Accounting Fundamentals--Summer 2000 1 Income Statement Classification • Operating income • Other income and expense • Income from continuing operations • Income, gains & losses from discontinued operations • Extraordinary gains and losses • Changes in accounting principles

Accounting Fundamentals--Summer 2000 1 Income Statement Classification Operating income Other income and expense Income from continuing operations Income,

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Fundamentals--Summer 2000

1

Income Statement Classification

• Operating income• Other income and expense• Income from continuing

operations• Income, gains & losses from

discontinued operations• Extraordinary gains and losses• Changes in accounting principles

Accounting Fundamentals--Summer 2000

2

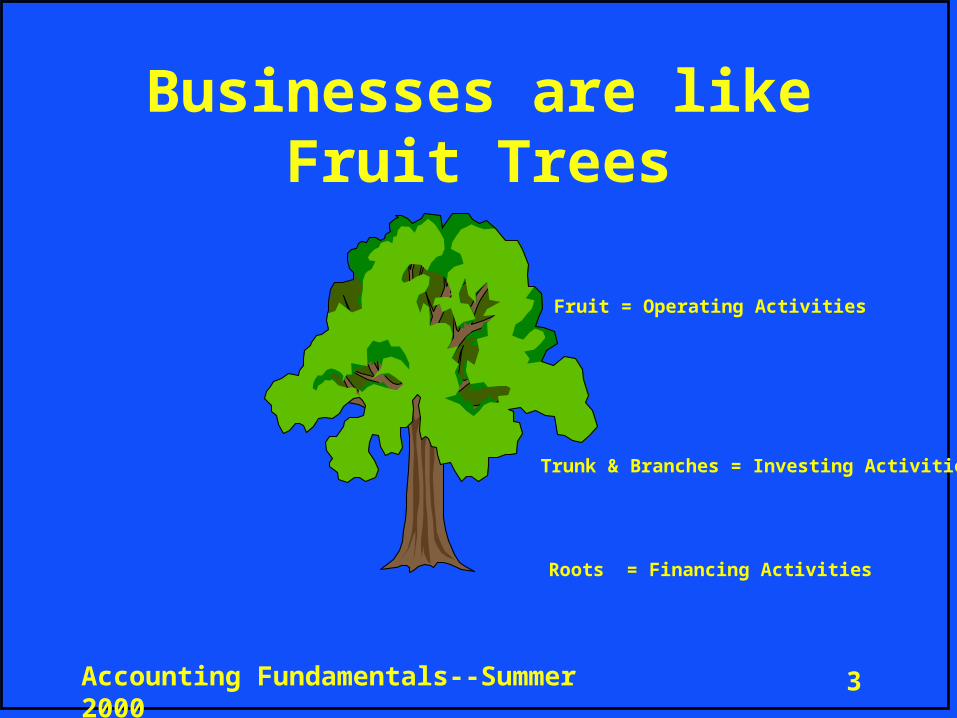

Statement of Cash Flows

• FASB 95--1987• Components

•Operating cash: Operations and working capital

• Investing cash: Non-current assets and investments

• Financing cash: L/T debt, equity and dividends

Accounting Fundamentals--Summer 2000

3

Roots = Financing Activities

Trunk & Branches = Investing Activities

Fruit = Operating Activities

Businesses are like Fruit Trees

Accounting Fundamentals--Summer 2000

4

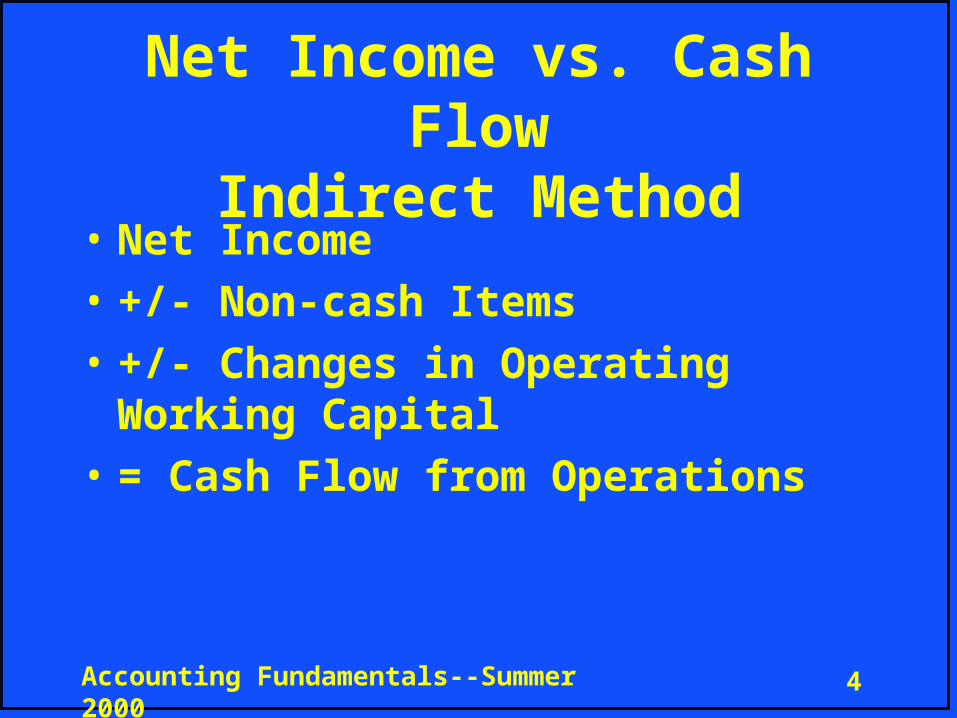

Net Income vs. Cash Flow

Indirect Method• Net Income• +/- Non-cash Items• +/- Changes in Operating

Working Capital• = Cash Flow from Operations

Accounting Fundamentals--Summer 2000

5

Indirect vs. Direct Method

• FASB prefers the direct method• FASB requires net income to cash

from operations reconciliation• Components:

• Cash from customers• Cash from dividends• Cash from interest income• Other operating cash receipts• Cash paid to suppliers• Cash paid to employees• Cash paid for taxes• Cash paid for interest• Other operating cash payments

Accounting Fundamentals--Summer 2000

6

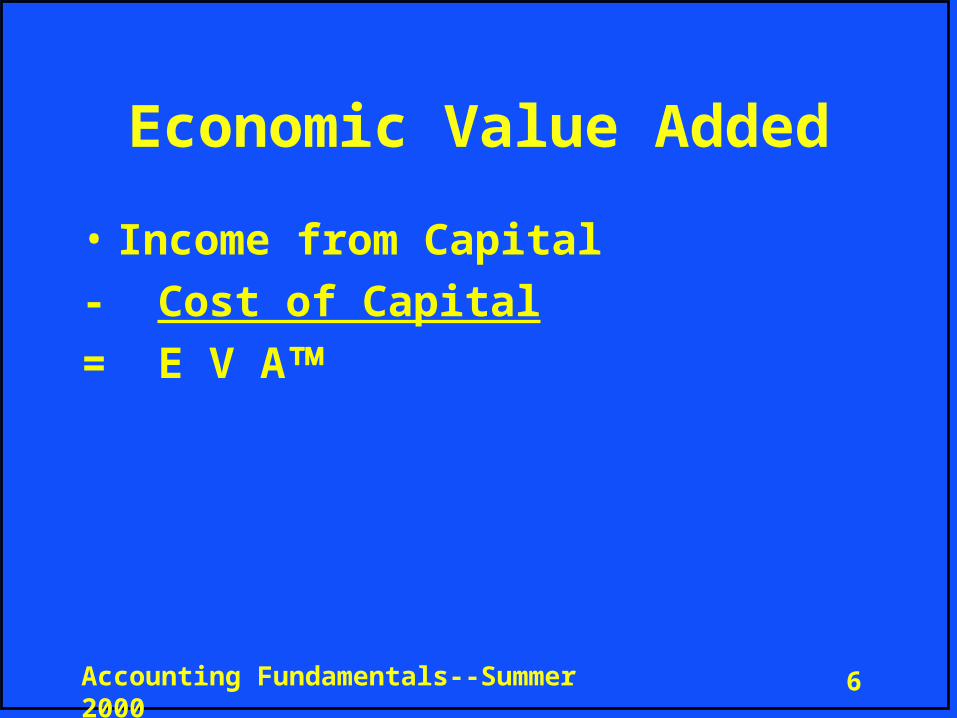

Economic Value Added

• Income from Capital- Cost of Capital= E V A

Accounting Fundamentals--Summer 2000

7

Sources of Capital

• Debt (interest %)• Equity (interest % + 6%)

Accounting Fundamentals--Summer 2000

8

Capital

• Working capital• Net tangible non-current

assets• Capitalized R & D• Capitalized Employee Devel.

Costs

Accounting Fundamentals--Summer 2000

9

Adj. Operating Income

• Operating income• Plus:

•R & D• Emp. Devel. Costs

• Minus:•R & D Amort.• Emp. Devel. Cost Amort

Accounting Fundamentals--Summer 2000

10

Keys to Success

• Make it a way of life• K I S S• CEO / Management buy-in• Gradual introduction• Thorough training

Accounting Fundamentals--Summer 2000

11

Today’s Session• Financial Statement Analysis• The Goal

Accounting Fundamentals--Summer 2000

12

Target Your Efforts

•Solvency assurance

•Wealth enhancement

•Performance improvement

Accounting Fundamentals--Summer 2000

13

Start with the 3 P’s

•Planning

•Processing

•Presenting

Accounting Fundamentals--Summer 2000

14

Include the Trifecta: Q-S-T

•Q: Quantitative analysis

•S: Strategic assessment

•T: Tactical feasibility

Accounting Fundamentals--Summer 2000

15

Tools for Financial Statement Analysis

•Ratio analysis•Trend analysis•Common-size analysis•Base period analysis•Comparative analysis•Horizontal and vertical

analyses

Accounting Fundamentals--Summer 2000

16

A Financial Statement Approach

•Look for key relationships•Focus on spending drivers•Don’t overlook the

Statement of Cash Flows•Remember to measure

trends•Tell a story

Accounting Fundamentals--Summer 2000

17

Guidelines for a Presentation

•Clarity•Accuracy•Simplicity•Visually friendly•Limit page content

Accounting Fundamentals--Summer 2000

18

Cash Flow Red-Flags

• Receivable and inventory growth rate exceeds sales growth rate

• Payables growth rate exceeds inventory growth rate

• Current liabilities grow faster than sales

• Sustained operating losses (negative net income)

Accounting Fundamentals--Summer 2000

19

Cash Flow Red-Flags (cont’d)

• Negative operating cash flow• Capital expenditures exceed

operating cash flow• Sustained capital expenditures

reductions• Sustained sales of marketable

securities in excess of purchases• Substantial shift from long to

short term borrowing• Dividend reduction or elimination

Accounting Fundamentals--Summer 2000

20

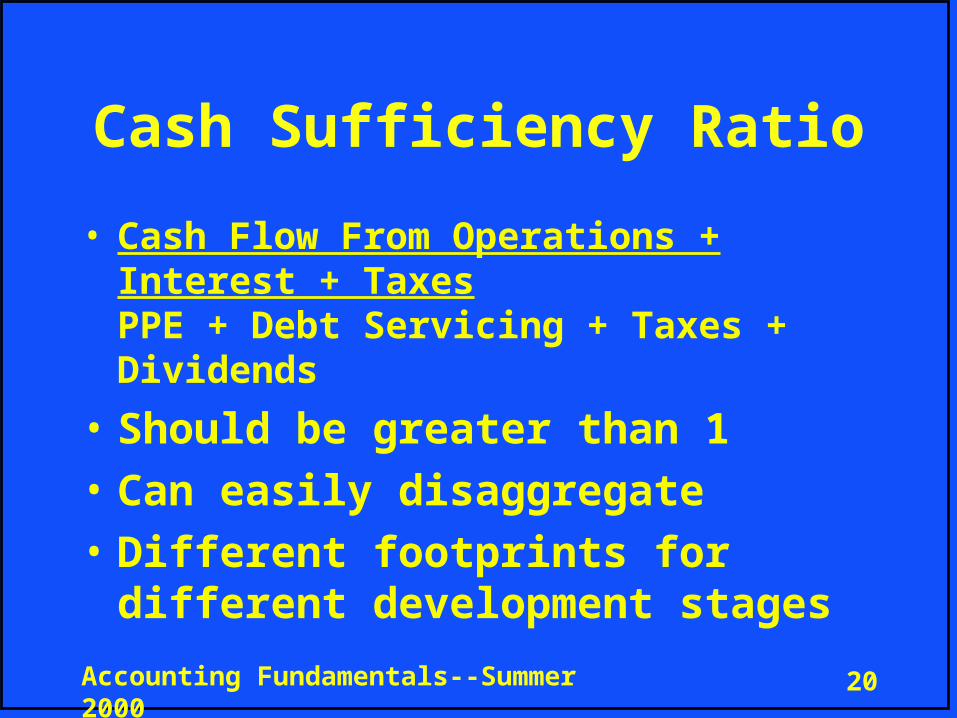

Cash Sufficiency Ratio

• Cash Flow From Operations + Interest + TaxesPPE + Debt Servicing + Taxes + Dividends

• Should be greater than 1• Can easily disaggregate• Different footprints for

different development stages

Accounting Fundamentals--Summer 2000

21

Cash Conversion Cycle

•Cash conversion cycle•Days in payables ≥ DSO + Days in

inventory

Accounting Fundamentals--Summer 2000

22

Typical Common Ratios

•Solvency & liquidity•Earnings•Performance

Accounting Fundamentals--Summer 2000

23

Ratio Analysis

•General guidelines:•Be consistent•Ascertain contents of

numerator and denominator•Apply common sense…

Accounting Fundamentals--Summer 2000

24

Trend Analysis

•Static analysis is virtually useless

•Trend direction is key•Combine with other

approaches

Accounting Fundamentals--Summer 2000

25

Common-size Analysis

•Helpful for size discrepancies

•Keyed to sales or total assets

•Helpful for industry comparisons

Accounting Fundamentals--Summer 2000

26

Base Period Analysis

•Combines trending and percentage analysis

•Select representative base year and set the index at 100

•Measure subsequent periods in terms of the base year

•Helpful for industry comparisons•Eliminates size bias

Accounting Fundamentals--Summer 2000

27

Comparative Analysis Cautions

•Timing variances•GAAP variances•Conservative vs. Aggressive

GAAP•Management attitude…”win at

all cost!”•Size•Geographic venues

Accounting Fundamentals--Summer 2000

28

Horizontal and Vertical Analysis

•The most basic…and most powerful analytical tool

•Key element in fraud detection

•Keeps the organization under control

Accounting Fundamentals--Summer 2000

29

Horizontal Analysis

•Period versus period changes•Value changes•Percentage changes

•Look for irregularities

Accounting Fundamentals--Summer 2000

30

Horizontal Analysis - Example

2009 2008 $ Change % Change

Current Assets $400 $300 $100 33%

Total Assets $2,500 $2,200 $300 14%

Current Liabilities $200 $150 $50 33%

Long-term Debt $1,600 $1,500 $100 7%

Equity $700 $550 $150 27%

Total Liabilities & Equity $2,500 $2,200 $300 14%

ABC CompanyPartial Balance Sheets

2008 and 2009

Accounting Fundamentals--Summer 2000

31

Vertical Analysis

•Relationships within the same period:•Numerical relationships•Percentage relationships

•Look for irregularities

Accounting Fundamentals--Summer 2000

32

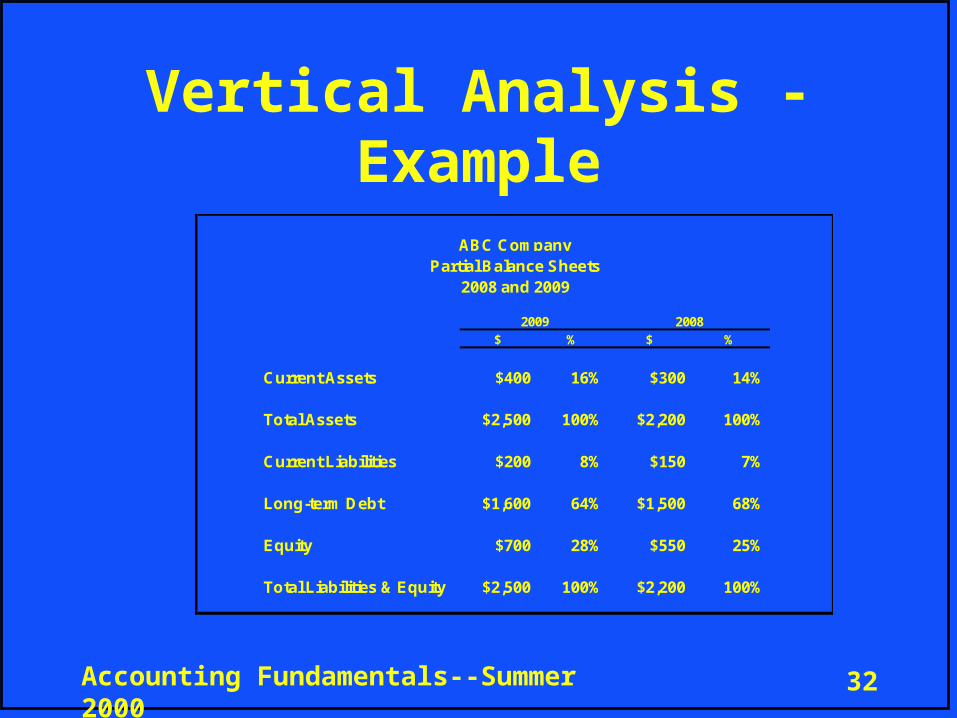

Vertical Analysis - Example

$ % $ %

Current Assets $400 16% $300 14%

Total Assets $2,500 100% $2,200 100%

Current Liabilities $200 8% $150 7%

Long-term Debt $1,600 64% $1,500 68%

Equity $700 28% $550 25%

Total Liabilities & Equity $2,500 100% $2,200 100%

ABC CompanyPartial Balance Sheets

2008 and 2009

2009 2008

Accounting Fundamentals--Summer 2000

33

Theory of Constraints

• The Concept• The Process• The Measures

Accounting Fundamentals--Summer 2000

34

The Concept• Presented in Eliyahu Goldratt’s

The Goal• The goal of a business is to

make money…consistent with customer satisfaction

• Continuous flow• Avoid the “herbies”• Eliminate the bottlenecks first

Accounting Fundamentals--Summer 2000

35

The Process

• Identify the constraints• Exploit the constraints (reduce

the bottlenecks)• Subordinate everything else• Elevate the constraints

(remove the bottlenecks)• Reiterate the process

Accounting Fundamentals--Summer 2000

36

The Measures

• Throughput - Net income• Inventory - ROI• Ops. Expenses - Cash Flow

Related Documents

![1st Quarter 2020 Earnings Call...2020/05/06 · Adjusted net earnings from continuing operations, before income taxes [Non-GAAP] 12.4 3.7 Income tax expense at 25% normalized tax](https://static.cupdf.com/doc/110x72/5f0429587e708231d40c9d88/1st-quarter-2020-earnings-call-20200506-adjusted-net-earnings-from-continuing.jpg)