Accounting Manual For Small Cities and Towns in Minnesota A joint publication of: League of Minnesota Cities Minnesota Association of Townships Office of the State Auditor Intergovernmental Information Systems Advisory Council

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Manual

For

Small

Cities and Towns

in Minnesota

A joint publication of:League of Minnesota Cities

Minnesota Association of TownshipsOffice of the State Auditor

Intergovernmental InformationSystems Advisory Council

This page left blank intentionally

This document can be made available in alternative formats upon request.Call 651-296-2551 [voice] or 1-800-627-3529 [relay service]

Accounting Manualfor Small Cities andTowns in Minnesota

June 13, 2001

Government Information DivisionOffice of the State AuditorState of Minnesota

525 Park Street, Suite 400, St. Paul, MN [email protected]

This page left blank intentionally

TABLE OF CONTENTS

Forward . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Chapter 1 - The Accounting Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Chapter 2 - Accounting Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Receipts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Disbursements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Enterprise Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Payroll Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Bond and Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Record of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Reconcilement Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Cash Control . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Chapter 3 - Budgets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Chapter 4 - Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

APPENDICES

Appendix A - Duties of City/Town Clerks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Appendix B - Chart of Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Appendix C - Sample Forms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Appendix D - Sample Town Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Appendix E - Sample City Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Appendix F - Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 1

Foreword

The original project, including the 1988 edition of this manual, was undertaken by the Office of theState Auditor and the League of Minnesota Cities in cooperation with the Minnesota Association ofTownships. They received financial aid from the state government under a grant from theIntergovernmental Information Systems Advisory Council (IISAC).

This accounting manual was created to facilitate the designing of personal computer accountingsoftware for cities and towns in Minnesota. This manual accounting system has been designed forsmall cities and towns, depending on their needs and complexity. The system is designed to facilitatea smooth transition from a basic manual system to a computer system.

The following individuals gave of their time and expertise by serving on the 1988 ComputerProgram Advisory Committee:

John Asmus, Intergovernmental Information Systems Advisory Council

Dan Elwood, City of Spring Valley

Ed Fuller, Office of the State Auditor

Constance Haberle, Minnesota Association of Townships

Ann Houle, League of Minnesota Cities

Linda Luoma, Great Scott Township

Charlotte Patterson, City of Minnetrista

Helen Schendel, League of Minnesota Cities

Le Sears, Barclay Township

Roger Sell, Intergovernmental Information Systems Advisory Council

Judy Uhde, City of Bayport

Jean Woorster, Rice Lake Township

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor2

Introduction

This accounting manual outlines a simple and effective system of records and procedures for use insmall to medium sized towns and cities in Minnesota. The manual discusses the design of uniformaccounting procedures that will benefit clerks and other officials who deal with a relatively lowvolume of transactions.

These procedures can provide several benefits:

> Assist in the preparation ofY Interim financial reports,Y Annual financial statements,Y Budgets;

> Provide financial information necessary to the administrative functions of the mayorand council or town supervisors;

> Assist in the use of personal computers, spreadsheet templates, and accountingpackages;

> Facilitate auditor's work;

> Reduce audit costs.

Several publications are available from the League of Minnesota Cities (LMC), the MinnesotaAssociation of Townships (MAT) and the Office of the State Auditor (OSA) that contain additionalinformation in areas covered by this manual. They may be helpful in answering any questions raisedduring the use of this manual.

1. Handbook for Minnesota Cities (LMC)2. The Procedures for Paying City Claims (LMC)3. Guidelines for Preparing City Budgets (LMC)4. City Deposits and Investments (LMC)5. The Auditing of Municipal Accounts (LMC)6. Public Purpose Expenditures (LMC)7. Township Officer’s Handbook (MAT)8. Minimum Reporting Requirements (OSA)9. Minnesota Accounting and Financial Reporting Standards (OSA)

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 3

Additionally, the following publications are recommended for purchase from the publishers.

Codification of Governmental Accounting and Financial Reporting Standards and OriginalPronouncements, as of June 30, 2000, 2000-2001 Edition, published by the GovernmentalAccounting Standards Board (GASB), 401 Merritt 7, P.O. Box 5116, Norwalk, CT 06856-5116.

Minnesota Legal Compliance Audit Guide for Local Government, published by the Office of theState Auditor, Suite 400, 525 Park Street, St. Paul, Minnesota 55103.

2001 GAAFR, published by the Government Finance Officers Association, 180 N. Michigan Avenue,Suite 800, Chicago, II 60601-7476.

Duties of Clerks under Minnesota Statutes

Generally, the statutes provide for keeping a minute book, an ordinance book, and an account bookin which all receipts and orders drawn upon the treasurer are recorded. The clerk is the designatedcustodian of records of the city or town and acts as the custodian of its seal and records, and doesmany other specific duties.

The complete text of Minnesota Statutes Sec. 412.151 duties of the city clerk, and the complete textof Minnesota Statutes Sec. 367.11 duties of the town clerk are in Appendix A.

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 5

Chapter 1The Accounting Process

Accounting is the recording, classifying, and summarizing of transactions in a useful manner, andinterpreting the results.

Any accounting system should start with a budget, prepared and approved before the accountingperiod begins.

A system of accounts in which transactions are recorded and summarized on a current basis canimmediately provide financial information to the mayor and council, or the board of supervisorsconcerning revenues, expenditures, comparisons to budget, and cash balances. The information isavailable on ledger accounts for immediate reference, or for the preparation of interim financialstatements, and year-end financial statements. The information is auditable and can lead tosignificant savings in the costs of an audit.

Essential Accounting Tools

Revenues

1. Annual revenue budget (including account codes)

2. Blank pre-numbered receipts

3. Blank receipt register sheets

4. Blank receipt ledger cards

5. Blank revenue report form

Expenditures

6. Annual expenditure budget (including account codes)

7. Blank pre-numbered checks

8. Blank claims

9. Blank disbursement register sheets

10. Blank disbursement ledger cards

11. Blank disbursement report form

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor6

Revenue Process

Expenditure Process

Figure 1

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 7

Funds

The General Fund is used in municipal finance administration for all financial resources that are notrequired to be accounted for in another fund. This encompasses the day-to-day operation of thegovernmental unit. Other fund types are used to help insure that certain receipts set aside for specificpurposes will be used for the purposes intended. This may be either for control as in a water utilityor municipal liquor store operation, or to comply with a legal requirement such as a tax levyauthorized for a specific purpose.

Types of Funds

Governmental Funds

1. General Fund2. Special Revenue Funds

Cities: Library, CDBG, ParkTowns: Road and Bridge, Fire, Cemetery

3. Capital Projects Funds4. Debt Service Funds

Proprietary Funds

1. Enterprise Funds2. Internal Service Funds

Fiduciary Funds

1. Trust and Agency Funds

Funds should be kept to a minimum number and should not be established merely for conveniencein separating certain classes of receipts or disbursements. Maintain the minimum number of fundsnecessary to meet legal and operating requirements. The clerk should determine the funds necessaryfor financial operation of the town or city and should secure a resolution by the board or councilauthorizing their establishment.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor8

Separate funds should be created under the following conditions:

1. Special Revenue Fund: As required by law or contractual agreement. When the lawrequires that a fund be created to administer certain receipts.

2. Capital Projects Fund: To receive and disburse the money from a bond issue.Bonds are authorized for specific purposes. The expenditure of the money obtainedfrom a bond issue for other than authorized purposes is usually illegal. To helpprevent illegal expenditures of money from a bond issue, the money should be placedin a separate fund. First, this designates bond proceeds for a specific purpose.Second, since each fund requires a separate accounting, a separate fund makes iteasier to control expenditures of the money from a bond issue. A capital projects fundis temporary in nature. When the project for which the bonds were issued iscompleted any remaining money should be transferred to the debt service fund unlessa different disposition is authorized by law.

3. Enterprise Fund: For each enterprise, such as water or sewer, operated by a townor city. Enterprise funds should be operated on a self-supporting basis. A separatefund makes it possible to determine the actual cost of operating the enterprise. Thisinformation can be used to determine a rate schedule for the utility as well as tocontrol and manage revenues and expenses.

Bank Accounts

How many bank accounts should a city or town maintain? This can vary with circumstances and isalways a matter of discretion for the city or town, but generally one bank account is sufficient. Oneaccount simplifies control of funds and makes the reconciliation of the bank balance much easier.A common, but not necessary, exception is a separate account for a municipal liquor store or anotherenterprise fund.

The city council or town board must designate the official depository for the funds at the beginningof each year. The depository so designated must furnish collateral for any funds on deposit in excessof the amount covered by insurance ($100,000 currently). This is especially important because anumber of depositories have failed as a result of deficient lending and borrowing policies.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 9

Chapter 2Accounting Procedures

Accounting Forms

The following forms have been designed to enable the clerk to fulfill the duties prescribed by statute:

1. Receipt: The original record of money received.

2. Claim: A form for the declaration of a claim against the city or town requestingpayment.

3. Order-Check: The instrument whereby money is disbursed.

4. Receipts Register: The chronological record of all receipts.

5. Disbursements Register: The chronological record of all disbursements.

6. Receipts Ledger: The record in which receipts are classified by source.

7. Disbursements Ledger: The record in which the disbursements are classified byfunction or activity and object.

8. Record of Bond Issue: A record of bond maturities, interest, and fiscal chargespayable.

9. Record of Investments: A record of bonds or certificates held for investment.

10. Employee Earnings Record: The record of earnings information for each employee.

11. Payroll Register (Journal): The record of time, earnings, deductions, and net payfor all employees by payroll period.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor10

Receipts

Receipt forms should be in triplicate and pre-numbered by the printer. The original is given to theperson making the payment. One copy is for the treasurer's records, and one copy is the clerk'srecord. If the offices of clerk and treasurer are combined as clerk/treasurer, only the original and onecopy are needed.

A separate receipt should be issued for all money received, including amounts received by mail suchas tax apportionments from the county treasurer and state shared taxes or grants from the state. Inthese cases the original receipt should be attached to the detailed statement accompanying theremittance and kept on file.

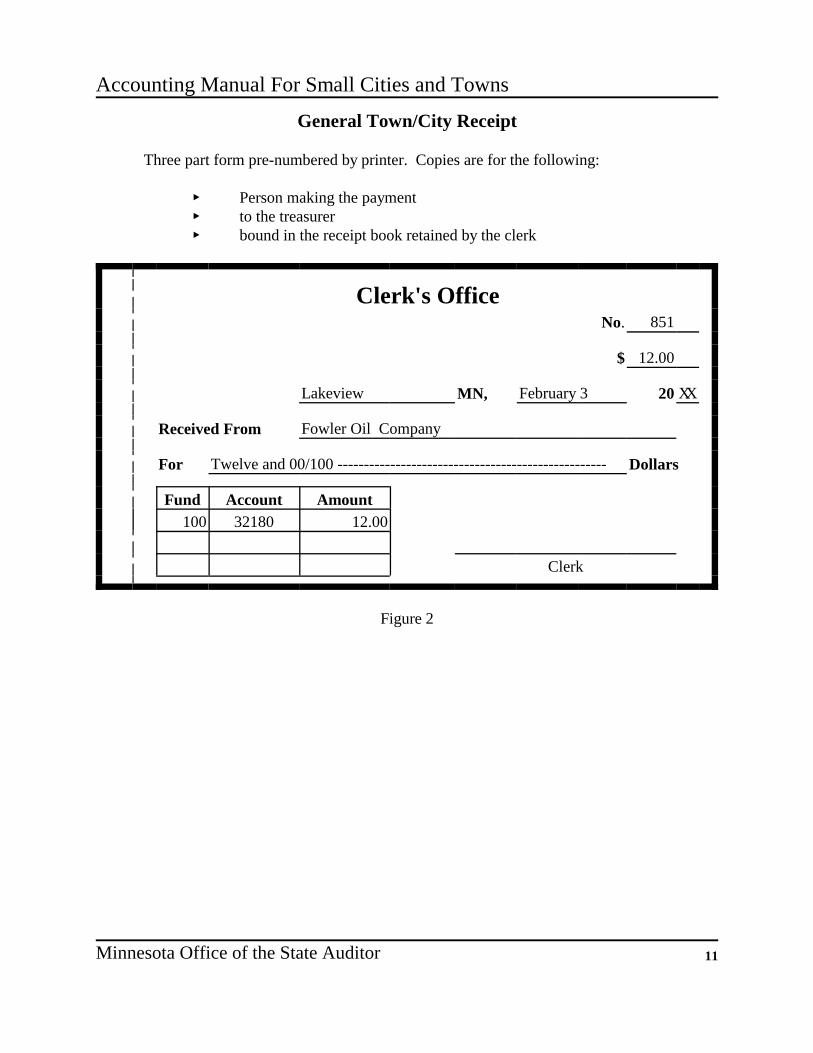

On page 11 is a sample form of a general receipt. This form provides spaces for all informationpertaining to the receipt of the money. The information must be filled in at the time of the transactionand is necessary for making entries in the accounting records and for providing supportingdocumentation for all receipts. Issuing the receipt is the first step in the recording of receipts andshould be done immediately upon receiving the payment.

The example on the following page has been filled in with an actual transaction. A total payment of$12 was received from the Fowler Oil Co. for a cigarette license on February 3, 20XX. This paymentwas allocated to the General Fund (100), Licenses and Permits (Account 32180).

Cash received should be deposited intact with the treasurer or in the depository each day. If themoney is deposited with the treasurer, it should be accompanied by the treasurer's copies of thereceipts, and the treasurer should make out the daily deposit. If the money is deposited directly inthe depository by the clerk, a copy of the deposit slip and the treasurer's copies of the receipts shouldbe furnished to the treasurer.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 11

General Town/City Receipt

Three part form pre-numbered by printer. Copies are for the following:

Y Person making the paymentY to the treasurerY bound in the receipt book retained by the clerk

Clerk's OfficeNo. 851

$ 12.00

Lakeview MN, February 3 20 XX

Received From Fowler Oil Company

For Twelve and 00/100 --------------------------------------------------- Dollars

Fund Account Amount100 32180 12.00

Clerk

Figure 2

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor12

Receipts Register

The receipts register is a chronological record of cash received. The recommended form for theregister is shown below. It contains an amount column for the total amount of the cash received, andfund columns for the amounts attributable to each fund. The register provides the information neededto prepare the monthly or annual summaries of cash received by fund. Figure 3 is a sample sectionfrom a page of the register. Forms may be obtained from printers specializing in forms formunicipalities.

RECEIPTS REGISTER

Month Of: February City/Town of Lakeview Page Reference No. 8

From WhomReceived

For WhatPurpose Date

ReceiptNumber Amount

AccountNumber

GeneralFund Fund

Fowler Oil Company Cigarette License 2/3 851 12 00 100-32180 12 00

Figure 3

Good accounting procedures require that the clerk make entries promptly in the register and ledgers.

Using the same transaction through the recording of the receipt from Fowler Oil Co. to the receiptsregister (Figure 3): First enter the name of the person from whom the money was received, date andreceipt number, and amount received.

Figure 3 shows that "Fowler Oil Co. " has been recorded. The next column is for a brief statementof the source (purpose) of the revenue. Here we have entered "Cigarette License" from the receiptform and, as on the form, this entry should be simple and to the point. In the next three columns thedate, receipt number, and amount have been entered. The next column is for the fund (100) andaccount number (32180) of the receipt (100-32180). The next step is to enter the total in theappropriate fund column. The recommended chart of accounts is contained in Appendix B of thispublication and is a condensed version of the chart of accounts for cities and towns. The larger, morecomplete chart of accounts is available from the Office of the State Auditor.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 13

Receipts Ledger

The receipts ledger is designed to provide a classification of revenues by source for each fund. Aledger card is prepared for each major revenue source. The forms are sufficiently flexible so that theymay be used for all funds. Figure 4 is a sample section from a page of the receipts ledger for theGeneral Fund. Figure 5, on page 14, shows the entire procedure for recording the cash receiptsexample: receipt form, cash receipts register, and cash receipts ledger.

RECEIPTS LEDGER

General Fund

Account No. 100-32180 Sheet No. 1

Source Original Budget 144.00

Account Name Cigarette License Fees Revised Budget

DateReceipt

No. Received FromAmountReceived

Month to DateReceived

Year to DateReceived

BudgetBalance

1/1/XX Budget 144 00

2/3/XX 851 Fowler Oil Company 12 00 12 00 12 00 132 00

Figure 4

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor14

RECEIPTSThe Flow of Receipt Transactions

1. RECEIPT FORM

Clerk's OfficeNo. 851

$ 12.00

Lakeview MN, February 3 20 XX

Received From Fowler Oil CompanyFor Twelve and 00/100 ------------------------------------------------ Dollars

Fund Account Amount100 32180 12.00

Clerk

2. RECEIPTS REGISTER

Month Of: February City/Town of Lakeview Page Reference No. 8

From WhomReceived

For WhatPurpose Date

ReceiptNumber Amount

AccountNumber

GeneralFund Fund

Fowler Oil Company Cigarette License 2/3 851 12 00 100-32180 12 00

3. RECEIPTS LEDGERGeneral Fund

Account No. 100-32180 Sheet No. 1

Source Original Budget 144.00

Account Name Cigarette License Fees Revised Budget

DateReceipt

No. Received FromAmountReceived

Month to DateReceived

Year to DateReceived

BudgetBalance

1/1/XX Budget 144 00

2/3/XX 851 Fowler Oil Company 12 00 12 00 12 00 132 00

Figure 5

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 15

DisbursementsForms designed to record disbursements are as follows:

1. Claims2. Order-Checks3. Disbursements Register4. Disbursements Ledger5. Subsidiary Payroll Records.

Claims

All payments must be supported by an approved claim. Claims should be prepared for every checkto be issued. Claims should be approved by the city council or town board regularly and a list of theapproved claims should be recorded in the minutes. After a claim has been approved a check shouldbe prepared, the claim should be marked "PAID,” and the date and check number entered on theclaim and coded for posting.

Order-Checks

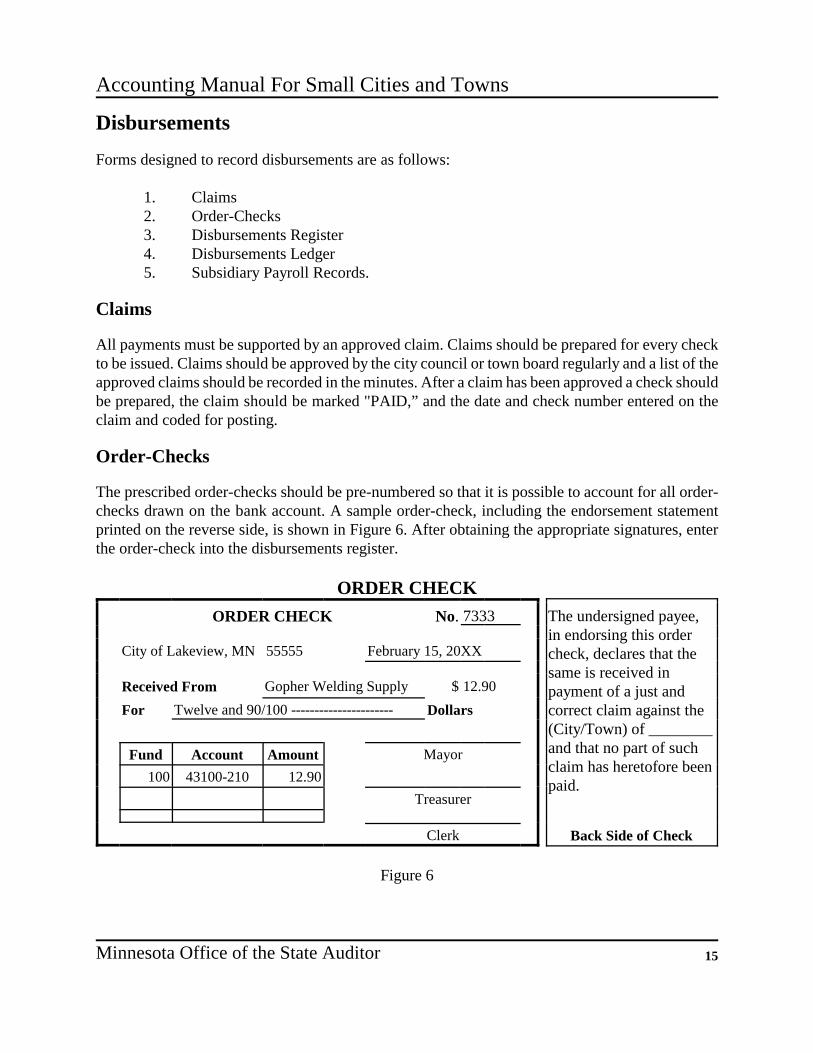

The prescribed order-checks should be pre-numbered so that it is possible to account for all order-checks drawn on the bank account. A sample order-check, including the endorsement statementprinted on the reverse side, is shown in Figure 6. After obtaining the appropriate signatures, enterthe order-check into the disbursements register.

ORDER CHECKORDER CHECK No. 7333 The undersigned payee,

in endorsing this ordercheck, declares that thesame is received inpayment of a just andcorrect claim against the(City/Town) of ________and that no part of suchclaim has heretofore beenpaid.

City of Lakeview, MN 55555 February 15, 20XX

Received From Gopher Welding Supply $ 12.90For Twelve and 90/100 ---------------------- Dollars

Fund Account Amount Mayor100 43100-210 12.90

Treasurer

Clerk Back Side of Check

Figure 6

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor16

Disbursements Register

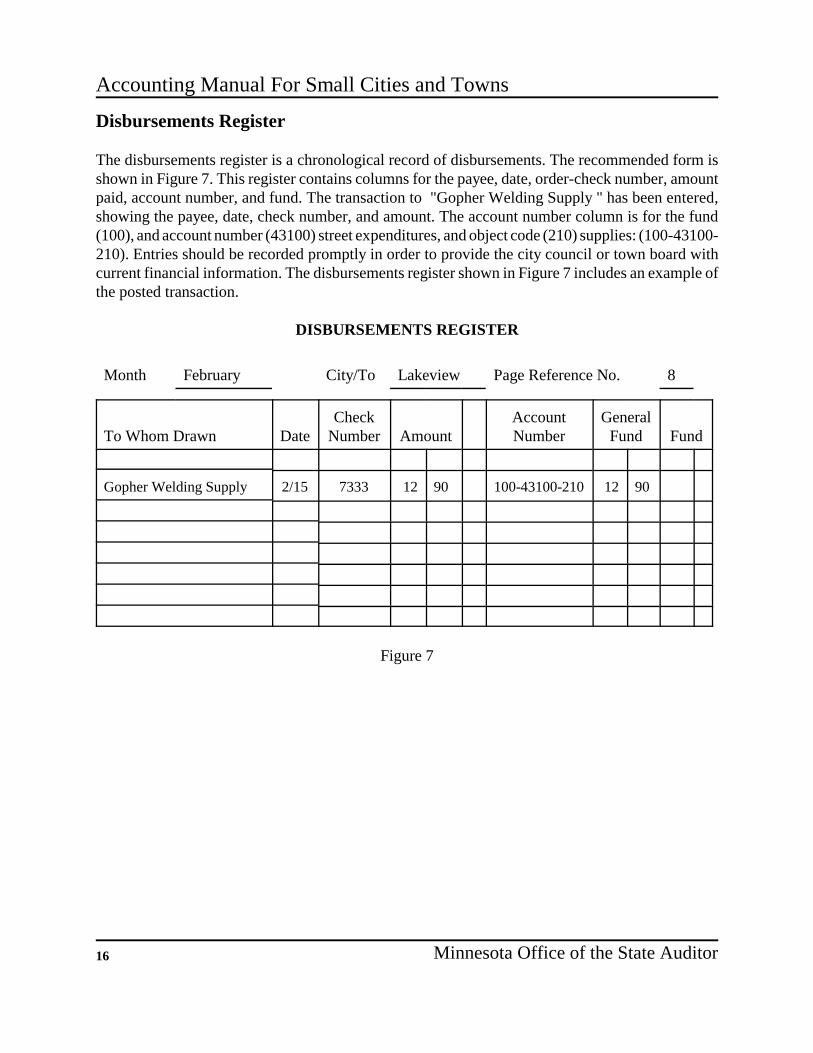

The disbursements register is a chronological record of disbursements. The recommended form isshown in Figure 7. This register contains columns for the payee, date, order-check number, amountpaid, account number, and fund. The transaction to "Gopher Welding Supply " has been entered,showing the payee, date, check number, and amount. The account number column is for the fund(100), and account number (43100) street expenditures, and object code (210) supplies: (100-43100-210). Entries should be recorded promptly in order to provide the city council or town board withcurrent financial information. The disbursements register shown in Figure 7 includes an example ofthe posted transaction.

DISBURSEMENTS REGISTER

Month February City/To Lakeview Page Reference No. 8

To Whom Drawn DateCheck

Number AmountAccountNumber

GeneralFund Fund

Gopher Welding Supply 2/15 7333 12 90 100-43100-210 12 90

Figure 7

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 17

Disbursements Ledger

Disbursements ledgers are similar in function to receipts ledgers in that they provide a classificationof the transaction. While receipts are classified by source, disbursements are classified by function,activity and object. Function relates to the purpose of the expenditure and activity relates to thespecific work performed to accomplish the function. A sample of a recommended disbursementsledger card is shown in Figure 8.

When disbursements are posted to a disbursements ledger the relationship between the actual amountdisbursed and the budgeted amount can readily be determined.

When the entries in the disbursements register have been completed, checked, and balanced, theclerk should post from the register to the ledger. Posting should be done on a regular basis, at leastmonthly. It is not necessary to post in detail, but rather a summary posting of totals by fund, accountnumber, and object may be made. A monthly recap may be prepared in the disbursements register,summarizing transactions for the month by fund and account. This can then serve as the postingsource to the ledgers.

DISBURSEMENTS LEDGER

General Fund

Account No. 100-43100-210 Sheet No. 1

Activity Street Maintenance Original Budget 1,800

Object Operating Supplies Revised Budget

DateCheck

No. DescriptionAmount

DisbursedMonth to Date

DisbursedYear to Date

DisbursedBudgetBalance

1/1/XX Budget 1,800 00

2/15/XX 7333 Gopher Welding Supply 12 90 12 90 12 90 1,787 10

Figure 8

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor18

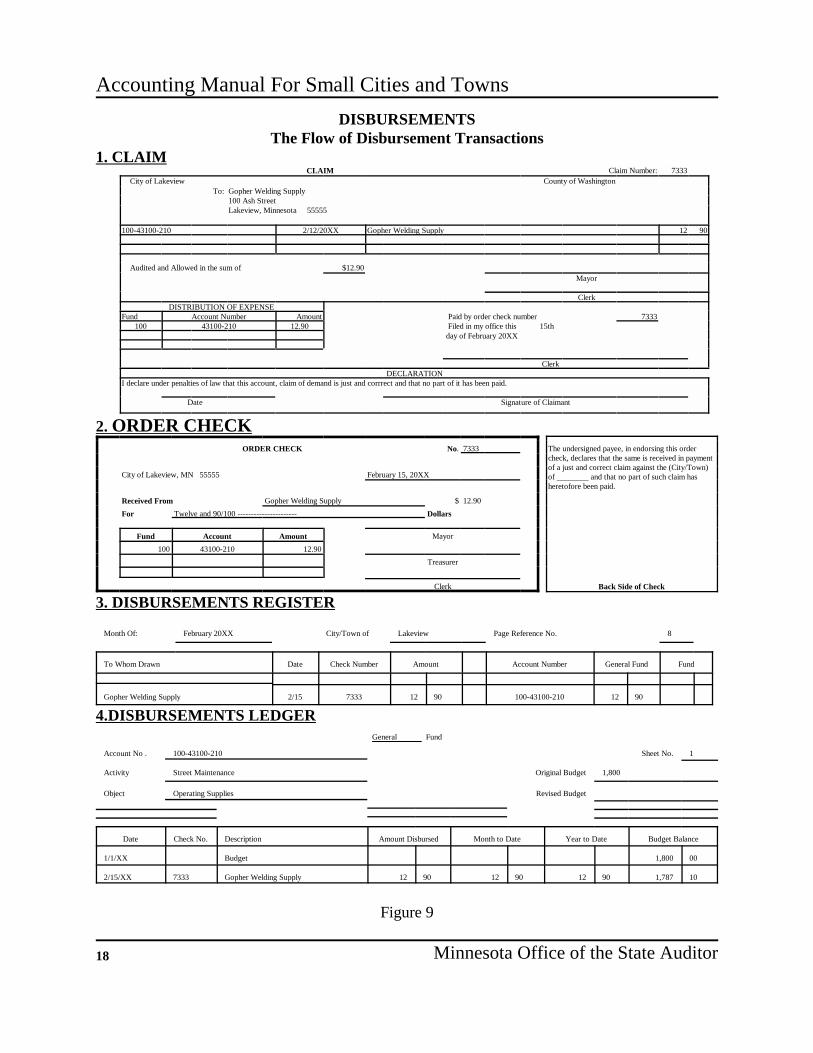

DISBURSEMENTSThe Flow of Disbursement Transactions

1. CLAIMCLAIM Claim Number: 7333

City of Lakeview County of WashingtonTo: Gopher Welding Supply

100 Ash StreetLakeview, Minnesota 55555

100-43100-210 2/12/20XX Gopher Welding Supply 12 90

Audited and Allowed in the sum of $12.90Mayor

ClerkDISTRIBUTION OF EXPENSE

Fund Account Number Amount Paid by order check number 7333100 43100-210 12.90 Filed in my office this 15th

day of February 20XX

ClerkDECLARATION

I declare under penalties of law that this account, claim of demand is just and corrrect and that no part of it has been paid.

Date Signature of Claimant

2. ORDER CHECKORDER CHECK No. 7333 The undersigned payee, in endorsing this order

check, declares that the same is received in paymentof a just and correct claim against the (City/Town)of ________ and that no part of such claim hasheretofore been paid.

City of Lakeview, MN 55555 February 15, 20XX

Received From Gopher Welding Supply $ 12.90For Twelve and 90/100 ---------------------- Dollars

Fund Account Amount Mayor100 43100-210 12.90

Treasurer

Clerk Back Side of Check

3. DISBURSEMENTS REGISTER

Month Of: February 20XX City/Town of Lakeview Page Reference No. 8

To Whom Drawn Date Check Number Amount Account Number General Fund Fund

Gopher Welding Supply 2/15 7333 12 90 100-43100-210 12 90

4.DISBURSEMENTS LEDGERGeneral Fund

Account No . 100-43100-210 Sheet No. 1

Activity Street Maintenance Original Budget 1,800

Object Operating Supplies Revised Budget

Date Check No. Description Amount Disbursed Month to Date Year to Date Budget Balance

1/1/XX Budget 1,800 00

2/15/XX 7333 Gopher Welding Supply 12 90 12 90 12 90 1,787 10

Figure 9

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 19

Enterprise Funds

Enterprise funds account for activities that are usually financed and operated in a manner similar toprivate business enterprises or when it is important to control or measure costs. The accrual basisof accounting as used for business enterprises is also recommended for municipal enterprise funds.Examples of enterprise funds are water, sewer, and municipal liquor operations. Individual typesof enterprise services should be accounted for in separate funds. This separation is necessary todetermine the cost of providing each service and to assure that the resources of one enterprise arenot used by another.

The financial statements of the enterprise fund should include a balance sheet, an operating statementand a statement of changes in financial position. The operating statement shows the operatingrevenues, (user charges), operating expenses (including depreciation), operating income, non-operating revenues and expenses, and net income. See Figure 10 below.

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN RETAINED EARNINGS

Water Fund

Operating revenues ................................................................................................. 82,817

Operating expenses ................................................................................................. 84,643

Operating Income ............................................................................................... (1,826)

Non-operating revenues (expenses)

Interest Income .............................................................................................. 6,821

Miscellaneous Income .................................................................................... 520

Total non-operating revenues (expenses) .................................................. 7,341

Income before operating transfers ....................................................... 5,515

Operating transfers out - Transfers .......................................................................... (10,000)

Free service provided ........................................................................................... (1,573)

Total operating transfers out ........................................................................... (11,573)

Net Income .............................................................................................. (6,058)

Retained earnings January 1..................................................................................... 954,555

Retained earnings - December 31 ............................................................................ 948,497

Figure 10

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor20

Payroll Accounting

The following forms have been designed to record the payroll.

1. Payroll Register (Journal)

2. Order-Check

3. Employee's Earning Record

Payroll Register (Journal)

The payroll register is a record of all payroll checks written for a payroll period. The recommendedform is shown in Figure 11. This register contains columns for the name of employee, hours worked,gross earnings, deductions, net pay, date, and order-check number. When the payroll has beencompleted order-checks should be written for each employee in the amount of the net pay and to theproper agencies for amounts withheld at the appropriate time, in accordance with the applicable rulesand regulations. The register should be balanced before any checks are issued. The order-checknumber should then be recorded in the payroll or disbursements register. The gross earnings shouldbe posted to the appropriate function or activity in the disbursements ledger as indicated by theaccount number. Only the total gross earnings for all employees should be posted in thedisbursements ledger along with the beginning and ending order-check numbers.

PAYROLL REGISTERPeriod from ________ 20___ to _________ 20___ Sheet No. _____ of _____ Sheets

Deductions

Hours Earnings Less Taxable Federal State Net Check

Name Reg O.T. Regular O.T Gross PERA Wages W.H. Tax FICA W.H. Tax Amount Date No.

Figure 11

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 21

Order-Check

A special order-check has been designed to provide the employee with a record of gross pay,deductions, and net pay as shown in Figure 12. If your check does not follow this design, a separatestatement of earnings and deductions should be provided to the employee.

ORDER-CHECK

No. 0000

City of _______________________, MN 55555 _______________ 20___

Pay to

The order of ____________________________________________ $____________

____________________________________________________________ Dollars

For Payroll

Fund Account Amount

Mayor

Treasurer

Clerk

Period Hours Gross Deductions Net

Reg OT Pay W.H. TAX Retire Pay

Figure 12

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor22

Employee's Earnings Record

A record of each employee's salary, deductions, and net pay must be kept in order to prepare requiredfederal and state quarterly payroll returns, and the required year-end forms, as well as the "W-2"form at the end of the calendar year. The form shown in Figure 13 has been designed to provide thisinformation. A separate sheet should be kept for each employee with the name and Social Securitynumber shown at the top of the page. The necessary quarterly or year-end information is obtainedby totaling and balancing the columns. Net pay plus ALL withholdings equals the gross pay.

EMPLOYEE'S INDIVIDUAL EARNINGS RECORDName _____________________________ Social Security Number ________________Address ___________________________ Date Employed _______________________

____________________________ Date Terminated ______________________PERA Plan __________________________

INCOME TAX DATAEffective Date _________ ___ Single ________________________No. of Withholdings _________ ___ Married ________________________Additional Withholdings _________ ________________________Hourly Rate of Salary _________ ________________________

Deductions Order

Hours Earnings Federal State Net Check

Reg. O..T. Reg. O.T. Gross W.H. Tax P.E.R.A. F.I.C.A. W.H. Tax Amount Date No.

1

2

3

4

5

6

7

Total forQuarter

TotalsYear-to-date

1

Figure 13

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 23

Bond and Interest

Record of Indebtedness

Bonds are issued to provide money for construction or improvements. When bonds are issued, theclerk should establish a capital projects fund to ensure that the proceeds received are disbursed onlyfor the intended purpose. A debt service fund should be established to record the receipts designatedfor bond payments, and the bond and interest payments.

Statutory cities may issue certificates of indebtedness for tax anticipation purposes (Minn. Stat. Sec.412.261), and for certain equipment purchases (Minn. Stat. Sec. 412.301). Towns can issuecertificates for any lawful purpose (Minn. Stat. Sec. 366.095).

Bond and Interest Record

The bond and interest record form is shown on page 58. This record contains all the informationrelating to the bond or certificate of indebtedness issues and should be filled in when the informationbecomes available.

Bond Maturity Record

The bond maturity record provides a record of all payments of principal, interest, and fiscal agentfees during the period in which the bonds are to be retired. As each payment is made, the date ofpayment should be entered in the last column. The bond maturity record should be kept current sothat the Statement of Indebtedness (Form Dl) can be prepared and returned to the county auditor.

BOND MATURITY RECORD

Paying

Date Bond Principal Interest Total Agent Date

Due Numbers Due Due Due Charges Paid

Figure 14

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor24

Record of Investments

Towns and cities should review their immediate cash needs throughout the year and invest any idlefunds to provide additional revenue. Investments should be kept simple and should of course be incompliance with Minnesota Statutes. This means investing in passbook savings, certificates ofdeposit, or other authorized short-term investments. Safety of principal and availability are primaryconsiderations. Collateral is required whenever investments exceed the $100,000 FDIC coveragefor bank CDs, just as in the case of FDIC and checking accounts. The excess amount must beprotected by a bond or collateral, which at market value is at least 10 percent more than the excessdeposit.

A record of all investments should be kept to maintain control over investments and to ensure thatthe city or town receives the correct interest payments as they become due. A record of investmentsshould have columns for the date purchased, description of the investment, date of maturity purchaseprice, date sold, and the proceeds when sold. All investment transactions must be recorded in thedisbursements register or receipts register at the time the investment is purchased or sold. A sampleform for the recording of investments is included in Appendix C, on page 57.

Reconcilement Procedures

The receipts register and the disbursements register should be totaled and balanced at the end of eachmonth. The total column in each register should equal the totals of all the fund columns (crossfoots).Year-to-date running totals of cash receipts and disbursements are very important, and providecontrol over the entire accounting system. Once the totals are accurately balanced, they may beposted to the cash control (Figure 15). Next the columns on the receipts and disbursements ledgersshould also be totaled. Totals of the receipts ledgers should equal the totals in the receipts register.Likewise, totals of the disbursements ledgers should also equal the totals in disbursements register.The receipts and disbursements registers and ledgers should also be balanced by fund.

The clerk's cash balance must also be reconciled with the bank balance at the end of each month.Compare cancelled order-checks to the clerk's disbursements register and make a list of outstandingchecks. Also, compare deposits with the receipts register and make a list of the deposits-in-transit.The bank balance plus the deposits-in-transit minus the total outstanding checks should equal theclerk's balance less any bank charges. This can be accomplished by using the cash control shown inFigure 15.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 25

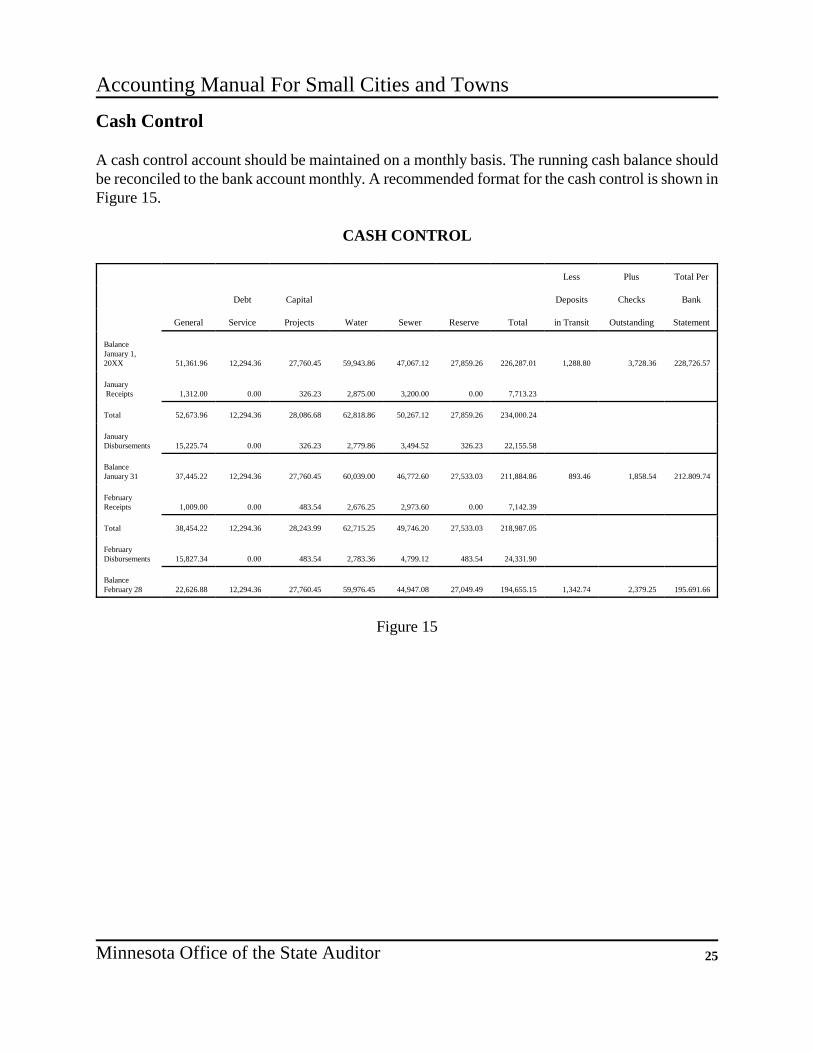

Cash Control

A cash control account should be maintained on a monthly basis. The running cash balance shouldbe reconciled to the bank account monthly. A recommended format for the cash control is shown inFigure 15.

CASH CONTROL

Less Plus Total Per

Debt Capital Deposits Checks Bank

General Service Projects Water Sewer Reserve Total in Transit Outstanding Statement

Balance January 1,20XX 51,361.96 12,294.36 27,760.45 59,943.86 47,067.12 27,859.26 226,287.01 1,288.80 3,728.36 228,726.57

January Receipts 1,312.00 0.00 326.23 2,875.00 3,200.00 0.00 7,713.23

Total 52,673.96 12,294.36 28,086.68 62,818.86 50,267.12 27,859.26 234,000.24

JanuaryDisbursements 15,225.74 0.00 326.23 2,779.86 3,494.52 326.23 22,155.58

Balance January 31 37,445.22 12,294.36 27,760.45 60,039.00 46,772.60 27,533.03 211,884.86 893.46 1,858.54 212.809.74

FebruaryReceipts 1,009.00 0.00 483.54 2,676.25 2,973.60 0.00 7,142.39

Total 38,454.22 12,294.36 28,243.99 62,715.25 49,746.20 27,533.03 218,987.05

FebruaryDisbursements 15,827.34 0.00 483.54 2,783.36 4,799.12 483.54 24,331.90

BalanceFebruary 28 22,626.88 12,294.36 27,760.45 59,976.45 44,947.08 27,049.49 194,655.15 1,342.74 2,379.25 195.691.66

Figure 15

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 27

Chapter 3Budgets

Although budgets are not required by law for townships or most cities of under 2,500 population,they are essential to good fiscal management by the council or town board. Without a budget thegoverning body can only make general estimates of expenditures and revenue required for the nextyear. This can result in either levying more taxes than necessary or in not providing enough revenueto carry out municipal functions.

In order for the governing body to determine the amount of expenditures needed to carry outmunicipal activities in the next year, it is recommended that these amounts be based on pastexperiences. Anticipated revenue for the coming year can be estimated on the basis of revenuereceived in the past and on projections by the Minnesota Revenue Department. The historicalinformation is found in the clerk's records. Unless the city or township has a finance director, it isusually the clerk's duty to prepare the budget.

Budget Preparation

State law provides that property tax levies must be certified to the county auditor by October 25 eachyear. In order for the governing body to determine the amount of taxes to levy, budget preparationfor the coming year should begin about three months before October 25. Under the "Truth inTaxation Law," cities of over 2,500 population must adopt proposed budgets and certify them to thecounty auditor by August 1, so their budget preparation should begin in April.

The first step in budget preparation is to list all sources of revenue and all expenditures by function.Columns should be provided for the preceding year, the current year and the next year for which thebudget is being prepared. The amounts for the preceding year should be taken from that year's annualfinancial statement. The amounts for the current year should be the budgeted amounts since actualamounts are not yet available. The amounts for the next year will be the budgeted revenue andexpenditures determined by the council. (See sample form, page 29.) Only some of the revenuesources and expenditure categories are listed. Others may be added as necessary.

After the clerk has prepared the forms and supplied the information for the first two years, the budgetshould be presented to the council or town board for its determination of amounts required for eachexpenditure item for the next year. The governing body may prefer that department heads preparebudget requests that the clerk assembles into the preliminary budget. Whichever method is used, theexpenditure amounts are added to arrive at the total. The revenues should also be reviewed and theanticipated amount from each source entered on the form. The total amount together with theanticipated balance or deficit from the current year will be the amount available to meet the budgetedexpenditures. If projected expenditures exceed the anticipated revenues, the governing body mustdecide which expenses should be lowered or how to raise revenue to balance the budget. Of course,

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor28

if projected revenues exceed expenditures, a reduction may be made in the amount of property taxesto be levied.

Although the foregoing has dealt only with the general fund, the same procedures should be followedwith each of the other funds. The council or town board may also want to prepare and adopt a multi-year capital expenditure program and budget. This would match available resources with proposedpublic improvements, facilities, and needed equipment.

When the budget has been completed for all funds and the property tax levy has been determined,the governing body should hold a public hearing. Although a hearing is required by law only forcities over 2,500 in population, it is a good idea to get citizen input. After adoption of the finalbudget and tax levy, the clerk should send the total tax levy to the county auditor. Cities over 2,500population must also certify compliance with the “Truth in Taxation Law” to the MinnesotaDepartment of Revenue.

Using the adopted budget, the clerk should prepare periodic reports for the city council or town boardshowing budgeted amounts and expenditures to date for each category. This allows the governingbody not only to compare actual expenditures to the budget, but also to adjust budget amounts ifnecessary.

Further information on budgeting is contained in the League of Minnesota Cities publication,"Guidelines for Preparing City Budgets," and the towns can refer to the "Township Officer’sHandbook " by the Minnesota Association of Townships. These publications are updated annually.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 29

City Summary Budget Statement

The purpose of this report is to provide summary 20X2 budget information concerning the City of Lakeview to interestedcitizens. The budget is published in accordance with Minn. Stat. Sec. 471.6965. This budget is not complete: thecomplete budget may be examined at (title of city office, address). The city council approved this budget on (date)

Table 1Governmental Funds 20X2 Adopted Budgeted

20X0 20X1 20X2Budgeted Governmental Funds Actual Budget Adopted

RevenuesProperty Taxes $ $ $Special AssessmentsLicenses and PermitsIntergovernmental Revenues

FederalStateCounty Other Local Units

Charges for ServicesFines and ForfeitsInterest on InvestmentsMiscellaneous

Total RevenuesOther Financing Sources

Proceeds from BorrowingTransfers from Other Funds

ExpendituresCurrent

General GovernmentPublic SafetyStreets and HighwaysSanitationHealthCulture and RecreationUrban & Economic Development &HousingMiscellaneous Total Current Expenditures

Debt Service - PrincipalInterest and Fiscal ChargesTotal Capital Outlay

Total ExpendituresOther Financing Uses

Transfers to Other Funds

Increase (Decrease) in Fund Balance

Property Tax Levy Requirement to Fund thisBudget

Figure 16

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 31

Chapter 4Financial Statements

City and town clerks are required to prepare an annual financial statement and present it to the townboard or city council. The financial statements allow the governing body to review the financialcondition of the city or town. It is recommended that interim financial reports be prepared for thetown board or city council to allow them to review the financial condition of the city or town on acurrent basis.

Interim Financial Statements

Interim financial reports can be used to control current operations, determine the compliance withbudgetary limitations, and to anticipate changes in the financial condition of the town or city. Interimreports should be prepared monthly, however, the small number of transactions in some towns orcities may make a bimonthly or quarterly report more practical. Figure 18 on page 33, is an exampleof an interim financial report.

Annual Financial Report

The explanation of schedules in this book covers the minimum reporting requirements for citiesunder 2,500 in population for cities reporting on a cash basis. It is recommended that towns use thesample financial statement shown in Appendix D, beginning on page 63, as a basis for preparingtheir annual financial report.

Schedule 1

Schedule 1 is a statement by fund of the receipts, disbursements, balances, and investments. Thissummary should contain all the funds, including enterprise funds. The clerk's balance on January 1should agree with the December 31 balance of the preceding year.

Schedule 2

Schedule 2 is a statement of receipts, disbursements, transfers in and out, and balances in the fundat the beginning and end of the year. In this schedule, receipts are classified by source anddisbursements are classified by function and activity. Statements for the general fund, specialrevenue funds, debt service funds, and capital projects funds should be included in this schedule.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor32

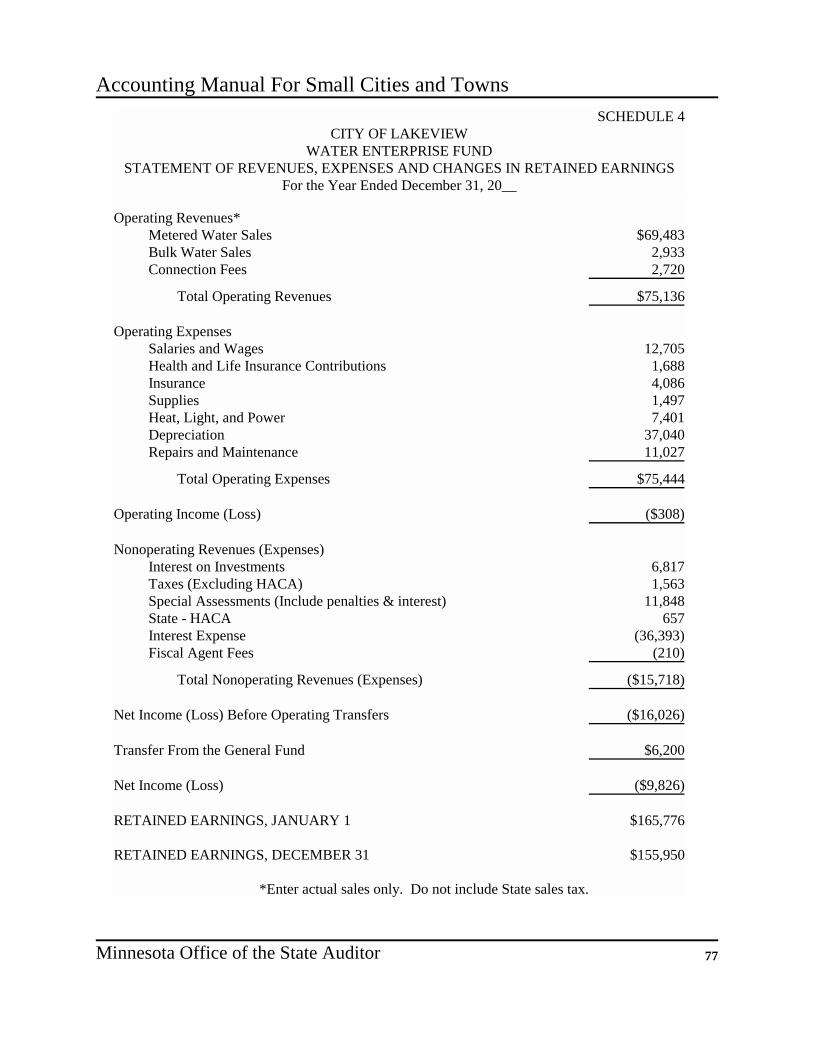

Schedule 3 and 4

The statement of the enterprise funds should be prepared on an accrual basis of accounting.Schedules 3 and 4 are the balance sheet and operating statement for each enterprise fund.

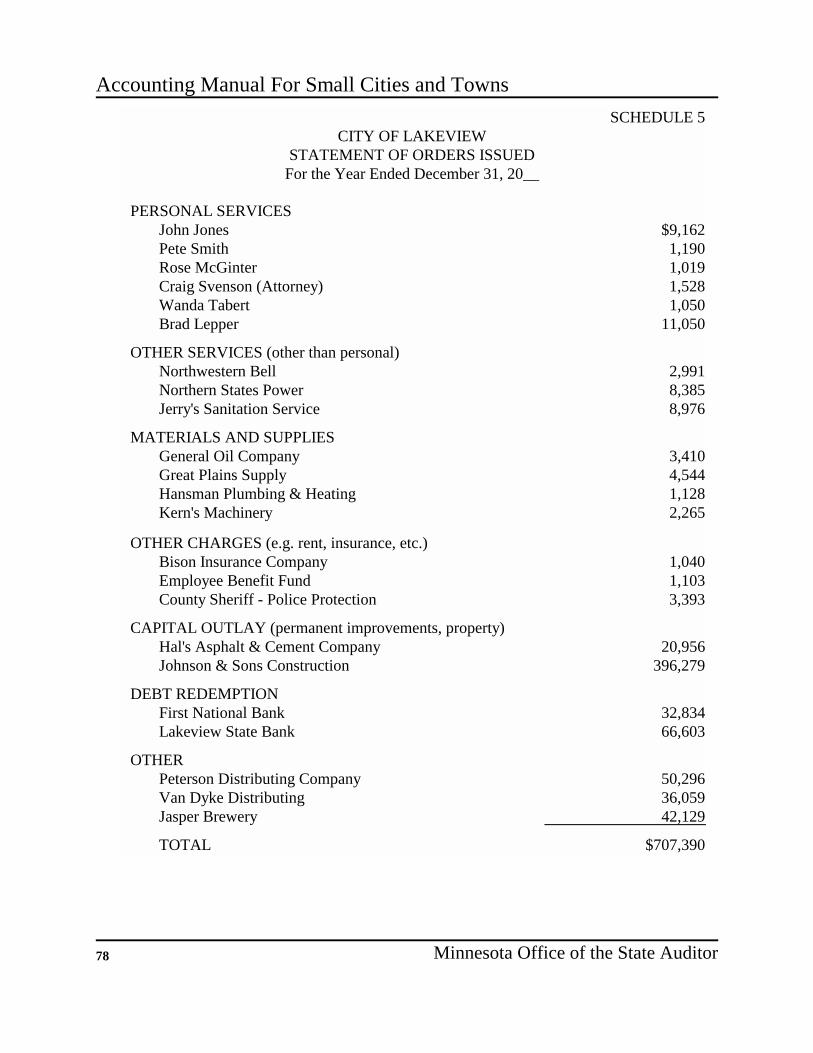

Schedule 5

Schedule 5 is a statement of orders issued by object classification, showing the total amount paidduring the year to each vendor or employee. Cities that publish the minutes of city council meetingsshowing to whom and for what purpose orders are drawn need not include Schedule 5 in their annualfinancial statement.

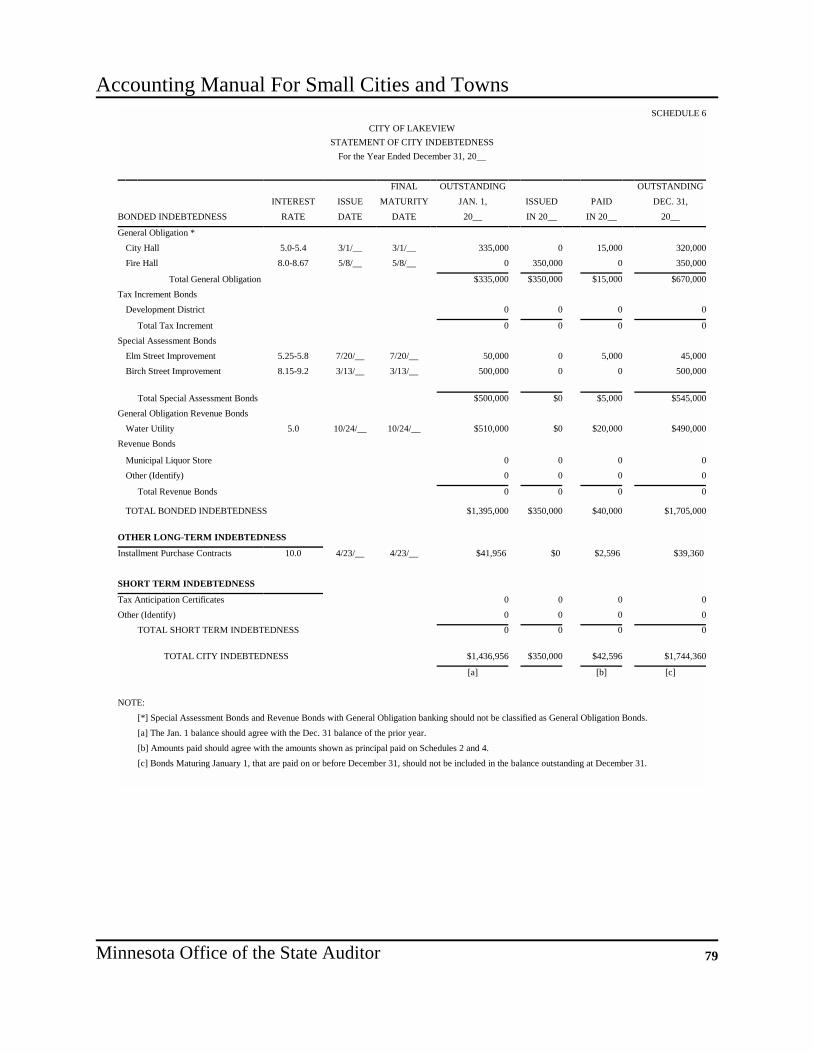

Schedule 6

Schedule 6 is the statement of indebtedness by type of debt. Each bond issue or certificate ofindebtedness should be listed separately. Other long-term indebtedness (i.e. installment purchasecontracts, contracts for deed, notes at the bank) should also be included on this schedule.

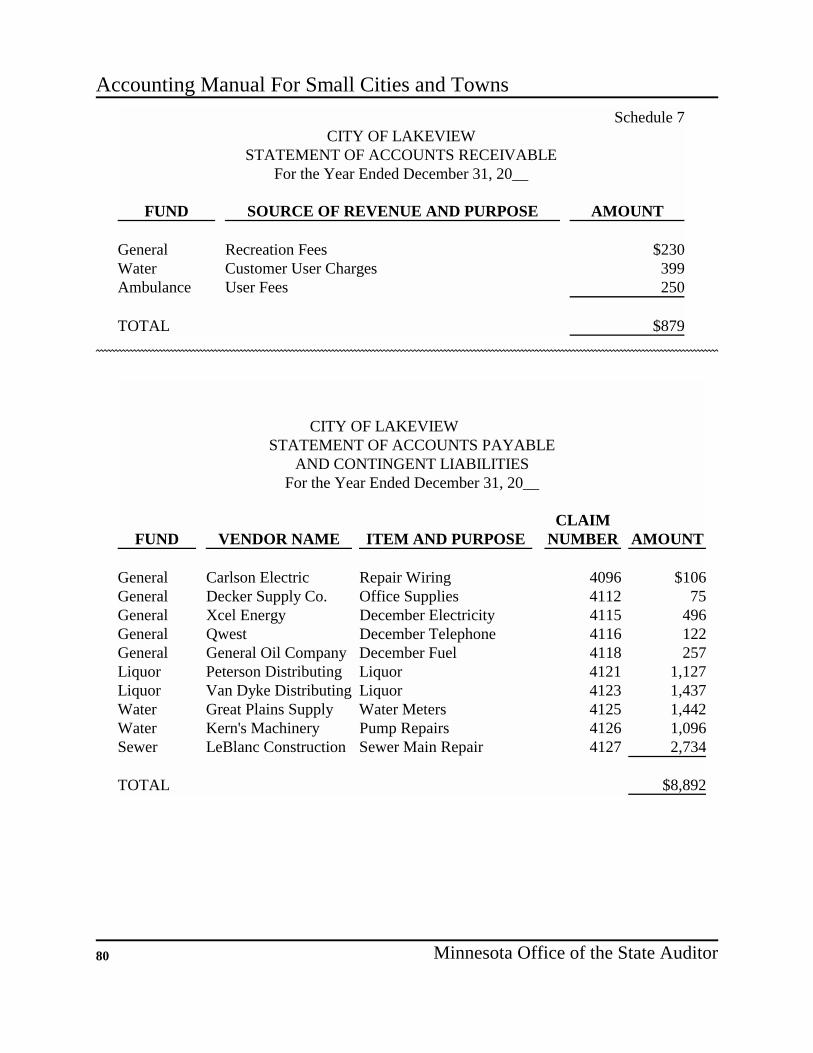

Schedule 7

Schedule 7 is a schedule of accounts receivable and accounts payable. List the receivables, cash notreceived during the current year, and payables, bills not paid until the following year, as of the endof the year.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 33

Name of CityInterim Financial Report

General FundFor the Period Ended February 28, 20X2

Revenues Budget Month Year-to-date Budget Remaining PercentProperty Taxes $ $ $ $ %Special AssessmentsLicenses and PermitsIntergovernmental Revenues

FederalStateCountyOther Local Units

Charges for ServicesFines and ForfeitsInterest on InvestmentsMiscellaneous

TOTAL REVENUES

ExpendituresCurrent

General GovernmentPublic SafetyStreets and HighwaysSanitationHealthCulture and RecreationUrban Redevelopment & HousingEconomic DevelopmentMiscellaneous Total Current Expenditures

Capital OutlayDebt Service - PrincipalInterest and Fiscal Charges

Total Expenditures

Other Financing Sources (Uses)Proceeds from BorrowingTransfers from Other FundsTransfers to Other Funds

Beginning Cash BalanceEnding Cash Balance $ $ $ $ $

Figure 17

This page left blank intentionally

Appendix A

Duties of City/Town Clerks

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 37

Duties of the City Clerk

Minnesota Statutes Section 412.51 Duties of Clerk

Subdivision 1. Listed; fees; deputy; absence. The clerk shall give the required notice of eachregular and special election, record the proceedings thereof, notify officials of their election orappointment to office, certify to the county auditor all appointments and the results of all cityelections. The clerk shall keep (1) a minute book, noting therein all proceedings of the council; (2)an ordinance book to record at length all ordinances passed by the council; and (3) an account bookto enter all money transactions of the city including the dates and amounts of all receipts and theperson from whom the money was received and all orders drawn upon the treasurer with their payeeand object. Ordinances, resolutions, and claims considered by the council need not be given in fullin the minute book if they appear in other permanent records of the clerk and can be accuratelyidentified from the description given in the minutes. The clerk shall act as the clerk and bookkeeperof the city, shall be the custodian of its seal and records, shall sign its official papers, shall post andpublish such notices, ordinances and resolutions as may be required and shall perform such otherappropriate duties as may be imposed by the council. For certified copies, and for filing andentering, when required, papers not relating to city business, the clerk shall receive the fees allowedby law to town clerks; but the council may require the clerk to pay such fees into the city treasury.With the consent of the council, the clerk may appoint a deputy for whose acts the clerk shall beresponsible and whom the clerk may remove at pleasure. In case of the clerk's absence from the cityor disability, the council may appoint a deputy clerk, if there is none, to serve during such absenceor disability. The deputy may discharge any of the duties of the clerk, except that deputy shall notbe a member of the council.

Subd. 2. Delegation; audit. The council by ordinance may delegate all or part of the clerk'sbookkeeping duties to another officer or employee. The officer or employee who by ordinance ismade responsible for the clerk's bookkeeping duties shall furnish a fidelity bond conditioned for thefaithful exercise of duties. The council may provide for the payment from city funds of the premiumon the official bond. If the bookkeeping functions of the clerk are delegated to the city treasurer, thecouncil shall provide for an annual audit of the city's financial affairs in accordance with theminimum procedures prescribed by the state auditor. A copy of the ordinance shall be provided tothe state auditor

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor38

Duties of the Town Clerk

Minnesota Statutes Section 367.11

It shall be the duty of the town clerk:

(1) to act as clerk of the town board and keep in the clerk's office a true record of all of itsproceedings;

(2) unless otherwise provided by law, to have custody of the records, books, and papers of thetown and file and safely keep all papers required by law to be filed in the clerk's office;

(3) to record minutes of the proceedings of every town meeting in the book of town records andenter in them at length every order or direction and all rules and regulations made by thetown meeting;

(4) to file and preserve all accounts audited by the town board or allowed at a town meeting andenter a statement of them in the book of records;

(5) to record every request for a special vote or special town meeting and properly post therequisite notices of them;

(6) to post, as required by law, fair copies of all bylaws made by the town, and make a signedentry in the town records, of the time when and the places where they were posted and recordin full all ordinances passed by the town board in an ordinance book;

(7) to furnish to the annual meeting of the town board of audit every statement from the countytreasurer of money paid to the town treasurer, and all other information about fiscal affairsof the town in the clerk's possession, and all accounts, claims, and demands against the townfiled with the clerk; and

(8) to perform any other duties required by law.

Appendix B

Chart of Accounts

This page left blank intentionally

Accounting Manual For Small Cities and Towns

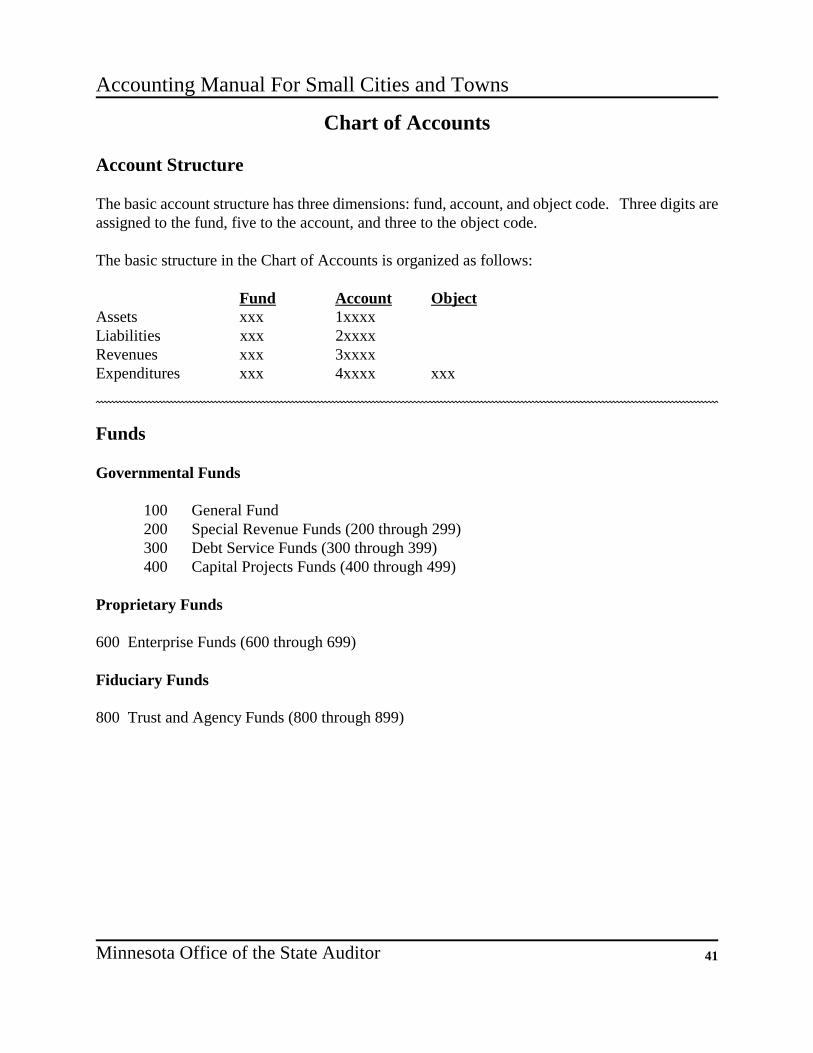

Minnesota Office of the State Auditor 41

Chart of Accounts

Account Structure

The basic account structure has three dimensions: fund, account, and object code. Three digits areassigned to the fund, five to the account, and three to the object code.

The basic structure in the Chart of Accounts is organized as follows:

Fund Account ObjectAssets xxx 1xxxxLiabilities xxx 2xxxxRevenues xxx 3xxxxExpenditures xxx 4xxxx xxx

Funds

Governmental Funds

100 General Fund200 Special Revenue Funds (200 through 299)300 Debt Service Funds (300 through 399)400 Capital Projects Funds (400 through 499)

Proprietary Funds

600 Enterprise Funds (600 through 699)

Fiduciary Funds

800 Trust and Agency Funds (800 through 899)

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor42

Revenues and Other Financing Sources

31000 General Property Taxes31800 Other Taxes31900 Penalties and Interest on Delinquent Taxes32000 LICENSES AND PERMITS32100 Business Licenses and Permits32200 Non-Business Licenses and Permits33000 INTERGOVERNMENTAL REVENUES33100 Federal Grants and Aids33400 State Grants and Aids33401 Local Government Aid33402 HACA (Homestead Credit)33403 Mobile Home Homestead Credit33418 State Aid for Streets33423 Disparity Reduction Aid33600 GRANTS AND AIDS FROM LOCAL GOVERNMENTAL UNITS33610 County Grants and Aids for Highways33620 Other County Grants and Aids33630 Grants and Aids From Other Local Governments34000 CHARGES FOR SERVICES34100 General Government34200 PUBLIC SAFETY34201 Police34202 Fire Protection34205 Ambulance Revenues34300 HIGHWAYS AND STREETS34400 SANITATION DEPARTMENT34500 HEALTH DEPARTMENT34700 CULTURE-RECREATION34900 OTHER CHARGES35000 FINES AND FORFEITS35100 Fines35200 Forfeits36100 SPECIAL ASSESSMENTS36101 Principal36102 Penalties and Interest36200 MISCELLANEOUS REVENUES36210 Interest Earnings36220 Rents and Royalties36230 Contributions and Donations from39200 OPERATING TRANSFERS36290 Sale of Investments

For more extensive revenue classifications, you may refer to the complete Chart of Accountsavailable from the Office of the State Auditor upon request.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 43

Expenditures and Other Financing Uses

41000 GENERAL GOVERNMENT41100 Legislative (Council or Board)41300 Executive (Mayor, Manager)41400 Clerk41500 Financial Administration41600 Legal Services41900 Other General Government42000 PUBLIC SAFETY42100 Police42130 Traffic Control42200 Fire42800 Other Protection43000 PUBLIC WORKS43100 Highways, Streets and Roadways43125 Ice and Snow Removal43126 Road and Bridge Equipment43130 Bridges, Viaducts and Grade Separations43160 Street Lighting43200 Sanitation43220 Street Cleaning43230 Waste Refuse Collection43240 Waste (Refuse) Disposal43250 Sewage Collection and Disposal43251 Sanitary Sewer Construction43252 Sanitary Sewer Maintenance43253 Sanitary Sewer Cleaning43260 Weed Control45000 CULTURE-RECREATION45100 Recreation45200 Parks45509 Branch Libraries46100 CONSERVATION OF NATURAL RESOURCES46102 Shade Tree Disease Control46103 Other Natural Resources47000 DEBT SERVICE49000 MISCELLANEOUS EXPENDITURES49010 Cemetery49200 Unallocated Expenditures49240 Insurance - Unallocated49300 Other Financing Uses49350 Purchase of Investments

For more extensive expenditure classifications, you may refer to the complete Chart of Accountsavailable from the Office of the State Auditor upon request.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor44

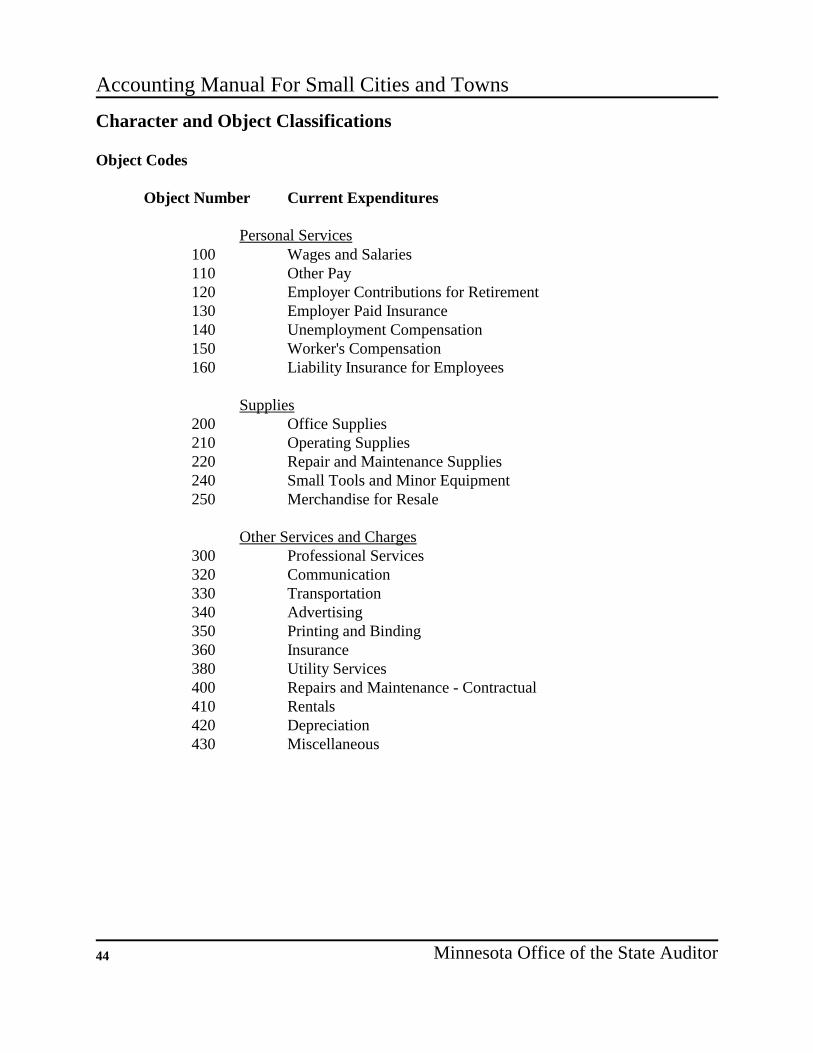

Character and Object Classifications

Object Codes

Object Number Current Expenditures

Personal Services100 Wages and Salaries110 Other Pay120 Employer Contributions for Retirement130 Employer Paid Insurance140 Unemployment Compensation150 Worker's Compensation160 Liability Insurance for Employees

Supplies200 Office Supplies210 Operating Supplies220 Repair and Maintenance Supplies240 Small Tools and Minor Equipment250 Merchandise for Resale

Other Services and Charges300 Professional Services320 Communication330 Transportation340 Advertising350 Printing and Binding360 Insurance380 Utility Services400 Repairs and Maintenance - Contractual410 Rentals420 Depreciation430 Miscellaneous

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 45

Character and Object Classifications (continued)

Object Number

Capital Outlay

510 Land520 Buildings and Structures530 Improvements Other than Buildings540 Heavy Machinery550 Motor Vehicles560 Furniture and Fixtures570 Office Equipment and Furnishings580 Other Equipment590 Books599 Leasehold Improvements

Debt Service

600 Principal610 Interest620 Fiscal Agents' Fees

Other Financing Uses

Transfers710 Residual Equity Transfers720 Operating Transfers730 Interfund Loans

800 Investments Purchased810 Refunds and Reimbursements

For more extensive character and object classifications, you may refer to the complete Chart ofAccounts available from the Office of the State Auditor upon request.

This page left blank intentionally

Appendix C

Sample Forms

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 49

RECEIPTS REGISTERMonth of ___________ 20___ Town/City of _______________________ Page Reference Number ____

From Whom Received For What Purpose DateReceiptNumber Amount

AccountNumber General Fund

_______Fund

_______Fund

_______Fund

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor50

___________________ Fund

RECEIPTS LEDGER

Account Number ______________________ Sheet Number _________________

Source ______________________________ Original Budget ________________

Account Name ________________________ Revised Budget ________________

____________________________________ _____________________________

____________________________________ _____________________________

DateReceipt

No. Received From

PageRef.No.

AmountReceived

MonthTo DateReceived

Year ToDate

ReceivedBudgetBalance

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 51

DISBURSEMENTS REGISTERMonth of ___________ 20___ Town/City of _______________________ Page Reference Number ____

To Whom Paid For What Purpose DateCheck

Number AmountAccountNumber General Fund

_______Fund

_______Fund

_______Fund

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor52

___________________ Fund

DISBURSEMENTS LEDGER

Account Number _____________________ Sheet Number _________________

Activity ____________________________ Original Budget ________________

Object _____________________________ Revised Budget ________________

___________________________________ _____________________________

___________________________________ _____________________________

DateCheck

No. Description

PageRef.No.

AmountDisbursed

Month ToDate

Disbursed

Year ToDate

DisbursedBudgetBalance

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 53

Claim Number ________

CLAIM

City/Town of ______________________ County of ____________________________

Date : ___________________ 20____

To

Address

Audited and Allowed in the Sum of ____________________________________

Mayor

Clerk

Distribution of Expense Paid by Order-Check Number __________

Fund Account Number Amount Filed in my office this _____________

day of _______________________, 20___

Clerk

DECLARATION

I declare under penalties of law that this account, claim or demand is just and correct and thatno part of it has been paid.

Date Signature of Claimant

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor54

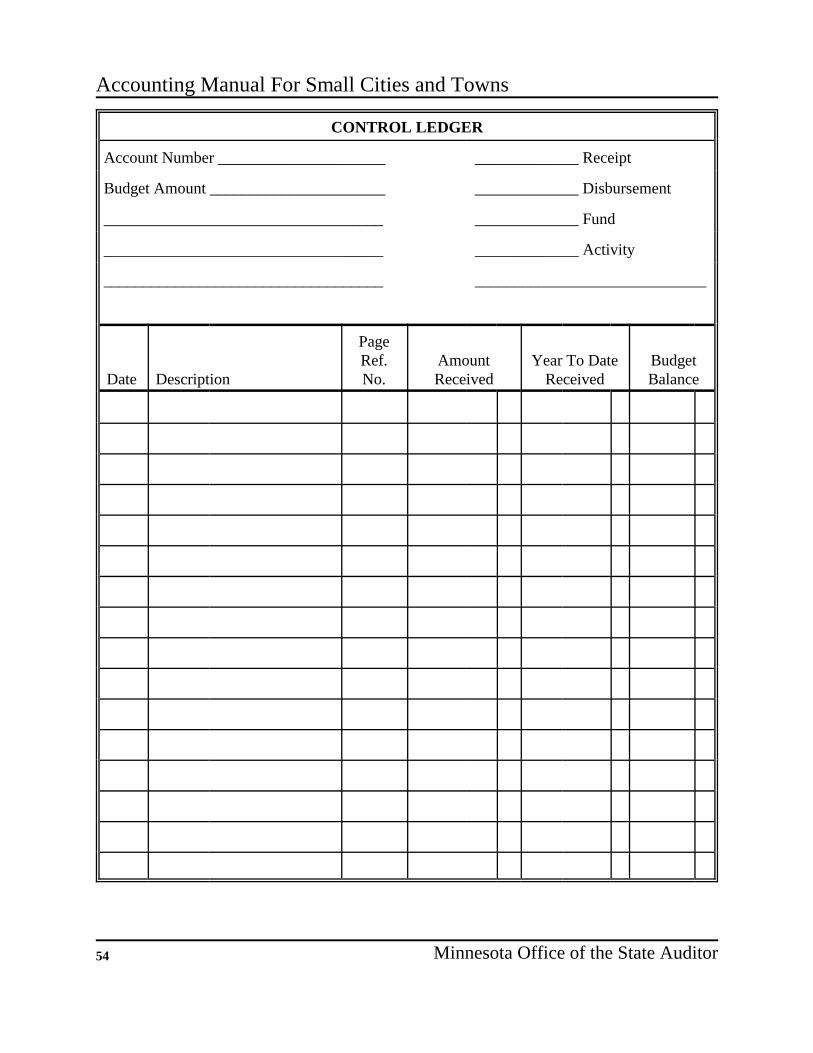

CONTROL LEDGER

Account Number _____________________ _____________ Receipt

Budget Amount ______________________ _____________ Disbursement

___________________________________ _____________ Fund

___________________________________ _____________ Activity

___________________________________ _____________________________

Date Description

PageRef.No.

AmountReceived

Year To DateReceived

BudgetBalance

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 55

PAYROLL REGISTERPeriod From ___________20___ to ___________ 20____ Sheet _______ of _______ Sheets

Deductions

Hours Earnings Less Taxable Federal State Net Check

Name Reg.

O.T. Regular O.T. Gross PERA Wages W.H. Tax FICA W.H. Tax Amount Date No.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor56

EMPLOYEE'S INDIVIDUAL EARNINGS RECORD

Name ________________________________ Social Security Number ______________

Address ______________________________ Date Employed _____________________

______________________________ Date Terminated ____________________

INCOME TAX DATA PERA Plan ________________________

Effective Date

No. of Exemptions

Additional Withholding

Hourly Rate of Salary

____ Single ___ MarriedDeductions Order

Hours Earnings Federal State Net Check

Reg. O..T. Reg. O.T. Gross W.H. Tax P.E.R.A. F.I.C.A. W.H. Tax Amount Date No.

1

2

3

4

5

6

7

Total forQuarter

TotalsYear-to-date

1

2

3

4

5

6

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 57

INVESTMENT RECORD

Fiscal Year

PurchaseDate Type of Investment

IDNumber Cost

InterestRate

MaturityDate

DateSold Proceeds

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor58

BOND AND INTEREST PAYMENT RECORD

Title of Issue

Amount of Issue $

Date of Issue

Date of Sale

Term

Purchaser

Price $

Interest Rates

Net Interest Rate %

Principal Due $

Interest Due $

Denominations

Paying Agent/Registrar

Redemption

Rating

Bond Buyer’s Index (BBI)

Legal Opinion

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 59

BOND MATURITY RECORD

Date DueBond

NumbersPrincipal

DueInterest

Due Total Due

PayingAgent

Charges Date Paid

This page left blank intentionally

Appendix D

Sample Town Financial Statements

The following statements are not a complete set of the required financial statements. For a completeset of recommended financial statements please refer to the Minimum Reporting Requirements forCities Reporting on a Cash Basis publication issued by the Office of the State Auditor

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 63

SCHEDULE 1

TOWN OF LAKEVIEWSTATEMENT OF CASH RECEIPTS, DISBURSEMENTS, BALANCES, AND INVESTMENTS

For the Year Ended December 31, 20__

Clerk's Clerk's InvestmentsBalance Sale of Transfers Disburse- Purchase of Transfers Balance Balance

Fund Name (a) Jan. 1 Receipts Investments In ments Investments Out Dec. 31 Dec. 31

General Fund $2,688 $9,788 $10,000 --- $9,051 $12,000 $1,000 $425 $42,000

Special Revenue FundsRoad and Bridge 930 19,722 --- --- 18,679 --- --- 1,973 30,000Fire 991 5,902 --- 1,000 5,868 --- --- 2,025 3,000

Total $4,609 $35,412 $10,000 $1,000 $33,598 $12,000 $1,000 $4,423 $75,000 (b) (b) (c)

NOTES: (a) Funds shown are for illustrative purposes only. All funds of the town should be shown.(b) Total Transfers In (for all funds) must equal total Transfers Out (for all funds). (c) Enter the total of certificates of deposit, investments, and savings accounts.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor64

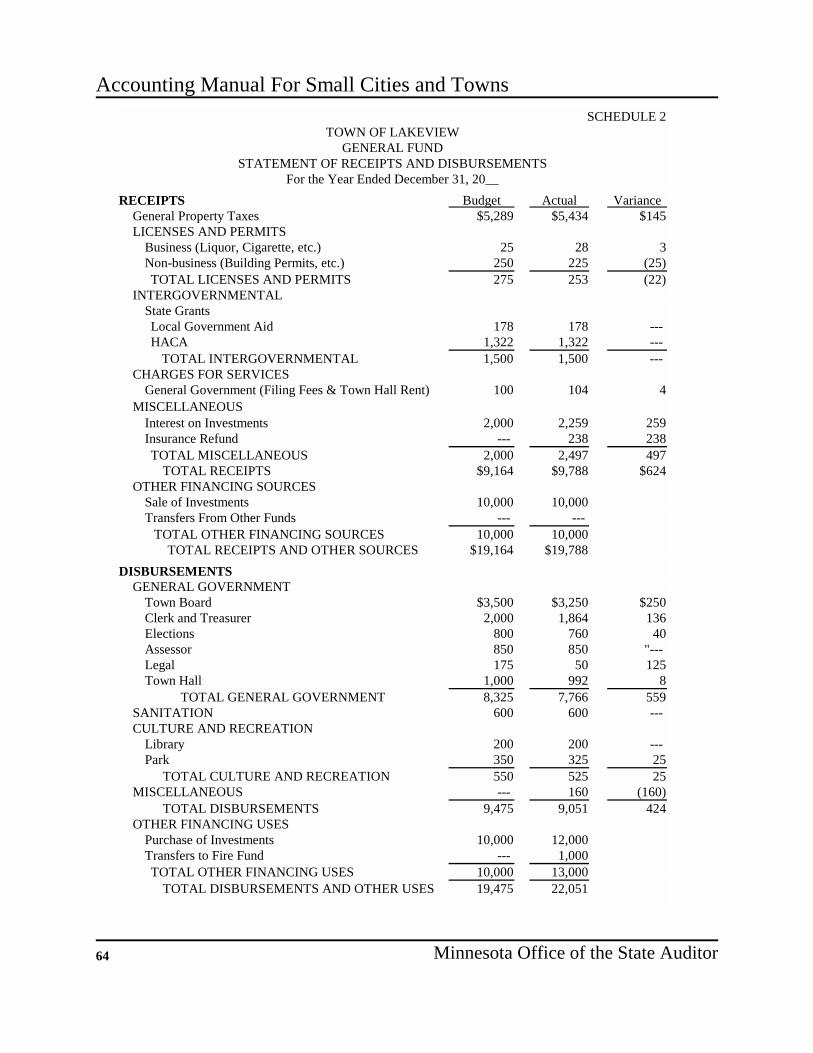

SCHEDULE 2TOWN OF LAKEVIEW

GENERAL FUNDSTATEMENT OF RECEIPTS AND DISBURSEMENTS

For the Year Ended December 31, 20__RECEIPTS Budget Actual Variance

General Property Taxes $5,289 $5,434 $145LICENSES AND PERMITS

Business (Liquor, Cigarette, etc.) 25 28 3Non-business (Building Permits, etc.) 250 225 (25)TOTAL LICENSES AND PERMITS 275 253 (22)

INTERGOVERNMENTAL State GrantsLocal Government Aid 178 178 --- HACA 1,322 1,322 --- TOTAL INTERGOVERNMENTAL 1,500 1,500 ---

CHARGES FOR SERVICESGeneral Government (Filing Fees & Town Hall Rent) 100 104 4

MISCELLANEOUS Interest on Investments 2,000 2,259 259Insurance Refund --- 238 238TOTAL MISCELLANEOUS 2,000 2,497 497

TOTAL RECEIPTS $9,164 $9,788 $624OTHER FINANCING SOURCES

Sale of Investments 10,000 10,000Transfers From Other Funds --- --- TOTAL OTHER FINANCING SOURCES 10,000 10,000 TOTAL RECEIPTS AND OTHER SOURCES $19,164 $19,788

DISBURSEMENTSGENERAL GOVERNMENT

Town Board $3,500 $3,250 $250Clerk and Treasurer 2,000 1,864 136Elections 800 760 40Assessor 850 850 "--- Legal 175 50 125Town Hall 1,000 992 8

TOTAL GENERAL GOVERNMENT 8,325 7,766 559SANITATION 600 600 --- CULTURE AND RECREATION

Library 200 200 --- Park 350 325 25

TOTAL CULTURE AND RECREATION 550 525 25MISCELLANEOUS --- 160 (160)

TOTAL DISBURSEMENTS 9,475 9,051 424OTHER FINANCING USES

Purchase of Investments 10,000 12,000 Transfers to Fire Fund --- 1,000 TOTAL OTHER FINANCING USES 10,000 13,000

TOTAL DISBURSEMENTS AND OTHER USES 19,475 22,051

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 65

SCHEDULE 2TOWN OF LAKEVIEW

ROAD AND BRIDGE FUNDSTATEMENT OF RECEIPTS AND DISBURSEMENTS

For the Year Ended December 31, 20__

RECEIPTS Budget Actual VarianceGeneral Property Taxes $12,000 $13,677 $1,677

INTERGOVERNMENTAL State Grants

HACA 1,925 1,925 --- Gas Tax 1,243 1,243 --- TOTAL INTERGOVERNMENTAL 3,168 3,168 ---

CHARGES FOR SERVICESRoad and Bridge 1,000 1,292 292

MISCELLANEOUS Interest on Investments 1,800 1,259 (541)Insurance Refund --- 326 326 TOTAL MISCELLANEOUS 1,800 1,585 (215)

TOTAL RECEIPTS $17,968 $19,722 $1,754

OTHER FINANCING SOURCESSale of Investments --- --- Transfers From Other Funds --- --- TOTAL OTHER FINANCING SOURCES --- ---

TOTAL RECEIPTS AND OTHER SOURCES $17,968 $19,722

DISBURSEMENTSROAD AND BRIDGE

WagesSupplies

$1,500 $1,417 $831,950 2,643 (693)

Road Signs 200 118 82Equipment Repair 500 358 142Snow and Ice Removal 1,950 2,643 (693)Capital Outlay

Bridge Repair 7,500 7,500 --- Snowplow 4,500 4,000 500

TOTAL ROAD AND BRIDGE 18,100 18,679 (579) TOTAL DISBURSEMENTS 18,100 18,679 (579)

OTHER FINANCING USESPurchase of Investments --- --- Transfers to Other Funds --- ---

TOTAL OTHER FINANCING USES --- --- TOTAL DISBURSEMENTS AND OTHER USES $18,100 $18,679

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor66

SCHEDULE 2TOWN OF LAKEVIEW

FIRE FUNDSTATEMENT OF RECEIPTS AND DISBURSEMENTS

For the Year Ended December 31, 20__

RECEIPTS Budget Actual VarianceGeneral Property Taxes $4,200 $4,426 $226

INTERGOVERNMENTAL State Grants

Local Government Aid 178 178 --- HACA 783 783 ---

TOTAL INTERGOVERNMENTAL 961 961 ---

CHARGES FOR SERVICESFire Calls 300 350 50

TOTAL CHARGES FOR SERVICES 300 350 50

MISCELLANEOUS Interest on Investments 100 150 50Insurance Refund --- 15 15

TOTAL MISCELLANEOUS 100 165 65

TOTAL RECEIPTS $5,561 $5,902 $341

OTHER FINANCING SOURCESSale of Investments --- --- Transfers From General Fund --- 1,000

TOTAL OTHER FINANCING SOURCES --- 1,000

TOTAL RECEIPTS AND OTHER SOURCES $5,561 $6,902

DISBURSEMENTSPUBLIC SAFETY

FIREContract $3,500 $4,368 ($868)Capital Outlay

Shared Purchase of Truck 1,500 1,500 --- TOTAL PUBLIC SAFETY 5,000 5,868 (868)

TOTAL DISBURSEMENTS 5,000 5,868 (868)

OTHER FINANCING USESPurchase of Investments --- --- Transfers to Other Funds --- ---

TOTAL OTHER FINANCING USES --- --- TOTAL DISBURSEMENTS AND OTHER USES 5,000 5,868

Appendix E

Sample City Financial Statements

The following statements are not a complete set of the required financial statements. For a completeset of required financial statements please refer to the Minimum Reporting Requirements for CitiesReporting on a Cash Basis publication issued by the Office of the State Auditor.

This page left blank intentionally

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 69

SCHEDULE 1

CITY OF LAKEVIEW

STATEMENT OF CASH RECEIPTS, DISBURSEMENTS, BALANCES, AND INVESTMENTS

For the Year Ended December 31, 20__

Clerk's Clerk's Investments

Balance Sale of Transfers Disburse- Purchase of Transfers Balance Balance

Fund Name (a) Jan. 1 Receipts Investments In ments Investments Out Dec. 31 Dec. 31

General Fund $16,815 $206,171 $11,979 $10,000 $180,104 $20,000 $6,200 $38,661 $80,767

Special Revenue Funds

Ambulance Fund 648 18,417 1,141 ---- 7,261 4,031 ---- 8,914 15,707

Park Improvement Fund 25,000 8,038 ---- ---- 28,312 ---- ---- 4,726 15,212

Debt Service Funds

City Hall Debt Service 5,607 27,339 ---- ---- 32,834 ---- ---- 112 ----

Street Improvement DebtService 17,351 11,416 ---- ---- 11,945 ---- ---- 16,822 26,302

Capital Projects Funds

Fire Hall 495 458,218 100,000 ---- 271,279 ---- ---- 287,434 ----

Street ImprovementConstruction ---- 474,456 ---- ---- 435,564 ---- ---- 38,892 25,000

Enterprise Funds

Water Fund 42,609 96,021 ---- 6,200 100,068 1,654 ---- 43,108 47,075

Sewer Fund 15,572 43,260 ---- ---- 36,622 11,000 ---- 11,210 108,852

Liquor Fund 23,374 142,473 ---- ---- 132,712 8,810 10,000 14,325 15,000

Total $147,471 $1,485,809 $113,120 $16,200 $1,236,701 $45,495 $16,200 $464,204 $333,915

(b) (b) (c)

NOTES: (a) Funds shown are for illustrative purposes only. All funds of the city should be shown.

(b) Total Transfers In (for all funds) must equal total Transfers Out (for all funds).

(c) Enter the total of certificates of deposit, investments, and savings accounts.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor70

SCHEDULE 2CITY OF LAKEVIEW

GENERAL FUNDSTATEMENT OF RECEIPTS

For the Year Ended December 31, 20__RECEIPTS

TAXESGeneral Property Tax Current, Delinquent, Penalties and Interest $68,364 TOTAL TAXES $68,364

LICENSES AND PERMITSBusiness (Liquor, Cigarette, etc.) 2,195Non-business (Building Permits, etc.) 105

TOTAL LICENSES AND PERMITS 2,300

INTERGOVERNMENTAL State Grants

Local Government Aid 74,195HACA 28,550Fire Relief Aid 2,661Other (Airport) 4,336

TOTAL INTERGOVERNMENTAL 109,742

CHARGES FOR SERVICESGeneral Government (Filing Fees & City Hall Rent) 92Public Safety 3,712Parks and Recreation 3,922Other (Cemetery) 1,292

TOTAL CHARGES FOR SERVICES 9,018

FINES AND FORFEITSCounty Court 4,128

MISCELLANEOUS Interest on Investments 5,591Insurance Claims 1,652Refunds Received 717Sale of Property 4,659

TOTAL MISCELLANEOUS 12,619

TOTAL RECEIPTS $206,171

OTHER FINANCING SOURCESSale of Investments 11,979Transfers From:

Liquor Fund 10,000 TOTAL OTHER FINANCING SOURCES 21,979

TOTAL RECEIPTS AND OTHER FINANCINGSOURCES $228,150

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 71

SCHEDULE 2CITY OF LAKEVIEW

GENERAL FUNDSTATEMENT OF DISBURSEMENTSFor the Year Ended December 31, 20__

DISBURSEMENTS

GENERAL GOVERNMENTMayor and Council

Current $1,720Finance-Municipal Clerk/Treasurer

Current 11,864Capital Outlay 1,840

Elections Current 760

AssessorCurrent 2,790

Independent Accounting and AuditingCurrent 4,000

LegalCurrent 925

City Hall, General Government BuildingsCurrent 8,258

TOTAL GENERAL GOVERNMENT $32,157

PUBLIC SAFETYPolice Protection

Current 35,999Capital Outlay 621

Fire ProtectionCurrent 9,015Capital Outlay 412

Protective InspectionCurrent 368

Civil DefenseCurrent 334

Animal Control (Dog Catcher)Current 453

TOTAL PUBLIC SAFETY 47,202

STREETS AND HIGHWAYS (Including Storm Sewers)Streets and Alley

Current 17,271Capital Outlay - Construction 23,456Capital Outlay - Equipment, Buildings, Etc. 1,540

Snow and Ice RemovalCurrent 3,430

Street LightingCurrent 10,555

TOTAL STREETS AND HIGHWAYS 56,252

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor72

DISBURSEMENTS (Continued)

SANITATIONRecycling

Current 5,600Capital Outlay 4,200

Weed EradicationCurrent 5,100Capital Outlay 2,800

TOTAL SANITATION 17,700

CULTURE AND RECREATIONLibrary

Current 4,875Capital Outlay 1,474

Recreational Activities, Facilities,Community Buildings

Current 3,495Capital Outlay 2,229

Parks and BoulevardsCurrent 5,249Capital Outlay 3,252

TOTAL CULTURE AND RECREATION 20,574

MISCELLANEOUS Airport

Current 2,560Capital Outlay 3,000

Other (Cemetery)Current 659

TOTAL MISCELLANEOUS 6,219

TOTAL DISBURSEMENTS $180,104

OTHER FINANCING USESPurchase of Investments 20,000Transfers to Water Fund 6,200

TOTAL OTHER FINANCING USES 26,200

TOTAL DISBURSEMENTS AND OTHER FINANCING USES $206,304

Note: Insurance, benefits, workers compensation etc. should be allocated to the proper functional category towhich it applies.

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 73

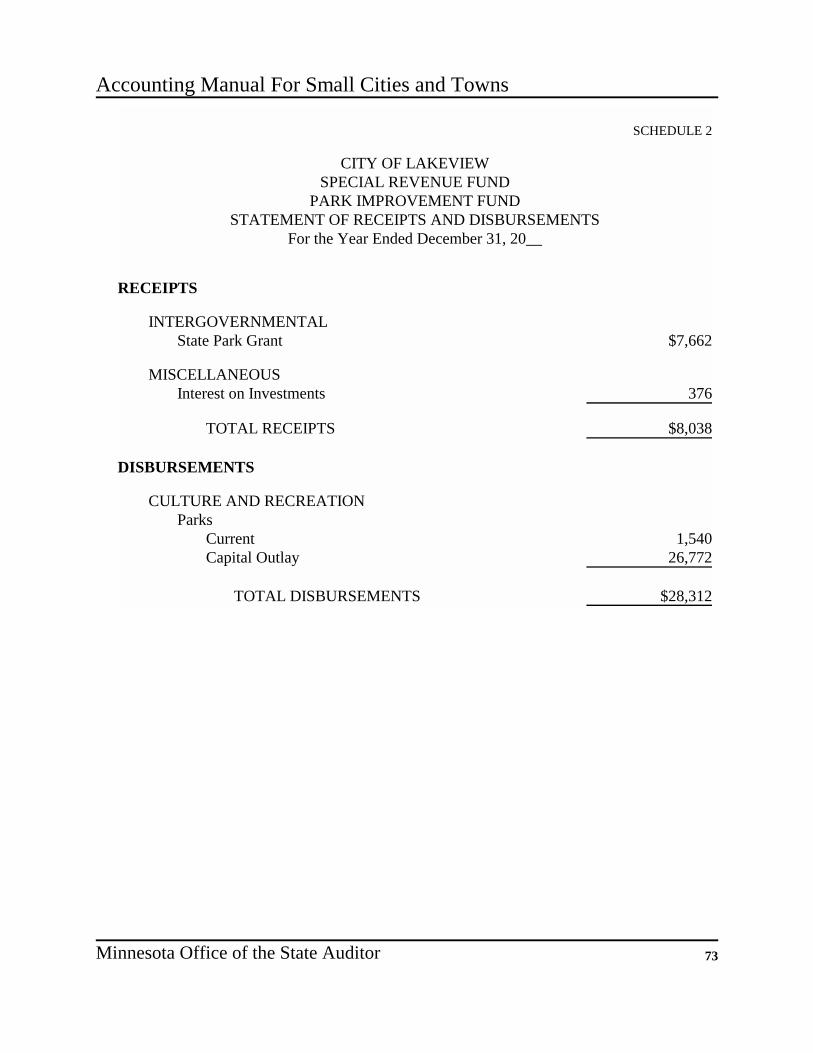

SCHEDULE 2

CITY OF LAKEVIEWSPECIAL REVENUE FUND

PARK IMPROVEMENT FUNDSTATEMENT OF RECEIPTS AND DISBURSEMENTS

For the Year Ended December 31, 20__

RECEIPTS

INTERGOVERNMENTAL State Park Grant $7,662

MISCELLANEOUS Interest on Investments 376

TOTAL RECEIPTS $8,038

DISBURSEMENTS

CULTURE AND RECREATIONParks

Current 1,540Capital Outlay 26,772

TOTAL DISBURSEMENTS $28,312

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor74

SCHEDULE 2

CITY OF LAKEVIEWSPECIAL REVENUE FUND

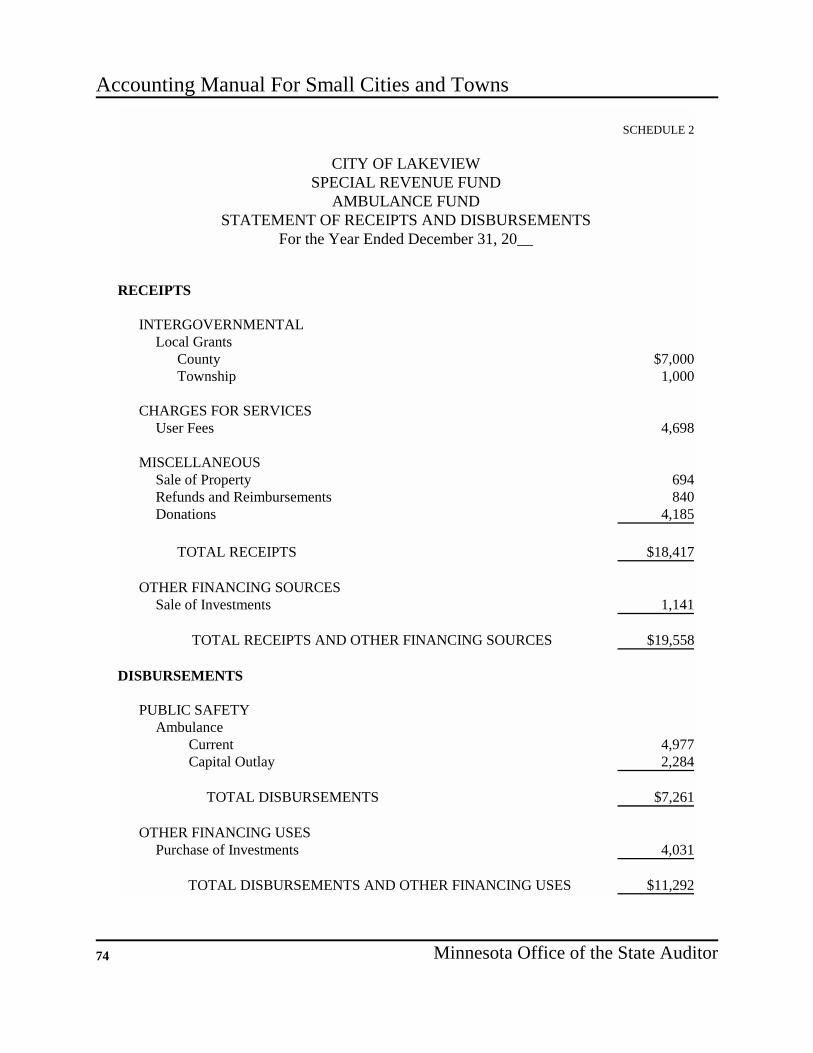

AMBULANCE FUNDSTATEMENT OF RECEIPTS AND DISBURSEMENTS

For the Year Ended December 31, 20__

RECEIPTS

INTERGOVERNMENTALLocal Grants

County $7,000Township 1,000

CHARGES FOR SERVICESUser Fees 4,698

MISCELLANEOUSSale of Property 694Refunds and Reimbursements 840Donations 4,185

TOTAL RECEIPTS $18,417

OTHER FINANCING SOURCESSale of Investments 1,141

TOTAL RECEIPTS AND OTHER FINANCING SOURCES $19,558

DISBURSEMENTS

PUBLIC SAFETYAmbulance Current 4,977 Capital Outlay 2,284

TOTAL DISBURSEMENTS $7,261

OTHER FINANCING USESPurchase of Investments 4,031

TOTAL DISBURSEMENTS AND OTHER FINANCING USES $11,292

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor 75

SCHEDULE 2

CITY OF LAKEWIEWCITY HALL DEBT SERVICE FUND

STATEMENT OF RECEIPTS AND DISBURSEMENTSFor the Year Ended December 31, 20__

RECEIPTS

TAXES General Property Tax

Current, Delinquent, Penalties and Interest $17,286

INTERGOVERNMENTAL State Grants and Aids

HACA 5,667

MISCELLANEOUSInterest on Investments 4,386

TOTAL RECEIPTS $27,339

DISBURSEMENTS

DEBT SERVICEPrincipal 15,000Interest 17,810Fiscal Charges 24

TOTAL DISBURSEMENTS $32,834

Accounting Manual For Small Cities and Towns

Minnesota Office of the State Auditor76

SCHEDULE 2