1 Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans 2021 Edition [Updated to reflect Accounting and Financial Reporting Issues Related to the Consolidated Appropriations Act, 2021] ___________________ 4 CPEs Publication Date: February 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Accounting and Financial Reporting for

COVID-19, the CARES Act and PPP Loans

2021 Edition

[Updated to reflect Accounting and Financial Reporting Issues Related

to the Consolidated Appropriations Act, 2021] ___________________

4 CPEs

Publication Date: February 2021

2

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Accounting and Financial Reporting for

COVID-19, the CARES Act and PPP Loans

2021 Edition

[Updated to reflect Accounting and Financial Reporting Issues Related

to the Consolidated Appropriations Act, 2021] ___________________

4 CPEs

This publication is designed to provide accurate and authoritative information in regard to the subject

matter covered. It is sold with the understanding that the author and sponsor are not engaged in rendering

legal, accounting, or other professional services. If legal advice or other expert assistance is required, the

services of a competent professional person should be sought- From a Declaration of Principles jointly

adopted by a Committee of the American Bar Association and a Committee of Publishers and

Associations.

Copyright © 2021: Fustolo Publishing LLC All rights reserved, Reno, Nevada

3

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

4

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Accounting and Financial Reporting for

COVID-19, CARES Act and PPP Loans

2021 Edition

The objective of this course is to review the impact that COVID-19 has on accounting and financial

reporting, and the changes made by the 2020 CARES Act, including accounting for Paycheck Protection

Program (PPP) loans and forgiveness.

Topics include: Disclosures of risks and uncertainties; going-concern reporting and disclosure issues;

impairment issues related to goodwill and other long-lived assets; accounting for variable consideration

revenue and onerous contracts; dealing with inventory costs and stock market investment losses;

collectability of trade receivables; exit and termination benefit obligations; contingencies, and

accounting and auditing engagement matters. With respect to the CARES Act, the course discusses the

accounting for PPP loans and forgiveness, accounting for tax changes made by the CARES Act, and

more.

After reading the course material, you will be able to:

• Recognize some types of concentrations that might require disclosure under the risk and

uncertainty rules

• Identify the definition of near term

• Recall the frequency in which an entity should test goodwill for impairment

• Recognize some exit and disposal costs

• Recall how to classify business interruption insurance proceeds on the financial statements

• Identify the benchmark used to determine going concern

• Recognize how to report on going concern

• Identify a method that can be used to measure variable consideration revenue

• Recognize an example of a construction-type contract

• Identify an advantage of remote auditing

• Recall how to present debt issuance costs in the financial statements

• Recognize how to account for PPP loan forgiveness

• Identify how to treat the forgiveness of a PPP loan for tax purposes, and

• Identify an example of a circumstance in which an emphasis-of-matter paragraph might be

necessary.

5

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Field of study:

Accounting and Auditing

Level of knowledge:

Overview

Prerequisite: General understanding of accounting, financial

reporting, auditing and compilation and review

standards

Advanced Preparation: None

Recommended CPE hours: 4 (Accounting 2 CPEs; Auditing 2 CPEs)

6

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Accounting and Financial Reporting for

COVID-19, CARES Act and PPP Loans

2021 Edition

Table of Contents

I. Introduction ................................................................................................................................... 8

II. Accounting and Auditing Issues Related to COVID-19............................................................... 8

III. Disclosure of Risks and Uncertainties ......................................................................................... 9

REVIEW QUESTIONS – Section 1 .................................................................................................. 16

SUGGESTED SOLUTIONS ............................................................................................................. 17

IV. Asset Impairments- Long-Lived Assets ..................................................................................... 18

A. Overview of Asset Impairment Rules ........................................................................................ 18

B. Goodwill Impairment Issues ...................................................................................................... 19

V. Writedowns and Disclosures of Stock Market Investments ..................................................... 26

A. Disclosure of Stock Losses ........................................................................................................ 26

REVIEW QUESTIONS – Section 2 .................................................................................................. 28

SUGGESTED SOLUTIONS ............................................................................................................. 29

VI. Inventory Costs and Valuation Issues ........................................................................................ 30

A. GAAP Review of Inventories .................................................................................................... 30

VII. Trade Receivables and the Allowance for Doubtful Accounts ................................................. 33

VIII. Exit and Termination Costs ....................................................................................................... 33

IX. Contingencies and Exposure to Third-Party and Employee Claims ......................................... 35

X. Business Interruption Insurance Recovery and Presentation ..................................................... 36

XI. Going Concern and COVID-19 ................................................................................................. 40

A. GAAP Requirements- Going Concern ...................................................................................... 41

B. Auditing and Review Engagement Requirements- Going Concern .......................................... 41

REVIEW QUESTIONS – Section 3 .................................................................................................. 48

SUGGESTED SOLUTIONS ............................................................................................................. 50

XII. Funded Status Deterioration- Multi-Employer Plan Obligations .............................................. 52

XIII. Revenue and Contracts ............................................................................................................. 53

A. Variable Consideration Revenue ............................................................................................... 53

B. Losses on Onerous Contracts..................................................................................................... 56

XIV. Loan Modifications and Covenants ......................................................................................... 60

XV. Impact of Lower Interest Rates on Lease Obligations ............................................................... 61

XVI. Auditing and Review Engagement Issues- COVID- 19 ........................................................... 63

7

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

A. Accounts Receivable Confirmations ......................................................................................... 64

B. Physical Inventory Observations ............................................................................................... 65

C. Emphasis-of-Matter Paragraph- COVID-19 .............................................................................. 68

D. Remote Auditing ........................................................................................................................ 69

REVIEW QUESTIONS – Section 4 .................................................................................................. 71

SUGGESTED SOLUTIONS ............................................................................................................. 73

XVII. Income Tax Issues- CARES Act ............................................................................................ 75

A. Tax Rate for Deferred Income Taxes under the CARES Act .................................................... 75

B. Deferred Tax Assets from NOLs- the CARES Act ................................................................... 75

C. New 50% Limitation on Interest Deduction- the CARES Act .................................................. 81

REVIEW QUESTIONS – Section 5 .................................................................................................. 84

SUGGESTED SOLUTIONS ............................................................................................................. 85

XVIII. Accounting for PPP Loans under the CARES Act ............................................................... 86

A. Introduction ................................................................................................................................ 86

B. Basic Rules for PPP Loans- SBA .............................................................................................. 86

C. How Should PPP Loans be Accounted for Under GAAP? ....................................................... 88

D. Accounting for a PPP Loan as Debt .......................................................................................... 88

E. Forgiveness of PPP Loan ........................................................................................................... 94

F. Tax Effects of PPP Loans ........................................................................................................ 102

G. Disclosures Required- PPP Loan Treated as Debt .................................................................. 104

H. Accounting for an Economic Injury Disaster Loan (EIDL) .................................................... 112

I. Other GAAP Approaches for PPP Loans ................................................................................ 114

J. Accountant and Auditor Reporting Issues- PPP Loans ........................................................... 114

REVIEW QUESTIONS – Section 6 ................................................................................................ 118

SUGGESTED SOLUTIONS ........................................................................................................... 120

Index ................................................................................................................................................. 122

Glossary ............................................................................................................................................ 123

8

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

I. Introduction

Status of the U.S. economy in 2021: COVID-19 the Legislative Relief

The COVID-19 pandemic has certainly had a dramatic effect on the U.S. economy across most sectors

and industries. Some businesses that were once financially strong prior to the economy crisis, are quickly

finding themselves in a financial tailspin, with cash flow challenges and risk of their ability to continue

as a going concern. Although forgivable loans received under the Paycheck Protection Program (PPP)

issued through the Small Business Administration (SBA) certainly have helped companies with cash

flow requirements, they cannot sustain companies indefinitely.

The CARES Act

On March 27, 2020, then President Trump signed the $2 trillion Coronavirus Aid, Relief and Economic

Security Act (the CARES Act). The Act has been supplemented by subsequent amendments. The purpose

of the CARES Act is to mitigate the effects of the COVID-19 pandemic on the U.S. economy.

The CARES Act has as its nucleus the $669 billion Paycheck Protection Program (PPP), which provides

forgivable loans to U.S. businesses. It also modifies several tax provisions previously made by the Tax

Cuts and Jobs Act (TCJA), including liberalizing the net operating loss (NOL) carryback and interest

deductibility provisions.

The Consolidated Appropriations Act, 2021

On December 27, 2020, then President Trump signed the $2.3 trillion Consolidated Appropriations

Act, 2021 (the Act), which combines approximately $900 billion in COVID-19 stimulus relief with $1.4

trillion of an omnibus spending bill for fiscal year 2021.

Embedded in the Act is the Economic Aid to Hard-Hit Small Businesses, Nonprofits, and Venues Act,1

which provides $284 billion of further funding under the CARES Act’s PPP loan program. The Act also

amends sections of the CARES Act to address the tax treatment of PPP loans and eligible expenses, and

clarify other aspects of PPP loans not otherwise covered in the CARES Act.

II. Accounting and Auditing Issues Related to COVID-19

Regardless of the timing of U.S. economy’s recovery, accountants and auditors must consider the impact

of COVID-19 on the financial health of their clients’ and how it is reflected in financial statements and

disclosures in 2020, 2021 and 2022. With a new round of PPP loans being issued in 2021 in accordance

with the Consolidated Appropriations Act, 2021, many companies will be seeking forgiveness of those

loans well into 2022. Therefore, the accounting and financial reporting effects of COVID-19 (including

PPP loans) may impact financial statements through 2022.

In this section, the author identifies some (but not all) of the accounting and financial reporting issues

that should be considered by businesses to capture the accounting and financial reporting effects of the

COVID-19 pandemic.

1 The Economic Aid to Hard-Hit Small Businesses, Nonprofits, and Venues Act, is found in Division N, Title III (Sections

301-348) of the Consolidated Appropriations Act, 2021.

9

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

The author has segregated this course into the following subsections:

Accounting Issues Related to COVID-19:

a. Disclosure of risks and uncertainties

b. Asset impairments- long-lived assets (including goodwill)

c. Writedowns and disclosures of stock market investments

d. Inventory costs and valuation issues

e. Trade receivables and the allowance for doubtful accounts

f. Exit and termination costs

g. Contingencies and exposure to third-party and employee claims

h. Business interruption insurance recovery and presentation

i. Going concern and COVID-19

j. Funded status deterioration- multi-employer plan obligations

k. Revenue and contracts

l. Loan modifications and covenants

m. Impact of lower interest rates on lease obligations

Auditing and Review Engagement Issues- COVID-19:

a. Accounts receivable confirmations

b. Physical inventory observations

c. Emphasis-of-matter paragraph- COVID-19

d. Remote auditing

Accounting Issues Related to the CARES Act:

a. Income tax issues under the CARES Act

b. Accounting for PPP loans and forgiveness under the CARES Act

III. Disclosure of Risks and Uncertainties

The impact of the coronavirus has uncovered the fact that many U.S. companies have a “current

vulnerability due to certain concentrations” that may not have been disclosed previously.

Examples of concentrations related to COVID-19 include companies that have:

1. A large percentage of materials, supplies and products customarily purchased from countries that

have closed or slowed down during COVID-19.

Example: A large percentage of supplies and goods are purchased from China and other countries.

2. A significant amount of revenue is concentrated within certain countries that have significant

exposure to COVID-19.

Example: A large percentage of sales are made to Europe that has restricted businesses and trade

during the COVID-19 pandemic.

10

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

3. Industry-specific risks related to COVID-19 shutdowns and business operating restrictions.

Example: A large percentage of operations are within the restaurant and hospitality business.

4. Geographic risk by being located in cities and states that have implemented severe restrictions on

conducting business during the COVID-19 pandemic.

5. Example: A large percentage of operations is located in New York City or Los Angeles which have

extremely restrictive rules on business operations during the COVID-19 pandemic.

In such circumstances, an entity may have a current vulnerability due to a concentration.

These concentrations create risk to companies, which may require a concentration of risk disclosure in

accordance with ASC 275, Risks and Uncertainties.

ASC 275 requires an entity to disclose concentrations if, based on information known to management

before the financial statements are issued or are available to be issued (for nonpublic entities), all of the

following criteria are met:

1. The concentration exists at the date of the financial statements.

2. The concentration makes the entity vulnerable to the risk of a near-term severe impact, and

3. It is at least reasonably possible that the events that could cause the severe impact, will occur in the

near term.

ASC 275 defines near term, severe impact, and reasonably possible, as follows:

Near term: a period of time not to exceed one year from the date of the financial statements.

Severe impact: a significant financially disruptive effect on the normal functioning of an entity.

Severe impact is a higher threshold than material. Matters that are important enough to

influence a user's decisions are deemed to be material, yet they may not be so significant as to

disrupt the normal functioning of the entity.

Reasonably possible: the change of a future event or events occurring is more than remote but

less than likely (probable).

Therefore, a concentration of a risk might require disclosure if it is reasonably possible that the

concentration (such as a supply-chain concentration or a concentration in an industry) could result in a

severe impact on the company within one year from the balance sheet date. Any risk outside one year

does not require disclosure although companies may choose to include such disclosures.

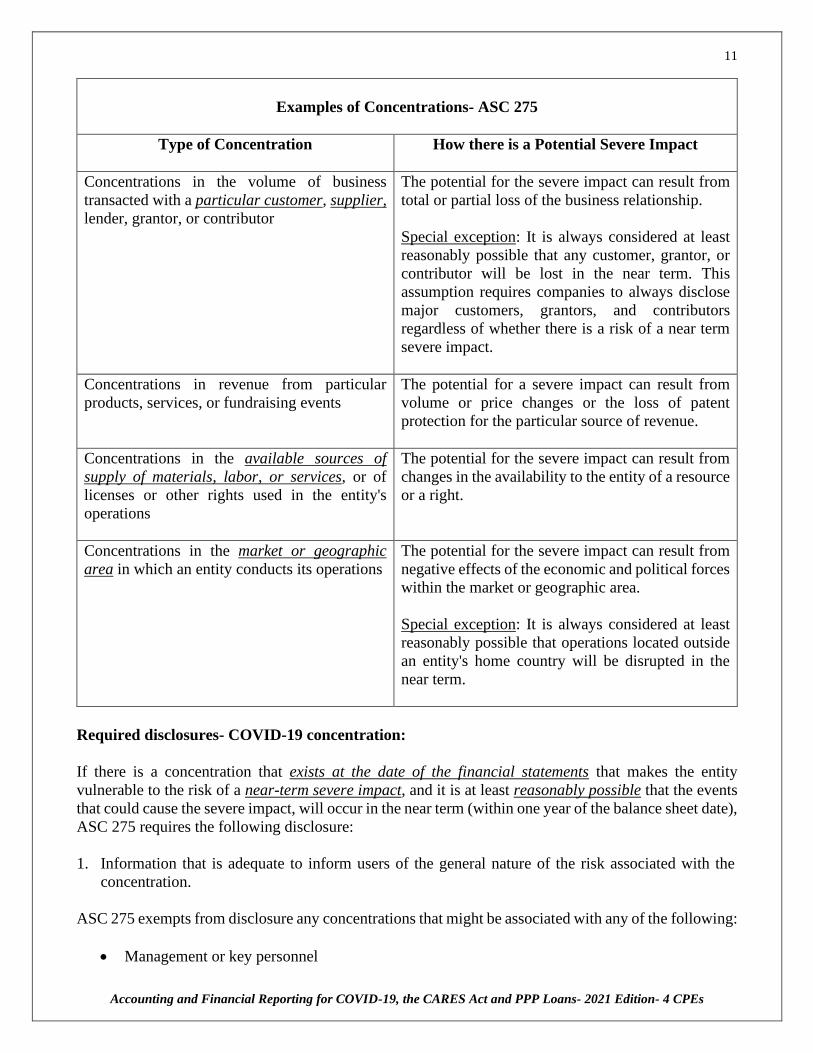

ASC 275 offers examples of categories of concentrations that have the potential for a severe impact on

a business, as identified in the following table:

11

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Examples of Concentrations- ASC 275

Type of Concentration How there is a Potential Severe Impact

Concentrations in the volume of business

transacted with a particular customer, supplier,

lender, grantor, or contributor

The potential for the severe impact can result from

total or partial loss of the business relationship.

Special exception: It is always considered at least

reasonably possible that any customer, grantor, or

contributor will be lost in the near term. This

assumption requires companies to always disclose

major customers, grantors, and contributors

regardless of whether there is a risk of a near term

severe impact.

Concentrations in revenue from particular

products, services, or fundraising events

The potential for a severe impact can result from

volume or price changes or the loss of patent

protection for the particular source of revenue.

Concentrations in the available sources of

supply of materials, labor, or services, or of

licenses or other rights used in the entity's

operations

The potential for the severe impact can result from

changes in the availability to the entity of a resource

or a right.

Concentrations in the market or geographic

area in which an entity conducts its operations

The potential for the severe impact can result from

negative effects of the economic and political forces

within the market or geographic area.

Special exception: It is always considered at least

reasonably possible that operations located outside

an entity's home country will be disrupted in the

near term.

Required disclosures- COVID-19 concentration:

If there is a concentration that exists at the date of the financial statements that makes the entity

vulnerable to the risk of a near-term severe impact, and it is at least reasonably possible that the events

that could cause the severe impact, will occur in the near term (within one year of the balance sheet date),

ASC 275 requires the following disclosure:

1. Information that is adequate to inform users of the general nature of the risk associated with the

concentration.

ASC 275 exempts from disclosure any concentrations that might be associated with any of the following:

• Management or key personnel

12

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

• Proposed changes in government regulations

• Proposed changes in accounting principles

• Deficiencies in the internal control structure, and

• The possible effects of acts of God, war, or sudden catastrophes.

Isn’t a disclosure of the risks associated with COVID-19 exempt under the act of God provision in

ASC 275?

No. ASC 275 provides that concentrations related to the possible effects of acts of God, war or sudden

catastrophes are not subject to the ASC 275 disclosure.

The overall impact of COVID-19 on the economy is not an act of God and not exempt from the

disclosure. In fact, the economic effects from COVID-19 (such as supply-chain shortages, customer and

geographic concentrations), are man-made and are based on decisions made for economic reasons.

COVID-19 has done nothing more than exposed the concentrations of risk that already existed within

U.S. businesses.

Accountant and auditors should be aware of concentrations of risk that have existed in businesses, and

that have been exacerbated by the COVID-19 pandemic, such as:

1. Concentration of customers

2. Concentration of supply of materials and products from foreign countries, and

3. Concentration of business operations in a particular geographic area or industry, such as restaurants

and hotels, or foreign operations.

Note: Although most companies do, in fact, include a disclosure of concentration in individual

customers (major customers), many fail to disclose concentrations in business operations and supply

chain sources in certain geographic areas, such as foreign countries. In particular, few nonpublic entities

disclose the risks associated with concentrations of supply, such as purchasing a large percentage of

materials and products from a particular country, such as China, or other parts of Asia. For many

companies, expansion of operations into foreign countries is deemed evidence of a growth-oriented

business model. Yet, it also indicates there is greater risk of having a concentration in a particular

geographic area that is outside the United States. That risk only comes to fruition when there is an

incident such as the COVID-19 pandemic. Investors and lenders must be aware of these risks through

disclosure of risks and uncertainties as required by ASC 275.

What about the concentration of risk associated with being located in a certain geographic area or

industry?

If nothing else, the COVID-19 pandemic has placed greater emphasis on two concentrations that may

exist within any particular business: One is the geographic location (state and city or town) in which the

business operates. The other concentration is the industry in which it operates, such as being in the

restaurant or hospitality business.

Consider two businesses:

13

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

• A restaurant located in New York City, and

• A liquor store located in Boca Raton, Florida.

All businesses have a concentration both geographically and within a particular industry.

A restaurant located in New York City has an industry concentration (restaurant industry) and a

geographic concentration (being located in New York City) where it is reasonably possible that both

concentrations will have a severe impact on its operations within the next year. The fact is, in 2020 and

2021, the state, city or town in which an entity operates can have a dramatic effect on whether that

business can operate and whether it will survive in the aftermath of COVID-19. A previously successful

restaurant in New York City has tremendous obstacles to survival over the next year due to being located

within New York City (geographic concentration), where there are severe restrictions on restaurant

operations (industry concentration) by local government.

Compare the New York City restaurant scenario with a liquor store located in Boca Raton, Florida,

where the business has been labeled an “essential business” that has remained open during the pandemic.

Moreover, the liquor store is located within Boca Raton, Florida, where local government has been

flexible in allowing businesses to operate during the pandemic. Both the restaurant and liquor store

businesses have concentrations (within a particular industry and geographical area), but only one (the

restaurant in New York City) is likely to have a risk of a severe impact on its operations within the next

year for which a disclosure might be required.

Example 1: U.S. Supplier with a Concentration of Supply Purchased from China- Concentration

of Risk Disclosure

Company X has a concentration of its product supply it purchases from China. In March 2020, X shuts

down its business based on a state mandate due to COVID-19 pandemic. Since then, the federal

government has restricted the import of certain goods from China.

Following is a sample disclosure in X’s December 31, 2020 financial statements:

NOTE X: Certain Concentrations

Historically, the Company purchases approximately 60% of its products from distributors located

in China and other parts of Asia. In early 2020, suppliers located in China shut down operations as

a result of the coronavirus (COVID-19) outbreak.

On January 31, 2020, the U.S. Health and Human Services Secretary declared the COVID-19

pandemic a public health emergency in the United States. Since that time, the Federal government

has placed restrictions on the import of supplies from China, some of which continue to remain in

effect.

As a result, the Company continues to have delays in receiving goods from China while it secures

alternative sources of goods from other countries. The concentration of supply of goods from China

means it is reasonably possible that these concentration could result in a severe impact on the

Company’s business in the near term.

14

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

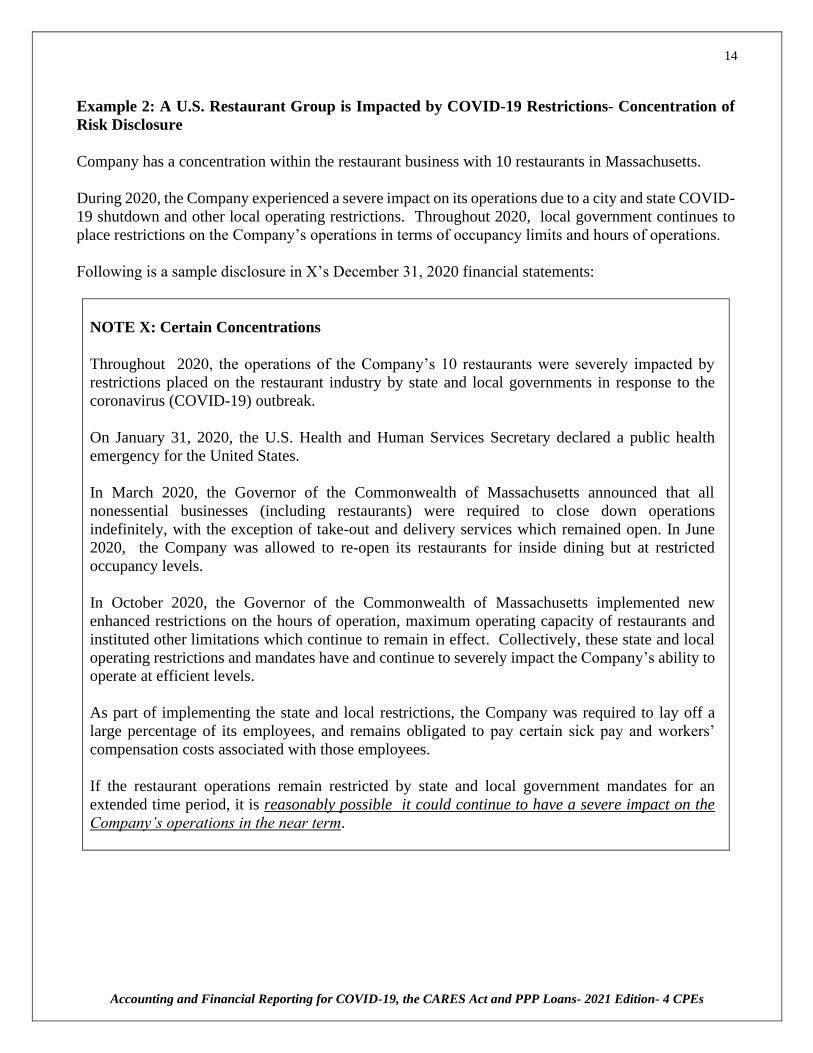

Example 2: A U.S. Restaurant Group is Impacted by COVID-19 Restrictions- Concentration of

Risk Disclosure

Company has a concentration within the restaurant business with 10 restaurants in Massachusetts.

During 2020, the Company experienced a severe impact on its operations due to a city and state COVID-

19 shutdown and other local operating restrictions. Throughout 2020, local government continues to

place restrictions on the Company’s operations in terms of occupancy limits and hours of operations.

Following is a sample disclosure in X’s December 31, 2020 financial statements:

NOTE X: Certain Concentrations

Throughout 2020, the operations of the Company’s 10 restaurants were severely impacted by

restrictions placed on the restaurant industry by state and local governments in response to the

coronavirus (COVID-19) outbreak.

On January 31, 2020, the U.S. Health and Human Services Secretary declared a public health

emergency for the United States.

In March 2020, the Governor of the Commonwealth of Massachusetts announced that all

nonessential businesses (including restaurants) were required to close down operations

indefinitely, with the exception of take-out and delivery services which remained open. In June

2020, the Company was allowed to re-open its restaurants for inside dining but at restricted

occupancy levels.

In October 2020, the Governor of the Commonwealth of Massachusetts implemented new

enhanced restrictions on the hours of operation, maximum operating capacity of restaurants and

instituted other limitations which continue to remain in effect. Collectively, these state and local

operating restrictions and mandates have and continue to severely impact the Company’s ability to

operate at efficient levels.

As part of implementing the state and local restrictions, the Company was required to lay off a

large percentage of its employees, and remains obligated to pay certain sick pay and workers’

compensation costs associated with those employees.

If the restaurant operations remain restricted by state and local government mandates for an

extended time period, it is reasonably possible it could continue to have a severe impact on the

Company’s operations in the near term.

15

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Example 2A: A U.S. Restaurant Group is Impacted by COVID-19 Restrictions- Concentration of

Risk Disclosure (Abbreviated Disclosure)

Same facts as Example 2 except the Company believes the Example 2 disclosure is too voluminous and

presents an abbreviated disclosure of risks and uncertainties as follows:

NOTE X: Certain Concentrations

Throughout 2020, the operations of the Company’s 10 restaurants were severely impacted by

restrictions placed on the restaurant industry by state and local government in response to the

coronavirus (COVID-19) outbreak. [Some of the restrictions remain in effect].

If the Company’s restaurant operations remain restricted by state and local government

mandates for an extended time period, it is reasonably possible it could continue to have a

severe impact on the Company’s operations in the near term.

16

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

REVIEW QUESTIONS – Section 1

Under the NASBA-AICPA self-study standards, self-study sponsors are required to present review

questions intermittently throughout each self-study course. Additionally, feedback must be given to the

course participant in the form of answers to the review questions and the reason why answers are correct

or incorrect. To obtain the maximum benefit from this course, we recommend that you complete each

of the following questions, and then compare your answers with the solutions that immediately follow.

1. Which of the following is a type of disclosure related to concentrations required to be made by a

company in certain instances under GAAP:

a. Revenue recognition

b. Going concern

c. Operating performance

d. Risks and uncertainties

2. Company X is having a bad year. It has risks associated with events, some of which are not X’s

responsibility. In accordance with ASC 275, which of the following is a type of concentration

that might require disclosure under the ASC 275 rules:

a. Concentration of business in the restaurant industry that was shut down due to a state mandate

from the COVID-19 pandemic

b. X’s largest plant is located in California along an earthquake fault line

c. X’s second largest plant is inside a flood area where the water level is rising from year to

year

d. X’s third largest plant is located in a part of the world where there are continuous local wars

17

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

SUGGESTED SOLUTIONS

1. Which of the following is a type of disclosure related to concentrations required to be made by a

company in certain instances under GAAP:

a. Incorrect. Although there are disclosures required for revenue recognition, they relate to

accounting policies and not concentrations making the answer incorrect.

b. Incorrect. In general, a going-concern disclosure might convey a risk related to an entity, but

it does not represent a concentration within a business.

c. Incorrect. Operating performance might be a management issue, but it is generally not

specific to a concentration within an entity.

d. Correct. ASC 275 requires disclosures related to certain concentrations that make an

entity vulnerable to the risk of a near-term severe impact.

2. Company X is having a bad year. It has risks associated with events, some of which are not X’s

responsibility. In accordance with ASC 275, which of the following is a type of concentration

that might require disclosure under the ASC 275 rules:

a. Correct. The concentration of business in the restaurant industry, which was shut down

due to a state mandate during the COVID-19 pandemic, is an example of a

concentration that could be the subject of a disclosure under the risk and uncertainty

rules. The concentrations within the industry and geographic area make X vulnerable

to the risk of a near-term severe impact.

b. Incorrect. Concentrations related to acts of God are exempt from the risks and uncertainties

disclosure rules. Being located on an earthquake fault line would be an example of a risk

associated with an act of God.

c. Incorrect. The concentration is related to an act of God (flooding) and excluded from the

risks and uncertainties disclosure rules.

d. Incorrect. Concentrations related to wars are exempt from the risks and uncertainties

disclosure rules.

18

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

IV. Asset Impairments- Long-Lived Assets

A. Overview of Asset Impairment Rules

GAAP provides all long-term assets with some form of required asset impairment test. Some are

performed automatically on an annual basis (such as goodwill), while others are performed only if there

is a triggering event.

When there is a decline in the economy, such as is the case during the COVID-19 pandemic, long-term

assets should be reviewed for impairment using the GAAP rules.

The following chart offers a summary of the existing GAAP rules for impairment of both intangible and

tangible assets.

Accounting for Impairments of Assets

Type of asset Authority for

impairment

Accounting

treatment

Type of impairment

test

INTANGIBLE ASSETS

Goodwill

General rule

ASC 350

Not amortized Tested annually for

impairment

[One-step approach]2

Private company

alternative-

ASU 2014-02

Amortized over

maximum of 10

years straight line

No annual test for

impairment unless there is a

triggering event

Intangibles with indefinite lives

(tradename, etc.)

ASC 350 Not amortized

until life is no

longer indefinite

Tested annually for

impairment

Intangibles with finite lives

(patent, agreement not to

compete, etc.)

ASC 360 Amortized Tested for impairment only

if there is an indication that

an impairment might exist

TANGIBLE ASSETS

Long-lived tangible assets

(equipment and real estate)

ASC 360 Depreciated Tested for impairment only

if there is an indication that

an impairment might exist

2 ASU 2017-04 changes goodwill from a two-step to a one-step test as follows: for public business entities for annual or

interim goodwill impairment tests in fiscal years beginning after December 15, 2019. For all other entities (including non-

public and not-for-profit entities), the amendments in ASU 2017-04 are effective for annual or interim goodwill impairment

tests in fiscal years beginning after December 15, 2020. Early implementation is permitted.

19

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Impact of COVID-19 pandemic on fair value and cash flows for all asset impairment tests

Each of the asset impairment tests identified in the previous table uses fair value or cash flows, both of

which are directly impacted by changes in economic circumstances from the COVID-19 pandemic.

An economic downturn affects business cash flows which, in turn, affects fair value for purposes of

determining whether an entity has an impairment of goodwill and other long-lived assets.

If fair value declines, an entity may be required to record an impairment loss for goodwill, and indefinite

lived assets such as patents, and plant and equipment.

Each of the GAAP impairment rules provides that a triggering event or qualitative factor may be the

precursor to performing a quantitative test for impairment. The list of triggering events includes negative

cash flow issues, operating losses, and external economic factors such as those created by the COVID-

19 pandemic. Consequently, a company that has historically operated profitably and has had no long-

lived asset impairments, now might find itself in the precarious situation of having a potential

impairment among its various long-lived assets.

All GAAP long-lived asset impairment models provide that once a long-lived asset is written down, it

may not be written back up in subsequent periods. Therefore, a short-term decline in fair value due to

the COVID-19 pandemic can result in a one-time impairment writedown of long-lived assets which

cannot reverse in future years when the fair value recovers.

B. Goodwill Impairment Issues

Both public and nonpublic entities with goodwill could be impacted by the decline in fair value from the

COVID-19 pandemic.

1. Public companies follow the general rule found in ASC 350, Intangibles- Goodwill and Other, which

states that:

a. Goodwill is not amortized, and

b. Goodwill must be tested annually for impairment.

2. Private (nonpublic) entities have two options to account for goodwill:

Option 1: Follow the general rule (goodwill is not amortized and must be tested annually for

impairment), or

Option 2: Elect an accounting alternative to amortize goodwill over 10 years with no annual test of

goodwill required unless there is a triggering event.

Regardless of whether a nonpublic entity does not amortize goodwill (Option 1) or elects to amortize it

under the 10-year private company accounting alternative (Option 2), a sudden decline in fair value of

the entity (due to the COVID-19 pandemic) might result in an impairment of goodwill.

Consider the following facts:

20

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

1. The impact of the economic downturn due to COVID-19 must be considered in measuring goodwill

for possible impairment, and may result in an otherwise healthy company having a writedown of

goodwill in 2020 and 2021, until it recovers financially in 2022 or beyond.

2. Moreover, if goodwill is written down, it may not be written back up in future years once the

economic and business recovers.

Both public and private (nonpublic) entities with material goodwill must consider that COVID-19

economic issues directly affect two elements of the goodwill impairment test:

1. Triggering events (qualitative factors): might exist such as a decline in economic environment,

industry, an entity’s cash flow and overall business, and

2. Fair value: might be adjusted downward in the first step of the impairment test, reflective of

discounting lower cash flows anticipated in the future.

Existing GAAP for goodwill

The existing accounting rules for goodwill are found in ASC 350: Intangibles: Goodwill and Other,

which offers two options to account for goodwill:

1. Apply the general model- available for all companies:

a. Goodwill is not amortized

b. An annual impairment test is performed using a one-step approach

c. Qualitative factors (triggering events) may be considered as a precursor to performing the one-

step impairment test, and

d. An impairment test at interim is required if there is a triggering event.

2. Private-company alternative: Election available to private (nonpublic) companies only:

a. Goodwill is amortized over a maximum of 10 years on a straight-line basis, and

b. An annual impairment test is not performed unless there is a triggering event.

Note: The private company alternative is not available to SEC companies. Instead, SEC companies

must follow the general rule of not amortizing goodwill and testing goodwill for impairment

annually.

Regardless of whether an entity is publicly held, or nonpublic/private and using the 10-year

amortization accounting alternative, a significant decline in the fair value of the entity from COVID-

19 could result in a goodwill impairment.

21

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

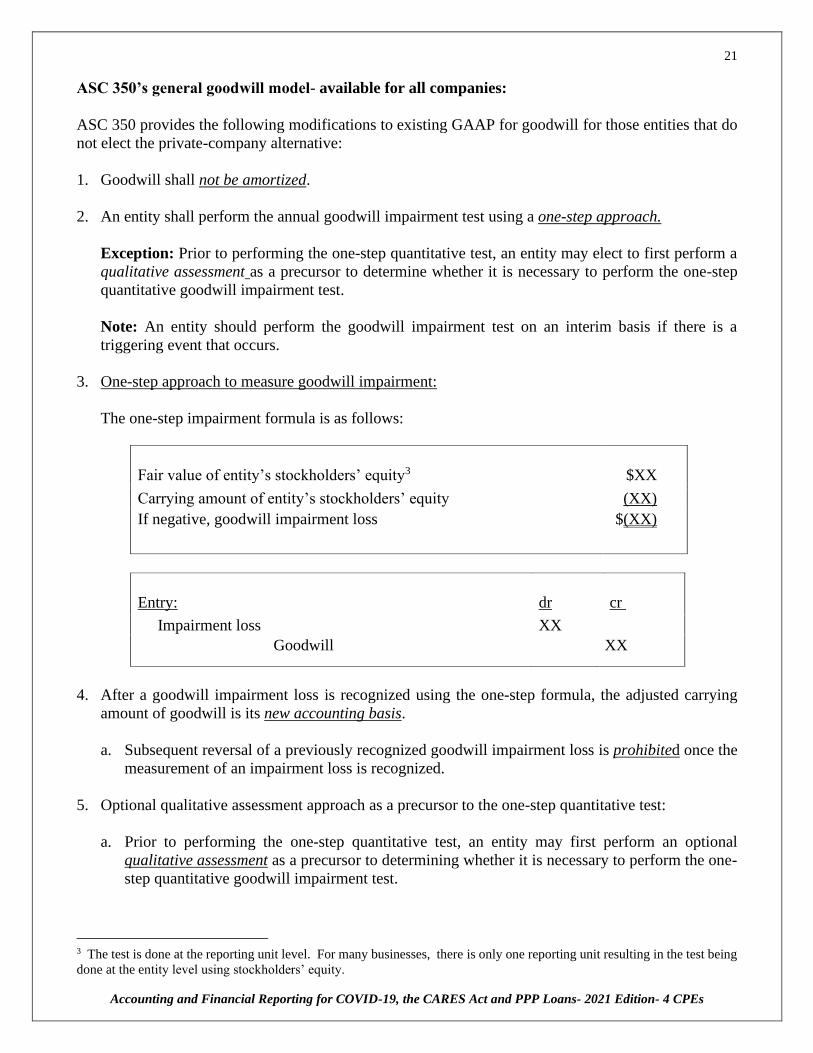

ASC 350’s general goodwill model- available for all companies:

ASC 350 provides the following modifications to existing GAAP for goodwill for those entities that do

not elect the private-company alternative:

1. Goodwill shall not be amortized.

2. An entity shall perform the annual goodwill impairment test using a one-step approach.

Exception: Prior to performing the one-step quantitative test, an entity may elect to first perform a

qualitative assessment as a precursor to determine whether it is necessary to perform the one-step

quantitative goodwill impairment test.

Note: An entity should perform the goodwill impairment test on an interim basis if there is a

triggering event that occurs.

3. One-step approach to measure goodwill impairment:

The one-step impairment formula is as follows:

Fair value of entity’s stockholders’ equity3

$XX

Carrying amount of entity’s stockholders’ equity (XX)

If negative, goodwill impairment loss $(XX)

Entry:

dr

cr

Impairment loss XX

Goodwill XX

4. After a goodwill impairment loss is recognized using the one-step formula, the adjusted carrying

amount of goodwill is its new accounting basis.

a. Subsequent reversal of a previously recognized goodwill impairment loss is prohibited once the

measurement of an impairment loss is recognized.

5. Optional qualitative assessment approach as a precursor to the one-step quantitative test:

a. Prior to performing the one-step quantitative test, an entity may first perform an optional

qualitative assessment as a precursor to determining whether it is necessary to perform the one-

step quantitative goodwill impairment test.

3 The test is done at the reporting unit level. For many businesses, there is only one reporting unit resulting in the test being

done at the entity level using stockholders’ equity.

22

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

b. Under the optional qualitative assessment, an entity assesses certain qualitative factors to

determine whether it is more likely than not (that is, a likelihood of more than 50%) that the fair

value of a reporting unit (stockholders’ equity) is less than its carrying amount, including

goodwill.

1) If based on the qualitative assessment, it is more likely than not (more than 50%) that the fair

value is less than the carrying amount, the entity must perform the one-step impairment test.

2) If based on the qualitative assessment, it is not more likely than not (not more than 50%) that

the fair value is less than the carrying amount, the entity is not required to perform the one-

step impairment test.

c. Examples of qualitative factors to consider whether the more-likely-than-not threshold is met

include:

1) Macroeconomic conditions: such as a deterioration in general economic conditions,

limitations on accessing capital, fluctuations in foreign exchange rates, or other developments

in equity and credit markets

2) Industry and market considerations: such as a deterioration in the environment in which an

entity operates, an increased competitive environment, a decline in market-dependent

multiples or metrics (consider in both absolute terms and relative to peers), a change in the

market for an entity’s products or services, or a regulatory or political development

3) Cost factors: such as increases in raw materials, labor, or other costs that have a negative

effect on earnings and cash flows

4) Overall financial performance: such as negative or declining cash flows or a decline in actual

or planned revenue or earnings compared with actual and projected results of relevant prior

periods

5) Other relevant entity-specific events: such as changes in management, key personnel,

strategy, or customers; contemplation of bankruptcy; or litigation

6) Events affecting a reporting unit: such as a change in the composition or carrying amount of

its net assets, a more-likely-than-not expectation of selling or disposing of all, or a portion,

of a reporting unit, the testing for recoverability of a significant asset group within a reporting

unit, or recognition of a goodwill impairment loss in the financial statements of a subsidiary

that is a component of a reporting unit, and

7) A sustained decrease in share price: (consider in both absolute terms and relative to peers).

Observation: Companies that have experienced a deterioration in their operations due to COVID-19

will likely fail the qualitative factors test in 2020 and perhaps 2021, resulting in the need to perform the

one-step quantitative test for goodwill impairment.

In particular, most companies (public and non-public, alike) are impacted by the economic conditions

occurring from the economic shutdown in the wake of COVID-19, including:

23

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

1. Deterioration in general economic conditions

2. Deterioration in the environment in which an entity operates

3. Negative or declining cash flows, and

4. Decline in actual or planned revenue or earnings compared with actual and projected results of

relevant prior periods.

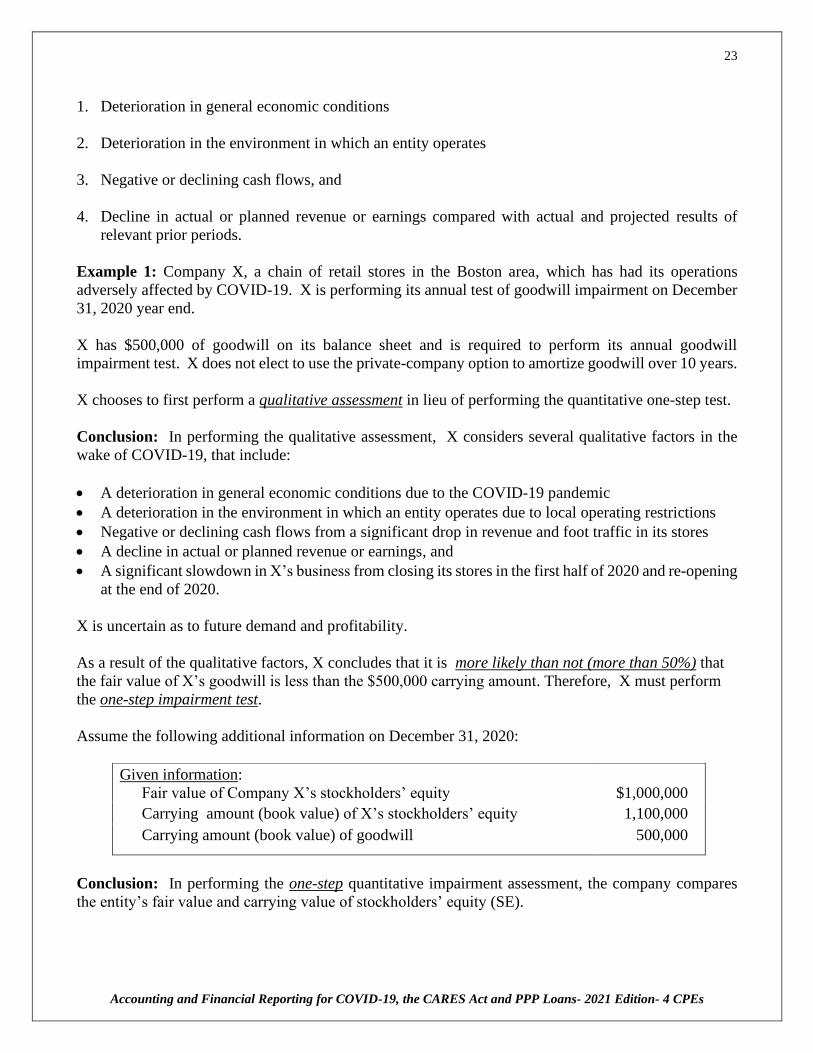

Example 1: Company X, a chain of retail stores in the Boston area, which has had its operations

adversely affected by COVID-19. X is performing its annual test of goodwill impairment on December

31, 2020 year end.

X has $500,000 of goodwill on its balance sheet and is required to perform its annual goodwill

impairment test. X does not elect to use the private-company option to amortize goodwill over 10 years.

X chooses to first perform a qualitative assessment in lieu of performing the quantitative one-step test.

Conclusion: In performing the qualitative assessment, X considers several qualitative factors in the

wake of COVID-19, that include:

• A deterioration in general economic conditions due to the COVID-19 pandemic

• A deterioration in the environment in which an entity operates due to local operating restrictions

• Negative or declining cash flows from a significant drop in revenue and foot traffic in its stores

• A decline in actual or planned revenue or earnings, and

• A significant slowdown in X’s business from closing its stores in the first half of 2020 and re-opening

at the end of 2020.

X is uncertain as to future demand and profitability.

As a result of the qualitative factors, X concludes that it is more likely than not (more than 50%) that

the fair value of X’s goodwill is less than the $500,000 carrying amount. Therefore, X must perform

the one-step impairment test.

Assume the following additional information on December 31, 2020:

Given information:

Fair value of Company X’s stockholders’ equity

$1,000,000

Carrying amount (book value) of X’s stockholders’ equity 1,100,000

Carrying amount (book value) of goodwill 500,000

Conclusion: In performing the one-step quantitative impairment assessment, the company compares

the entity’s fair value and carrying value of stockholders’ equity (SE).

24

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

Step: Identify a Potential Impairment:

Fair value of X’s stockholders’ equity $1,000,000

Less: Carrying amount of X’s stockholders’ equity 1,100,000

Equals: Goodwill impairment $(100,000)

Entry: December 31, 2020:

Goodwill Impairment loss

dr

100,000

cr

Goodwill 100,000

Once written down to $400,000, X is not permitted to write goodwill back up in future years.

Does a private (nonpublic) company have to worry about fair value if using the 10-year accounting

alternative to account for goodwill?

Generally, a private (nonpublic) company ignores impairment if it elects the 10-year accounting

alternative to account for goodwill. The reason is because an annual test for impairment of goodwill is

not required under the accounting alternative. Therefore, a private company may elect to amortize

goodwill over 10 years on a straight-line basis and avoid an annual test of goodwill impairment.

However, ASC 350, Intangibles- Goodwill and Other (as amended by ASU 2014-02) provides an

exception. A private company that elects the 10-year accounting alternative is required to perform an

impairment test in a limited situation if there is a triggering event on the balance sheet date.

The list of triggering events is the same list used to perform the qualitative assessment for goodwill, and

includes a deterioration in:

• Macroeconomic conditions

• Industry and market considerations

• Cost factors

• Overall financial performance

• Other relevant entity-specific events, and

• Events affecting a reporting unit.

In reviewing the previous list of triggering events, in 2020 and 2021, a private (nonpublic) entity electing

to amortize goodwill over 10 years may find that it has one or more triggering events that requires it to

test goodwill for impairment, even though it is amortizing goodwill over 10 years using the accounting

alternative.

Consider the following potential triggering events that could exist in 2020 and 2021, in light of the

economic impact of COVID-19 on businesses:

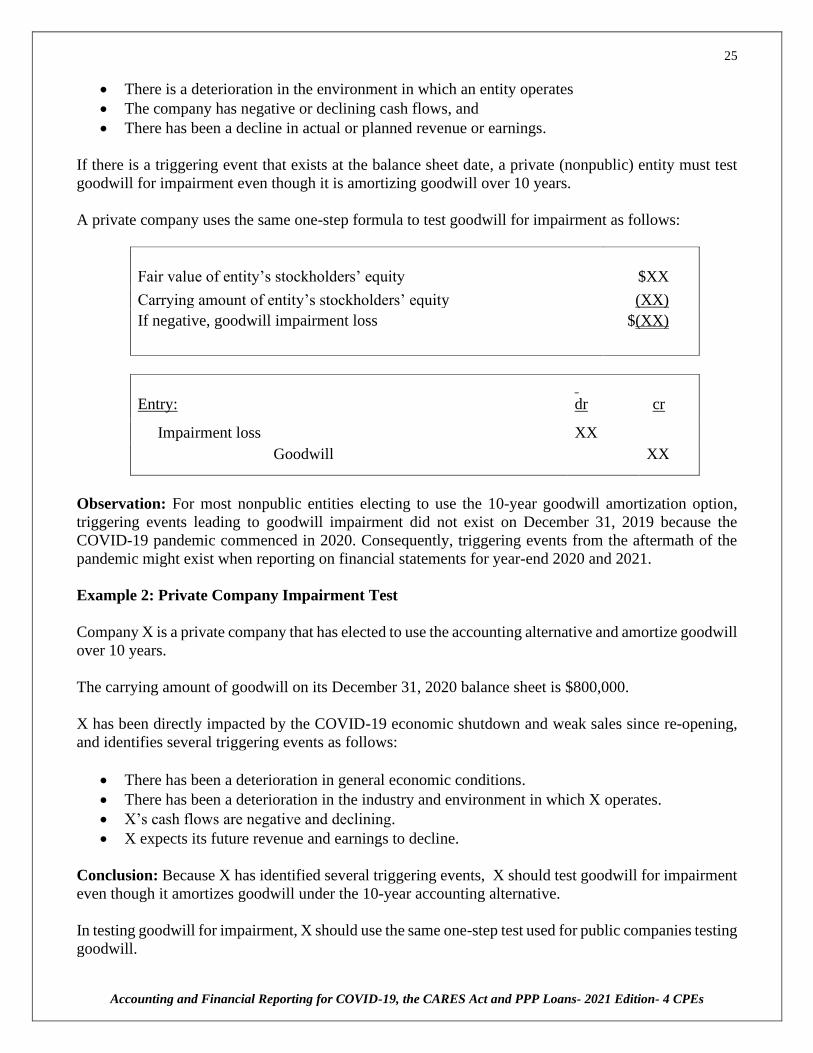

• There is a deterioration in general economic conditions

25

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

• There is a deterioration in the environment in which an entity operates

• The company has negative or declining cash flows, and

• There has been a decline in actual or planned revenue or earnings.

If there is a triggering event that exists at the balance sheet date, a private (nonpublic) entity must test

goodwill for impairment even though it is amortizing goodwill over 10 years.

A private company uses the same one-step formula to test goodwill for impairment as follows:

Fair value of entity’s stockholders’ equity

$XX

Carrying amount of entity’s stockholders’ equity (XX)

If negative, goodwill impairment loss $(XX)

Entry:

dr

cr

Impairment loss XX

Goodwill XX

Observation: For most nonpublic entities electing to use the 10-year goodwill amortization option,

triggering events leading to goodwill impairment did not exist on December 31, 2019 because the

COVID-19 pandemic commenced in 2020. Consequently, triggering events from the aftermath of the

pandemic might exist when reporting on financial statements for year-end 2020 and 2021.

Example 2: Private Company Impairment Test

Company X is a private company that has elected to use the accounting alternative and amortize goodwill

over 10 years.

The carrying amount of goodwill on its December 31, 2020 balance sheet is $800,000.

X has been directly impacted by the COVID-19 economic shutdown and weak sales since re-opening,

and identifies several triggering events as follows:

• There has been a deterioration in general economic conditions.

• There has been a deterioration in the industry and environment in which X operates.

• X’s cash flows are negative and declining.

• X expects its future revenue and earnings to decline.

Conclusion: Because X has identified several triggering events, X should test goodwill for impairment

even though it amortizes goodwill under the 10-year accounting alternative.

In testing goodwill for impairment, X should use the same one-step test used for public companies testing

goodwill.

26

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

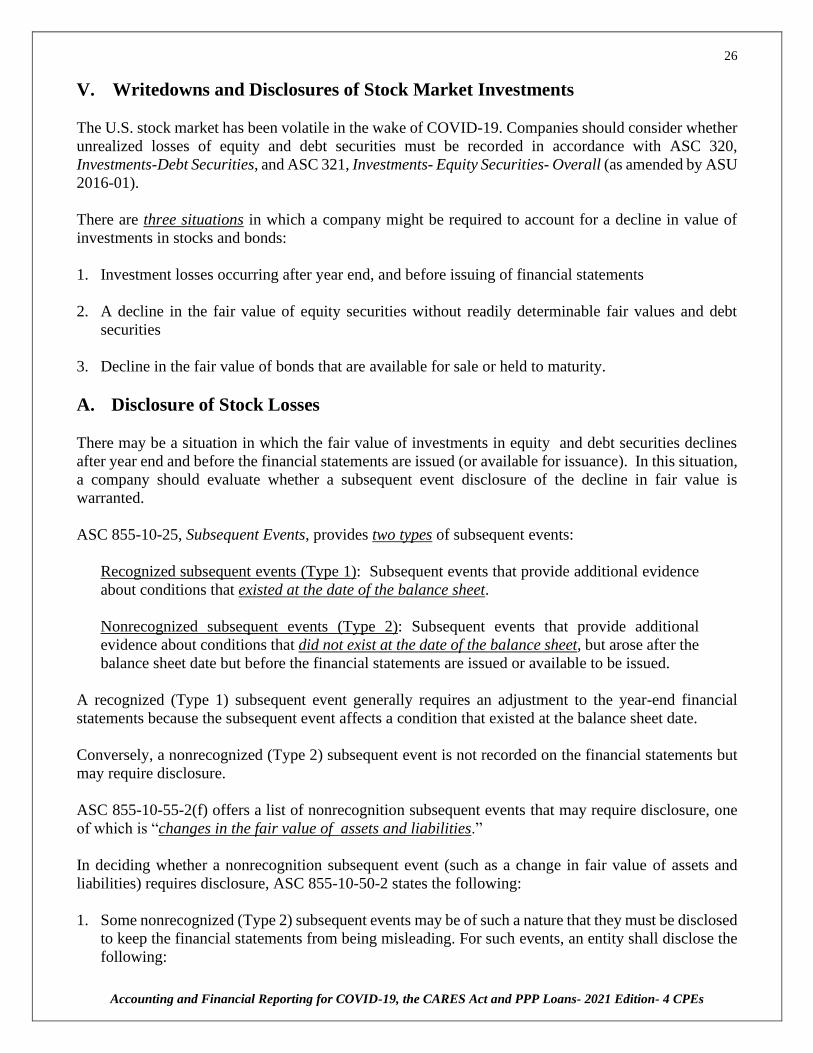

V. Writedowns and Disclosures of Stock Market Investments

The U.S. stock market has been volatile in the wake of COVID-19. Companies should consider whether

unrealized losses of equity and debt securities must be recorded in accordance with ASC 320,

Investments-Debt Securities, and ASC 321, Investments- Equity Securities- Overall (as amended by ASU

2016-01).

There are three situations in which a company might be required to account for a decline in value of

investments in stocks and bonds:

1. Investment losses occurring after year end, and before issuing of financial statements

2. A decline in the fair value of equity securities without readily determinable fair values and debt

securities

3. Decline in the fair value of bonds that are available for sale or held to maturity.

A. Disclosure of Stock Losses

There may be a situation in which the fair value of investments in equity and debt securities declines

after year end and before the financial statements are issued (or available for issuance). In this situation,

a company should evaluate whether a subsequent event disclosure of the decline in fair value is

warranted.

ASC 855-10-25, Subsequent Events, provides two types of subsequent events:

Recognized subsequent events (Type 1): Subsequent events that provide additional evidence

about conditions that existed at the date of the balance sheet.

Nonrecognized subsequent events (Type 2): Subsequent events that provide additional

evidence about conditions that did not exist at the date of the balance sheet, but arose after the

balance sheet date but before the financial statements are issued or available to be issued.

A recognized (Type 1) subsequent event generally requires an adjustment to the year-end financial

statements because the subsequent event affects a condition that existed at the balance sheet date.

Conversely, a nonrecognized (Type 2) subsequent event is not recorded on the financial statements but

may require disclosure.

ASC 855-10-55-2(f) offers a list of nonrecognition subsequent events that may require disclosure, one

of which is “changes in the fair value of assets and liabilities.”

In deciding whether a nonrecognition subsequent event (such as a change in fair value of assets and

liabilities) requires disclosure, ASC 855-10-50-2 states the following:

1. Some nonrecognized (Type 2) subsequent events may be of such a nature that they must be disclosed

to keep the financial statements from being misleading. For such events, an entity shall disclose the

following:

27

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

a. The nature of the event, and

b. An estimate of its financial effect, or a statement that such an estimate cannot be made.

Does a significant decline in the fair value of an investment after year end require disclosure as a

Type 2 subsequent event?

ASC 855 states that subsequent events should be disclosed if they are of “such a nature that they must

be disclosed to keep the financial statements from being misleading.” Yet, ASC 855 is not specific as

to whether a decline om fair value of investments after year end meets the requirement for disclosure.

The author suggests that a decline in the fair value of an investment portfolio after year end is not

typically disclosed as a subsequent event unless such a decline is permanent and material. If, instead,

the decline is nothing more than a recurring event within the typical ebb and flow of stock market values,

disclosure as a subsequent event is not warranted.

28

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

REVIEW QUESTIONS – Section 2

Under the NASBA-AICPA self-study standards, self-study sponsors are required to present review

questions intermittently throughout each self-study course. Additionally, feedback must be given to the

course participant in the form of answers to the review questions and the reason why answers are correct

or incorrect. To obtain the maximum benefit from this course, we recommend that you complete each

of the following questions, and then compare your answers with the solutions that immediately follow.

1. Which of the following is correct as it relates to the general rule for accounting for goodwill:

a. Goodwill should be amortized over 15 years with no test for impairment required

b. Goodwill should not be amortized. It should test for impairment only if there is a reason to

do so

c. Goodwill should be amortized over its useful life and tested for impairment

d. Goodwill should not be amortized and should be tested for impairment annually

2. Company X is an SEC company and has goodwill. Which of the following is correct:

a. X may amortize goodwill over a 10-year period

b. X may amortize goodwill over a 15-year tax life

c. X may not amortize goodwill

d. X has a choice of amortizing goodwill or not amortizing goodwill

3. Under GAAP, once goodwill is written down for an impairment loss, the writedown __________:

a. May be written back up to the original cost

b. May be written back up without limit

c. May not be restored

d. May be restored only if there are certain factors met that warrant a restoration

4. Facts: An entity is performing a qualitative assessment of impairment of its goodwill. The entity

concludes that it is not more likely than not that the fair value of the entity is less than its carrying

amount. Which of the following is correct:

a. The entity must perform a one-step impairment test

b. The impairment test does not apply to entities that qualify to use a qualitative assessment

c. The entity is not required to perform a one-step impairment test

d. The entity must perform a two-step impairment test

29

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

SUGGESTED SOLUTIONS

1. Which of the following is correct as it relates to the general rule for accounting for goodwill:

a. Incorrect. Goodwill is not amortized over 15 years and a test for impairment is required

under GAAP.

b. Incorrect. Although goodwill should not be amortized, it must be tested for impairment,

regardless of whether there is a reason to do so.

c. Incorrect. Goodwill should not be amortized over its useful life, although it is correct that it

should be tested for impairment.

d. Correct. GAAP requires that goodwill should not be amortized and should be tested

for impairment.

2. Company X is an SEC company and has goodwill. Which of the following is correct:

a. Incorrect. A special election to amortization goodwill is available. However, it is only

available for non-public (private) companies, and not SEC companies.

b. Incorrect. If X were a non-public company, it could amortize goodwill over 10 years, not

15 years, making the answer incorrect.

c. Correct. GAAP does not permit goodwill to be amortized for an SEC company, making

the answer correct.

d. Incorrect. Only non-public entities have a choice of amortizing goodwill or not amortizing

it, under the private company alternative. Because X is an SEC company, such a choice is

not available.

3. Under GAAP, once goodwill is written down for an impairment loss, the writedown ________:

a. Incorrect. The writedown may not be written back up to cost, making the answer incorrect.

b. Incorrect. Under no circumstances may the writedown be written back up, making the

answer incorrect.

c. Correct. GAAP states that subsequent reversal of a goodwill impairment loss is

prohibited once the impairment loss is recognized.

d. Incorrect. There are no factors that permit a restoration of a writedown making the answer

incorrect.

4. Facts: An entity is performing a qualitative assessment of impairment of its goodwill. The entity

concludes that it is not more likely than not that the fair value of the entity is less than its carrying

amount. Which of the following is correct:

a. Incorrect. Because the qualitative assessment indicates there is not an impairment, the entity

is permitted to bypass the one-step impairment test.

b. Incorrect. The qualitative assessment is a precursor to performing the one-step impairment

test. It does not automatically exempt an entity from the impairment test altogether.

c. Correct. Because it is not more likely than not that the fair value is less than its carrying

amount, there is no impairment and the entity is not required to perform the one-step

impairment test.

d. Incorrect. First, there is no impairment. Second, the impairment test is only one step. Thus,

the answer is incorrect.

30

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

VI. Inventory Costs and Valuation Issues

Throughout 2020 and into 2021, U.S. manufacturers have experienced reduced manufacturing volume

due to the sudden decline in product demand and the inability to purchase supplies and materials to

complete the manufacturing process.

These facts have resulted in several unintended consequences in valuing inventories:

1. Manufacturers may be allocating fixed overhead to inventories using a lower-than-normal capacity,

thereby creating an artificially higher unit cost that exceeds net realizable value.

2. Manufacturers may be capitalizing as fixed overhead costs certain abnormal idle facility costs

incurred during the pandemic shutdown. These costs should be expensed as period costs.

3. Declining sales prices have resulted in a lower net realizable value (NRV), which directly impacts

inventory valuations. NRV is used to value both:

a. Lower of cost and net realizable value, if FIFO or average cost method is used, and

b. Lower of cost or market, if LIFO or retail method is used.

A. GAAP Review of Inventories

ASC 330, Inventory, requires that certain rules be followed in valuing inventories:

1. Inventory costing rules required by GAAP follow:

a. Lower of cost and net realizable value is used to value FIFO and average cost inventories, and

b. Lower of cost or market is used to value LIFO and retail method inventories.

2. Inventory cost includes an allocation of variable production overheads and fixed production

overheads.

3. Overheads are allocated to inventories using the following approach:

a. Variable production overheads: are allocated to each unit of production based on actual use of

the production facilities (e.g., actual production volume).

b. Fixed production overheads: are allocated to inventories based on normal capacity of the

production facilities

4. Normal capacity: is the production expected to be achieved over a number of periods or seasons

under normal circumstances, taking into account the loss of capacity resulting from planned

maintenance.

a. Normal capacity includes a range of production levels within which ordinary variations in

production levels are expected.

31

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

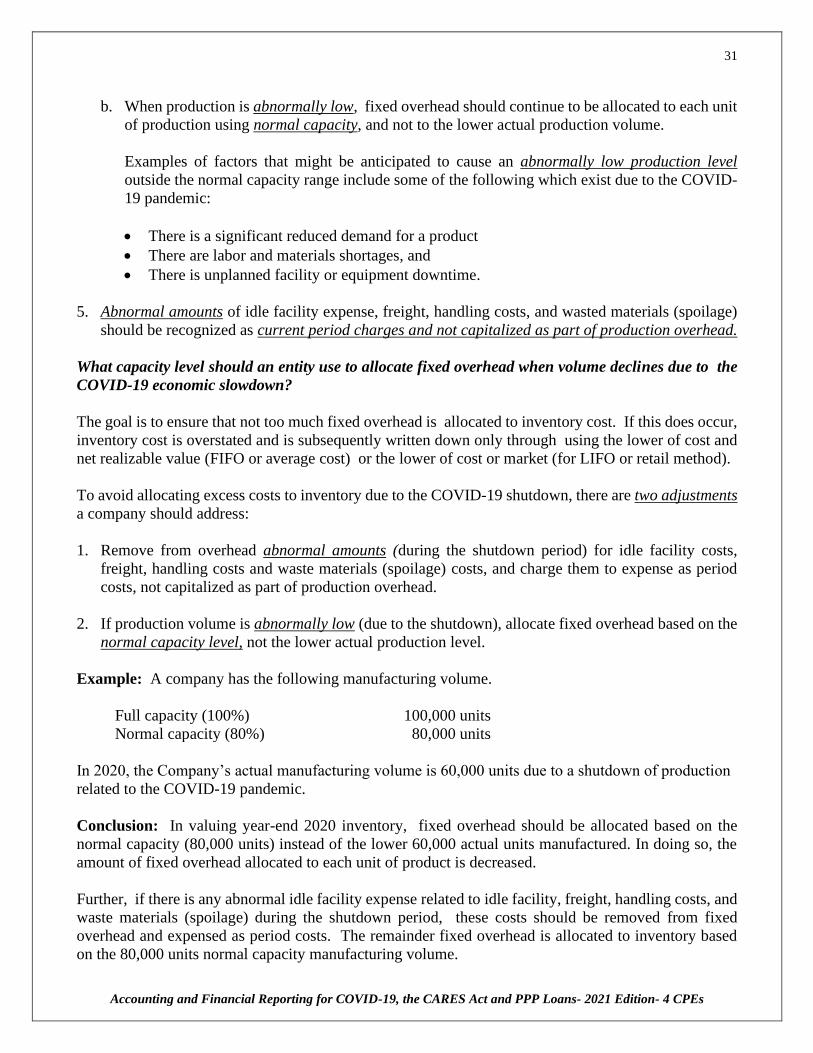

b. When production is abnormally low, fixed overhead should continue to be allocated to each unit

of production using normal capacity, and not to the lower actual production volume.

Examples of factors that might be anticipated to cause an abnormally low production level

outside the normal capacity range include some of the following which exist due to the COVID-

19 pandemic:

• There is a significant reduced demand for a product

• There are labor and materials shortages, and

• There is unplanned facility or equipment downtime.

5. Abnormal amounts of idle facility expense, freight, handling costs, and wasted materials (spoilage)

should be recognized as current period charges and not capitalized as part of production overhead.

What capacity level should an entity use to allocate fixed overhead when volume declines due to the

COVID-19 economic slowdown?

The goal is to ensure that not too much fixed overhead is allocated to inventory cost. If this does occur,

inventory cost is overstated and is subsequently written down only through using the lower of cost and

net realizable value (FIFO or average cost) or the lower of cost or market (for LIFO or retail method).

To avoid allocating excess costs to inventory due to the COVID-19 shutdown, there are two adjustments

a company should address:

1. Remove from overhead abnormal amounts (during the shutdown period) for idle facility costs,

freight, handling costs and waste materials (spoilage) costs, and charge them to expense as period

costs, not capitalized as part of production overhead.

2. If production volume is abnormally low (due to the shutdown), allocate fixed overhead based on the

normal capacity level, not the lower actual production level.

Example: A company has the following manufacturing volume.

Full capacity (100%) 100,000 units

Normal capacity (80%) 80,000 units

In 2020, the Company’s actual manufacturing volume is 60,000 units due to a shutdown of production

related to the COVID-19 pandemic.

Conclusion: In valuing year-end 2020 inventory, fixed overhead should be allocated based on the

normal capacity (80,000 units) instead of the lower 60,000 actual units manufactured. In doing so, the

amount of fixed overhead allocated to each unit of product is decreased.

Further, if there is any abnormal idle facility expense related to idle facility, freight, handling costs, and

waste materials (spoilage) during the shutdown period, these costs should be removed from fixed

overhead and expensed as period costs. The remainder fixed overhead is allocated to inventory based

on the 80,000 units normal capacity manufacturing volume.

32

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

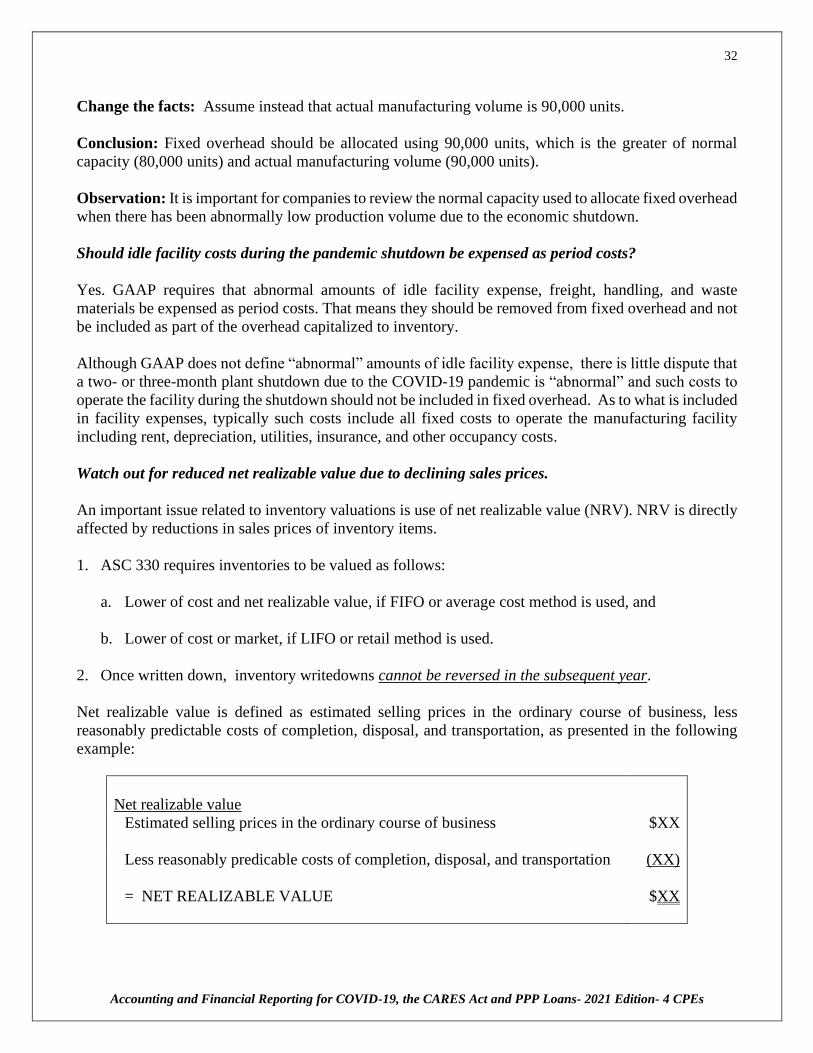

Change the facts: Assume instead that actual manufacturing volume is 90,000 units.

Conclusion: Fixed overhead should be allocated using 90,000 units, which is the greater of normal

capacity (80,000 units) and actual manufacturing volume (90,000 units).

Observation: It is important for companies to review the normal capacity used to allocate fixed overhead

when there has been abnormally low production volume due to the economic shutdown.

Should idle facility costs during the pandemic shutdown be expensed as period costs?

Yes. GAAP requires that abnormal amounts of idle facility expense, freight, handling, and waste

materials be expensed as period costs. That means they should be removed from fixed overhead and not

be included as part of the overhead capitalized to inventory.

Although GAAP does not define “abnormal” amounts of idle facility expense, there is little dispute that

a two- or three-month plant shutdown due to the COVID-19 pandemic is “abnormal” and such costs to

operate the facility during the shutdown should not be included in fixed overhead. As to what is included

in facility expenses, typically such costs include all fixed costs to operate the manufacturing facility

including rent, depreciation, utilities, insurance, and other occupancy costs.

Watch out for reduced net realizable value due to declining sales prices.

An important issue related to inventory valuations is use of net realizable value (NRV). NRV is directly

affected by reductions in sales prices of inventory items.

1. ASC 330 requires inventories to be valued as follows:

a. Lower of cost and net realizable value, if FIFO or average cost method is used, and

b. Lower of cost or market, if LIFO or retail method is used.

2. Once written down, inventory writedowns cannot be reversed in the subsequent year.

Net realizable value is defined as estimated selling prices in the ordinary course of business, less

reasonably predictable costs of completion, disposal, and transportation, as presented in the following

example:

Net realizable value

Estimated selling prices in the ordinary course of business

$XX

- Less reasonably predicable costs of completion, disposal, and transportation (XX)

= NET REALIZABLE VALUE

$XX

33

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

A decline in estimated sales price results in a lower NRV, which, in turn, results in both a lower of cost

and net realizable value computation (for FIFO and average cost), and lower of cost or market4 (for LIFO

and retail).

With the economic decline from COVID-19, estimated selling prices could decline simply because

demand for products is disproportionately low relative to historical levels. If sales prices decline, net

realizable value (NRV) also declines, resulting in lower inventory valuations. Management, accountants,

and auditors should be aware of the impact NRV may have on inventory valuations in 2020 and 2021.

VII. Trade Receivables and the Allowance for Doubtful Accounts

Companies should pay close attention to trade receivables and the collectability of those receivables in

light of the economic downturn. Collectibility of trade receivables is likely to be an issue well into 2020

and 2021 as companies re-open and need to rebalance their cash flow needs.

Consider the following:

1. Companies that have long-term customers who have historically paid their balances timely, may

learn that those same customers are now encountering significant cash flow problems in the

aftermath of the COVID-19 shutdown or slowdown of their operations.

2. Using historical trends and ratios for estimating trade receivable bad debts may not be meaningful

given the current economic climate as customer payment experience might not be an indication of

future ability to pay.

3. Even after businesses re-open their operations after the COVID-19 shutdown, it may take months,

perhaps years, for some businesses to stabilize their liquidity to the extend they can regain the ability

to make timely payments on receivables.

Companies should consider whether the allowance for doubtful accounts is sufficient to accommodate

bad debts within a volatile economic climate.

VIII. Exit and Termination Costs

In light of COVID-19, companies should assess whether they have properly recorded a liability for

termination and other employee benefits to be paid to employees during the shutdown and for periods

thereafter. Some benefits might be required by law, such as sick pay, while others could be voluntarily

paid to support employees on a short-term basis until the business is revived.

Companies should consider whether such benefits must be accrued and are subject to ASC 420, Exit or

Disposal Cost Obligations, in cases in which there is no contractual obligation to pay benefits, such as

severance pay.

The GAAP rules related to exit and disposal costs follow:

4 Using LCM, market value is based on replacement cost. The ceiling for replacement cost is NRV.

34

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

1. Exit and Disposal Costs covered by ASC 420, Exit or Disposal Cost Obligations, consist of those

costs incurred as a result of a one-time event that might include:

a. A sale or termination of a line of business

b. The closing of business activities in a particular location- such as due to COVID-19

c. The relocation of business activities from one location to another

d. Changes in a management structure

e. A fundamental reorganization that affects the nature and focus of operations

f. A natural disaster

2. If a closing is temporary, it may not qualify as an exit or disposal cost obligation under ASC 420.

3. Costs associated with exit plans include:

a. Involuntary employee termination benefits pursuant to a one-time benefit arrangement that is

not an ongoing benefit arrangement or an individual deferred compensation contract

b. Costs to consolidate facilities to relocate employees

c. Costs to terminate a contract that is not a lease

d. Costs associated with a disposal activity covered as a discontinued operation, and

e. Costs associated with an exit activity, including exit activities associated with an entity newly

acquired in a business combination or an acquisition by a not-for-profit entity.

4. Exit costs do not include costs covered by other GAAP such as postemployment benefits and

contractual arrangements.

What costs are considered exit and disposal costs related to COVID-19?

Exit and disposal costs related to the COVID-19 pandemic shutdown and business decline might

include:

• Event cancellation costs

• Safety and pandemic protection costs including screening costs, personal protection equipment

(PPE) for employees and customers, etc.

• Medical and security costs

• Transportation of employees

• Cleaning of facilities, and

• Housing of employees during the shutdown.

With respect to exit costs, GAAP requires that certain actions be taken that include:

35

Accounting and Financial Reporting for COVID-19, the CARES Act and PPP Loans- 2021 Edition- 4 CPEs

1. An entity shall record a liability for a cost associated with an exit or disposal activity measured at

fair value in the period in which the liability is incurred.