ACCOUNTING FOR ACCOUNTING FOR RECEIVABLES RECEIVABLES Wed, Nov 26 will be Unit 3 Test Wed, Nov 26 will be Unit 3 Test (covering chapter 7 and 8) (covering chapter 7 and 8) CHAPTER CHAPTER 8 8

ACCOUNTING FOR RECEIVABLES Wed, Nov 26 will be Unit 3 Test (covering chapter 7 and 8) CHAPTER 8.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACCOUNTING FOR ACCOUNTING FOR RECEIVABLESRECEIVABLES

Wed, Nov 26 will be Unit 3 Test Wed, Nov 26 will be Unit 3 Test (covering chapter 7 and 8) (covering chapter 7 and 8)

CHAPTERCHAPTER

88

• Since Adorable Garment has many companies (and individuals) as customer, they would like to keep track of each customer’s AR.

• Most companies use a subsidiary ledger to keep track of individual customer accounts.

• Each entry which affects AR is posted twice – once to the subsidiary ledger and once to the general ledger. (manual system)

• In computerized accounting you just have to post once to the subsidiary ledger.

Subsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR Ledger

• Normally entries to the subsidiary ledger are posted daily while entries to the general ledger are summarized and posted monthly.

• For example, the previous transaction was posted to subsidiary ledger called, “AR – Zellers” on July 1.

• On July 31, this transaction will be combined with other sales entries of the month ($6000 + 3000+ 1000 = 10000) in a special sales journal and posted to the accounts receivable control account in the general ledger at the end of the month.

Subsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR Ledger

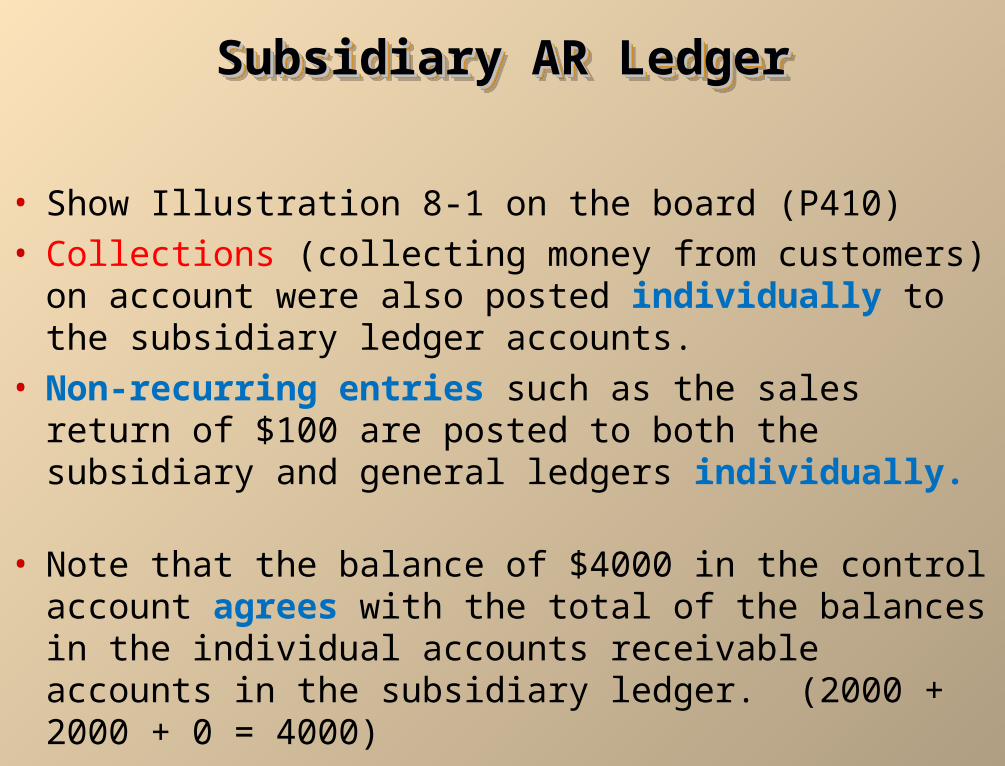

• Show Illustration 8-1 on the board (P410)• Collections (collecting money from customers) on account

were also posted individually to the subsidiary ledger accounts.

• Non-recurring entries such as the sales return of $100 are posted to both the subsidiary and general ledgers individually.

• Note that the balance of $4000 in the control account agrees with the total of the balances in the individual accounts receivable accounts in the subsidiary ledger. (2000 + 2000 + 0 = 4000)

Subsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR LedgerSubsidiary AR Ledger

• If the customer does not pay their AR debt in 30 days, then the business can charge interest revenue.

• The interest rate depends on the negotiations that buyer and seller made while negotiating the terms.

• If Kids Online Store still owes $2000 on August 31, then the business will charge $30 = ($2000 * 0.18 *1/12)

• August 31 AR – Kids Online 30

Interest Revenue 30

To record interest on amount due• Interest Revenue is included in other revenues in the non-

operating section of the Income Statement because this company’s business operation is manufacturing.

Interest RevenueInterest RevenueInterest RevenueInterest Revenue

• In Chapter 7, we learned that debit and bank credit card sales are cash sales. •Store credit card sales (such as Canadian Tire credit card and Sears credit card) are not cash sales. (debit AR until the credit card company pays the amount)

Nonbank Credit Card SalesNonbank Credit Card SalesNonbank Credit Card SalesNonbank Credit Card Sales

•Example: Suppose Long M Music accepts a nonbank credit card (= store credit card) on October 24 for $500 sale.

Oct 24 AR – Credit card company 480

Credit Card expense (4%) 20

Sales 500•20 = 0.04 * 500•Credit card expense and debit card expenses are reported as an operating expense in the income statement.

Nonbank Credit Card SalesNonbank Credit Card SalesNonbank Credit Card SalesNonbank Credit Card Sales

• Some receivables ends up becoming uncollectible. (= customer will not be able to pay his or her debt…going bankrupt)

• Only collectible receivables can be reported as assets in the financial statements.

• This collectible amount is called the net realizable value of the receivables.

Valuing ARValuing ARValuing ARValuing AR

• To ensure that receivables are not overstated on the balance sheet, they are stated at their net realizable value.

• Net realizable value is the net amount expected to be received in cash and excludes amounts that the company estimates it will not be able to collect.

• NRV = AR – Bad debt (uncollectible AR)

VALUING VALUING ACCOUNTS RECEIVABLEACCOUNTS RECEIVABLEVALUING VALUING

ACCOUNTS RECEIVABLEACCOUNTS RECEIVABLE

• No matter how reliable (in terms of paying their AR on time) the customer has been in the past, some AR becomes uncollectible.

• When receivables are written down to their net realizable value because of credit losses, owner’s equity must also be reduced. (by debiting bad debt expense account)

Valuing ARValuing ARValuing ARValuing AR

• The key issue is “when do you record these uncollectible AR (credit losses)?”

• If the company waits until it knows for sure that the specific account will not be collected, then it could end up recording the bad debt expense in a different period than when the revenue is recorded.

• Violating which GAAP principle?

Valuing ARValuing ARValuing ARValuing AR

• Two methods of accounting for

uncollectible accounts are:

1. Allowance method

(honors matching principle)

2. 2.Direct write-off method

VALUINGVALUING

ACCOUNTS RECEIVABLEACCOUNTS RECEIVABLE

VALUINGVALUING

ACCOUNTS RECEIVABLEACCOUNTS RECEIVABLE

• Under the direct write-off method, no entries are made for bad debts until an account is determined to be uncollectible at which time the loss is charged to Bad Debts Expense.

• No attempt is made to match bad debts to sales revenues or to show the net realizable value of accounts receivable on the balance sheet.

• Is allowed by IFRS and US IRS (but US GAAP does not allow)

DIRECT WRITE-OFF METHODDIRECT WRITE-OFF METHODDIRECT WRITE-OFF METHODDIRECT WRITE-OFF METHOD

• The allowance method is required when bad debts are deemed to be material in amount.

• Uncollectible amounts are estimated (before the it is deemed uncollectible) and the expense for the uncollectible accounts is matched against sales in the same accounting period in which the sales occurred.

• It honors matching principle• IFRS and US GAAP allows this method. • But US IRS (Tax agency) does not allow this

method.

THE ALLOWANCE METHODTHE ALLOWANCE METHODTHE ALLOWANCE METHODTHE ALLOWANCE METHOD

Estimated uncollectible amounts are debited to Bad Debts Expense and credited to Allowance for Doubtful Accounts (a contra asset account of AR account) at the end of each period.

Estimated uncollectible amounts are debited to Bad Debts Expense and credited to Allowance for Doubtful Accounts (a contra asset account of AR account) at the end of each period.

THE ALLOWANCE METHODTHE ALLOWANCE METHODTHE ALLOWANCE METHODTHE ALLOWANCE METHOD

Date Account Title and Explanation Debit CreditDec. 31 Bad Debts Expense 24,000

Allowance for Doubtful Accounts 24,000 To record estimate of uncollectible accounts.

GENERAL JOURNAL

• Companies use either of two methods in the estimation of uncollectible accounts:

1. Percentage of sales

2. Percentage of receivables

• Both bases are GAAP; the choice is a management decision.

BASES USED FOR THE BASES USED FOR THE ALLOWANCE METHODALLOWANCE METHODBASES USED FOR THE BASES USED FOR THE ALLOWANCE METHODALLOWANCE METHOD

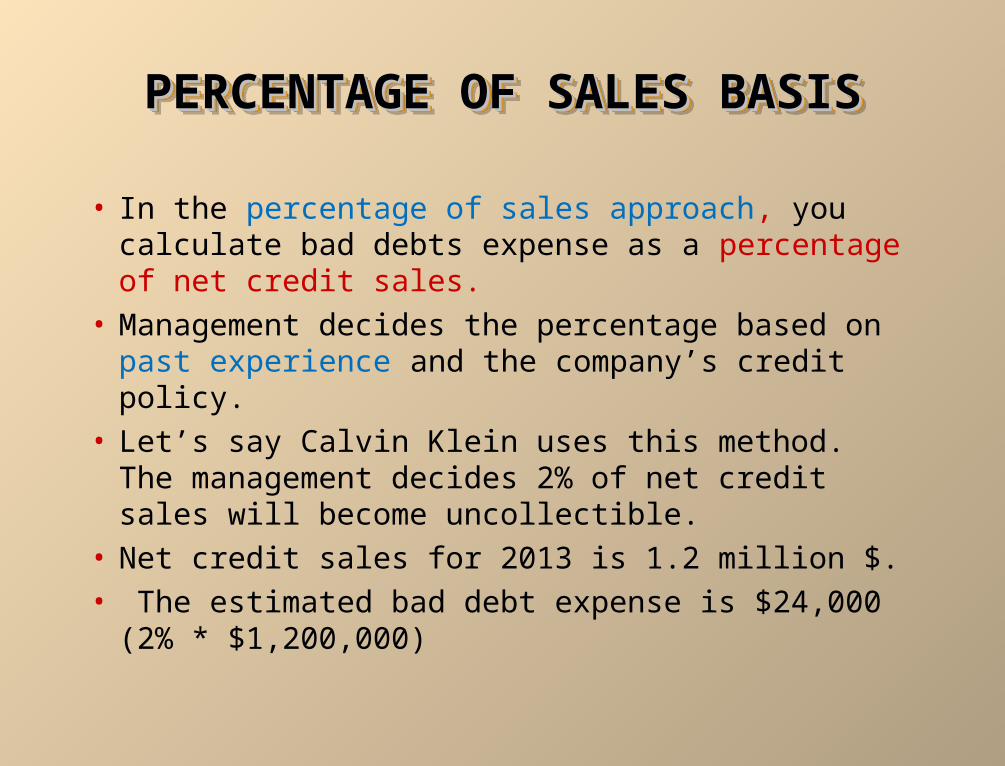

• In the percentage of sales approach, you calculate bad debts expense as a percentage of net credit sales.

• Management decides the percentage based on past experience and the company’s credit policy.

• Let’s say Calvin Klein uses this method. The management decides 2% of net credit sales will become uncollectible.

• Net credit sales for 2013 is 1.2 million $. • The estimated bad debt expense is $24,000 (2% *

$1,200,000)

PERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASIS

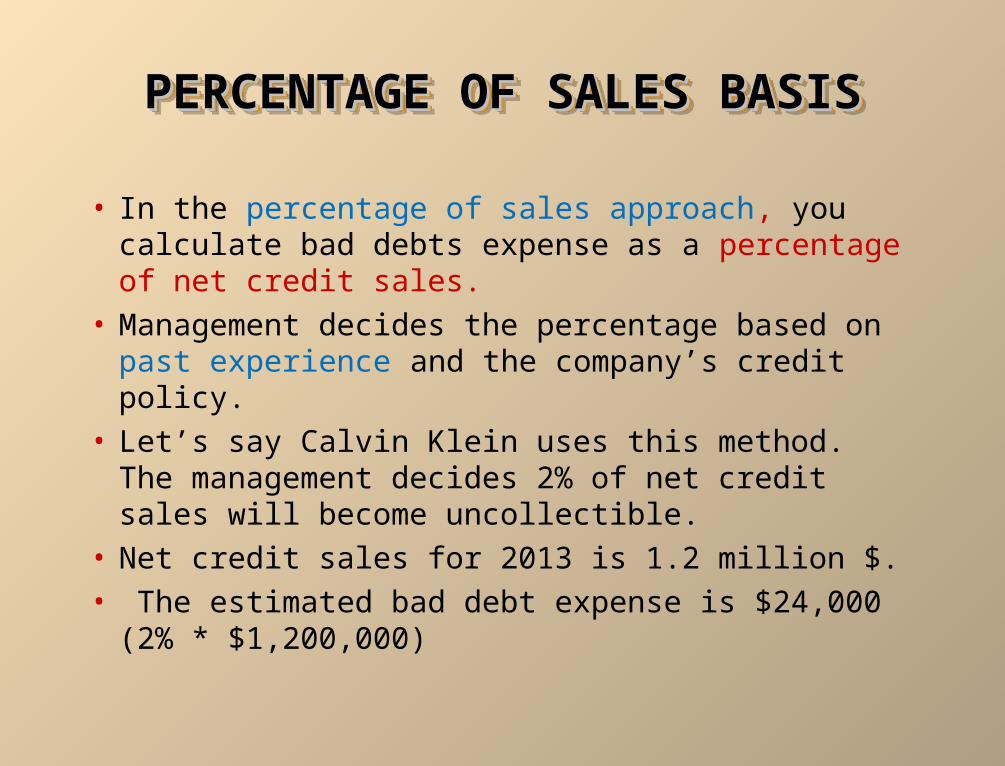

• In the percentage of sales approach, you calculate bad debts expense as a percentage of net credit sales.

• Management decides the percentage based on past experience and the company’s credit policy.

• Let’s say Calvin Klein uses this method. The management decides 2% of net credit sales will become uncollectible.

• Net credit sales for 2013 is 1.2 million $. • The estimated bad debt expense is $24,000 (2% *

$1,200,000)

PERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASIS

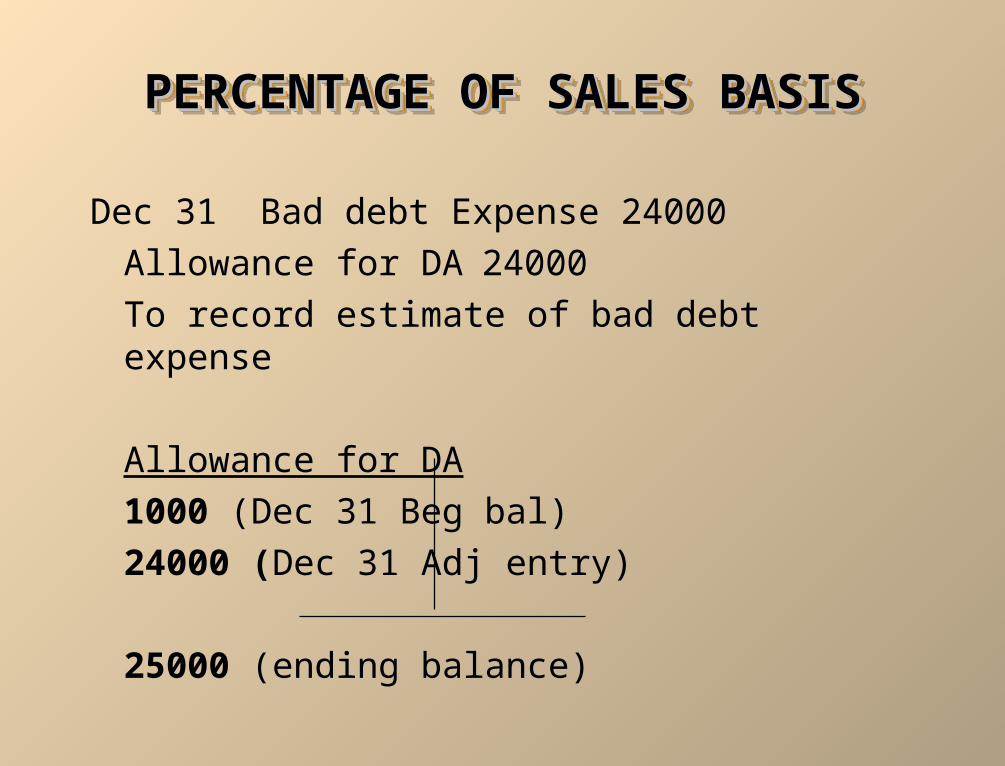

Dec 31 Bad debt Expense 24000

Allowance for DA 24000

To record estimate of bad debt expense

Allowance for DA

1000 (Dec 31 Beg bal)

24000 (Dec 31 Adj entry)

25000 (ending balance)

PERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASIS

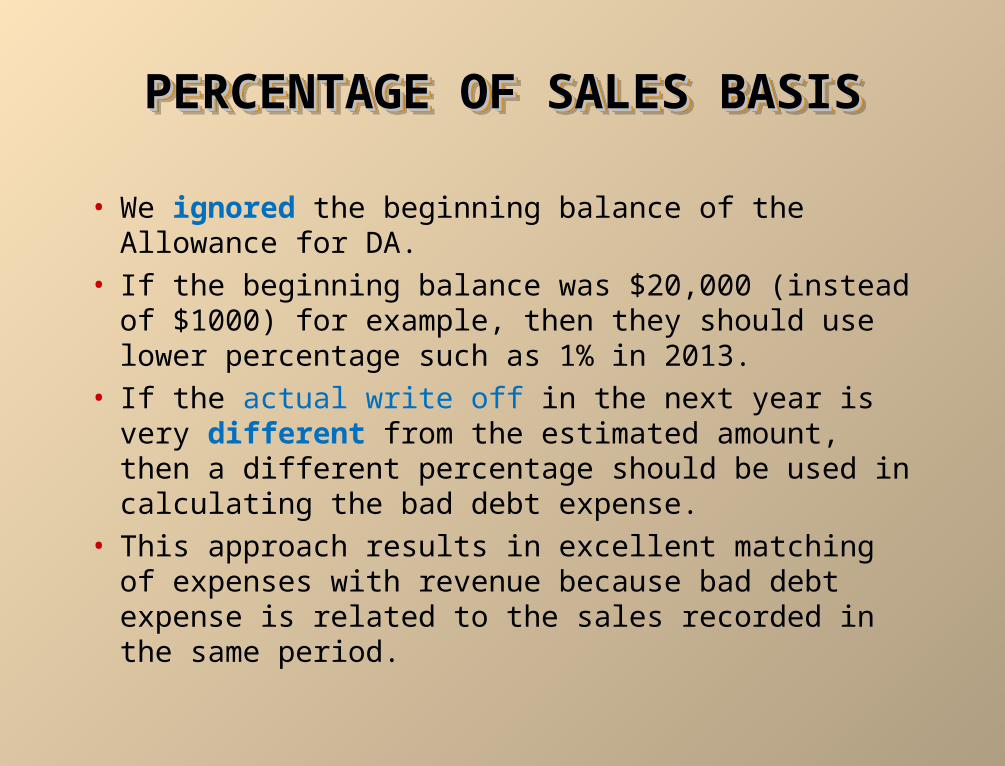

• We ignored the beginning balance of the Allowance for DA.

• If the beginning balance was $20,000 (instead of $1000) for example, then they should use lower percentage such as 1% in 2013.

• If the actual write off in the next year is very different from the estimated amount, then a different percentage should be used in calculating the bad debt expense.

• This approach results in excellent matching of expenses with revenue because bad debt expense is related to the sales recorded in the same period.

PERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASIS

• This method is easier than percentage of receivables approach.

• Some people call this one as income statement approach.

PERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASISPERCENTAGE OF SALES BASIS

• P434 be8-4, • P436 e8-2, e8-3, e8-4 (sales basis)

Classwork / HomeworkClasswork / HomeworkClasswork / HomeworkClasswork / Homework

Related Documents