Accounting Practices 501 Chapter 8 Balance Day Adjustments (Allowance for Doubtful Debts) Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

Accounting Practices 501 Chapter 8 Balance Day Adjustments (Allowance for Doubtful Debts) Cathy Saenger, Senior Lecturer, Eastern Institute of Technology.

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Practices 501

Chapter 8

Balance Day Adjustments

(Allowance for Doubtful Debts)

Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

Allowance for Doubtful Debts

Ch8E - Doubtful debts 2

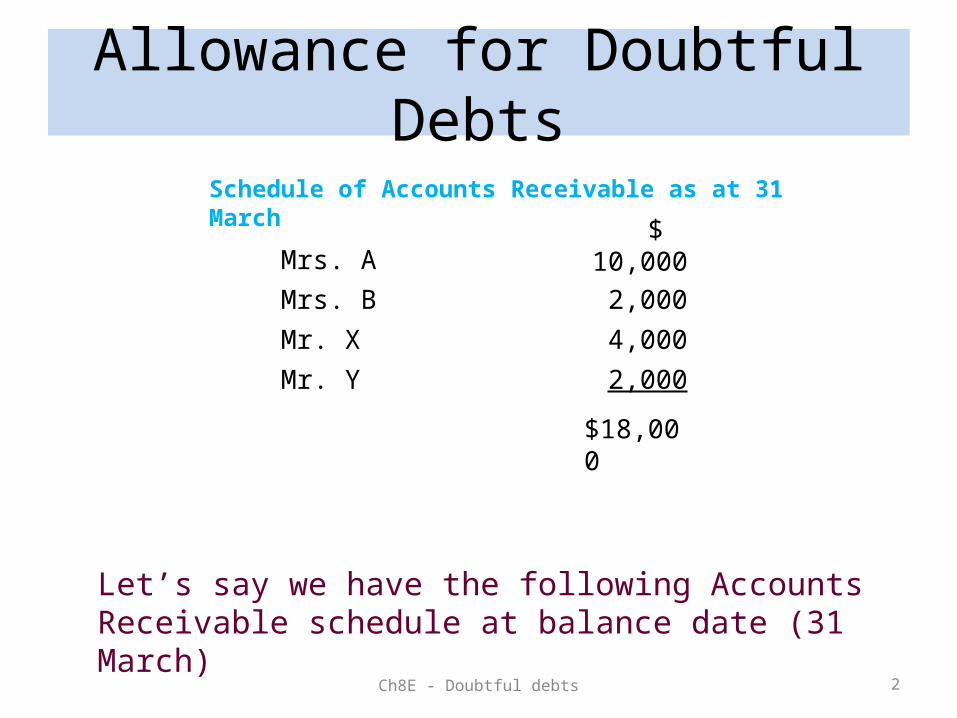

Let’s say we have the following Accounts Receivable schedule at balance date (31 March)

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Allowance for Doubtful Debts

Ch8E - Doubtful debts 3

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The outstanding $18,000 will only be received in the next accounting period

Allowance for Doubtful Debts

Ch8E - Doubtful debts 4

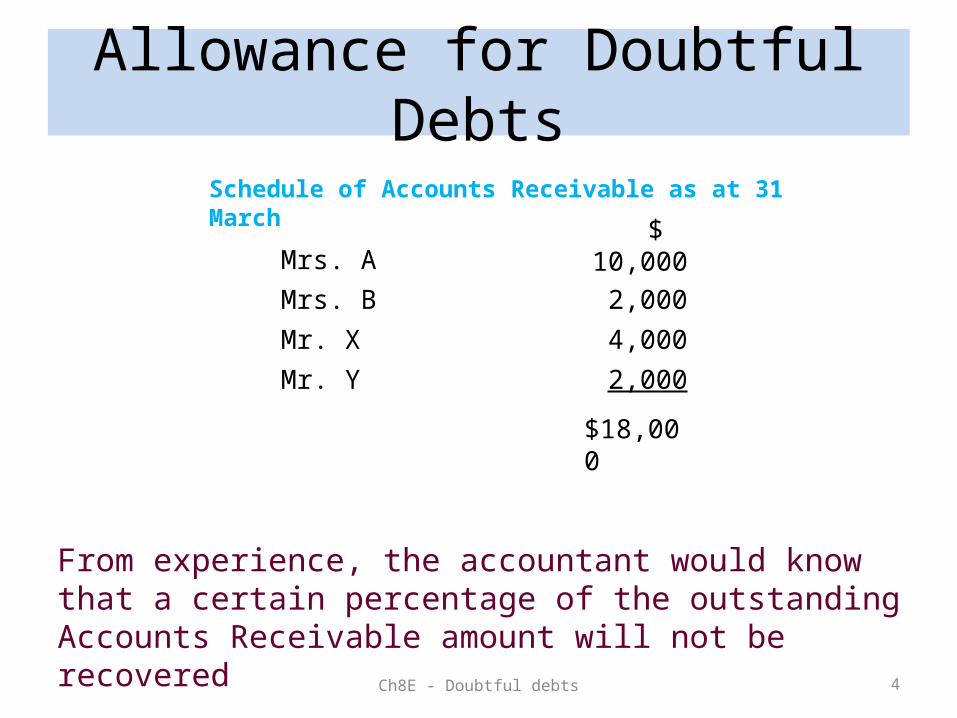

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

From experience, the accountant would know that a certain percentage of the outstanding Accounts Receivable amount will not be recovered

Allowance for Doubtful Debts

Ch8E - Doubtful debts 5

Schedule of Accounts Receivable as at 31 March

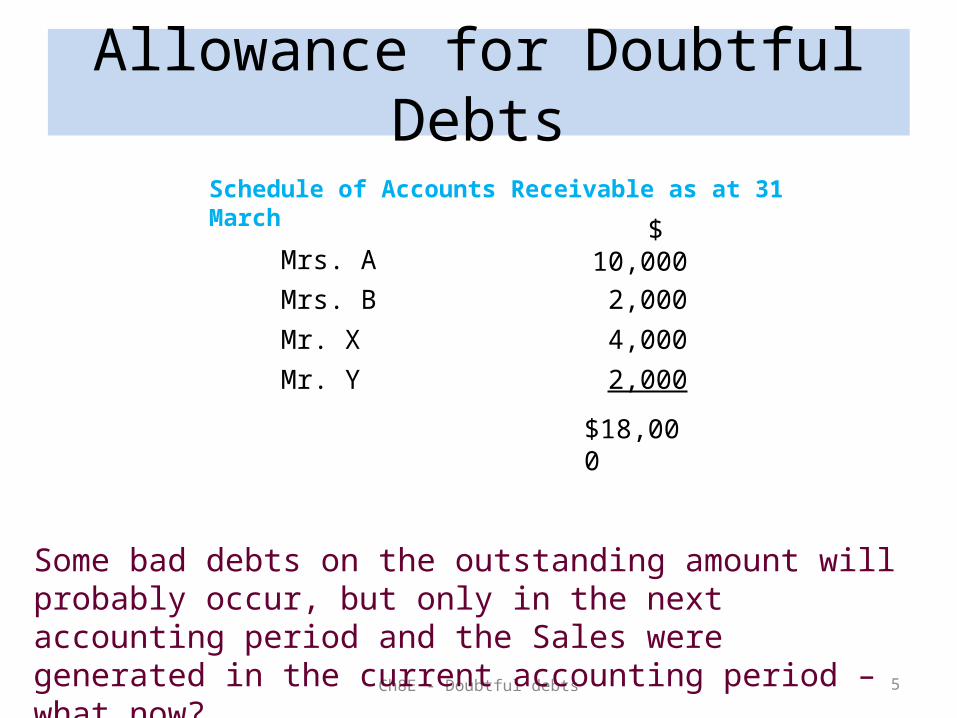

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Some bad debts on the outstanding amount will probably occur, but only in the next accounting period and the Sales were generated in the current accounting period – what now?

Ch8E - Doubtful debts 6

This is what happens ……..

interesting stuff!!

Allowance for Doubtful Debts

Allowance for Doubtful Debts

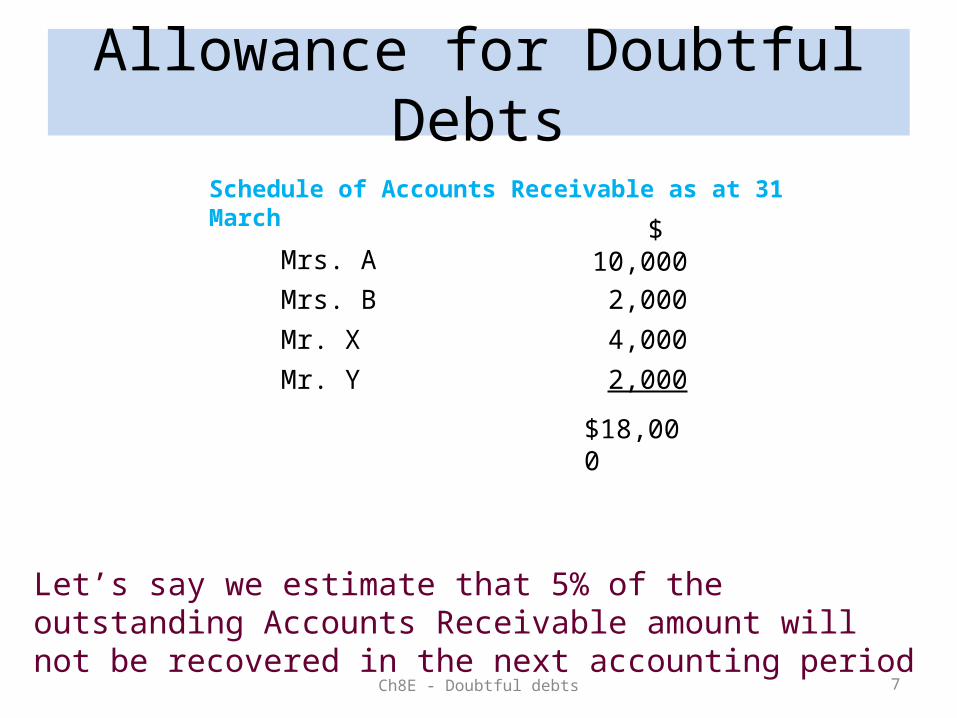

Ch8E - Doubtful debts 7

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

Let’s say we estimate that 5% of the outstanding Accounts Receivable amount will not be recovered in the next accounting period

Allowance for Doubtful Debts

Ch8E - Doubtful debts 8

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

We then need to push the Accounts Receivable amount down by 5% ($900) to provide a more realistic value

Allowance for Doubtful Debts

Ch8E - Doubtful debts 9

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The question is - which account will we write the $900 off from?

?

Don’t know!

- 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 10

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

The solution is to create an account called Allowance for Doubtful Debts which will be used to push down the total of Accounts Receivable in the Balance Sheet to show a more realistic figure

?- 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 11

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

?- 900

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

Allowance for Doubtful Debts

Ch8E - Doubtful debts 12

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

The Allowance for Doubtful Debts account is a negative asset (used to push down Acc Rec) and is therefore credited

The million dollar question – what will it balance with?

Allowance for Doubtful Debts

Ch8E - Doubtful debts 13

General JournalDate

Account Titles

Ref no Debit Credit31/3

Allowance for Doubtful Debts 900

A Doubtful Debts expense account is created to balance the amount

Doubtful Debts expense 900

Being entry to create an allowance for doubtful debts (5% of Acc Rec)

The Doubtful Debts expense account will in turn push down the profit to show a more realistic profit

Allowance for Doubtful Debts

Ch8E - Doubtful debts 14

Schedule of Accounts Receivable as at 31 March

10,0002,000

4,000

2,000

$18,000

Mrs. A

Mrs. B

Mr. X

Mr. Y

$

General JournalDate

Account Titles

Ref no Debit Credit31/3 Doubtful Debts expense 900

Allowance for Doubtful Debts 900

Being entry to create an allowance for doubtful debts (5% of Acc Rec)

Ch8E - Doubtful debts 15

The Doubtful Debts Expense will be classified as a Finance Expense in the Income Statement

The Allowance for Doubtful Debts account is classified as a Current Asset (negative) in the Balance Sheet

This means that the Profit will decrease and the Current Assets will decrease, which gives a truer picture of the financial position and performance of the business

Let’s look at the financial statements

Week 7 (E) - Doubtful Debts 16

……….

Less Expenses

Finance Expenses

Doubtful Debts $900

……….

Current Assets

Accounts Receivable $18,000Less Allowance for Doubtful Debts 900 17,100

Extract from the Income Statement for the year ended ……..

Extract from the Balance Sheet as at …

Related Documents