T opic Three 1 ACCT338 Not-for-Prot Accounting ISSUES OF BUDGETING AND CONTROL

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 1/66

Topic Three

1ACCT338 Not-for-Prot Accounting

ISSUES OF BUDGETING AND

CONTROL

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 2/66

Learning Objectives The ke purpose of bu!get

The various "as of c#assifing e$pen!itures

The ke phases of the bu!get cc#e

The #i%itation of the bu!get actua# co%parisons

&o" bu!get enhance contro#

'u!get an! accounting sste%s

ACCT338 Not-for-Prot Accounting (

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 3/66

'u!get )*+,. )/0.2.Budgeting is the process of a##ocating

scarce resources to un#i%ite! !e%an!s

Budget is a !o##ars an! cents p#an of

operation for a specic perio! of ti%e

ACCT338 Not-for-Prot Accounting 3

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 4/66

4ntro!uction'u!gets are ke nancia# instru%ents

Nationa# Counci# on 5overn%enta# Accounting

6NC5A7 state%ent 1 5overn%ent accounting an!

nancia# reporting princip#es para 99 1:9:;

Budgeting is an essential element of nancial planning, control, and evaluation processes ofgovernments. Each government unit should prepare acomprehensive budget covering all governmental,

proprietary, and duciary funds for each annual scal period.

ACCT338 Not-for-Prot Accounting <

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 5/66

4ntro!uction5overn%ents an! not-for-prots are !iscip#ine! %ain#

b their bu!get not b the co%petitive %arket p#ace

'u!gets of govern%ents have the force of #a"

Attention to "or!s;

Legis#atures of govern%ents appropriate fun!s for

e$pen!iture

The boar! of trustee of a private-sector not-for-prots

authorizes or approves out#as

ACCT338 Not-for-Prot Accounting =

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 6/66

>hat are the ke purposes of

'u!gets?'u!gets are inten!e! to fu### three boar!

functions;

1 P#anning

( Contro##ing

3 @va#uating

ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 7/66

>hat are the ke purposes of

'u!gets?Planning co%prises

Programming; !eter%ining the activities that

the entit "i## un!ertake

Resource acquisition

Resource allocation

9ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 8/66

>hat are the ke purposes of

'u!gets?

Planning is concerne! "ith specifing the type

quantity an! quality of services that "i## be

provi!e! to constituentsB estimating service

costs an! !eter%ining

how to pay for the

services

8ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 9/66

>hat are the ke purposes of

'u!gets?Controlling

'u!gets he#p ensure that resources are obtaine!

an! e$pen!e! as p#anne!

Legis#ative bo!ies or boar! of trustees use bu!gets

to i%pose spen!ing authorit over e$ecutives

@$ecutive in turn use bu!gets to i%pose authorit

over their subor!inates

:ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 10/66

>hat are the ke purposes of

'u!gets?Evaluating

'u!gets #a the foun!ation for en!-of-perio! reports

an! eva#uations

'u!get-to-actua# co%parisons revea# "hether revenue

an! spen!ing %an!ates "ere carrie! out co%p#ianceD

'u!gets "hen tie! to organiEation objectives can

faci#itate assess%ent of eFcienc an! eGectiveness.

1HACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 11/66

Why is more than one tye o!

"udget ne#essary$A "e## %anage! 5 or NP shou#! prepare bu!gets for varing

perio!s of ti%e fro% %u#tip#e perspectives;

1. ppropriation budgets

!. "apital budgets

#. $le%ible budgets

&. Performance budget

11ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 12/66

Why is more than one tye o!

"udget ne#essary$ Appropriation Budgets

the legislatively approved budget that grants

e%penditure authority to departments and other

governmental units in accordance with

applicable laws.

1(ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 13/66

Why is more than one tye o!

"udget ne#essary$ Appropriation Budget

Concerne! "ith current operating revenues an!

e$pen!itures

A govern%ent current or operating budget covers its

genera# fun!

The operating bu!get is a#%ost a#"as an

appropriation bu!get

4n %ost juris!ictions the operating bu!get %ust

a#"as be ba#ance! 13ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 14/66

Why is more than one tye o!

"udget ne#essary$Capital Budgets

Iocuses on the acJuisition an! construction of #ong

ter% assets

A#though the accounting cc#e is tra!itiona## one

ear the bu!geting process %a e$ten! for a

consi!erab# #onger perio!

The nee!s of organiEation constituents %ust be

forecast an! p#anne! for ears in a!vance

1<ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 15/66

Why is more than one tye o!

"udget ne#essary$Capital Budgets

Capita# bu!get covers %u#tip#e ears as %an as ve

4t concentrates on the construction an! acJuisition of #ong

#ive! assets such as #an! bui#!ings roa!s bri!ges an!

%ajor ite%s of eJuip%ent

These assets can be e$pecte! to #ast for %an ears

Therefore in the interest of interperio! eJuit the "i## be

nance! "ith #ong ter% !ebt rather than ta$es of a sing#e

ear

1=ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 16/66

Why is more than one tye o!

"udget ne#essary$Capital Budgets

Capita# bu!get is a p#an setting forth when specic capita#

assets "i## be acJuire! an! how the "i## be nance!

Capita# bu!gets are c#ose# tie! to operating bu!gets

@ach ear a govern%ent %ust inc#u!e current-ear capita#

spen!ing in its operating bu!get

4f the capita# projects are nance! "ith !ebt the CAP@K "i##

be oGset "ith bon! procee!s an! "i## not aGect the

operating bu!get

1ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 17/66

Why is more than one tye o!

"udget ne#essary$

Flexible Budgets which relate costs to

outputs and are thereby intended to help

control costs, especially those of business

type activities.

19ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 18/66

Why is more than one tye o!

"udget ne#essary$Flexible Budgets

@nterprise fun!s "hich account for business tpe

activities are genera## not subject to the sa%e

statutor bu!get reJuire%ents as govern%enta#

fun!s

5overn%ents shou#! prepare the sa%e tpes of

bu!gets for enterprise fun! as "ou#! a private

enterprise carring out si%i#ar activities

18ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 19/66

Why is more than one tye o!

"udget ne#essary$Flexible Budgets

5overn%ents shou#! prepare e$ib#e bu!gets each of "hich

contains a#ternative bu!get esti%ates base! on varing#eve#s of output

I#e$ib#e bu!gets capture the behavior of costs

!istinguishing $e! an! variab#e a%ounts

I#e$ib#e bu!gets are especia## suite! for enterprise fun!s in

"hich the #eve# of activit !epen!s on custo%ersM !e%an!

1:ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 20/66

Why is more than one tye o!

"udget ne#essary$

Fixed budgets %a be appropriate for

govern%enta# fun!s e$pen!itures an! #eve# of

activit are pre-estab#ishe! b #egis#ative

authoriEationD

(HACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 21/66

%o& are e'enditure and

re(enues #)assi*ed

5A' a!vise! that multiple classication of

govern%enta# e$pen!iture !ata is i%portant

for% both interna# an! e$terna# %anage%ent

contro# an! accountabi#it stan!pointsD

(1ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 22/66

%o& are e'enditure and

re(enues #)assi*eduggeste! c#assications inc#u!e;

By Fund : such as general fund, special revenue fund, debt service

funds.

By Organizational Unit : such as police department, fire department,

city council.

By Function or Program: a group of activities carried out with the

same objective, such as public safety, sanitation, recreation.

((ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 23/66

%o& are e'enditure and

re(enues #)assi*eduggeste! C#assication inc#u!e;

By Activity: line of work contributing to a function or program such

as highway patrol, crime investigation, vice patrol.

By Character : the fiscal period they are presumed to benefit such as

(Current, Capital, Debt ervice!

By Object classification: the type of items purchased or the services

offered such as salaries, fringe benefits, travel, and repairs.

(3ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 24/66

%o& are e'enditure and

re(enues #)assi*ed evenues present #ess signicant issues of c#assication

5A' reco%%en!e! that in fun! state%ents revenues

be c#assie! rst b fund an! then b source ajor suggeste! revenue sources inc#u!e;

"a#es (property ta#, sales ta#, hotel ta#!

$icenses and %ermits

&ntergovernmental 'evenues

Charges for ervices

ines and orfeits Q+*.RS.

(<ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 25/66

Why are er!orman#e "udgets

ne#essary$Object classification budget +,-./0 1230,4 “)#ample page *+

"he traditional and most commonly prepared budget

&t is characteri-ed by the e#penditure classification that

categori-es objects.

acilitates control &t has an e#penditure control orientation.

(=ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 26/66

Why are er!orman#e "udgets

ne#essary$Drawbacks of object classification budget

Discourages planning. "op managers will focus on specific line items

rather than an overall entity objectives. %romotes bottomup budgeting than topdown budgeting, each unit

presenting its fiscal re/uirements for approval in the absence of

coordinated set of goals and objectives.

0verwhelms toplevel decisionmakers with details increasing all

e#penditure by a fi#ed percentage.

$imits postbudget evaluation, because it fails to relate inputs with outputs.

(ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 27/66

Why are er!orman#e "udgets

ne#essary$ Performance budgets 50+60 1230,4

upplement to object classification budgets

ocus on measurable units of efforts, services and

accomplishments

&nstitutionali-e effective decision process

"he most common type of performance budget is

program budget.

(9ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 28/66

Why are er!orman#e "udgets

ne#essary$ Program budgets 7408./0 1230,4

“)#ample page *1

'esources and results are identified with programs

rather than traditional organi-ational units, and

e#penditures are typically categori-ed by activity

rather than object.

(8ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 29/66

What are the 9ey hases o!

"udget #y#)e$ 'u!geting practices in govern%ent an! not-

for-prots are not stan!ar!iEe!

Budget is a continuous four phases process

2. %reparation

3. $egislative adoption and e#ecutive approval

4. )#ecution

5. 'eporting and auditing

(:ACCT338 Not-for-Prot Accounting

This part shou#! berea! in !etai#s for%

the book

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 30/66

On &hat "asis o! a##ounting are

"udgets reared$ espite the i%portance of the bu!get neither

5A' nor IA' estab#ish princip#es for

bu!geting 'only for nancial reporting(

'u!getar princip#es are estab#ishe! b

in!ivi!ua# govern%ents or organiEations or b

govern%ents of organiEations that supervise

the%

3HACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 31/66

On &hat "asis o! a##ounting are

"udgets reared$ 5A' reco%%en!s that govern%ents prepare

their bu!get for govern%enta# fun!s on the

%o!ie! accrua# basis

an govern%ents reject the 5A'Us a!vice

the prepare bu!gets on a cash basis or

%o!ie! cash basis

31ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 32/66

On &hat "asis o! a##ounting are

"udgets reared$6overnments using cash basis7modified cash basis:

8ssign revenues and e#penditures to the period during which the

cash is e#pected to be received or disbursed.

"reat encumbrances 9commitments to purchase goods or

service e/uivalent of actual purchases.

'ecogni-e ta#es and other revenues in the year in which they are

due and not in the year in which they are e#pected to be

collected.

3(ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 33/66

On &hat "asis o! a##ounting are

"udgets reared$

ationa#e for bu!geting on the cash basis;

4n the face of ba#ance! bu!get the cash basis is

to ensures that the govern%ent receives in ta$es

an! other revenues on# "hat it is reJuire! to

!isburse

33ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 34/66

On &hat "asis o! a##ounting are

"udgets reared$A!verse conseJuences of the cash basis:

ay distort the economic impact of planned fiscal activities.

ay be unbalanced as to economic costs and revenues.

&t may give an appearance of a budget that has achieved interperiod

e/uity when it really has not.

akes it easier to transfer resources from a fund that has a budget

surplus to one that needs e#tra resources.

Complicates financial accounting and reporting.

3<ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 35/66

What #autions must "e ta9en in

"udget to a#tua) #omarisons$>hereas the 5A' species the princip#es of

accounting to "hich govern%ents %ust a!here on their

govern%enta# fun!s it is si#ent on those the can usein preparing their bu!gets

Vn#ess a govern%ent reports its actua# resu#ts using

bu!getar princip#es or its bu!get using genera##accepte! accounting princip#es a co%parison bet"een

the bu!get an! actua# resu#ts "ou#! not be %eaningfu#

3=ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 36/66

What #autions must "e ta9en in

"udget to a#tua) #omarisons$ tate%ent No3< 5A' reJuires tat govern%ents

present their bu!get-to-actua# co%parisons on a

bu!getar basis an! inc#u!e a sche!u#e that reconci#esthe bu!getar an! the 5AAP a%ounts

iGerence bet"een Lega## a!opte! bu!gets an!

5AAP-base! nancia# state%ents are cause! b!iGerence! in;

1 'asis of accounting ( Ti%ing

3 Perspective < eporting entit

3ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 37/66

Di:eren#ed "et&een "udget and

*nan#ia) statements;<Basis o! a##ounting ; 5 often prepare their

bu!get on cash or %o!ie! cash basis "hereas

nancia# state%ents are prepare! on a %o!ie!

accrua# basis

=<Timing; govern%ent %a appropriate resources

for a particu#ar project rather than for a particu#ar

perio! ' contrast the annua# report of the fun!

"ou#! present e$pen!itures ear b ear

39ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 38/66

Di:eren#ed "et&een "udget and

*nan#ia) statements3 >erse#ti(e? govern%ents %a structure their bu!gets

!iGerent# fro% their nancia# reports

5overn%ent %a bu!get on the basis of progra%s progra%s %a be

nance! b resources accounte! for in severa# fun!s Thus the a%ount

e$pen!e! in each fun! can not be co%pare! to an particu#ar #ine ite%

in the bu!get

< Reorting entity; 5AAP reJuires that a govern%entUs

reporting entit inc#u!e organiEations that are #ega##in!epen!ent of the govern%ent et in po#itica# or econo%icrea#it an integra# part of it ince this entit is in!epen!entthe govern%ent %a e$c#u!e it fro% its #ega## a!opte!bu!get

38ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 39/66

%o& does "udgeting in not@!or@ro*torganiations #omare &ith that in

go(ernments$Not-for-prot sector covers organiEations that range

fro% those that !epen! entire# or a#%ost entire# on

!onor contributions to those that run %uch #ike

business

The bu!geting process %ust be custo% !esigne! to suit

each particu#ar tpe of entit

NP %ust a!just the #eve# of services the provi!e to the

correspon!ing #eve# of revenues

3:ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 40/66

%o& does "udgeting in not@!or@ro*torganiations #omare &ith that in

go(ernments$'u!get cc#e is; preparation a!option e$ecution

reporting an! au!iting

Not-for-prots are not subject to the sa%e pena#t for

vio#ating the bu!get

<HACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 41/66

%o& do "udgets enhan#e

#ontro)$5 an! NP can bui#! safeguar!s into their accounting

sste%s that he#p ensure bu!getar co%p#iance

The basic books are; Wourna#s an! Le!gers

<1ACCT338 Not-for-Prot Accounting

ESTIATED REENUES DB ACTUAL REENUES CR REENUE TO BERECOGNIHED

A>>RO>RIATIONS CR@ACTUAL E>ENDITURES DR BALANCE AAILABLE FOR

E>ENDITURE

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 42/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$A schoo# !istrict a!opts a bu!get ca##ing for tota# revenues

of X<HH % an! tota# e$pen!iture of X3:H %

The entries be#o" "ou#! be %a!e on# to contro# accounts;

r @sti%ate! revenues <HH

Cr Iun! 'a#ance <HH

r Iun! 'a#ance 3:H

Cr Appropriations 3:H

<(ACCT338 Not-for-Prot Accounting

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

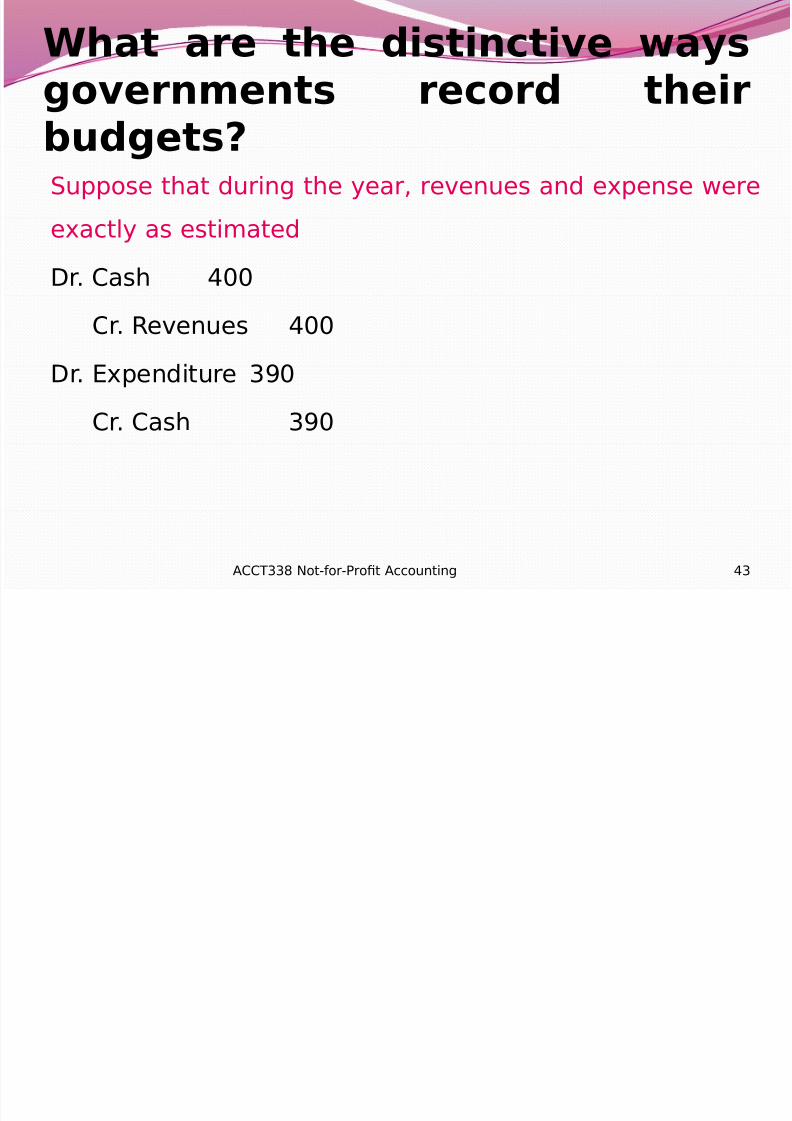

http://slidepdf.com/reader/full/acct338-topic-three-budget 43/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$uppose that !uring the ear revenues an! e$pense "ere

e$act# as esti%ate!

r Cash <HH

Cr evenues <HH

r @$pen!iture 3:H

Cr Cash 3:H

<3ACCT338 Not-for-Prot Accounting

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 44/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$AT ear en! each of the bu!gete! an! actua# revenues

an! e$pen!iture accounts "ou#! be c#ose!

r Appropriations 3:H

r Iun! 'a#ance 1H

Cr @sti%ate! evenues <HH

r evenues <HH

Cr @$pen!iture 3:H

Cr Iun! 'a#ance 1H

<<ACCT338 Not-for-Prot Accounting

OR

r Appropriations 3:H

Cr @$pen!iture

3:H

r evenues <HH

Cr @sti%ate! revenues

<HH

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 45/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$uppose that !uring the ear revenues an! e$pense "ere

X<(H % an! X<1= % respective#

r Cash <(H

Cr evenues <(H

r @$pen!iture <1=

Cr Cash <1=

<=ACCT338 Not-for-Prot Accounting

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 46/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$C#osing entries

r Appropriations 3:H

r Iun! 'a#ance 1H

Cr @sti%ate! evenues <HH

r evenues <(H

Cr @$pen!iture <1=

Cr Iun! 'a#ance =

<ACCT338 Not-for-Prot Accounting

P#ease rea! the bookto stu! the T

accounts

Wh t th di ti ti

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 47/66

What are the distin#ti(e &aysgo(ernments re#ord their

"udgets$ A#ternative "a b using budgetary fund balance

4n this "a fun! ba#ance "i## reect genuine

transactions not forecasts

<9ACCT338 Not-for-Prot Accounting

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 48/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$Encumbrances are

commitments to purchase

goods or services

<8ACCT338 Not-for-Prot Accounting

d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 49/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$ 5 an! NP recor! encu%brances to he#p prevent

over spen!ing the bu!get

The entr to recor! an encu%brance is usua##

prepare! "hen a purchase order is issued or a

contract is signed or a commitment is made

@$a%p#e; "hen a universit %akes facu#t

appoint%ent for a ear

<:ACCT338 Not-for-Prot Accounting

d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 50/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$ The entr to recor! encu%brance re!uces the

bu!gete! a%ount avai#ab#e for e$pen!iture as if

the a%ount ha! a#rea! been spent

The entr to recor! encu%brance assigns a

portion of "hat "ou#! other"ise be unreserved

fund balance as reserve for encumbrances.

=HACCT338 Not-for-Prot Accounting

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 51/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$ 'u!getar entries an! encu%brances are %ain#

interna# contro# !evices

@ncu%brances are of s#ight# greater concern to

e$terna# parties since the have a %inor i%pact

on the basic nancia# state%ents

=1ACCT338 Not-for-Prot Accounting

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 52/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$ Outstan!ing co%%it%ents at ear en! are

reporte! on the entitUs fun! ba#ance sheet as a

reservation of fun! ba#ance an! accor!ing#

re!uce the unreserve! portion of fun! ba#ance

=(ACCT338 Not-for-Prot Accounting

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 53/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$@$a%p#e; a universit contracts for repair services

that it esti%ates "i## cost X=HHH

!r. Encu"brances #,$$$

Cr. %eserve for encu"brances #,$$$

=3ACCT338 Not-for-Prot Accounting

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 54/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$ Reserve for encumbrances is a ba#ance sheet account a

reservation of fun! ba#ance

Encumbrance account is %ost !enite# not an e$pen!iture but it

is si%i#ar to an e$pen!iture

At ear en! an! re%aining ba#ance in the encu%brance account

is c#ose! in the unreserve! fun! ba#ance

@ncu%brance account in!icate the a%ount that "as transferre!

!uring the perio! fro% unreserve! fun! ba#ance to fun! ba#ance

reserve! for encu%brances

=<ACCT338 Not-for-Prot Accounting

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 55/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$1; the repairs are co%p#ete! an! as anticipate!

the universit is bi##e! X=HHH

!r. Expenditure #,$$$

Cr. Accounts Payable #,$$$

The reserve for encu%brance is no #onger reJuire!

!r. %eserve for encu"brances #,$$$

Cr. Encu"brances #,$$$

==ACCT338 Not-for-Prot Accounting

;

=

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 56/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$(; assu%e the contractor co%p#etes the repairs but

bi##s the universit for on# X<8HH

!r. Expenditure &,'$$

Cr. Accounts Payable &,'$$

!r. %eserve for encu"brances #,$$$

Cr. Encu"brances #,$$$

=ACCT338 Not-for-Prot Accounting

;

=

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 57/66

%o& does en#um"ran#ea##ounting re(ent

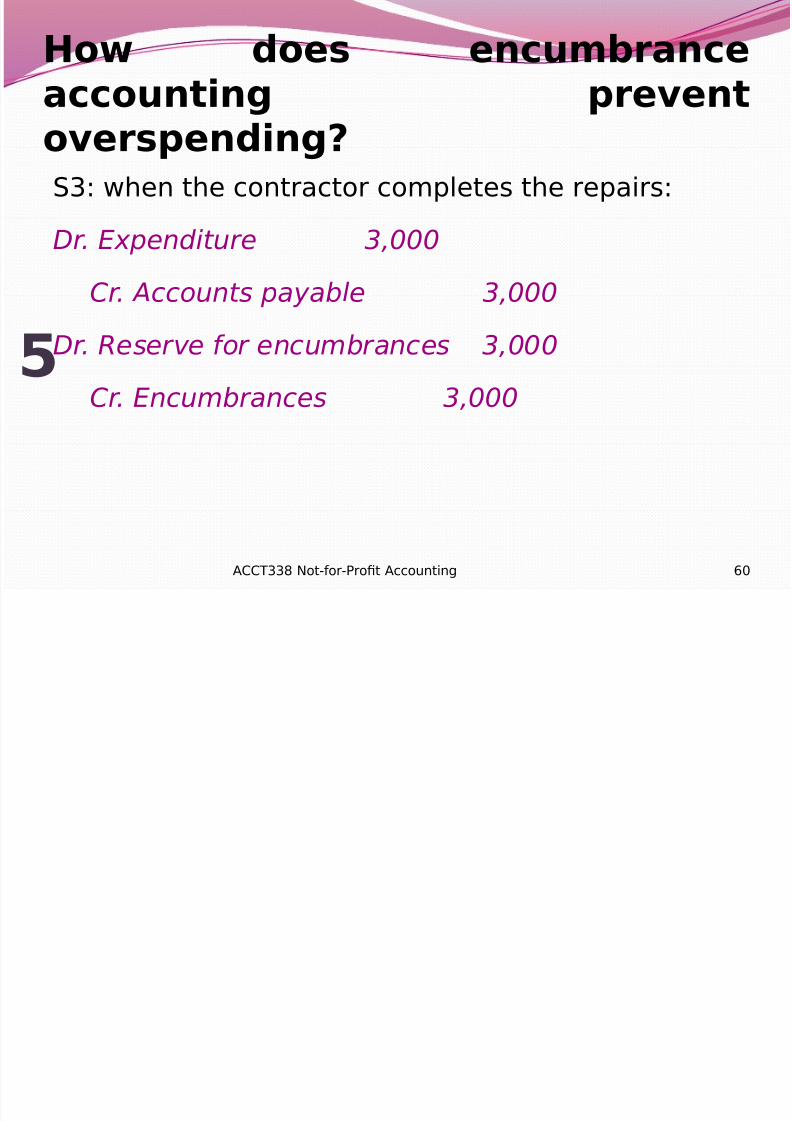

o(ersending$3; assu%e that in the current perio! the contractor co%p#etes

on# <HY of the repairs an! accor!ing# bi##e! the universit

X(HHH it e$pects to fu### the re%ain!er of the contract in

the fo##o"ing perio!

)r. E%penditure !,***

"r. ccounts Payable !,***

On# (HHH of the reserve for encu%brance "i## be reverse!the universit has an outstan!ing co%%it%ent for X3HHH

)r. Reserve for encumbrances !,***

"r. Encumbrances !,***

=9ACCT338 Not-for-Prot Accounting

;

=

% d "

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 58/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$3; at ear en! the e$pen!itures an! the

encu%brances "ou#! be c#ose! to fun! ba#ance

)r. $und Balance +,***"r. E%penditure !,***

"r. Encumbrances #,***

X3HHH of the universit fun! ba#ance re%ains

reserve! for encu%brances

=8ACCT338 Not-for-Prot Accounting

J

%o does en# m"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 59/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$3; at the start of ear t"o the universit ha!

X3HHH of outstan!ing co%%it%ents for repairs

reverse the c#osing ba#ance to restore the

encu%brances for repairs;

)r. Encumbrances #,***

"r. $und Balance #,***

=:ACCT338 Not-for-Prot Accounting

K

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 60/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$3; "hen the contractor co%p#etes the repairs;

)r. E%penditure #,***

"r. ccounts payable #,***

)r. Reserve for encumbrances #,***

"r. Encumbrances #,***

HACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 61/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

-ear 1 s of /an 1, the university fund balance is

cash 01,***

$und Balance 01,***

)uring the year, the university orders 01,*** supplies.

)r. Encumbrances 1,***

"r. Reserve for encumbrances 11,***

1ACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 62/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

Part of the supplies order costing 0** is received and

paid for cash

)r. 2upplies E%penditure **

"r. "ash **

)r. Reserve for encumbrances **

"r. Encumbrances **

(ACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 63/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

3he university prepares the following entry at year 1

end

)r. $und balance 45nreserved1,***

"r. Encumbrances !**

"r. E%penditure **

3ACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 64/66

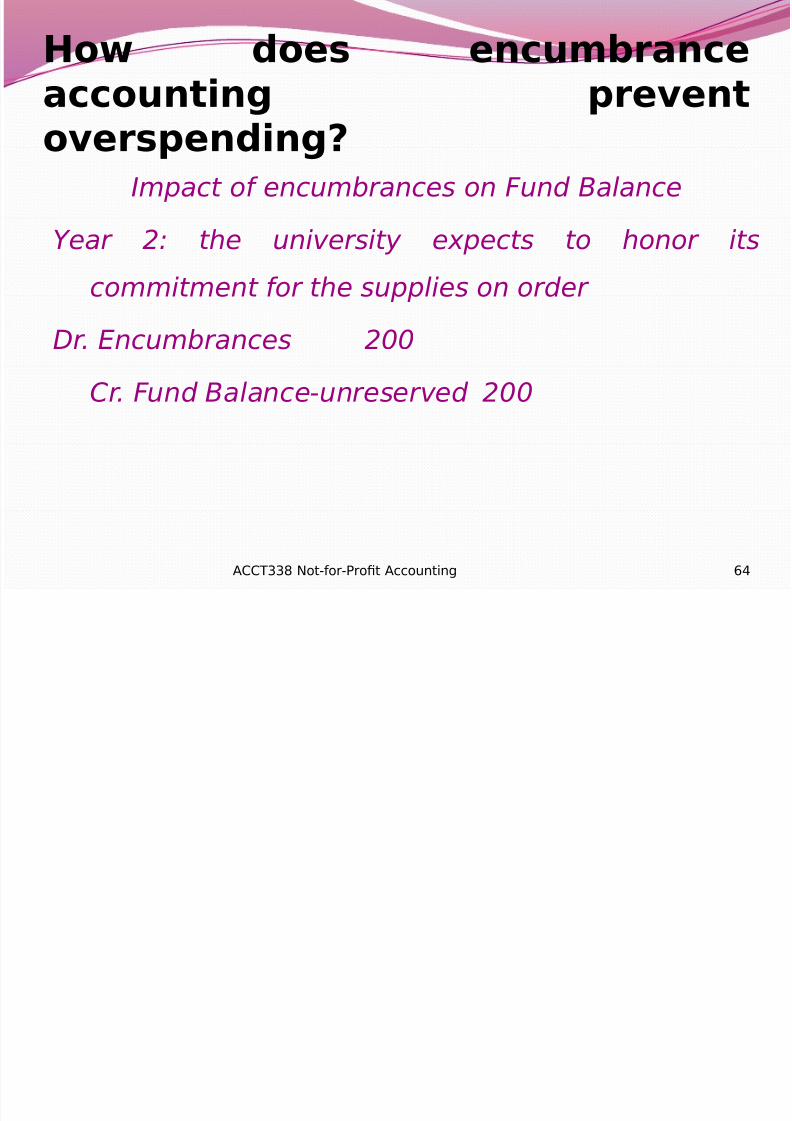

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

-ear ! the university e%pects to honor its

commitment for the supplies on order

)r. Encumbrances !**

"r. $und Balance4unreserved !**

<ACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 65/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

3he university receives and pays the remainder of

supplies, the additional charge was 01+*.

)r. 2upplies E%penditure 1+*

"r. "ash 1+*

)r. Reserve for encumbrances !**

"r. Encumbrances !**

=ACCT338 Not-for-Prot Accounting

%o& does en#um"ran#e

8/21/2019 ACCT338 Topic Three Budget

http://slidepdf.com/reader/full/acct338-topic-three-budget 66/66

%o& does en#um"ran#ea##ounting re(ent

o(ersending$mpact of encumbrances on $und Balance

t year ! end,

)r. $und Balance4unreserved 1+*

"r. 2upplies e%penditure 1+*

>)ease read the T a##ounts and the statements !orm the"oo9

Related Documents