Accounting Planning, recording, analyzing, and interpreting financial information

Jan 01, 2016

What is Accounting?. Accounting Planning, recording, analyzing, and interpreting financial information Accounting System A planned process for providing financial information that will be useful to management. What is Accounting?. Accounting Records - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

• AccountingAccounting– Planning, recording, analyzing, and Planning, recording, analyzing, and

interpreting financial informationinterpreting financial information

• Accounting SystemAccounting System– A planned process for providing financial A planned process for providing financial

information that will be useful to information that will be useful to managementmanagement

What is Accounting?What is Accounting?

• AccountingAccounting RecordsRecordsOrganized summaries of a business’s Organized summaries of a business’s financial activitiesfinancial activities

• Financial StatementsFinancial Statements–Financial Reports that summarize the Financial Reports that summarize the financial condition and operations of a financial condition and operations of a businessbusiness

What is Accounting?What is Accounting?

• Service BusinessService Business– Performs an activity for a feePerforms an activity for a fee

• Ex: McDonald’s cooks your food for youEx: McDonald’s cooks your food for you

• Proprietorship (Sole Proprietorship)Proprietorship (Sole Proprietorship)– A business owned by one personA business owned by one person

THE BUSINESS – TECHKNOW CONSULTINGTHE BUSINESS – TECHKNOW CONSULTING

Forming and Dissolving a Proprietorship

Critical ThinkingCritical Thinking1.1. Why do you think more businesses are Why do you think more businesses are

organized as proprietorships than any organized as proprietorships than any other form of business organization?other form of business organization?

2.2. What kinds of people do you think What kinds of people do you think would be most successful as owners of would be most successful as owners of a proprietorship?a proprietorship?

BUSINESS STRUCTURESBUSINESS STRUCTURES( )( )

• AssetAsset– Anything of value owned by a businessAnything of value owned by a business

• EquitiesEquities– Financial rights to the assets of the Financial rights to the assets of the

businessbusiness

• LiabilityLiability– Any amount owed by a businessAny amount owed by a business

Assets = Liabilities + Owner’s EquityLeft side amount Right side amount

$0 $0 + $0=

The Accounting EquationThe Accounting Equation

• Owner’s EquityOwner’s Equity– The amount remaining after the value of all The amount remaining after the value of all

liabilities is subtracted from the value of all liabilities is subtracted from the value of all assetsassets

• Accounting EquationAccounting Equation– Equation showing the relationship among Equation showing the relationship among

assets, liabilities and owner’s equityassets, liabilities and owner’s equity

Accounting Scandals Rock the Financial World

• EthicsEthics– The principles of right and wrong that The principles of right and wrong that

guide an individual in making decisionsguide an individual in making decisions

• Business EthicsBusiness Ethics– The use of ethics in making The use of ethics in making

business decisionsbusiness decisions

CHARACTER COUNTSCHARACTER COUNTS( )( )

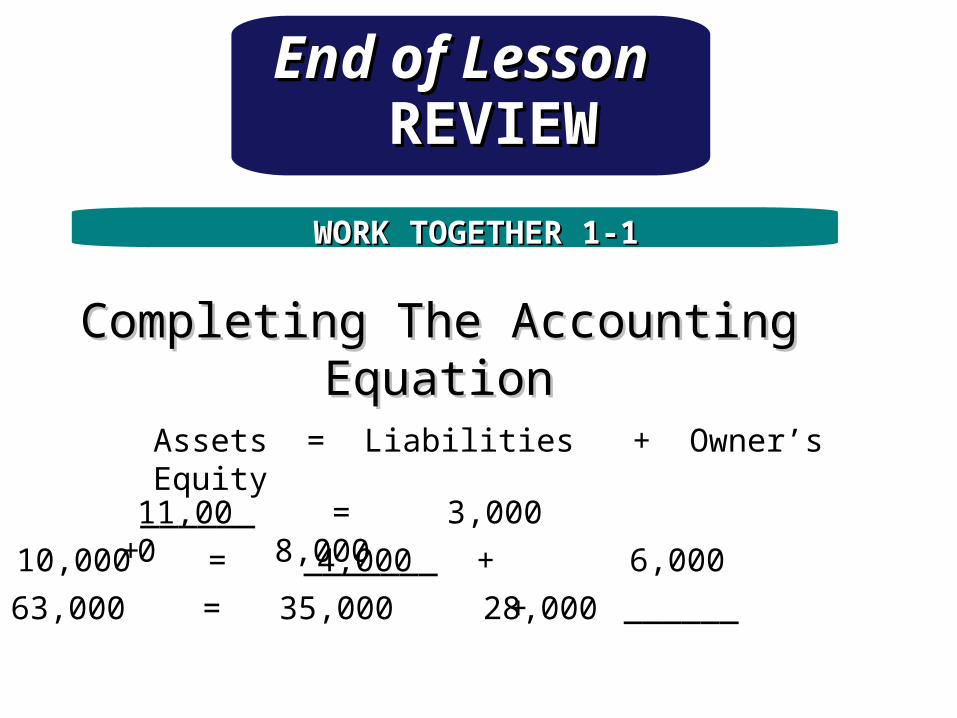

Completing The Accounting EquationCompleting The Accounting Equation

Assets = Liabilities + Owner’s Equity

______ = 3,000 + 8,00011,000

End of LessonEnd of Lesson REVIEWREVIEW

10,000 = _______ + 6,000

63,000 = 35,000 + ______

4,000

28,000

WORK TOGETHER 1-1WORK TOGETHER 1-1

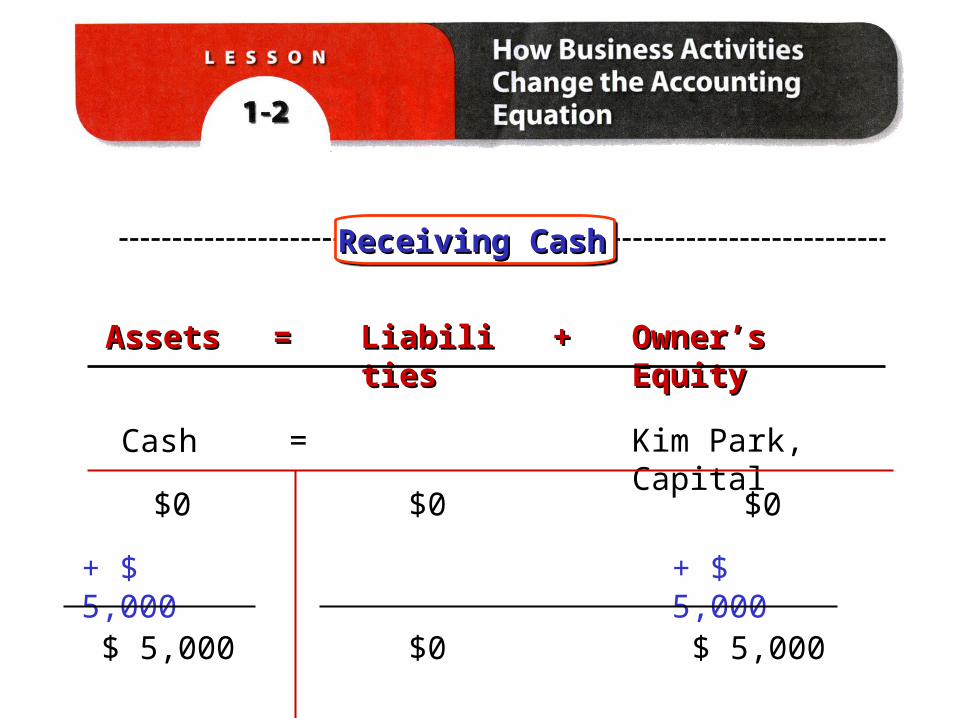

Receiving CashReceiving Cash

AssetsAssets == LiabilitiesLiabilities ++ Owner’s EquityOwner’s Equity

Cash Kim Park, Capital=

$0 $0 $0

+ $ 5,000 + $ 5,000

$ 5,000 $ 5,000$0

• TransactionTransaction– Business activity that changes assets, Business activity that changes assets,

liabilities, or owner’s equityliabilities, or owner’s equity

• AccountAccount– Record summarizing all information pertaining Record summarizing all information pertaining

to a single item in the accounting equationto a single item in the accounting equation

• Account TitleAccount Title– The name given to an accountThe name given to an account

• Account BalanceAccount Balance– The amount/value in an accountThe amount/value in an account

• CapitalCapital– Account used to summarize the owner’s equityAccount used to summarize the owner’s equity

AssetsAssets == LiabilitiesLiabilities ++ Owner’s Owner’s EquityEquity

=

$0

$0

- 275$0$ 5,000 $ 5,000

$0

Cash Kim Park, Capital+ Supplies Prepaid Insurance

+

$0 + 275

$ 4,725 $ 275 $0 $ 5,000 - 1,200 + 1,200

$ 3,525 $ 275 $1,200 $ 5,000

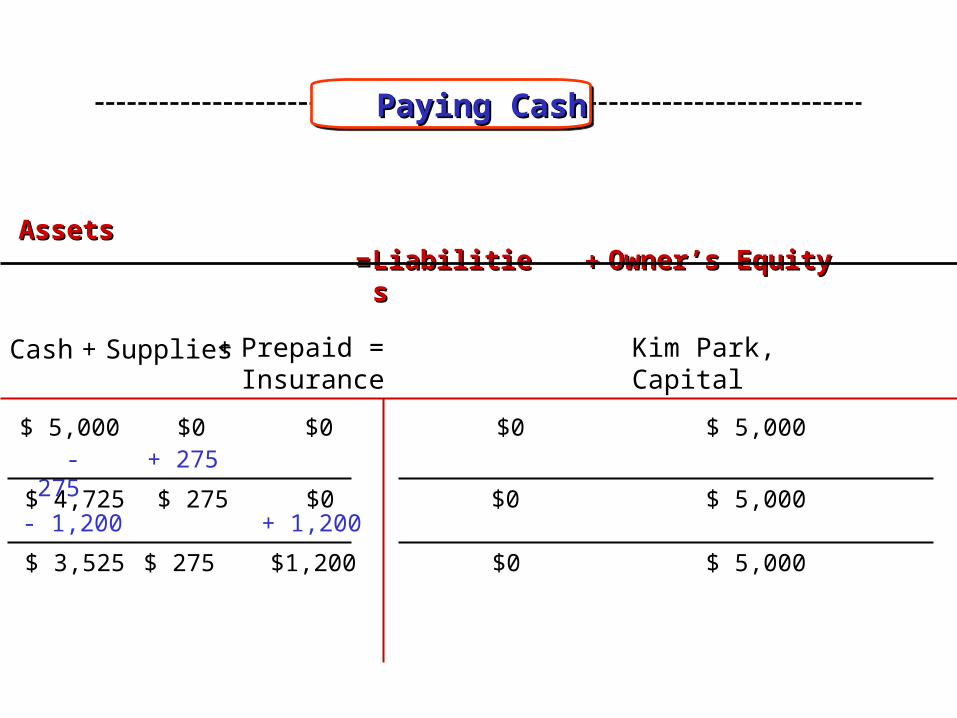

Paying CashPaying Cash

AssetsAssets == LiabilitiesLiabilities ++ Owner’s Owner’s EquityEquity

Cash Kim Park, Capital=+ Supplies Prepaid Insurance

+

$0 $3,525 $ 275 $1,200 $ 5,000

Accts. Pay. Supply Depot

+

+ 500 + 500

$3,525 $ 775 $1,200 $ 500 $ 5,000 - 300 - 300

$ 200 $3,225 $ 775 $1,200 $ 5,000

Transactions on AccountTransactions on Account

End of LessonEnd of Lesson REVIEWREVIEW

WORK TOGETHER 1-2WORK TOGETHER 1-2

Determining how transactions change an accounting equationDetermining how transactions change an accounting equation

Assets = Liabilities + Owner’s EquityTrans.No.

1.

2.

3.

4.

+ +

+ +

+ -- -

AssetsAssets == LiabilitiesLiabilities ++ Owner’s EquityOwner’s Equity

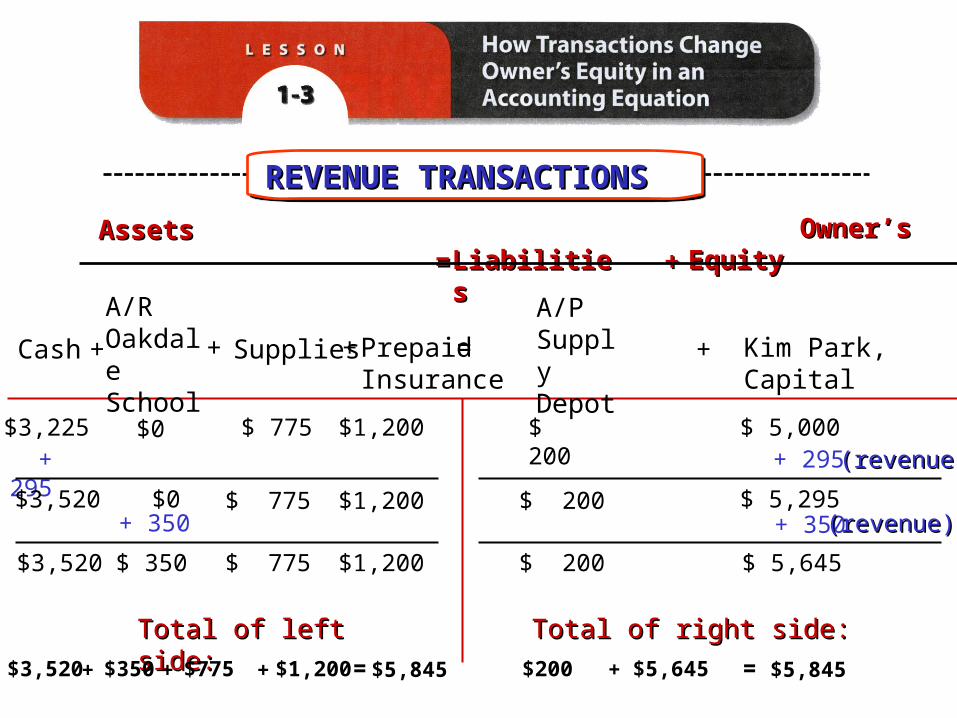

Cash Kim Park, Capital=

$ 775 + 295

$ 200$3,225 $ 5,000

+ Supplies Prepaid Insurance

+

+ 295

$3,520 $0 $ 5,295 + 350

$3,520 $ 350 $1,200 $ 5,645

+

A/R OakdaleSchool

A/P SupplyDepot

+

$0(revenue)(revenue)

$ 775

$ 775

$1,200

$1,200

$ 200

$ 200

+ 350 (revenue)(revenue)

Total of left side:Total of left side: Total of right side:Total of right side:

$3,520 $350 $1,200$775+ + + = $5,845 $5,845$200 $5,645+ =

REVENUE TRANSACTIONSREVENUE TRANSACTIONS

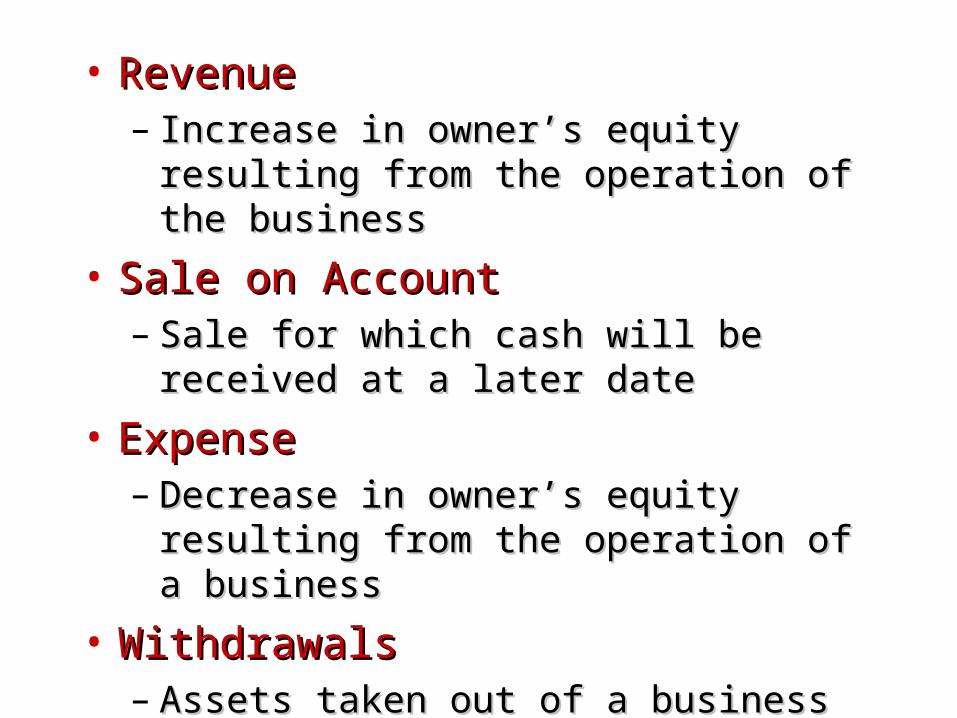

• RevenueRevenue– Increase in owner’s equity resulting from Increase in owner’s equity resulting from

the operation of the businessthe operation of the business

• Sale on AccountSale on Account– Sale for which cash will be received at a Sale for which cash will be received at a

later datelater date

• ExpenseExpense– Decrease in owner’s equity resulting from Decrease in owner’s equity resulting from

the operation of a businessthe operation of a business

• WithdrawalsWithdrawals– Assets taken out of a business for the Assets taken out of a business for the

owner’s personal useowner’s personal use

EXPENSE TRANSACTIONSEXPENSE TRANSACTIONS

AssetsAssets == LiabilitiesLiabilities ++ Owner’s EquityOwner’s Equity

Cash =

$ 775 - 300

$ 200$3,520 $ 5,645

+ Supplies Prepaid Insurance

+

- 300 (expense)

$ 350 $ 5,345 - 40

$3,180 $350 $1,200 $ 5,305

+

A/R OakdaleSchool

A/P SupplyDepot

+

$ 350

$ 775

$ 775

$1,200

$1,200

$ 200

$ 200

- 40 (expense)

Total of left side:Total of left side: Total of right side:Total of right side:

$350 $1,200$ 775+ + + = $ 5,505 $ 5,505$ 200 $ 5,305+ =

Kim Park, Capital

$3,220

$3,180

AssetsAssets == LiabilitiesLiabilities ++ Owner’s EquityOwner’s Equity

Cash Kim Park, Capital=

$ 775 + 200

$ 200$3,180 $ 5,305

+ Supplies Prepaid Insurance

+

- 200

$3,380 $150 $ 5,305 - 125

$3,255 $150 $1,200 $ 5,180

+

A/R OakdaleSchool

A/P SupplyDepot

+

$350

$ 775

$ 775

$1,200

$1,200

$ 200

$ 200

- 125 (withdrawal)(withdrawal)

Total of left side:Total of left side: Total of right side:Total of right side:

$3,255 $150 $1,200$ 775+ + + = $5,380 $ 5,380$ 200 $ 5,180+ =

OTHER CASH TRANSACTIONSOTHER CASH TRANSACTIONS

End of LessonEnd of Lesson REVIEWREVIEW

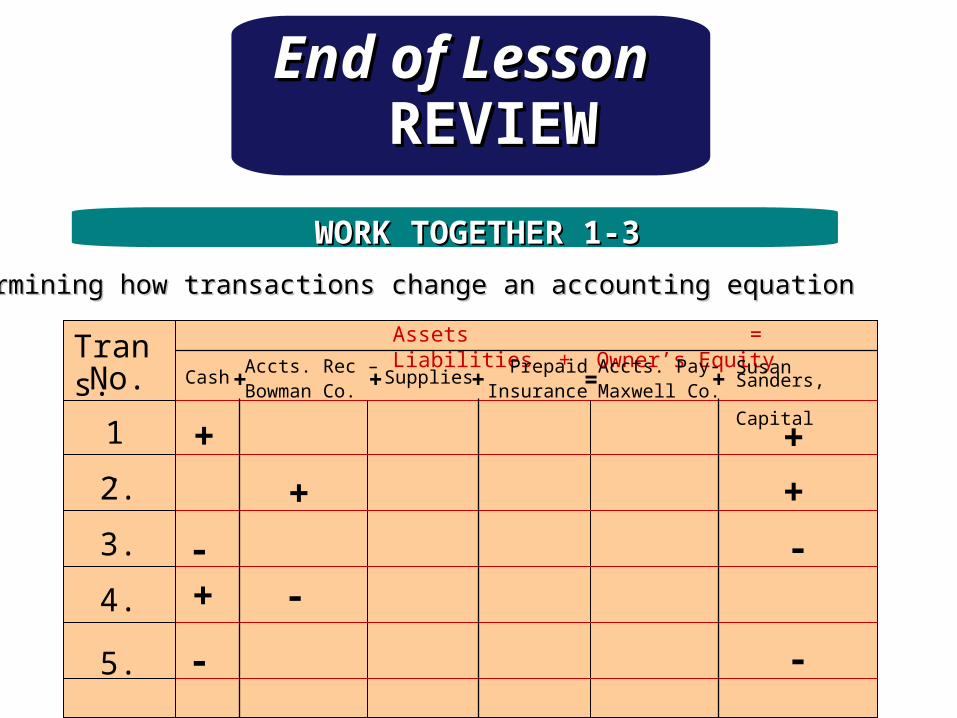

WORK TOGETHER 1-3WORK TOGETHER 1-3

Determining how transactions change an accounting equationDetermining how transactions change an accounting equation

Assets = Liabilities + Owner’s EquityTrans.No.

1.

2.

3.

4.

+ +

+ +

- -+ -

5. - -

CashAccts. Rec –Bowman Co.

Supplies PrepaidInsurance

Accts. Pay-Maxwell Co.

Susan Sanders, Capital

+ + + = +

• Standards and rules accountants Standards and rules accountants follow while recording and reporting follow while recording and reporting financial activities. financial activities. Written by FASBWritten by FASB

• Why is it necessary?Why is it necessary?• Users of financial statements rely on the Users of financial statements rely on the

information those statements contain. information those statements contain. • Consistent methods allow users to be confident of Consistent methods allow users to be confident of

the information’s validity.the information’s validity.

EXPLORE ACCOUNTINGEXPLORE ACCOUNTING(( ))

Related Documents