PART- A FINANCIAL ACCOUNTING - I

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PART- A

FINANCIAL ACCOUNTING - I

1.INTRODUCTION TO ACCOUNTING

Book-Keeping Accounting Accountancy Their Differences Features, nature, types and limitations Qualitative Characteristics of Accounting

Information Basic terms

BOOK-KEEPING

Book-keeping is the proper and systematic keeping or maintenance of the books of accounts.

Book keeping starts from the identification of business transaction.

These transaction must be in monitory terms.

Eg. Selling goods for cash.

Cont…..

Another definition – Book-Keeping is a science and art of identifying and recording accounting transactions systematically in the proper books of accounts.

PROCESS OF BOOK-KEEPING

Identifying

Recoding

Classifying/ preparation

of ledger

Balancing and

summarizing

ACCOUNTING

Accounting is the systematic recorded presentation of the financial activities of the business/enterprise.

OR Accounting may be defined as the

identifying, measuring, recording and communicating of financial information.

Accountancy

Accountancy refers to the entire body of the theory and practice of accounting.

It is more wider concept then book-keeping and accounting. it absorbs both book-keeping and accounting.

Difference B/W book-keeping and accounting

S.N.

BASIS Book-Keeping Accounting

1. Objective To prepare original books of accounts. it restricted to only recording and classifying.

To record, analyze and interpret the transaction.

2. Scope Limited Wider then book-keeping

3. Level of work Low level Low/medium even top level

4. Mutual Dependence

It has to depended on accounting

Based on Book-keeping

5. Result of business

Not show net/final result Show net/final result

6. Principles of accountancy

Follow accounting concepts and conventions

Methods vary to firm to firm

Book-keeping, Accounting and Accountancy

Book-Keeping is the proper and systematic maintenance of the books of accounts. it includes :-Identifying RecordingClassifyingAnalyzing

Accounting is book-keeping plus summarizing and interpretation of transactions.

Accountancy is the systemic knowledge of accounting.

Characteristics of Accounting

Economic events Identification Record Analyzing Communication Organization Interested users of information

Types of Accounting:-

The economic development and technological improvements have resulted in anincrease in the scale of operations and the advent of the company form of businessorganization.

This has made the management function more and more complex andincreased the importance of accounting information.

This gave rise to special branchesof accounting. These are briefly explained below

Financial accounting :

The purpose of this branch of accounting is to keep a record of all financial transactions so that:

(a) the profit earned or loss sustained by the business during an accounting period can be worked out,

(b) the financial position of the business as at the end of the accounting period can be ascertained, and

(c) the financial information required by the management

and other interested parties can be provided.

Cost Accounting :

1. The purpose of cost accounting is to analyze the expenditure so as to ascertain the cost of various products manufactured by the firm and fix the prices.

2. It also helps in controlling the costs and providing necessary costing information to management for decision-making.

Management Accounting :

The purpose of management accounting is to assist the management in taking rational policy decisions and to evaluate the impact of its decisions and actions.

Process of accounting

Accounting LINKS decision makers with Economic Events and with the result of their

decision

Need/Objectives/Advantages

Maintaining of records. Calculation of profit or loss. Depiction of financial position. Providing effective control over the

business. Making information available to various

groups.

Limitations

Incomplete information. inexactness. Showing valueless assets. Manipulation. Ignorance about the present value of

business.

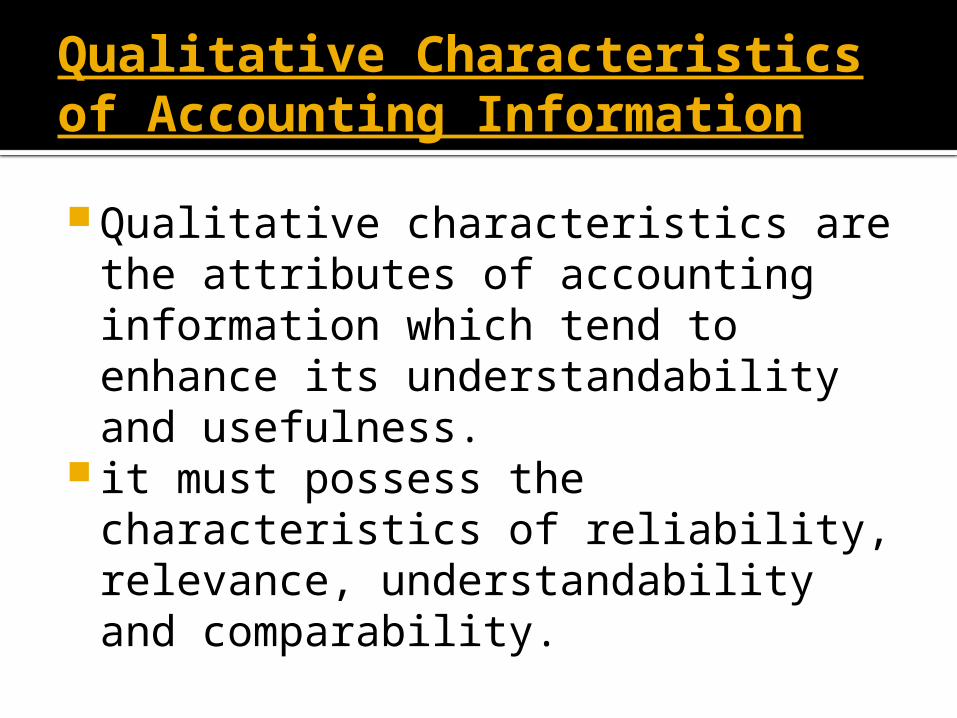

Qualitative Characteristics of Accounting Information

Qualitative characteristics are the attributes of accounting information which tend to enhance its understandability and usefulness.

it must possess the characteristics of reliability, relevance, understandability and comparability.

Reliability Reliability means the users must be able

to depend on the information. The reliability of accounting information is

determined by the degree of correspondence between what the information conveys about the transactions or events that have occurred, measured and displayed.

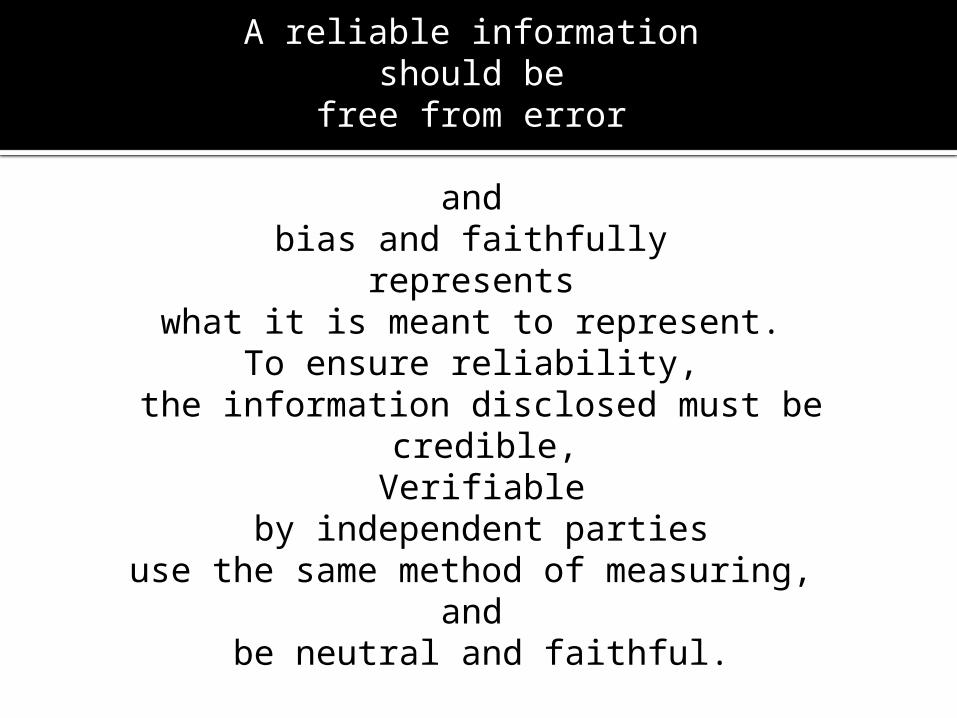

A reliable information should be

free from error

and bias and faithfully

represents what it is meant to represent.

To ensure reliability, the information disclosed must be credible,

Verifiable by independent parties

use the same method of measuring, and

be neutral and faithful.

Relevance To be relevant, information must be available in time,

must help in prediction and feedback, and must influence the decisions of users by :

(a) helping them form prediction about the outcomes of past, present or future events; and/or

(b) confirming or correcting their past evaluations.

Understandability – means decision-makers must interpret accounting information in the same sense as it is prepared and conveyed to them.

The qualities that distinguish between good and bad communication in a message are fundamental to the understandability of the message.

A message is said to be effectively communicated when it is interpreted by the receiver of the message in the same sense in which the sender has sent.

Accountants should present the comparable information in the most intelligible manner without sacrificing relevance and reliability.

Comparability -It is not sufficient that the financial information is relevant

and reliable at aparticular time, in a particular circumstance or for a particular

reporting entity.But it is equally important that the users of the general

purpose financial reportsare able to compare various aspects of an entity over

different time period andwith other entities. To be comparable, accounting reports

must belong to acommon period and use common unit of measurement and

format of reporting.

BASIC TERMS

Entity – means a thing that has a definite individual existence. There are 2 types of entities:

1. Business entity2. Non-business entity Business transaction/economic events –

economic events that relates to business entity is called business transaction.

Cont….

Assets – the valuable things owned by the business are known as assets. like buildings, plant, machinery etc.

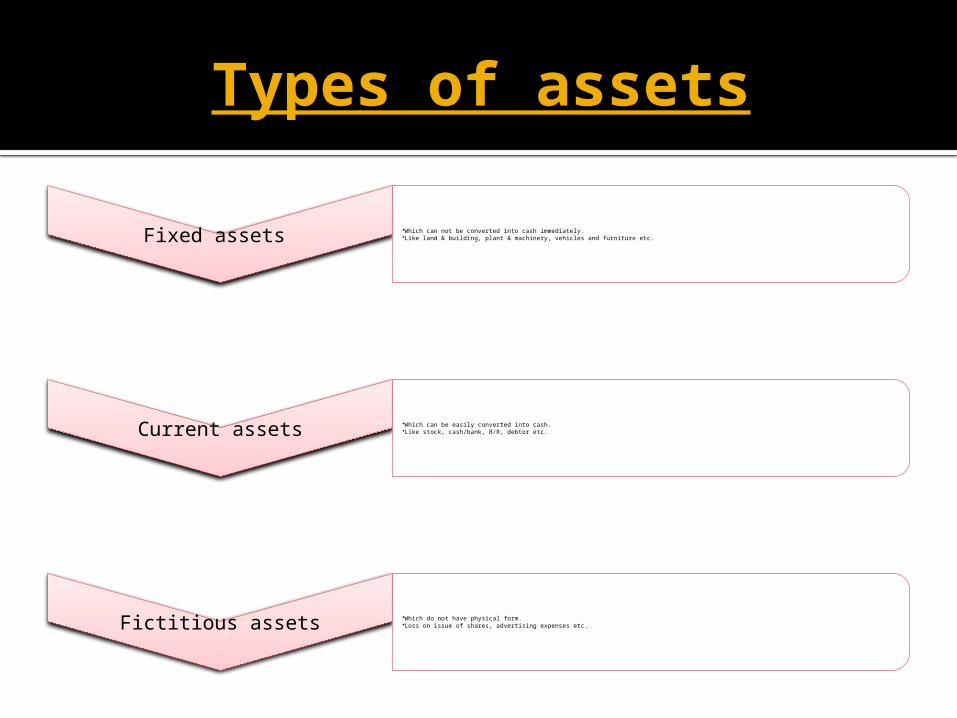

Types of assets

Fixed assets •Which can not be converted into cash immediately.•Like land & building, plant & machinery, vehicles and furniture etc.

Current assets •Which can be easily converted into cash.•Like stock, cash/bank, B/R, debtor etc.

Fictitious assets •Which do not have physical form.•Loss on issue of shares, advertising expenses etc.

Tangible assets• Having physical existence and can be

seen and touched.• Like plant & machinery, furniture etc.

Intangible assets • Not normally can be purchased & sold

in open market.• Like goodwill, patents etc

Wasting assets • Whose value goes on declining with

the passage of time.• Like mine, patents.

Liquid assets

•Which can be converted into cash faster then current assets..•Like cash/bank, debtors, B/R etc.

Capital – Amount invested by the owner in the firm is known as capital. It may be brought in the form of cash or assets by the owner for the business entity.

Capital is an obligation and a claim on the assets of business. It is, therefore, shown as capital on the liabilities side of the balance

sheet. Eg.- in our daily life we need food, cloths etc various necessary things

to purchase them we need money that part of money used to buy things are CAPITAL.

Same as in our business if we want to establish our plant factory, new equipment and so on so we need money or we can say fund so that part of fund/investment is capital.

Capital consist of all current assets and fixed assets. It is further classified as :

1. Fixed capital2. Current floating capital3. Working capital

Fixed Capital –The amount invested in acquiring fixed assets. like• Purchase of

plant and machinery , land and buildings, Vehicles etc.

Floating Capital :• Assets purchased

with intention of sales, such as

• Stock and investments.

Working Capital• A part of capital

used in firm’s day to day working.

• All the current assets and current liabilities.

• W.C.= C.A.+C.L.

Equity and liability – Liabilities are obligations or debts that an

enterprise has to pay at some time in the future. Like creditors, bills payable etc.

They represent creditors’ claims on the firm’s assets. Both small and big businesses find it necessary to borrow money at one time or the other, and to purchase goods on credit.

For example

SUPER BAZAR, purchases goods for Rs.10,000 on credit for a month from Fast Food Products on March 25, 2005.

If the balance sheet of Super Bazaar is prepared as at March 31, 2005, Fast Food Products will be shown as creditors on the liabilities side of the balance sheet.

If Super Bazaar takes a loan for a period of three years from Delhi State Co-operative Bank, this will also be shown as a liability in the balance sheet of Super Bazaar.

LIABILITIES ARE CLASSIFIED AS LONG-TERM LIABILITIES AND SHORT-TERM LIABILITIES :

• Long-term liabilities are those that are usually payable after a period of one year, for example, a term loan from a financial institution or debentures (bonds) issued by a company.

• Short-term liabilities are obligations that are payable within a period of one year, for example, creditors, bills payable, bank overdraft.

Purchase and Sales

Purchase :-To buy something used

in business like purchase of raw material for production or in our daily life purchase of vegetables for food.

Sales :-The ultimate end of goods

purchased or produced by business is their sale.

Sales are total revenues from goods or services sold or provided to customers. Sales may be cash sales or credit sales.

Purchase return and Sales return

Purchase return/return outward :-

It is that part of the purchased goods, which is returned to seller.

Suppose we purchase wood for manufacturing furniture but the woods are so weak and lower in quality so we return back that to seller that return good is called return outward.

Sales return/return inward :-

It is that part of sales of goods which is actually return to us by purchaser.

Suppose we sale furniture to purchaser but the furniture may be damaged in delivery or because of any other reason furniture returned back to us by purchaser.

Revenues - Revenue in accounting means the amount realized or receivable from the sale of goods Other items of revenue common to many businesses are: commission, interest, dividends, royalties, rent received, etc. Revenue is also called income.

Expenses :-

Expenses are cost incurred by the business in the process of earning revenues.

Like freight, carriage, loading-unloading charges.

Expenditure :-

Expenditure is the amount of resources consumed. it is long term in nature.

Like advertising expenditure for increasing sales

Difference B/W expense and expenditure

Expense It indicate the amount

spent to meet short term need of business.

Eg. salary paid to employees.

Expenditure It indicates the

amount spent to meet long term need of business.

Eg. Cost of machine or furniture or building.

Profit and Loss

Profit :- Excess of revenue over

expenses.

OR Excess of sale proceeds over

cost of good soled. For example if the cost of goods

which we want to sale is Rs.2000,we spend some more money like payment of some duties and other expenses Rs.500 and we sale the good for Rs.3000 in that case our cost of good sold is Rs.2500, sale Rs.3000 and profit Rs.500.

Loss :-

Losses are the unwanted burden which the business is forced to bear.

Like loss due to theft/fire/flood/storm/accidents.

INCOME & GAIN

Income:Increase in the net worth

of the enterprise either from business activities or other activities is termed as income.

Gain:Change in net worth due

to change in the form and place of goods and holding of assets for long period, termed as gain.

Bills receivable & Bills payable

B/R:What business has to

receive from outside parties on revenue account.

Eg. If we sale goods on credit then we dawn a bill to purchaser that bill is B/R for us which is to be received in some time.

B/P:What business has to

pay to outside parties.Eg. When we purchase

goods on credit seller drawn a bill acceptable to us is payable to seller by us in some time.

Debtors & Creditors

Debtors:Means a person or parties

who have purchased goods on credit from us an have not paid for the goods sold to them.

Suppose Ram purchased goods from us worth Rs.20000.he pay Rs.16000 & promises to pay Rs.4000 after 2 months then he will remain to be debtor for Rs.4000.

Creditors: If we purchase goods on

credit to any firm or business then we are the creditor that we have to pay for the credit purchase to the seller .

Drawings and Bad debts

Drawings:Goods or amount

withdrawn for personal/private use by businessman from business.

Bad debts:The amount which is no

more receivable from the party/debtors is known as BAD DEBTS.

For example we sold goods worth Rs.12000 to Ram on credit. Ram made a promise to us to pay the amount after a month. but Ram could pay only Rs.9000 so the rest of amount Rs.3000 will be considered as bad debts.

Solvent & Insolvent

Solvent:A

person/firm/business/company which is in a position to pay its debts, is called Solvent.

Insolvent:A

person/firm/business/company which is not in a position to pay its debts, is called Insolvent.

Related Documents