Accounting Policies & Procedures 2013-2014 Prepared by the Accounting Department

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Policies & Procedures 2013-2014

Prepared by the Accounting Department

UNITED INDEPENDENT SCHOOL DISTRICT ACCOUNTING POLICIES & PROCEDURES

TABLE OF CONTENTS

Introduction ............................................................................................................................................. 1 Organizational Chart ............................................................................................................................... 4 Personnel Listing .................................................................................................................................... 5 UISD Calendar ........................................................................................................................................ 6 SECTION 1 – CASH MANAGEMENT AND INESTMENT

Cash Practices .................................................................................................................................... 9 Depository Bid ................................................................................................................................... 9 Reconciliations .................................................................................................................................. 9 Courier Process .................................................................................................................................. 9 CDA Legal Requirements .................................................................................................................. 10 CDA Local Requirements .................................................................................................................. 21 Investment Strategy Statement .......................................................................................................... 25 Investment Strategy by Fund ............................................................................................................. 26 Internal Control Structure .................................................................................................................. 29

SECTION 2 – ACCOUNTS PAYABLE

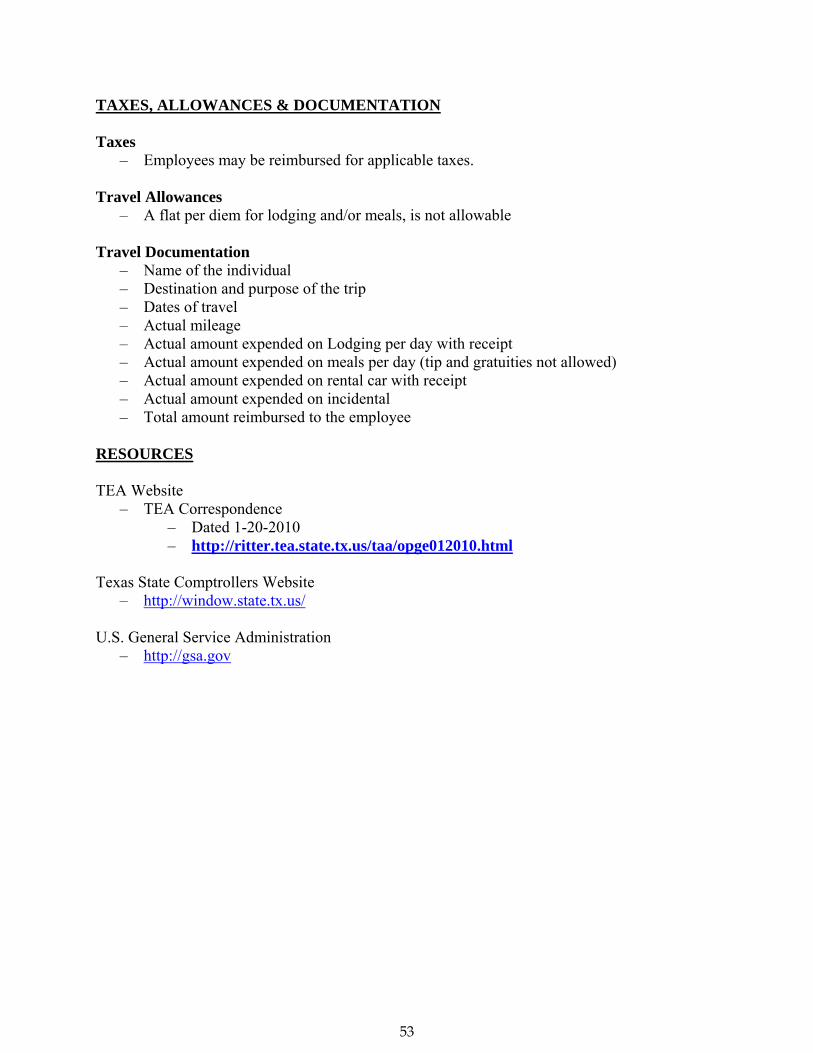

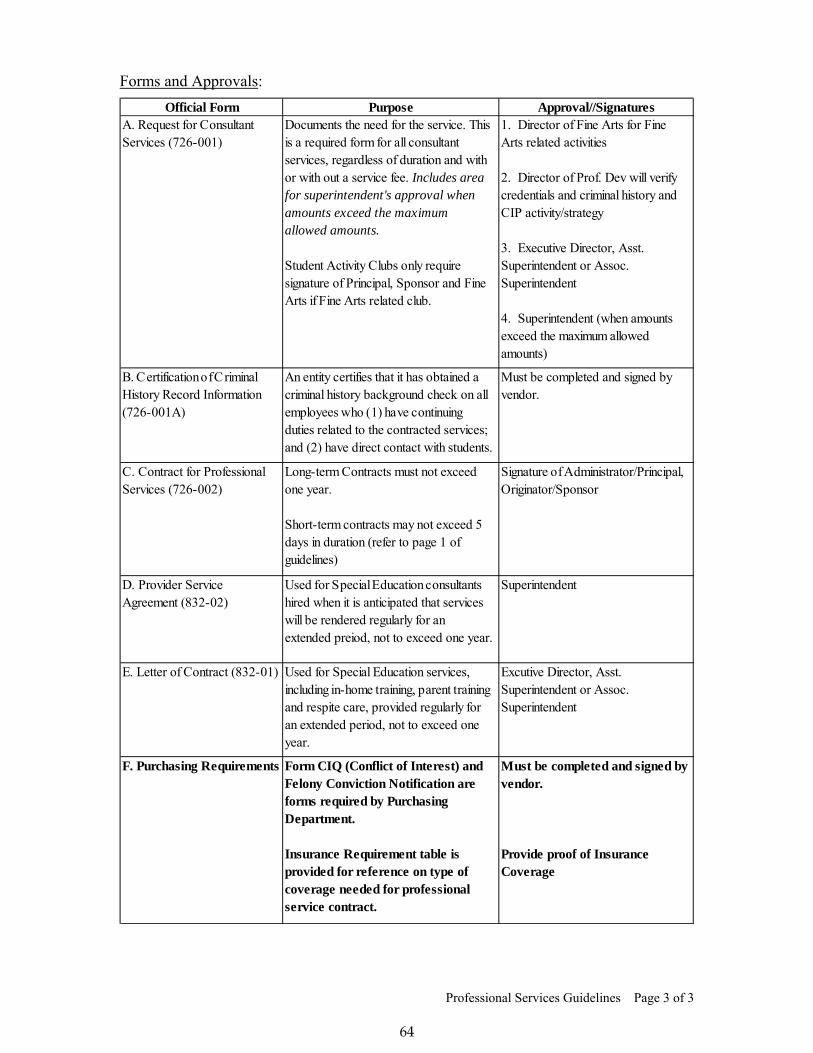

Objective ............................................................................................................................................ 33 Staff ................................................................................................................................................... 33 Staff Responsibilities ......................................................................................................................... 35 Batch A/P Checks .............................................................................................................................. 37 Monthly Disbursements Report ......................................................................................................... 40 Received Ordered Materials Report .................................................................................................. 42 Void a Check ..................................................................................................................................... 45 Purchase Order Report ....................................................................................................................... 47 Travel Guidelines ............................................................................................................................... 48 Travel Voucher .................................................................................................................................. 54 Travel Settlement Voucher ................................................................................................................ 56 Monthly Travel Report Instruction .................................................................................................... 59 Monthly Travel Report ...................................................................................................................... 60 Mileage Record .................................................................................................................................. 61 Professional Service Guidelines ........................................................................................................ 62 Professional Service Forms ............................................................................................................... 65

SECTION 3 - PAYROLL Objective ............................................................................................................................................ 79 Staff ................................................................................................................................................... 79 Staff Responsibilities ......................................................................................................................... 79 Exceptions ......................................................................................................................................... 80 Teacher Retirement System ............................................................................................................... 80 Kronos ............................................................................................................................................... 81 Payroll Deduction Assistants ............................................................................................................. 81 Other Deductions ............................................................................................................................... 81 Deduction Premiums ......................................................................................................................... 81 Miscellaneous .................................................................................................................................... 81 Screens ............................................................................................................................................... 83

Biweekly Payroll Dates ..................................................................................................................... 98 Monthly Payroll Dates ....................................................................................................................... 99 Supplemental Duty Guidelines .......................................................................................................... 100 Forms ................................................................................................................................................. 102 Finance Plus Main Menus ................................................................................................................. 120 Overtime/Compensatory Procedures ................................................................................................. 134 Kronos Editing and Approval Procedures ......................................................................................... 140

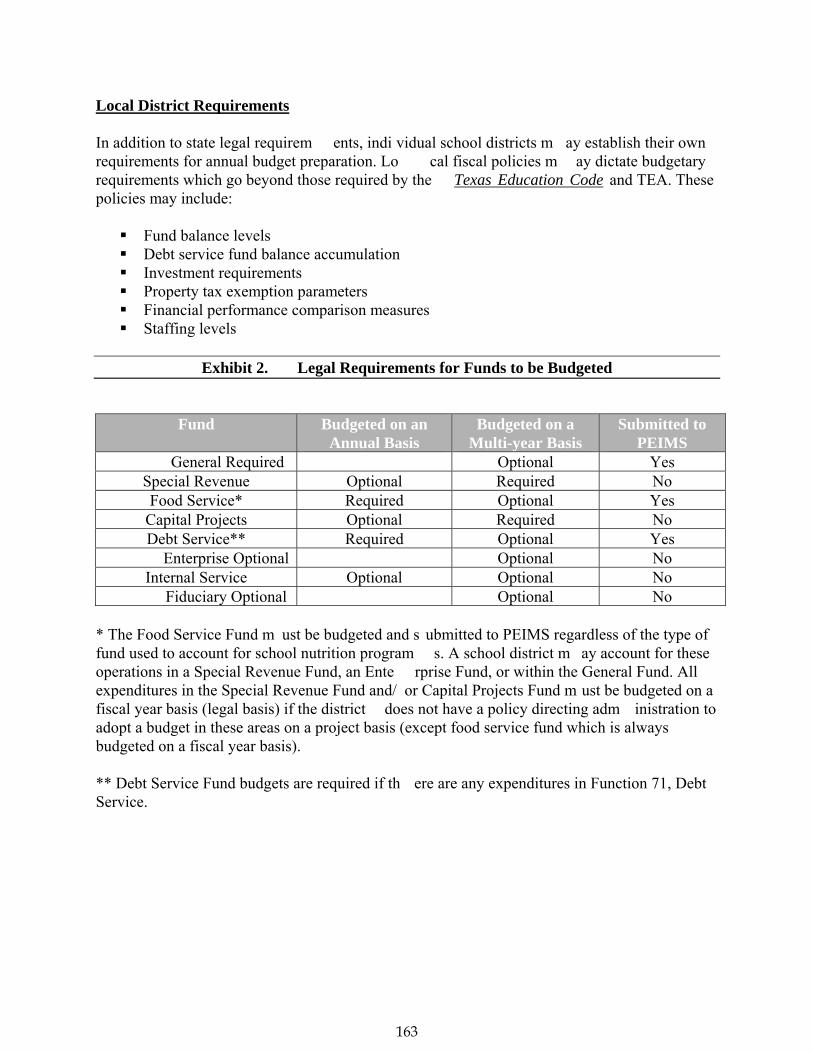

SECTION 4 - BUDGET Budget Process Mission Statement and Introduction ........................................................................ 155 Budget Development Process ............................................................................................................ 156 Budget Planning ................................................................................................................................. 156 Budget Explained ............................................................................................................................... 157 Development of a Campus Budget .................................................................................................... 158 Development of a Department Budget .............................................................................................. 159 Budget Worksheets/Forms Instructions ............................................................................................. 159 Legal Requirements ........................................................................................................................... 160 Statement of Texas Law .................................................................................................................... 161 TEA Legal Requirements .................................................................................................................. 162 Local District Requirements .............................................................................................................. 163 Budget Amendments & Transfers ..................................................................................................... 164 Printing of Budget Transfers.............................................................................................................. 168 Budget Amendment/Transfer Form ................................................................................................... 170

SECTION 5 - GRANTS Expenditure Report Guidelines .......................................................................................................... 173 Expenditure Analysis Report ............................................................................................................. 188 ARRA 1512 Quarterly Report Guidelines ......................................................................................... 189

SECTION 6 – STUDENT ACTIVITY Introduction........................................................................................................................................ 201 Policies and Procedures ..................................................................................................................... 206 Basic Records and Filing Guidelines ................................................................................................. 213 Bank Accounts ................................................................................................................................... 215 Payments from Student Activity and Campus Activity Funds .......................................................... 216 Receiving Cash .................................................................................................................................. 220 Documenting Fund Raisers ................................................................................................................ 228 Accounting Practices ......................................................................................................................... 233 Sales Tax ............................................................................................................................................ 235 Other Issues ....................................................................................................................................... 239

United Independent School District

Accounting Policies and Procedures

Introduction

Intro

ductio

n

1

2

Introduction The Accounting Department Manual for Financial Activities was written to provide guidance on the accuracy of completing and processing of required documentation (forms) for requested services. All UISD employees should become knowledgeable of the instructions and requirements in this manual. The Accounting Department would like to remind employees of the expectation of full compliance with Board Policy, state purchasing laws, and administrative regulations. There must be a clear understanding of the consequences for failure to follow such policies, laws, and regulations. Organizational Chart The following departments fall under the umbrella of the Accounting Department: Accounts Payable Budget Services Payroll Accounts Receivable Student Activities Attached is the organizational chart of the department. Employee Roster (Contact Personnel) A listing of employee telephone numbers and e-mail addresses are attached for each division of the Accounting Department.

3

AC

CO

UN

TIN

G D

EP

AR

TM

EN

TO

RG

AN

IZA

TIO

NA

L C

HA

RT

Asst. Sup

erintend

ent For Business &

Fina

nce

Laida P. Ben

avides

Accoun

ting Director

Samue

l D. Flores

Stud

ent A

ctivities

Manager

Felipe Jim

enez

Payroll M

anager

Marcos C

eballos

Budget M

anager

Belinda

E. Salazar

Accoun

ting Manager

Rosa I. Cabello

Activ

ity

Bookkeep

ers (4)

Jr. Accou

ntant (1)

Specialist (1)

Payroll A

ssistants

(5)

Budget

Accoun

tant (1)

Fede

ral Fun

ds Sr.

Accoun

tant (1)

Capital Projects

Accoun

tant (1)

Bookkeep

er (1

)

Specialist (1)

Assistant (1)

A/P Assistants (4)

4

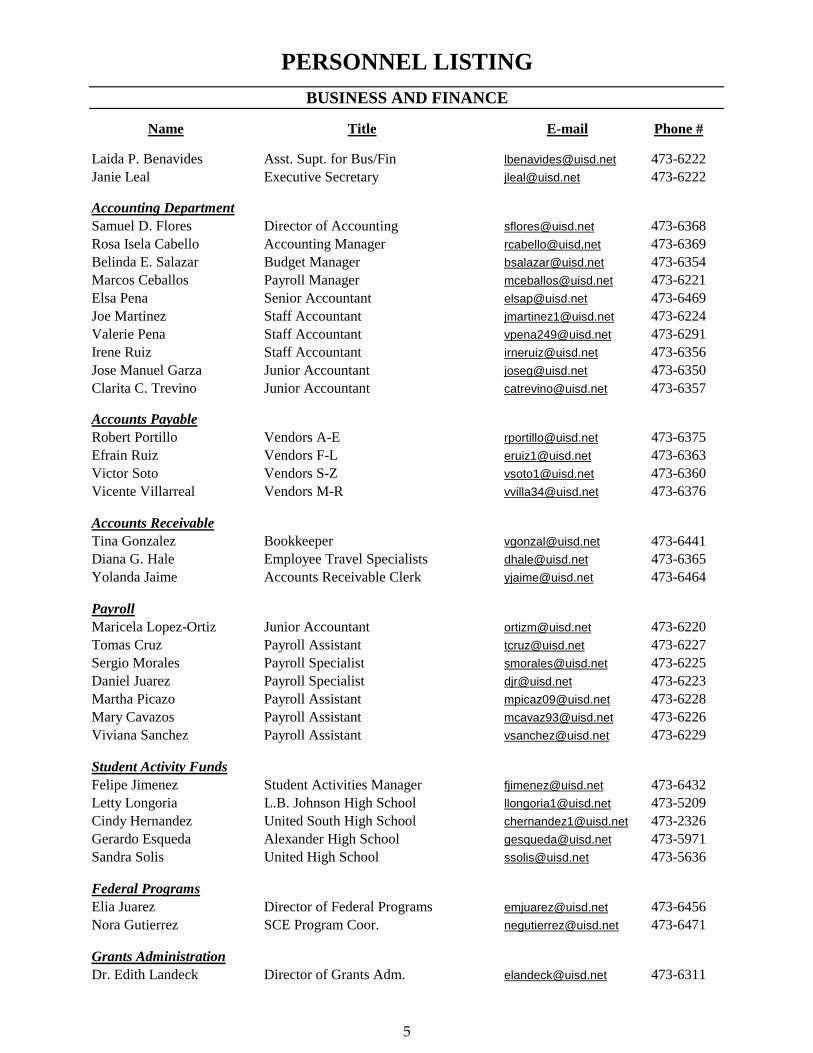

PERSONNEL LISTINGBUSINESS AND FINANCE

Name Title E-mail Phone #

Laida P. Benavides Asst. Supt. for Bus/Fin [email protected] 473-6222Janie Leal Executive Secretary [email protected] 473-6222

Accounting DepartmentSamuel D. Flores Director of Accounting [email protected] 473-6368Rosa Isela Cabello Accounting Manager [email protected] 473-6369Belinda E. Salazar Budget Manager [email protected] 473-6354Marcos Ceballos Payroll Manager [email protected] 473-6221Elsa Pena Senior Accountant [email protected] 473-6469Joe Martinez Staff Accountant [email protected] 473-6224Valerie Pena Staff Accountant [email protected] 473-6291Irene Ruiz Staff Accountant [email protected] 473-6356Jose Manuel Garza Junior Accountant [email protected] 473-6350Clarita C. Trevino Junior Accountant [email protected] 473-6357

Accounts PayableRobert Portillo Vendors A-E [email protected] 473-6375Efrain Ruiz Vendors F-L [email protected] 473-6363Victor Soto Vendors S-Z [email protected] 473-6360Vicente Villarreal Vendors M-R [email protected] 473-6376

Accounts ReceivableTi G l B kk l@ i d t 473 6441Tina Gonzalez Bookkeeper [email protected] 473-6441Diana G. Hale Employee Travel Specialists [email protected] 473-6365Yolanda Jaime Accounts Receivable Clerk [email protected] 473-6464

PayrollMaricela Lopez-Ortiz Junior Accountant [email protected] 473-6220Tomas Cruz Payroll Assistant [email protected] 473-6227Sergio Morales Payroll Specialist [email protected] 473-6225Daniel Juarez Payroll Specialist [email protected] 473-6223Martha Picazo Payroll Assistant [email protected] 473-6228Mary Cavazos Payroll Assistant [email protected] 473-6226Viviana Sanchez Payroll Assistant [email protected] 473-6229

Student Activity FundsFelipe Jimenez Student Activities Manager [email protected] 473-6432Letty Longoria L.B. Johnson High School [email protected] 473-5209Cindy Hernandez United South High School [email protected] 473-2326Gerardo Esqueda Alexander High School [email protected] 473-5971Sandra Solis United High School [email protected] 473-5636

Federal ProgramsElia Juarez Director of Federal Programs [email protected] 473-6456Nora Gutierrez SCE Program Coor. [email protected] 473-6471

Grants AdministrationDr. Edith Landeck Director of Grants Adm. [email protected] 473-6311

5

Scan

this

imag

e w

ith y

our s

mar

tpho

ne to

be

dire

cted

to th

e di

stric

t’s w

ebsi

te o

r vis

it w

ww.

uisd

.net

Aca

dem

ic C

alen

dar 2

013

- 201

4U

nite

d In

depe

nden

t Sch

ool D

istri

ctTA

KS/

STA

AR

Ass

essm

ent D

ates

Oct

. 21

TAKS

Exi

t Lev

el E

LA R

etes

tO

ct. 2

2 TA

KS E

xit L

evel

Mat

h R

etes

tO

ct. 2

3 TA

KS E

xit L

evel

Sci

ence

Ret

est

Oct

. 24

TAKS

Exi

t Lev

el S

ocia

l Stu

dies

Ret

est

Dec

. 2

STAA

R/E

OC

Eng

lish

I Writ

ing

Dec

. 3

STAA

R/E

OC

Eng

lish

I Rea

ding

Dec

. 4

STAA

R/E

OC

Eng

lish

II W

ritin

gD

ec. 5

ST

AAR

/EO

C E

nglis

h II

Rea

ding

Dec

. 10

STAA

R/E

OC

Alg

ebra

ID

ec. 1

1 ST

AAR

/EO

C B

iolo

gyD

ec. 1

2 ST

AAR

/EO

C U

.S. H

isto

ry

Mar

. 3

TAKS

Exi

t Lev

el E

LAM

ar. 4

TA

KS E

xit L

evel

Mat

hM

ar. 5

TA

KS E

xit L

evel

Sci

ence

Mar

. 6

TAKS

Exi

t Lev

el S

ocia

l Stu

dies

Mar

. 31

STAA

R/E

OC

Eng

lish

I

Apr.

1 ST

AAR

Gra

de 4

& 7

Writ

ing

Day

1Ap

r. 1

STAA

R G

rade

5 &

8 M

ath

ST

AAR

/EO

C E

nglis

h II

Apr.

2 ST

AAR

Gra

de 4

& 7

Writ

ing

Day

2

STAA

R G

rade

5 &

8 R

eadi

ngAp

r. 21

TA

KS E

xit L

evel

ELA

Apr.

22

STAA

R G

rade

3, 4

, 6 &

7 M

ath

TA

KS E

xit L

evel

Mat

h

STAA

R G

rade

8 S

ocia

l Stu

dies

Apr.

23

STAA

R G

rade

s 3,

4, 6

& 7

Rea

ding

ST

AAR

Gra

de 5

& 8

Sci

ence

TAKS

Exi

t Lev

el S

cien

ceAp

r. 24

TA

KS E

xit L

evel

Soc

ial S

tudi

es

May

5

STAA

R/E

OC

Alg

ebra

IM

ay 6

ST

AAR

/EO

C B

iolo

gyM

ay 6

ST

AAR

/EO

C U

.S. H

isto

ryM

ay 5

- 9

STAA

R A

sses

smen

t Win

dow

for:

Al

gebr

a I,

Biol

ogy,

U.S

.His

tory

May

13

STAA

R G

rade

5 &

8 M

ath

Ret

est

May

14

STAA

R G

rade

5 &

8 R

eadi

ng R

etes

t

June

24

STAA

R G

rade

5 &

8 M

ath

Ret

est

June

25

STAA

R G

rade

5 &

8 R

eadi

ng R

etes

t

Cal

enda

r app

rove

d by

Uni

ted

I.S.D

.B

oard

of T

rust

ees N

ovem

ber 2

8, 2

012.

Rev

ised

July

15,

201

3

n N

ew E

mpl

oyee

Orie

ntat

ion

n F

irst D

ay o

f Cla

ssn S

taff/

Stud

ent H

olid

ayn T

each

er W

ork-

day

n P

rofe

ssio

nal D

evel

opm

ent

n E

arly

Rel

ease

n E

arly

Rel

ease

Hig

h Sc

hool

n F

ood

of M

inim

al N

utrit

iona

l

Valu

e Ex

empt

Day

T In

clem

ent W

eath

er M

ake-

up D

ays

n T

AK

Sn S

TAA

R E

lem

enta

ry &

Mid

dle

n S

TAA

R H

igh

Scho

oln H

igh

Scho

ol G

radu

atio

ns

Frid

ay, J

une

6, 2

014

Uni

ted

H.S

. - 6

:30

P.M

.

Satu

rday

, Jun

e 7,

201

4

A

lexa

nder

H.S

. - 0

9:30

A.M

.

U

nite

d So

uth

H.S

. - 2

:00

P.M

.

Ly

ndon

B.J.

H.S

. - 6

:00

P.M

.

Impo

rtan

t Dat

esA

ug. 2

6 - F

irst D

ay o

f Cla

sses

Jan.

13

- Sta

rt of

Sec

ond

Sem

este

rJu

n. 5

- La

st D

ay o

f Cla

sses

/Ear

ly R

elea

se

Gra

ding

Per

iod

Six

Wee

ksA

ug. 2

6 - O

ct. 4

(29)

; Oct

. 7 -

Nov

. 15

(29)

;N

ov. 1

8 - J

an. 1

7 (2

9); J

an. 2

1 - F

eb. 2

8 (2

7);

Mar

. 3 -

Apr

. 25

(33)

; Apr

. 28

- Jun

. 5 (2

8)

Gra

ding

Per

iod

Nin

e Wee

ksA

ug. 2

6 - O

ct. 2

5 [4

3];

Oct

. 28

- Jan

. 10

[39]

;Ja

n. 1

3 - M

ar. 2

8 [4

7];

Mar

. 31

- Jun

. 5 [4

6]

Firs

t Sem

este

r

82Se

cond

Sem

este

r

93

17

5

SM

TW

ThF

S1

23

4)5

6(7

89

1011

1213

1415

1617

1819

2021

2223

2425

]26

27[2

829

3031

23-E

OC

TOBE

R 2

013

22-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

)16

17(1

819

2021

2223

2425

2627

2829

30

16-E

NO

VEM

BER

201

316

-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

2627

2829

3031

15-E

DEC

EMBE

R 2

013

14-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

[(26

2728

2930

31

22/1

0-E

AU

GU

ST 2

013

5-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

2627

2829

30

21-E

SEPT

EMBE

R20

-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

2627

2829

3031

23-E

JULY

201

3

SM

TW

ThF

S1

23

45

67

89

10]

1112

[13

1415

1617

)18

1920

(21

2223

2425

2627

2829

3031

20-E

JAN

UA

RY

201

419

-S

SM

TW

ThF

S 12

34

56

78

910

1112

1314

1516

1718

1920

2122

2324

2526

2728

)

19-E

FEBR

UA

RY

201

418

-S

SM

TW

ThF

S2

(34

56

71/

89

1011

1213

1415

1617

1819

2021

2223

2425

2627

28]

2930

[31

16-E

MA

RC

H 2

014

16-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

)26

27(2

829

30

20-E

APR

IL 2

014

20-S

SM

TW

ThF

S1

23

45

67

89

1011

1213

1415

1617

1819

2021

2223

2425

2627

2829

3031

22-E

MAY

201

421

-S

SM

TW

ThF

S1

23

45)

]6

78

910

1112

1314

1516

1718

1920

2122

2324

2526

2728

2930

5-E

JUN

E 20

144-

S

T

T

It is

the

polic

y of

the

Uni

ted

Inde

pend

ent S

choo

l Dis

trict

not

to d

iscr

imin

ate

on th

e ba

sis

of ra

ce, c

olor

, nat

iona

l orig

in, s

ex, o

r dis

abilit

y in

its

Educ

atio

nal

prog

ram

s, s

ervi

ces

or a

ctiv

ities

, as

requ

ired

by T

itle

VI o

f the

Civ

il R

ight

s Ac

t of 1

964,

as

amen

ded;

Titl

e IX

of t

he E

duca

tiona

l Am

endm

ents

of 1

972;

the

Age

Dis

crim

inat

ion

Act o

f 197

5, a

s am

ende

d; a

nd S

ectio

n 50

4 of

the

Reh

abilit

atio

n Ac

t of 1

973,

as

amen

ded.

6

United Independent School District

Accounting Policies and Procedures

Cash Management & Investment

Cash

Man

agement &

Inve

stment

7

8

CASH PRACTICES The Accounting Department is charged with the responsibility of providing controls over cash deposits, reconciliations, investment and handling of the department’s goal of being a 100% cashless District by 2014. Currently, the District offers electronic payments for Student Meals, Student Activities, Tax Payments, and After School Tuition. The District also offers direct deposit to all employees and ACH payments for all payroll transactions. DEPOSITORY CONTRACT Depository Bid - Each school district is to use a uniform bid blank form as specified in Texas Education Code, §45.206. A school district may add other terms to the uniform bid blank form based on additional requirements. This form must be mailed to each bank located in the school district at least 30 days before the termination of the current depository contract. This form must be filed with the Texas Education Agency in accordance with filing instructions specified in the form. House Bill 2411 from the 80th Legislative Session provided school districts with the option to extend a depository contract for two (2) additional two-year terms provided the bank agrees as well (refer to TEC Section 45.205). In order to extend the contract (assuming the bank agrees), the District must have the Board approve a resolution (see TEA website for sample resolution). RECONCILIATIONS The Accountants reconcile all Central Office cash and investment accounts on a monthly basis, usually by the 10th of the next month. Once all reconciling entries have been made, the reconciliations are then reviewed and approved by the Accounting Manager. The Student Activity bank accounts are reconciled by the 20th of the following month by the Activity Bookkeepers. COURIER PROCESS The District contracts with a courier service for the transportation of deposits to the bank. All deposits are picked up by the Courier based on a pre-determined schedule and the Accounting Department has a roster (with photos) of all potential employees of the courier service. Each District location has designated Bookkeepers/Secretaries that prepare the deposit. Food Service deposits are prepared by the designated Food Service Personnel

9

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

OTHER REVENUES - INVESTMENTS All investments made by the District shall comply with the Public Funds Investment Act (Texas Government Code Chapter 2256, Subchapter A) and all federal, state, and local statutes, rules or regulations. Gov’t Code 2256.026

WRITTEN POLICIES Investments shall be made in accordance with written policies approved by the Board. The investment policies must primarily emphasize safety of principal and liquidity and must address investment diversification, yield, and maturity and the quality and capability of investment management. The policies must include: 1. A list of the types of authorized investments in which the District’s funds may be

invested;

2. The maximum allowable stated maturity of any individual investment owned by the District;

3. For pooled fund groups, the maximum dollar weighted average maturity allowed based on the stated maturity date of the portfolio;

4. Methods to monitor the market price of investments acquired with public funds; and

5. A requirement for settlement of all transactions, except investment pool funds and mutual funds, on a delivery versus payment basis.

Gov’t Code 2256.005(b)

ANNUAL REVIEW The investment policy and the investment strategy shall be reviewed not less than annually. The Board shall adopt a written instrument stating that it has reviewed the investment policy and investment strategies and that the written instrument so adopted shall record any changes made to either the investment policy or investment strategies. Gov’t Code 2256.005(e) ANNUAL AUDIT The Board shall perform a compliance audit of management controls on investments and adherence to the Board’s established investment policies. The compliance audit shall be performed in conjunction with the annual financial audit. Gov’t Code 2256.005(m)

10

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

INVESTMENT STRATEGIES As part of the investment policy, the Board shall adopt a separate written investment strategy for each of the funds or group of funds under the Board’s control. Each investment strategy must describe the investment objectives for the particular fund under the following priorities in order of importance: 1. Understanding of the suitability of the investment to the financial requirements of the

Board;

2. Preservation and safety of principal;

3. Liquidity;

4. Marketability of the investment if the investment needs to be liquidated before maturity;

5. Diversification of the investment portfolio; and

6. Yield.

Gov’t Code 2256.005(d)

INVESTMENT OFFICER The Board shall designate one or more officers or employees as investment officer(s) to be responsible for the investment of its funds. If the Board has contracted with another investing entity to invest its funds, the investment officer of the other investing entity is considered to be the investment officer of the contracting Board’s District. In the administration of the duties of an investment officer, the person designated as investment officer shall exercise the judgment and care, under prevailing circumstances that a prudent person would exercise in the management of the person’s own affairs, but the Board retains the ultimate responsibility as fiduciaries of the assets of the District. Unless authorized by law, a person may not deposit, withdraw, transfer, or manage in any other manner the funds of the investing entity. Authority granted to a person to invest an entity’s funds is effective until rescinded by the Board or until termination of the person’s employment by the District. Gov’t Code 2256.005(f) A District or investment officer may use the District’s employees or the services of a contractor of the District to aid the investment officer in the execution of the officer’s duties under Government Code, Chapter 2256. Gov’t Code 2256.003(c)

11

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

INVESTMENT TRAINING INITIAL - Within 12 months after taking office or assuming duties, the treasurer or chief financial officer and the investment officer of the District shall attend at least one training session from an independent source approved either by the Board or by a designated investment committee advising the investment officer. This initial training must contain at least ten hours of instruction relating to their respective responsibilities under the Public Funds Investment Act. Gov’t Code 2256.008(a) WITHIN A 2 YEAR PERIOD - The treasurer or chief financial officer and the investment officer must also attend an investment training session not less than once in a two-year period and receive not less than ten hours of instruction relating to investment responsibilities under the Public Funds Investment Act from an independent source approved by the Board or a designated investment committee advising the investment officer. If the District has contracted with another investment entity to invest the District’s funds, this training requirement may be satisfied by having a Board officer attend four hours of appropriate instruction in a two-year period. Gov’t Code 2256.008(a), (b) Investment training shall include education in investment controls, security risks, market risks, diversification of investment portfolio, and compliance with the Government Code, Chapter 2256. Gov’t Code 2256.008(c)

STANDARD OF CARE Investment shall be made with judgment and care, under prevailing circumstances that a person of prudence, discretion, and intelligence would exercise in the management of his or her own affairs, not for speculation, but for investment, considering the probable safety of capital and the probable income to be derived. Investments shall be governed by the following objectives in order of priority: 1. Preservation and safety of principal;

2. Liquidity; and

3. Yield.

In determining whether an investment officer has exercised prudence with respect to an investment decision, the following shall be taken into consideration:

1. The investment of all funds, rather than the prudence of a single investment, over

which the officer had responsibility.

12

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

2. Whether the investment decision was consistent with the Board’s written investment policy.

Gov’t Code 2256.006

PERSONAL INTEREST A District investment officer who has a personal business relationship with a business organization offering to engage in an investment transaction with the District shall file a statement disclosing that personal business interest. An investment officer who is related within the second degree by affinity or consanguinity, as determined by Government Code Chapter 573, to an individual seeking to sell an investment to the District shall file a statement disclosing that relationship with the Board and with the Texas Ethics Commission. For the purposes of this policy, and investment officer has a personal business relationship with a business organization if:

1. The investment officer owns ten percent or more of the voting stock or shares of the business organization or owns $5,000 or more of the fair market value of the business organization;

2. Funds received by the investment officer from the business organization exceed ten percent of the investment officer’s gross income for the previous year; or

3. The investment officer has acquired from the business organization during the pervious year investments with a book value of $2,500 or more for the personal account of the investment officer.

Gov’t Code 2256.005(i)

QUARTERLY REPORTS Not less than quarterly, the investment officer shall prepare and submit to the Board a written report of investment transactions for all funds covered by the Public Funds Investment Act. This report shall be presented to the Board and the Superintendent not less than quarterly, within a reasonable time after the end of the period. The report must: 1. Contain a detailed description of the investment position of the District on the date of

the report;

2. Be prepared jointly and signed by all District investment officer.

3. Contain a summary statement for each pooled fund group (i.e. each internally created fund in which one or more accounts are combined for investing purposes). The report

13

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

must be prepared in compliance with generally accepted accounting principles and must state:

a. Beginning market value for the reporting period;

b. Additions and changes to the market value during the period;

c. Ending market value for the period; and

d. Fully accrued interest for the reporting period.

4. State the book value and market value of each separately invested asset at the beginning and end of the reporting period by the type of asset and fund type invested.

5. State the maturity date of each separately invested asset that has a maturity date.

6. State the account or fund or pooled group fund in the District for each individual investment was acquired.

7. State the compliance of the investment portfolio of the District as it relates to the District’s investment strategy expressed in the District’s investment policy and relevant provisions of Government Code, Chapter 2256.

If the District invests in other than money market mutual funds, investment pools or accounts offered by its depository bank in the form of certificates of deposit or money market accounts or similar accounts, the reports shall be formally reviewed at least annually by an independent auditor, and the result of the review shall be reported to the Board by that auditor. Gov’t Code 2256.023

SELECTION OF BROKER The Board or a designated investment committee, shall, at least annually review, revise, and adopt a list of qualified brokers that are authorized to engage in investment transactions with the District. Gov’t Code 2256.025 AUTHORIZED INVESMTENTS The Board may purchase, sell, and invest its funds and funds under its control in investments described below, in compliance with the adopted investment policies and according to the standard of care set out in this policy. Investments may be made directly by the Board or by a nonprofit corporation acting on behalf of the Board or an investment pool acting on behalf of two or more local governments, state agencies, or a combination of the two. Gov’t Code 2256.003(a)

14

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

In the exercise of these powers, the Board may contract with an investment management firm registered under the Investment Advisers Act of 1940 (15U.S.C. Section 80b-1 et seq.) or with the State Securities Board to provide for the investment and management of its public funds or other funds under its control. A contract made for such purpose may not be for a term longer than two years. A renewal or extension of the contract must be made by the Board by order, ordinance, or resolution. Gov’t Code 2256.003(b) The following investments are authorized: 1. Obligations, including letters of credit, of the United States or its agencies and

instrumentalities; direct obligations of the state of Texas or its agencies and instrumentalities; collateralized mortgage obligations directly issued by a federal agency or instrumentality of the United States, the underlying security for which is guaranteed by an agency or instrumentality of the United States; other obligations, the principal and interest of which are unconditionally guaranteed or insured by, or backed by the full faith and credit of, the state of Texas, the United States, or their respective agencies and instrumentalities; obligations of states, agencies, counties, cities, and other political subdivisions of any state rated as to investment quality by a nationally recognized investment rating firm not less than A or its equivalent; and bonds issued, assumed, or guaranteed by the state of Israel. Gov’t Code 2256.009(a)

The following investments are not authorized:

a. Obligations whose payment represents the coupon payments on the outstanding principal balance of the underlying mortgage-backed security collateral and pays no principal.

b. Obligations whose payment represents the principal stream of cash flow from the underlying mortgage backed security collateral and bears no interest.

c. Collateralized mortgage obligations that have a stated final maturity date of greater than ten years.

d. Collateralized mortgage obligations the interest rate of which is determined by an index that adjusts opposite to the changes in a market index.

Gov’t Code 2256.009(b)

2. Certificates of deposit or share certificates issued by a depository institution that has its main office or a branch office in Texas that is guaranteed or insured by the FDIC or its successor or the National Credit Union Share Insurance Fund or its successor and is secured by obligations described in item 1 above, including mortgage-backed securities directly issued by a federal agency or instrumentality that have a market value of not less than the principal amount of the certificates (but excluding those mortgage-backed securities described in Section 2256.009[b]) or secured in any other

15

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

manner and amount provided by law for the deposits of the investing entity. Gov’t Code 2256.010(a)

a. The funds are invested by the District through a depository institution that has its main office or a branch office in this state and that is selected by the District;

b. The depository institution selected by the District arranges for the deposit of the funds in certificates of deposit in one or more federally insured depository institutions, wherever located, for the account of the District;

c. The full amount of the principal and accrued interest of each of the certificates of deposit is insured by the United States or an instrumentality of the United States;

d. The depository institution selected by the District acts as custodian for the District with respect to the certificates of deposit issued for the account of the District entity; and

e. At the same time that the funds are deposited and the certificates of deposit are issued for the account of the District, the depository institution selected by the District receives an amount of deposits from customers of other federally insured depository institutions, wherever located, that is equal to or greater than the amount of the funds invested by the District through the depository institution.

Gov’t Code 2256.010(b) The investment policies may prove that bids for certificates of deposit be solicited orally, in writing, electronically, or in any combination of those methods. Gov’t Code 2256.005(c)

3. Fully collateralized repurchase agreements that have a defined termination dated, are

secured by obligations of the United States or its agencies and instrumentalities, are pledged to the District, held in the District’s name, and deposited with the District or a third party selected and approved by the Board, and placed through a primary government securities dealer, as defined by the Federal Reserve or a financial institution doing business in Texas. The term of any reverse security repurchase agreement may not exceed 90 days after the date the reverse security repurchase agreement is delivered. Money received by the District under the terms of a reverse security repurchase agreement shall be used to acquire additional authorized investments, but the term of the authorized investments acquired must mature no later than the expiration date stated in the reverse security repurchase agreement. Gov’t Code 2256.011

16

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

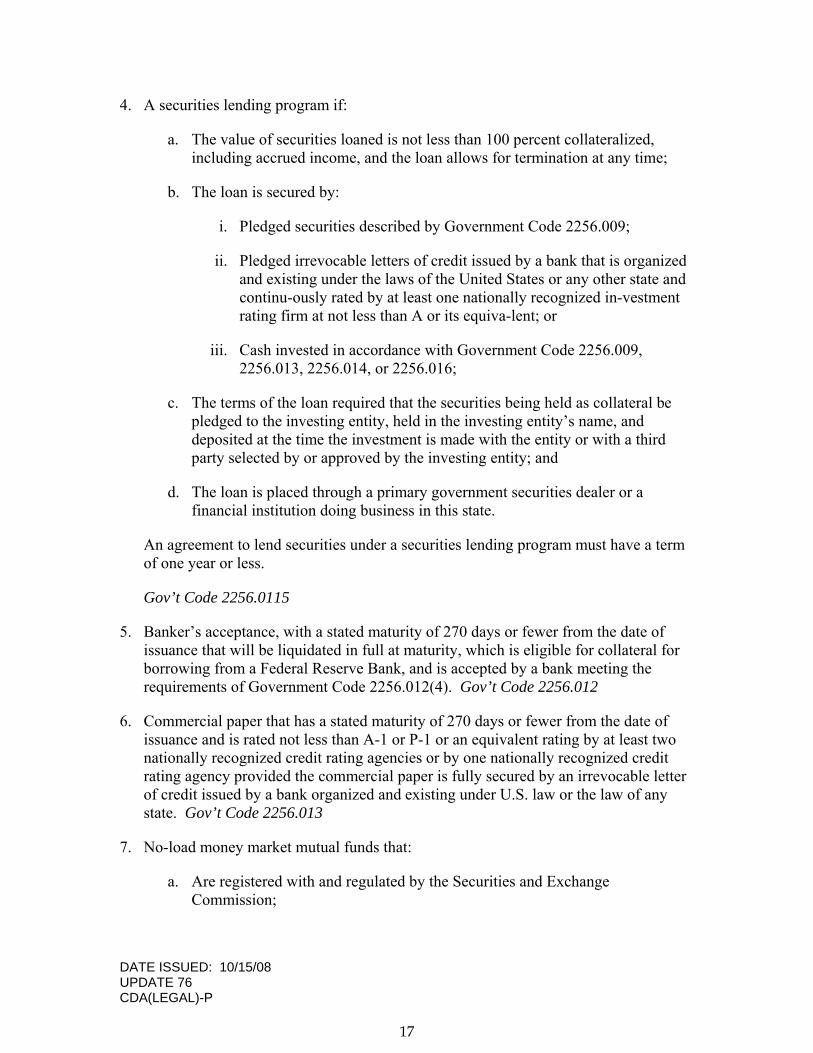

4. A securities lending program if:

a. The value of securities loaned is not less than 100 percent collateralized, including accrued income, and the loan allows for termination at any time;

b. The loan is secured by:

i. Pledged securities described by Government Code 2256.009;

ii. Pledged irrevocable letters of credit issued by a bank that is organized and existing under the laws of the United States or any other state and continu-ously rated by at least one nationally recognized in-vestment rating firm at not less than A or its equiva-lent; or

iii. Cash invested in accordance with Government Code 2256.009, 2256.013, 2256.014, or 2256.016;

c. The terms of the loan required that the securities being held as collateral be pledged to the investing entity, held in the investing entity’s name, and deposited at the time the investment is made with the entity or with a third party selected by or approved by the investing entity; and

d. The loan is placed through a primary government securities dealer or a financial institution doing business in this state.

An agreement to lend securities under a securities lending program must have a term of one year or less.

Gov’t Code 2256.0115

5. Banker’s acceptance, with a stated maturity of 270 days or fewer from the date of issuance that will be liquidated in full at maturity, which is eligible for collateral for borrowing from a Federal Reserve Bank, and is accepted by a bank meeting the requirements of Government Code 2256.012(4). Gov’t Code 2256.012

6. Commercial paper that has a stated maturity of 270 days or fewer from the date of issuance and is rated not less than A-1 or P-1 or an equivalent rating by at least two nationally recognized credit rating agencies or by one nationally recognized credit rating agency provided the commercial paper is fully secured by an irrevocable letter of credit issued by a bank organized and existing under U.S. law or the law of any state. Gov’t Code 2256.013

7. No-load money market mutual funds that:

a. Are registered with and regulated by the Securities and Exchange Commission;

17

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

b. Provide the District with a prospectus and other information required by the Securities and Exchange Act of 1934 (15 U.S.C. 78aet seq.) or the Investment Company Act of 1940 (15 U.S.C. 80a-1 et seq.);

c. Have a dollar-weighted average stated maturity of 90 days of fewer; and

d. Include in their investment objectives the maintenance of a stable net asset value of $1 for each share.

However, investments in no-load money market mutual funds shall be limited to the percentages authorized by Government Code 2256.014(c)

8. No-load mutual funds that:

a. Are registered with the Securities & Exchange Commission;

b. Have an average weighted maturity of less than two years;

c. Are invested exclusively in obligations approved by Government Code Chapter 2256, Subchapter A, regarding authorized investments (Public Funds Investment Act);

d. Are continuously rated by at least one nationally recognized investment rating firm of not less than AAA or its equivalent; and

e. Conform to the requirements in Government Code Section 2256.016(b) and (c) relating to the eligibility of investment pools to receive and invest funds of investing entities.

Investments in no-load mutual funds shall be limited to the percentages authorized by Government Code 2256.014(c). In addition, the District may not invest any portion of bond proceeds, reserves, and funds held for debt service, in no-load mutual funds described in this item.

Gov’t Code 2256.014

9. A guaranteed investment contract, as an investment vehicle for bond proceeds, if the guaranteed investment contract:

a. Has a defined termination date.

b. Is secured by obligations described by Government Code Section 2256.009(a)(1), excluding those obligations described by Section 2256.009(b), in an amount at least equal to the amount of bond proceeds invested under the contract.

18

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

c. Is pledged to the District and deposited with the District or with a third party selected and approved by the District.

Bond proceeds, other than bond proceeds representing reserves and funds maintained for debt service purposes, may not be invested in a guaranteed investment contract with a term longer than five years form the date of issuance of the bonds.

To be eligible as an authorized investment:

d. The Board must specifically authorize guaranteed investment contracts as eligible investments in the order, ordinance, or resolution authorizing the issuance of bonds.

e. The District must receive bids from at least three separate providers with no material financial interest in the bonds from which proceeds were received.

f. The District must purchase the highest yielding guaranteed investment contract for which a qualifying bid is received.

g. The price of the guaranteed investment contract must take into account the reasonably expected breakdown schedule for the bond proceeds to be invested.

h. The provider must certify the administrative costs reasonably expected to be paid to third parties in connection with the guaranteed investment contract.

Gov’t Code 2256.015

10. A public funds investment pool meeting the requirements of Government Code 2256.016 and 2256.019, if the Board authorizes the investment in the particular pool by resolution. Gov’t Code 2256.016, 2256.019

CHANGE IN LAW The District is not required to liquidate investments that were authorized investments at the time of purchase. Gov’t Code 2256.017 SELLERS OF INVESTMENTS A written copy of the investment policy shall be presented to any person offering to engage in an investment transaction with an investing entity or to an investment management firm under contract with an investing entity to invest or manage the entity’s investment portfolio. For purposes of this policy, a business organization includes investment pools and an investment management firm under contract with an investing

19

DATE ISSUED: 10/15/08 UPDATE 76 CDA(LEGAL)-P

entity to invest or manage the entity’s investment portfolio. The qualified representative of the business organization offering to engage in an investment transaction with the District shall execute a written instrument in a form acceptable to the District and the business organization substantially to the effect that the business organization has:

1. Received and thoroughly reviewed the District investment policy; and

2. Has acknowledged that the business organization has implemented reasonable procedures and controls in an effort to preclude investment transactions conducted between the District and the organization that are not authorized by the District’s policy, except to the extent that this authorization is dependent on an analysis of the makeup of the entity’s entire portfolio or requires an interpretation of subjective investment standards.

The investment officer may not acquire or otherwise obtain any authorized investment described in the District’s investment policy from a person who has not delivered to the District the instrument described above. Gov’t Code 2256.005

DONATIONS A gift, devise, or bequest made to provide college scholarships for District graduates may be invested by the Board as provided in Property Code 117.004, unless otherwise specifically provided by the terms of the gift, devise, or bequest. Education Code 45.107 Investments donated to the District for a particular purpose or under terms of use specified by the donor are not subject to the requirements of Government Code Chapter 2256, Subchapter A. Gov’t Code 2256.004(b)

ELECTRONIC FUNDS TRANSFER The District may use electronic means to transfer or invest all funds collected or controlled by the District. Gov’t Code 2256.051

20

United ISD 240903 OTHER REVENUES CDA INVESTMENTS (LOCAL)

DATE ISSUED: 10/15/08 LDU-32-06 CDA(LOCAL)-X

INVESTMENT The assistant superintendent for business/finance or other person des- AUTHORITY ignited by Board resolution shall serve as the investment officer of the

District and shall invest District Funds in accordance with the Public Funds Investment Act, the District’s approved investment policy, and generally accepted accounting procedures. All investment transactions except investment pool funds and mutual funds shall be executed on a delivery versus payment basis.

APPROVED From those investments authorized by law and described further in CDA INVESTMENT (LEGAL), the Board shall permit investment of District funds in only the INSTRUMENTS following investment types, consistent with the strategies and maturities

defined in this policy:

1. Obligations of, or guaranteed by, governmental entities as permitted by Government Code 2256.009;

2. Certificates of deposit and share certificates a permitted by Government Code 2256.010;

3. Fully collateralized repurchase agreements permitted by Government Code 2256.011;

4. A securities lending program as permitted by Government Code 2256.015;

5. Banker’s acceptances as permitted by Government Code 2256.012;

6. Commercial paper as permitted by Government Code 2256.013;

7. No-load money market mutual funds and no-load mutual funds permitted by Government Code 2256.014;

8. A guaranteed investment contract as an investment vehicle for bond proceeds, provided it meets the criteria and eligibility requirements established by Government Code 2256.015;

9. Public funds investment pools as permitted by Government Code 2256.16.

SAFETY AND The main goal of the investment program is to ensure its safety and INVESTMENT maximize financial returns within current market conditions in MANAGEMENT accordance with this policy. Investments shall be made in manner that

ensures the preservation of capital in the overall portfolio, and offsets during a 12-month period any market price losses resulting from interest-rate fluctuations by income received from the balance of the portfolio. No individual investment transaction shall be undertaken that jeopardizes the total capital position of the overall portfolio.

21

United ISD 240903 OTHER REVENUES CDA INVESTMENTS (LOCAL)

DATE ISSUED: 10/15/08 LDU-32-06 CDA(LOCAL)-X

LIQUIDITY AND Any internally created pool fund group of the District shall have a MATURITY maximum dollar weighted maturity of 180 days. The maximum allowable

stated maturity of any other non-capital project or non-bonded proceeds individual investment owned by the District shall not exceed one year form the time of purchase. The maximum allowable stated maturity of any capital project or bond proceeds individual investment owned by the District shall not exceed the lesser of the anticipated expenditure date or three years from the time of purchase, whichever is sooner. The Board may specifically authorize a longer maturity for a given investment, within legal limits.

The District’s investment portfolio shall have sufficient liquidity to meet anticipated cash flow requirements.

DIVERSITY The investment portfolio shall be diversified in terms of investment

instruments, maturity scheduling, and financial institutions to reduce risk of loss resulting from overconcentration of assets in a specific class of investments, specific maturity, or specific issuer.

MONITORING MARKET The investment officer shall monitor the investment portfolio and shall PRICES keep the Board informed of significant declines in the market value of the

District’s investment portfolio. Information sources may include financial/investment publications and electronic media, available software for tracking investments, depository banks, commercial or investment banks, financial advisors, and representatives/advisors of investment pools or money market funds. Monitoring shall be done at least quarterly, as required by law, and more often as economic conditions warrant by using appropriate reports, indices, or benchmarks for the type of investment.

FUNDS / STRATEGIES Investments of the following fund categories shall be consistent with this

policy and in accordance with the strategy defined below. OPERATING FUNDS Investment strategies for operating funds (including any commingled

pools containing operating funds) shall have as their primary objectives safety, investment liquidity, and maturity sufficient to meet anticipated cash flow requirements.

AGENCY FUNDS Investment strategies for agency funds shall have as their objectives

safety, investment liquidity, and maturity sufficient to meet anticipated cash flow requirements.

DEBT SERVICE Investment strategies for debt service funds shall have as their objective FUNDS sufficient investment liquidity to timely meet debt service payment

obligations in accordance with provisions in the bond documents. Maturities longer than one year are authorized provided legal limits are not exceeded.

CAPTIAL PROJECTS Investment strategies for capital project funds shall have as their

objective sufficient investment liquidity to timely meet capital project

22

United ISD 240903 OTHER REVENUES CDA INVESTMENTS (LOCAL)

DATE ISSUED: 10/15/08 LDU-32-06 CDA(LOCAL)-X

obligations. Maturities longer than one year are authorized provided legal limits are not exceeded.

SAFEKEEPING AND The District shall retain clearly marked receipts providing proof of the

District’s ownership. The District may delegate, however, to an investment pool the authority to hold legal title as custodian of invest-ments purchased with District funds by the investment pool.

BROKERS / DEALERS Prior to handling investments on behalf of the District, brokers/dealers

must submit required written documents in accordance with law. [See SELLERS OF INVESTMENTS, CDA(LEGAL)] Representatives of brokers/dealers shall be registered with the Texas State Securities Board and must have membership in the Securities Investor Protection Corporation (SIPC), and be in good standing with the National Association of Securities Dealers.

SOLICITING BIDS FOR In order to get the best return on its investments, the District may solicit CD’S bids for certificates of deposit in writing, by telephone, or electronically,

or by a combination of these methods. INTEREST RATE RISK To reduce exposure to changes in interest rates that could adversely

affect the value of investments, the District shall use final and weighted-average-maturity limits and diversification.

The District shall monitor interest rate risk using weighted average maturity and specific identification.

INTERNAL CONTROLS A system of internal controls shall be established and documented in writing and must include specific procedures designated who has authority to withdraw funds. Also, they shall be designated to protect against losses of public funds arising from fraud, employee error, misrepresentation by third parties, unanticipated changes in financial markets, or imprudent actions by employees and officers of the District. Controls deemed most important shall include:

1. Separation of transaction authority from accounting and

recordkeeping and electronic transfer of funds.

2. Avoidance of collusion.

3. Custodial safekeeping.

4. Clear delegation of authority

5. Written confirmation of telephone transactions.

6. Documentation of dealer questionnaires, quotations and bids, evaluations, transactions, and rationale.

23

United ISD 240903 OTHER REVENUES CDA INVESTMENTS (LOCAL)

DATE ISSUED: 10/15/08 LDU-32-06 CDA(LOCAL)-X

7. Avoidance of bearer-form securities.

These controls shall be reviewed by the District’s independent auditing firm.

PORTFOLIO REPORT In addition to the quarterly report required by law and signed by the District’s investment officer, a comprehensive report on the investment program and investment activity shall be presented annually to the Board. This report shall include a performance evaluation that may include, but not limited to, comparisons to 91-day U.S. Treasury Bills, six-month U.S. Treasury Bills, the Fed Fund rate, the Lehman bond index, and rates from investment pools. The annual report shall include a review of the activities and total yield for the preceding 12 months, suggest policies, strategies, and improvements that might enhance the investment program, and propose an investment plan for the ensuing year. Weighted average yield to maturity shall be the portfolio performance measurement standard for all investment reporting.

24

INVESTMENT STRATEGY STATEMENT

The Investment Strategy applies to the inve stment activities of the United Independent School District (the “District”). These strategies serve to satisfy the statutory requirement of chapter 2256, Texas Governm ent Code (“the Public F inds Investm ent Act”), to define and approve investment strategies. It is the po licy of District that, giving due regard to the safe ty and risk of investm ent, all available funds shall be invested in conf ormance with State and Federal Regulation, applicable Loan docum entation and Bond reso lution requirem ents, adopted Investm ent Policy and adopted Investment Strategy. In accordance with the Public Funds Investm ent Act, District investment strategies shall address the following priorities (in order of importance):

• Understanding the su itability of the inves tment to the f inancial requirements of District;

• Preservation and safety of principal;

• Liquidity;

• Marketability of the inv estment if the n eed arises to liqu idate the investment

prior to maturity;

• Diversification of the investment portfolio; and

• Yield. Effective investm ent strategy developm ent coordinates the prim ary objectives of District’s Investm ent Policy and cash m anagement procedures. Aggressive cash management to incr ease the availab le “inve stment per iod” will enhanc e the ability of District to e arn inte rest incom e. Matur ity selections shall be based on cash flow and market conditions to take advantage of interest rate cycles as viable and material revenue to all District funds. Dist rict’s portfolio shall be designed and m anaged in a m anner responsive to the public trust and consistent with the Investment Policy. Each major Fund type has varying cash flow requirements and liquidity needs. Therefore specific strategies shall be i mplemented c onsidering the Fund’s unique requirements. District fun ds shall be analyzed an d i nvested accord ing to the follo wing m ajor Fund types:

A. Operating Funds B. Agency Funds C. Debt Service Funds D. Capital Project Funds

25

INVESTMENT STRATEGY

In order to m inimize risk of lo ss due to interes t ra te f luctuations, investment maturities will no t ex ceed th e a nticipated c ash flow requirements of the Fun ds. Inv estment guidelines by Fund-type are as follows: A. Operating Funds Suitability - Any investm ent eligible in the Inv estment Policy is suitable f or Operating Funds. Safety of Principal - All investments shall be of high quality securities with no perceived default r isk. Marke t pr ice f luctuations will oc cur. However, m anaging the weig hted average days to m aturity for the Operati ng Fund’s portfolio to less than 180 days and restricting the maximum allowable maturity to one year will minimize the price volatility of the overall portfolio. Marketability - Securities with active and efficient secondary markets are necessary in the event of an unanticipated cash flow requirem ent. Historical m arket “spreads” between the bid and offer prices of a pa rticular security-type of less than a tenth of a percentage point will define an efficient secondary market. Liquidity - The Operating Fund requires the greates t short-term liquidity of any of the Fund types. Short-term investment pools a nd money m arket mutual funds will prov ide daily liqu idity and m ay be utiliz ed as a co mpetitive yie ld a lternative to f ixed m aturity investments. Diversification - Investm ent maturities should be staggered throughout the budget cycle to provide cash flow based on the anticipated operating needs of District. Diversifying the appropriate maturity structure out through two years will reduce market cycle risk. Yield - Attaining a competitive m arket yield for comparable security-types and portfolio restrictions is the de sired objective. The yi eld of an equally weighted, rolling six-month Treasury bill portfolio will be the minimum yield objective. B. Agency Funds Suitability - Any investm ent eligible in the Inv estment Policy is s uitable f or Agency Funds. Safety of Principal - All investments shall be of high quality securities with no perceived default risk. Market price fluctuations w ill occur. However, by m anaging weighted average days to maturity for the Investment Pool to less than 180 da ys and restricting the maximum allowable maturity to one year, th e price volatility of the overall portfolio will be minimized.

26

Marketability - Securities with active and efficient secondary markets are necessary in the event of an unanticipated cash flow requirem ent. Historical m arket “spreads” between the bid and offer prices of a pa rticular security-type of less than a tenth of a percentage point will define an efficient secondary market. Liquidity – Agency Funds require reasonable short-term liquidity. Short-term investment pools and money market mutual funds will provide daily liquidity and may be utilized as a competitive yield alternative to fixed maturity investments. Diversification - Investm ent maturities should be staggered throughout the budget cycle to provide cash flow based on the anticipated needs of District. Diversifying the appropriate maturity structure out through one year will reduce market cycle risk. Yield - Attaining a competitive m arket yield for comparable security-types and portfolio restrictions is the de sired objective. The yi eld of an equally weighted, rolling six-month Treasury bill portfolio will be the minimum yield objective. C. Debt Service Funds Suitability - Any investm ent eligible in the Inv estment Policy is suitab le f or the Debt Service Fund. Safety of Principal - All investments shall be of high quality securities with no perceived default risk. Market pr ice fluctuations will occur. However, by m anaging Debt Service Funds to not exceed the debt serv ice paym ent schedule th e m arket risk of the overall portfolio will be minimized. Marketability - Securities with activ e and efficien t secondary markets are not neces sary as the event of an unanticipated cash flow requirement is not probable. Liquidity - Debt Service Funds have predic table paym ent schedules. Therefore investment m aturities s hould not exceed th e anticipated cash flow requirem ents. Investments pools and money m arket m utual funds m ay provide a com petitive yield alternative for short term fixe d maturity investments. A singular repurchase agreem ent may be utilized if disbursem ents are allowed in the amount necessary to satisfy any debt service paym ent. This investm ent structur e is commonly referred to as a flexible repurchase agreement. Diversification - Ma rket cond itions inf luence the attractiveness of fully extending maturity to the next “unfunded” paym ent da te. Generally, if investm ent rates are anticipated to decrease o ver time, District is best served by locking in m ost investments. If the interest rates are potentially rising, th en investing in shorter and larger am ounts may provide advantage. At no tim e shall th e debt service schedule b e exceeded in an attempt to bolster yield.

27

Yield - Attaining a competitive m arket yield for comparable security-types and portfolio restrictions is the desired objective. The yield of an equa lly weighted, rolling three-month Treasury bill portfolio shall be the minimum yield objective. D. Capital Project Funds Suitability - Any inves tment eligible in the In vestment Policy is suitable f or Ca pital Project Funds. Safety of Pr incipal - All investm ents will be of high quality s ecurities with no perceiv ed default r isk. Mark et p rice f luctuations wi ll occur. How ever, by m anaging Capital Project Funds to not exceed the anticipated ex penditure schedule the market risk of the overall portfolio will be minimized. Marketability - Securities with active and efficient secondary markets are necessary in the event of an unanticipated cash flow requirem ent. Historical m arket “spreads” between the bid and offer prices of a pa rticular security-type of less than a tenth of a percentage point will define an efficient secondary market. Liquidity - Capital Project Fund program s have reasonably predictable draw down schedules. Therefore investm ent maturities should generally follow the anticipated cash flow requirem ents. Investm ent pools and money m arket m utual funds will provide readily available funds generally equal to one month’s anticipated cash f low needs, or a competitive yield alter native f or s hort term f ixed m aturity inves tments. A s ingular repurchase agreem ent m ay be utilized if disbursements are allowed in the am ount necessary to satisfy any expenditure request . This investm ent structure is commonly referred to as a flexible repurchase agreement. Diversification - Market conditions and arbitrage re gulations influence the attractiveness of staggering the m aturity of fixed rate investments for c onstruction, loan and bond proceeds. Generally, when investm ent rate s exceed the applicable cost of borro wing, District is best served by locking in most investments. If the cost of borrowing cannot be exceeded, then concurrent m arket conditio ns will determ ine the attractiveness of diversifying maturities or investing in sho rter and larg er amounts. At no tim e shall the anticipated expenditure schedule be exceeded in an attempt to bolster yield. Yield - Achieving a po sitive sprea d to the cos t of borrowing is the de sired objective, within th e lim its of the Investm ent Policy’s risk constraints. The yield of an equally weighted, rolling six-month Treasury bill por tfolio will be the m inimum yield objectiv e for non-borrowed funds.

28

INTERNAL CONTROL STRUCTURE - INVESTMENTS

A. Purpose - To ensure that United Independent School District (a) maintains the integrity of

financial accountability and (2) to prevent fraudulent activities that may lead to inaccurate financial data or loss of financial assets.

B. Accountability - The Assistant Superintendent of Business and Finance is assigned the authority to implement internal controls in the area of investments as well as adhering to the internal controls by the Accounting Department in order to safeguard the district’s assets.

C. Elements of Fraud

1. Incentive 2. Opportunity 3. Rationalization 4. Potential

D. Risk Assessment - This process is performed by the overview of investment locations and

to determine areas that require securing investments. • The person purchasing the investment is different from the one that is recording the

investment. • Any investment purchase is reviewed and approved by more than one investment

officer • Accrued interest is recorded monthly. • At the maturity of the investments, the person verifying the investment is different

from the person reconciling the bank statements. • Investments are received by the bank not to include investment pools. • The quarterly investment reports are reviewed for accuracy and signed by three

investment officers; and prepared in accordance with the Public Funds Investment Act (PFIA).

• All investments are precluded with a cash flow analysis for the current fiscal year.

E. Responsibility of Administrator in Charge

1. Review internal controls annually 2. Provide training for staff as required by policy and PFIA 3. Conduct risk assessments 4. Maintain and monitor internal controls 5. Assure investments are made in accordance with board policy and PFIA

29

This Page Intentionally Left Blank

30

United Independent School District

Accounting Policies and Procedures

Accounts Payable

Acco

unts P

ayable

31

32

Accounts Payable staff, procedures, and responsibilities. Accounts Payable Objective The Accounts Payable department mission is to pay all invoices promptly in an accurate and efficient manner. Accounts Payable Staff The Accounts Payable department staff consists of a supervisor and four assistants. Staff Responsibilities Accounts Payable Staff will log in to Finance Plus program with the user id and password provided by the Technology Department. The assistants’ primary responsibility is to pay all invoices in a timely and accurate manner. The four assistants are assigned vendors by alphabetical order in equal amount of workload. All documentation received by the assistants, i.e. Purchase Order copies, invoices, and statements, have to be stamped “Received” and dated. After reviewing the documents, the assistants will call the Budget Technicians or campus Secretaries to identify which orders are complete and ready to be paid and the ones that will be processed in the future. When payment is made, the A/P assistants should stamp all invoices Posted and Paid. The files are to be maintained in the same order by all four assistants and the files consist of three basic groups and are kept by “alphabet letter”, all assistants will have three folders for each alphabet letter that each are responsible for. 1-The first folder for each letter will hold the blue copies of the purchase order and they will be kept in alphabetical order according to the vendor’s name, and if there are several p.o.s for that particular vendor, then they will be kept in numerical sequence. It is the responsibility of the assistant to obtain the invoices from the vendors and the approval for payment from the secretary/budget technician so that a check can be generated. 2-The second folder for each letter consists of blue copies of the p.o. and their corresponding invoices, these documents are to be kept in alphabetical order by vendor’s name and in the case of several p.o.s for the same vendor, they will be kept in numerical sequence. It is the assistant’s responsibility to obtain the on-line received approval for payment from the secretary/budget technician as soon as possible so that a check can be generated. 3-The third folder consists of a blue copy of the p.o. and the received ordered materials approval for payment these are also kept in alphabetical order by vendors’ name and numerical sequence in case of several p.o.s. for the same vendor. It is the assistant’s

33

responsibility to obtain the invoices from the vendors via mail, e-mail or fax so that a check can be generated. All invoices received are to be screened for accuracy and should reflect the exact merchandise that was described in the purchase order. If the invoice includes state taxes or finance charges, they should not be paid; the assistant will call or e-mail the vendor notifying them of the tax exemption status of the District and request an adjustment on the invoices. All communications with the vendors have to be recorded in a Vendor Communication Form (VCF) along with the vendor’s name, the contact person, the time and date and any topic of discussion. In case that the invoice totals more than the purchase order amount, the assistant will call the campus/department that originated the p.o. in most cases they will approve up to 10% for freight charges, but if the amount disputed is more than 10%, then the secretaries will have to ask for a Change Order on the original purchase order. The assistants are also responsible for paying all consultants invoices and uniform vouchers for which no purchase orders were created but are handled with a Check Request Form, this form must include the vendor’s name and number, date, budget code, account number, description of merchandise, amount, name of person requesting the check and the approval /signature of the budget accountant. Vendor checks are run bi-weekly in the Finance-Plus system or can be generated manually if they are needed sooner. In order to generate a vendor check the assistants are responsible to input all necessary information in Finance Plus following the instructions in exhibit A. Once the checks are done, the a/p assistants will review them, put them in envelopes then hand them to the mail room personnel to be mailed out. The a/p assistants will include a letter to the vendor inviting them to join our ACH program (See exhibit E). The assistants will make the necessary notes in the original documentation, scan them and input them in the Papervision System. The vendors will be rotated to the assistants every two years as part of the internal controls. The assistants may be assigned to perform other duties such as duties for absent staff, front desk reception, deliver documents, etc.

34