Accounting Exposure Eiteman et al., Chapter 10 Winter 2004 Accounting Exposure Accounting exposure, also called translation exposure, results from the need to restate foreign subsidiaries’ financial statements, usually stated in foreign currency, into the parent’s reporting currency when preparing the consolidated financial statements. Restating financial statements may lead to changes in the parent’s net worth or net income. 2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting Exposure

Eiteman et al., Chapter 10

Winter 2004

Accounting Exposure

Accounting exposure, also calledtranslation exposure, results

from the need to restate foreign subsidiaries’ financial statements,

usually stated in foreign currency, into the parent’s reporting

currency when preparing the consolidated financial statements.

Restating financial statements may lead to changes in the

parent’s net worth or net income.

2

Translation Exposure

When converting financial statement items (transactions)

denominated in currencies other than the parent currency, two

choices of exchange rate are possible:

• Thehistorical rate, the exchange rate prevailing at the time

of the transaction

• Thecurrent rate, the exchange rate prevailing at the balance

sheet date or during the income statement period

3

Translation Exposure

Conversion of financial statements into the parent’s currency

creates the following concerns:

• The exposure to exchange rate changes

• The treatment of translation gains or losses

4

Translation Exposure

SFAS 52 provides two translation methods:

• Thetemporal method, or remeasurementprocess

• Thecurrent rate method, or translationprocess

5

Translation Exposure

The method used to restate financial statements is based on the

choice offunctional currencyfor each subsidiary.

The functional currency is the primary currency used in the

subsidiary’s operations.

This currency may be the foreign subsidiary’s local currency, the

parent’s currency, or a third currency.

6

Translation Exposure

There exists three categories of foreign operations:

• Relatively self-contained, independent entities operating primarily in

local markets. The functional currency of these entities is generally the

local currency.

• Significantly integrated operations that serve as sales outlets for the

parent’s products and services. The functional currency should be the

parent’s currency in this case.

• Subsidiaries operating in highly inflationary economies. The use of the

parent’s currency as the functional currency is required in this case.

7

Translation Exposure

• If the foreign entity’s functional currency is the local

currency, financial statements are translated using the

current rate method.

• If the foreign entity’s functional currency is the parent’s

currency, financial statements are remeasured using the

temporal method.

8

Translation Exposure

If the functional currency of a foreign subsidiary is not the local

currency, then the subsidiary’s financial statements are

1. Remeasured in the subsidiary’s functional currency using the

temporal method;

2. Translated from functional to parent’s currency using the

current rate method.

9

The Current Rate Method

• All assets and liabilities are translated at the rate in effect on the balance

sheet date.

• All items on the income statement are translated at an appropriate average

exchange rate or at the rate prevailing when the various revenues,

expenses, gains and losses were incurred (historical rate).

• Dividends paid are translated at the rate in effect on the payment date.

• Common stock, paid-in capital and retained earnings are translated at

historical rates.

10

The Current Rate Method

When the current rate method is used, gains and losses from

translation are reported in a separate equity account called

cumulative translation adjustment (CTA).

Gains and losses do not appear in the income statement when the

current rate method is used.

11

The Current Rate Method

Advantages of CTA

• Eliminates the variability of net earnings due to translation gains or

losses.

• The relative proportions of individual balance sheet accounts remain the

same (debt-to-equity ratio, for example).

Main disadvantage of CTA

• Violates the accounting principle of carrying balance sheet accounts at

historical cost.

12

The Current Rate Method

Under the current rate method, translation exposure is

Assets(A) − Liabilities(L) = stockholders’ equity(SE).

Common stock and retained earnings, for example, are part of

SE. If common stock is issued at some point in time, then the

value of the issue in the parent’s currency is determined by the

exchange rate prevailing when the shares were issued.

13

The Current Rate Method

Similarly, the value of the earnings retained during a year in the

parent’s currency is based on the exchange rate used to translate

the income statement in that year.

When the exchange rate changes, the value ofA−L in the

parent’s currency varies but the value ofSE in the parent’s

currency stays the same or, at least, changes according to a

different rate. The CTA account is needed for the balance sheet

to balance.

14

The Current Rate Method: An Example

Foreign Subsidiary, Inc., (FSI) has been acquired on December

31, 2000 when the exchange rate was LC1.25/$ (LC stands for

FSI’s local currency).

On December 31, 2001, the exchange rate was LC1.15/$. The

average exchange rate during 2001 was LC1.18/$.

On December 31, 2002, the exchange rate was LC1.22/$. The

average exchange rate during 2002 was LC1.20/$.

15

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Assets as of December 31 (in LC)

2000 2001 2002

Cash 41 204 400Accounts receivable 360 492 570Inventory 210 264 372Current assets 611 960 1,342Fixed assets 1,032 1,512 2,208Accumulated depreciation 180 432 732Net fixed assets 852 1,080 1,296Total assets 1,463 2,040 2,638

16

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Liabilities and Equity as of December 31 (in LC)

2000 2001 2002

Accounts payable 306 348 288Notes payable 132 156 216Long-term debt 168 528 948Total liabilities 606 1,032 1,452Common stock 276 276 276Retained earnings 581 732 910Total equity 857 1,008 1,186Total liabilities and equity 1,463 2,040 2,638

17

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Income Statement (in LC)

2001 2002

Revenues 1,548 1,716COGS 648 733Gross margin 900 983Depreciation 252 300Other expenses 497 505Net income 151 178

18

The Current Rate Method: An Example

Under the current rate method, all assets and all liabilities are

translated using the exchange rate in effect on the balance sheet

date (December 31 of each year).

Equity items are translated using the appropriate historical

exchange rate and all income statement items are translated at the

exchange rate at the time of the transaction (the average annual

exchange rate).

19

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Assets as of December 31 (in $)

2000 2001 2002(Rate) (LC1.25/$) (LC1.15/$) (LC1.22/$)

Cash 33 177 328Accounts receivable 288 428 467Inventory 168 230 305Current assets 489 835 1,100Fixed assets 826 1,315 1,662Accumulated depreciation 144 376 600Net fixed assets 682 939 1,062Total assets 1,170 1,774 2,162

20

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Liabilities and Equity as of December 31 (in $)

2000 2001 2002

Accounts payable 245 303 236Notes payable 106 136 177Long-term debt 134 459 777Total liabilities 485 897 1,190Common stock ? ? ?Retained earnings ? ? ?Total equity ? ? ?Cumulative translation adjustment ? ? ?Total liabilities and equity 1,170 1,774 2,162

21

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Income Statement (in $)

2001 2002(Rate) (LC1.18/$) (LC1.20/$)

Revenues 1,312 1,430COGS 549 611Gross margin 763 819Depreciation 214 250Other expenses 421 421Net income 128 148

22

The Current Rate Method: An Example

What happens to common stock (CS)?

The subsidiary was acquired on December 31, 2000, and thus the

initial value for common stock, 276, is translated using the

exchange rate on December 31, 2000, which gives

CS2000 =2761.25

= $221.

Since common stock does not change in 2001 and 2002, the

translated value is $221 in these years, too.

23

The Current Rate Method: An Example

What happens to retained earnings (RE)?

Retained earnings in 2000 are translated at the rate prevailing

when the company was acquired, i.e. LC1.25/$, which gives

RE2000 = 5811.25 = $465.

In 2001, retained earnings increased by LC151. The appropriate

rate for this change being the average exchange rate LC1.18/$,

translated retained earnings in 2001 are

RE2001 = RE2000 + 1511.18 = 465 + 128 = $593.

24

The Current Rate Method: An Example

In 2002, retained earnings increased by LC178 and the 2002

average exchange rate is LC1.20/$. Translated retained earnings

in 2002 are then

RE2002 = RE2001 + 1781.20 = 593 + 148 = $741.

25

The Current Rate Method: An Example

Foreign Subsidiary, Inc.Liabilities and Equity as of December 31 (in $)

2000 2001 2002

Accounts payable 245 303 236Notes payable 106 136 177Long-term debt 134 459 777Total liabilities 485 897 1,190Common stock 221 221 221Retained earnings 465 593 741Total equity 685 814 962Cumulative translation adjustment – 63 10Total liabilities and equity 1,170 1,774 2,162

26

The Temporal Method

• Monetary assets (cash, marketable securities, accounts

receivable,inventory) and monetary liabilities (current

liabilities and long-term debt) are translated at the current

exchange rate (exchange rate at the balance sheet date).

• Non-monetary assets (inventory, fixed assets, etc.) and

non-monetary liabilitites are translated at their historical

rate.

27

The Temporal Method

Note:

• Inventory is considered a monetary asset if it is recorded at

market value on the balance sheet. If it is recorded at

historical cost, then it is considered a non-monetary asset.

28

The Temporal Method

• Income statement items are translated at the average exchange rate

over the period, except for items that are associated with

non-monetary assets or liabilities, such as cost of goods sold

(inventory) and depreciation (fixed assets), which are translated at

their historical rate.

• Dividends paid are translated at the rate in effect on the payment

date.

• Equity items are translated at their historical rate, and include any

imbalance.

29

The Temporal Method

Under this method, gains and losses appear on the income

statement.

Gains and losses on the balance sheet will be hidden in

stockholders’ equity.

The exposure to exchange rate changes under this method is

Monetary Assets− Monetary Liabilities.

30

The Temporal Method

Logic behind differentiating monetary and non-monetary assets:

• Translation gains and losses on monetary accounts are

presumed meaningful components of expenses or revenue

because monetary accounts closely approximate market

values.

• Translation gains and losses on non-monetary accounts are

less meaningful since non-monetary accounts reflect

historical costs.

31

The Temporal Method: An Example

Let us remeasure FSI’s financial statements using the temporal

method.

The methodology is the same as with the current rate method for

cash, accounts receivable, accounts payable, notes payable,

long-term debt, common stock, revenues and other expenses.

32

The Temporal Method: An Example

Foreign Subsidiary, Inc.Assets as of December 31 (in $)

2000 2001 2002

Cash 33 177 328Accounts receivable 288 428 467Inventory 168 ? ?Current assets 489 ? ?Fixed assets 826 ? ?Accumulated depreciation 144 ? ?Net fixed assets 682 ? ?Total assets 1,170 ? ?

33

The Temporal Method: An Example

Foreign Subsidiary, Inc.Liabilities and Equity as of December 31 (in $)

2000 2001 2002

Accounts payable 245 303 236Notes payable 106 136 177Long-term debt 134 459 777Total liabilities 485 897 1,190Common stock 221 221 221Retained earnings 465 ? ?Total equity 685 ? ?Total liabilities and equity 1,170 ? ?

34

The Temporal Method: An Example

Foreign Subsidiary, Inc.Income Statement (in $)

2001 2002

Revenues 1,312 1,430COGS ? ?Gross margin ? ?Depreciation ? ?Other expenses 421 421Foreign exchange gain (loss) ? ?Net income ? ?

35

The Temporal Method: An Example

COGS

COGS was LC648 in 2001. Assuming FIFO as the inventory

accounting method, this means that the 2000 inventory of 210

has been sold and the rest has been purchased throughout 2001 at

the 2001 average exchange rate. That is,

COGS2001 =2101.25

+648−210

1.18= $539.

The same procedure can be applied to obtain 2002 COGS.

36

The Temporal Method: An Example

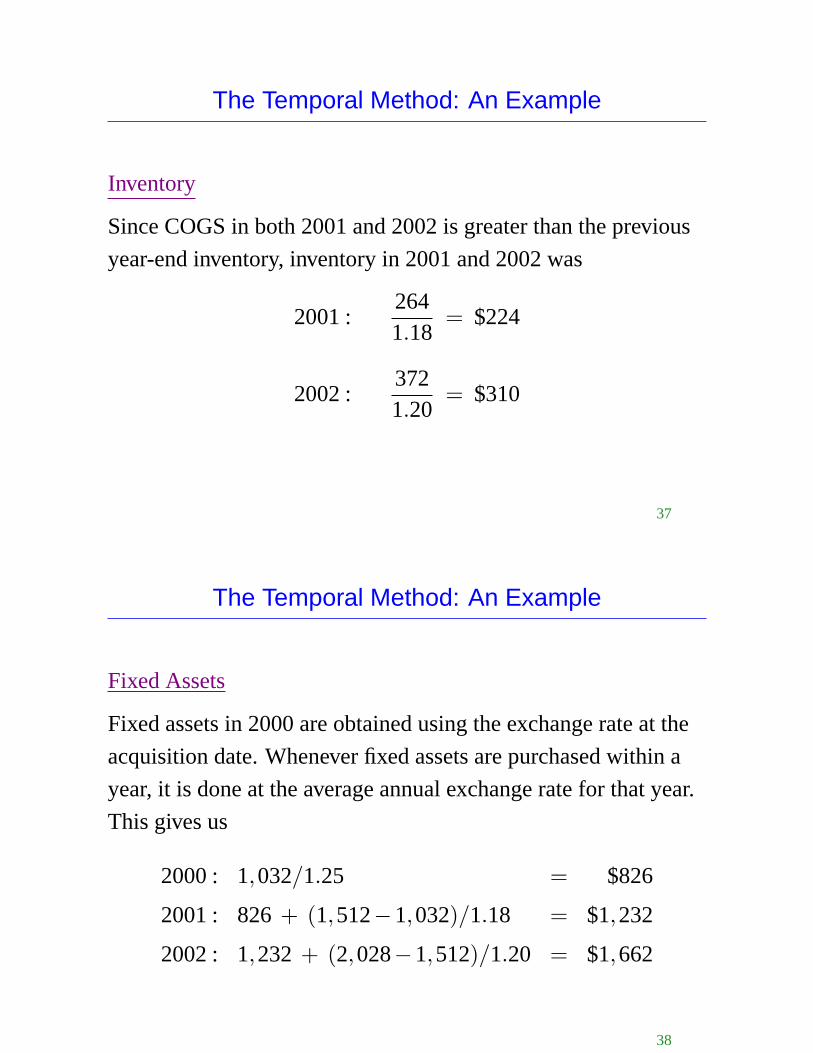

Inventory

Since COGS in both 2001 and 2002 is greater than the previous

year-end inventory, inventory in 2001 and 2002 was

2001 :2641.18

= $224

2002 :3721.20

= $310

37

The Temporal Method: An Example

Fixed Assets

Fixed assets in 2000 are obtained using the exchange rate at the

acquisition date. Whenever fixed assets are purchased within a

year, it is done at the average annual exchange rate for that year.

This gives us

2000 : 1,032/1.25 = $826

2001 : 826+ (1,512−1,032)/1.18 = $1,232

2002 : 1,232 + (2,028−1,512)/1.20 = $1,662

38

The Temporal Method: An Example

Depreciation

The rate used to remeasure depreciation has to be consistent with the

rates used to remeasure fixed assets. To do so, we can define blended

rates that will be used with depreciation. In 2001, for example, the

blended rate would be

Blended rate for 2001=FA2001 in LCFA2001 in $

=1,5121,232

= 1.227

and thus

Dollar depreciation in 2001=252

1.227= $205.

39

The Temporal Method: An Example

Depreciation

The same procedure applies for depreciation in 2002 and

accumulated depreciation increases with the depreciation

expense on the income statement.

Retained earningsare such that the balance sheet balances, and

thus a line for foreign exchange gain (or loss) has to be added to

the income statement.

40

The Temporal Method: An Example

Foreign Subsidiary, Inc.Assets as of December 31 (in $)

2000 2001 2002

Cash 33 177 328Accounts receivable 288 428 467Inventory 168 224 310Current assets 489 829 1,105Fixed assets 826 1,232 1,662Accumulated depreciation 144 349 595Net fixed assets 682 883 1,067Total assets 1,170 1,712 2,172

41

The Temporal Method: An Example

Foreign Subsidiary, Inc.Liabilities and Equity as of December 31 (in $)

2000 2001 2002

Accounts payable 245 303 236Notes payable 106 136 177Long-term debt 134 459 777Total liabilities 485 897 1,190Common stock 221 221 221Retained earnings 465 594 761Total equity 685 815 982Total liabilities and equity 1,170 1,712 2,172

42

The Temporal Method: An Example

Foreign Subsidiary, Inc.Income Statement (in $)

2001 2002

Revenues 1,312 1,430COGS 539 615Gross margin 773 815Depreciation 205 246Other expenses 421 421Foreign exchange gain (loss) (17) 19Net income 129 167

43

Current Rate vs Temporal

What effect does each method have on the firm’s ratios?

44

Related Documents