Accounting, Common Knowledge and the Dynamics of Stock Markets Shyam Sunder, Yale University Mini-conference on Overcoming Financialization and Its Crisis: Ideas from and Suggestions for Accounting, Economics and Law 21 st Annual Conference of the Society of the Advancement of Socio-economics, Paris, July 16-18, 2009

Accounting, Common Knowledge and the Dynamics of Stock Markets Shyam Sunder, Yale University Mini-conference on Overcoming Financialization and Its Crisis:

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting, Common Knowledge and the Dynamics of Stock

MarketsShyam Sunder, Yale University

Mini-conference on Overcoming Financialization and Its Crisis: Ideas from and Suggestions for Accounting,

Economics and Law21st Annual Conference of the Society of the Advancement of

Socio-economics, Paris, July 16-18, 2009

An Overview• Common knowledge is a basic and oft-used assumption in

analyses of accounting and stock markets• However, absence and not presence of common knowledge is the

norm in the world (Hayek) • Absence of common knowledge undermines the standard present

value models of security valuation• Without common knowledge, markets are susceptible to

speculative indeterminacy• Blocked from a reasonable basis for backward induction, investors

resort to forward induction from history, and use historical data from financial reports

• FASB/IASB attempts to mark-to-market accounting undermine this important use of accounting by investors

• To safeguard from speculative bubbles and financial crises, accounting can serve investors better by providing reliable statistical history, leaving adjustments about the future to non-accountants

Emperor Has No Clothes

Stock Market

• Stock Market is like a newspaper beauty contest

• John Maynard Keynes, (1936)

Newspaper Beauty Contest

Which Face is the prettiest?

Which Face is the prettiest? Which Face is the prettiest? Which Face is the prettiest?

Which face will they judge to be the prettiest?

Which Face is the prettiest? Which Face is the prettiest? Which Face is the prettiest?

Which face will they judge to be the prettiest?

Which Face is the prettiest? Which Face is the prettiest? Which Face is the prettiest?

Which face will they judge to be the prettiest?

Which Face is the prettiest? Which Face is the prettiest? Which Face is the prettiest?

Which face will they judge to be the prettiest?

Which face will they judge to be the prettiest?

Beliefs About Others’ Beliefs

• Common elements to the three stories about the emperor‘s clothes and stock market

• Central role of what we believe about others, and about their beliefs

Emperor’s Clothes

• The scoundrels made people believe that the clothes will be invisible only to the incompetent and the stupid

• People thought that others believed it

• Nobody wants to be seen as stupid or incompetent by others, lose his/her job

• Visibility of clothes was private, it was easy to fake seeing the clothes

Emperor’s Clothes (Contd.)

• Scenario 1: Everyone was privately convinced of their incompetence, and cheered to deny it publicly

• Scenario 2: People did not believe they were incompetent just because they could see the naked emperor, but believed that others so believed, and cheered to avoid being seen as stupid

What about the Child?

• The child did not know the link between visibility and competence

• Child was innocent, and said what he saw

• People know children to be innocent

• People knew that people knew this

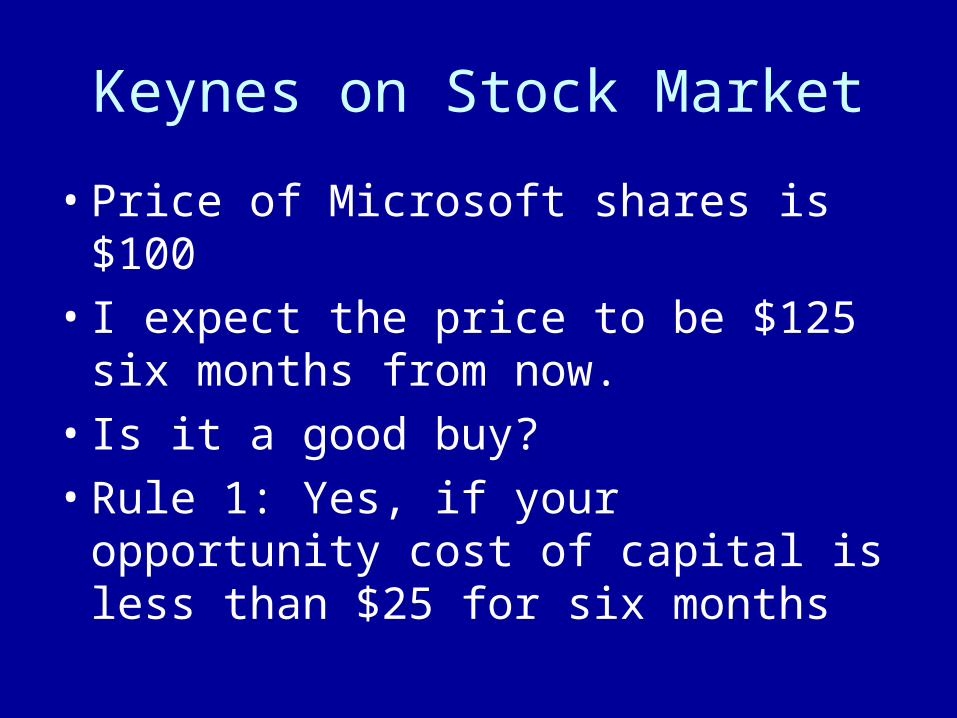

Keynes on Stock Market

• Price of Microsoft shares is $100

• I expect the price to be $125 six months from now.

• Is it a good buy?

• Rule 1: Yes, if your opportunity cost of capital is less than $25 for six months

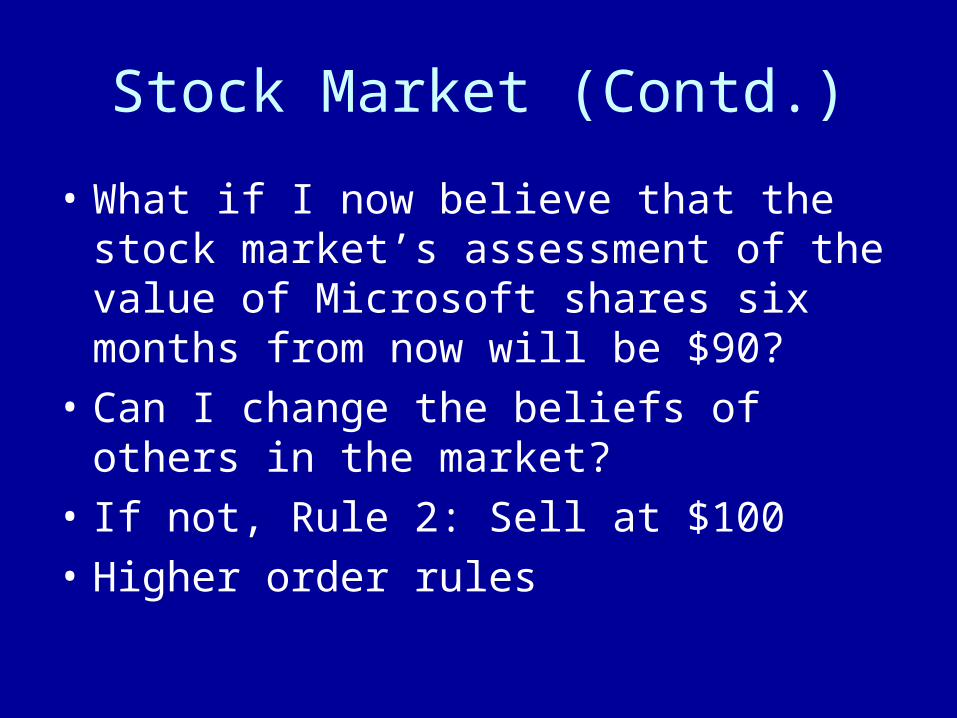

Stock Market (Contd.)

• What if I now believe that the stock market’s assessment of the value of Microsoft shares six months from now will be $90?

• Can I change the beliefs of others in the market?

• If not, Rule 2: Sell at $100

• Higher order rules

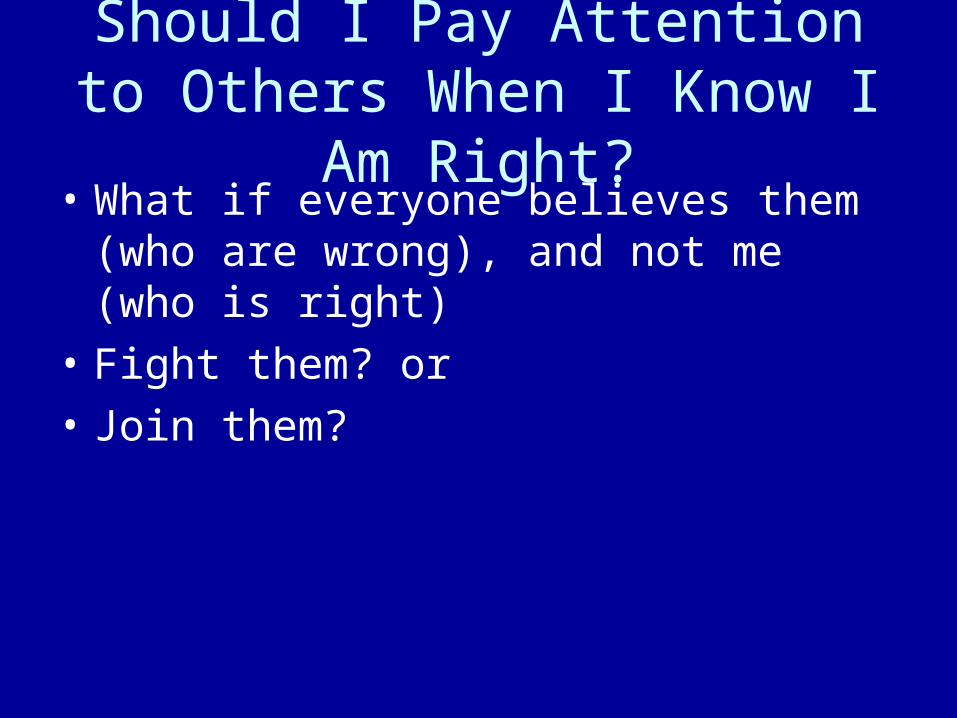

Should I Pay Attention to Others When I Know I Am Right?

• What if everyone believes them (who are wrong), and not me (who is right)

• Fight them? or

• Join them?

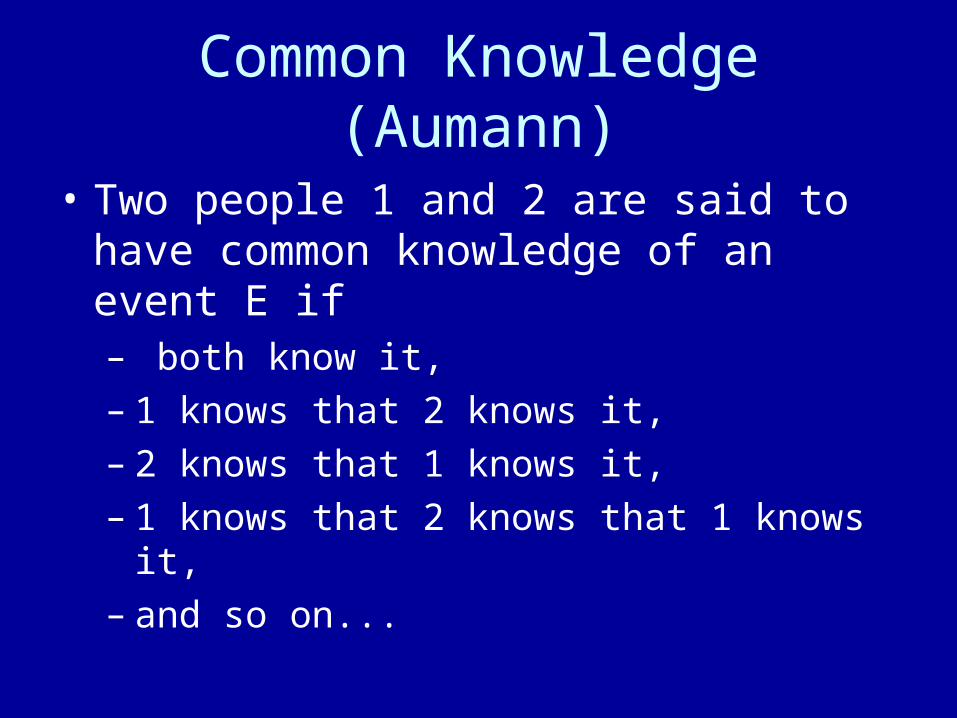

Common Knowledge (Aumann)

• Two people 1 and 2 are said to have common knowledge of an event E if– both know it, – 1 knows that 2 knows it, – 2 knows that 1 knows it, – 1 knows that 2 knows that 1 knows it, – and so on...

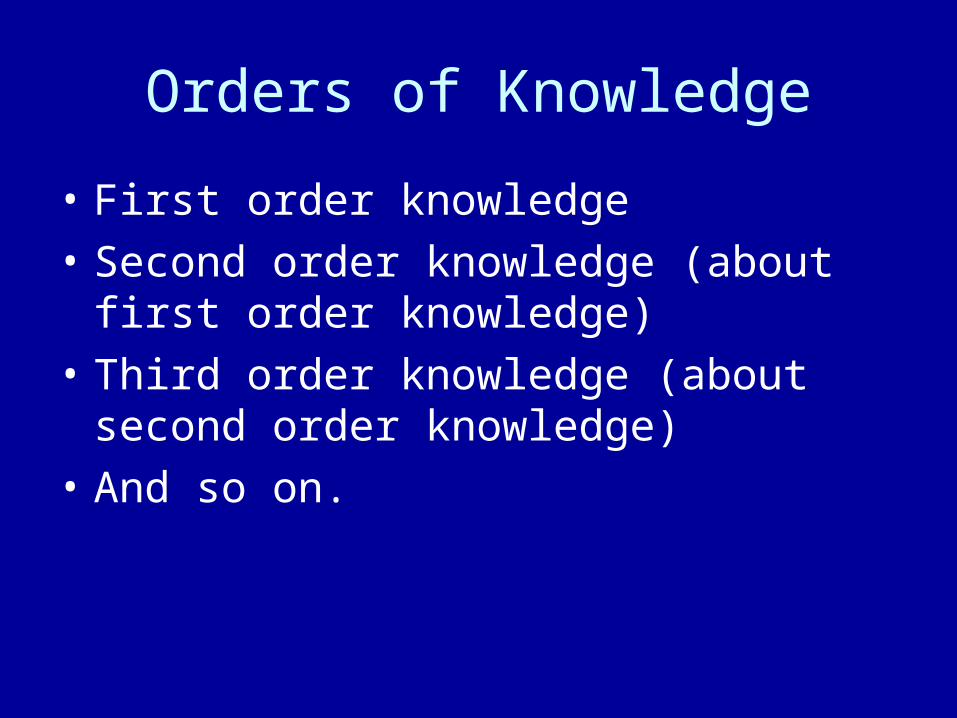

Orders of Knowledge

• First order knowledge

• Second order knowledge (about first order knowledge)

• Third order knowledge (about second order knowledge)

• And so on.

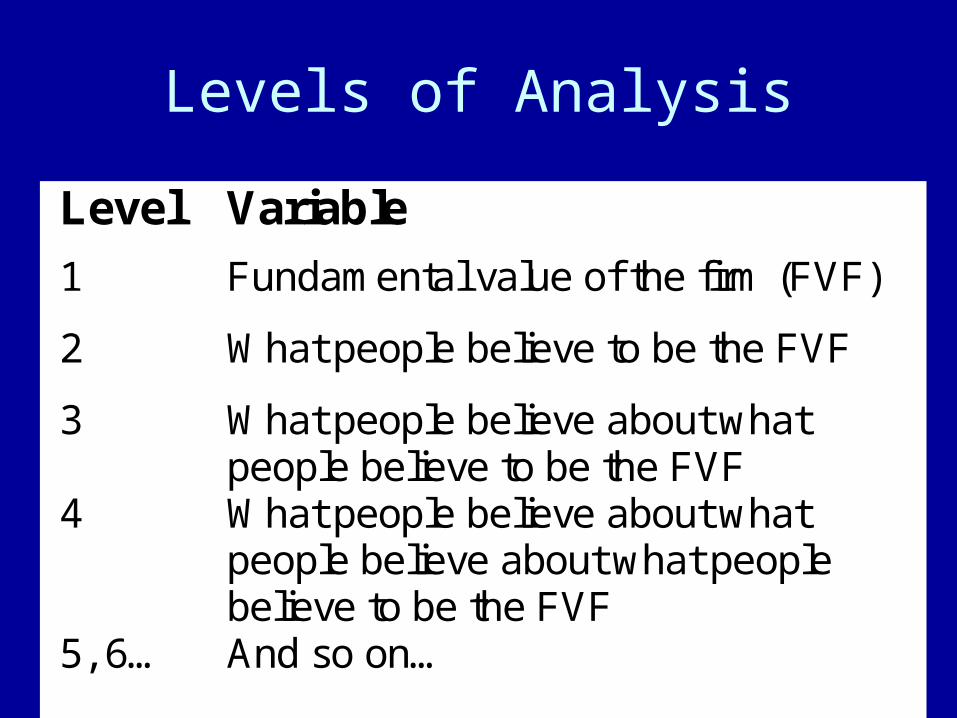

Levels of Analysis

Level Variable

1 Fundamental value of the firm (FVF)

2 What people believe to be the FVF

3 What people believe about what people believe to be the FVF

4 What people believe about what people believe about what people believe to be the FVF

5, 6… And so on…

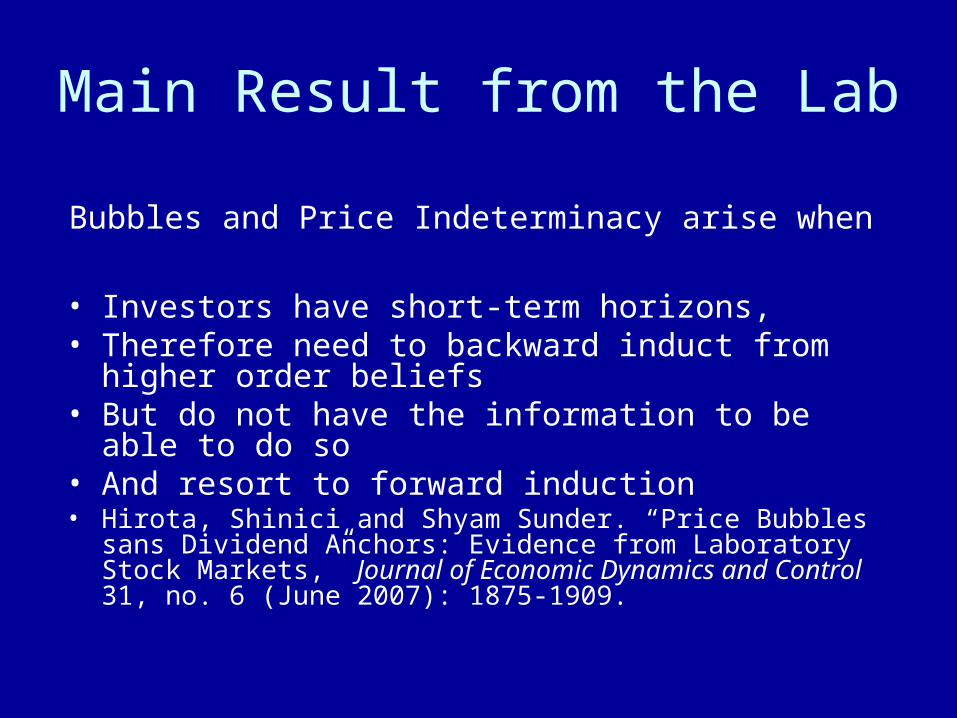

Main Result from the Lab

Bubbles and Price Indeterminacy arise when

• Investors have short-term horizons,• Therefore need to backward induct from higher order

beliefs• But do not have the information to be able to do so• And resort to forward induction• Hirota, Shinici and Shyam Sunder. “Price Bubbles sans Dividend

Anchors: Evidence from Laboratory Stock Markets,” Journal of Economic Dynamics and Control 31, no. 6 (June 2007): 1875-1909.

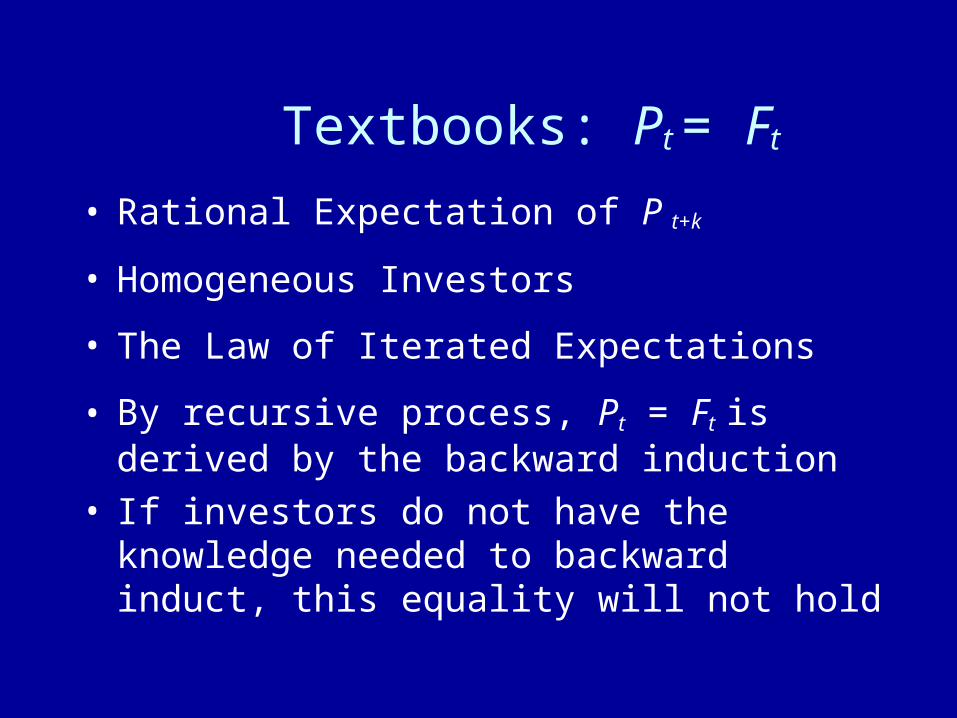

Textbooks: Pt = Ft

• Rational Expectation of P t+k

• Homogeneous Investors

• The Law of Iterated Expectations

• By recursive process, Pt = Ft is derived by the backward induction

• If investors do not have the knowledge needed to backward induct, this equality will not hold

Our Experimental Study

• What happens when short-term investors have difficulty in the backward induction?

• Two kinds of the lab markets – (1) Long-term Horizon Session

– (2) Short-term Horizon Session

• Bubbles are more likely to arise in (2)?

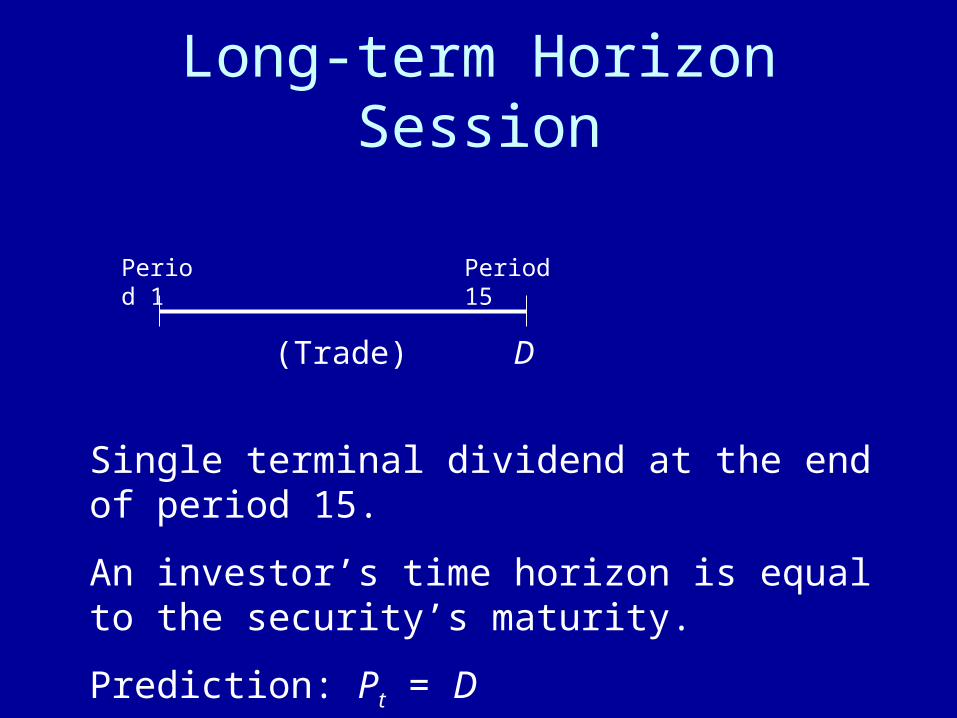

Long-term Horizon Session

Single terminal dividend at the end of period 15.

An investor’s time horizon is equal to the security’s maturity.

Prediction: Pt = D

Period 1 Period 15

D(Trade)

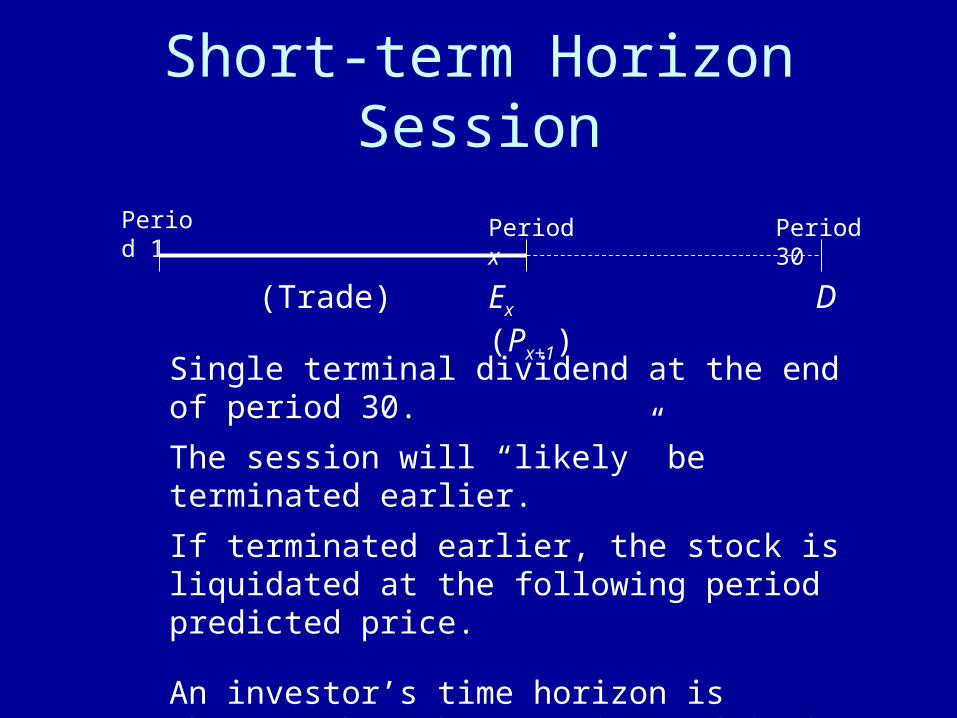

Short-term Horizon Session

Single terminal dividend at the end of period 30.

The session will “likely” be terminated earlier.

If terminated earlier, the stock is liquidated at the following period predicted price.

An investor’s time horizon is shorter than the maturity and it is difficult to backward induct.

Prediction: Pt D

Period 1 Period x Period 30

DEx (Px+1)(Trade)

Result 1

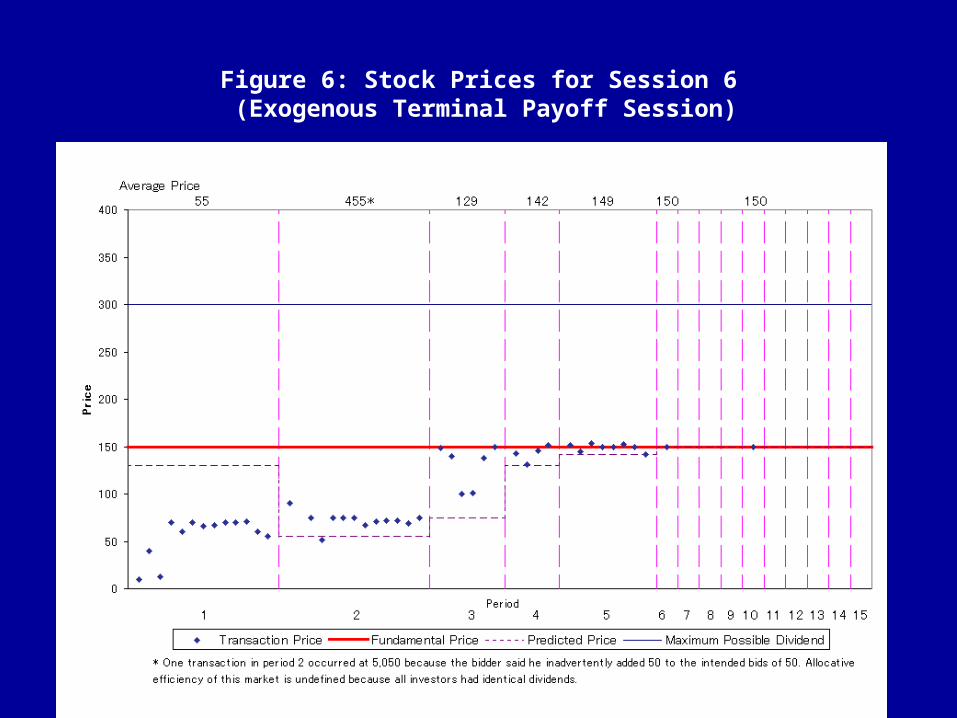

• In the long-horizon sessions, security prices converge to the fundamental values.

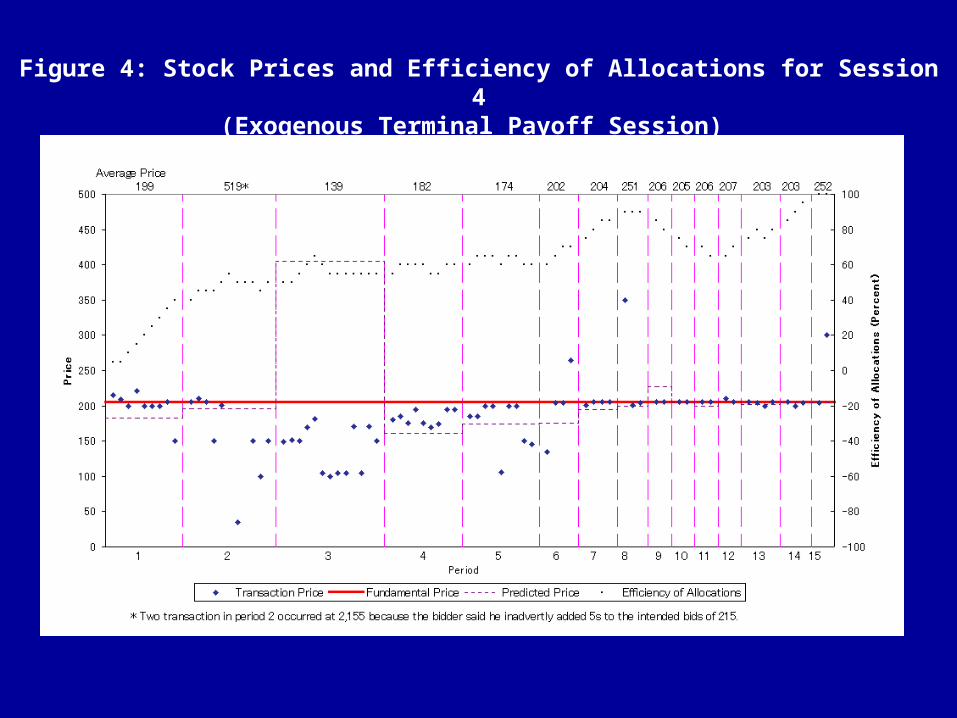

Figure 4: Stock Prices and Efficiency of Allocations for Session 4(Exogenous Terminal Payoff Session)

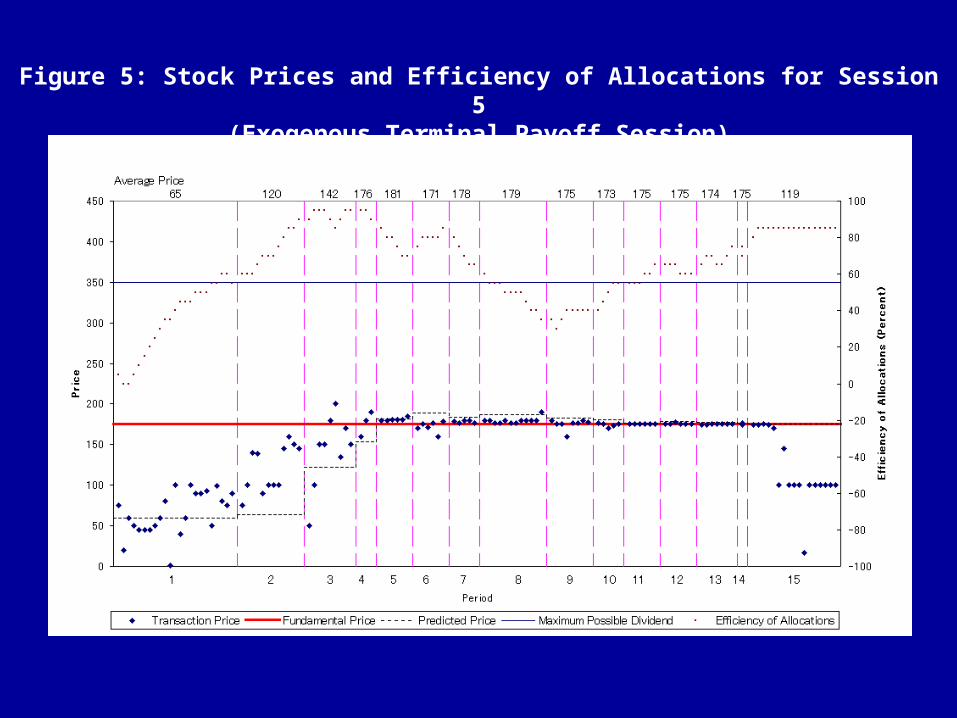

Figure 5: Stock Prices and Efficiency of Allocations for Session 5(Exogenous Terminal Payoff Session)

Figure 6: Stock Prices for Session 6 (Exogenous Terminal Payoff Session)

Figure 7: Stock Prices and Efficiency of Allocations for Session 7(Exogenous Terminal Payoff Session)

Discussion (long-horizon sessions)

• Long-horizon Investors play a crucial role in assuring efficient pricing.– Their arbitrage brings prices to the

fundamentals.

• Speculative trades do not seem to destabilize prices.– 39.0% of transactions were speculative

trades.

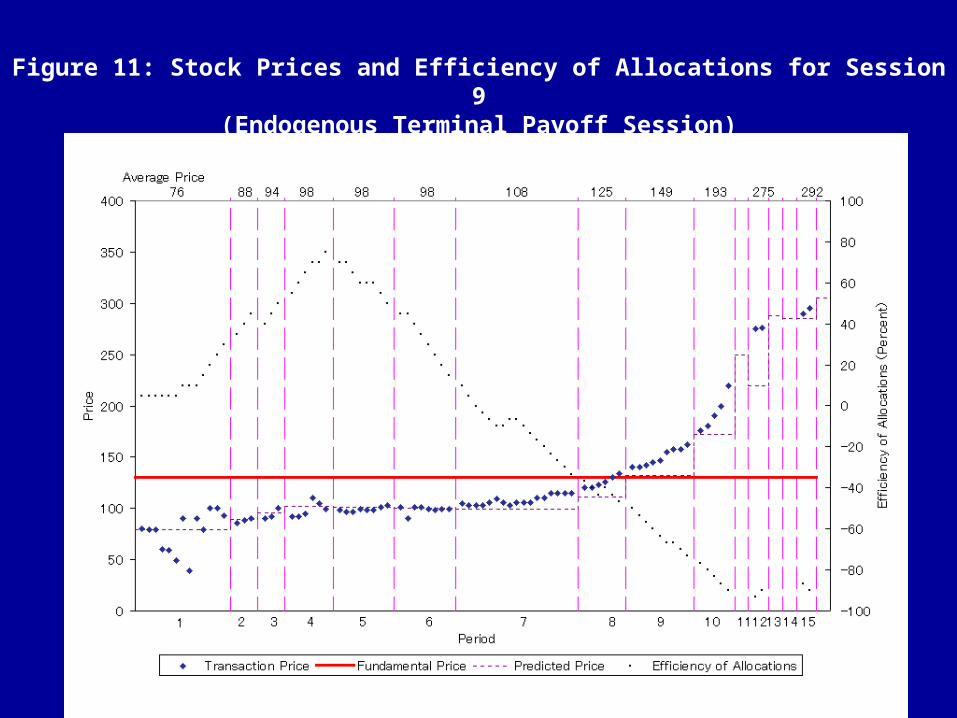

Result 2

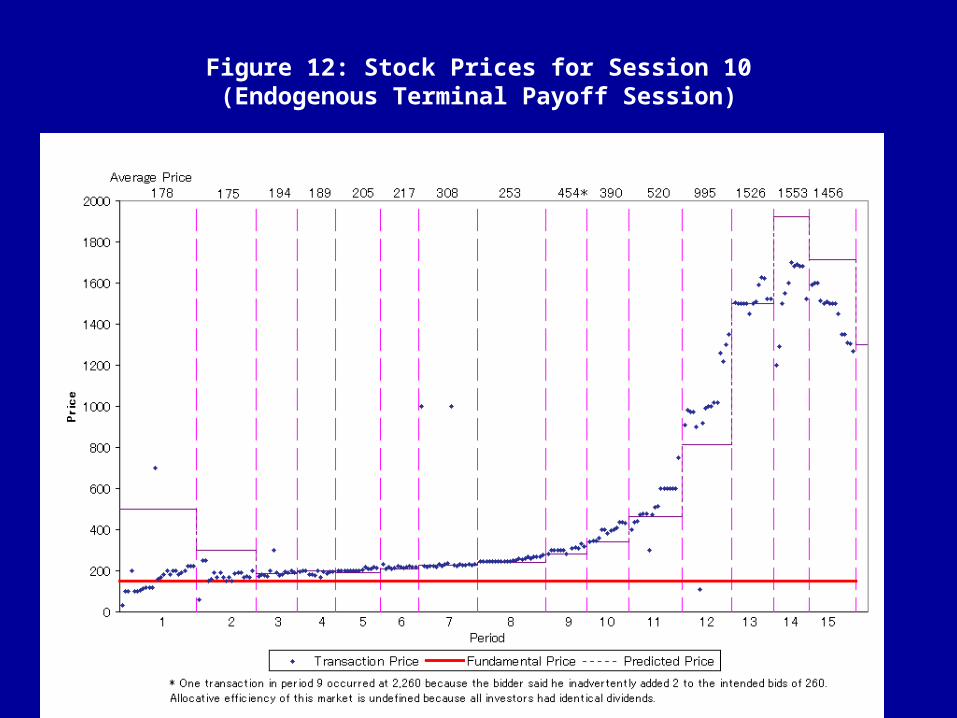

• In the short-horizon sessions, the security prices deviate from the fundamental values to form bubbles.

Figure 8: Stock Prices and Efficiency of Allocations for Session 1 (Endogenous Terminal Payoff Session)

Figure 9: Stock Prices and Efficiency of Allocations for Session 2 (Endogenous Terminal Payoff Session)

Figure 10: Stock Prices and Efficiency of Allocations for Session 8(Endogenous Terminal Payoff Session)

Figure 11: Stock Prices and Efficiency of Allocations for Session 9(Endogenous Terminal Payoff Session)

Figure 12: Stock Prices for Session 10(Endogenous Terminal Payoff Session)

Figure 13: Stock Prices for Session 11 (Endogenous Terminal Payoff Session)

Result 3

• In the long-horizon sessions, price expectations are consistent with backward induction.

• In the short-horizon sessions, price expectations are consistent with forward induction.

Discussion (Price Expectation)

• In long-horizon sessions, future price expectations are formed by fundamentals.

– Speculation stabilizes prices.

• In short-term sessions, future price expectations are formed by their own or actual prices.

– Speculation may destabilize prices.

Conclusion• Investors’ short-term horizons, and the

attendant difficulty of the backward induction, tends to give rise to price bubbles.

– Prices lose dividend anchors and become indeterminate.

– Future price expectations are formed by forward induction.

Implications (1)

• Bubbles are known to occur more often in markets for securities with – (i) longer maturity and duration

– (ii) higher uncertainty

• Consistent with our lab observations.

• Inputs to expectation formation matter:– Dividend policy matters!

– Accounting reports matter!

Implications (2)

• Ex post, market inefficiency, anomalies, and behavioral phenomena more likely to be observed in markets dominated by short-horizon investors (difficulty of backward induction)

• Ex ante, it is difficult to define them, because we do not know the fundamental values

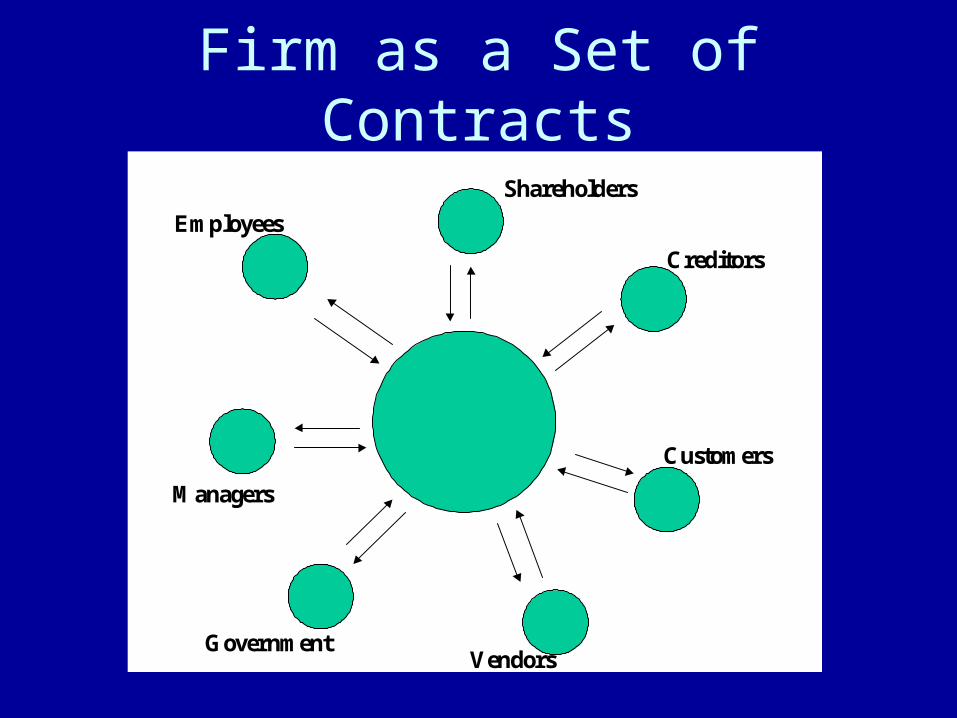

Theory of Accounting and Control

• Firm as a set of contracts• Agents try to attain their own goals• Agents contribute resources• Agents receive resources in exchange• Accounting as a mechanism to implement

and enforce contracts• Shyam Sunder. 1997. Theory of

Accounting and Control. Cengage Publishing.

Figure 1

Resource Flows in Private-Good Organization

Employees

Shareholders

Creditors

Customers

VendorsGovernment

Managers

Firm as a Set of Contracts

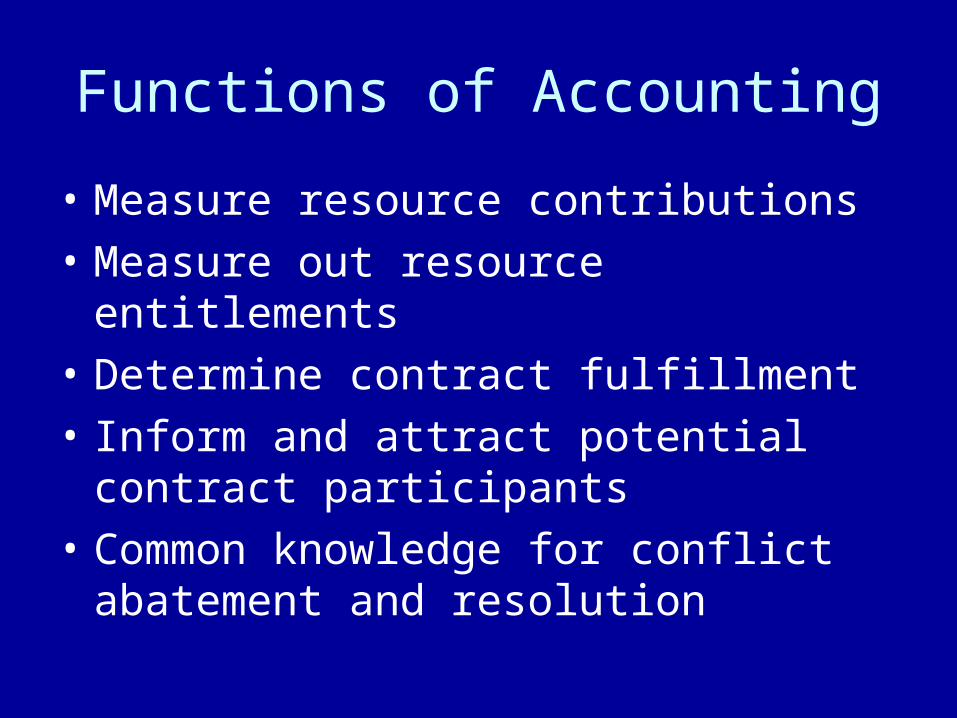

Functions of Accounting

• Measure resource contributions

• Measure out resource entitlements

• Determine contract fulfillment

• Inform and attract potential contract participants

• Common knowledge for conflict abatement and resolution

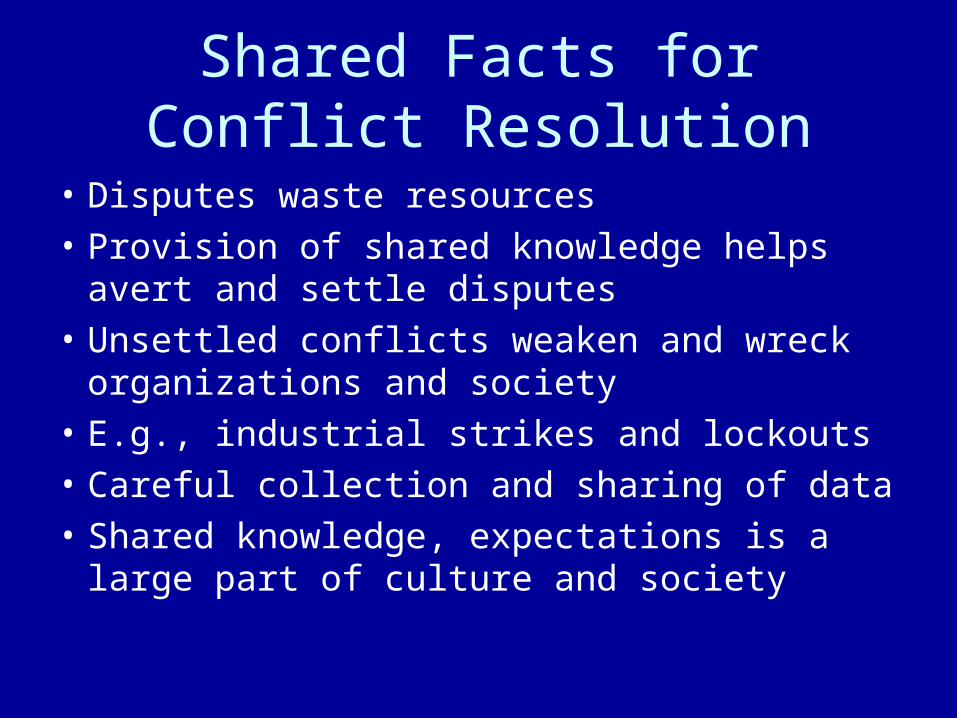

Shared Facts for Conflict Resolution

• Disputes waste resources• Provision of shared knowledge helps avert

and settle disputes• Unsettled conflicts weaken and wreck

organizations and society• E.g., industrial strikes and lockouts• Careful collection and sharing of data• Shared knowledge, expectations is a large

part of culture and society

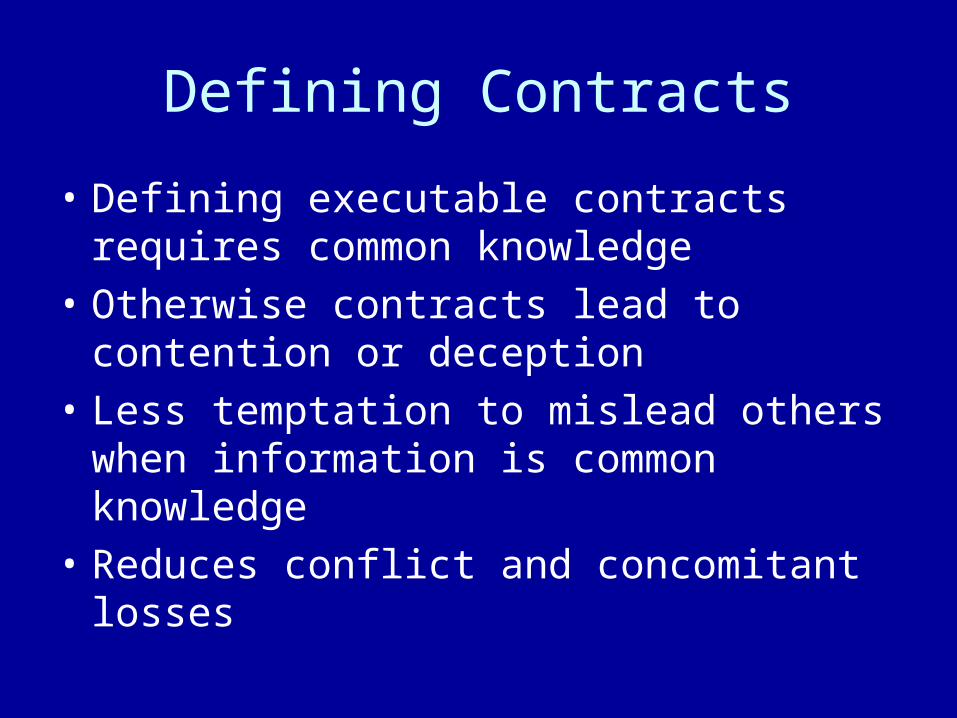

Defining Contracts

• Defining executable contracts requires common knowledge

• Otherwise contracts lead to contention or deception

• Less temptation to mislead others when information is common knowledge

• Reduces conflict and concomitant losses

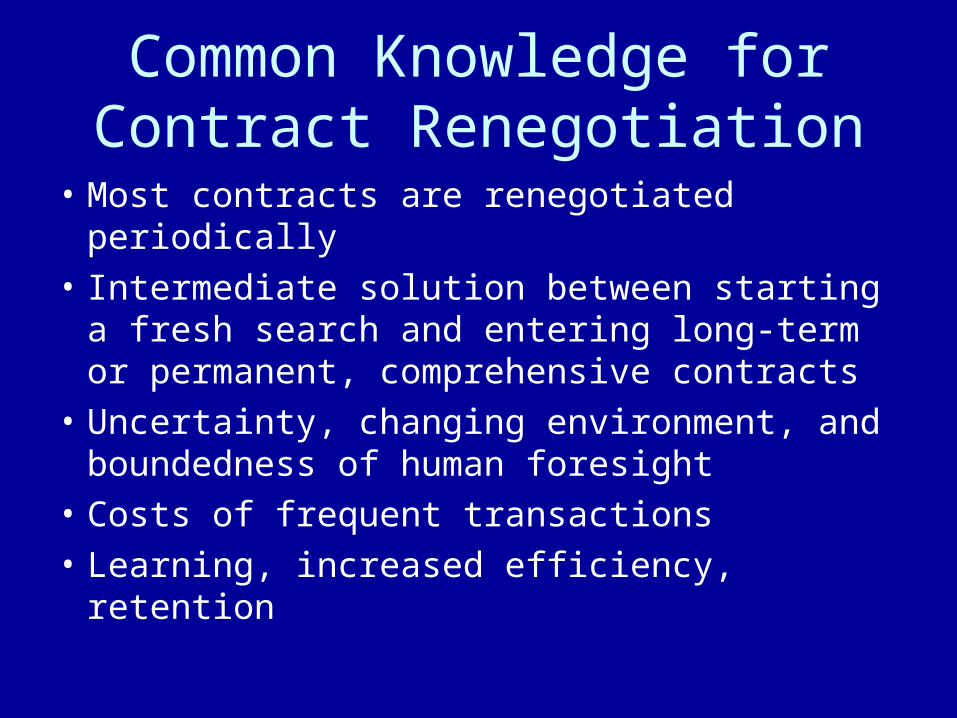

Common Knowledge for Contract Renegotiation

• Most contracts are renegotiated periodically• Intermediate solution between starting a

fresh search and entering long-term or permanent, comprehensive contracts

• Uncertainty, changing environment, and boundedness of human foresight

• Costs of frequent transactions• Learning, increased efficiency, retention

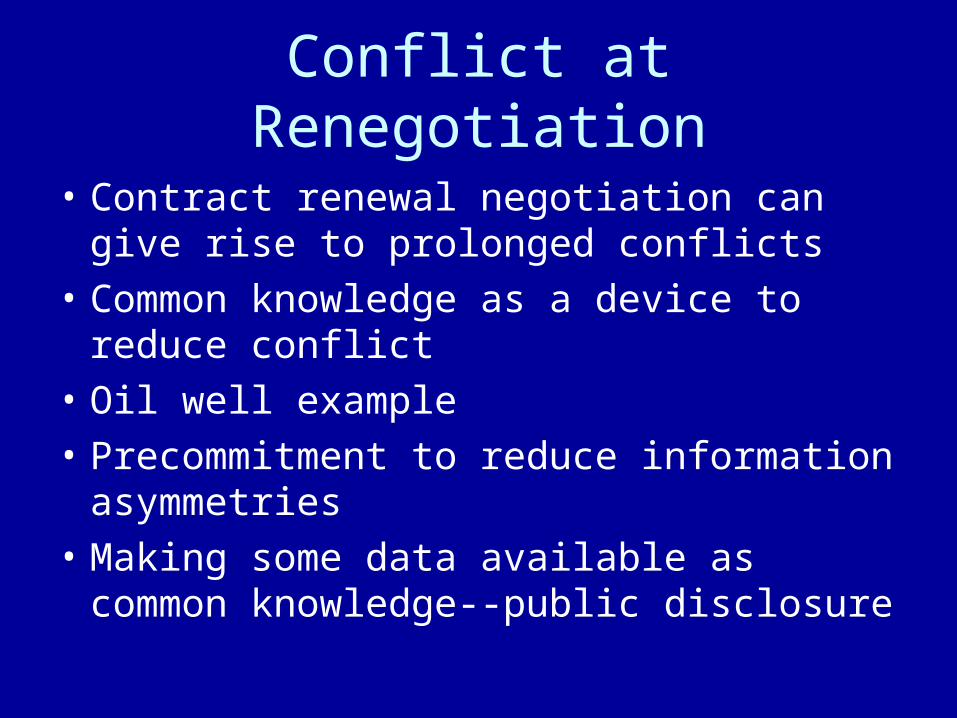

Conflict at Renegotiation

• Contract renewal negotiation can give rise to prolonged conflicts

• Common knowledge as a device to reduce conflict

• Oil well example• Precommitment to reduce information

asymmetries• Making some data available as common

knowledge--public disclosure

Accounting Standards

• Standards as rules of the game

• Must be common knowledge

• Effort expanded on making them CK

• How close do we get to CK

• Penetration into various segments

• Variation across standards

• Link between compliance and CK

• Optimal allocation of resources

Financial Analysis, Trading Volume and Bubbles

• Mostly fundamental analysis, assumes common knowledge

• Assumption relaxed by convenience

• Models of price bubbles based on relaxing the common knowledge assumption

• Trading volume models based on diverse beliefs

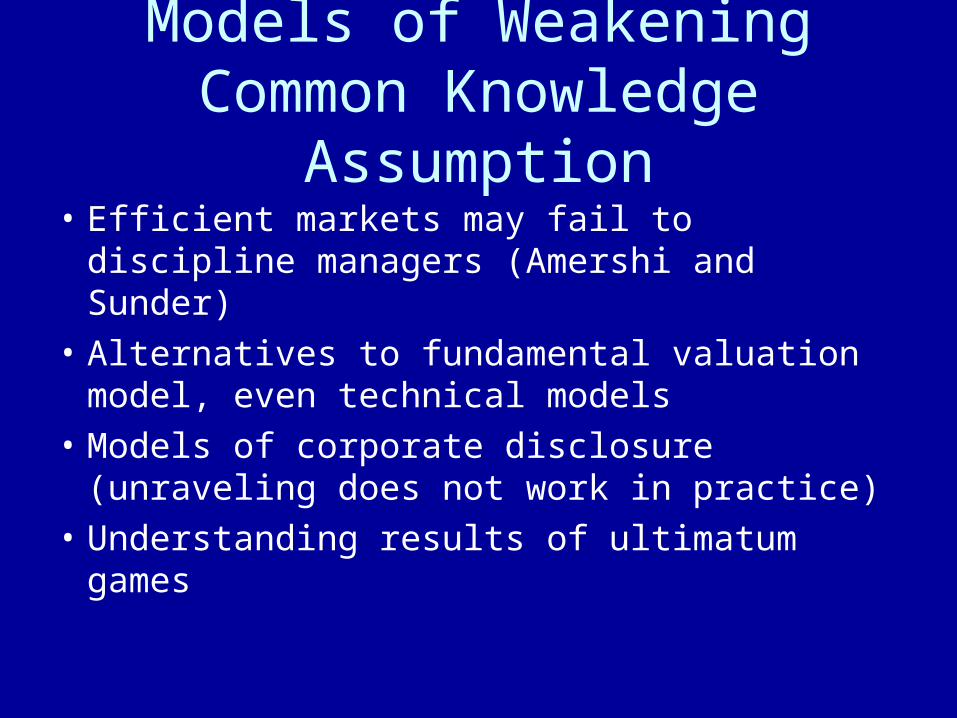

Models of Weakening Common Knowledge Assumption

• Efficient markets may fail to discipline managers (Amershi and Sunder)

• Alternatives to fundamental valuation model, even technical models

• Models of corporate disclosure (unraveling does not work in practice)

• Understanding results of ultimatum games

Figure 1: Frequency of acceptance in Slembeck (1999) data(No. of observations at the top of each bar)

0

0.2

0.4

0.6

0.8

1

0.05 0.15 0.25 0.35 0.45 0.55 0.65 0.75 0.85 0.95

Fraction of Demand by player 1

Frequencyofacceptanceby

player2

5 4 3

7 171

88

33

16 1835

To Summarize

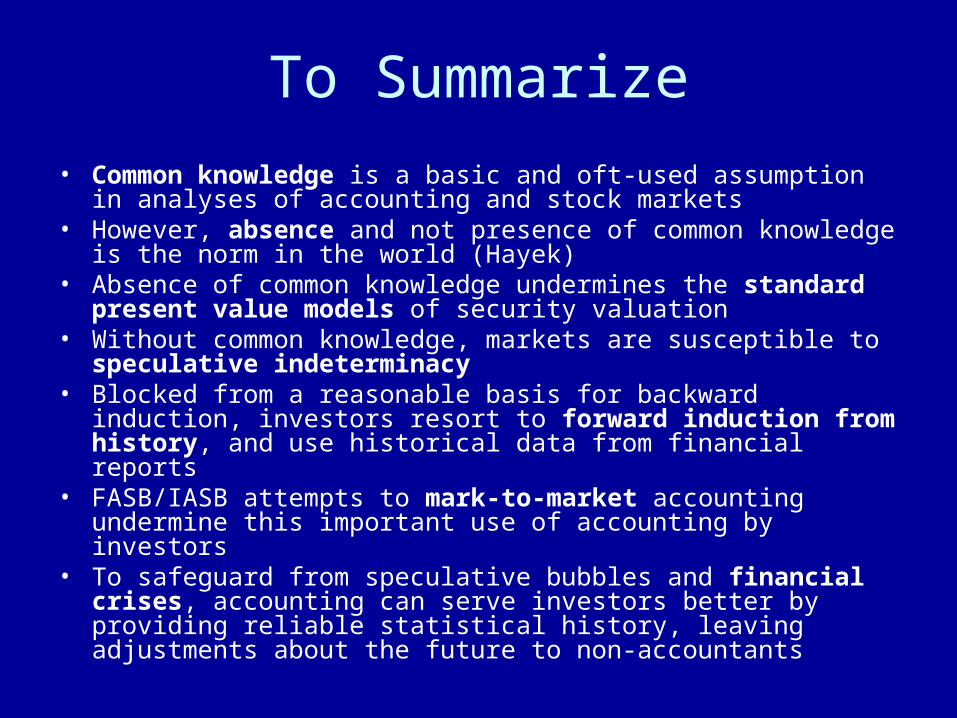

• Common knowledge is a basic and oft-used assumption in analyses of accounting and stock markets

• However, absence and not presence of common knowledge is the norm in the world (Hayek)

• Absence of common knowledge undermines the standard present value models of security valuation

• Without common knowledge, markets are susceptible to speculative indeterminacy

• Blocked from a reasonable basis for backward induction, investors resort to forward induction from history, and use historical data from financial reports

• FASB/IASB attempts to mark-to-market accounting undermine this important use of accounting by investors

• To safeguard from speculative bubbles and financial crises, accounting can serve investors better by providing reliable statistical history, leaving adjustments about the future to non-accountants

Thank You

• The paper, and slides will be available next week at

• http://www.som.yale.edu/faculty/sunder/research.html

• or email to [email protected]

Related Documents