Adaptive Firm Structure under Market Competition: Efficiency, Incentives, and Risk Control Tiangle Song and Susheng Wang 1 May 12, 2015 Abstract: This paper presents a theory on how firm structure responds to market competi- tiveness. Firms have often been observed to reallocate control rights, sometimes in response to market competition. We develop a theory on the dependence of firm structure on market competition using an incomplete contract approach. We show that a reallocation of control rights can be an effective way of adapting to changing market competitiveness. We find that when market competitiveness changes, depending on demand elasticity, firms may centralize or decentralize control rights to encourage work incentives or to control risk. We present a few case studies in support of this result. We also investigate the effect of changing demand elas- ticity and production cost on firm structure, as well as the effect of market competition on efficiency, incentives and risk control after taking into account the endogenous, competition- driven firm structure. Keywords: adaptive firm structure, market competition, incomplete contract, control rights, income rights, efficiency, incentives, risk control JEL classification: L22, L23 1 Address: Hong Kong University of Science and Technology. Email: [email protected] and [email protected]. Phone: (852) 2358-7600.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Adaptive Firm Structure under Market Competition:

Efficiency, Incentives, and Risk Control

Tiangle Song and Susheng Wang1

May 12, 2015

Abstract: This paper presents a theory on how firm structure responds to market competi-

tiveness. Firms have often been observed to reallocate control rights, sometimes in response to

market competition. We develop a theory on the dependence of firm structure on market

competition using an incomplete contract approach. We show that a reallocation of control

rights can be an effective way of adapting to changing market competitiveness. We find that

when market competitiveness changes, depending on demand elasticity, firms may centralize

or decentralize control rights to encourage work incentives or to control risk. We present a few

case studies in support of this result. We also investigate the effect of changing demand elas-

ticity and production cost on firm structure, as well as the effect of market competition on

efficiency, incentives and risk control after taking into account the endogenous, competition-

driven firm structure.

Keywords: adaptive firm structure, market competition, incomplete contract, control rights,

income rights, efficiency, incentives, risk control

JEL classification: L22, L23

1 Address: Hong Kong University of Science and Technology. Email: [email protected] and [email protected]. Phone:

(852) 2358-7600.

Page 2 of 30

1. Introduction

Companies often adjust their internal control structures in response to market competi-

tion. We present a theory of adaptive firm structure under market competition. In our model,

firms in the market compete in a Bertrand equilibrium; within each firm, with a principal-

agent setting, the firm allocates income and control rights between the principal and the agent.

As an example of control rights, we focus on the risk control right. When the principal controls

the right, output risk can be effectively reduced/mitigated; when the agent controls the right,

work incentives can be improved. We find that, if demand elasticity is low (high), firms tend to

decentralize (centralize) control rights in response to increased market competition. To our

knowledge, we are the first to present a theory of adaptive firm structure under market compe-

tition using an incomplete contract approach.

The incomplete contract approach was proposed by Grossman & Hart (1986), Hart (1988)

and Hart & Moore (1990). Based on Coase’s (1960) idea of resolving conflicts of interest

through an organizational approach, the incomplete contract approach allows control rights to

play a role in business relationships. This approach treats control rights as mechanisms for

dealing with informational and incentive problems. We adopt this approach to establish a

theory of adaptive firm structure under market competition.

In the literature, income rights are the main mechanism through which companies pro-

vide incentives at work. In our model, both income and control rights provide incentives. A

reallocation of control rights involves moving some control rights from a higher level of a

firm’s management hierarchy to a lower level or vice versa, while the allocation of income

rights involves a contractual agreement on revenue sharing. In this paper, our focus is on the

allocation of control rights and its dependence on market competition.

The effect of markets on firm structure has been an important topic in the literature. As

an extension of the contingency theory, the structural contingency theory proposed by Law-

rence & Lorsch (1969) looks closely into the relationship between firm structure and the envi-

ronment and argues that the firm should constantly improve its relationship with the envi-

ronment by adjusting its control structure. Lenz (1981), Bartunek (1984) and Huff & Schwenk

(1990) describe how an environmental change can lead to an internal organizational change.

Lenz (1981) points out that firm structure affects performance. This has been confirmed by

ample evidence and is consistent with our theoretical conclusion. Defining an innovation as an

organizational change in response to an environmental change, Damanpour & Evan (1984)

find that active organizational restructuring tends to encourage innovations and in turn im-

prove organizational performance. Our approach is distinctly different from traditional ap-

proaches on corporate adaptation: we emphasize that firm structure responds to changes in

Page 3 of 30

market competitiveness, whereas traditional approaches typically either ignore firm structure

or discuss firm structure and corporate adaptation separately.

On the allocation of control rights, Palmon & Wald (2002) investigate the effect of switch-

ing from one control structure to another. They find that small firms benefit more from the

clarity in decision-making under a single executive, while large firms benefit more from the

checks and balances under two executives. Inderst & Müller (2003) compare two organiza-

tional structures: under a centralized structure, the headquarters raise funds on behalf of

multiple projects; under a decentralized structure, each project raises funds on its own from

the capital market. They find that centralization (decentralization) is better for projects with a

low (high) expected return. Façanha & Resende (2006) find that incentive mechanisms are

important and point in the direction of decentralization in Brazilian industries. Using a gen-

eral equilibrium approach, Marin & Verdier (2008) show that firms will decentralize when

competition is moderate. In a model in which commitment to a narrow business strategy is

valuable, Ferreira & Kittsteiner (2011) show that a monopolist may not be able to make such

commitment. However, competition can make commitment credible, leading to organizational

change and greater operating efficiency. Chen & Wang (2012) investigate the firm’s internal

reorganization when facing environmental changes. Alonso et al. (2014) show that if incentive

conflicts are negligible and lower-level managers have superior information, centralization is

better for adapting local information. In an empirical study, Aghion et al. (2014) find that

decentralization is particularly beneficial to firm performance in bad times. Our study indi-

cates that, taking into account the effect on risk control and incentive stimulation, whether

firms should choose centralization or decentralization depends on marginal cost, demand

elasticity and market competition.

In our model, firms compete in the market in a Bertrand equilibrium. Each firm is defined

by a principal-agent relationship, in which the principal hires the agent through a contract and

the agent provides output-enhancing effort. Each firm faces a risk of failure. This risk can be

controlled through risk control effort made either by the principal (centralization) or by the

agent (decentralization). We have two types of results. Regarding adaptive firm structure, we

find that (1) if demand elasticity is high (or low), increased competition will induce firms to

centralize (or decentralize); (2) if the marginal cost of production is sufficiently large, in-

creased (or decreased) demand elasticity will induce firms to centralize (or decentralize) and

receive lower payoffs; and (3) if demand elasticity is low (or high), an increased marginal cost

of production will induce firms to decentralize (or centralize) and receive higher (or lower)

payoffs. Regarding the effect of competition on efficiency, incentives and risk control, we find

that if demand elasticity is low (or high), increased market competition will lead to larger (or

smaller) output-enhancing effort, risk control effort, and payoffs.

Our results contribute to prior literature on (1) the adaptive firm structure and the effect

of competition, demand elasticity and production cost on firm structure; (2) the effect of

Page 4 of 30

competition on efficiency; (3) the effect of competition on incentives; and (4) the effect of

competition on risk control. Our results are based on the endogenous firm structure. In our

theory, increased competition induces a change of firm structure, which in turn affects firms’

efficiency, incentives and risk control. Such effects are discussed under a fixed firm structure

in most studies, such as Scharfstein (1988), Raith (2003), Bolt & Tieman (2004), and Boyd &

Nicoló (2005).

This paper is organized as follows. Section 2 presents the model. Section 3 presents a par-

ametric solution. Section 4 analyzes the solution and derives our main results. Section 5 ap-

plies our theory to several real-world cases of adaptive firm structure under market competi-

tion. Section 6 concludes the paper with a few remarks. Proofs and derivations are given in the

Appendix.

2. The Model

There are firms in an industry, competing in a Bertrand equilibrium. We first define the

internal structure of a representative firm, and then define the competitive market.

2.1. The Representative Firm

Consider the internal structure of a representative firm, firm . The firm is defined by a

principal-agent relationship, in which the principal (she) hires an agent (he) to work for the

firm. The principal offers a take-or-leave-it contract to the agent. The contract specifies not

only a revenue-sharing scheme but also an allocation of control rights. Two unverifiable varia-

bles are important in this model: the agent’s output effort and the firm’s risk control effort.

After accepting the contract, the agent decides on a certain level of output-enhancing effort.

But the right over risk control can be given either to the principal or to the agent. The question

is: when market competition intensifies or eases, should the firm reallocate the control right

from the principal to the agent or vice versa?

Specifically, we use variable to represent the agent’s effort made to enhance out-

put and variable to represent the controlling party’s effort made to control risk. As-

sume that both effort variables are unverifiable. The control of risk is represented by the right

to determine The question becomes: when market competiveness changes, how will the

firm reallocate the control over ? Note that a reallocation of control rights will typically be

accompanied by a corresponding adjustment of the revenue-sharing scheme.

Let and be the utility functions of the principal and agent, respectively. Assume

that Let the agent’s cost of supplying be the agent’s cost of supplying

be and the principal’s cost of supplying be All the cost functions are increasing

and convex.

Page 5 of 30

Let be firm ’s price, , and The market de-

mand for firm i’s output is dependent on its investment and prices :

. The project may fail. If the project fails, there is no output; if the project suc-

ceeds, the demand can be satisfied. The success probability of the project is , depending

on the risk control effort . Hence, firm ’s sales is random ex ante with two possible states:

where and are concave and strictly increasing functions in and , respectively.

The production cost is , where the marginal cost of production is a fixed constant. We

have two kinds of costs: is verifiable cost, and is nonverifiable cost. The revenue is

Assume that the revenue is verifiable. Then, there can be a revenue-sharing scheme

between the principal and the agent, where is the payment to the agent if revenue turns

out to be . An admissible revenue-sharing scheme is a piecewise-smooth function

where the condition is the so-called limited liability condition for the agent. Denote

the set of admissible revenue-sharing schemes by i.e.,

In particular, a linear revenue-sharing scheme has the form where and

are two constants, and the share of revenue is fixed. In our solution, we find a linear

sharing scheme to be optimal. Since we do not restrict our admissible sharing schemes to

linear ones only, our linear sharing scheme is better than any non-linear sharing scheme.

We will solve the problem backward in two steps: (1) given control and income rights,

solve for and ; (2) determine the allocations of income and control rights. The first step

implies the incentive compatibility (IC) conditions; i.e., the IC conditions determine and in

the first step, conditional on the allocations of income and control rights. The second step is

the principal’s problem, which is to allocate income and control rights properly in order to

maximize her own expected utility, taking into account the IC conditions. Given that a reve-

nue-sharing scheme is dependent on the allocation of control rights, how will the allocation

change when market competitiveness changes?

We impose two structural assumptions in our model. First, we assume that the principal

is more risk averse than the agent. This assumption is justifiable in practice. In many organi-

zations, the burden of risks tends to fall on the shoulders of top managers. They make busi-

ness decisions and hence take responsibilities for the outcomes. An empirical study by Saun-

ders et al. (1990) confirms this by showing that a “manager-controlled” bank takes on less risk

than a “stockholder-controlled” bank.

Page 6 of 30

is the relative cost when a job is performed by the principal rather than the

agent. Since the principal is distant from the client (in terms of hierarchical layers), she does

the same job as the agent at a higher cost. Hence, our second assumption is that

This higher cost can be due to the loss of information along the hierarchy, so that a higher cost

must be paid to obtain the same amount of information at a higher level of management.

A contract in our model consists of two parts: income rights and control rights. The in-

come rights of a manager are stipulated in a revenue-sharing scheme, which follows the

standard agency theory developed by Mirrlees (1974, 1975, 1976) and Holmström (1979). The

control rights define the controlling party’s right to decide the risk control variable . Our

contract is incomplete since the income rights do not include all the rights, unlike in the tradi-

tional principal-agent approach.

2.2. The Competitive Market

There are firms in the industry competing in a Bertrand equilibrium. The firms produce

similar products with prices where is the price for firm i’s product. The substi-

tutability between and represents how closely related the firms’ products are. For trac-

tability, we assume that the firms are symmetric and define the competitiveness by the cross

elasticity

⋯Normally, this depends on and . However, for tractability, in our choice of the parametric

demand functions later, we will make sure that this is independent of and

For example, in an extreme case, an industry has two identical firms producing the same

product (perfectly substitutable). Let be the overall market demand for the prod-

uct and let be the market demand for firm . Then,

, ,The substitutability is

That is, the market is perfectly competitive if the firms are producing exactly the same product.

Page 7 of 30

2.3. Organizational Structures of Firms

We now present a typical firm (firm i)’s problem conditional on its internal structure. For

convenience we will suppress the subscript .

The Decentralized Structure

Consider first a lower control structure in which the agent controls the risk variable

That is, the agent chooses and , while the principal designs . Here subscript repre-

sents a lower control structure. With a limited liability condition of the form an

optimal revenue-sharing scheme implies Then, the agent’s payoff function is

(1)

The principal’s payoff function is

(2)

Upon accepting the contract, the agent considers the following problem to determine his

choice of :

, ∈ℝ (3)

which implies two IC conditions:

Hence, the principal’s problem is

, ∈ℝ , (⋅)∈(4)

where the last condition is the individual rationality (IR) condition. We include the second-

order conditions (SOCs) of (3) to ensure the validity of the first-order approach.2 The proof of

the following proposition is in the Appendix.

2 For discussions about the first-order approach, see Holmström (1979), Rogerson (1985) and Jewitt (1988).

Page 8 of 30

Proposition 1 (Decentralized Structure). Problem (4) can be solved in two steps. First, the

principal chooses ∗ ∗ from the following problem:

, ∈ℝ

(5)

Second, given ∗ ∗ the principal designs a linear revenue-sharing scheme to satisfy the

two IC conditions and the SOCs.

The Centralized Structure

Consider now a higher control structure in which the principal controls the risk variable

That is, the principal designs and chooses , while the agent chooses . Then, the

agent’s payoff is

The principal’s payoff is

In this case, the principal does not need to offer the agent an incentive to choose a proper

instead, she needs an incentive herself to commit to a proper Upon contract acceptance,

assume that the two parties choose and in a Nash equilibrium. The agent considers the

following problem to determine his choice of :

∈ℝ (6)

The principal considers the following problem to determine her choice of :

∈ℝ (7)

Problems (6) and (7) imply the following two IC conditions:

These two conditions determine a Nash equilibrium of efforts Hence, the principal’s

problem is

Page 9 of 30

, ∈ℝ , (⋅)∈(8)

where the last condition is the IR condition. Again, we include the SOCs of (6) and (7) to en-

sure the validity of the first-order approach. The proof of the following proposition is in the

Appendix.

Proposition 2 (Centralized Structure). Problem (8) can be solved in two steps. First, the

principal chooses ∗ ∗ from the following problem:

,

(9)

Second, given ∗ ∗ the principal designs a linear revenue-sharing scheme to satisfy

the two IC conditions and the SOCs.

2.4. Firm Structure under Market Competition

There are possible combinations of firm structures in this economy. However, since the

firms are similar, when one firm responds to market competition by choosing a lower or high-

er control structure, all other firms will follow suit. Hence, there are actually only two possible

combinations of firm structures in this economy: either all firms adopt a lower control struc-

ture, or all firms adopt a higher control structure.

If all firms adopt a lower control structure, firm considers the following problem:

Then, the Bertrand equilibrium ∗ ∗ is determined by

The equilibrium value is ∗ ∗ ∗ Similarly, when all firms adopt a higher control

structure, the Bertrand equilibrium ∗ ∗ is determined by

Page 10 of 30

and the equilibrium value is ∗ The firms will adopt the optimal control structure by compar-

ing ∗ with ∗. We are interested to see how firm structure changes when market competitive-

ness changes.

3. The Solution

To analyze the solution, we need to define a set of parametric functions so that we can

represent a few important factors by parameters and find a closed-form solution. First, for

positive constants and , define the demand by

Then, is the demand elasticity of all firms, and is the cross elasticity between any two firms.

Suppose all firms have a fixed marginal cost of production , i.e., the cost of production is

for firm Then, the revenue function of firm is

Further, let

where

and and are constants.

We call the competitiveness of the market. Between any two firms and when

firm lowers its price demand for its own product will rise but demand for firm ’s product

will drop. is the percentage drop in when is lowered by 1%. Symmetrically, is the

percentage drop in when is lowered by 1%. The market is more competitive if is larger.

We call the revenue multiplier, since revenue . Here, effort is heavily influ-

enced by the firm’s internal structure, while the revenue multiplier is heavily influenced by

market conditions. The firm’s internal structure depends on market conditions via the influ-

ence of market conditions on the multiplier.

is the relative cost when a job is performed by the principal rather than the

agent. We assume This higher cost can be due to the loss of information along the hier-

archy as explained before. The principal’s risk attitude is represented by the constant relative

risk aversion , where we restrict to avoid a negative utility value. Productivity of effort

is represented by Finally, by the SOCs for problems (5) and (9), we require that

Page 11 of 30

that is, the SOCs are satisfied if the cost function is sufficiently convex. We will explain later

that we also need . Finally, in the solution, we need to control parameter values so that ∗ since we need probability ∗

Given the parametric functions in (12), we can solve problems (5) and (9) to obtain

and for the representative firm. By market equilibrium conditions in (10)

and (11), we can further obtain ∗ and ∗.

3.1. Decentralization Solution

Assuming a lower control structure, the following proposition presents a closed-form so-

lution given the parametric functions in (12).

Proposition 3 (Decentralization). When the firms have a lower control structure, the solu-

tion for firm is

( )

The income rights are defined by a linear revenue-sharing scheme

where is a constant.

The share of revenue increases when the agent’s productivity decreases or when the

principal’s risk aversion increases. The explanation is that if the agent is more productive,

there is less need to offer incentives through the sharing scheme; if the principal is more risk

averse, she is more willing to offer incentives to the agent in order to reduce output uncertain-

ty.

Page 12 of 30

3.2. Centralization Solution

Assuming a higher control structure, the following proposition presents a closed-form so-

lution given the parametric functions in (12).

Proposition 4 (Centralization). When the firms have a higher control structure, the solution

for firm is

The income rights are defined by a linear revenue-sharing scheme

where is a constant.

It is interesting to see that the agent takes all the residual revenue after making a fixed

payment to the principal. This implies that the agent bears all the risk. Since the agent is risk

neutral and the principal is risk averse, the principal has the tendency to let the agent to bear

all the risk. Besides, the agent’s incentive is negatively affected by the fact that he has less

control right. Hence, the principal uses risk to induce the agent to work hard. That is, risk is

used as an incentive mechanism here.

In each case, we have an optimal linear revenue-sharing scheme, which consists of a fixed

wage plus a bonus component. This is consistent with practice, where labor contracts general-

ly contain linear payment schemes.

Comparing the two revenue-sharing schemes in Propositions 3 and 4, we can see that the

allocation of control rights and revenue-sharing schemes are dependent on each other. The

explanation is that the principal has more control rights under centralization and thus is less

dependent on the revenue-sharing scheme, so it is possible to have a very simple scheme; but

when the principal has fewer control rights under decentralization, the revenue-sharing

scheme needs to be fine-tuned to offer incentives.

3.3. Market Equilibrium

We have derived a firm’s optimal solution under a given control structure. But the firm

faces competition in the market, which may affect its control structure. We now derive the

equilibrium of firms in the market.

Page 13 of 30

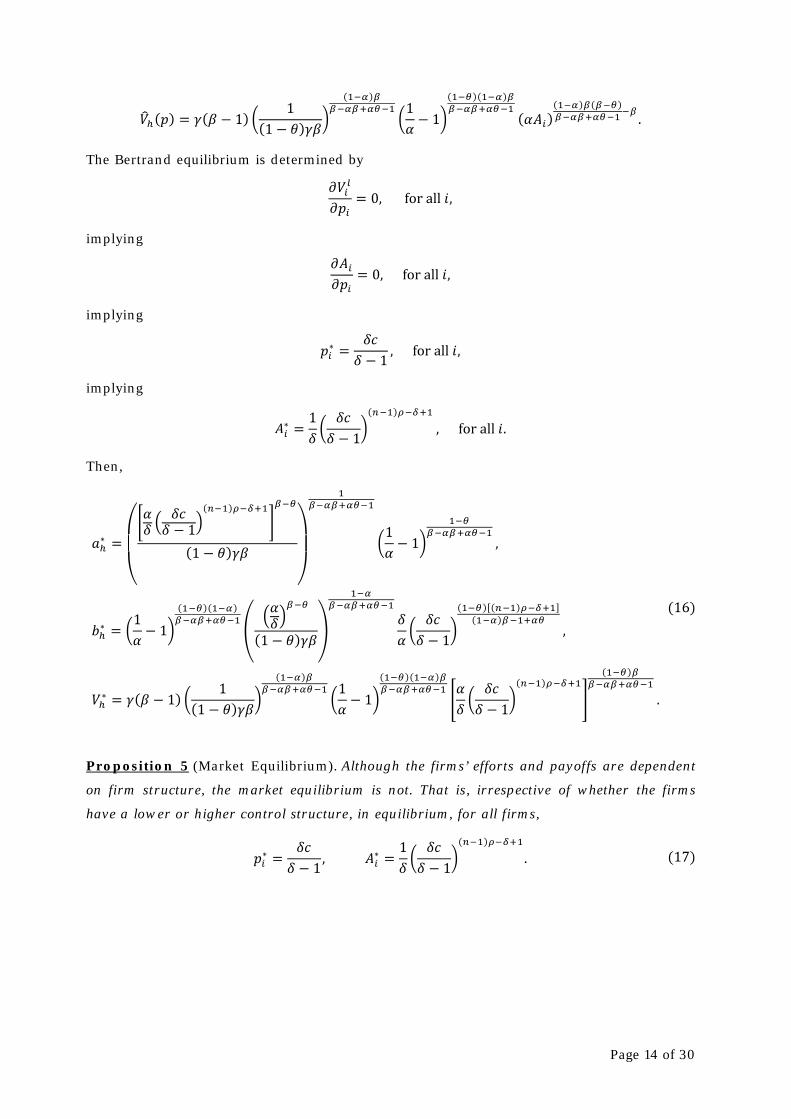

A Lower Control Structure

If control resides at a lower level, by Proposition 3 the payoff function for a typical firm,

firm is

( ) ( )( ) ( )( )( )Then, the Bertrand equilibrium is determined by

implying

By the definition of in (13), we find the Bertrand equilibrium prices:

∗We need to ensure ∗ . Then,

∗ ( )implying

∗ ( ) ( )

∗ ( ) ( )∗ ( )( ) ( )( )( )

( ) ( )The equilibrium prices are not dependent on competitiveness, but the revenue is. As market

competitiveness changes, the revenue will change, which will in turn affect incentives and thus

the control structure.

A Higher Control Structure

If control resides at a higher level, by Proposition 4 the payoff function for a typical firm,

firm is

Page 14 of 30

( ) ( )( ) ( ) ( )The Bertrand equilibrium is determined by

implying

implying

∗implying

∗ ( )Then,

∗( )

∗ ( )( ) ( ) ( )( )

∗ ( ) ( )( ) ( ) ( )

Proposition 5 (Market Equilibrium). Although the firms’ efforts and payoffs are dependent

on firm structure, the market equilibrium is not. That is, irrespective of whether the firms

have a lower or higher control structure, in equilibrium, for all firms,

∗ ∗ ( )

Page 15 of 30

4. Analysis

We have derived the market equilibrium of firms for each given firm structure. The

firms’ optimal structure is determined by the comparison of ∗ with ∗. We now analyze how

this firm structure reacts to market competition and present out main results.

To analyze the effect of competition on payoffs, define the effect of a change in on pay-

offs by elasticities

∗ ∗ ∗ ∗If , then for a 1% increase in , the percentage increase in ∗ will be larger than that in ∗. If so, when increases, the firms will have a tendency to choose a lower control structure,

i.e., to decentralize. Since the agent has no surplus (as shown in the proofs of Propositions 3

and 4), the payoff in our model measures firm efficiency.

Proposition 6 (Effect of Competition on Firm Structure). Suppose

(a) If , we have . That is, if demand is moderately elastic, firms tend to decen-

tralize (or centralize) when the market becomes more (or less) competitive.

(b) If , we have . That is, if demand is highly elastic, firms tend to centralize

(or decentralize) when the market becomes more (or less) competitive.

Proposition 6 suggests that if demand is moderately elastic, stronger competition tends to

induce the firms to decentralize. Competition improves overall efficiency. When demand is

moderately elastic, consumers will react moderately to price changes so that the firms can

manage to gain a bigger share from improved efficiency. This gain is reflected by a larger

revenue multiplier . With a larger multiplier, since the return on investment in

will be higher so that the firms have the tendency to sacrifice security for work incentives. We

know that when the agent has more control rights, he has better incentives to offer output-

enhancing effort . Hence, the firms tend to decentralize so that the agent would have better

incentives to provide output-enhancing effort.

On the other hand, when demand is highly elastic, consumers will overreact to price

changes so that the firms cannot manage to gain a bigger share from improved efficiency. This

is reflected by a smaller revenue multiplier . With a smaller multiplier, since the

return on investment in will be lower so that the firms have the tendency to sacrifice work

incentives for security. They achieve this by centralizing so that the principal will take control

of the risk variable . Since the principal is risk averse, she is likely to make an effort to con-

trol risk.

Page 16 of 30

Empirical evidence on the effect of competition on firm structure is mixed. This is ex-

pected based on our theory since the effect is conditional on demand elasticity.

Proposition 7 (Effect of Competition on Efficiency). Suppose

(a) If , competition has a positive effect on payoffs.

(b) If , competition has a negative effect on payoffs.

Proposition 7 suggests that if demand is moderately elastic, competition is good for the

firms as it raises their payoffs. In this case, the firms can manage to gain a bigger share from

improved efficiency, which is reflected by a larger revenue multiplier . As Proposition 6

suggests, the firms tend to decentralize so that the agent has better incentives to provide out-

put-enhancing effort . Hence, the firms’ payoffs are larger. On the other hand, if demand is

highly elastic, competition is bad for the firms as it reduces their payoffs. In this case, the

firms cannot manage to gain a bigger share from improved efficiency, which is reflected by a

smaller revenue multiplier . As Proposition 6 suggests, the firms tend to centralize, which

adversely affects the agent’s incentives. Hence, the firms’ payoffs are lower.

Distinct from prior literature, our results are conditional on the endogenous firm struc-

ture. If demand is moderately elastic, increased competition leads to decentralization as indi-

cated by Proposition 6(a), which in turn implies better firm performance. If demand is highly

elastic, increased competition leads to centralization as indicated by Proposition 6(b), which

in turn implies worse firm performance.

Proposition 7 addresses the hot issue of whether market competition improves firm effi-

ciency. The answer is yes according to many studies including Alchian (1950), Stigler (1958),

Hart (1983), Nickell (1996), Schmidt (1997) and Aghion et al. (1999). In particular, Aghion et

al. (2014) find a positive correlation between decentralization and firm performance, especial-

ly in times of crisis. Yet, market competition has also been shown to reduce firm efficiency by

many studies, including Scharfstein (1988), Caves & Barton (1990), Caves (1992), Hermalin

(1992) and Raith (2003). Our results reconcile these two opposite results in the literature by

suggesting that the effect of competition on efficiency is dependent on demand elasticity. As

shown in Proposition 6, demand elasticity plays a role through the endogenous, competition-

dependent firm structure.

Proposition 8 (Effect of Competition on Incentives and Risk Control). Suppose

(a) If , more competition induces more effort in enhancing output and in controlling

risk.

(b) If , more competition induces less effort in enhancing output and in controlling

risk.

Page 17 of 30

When demand is moderately elastic, as Proposition 6 indicates, the firms will decentralize.

An agent who has more control rights will have more incentives to make an effort. On the

other hand, when demand is highly elastic, as Proposition 6 indicates, the firms will centralize.

An agent who has less control rights will have less incentives to make an effort.

Proposition 8(a) supports the popular belief held by Adam Smith, John Hicks and others

that market competition has a positive effect on managerial incentives. Empirical evidence in

the literature, however, offers weak support for this view (see Leibenstein (1966), Nickell

(1996) and Schmidt (1997)). In particular, Nickell et al. (1997) show that more competition

leads to higher productivity growth. Fabrizio et al. (2010) find that competition resulting from

U.S. utility deregulation in 1990s induced productivity growth. In contrast, Scharfstein (1988)

argues that competition may exacerbate incentive problems. Our result reconcile both findings

as we show that competition may mitigate or exacerbate incentive problems depending on

demand elasticity. Our work complements these studies by taking into account the endoge-

nous firm structure.

A second issue is firms’ investment in risk control under competition. Intuitively, firms

may take a risky strategy in an intensely competitive market in order to survive. A well-known

example is the banking sector. In order to survive under intense competition, banks may

choose to invest in high-yield but high-risk projects. A large body of literature has shown that

increased competition induces banks to build riskier portfolios. Bolt & Tieman (2004) show

that increased competition in the banking sector leads to riskier bank behavior. The fully

fledged banking liberalization in the 1980s in many countries caused a notable rise in banking

failures. Boyd & Nicoló (2005) point out that although increased competition may drive banks

to build riskier portfolios, it may improve incentives to control risk. Our Proposition 8(a)

supports this argument, but we further contend that this improved incentive in risk control is

due to decentralization. With the endogenous firm structure, if demand is moderately elastic,

increased competition will induce decentralization, which will in turn induce more effort on

controlling risk.

Proposition 9 (Effect of Demand Elasticity on Firm Structure).

(a) If , when demand elasticity increases (or decreases), firms tend to centralize (or

decentralize) and receive smaller payoffs.

(b) If , there exists such that

1) for , when demand elasticity increases (or decreases), firms tend to centralize

(or decentralize) and receive smaller payoffs.

2) for , when demand elasticity increases (or decreases), firms tend to decen-

tralize (or centralize) and receive larger payoffs.

Page 18 of 30

(c) The cut-off value of demand elasticity is increasing in both the marginal cost and the

market competitiveness .

Proposition 9 suggests that the effect of demand elasticity on firm structure is dependent

on production cost. If the marginal cost of production is large, demand elasticity will be the

dominant factor in determining firm structure. When consumers become more sensitive to

price changes, if the marginal cost of production is large, the firms will emphasize risk control

over incentive stimulation, implying a tendency for centralization.

If the marginal cost of production is small, production cost is no longer a major factor. As

demand elasticity increases, consumers will become more sensitive to price changes. With less

room for raising prices, provided that the demand elasticity remains moderate, the firms tend

to emphasize risk control over incentive motivation, which will induce the firms to centralize.

On the other hand, if demand elasticity is large, benefit from competition is overwhelming.

Hence, when demand elasticity increases, the firms have a tendency to encourage output by

decentralization.

Proposition 10 (Effect of Production Cost on Firm Structure).

(a) If , when the marginal cost of production is larger (or smaller), firms

tend to decentralize (or centralize) and receive larger (or smaller) payoffs.

(b) If , when the marginal cost of production is larger (or smaller), firms

tend to centralize (or decentralize) and receive smaller (or larger) payoffs.

When demand elasticity is small, as pointed out in Proposition 7, competition has a posi-

tive effect on payoffs. An increase in the marginal cost has a negative effect on production. To

encourage production, the firms will decentralize in an attempt to boost incentives. On the

other hand, when demand elasticity is large, competition has a negative effect on payoffs as

pointed out in Proposition 7. An increase in the marginal cost discourages investment in pro-

duction. With less need to encourage production, the firms tends to centralize in an attempt to

control risk.

There is empirical evidence in support of Proposition 10. When the Sarbanes Oxley Act

(SOX) was passed, it significantly reduced production and administrative costs. Chhaochharia

et al. (2012) find that, after SOX was passed, firms in concentrated industries improved in

operational efficiency to a greater extent than did firms in non-concentrated industries. Our

explanation for this finding is that in a concentrated industry, demand elasticity tends to be

high because the price is likely to be high, as argued by Becker (1971) and supported with

empirical evidence by Pagoulatos & Sorensen (1986). If the demand curve is roughly linear,

demand elasticity is high when the price is high. With high demand elasticity, Proposition 10(b)

Page 19 of 30

confirms Chhaochharia et al.’s (2012) finding of improved efficiency when the marginal cost of

production decreases.

Our results in Propositions 6-10 remain true if we measure competitiveness by the num-

ber of firms instead of the cross elasticity .

5. Applications

In this section, we present a few case studies. In practice, companies often adjust their

control structures in response to market competition. They tend to centralize amid intense

market competition, but decentralize when their businesses are expanding. Our theory is

consistent with this phenomenon.

Microsoft Corporation

Microsoft started to face serious competition in 2005. In September 2005, Microsoft cen-

tralized its control structure by reorganizing itself into three newly created divisions. In July

2013, under the slogan of “One Microsoft”, Microsoft further centralized its technology deci-

sions and collapsed eight divisions into four. This centralization bundled functional responsi-

bilities of all products and services into a single organizational division.

Acer Inc.

In 1991, as an expanding company, Acer decentralized many decision-making rights.

However, by the end of 1998, with worsening performance, Acer reversed its decentralization

trend and centralized its dispersed product management, manufacturing, customer services

and brand management functions. In December 2000, Acer further centralized its control

structure by streamlining its five business units into four.

Sony Corporation

Sony began facing fierce competition in 2005, especially from Samsung and Apple. In

September 2005, Sony centralized its control structure by eliminating some product lines. In

March 2012, under the slogan of “One Sony”, Sony carried out another major centralization by

reallocating the decision rights of its top executives and streamlining its decision-making

process.

Chinese Banks

The Chinese banking market is dominated by a few large state-owned banks (SOBs). As

required by the World Trade Organization, the Chinese banking market completely opened up

Page 20 of 30

to foreign competition by the end of 2006. The SOBs began to lose market share substantially

in 2000. After two to three years of a persistent decline in market share, the SOBs centralized

their decision-making rights in 2003 and 2004 by moving the right of credit extension from

municipal branches to provincial branches or even the headquarters.

6. Concluding Remarks

In this paper, we have presented a theory on how firm structure depends on market com-

petition. Our main conclusion is that when market competitiveness changes, depending on

demand elasticity, firms may centralize or decentralize control rights to encourage work incen-

tives or to control risk. This phenomenon is widely observed in practice, as our case studies

have illustrated.

We have also investigated the effect of demand elasticity and production cost on firm

structure. In addition, we have examined the effect of market competition on efficiency, incen-

tives and risk control, after taking into account the endogenous, competition-dependent firm

structure.

Although we have assumed a risk-averse principal and a risk-neutral agent, our results

remain true if the principal and the agent are both risk averse but the principal is more so than

the agent. When both are risk averse, we would only be able to carry out a numerical analysis

since we do not have a closed-form solution. However, if the agent is more risk averse than the

principal, then it is always better for the right of risk control to reside with the agent for the

purposes of risk control and incentive motivation. But if so, decentralization would be strongly

favored, which is inconsistent with our case studies.

Page 21 of 30

Appendix3

Proof of Proposition 3

Given the parametric functions in (12), problem (5) becomes

, (18)

By introducing a Lagrange multiplier the FOCs are

(19)

(20)

and the Kuhn-Tucker condition is

(21)

Equation (19) implies that By (21), we know that the constraint in (18) is binding. This

implies that the solution cannot achieve efficiency. Substituting (19) into (20) eliminates and

yields

(22)

Using the binding constraint to replace the term by in (22) yields

Using the binding constraint again to eliminate in (22), we find

which implies and in Proposition 3. Social welfare is

(23)

Notice that since is a probability, we require which represents a condition on

the parameters.

Given and , the optimal revenue-sharing scheme is determined by the two IC

conditions in (4):

3 This appendix is for referees only and is not intended for publication. Proofs of Propositions 1 and 2 are

available upon request.

Page 22 of 30

Consider a linear scheme . Given the parametric functions in (12), the two IC

conditions become

implying

Then,

( )and

( )and

( )( ) ( )

Proof of Proposition 4

Given the parametric functions in (12), problem (9) becomes

,By introducing a Lagrange multiplier the FOCs are

(25)

(26)

The Kuhn-Tucker condition is

(27)

If then (25) implies which cannot possibly be an optimal solution. Hence, we

must have Then, equation (26) implies that

Page 23 of 30

(28)

and (27) implies a binding constraint:

(29)

Substituting (28) into (29) yields

( )( )which implies and in Proposition 4. Social welfare is

(30)

Given and , the optimal revenue-sharing scheme is determined by the two IC

conditions in (8), i.e.,

Consider a linear scheme . Given the parametric functions, the two IC condi-

tions become

implying

Then,

and ( )( )

Proof of Proposition 6

We allow any ; no need to restrict to be in We can write ∗ and ∗ as

∗ ( ) ( ) ∗ ( ) ( )

Page 24 of 30

where and are some constants that are independent of . We have

∗ ( ) ( )

and similarly

If , then and , and if and only if

which obviously holds. That is, if , we always have .

If , then and , and if and only if

which always holds. That is, if , the negative effect on payoff under a lower control

structure is stronger than that under a higher control structure.

Proof of Proposition 7

We allow any ; no need to restrict to be in In the above proof, we find that if

, then and ; and if , then and . Hence, if

, then ∗

and ∗

; and if , then ∗

and ∗

.

Proof of Proposition 8

We allow any ; no need to restrict to be in We can write ∗ and ∗ as

∗ ( )( )∗ ( )( )∗ ( ) ( )( )∗ ( ) ( )( )

Page 25 of 30

where and are some constants that are independent of . Since and , if

we obviously have ∗ ∗ ∗ ∗And, if the above four derivatives have the opposite sign.

Proof of Proposition 9

We can write ∗ and ∗ as

∗ ( ) ( ) ∗ ( ) ( )

where and are some constants that are independent of . Let ( )Then, ( )

( ) ( )( ) ( )

( )implying

Then,

∗ ∗

∗ ∗We have

Also,

Page 26 of 30

Also,

where and

Let

If then implying . Hence, , and This means

that, if rises, the firms’ payoffs will be lower, and a higher control structure means a smaller

reduction in payoffs.

If then if and only if If so, . Hence, , and

This means that, if rises, the firms’ payoffs will be lower, and a higher control

structure means a smaller reduction in payoffs.

If then if and only if We have

Hence, there is a such that if and only if Note that we have .

Hence, we have . Hence, if , we have , and This means

that, if rises, the firms’ payoffs will be lower, and a higher control structure means a smaller

reduction in payoffs. On the other hand, if , we have , and This

means that, if rises, the firms’ payoffs will be higher for both structures.

Finally, is determined by the equation

By taking the derivative of the above equation w.r.t. and denoting , we find

Since , we have . Hence, the above implies .

Similarly, By taking the derivative of (31) w.r.t. and denoting , we find

Since , we have . Hence, the above implies .

Page 27 of 30

Proof of Proposition 10

We can write ∗ and ∗ as

∗ ( ) ( ) ∗ ( ) ( )where and are some constants that are independent of . We have

If , then and , and if and only if

which obviously holds. That is, if , we always have . Since and

, we have ∗ ∗If , then and , and if and only if

which always holds. That is, if , the negative effect on payoff under a lower

control structure is stronger than that under a higher control structure. Since and

, we have ∗ ∗

References

Aghion, P, Bloom, N, Sadun, R, Van Reenen, J. (2014). Never Waste a Good Crisis?

Growth and Decentralization in the Great Recession. Working Paper, Harvard University.

Aghion P, Dewatripont, M, Rey, P. (1999). Competition, Financial Discipline, and Growth.

Review of Economic Studies, 66, 825-852.

Alchian, A. (1950). Uncertainty, Evolution, and Economic Theory. Journal of Political

Economy, 58, 211-221.

Page 28 of 30

Alonso, R, Dessein, W, Matouschek, N. (2014). Organizing to Adapt and Compete. Ameri-

can Economic Journal: Microeconomics, Article, forthcoming.

Bartunek, JM. (1984). Changing interpretive schemes and organizational restructuring:

The example of a religious order. Administrative Science Quarterly, 29, 355-372.

Becker, G.S. (1971). Economic Theory. Knopf, New York.

Bolt, W, Tieman, AF. (2004). Banking Competition, Risk and Regulation. Scandinavian

Journal of Economics, 106(4), 783-804.

Boyd, JH, Nicoló, G. (2005). The Theory of Bank Risk Taking and Competition Revisited.

Journal of Finance, LX(3), 1329-1343.

Caves, R. (1992). Technical efficiency, rent seeking and excess profits in US manufactur-

ing industries, 1977. In D.B. Audretsch and J.J. Siegfried, eds, Empirical Studies in Industrial

Organization: Essays in honor of Leonard W Weiss. Dordrecht: Kluwer Academic. 187-206.

Caves, RE, Barton D. (1990). Efficiency in U.S. Manufacturing Industries. MIT Press.

Chen, S, Wang, S (2012). A Contingency Theory of Internal Reorganization: Risk and

Output Management. Working Paper, HKUST.

Chhaochharia, V, Grinstein, Y, Grullon, G, Michaely, R. (2012). Product Market Competi-

tion and Internal Governance: Evidence from the Sarbanes Oxley Act. Working Paper, Univer-

sity of Miami.

Coase, R. (1960). The Problem of Social Cost. Journal of Law and Economics, 3, 1-44.

Damanpour, F, Evan, WM. (1984). Organizational Innovation and Performance: The

Problem of “Organizational Lag”. Administrative Science Quarterly, 29, 392-409.

Fabrizio, KR, Rose, NL, Wolfram, CD. (2010). Do Markets Reduce Costs? Assessing the

Impact of Regulatory Restructuring on U.S. Electric Generation Efficiency. American Eco-

nomic Review, forthcoming.

Façanha, LO, Resende, M. (2006). Hierarchical Structure in Brazilian Industrial Firms:

an Econometric Study. Working Paper, European University Institute.

Ferreira, D, Kittsteiner, T. (2011). Competition and Organizational Change. Working Pa-

per, RWTH Aachen University.

Grossman, SJ, Hart, OD. (1986). The Costs and Benefits of Ownership: A Theory of Verti-

cal and Lateral Integration. Journal of Political Economy, 94 (4), 691-719.

Hart, OD. (1983). The Market as an Incentive Mechanism. Bell Journal of Economics, 14,

366-382.

Hart, OD. (1988). Incomplete Contracts and the Theory of the Firm. Journal of Law,

Economics, and Organization, 4 (1), 119-139.

Page 29 of 30

Hart, OD, Moore, J. (1990). Property Rights and the Nature of the Firm. Journal of Politi-

cal Economy, 98 (6), 1119-1158.

Hermalin B. (1992). The Effects of Competition on Executive Behavior. Rand Journal of

Economics, 23, 350-365.

Holmström, B. (1979). Moral Hazard and Observability. Bell Journal of Economics, 10,

74-91.

Huff, AS, Schwenk, C. (1990). Bias and sense making in good times and bad. In A.S. Huff

(ed.), Mapping Strategic Thought. Wiley, Chichester, 89-108.

Inderst, H, Müller, HM. (2003). Internal Versus External Financing: An Optimal Con-

tracting Approach. Journal of Finance, 58, 1033-1062.

Jewitt, I. (1988). Justifying the First-Order Approach to Principal-Agent Problems.

Econometrica, 56, 1177-1190.

Lawrence, PR, Lorsch, JW. (1969). Organization and Environment. Homewood, Ill.:

Richard D. Irwin.

Leibenstein, H. (1966). Allocative Efficiency vs. ‘X-Efficiency’. American Economic Re-

view, 56(3), 392-415.

Lenz, RT. (1981). ‘Determinants’ of organizational performance: An interdisciplinary re-

view. Strategic Management Journal, 2, 131-154.

Marin, D, Verdier, T. (2008). Power inside the firm and the market: A general equilibrium

approach. Journal of the European Economic Association, 86(4), 752-788.

Mirrlees, JA. (1974). The Theory of Moral Hazard and Unobservable Behavior. Working

Paper, appear in Review of Economic Studies, 66, 3-21, 1999.

Mirrlees, JA. (1975). Notes on Welfare Economics, Information and Uncertainty. In Balch,

M, McFadden, D, Wu, S. (eds). Essays in Economic Behavior Under Uncertainty. North-

Holland, 243-258.

Mirrlees, JA. (1976). The Optimal Structure of Authority and Incentives Within an Organ-

ization, Bell Journal of Economics, 7, 105-131.

Nickell, S. (1996). Competition and Corporate Performance. Journal of Political Economy,

104(4), 724-746.

Nickell, S, Nicolitsas, D, Dryden, N. (1997). What Makes Firms Perform Well? European

Economic Review, 783-796.

Pagoulatos, E, Sorensen, R. (1986). What Determines The Elasticity Of Industry Demand?

International Journal of Industrial Organization, 4, 237-250.

Page 30 of 30

Palmon, O, Wald, JK. (2002). Are two heads better than one? The impact of changes in

management structure on performance by firm size. Journal of Corporate Finance, 8, 213-226.

Raith, M. (2003). Competition, Risk, and Managerial Incentives. American Economic Re-

view, 93, 1425-1436.

Rogerson, WP. (1985). The First-Order Approach to Principal-Agent Problems. Econo-

metrica, 53 (6), 1357-1367.

Saunders, A, Strock, E, Travlos, N. (1990). Ownership Structure, Deregulation, and Bank

Risk-Taking. Journal of Finance, 45, 643-654.

Scharfstein, D. (1988). Product Market Competition and Managerial Slack. Rand Journal

of Economics, 19, 147-155.

Schmidt, KM. (1997). Managerial Incentives and Product Market Competition. Review of

Economic Studies, 64(2), 191-213.

Stigler, G. (1958). The Economics of Scale. Journal of Law and Economics, 1, 54-71.

Related Documents