions

- Design an optimal capital structure for an organisation

- Predict corporate failure

- Apply derivatives in financial risk management

- Apply financial management skills in the public sector

- Understand concepts of corporate restructuring and re-organisation

- Apply valuation techniques in real estate finance

CONTENT

15.1Advanced capital budgeting decision

- Incorporating risk/uncertainty in capital investment decisions

- Nature and measurement of risk and uncertainty

- Techniques of handling risk: sensitivity analysis, scenario analysis, decision trees, simulation

analysis, utility analysis, risk adjusted discounting rate(radr) and certainty equivalent method

- Incorporating capital rationing in capital investment appraisal

- Incorporating inflation in capital investment appraisal

- Evaluation of projects of unequal lives

- The real options-strategic investment option, timing option, abandonment option and the

replacement option

- Common capital budgeting pitfalls

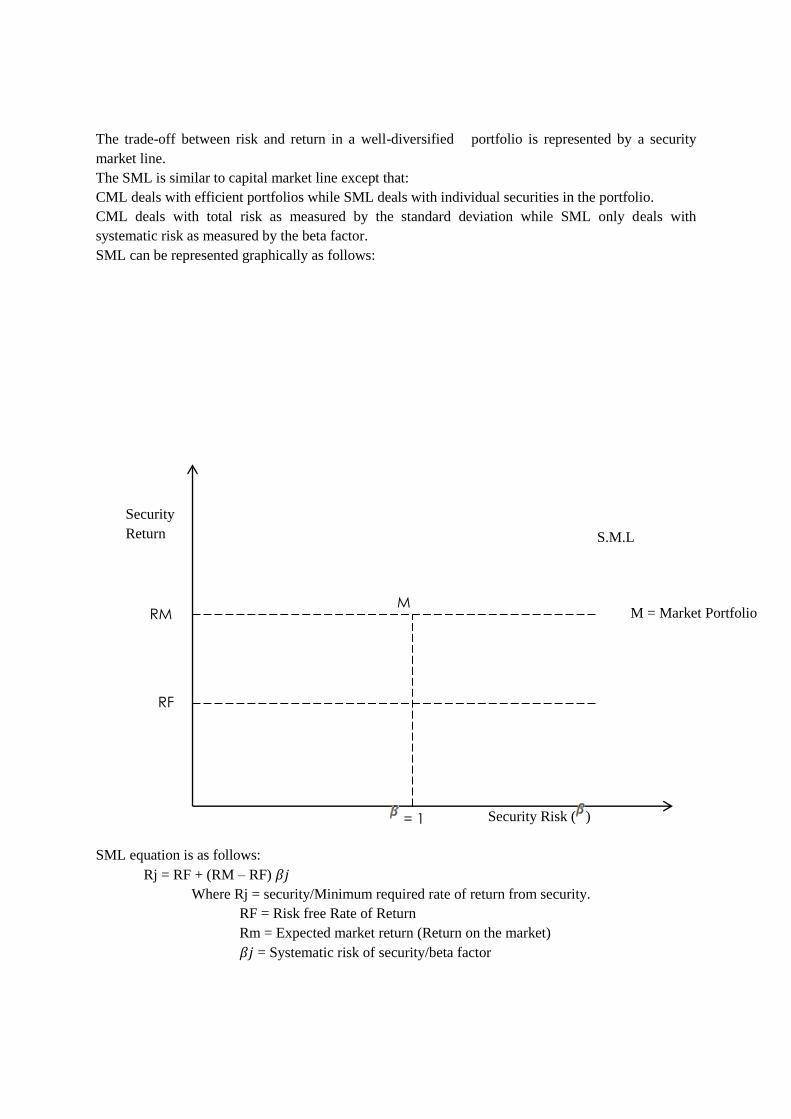

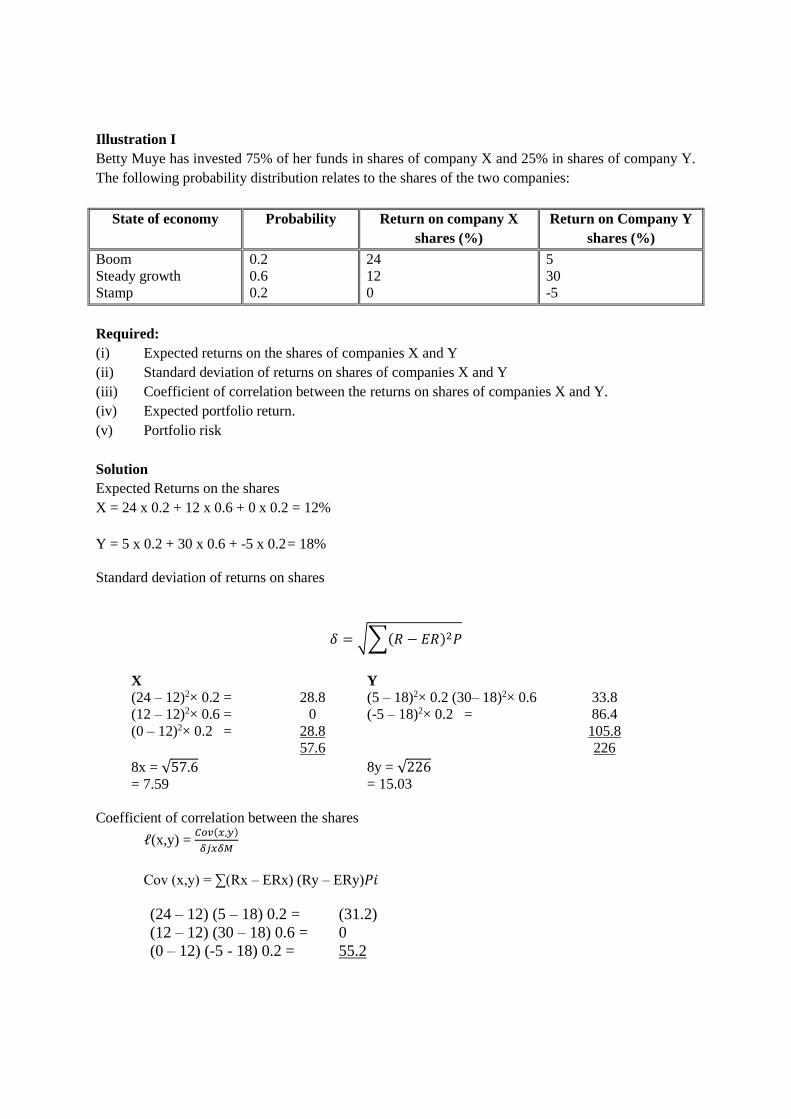

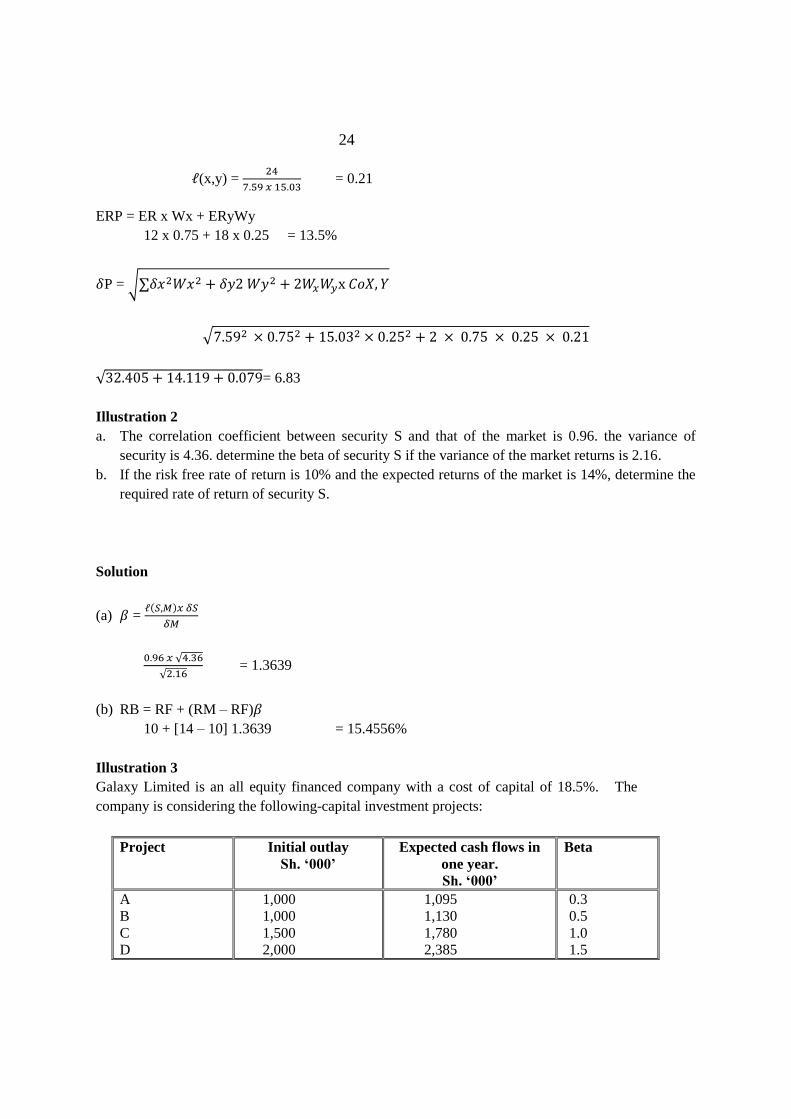

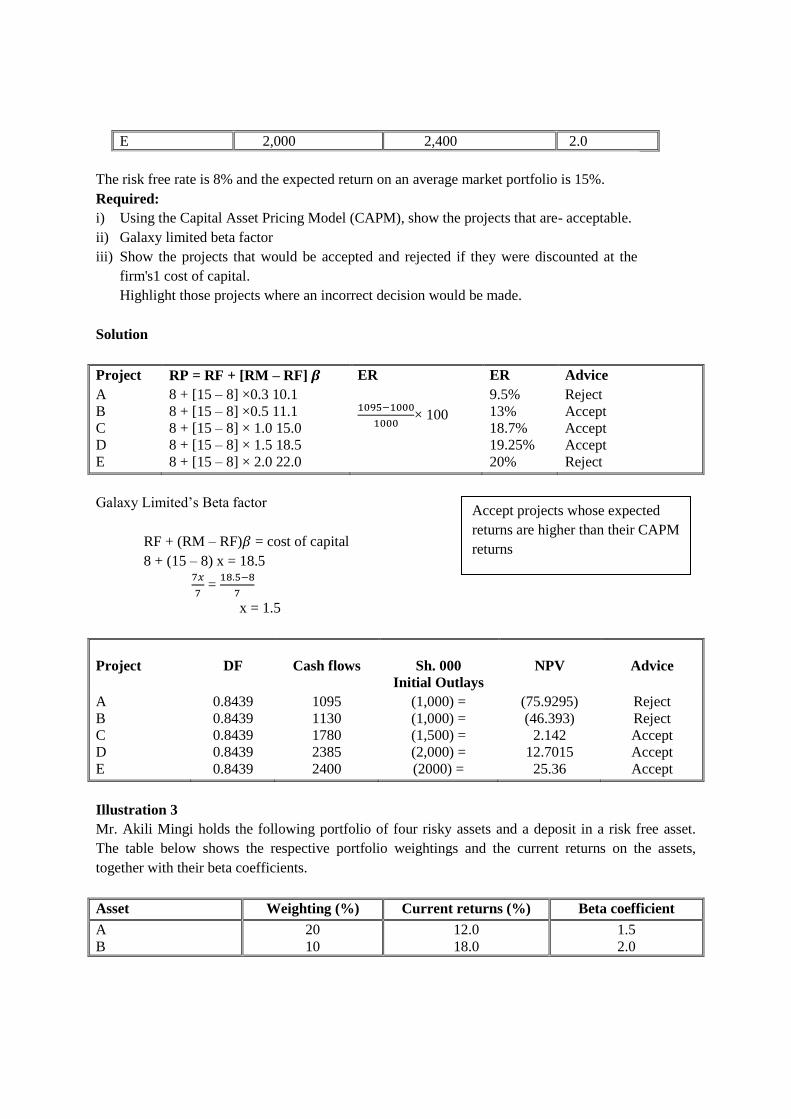

15.2Portfolio theory and analysis:

- The modern portfolio theory: background of the theory; portfolio expected return; the actual

and weighted portfolio risk; derivation of efficient sets; the capital market line (CML) model

and its applications, the mean variance dominance rule; short comings of portfolio theory

- Capital Asset Pricing Model-CAPM : background of the theory; assumptions; beta estimation

- beta coefficient of an individual asset and that of a portfolio and the interpretation of the

result; security market line(SML) model and its applications; conceptual differences between

portfolio theory and capital asset pricing model

- Shortcomings of the capital asset pricing model

- The Arbitrage pricing model (APM) and other multifactor models: background of the theory;

conceptual differences between the Capital asset pricing model and the Arbitrage pricing

model; application of the Arbitrage pricing model, shortcomings of Arbitrage pricing model;

Pastor Stambaugh model

- Evaluation of portfolio performance: Treynor’s measure, Sharpe’s measure, Jensen’s

measure, appraisal ratio measure, information ratio, Modigliani and Modigliani (M2)

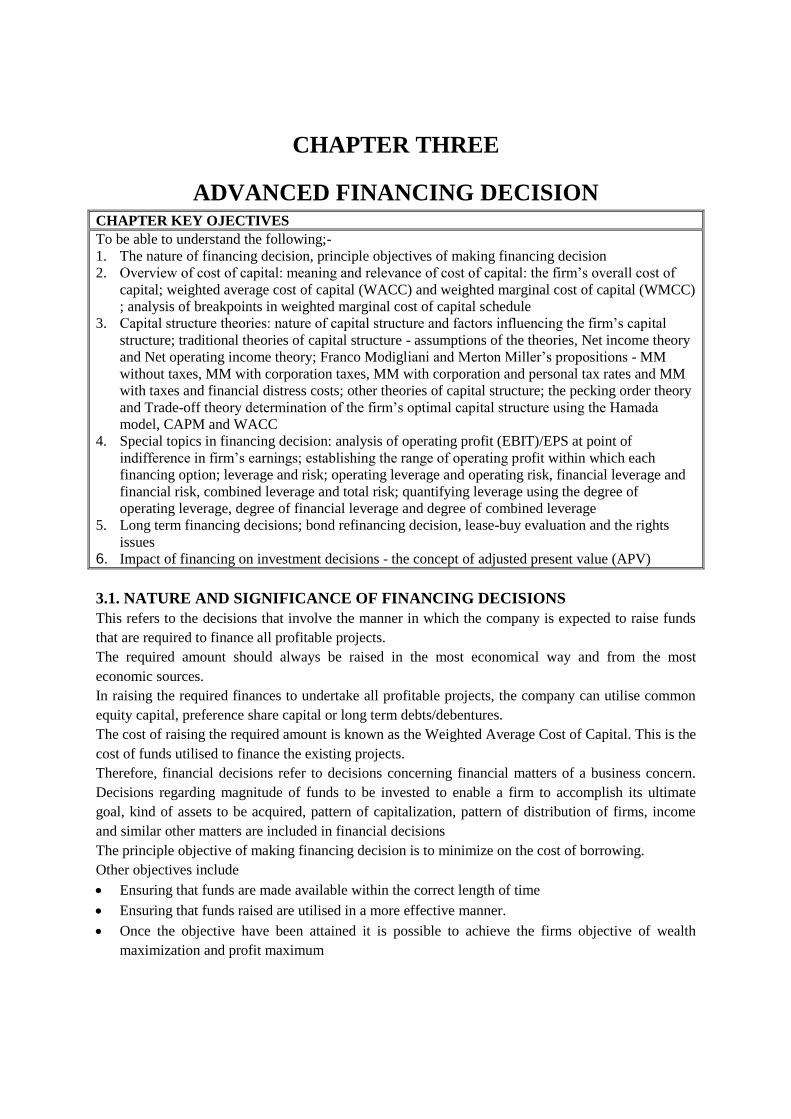

15.3Advanced financing decision

- The nature of financing decision, principle objectives of making financing decision

Page 2

- Overview of cost of capital: meaning and relevance of cost of capital: the firm’s overall cost

of capital; weighted average cost of capital (WACC) and weighted marginal cost of capital

(WMCC) ; analysis of breakpoints in weighted marginal cost of capital schedule

- Capital structure theories: nature of capital structure and factors influencing the firm’s capital

structure; traditional theories of capital structure - assumptions of the theories, Net income

theory and Net operating income theory; Franco Modigliani and Merton Miller’s propositions

- MM without taxes, MM with corporation taxes, MM with corporation and personal tax rates

and MM with taxes and financial distress costs; other theories of capital structure; the pecking

order theory and Trade-off theory determination of the firm’s optimal capital structure using

the Hamada model, CAPM and WACC

- Special topics in financing decision: analysis of operating profit (EBIT)/EPS at point of

indifference in firm’s earnings; establishing the range of operating profit within which each

financing option; leverage and risk; operating leverage and operating risk, financial leverage

and financial risk, combined leverage and total risk; quantifying leverage using the degree of

operating leverage, degree of financial leverage and degree of combined leverage

- Long term financing decisions; bond refinancing decision, lease-buy evaluation and the rights

issues

- Impact of financing on investment decisions - the concept of adjusted present value (APV)

15.4Mergers and acquisitions

- Nature of mergers and acquisitions

- Reasons of mergers and acquisitions

- Acquisition and Mergers verses organic growth

- Valuation of acquisitions and mergers

- Prediction of a takeover target

- Defence tactics against hostile takeovers

- Financing of mergers and acquisitions

- Analysis of combined operating profit (EBIT) and post-acquisition earning per share at the

point of indifference in firms earnings under various financing options.

- Determination of range of combined operating profit.

- Regulatory frame work for mergers and acquisitions

- Reasons why there are failed mergers and acquisitions

- Mergers and acquisitions in a global context

15.5Corporate restructuring and re-organisation

- Background on restructuring and re organisation

- Indicators/symptoms of restructuring

- Considerations in designing an appropriate restructuring programme

- Financial reconstruction: forms of financial reconstruction; impact of financial reconstruction

on share price; impact of financial reconstruction on the weighted Average cost of capital

(WACC)

- Portfolio reconstruction: various ways of unbundling a firm: divestment, de-merger, spin-off,

liquidation, sell-offs, equity curve outs, strategic alliances, management buyout, leveraged

buyouts and the management buy-ins.

- The relevance of the various forms of portfolio reconstruction

- Organisational reconstruction: The nature and benefits of this form of restructuring; models of

predicting corporate failure; Multiple discriminant analysis (Z-Score model), Beaver failure

ratio, Argenti model, Taffler’s model

- Causes of financial distress

Page 3

- Forms of financial distress and solutions to financial distress

15.6Derivatives in financial risk management

- The meaning, nature and importance of derivative instruments: futures, forwards, options and

swaps

- Pricing and valuations of derivatives: futures, forwards, options and swaps

- Types of risks: operational risks, political risks, economic risks, fiscal risks, regulatory risks,

currency risks and interest rate risks

- Foreign currency risk management: Types of forex risks, hedging currency risks, forward

contracts, money market hedge, currency options, currency futures and currency swaps

- Interest rate risks: Term structure of interest rates, forward rate agreement, interest rate

futures, interest rate swaps, interest rate options

15.7International financial management

- International investments

- International financial markets

- International financial institutions

- Methods of financing international trade

- International parity conditions: Interest rate parity, purchasing power parity and International

fisher effect

- International arbitrage: locational arbitrage, triangular arbitrage and covered interest arbitrage

- Divided policy for multinationals

- International debt instruments: International bonds (euro bond), certificate of deposits,

securitisation of loans, commercial paper

- Availability and timing of remittances

- Transfer pricing: impact on taxes and dividends

15.8Real estate finance

- Overview of real estate business - nature of real estate business, legal and economic

framework and participants in real estate business in Kenya

- Valuation approaches (income, cost and sales comparison approaches)

- REITS: types; advantages and disadvantages; valuation: net asset value per share (NAVPS);

use of funds from operations (FFO), adjusted funds from operations (AFFO) in REIT

valuation

- Instruments of real estate financing - mortgages, lien, title, mortgage requirements and

mortgage clauses

- Rights in case of debt - default and its consequence, equity of redemption, foreclosure,

statutory redemptions

- Mortgage and financial markets: demand for funds in mortgage market, disintermediation

effects, primary and secondary mortgage market, mortgage market and cost of money, role of

central bank and the role of government in mortgage markets

- Savings and loan association - classification, state accounts, insurers. Mortgage backed bonds

and services

15.9 Emerging issues and trends

Page 4

CONTENT PAGE

Topic 1: Advanced capital budgeting decision…………………………….…….…6

Topic 2: Portfolio theory and analysis…………………………………………..…69

Topic 4: Advanced financing decision……………………………………………112

Topic 4: Mergers and acquisitions………………………………………..…….…186

Topic 5: Corporate restructuring and re-organisation…………….………….……217

Topic 6: Derivatives in financial risk management……………………….………228

Topic 7: International financial management………………………………..……283

Topic 8: Real estate finance……………………………………………….…....…306

Page 5

CHAPTER ONE

ADVANCED CAPITAL BUDGETING DECISION

CHAPTER KEY OBJECTIVES

To be able to understand the following with regard to capital budgeting decisions;-

1. Incorporating risk/uncertainty in capital investment decisions

2. Nature and measurement of risk and uncertainty

3. Techniques of handling risk: sensitivity analysis, scenario analysis, decision trees, simulation

analysis, utility analysis, risk adjusted discounting rate(RADR) and certainty equivalent method

4. Incorporating capital rationing in capital investment appraisal

5. Incorporating inflation in capital investment appraisal

6. Evaluation of projects of unequal lives

7. The real options-strategic investment option, timing option, abandonment option and the

replacement option

8. Common capital budgeting pitfalls

1.1 INTRODUCTION

These decisions involve investing of a company’s funds in long term projects that are more beneficial

to the firm i.e. projects that aim at maximisation of shareholders’ wealth or value of the firm. It is the

process of determining viability of projects.

Capital investment refers to the real act of expenditure that involves allocation of capital/resources

the available company projects.

Capital Budgeting refers to the process of planning and evaluating the profitability/viability of the

available projects to be undertaken with an aim of implementing the most profitable i.e. the project

that would maximise the value of the firm/shareholders wealth.

Importance of capital budgeting.

Most projects involve a heavy investment of funds, which may lead to significant losses if not

properly planned.

Such decisions would affect the long-term growth of the firm. Profitable projects would increase

the value of the firm and the shareholders’ wealth, which is the main objective of any company.

Such decisions are largely irreversible and if reversed it will be at a substantial loss.

1.2 INCORPORATING RISK/UNCERTAINTY IN CAPITAL INVESTMENT

DECISIONS

Investment Decisions under Uncertainty/Risk

Investment appraisal faces the following problems;

The decisions made are based on forecasted cash flows

Page 6

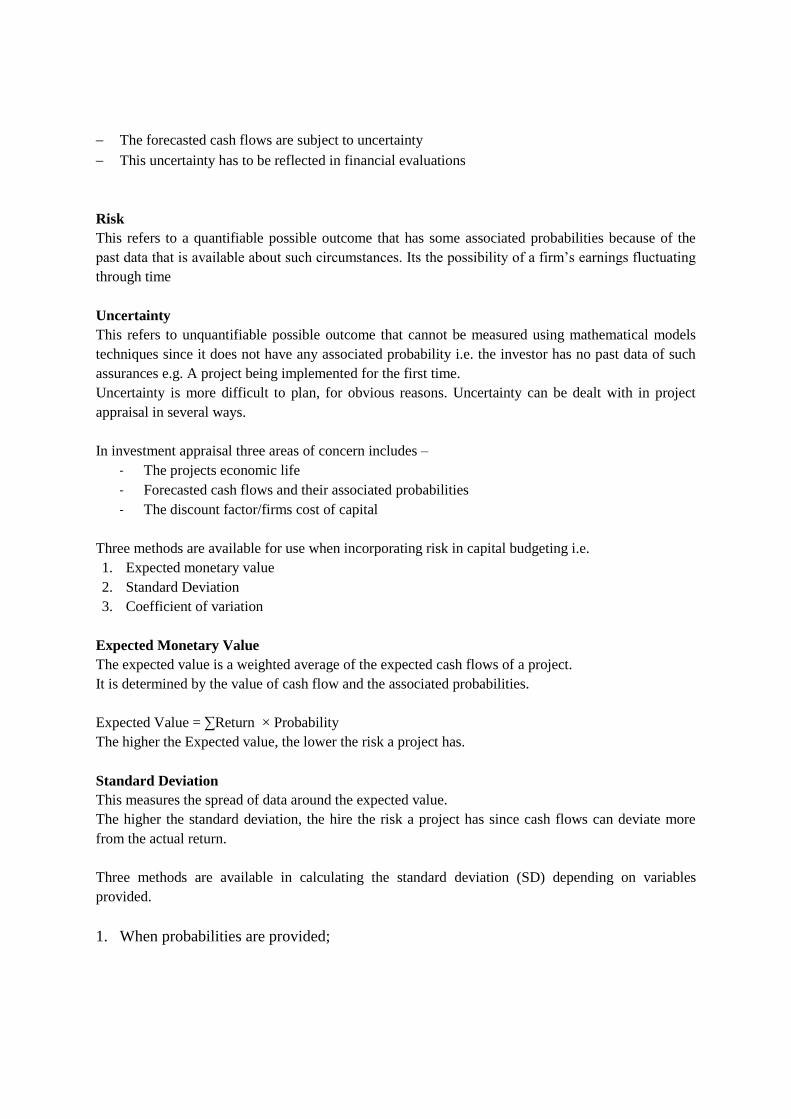

The forecasted cash flows are subject to uncertainty

This uncertainty has to be reflected in financial evaluations

Risk

This refers to a quantifiable possible outcome that has some associated probabilities because of the

past data that is available about such circumstances. Its the possibility of a firm’s earnings fluctuating

through time

Uncertainty

This refers to unquantifiable possible outcome that cannot be measured using mathematical models

techniques since it does not have any associated probability i.e. the investor has no past data of such

assurances e.g. A project being implemented for the first time.

Uncertainty is more difficult to plan, for obvious reasons. Uncertainty can be dealt with in project

appraisal in several ways.

In investment appraisal three areas of concern includes –

- The projects economic life

- Forecasted cash flows and their associated probabilities

- The discount factor/firms cost of capital

Three methods are available for use when incorporating risk in capital budgeting i.e.

1. Expected monetary value

2. Standard Deviation

3. Coefficient of variation

Expected Monetary Value

The expected value is a weighted average of the expected cash flows of a project.

It is determined by the value of cash flow and the associated probabilities.

Expected Value = ∑Return × Probability

The higher the Expected value, the lower the risk a project has.

Standard Deviation

This measures the spread of data around the expected value.

The higher the standard deviation, the hire the risk a project has since cash flows can deviate more

from the actual return.

Three methods are available in calculating the standard deviation (SD) depending on variables

provided.

1. When probabilities are provided;

Page 7

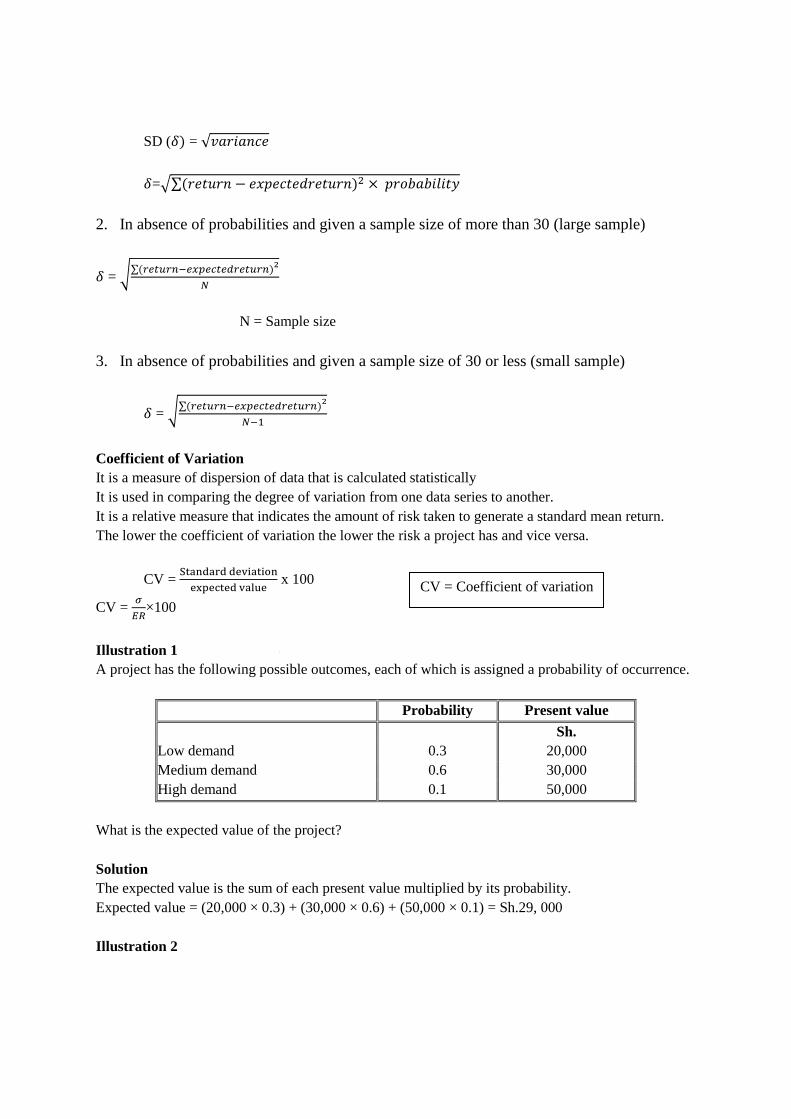

SD (𝛿) = √𝑣𝑎𝑟𝑖𝑎𝑛𝑐𝑒

𝛿=√∑(𝑟𝑒𝑡𝑢𝑟𝑛 − 𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑𝑟𝑒𝑡𝑢𝑟𝑛)2 × 𝑝𝑟𝑜𝑏𝑎𝑏𝑖𝑙𝑖𝑡𝑦

2. In absence of probabilities and given a sample size of more than 30 (large sample)

𝛿 = √∑(𝑟𝑒𝑡𝑢𝑟𝑛−𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑𝑟𝑒𝑡𝑢𝑟𝑛)

2

𝑁

N = Sample size

3. In absence of probabilities and given a sample size of 30 or less (small sample)

𝛿 = √∑(𝑟𝑒𝑡𝑢𝑟𝑛−𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑𝑟𝑒𝑡𝑢𝑟𝑛)

2

𝑁−1

Coefficient of Variation

It is a measure of dispersion of data that is calculated statistically

It is used in comparing the degree of variation from one data series to another.

It is a relative measure that indicates the amount of risk taken to generate a standard mean return.

The lower the coefficient of variation the lower the risk a project has and vice versa.

CV = Standard deviation

expected value x 100

CV = 𝜎

𝐸𝑅×100

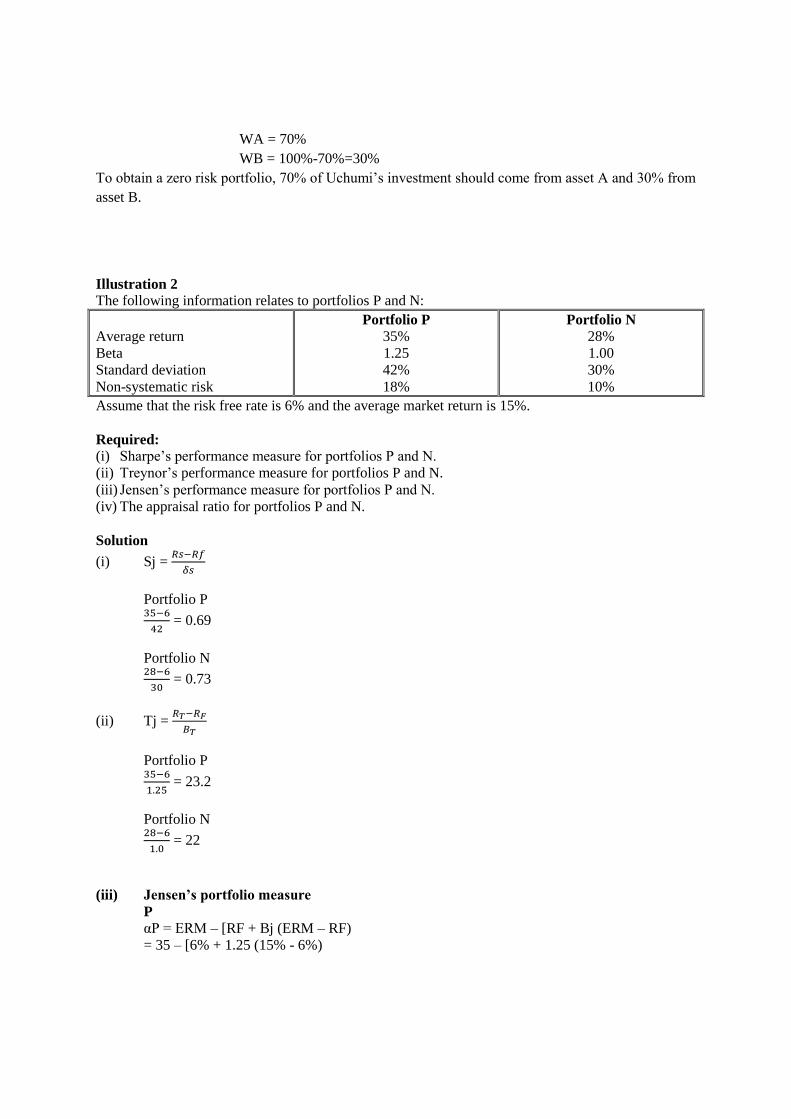

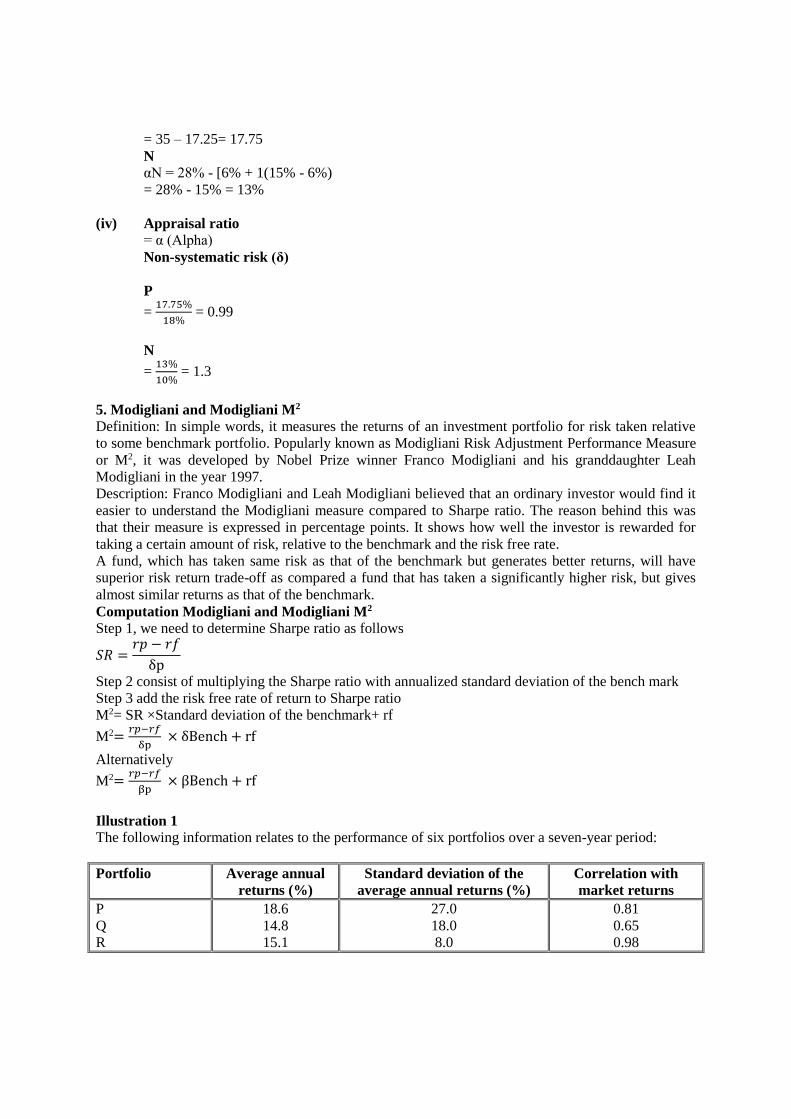

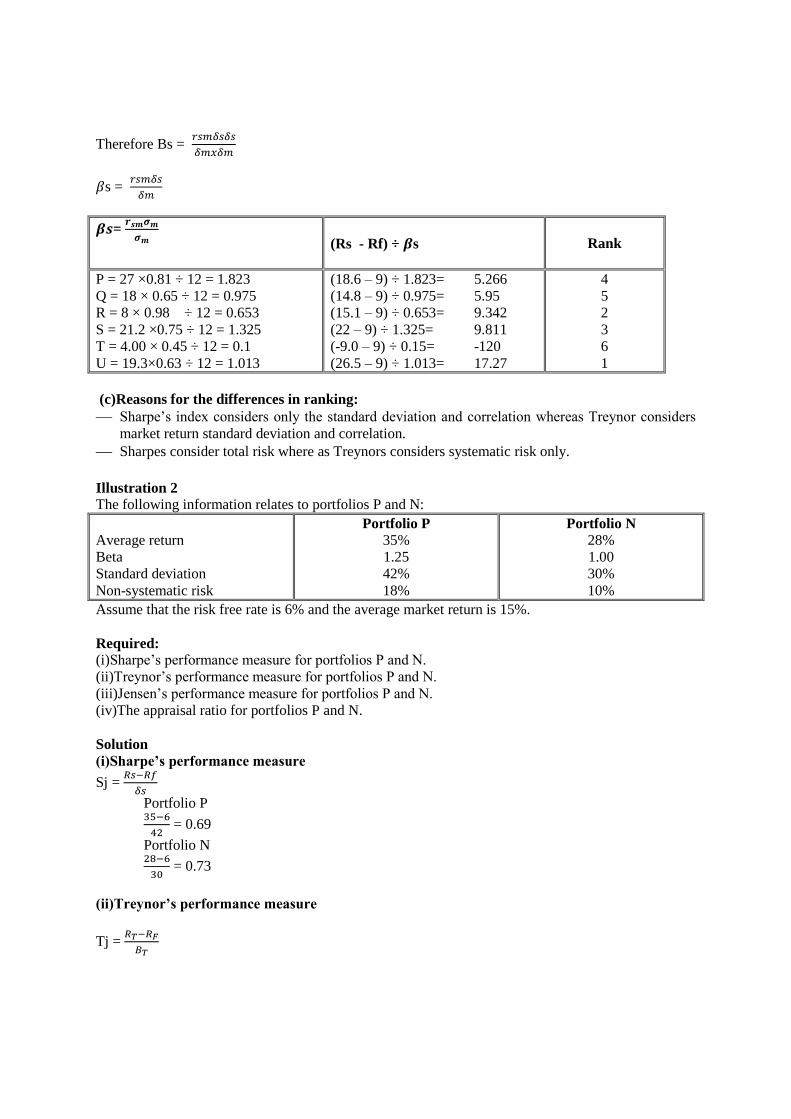

Illustration 1

A project has the following possible outcomes, each of which is assigned a probability of occurrence.

Probability Present value

Sh.

Low demand 0.3 20,000

Medium demand 0.6 30,000

High demand 0.1 50,000

What is the expected value of the project?

Solution

The expected value is the sum of each present value multiplied by its probability.

Expected value = (20,000 × 0.3) + (30,000 × 0.6) + (50,000 × 0.1) = Sh.29, 000

Illustration 2

CV = Coefficient of variation

Page 8

What would happen to the expected value of the project above if the probability of medium demand

fell to 0.4 and the probability of low demand increased to 0.5?

Solution

Expected value = (20,000 x 0.5) + (30,000 x 0.4) + (50,000 x 0.1) = sh.27, 000

The project is riskier than before, as there is a greater probability of demand being low, which results

in a lower expected value.

Illustration 3

Tajiri Ltd is considering investment of sh.50, 000,000. The estimated annual net cash inflows over the

next five years under the three states of nature are as follows:

Project A

State of nature Probability Amount

Sh. “000”

Most pessimistic

Most likely

Most optimistic

0.25

0.50

0.25

13,500

18,000

20,000

Concerns have been raised about the possibility that this project will infringe on a competitor’s patent.

If this was the case and the competitor successfully pursued a claim for damages, the competitor may

have to be paid as much as sh.100, 000,000 in the third year. Lawyers estimate that there is only a 0.1

probability that this will happen.

Project B

This project will require an initial outlay of sh.50, 000,000 spread in equal instalments over the next

three years to finance a research project. If this project is successful and there is a probability of 0.5 of

this happening, it will lead to issuance of a patent right with an estimated value at the end of the end

of the three years of sh.200, 000,000. If not successful, the whole of the expenditure would have to be

written off.

Project C

This project will have an initial cost of sh.20, 000,000 and is expected to yield annual cash flows of

sh.8,000,000 in each of its first two years. Thereafter, the outcome is so uncertain that no estimate can

be given.

The company’s cost of capital is 14% per annum.

Required;-

Advise Tajiri Ltd on whether they should undertake the projects above.

Solution

Page 9

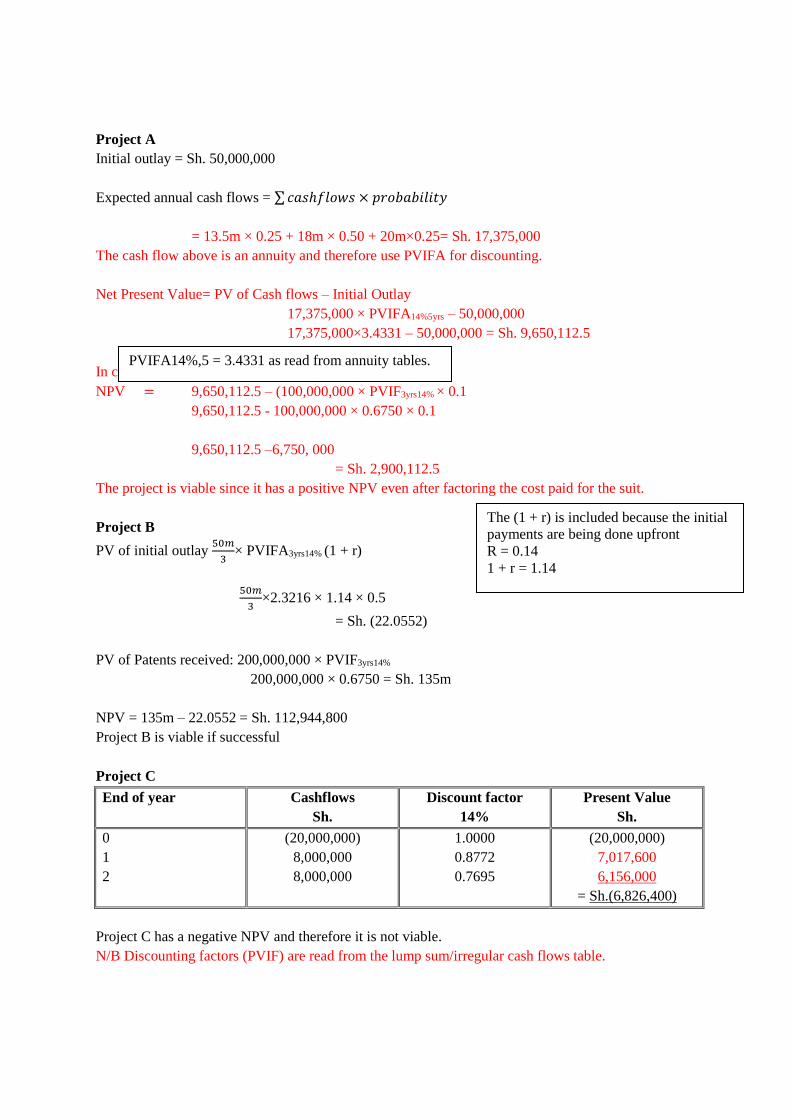

Project A

Initial outlay = Sh. 50,000,000

Expected annual cash flows = ∑ 𝑐𝑎𝑠ℎ𝑓𝑙𝑜𝑤𝑠 × 𝑝𝑟𝑜𝑏𝑎𝑏𝑖𝑙𝑖𝑡𝑦

= 13.5m × 0.25 + 18m × 0.50 + 20m×0.25= Sh. 17,375,000

The cash flow above is an annuity and therefore use PVIFA for discounting.

Net Present Value= PV of Cash flows – Initial Outlay

17,375,000 × PVIFA14%5yrs – 50,000,000

17,375,000×3.4331 – 50,000,000 = Sh. 9,650,112.5

In case the competitor succeeds in the suit

NPV = 9,650,112.5 – (100,000,000 × PVIF3yrs14% × 0.1

9,650,112.5 - 100,000,000 × 0.6750 × 0.1

9,650,112.5 –6,750, 000

= Sh. 2,900,112.5

The project is viable since it has a positive NPV even after factoring the cost paid for the suit.

Project B

PV of initial outlay 50𝑚

3× PVIFA3yrs14% (1 + r)

50𝑚

3×2.3216 × 1.14 × 0.5

= Sh. (22.0552)

PV of Patents received: 200,000,000 × PVIF3yrs14%

200,000,000 × 0.6750 = Sh. 135m

NPV = 135m – 22.0552 = Sh. 112,944,800

Project B is viable if successful

Project C

End of year Cashflows

Sh.

Discount factor

14%

Present Value

Sh.

0

1

2

(20,000,000)

8,000,000

8,000,000

1.0000

0.8772

0.7695

(20,000,000)

7,017,600

6,156,000

= Sh.(6,826,400)

Project C has a negative NPV and therefore it is not viable.

N/B Discounting factors (PVIF) are read from the lump sum/irregular cash flows table.

The (1 + r) is included because the initial

payments are being done upfront

R = 0.14

1 + r = 1.14

PVIFA14%,5 = 3.4331 as read from annuity tables.

Page 10

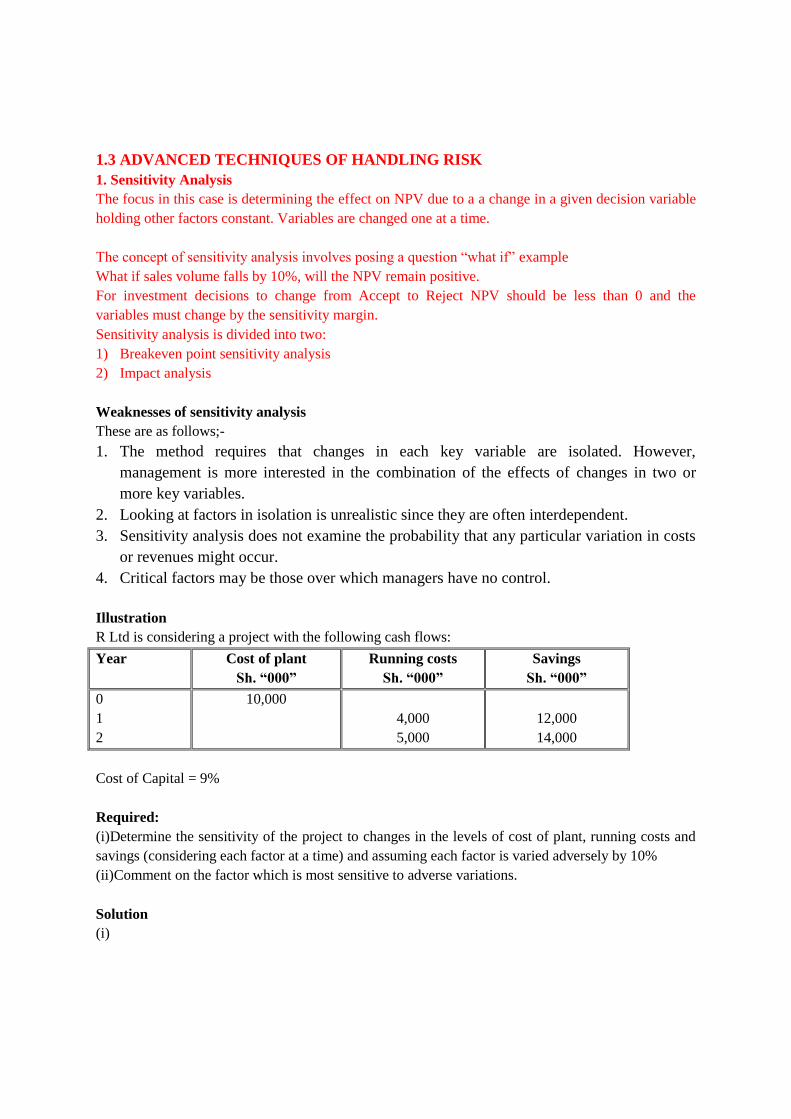

1.3 ADVANCED TECHNIQUES OF HANDLING RISK

1. Sensitivity Analysis

The focus in this case is determining the effect on NPV due to a a change in a given decision variable

holding other factors constant. Variables are changed one at a time.

The concept of sensitivity analysis involves posing a question “what if” example

What if sales volume falls by 10%, will the NPV remain positive.

For investment decisions to change from Accept to Reject NPV should be less than 0 and the

variables must change by the sensitivity margin.

Sensitivity analysis is divided into two:

1) Breakeven point sensitivity analysis

2) Impact analysis

Weaknesses of sensitivity analysis

These are as follows;-

1. The method requires that changes in each key variable are isolated. However,

management is more interested in the combination of the effects of changes in two or

more key variables.

2. Looking at factors in isolation is unrealistic since they are often interdependent.

3. Sensitivity analysis does not examine the probability that any particular variation in costs

or revenues might occur.

4. Critical factors may be those over which managers have no control.

Illustration

R Ltd is considering a project with the following cash flows:

Year Cost of plant

Sh. “000”

Running costs

Sh. “000”

Savings

Sh. “000”

0

1

2

10,000

4,000

5,000

12,000

14,000

Cost of Capital = 9%

Required:

(i)Determine the sensitivity of the project to changes in the levels of cost of plant, running costs and

savings (considering each factor at a time) and assuming each factor is varied adversely by 10%

(ii)Comment on the factor which is most sensitive to adverse variations.

Solution

(i)

Page 11

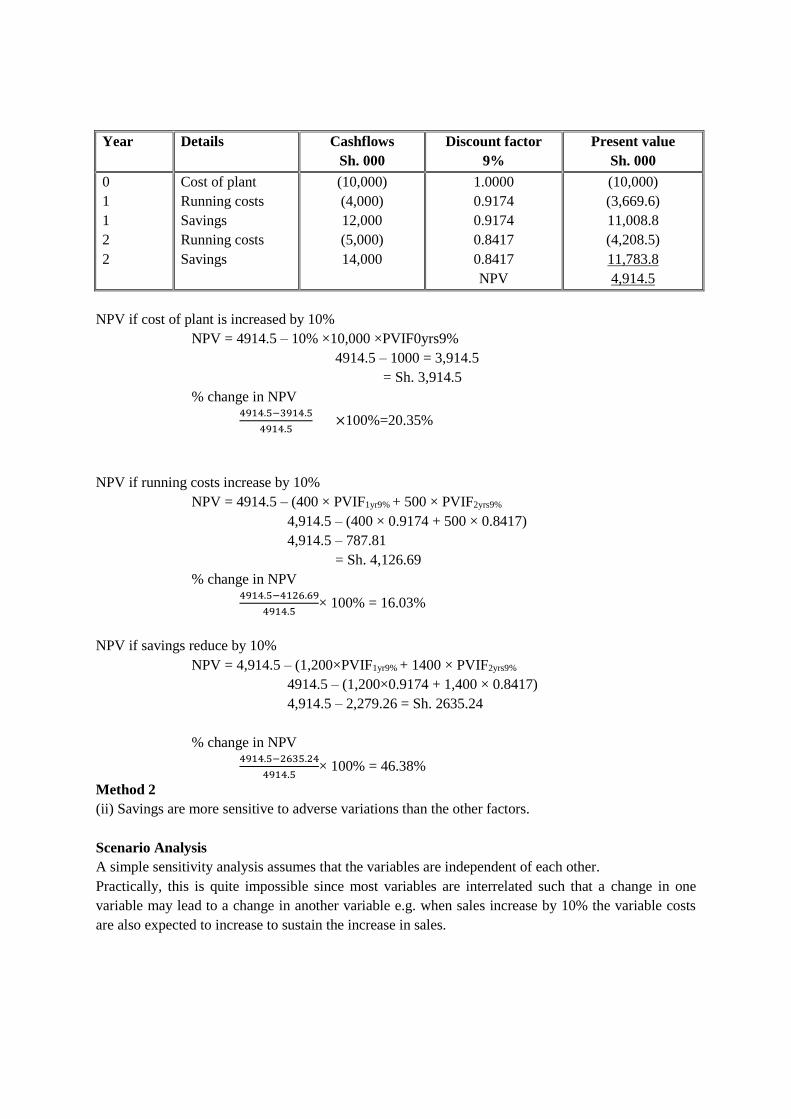

Year Details Cashflows

Sh. 000

Discount factor

9%

Present value

Sh. 000

0

1

1

2

2

Cost of plant

Running costs

Savings

Running costs

Savings

(10,000)

(4,000)

12,000

(5,000)

14,000

1.0000

0.9174

0.9174

0.8417

0.8417

NPV

(10,000)

(3,669.6)

11,008.8

(4,208.5)

11,783.8

4,914.5

NPV if cost of plant is increased by 10%

NPV = 4914.5 – 10% ×10,000 ×PVIF0yrs9%

4914.5 – 1000 = 3,914.5

= Sh. 3,914.5

% change in NPV

4914.5−3914.5

4914.5 ×100%=20.35%

NPV if running costs increase by 10%

NPV = 4914.5 – (400 × PVIF1yr9% + 500 × PVIF2yrs9%

4,914.5 – (400 × 0.9174 + 500 × 0.8417)

4,914.5 – 787.81

= Sh. 4,126.69

% change in NPV

4914.5−4126.69

4914.5× 100% = 16.03%

NPV if savings reduce by 10%

NPV = 4,914.5 – (1,200×PVIF1yr9% + 1400 × PVIF2yrs9%

4914.5 – (1,200×0.9174 + 1,400 × 0.8417)

4,914.5 – 2,279.26 = Sh. 2635.24

% change in NPV

4914.5−2635.24

4914.5× 100% = 46.38%

Method 2

(ii) Savings are more sensitive to adverse variations than the other factors.

Scenario Analysis

A simple sensitivity analysis assumes that the variables are independent of each other.

Practically, this is quite impossible since most variables are interrelated such that a change in one

variable may lead to a change in another variable e.g. when sales increase by 10% the variable costs

are also expected to increase to sustain the increase in sales.

Page 12

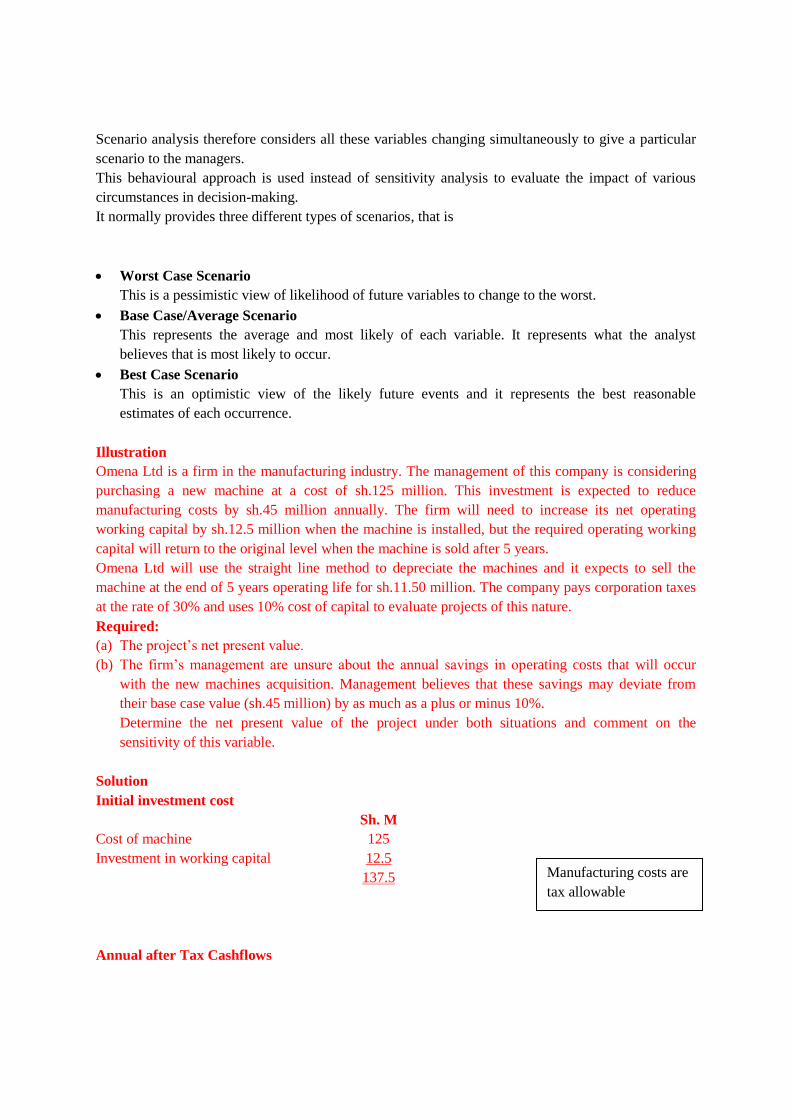

Scenario analysis therefore considers all these variables changing simultaneously to give a particular

scenario to the managers.

This behavioural approach is used instead of sensitivity analysis to evaluate the impact of various

circumstances in decision-making.

It normally provides three different types of scenarios, that is

Worst Case Scenario

This is a pessimistic view of likelihood of future variables to change to the worst.

Base Case/Average Scenario

This represents the average and most likely of each variable. It represents what the analyst

believes that is most likely to occur.

Best Case Scenario

This is an optimistic view of the likely future events and it represents the best reasonable

estimates of each occurrence.

Illustration

Omena Ltd is a firm in the manufacturing industry. The management of this company is considering

purchasing a new machine at a cost of sh.125 million. This investment is expected to reduce

manufacturing costs by sh.45 million annually. The firm will need to increase its net operating

working capital by sh.12.5 million when the machine is installed, but the required operating working

capital will return to the original level when the machine is sold after 5 years.

Omena Ltd will use the straight line method to depreciate the machines and it expects to sell the

machine at the end of 5 years operating life for sh.11.50 million. The company pays corporation taxes

at the rate of 30% and uses 10% cost of capital to evaluate projects of this nature.

Required:

(a) The project’s net present value.

(b) The firm’s management are unsure about the annual savings in operating costs that will occur

with the new machines acquisition. Management believes that these savings may deviate from

their base case value (sh.45 million) by as much as a plus or minus 10%.

Determine the net present value of the project under both situations and comment on the

sensitivity of this variable.

Solution

Initial investment cost

Sh. M

Cost of machine

Investment in working capital

125

12.5

137.5

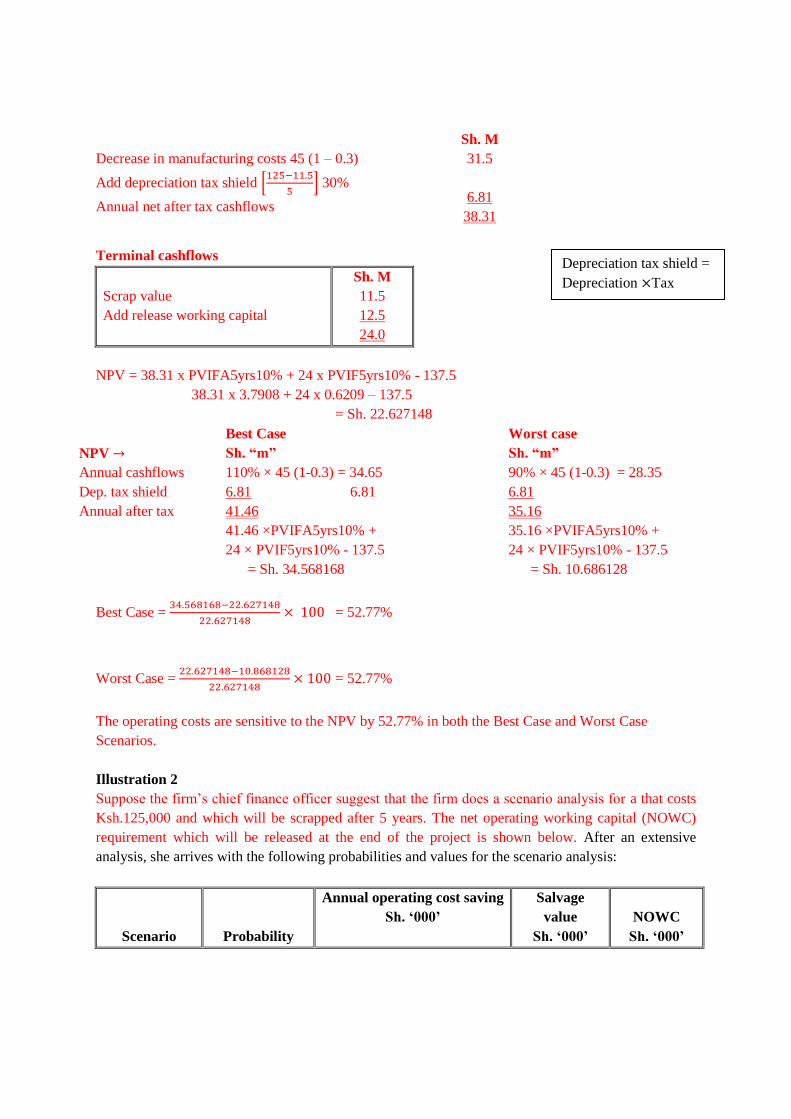

Annual after Tax Cashflows

Manufacturing costs are

tax allowable

Page 13

Sh. M

Decrease in manufacturing costs 45 (1 – 0.3)

Add depreciation tax shield [125−11.5

5] 30%

Annual net after tax cashflows

31.5

6.81

38.31

Terminal cashflows

Scrap value

Add release working capital

Sh. M

11.5

12.5

24.0

NPV = 38.31 x PVIFA5yrs10% + 24 x PVIF5yrs10% - 137.5

38.31 x 3.7908 + 24 x 0.6209 – 137.5

= Sh. 22.627148

NPV →

Best Case

Sh. “m”

Worst case

Sh. “m”

Annual cashflows

Dep. tax shield

Annual after tax

110% × 45 (1-0.3) = 34.65

6.81 6.81

41.46

90% × 45 (1-0.3) = 28.35

6.81

35.16

41.46 ×PVIFA5yrs10% +

24 × PVIF5yrs10% - 137.5

= Sh. 34.568168

35.16 ×PVIFA5yrs10% +

24 × PVIF5yrs10% - 137.5

= Sh. 10.686128

Best Case = 34.568168−22.627148

22.627148× 100 = 52.77%

Worst Case = 22.627148−10.868128

22.627148× 100 = 52.77%

The operating costs are sensitive to the NPV by 52.77% in both the Best Case and Worst Case

Scenarios.

Illustration 2

Suppose the firm’s chief finance officer suggest that the firm does a scenario analysis for a that costs

Ksh.125,000 and which will be scrapped after 5 years. The net operating working capital (NOWC)

requirement which will be released at the end of the project is shown below. After an extensive

analysis, she arrives with the following probabilities and values for the scenario analysis:

Scenario

Probability

Annual operating cost saving

Sh. ‘000’

Salvage

value

Sh. ‘000’

NOWC

Sh. ‘000’

Depreciation tax shield =

Depreciation ×Tax

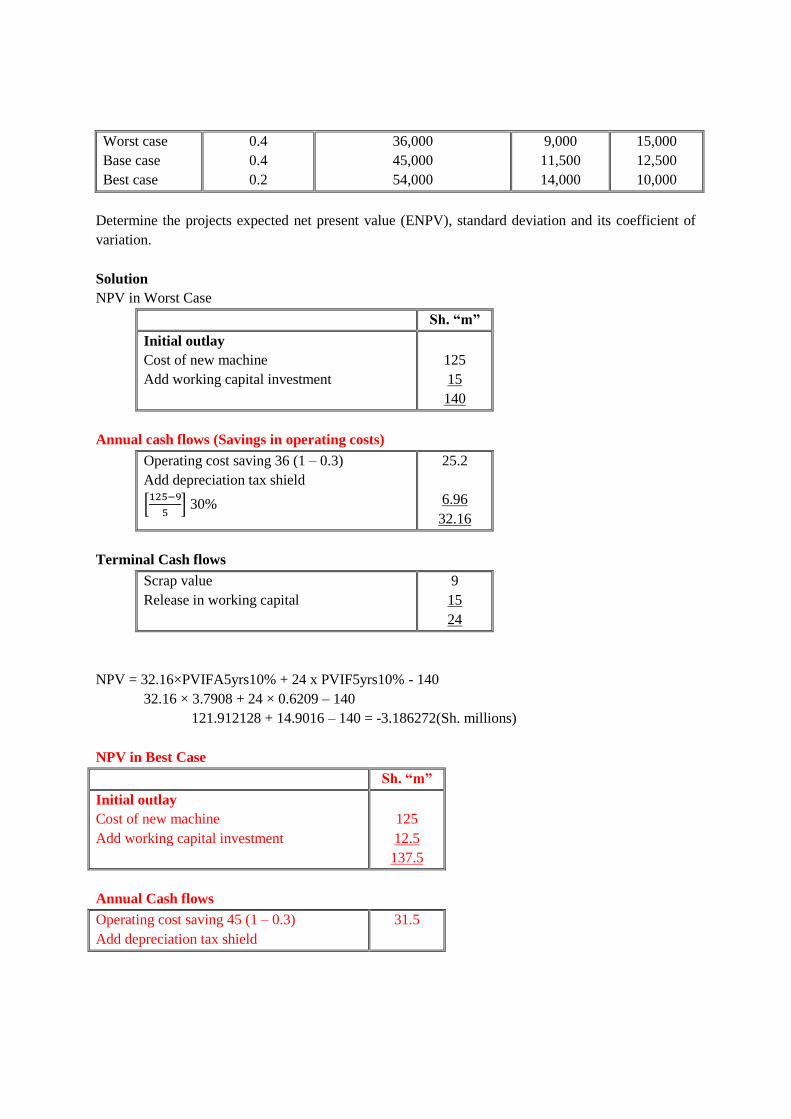

Page 14

Worst case

Base case

Best case

0.4

0.4

0.2

36,000

45,000

54,000

9,000

11,500

14,000

15,000

12,500

10,000

Determine the projects expected net present value (ENPV), standard deviation and its coefficient of

variation.

Solution

NPV in Worst Case

Sh. “m”

Initial outlay

Cost of new machine

Add working capital investment

125

15

140

Annual cash flows (Savings in operating costs)

Operating cost saving 36 (1 – 0.3)

Add depreciation tax shield

[125−9

5] 30%

25.2

6.96

32.16

Terminal Cash flows

Scrap value

Release in working capital

9

15

24

NPV = 32.16×PVIFA5yrs10% + 24 x PVIF5yrs10% - 140

32.16 × 3.7908 + 24 × 0.6209 – 140

121.912128 + 14.9016 – 140 = -3.186272(Sh. millions)

NPV in Best Case

Sh. “m”

Initial outlay

Cost of new machine

Add working capital investment

125

12.5

137.5

Annual Cash flows

Operating cost saving 45 (1 – 0.3)

Add depreciation tax shield

31.5

Page 15

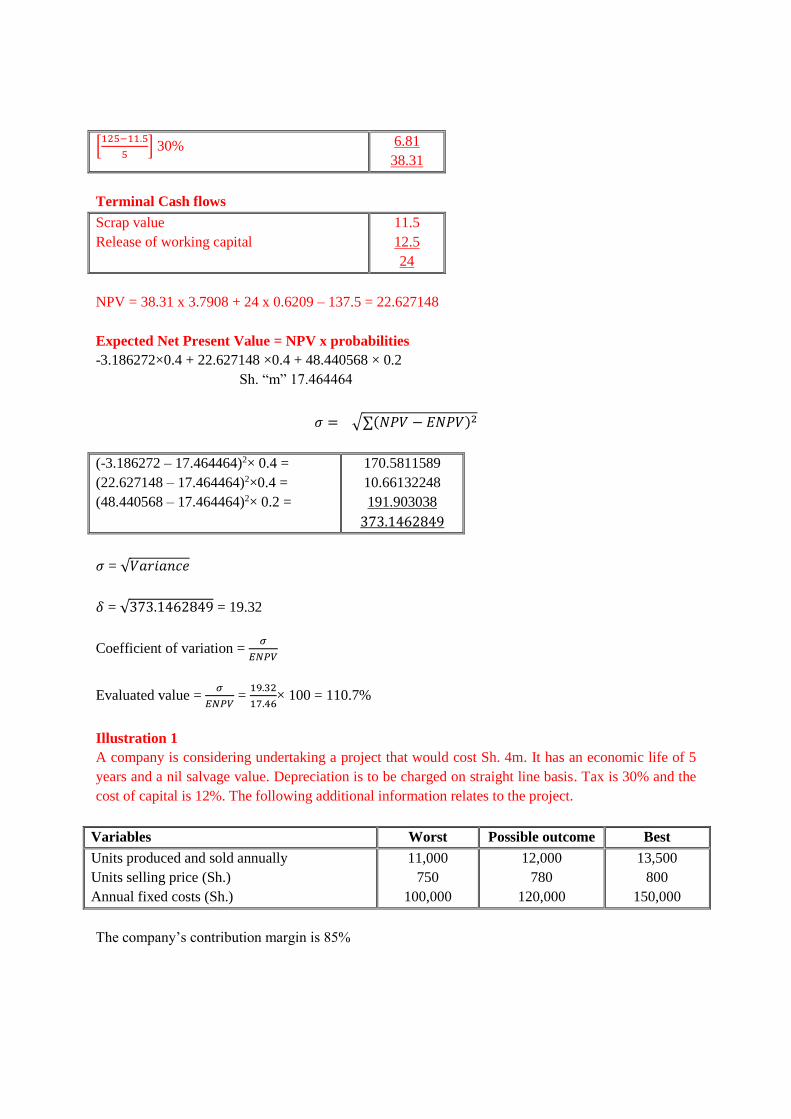

[125−11.5

5] 30% 6.81

38.31

Terminal Cash flows

Scrap value

Release of working capital

11.5

12.5

24

NPV = 38.31 x 3.7908 + 24 x 0.6209 – 137.5 = 22.627148

Expected Net Present Value = NPV x probabilities

-3.186272×0.4 + 22.627148 ×0.4 + 48.440568 × 0.2

Sh. “m” 17.464464

𝜎 = √∑(𝑁𝑃𝑉 − 𝐸𝑁𝑃𝑉)2

(-3.186272 – 17.464464)2× 0.4 =

(22.627148 – 17.464464)2×0.4 =

(48.440568 – 17.464464)2× 0.2 =

170.5811589

10.66132248

191.903038

373.1462849

𝜎 = √𝑉𝑎𝑟𝑖𝑎𝑛𝑐𝑒

𝛿 = √373.1462849 = 19.32

Coefficient of variation = 𝜎

𝐸𝑁𝑃𝑉

Evaluated value = 𝜎

𝐸𝑁𝑃𝑉 =

19.32

17.46× 100 = 110.7%

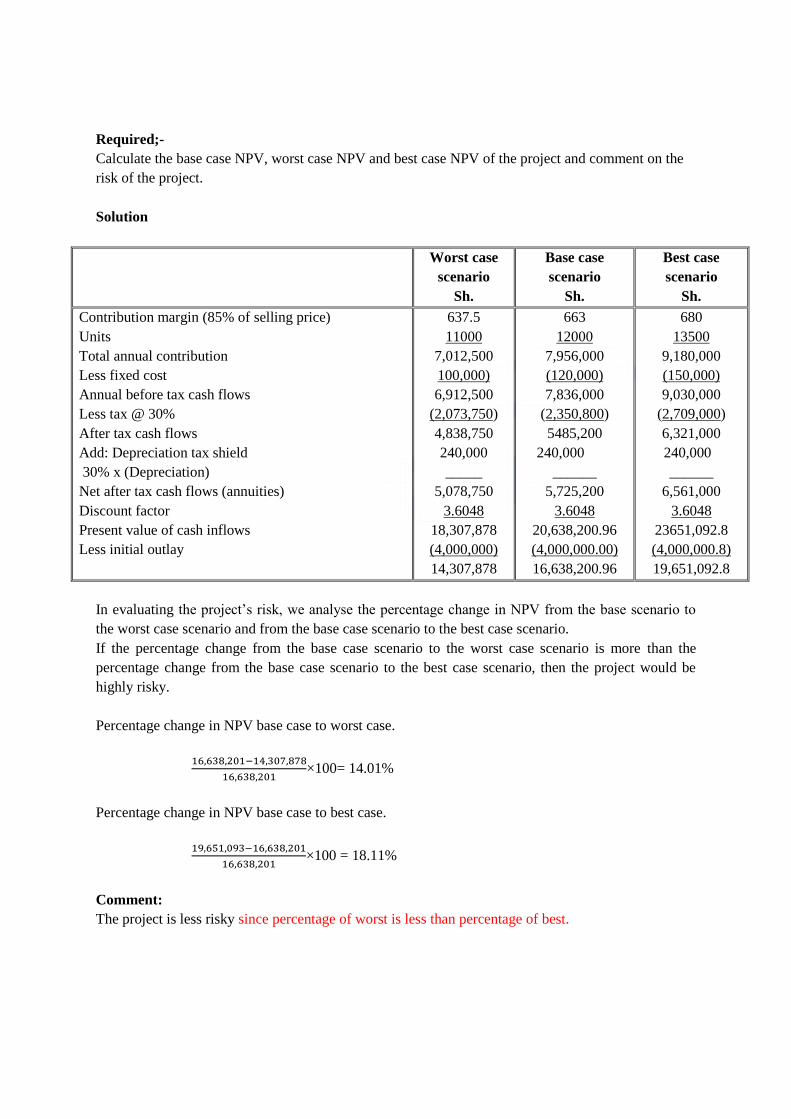

Illustration 1

A company is considering undertaking a project that would cost Sh. 4m. It has an economic life of 5

years and a nil salvage value. Depreciation is to be charged on straight line basis. Tax is 30% and the

cost of capital is 12%. The following additional information relates to the project.

Variables Worst Possible outcome Best

Units produced and sold annually

Units selling price (Sh.)

Annual fixed costs (Sh.)

11,000

750

100,000

12,000

780

120,000

13,500

800

150,000

The company’s contribution margin is 85%

Page 16

Required;-

Calculate the base case NPV, worst case NPV and best case NPV of the project and comment on the

risk of the project.

Solution

Worst case

scenario

Sh.

Base case

scenario

Sh.

Best case

scenario

Sh.

Contribution margin (85% of selling price)

Units

Total annual contribution

Less fixed cost

Annual before tax cash flows

Less tax @ 30%

After tax cash flows

Add: Depreciation tax shield

30% x (Depreciation)

Net after tax cash flows (annuities)

Discount factor

Present value of cash inflows

Less initial outlay

637.5

11000

7,012,500

100,000)

6,912,500

(2,073,750)

4,838,750

240,000

_____

5,078,750

3.6048

18,307,878

(4,000,000)

14,307,878

663

12000

7,956,000

(120,000)

7,836,000

(2,350,800)

5485,200

240,000

______

5,725,200

3.6048

20,638,200.96

(4,000,000.00)

16,638,200.96

680

13500

9,180,000

(150,000)

9,030,000

(2,709,000)

6,321,000

240,000

______

6,561,000

3.6048

23651,092.8

(4,000,000.8)

19,651,092.8

In evaluating the project’s risk, we analyse the percentage change in NPV from the base scenario to

the worst case scenario and from the base case scenario to the best case scenario.

If the percentage change from the base case scenario to the worst case scenario is more than the

percentage change from the base case scenario to the best case scenario, then the project would be

highly risky.

Percentage change in NPV base case to worst case.

16,638,201−14,307,878

16,638,201×100= 14.01%

Percentage change in NPV base case to best case.

19,651,093−16,638,201

16,638,201×100 = 18.11%

Comment:

The project is less risky since percentage of worst is less than percentage of best.

Page 17

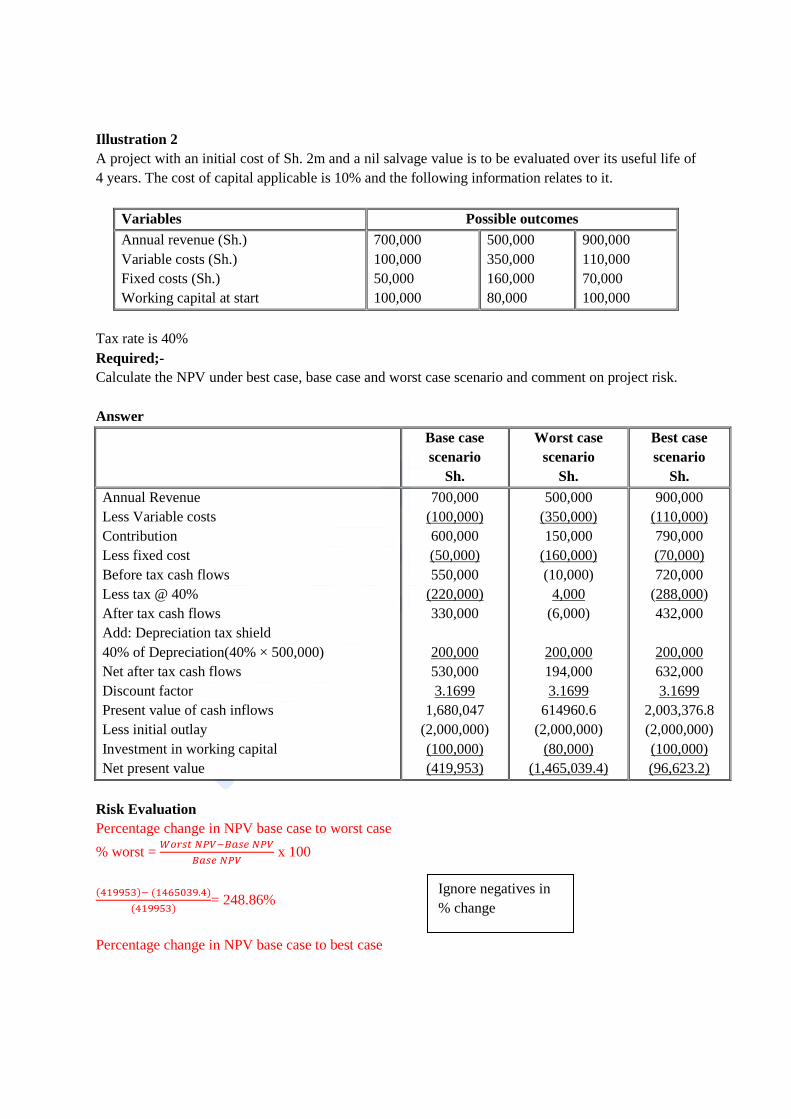

Illustration 2

A project with an initial cost of Sh. 2m and a nil salvage value is to be evaluated over its useful life of

4 years. The cost of capital applicable is 10% and the following information relates to it.

Variables Possible outcomes

Annual revenue (Sh.)

Variable costs (Sh.)

Fixed costs (Sh.)

Working capital at start

700,000

100,000

50,000

100,000

500,000

350,000

160,000

80,000

900,000

110,000

70,000

100,000

Tax rate is 40%

Required;-

Calculate the NPV under best case, base case and worst case scenario and comment on project risk.

Answer

Base case

scenario

Sh.

Worst case

scenario

Sh.

Best case

scenario

Sh.

Annual Revenue

Less Variable costs

Contribution

Less fixed cost

Before tax cash flows

Less tax @ 40%

After tax cash flows

Add: Depreciation tax shield

40% of Depreciation(40% × 500,000)

Net after tax cash flows

Discount factor

Present value of cash inflows

Less initial outlay

Investment in working capital

Net present value

700,000

(100,000)

600,000

(50,000)

550,000

(220,000)

330,000

200,000

530,000

3.1699

1,680,047

(2,000,000)

(100,000)

(419,953)

500,000

(350,000)

150,000

(160,000)

(10,000)

4,000

(6,000)

200,000

194,000

3.1699

614960.6

(2,000,000)

(80,000)

(1,465,039.4)

900,000

(110,000)

790,000

(70,000)

720,000

(288,000)

432,000

200,000

632,000

3.1699

2,003,376.8

(2,000,000)

(100,000)

(96,623.2)

Risk Evaluation

Percentage change in NPV base case to worst case

% worst = 𝑊𝑜𝑟𝑠𝑡 𝑁𝑃𝑉−𝐵𝑎𝑠𝑒 𝑁𝑃𝑉

𝐵𝑎𝑠𝑒 𝑁𝑃𝑉 x 100

(419953)− (1465039.4)

(419953)= 248.86%

Percentage change in NPV base case to best case

Ignore negatives in

% change

Page 18

% best case = 𝐵𝑒𝑠𝑡 𝑁𝑃𝑉−𝐵𝑎𝑠𝑒 𝑁𝑃𝑉

𝐵𝑎𝑠𝑒 𝑁𝑃𝑉

(419,953)− (96,623.2)

(419,953)= 77%

Comment:

The project is highly risky since percentage of worst is more than percentage of best.

3. Simulation Analysis

To simulate is to imitate. It involves conducting of a series of trial and error experiments. Where there

is a large number of random variables in an investment decision, simulation analysis may provide a

more satisfactory results in evaluating that project provided. Simulation can only apply when the

probability distribution of projects variables is given and a large number of trials are conducted to

reach a steady state.

Monte Carlo simulation and investment appraisal

Monte Carlo method

This section provides a brief outline of the Monte Carlo method in investment appraisal. The method

appeared in 1949 and is widely used in situations involving uncertainty. The method amounts to

adopting a particular probability distribution for the uncertain (random) variables that affect the NPV

and then using simulations to generate values of the random variables.

The basic idea is to generate through simulation thousands of values for the parameters or variables of

interest and use those variables to derive the NPV for each possible simulated outcome.

From the resulting values we can derive the distribution of the NPV.

Basic steps

1) Identify probabilistic variables

2) Determine cumulative probabilities

3) Assign RN – Ranges

NB: The Ranges will contain digits that correspond to the decimal places of probabilities i.e. if a

series has:

1) 1 decimal place probabilities that we use 1 digit (0 – 9)

2) 2 decimal places – 2 digits (00 – 99)

3) 3 decimal places – 2 digits (000 – 999)

Illustration 1

Determine random number range of the following distribution

Page 19

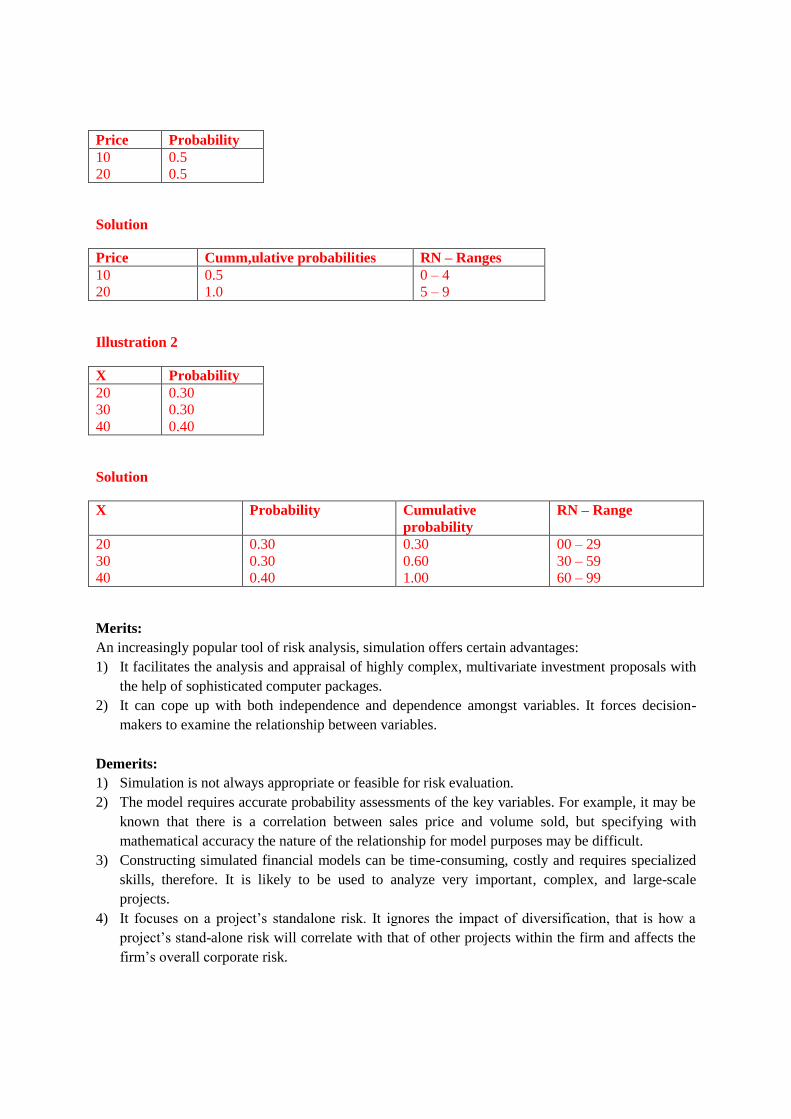

Price Probability

10

20

0.5

0.5

Solution

Price Cumm,ulative probabilities RN – Ranges

10

20

0.5

1.0

0 – 4

5 – 9

Illustration 2

X Probability

20

30

40

0.30

0.30

0.40

Solution

X Probability Cumulative

probability

RN – Range

20

30

40

0.30

0.30

0.40

0.30

0.60

1.00

00 – 29

30 – 59

60 – 99

Merits:

An increasingly popular tool of risk analysis, simulation offers certain advantages:

1) It facilitates the analysis and appraisal of highly complex, multivariate investment proposals with

the help of sophisticated computer packages.

2) It can cope up with both independence and dependence amongst variables. It forces decision-

makers to examine the relationship between variables.

Demerits:

1) Simulation is not always appropriate or feasible for risk evaluation.

2) The model requires accurate probability assessments of the key variables. For example, it may be

known that there is a correlation between sales price and volume sold, but specifying with

mathematical accuracy the nature of the relationship for model purposes may be difficult.

3) Constructing simulated financial models can be time-consuming, costly and requires specialized

skills, therefore. It is likely to be used to analyze very important, complex, and large-scale

projects.

4) It focuses on a project’s standalone risk. It ignores the impact of diversification, that is how a

project’s stand-alone risk will correlate with that of other projects within the firm and affects the

firm’s overall corporate risk.

Page 20

5) Simulation is inherently imprecise. It provides a rough approximation of the probability

distribution of net present value (or any other criterion of merit).

6) A realistic simulation model, likely to be complex, would most probably be constructed by a

management scientist, not the decision maker. The decision maker, lacking understanding of the

model, may not use it.

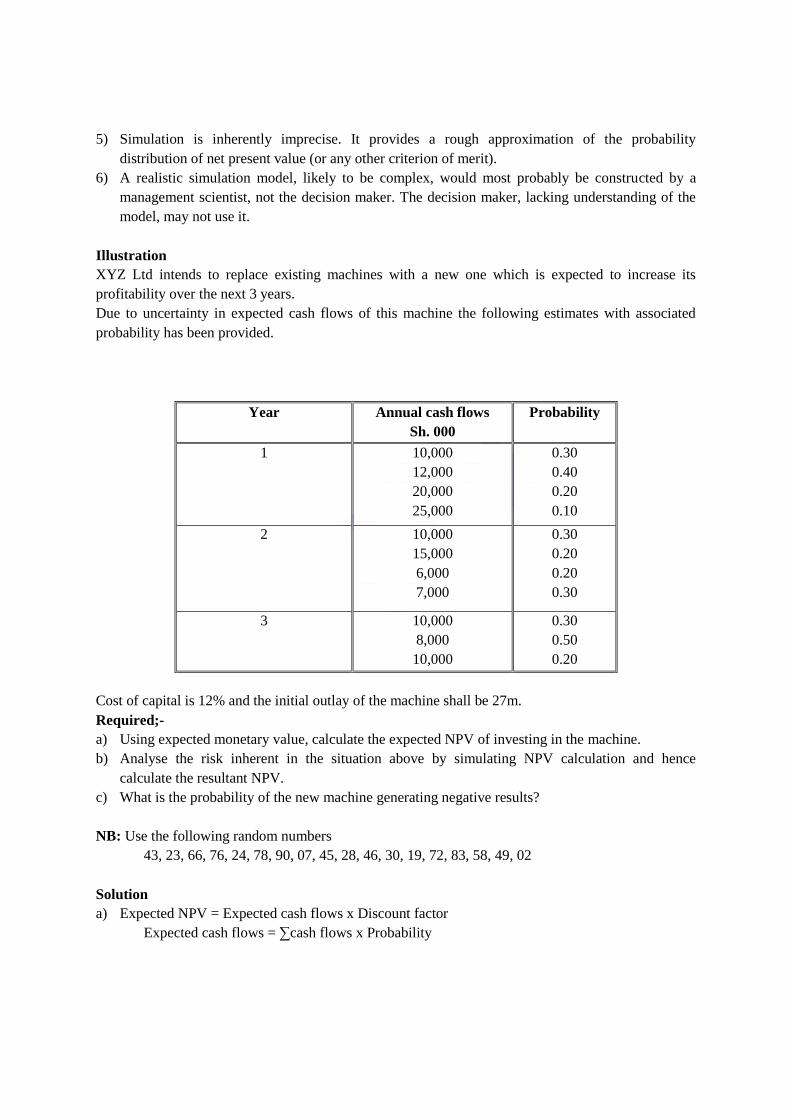

Illustration

XYZ Ltd intends to replace existing machines with a new one which is expected to increase its

profitability over the next 3 years.

Due to uncertainty in expected cash flows of this machine the following estimates with associated

probability has been provided.

Year Annual cash flows

Sh. 000

Probability

1

10,000

12,000

20,000

25,000

0.30

0.40

0.20

0.10

2

10,000

15,000

6,000

7,000

0.30

0.20

0.20

0.30

3 10,000

8,000

10,000

0.30

0.50

0.20

Cost of capital is 12% and the initial outlay of the machine shall be 27m.

Required;-

a) Using expected monetary value, calculate the expected NPV of investing in the machine.

b) Analyse the risk inherent in the situation above by simulating NPV calculation and hence

calculate the resultant NPV.

c) What is the probability of the new machine generating negative results?

NB: Use the following random numbers

43, 23, 66, 76, 24, 78, 90, 07, 45, 28, 46, 30, 19, 72, 83, 58, 49, 02

Solution

a) Expected NPV = Expected cash flows x Discount factor

Expected cash flows = ∑cash flows x Probability

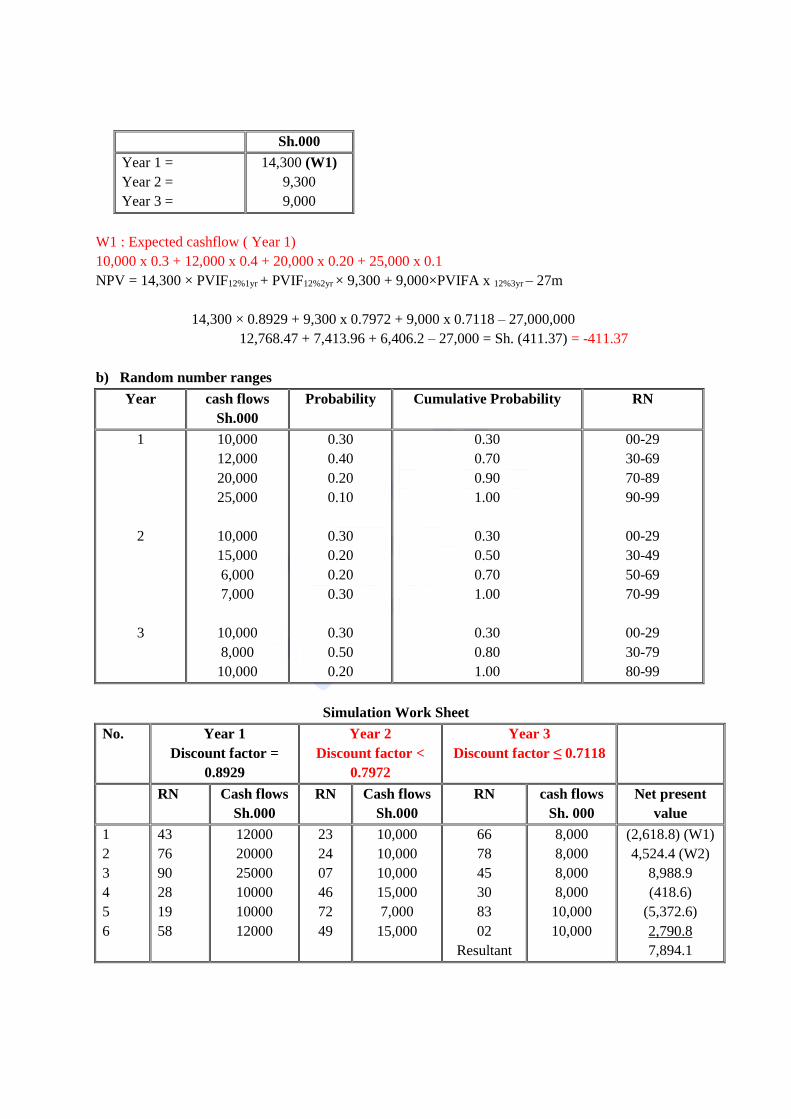

Page 21

Sh.000

Year 1 =

Year 2 =

Year 3 =

14,300 (W1)

9,300

9,000

W1 : Expected cashflow ( Year 1)

10,000 x 0.3 + 12,000 x 0.4 + 20,000 x 0.20 + 25,000 x 0.1

NPV = 14,300 × PVIF12%1yr + PVIF12%2yr × 9,300 + 9,000×PVIFA x 12%3yr – 27m

14,300 × 0.8929 + 9,300 x 0.7972 + 9,000 x 0.7118 – 27,000,000

12,768.47 + 7,413.96 + 6,406.2 – 27,000 = Sh. (411.37) = -411.37

b) Random number ranges

Year cash flows

Sh.000

Probability Cumulative Probability RN

1

2

3

10,000

12,000

20,000

25,000

10,000

15,000

6,000

7,000

10,000

8,000

10,000

0.30

0.40

0.20

0.10

0.30

0.20

0.20

0.30

0.30

0.50

0.20

0.30

0.70

0.90

1.00

0.30

0.50

0.70

1.00

0.30

0.80

1.00

00-29

30-69

70-89

90-99

00-29

30-49

50-69

70-99

00-29

30-79

80-99

Simulation Work Sheet

No. Year 1

Discount factor =

0.8929

Year 2

Discount factor <

0.7972

Year 3

Discount factor ≤ 0.7118

RN Cash flows

Sh.000

RN Cash flows

Sh.000

RN cash flows

Sh. 000

Net present

value

1

2

3

4

5

6

43

76

90

28

19

58

12000

20000

25000

10000

10000

12000

23

24

07

46

72

49

10,000

10,000

10,000

15,000

7,000

15,000

66

78

45

30

83

02

Resultant

8,000

8,000

8,000

8,000

10,000

10,000

(2,618.8) (W1)

4,524.4 (W2)

8,988.9

(418.6)

(5,372.6)

2,790.8

7,894.1

Page 22

NPV

W1: 12,000 × 0.8929 + 100,000 × 0.7972 + 8,000 × 0.7118 – 27,000 = 2618.8

W2: 20,000 × 0.8929 + 10,000×0.7972 + 8,000×0.7118 – 27,000 = 4524.4

c) Probability of negative NPVS = 𝑁𝑜.𝑜𝑓𝑛𝑒𝑔𝑎𝑡𝑖𝑣𝑒 𝑁𝑃𝑉𝑆

𝑁𝑜.𝑜𝑓𝑅𝑢𝑛𝑠 =

3

6 = 0.5

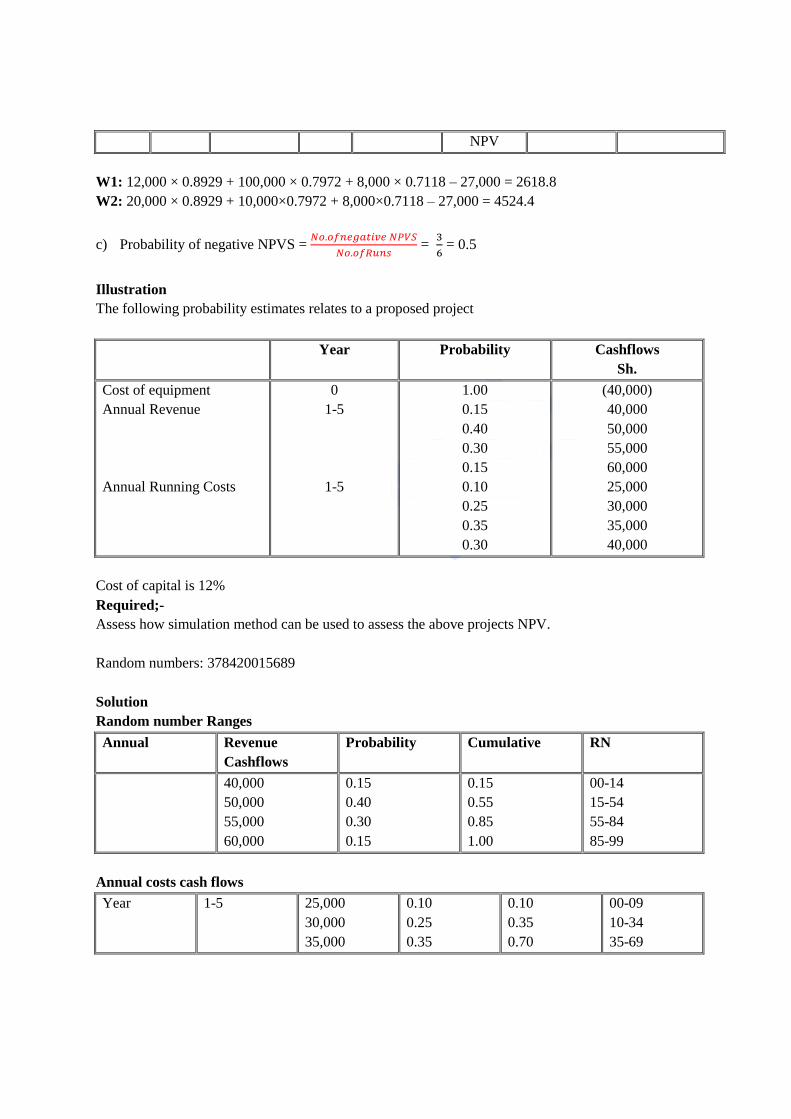

Illustration

The following probability estimates relates to a proposed project

Year Probability Cashflows

Sh.

Cost of equipment

Annual Revenue

Annual Running Costs

0

1-5

1-5

1.00

0.15

0.40

0.30

0.15

0.10

0.25

0.35

0.30

(40,000)

40,000

50,000

55,000

60,000

25,000

30,000

35,000

40,000

Cost of capital is 12%

Required;-

Assess how simulation method can be used to assess the above projects NPV.

Random numbers: 378420015689

Solution

Random number Ranges

Annual Revenue

Cashflows

Probability Cumulative RN

40,000

50,000

55,000

60,000

0.15

0.40

0.30

0.15

0.15

0.55

0.85

1.00

00-14

15-54

55-84

85-99

Annual costs cash flows

Year 1-5 25,000

30,000

35,000

0.10

0.25

0.35

0.10

0.35

0.70

00-09

10-34

35-69

Page 23

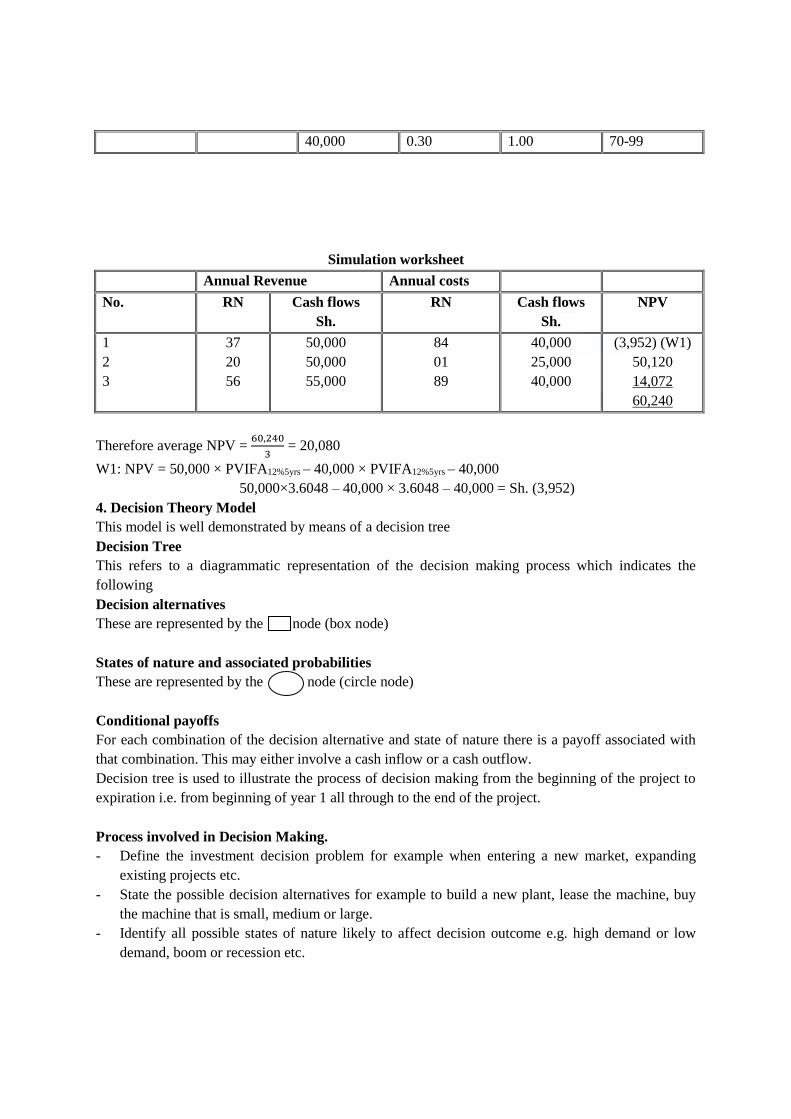

40,000 0.30 1.00 70-99

Simulation worksheet

Annual Revenue Annual costs

No. RN Cash flows

Sh.

RN Cash flows

Sh.

NPV

1

2

3

37

20

56

50,000

50,000

55,000

84

01

89

40,000

25,000

40,000

(3,952) (W1)

50,120

14,072

60,240

Therefore average NPV = 60,240

3 = 20,080

W1: NPV = 50,000 × PVIFA12%5yrs – 40,000 × PVIFA12%5yrs – 40,000

50,000×3.6048 – 40,000 × 3.6048 – 40,000 = Sh. (3,952)

4. Decision Theory Model

This model is well demonstrated by means of a decision tree

Decision Tree

This refers to a diagrammatic representation of the decision making process which indicates the

following

Decision alternatives

These are represented by the node (box node)

States of nature and associated probabilities

These are represented by the node (circle node)

Conditional payoffs

For each combination of the decision alternative and state of nature there is a payoff associated with

that combination. This may either involve a cash inflow or a cash outflow.

Decision tree is used to illustrate the process of decision making from the beginning of the project to

expiration i.e. from beginning of year 1 all through to the end of the project.

Process involved in Decision Making.

- Define the investment decision problem for example when entering a new market, expanding

existing projects etc.

- State the possible decision alternatives for example to build a new plant, lease the machine, buy

the machine that is small, medium or large.

- Identify all possible states of nature likely to affect decision outcome e.g. high demand or low

demand, boom or recession etc.

Page 24

- Estimate the probabilities associated with different states of nature identified above.

- Estimate conditional payoff for each combination of decision alternative and states of nature.

- Draw the decision tree.

- Calculate the expected value/expected monetary value of each of the alternatives available.

- Calculate the NPV of each of the available options we use the rollback technique in calculating

the resultant NPV of the project at hand i.e. we start from the furthest year then calculate NPV in

backward scenario up to year 0.

Merits

The sensitivity analysis has the following advantages:

It compels the decision maker to identify the variables affecting the cash flow forecasts

which helps in understanding the investment project in totality.

It identifies the critical variables for which special actions can be taken.

It guides the decision maker to concentrate on relevant variables for the project.

Demerits:

The sensitivity analysis suffers from following limitations:

The range of values suggested by the technique may not be consistent. The terms

‘optimistic’ and ‘pessimistic’ could mean different things to different people.

It fails to focus on the interrelationship between variables. The study of variability of one

factor at a time, keeping other variables constant may not much sense. For example, sales

volume may be related to price and cost. One cannot study the effect of change in price

keeping quantity constant.

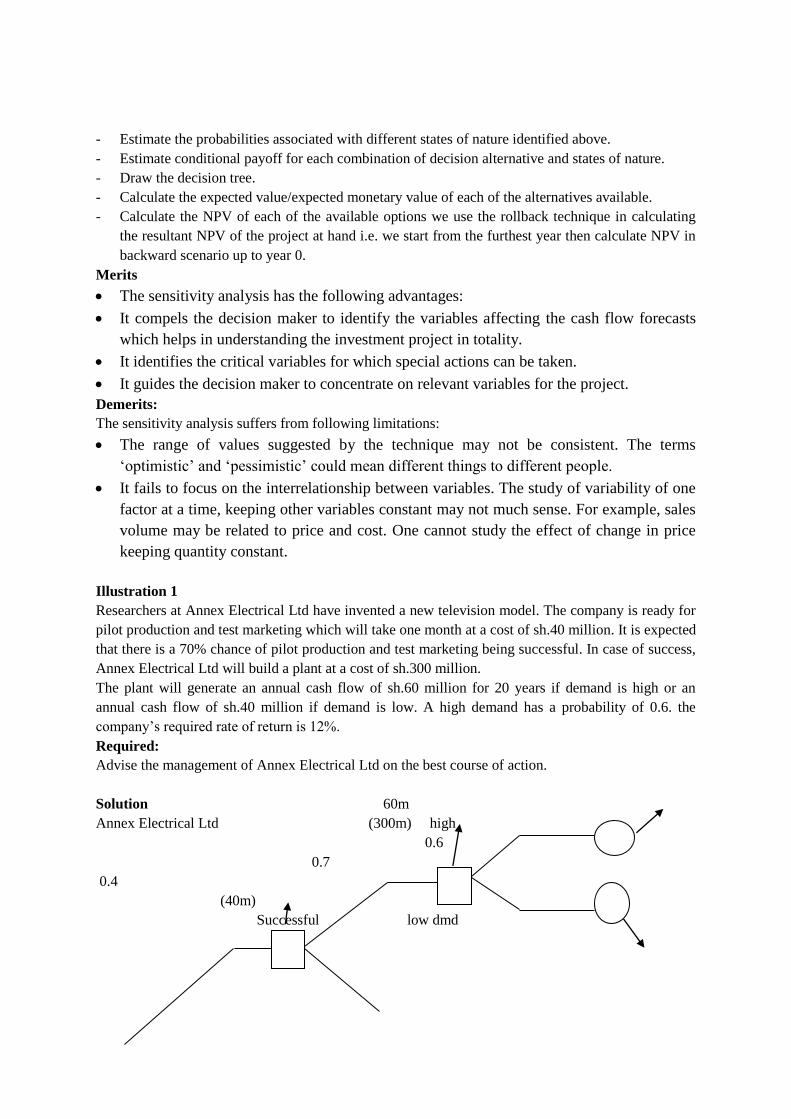

Illustration 1

Researchers at Annex Electrical Ltd have invented a new television model. The company is ready for

pilot production and test marketing which will take one month at a cost of sh.40 million. It is expected

that there is a 70% chance of pilot production and test marketing being successful. In case of success,

Annex Electrical Ltd will build a plant at a cost of sh.300 million.

The plant will generate an annual cash flow of sh.60 million for 20 years if demand is high or an

annual cash flow of sh.40 million if demand is low. A high demand has a probability of 0.6. the

company’s required rate of return is 12%.

Required:

Advise the management of Annex Electrical Ltd on the best course of action.

Solution 60m

Annex Electrical Ltd (300m) high

0.6

0.7

0.4

(40m)

Successful low dmd

Page 25

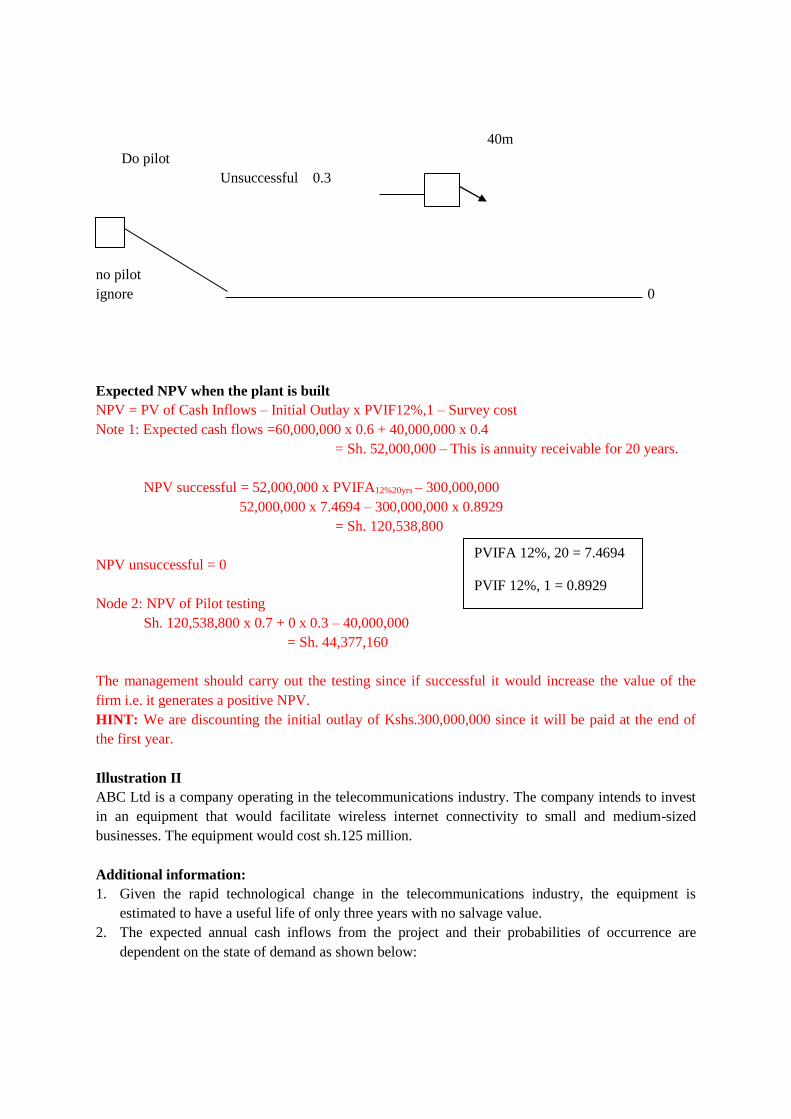

40m

Do pilot

Unsuccessful 0.3

no pilot

ignore 0

Expected NPV when the plant is built

NPV = PV of Cash Inflows – Initial Outlay x PVIF12%,1 – Survey cost

Note 1: Expected cash flows =60,000,000 x 0.6 + 40,000,000 x 0.4

= Sh. 52,000,000 – This is annuity receivable for 20 years.

NPV successful = 52,000,000 x PVIFA12%20yrs – 300,000,000

52,000,000 x 7.4694 – 300,000,000 x 0.8929

= Sh. 120,538,800

NPV unsuccessful = 0

Node 2: NPV of Pilot testing

Sh. 120,538,800 x 0.7 + 0 x 0.3 – 40,000,000

= Sh. 44,377,160

The management should carry out the testing since if successful it would increase the value of the

firm i.e. it generates a positive NPV.

HINT: We are discounting the initial outlay of Kshs.300,000,000 since it will be paid at the end of

the first year.

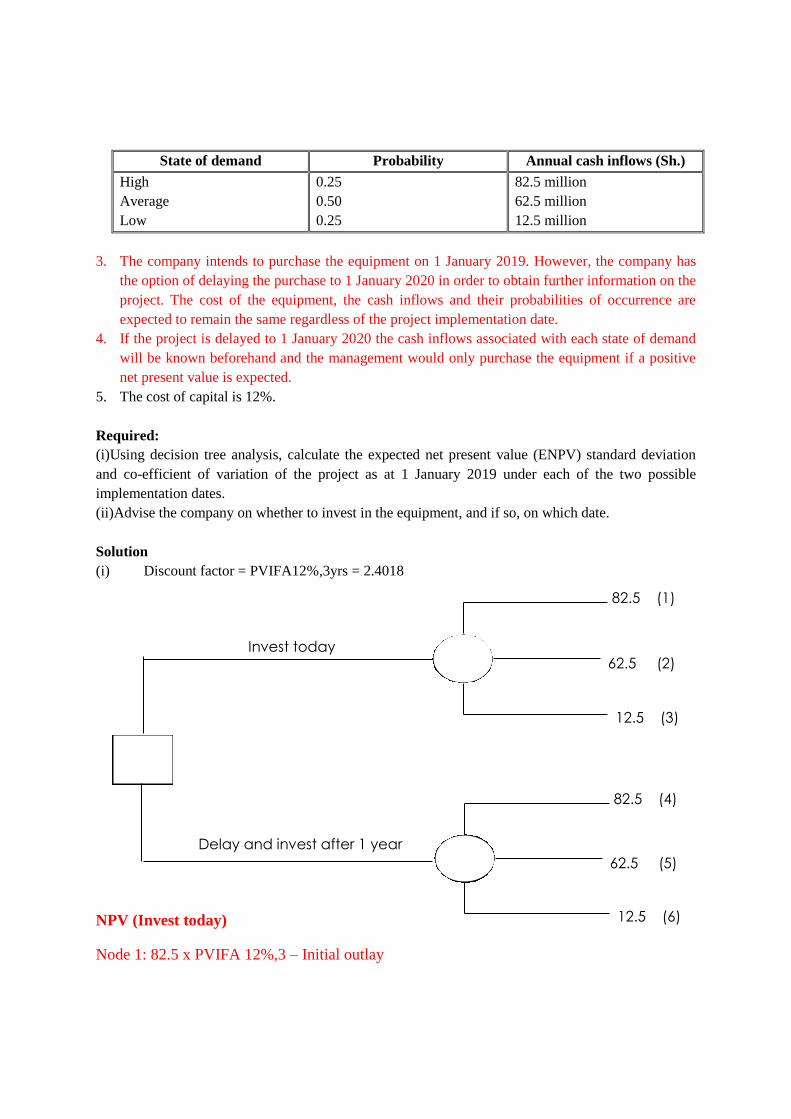

Illustration II

ABC Ltd is a company operating in the telecommunications industry. The company intends to invest

in an equipment that would facilitate wireless internet connectivity to small and medium-sized

businesses. The equipment would cost sh.125 million.

Additional information:

1. Given the rapid technological change in the telecommunications industry, the equipment is

estimated to have a useful life of only three years with no salvage value.

2. The expected annual cash inflows from the project and their probabilities of occurrence are

dependent on the state of demand as shown below:

PVIFA 12%, 20 = 7.4694

PVIF 12%, 1 = 0.8929

Page 26

State of demand Probability Annual cash inflows (Sh.)

High

Average

Low

0.25

0.50

0.25

82.5 million

62.5 million

12.5 million

3. The company intends to purchase the equipment on 1 January 2019. However, the company has

the option of delaying the purchase to 1 January 2020 in order to obtain further information on the

project. The cost of the equipment, the cash inflows and their probabilities of occurrence are

expected to remain the same regardless of the project implementation date.

4. If the project is delayed to 1 January 2020 the cash inflows associated with each state of demand

will be known beforehand and the management would only purchase the equipment if a positive

net present value is expected.

5. The cost of capital is 12%.

Required:

(i)Using decision tree analysis, calculate the expected net present value (ENPV) standard deviation

and co-efficient of variation of the project as at 1 January 2019 under each of the two possible

implementation dates.

(ii)Advise the company on whether to invest in the equipment, and if so, on which date.

Solution

(i) Discount factor = PVIFA12%,3yrs = 2.4018

NPV (Invest today)

Node 1: 82.5 x PVIFA 12%,3 – Initial outlay

82.5 (1)

62.5 (2)

12.5 (3)

82.5 (4)

62.5 (5)

12.5 (6)

Invest today

Delay and invest after 1 year

Page 27

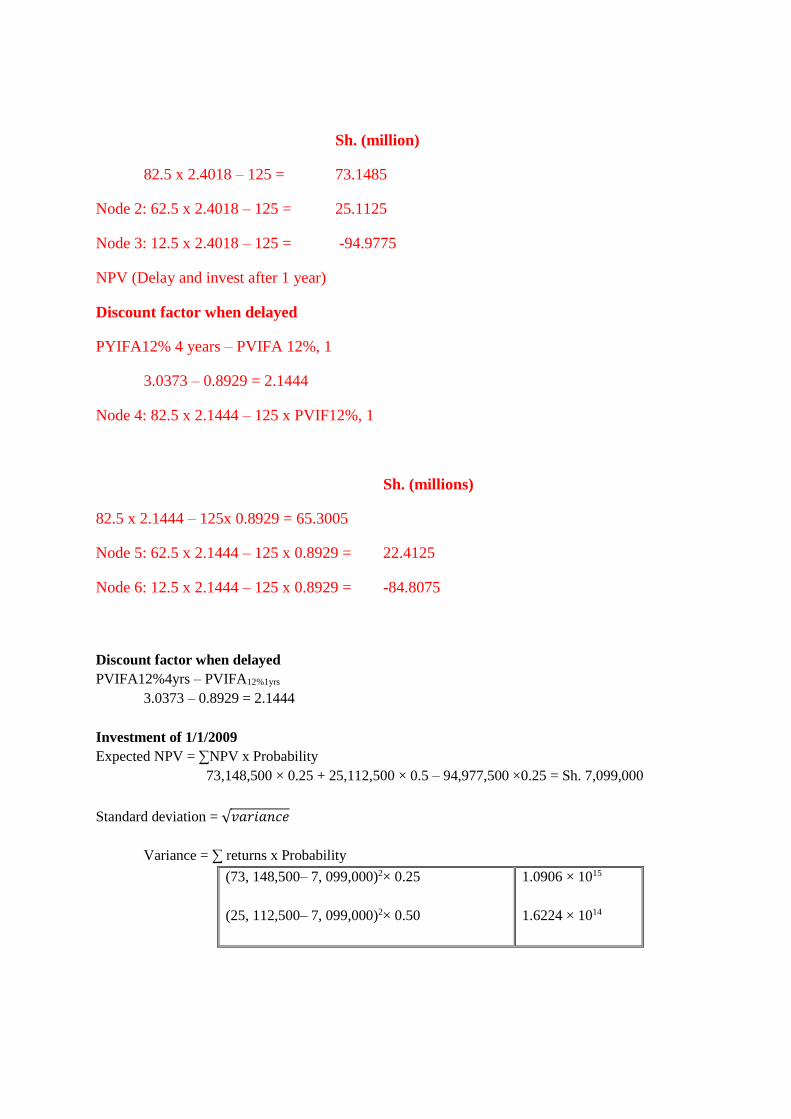

Sh. (million)

82.5 x 2.4018 – 125 = 73.1485

Node 2: 62.5 x 2.4018 – 125 = 25.1125

Node 3: 12.5 x 2.4018 – 125 = -94.9775

NPV (Delay and invest after 1 year)

Discount factor when delayed

PYIFA12% 4 years – PVIFA 12%, 1

3.0373 – 0.8929 = 2.1444

Node 4: 82.5 x 2.1444 – 125 x PVIF12%, 1

Sh. (millions)

82.5 x 2.1444 – 125x 0.8929 = 65.3005

Node 5: 62.5 x 2.1444 – 125 x 0.8929 = 22.4125

Node 6: 12.5 x 2.1444 – 125 x 0.8929 = -84.8075

Discount factor when delayed

PVIFA12%4yrs – PVIFA12%1yrs

3.0373 – 0.8929 = 2.1444

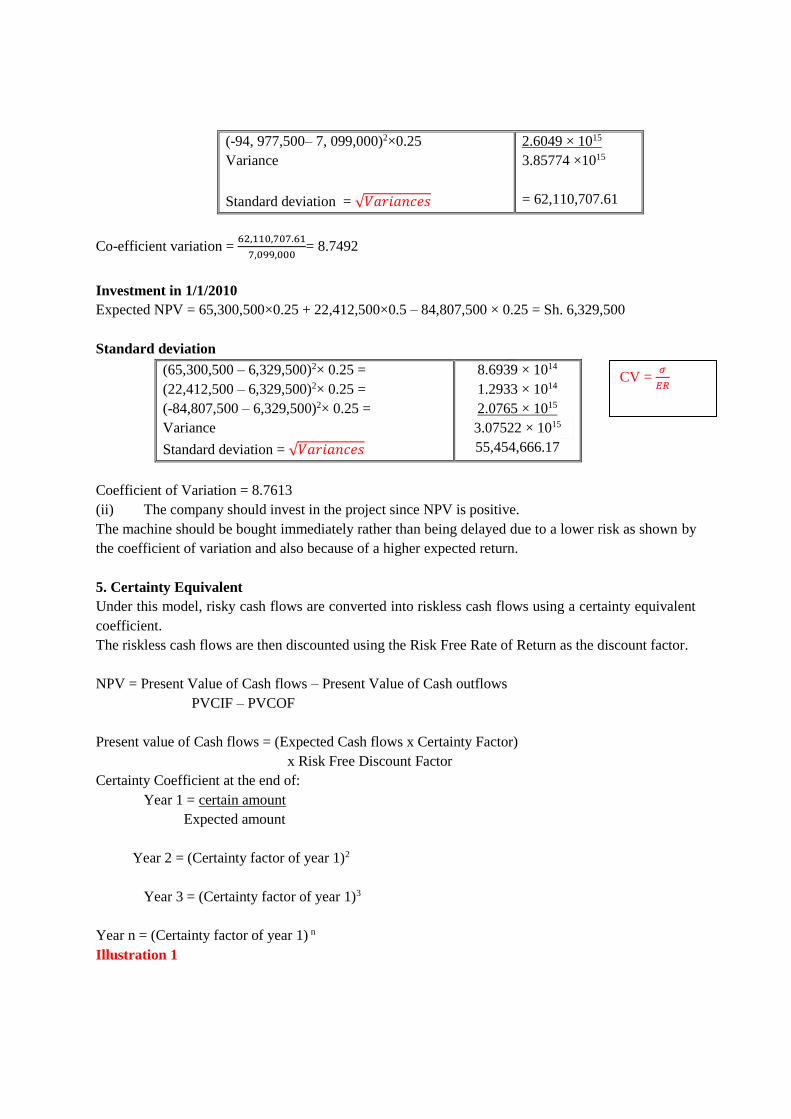

Investment of 1/1/2009

Expected NPV = ∑NPV x Probability

73,148,500 × 0.25 + 25,112,500 × 0.5 – 94,977,500 ×0.25 = Sh. 7,099,000

Standard deviation = √𝑣𝑎𝑟𝑖𝑎𝑛𝑐𝑒

Variance = ∑ returns x Probability

(73, 148,500– 7, 099,000)2× 0.25

(25, 112,500– 7, 099,000)2× 0.50

1.0906 × 1015

1.6224 × 1014

Page 28

(-94, 977,500– 7, 099,000)2×0.25

Variance

Standard deviation = √𝑉𝑎𝑟𝑖𝑎𝑛𝑐𝑒𝑠

2.6049 × 1015

3.85774 ×1015

= 62,110,707.61

Co-efficient variation = 62,110,707.61

7,099,000= 8.7492

Investment in 1/1/2010

Expected NPV = 65,300,500×0.25 + 22,412,500×0.5 – 84,807,500 × 0.25 = Sh. 6,329,500

Standard deviation

(65,300,500 – 6,329,500)2× 0.25 =

(22,412,500 – 6,329,500)2× 0.25 =

(-84,807,500 – 6,329,500)2× 0.25 =

Variance

Standard deviation = √𝑉𝑎𝑟𝑖𝑎𝑛𝑐𝑒𝑠

8.6939 × 1014

1.2933 × 1014

2.0765 × 1015

3.07522 × 1015

55,454,666.17

Coefficient of Variation = 8.7613

(ii) The company should invest in the project since NPV is positive.

The machine should be bought immediately rather than being delayed due to a lower risk as shown by

the coefficient of variation and also because of a higher expected return.

5. Certainty Equivalent

Under this model, risky cash flows are converted into riskless cash flows using a certainty equivalent

coefficient.

The riskless cash flows are then discounted using the Risk Free Rate of Return as the discount factor.

NPV = Present Value of Cash flows – Present Value of Cash outflows

PVCIF – PVCOF

Present value of Cash flows = (Expected Cash flows x Certainty Factor)

x Risk Free Discount Factor

Certainty Coefficient at the end of:

Year 1 = certain amount

Expected amount

Year 2 = (Certainty factor of year 1)2

Year 3 = (Certainty factor of year 1)3

Year n = (Certainty factor of year 1) n

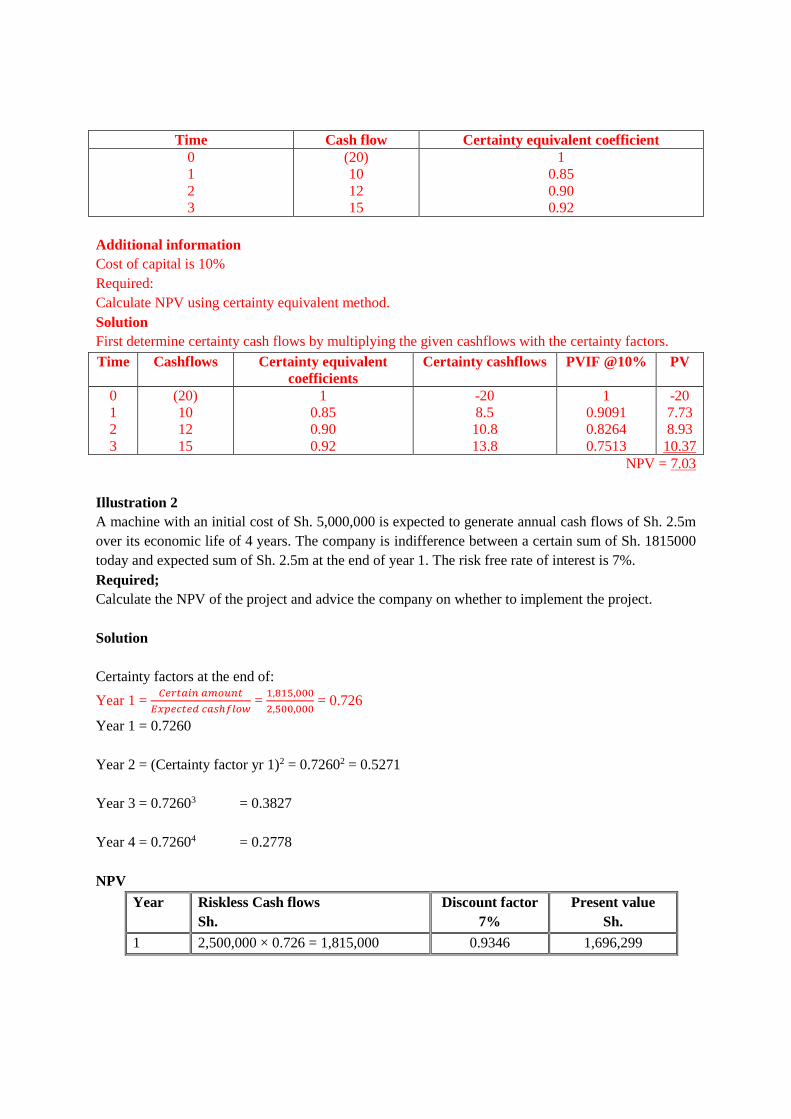

Illustration 1

CV = 𝜎

𝐸𝑅

Page 29

Time Cash flow Certainty equivalent coefficient

0

1

2

3

(20)

10

12

15

1

0.85

0.90

0.92

Additional information

Cost of capital is 10%

Required:

Calculate NPV using certainty equivalent method.

Solution

First determine certainty cash flows by multiplying the given cashflows with the certainty factors.

Time Cashflows Certainty equivalent

coefficients

Certainty cashflows PVIF @10% PV

0

1

2

3

(20)

10

12

15

1

0.85

0.90

0.92

-20

8.5

10.8

13.8

1

0.9091

0.8264

0.7513

-20

7.73

8.93

10.37

NPV = 7.03

Illustration 2

A machine with an initial cost of Sh. 5,000,000 is expected to generate annual cash flows of Sh. 2.5m

over its economic life of 4 years. The company is indifference between a certain sum of Sh. 1815000

today and expected sum of Sh. 2.5m at the end of year 1. The risk free rate of interest is 7%.

Required;

Calculate the NPV of the project and advice the company on whether to implement the project.

Solution

Certainty factors at the end of:

Year 1 = 𝐶𝑒𝑟𝑡𝑎𝑖𝑛 𝑎𝑚𝑜𝑢𝑛𝑡

𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑐𝑎𝑠ℎ𝑓𝑙𝑜𝑤 =

1,815,000

2,500,000 = 0.726

Year 1 = 0.7260

Year 2 = (Certainty factor yr 1)2 = 0.72602 = 0.5271

Year 3 = 0.72603 = 0.3827

Year 4 = 0.72604 = 0.2778

NPV

Year Riskless Cash flows

Sh.

Discount factor

7%

Present value

Sh.

1 2,500,000 × 0.726 = 1,815,000 0.9346 1,696,299

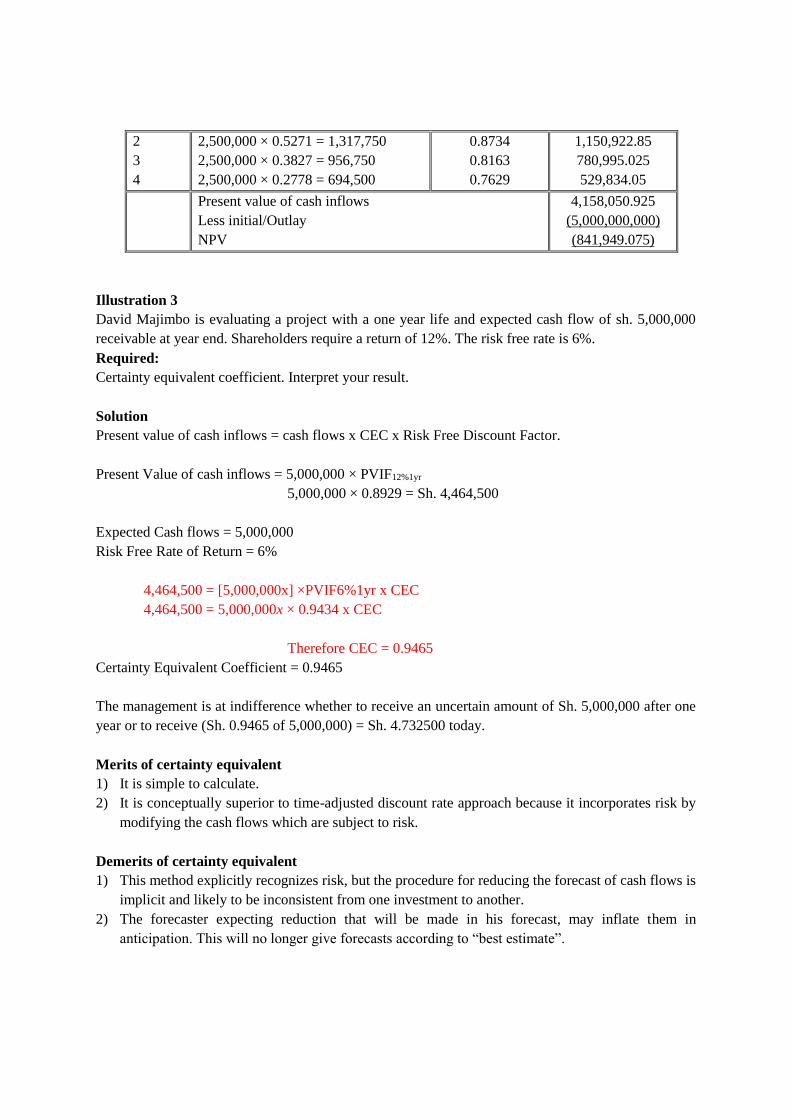

Page 30

2

3

4

2,500,000 × 0.5271 = 1,317,750

2,500,000 × 0.3827 = 956,750

2,500,000 × 0.2778 = 694,500

0.8734

0.8163

0.7629

1,150,922.85

780,995.025

529,834.05

Present value of cash inflows

Less initial/Outlay

NPV

4,158,050.925

(5,000,000,000)

(841,949.075)

Illustration 3

David Majimbo is evaluating a project with a one year life and expected cash flow of sh. 5,000,000

receivable at year end. Shareholders require a return of 12%. The risk free rate is 6%.

Required:

Certainty equivalent coefficient. Interpret your result.

Solution

Present value of cash inflows = cash flows x CEC x Risk Free Discount Factor.

Present Value of cash inflows = 5,000,000 × PVIF12%1yr

5,000,000 × 0.8929 = Sh. 4,464,500

Expected Cash flows = 5,000,000

Risk Free Rate of Return = 6%

4,464,500 = [5,000,000x] ×PVIF6%1yr x CEC

4,464,500 = 5,000,000x × 0.9434 x CEC

Therefore CEC = 0.9465

Certainty Equivalent Coefficient = 0.9465

The management is at indifference whether to receive an uncertain amount of Sh. 5,000,000 after one

year or to receive (Sh. 0.9465 of 5,000,000) = Sh. 4.732500 today.

Merits of certainty equivalent

1) It is simple to calculate.

2) It is conceptually superior to time-adjusted discount rate approach because it incorporates risk by

modifying the cash flows which are subject to risk.

Demerits of certainty equivalent

1) This method explicitly recognizes risk, but the procedure for reducing the forecast of cash flows is

implicit and likely to be inconsistent from one investment to another.

2) The forecaster expecting reduction that will be made in his forecast, may inflate them in

anticipation. This will no longer give forecasts according to “best estimate”.

Page 31

3) If forecast have to pass through several layers of management, the effect may be to greatly

exaggerate the original forecast or to make it ultra conservative.

4) By focusing explicit attention only on the gloomy outcomes, chances are increased for passing by

some good investments.

6. Risk Adjusted Discount Rates (RADR)

Under this model, the discount factors for different projects are determined which are used in

calculating the NPV of the specific projects based on their risk level.

Traditionally, the same discount factor fact is used when evaluating different projects irrespective of

the difference in their level of risks.

Different projects are always affected by different factors which may not be similar to the risks of the

company hence the need to use Risk Adjusted Discount Factors/Discount factors when evaluating the

risks.

Decision Rule:

The risk adjusted approach can be used for both NPV and IRR.

If NPV method is used for evaluation, the NPV would be calculated using risk adjusted rate. If

NPV is positive, the proposal would qualify for acceptance, if it is negative, the proposal would

be rejected.

In case of IRR, the IRR would be compared with the risk adjusted required rate of return. If the

‘IRR’ exceeds risk adjusted rate, the proposal would be accepted, otherwise not.

Merits of risk adjusted discount rates

1) It is simple to calculate and easy to understand.

2) It has a great deal of intuitive appeal for risk-averse businessman.

3) It incorporates an attitude towards uncertainty.

Demerits of risk adjusted discount rates

1) The determination of appropriate discount rates keeping in view the differing degrees of risk is

arbitrary and does not give objective results.

2) Conceptually this method is incorrect since it adjusts the required rate of return. As a matter fact it

is the future cash flows which are subject to risk.

3) This method results in compounding of risk over time, thus it assumes that risk necessarily

increases with time which may not be correct in all cases.

4) The method presumes that investors are averse to risk, which is true in most cases. However,

there are risk seeker investors and are prepared to pay premium for taking risk and for them

discount rate should be reduced rather than increased with increase in risk.

Thus, this approach can be best described as a crude method of incorporating risk into capital

budgeting.

Illustration

Page 32

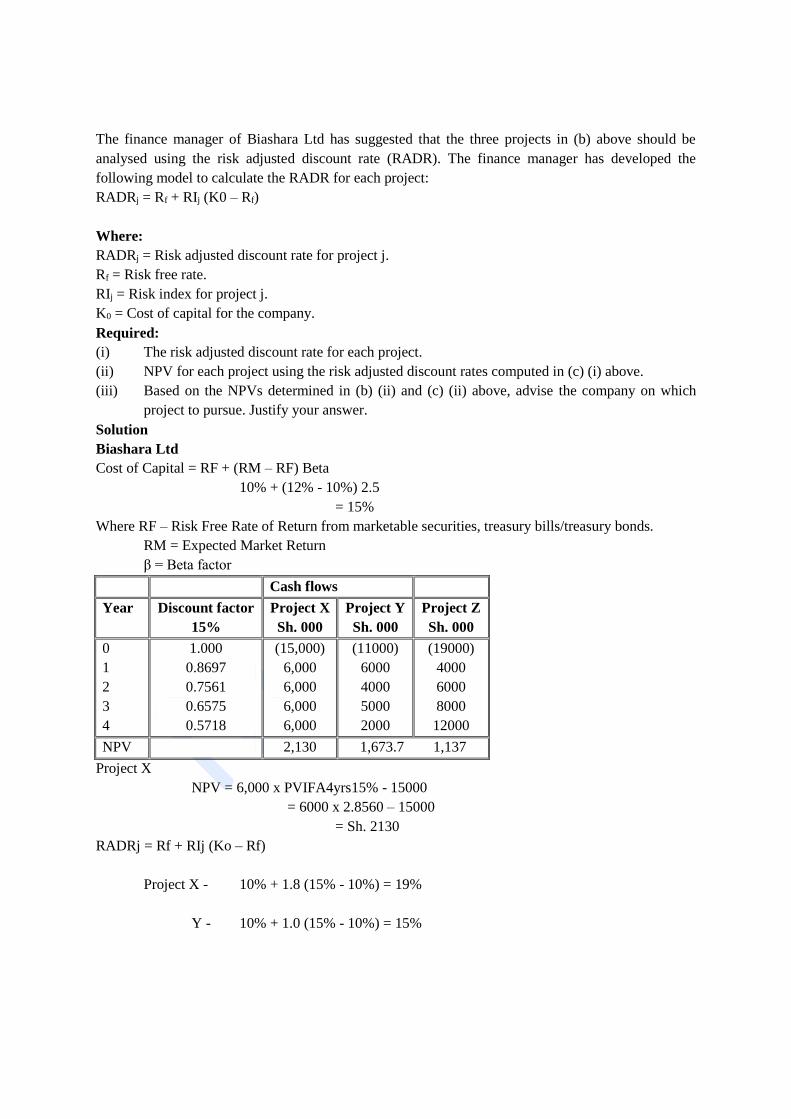

The finance manager of Biashara Ltd has suggested that the three projects in (b) above should be

analysed using the risk adjusted discount rate (RADR). The finance manager has developed the

following model to calculate the RADR for each project:

RADRj = Rf + RIj (K0 – Rf)

Where:

RADRj = Risk adjusted discount rate for project j.

Rf = Risk free rate.

RIj = Risk index for project j.

K0 = Cost of capital for the company.

Required:

(i) The risk adjusted discount rate for each project.

(ii) NPV for each project using the risk adjusted discount rates computed in (c) (i) above.

(iii) Based on the NPVs determined in (b) (ii) and (c) (ii) above, advise the company on which

project to pursue. Justify your answer.

Solution

Biashara Ltd

Cost of Capital = RF + (RM – RF) Beta

10% + (12% - 10%) 2.5

= 15%

Where RF – Risk Free Rate of Return from marketable securities, treasury bills/treasury bonds.

RM = Expected Market Return

β = Beta factor

Cash flows

Year Discount factor

15%

Project X

Sh. 000

Project Y

Sh. 000

Project Z

Sh. 000

0

1

2

3

4

1.000

0.8697

0.7561

0.6575

0.5718

(15,000)

6,000

6,000

6,000

6,000

(11000)

6000

4000

5000

2000

(19000)

4000

6000

8000

12000

NPV 2,130 1,673.7 1,137

Project X

NPV = 6,000 x PVIFA4yrs15% - 15000

= 6000 x 2.8560 – 15000

= Sh. 2130

RADRj = Rf + RIj (Ko – Rf)

Project X - 10% + 1.8 (15% - 10%) = 19%

Y - 10% + 1.0 (15% - 10%) = 15%

Page 33

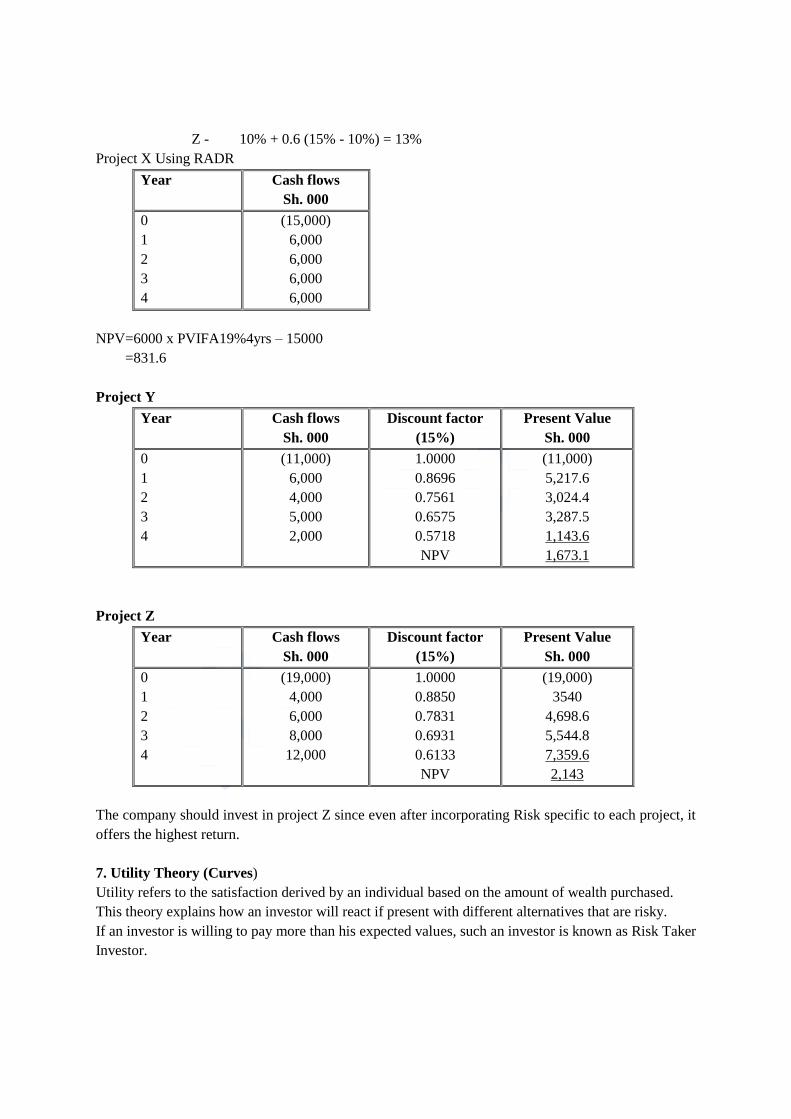

Z - 10% + 0.6 (15% - 10%) = 13%

Project X Using RADR

Year Cash flows

Sh. 000

0

1

2

3

4

(15,000)

6,000

6,000

6,000

6,000

NPV=6000 x PVIFA19%4yrs – 15000

=831.6

Project Y

Year Cash flows

Sh. 000

Discount factor

(15%)

Present Value

Sh. 000

0

1

2

3

4

(11,000)

6,000

4,000

5,000

2,000

1.0000

0.8696

0.7561

0.6575

0.5718

NPV

(11,000)

5,217.6

3,024.4

3,287.5

1,143.6

1,673.1

Project Z

Year Cash flows

Sh. 000

Discount factor

(15%)

Present Value

Sh. 000

0

1

2

3

4

(19,000)

4,000

6,000

8,000

12,000

1.0000

0.8850

0.7831

0.6931

0.6133

NPV

(19,000)

3540

4,698.6

5,544.8

7,359.6

2,143

The company should invest in project Z since even after incorporating Risk specific to each project, it

offers the highest return.

7. Utility Theory (Curves)

Utility refers to the satisfaction derived by an individual based on the amount of wealth purchased.

This theory explains how an investor will react if present with different alternatives that are risky.

If an investor is willing to pay more than his expected values, such an investor is known as Risk Taker

Investor.

Page 34

If an investor is willing to pay less than his expected return value, such an investor is known as

Risk Averse Investor.

In case the investor is willing to pay the same amount as his expected return, such an investor is

known as a Risk Neutral Investor.

As regards the attitude of individual investors towards risk, they can be classified in three categories. ·

Risk-averse investors attach lower utility to increasing wealth i.e. for a given wealth or return, they

prefer less risk to more risk. ·

Risk-neutral investors attach same utility to increasing or decreasing wealth i.e. they are indifferent to

less or more risk for a given wealth or return.

Risk-seeking investors attach more utility to the potential of additional wealth to the loss from the

possible loss from the decrease in wealth. I.e. for earning a given wealth or return, they are prepared

to assume higher risk. It is well established by many empirical studies that individuals are generally

risk averse and demonstrate a decreasing marginal utility for money function.

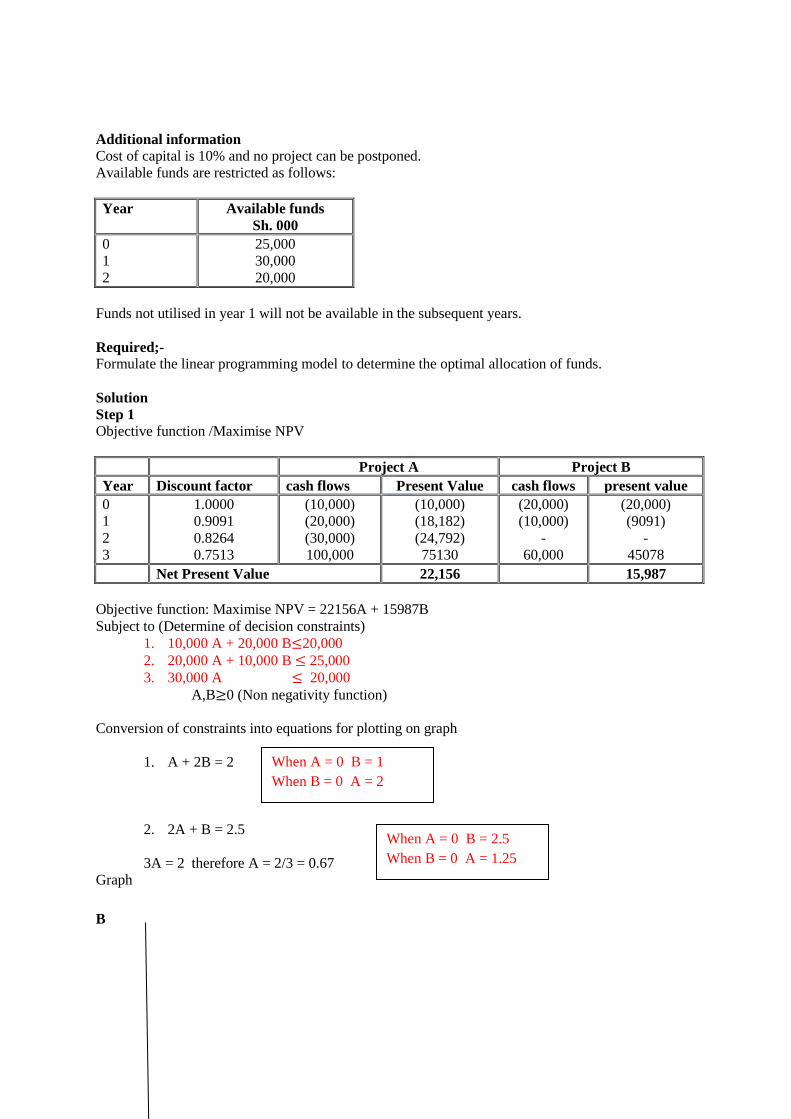

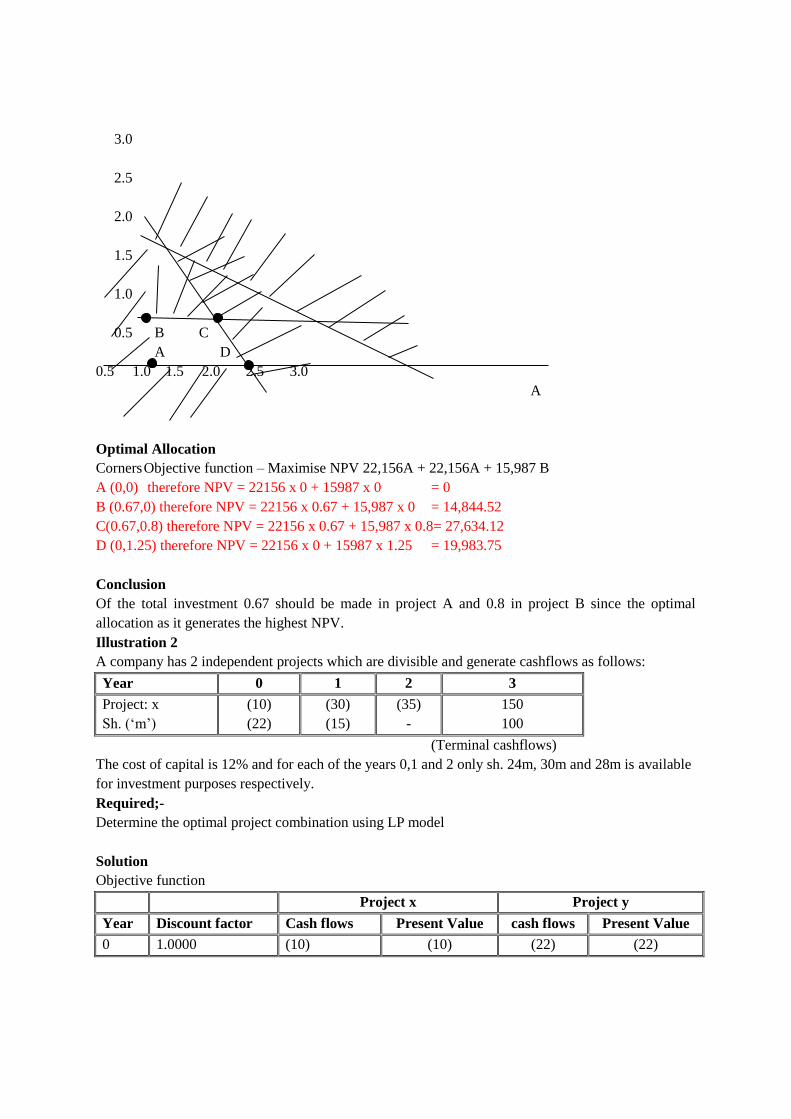

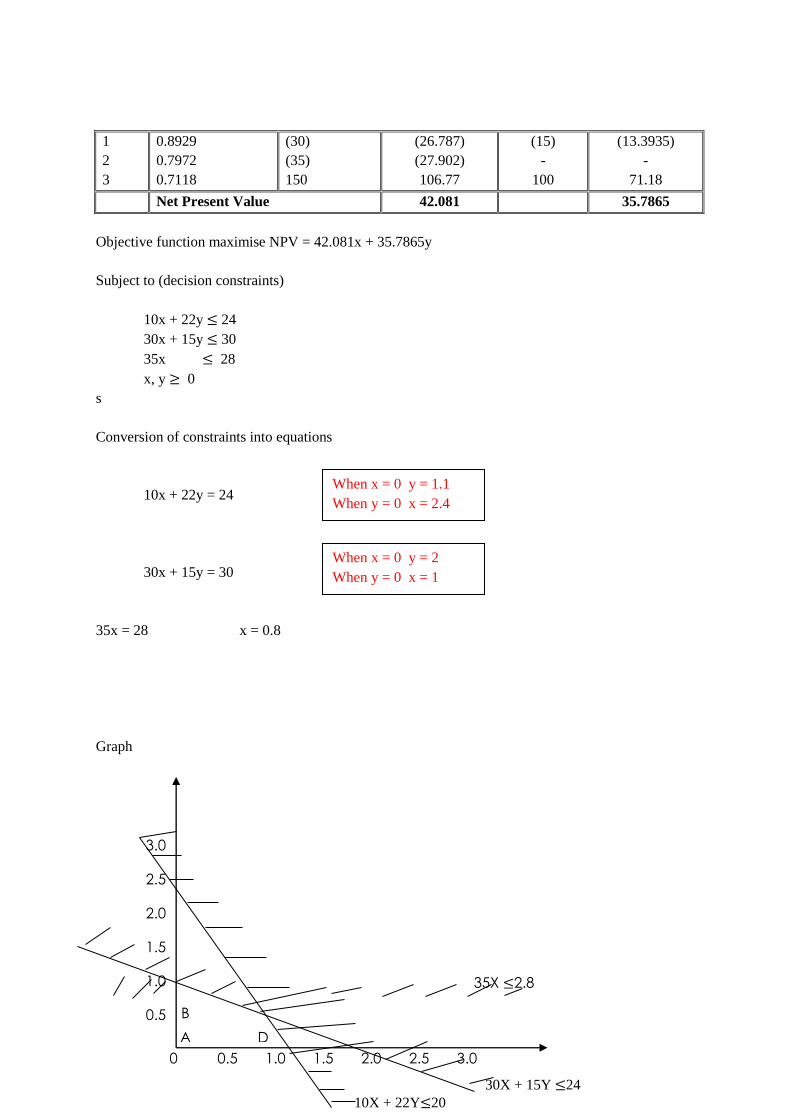

1.3 INCORPORATING CAPITAL RATIONING IN CAPITAL INVESTMENT

APPRAISAL

Capital rationing implies investment in projects within limited capital resources. It is the process of

allocating money among different projects, where the amount of money to be invested is limited.

Companies ration their capital and investments among different opportunities as countries use

rationing of food. In case of capital rationing, the company may not be able to invest in all profitable

projects.

Types of capital rationing

1. Internal/Soft Capital Rationing

In this case the decisions of the management leads to the company not being able to raise all the

required funds necessary for undertaking all profitable projects examples.

(i)Issue of additional shares to the public may be avoided so as not to dilute the firm’s earnings per

share.

(ii)Issue of additional debt may be avoided so as not to increase the firm’s gearing/financial risk.

(iii)Use of debt finance may be avoided so as not to increase the fixed finance costs inform of

interests.

(iv)The management may opt to maintain their investments at a level that can only be financed by

internally generated funds.

2. External/Hard capital rationing

It arises due to external factors which are beyond the control of the management, i.e. the firm is

unable to raise all the required funds due to the restrictions from the financial markets among other

external factors for example;

i) Raising of funds from the public through ordinary shares or debentures is not possible for a

company that is not listed (Quoted at the securities market).

ii) Raising of funds through debt may be difficult for a firm without collateral to pledge a security.

iii) The existing shareholders/investors may be unwilling to increase their investments to the firm.

Page 35

iv) The existing contractual obligations may prohibit the firm from raising additional funds from

other sources.

v) Government policies with respect to regulations of financial markets may prevent the firm from

additional borrowing through an increase in minimum lending rates.

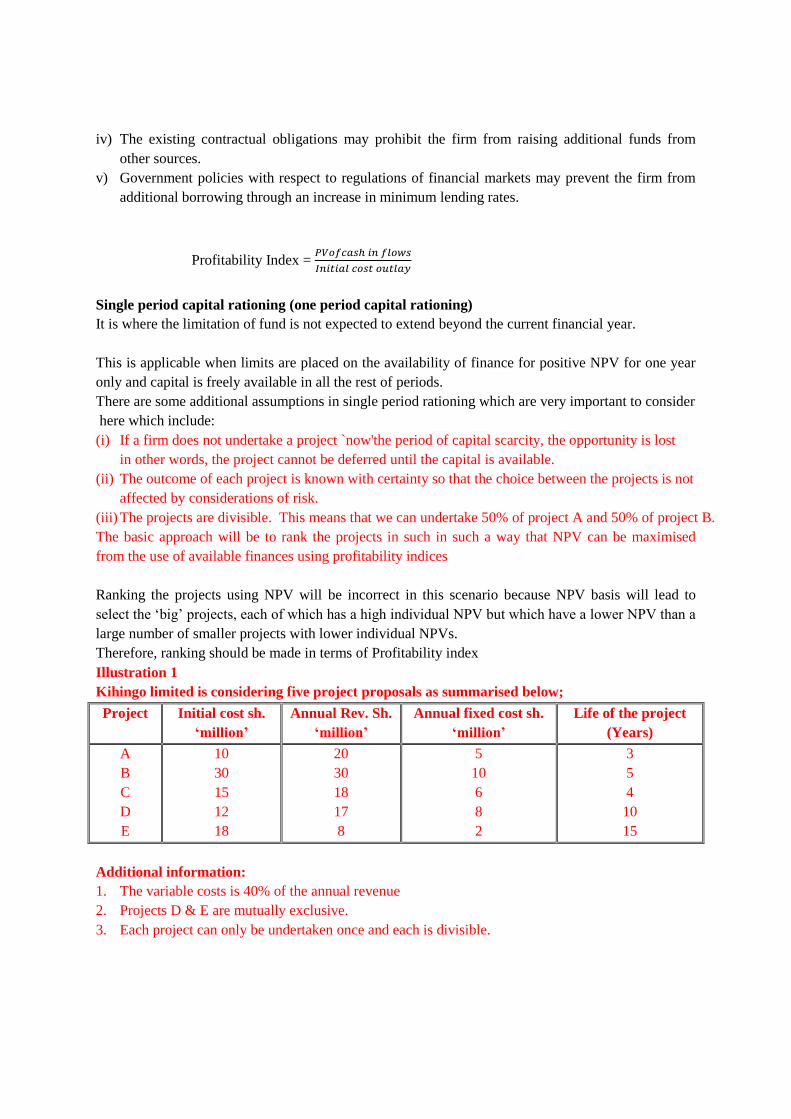

Profitability Index = 𝑃𝑉𝑜𝑓𝑐𝑎𝑠ℎ 𝑖𝑛 𝑓𝑙𝑜𝑤𝑠

𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝑐𝑜𝑠𝑡 𝑜𝑢𝑡𝑙𝑎𝑦

Single period capital rationing (one period capital rationing)

It is where the limitation of fund is not expected to extend beyond the current financial year.

This is applicable when limits are placed on the availability of finance for positive NPV for one year

only and capital is freely available in all the rest of periods.

There are some additional assumptions in single period rationing which are very important to consider

here which include:

(i) If a firm does not undertake a project `now'the period of capital scarcity, the opportunity is lost

in other words, the project cannot be deferred until the capital is available.

(ii) The outcome of each project is known with certainty so that the choice between the projects is not

affected by considerations of risk.

(iii) The projects are divisible. This means that we can undertake 50% of project A and 50% of project B.

The basic approach will be to rank the projects in such in such a way that NPV can be maximised

from the use of available finances using profitability indices

Ranking the projects using NPV will be incorrect in this scenario because NPV basis will lead to

select the ‘big’ projects, each of which has a high individual NPV but which have a lower NPV than a

large number of smaller projects with lower individual NPVs.

Therefore, ranking should be made in terms of Profitability index

Illustration 1

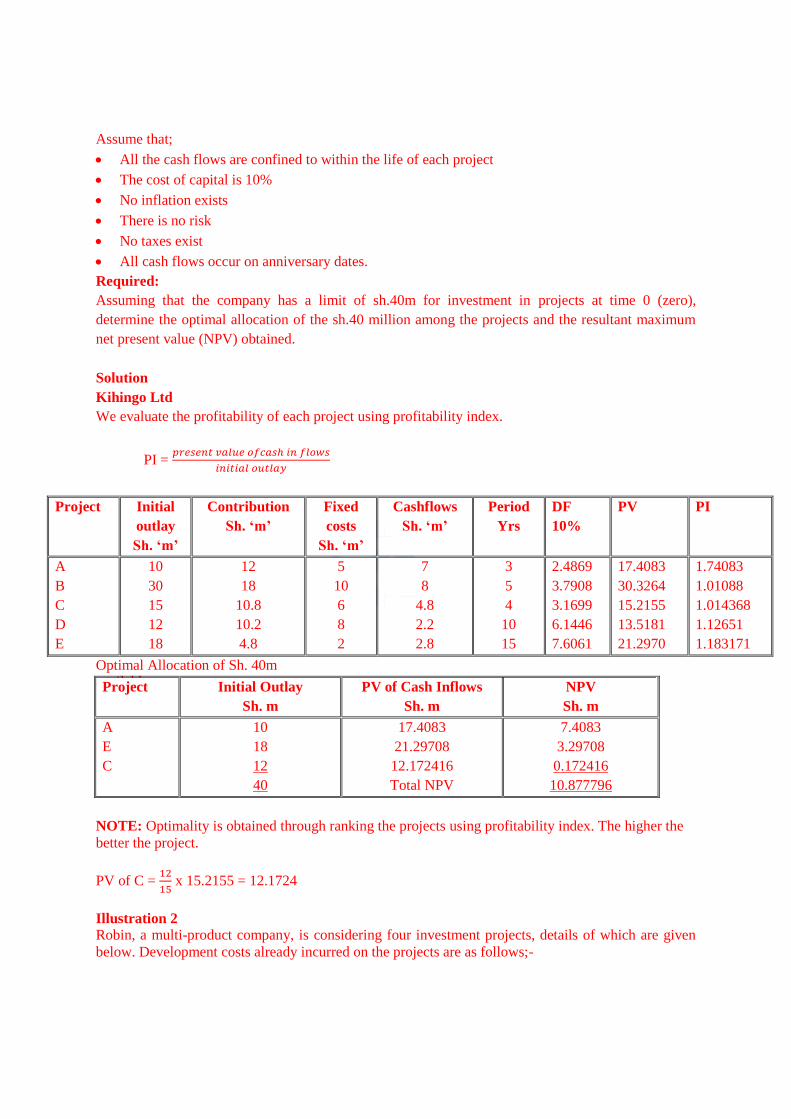

Kihingo limited is considering five project proposals as summarised below;

Project Initial cost sh.

‘million’

Annual Rev. Sh.

‘million’

Annual fixed cost sh.

‘million’

Life of the project

(Years)

A

B

C

D

E

10

30

15

12

18

20

30

18

17

8

5

10

6

8

2

3

5

4

10

15

Additional information:

1. The variable costs is 40% of the annual revenue

2. Projects D & E are mutually exclusive.

3. Each project can only be undertaken once and each is divisible.

Page 36

Assume that;

All the cash flows are confined to within the life of each project

The cost of capital is 10%

No inflation exists

There is no risk

No taxes exist

All cash flows occur on anniversary dates.

Required:

Assuming that the company has a limit of sh.40m for investment in projects at time 0 (zero),

determine the optimal allocation of the sh.40 million among the projects and the resultant maximum

net present value (NPV) obtained.

Solution

Kihingo Ltd

We evaluate the profitability of each project using profitability index.

PI = 𝑝𝑟𝑒𝑠𝑒𝑛𝑡 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓𝑐𝑎𝑠ℎ 𝑖𝑛 𝑓𝑙𝑜𝑤𝑠

𝑖𝑛𝑖𝑡𝑖𝑎𝑙 𝑜𝑢𝑡𝑙𝑎𝑦

Project Initial

outlay

Sh. ‘m’

Contribution

Sh. ‘m’

Fixed

costs

Sh. ‘m’

Cashflows

Sh. ‘m’

Period

Yrs

DF

10%

PV PI

A

B

C

D

E

10

30

15

12

18

12

18

10.8

10.2

4.8

5

10

6

8

2

7

8

4.8

2.2

2.8

3

5

4

10

15

2.4869

3.7908

3.1699

6.1446

7.6061

17.4083

30.3264

15.2155

13.5181

21.2970

1.74083

1.01088

1.014368

1.12651

1.183171

Optimal Allocation of Sh. 40m available

Project Initial Outlay

Sh. m

PV of Cash Inflows

Sh. m

NPV

Sh. m

A

E

C

10

18

12

40

17.4083

21.29708

12.172416

Total NPV

7.4083

3.29708

0.172416

10.877796

NOTE: Optimality is obtained through ranking the projects using profitability index. The higher the

better the project.

PV of C = 12

15 x 15.2155 = 12.1724

Illustration 2

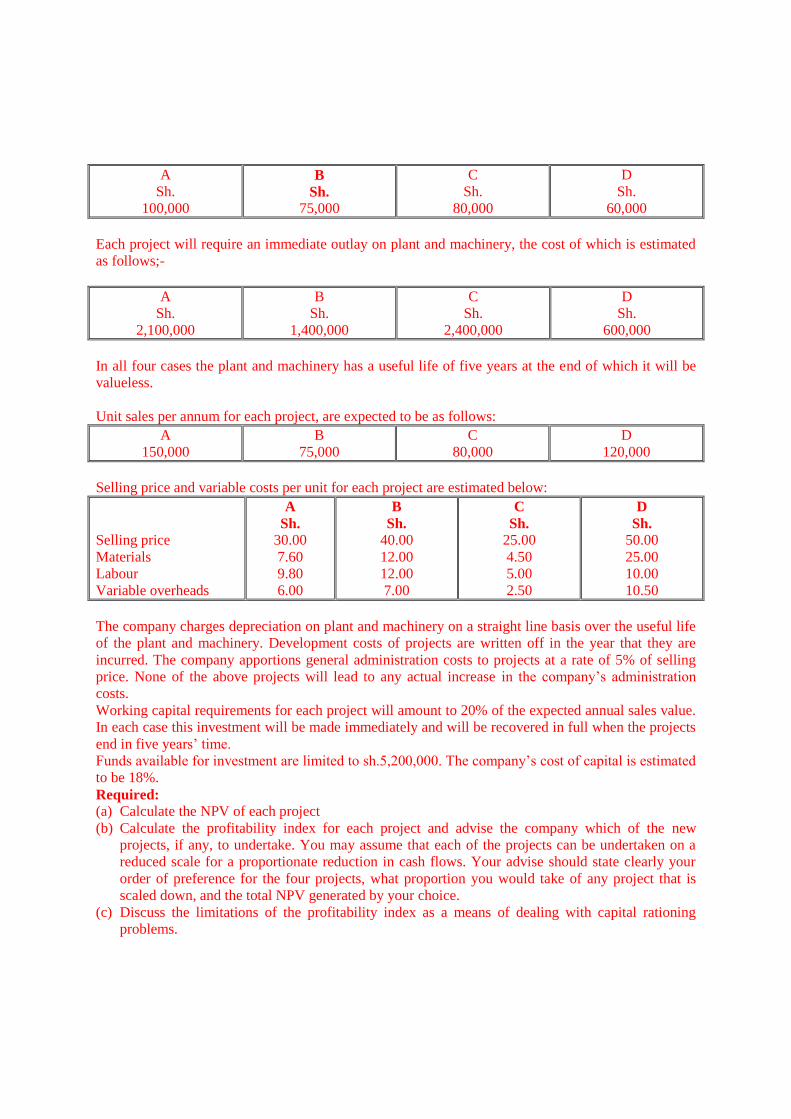

Robin, a multi-product company, is considering four investment projects, details of which are given

below. Development costs already incurred on the projects are as follows;-

Page 37

A

Sh.

100,000

B

Sh.

75,000

C

Sh.

80,000

D

Sh.

60,000

Each project will require an immediate outlay on plant and machinery, the cost of which is estimated

as follows;-

A

Sh.

2,100,000

B

Sh.

1,400,000

C

Sh.

2,400,000

D

Sh.

600,000

In all four cases the plant and machinery has a useful life of five years at the end of which it will be

valueless.

Unit sales per annum for each project, are expected to be as follows:

A

150,000

B

75,000

C

80,000

D

120,000

Selling price and variable costs per unit for each project are estimated below:

Selling price

Materials

Labour

Variable overheads

A

Sh.

30.00

7.60

9.80

6.00

B

Sh.

40.00

12.00

12.00

7.00

C

Sh.

25.00

4.50

5.00

2.50

D

Sh.

50.00

25.00

10.00

10.50

The company charges depreciation on plant and machinery on a straight line basis over the useful life

of the plant and machinery. Development costs of projects are written off in the year that they are

incurred. The company apportions general administration costs to projects at a rate of 5% of selling

price. None of the above projects will lead to any actual increase in the company’s administration

costs.

Working capital requirements for each project will amount to 20% of the expected annual sales value.

In each case this investment will be made immediately and will be recovered in full when the projects

end in five years’ time.

Funds available for investment are limited to sh.5,200,000. The company’s cost of capital is estimated

to be 18%.

Required:

(a) Calculate the NPV of each project

(b) Calculate the profitability index for each project and advise the company which of the new

projects, if any, to undertake. You may assume that each of the projects can be undertaken on a

reduced scale for a proportionate reduction in cash flows. Your advise should state clearly your

order of preference for the four projects, what proportion you would take of any project that is

scaled down, and the total NPV generated by your choice.

(c) Discuss the limitations of the profitability index as a means of dealing with capital rationing

problems.

Page 38

Solution

(a) The first step is to calculate the annual contribution from each project, together with the working

capital cash flows. These cash flows, together with the initial outlay, can then be discounted at the

cost of capital to arrive at the NPV of each project. Development costs already incurred are

irrelevant. There are no additional administration costs associated with the projects and

depreciation is also irrelevant tax rate is not provided.

First, calculate annual contribution

Unit sales

Selling price per unit

Material cost per unit

Labour cost per unit

Variable overheads per unit

Sales per annum

Materials

Labour

Variable overheads

Annual contribution

Working capital requirement

(20% annual sales value)

A

150,000

Sh.

30.00

7.60

9.80

6.00

Sh.000

4,500

(1,140)

(1,470)

(900)

990

A

Sh.000

900

B

75,000

Sh.

40.00

12.00

12.00

7.00

Sh.000

3,000

(900)

(900)

(525)

675

B

Sh.000

600

C

80,000

Sh.

25.00

4.50

5.00

2.50

Sh.000

2,000

(360)

(400)

(200)

1,040

C

Sh.000

400

D

120,000

Sh.

50.00

25.00

10.00

10.50

Sh.000

6,000

(3,000)

(1,200)

(1,260)

540

D

Sh.000

1,200

Project A

Example:

Time 0 = Initial outlay + working capital

= 2100 + 900 = 3000

1 – 5 990

5 900 (Release of working capital)

Time

0

1 – 5

5

NPV

A

(3,000)

990

900

489

B

(2,000)

675

600

373

C

(2,800)

1040

400

627

D

(1,800)

540

1200

413

PVIF18%

1

3.1272 (w1)

0.4371

Working 1 (W1)

NPV for A = -3000 × 1 + 990 × 3.1272 + 900 × 0.4371 = 489.318

(b) The probability index provides a means of optimizing the NPV when there are more projects

available which yield a positive NPV than funds to invest in them. The profitability index

measures the ratio of the present value of cash inflows to the initial outlay and represents the net

present value per sh.1 invested.

Page 39

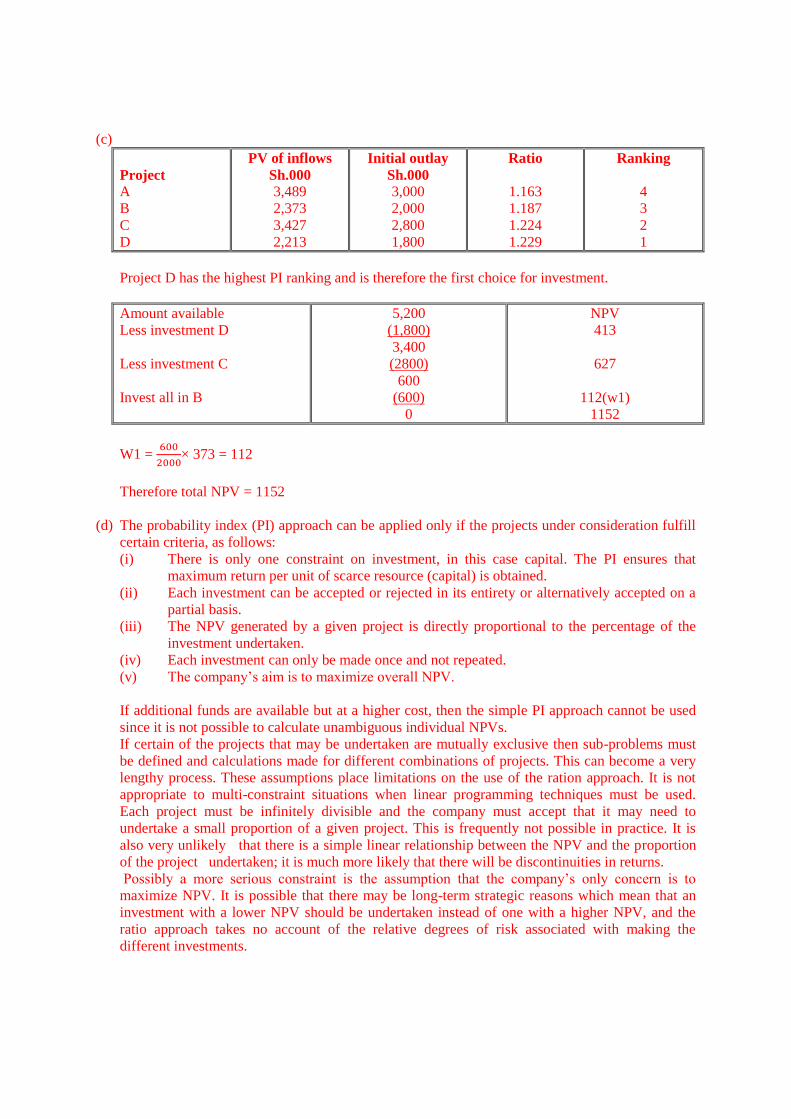

(c)

Project

A

B

C

D

PV of inflows

Sh.000

3,489

2,373

3,427

2,213

Initial outlay

Sh.000

3,000

2,000

2,800

1,800

Ratio

1.163

1.187

1.224

1.229

Ranking

4

3

2

1

Project D has the highest PI ranking and is therefore the first choice for investment.

Amount available

Less investment D

Less investment C

Invest all in B

5,200

(1,800)

3,400

(2800)

600

(600)

0

NPV

413

627

112(w1)

1152

W1 = 600

2000× 373 = 112

Therefore total NPV = 1152

(d) The probability index (PI) approach can be applied only if the projects under consideration fulfill

certain criteria, as follows:

(i) There is only one constraint on investment, in this case capital. The PI ensures that

maximum return per unit of scarce resource (capital) is obtained.

(ii) Each investment can be accepted or rejected in its entirety or alternatively accepted on a

partial basis.

(iii) The NPV generated by a given project is directly proportional to the percentage of the

investment undertaken.

(iv) Each investment can only be made once and not repeated.

(v) The company’s aim is to maximize overall NPV.

If additional funds are available but at a higher cost, then the simple PI approach cannot be used

since it is not possible to calculate unambiguous individual NPVs.

If certain of the projects that may be undertaken are mutually exclusive then sub-problems must

be defined and calculations made for different combinations of projects. This can become a very

lengthy process. These assumptions place limitations on the use of the ration approach. It is not

appropriate to multi-constraint situations when linear programming techniques must be used.

Each project must be infinitely divisible and the company must accept that it may need to

undertake a small proportion of a given project. This is frequently not possible in practice. It is

also very unlikely that there is a simple linear relationship between the NPV and the proportion

of the project undertaken; it is much more likely that there will be discontinuities in returns.

Possibly a more serious constraint is the assumption that the company’s only concern is to

maximize NPV. It is possible that there may be long-term strategic reasons which mean that an

investment with a lower NPV should be undertaken instead of one with a higher NPV, and the

ratio approach takes no account of the relative degrees of risk associated with making the

different investments.

Page 40

Illustration 3

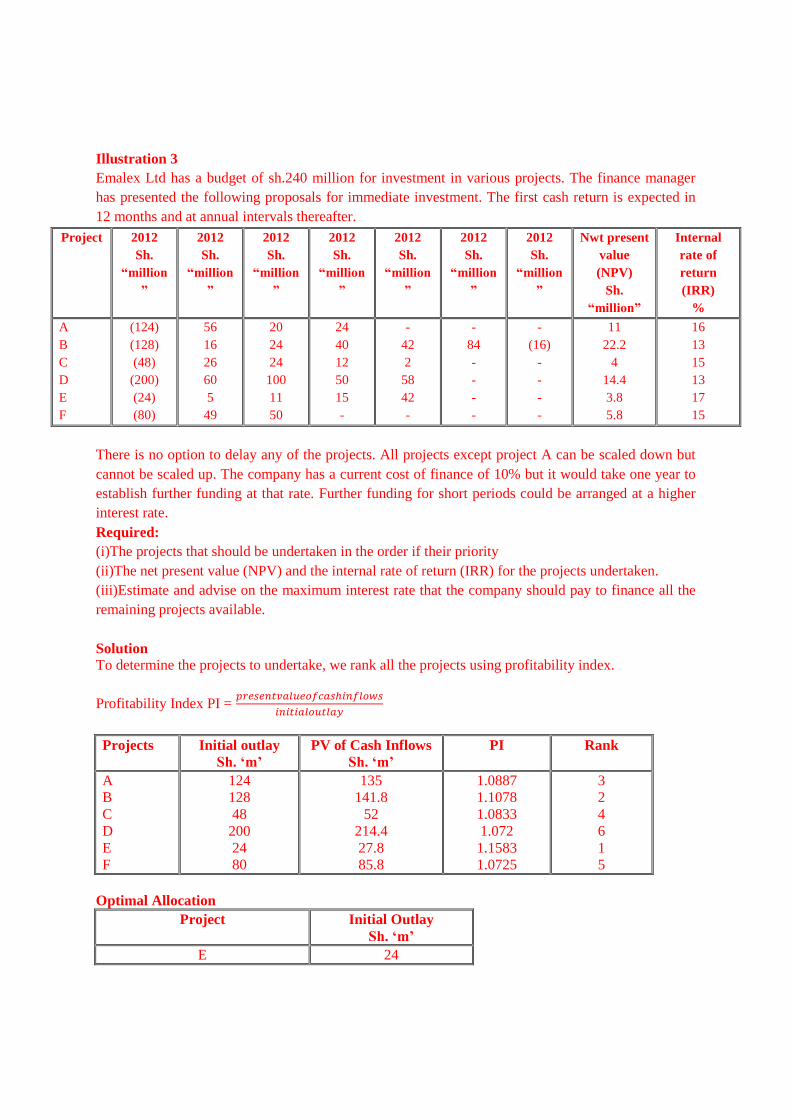

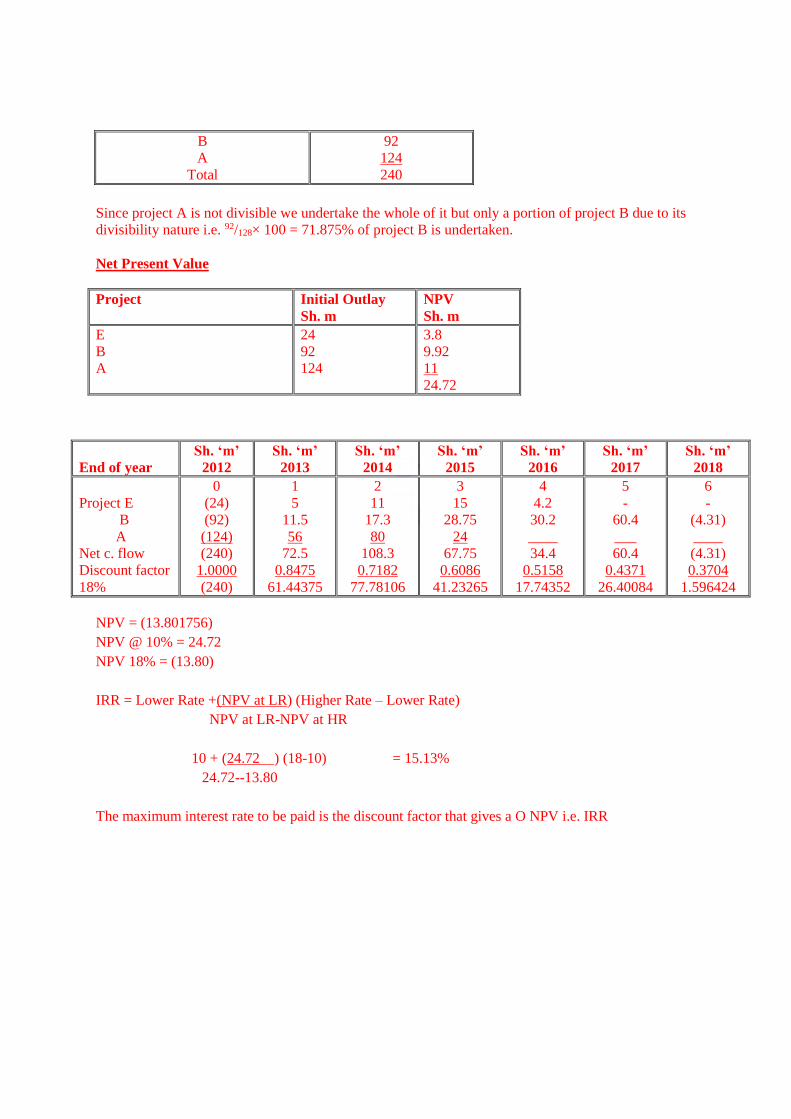

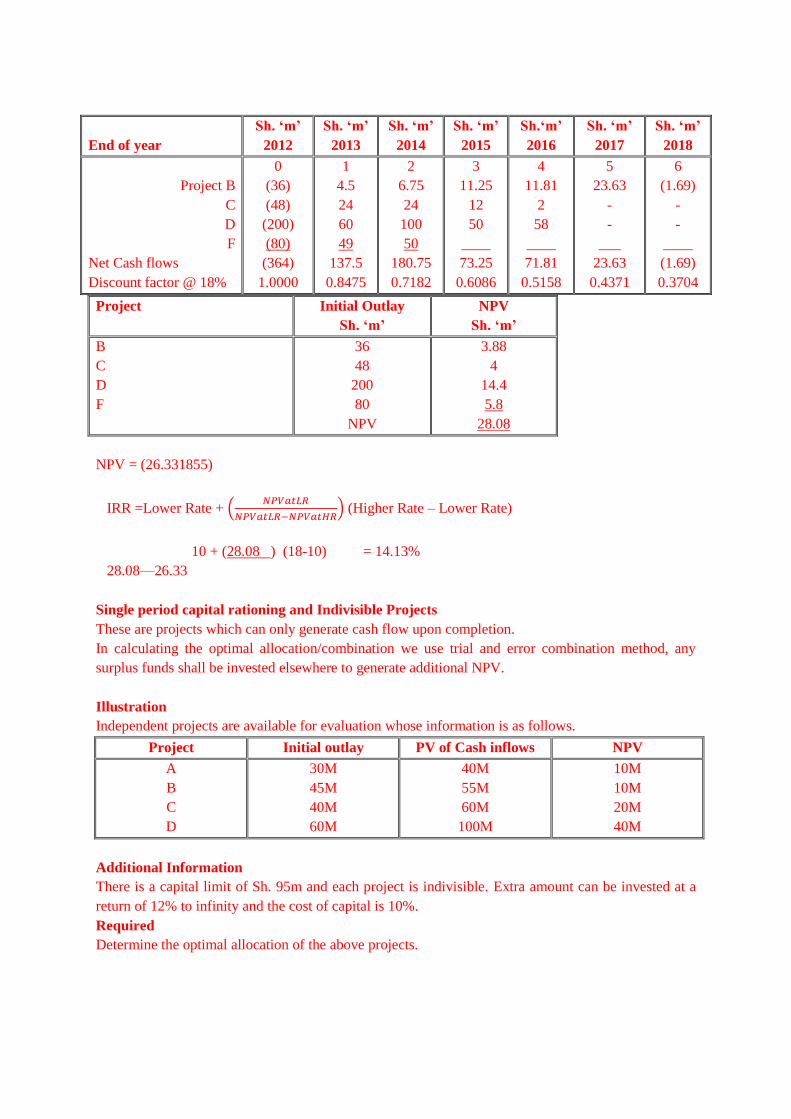

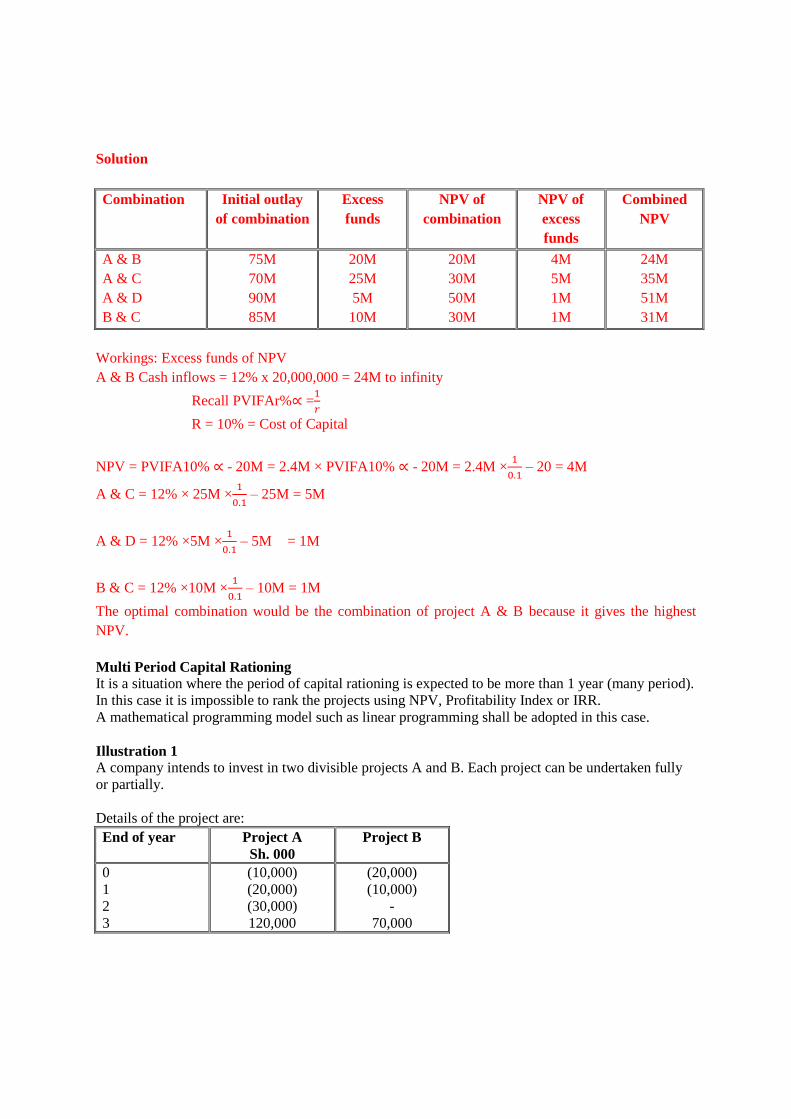

Emalex Ltd has a budget of sh.240 million for investment in various projects. The finance manager

has presented the following proposals for immediate investment. The first cash return is expected in

12 months and at annual intervals thereafter.

Project 2012

Sh.

“million

”

2012

Sh.

“million

”

2012

Sh.

“million

”

2012

Sh.

“million

”