Accounting Rules to Accounting Rules to Remember Remember Georgia CTAE Resource Network Georgia CTAE Resource Network Instructional Resources Office Instructional Resources Office Written by: Dr. Marilynn K. Skinner Written by: Dr. Marilynn K. Skinner May 2009 May 2009

Accounting Rules to Remember Georgia CTAE Resource Network Instructional Resources Office Written by: Dr. Marilynn K. Skinner May 2009.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Rules to Accounting Rules to RememberRemember

Georgia CTAE Resource NetworkGeorgia CTAE Resource Network

Instructional Resources OfficeInstructional Resources Office

Written by: Dr. Marilynn K. SkinnerWritten by: Dr. Marilynn K. Skinner

May 2009May 2009

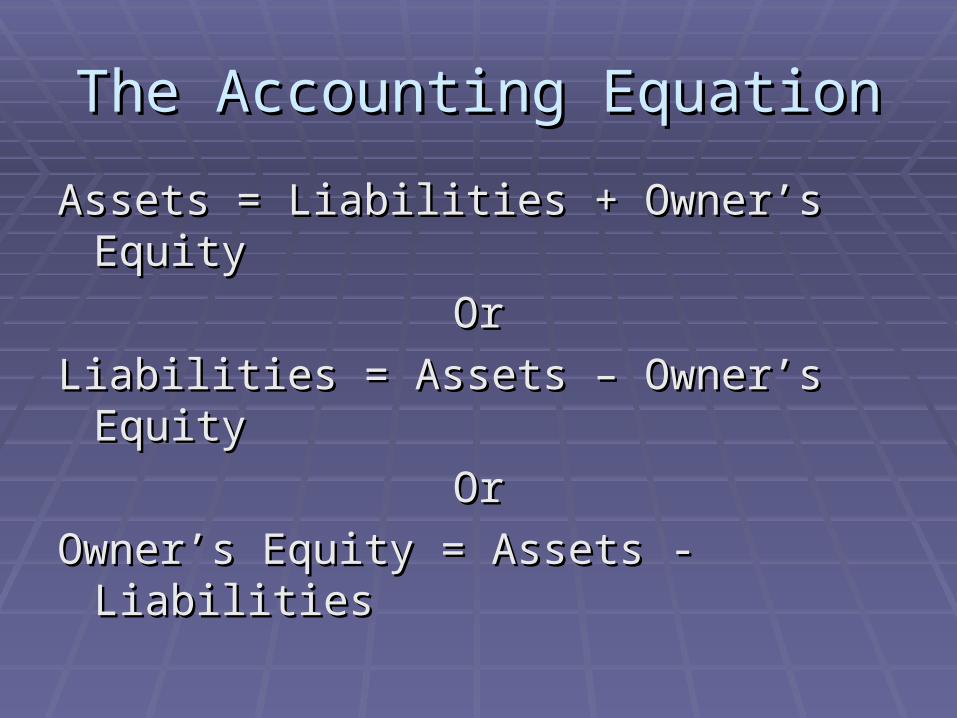

The Accounting EquationThe Accounting Equation

Assets = Liabilities + Owner’s EquityAssets = Liabilities + Owner’s Equity

OrOr

Liabilities = Assets – Owner’s EquityLiabilities = Assets – Owner’s Equity

OrOr

Owner’s Equity = Assets - LiabilitiesOwner’s Equity = Assets - Liabilities

Debits and CreditsDebits and Credits

In any transaction:In any transaction:

Debits = CreditsDebits = Credits

Account TypeAccount Type Increases withIncreases with Decreases withDecreases with

AssetAsset DebitDebit CreditCredit

LiabilityLiability CreditCredit DebitDebit

Owner’s CapitalOwner’s Capital CreditCredit DebitDebit

Owner’s DrawOwner’s Draw DebitDebit CreditCredit

RevenueRevenue CreditCredit DebitDebit

ExpensesExpenses Debit Debit CreditCredit

Steps in Analyzing a TransactionSteps in Analyzing a Transaction

1.1. Determine the accounts affectedDetermine the accounts affected

2.2. Will the accounts be increased or Will the accounts be increased or decreaseddecreased

3.3. Does the increase/decrease require a Does the increase/decrease require a debit or a creditdebit or a credit

4.4. Do debits = creditsDo debits = credits

ExampleExample

Quinn Corporation paid their April rent, Quinn Corporation paid their April rent, $1,450, to Thomas Real Estate$1,450, to Thomas Real Estate

1.1. What accounts would be affected?What accounts would be affected?

Rent Expense Rent Expense

CashCash

ExampleExample

Quinn Corporation paid their April rent, Quinn Corporation paid their April rent, $1,450, to Thomas Real Estate$1,450, to Thomas Real Estate

2. Will the accounts be increased or 2. Will the accounts be increased or decreased?decreased?

Rent Expense – IncreasedRent Expense – Increased

Cash - DecreasedCash - Decreased

ExampleExample

Quinn Corporation paid their April rent, Quinn Corporation paid their April rent, $1,450, to Thomas Real Estate$1,450, to Thomas Real Estate

3. Does the increase/decrease require a 3. Does the increase/decrease require a debit or a credit?debit or a credit?

Rent Expense Increases with a debitRent Expense Increases with a debit

Cash decreases with a creditCash decreases with a credit

ExampleExample

4. Do debits = credits4. Do debits = credits

General JournalGeneral Journal

DateDate DescriptionDescription DebitDebit CreditCredit

4/14/1 Rent ExpenseRent Expense 1,4501,450

CashCash 1,4501,450

April rent paymentApril rent payment

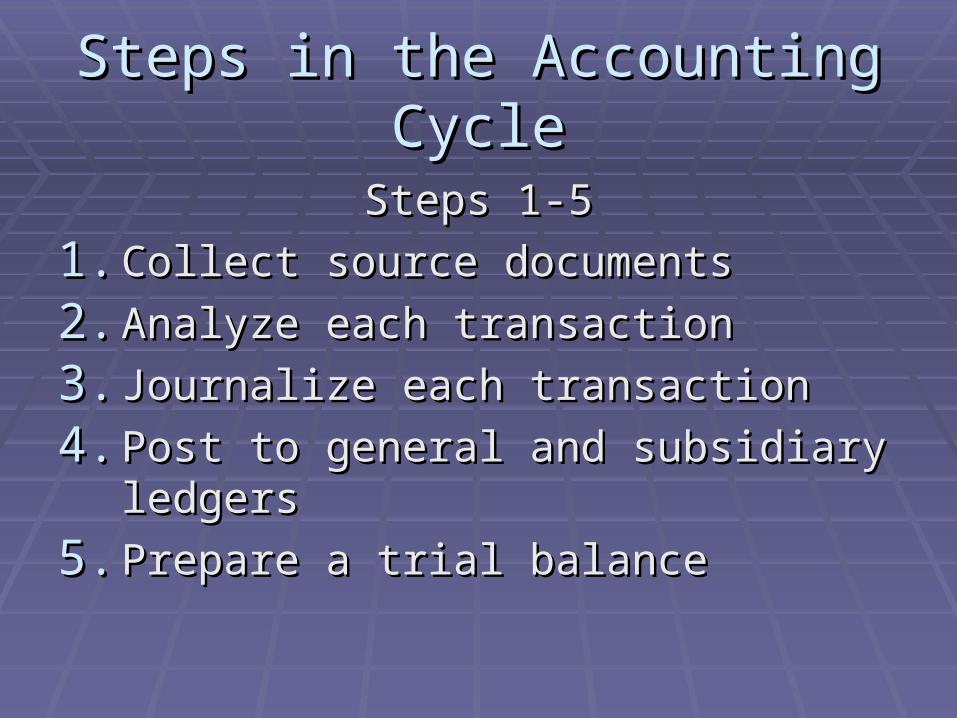

Steps in the Accounting CycleSteps in the Accounting Cycle

Steps 1-5Steps 1-5

1.1. Collect source documentsCollect source documents

2.2. Analyze each transactionAnalyze each transaction

3.3. Journalize each transactionJournalize each transaction

4.4. Post to general and subsidiary ledgersPost to general and subsidiary ledgers

5.5. Prepare a trial balancePrepare a trial balance

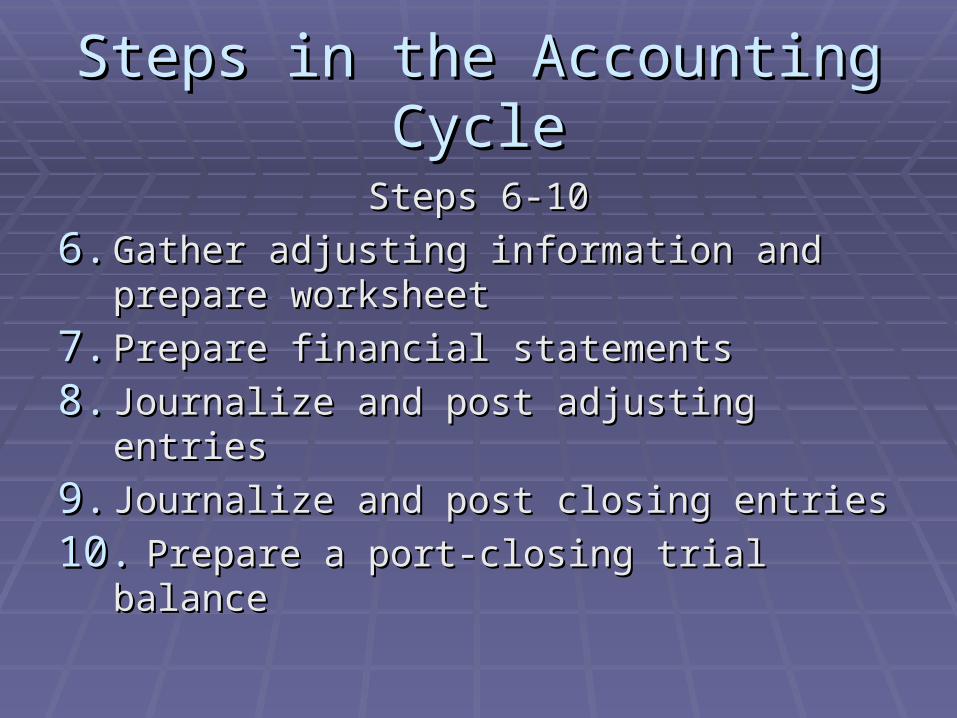

Steps in the Accounting CycleSteps in the Accounting Cycle

Steps 6-10Steps 6-10

6.6. Gather adjusting information and prepare Gather adjusting information and prepare worksheetworksheet

7.7. Prepare financial statementsPrepare financial statements

8.8. Journalize and post adjusting entriesJournalize and post adjusting entries

9.9. Journalize and post closing entriesJournalize and post closing entries

10.10. Prepare a port-closing trial balancePrepare a port-closing trial balance

Steps in the Closing ProcessSteps in the Closing Process

1.1. Close revenues to income summaryClose revenues to income summary

2.2. Close expenses to income summaryClose expenses to income summary

3.3. Close income summary to capitalClose income summary to capital

4.4. Close draw to capitalClose draw to capital

When your trial balance When your trial balance doesn’t balancedoesn’t balance

Try these steps –Try these steps –

1.1. Add your columns again from bottom to Add your columns again from bottom to top.top.

2.2. Calculate the difference in your columnsCalculate the difference in your columns

3.3. Divide your difference by 9, if it divides Divide your difference by 9, if it divides evenly, you have a transposition evenly, you have a transposition (entering 123 rather than 132) or a slide, (entering 123 rather than 132) or a slide, (entering 100 rather than 10)(entering 100 rather than 10)

When your trial balance When your trial balance doesn’t balancedoesn’t balance

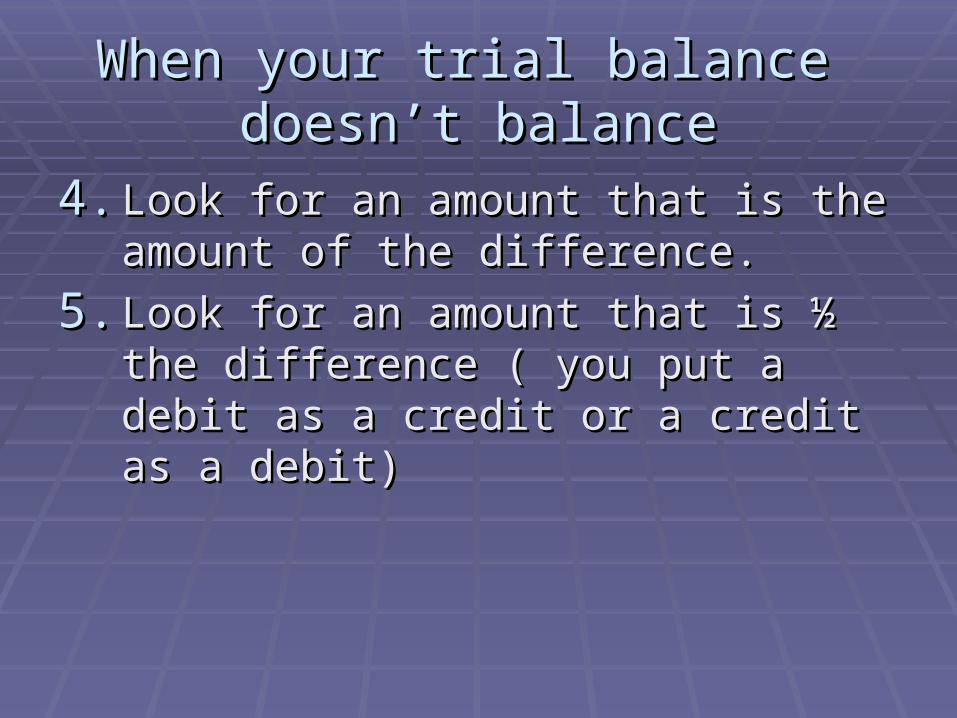

4.4. Look for an amount that is the amount of Look for an amount that is the amount of the difference.the difference.

5.5. Look for an amount that is ½ the Look for an amount that is ½ the difference ( you put a debit as a credit or difference ( you put a debit as a credit or a credit as a debit)a credit as a debit)

When your trial balance When your trial balance doesn’t balancedoesn’t balance

6.6. Check for the preceding amounts in this Check for the preceding amounts in this order:order:1.1. Check that you wrote down the totals from the Check that you wrote down the totals from the

ledger correctly on the trial balance, checking not ledger correctly on the trial balance, checking not only the amount but that debits are recorded as only the amount but that debits are recorded as debits and credits as credits.debits and credits as credits.

2.2. Retotal you ledger accountsRetotal you ledger accounts

3.3. Retotal your journalsRetotal your journals

4.4. Check journal entries against ledger postings.Check journal entries against ledger postings.

And other rulesAnd other rules

Assets when they are used up become expensesAssets when they are used up become expenses

The Balance Sheet contains only permanent The Balance Sheet contains only permanent accounts ( the balances never go to 0).accounts ( the balances never go to 0).

The Income Statement Contains only the The Income Statement Contains only the temporary accounts (balances are brought to 0 temporary accounts (balances are brought to 0 every month).every month).

Adjusting entries always affect both a balance Adjusting entries always affect both a balance sheet and an income statement accountsheet and an income statement account

And other rulesAnd other rules

Order of accounts in the general ledger:Order of accounts in the general ledger:AssetsAssetsLiabilitiesLiabilitiesOwner’s capitalOwner’s capitalOwner’s drawOwner’s drawRevenueRevenueExpensesExpensesThis is also the order of accounts in the trial This is also the order of accounts in the trial

balancebalance

Financial StatementsFinancial Statements

The Balance SheetThe Balance Sheet

Reflects the accounting equation by Reflects the accounting equation by proving that assets = liabilities + owner’s proving that assets = liabilities + owner’s equityequity

Dated for a specific dateDated for a specific date

Financial StatementsFinancial Statements

The income statement reflects the activities The income statement reflects the activities of the current accounting period.of the current accounting period.

Format:Format:

Revenues – Expenses = Net IncomeRevenues – Expenses = Net Income

Financial StatementsFinancial Statements

Statement of Owner’s EquityStatement of Owner’s Equity

Ties the Income Statement and Balance Ties the Income Statement and Balance Sheet together by showing the effect of Sheet together by showing the effect of the period activity on the balance sheet.the period activity on the balance sheet.

Beginning Owner’s Equity + Net Income Beginning Owner’s Equity + Net Income (Loss) = Ending Owner’s Equity(Loss) = Ending Owner’s Equity

From Income Statement

To Balance Sheet

Related Documents