Topic: Times Series Econometrics By: Zaheer Khan Kamroon T aj To: Dr . M. Afzal

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 1/46

Topic:

Times Series Econometrics

By:

Zaheer KhanKamroon Taj

To:

Dr. M. Afzal

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 2/46

Time series is a sequence of data points, measured

typically at successive time spaced at uniform time

intervals.

Example of Time Series:

Daily stock prices, Exchange rate, CPI, GDP, etc.

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 3/46

Time series analysis is distinct from the other

data analysis problem in which there is no naturalobservation

A time series model will generally reflect the fact

that observation close together in time will be more

closely related then the observations further apart

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 4/46

Time Series analysis is divided into two main category.

Linear Analysis

Non Linear Analysis

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 5/46

Linear analysis three major model are mostly used.

1. AR (Auto-Regressive Integrated 1)2. MA (Moving Average Model)

3. ARMA (Auto-Regressive Moving Average)

4. ARIMA (Auto-Regressive Integrated Moving

Average)

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 6/46

In time series econometrics for Non-linear analysisfollowing model for used

1. ARCH2. GARCH

3. TARCH

4. EGARCH

5. FIGARCH

6. CGARCH

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 7/46

For the analysis of time sequence data in econometricsfollowing tests are used.

StationarityUnit Root

Correlogram

Co-integration

Causality

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 8/46

A time series is stationary if its mean and variance

do not vary systematically over time

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 9/46

Mean E(Yt) = µ

Variance var(Yt) = E(Yt- µ)² = ²

Covariance k = E[(Yt-µ)(Yt+k-µ)]

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 10/46

For econometrics analysis data must be stationary,

which should be check through graphical analysis.

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 11/46

A test of Stationarity which help to widely used for

the major purpose of time series econometrics

(stationarity of data)

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 12/46

Ho==1

Data is non-stationary

This hypothesis is going to be tested

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 13/46

Its known as the auto-correlation plot which is mostly

used to check the randomness of data

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 14/46

1. Shows that the data is random

2. Is the observed time series are auto-regressive

3. Is the time series are white-noise

4. Is an observation related to the adjacent observation

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 15/46

If two or more series are individually integrated

but some linear combination of them has a low

order of integration then the series are said to be

co-integrated

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 16/46

Is the relationship between an event (the cause)

and a second event (the effect) where the second

event is the consequences of the first event

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 17/46

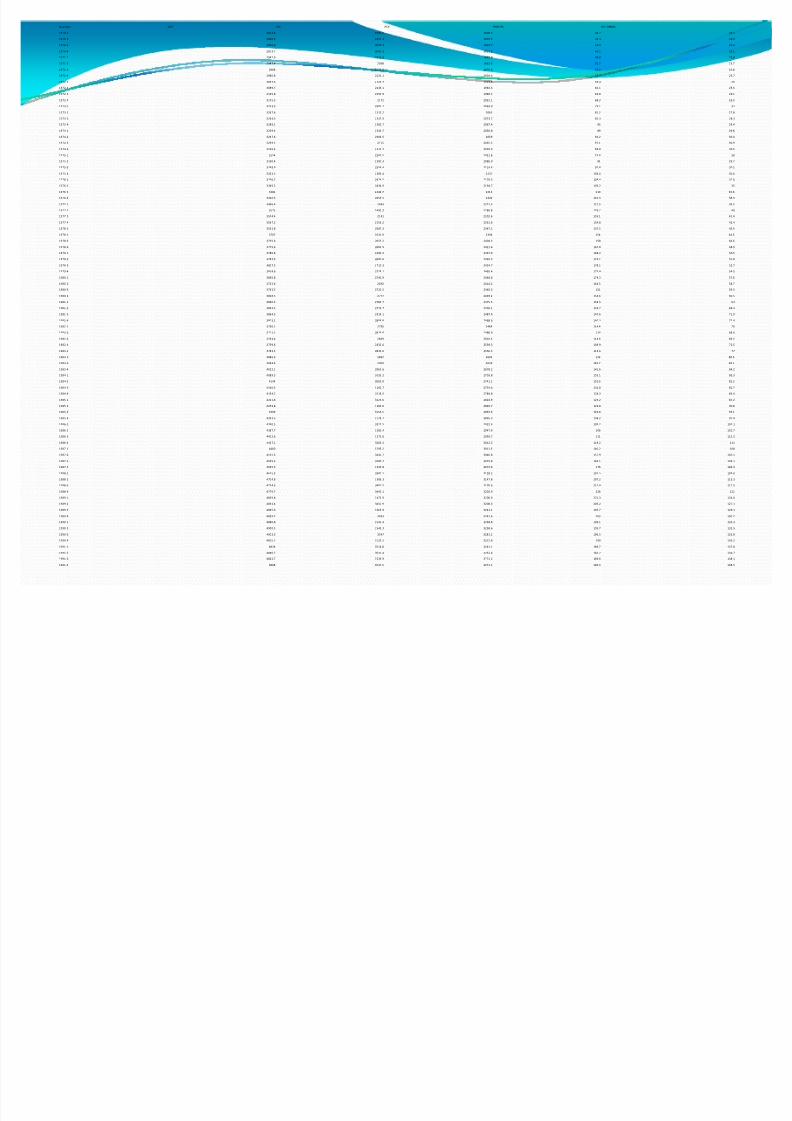

Quarters GDP PDI PCE PROFITS DIVIDENDS

1970-1 2872.8 1990.6 1800.5 44.7 24.5

1970-2 2860.3 2020.1 1807.5 44.4 23.9

1970-3 2896.6 2045.3 1824.7 44.9 23.3

1970-4 2873.7 2045.2 1821.2 42.1 23.1

1971-1 2942.9 2073.9 1849.9 48.8 23.8

1971-2 2947.4 2098 1863.5 50.7 23.7

1971-3 2966 2106.6 1876.9 54.2 23.8

1971-4 2980.8 2121.1 1904.6 55.7 23.7

1972-1 3037.3 2129.7 1929.3 59.4 25

1972-2 3089.7 2149.1 1963.3 60.1 25.5

1972-3 3125.8 2193.9 1989.1 62.8 26.1

1972-4 3175.5 2272 2032.1 68.3 26.5

1973-1 3253.3 2300.7 2063.9 79.1 27

1973-2 3267.6 2315.2 2062 81.2 27.8

1973-3 3264.3 2337.9 2073.7 81.3 28.3

1973-4 3289.1 2382.7 2067.4 85 29.4

1974-1 3259.4 2334.7 2050.8 89 29.8

1974-2 3267.6 2304.5 2059 91.2 30.4

1974-3 3239.1 2315 2065.5 97.1 30.9

1974-4 3226.4 2313.7 2039.9 86.8 30.5

1975-1 3154 2282.5 2051.8 75.8 30

1975-2 3190.4 2390.3 2086.9 81 29.7

1975-3 3249.9 2354.4 2114.4 97.8 30.1

1975-4 3292.5 2389.4 2137 103.4 30.6

1976-1 3356.7 2424.5 2179.3 108.4 32.6

1976-2 3369.2 2434.9 2194.7 109.2 35

1976-3 3381 2444.7 2213 110 36.6

1976-4 3416.3 2459.5 2242 110.3 38.3

1977-1 3466.4 2463 2271.3 121.5 39.2

1977-2 3525 2490.3 2280.8 129.7 40

1977-3 3574.4 2541 2302.6 135.1 41.4

1977-4 3567.2 2556.2 2331.6 134.8 42.4

1978-1 3591.8 2587.3 2347.1 137.5 43.5

1978-2 3707 2631.9 2394 154 44.5

1978-3 3735.6 2653.2 2404.5 158 46.6

1978-4 3779.6 2680.9 2421.6 167.8 48.9

1979-1 3780.8 2699.2 2437.9 168.2 50.5

1979-2 3784.3 2697.6 2435.4 174.1 51.8

1979-3 3807.5 2715.3 2454.7 178.1 52.7

1979-4 3814.6 2728.1 2465.4 173.4 54.5

1980-1 3830.8 2742.9 2464.6 174.3 57.6

1980-2 3732.6 2692 2414.2 144.5 58.7

1980-3 3733.5 2722.5 2440.3 151 59.3

1980-4 3808.5 2777 2469.2 154.6 60.5

1981-1 3860.5 2783.7 2475.5 159.5 64

1981-2 3844.4 2776.7 2476.1 143.7 68.4

1981-3 3864.5 2814.1 2487.4 147.6 71.9

1981-4 3803.1 2808.8 2468.6 140.3 72.4

1982-1 3756.1 2795 2484 114.4 70

1982-2 3771.1 2824.8 2488.9 114 68.4

1982-3 3754.4 2829 2502.5 114.6 69.2

1982-4 3759.6 2832.6 2539.3 109.9 72.5

1983-1 3783.5 2843.6 2556.5 113.6 77

1983-2 3886.5 2867 2604 133 80.5

1983-3 3944.4 2903 2639 145.7 83.1

1983-4 4012.1 2960.6 2678.2 141.6 84.2

1984-1 4089.5 3033.2 2703.8 155.1 83.3

1984-2 4144 3065.9 2741.1 152.6 82.2

1984-3 4166.4 3102.7 2754.6 141.8 81.7

1984-4 4194.2 3118.5 2784.8 136.3 83.4

1985-1 4221.8 3123.6 2824.9 125.2 87.2

1985-2 4254.8 3189.6 2849.7 124.8 90.8

1985-3 4309 3156.5 2893.6 129.8 94.1

1985-4 4333.5 3178.7 2895.3 134.2 97.4

1986-1 4390.5 3227.5 2922.4 109.2 105.1

1986-2 4387.7 3281.4 2947.9 106 110.7

1986-3 4412.6 3272.6 2993.7 111 112.3

1986-4 4427.1 3266.2 3012.5 119.2 111

1987-1 4460 3295.2 3011.5 140.2 108

1987-2 4515.3 3241.7 3046.8 157.9 105.5

1987-3 4559.3 3285.7 3075.8 169.1 105.1

1987-4 4625.5 3335.8 3074.6 176 106.3

1988-1 4655.3 3380.1 3128.2 195.5 109.6

1988-2 4704.8 3386.3 3147.8 207.2 113.3

1988-3 4734.5 3407.5 3170.6 213.4 117.5

1988-4 4779.7 3443.1 3202.9 226 121

1989-1 4809.8 3473.9 3200.9 221.3 124.6

1989-2 4832.4 3450.9 3208.6 206.2 127.1

1989-3 4845.6 3466.9 3241.1 195.7 129.1

1989-4 4859.7 3493 3241.6 203 130.7

1990-1 4880.8 3531.4 3258.8 199.1 132.3

1990-2 4900.3 3545.3 3258.6 193.7 132.5

1990-3 4903.3 3547 3281.2 196.3 133.8

1990-4 4855.1 3529.5 3251.8 199 136.2

1991-1 4824 3514.8 3241.1 189.7 137.8

1991-2 4840.7 3537.4 3252.4 182.7 136.7

1991-3 4862.7 3539.9 3271.2 189.6 138.1

1991-4 4868 3547.5 3271.1 190.3 138.5

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 18/46

This is the quarterly data of five major

macro-economic variable which is used for theapplication of time series econometrics

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 19/46

This have following steps to analysis the time series

econometrics1. Graphical analysis

2. Correlogram

3. Unit Root Test

4. Co-intergration Test

5. Causality Test

6. Chow Break Test

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 20/46

Dependent Variable: LNGDP

Method: Least Squares

Date: 12/03/10 Time: 03:12

Sample: 1970Q1 1991Q4

Included observations: 88

Variable Coefficient Std. Error t-Statistic Prob.

LNPCE 1.034618 0.115599 8.950079 0.0000

LNPDI 0.093431 0.097578 0.957501 0.3411

LNP

O ¡ 1.¢ 03905 0.167793 7.174936 0.0000

LNDVD 1.471¢ 57 0.6¢ 454 ¢ ¢ .355738 0.0¢ 08

C 719. ¢ 76¢ 99.79¢ ¢ 1 7.¢ 07739 0.0000

-squared 0.997318 Mean dependent var 3865.606

Adjusted

-squared 0.997189 S.D. dependent var 630.0349

S.E. of regression 33.40619 Akaike info criterion 9.910500

Sum squared resid 9 ¢ 6¢ 5.81 Schwarz criterion 10.051¢ 6

Log likelihood -431.06¢ 0 ¡ -statistic 7715.573

Dur £ in-Watson stat 0.478548 Pro£ ( ¡ -statistic) 0.000000

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 21/46

From the above result shows that only PDI is

insignificant while the other variables are significant.It also point out that the problem of hetroscedasticity

and auto-correlation occurred in the observed data

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 22/46

Dependent Variable: LNGDP

Method: Least Squares

Date: 12/06/10 Time: 03:0 ¤

Sample (adjusted): 1¥ ¤

0 ¦ 2 1¥ ¥

1¦ §

Included observations: 8 ¤ after adjustments

Convergence achieved after 10 iterations

Variable Coefficient Std. Error t-Statistic Prob.

LNPCE 0.817576 0.124656 6.558656 0.0000

LNPDI 0.301080 0.094193 3.196406 0.0020

LNPR ̈

F 1.387688 0.262312 5.290212 0.0000

LNDVD 1.406317 1.100136 1.278312 0.2048

C 666.7647 187.3353 3.559205 0.0006

AR(1) 0.789442 0.069469 11.36394 0.0000

R-squared 0.998912 Mean dependent var 3877.017

Adjusted R-squared 0.998845 S.D. dependent var 624.4732

S.E. of regression 21.22632 Akaike info criterion 9.014833

Sum squared resid 36495.09 Schwarz criterion 9.184895

Log likelihood -386.1452 F-statistic 14870.78

Durbin-©

atson stat 2.007510 Prob(F-statistic) 0.000000

.7

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 23/46

WhenWhite test apply along with AR1 this

will reduce the problem of cross productsbut still it shows the problem of

autocorrelation

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 24/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 25/46

To check the randomness of the data Q-statistics is apply which plot theautocorrelation

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 26/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 27/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 28/46

The graphicall analysis shows that the data is not stationary,

for this the Unit Root Test(ADF) is apply, on the integratedorder 1.

Stationarity of data is the necessary condition of the time

series analysis.

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 29/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 30/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 31/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 32/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 33/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 34/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 35/46

The unit root test shows that the data is stationary at the first

order integrationIn the observed data after applying the unit root test the data

become stationary

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 36/46

After the test apply there is the visual view of the stationarity

of data.

Which is obtained by plotting the residual of the observation

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 37/46

This is the graphical analysis of the residual which shows that

data is stationary

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 38/46

It shows that the variable have a long run relationship among

each other

n the observed data co-integration is apply for this purpose

we many test are used but Engle Granger test is apply to check

the relationship of the observed data.

ur Ho= No Co-integration in the data

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 39/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 40/46

Calculated values shows that at the level of 5% our Ho is

Rejected .

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 41/46

To check the casuality of the observed data a test of Granger

Casuality is used

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 42/46

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 43/46

For the structural stability of the observed data a test of chow

break is used in the above data

For this test there must be an a point of break which is

necessary for this 1982 is our break point for the above data

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 44/46

Our Ho is that there is no structural stability in the data is

going to be tested

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 45/46

While the result shows that the calculated F-statistics is grater

then the critical value of F which is 2.63.This should reject our Ho that there is no structural stability

8/8/2019 Advance Eco No Metrics Techniques & Forecasting

http://slidepdf.com/reader/full/advance-eco-no-metrics-techniques-forecasting 46/46

The maximum log like hood ratio shows that distribution withDOF (m-1)*(k+1) is rejected the null hypothesis, because ourcritical value 9.49 is less then the calculated value.

Ho is rejected which mean the results are statistically significant

and there is a structural stability in the data

Related Documents