Accounting Level 3 Model Answers Series 2 2005 (Code 3001)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Level 3

Model Answers Series 2 2005 (Code 3001)

© Education Development International plc 2005 Company Registration No: 3914767 All rights reserved. This publication in its entirety is the copyright of Education Development International plc.

Reproduction either in whole or in part is forbidden without written permission from Education Development International plc.

International House, Siskin Parkway East, Middlemarch Business Park, Coventry, CV3 4PE Telephone: +44 (0) 8707 202909 Facsimile: + 44 (0) 24 7651 6566

Email: [email protected]

Vision Statement Our vision is to contribute to the achievements of learners around

the world by providing integrated assessment and learning services, adapted to meet both local market and wider occupational needs

and delivered to international standards.

1

Accounting Level 3 Series 2 2005

How to use this booklet

Model Answers have been developed by Education Development International plc (EDI) to offer additional information and guidance to Centres, teachers and candidates as they prepare for LCCI International Qualifications. The contents of this booklet are divided into 3 elements: (1) Questions – reproduced from the printed examination paper (2) Model Answers – summary of the main points that the Chief Examiner expected to

see in the answers to each question in the examination paper, plus a fully worked example or sample answer (where applicable)

(3) Helpful Hints – where appropriate, additional guidance relating to individual

questions or to examination technique Teachers and candidates should find this booklet an invaluable teaching tool and an aid to success. EDI provides Model Answers to help candidates gain a general understanding of the standard required. The general standard of model answers is one that would achieve a Distinction grade. EDI accepts that candidates may offer other answers that could be equally valid.

© Education Development International plc 2005 All rights reserved; no part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission of the Publisher. The book may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover, other than that in which it is published, without the prior consent of the Publisher.

2

3

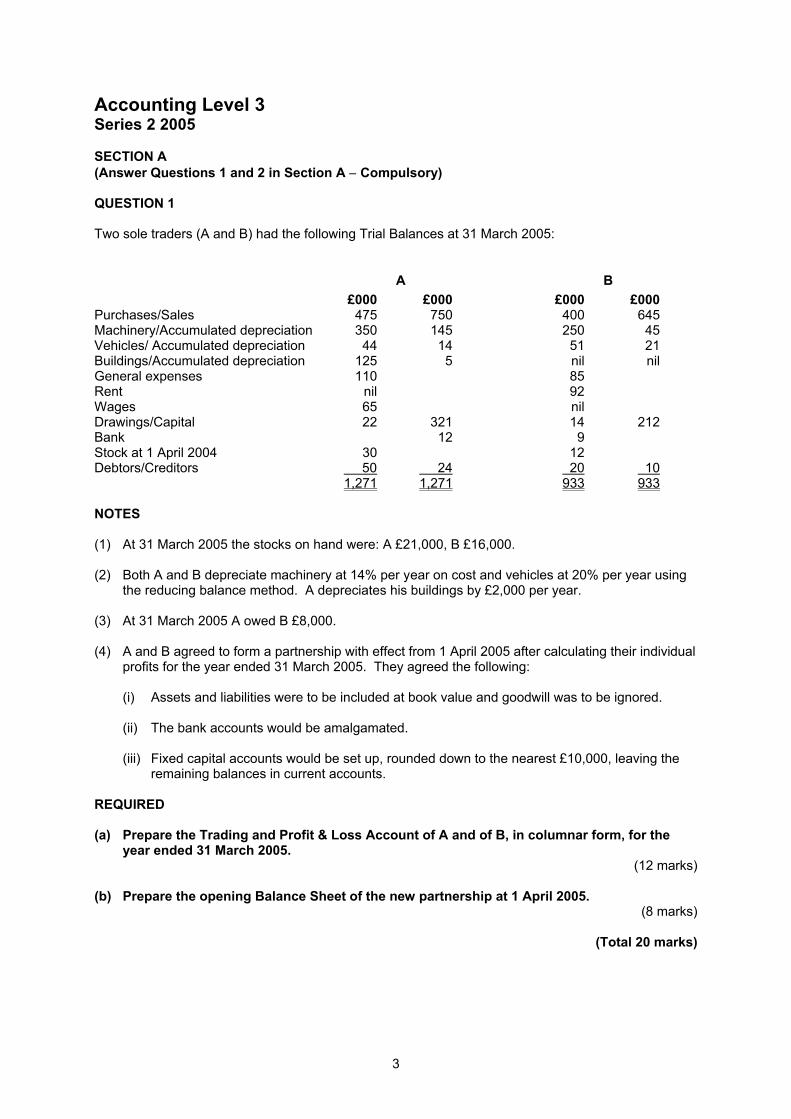

Accounting Level 3 Series 2 2005 SECTION A (Answer Questions 1 and 2 in Section A − Compulsory) QUESTION 1 Two sole traders (A and B) had the following Trial Balances at 31 March 2005:

A B £000 £000 £000 £000 Purchases/Sales 475 750 400 645 Machinery/Accumulated depreciation 350 145 250 45 Vehicles/ Accumulated depreciation 44 14 51 21 Buildings/Accumulated depreciation 125 5 nil nil General expenses 110 85 Rent nil 92 Wages 65 nil Drawings/Capital 22 321 14 212 Bank 12 9 Stock at 1 April 2004 30 12 Debtors/Creditors 50 24 20 10 1,271 1,271 933 933 NOTES (1) At 31 March 2005 the stocks on hand were: A £21,000, B £16,000. (2) Both A and B depreciate machinery at 14% per year on cost and vehicles at 20% per year using

the reducing balance method. A depreciates his buildings by £2,000 per year. (3) At 31 March 2005 A owed B £8,000. (4) A and B agreed to form a partnership with effect from 1 April 2005 after calculating their individual

profits for the year ended 31 March 2005. They agreed the following: (i) Assets and liabilities were to be included at book value and goodwill was to be ignored. (ii) The bank accounts would be amalgamated. (iii) Fixed capital accounts would be set up, rounded down to the nearest £10,000, leaving the

remaining balances in current accounts. REQUIRED (a) Prepare the Trading and Profit & Loss Account of A and of B, in columnar form, for the

year ended 31 March 2005. (12 marks)

(b) Prepare the opening Balance Sheet of the new partnership at 1 April 2005.

(8 marks)

(Total 20 marks)

CONTINUED ON THE NEXT PAGE 4

Model Answer for Question 1 (a) Trading and Profit & Loss Accounts

for year ended 31 March 2005

A B £000 £000 £000 £000 Sales 750 645 Cost of goods sold: Opening stock 30 12 Purchases 475 400 505 412 Closing stock 21 484 16 396 Gross Profit 266 249 General expenses 110 85 Rent - 92 Wages 65 - Depreciation: Machinery (.14 x 350) 49 (.14 x 250) 35 Vehicles [.2 x (44 – 14)] 6 [.2 x (51 – 21)] 6 Buildings 2 232 - 218 Net profit 34 31

5

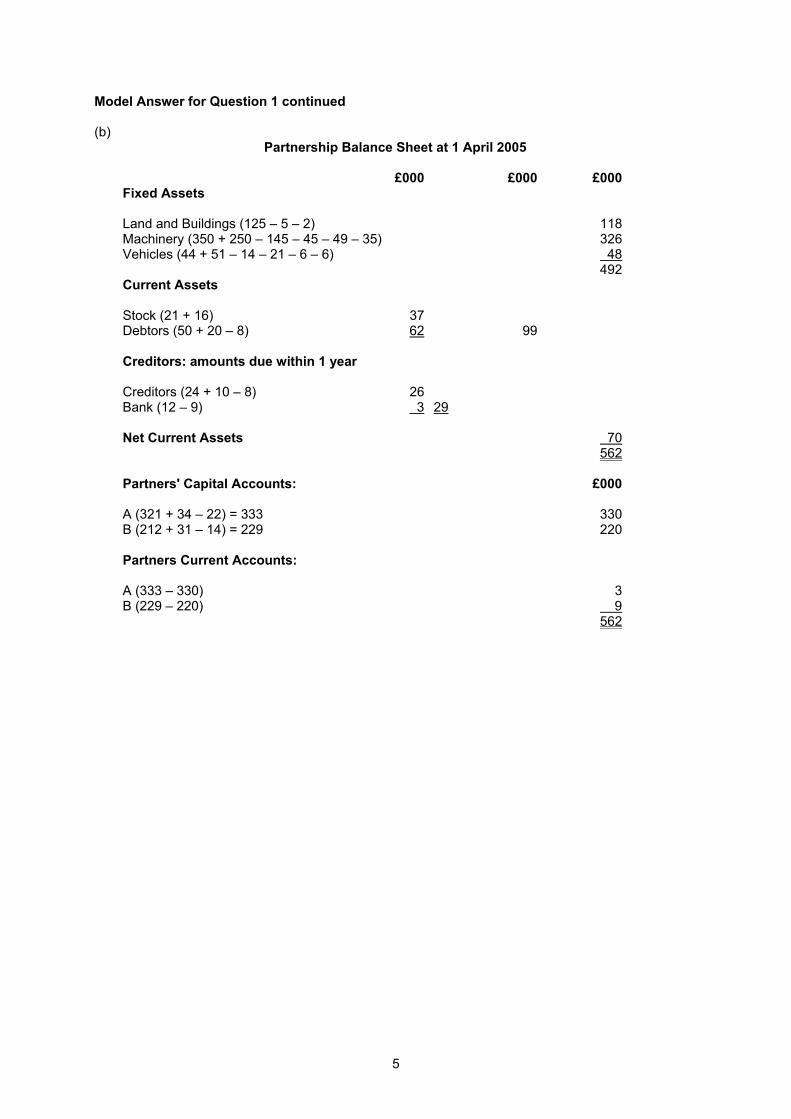

Model Answer for Question 1 continued (b) Partnership Balance Sheet at 1 April 2005 £000 £000 £000 Fixed Assets Land and Buildings (125 – 5 – 2) 118 Machinery (350 + 250 – 145 – 45 – 49 – 35) 326 Vehicles (44 + 51 – 14 – 21 – 6 – 6) 48 492 Current Assets Stock (21 + 16) 37 Debtors (50 + 20 – 8) 62 99 Creditors: amounts due within 1 year Creditors (24 + 10 – 8) 26 Bank (12 – 9) 3 29 Net Current Assets 70 562 Partners' Capital Accounts: £000 A (321 + 34 – 22) = 333 330 B (212 + 31 – 14) = 229 220 Partners Current Accounts: A (333 – 330) 3 B (229 – 220) 9 562

CONTINUED ON THE NEXT PAGE 6

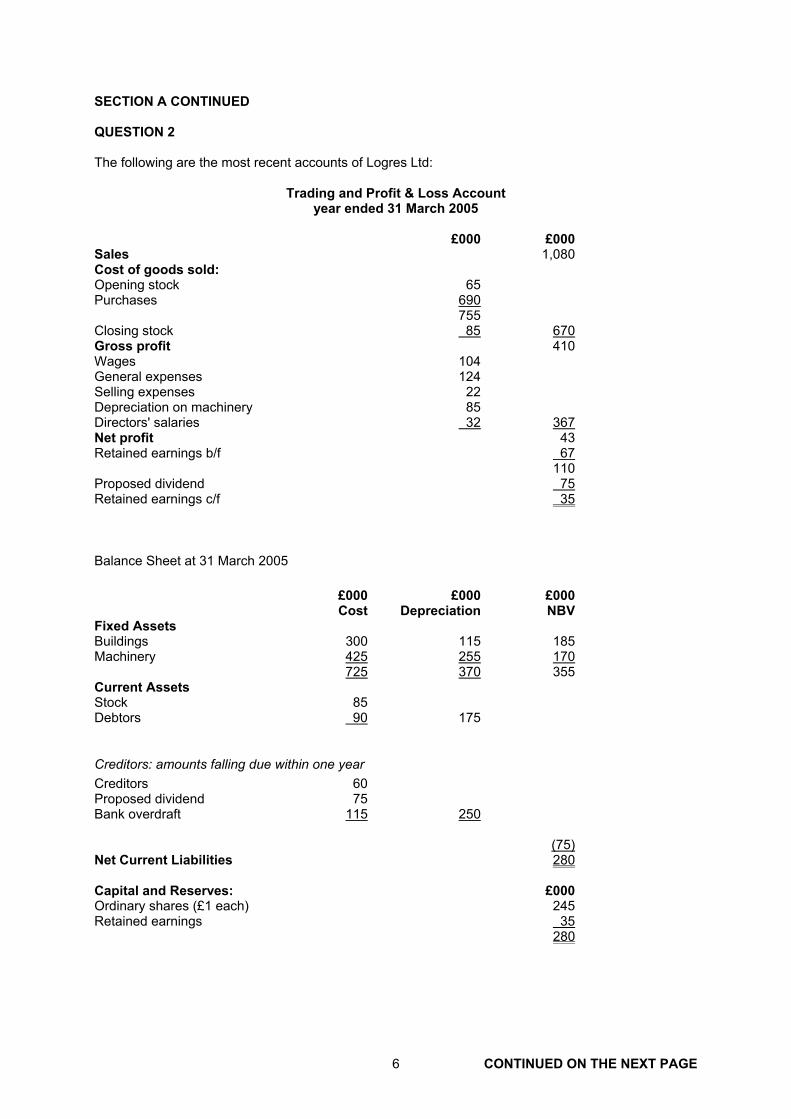

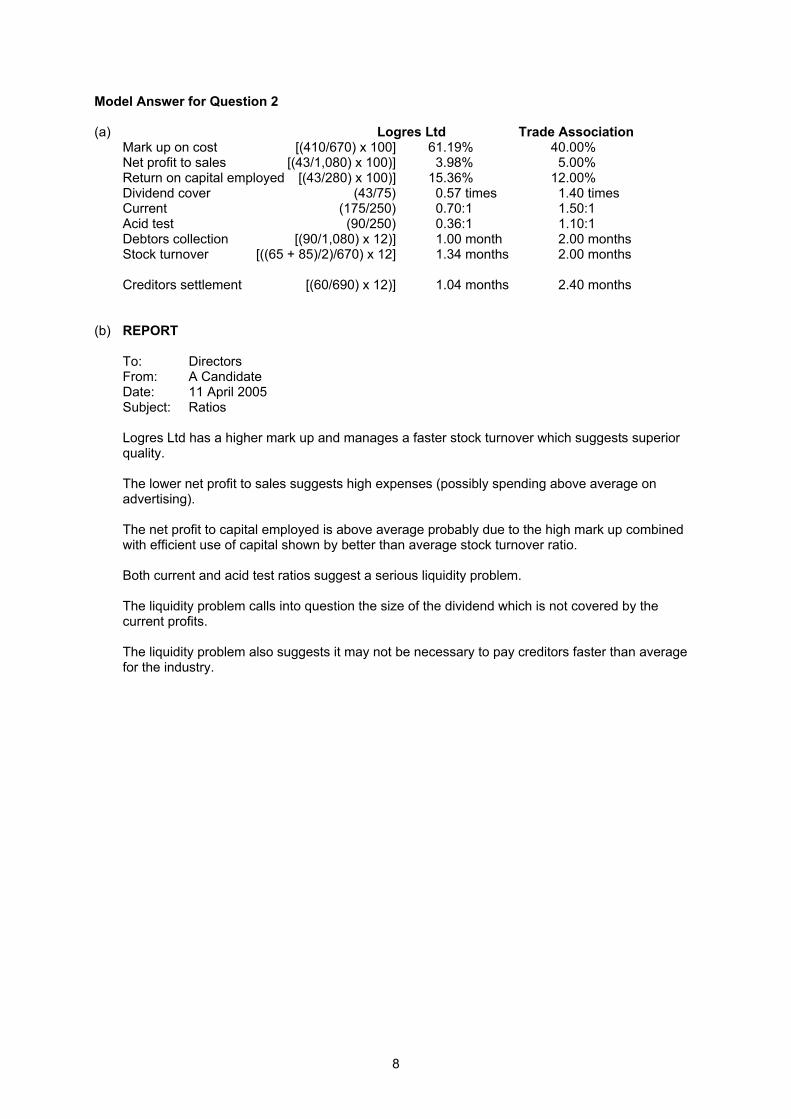

SECTION A CONTINUED QUESTION 2 The following are the most recent accounts of Logres Ltd:

Trading and Profit & Loss Account year ended 31 March 2005

£000 £000 Sales 1,080 Cost of goods sold: Opening stock 65 Purchases 690 755 Closing stock 85 670 Gross profit 410 Wages 104 General expenses 124 Selling expenses 22 Depreciation on machinery 85 Directors' salaries 32 367 Net profit 43 Retained earnings b/f 67 110 Proposed dividend 75 Retained earnings c/f 35

Balance Sheet at 31 March 2005 £000 £000 £000 Cost Depreciation NBV Fixed Assets Buildings 300 115 185 Machinery 425 255 170 725 370 355 Current Assets Stock 85 Debtors 90 175

Creditors: amounts falling due within one year Creditors 60 Proposed dividend 75 Bank overdraft 115 250 (75) Net Current Liabilities 280 Capital and Reserves: £000 Ordinary shares (£1 each) 245 Retained earnings 35 280

7

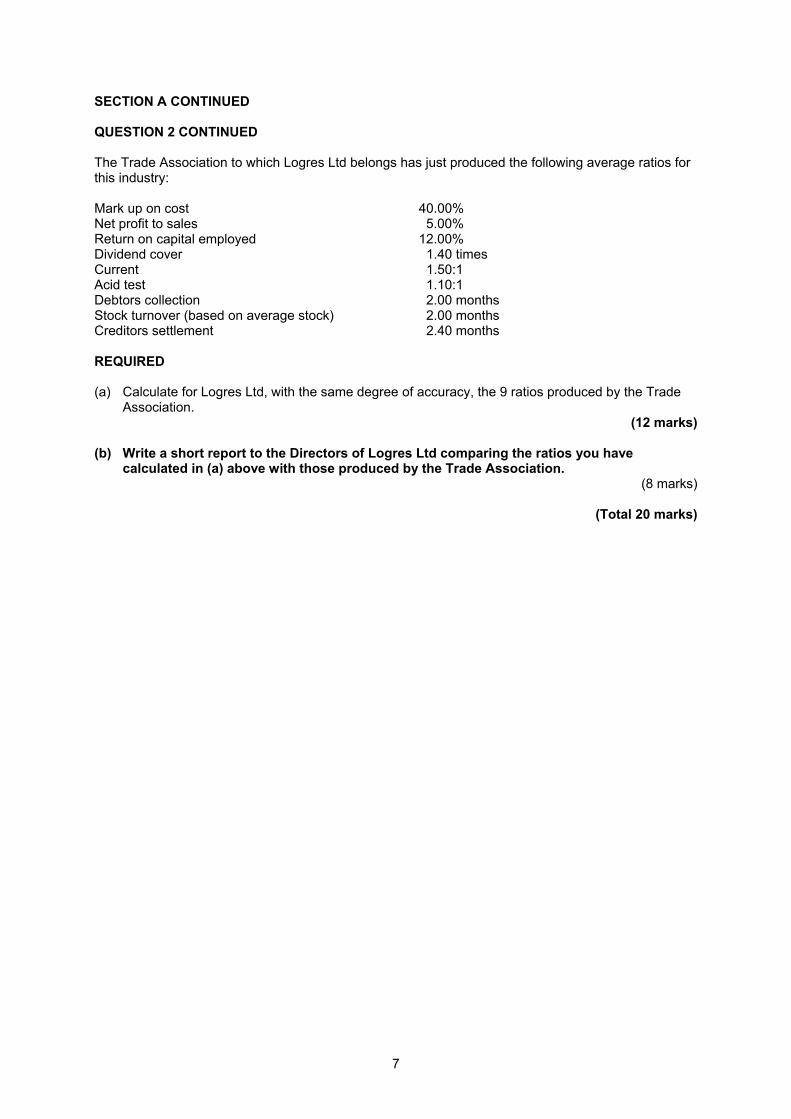

SECTION A CONTINUED QUESTION 2 CONTINUED The Trade Association to which Logres Ltd belongs has just produced the following average ratios for this industry: Mark up on cost 40.00% Net profit to sales 5.00% Return on capital employed 12.00% Dividend cover 1.40 times Current 1.50:1 Acid test 1.10:1 Debtors collection 2.00 months Stock turnover (based on average stock) 2.00 months Creditors settlement 2.40 months REQUIRED (a) Calculate for Logres Ltd, with the same degree of accuracy, the 9 ratios produced by the Trade

Association. (12 marks)

(b) Write a short report to the Directors of Logres Ltd comparing the ratios you have

calculated in (a) above with those produced by the Trade Association. (8 marks)

(Total 20 marks)

8

Model Answer for Question 2 (a) Logres Ltd Trade Association Mark up on cost [(410/670) x 100] 61.19% 40.00% Net profit to sales [(43/1,080) x 100)] 3.98% 5.00% Return on capital employed [(43/280) x 100)] 15.36% 12.00% Dividend cover (43/75) 0.57 times 1.40 times Current (175/250) 0.70:1 1.50:1 Acid test (90/250) 0.36:1 1.10:1 Debtors collection [(90/1,080) x 12)] 1.00 month 2.00 months Stock turnover [((65 + 85)/2)/670) x 12] 1.34 months 2.00 months Creditors settlement [(60/690) x 12)] 1.04 months 2.40 months (b) REPORT To: Directors From: A Candidate Date: 11 April 2005 Subject: Ratios Logres Ltd has a higher mark up and manages a faster stock turnover which suggests superior quality.

The lower net profit to sales suggests high expenses (possibly spending above average on advertising).

The net profit to capital employed is above average probably due to the high mark up combined

with efficient use of capital shown by better than average stock turnover ratio.

Both current and acid test ratios suggest a serious liquidity problem. The liquidity problem calls into question the size of the dividend which is not covered by the current profits.

The liquidity problem also suggests it may not be necessary to pay creditors faster than average for the industry.

9

SECTION B (Answer any THREE questions from Section B)

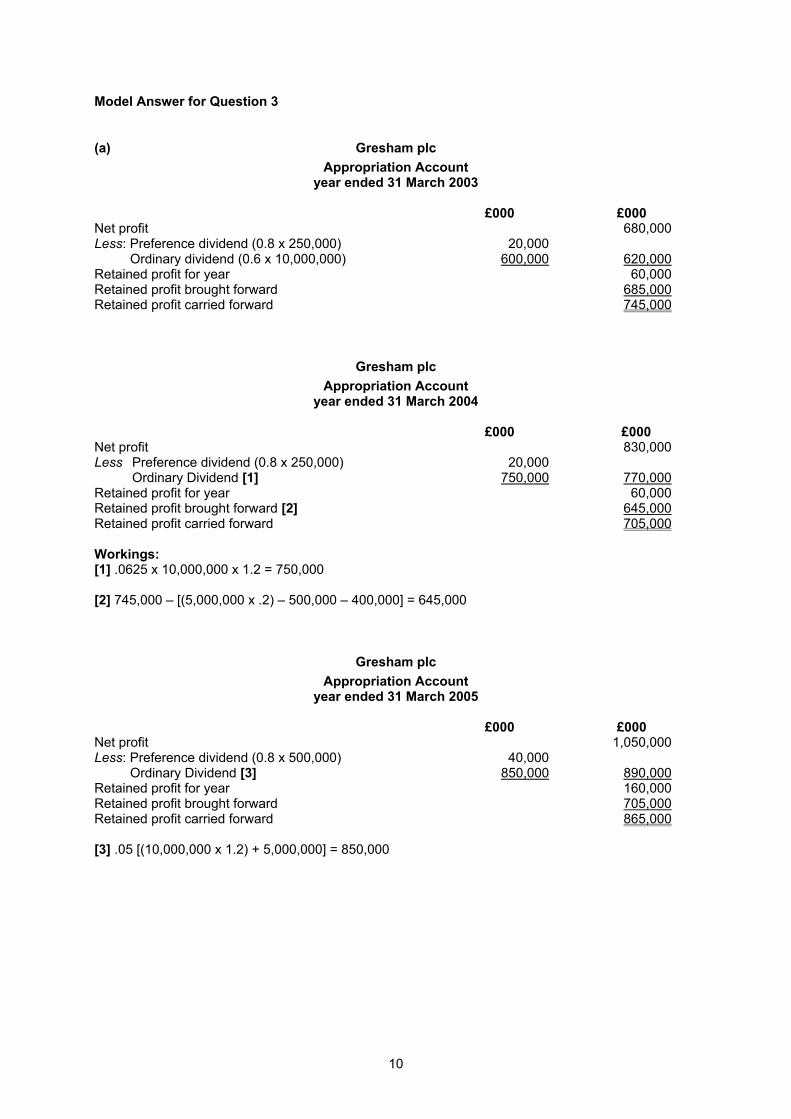

QUESTION 3 The following information appeared in Gresham plc's Balance Sheet at 31 March 2002:

Authorised capital £000 20,000,000 Ordinary shares of £0.50 each 10,000 500,000 8% Preference shares of £1 each 500 10,500 Issued capital and reserves £000 10,000,000 Ordinary shares of £0.50 each 5,000 250,000 8% Preference shares of £1 each 250 Share premium 500 Retained earnings 685 6,435 (1) For the year ended 31 March 2003 Gresham plc made a net profit of £680,000 and an ordinary

share dividend of £0.06 per share was approved. (2) On 1 September 2003 the company's buildings were re-valued and a revaluation reserve of

£400,000 was created. (3) On 1 October 2003 a bonus (capitalisation) issue of 1 ordinary share for every five held was

made. Maximum use was made of non-distributable reserves. (4) For the year ended 31 March 2004 Gresham plc made a net profit of £830,000. An Ordinary

dividend of £0.0625 per share was approved. (5) On 1 April 2004 the remaining Preference shares were issued at par. (6) On 1 October 2004 five million Ordinary shares were issued at a premium of £0.25 per share. (7) For the year ended 31 March 2005 Gresham plc made a net profit of £1,050,000. An Ordinary

dividend of £0.05 per share was approved.

REQUIRED (a) Prepare for Gresham plc the Appropriation account for each of the years ended 31 March 2003, 2004 and 2005.

(13 marks) (b) Show the Issued Capital and Reserves section of Gresham plc's Balance Sheet at 31 March 2005.

(7 marks)

(Total 20 marks)

10

Model Answer for Question 3

(a) Gresham plc Appropriation Account

year ended 31 March 2003 £000 £000 Net profit 680,000 Less: Preference dividend (0.8 x 250,000) 20,000 Ordinary dividend (0.6 x 10,000,000) 600,000 620,000 Retained profit for year 60,000 Retained profit brought forward 685,000 Retained profit carried forward 745,000

Gresham plc Appropriation Account

year ended 31 March 2004 £000 £000 Net profit 830,000 Less Preference dividend (0.8 x 250,000) 20,000 Ordinary Dividend [1] 750,000 770,000 Retained profit for year 60,000 Retained profit brought forward [2] 645,000 Retained profit carried forward 705,000 Workings: [1] .0625 x 10,000,000 x 1.2 = 750,000 [2] 745,000 – [(5,000,000 x .2) – 500,000 – 400,000] = 645,000

Gresham plc Appropriation Account

year ended 31 March 2005 £000 £000 Net profit 1,050,000 Less: Preference dividend (0.8 x 500,000) 40,000 Ordinary Dividend [3] 850,000 890,000 Retained profit for year 160,000 Retained profit brought forward 705,000 Retained profit carried forward 865,000 [3] .05 [(10,000,000 x 1.2) + 5,000,000] = 850,000

11

Model Answer for Question 3 continued

(b) Gresham plc

Balance Sheet at 31 March 2005

Capital and Reserves £000

17,000,000 Ordinary shares of £0.50 each 8,500 500,000 8% Preference shares of £1 each 500 Share premium (5,000,000 x .25) 1,250 Retained earnings 865 11,115

12

SECTION B CONTINUED QUESTION 4 Mirabelle does not use control accounts. At the most recent year end the Trial Balance did not balance as the credit total exceeded the debit total by £541. A Suspense Account was opened and this balance was treated as a current asset when the draft accounts were prepared. The accounts showed a gross profit of £42,350 and a net profit of £13,400. The accountant has now found the following errors: (1) A sales return of £60 had been credited to the customer's account and credited to Sales Returns

Account. (2) Postage expenses of £87 had been correctly entered in the Bank Account but entered as £78 in

the Postage Expenses Account. (3) A customer, Jones, owing £240, had paid his account less 5% cash discount. Jones' account

had been credited with £228, but no entry had been made in the Bank Account and the discount remained unrecorded.

(4) £8,400, including £150 for the licence and £350 for insurance, was paid to the supplier of a new vehicle. The Motor Vehicles Account had been debited with £8,400 and the Bank Account credited with £8,400. A full year’s depreciation of 25% has been charged on the cost of all vehicles.

(5) The Petty Cash Account had been omitted from the Trial Balance. When all the above errors had been corrected the Suspense Account was eliminated. REQUIRED (a) Show the Suspense Account of Mirabelle.

(8 marks) (b) Show calculations of the revised: (i) Gross profit

(ii) Net profit. (12 marks)

(Total 20 marks)

13

Model Answer for Question 4 (a) Suspense Account £ £ Balance per Trial Balance 541 Sales returns (60 x 2) 120 Postage (87 – 78) 9 Bank 228 541 Petty cash (R) 184 541

Must include narratives (b) (i) £ Gross profit as per accounts 42,350 Less sales returns (60 x 2) 120 Revised gross profit 42,230 (ii) £ £ Net profit as per accounts 13,400 Sales returns (120) Postage ( 9) Discount allowed (240 – 228) ( 12) Licences (150) Insurance (350) Depreciation [(150 + 350) x 0.25] 125 (516) Revised net profit 12,884

14

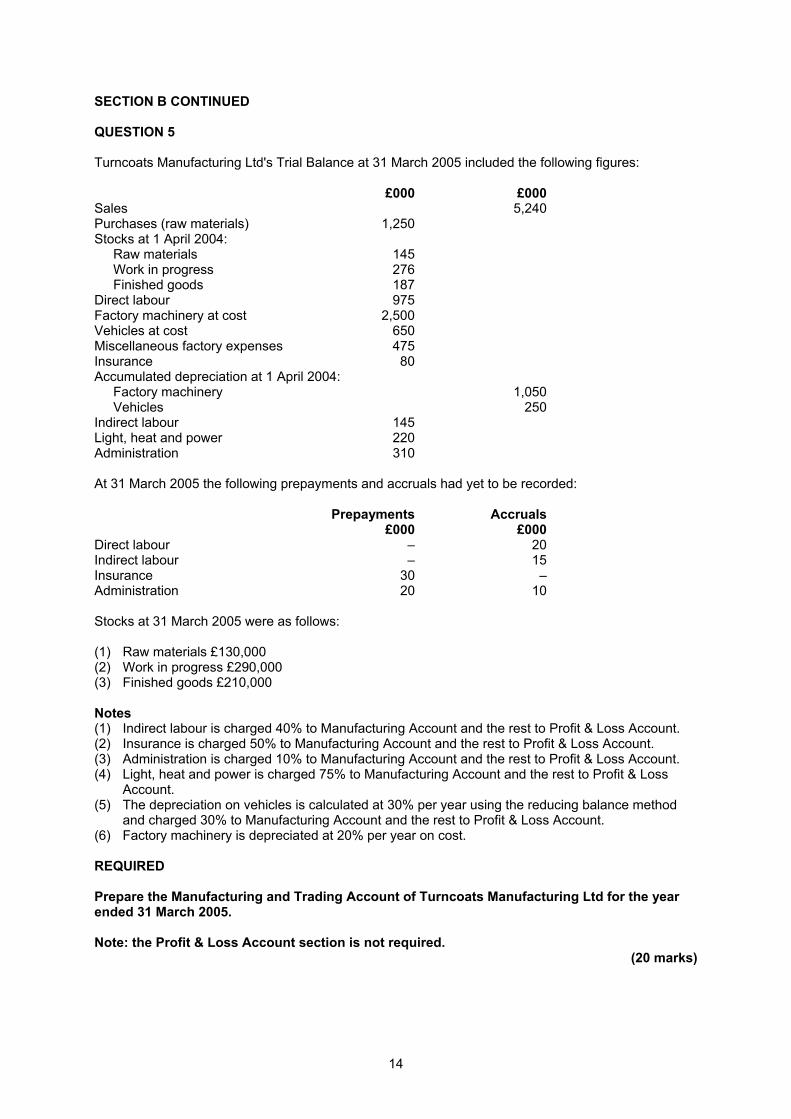

SECTION B CONTINUED QUESTION 5 Turncoats Manufacturing Ltd's Trial Balance at 31 March 2005 included the following figures: £000 £000 Sales 5,240 Purchases (raw materials) 1,250 Stocks at 1 April 2004: Raw materials 145 Work in progress 276 Finished goods 187 Direct labour 975 Factory machinery at cost 2,500 Vehicles at cost 650 Miscellaneous factory expenses 475 Insurance 80 Accumulated depreciation at 1 April 2004: Factory machinery 1,050 Vehicles 250 Indirect labour 145 Light, heat and power 220 Administration 310 At 31 March 2005 the following prepayments and accruals had yet to be recorded: Prepayments Accruals £000 £000 Direct labour – 20 Indirect labour – 15 Insurance 30 – Administration 20 10 Stocks at 31 March 2005 were as follows: (1) Raw materials £130,000 (2) Work in progress £290,000 (3) Finished goods £210,000 Notes (1) Indirect labour is charged 40% to Manufacturing Account and the rest to Profit & Loss Account. (2) Insurance is charged 50% to Manufacturing Account and the rest to Profit & Loss Account. (3) Administration is charged 10% to Manufacturing Account and the rest to Profit & Loss Account. (4) Light, heat and power is charged 75% to Manufacturing Account and the rest to Profit & Loss Account. (5) The depreciation on vehicles is calculated at 30% per year using the reducing balance method

and charged 30% to Manufacturing Account and the rest to Profit & Loss Account. (6) Factory machinery is depreciated at 20% per year on cost. REQUIRED Prepare the Manufacturing and Trading Account of Turncoats Manufacturing Ltd for the year ended 31 March 2005. Note: the Profit & Loss Account section is not required.

(20 marks)

15

Model Answer for Question 5

Turncoats Manufacturing Ltd Manufacturing Account and Trading Account

for the year ended 31 March 2005 £000 £000 Raw materials: Opening stock 145 Purchases 1,250 1,395 Closing stock 130 1,265 Direct labour (975 + 20) 995 Prime Cost 2,260 Miscellaneous factory expenses 475 Insurance [(80 – 30) x 0.5] 25 Indirect labour [(145 + 15) x 0.4] 64 Light, heat and power (220 x 0.75) 165 Administration [(310 + 10 – 20) x 0.1] 30 Depreciation: Factory machinery (2,500 x 0.2) 500 Vehicles [(650 – 250) x 0.3) x 0.3] 36 1,295

3,555 Opening work in progress 276 3,831 Closing work in progress 290 Cost of Manufacture 3,541 £000 £000 Sales 5,240 Cost of goods sold: Opening stock 187 Cost of manufacture 3,541 3,728 Closing stock 210 3,518 Gross Profit 1,722

16

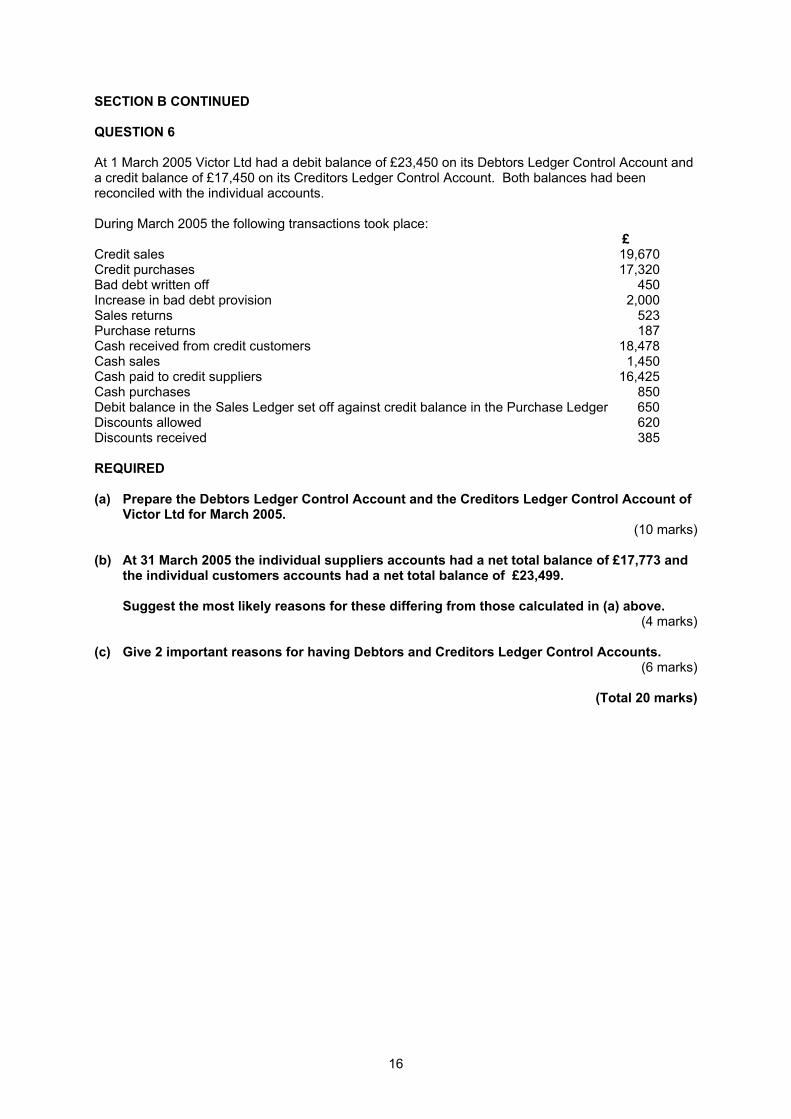

SECTION B CONTINUED QUESTION 6 At 1 March 2005 Victor Ltd had a debit balance of £23,450 on its Debtors Ledger Control Account and a credit balance of £17,450 on its Creditors Ledger Control Account. Both balances had been reconciled with the individual accounts. During March 2005 the following transactions took place: £ Credit sales 19,670 Credit purchases 17,320 Bad debt written off 450 Increase in bad debt provision 2,000 Sales returns 523 Purchase returns 187 Cash received from credit customers 18,478 Cash sales 1,450 Cash paid to credit suppliers 16,425 Cash purchases 850 Debit balance in the Sales Ledger set off against credit balance in the Purchase Ledger 650 Discounts allowed 620 Discounts received 385 REQUIRED (a) Prepare the Debtors Ledger Control Account and the Creditors Ledger Control Account of

Victor Ltd for March 2005. (10 marks)

(b) At 31 March 2005 the individual suppliers accounts had a net total balance of £17,773 and

the individual customers accounts had a net total balance of £23,499. Suggest the most likely reasons for these differing from those calculated in (a) above.

(4 marks) (c) Give 2 important reasons for having Debtors and Creditors Ledger Control Accounts.

(6 marks)

(Total 20 marks)

17

Model Answer for Question 6 (a) Debtors Control Account £ £ Opening balance 23,450 Bad debts 450 Credit sales 19,670 Sales returns 523 Cash received 18,478 Contra 650 Discounts allowed 620 Closing balance (R) 22,399 43,120 43,120

Creditors Control Account £ £ Purchase returns 187 Opening balance 17,450 Cash paid 16,425 Credit purchases 17,320 Contra 650 Discounts received 385 Closing balance (R) 17,123 34,770 34,770 NO marks for closing figures if aliens included (b) £ £ Individual debtors 23,499 Individual creditors 17,773 Debtors Control Account 22,399 Creditors Control Account 17,123 1,100 650

Excess of individual balances suggests that the contra item has not been recorded in the individual accounts. This would reconcile the creditors. The bad debt may not have been recorded in the individual account. This with the contra reconciles the debtors (650 + 450 = £1,100).

(c) Prevention of fraud, location of errors, control of total credit, preparation of interim accounts.

18

Related Documents