Activity-Based Management and Strategic Costing at CIPO January 27 th , 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Activity-Based Management and

Strategic Costing at CIPO

January 27th, 2015

2

Agenda

• CIPO at a Glance

• Value of Strategic Costing

• Activity-Based Management (ABM)

– What is ABM?

– Components of ABM

• Activity-Based Costing (ABC)

– Basic Concepts

– ABC Methodology at CIPO

– ABC Model at CIPO

• How ABM is used at CIPO

• Challenges

• Success Factors

CIPO at a Glance

• Special Operating Agency

– Funded by a Revolving Fund fully-financed by user fees

– $150 million revenue generated per year, by clients

• Workforce

– Approximately 900 employees

– Mostly technical: engineers, scientists and researchers

• Volume

– CIPO receives about 100,000 IP applications per year

3

IP Volume Patents Trademarks Industrial

Designs Copyright

Applications 36,900 49,500 5,200 8,200

Grants/Registrations 20,900 26,800 4,600 8,150

4

Value of Strategic Costing

• Intense pressure to do more with less

– Increase quality and productivity

– Reduce backlog or processing time

– Lower costs

– Etc…

• The solution for governments under pressure cannot be to simply

uncover new sources of revenue or increase taxes

• Meeting this challenge often requires information such as:

– Accessing accurate and easy‐to‐understand financial data

– Establishing and understanding the actual costs of products/services,

business activities and access/distribution channels

– Identifying and implementing process improvements

– Evaluating outsourcing or privatization options

– Aligning activities to the organization’s vision, mission, and its strategic plan

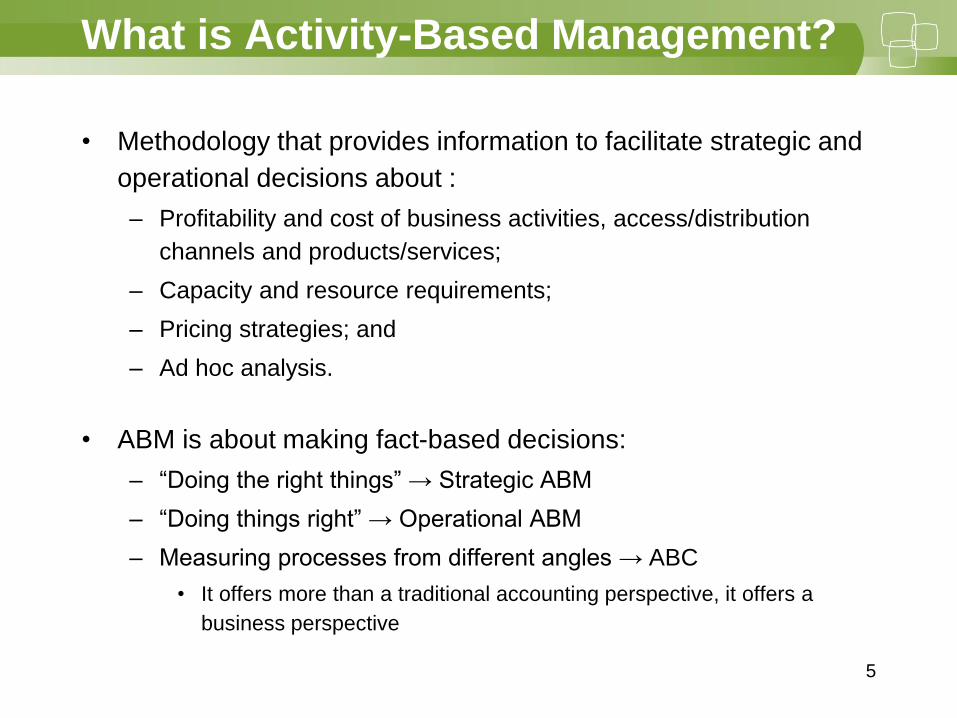

What is Activity-Based Management?

• Methodology that provides information to facilitate strategic and

operational decisions about :

– Profitability and cost of business activities, access/distribution

channels and products/services;

– Capacity and resource requirements;

– Pricing strategies; and

– Ad hoc analysis.

• ABM is about making fact-based decisions:

– “Doing the right things” → Strategic ABM

– “Doing things right” → Operational ABM

– Measuring processes from different angles → ABC

• It offers more than a traditional accounting perspective, it offers a

business perspective

5

6

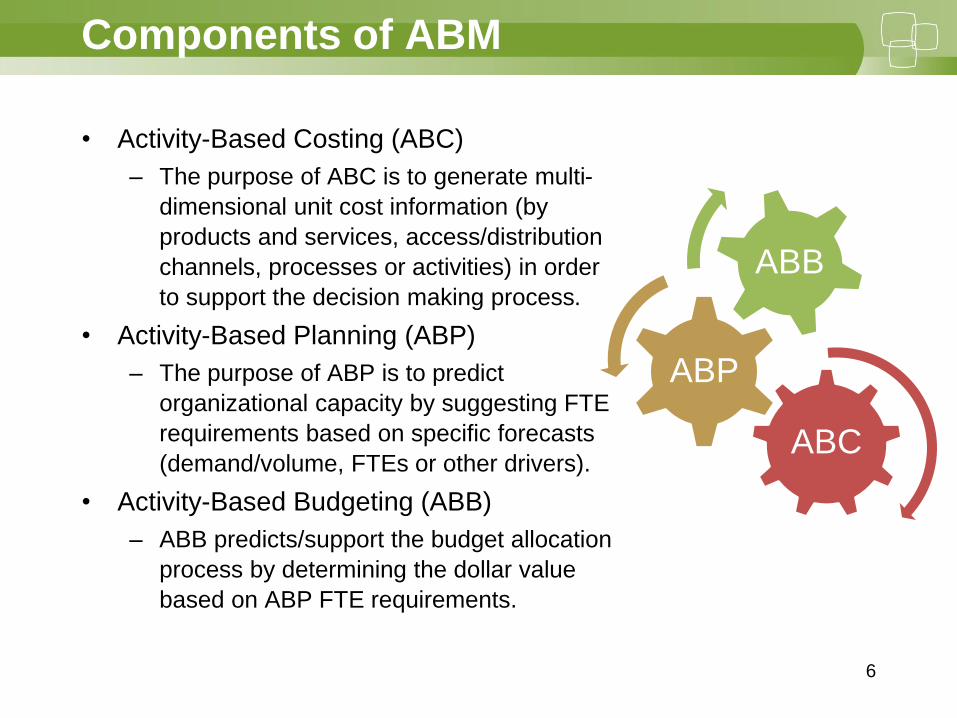

Components of ABM

• Activity-Based Costing (ABC)

– The purpose of ABC is to generate multi-

dimensional unit cost information (by

products and services, access/distribution

channels, processes or activities) in order

to support the decision making process.

• Activity-Based Planning (ABP)

– The purpose of ABP is to predict

organizational capacity by suggesting FTE

requirements based on specific forecasts

(demand/volume, FTEs or other drivers).

• Activity-Based Budgeting (ABB)

– ABB predicts/support the budget allocation

process by determining the dollar value

based on ABP FTE requirements.

ABC

ABP

ABB

7

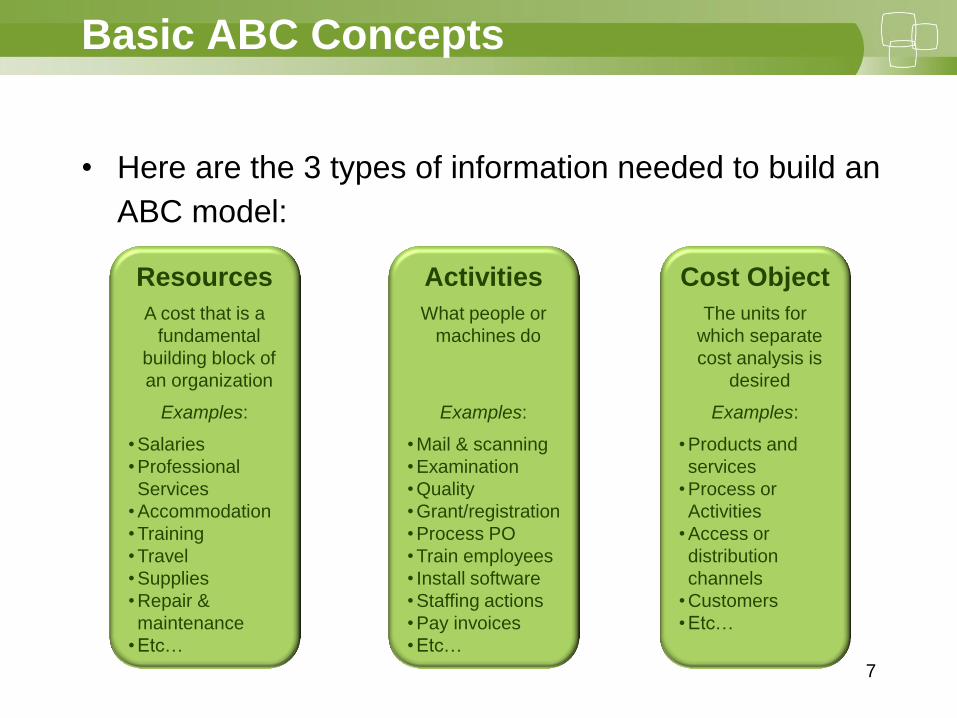

Basic ABC Concepts

• Here are the 3 types of information needed to build an

ABC model:

Resources

A cost that is a

fundamental

building block of

an organization

Examples:

• Salaries

• Professional

Services

• Accommodation

• Training

• Travel

• Supplies

• Repair &

maintenance

• Etc…

Activities

What people or

machines do

Examples:

• Mail & scanning

• Examination

• Quality

• Grant/registration

• Process PO

• Train employees

• Install software

• Staffing actions

• Pay invoices

• Etc…

Cost Object

The units for

which separate

cost analysis is

desired

Examples:

• Products and

services

• Process or

Activities

• Access or

distribution

channels

• Customers

• Etc…

Business

Sustaining

Drivers Drivers

Drivers

8

ABC Methodology at CIPO

• Measuring processes from different angles:

Resources Financial System

Activities

Cost Object

Corporate

Costs

•Salaries

•O&M

Corporate

Activities

Business

Sustaining

Costs (BSC)

Operational

Costs

•Salaries

•O&M

Operational

Activities

Products/

Services

Mark-up

Tra

ditio

nal C

ost A

ccounting

$1

50

M

AB

C A

ccountin

g

$1

50

M

Drivers

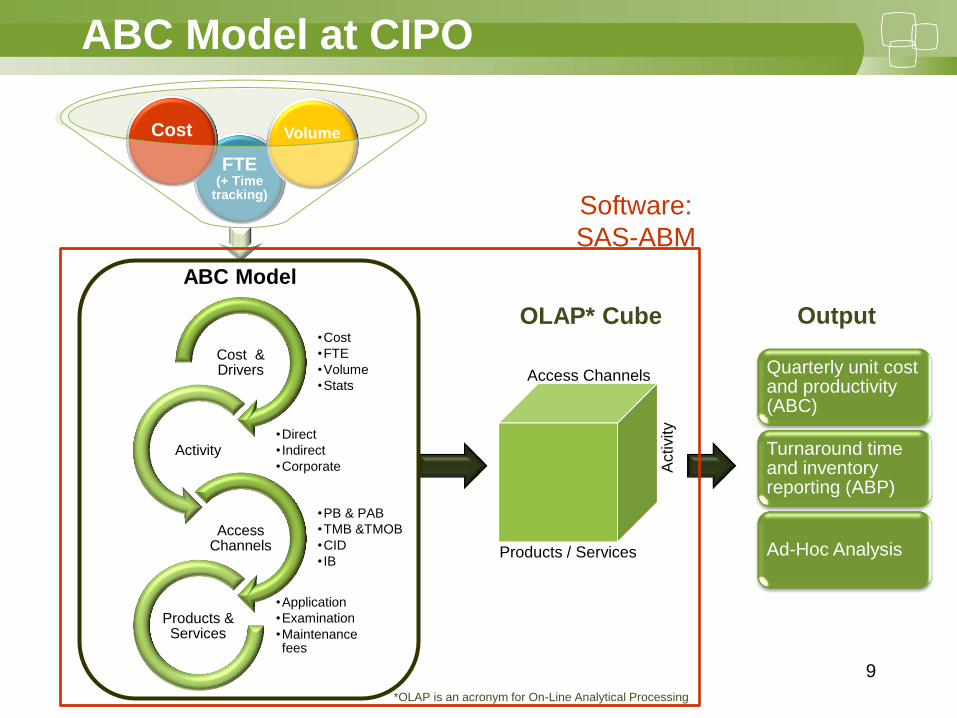

ABC Model at CIPO

Quarterly unit cost and productivity (ABC)

Turnaround time and inventory reporting (ABP)

Ad-Hoc Analysis

Output OLAP* Cube •Cost

•FTE

•Volume

•Stats

Cost & Drivers

•Direct

• Indirect

•Corporate

Activity

•PB & PAB

•TMB &TMOB

•CID

• IB

Access Channels

•Application

•Examination

•Maintenance fees

Products & Services

Access Channels

Products / Services

Activity

ABC Model

FTE (+ Time

tracking)

Cost

Volume

9

*OLAP is an acronym for On-Line Analytical Processing

Software:

SAS-ABM

10

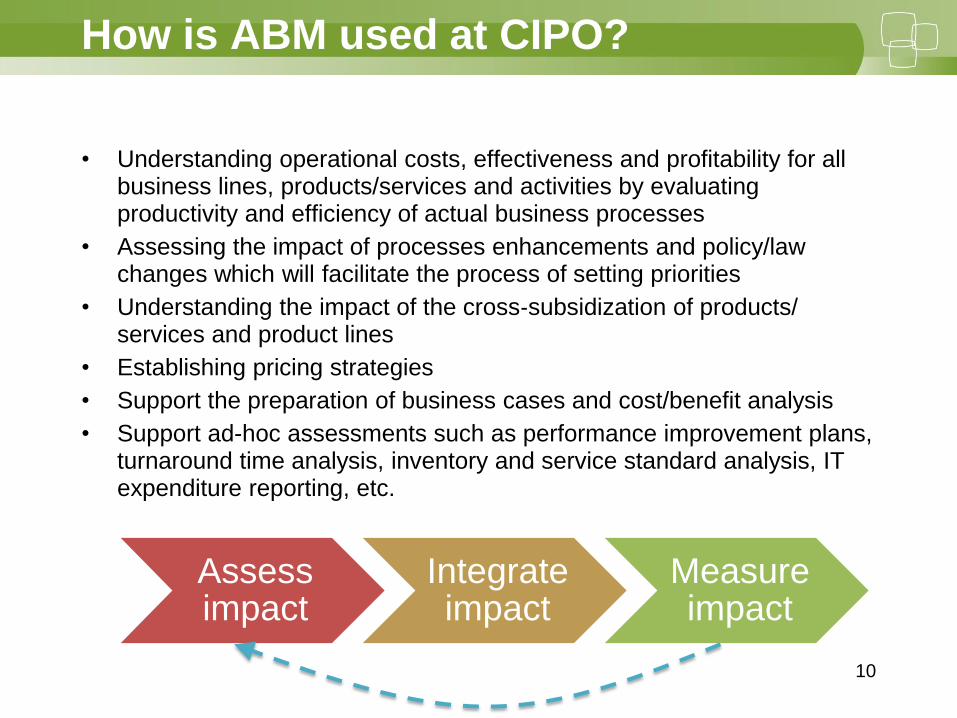

How is ABM used at CIPO?

• Understanding operational costs, effectiveness and profitability for all business lines, products/services and activities by evaluating productivity and efficiency of actual business processes

• Assessing the impact of processes enhancements and policy/law changes which will facilitate the process of setting priorities

• Understanding the impact of the cross‐subsidization of products/ services and product lines

• Establishing pricing strategies

• Support the preparation of business cases and cost/benefit analysis

• Support ad-hoc assessments such as performance improvement plans, turnaround time analysis, inventory and service standard analysis, IT expenditure reporting, etc.

Assess impact

Integrate impact

Measure impact

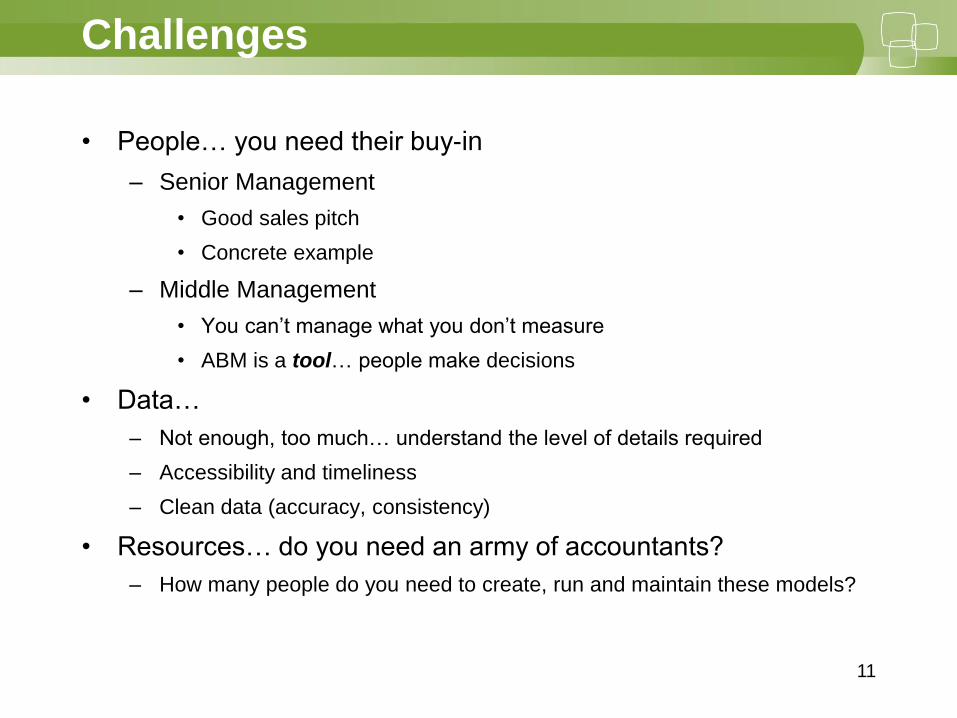

Challenges

• People… you need their buy-in

– Senior Management

• Good sales pitch

• Concrete example

– Middle Management

• You can’t manage what you don’t measure

• ABM is a tool… people make decisions

• Data…

– Not enough, too much… understand the level of details required

– Accessibility and timeliness

– Clean data (accuracy, consistency)

• Resources… do you need an army of accountants?

– How many people do you need to create, run and maintain these models?

11

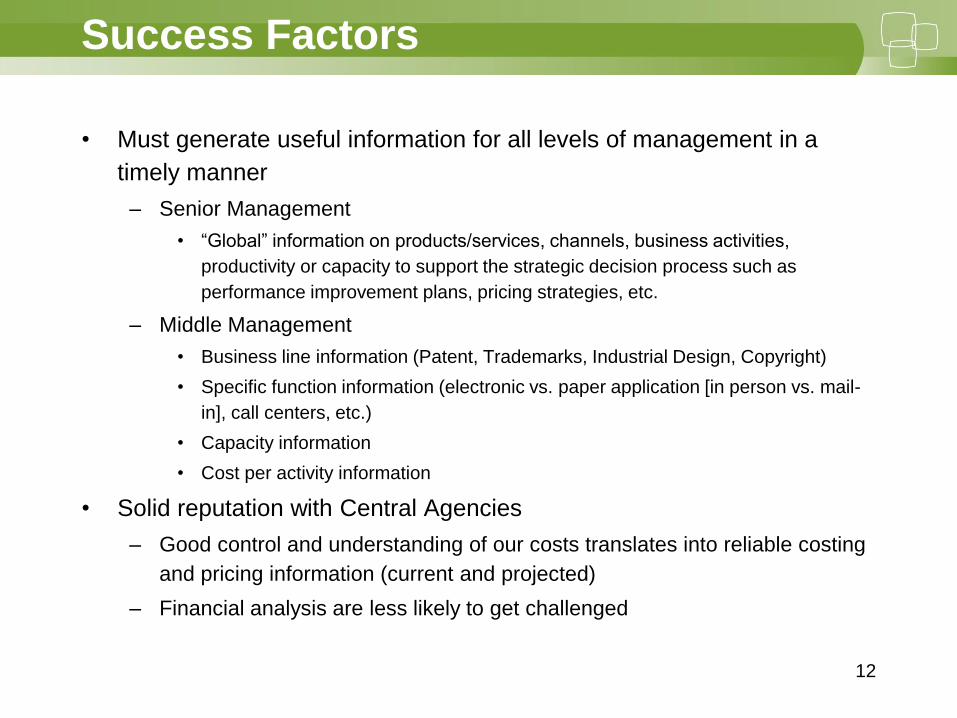

Success Factors

• Must generate useful information for all levels of management in a

timely manner

– Senior Management

• “Global” information on products/services, channels, business activities,

productivity or capacity to support the strategic decision process such as

performance improvement plans, pricing strategies, etc.

– Middle Management

• Business line information (Patent, Trademarks, Industrial Design, Copyright)

• Specific function information (electronic vs. paper application [in person vs. mail-

in], call centers, etc.)

• Capacity information

• Cost per activity information

• Solid reputation with Central Agencies

– Good control and understanding of our costs translates into reliable costing

and pricing information (current and projected)

– Financial analysis are less likely to get challenged

12

So Why Use ABM?

• To understand current and future cost and

capacity in order to facilitate strategic and

operational decisions in an ever changing

environment.

• “ABM is more than an accounting tool; it's a

system for continuous improvements”.1

13

1Chartered Institute of Management Accountants: http://www.cimaglobal.com/Documents/ImportedDocuments/ABM_techrpt_0401.pdf

14

Questions / Comments

Christian Bergeron, MBA, CPA, CMA Canadian Intellectual Property Office (CIPO)

Deputy Director, Costing, Performance

Measurement and Managerial Accounting

Email: [email protected]

Tel: 819-953-9660

Jean-René Drapeau, CPA, CGA Canadian Intellectual Property Office (CIPO)

Director, Business Improvement Services

Email: [email protected]

Tel: 819-934-0510

Related Documents