Advanced Apportionment Issues Confronting Multi-State Companies Reporting Accurately and Strategically, Preparing for Problematic States, and Avoiding Potentially Costly Apportionment Errors Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. TUESDAY, OCTOBER 8, 2013 Presenting a live 110-minute teleconference with interactive Q&A Mark Nachbar, Principal, Ryan, Downers Grove, Ill. Gary Bingel, Partner, EisnerAmper, Iselin, N.J.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Advanced Apportionment Issues

Confronting Multi-State Companies Reporting Accurately and Strategically, Preparing for Problematic States,

and Avoiding Potentially Costly Apportionment Errors

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers.

Please refer to the instructions emailed to registrants for additional information. If you have any questions,

please contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, OCTOBER 8, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Mark Nachbar, Principal, Ryan, Downers Grove, Ill.

Gary Bingel, Partner, EisnerAmper, Iselin, N.J.

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Attendees must listen throughout the program, including the Q & A session, in

order to qualify for full continuing education credits. Strafford is required to

monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Advanced Apportionment Issues Confronting Multi-State Companies Seminar

Oct. 8, 2013

Mark Nachbar, Ryan

Gary Bingel, EisnerAmper

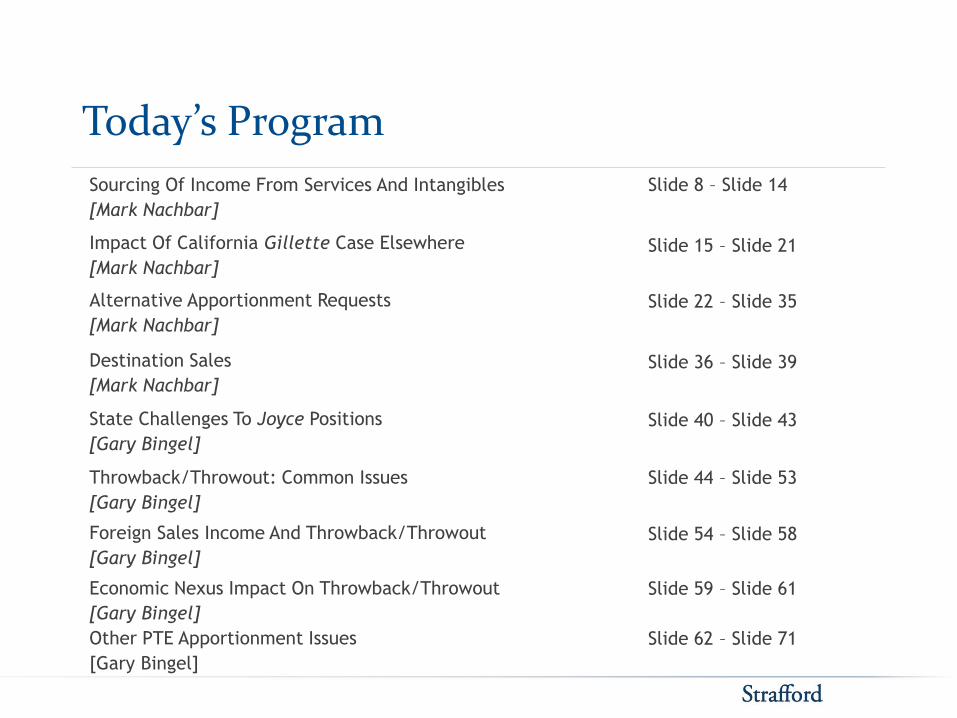

Today’s Program

Sourcing Of Income From Services And Intangibles

[Mark Nachbar]

Impact Of California Gillette Case Elsewhere

[Mark Nachbar]

Alternative Apportionment Requests

[Mark Nachbar]

Destination Sales

[Mark Nachbar]

State Challenges To Joyce Positions

[Gary Bingel]

Throwback/Throwout: Common Issues

[Gary Bingel]

Foreign Sales Income And Throwback/Throwout

[Gary Bingel]

Economic Nexus Impact On Throwback/Throwout

[Gary Bingel]

Other PTE Apportionment Issues

[Gary Bingel]

Slide 8 – Slide 14

Slide 44 – Slide 53

Slide 54 – Slide 58

Slide 59 – Slide 61

Slide 62 – Slide 71

Slide 15 – Slide 21

Slide 22 – Slide 35

Slide 36 – Slide 39

Slide 40 – Slide 43

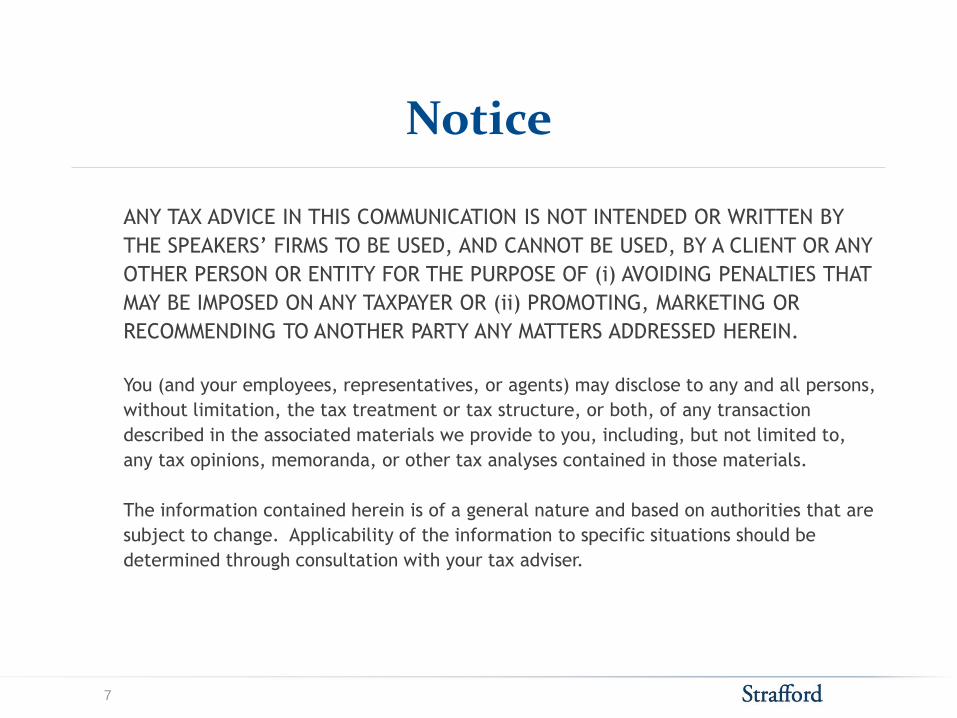

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

7

SOURCING OF SALES FROM SERVICES AND INTANGIBLES

Mark Nachbar, Ryan LLC

Sourcing Of Receipts From The Sale Of Non-Tangible Property

• Cost of performance

— Receipts from the sales of other than tangible personal property

— UDITPA Sect. 17

— Has been adopted by a majority of states

— Provides sales of tangible personal property are in a state

if:

— Income producing activity is in the state, or

— A greater proportion of income producing is in the

state.

— Sect. 17 prescribes the preponderance method.

— Alternative cost of performance measurements

— Majority of costs

— Proportionate method

9

Sourcing Of Receipts From The Sale Of Non-Tangible Property (Cont.)

— Basic issues

— What is an income-producing activity?

— At what level is it determined?

— What are direct costs?

— What costs are actually included?

— Administrative costs

— Third-party costs

— Independent contractors

— South Carolina PLR 133 (8/7/13)

— On the “behalf rule”

— Costs from other members of the unitary group

10

Sourcing Of Receipts From The Sale Of Non-Tangible Property (Cont.)

— Market-based sourcing

— Shift to market-based sourcing

— A number of states have changed their sales factor sourcing

rules, shifting from a cost of performance approach to adopt

market-based sourcing regimes for services and intangibles

receipts.

— Rationale for the shift

— The complexity of sourcing receipts from non-tangible

property

— Administrative burden on all parties to determine cost of

performance components

— Aimed at attributing revenue to the state-based “market” (i.e.,

state) that contributes to taxpayer’s income.

— If a pure market-sourcing approach applied, then the taxpayer’s

costs of performance would not be considered.

11

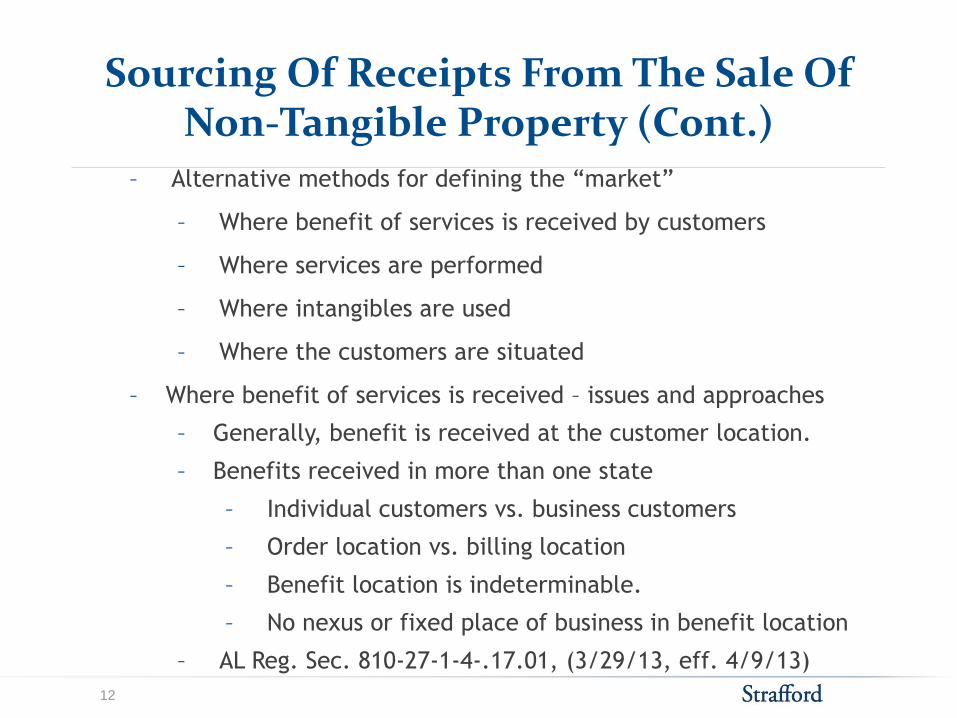

Sourcing Of Receipts From The Sale Of Non-Tangible Property (Cont.)

– Alternative methods for defining the “market”

– Where benefit of services is received by customers

– Where services are performed

– Where intangibles are used

– Where the customers are situated

– Where benefit of services is received – issues and approaches

– Generally, benefit is received at the customer location.

– Benefits received in more than one state

– Individual customers vs. business customers

– Order location vs. billing location

– Benefit location is indeterminable.

– No nexus or fixed place of business in benefit location

– AL Reg. Sec. 810-27-1-4-.17.01, (3/29/13, eff. 4/9/13)

12

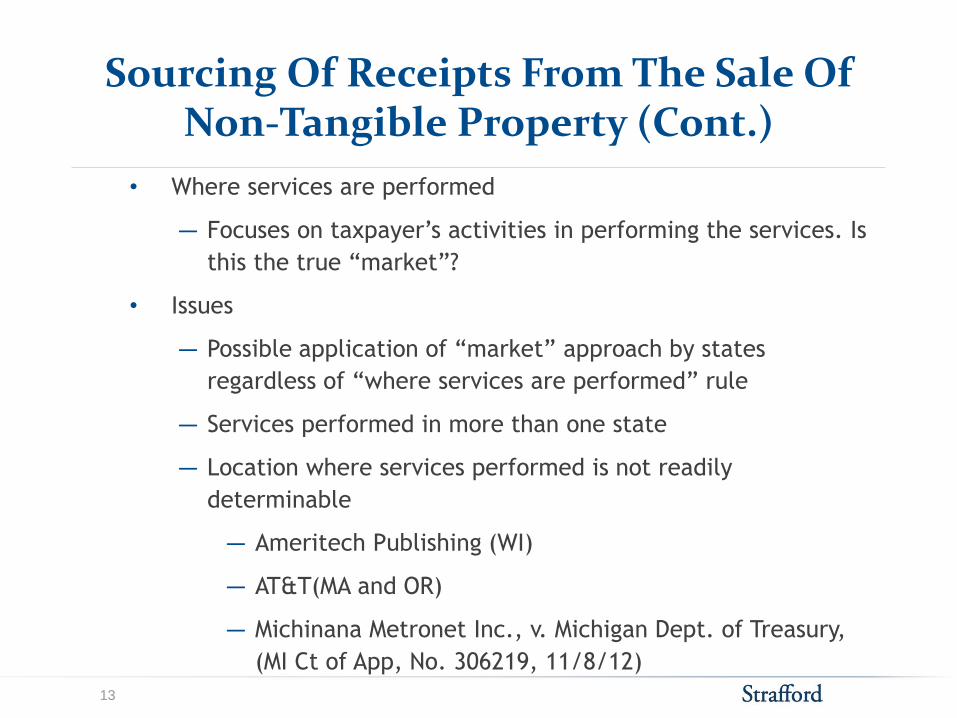

Sourcing Of Receipts From The Sale Of Non-Tangible Property (Cont.)

• Where services are performed

— Focuses on taxpayer’s activities in performing the services. Is

this the true “market”?

• Issues

— Possible application of “market” approach by states

regardless of “where services are performed” rule

— Services performed in more than one state

— Location where services performed is not readily

determinable

— Ameritech Publishing (WI)

— AT&T(MA and OR)

— Michinana Metronet Inc., v. Michigan Dept. of Treasury,

(MI Ct of App, No. 306219, 11/8/12)

13

Sourcing Of Receipts From The Sale Of Non-Tangible Property (Cont.)

— Receipts from intangibles

— Sourcing receipts derived from the sale or license of intangible property

is difficult because intangibles, by their nature, do not have a definite

geographical locations.

— Receipts are derived from intangibles through the following transactions:

— Sales of intangibles

— Licensing of intangibles in exchange for royalties

— Where intangibles are utilized – issues

— Where utilized by payor (e.g., licensee)

— Is utilization where licensee is located?

— Where licensee manufactures product?

— Where licensee sells product?

— What if location of utilization cannot be determined?

— What if taxpayer/licensor not taxable where intangibles utilized?

14

IMPACT OF CALIFORNIA GILLETTE CASE ELSEWHERE

Mark Nachbar, Ryan LLC

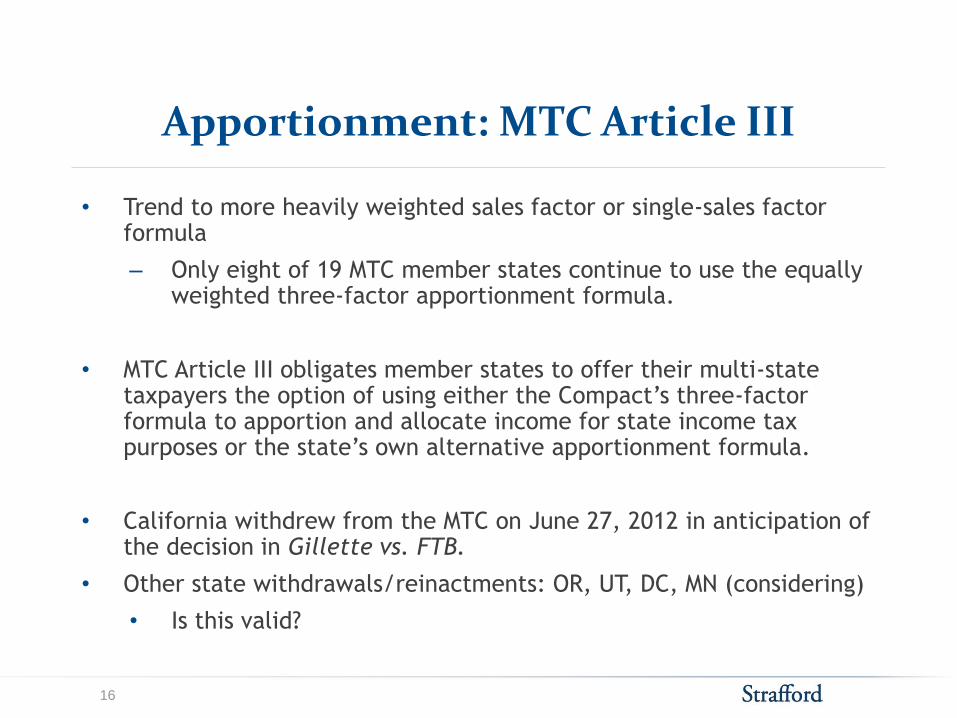

Apportionment: MTC Article III

• Trend to more heavily weighted sales factor or single-sales factor formula

– Only eight of 19 MTC member states continue to use the equally weighted three-factor apportionment formula.

• MTC Article III obligates member states to offer their multi-state taxpayers the option of using either the Compact’s three-factor formula to apportion and allocate income for state income tax purposes or the state’s own alternative apportionment formula.

• California withdrew from the MTC on June 27, 2012 in anticipation of the decision in Gillette vs. FTB.

• Other state withdrawals/reinactments: OR, UT, DC, MN (considering)

• Is this valid?

16

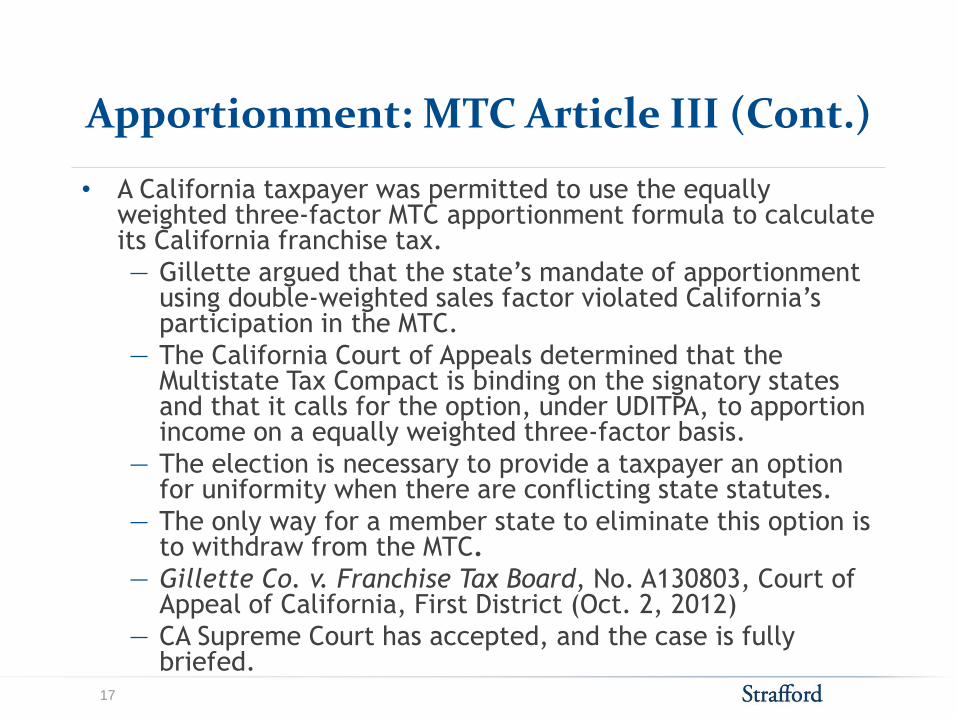

• A California taxpayer was permitted to use the equally weighted three-factor MTC apportionment formula to calculate its California franchise tax.

― Gillette argued that the state’s mandate of apportionment using double-weighted sales factor violated California’s participation in the MTC.

― The California Court of Appeals determined that the Multistate Tax Compact is binding on the signatory states and that it calls for the option, under UDITPA, to apportion income on a equally weighted three-factor basis.

― The election is necessary to provide a taxpayer an option for uniformity when there are conflicting state statutes.

― The only way for a member state to eliminate this option is to withdraw from the MTC.

― Gillette Co. v. Franchise Tax Board, No. A130803, Court of Appeal of California, First District (Oct. 2, 2012)

― CA Supreme Court has accepted, and the case is fully briefed.

Apportionment: MTC Article III (Cont.)

17

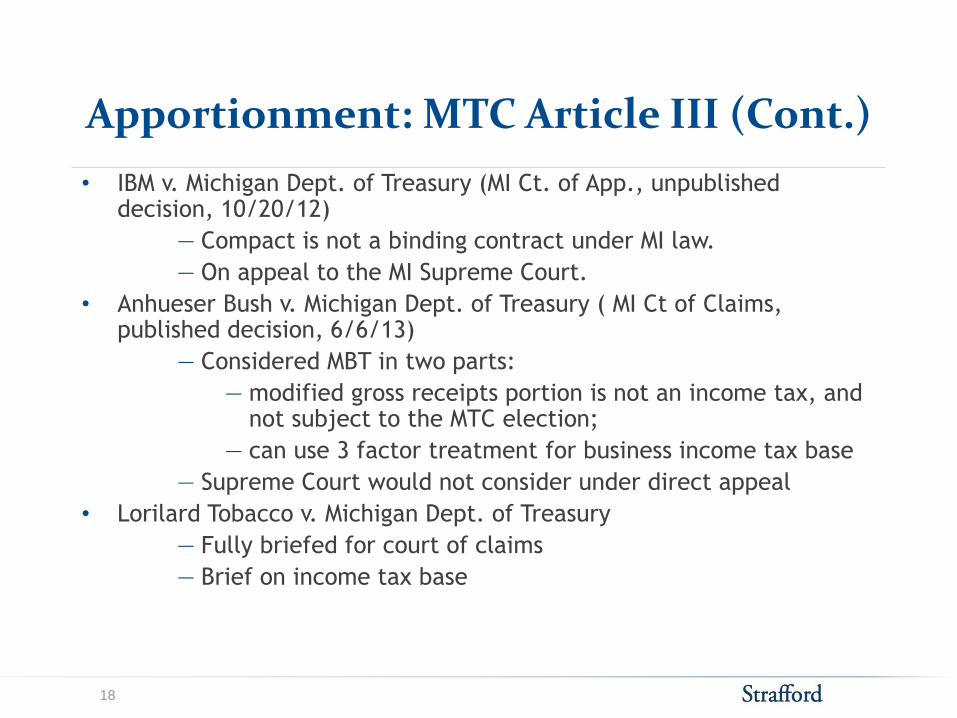

Apportionment: MTC Article III (Cont.)

• IBM v. Michigan Dept. of Treasury (MI Ct. of App., unpublished decision, 10/20/12)

― Compact is not a binding contract under MI law.

― On appeal to the MI Supreme Court.

• Anhueser Bush v. Michigan Dept. of Treasury ( MI Ct of Claims, published decision, 6/6/13)

― Considered MBT in two parts:

― modified gross receipts portion is not an income tax, and not subject to the MTC election;

― can use 3 factor treatment for business income tax base

― Supreme Court would not consider under direct appeal

• Lorilard Tobacco v. Michigan Dept. of Treasury

― Fully briefed for court of claims

― Brief on income tax base

18

Apportionment: MTC Article III (Cont.)

• In an Oregon Tax Court case, an out-of-state taxpayer is asserting that it has a

right to elect to apportion its income under the Multistate Tax Compact’s

evenly weighted three-factor formula.

• The complaint to the tax court’s magistrate division was filed on July 2. The

parties met in a case management conference in August, and on Sept. 17 filed

for a petition of special designation to bypass the magistrate division and

start the proceedings in the regular division. That petition is awaiting a ruling

by the judge.

• Oregon adopted the compact in 1967 and is still a full member. However, in

1993, the state enacted Revised Statute 314.606, which says that when

Oregon enacts an apportionment formula that conflicts with the Multistate

Tax Compact election provision, the state statute is controlling.

• Oregon currently requires single-sales-factor apportionment.

• Health Net, Incorporated and Subsidiaries v. Department of Revenue (Case

No. 120649D)

19

Apportionment: MTC Article III (Cont.)

• In orders released by the Texas Controller of Public Accounts on 9/12/12,

5/16/13, 6/18/13 and 8/14/13, denied the refund claims of three

unidentified out-of-state businesses that attempted to elect to apportion

their income under the Multistate Tax Compact’s evenly weighted three-

factor formula.

• In the 6/18/13 case the taxpayer introduced the CA Gillette win into the

record. The Comptroller ruled that no weight can be given to Gillette as it

was depublished, and cert was granted by the California Supreme Court.

• Texas adopted the Multistate Tax Compact in 1967 and is still a full member,

with the compact codified as chapter 141 of the Texas Tax Code. However,

Sect. 171.106(a) of the Code requires that a taxable entity’s margin be

apportioned to Texas under a single-factor formula based on gross receipts.

• Texas is a bit more complex than California, as there is a question as to

whether the Texas gross margins tax is an “income tax.”

20

Slide Intentionally Left Blank

ALTERNATIVE APPORTIONMENT REQUESTS

Mark Nachbar, Ryan LLC

Alternative Apportionment

• The standard alternative apportionment provision is found in

UDITPA

18.

– “If the allocation and apportionment provisions of this Act

do not fairly represent the extent of the taxpayer’s

business activity in this state, the taxpayer may petition

for or the [tax administrator] may require” alternative

apportionment.

• Under UDITPA, the burden of proof is on the party (state tax

authority or taxpayer) seeking to diverge from the standard

apportionment formula to prove that distortion exists, and

that a proposed alternative method is reasonable.

23

Invoking Alternative Apportionment

• Many states have either adopted UDITPA or similar language granting them the authority to use an alternative apportionment method.

• When a state or taxpayer wants to use an alternative apportionment method, they carry the burden of proof in showing:

– Distortion exists, and

– That a proposed alternative method is reasonable.

• Example: In Microsoft Corp. v. Franchise Tax Board, the California Supreme Court stated:

– As the party invoking section 25137, the Board has the burden of proving by clear and convincing evidence that (1) the approximation provided by the standard formula is not a fair representation, and (2) its proposed alternative is reasonable.

– 139 P.3d 1169, 1178 (Cal. 2006) (emphasis added)

24

Invoking Alternative Apportionment (Cont.)

• Burden of proof

– What standard of proof must be met for a taxpayer or state to prove distortion?

– Clear and convincing evidence

– Somewhere between preponderance of evidence and beyond a reasonable doubt

– Example: California – Microsoft v. Franchise Tax Board, 139 P.3d 1169 (Cal. 2006).

– Clear and cogent evidence

– Example: New York

– Must demonstrate by clear and cogent evidence that the standard apportionment formula does not properly reflect a taxpayer’s presence. British Land (Maryland) Inc. v. N.Y. Tax App. Trib., 85 N.Y.2d 139, 147-48 (N.Y. Ct. App. 1995)

– Prima facie evidence

25

Invoking Alternative Apportionment: Distortion

• What level of distortion must be shown in order for a taxpayer or state to be entitled to alternative apportionment?

• Constitutional “gross distortion”

– Twentieth Century-Fox Films v. Dep’t of Revenue, 700 P.2d 1035 (Ore. 1985)

– Oregon Supreme Court reviewed whether the department proved that the statutory three-factor apportionment formula did not fairly represent the extent of taxpayer’s business activity in this state, thus permitting the department to employ a different method.

– Court held that alternative apportionment is only applicable to remedy unconstitutional situations or when the UDITPA formula does not fairly represent the business activity of the taxpayer.

– Florida and Illinois – regulations provide if the statutory formula will lead to “grossly distorted” results in a particular case, a fair and accurate alternative method is appropriate. Fla. Admin. Code Ann.

12C-1.0152; 86 Ill. Admin. Code

100.3390(c)

26

Invoking Alternative Apportionment: Distortion (Cont.)

• Most states have found that the constitutional “gross

distortion” requirement is not necessary to justify alternative

apportionment – some lesser standard usually applies.

• Consistent with Sect. 18, many states require only a showing

that the statutory formula does not fairly reflect the extent of

the taxpayer’s activities in the state.

27

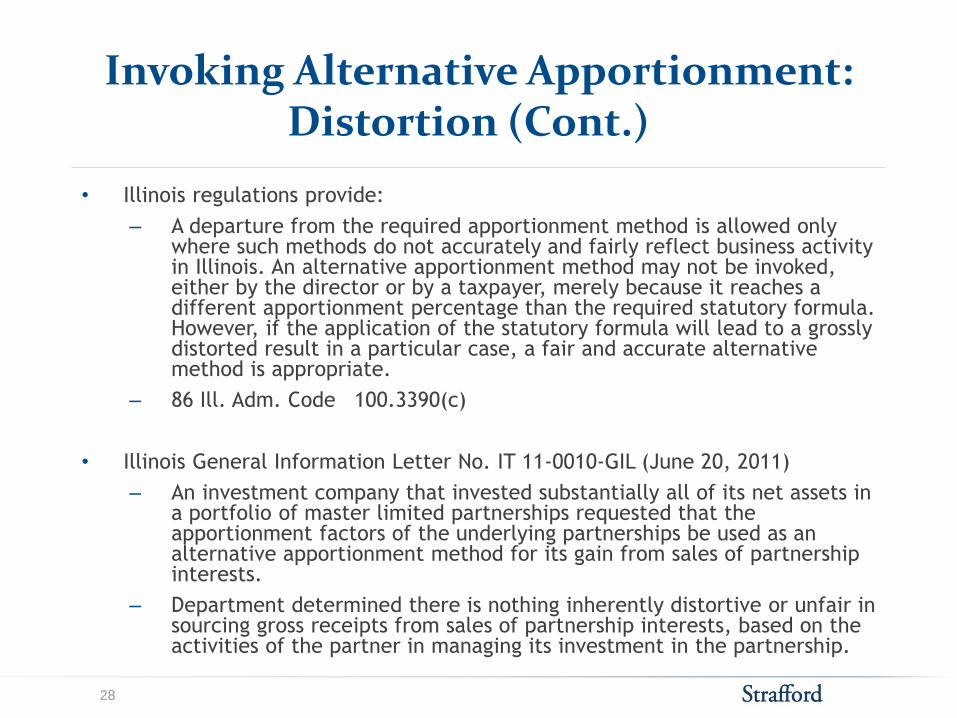

Invoking Alternative Apportionment: Distortion (Cont.)

• Illinois regulations provide:

– A departure from the required apportionment method is allowed only where such methods do not accurately and fairly reflect business activity in Illinois. An alternative apportionment method may not be invoked, either by the director or by a taxpayer, merely because it reaches a different apportionment percentage than the required statutory formula. However, if the application of the statutory formula will lead to a grossly distorted result in a particular case, a fair and accurate alternative method is appropriate.

– 86 Ill. Adm. Code

100.3390(c)

• Illinois General Information Letter No. IT 11-0010-GIL (June 20, 2011)

– An investment company that invested substantially all of its net assets in a portfolio of master limited partnerships requested that the apportionment factors of the underlying partnerships be used as an alternative apportionment method for its gain from sales of partnership interests.

– Department determined there is nothing inherently distortive or unfair in sourcing gross receipts from sales of partnership interests, based on the activities of the partner in managing its investment in the partnership.

28

Invoking Alternative Apportionment: Distortion (Cont.)

• California uses qualitative and quantitative analyses to determine if distortion exists.

― Qualitatively different

― The qualitative analysis examines the type of business conducted by the taxpayer in comparison to any activity that may create distortion.

― Quantitative distortion

― Quantitative distortion may be demonstrated by various methods including separate accounting, comparison of profit margins, comparison of apportionment percentages, comparison of income and gross receipts from various activities, etc.

― Profit margin from a taxpayer’s primary business is several orders of magnitude different from the profit margin on the treasury function.

― Courts in Microsoft and Square D found distortion where operational profit margin far exceeded treasury profit margin.

― Microsoft: Operational margin 167x greater than treasury profit margin.

― Square D: Operational margin 74x greater than treasury profit margin.

29

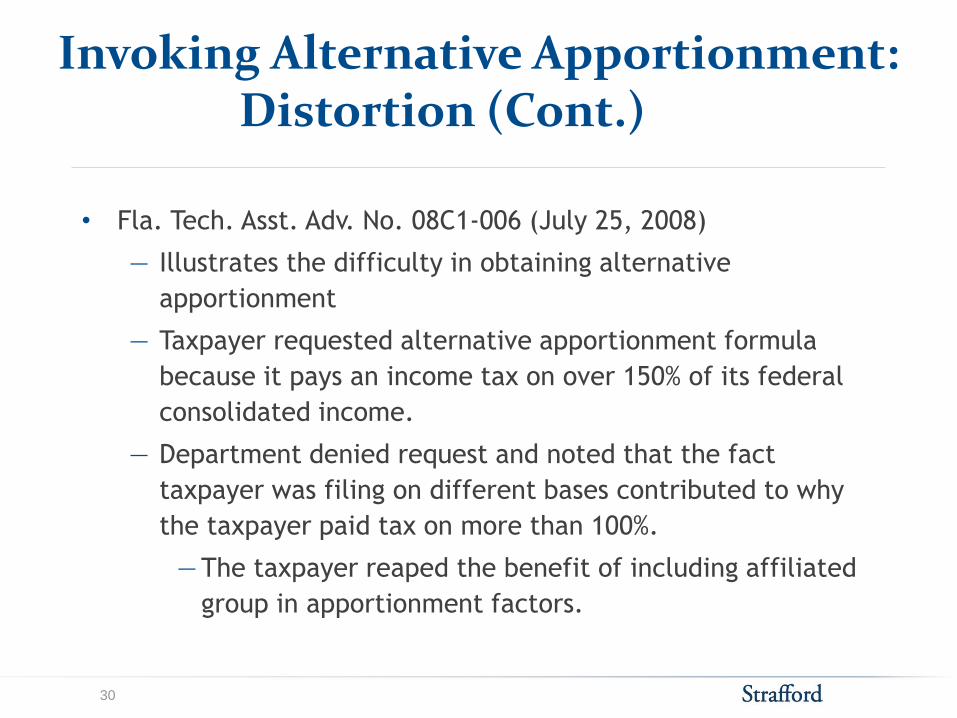

• Fla. Tech. Asst. Adv. No. 08C1-006 (July 25, 2008)

― Illustrates the difficulty in obtaining alternative

apportionment

― Taxpayer requested alternative apportionment formula

because it pays an income tax on over 150% of its federal

consolidated income.

― Department denied request and noted that the fact

taxpayer was filing on different bases contributed to why

the taxpayer paid tax on more than 100%.

― The taxpayer reaped the benefit of including affiliated

group in apportionment factors.

Invoking Alternative Apportionment: Distortion (Cont.)

30

Invoking Alternative Apportionment: Distortion (Cont.)

• BellSouth Adv. & Pub. Co. v. Chumley, 308 S.W.3d 350 (Tenn. Ct. App. 2009),

appeal denied (March 1, 2010)

― Court held that the commissioner could apply alternative apportionment

formula.

― Taxpayer sourced receipts in accordance with statute using cost of

performance (i.e., receipts sourced to Tennessee if a majority of

taxpayer’s income-producing activity occurs in Tennessee).

― Commissioner invoked an alternative apportionment formula and required

the taxpayer to use market sourcing rules.

― Court held that the commissioner established that the statutory formula

did not adequately represent the taxpayer’s business activity in the state,

based solely on the fact that BellSouth generated substantial revenue

from the distribution of advertising within the state.

― Court granted commissioner wide latitude to disregard the statutory

formula in any case in which the commissioner believes Tennessee should

be entitled to greater tax revenue, as opposed to extraordinary and

unique circumstances. 31

Invoking Alternative Apportionment: Distortion Cont.)

• While BAPCO’s “all or nothing” argument is appealing, in that the commissioner can virtually ignore the statutorily required cost of performance formula when the results are unfavorable to the Department, the fact remains that Tenn. Code Ann.

67–4–2014(a) and 67–4–2112(a) were enacted by the legislature to provide the commissioner with the authority to permit or require a departure from the standard apportionment formula, when application of the formula does not fairly represent the extent of the taxpayer’s business activity in Tennessee and the commissioner is given the authority to use any method to source receipts for purposes of the receipts factor or factors of the apportionment formula numerator or numerators.

32

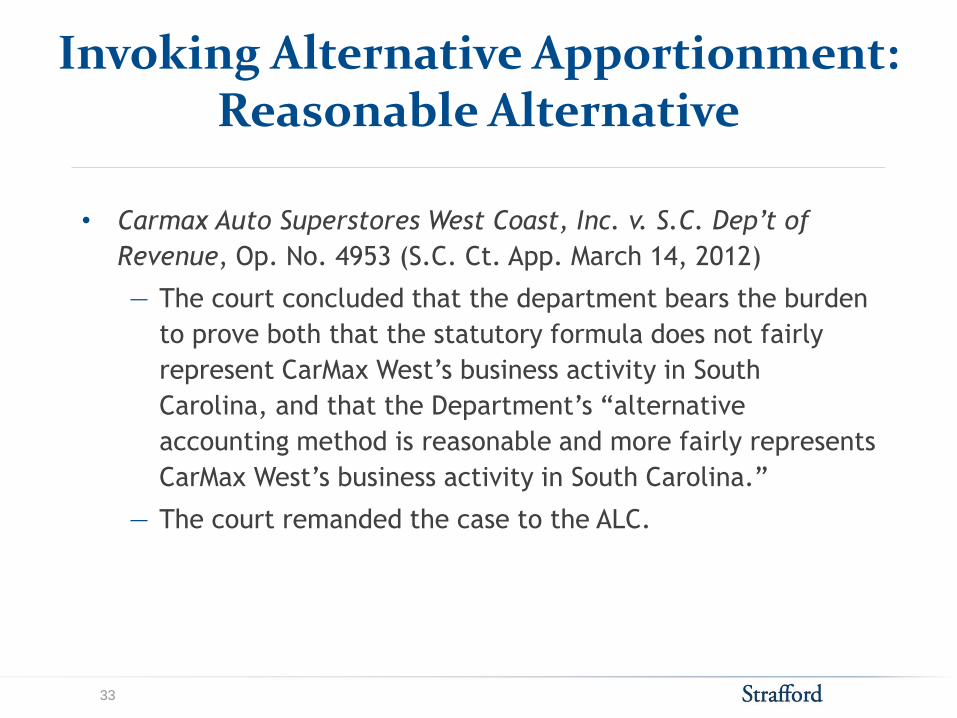

Invoking Alternative Apportionment: Reasonable Alternative

• Carmax Auto Superstores West Coast, Inc. v. S.C. Dep’t of

Revenue, Op. No. 4953 (S.C. Ct. App. March 14, 2012)

― The court concluded that the department bears the burden

to prove both that the statutory formula does not fairly

represent CarMax West’s business activity in South

Carolina, and that the Department’s “alternative

accounting method is reasonable and more fairly represents

CarMax West’s business activity in South Carolina.”

― The court remanded the case to the ALC.

33

Invoking Alternative Apportionment (Cont.)

• Taxpayers, however, should consider asserting alternative

apportionment where appropriate.

– Media General, Inc. et al. v. S.C. Dep’t of Revenue, 694

S.E.2d 525 (S. Car. 2010)

– “The Department need not automatically use the

method requested by the taxpayer as it has the

discretion to select an alternative method that fairly

measures the taxpayer's income in South Carolina.”

– Upheld taxpayer’s assertion of alternative

apportionment using combined filing method, when

state stipulated to fact that separate filing resulted in

distortion

34

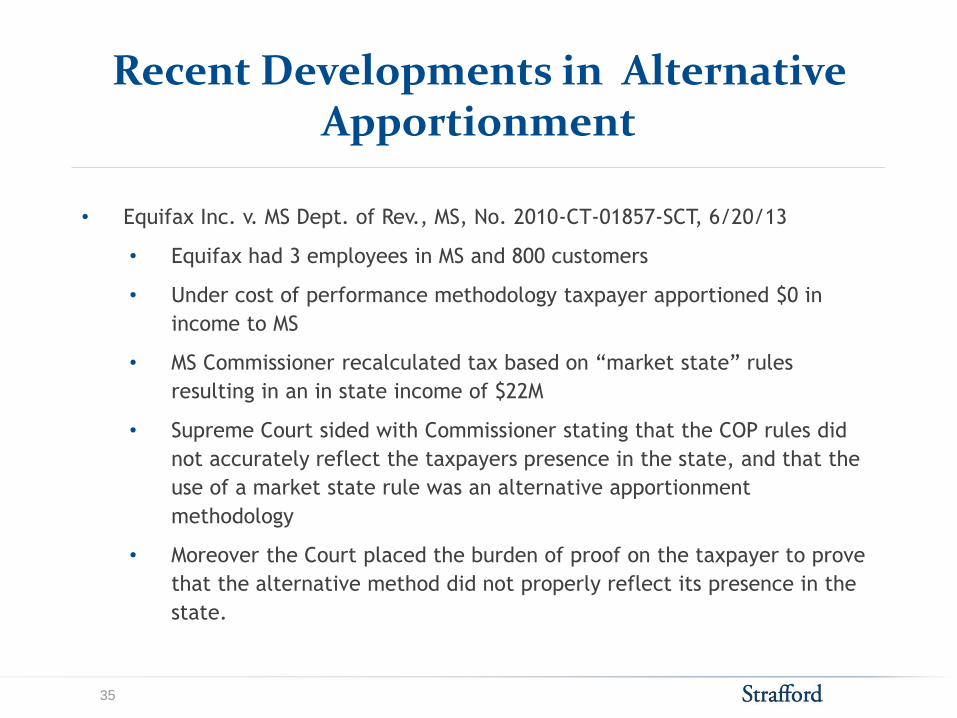

Recent Developments in Alternative Apportionment

• Equifax Inc. v. MS Dept. of Rev., MS, No. 2010-CT-01857-SCT, 6/20/13

• Equifax had 3 employees in MS and 800 customers

• Under cost of performance methodology taxpayer apportioned $0 in

income to MS

• MS Commissioner recalculated tax based on “market state” rules

resulting in an in state income of $22M

• Supreme Court sided with Commissioner stating that the COP rules did

not accurately reflect the taxpayers presence in the state, and that the

use of a market state rule was an alternative apportionment

methodology

• Moreover the Court placed the burden of proof on the taxpayer to prove

that the alternative method did not properly reflect its presence in the

state.

35

DESTINATION SOURCING

Mark Nachbar, Ryan LLC

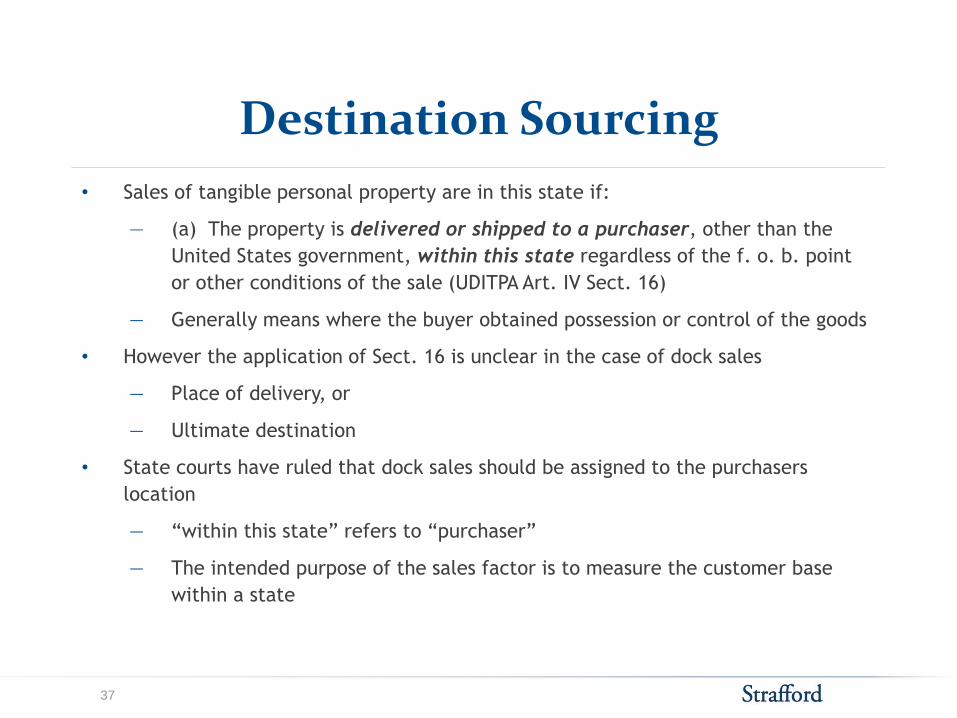

Destination Sourcing

• Sales of tangible personal property are in this state if:

― (a) The property is delivered or shipped to a purchaser, other than the

United States government, within this state regardless of the f. o. b. point

or other conditions of the sale (UDITPA Art. IV Sect. 16)

― Generally means where the buyer obtained possession or control of the goods

• However the application of Sect. 16 is unclear in the case of dock sales

― Place of delivery, or

― Ultimate destination

• State courts have ruled that dock sales should be assigned to the purchasers

location

― “within this state” refers to “purchaser”

― The intended purpose of the sales factor is to measure the customer base

within a state

37

Destination Sourcing (Cont.)

• Department of Revenue v. Parker Banana, 391 So. 2d 762, FL 1980

― Involved the sale of bananas which were picked up in Florida by out of state

purchasers

• McDonnell Douglas Corp., v FTB 26 Cal. App. 4th 1789, 7/7/94

― Customer picks up aircraft from a facility located in CA, and transports the

aircraft to an out of state location

• Indiana Dept of Revenue v. Miller Brewing Co., Indiana Supreme Court Docket

Number 49S10-1203-TA-136. 7/26/12

― Sales of beer to Indiana distributors, picked up by the distributor at an Ohio

brewery, and brought into Indiana were Indiana sales

• Virginia PLR 12-168, 10/23/12

― Intercompany sales to an instate affiliate, held by the affiliate in VA prior to

the shipment out of state, were VA sales

38

Slide Intentionally Left Blank

JOYCE / FINNIGAN POSITIONS Gary Bingel, EisnerAmper

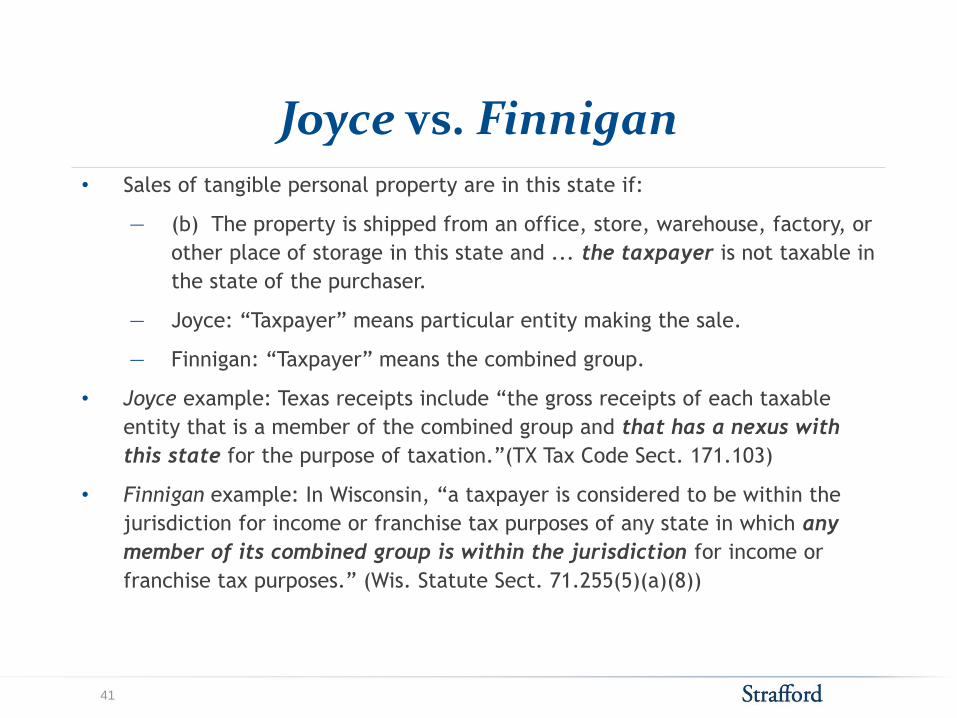

Joyce vs. Finnigan • Sales of tangible personal property are in this state if:

― (b) The property is shipped from an office, store, warehouse, factory, or

other place of storage in this state and ... the taxpayer is not taxable in

the state of the purchaser.

― Joyce: “Taxpayer” means particular entity making the sale.

― Finnigan: “Taxpayer” means the combined group.

• Joyce example: Texas receipts include “the gross receipts of each taxable

entity that is a member of the combined group and that has a nexus with

this state for the purpose of taxation.”(TX Tax Code Sect. 171.103)

• Finnigan example: In Wisconsin, “a taxpayer is considered to be within the

jurisdiction for income or franchise tax purposes of any state in which any

member of its combined group is within the jurisdiction for income or

franchise tax purposes.” (Wis. Statute Sect. 71.255(5)(a)(8))

41

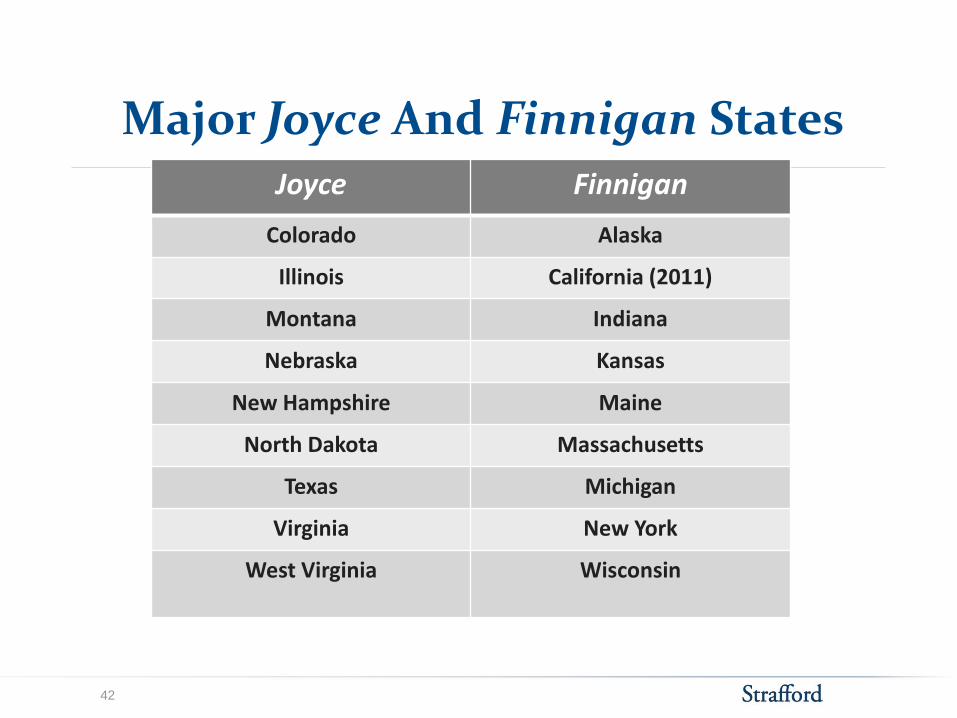

Major Joyce And Finnigan States

Joyce Finnigan

Colorado Alaska

Illinois California (2011)

Montana Indiana

Nebraska Kansas

New Hampshire Maine

North Dakota Massachusetts

Texas Michigan

Virginia New York

West Virginia Wisconsin

42

Joyce / Finnigan Nexus Controversies

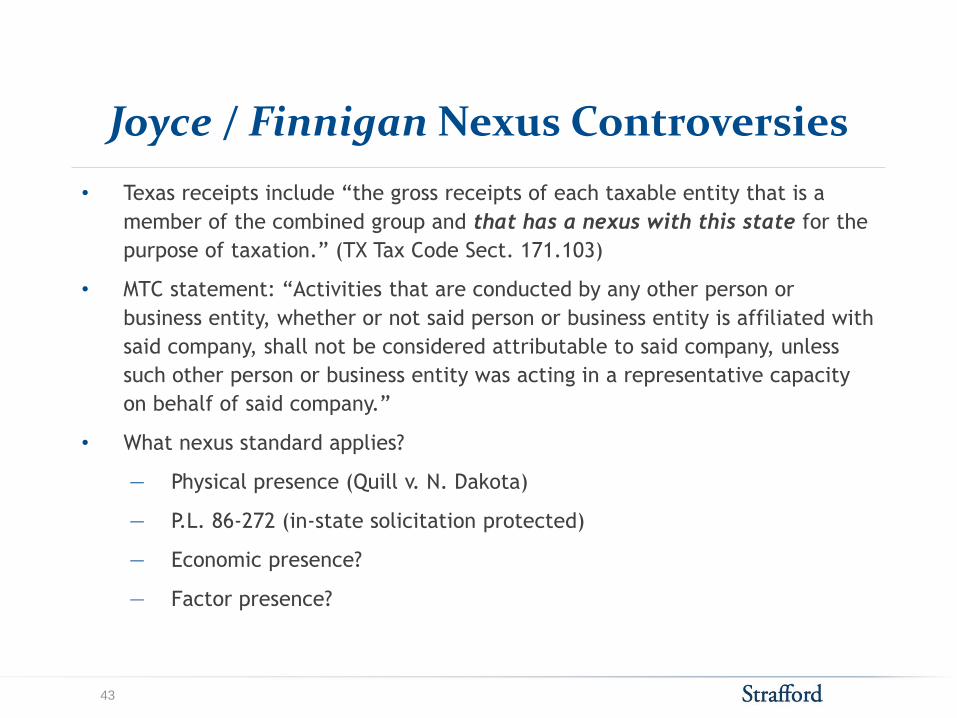

• Texas receipts include “the gross receipts of each taxable entity that is a

member of the combined group and that has a nexus with this state for the

purpose of taxation.” (TX Tax Code Sect. 171.103)

• MTC statement: “Activities that are conducted by any other person or

business entity, whether or not said person or business entity is affiliated with

said company, shall not be considered attributable to said company, unless

such other person or business entity was acting in a representative capacity

on behalf of said company.”

• What nexus standard applies?

― Physical presence (Quill v. N. Dakota)

― P.L. 86-272 (in-state solicitation protected)

― Economic presence?

― Factor presence?

43

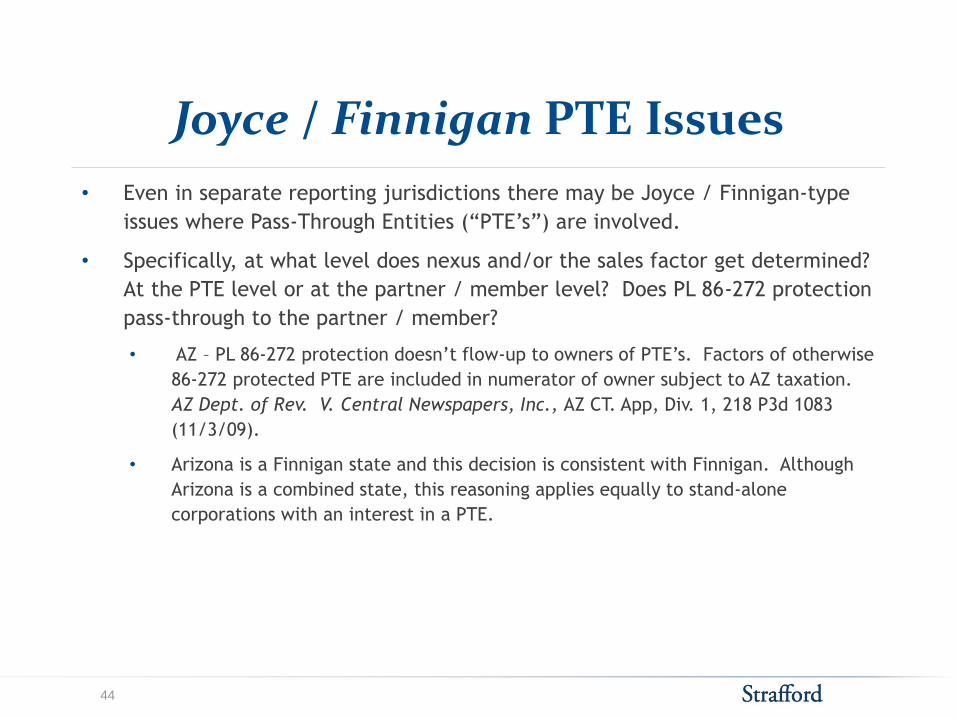

Joyce / Finnigan PTE Issues

• Even in separate reporting jurisdictions there may be Joyce / Finnigan-type

issues where Pass-Through Entities (“PTE’s”) are involved.

• Specifically, at what level does nexus and/or the sales factor get determined?

At the PTE level or at the partner / member level? Does PL 86-272 protection

pass-through to the partner / member?

• AZ – PL 86-272 protection doesn’t flow-up to owners of PTE’s. Factors of otherwise

86-272 protected PTE are included in numerator of owner subject to AZ taxation.

AZ Dept. of Rev. V. Central Newspapers, Inc., AZ CT. App, Div. 1, 218 P3d 1083

(11/3/09).

• Arizona is a Finnigan state and this decision is consistent with Finnigan. Although

Arizona is a combined state, this reasoning applies equally to stand-alone

corporations with an interest in a PTE.

44

Joyce / Finnigan PTE Issues

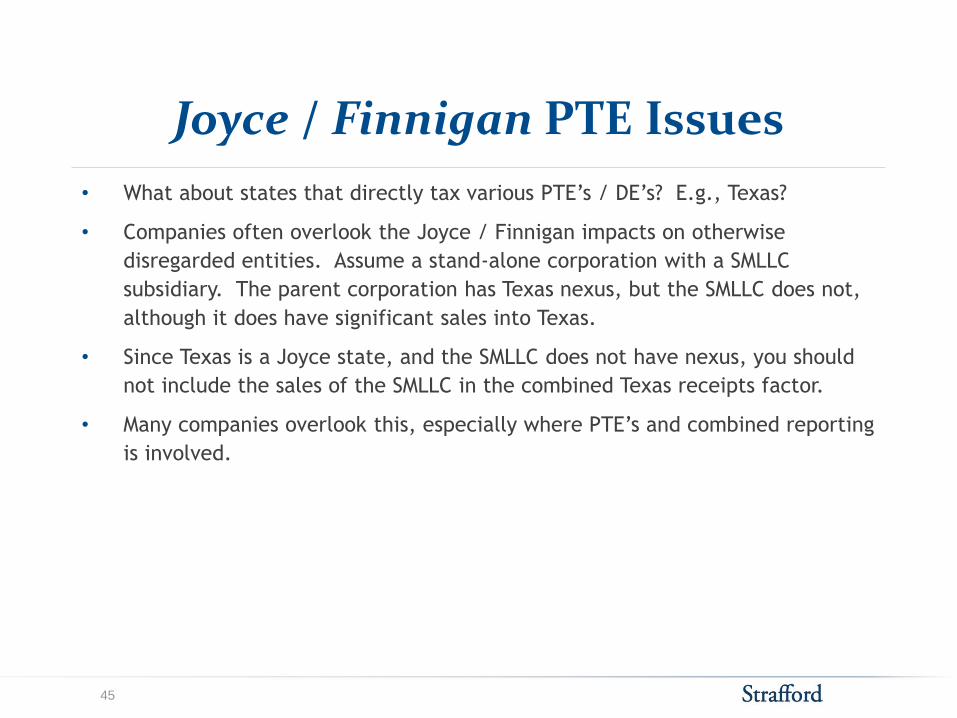

• What about states that directly tax various PTE’s / DE’s? E.g., Texas?

• Companies often overlook the Joyce / Finnigan impacts on otherwise

disregarded entities. Assume a stand-alone corporation with a SMLLC

subsidiary. The parent corporation has Texas nexus, but the SMLLC does not,

although it does have significant sales into Texas.

• Since Texas is a Joyce state, and the SMLLC does not have nexus, you should

not include the sales of the SMLLC in the combined Texas receipts factor.

• Many companies overlook this, especially where PTE’s and combined reporting

is involved.

45

THROWBACK/THROWOUT: COMMON ISSUES

Gary Bingel, EisnerAmper

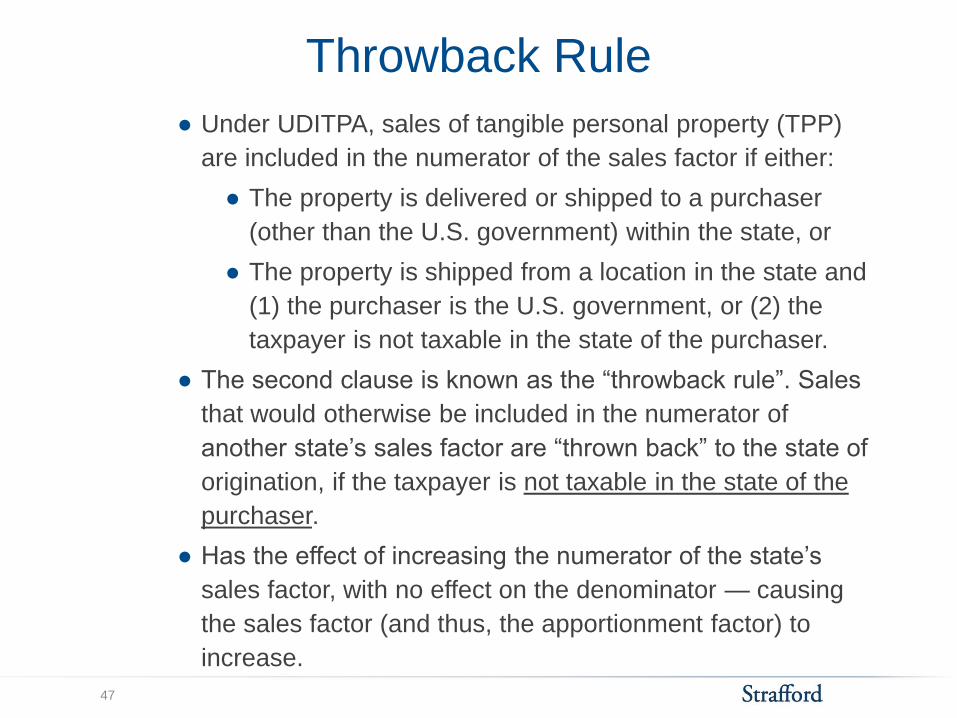

Throwback Rule

● Under UDITPA, sales of tangible personal property (TPP)

are included in the numerator of the sales factor if either:

● The property is delivered or shipped to a purchaser

(other than the U.S. government) within the state, or

● The property is shipped from a location in the state and

(1) the purchaser is the U.S. government, or (2) the

taxpayer is not taxable in the state of the purchaser.

● The second clause is known as the “throwback rule”. Sales

that would otherwise be included in the numerator of

another state’s sales factor are “thrown back” to the state of

origination, if the taxpayer is not taxable in the state of the

purchaser.

● Has the effect of increasing the numerator of the state’s

sales factor, with no effect on the denominator — causing

the sales factor (and thus, the apportionment factor) to

increase.

47

Throwback Rule: Common Issues ● The phrase “taxable in the state of the purchaser” is not defined in UDITPA.

● However, another section of UDITPA (relating to whether the taxpayer

has the right to apportion) provides that a taxpayer is “taxable in

another state” if:

● (1) In that state, it is subject to a net income tax, a franchise tax

measured by net income, a franchise tax for the privilege of doing

business, or a corporate stock tax; or (2) that state has jurisdiction

to subject the taxpayer to a net income tax regardless of whether,

in fact, the state does or does not.

● Some common circumstances in which a state might attempt to require

throwback:

● The taxpayer does not have nexus with the destination state.

● The taxpayer is protected by P.L 86-272 in the destination state.

● The destination state does not impose an income tax or franchise

tax.

● The taxpayer does not actually file an income or franchise tax

return in the destination state.

48

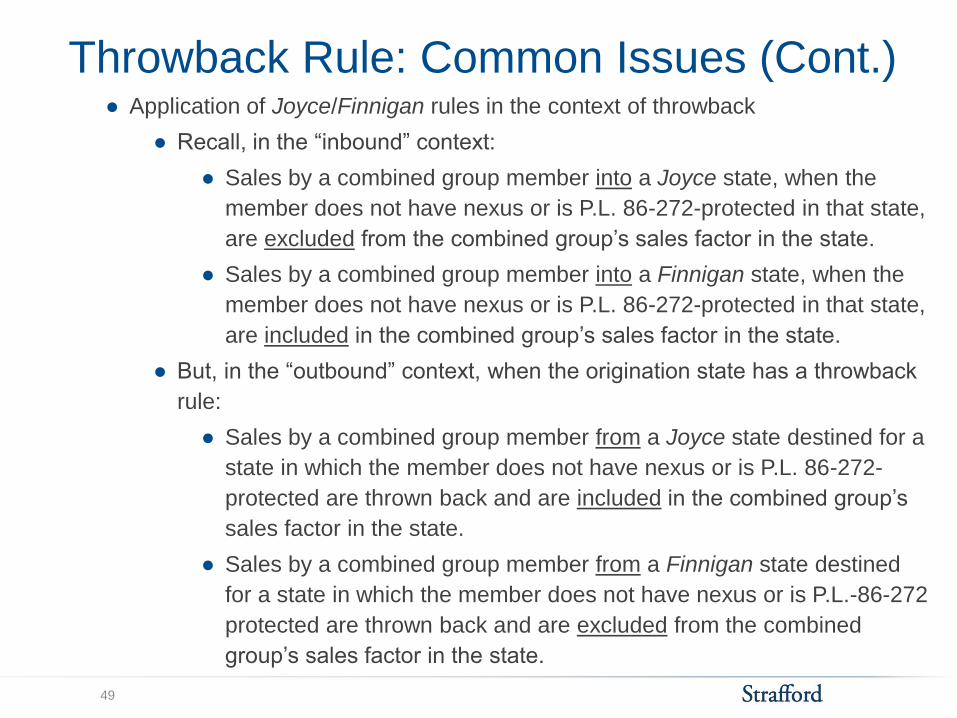

Throwback Rule: Common Issues (Cont.) ● Application of Joyce/Finnigan rules in the context of throwback

● Recall, in the “inbound” context:

● Sales by a combined group member into a Joyce state, when the

member does not have nexus or is P.L. 86-272-protected in that state,

are excluded from the combined group’s sales factor in the state.

● Sales by a combined group member into a Finnigan state, when the

member does not have nexus or is P.L. 86-272-protected in that state,

are included in the combined group’s sales factor in the state.

● But, in the “outbound” context, when the origination state has a throwback

rule:

● Sales by a combined group member from a Joyce state destined for a

state in which the member does not have nexus or is P.L. 86-272-

protected are thrown back and are included in the combined group’s

sales factor in the state.

● Sales by a combined group member from a Finnigan state destined

for a state in which the member does not have nexus or is P.L.-86-272

protected are thrown back and are excluded from the combined

group’s sales factor in the state.

49

Throwback Rule: Common Issues (Cont.)

● Application of Joyce/Finnigan rules in the context of throwback

● May cause perceived under-inclusion or over-inclusion of

sales

● Sales of TPP made by a combined group member

from a Joyce state that has a throwback rule into a

Finnigan state in which another group member is

taxable will be included in the combined group’s sales

factor numerator in both states.

● Potentially beneficial to create a taxable presence

in the Finnigan state by the entity in the Joyce

state, which would cause the throwback rule to

not apply

● Sales of TPP made by a combined group member

from a Finnigan state that has a throwback rule into a

Joyce state in which another group member is taxable

will be excluded from the combined group’s sales

factor numerator in both states.

50

Throwout Rule: Whirlpool

•Whirlpool v. Div. of Taxation (N.J., July 28, 2011)

● The taxpayer argued that New Jersey’s throwout rule was facially

unconstitutional.

● New Jersey Supreme Court held the throwout rule was not facially

unconstitutional as applied to receipts attributed to states in which

the taxpayer was not subject to tax by virtue of P.L. 86-272 or did not

have requisite contacts to establish nexus.

― However, the throwout rule did not operate permissibly

with respect to receipts attributed to states that choose

not to impose a business activity tax.

● Court determined the Legislature intended rule to be applied

narrowly; thus, the rule was not unconstitutional on its face.

51

Sales Factor: Throwback/Throwout Rules

Sales Of TPP (2012)

52

No Tax

No throwback or throw-out

Throwback (DC, RI)

Throwback/Double Throwback (AK, HI)

Throw-out

TX – Throwback rule for the former

franchise tax; no throwback rule

under revised franchise tax

MO – Throwback

only applies for

purposes of the

three-factor formula;

there is no throwback

for single factor

formula.

MA – Unique

throwback rule

based on sales

office

NJ – Throw-

out repealed

beginning for

periods on or

after July 1,

2010

KY & TN –

Throwback for sales

to U.S. govt. only

Slide Intentionally Left Blank

FOREIGN SALES INCOME AND THROWBACK/THROWOUT

Gary Bingel, EisnerAmper

Throwback/Throwout: Foreign Sales

● How does a taxpayer apply a throwback or throwout rule, when a

sale is made into a foreign country?

● Note that UDITPA’s definition of “state” includes foreign countries.

Accordingly, sales into a foreign country may be thrown back if

both (1) the taxpayer is not subject to tax in the foreign country,

and (2) the foreign country does not have jurisdiction to tax the

taxpayer.

● One of the more difficult questions: How does a taxpayer determine

whether the foreign country has jurisdiction to tax the taxpayer?

● Apply U.S. jurisdictional principles?

● Apply jurisdictional principles of the foreign country?

● How does an income tax treaty affect the analysis, if at all?

55

Throwback/Throwout: Foreign Sales (Cont.)

● Apply U.S. jurisdictional principles to determine taxability

● Some states apply U.S. constitutional nexus principles and

P.L. 86-272 to foreign countries.

● Basically, treat the foreign country as if it is one of the

states

● Other states may apply U.S. constitutional nexus principles

but not P.L. 86-272.

● By its terms, P.L. 86-272 applies to “interstate” — and not

international — commerce.

● This is favorable for taxpayers in the throwback context;

solicitation of sales of TPP alone may be enough to

prevent throwback.

56

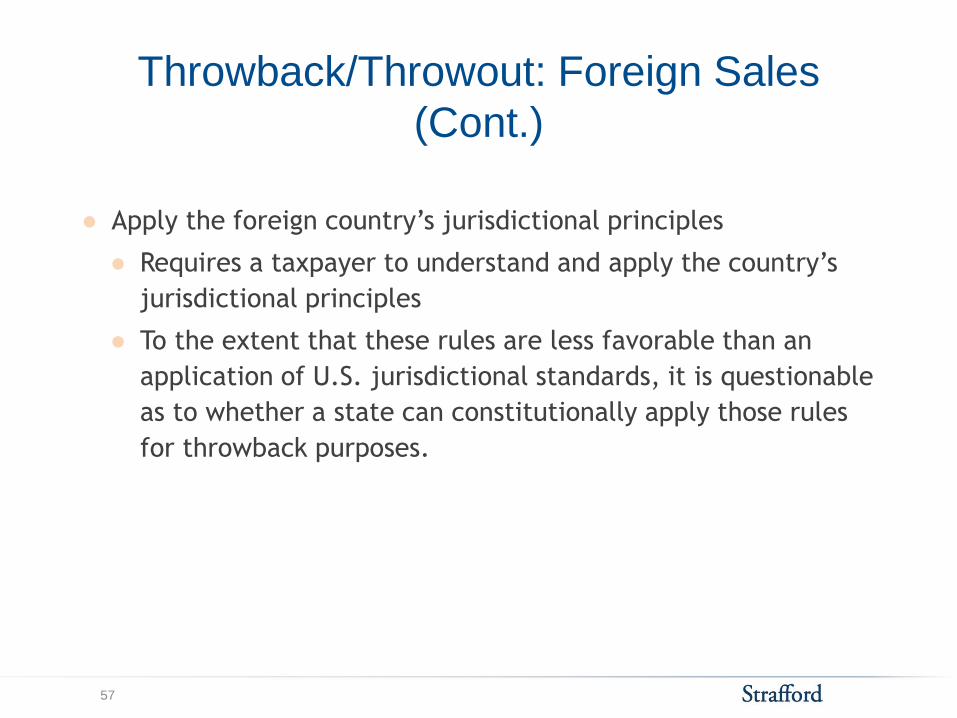

Throwback/Throwout: Foreign Sales

(Cont.)

● Apply the foreign country’s jurisdictional principles

● Requires a taxpayer to understand and apply the country’s

jurisdictional principles

● To the extent that these rules are less favorable than an

application of U.S. jurisdictional standards, it is questionable

as to whether a state can constitutionally apply those rules

for throwback purposes.

57

Throwback/Throwout: Foreign Sales

(Cont.)

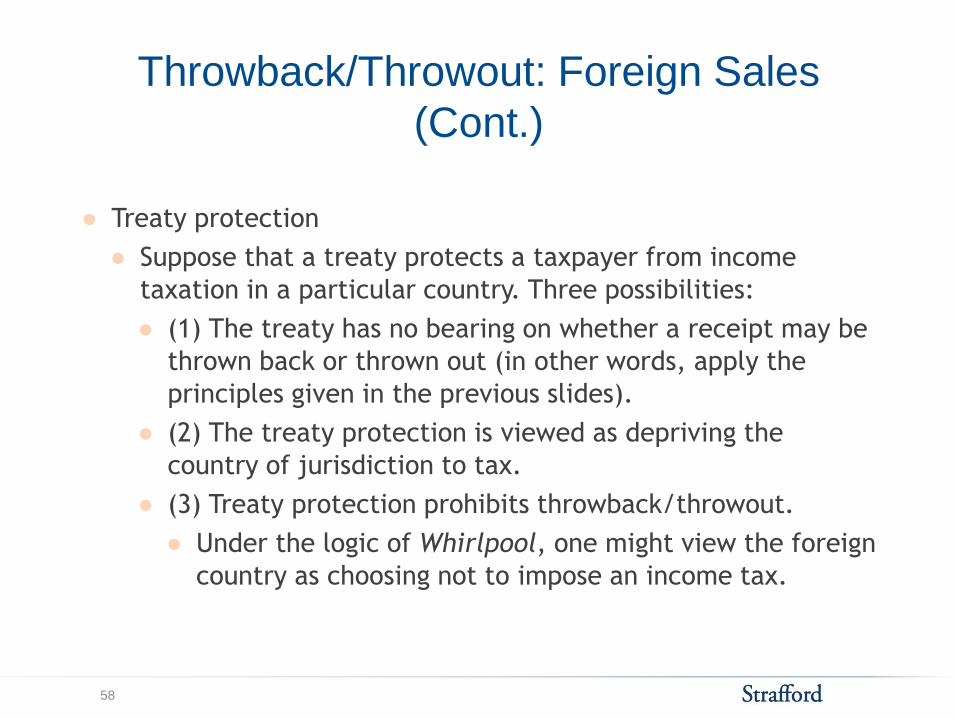

● Treaty protection

● Suppose that a treaty protects a taxpayer from income

taxation in a particular country. Three possibilities:

● (1) The treaty has no bearing on whether a receipt may be

thrown back or thrown out (in other words, apply the

principles given in the previous slides).

● (2) The treaty protection is viewed as depriving the

country of jurisdiction to tax.

● (3) Treaty protection prohibits throwback/throwout.

● Under the logic of Whirlpool, one might view the foreign

country as choosing not to impose an income tax.

58

ECONOMIC NEXUS IMPACT ON THROWBACK/THROWOUT

Gary Bingel, EisnerAmper

Throwback/Throwout: Economic Nexus

Provisions

● How do state “doing business” rules affect throwback/throwout?

● Specifically, if a state has an economic nexus statute, to

determine throwback/throwout, should a taxpayer apply those

economic nexus provisions?

● Yes – otherwise, would violate “internal consistency” doctrine

● Example

● Assume a California taxpayer has more than $500,000 in sales

of TPP destined for State X. Further assume that the taxpayer

is not protected by P.L. 86-272 in State X.

● Under these facts, the taxpayer would not have to throw

back sales made into State X to California. Chief Counsel

Ruling 2012-03

60

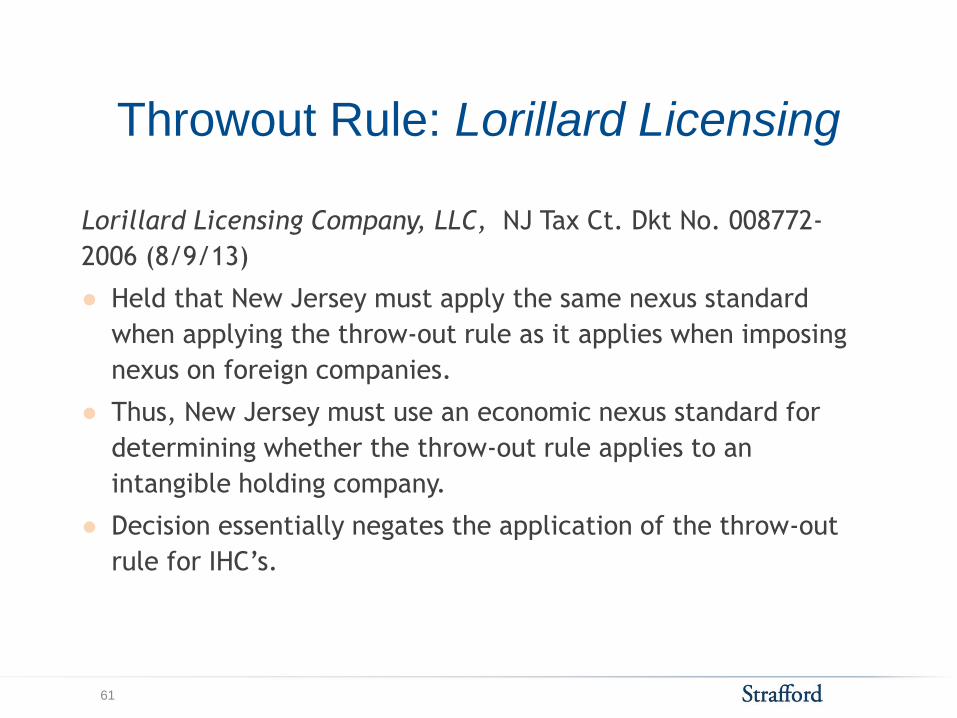

Throwout Rule: Lorillard Licensing

Lorillard Licensing Company, LLC, NJ Tax Ct. Dkt No. 008772-

2006 (8/9/13)

● Held that New Jersey must apply the same nexus standard

when applying the throw-out rule as it applies when imposing

nexus on foreign companies.

● Thus, New Jersey must use an economic nexus standard for

determining whether the throw-out rule applies to an

intangible holding company.

● Decision essentially negates the application of the throw-out

rule for IHC’s.

61

OTHER PTE APPORTIONMENT ISSUES

Gary Bingel, EisnerAmper

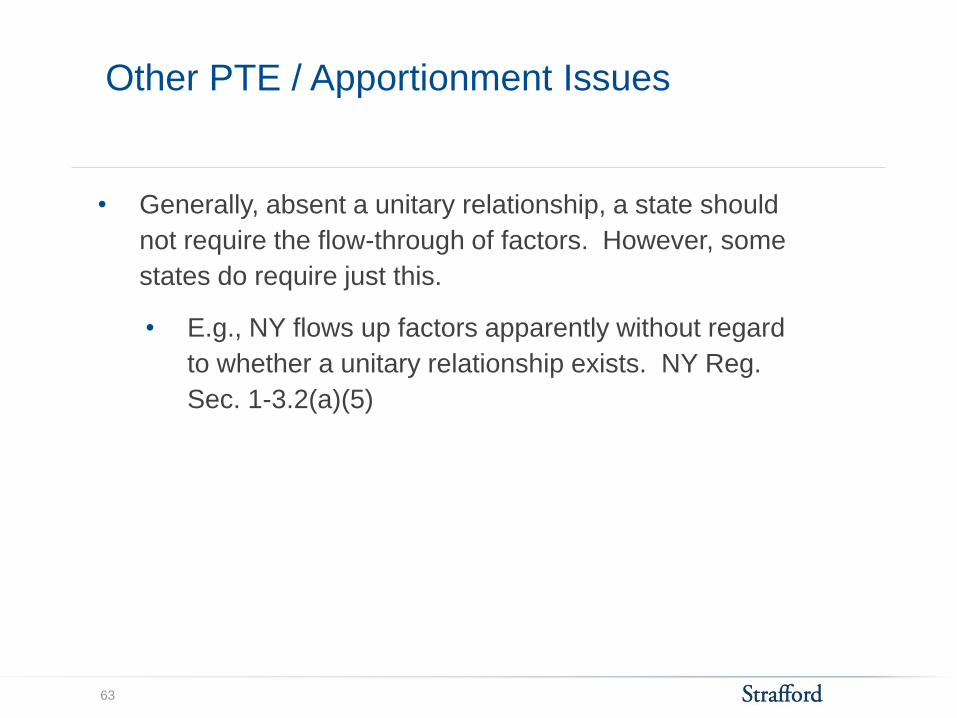

Other PTE / Apportionment Issues

• Generally, absent a unitary relationship, a state should

not require the flow-through of factors. However, some

states do require just this.

• E.g., NY flows up factors apparently without regard

to whether a unitary relationship exists. NY Reg.

Sec. 1-3.2(a)(5)

63

Other PTE Apportionment Issues

I. Possible factors to consider include:

• Is there a unitary relationship?

• Did the owner elect flow-through treatment for the

PTE (as opposed to it being the default)?

• Limited liability?

• Is ownership freely transferable?

• Is ownership greater than 50%?

• Is the ownership an investment?

64

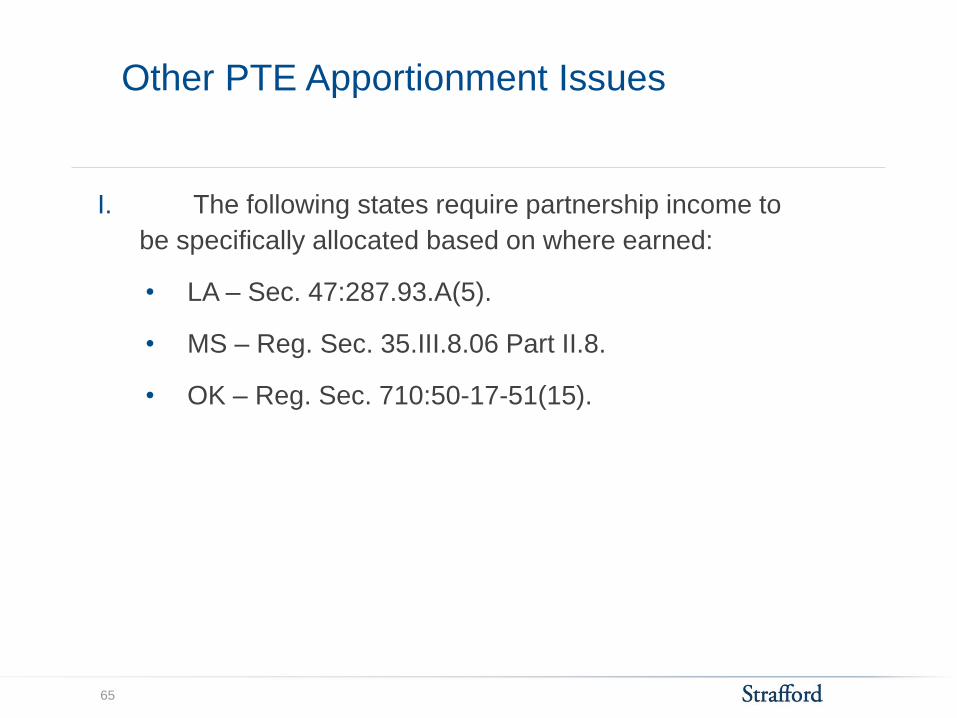

Other PTE Apportionment Issues

I. The following states require partnership income to

be specifically allocated based on where earned:

• LA – Sec. 47:287.93.A(5).

• MS – Reg. Sec. 35.III.8.06 Part II.8.

• OK – Reg. Sec. 710:50-17-51(15).

65

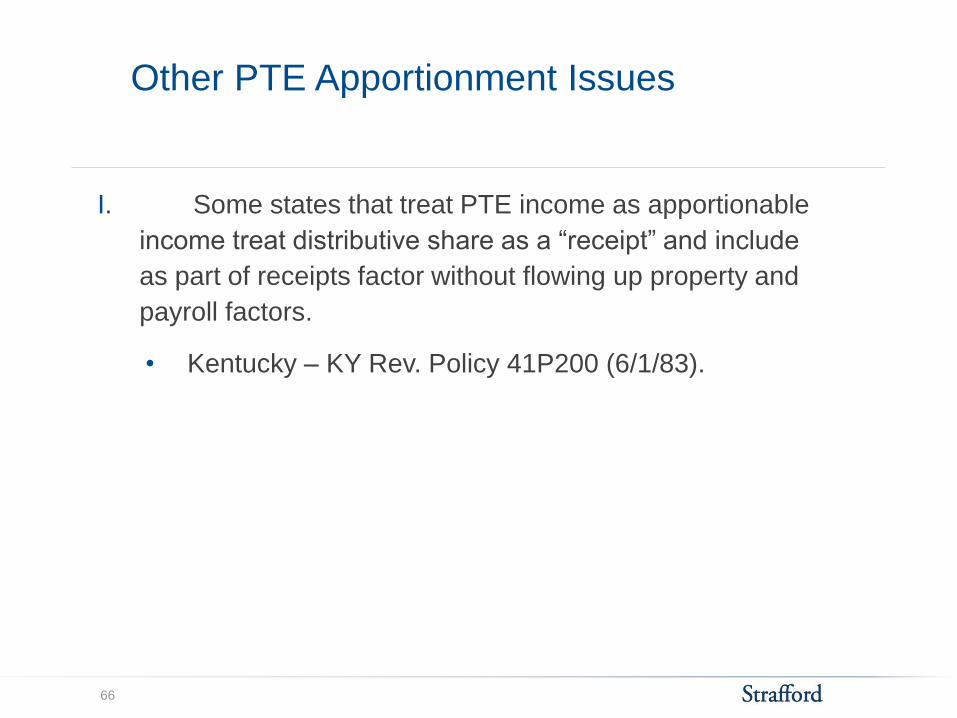

Other PTE Apportionment Issues

I. Some states that treat PTE income as apportionable

income treat distributive share as a “receipt” and include

as part of receipts factor without flowing up property and

payroll factors.

• Kentucky – KY Rev. Policy 41P200 (6/1/83).

66

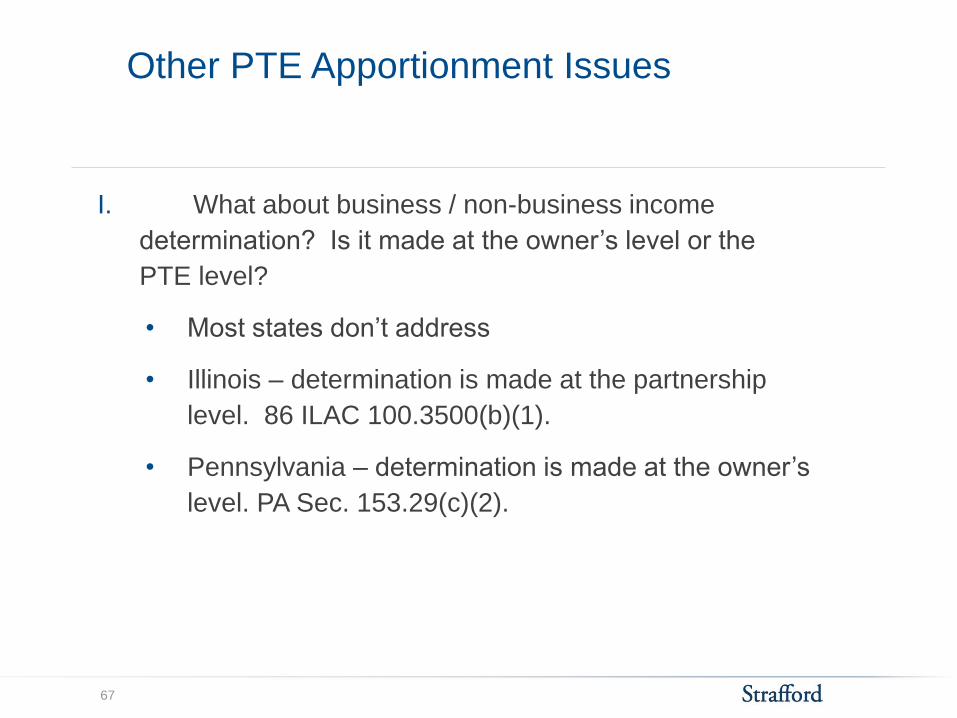

Other PTE Apportionment Issues

I. What about business / non-business income

determination? Is it made at the owner’s level or the

PTE level?

• Most states don’t address

• Illinois – determination is made at the partnership

level. 86 ILAC 100.3500(b)(1).

• Pennsylvania – determination is made at the owner’s

level. PA Sec. 153.29(c)(2).

67

Other PTE Apportionment Issues

I. When flowing-through the apportionment factors of

the PTE to the owners, should intercompany

transactions be eliminated?

• Transactions between the PTE and the owner?

• Transactions between commonly owned PTE’s?

68

Other PTE Apportionment Issues

• For Illinois purposes, transactions between PTE and its

owner are eliminated.

• IL DOR Ruling IT 08-0001-PLR (5/19/08).

• California provides for eliminations.

• CA Reg. Sec. 25137-1(f).

• Pennsylvania also eliminates intercompany transactions

• PA Reg. Sec. 153.29.

• Oregon provides for elimination between a corporate

member and LLC’s.

• OR Reg. Sec. 150-314.650(9)

69

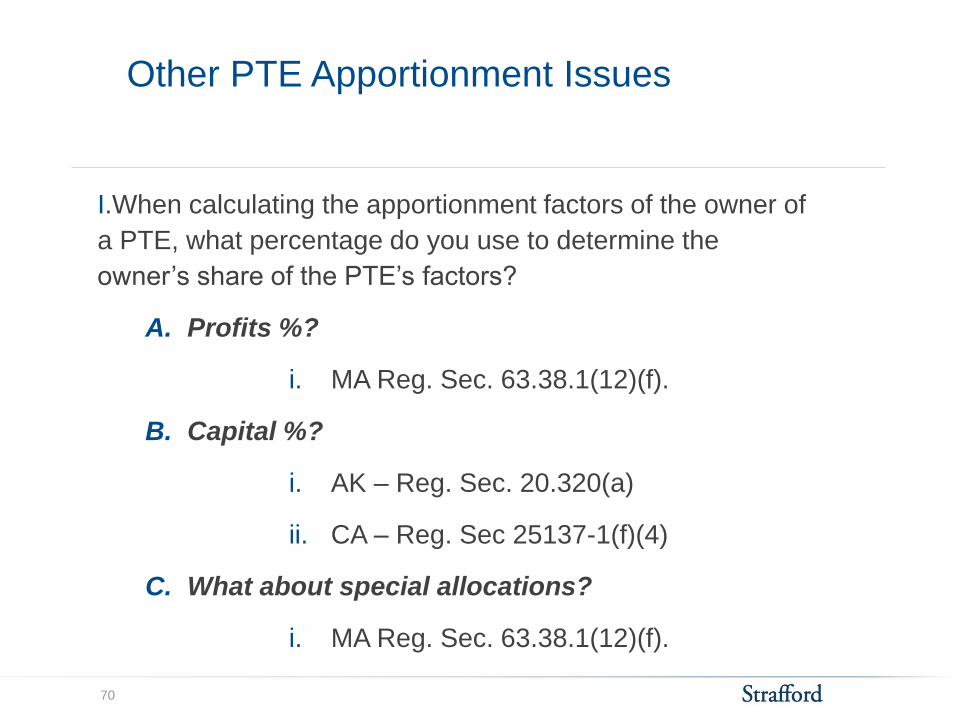

Other PTE Apportionment Issues

I.When calculating the apportionment factors of the owner of

a PTE, what percentage do you use to determine the

owner’s share of the PTE’s factors?

A. Profits %?

i. MA Reg. Sec. 63.38.1(12)(f).

B. Capital %?

i. AK – Reg. Sec. 20.320(a)

ii. CA – Reg. Sec 25137-1(f)(4)

C. What about special allocations?

i. MA Reg. Sec. 63.38.1(12)(f).

70

Slide Intentionally Left Blank

Related Documents