Accounting and Auditing Update www.kpmg.com/in Issue no. 05/2016 December 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting and Auditing Update

www.kpmg.com/in

Issue no. 05/2016

December 2016

Editorial

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Sai Venkateshwaran

Partner and HeadAccounting Advisory Services KPMG in India

Ruchi Rastogi

Executive DirectorAssuranceKPMG in India

In this month, the Ministry of Corporate Affairs (MCA) notified the much awaited sections of the Companies Act, 2013 relating to restructuring of companies and certain sections concerning winding-up of companies. These notifications also bring certain sections, relating to winding-up of companies in the Insolvency and Bankruptcy Code, 2016 to life. This edition of Accounting and Auditing Update (AAU) includes a detailed analysis on these recent notifications from the MCA along with our comments.

The Institute of Chartered Accountants of India issued a revised guidance note on reports or certificates for special purposes. The revised guidance note requires management of entities and practitioners to carefully assess the scope of such engagements i.e. to provide reasonable assurance or limited assurance on such reports. It also discusses the format to be used for certificates or reports when law or regulation prescribes a format or phrasing to be used for the assurance report. Our article provides an overview of key elements of the guidance note and highlights additional considerations

for management of entities and practitioners.

Ind AS provides a wider definition of control in comparison to Accounting Standards. Thus, the universe of entities that fall within the definition of a ‘subsidiary’ is likely to change under Ind AS. Such change is bound to give rise to certain practical issues while preparing Consolidated Financial Statements (CFS). Our article covers some of these issues and explains the accounting under Ind AS with the help of examples.

Entities may receive or give interest free or low-interest loans either from the government or their group entities. Ind AS 109, Financial Instruments provides guidance on accounting for such loans. Our article on this topic explains the accounting for low-interest and interest-free loans with the help of illustrative examples and a detailed flowchart.

As is the case each month, we also cover a regular round-up of the recent regulatory updates in India.

We would be delighted to receive feedback/suggestions from you on the topics that we should cover in forthcoming issues of the AAU.

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Table of contentsMCA’s recent notifications: Easier restructuring 01

Guidance Note on reports or certificates for special purposes 05

Consolidated financial statements and first-time adoption of Ind AS

09

Accounting for low-interest and interest-free loans 15

Regulatory updates 21

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

MCA’s recentnotifications:Easier restructuringOn 7 December 2016, the Ministry of Corporate Affairs (MCA) issued a notification, whereby certain sections of the Companies Act, 2013 (2013 Act) were notified to come into force. These sections amongst others, relate to:• reduction of capital and variations of

shareholders’ right;• compromises, arrangements and

amalgamations.

In addition to the above, certain winding-up sections were also notified by MCA. The notification states that the aforementioned sections come into effect on 15 December 2016.

MCA on 7 December 2016 also notified the Companies (Transfer of Pending Proceedings), Rules 2016 (Transfer Rules) and furthermore issued the Companies (Removal of Difficulties) Fourth Order, 2016 (Difficulties Order) to facilitate a smooth transition of the proceedings initiated under the Companies Act, 1956 (1956 Act) and pending before any district court or high courts to the National Company Law Tribunal (NCLT).

The rules in relation to compromise, arrangements and amalgamation came into effect on 15 December 2016, while rules in relation to procedure for reduction of share capital of company will come into effect from date of publication in Official Gazette.

In this article, we aim to provide an overview of some key provisions of the sections pertaining to reduction of capital, variations of shareholders’ right and compromises, arrangements and amalgamations and the list of pending proceedings which shall be transferred to NCLT.

Sections pertaining to reduction of capital (Section 66)

NCLT to assume jurisdiction of the high courts as the sanctioning authority in relation to capital reduction. Following are some key provisions on reduction of capital under the 2013 Act:• Companies cannot undertake

reduction of capital if the company is in arrears in the repayment of any deposits accepted by it or the interest payable thereon.

• NCLT to give notice of every capital reduction application to the Central Government (CG), Registrar of Companies (ROC), Securities and Exchange Board of India (SEBI) (in case of listed companies) and to the creditors of the company.

• CG and others may make representations within three months from the date of receipt of the notice, and if no representation has been received within the said period, it will be presumed that they have no objection to the reduction of capital.

• Notice to the creditors is now made mandatory in all cases, whether it involves repayment of capital or not.

• The company needs to file a certificate (to the NCLT) from its auditor to the effect that the accounting treatment for such reduction is in conformity with the prescribed accounting standards.

1

This article aims to

• Summarise key provisions of the sections pertaining to reduction of capital, variations of shareholders’ right and compromises, arrangements and amalgamations

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Sections pertaining to variation of shareholders’ right (Section 48)

Following are the some key provisions on variation of shareholders’ right under the 2013 Act:• Where a share capital of the company

is divided into different classes of shares, the rights attached to the shares of any class may be varied with the consent of not less than three-fourth of the issued shares of that class or by means of a special resolution passed at a separate meeting of the holders of shares of that class.

• If the variation of rights of one class of shareholders affects the rights of any other class of shareholders, the consent of three-fourths of such other class of shareholders shall also be obtained and provisions relating to Section 48 shall apply to such variation.

• Where the holders of not less than 10 per cent of the issued shares of a class did not consent to such variation or vote in favour of the special resolution for the variation, they may apply to the NCLT to have the variation cancelled.

Simplifying procedures for restructuring

A serious effort has been made to address the shortcomings of the 1956 Act and provide for a simpler and faster process of mergers and acquisitions and other restructuring. In the 2013 Act, separate procedures have been prescribed for ‘compromise or arrangement’ and ‘amalgamation or demerger’. The NCLT assumes the jurisdiction of the high court as sanctioning authority in relation to restructuring.

Arrangements with shareholders/creditors (Section 230 and 232)• The scope of this section includes

– reduction of capital – corporate debt restructuring – takeover of listed companies

(through a scheme) – reorganisation of the company’s

share capital by consolidating the shares of different classes or by division of shares into shares of different classes, or by both of those methods

– amalgamation of companies – demerger of companies – winding up of a company.

• Increased disclosure requirements in the notice to members/creditors in a bid to boost transparency and keeping all stakeholders well informed

• To encourage maximum participation from members, postal ballot or through electronic means has been made compulsory and combined results of voting by members present at the meeting and by postal ballot needs to be considered

• Arrangement can be objected only by a person holding at least 10 per cent shareholding or owning five per cent debt as per latest audited financial statements. This will avoid all superfluous objections and litigations

• Notice of compromise or arrangement to be given to the Central Government (CG), Income tax department, Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Stock exchanges, Registrar of Companies (ROC), Official Liquidator (OL), Competition Commission of India (CCI), and other sector regulators/authorities as necessary. The authorities are allowed a period of 30 days from receipt of the notice to respond and if no response is received within such time, it is presumed that they have no representation. This would effectively act as a pre-approval and make the process time bound

• An important change is the requirement to furnish the auditor’s certificate (to the NCLT) to the effect that the accounting treatment specified in the scheme is in conformity with the prescribed Accounting Standards in all cases. Currently, such certificate was required only in relation to listed companies as per the listing regulations with stock exchanges.

In addition, following significant changes are made in the amalgamation process in comparison to the Companies Act, 1956:• Creation of treasury stock pursuant

to amalgamation/demerger. Cross holding of shares resulting in creation of treasury stock should be cancelled and no shares should be issued against the same

• Yearly statement confirming implementation of the scheme, to be in accordance with the Order, is required to be submitted till completion of the scheme

• In the case of amalgamation of a listed transferor company into an unlisted transferee company, the 2013 Act allows an unlisted company to remain unlisted by giving an exit option to the dissenting shareholders. This provision seems to suggest automatic delisting even without complying with the SEBI Delisting Guidelines.

Fast track amalgamations/demergers• The 2013 Act has introduced a

simplified procedure for merger and amalgamation between: – holding company and its wholly

owned subsidiary – two or more ‘small companies’, or – such other prescribed classes of

companies.

Any such merger can be given effect to without the approval of the NCLT, subject to compliance with certain other procedures.• Small company is defined as follows:

– A non-public company – Not being a holding/subsidiary

company, a company for charitable purposes or a company established under a special Act

– Having a paid-up capital less than INR5 million (the amount can be prescribed up to INR50 million) or turnover less than INR20 million (the amount can be prescribed up to INR200 million) as per the last audited financials.

Thus, a company not meeting the above criteria would not be considered as a small company.

• Transferor and transferee companies need to file declaration of solvency. Prima facie it appears that companies with negative net worth cannot use the fast track route.

2

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

• The scheme would need to be approved by majority representing 90 per cent of the members and 90 per cent in value of the creditors or class of creditors of respective companies.

• CG may, if it receives objections or suggestions or for any other reason is of the opinion that the scheme is not in public interest or in interest of creditors, instead of approving the scheme, may refer the scheme to the NCLT. In such a case, the NCLT may direct that process under Section 232 to be carried out.

Purchase of minority shareholding (Section 236)• The 2013 Act allows any person or

group of persons holding 90 per cent or more of the issued equity capital of a company to purchase the remaining equity shares of the company from minority shareholders at a price determined by a registered valuer in accordance with the prescribed rules

• Similarly, the minority shareholders of the company may also offer the majority shareholders to purchase the minority equity shareholding of the company

• Although this provision applies to all companies, it may prove beneficial to delisted companies with minority shareholding and enable the majority shareholder to buy-out minority shareholder at a fair price.

Transfer of pending proceedings

Following matters shall stand transferred to NCLT with effect from 15 December 2016:• All proceedings under the 1956

Act, including proceedings relating to arbitration, compromise, arrangements and reconstruction, other than proceedings relating to winding-up and those reserved for orders.

• All petitions relating to winding-up under Section 433(e) of the 1956 Act on the ground of inability to pay its debts pending before a high court, and where the petition has not been served on the respondent, such petition shall be disposed of in accordance with Insolvency and Bankruptcy Code, 2016. However, all cases where an opinion has been forwarded by the Board for Industrial and Financial Reconstruction for winding-up of a company to a high court and where no appeal is pending, and proceeding for winding-up has been initiated, shall continue to be dealt with by such high court in accordance with the provisions of the 1956 Act.

• All petitions relating to winding-up under Section 433(a) and (f) of the 1956 Act pending before high court and where the petition has not been served on the respondent.

This step further helps towards operationalisation of the Insolvency and Bankruptcy Code, 2016 (Code). The CG has notified Section 33 to Section 54 of the Code relating to liquidation process for corporate persons, to be effective from 15 December 2016 and Section 59 of the Code relating to Voluntary Winding up, to be effective from 1 April 2017.

3

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Companies (Removal of Difficulties) Fourth Order, 2016

While the order gives clarity on which of the proceedings get transferred to NCLT, does it provide clarity on the process to be followed. For instance, if shareholders’ approval has been obtained under the 1956 Act, can they now file with NCLT instead of a High Court, or will they need to follow the new process under the 2013 Act before filing with NCLT, i.e. file with all relevant regulators, etc. before filing with NCLT.

Registered valuer

The recent notification does not notify Section 247 that deals with the registered valuer. The 2013 Act requires valuation in respect of any property, stocks, shares, debentures, securities, goodwill or any other assets or net worth of a company or its liabilities under various provisions. To be specific, Section 230 requires a valuation report in respect of shares and property and all assets, tangible and intangible, movable and immovable, of the company by a registered valuer. Similarly, Section 236 requires the acquirer to offer to the minority shareholders of the company for buying the equity shares held by minority shareholders at a price determined on the basis of valuation by a registered valuer.

The rules specify that till the registration of persons as valuers is prescribed under Section 247 of the 2013 Act, the valuation report would be made by an independent merchant banker who is registered with the SEBI or an independent Chartered Accountant in practice having minimum experience of 10 years.

Purchase of minority shareholding (Section 236)

The 2013 Act has introduced new provisions relating to buy-out of minority shareholding under certain circumstances. This is likely to provide greater flexibility to the promoters/acquirers in realigning the control and management of a company as unnecessary interference from minority shareholders is removed.

Currently, it is not clear whether an offer from a majority shareholder to purchase the shareholding of minority shareholders would be binding on the minority. Additionally, timeline and other procedures for offer from a minority are not clearly specified in the 2013 Act. Another area of challenge is that the mechanism for higher price sharing with minority shareholders is not clear.

The 2013 Act uses the term ‘transferor company’ in Section 236. However, this term has not been defined in the 2013 Act. Therefore, the Company Law Committee in its report in February 2016 recommended to amend Section 236 and suggested that references to the phrase ‘transferor company’ in Section 236, to be modified to a ‘company whose shares are being transferred’ or alternatively, an explanation to be provided in the provision clarifying that Section 236 only applies to the acquisition of shares. Therefore, the Companies (Amendment) Bill, 2016 proposes to amend Section 236 of the 2013 Act to substitute the words ‘transferor company’ with the words ‘company whose shares are being transferred’ for providing clarity.

Treasury stock

There is lack of clarity on treatment of treasury shares already held by companies.

Yearly statement

The MCA should provide clarity about the time till when a yearly statement about implementation of scheme is required to be filed with the Registrar of Companies.

Fast track mergers/demergers

Significant benefits of fast track are:• Approval of NCLT is not required• Notice is not required to be given

to various authorities like income tax, etc. (as required in normal amalgamation/demerger process)

• Auditor’s certificate of compliance with applicable accounting standards is not required

• All the above is likely to result in reduction in burden of administration, compliances, timelines and costs.

If the CG refers the scheme to NCLT then this is expected to result in duplication of efforts and may take away the benefits of the fast track process.

Another area of challenge is to receive the necessary positive confirmation from shareholders and creditors holding 90 per cent in value.

Sections not notified

Some of the important sections that are yet to be notified are:• Section 234 on Merger or

amalgamation of company with foreign company

• Section 247 on Valuation by registered valuers

• Section 304 to 314 on voluntary winding up.

Our comments

4

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Guidance Note on reports or certificates for special purposesIntroductionIn September 2016, the Auditing and Assurance Standards Board (AASB) of the Institute of Chartered Accountants of India (ICAI) issued a thoroughly revised and detailed guidance note on reports or certificates for special purposes (guidance note). The earlier version of the guidance note was issued in 1984.

This article aims to highlight key elements of the guidance note that provide additional guidance in comparison to the earlier version.

Special purpose reports or certificates

The guidance note does not deal with the reports issued in audits or reviews of historical data. It specifically caters to the reports or certificates in support of statements or other information provided by an entity, such as, reports or certificates:

a. To fulfil a contractual reporting obligation

b. Required by those charged with governance of an entity

c. Required by laws and regulations.

For example, a practitioner’s report for turnover/net worth/net profit/working capital/similar engagement pursuant to a tender, an auditor’s annual activity certificate for Indian branch office/liaison office of foreign companies, an auditor’s report on the manner of utilisation of funds required under the Securities and Exchange Board of India (Listing Regulations and Disclosure Requirements) Regulations, 2015, etc.

Certain engagements are not covered by the guidance note, such as, engagements covered by Standards on Related Services (SRS) - agreed-upon procedures and compilation engagements, the preparation of tax returns where no assurance opinion/conclusion is expressed, consulting (or advisory) engagements - management and tax consulting.

This article aims to

• This article aims to provide an overview of the key elements in the revised guidance note for entities while obtaining a report/certificate for special purpose from practitioners

5

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Engagement risk – reasonable or limited assurance

The words or phrases like ‘certify’ or ‘true or correct’ could give an impression that an absolute level of assurance is provided by the practitioner on the subject matter. Absolute assurance

could indicate that a practitioner has performed procedures as considered appropriate to reduce the engagement risk to zero.

The guidance note, on the other hand, specifies that a practitioner would either provide a reasonable assurance or limited assurance.

A practitioner is not expected to reduce the engagement risk to zero. This is because there are inherent limitations attached to the procedures which a practitioner may perform in relation to issuance of a report or a certificate, as the case may be. The inherent limitations may arise from the following factors:• The nature of financial reporting• The use of selective testing

• The inherent limitations of internal controls

• The fact that much of the evidence available to the practitioner is persuasive rather than conclusive

• The nature of procedures to be performed in a specific situation. The use of professional judgement in gathering and evaluating evidence and forming conclusions based on that evidence

• In some cases, the characteristics of the underlying subject matter when evaluated or measured against the criteria

• The need for the engagement to be concluded within a reasonable period of time and at a reasonable cost.

Reasonable assurance engagement: An assurance engagement in which the practitioner reduces engagement risk to an acceptable low level in the circumstances of the engagement, as the basis for the practitioner’s opinion. The practitioner’s opinion is expressed in a form that conveys the practitioner’s opinion on the outcome of the measurement or evaluation of the underlying subject matter against the criteria.

Limited assurance engagement: An assurance engagement in which the practitioner reduces the engagement risk to a level that is acceptable in the circumstances of the engagement but where that risk is greater than for a reasonable assurance engagement, as the basis for expressing a conclusion in a form that conveys whether, based on the procedures performed and evidence obtained, a matter(s) has(have) come to the practitioner’s attention to cause the practitioner to believe that the subject matter information is materially misstated. The nature, timing, and extent of procedures performed in a limited assurance engagement is limited compared with that necessary in a reasonable assurance engagement but is planned to obtain a level of assurance that is, in the practitioner’s judgement meaningful.

6

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Scope of the engagement – careful evaluation

A practitioner needs to carefully evaluate the scope of the engagement i.e. whether the practitioner would be able to provide reasonable assurance or limited assurance on the subject matter.

The word ‘certificate’ as described in the laws and regulations or even in the contract that an entity might have entered into can normally be associated with reasonable assurance. However, depending upon the circumstances and based upon the nature, timing and extent of the procedures which a practitioner can perform, the guidance note provides that a practitioner can conclude that a reasonable assurance cannot be expressed on the subject matter of the ‘certificate’ and only ‘limited assurance conclusion’ can be given.

Additionally, if the engaging party imposes a limitation on the scope of the practitioner’s work and if the practitioner believes that the limitation is expected to result in the practitioner disclaiming an opinion/a conclusion on the subject matter information, the practitioner should not accept such an engagement as an assurance engagement, unless required by law or regulation to do so.

Additional considerations

Some of the additional considerations emanating from the guidance note are as set out below:• Identification of basic elements

forming part of the assurance report: Whilst the guidance note does not require a standardised format for reporting on all assurance engagements, it does prescribe the basic elements required to form part of the assurance report.

Basic elements include title, addressee, identification or description of the level of assurance obtained by the practitioner, the subject matter information and, when appropriate, the underlying subject matter, identification of the applicable

criteria, description of any significant inherent limitations associated with the measurement or evaluation of the underlying subject matter against the applicable criteria, where appropriate, restriction on usage, statement to identify responsible party and description of their responsibilities and the practitioner’s responsibility, informative summary of the work performed, practitioner’s opinion/conclusion, etc.

• Statement on meeting the requirements of the guidance note: The assurance report to be issued by the practitioner needs to contain a statement that the engagement was performed in accordance with the requirements of the guidance note issued by ICAI and that the practitioner complies with the independence and other ethical requirements of the Code of Ethics issued by the ICAI. A practitioner who performs assurance engagements covered under this guidance note is governed by the same ethical and quality control requirements as laid down in the Framework for Assurance Engagements.

• Statement on compliance with requirements of SQC 1: The practitioner is required to explicitly state in the assurance report on the compliance procedures followed by the firm of which the practitioner is a partner, of relevant applicable requirements of the Standard on Quality Control (SQC) 1, Quality Control for Firms that Perform Audits and Reviews of Historical Financial Information, and Other Assurance and Related Services Engagements. SQC 1 requires establishment of policies and procedures for the timely completion of the assembly of engagement files.

• Materiality: The guidance note thoroughly addresses the materiality considerations which a practitioner can apply while performing the assurance engagement. Materiality

is considered in the context of qualitative factors and, when applicable, quantitative factors. The practitioner has to apply his/her professional judgement when determining the relative importance of such factors when considering materiality.

• Subsequent events: The practitioner should consider the effect on the subject matter information and on the assurance reports of events up to the date of the assurance report, and should respond appropriately to the facts that become known to the practitioner after the date of the assurance report, that had they been known to the practitioner at that date, may have caused the practitioner to amend the assurance report.

• Written representations: The guidance note also explicitly provides insights into the written representation which the practitioner should request from appropriate parties.

Assurance report prescribed by law or regulation

In some cases, law or regulation prescribes the layout or wording of the assurance report. The guidance note provides insights into how the same should be dealt with by both the practitioner and the entity involved i.e., the engaging party.

To begin with, it is pertinent that the practitioner after a discussion of the matter provides a draft of the assurance report to be issued that duly incorporates the essential elements as prescribed by the guidance note. There should be an agreement between the practitioner and the engaging party on the resulting modifications to the layout or wording prescribed under the laws or regulations. The agreement on layout or wording of the assurance report should be duly documented in the engagement letter.

7

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

There could be situations wherein the concerned authorities reject the aforesaid assurance report issued by the practitioner on account of the modifications made to the prescribed layout or wording. The guidance note prescribes that in such circumstances, the practitioner should obtain evidence of rejection of the assurance report by the concerned authorities and make it part of the engagement documentation. Further, the practitioner can also consider enclosing a statement containing essential elements of an assurance report as prescribed in the guidance note in accordance to the format prescribed under the law or regulation. Such enclosure should also state the fact that a report issued earlier in accordance with the guidance note had been rejected by the concerned authorities.

The guidance note also envisages practical challenges in cases wherein the concerned regulator has expressly indicated that any modification to the layout or wording of the format is not acceptable and where time available to follow the process highlighted in the aforesaid paragraph is not sufficient. In such cases, the practitioner may issue the assurance report in the format prescribed under law or regulation after ensuring that all the requirements of the guidance note have been complied with and enclose a statement as referred above giving suitable reference of such statement in the format. (e.g. ‘in terms of our statement of even date’ or ‘to be read with the enclosed statement of even date’, etc.)

Obtaining the assurance opinion/conclusion

The guidance note provides a detailed direction for obtaining an assurance report. An assurance report should be in writing and should contain a clear expression of the practitioner’s opinion/conclusion about the subject matter information. Various types of assurance reports which a practitioner can issue based on his/her opinion/conclusion of work performed by him/her are as given:

• Unmodified opinion/conclusion on the assurance reports/certificates

Where the subject matter under examination complies with or has been prepared, as the case may be, in all material respects, in accordance with the applicable criteria, an unmodified opinion/certificate will be issued.

If a practitioner considers it necessary to draw attention of the intended users to a matter presented or disclosed in the subject matter information which may be of such importance that it is fundamental for the understanding of the subject matter information, such matter may be highlighted by issuing an ‘emphasis of matter’ paragraph.

• Modified opinion/conclusion

A modified opinion or conclusion would be issued in case of an assurance report or certificate where either the subject matter information is materially misstated or the practitioner has not been able to obtain access to all the information and explanation necessary for the purpose of the engagement. The types of reports that may be issued is also affected by the materiality and pervasiveness of the misstatement/possible misstatement on the subject matter information.

ConclusionWith an increase in complexities due to the revised laws and regulations and surge in the number of reports and certifications required by various legal authorities and other parties from practitioners, a clear guidance is expected to help both the management as well as the practitioner on their roles and responsibilities with respect to such engagements.

The guidance note issued by the ICAI provides details of each aspect

of the engagement in order to avoid misunderstandings between the parties to the engagement and guides them with the manner in which the engagement is to be conducted. Additionally, the guidance note is based on ISAE 3000, Assurance Engagements Other than Audits or Reviews of Historical Financial Information, therefore, the certificates obtained by companies are in line with international practices.

8

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Consolidated financial statements and first-time adoption of Ind ASIntroductionIndian Accounting Standard (Ind AS) 110, Consolidated Financial Statements, establishes principles for the preparation of Consolidated Financial Statements (CFS) when an entity controls one or more entities. It defines the principle of control, provides how to apply the principle and sets out the accounting requirements for the preparation of consolidated financial statements.

Accounting Standard (AS) 21, Consolidated Financial Statements, also sets out the framework for the preparation and presentation of CFS for a group of entities under the control of a parent. However, AS 21 does not mandate an entity to present CFS but, if the entity presents CFS for complying with the requirements of any statute or otherwise, it should prepare and present CFS in accordance with the principles given under AS 21.

This article aims to highlight important implementation issues while an entity prepares CFS for the first-time under Ind AS.

Wholly owned and partially owned subsidiaries

With regard to statutory requirement for preparing CFS, the Companies Act, 2013 (2013 Act) mandates preparation of CFS under Section 129 by all the companies, including unlisted companies, having one or more subsidiaries, joint ventures or

associates. Before the commencement of the 2013 Act, the Securities and Exchange Board of India (SEBI) required listed companies to prepare CFS.

The 2013 Act at the time of its implementation did not provide any exemption in relation to CFS, which could lead to preparation of CFS at multiple levels for companies with multi-layered structures within a group. However, the Ministry of Corporate Affairs (MCA) amended the Companies (Accounts) Rules, 2014 on 14 October 2016 and provided exemption to a company from preparation of CFS if it meets the following conditions:

i. it is a wholly-owned subsidiary, or is a partially-owned subsidiary of another company and all its other members, including those not otherwise entitled to vote, having been intimated in writing and for which the proof of delivery of such intimation is available with the company, do not object to the company not presenting consolidated financial statements,

ii. it is a company whose securities are not listed or are not in the process of listing on any stock exchange, whether in India or outside, and

iii. its ultimate or any intermediate holding company files consolidated financial statements with the Registrar of Companies (ROC) which are in compliance with the applicable Accounting Standards.

This article aims to

• Highlight key implementation issues while preparing consolidated financial statements for the first time under Ind AS

9

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

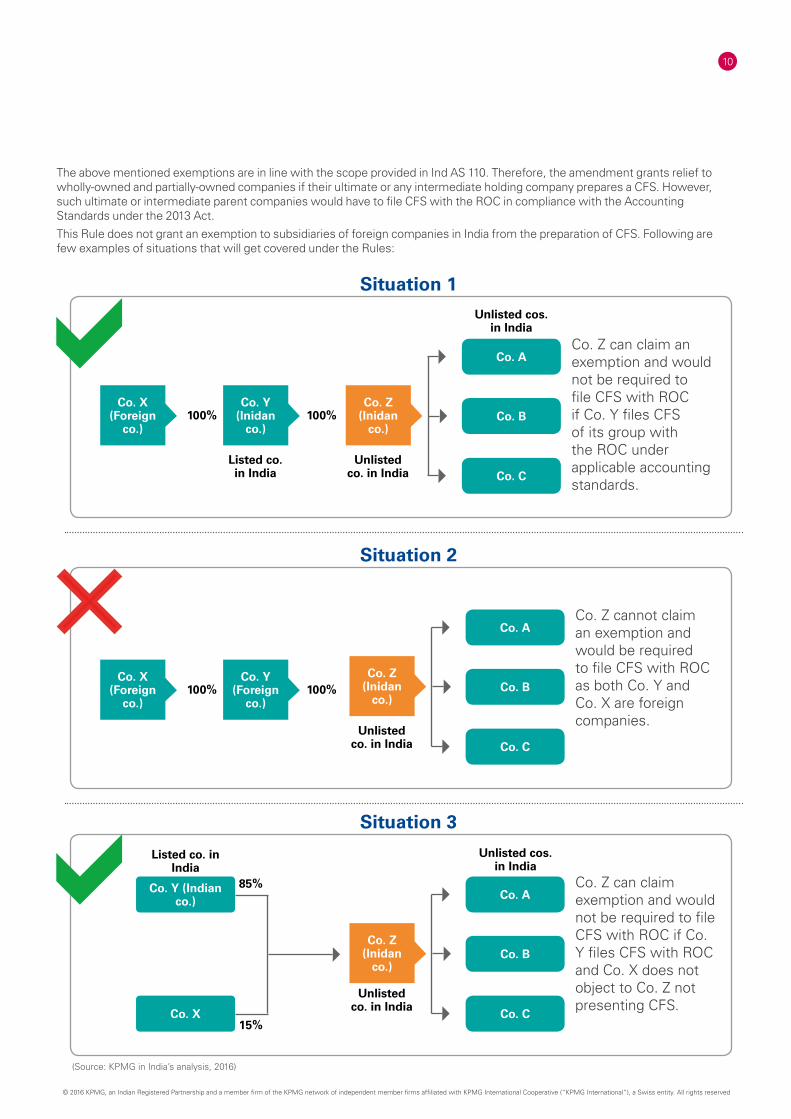

The above mentioned exemptions are in line with the scope provided in Ind AS 110. Therefore, the amendment grants relief to wholly-owned and partially-owned companies if their ultimate or any intermediate holding company prepares a CFS. However, such ultimate or intermediate parent companies would have to file CFS with the ROC in compliance with the Accounting Standards under the 2013 Act.

This Rule does not grant an exemption to subsidiaries of foreign companies in India from the preparation of CFS. Following are few examples of situations that will get covered under the Rules:

10

Situation 1

Co. X (Foreign

co.)

Co. Y (Inidan

co.)

Co. Z (Inidan

co.)

Co. A

Co. B

Co. CListed co. in India

Unlisted co. in India

Unlisted cos. in India

100% 100%

Co. Z can claim an exemption and would not be required to file CFS with ROC if Co. Y files CFS of its group with the ROC under applicable accounting standards.

(Source: KPMG in India’s analysis, 2016)

Situation 2

Co. X (Foreign

co.)

Co. Y (Foreign

co.)100%

Co. Z (Inidan

co.)

Co. A

Co. B

Co. CUnlisted

co. in India

100%

Co. Z cannot claim an exemption and would be required to file CFS with ROC as both Co. Y and Co. X are foreign companies.

Situation 3

Co. Z (Inidan

co.)

Co. ACo. Y (Indian co.)

Co. B

Co. X Co. C

Unlisted co. in India

Unlisted cos. in India

Co. Z can claim exemption and would not be required to file CFS with ROC if Co. Y files CFS with ROC and Co. X does not object to Co. Z not presenting CFS.

85%

15%

Listed co. in India

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Practical issues and perspectives

Previously unconsolidated subsidiaries

Ind AS 110 requires entities to present CFS by consolidating all its entities other than those which are specifically provided exemption under the standard. However, a first time adopter under Ind AS, may not have consolidated an entity under AS that is considered

as a subsidiary under Ind AS. Such a subsidiary may have been classified as an investment in an associate or a joint venture under AS because the definitions under AS of subsidiaries, associates and joint ventures are different from the definitions of those entities under Ind AS.

Ind AS 110 introduces a new definition of control which is wider in scope as

compared to AS 21. It provides a single control model and requires consideration of veto rights with minority shareholders, structured entities, potential voting rights, other contractual arrangements, special relationships and de facto control. The change in definition could result in more number of entities to be classified as subsidiaries under Ind AS.

Ind AS 101 provides that when a subsidiary (acquired in a past business combination) is being consolidated for the first time, the following steps are to be followed at the date of transition:

a. The first-time adopter shall adjust the carrying amounts of the subsidiary’s assets and liabilities to the amounts that Ind ASs would require in the subsidiary’s balance sheet.

b. Measure goodwill at the date of transition as the difference between:

– the parent’s interest in the amounts attributed to the assets and liabilities of the subsidiary in (a) above, and

– the cost of the investment in the subsidiary as it would be reflected in the parent’s separate financial statements.

– This calculation effectively increases goodwill by the amount of any post-acquisition losses and reduces goodwill by the amount of any post-acquisition profits.

Previously consolidated entities that are not subsidiaries

Under Ind AS, the definition of a subsidiary is not solely based on the majority voting interest or ability to control the composition of the Board of Directors (BOD), but is also influenced by the rights of the investors (as mentioned earlier). Thus, there can be a situation where a first-time adopter may have consolidated an entity that does not meet the definition of a subsidiary under Ind AS. As a result, a first-time adopter should consider all facts and circumstances when assessing whether it controls an investee and determine the appropriate classification under Ind AS.

In such a case, a previously consolidated entity can be treated as follows:• Investments in associates and

jointly controlled entities: As a result of change in definition of control, previously consolidated subsidiaries may now need to be treated as jointly controlled entities or associates under Ind AS. Each investor would account for its interest in the investee in accordance with the relevant Ind ASs, such as Ind AS 111, Joint Arrangements or Ind AS 28, Investments in Associates and Joint Ventures.

• Investment under Ind AS 109, Financial Instruments: In case if it is ascertained that the investment is neither an associate nor a jointly controlled entity then such investment should be accounted for in accordance with Ind AS 109.

For example: Company A Ltd. is a first-time adopter of Ind AS on 1 April 2016. A Ltd. acquired 49 per cent shares in company C Ltd. in 2012. B Ltd. holds 51 per cent stake in C Ltd.

A Ltd. holds the call option to acquire 31 per cent shares of B Ltd. in C Ltd.

C Ltd was not consolidated by A Ltd under AS since under AS potential voting interests in a company are not considered in the assessment of control over an entity.

On transition to Ind AS, A Ltd. evaluated the call option rights and considered them as substantive and therefore, such rights are considered in the control assessment of C Ltd. Based on this evaluation C Ltd. would be treated as a subsidiary of A Ltd. under Ind AS and, hence, would be consolidated in its Ind AS CFS.

11

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Non-controlling Interest (NCI)

NCI represents the equity in a subsidiary that is not attributable directly or indirectly to the parent. For example, if a parent owns 80 per cent of a subsidiary directly and the remaining 20 per cent is owned by a third party, then in the parent’s consolidated financial statements the 20 per cent interest held by the third party is the NCI in that subsidiary.

Ind AS 101 provides an optional exemption to a first-time adopter from applying the business combination accounting retrospectively to business combinations that occurred prior to the date of transition. If a first-time adopter opts to avail this exemption then in such a case the balance of NCI under AS is not changed other than for adjustments made as part of the transition to Ind AS.

With respect to the business combinations that are not restated, a first-time adopter should apply the following requirements of Ind AS 110, in relation to accounting for NCI, prospectively from the date of transition to Ind AS:

a. An entity should attribute the profit or loss and each component of the Other Comprehensive Income (OCI) to the owners of the parent and to the NCI, even if this results in the NCI having a deficit balance.

b. When the proportion of the equity held by owners of the parent and NCI changes (without loss of control), an entity should adjust the carrying amounts of the owners of the parent and NCI to reflect the changes in their relative interests in the subsidiary. Such transactions would be recognised directly in equity (i.e. difference between the amount by which the NCI is adjusted and the fair value of the consideration paid or received, and attribute it to the owners of the parent).

c. When there is loss of control over a subsidiary, account for it in accordance with Ind AS and related

requirements of Ind AS 105, Non-current Assets Held for Sale and Discontinued Operations.

Additionally, if a subsidiary is being consolidated for the first time, then NCI are recognised as part of the initial consolidation adjustment.

On the other hand, if a first-time adopter elects to restate past business combinations in accordance with Ind AS, then the balance of NCI related to all such restated business combinations would be determined retrospectively, taking into account the impact of other elections made as part of the adoption of Ind AS.

Consider auditing aspects of CFS

The Institute of Chartered Accountants of India (ICAI) has recently issued a Guidance Note on Consolidated Financial Statements (guidance note) (in October 2016) to help understand and resolve critical issues that might arise while auditing CFS.

The revised guidance note considers the requirements of Ind AS and provides certain important audit considerations which the auditor needs to consider while auditing the CFS prepared under Ind AS, such as:• the financial statements of the parent

and its subsidiaries are combined as per Ind AS 110, on a line by line basis by adding together like items of assets, liabilities, income, expenses and cash flows,

• related goodwill/capital reserve and NCI is determined as per Ind AS 103, Business Combinations,

• adjustments like elimination of intra group transactions, balances, unrealised profits and deferred tax, etc. are made in accordance with the requirements of Ind AS 110,

• investments in associates and joint ventures are accounted for using the equity method as prescribed in Ind AS 28. Interests in assets, liabilities, revenues and expenses in a joint

operation are accounted for as part of separate financial statements of the entity in accordance with Ind AS 111, Joint Arrangements.

Additionally, the guidance note provides that the auditor should verify that the adjustments warranted by the relevant accounting standards under the applicable financial reporting framework have been made wherever required and have been properly approved by the management of the parent. The preparation of CFS gives rise to permanent consolidation adjustments and current period consolidation adjustments. No adjustments, other than those envisaged in the guidance note, should be carried out in the preparation of CFS at the group level.

12

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Consider this….

Change in definition of control: Ind AS 110 introduces a new definition of control which is wider in scope as compared to AS 21. It provides a single control model as per which an investor controls an investee when the investor is exposed, or has rights, to variable returns from its involvement with the investee, and has the ability to affect those returns through its power over the investee.

Ind AS 110 introduces new terms as compared to the current Indian GAAP such as de facto control, delegated power and structured entities.

Uniform accounting policies and date of financial statements: Under Ind AS, when preparing consolidated financial statements, an entity must use uniform accounting policies and there is no impracticability exemption similar to AS 21.

Additionally, under Ind AS the financial statements of the parent and its subsidiary are prepared for the same reporting period. To achieve this, if the entities have different reporting periods, then additional financial statements of the subsidiary are prepared as at the parent’s reporting date unless it is impracticable to do so. In any case, the difference between the year end of the parent and subsidiary cannot be greater than three months and adjustments are required to be made for the effects of significant transactions and events in that period.

Dilution of the parent’s ownership interest: Under Ind AS, changes in the parent’s ownership interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions (transactions between shareholders). Accordingly, if a parent sells a portion of the shares in a subsidiary, but there is no loss of control, no gain or loss should be recognised in the consolidated statement of profit and loss. However, if there is loss of control, realised gains or losses are recognised in the statement of profit and loss. Further, in such cases, any retained investment is recognised at fair value, with the differential being recognised in the statement of profit and loss.

ConclusionThe implementation of this standard requires the management to exercise significant judgement to determine which entities are controlled, and therefore, are required to be consolidated by a parent. With the application of the new requirements

under Ind AS 110, the current structures may be modified and companies may be required to consolidate additional entities based on revised group structures. In addition, some of the existing consolidated entities may get deconsolidated. Companies should

consider all the facts and circumstances and revised guidance while arriving at appropriate conclusion. This is likely to be a high impact standard for companies that have complex holding structures and operate through special purpose vehicles/structured entities.

13

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Accounting for low-interest and interest-free loansInd AS 109, Financial Instruments requires all financial instruments to be recognised initially at their fair value, which is normally the transaction price. However, an entity may sometimes receive or give interest-free or low interest loans, e.g. inter-company loans received from parent/group entities, government loans or tax deferral schemes, subsidised loans to staff, etc.

To determine the fair value of such low-interest or interest-free loans, an entity should first assess whether the interest charged on the loan is at a below-market

rate based on the terms and conditions of the loan, local industry practice and local market circumstances. The fair value of such loans is then determined in accordance with Ind AS 113, Fair Value Measurement.

In this article, we analyse four types of financial instruments to determine if these are in the nature of low-interest or interest-free loans and analyse the appropriate recognition and measurement requirements under Ind AS.

Key characteristics of the financial instruments

M Private Limited (the entity/company), operates in the industrial manufacturing sector and has entered into the following types of transactions during the quarter ended 30 September 2016.

Table 1: Key characteristics of the financial instruments

Particulars Amount (in INR) Additional information

Deferred sales tax liability (unsecured) 90,000,000 This represents the sales tax liability of the company for sales made during the quarter ended 30 September 2016. The company is covered under a sales tax deferral scheme which permits the company to pay its quarterly sales tax liability after a period of 10 years from the end of the quarter, with no interest being charged to the company during this term. The company is eligible for this scheme due to the nature of capital investment made by the company. The company would be able to borrow funds for a similar amount and term at an interest rate of 15 per cent per annum.

Unsecured, interest free loan received from ABC Private Limited on 1 August 2016 (immediate holding company of M Private Limited). There are no stated terms of repayment. However, M Private Limited is expected to repay the loan from funds generated from its business.

200,000,000 Market rate for a short-term loan, repayable on demand, is 11.5 per cent per annum.

This article aims to

• Provide an overview of the recognition and measurement requirements for low-interest and interest-free loans

15

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Accounting issue

Ind AS 109 requires all financial instruments to be initially recognised at their fair value. As mentioned earlier, this is normally evidenced by the transaction price. However, M Private Limited is required to identify loans that may be interest-free or low interest in nature and determine their fair value in accordance with Ind AS 113 on initial recognition.

The company is also required to determine if the difference between the amount lent/borrowed and the fair value qualifies for recognition as an asset or liability or whether it should be recognised as a gain or loss.

Accounting guidance

Figure 1 illustrates the applicable guidance in Ind AS 109 for measuring financial instruments at fair value on initial recognition.

Source: KPMG in India’s analysis 2016

Source: KPMG’s Insights into IFRS 13th edition 2016-17 and KPMG in India’s analysis 2016

Key terms of the loans received and given Amount (in INR) Additional information

The company has extended an unsecured loan on 1 July 2016 (under its staff policies) to an employee at a nominal interest rate of 2 per cent per annum. This loan will be repayable over a period of 3 years (in equal instalments) or when the employee leaves the organisation, whichever is earlier.

600,000 The employee would be able to obtain a similar loan at a market rate of 14 per cent per annum.

The company has extended a loan to its subsidiary, XYZ Private Limited on 30 September 2016 at an interest rate of 5 per cent per annum. The loan is repayable after 5 years.

100,000,000 Unsecured loan of the same denomination, for the same period and at same terms would be extended by banks to XYZ Private Limited at an interest rate of 13 per cent per annum.

Does the transaction price represent fair value, i.e. is the interest charged at market rates?

Bifurcate the transaction price into two components

Fair value of the loan (within scope of Ind AS 109)

‘Other component’ (gain or loss unless it qualifies for recognition as an asset or liability)

Determine fair value under Ind AS 113

‘Other component’ recognised under relevant standard (based on relationship between borrower and lender)

Classification and subsequent measurement under Ind AS 109

Recognise loan at the transaction price

No

Yes

16

Table 1: Key characteristics of the financial instruments

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

In determining whether a loan is offered at a below-market rate, the company should consider the following aspects:• All the terms and conditions of the

loan• Local market circumstances and the

industry practice• Interest rates currently charged by

or offered to the entity for loans with similar risks and characteristics.

Ind AS 113 defines fair value as ‘the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date’. In determining fair value, Ind AS 113 requires an entity to maximise the use of quoted prices or other relevant

observable inputs. However, if these are not available, a valuation technique may also be used, such as a present value technique with inputs that include future cash flows and discount rates that reflect assumptions that market participants would apply in pricing the financial instrument.

Ind AS 109 requires the difference between the transaction price and the fair value of a low-interest or interest-free loan to be recognised as a gain or loss (if the fair value is based on observable inputs), unless it qualifies for recognition as an asset or liability. This normally depends on the relationship between the lender and borrower or the reason for providing the loan.

Analysis

The loans received and given by M Private Limited in the illustration above would be considered as below market since they are not at market rates that would apply to a normal commercial arrangement between market participants.

Table 2 below summarises the accounting and measurement requirements for the low-interest/interest-free loans borrowed and lent by the company, based on the guidance above.

The following is an analysis of each of the financial instruments mentioned in the table above.

Deferred sales tax liability

The deferred sales tax liability is an incentive received by the company from the government under a sales tax deferral scheme. Since the loan is interest-free in nature, its face value or the transaction price is not considered to represent fair value. Therefore, the company is required to determine the fair value based on the guidance in Ind AS 113.

The company considers that the use of a present value technique based on the cash flows payable under the

scheme is an appropriate method of determining fair value. In order to determine the discount rate to be used, the company is required to assess the interest rate based on assumptions that market participants would use to price a liability with similar terms, risk exposures and characteristics as this loan. For the purpose of this illustration, this rate is determined on the basis of the company’s incremental borrowing rate (i.e. the rate at which the company would be able to borrow funds on similar terms from market participants in an arms’ length transaction) as 15 per cent per annum.

Using this rate to discount the cash flows payable by the company under

the sales tax deferral scheme, the fair value of the liability on 30 September 2016 is determined as INR22,229,593. The difference between the fair value of the loan and the amount payable is INR67,770,407. This represents the ‘other component’ which is considered to be in the nature of a government grant since it represents an incentive received by the company from the government. This should be accounted for in accordance with Ind AS 20, Accounting for Government Grants based on the terms of the scheme applicable to the company, and may be either deferred and amortised to the statement of profit and loss over the period of the sales tax deferral loan or recognised up front, if appropriate.

Particulars

Borrowings Loans given

Deferred sales tax liability Loan taken from holding company

Employee loans Loan extended to subsidiary

Face amount of the loan (in INR) 90,000,000 200,000,000 600,000 100,000,000

Approximate fair value of the loan initially recognised as per Ind AS 109 (in INR)

22,229,593 200,000,000 483,708 71,842,044

The ‘other than market terms’ element of the loan

67,770,407 NIL 116,292 28,157,956

Nature of the ‘other than market terms’ element of the loan recognised by the company

Government grant N.A. Employee benefit expense Investment in subsidiary

Source: KPMG in India’s analysis 2016

17

Table 2: Summarised analysis of the loans given and received

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The company would have to accrue interest expense on the loan liability at the effective interest rate (being the discount rate used to determine initial fair value) over the term of the sales tax deferral loan.

Loan from parent

The unsecured loan received by the company from its parent, ABC Private Limited, is also in the nature of an interest-free loan and should be recognised initially at its fair value. This loan has no fixed contractual cash flows or stated repayment terms. In order to determine the appropriate recognition and measurement requirements for this loan, the company may consider various factors, including whether:• Classification as a liability is

appropriate, i.e. whether there is a contractual obligation,

• There is any agreed means of repayment specified in the loan agreement or in a side agreement, or

• It is possible to estimate the timing of the loan repayments.

For the purpose of this illustration, the company is expected to repay this loan from available funds that are internally generated from its business. This indicates that the company has an obligation to repay this loan even though there is no specific repayment date, and it may be appropriately classified as a financial liability.

Since it is not practicable to estimate the timing of repayment of this loan (although the company is expected to have sufficient funds for repayment), this liability could be considered as repayable on demand by the lender, i.e. the parent company. In this scenario, Ind AS 113 states that ‘the fair value of a financial liability with a demand feature is not less than the amount payable on demand, discounted from the first date that the amount could be required to be paid.’ Assuming that this loan is considered as repayable on demand at any time, no discounting would be required on initial recognition.

Accordingly, the loan from the parent company would be measured by M Private Limited at its face value, which is also its fair value.

However, a detailed analysis would be required on initial recognition to ascertain all the facts and circumstances related to this type of a loan to determine the expected repayment terms and the appropriate accounting treatment, including the need for discounting, if any. For example, if the loan has no fixed maturity date and is available in perpetuity, then its fair value would be measured by applying a present value/discounting technique that considered these terms.

Unsecured loan to employee

The staff loan provided to an employee under the company’s policies is a low-interest loan that should be measured at its fair value on initial recognition. The use of a present value technique is considered as an appropriate method for determining fair value by the company.

As mentioned above, the discount rate is determined based on the guidance in Ind AS 113 using assumptions that market participants would use to price a financial asset with similar terms and characteristics. In this illustration, the discount rate is determined as 14 per cent per annum on the basis of the rate at which the employee would be able to obtain a similar loan from independent market participants.

Using this rate to discount the cash flows receivable by the company, the fair value of the loan asset on 1 July 2016 (date of initial recognition) is determined as INR483,708. The difference between the fair value of the loan and the amount lent, i.e. the ‘other component’ is INR116,292. This would be considered as an employee benefit provided by the company and should be generally recognised as an expense over the term of the loan.

The loan asset would generally be classified as measured at amortised cost and the company would be required to accrue interest income at the effective interest rate (i.e. the discount rate used to determine fair value) over the term of the loan.

Loan to subsidiary

The 5 per cent, unsecured loan given by the company to its subsidiary is a low-interest loan that should be measured at fair value on initial recognition. The fair value is determined in a manner similar to that described above, using a present value technique. The appropriate discount rate is estimated as 13 per cent per annum, being the incremental borrowing rate of the subsidiary, XYZ Private Limited, i.e. the rate at which market participants would price a financial asset with similar terms and risk characteristics.

Using this discount rate, the fair value of the loan to the subsidiary is determined as INR71,842,044 on initial recognition as on 30 September 2016. The loan was provided by the company in its capacity as the major shareholder of XYZ Private Limited. Therefore, the difference of INR28,157,956 between the fair value and the amount lent, may be considered as an additional equity contribution by the company to its subsidiary. Accordingly, this amount would be recognised as an additional investment in the subsidiary in the separate financial statements of the company at the time of initial recognition of the loan.

The loan asset would generally be classified into the amortised cost category and the company would be required to subsequently accrue interest income at the effective interest rate (i.e. unwind the discount) over the five-year term of the loan

18

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Consider this….

• The measurement of fair value of a loan repayable on demand by the lender would be based on the perspective of an independent market participant acting in its economic best interest. Accordingly, the lender may also measure such a loan at its face value, being the amount repayable on demand.

• In the absence of stated repayment terms for an interest-free/low-interest loan between group companies, entities are required to apply judgement to determine if a loan may be classified as a financial liability or an equity instrument of the borrower. For example, a loan that is not repayable in perpetuity, where the borrower does not have access to any means of repayment, or repayment is at the discretion of the borrower, may not qualify for classification as a financial liability. A detailed analysis of the facts and circumstances surrounding the grant of the loan would be required in this scenario to determine the appropriate classification as well as measurement for the loan.

• On fair valuation of an interest-free loan from a parent to a subsidiary, the ‘other component’ being the difference between the fair value and the face value of the loan may be considered as an equity infusion by the parent. Conversely, the difference between fair value and face value of an interest-free loan provided by a subsidiary to its parent, could be considered as a distribution/return of capital by the subsidiary to the parent entity, based on an analysis of relevant facts and circumstances.

19

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

20

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Regulatory updatesInd AS Transition Facilitation Group (ITFG) issues Clarification Bulletin 6With Indian Accounting Standards (Ind AS) being applicable to large corporates from 1 April 2016, the Institute of Chartered Accountants of India (ICAI) on 11 January 2016 announced the formation of the Ind AS Transition Facilitation Group (ITFG) in order to provide clarifications on issues arising due to applicability and/or implementation of Ind AS under the Companies (Indian Accounting Standards) Rules, 2015 (Ind AS Rules, 2015).

Earlier this year, ITFG issued five bulletins to provide guidance on issues relating to the application of Ind AS.

New developmentThe ITFG held its sixth meeting and issued its bulletin (Bulletin 6) on 29 November 2016 to provide clarifications on four issues in relation to the application of Ind AS, as considered in its meeting.

Overview of the clarification in ITFG’s Bulletin 6

The following issues relating to the applicability of Ind AS have been clarified in this bulletin: • Period for calculation of net worth for

applicability of Ind AS

• Associate companies covered under Section 8 of the Companies Act, 2013

• Date of applicability of Ind AS for an unlisted NBFC and its subsidiary

• Inclusion of capital reserve for computation of net worth

1. Period for calculation of net worth for applicability of Ind AS As per Rule 4(2) of the Ind AS Rules, 2015, net worth for determining the applicability of Ind AS should be calculated in accordance with the stand-alone financial statements of the company as on 31 March 2014 or the first audited financial statements for an accounting period which ends after that date. However, net worth for companies which were not in existence as on 31 March 2014 should be calculated on the basis of the first audited financial statements ending after that date, in respect of which it meets the threshold specified for Ind AS applicability.

21

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The ITFG considered a situation where a company meets the net worth criteria on 31 March 2014 but the net worth falls below the specified threshold on later reporting dates. Based on the above guidance, ITFG has clarified that the net worth of a company should be calculated in accordance with the stand-alone financial statements of the company as on 31 March 2014. Once a company meets the net worth threshold criteria it is then required to comply with the Ind AS road map, irrespective of the fact that its net worth falls below the criteria specified at a later date.

The ITFG in its Bulletin 3 issued on 2 July 2016 provided guidance with respect to the listing criteria for Ind AS applicability. In Bulletin 3 ITFG stated that if a company ceases to meet the listing criteria in the Ind AS road map, immediately before the mandatory Ind AS application date, then it would not be required to comply with Ind AS even if it met the criteria on a prior date. However, ITFG has clarified in Bulletin 6 that this guidance (given in Bulletin 3) applies only to the listing criteria and not the net worth criteria.

2. Associate companies covered under Section 8 of the Companies Act, 2013 (2013 Act) As per Rule 4(1)(ii) of the Ind AS Rules, 2015, the following companies are required to comply with Ind AS from accounting periods beginning on or after 1 April 2016 (FY2016-17) with comparatives for the period ending 31 March 2016:

a. whose equity or debt securities are listed or are in the process of being listed on any stock exchange in India or outside India and having net worth of INR500 crore or more

b. other than those covered in (a) above and having net worth of INR500 crore or more

c. holding, subsidiary, joint venture or associate companies of companies covered under (a) or (b) above, as the case may be.

The ITFG considered a situation where an associate of a company covered under Phase I (Ind AS

applicable from FY2016-17) of the Ind AS road map is a charitable organisation registered under Section 8 of the 2013 Act. In accordance with the above guidance, ITFG clarified that Section 8 companies are also required to comply with the provisions of the 2013 Act unless any exemption is specifically provided. Additionally, Section 8 companies are not exempt from the requirements of Sections 133 and 129 of the 2013 Act. Therefore, such an associate company (covered under Section 8) is also required to comply with Ind AS from FY2016-17 onwards.

3. Date of applicability of Ind AS for an unlisted NBFC and its subsidiary As per Rule 4(1)(iv)(b) of Ind AS Rules, 2015, NBFCs with net worth less than INR500 crore are required to apply Ind AS from 1 April 2019. Further, the holding, subsidiary, joint venture or associate company of such an Non-Banking Financial Company (NBFC), other than those covered by the corporate Ind AS road map are also required to apply Ind AS from 1 April 2019 onwards.

NBFC and group companies with different Ind AS adoption dates

The ITFG considered a scenario where a subsidiary of an NBFC falling within Phase II of the corporate road map, is required to comply with Ind AS from 1 April 2017 onwards, but the NBFC parent is required to implement Ind AS from 1 April 2019 onwards. In this context, the ITFG clarified that in accordance with the explanation to Rule 4(1)(iv) the subsidiary would be required to provide relevant financial statement data in accordance with:• NBFC parent’s accounting policies:

for preparation of consolidated financial statements under the Companies (Accounting Standards) Rules, 2006, and

• Ind AS in its individual financial statements: from the accounting period commencing 1 April 2017 onwards.

22

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

This requirement is illustrated in the table below (on the basis that the NBFC parent falls within Phase II of the NBFC road map):

NBFC parent with a subsidiary within Ind AS road map (Phase II)

NBFC subsidiary with parent entity within Ind AS road map (Phase I)

In situations where a parent entity that falls within the corporate Ind AS road map has an NBFC subsidiary, associate or joint venture, the NBFC would be required to provide relevant financial statement data in accordance with the Ind AS policies followed by the parent for consolidation purposes. This requirement is illustrated below (assuming that the parent entity falls within Phase I of the corporate road map and the NBFC falls within Phase I of the NBFC road map):

Financial year NBFC parent Subsidiary/associate/joint venture

Stand-alone Consolidated Stand-alone For consolidation

2017-18 Indian GAAP Indian GAAP Ind AS Indian GAAP

2018-19 Indian GAAP Indian GAAP Ind AS Indian GAAP

2019-20 Ind AS Ind AS Ind AS Ind AS

Financial year NBFC subsidiary/associate/joint venture Parent company

Stand-alone For consolidation Stand-alone Consolidated

2016-17 Indian GAAP Ind AS Ind AS Ind AS

2017-18 Indian GAAP Ind AS Ind AS Ind AS

2018-19 Ind AS Ind AS Ind AS Ind AS

4. Inclusion of capital reserve for computation of net worth As per Section 2(57) of the 2013 Act, ‘net worth’ means the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet but does not include the following:a. Reserves created out of

revaluation of assets

b. Write-back of depreciation, and

c. Write-back of amalgamation.

The ITFG considered a situation where a company has received a government grant in the nature of promoter’s contribution and included this in the capital reserve. The amount of grant was accounted as per AS 12, Accounting for Government Grants.

Based on the above definition, the ITFG has clarified that the capital reserve in the nature of promoter’s contribution is a capital contribution by promoters. Further, AS 12 also states that government grants in the nature of promoter’s contribution should be recognised in the shareholders’ funds. Therefore, in this context, the capital reserve should

be included in the computation of net worth. However, such an amount should be included only for the purpose of determining Ind AS applicability based on the net worth criteria and should not be applied by analogy for determining net worth under other provisions of the 2013 Act.(Source: ITFG Bulletin 6 issued by ICAI and KPMG in India’s IFRS Notes dated 2 December 2016)

23

© 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

MCA notifies amendment to Schedule II of Companies Act, 2013