Critical Perspectives on Accounting 23 (2012) 213–229 Contents lists available at SciVerse ScienceDirect Critical Perspectives on Accounting journa l h o me pa g e: www.elsevier.com/locate/cpa Accountability and corporate governance of public private partnerships Jean Shaoul, Anne Stafford, Pamela Stapleton ∗ Manchester Business School, University of Manchester, Manchester, UK a r t i c l e i n f o Article history: Received 21 August 2009 Received in revised form 30 September 2011 Accepted 1 November 2011 Keywords: PPPs Accountability Corporate governance Future research agenda a b s t r a c t Brennan and Solomon (2008) identify six new frontiers in accountability and corporate gov- ernance research to stimulate research. This paper contributes to such research by devising a reporting framework and research agenda that relates to Brennan and Solomon’s fourth frontier, sectors and context, focusing on the regulated hybrid organisational forms of Public Private Partnerships, which operate at the interface of the public and private sectors. As the framework shows, these organisations are subject to multiple influences and demands. There is a need for more and different reporting than is the norm under the private sector’s decision-useful reporting framework. Although the framework focuses on what Mulgan (2000) describes as the core of accountability, it is not only a financial reporting framework but it also seeks to make concrete Kamuf’s (2007) argument that accountability might include accounting through narrative as well as the prevailing numeric evaluation. The paper stresses the need for information to be accessible to the public, and in par- ticular argues that a stream of information between the public and private sector partners needs to be developed and disseminated to achieve accountability for public money that is increasingly spent in the private sector. © 2012 Elsevier Ltd. All rights reserved. 1. Introduction Brennan and Solomon (2008) identify six new frontiers to corporate governance and accountability research that are extending such research beyond the traditional and primarily quantitative approaches of prior research based pre- dominantly on agency theory. These authors seek thereby to stimulate the development of new approaches, using new theoretical perspectives and methodological approaches that examine new and different accountability mechanisms, sectors or contexts and timeframes. This paper pursues Brennan and Solomon’s fourth frontier of corporate governance and accountability research: sec- tors and context. They note that accounting and finance research in this area has largely focused on the corporate sector, particularly listed companies, sidelining the direction and control of other types of organisations, particularly the public sector, although they do not identify the interface between the public and private sectors. This paper therefore examines the potential for corporate governance and accountability research in organisations that have been shaped by explicit public policy and regulation as part of New Public Management (NPM) reforms; the ‘regulated hybrids’ (Miller et al., 2008, p. 85). Internationally, NPM reforms have sought to reduce the scale and scope of the public sector in various ways. One objec- tive has been to encourage the involvement of the private sector in managing and delivering infrastructure and services, ∗ Corresponding author at: Accounting and Finance Division, Crawford House, Manchester Business School, University of Manchester, Manchester M15 6PB, UK. E-mail address: [email protected] (P. Stapleton). 1045-2354/$ – see front matter © 2012 Elsevier Ltd. All rights reserved. doi:10.1016/j.cpa.2011.12.006

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ap

JM

a

ARR3A

KPACF

1

adto

tpstp

t

6

1d

Critical Perspectives on Accounting 23 (2012) 213– 229

Contents lists available at SciVerse ScienceDirect

Critical Perspectives on Accounting

journa l h o me pa g e: www.elsev ier .com/ locate /cpa

ccountability and corporate governance of public privateartnerships

ean Shaoul, Anne Stafford, Pamela Stapleton ∗

anchester Business School, University of Manchester, Manchester, UK

r t i c l e i n f o

rticle history:eceived 21 August 2009eceived in revised form0 September 2011ccepted 1 November 2011

eywords:PPsccountabilityorporate governanceuture research agenda

a b s t r a c t

Brennan and Solomon (2008) identify six new frontiers in accountability and corporate gov-ernance research to stimulate research. This paper contributes to such research by devisinga reporting framework and research agenda that relates to Brennan and Solomon’s fourthfrontier, sectors and context, focusing on the regulated hybrid organisational forms of PublicPrivate Partnerships, which operate at the interface of the public and private sectors.

As the framework shows, these organisations are subject to multiple influences anddemands. There is a need for more and different reporting than is the norm under the privatesector’s decision-useful reporting framework. Although the framework focuses on whatMulgan (2000) describes as the core of accountability, it is not only a financial reportingframework but it also seeks to make concrete Kamuf’s (2007) argument that accountabilitymight include accounting through narrative as well as the prevailing numeric evaluation.

The paper stresses the need for information to be accessible to the public, and in par-ticular argues that a stream of information between the public and private sector partnersneeds to be developed and disseminated to achieve accountability for public money that isincreasingly spent in the private sector.

© 2012 Elsevier Ltd. All rights reserved.

. Introduction

Brennan and Solomon (2008) identify six new frontiers to corporate governance and accountability research thatre extending such research beyond the traditional and primarily quantitative approaches of prior research based pre-ominantly on agency theory. These authors seek thereby to stimulate the development of new approaches, using newheoretical perspectives and methodological approaches that examine new and different accountability mechanisms, sectorsr contexts and timeframes.

This paper pursues Brennan and Solomon’s fourth frontier of corporate governance and accountability research: sec-ors and context. They note that accounting and finance research in this area has largely focused on the corporate sector,articularly listed companies, sidelining the direction and control of other types of organisations, particularly the publicector, although they do not identify the interface between the public and private sectors. This paper therefore examines

he potential for corporate governance and accountability research in organisations that have been shaped by explicit publicolicy and regulation as part of New Public Management (NPM) reforms; the ‘regulated hybrids’ (Miller et al., 2008, p. 85).Internationally, NPM reforms have sought to reduce the scale and scope of the public sector in various ways. One objec-ive has been to encourage the involvement of the private sector in managing and delivering infrastructure and services,

∗ Corresponding author at: Accounting and Finance Division, Crawford House, Manchester Business School, University of Manchester, Manchester M15PB, UK.

E-mail address: [email protected] (P. Stapleton).

045-2354/$ – see front matter © 2012 Elsevier Ltd. All rights reserved.oi:10.1016/j.cpa.2011.12.006

214 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

previously the exclusive preserve of the public sector. In this context, the PPP has emerged as a hybrid with organisationalstructures that use resources from previously separate public and private entities. These increasingly popular hybrid formsof organisation are designed for risk sharing and co-production between government and private agents (Skelcher, 2005),and they have reformed and transformed the provision of services. The PPP concept encompasses a wide range of differentarrangements or as Hodge and Greve (2007) describe it, at least five families of arrangements, some of which are purelyeconomic arrangements, while others seek to learn new ways of producing and delivering services and sharing risks andrewards (Hodge and Greve, 2005). In this paper, we focus on PPPs that exhibit three key elements.

Firstly, they involve clearly defined projects, the risks and rewards of which are shared between the public and privatesectors. That is, usually a long-term relationship between a public sector procurer and multiple private sector companiesexists to design and construct infrastructure, maintain it and provide some related services. Compared with traditionalmodes of procurement, PPPs represent highly complex contractualisations of bundled infrastructure arrangements (Hodgeand Greve, 2007), which transform the public sector from provider to purchaser. The public sector and the companies thatprovide the various contractual services must manage their relationships over the long-term.

Secondly, the projects have decision-making, construction, operation and termination stages during which different typesof information are needed for public accountability purposes. Thirdly, a bank or financial institution provides private financefor projects that traditionally have been publicly financed.

This partnership policy transforms the nature of service provision. Whereas previously, the state exercised coordinationand steering through hierarchy, bureaucracy and detailed regulation, the PPP ‘regulated hybrid’ creates governance throughnetworks based on interdependence, negotiation and trust among a number of public and private actors (Bevir, 2004;Sørensen and Torfing, 2005). The aspiration is for a hybridising of expertise, modes of working and modes of deliveringservices (Miller et al., 2008).

However, one implication of this transformation is that much public expenditure is now outside direct state control.This raises questions about whether the system of public expenditure reporting and disclosure can deliver accountabilityfor public monies and services (Skelcher, 2005), especially in the context of hybrid organisational forms, where there arealtered corporate governance and accountability assumptions and arrangements (Hodge and Greve, 2007). In these hybrids,where there is blurring of the boundary between the public and private sectors, private sector corporate governance whichis focused on the relationship between a for-profit organisation and its shareholders, has intruded into a well established,although changing, public sector accountability regime. The public sector accountability regime, which recognises multiplestakeholders, has sometimes been categorised into two aspects which we explain further below: an upward accountabilitythrough public sector hierarchies and processes to Parliament and a downward accountability to citizens. The researchapproach in this paper is to explore the problematical interrelationships between downward accountability to citizens andprivate sector corporate governance within the setting of PPPs.

While accountability may have wide ranging meanings and may be achieved in many different ways, this paper focuses ontransparency and the information disclosures that are needed to achieve accountability to citizens, and in particular the roleof financial reporting in providing relevant information. While there has been an increased awareness of the role of annualreporting in discharging accountability obligations (Ryan et al., 2002), there is little accounting literature that examines howaccountability can be, or is, delivered by means of financial reporting and disclosure in relation to hybrid organisations.

The paper has three research questions. Firstly, from corporate governance and public accountability perspectives whatare the significant influences over and demands upon the hybrid organisational structure? Secondly, what is the role offinancial reporting and corporate governance disclosure in delivering accountability to citizens within this complex organ-isational form? Thirdly, what questions does this organisational form raise about corporate governance and accountabilityfor accounting researchers?

In order to answer the first two questions, the paper devises a reporting framework based on relevant literature, whichincludes the influences over and demands upon these organisations from both the public and private sector traditions.Although, PPPs have been widely adopted internationally using a range of organisational structures, we use a British variant– the Private Finance Initiative (PFI) – as an exemplar of the corporate governance and accountability environment of these‘regulated hybrid’ organisational structures. Since Britain’s PFI model1 was one of the earliest forms of PPP, there is now aconsiderable body of directly relevant PFI literature to draw upon to create our framework.

The framework develops the work of Smith et al. (2006), discussed further below, who argue that corporate governanceand accountability are multi-faceted concepts in the public sector, but they draw attention to the democratic deficit exhibitedby partnership arrangements in relation to citizens. Although corporate governance is usually explained in terms of directingand controlling entities, in reality it may encompass the way in which various stakeholders interact with one another(Hyndman and McDonnell, 2009). Thus, the framework recognises that reporting by hybrid partnerships must address

multiple information needs, if it is to play a role in achieving both the objectives of private sector corporate governance andpublic sector accountability, especially the downward accountability to citizens. From this framework, the paper draws out1 A PFI project is a contractual arrangement between a public authority and a private sector special purpose vehicle (SPV) in which the public sector bodydepends on the SPV to provide finance and capital for infrastructure, as well as constructing the assets and providing some maintenance and operationalservices.

ar

stbfin

alpsp(totis

racb

paosts

osnafs

2

ad‘wgs

ra

2

ivqfg

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 215

research agenda specifically for accounting researchers, in order to answer the third question. Both the framework andesearch agenda recognise explicitly that two regimes, each with different reporting needs, co-exist, possibly in competition.

The paper argues that firstly, a distinction needs to be drawn between corporate governance in the private and publicectors. In the former sector, where the corporate governance tradition is very narrowly focused, there has been an attempto either limit information asymmetries or specify information flows between some central players (Hood, 2006), normallyy means of disclosure in financial statements. The regulators’ intention is that better quality information, especially of anancial nature, enables shareholders to make better-informed investment decisions. In recent times, this practice has in aumber of countries been transferred to the public sector, where its relevance may be questioned.

Secondly, this financially focused private sector corporate governance tradition meets an alternative tradition of publicccountability in Westminster-style government processes that is so broadly based that it has been described as a chameleon-ike term attached to a wide range of causes and agendas (Dubnick and Justice, 2006). Nevertheless, it is an establishedrinciple that citizens, or at least their representatives, can see how society’s resources are used and that no members ofociety have an explicitly sanctioned unfair advantage over others in relation to how those resources are spent. While theurpose of this accountability tradition is less clear-cut, we are adopting an ethical perspective in relation to stakeholdersDeegan and Unerman, 2011, p. 349). That is, we adopt a normative position that citizens have certain rights, includinghe right to information, about how they should be treated by an organisation regardless of their role in relation to thatrganisation. At a minimum, even if this has not occurred previously under public sector reporting, information should beransferred so that the parties to whom an organisation is accountable can compel it to adjust its behaviour on the basis ofnformation provided (Hyndman and McDonnell, 2009). Financial reporting, while not the only possible source, is a majorource of such information.

Thirdly, the corporate governance structures of the private sector are fundamentally different to those of the public sector,aising questions about the nature of accountability in these hybrid organisations. For example, the procedural regularitynd transparency that informs the normative practice of government is tested by private actors with their conventions ofommercial confidence in pursuit of competitive advantage, because confidentiality is as much part of the core value set ofusiness as transparency is allegedly that of government (Skelcher, 2005).

Fourthly, the context of hybrid organisations offers a challenging arena in which to develop new approaches to cor-orate governance research, because the realities of the new public sector have exposed an accountability gap betweenccountability doctrine, conventions and reality and a need for hybrid models of accountability (Sands, 2006). In hybridrganisational structures where the boundaries between the public and private sector are blurred, there are three separateets of demands variously impacting on the network of organisations. These demands emanate from traditional private sec-or corporate governance, from corporate governance as it has transferred to the public sector, and from traditional publicector accountability, albeit an accountability that has changed as the public sector has been reformed.

The paper is organised into five further sections. The next (second) section briefly examines the contextual environmentf PFIs, in terms of their reporting, public accountability and corporate governance. It examines both the public and privateector contexts since both affect the hybrid PPP type organisation. The third section demonstrates that PFIs represent aew and special accountability case, because of the role of private finance, the relationships between the multiple entities,nd the payment mechanism, which relies on performance measurement systems controlled by the private sector. Theourth section develops an accountability-based reporting framework the work of Smith et al. (2006). A fifth section sets outuggestions for future research based on this framework. The final section makes some brief concluding remarks.

. The reporting, accountability and corporate governance context

The definition and nature of accountability has changed over time. Traditionally, in its simplest form, accountability entails relationship whereby some people are required by others to explain and take responsibility for their actions: “giving andemanding reasons for conduct” (Roberts and Scapens, 1985, p. 447). It focuses on ‘who’ is to be accountable to ‘whom’ and

for what’. But it has changed beyond its core sense of being called to account for one’s actions (Mulgan, 2000) in such aay that it may have become a garbage can filled with good intentions loosely defined concepts and vague images of good

overnance (Bovens, 2005). Accountability has become multi-faceted, involving account giving, holding to account but alsoitting in judgement and applying sanctions, and being responsive to citizens.

Hybrid organisations are subject to influences and demands from the traditions of both sectors. We now examine theireporting context in the UK, focusing on the changes that the NPM agenda has created in terms of the changing notions ofccountability in the public sector and the transfer of private sector corporate governance norms into the public sector.

.1. Public sector context

A number of commentators have identified various aspects or features of accountability in the public sector. Bovens (2005)dentifies three elements or stages to account giving: first, an obligation felt by an account-giver to inform by providing

arious data about performance, outcomes or procedures; second, an account-receiver is prompted by this information touestion the account-giver; and third, the account-receiver is able to pass judgement and may impose sanctions, whetherormal or informal. Accountability is said to have three aspects: first, compliance, being held to account; second, transparency,iving an account; and third, responsiveness, taking account (AccountAbility, 2004). Mulgan (2000) notes three features:

216 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

accountability is external to the account-giver, involves social interaction and exchange, and implies rights of authority.Bovens (2005) identifies five elements: that accountability is public not internal; involves explanation and justification notpropaganda; is specifically directed at a target audience not a random explanation; involves an obligation on actors to comeforward to be accountable; resulting in debate and judgement not a monologue without engagement.

Accountability has adopted many forms as it slowly struggled out of its etymological bondage with accounting (Bovens,2005). These include the interconnected accountability systems of communal, contractual, managerial and parliamentaryaccountabilities (Demirag et al., 2004). Furthermore, Dubnick (2007) explores four types, or as he labels them orders ofaccountability. Firstly, performative accountability: explicit and direct acts of account giving such as the annual accountsthat are responses to a direct, possibly implied, solicitation from real or potential account-receivers. The assumption isthat such explicit acts provide the necessary information to hold the account-giver to account. But the nature and value ofinformation has been questioned in practice. Kamuf (2007) argues that although accountability might include accountingfor something through narrative this is unlikely in practice because of the inertia of habitual use, and because numericevaluation has assumed a prevailing place in public discourse.

Secondly, regulatory accountability involves the account-giver following rules and operating standards intended to con-trol behaviour. Control may also be achieved by the threat of performative account giving. In this context, when called toaccount the account-giver who has acted within the architecture of the regulated environment would refer to the operatingrules to justify behaviour. Thirdly, managerial accountability focuses on motivating not restraining behaviour. Behaviour isimproved by the act of measurement. The focus is to design architecture that motivates. Fourthly, embedded accountabilityoperates through the norms and values of the account-giver and internalises the moral responsibility often associated withprofessional standards.

Bovens (2005) notes that accountability suffers from the problems of too many hands and too many eyes, that is, ofmultiple account-givers and receivers. Public officials may have accountability relations with five different constituencies:organisational in terms of their superiors, political in terms of elected representatives, legal to the courts of law, admin-istrative to auditors and inspectors and professional to their peers (Bovens, 2005). In relation to too many hands, Bovens(2005) notes that it may be difficult for account-receivers to pin down individual responsibility and unravel who within anorganisation has contributed to its conduct.

The NPM reforms of the public sector have placed more public expenditure in the hands of Executive Agencies2 and outsidedirect state control by splitting the roles of purchaser and provider as is common in PPPs. This use of Executive Agencies mayhave impacted on political accountability because it has affected the normal channels of ministerial accountability associatedwith government departments (Mayston, 1993). In the traditional practice of public administration, individual and groupaccountability to agency and program goals is achieved through hierarchical relationships, standardised procedures, policydirectives and bureaucratic control all of which have been weakened by the widespread practice of contracting out (Dubnickand Frederickson, 2010).

In terms of the formal structures, the split between purchaser and provider imposes a break in the hierarchical chainof ministerial and departmental control even though Mulgan (2002) argues, on the basis of a few cases studies, that inpractice the delegation of accountability to heads of executive agencies has been resisted. Nevertheless, the strengthof agency accountability to program goals reduces as implementation involves multiple layers of third parties (Dubnickand Frederickson, 2010). In particular, Executive Agencies have weakened the legitimacy of political control through theresponsible minister, which may in part explain the rise in legal and administrative accountability forms (Bovens, 2005).

The NPM reform process creates a shift to corporate governance by market principles, legitimised by an institutionaleconomics markets and hierarchies framework. NPM is premised on the belief that market-based transactions provide amore rational and efficient way of organising than hierarchical or clan forms of governance. It is based on agency theory,forms of financial control (Cochrane, 1993), and a strong belief in the objectivity of financial measures. Although publicsector accountability is still associated with a wide range of activities, including compliance, the use of funds for the purposesintended by Parliament, VFM, transparency and responsiveness, these changes re-modelled the UK’s public sector as variantsof the private sector. Further re-modelling occurred as private sector notions of corporate governance were imported intothe public sector with the publication of a number of governance codes that followed the principles of the UK Cadbury report(Hodges et al., 1996). These, and later amendments that imported ideas from subsequent corporate governance reports, arediscussed in more detail later.

As NPM reforms re-modelled the public sector, a corresponding transition in the nature of accountability has been widelyrecognised in the literature (Poulsen, 2009). Accountability has changed from procedural accountability, which focuseson adherence to proper procedures in relation to accountability for finances and fairness (Bovens, 2006), to performanceaccountability, which became the fashion of the day (Dubnick and Frederickson, 2010). However, Bovens (2005) concludes

that whatever its nature, the first and foremost function of public accountability is democratic control so that citizens canjudge the performance of the government and sanction their political representatives. Thus, account-giving should be public2 Executive Agencies are semi-independent organisations set up by the Government to carry out some of their responsibilities instead of a governmentdepartment. They enable executive functions within government to be carried out by a well-defined business unit with a clear focus on delivering specifiedoutputs within a framework of accountability to Ministers. (http://www.parliament.uk/site-information/glossary/executive-agencies/)

ac

aeI(t

edaa

aat(aGtp

dpRsttr

no

2

brtiAwSto

mot

t(atte(

b

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 217

nd open or at least accessible to citizens. Mulgan (2000) identifies the key accountability relationships as those betweenitizens and holders of public office and within the ranks of office holders between elected politicians and bureaucrats.

From the perspective of this paper, this NPM reform process had four inter-related and significant impacts on UK reportingnd accountability. Firstly, it promoted accountable management (Gray and Jenkins, 1993) in government. For example,ach central government department was to have clearly defined objectives and responsibilities (CMND, 1982, p. 8616).nformation, such as performance measures, would enable management to fulfil their responsibilities. Bennett and Krebs1991) argued that the intention was to make the public sector more like the private sector, thereby enabling the two sectorso work more closely together, as in PPPs.

Secondly, the reform process involved the loss of functions by central government to alternative service delivery systems:xecutive agencies (Rhodes, 1994). These agencies were to have a measure of organisational independence to execute andeliver policy and strategic management determined by Ministers. Greater external accountability was to be achieved by

framework document that would explicitly set out each agency’s aims and objectives and the monitoring, accountabilitynd reporting between the agency and its parent department (HMSO, 1989).

The third aspect of these reforms was the demand for more inspection and more effective external scrutiny from andccountability to Parliament. Revamped in 1979, the Departmental Select Committees were charged with examining threespects of each Department and its associated public bodies: spending, policies and administration. A number of committeeshat have cross-Departmental remits carry out additional oversight. The most important is the Public Accounts CommitteePAC) whose remit is to examine accounts that show the expenditure of appropriations granted by Parliament and any otherccounts laid before Parliament it thinks fit (www.parliament.uk/parliamentary committees). The Comptroller and Auditoreneral has the power to report on the economy, efficiency and effectiveness of government bodies’ use of public funds and

hus on the value for money (VFM) achieved by Departments. These reports are considered by the PAC, which also has theower to request the National Audit Office (NAO) to carry out investigations.

Finally, the reform process in the UK, although notably not in most other countries that use PPPs, included HM Treasury’secision that the public sector’s financial reporting should comply with private sector reporting regulations, initially asromulgated by the UK’s Accounting Standards Board and later adapted in the light of recommendations from the Financialeporting Advisory Board (FRAB). More recently, HM Treasury has decreed a transition to international financial reportingtandards (IFRS) issued by the International Accounting Standards Board (IASB), again with adaptations by FRAB. This meanshat UK reporting will be subject to international private sector regulation in both the public and private sectors, in contrasto other countries that will follow the International Public Sector Accounting Standards Board (IPSASB) for their public sectoreporting.

In essence, the NPM reform process changed the nature of public sector accounting and accountability. There was aotable advance in cost awareness and a switch from management of policy to management of resources, with an emphasisn individual responsibility and accountability for resources rather than collective stewardship (Gray and Jenkins, 1993).

.2. Transferring private sector corporate governance into the public sector

Although corporate governance may also be an issue in small or privately controlled firms, it is normally considered toe a much more significant issue in large public companies (Hart, 1995) with widely dispersed shareholders who may freeide rather than participate in decision making (Berle and Means, 1932) or conduct monitoring. Consequently, the agencyheory approach focuses attention on the monitoring tasks that various corporate governance mechanisms may performn listed companies, but pays little attention to corporate governance in subsidiary, associate or joint venture companies.gency theory postulates a conflict of interest between members of an organisation in which owners are characterised aseak relative to managers (Roe, 1994). Thus, owners must reduce agency costs and control the opportunism of managers.

ince the development of corporate governance has often progressed in the face of financial scandal, regulators have soughto control the relationship between the board room and shareholders, and to tighten controls over the preparation and auditf financial statements.

Good corporate governance is deemed to provide control while promoting economic enterprise and corporate perfor-ance (Keasey et al., 2005), so that shareholder value is enhanced and shareholders’ funds are not expropriated or wasted

n unattractive projects (Shleifer and Vishny, 1997). That is, the focus of attention is on the economic decision maker, i.e.,he shareholder.

This unitary stakeholder approach contrasts with the public sector’s long standing commitment of public accountabilityo multiple stakeholders. Government is a serial set of principal–agent relationships with citizens as the ultimate principalMoe, 1984; Mayston, 1993). Thus, the public sector has different and potentially conflicting corporate governance andccountability relationships to manage compared to the single driving relationship between the board and shareholdershat is the focus of private sector corporate governance. Accountability ‘for what’ is thus also likely to be more complex in

he public sector. Despite this difference, the transfer of corporate governance to the public sector has occurred to such anxtent that it may have replaced public accountability (Hodges et al., 1996), although the present authors agree with Poulsen2009) that two regimes co-exist: public accountability and corporate governance regimes.In the next section, we consider the special accountability issues raised by the PPP hybrids, which are particularly affectedy the dual influences of private sector corporate governance and public sector notions of accountability.

218 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

3. PPPs: a special accountability case

PPPs are worthy of special consideration in relation to accounting and accountability for a number of reasons. Not onlydo they offer short-term political attractions to governments by quickly providing project infrastructure, but also they alsocreate multiple conflicts of interests for government. Government acts in the roles of policy advocate, economic developer,steward for public funds, elected representative for decision making, regulator over the contract life, commercial signatory tothe contract and planner (Hodge and Greve, 2005). Furthermore, because government acts as guarantor this reduces marketincentives and increases the need for greater oversight (Skelcher, 2005), especially because the paucity of information avail-able to citizens under these market-based methods of service delivery undermines the social contract between governmentand its citizens (Sands, 2006). PPPs present problems for public sector accountability because the public sector remainsresponsible for services it does not deliver. As such, they constitute a further example of a process described by Rhodes(1994) as “the hollowing out of the state” following on from the outsourcing of ‘non core’ services and the liberalisation andcommercialisation of services.

A number of political and service performance risks and thus accountability, corporate governance and reporting issuesflow from the nature and structure of PPPs. These include: the involvement of private financiers in the structuring of projectsand the impact of their risk-return criteria on project formulation; the nature of the relationships and the organisationalstructures of the parties to the contract and the relative power of the contracting parties; and problems of performancemeasurement, especially related to the self-monitoring nature of contracts. We consider each in turn using the UK’s PFI asour exemplar.

3.1. The role of private finance

While the private sector has always built infrastructure for the public sector and is increasingly involved in the provisionof services due to outsourcing and privatisation, PPPs introduce a new element, private finance, subjecting key investmentand procurement decisions to the financiers’ risk-return criteria. As a result, the financiers may require guarantees (implicitor explicit) from the public sector and therefore determine the characteristics, content, and payment mechanisms of projectsin order to meet their expectations. This has led to frequent amendments to projects in the UK at preferred bidder stage,when there is a lack of competitive pressure. A project may therefore be very different at financial close to that originallyadvertised. Furthermore, as the Business Cases and contractual documents typically remain secret, it is impossible to examinethe impact of such requirements on the project.

This raises accountability, corporate governance and related reporting issues about risk-return management of the projectprior to financial close and about whether and how the risk priced into the contract is actually transferred at later stages,especially when risk is to be shared across organisations. Moreover, risk management processes that focus only on theproject or at unit level, as is common in the private sector, deny the particular characteristics of government as responsiblefor planning, organising and monitoring public service provision and risk bearer of last resort (Froud, 2003).

3.2. Relationships and organisational structures

The nature of PFI relationships and the organisational forms associated with them are different and more complex thanthe contracting out of services that were simple, legally protected, market-based, arms-length purchases of a relativelyshort duration (Broadbent and Laughlin, 2003). PFIs are long-term contracts with extended supply chains and multiple andchanging partners, necessitating extensive contractual documentation for all financial flows and relationships between mul-tiple partners (Hodge, 2005). These contractual and quasi-commercial relationships blur the distinctions between politicalaccountability and more technical forms of accountability (Alexander, 1991). The issue is not only of complexity but alsohow it is handled.

Partnerships are not by definition, fair, equal or good (Nelson, 2002). The unequal power relations between the partnersbecome evident in the context of poor performance when procurers lack effective sanctions and/or the resources to imposethem (Edwards et al., 2004). Furthermore, the political sensitivity and the essential nature of the services, as well as broaderpolitical choices by the government make it impossible in practice to terminate contracts (Edwards and Shaoul, 2003). Thatis, neither market forces nor contractual terms are capable of ensuring efficient and effective performance.

In addition, non-elected agencies spend large sums of public money and work through complex networks where the leadagency and the channels of accountability may be unclear (Cochrane, 1993). Many PFIs are signed by such agencies whosefinancial objectives may diverge from the interests of their users, particularly if there is limited competition and asymmetricinformation between consumers and producers. There is no guarantee that information will be public: it may be withheldto protect the agency’s profitability (Rutherford, 1992). While the creation of agencies need not have a major impact onfinancial control and accountability (Pendlebury et al., 1994), there is pressure to recognise their independence (Rutherford,1992).

Furthermore, the private sector partners in PFI projects also have complex organisational structures. This is due in partto the stated objective of generating savings by integrating the design, construction and operations over the life of a long-term contract. While the public sector normally signs the PFI deal with a single entity, special purpose vehicle (SPV), thisSPV is in fact a consortium of companies, which subcontracts the different elements of the project to its sister companies.

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 219

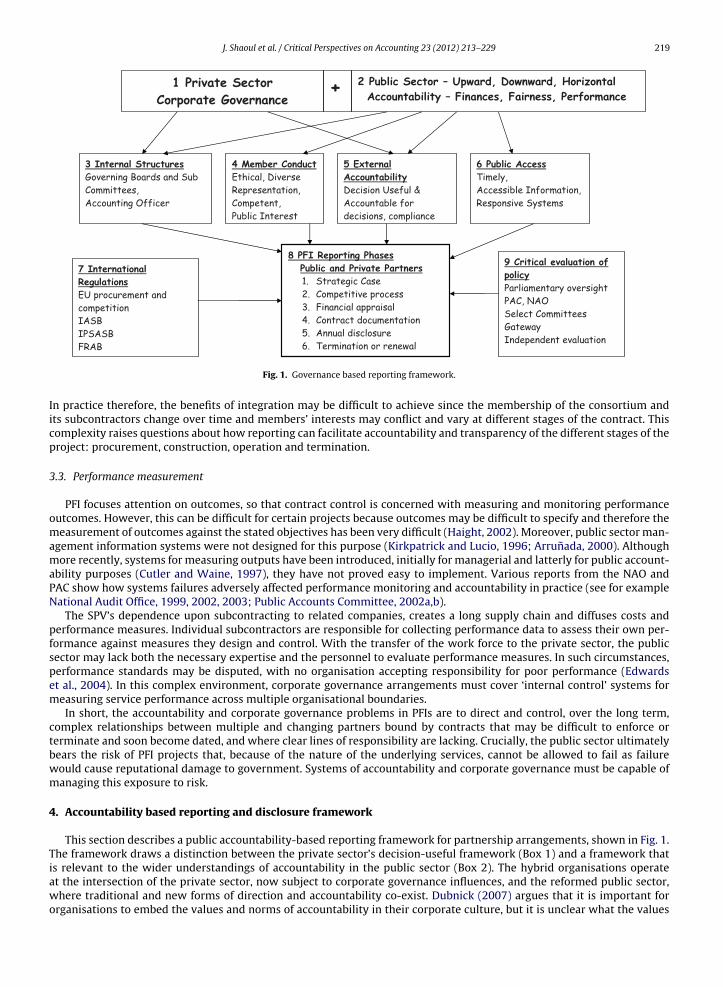

1 Priv ate Sec tor Corpor ate Gove rnance

2 Public Sector – Upward, Downw ard , Horiz ontal Accountability – Fina nces , Fairness , Perf orma nce

3 Inter nal Stru ctu resGovern ing Board s and Sub Committees, Accounting Off icer

4 Member ConductEthical, Diverse Representation, Competent, Pub lic Int eres t

5 Extern al AccountabilityDecision Useful & Accou nta ble for decisions, co mpli ance

6 Pub lic Acces sTimely, Accessibl e Informa tion, Responsive System s

7 Intern ationa l Regulati onsEU procu rement and com petition IASB IPSASB

8 PFI Reportin g Phases Public and Private Partners

1. Str ate gic Case 2. Com petiti ve pro cess 3. Fin ancial appraisal 4. Contract documentat ion 5. Annual disclosure 6. Termin ation o r r ene wal

9 Critica l evalua tion of policyParliamentary over sight PAC, NAO Selec t Comm ittees Gateway Independ ent evalu ation

+

Iicp

3

omamaPN

pfspem

ctbwm

4

Tiawo

FRAB

Fig. 1. Governance based reporting framework.

n practice therefore, the benefits of integration may be difficult to achieve since the membership of the consortium andts subcontractors change over time and members’ interests may conflict and vary at different stages of the contract. Thisomplexity raises questions about how reporting can facilitate accountability and transparency of the different stages of theroject: procurement, construction, operation and termination.

.3. Performance measurement

PFI focuses attention on outcomes, so that contract control is concerned with measuring and monitoring performanceutcomes. However, this can be difficult for certain projects because outcomes may be difficult to specify and therefore theeasurement of outcomes against the stated objectives has been very difficult (Haight, 2002). Moreover, public sector man-

gement information systems were not designed for this purpose (Kirkpatrick and Lucio, 1996; Arrunada, 2000). Althoughore recently, systems for measuring outputs have been introduced, initially for managerial and latterly for public account-

bility purposes (Cutler and Waine, 1997), they have not proved easy to implement. Various reports from the NAO andAC show how systems failures adversely affected performance monitoring and accountability in practice (see for exampleational Audit Office, 1999, 2002, 2003; Public Accounts Committee, 2002a,b).

The SPV’s dependence upon subcontracting to related companies, creates a long supply chain and diffuses costs anderformance measures. Individual subcontractors are responsible for collecting performance data to assess their own per-ormance against measures they design and control. With the transfer of the work force to the private sector, the publicector may lack both the necessary expertise and the personnel to evaluate performance measures. In such circumstances,erformance standards may be disputed, with no organisation accepting responsibility for poor performance (Edwardst al., 2004). In this complex environment, corporate governance arrangements must cover ‘internal control’ systems foreasuring service performance across multiple organisational boundaries.In short, the accountability and corporate governance problems in PFIs are to direct and control, over the long term,

omplex relationships between multiple and changing partners bound by contracts that may be difficult to enforce orerminate and soon become dated, and where clear lines of responsibility are lacking. Crucially, the public sector ultimatelyears the risk of PFI projects that, because of the nature of the underlying services, cannot be allowed to fail as failureould cause reputational damage to government. Systems of accountability and corporate governance must be capable ofanaging this exposure to risk.

. Accountability based reporting and disclosure framework

This section describes a public accountability-based reporting framework for partnership arrangements, shown in Fig. 1.he framework draws a distinction between the private sector’s decision-useful framework (Box 1) and a framework that

s relevant to the wider understandings of accountability in the public sector (Box 2). The hybrid organisations operatet the intersection of the private sector, now subject to corporate governance influences, and the reformed public sector,here traditional and new forms of direction and accountability co-exist. Dubnick (2007) argues that it is important forrganisations to embed the values and norms of accountability in their corporate culture, but it is unclear what the values

220 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

and norms of these hybrid organisations are or how any conflicts between the values and norms of the partners can beresolved and embedded in the hybrids’ corporate culture.

Thus Boxes 1 and 2 of the framework are joined by a plus sign, showing that citizens must be able to hold providers andprocurers of services to account and to challenge sub-standard governance (CIPFA, 2005b), while the organisations mustalso comply with the norms of private sector corporate governance and deliver decision-useful information to shareholders.

The framework identifies the influences and demands on the reporting process. While the detail is specific to our UK PFIexemplar, similar influences and demands may be expected for other PPP type arrangements. These include three separatestreams of accountability in Box 2, and four elements of corporate governance in Boxes 3–6 (Smith et al., 2006). Whilecorporate governance does have some expectations about private sector directors conduct and the availability of informationthese aspects are much more narrowly drawn than in the public sector. For example, directors do not act in the public interest,but in the interests of shareholders to whom financial statements are addressed. International regulatory influences areshown in Box 7. Box 8 shows six reporting phases, identified by Shaoul et al. (2008), that cover the long contract period ofPFIs, and Box 9 includes the critical evaluation of policy. We consider each in turn.

4.1. Three accountability streams

Dubnick (2007) argues that private sector corporate governance takes a myopic approach in which shareholders areelevated above other stakeholders because it is by investors and financiers for investors and financiers. In the public sectorfinancial reporting and accountability for finances are embedded in the upward stream of accountability from each publicsector unit to Parliament through the hierarchy of the public sector. Although there are evident distinctions, this reportingline has similarities with the relationship between management and shareholder in the private sector. However, this paperdraws attention to reporting needs for the other two accountability streams. Accountability to multiple stakeholders in thecommunity, to whom public sector accountability is also owed, focuses attention on the downward stream of accountability.

Smith et al. (2006, p. 166) describe partnerships as having a horizontal accountability between the private sector compa-nies and the public sector procurer, which is relevant to PPPs (Shaoul et al., 2008). Miller et al. (2008) agree that in hybridsthe lateral relationships are very significant. Because much financial and non-financial information is held by the numer-ous companies that provide services under the PFI contract, both upward and downward accountability are dependentupon the provision of, or access to, information that flows first upwards to the SPV and then across through the horizontalaccountability stream. That is, traditional accountability for finance and fairness, (Bovens, 2006) and newer assessments ofperformance depend upon not only public sector reporting, but also reporting from the private sector. This in turn suggeststhat the norms of public sector accountability should apply not only to the public sector partner but also to some extent atleast to the private sector partners who are in receipt of public money to provide public services.

4.2. Four elements of accountability

Smith et al. (2006) argue that in the public sector there are four elements of governance: structures of internal governance,external accountability, member conduct and public access. These overlap with, but are not identical to, notions aboutcorporate governance in the private sector, where, as will be highlighted below, requirements tend to be less extensive. Weconsider these elements in turn.

4.3. Internal structures

Since the early 1990s, there has been a spate of reports in the private sector, (Cadbury, 1992; Greenbury, 1995; Hampel,1998; Turnbull, 1999; Higgs, 2003; Smith, 2003), which recommend monitoring procedures and structures that seek toachieve two major outcomes. Firstly, improvements in the quality of reporting typically by increasing the quality of internalcontrol systems, disclosures, and the independence of external auditors. Secondly, changes in the operation of the Board.Three authoritative sources (CIPFA, 2005a,b; Treasury, 2005; Audit Commission, 2006) show that, as in the private sector,corporate governance in the public sector has also copied these two objectives.

In relation to the second objective, the private sector reports have typically: highlighted the need for and controlledthe content of corporate charters; attempted to tighten control of internal mechanisms around decision-making processesin the board room; and focused on ways to encourage institutional shareholder activism and more independent boardsby using remuneration policy to align executive and shareholder interests (Watson and Ezzamel, 2005). To achieve theseobjectives, private sector regulators concentrate on the membership of the Board, emphasising the role of outside indepen-dent directors, whose rising numbers have been one of the most visible elements of private sector corporate governancereform internationally (Dahya et al., 2002). They also recommended the creation and then strengthened the role of boardsub-committees, such as audit, nomination and remuneration committees.

The public sector governance guidance also stresses the importance of the Management Board. For example, the HMTreasury Code focuses on how, within the strategic framework set by the Minister, the Department Management Boards cansupport the head of Department by advising the Minister and taking ownership of the Department’s performance (Treasury,2005).

ddoaccC

tFm2(eat(

4

ag

beEpT

rotmle

sat

swi

pImditt

4

o

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 221

The public sector has also introduced board sub-committees and notions of corporate governance by disclosure. Thisespite criticisms of the lack of clarity about what these mechanisms are supposed to achieve or how they are to holdirectors to account (Ezzamel and Watson, 1997), and a lack of evidence that audit committees can further the interestf the public (Guthrie and Turnbull, 1995). For example, HM Treasury (2005) says that an internal audit service and anudit committee, chaired by an independent non-executive member, should independently advise Governing Boards. Auditommittees should have terms of reference that include overseeing the production of the annual accounts, reviewing thehoice of accounting policies and practices, the internal control systems and the work of internal and external auditors (Auditommission, 2006). Furthermore, CIPFA (2005a) argues that disclosures about such activities demonstrate good governance.

In addition, some of the Codes of Practice for the public sector are concerned with the quality of organisational rela-ionships and levels of morale, issues that are generally absent from private sector codes. The Independent Commissionor Good Governance In Public Services recognises that governance is a dynamic process, which if good may lead to goodanagement, good performance, good stewardship of public money, good public engagement and good outcomes (CIPFA,

005b), but if bad may foster low morale and adversarial relationships, poor performance and dysfunctional organisationsCIPFA, 2005b). Corporate governance is intended to “encourage high standards of propriety and promote the efficient andffective use of staff and other resources throughout the Commission” (Audit Commission, 2006, p. 8). But this cannot bechieved simply by following rules and procedures, as it flows from a shared ethos or culture and therefore CIPFA suggestshat governors have a responsibility to the organisation’s staff, which they should actively discharge in a planned mannerCIPFA, 2005b).

.4. External accountability

The Anglo-American market-based corporate governance model equates institutional transparency with the disclosurend dissemination of financial information, to enable monitoring by diversified shareholders. Especially in the UK, corporateovernance by disclosure has been pursued (Ezzamel and Watson, 1997).

However, external public accountability encompasses the reporting not only of the decision-useful information requiredy private sector conventions, but also of information that enables an assessment of past decisions and compliance withxpenditure allocations by Parliament. In the public sector in the UK, the role of the designated Accounting Officer is crucial.ach public sector entity must have a role holder who fulfils a number of well-specified statutory duties in relation toublic money allocated to the entity, and is personally responsible to Parliament for the resources under his/her control.he Accounting Officer acts as expert witness before the Public Accounts Committee when it scrutinises expenditure.

If reporting is to provide external public accountability for PFIs, then there is a need for multi-dimensional externaleporting that covers: the use and stewardship of resources; the quality of services; financial probity; and financial controlver public monies, whether held in the public or private sectors. In other words, it entails horizontal accountability. Dueo the longevity of PFI contracts, which are legally binding commitments on future governments, external accountability

ust also entail an assessment of any future risks and liabilities that may flow from these contracts, including contingentiabilities, the financial viability of the private sector partners and the ring fencing of the surpluses for future maintenancexpenditure.

However, the use of private sector reporting standards, which aim to provide information that is decision-useful tohareholders, by public authorities raises questions about whether there is sufficient information to deliver external publicccountability. In particular, Shaoul et al. (2008) note financial statements do not present budget information routinely, sohat it is difficult to compare actual expenditure against Parliament’s allocations.

Furthermore, external accountability in the public sector is specified in terms of ensuring good quality outcomes forervice users, especially the most needy. For example, the Audit Commission seeks to achieve “better outcomes for citizens,ith a focus on those people who need public services most” (Audit Commission, 2006, p. 3). Similarly, the role of governance

s:

“to ensure that an organisation or partnership fulfils its overall purpose, achieves its intended outcomes for citizensand service users, and operates in an effective, efficient and ethical manner” (CIPFA, 2005b, p. 7).

Thus, it may be appropriate to separate out different kinds of activities, individual transactions or specific outcomes fromrojects rather than relying upon a single measure of financial performance as is common in the private sector (Hood, 2006).

n reporting terms, the disclosure of disaggregated financial information for each individual large-scale project (such as aajor road project) is critical if an independent assessment of value for money and affordability is to be possible. Similarly,

isaggregated non-financial information for individual large projects is critical if independent assessment of service qualitys to be possible. Such disclosure depends upon information held by private sector partners, who must either report it orransfer it horizontally for disclosure by the public sector. Thus, accountability for public money requires greater disclosurehan is usual under the private sector decision-usefulness framework.

.5. Board members’ conduct

Board members’ conduct includes issues about ethical behaviour, acting competently in the public interest, and diversityf representation on governing boards. The public sector guidance expects that corporate governance leadership will be

222 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

given (CIPFA, 2005a) and decisions will be made in the public interest (Treasury, 2005). Governors are expected to operatein an ethical manner with probity and integrity in line with the seven Nolan principles3 (Nolan, 1996) for the conduct ofpeople in public life (CIPFA, 2005b; Treasury, 2005). While this element raises wide-ranging questions about how the publicare to be represented, there are difficult questions from a reporting perspective about how member conduct attributes, suchas the Nolan principle of selflessness, are to be measured, monitored or reported.

In accountability terms, Smith et al. (2006) draw attention to potential conflicts of interest, usually deemed to be controlledif their existence is declared. However, it is unclear whether this is sufficient in the context of PFIs, where the members of theprivate sector consortium may vary across the phases of the contract and may themselves have conflicting interests. Becauseconflicts of interest are particularly important at procurement phase when PFI is the only available funding mechanism,procurers need to consider whether any such conflicts undermine value for money.

4.6. Public access

Public access refers to the existence of institutionalised practices that ensure transparency and openness. For example,within the public sector it is expected that systems should be responsive (Mulgan, 2000), and that mechanisms such ascomplaints procedures and ombudsmen should be in place. Such institutions of accountability are designed to make publicofficials more responsive to the public. There are therefore recommendations in public sector governance guidance thatgovernors should provide the public the means to challenge an organisation for failure to demonstrate the spirit and ethosof good governance (CIPFA, 2005b). Furthermore, the Governing Board should approve, publish and maintain a complaintsprocedure that includes holding the Chairman responsible for responding to such complaints (Audit Commission, 2006).

However, although CIPFA (2005b) includes engaging stakeholders and making accountability real as one of its six coreprinciples common to all public service organisations, practical guidance on how this downward stream of accountabilityis intended to operate is not well specified (Shaoul et al., 2008), raising the possibility that it may not work well in practice.

In financial reporting transparency is closely associated with the disclosure of information, but the nature of its pre-sentation and the location of information affects public accessibility. For example, O’Neill (2006) draws an importantdistinction between disclosure or dissemination and communication. She argues that transparency achieves little if it doesnot meet elementary epistemic and ethical standards. That is, material disseminated must be accessible to relevant audi-ences. Deighton-Smith (2004) argues that transparency tools include the use of plain language, standardisation, electronicaccess, consultation, and appeal rights.

However, commercial confidentiality may militate against public access to information about PFIs. Heald (2006) thereforeargues governments should construct an effective framework for transparency that includes respect for time sensitivity. Thisimplies allowing confidentiality for a period of time that is sufficiently long to make the information of little value to hostileparties (such as competitors) but sufficiently short to allow for accountability (Prat, 2006).

In summary, the framework shows the complex environment of the hybrid organisations and the ever-expanding formsof accountability to which they are subject. Mulgan (2000) cautions that such extensions, which include internal aspects ofofficial behaviour beyond the external focus implied by being called to account, may be weakening the importance of externalscrutiny. Financial reporting is above all a mechanism for external scrutiny but external scrutiny may also require more ordifferent forms of financial and non-financial information than is commonly provided both by private sector companies tomeet the norms of corporate governance and by public sector organisations.

4.7. International regulatory influences

Accountability depends upon the free flow of appropriate information (Mulgan, 2000). This is especially important in rela-tion to PPPs because of the possibilities for opportunistic behaviour by contractors due to information asymmetry betweencontractor and client, which can lead to quality shading (Skelcher, 2005). The public sector procurer relies upon perfor-mance measurement data collected by the service provider – a self-monitoring process – and Skelcher (2005) argues thatcontractors can control the quality, quantity and timeliness of that data, giving then a powerful resource in the relationship.

Regulations covering public sector procurement and financial reporting are increasingly international. Such regulatoryinfluences come from the European Union in terms of procurement and competition, and the IASB and IPSASB in termsof reporting. While EU procurement and competition regulation particularly affect the procurement process, it may alsoaffect later phases, such as contract amendments that occur throughout the life of the project, as well as the renewal phase.Regulation from the IASB will most directly affect the annual reporting but may also indirectly affect earlier phases to theextent that contracts are written to satisfy particular accounting requirements, especially in relation to risk transfer.

Moreover, the definition of appropriate information that will enable accountability is complex. The IASB’s framework(IASC, 1989), adopted in 2002, assumes that financial statements that meet the needs of the providers of risk capital will also

meet most of the general financial information needs of other classes of user. However, IPSASB (2006) disputes this view andstates that more comprehensive financial statements are required for service users and citizens. Furthermore, Hood (2006)argues that government should operate accounting regimes that separate out different kinds of activities so that it is possible3 These principles are: selflessness, integrity, objectivity, accountability, openness, honesty and leadership.

tnn

4

rada

aaiCef

gdbp

ptap

Fspbruaus

ptbfaae

4

pahaB

a

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 223

o identify who pays and who benefits from particular programmes. That is, he argues, transparency and accountability areot only about openness in policy they also require that subsidies and other forms of public support should be explicit andot hidden.

.8. PFI reporting phases

Shaoul et al. (2008) show that the reporting of PFIs spans six separate phases, each of which has specific informationequirements. They cover: creating the strategic case and the economic appraisal; competitive processes and the biddingrrangements; financial appraisal leading to financial close; contract documentation and the financial arrangements; annualisclosure and scrutiny relating to ex post performance information, value for money and affordability in the public sector,nd scrutiny of performance in the private sector; and the termination or renewal of the contract.

Demirag et al. (2004) agree that it is important to explore PFI as a long-term staged process, because they argue differentccountability issues may arise at various stages of the PFI process. This implies a need for different types of informationt different stages. However, in the decision-making stages prior to financial close Shaoul et al. (2008) show that essentialnformation about the financial case, value for money, risk transfer and affordability can only be found in the Full Businessases4, but that these documents may not be publicly available for commercial confidentiality reasons. In later phases,ssential information for accountability purposes can only be found in the contract documentation that may also be withheldor similar reasons.

Dubnick and Frederickson (2010) find that whereas previously the obligation to give an account tended to imply account-iving after the fact, in more modern times organisational and political mechanisms seek to monitor individuals and agenciesecisions before actions are initiated. Although recognising that there is little research that has investigated the linkagesetween PFI stage and type of accountability, Demirag et al. (2004) suggest there has been a myopic focus on the design androcurement stages of PFIs, to the detriment of the operating phase.

Shaoul et al. (2008) show that there is a need for more disclosure about PFI projects from both public and private sectorartners. They argue that the public sector should provide additional information about how the project is operating inerms of both financial and physical performance. This additional information should make a comparison between actualnd budget expenditure easier, and should enable a comparison of actual risk allocation in practice versus the risk allocationroposed in the PFI contract. Furthermore, there should be greater transparency about contingent liabilities.

From the private sector, these authors argue that additional information is required about the viability of the project.irstly, there needs to be transparency about whether there is adequate ring fencing of advance payments made to the privateector that are intended to cover future maintenance needs. Secondly, Shaoul et al. argue that insufficient attention has beenaid to the termination phase of PFI contracts, when the infrastructure is to be handed back to the public sector. There shoulde a process in place to ensure that the asset handed back is in a good state of repair, especially for infrastructure such asoads, which will be handed back long before the end of the assets’ expected useful life. However, Shaoul et al. argue that isnclear whether such processes exist and whether they are adequate. Furthermore, they show that information is lackingbout how, if at all, summative evaluation of the project is to take place, and that there is no transparency about the windingp arrangements for the private partner. In essence, without accountability at each phase, the public cannot understand theustainability of the contract and thus of public expenditure (Shaoul et al., 2008, p. 41).

The important issue is that at each phase the relevant information is held in a number of different entities in both theublic and private sectors. In the private sector, there are multiple different companies involved in financing and deliveringhe PFI project. In the public sector several entities may be involved in a given PFI project either as joint commissioners orecause they must approve the investment. Across a number of organisations interests tend to vary and their objectivesor the program may not necessarily be compatible with each other (Moynihan, 2006). Thus, the framework explicitlycknowledges the tensions and potential conflicts that arise when people are involved in co-operative enterprise (Hyndmannd McDonnell, 2009). It also challenges the notions of complementarity, synergy and positive sum outcomes that are keylements of the discourse around PFIs (Skelcher, 2005).

.9. Critical evaluation of policy

The final influences on public sector corporate governance, shown in Fig. 1 Box 9, are the oversight and evaluationrocesses. Mulgan (2000) argues that accountability depends upon effective forums for discussion and cross-examination,nd Skelcher (2005) that stronger institutional means for accountability are necessary to assert the publicness of these PPPybrids. In this context, Mulgan (2000) reminds us that although there are potentially many institutions which have account-bility as part of their remit, those whose primary function is to call public officials to account are especially important. Thus,

ox 9 includes the PAC, NAO and Select Committees, that are the relevant bodies in the UK.While ad hoc independent evaluations are valuable, Broadbent and Laughlin (1997) argue if accountability is to bechieved then government must critically evaluate, not merely justify, its actions. As Box 9 shows there are processes of

4 The Full Business Case is a document required by HM Treasury and upon which approval of the scheme will be based.

224 J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229

Parliamentary oversight which may be capable of such evaluation. However, although oversight mechanisms have increasedsince the 1980s, the literature suggests that their impact falls short of critical evaluation for six reasons.

Firstly, the introduction of executive agencies has reduced both the detailed scrutiny by individual elected representa-tives and the Parliamentary accountability of Ministers (Mayston, 1993). Secondly, civil servants rather than Ministers maybe called to account before Parliament (Gray and Jenkins, 1993) so that ministerial accountability and scrutiny is patchyand spasmodic. Thirdly, select committees are hindered by: the non-attendance of witnesses, rapid turnover of members,premature disclosure of reports, the nature of the Prime Minister’s accountability to select committees, and the prolifera-tion of executive agencies (HC, 2002). Fourthly, the National Audit Act 1983 does not permit the NAO to question policy.Fifthly, there may be a failure to follow through the recommendations of scrutineers. For example, the Modernisation SelectCommittee (1998/1999) noted a failure to debate select committee reports in the House of Commons, and a lack of consis-tent analysis of whether recommendations are taken up by the relevant Department. Finally, the Gateway Review Processspecifically designed to evaluate projects post implementation does not apply to the earliest PFI projects.

In terms of institutional arrangements, Hodge and Greve (2005) argue that the parliamentary committees, auditorsgeneral and regulators all need strengthening and that governments need to understand how to separate and strengthentheir intelligent long term corporate governance role from any commercial responsibilities. But Bovens (2005) complainsthat even where there is a clear public interest, PFI managers do not open up to scrutiny, and even where there is theappearance of full disclosure crucial documentation may be withheld from citizens (English, 2005). Sands (2006) argues thatcommercial confidentiality jeopardises the chance of informed public debate and healthy public accountability outcomes,but acknowledges that a balance must be struck between confidentiality clauses and the public’s right to know. Such abalance might be struck by leaving assessment to parliamentary institutions because of the lack of information in the publicdomain (Broadbent et al., 2003), but Demirag et al. (2004) argue that the public sector is ultimately accountable to users andtaxpayers, and that therefore contractual, managerial and parliamentary accountability processes need to feedback to thecommunal accountability process.

This analysis has implications for our accountability based reporting and disclosure framework. In the context of theprivate sector, Millar et al. (2005) have argued that while institutional transparency is generally required, there is no one idealcorporate governance system. Empirical evidence suggests that companies’ choice of corporate governance mechanisms isnot random but is related to characteristics such as: sector, size, concentration of ownership, the strength of shareholderinfluence, nature of performance measures, and whether it has a single or two tier board structure. That is, different corporategovernance models exist. Each firm’s system consists of individual elements that are inter-dependent (Agrawal and Knoeber,1996; Weir et al., 2002), and interact to determine a firm’s governance environment (Jensen, 1993; Shleifer and Vishny, 1997;John and Senbet, 1998). However, in the context of PFIs, the private sector partners must also structure their corporategovernance systems to reflect the public accountability needs of horizontal accountability, as they share responsibility forpublic money.

Hence, we argue that these hybrid organisations need a hybrid accountability framework. Our framework recognisesthat these organisations face demands from corporate governance as it is practiced in the private sector, from public sectoraccountability, and from corporate governance as it has been transferred to and adapted in the public sector. In particular,we argue that additional reporting and transparency are necessary to meet the demands placed upon such organisations.

However, as in the private sector, each public authority must design its own systems within the general frameworkprovided by official sources to meet its needs. PPPs present particular problems and complexities. They feature: long-termmulti stage and often bundled projects; multiple public agencies involved in the development, approval and managementof contracts; services provided by numerous companies that may change over time; and government commitments to astream of future expenditure, affecting the sustainability of public finances, under conditions of uncertainty about futureservice needs. Consequently, there is public interest in the probity, stewardship, and accountability of individual large-scaleprojects.

5. Future research agenda

There is a need to address the hybridising of the practices, processes and expertises that make it possible for hybridorganisations, such as PPPs, to intervene in distinctive ways (Skelcher, 2005). This raises general questions about howaccountability is practiced in PPPs (Hodge and Greve, 2007) and the nature of accountability challenges in the future. Theframework acknowledges the extending nature of accountability, however, we nevertheless agree with Mulgan (2000) thatthe core of accountability with its emphasis on external scrutiny should not be forgotten, and that the information needs ofexternal scrutineers are particularly important.

As accounting researchers the role of financial reporting is especially important because private finance, which oftenforms part of the partnership arrangements, comes at a cost premium, and the risk-return requirements of the financiersmay affect the contract. From an accountability perspective, it is important to articulate the size of this premium paid over

the life of the project (Hodge, 2006), especially in circumstances where the clarity of partnership financial arrangementscan be difficult to fathom (Hodge and Greve, 2005). Furthermore, accounting researchers may be especially interestedin the external scrutineers’ needs for information, whether financial or non-financial, to enable assessment of contractorperformance. Drawing on the framework devised in this paper we offer a research agenda – necessarily only partial (Hyndman

ao

am

ama

nEtfTto

cp

taifabal

aa

dwg

poAIo

mDA2

mrfal

a

tsmtF

J. Shaoul et al. / Critical Perspectives on Accounting 23 (2012) 213– 229 225

nd McDonnell, 2009) and presented in the form of questions – for accounting researchers interested in adding to knowledgef accountability and corporate governance at the inter-face between the public and private sectors.

Is guidance about the directing and controlling of hybrid organisations adequate for the purposes of both public account-bility and corporate governance, and how is such guidance implemented in practice? How can conflicts of interest beanaged?In both the public and the private sectors best practice guidance exists about how public or private sector organisations

re expected to be governed, and in the public sector about how accountability should function, but in neither sector is thereuch guidance that is specifically tailored to the needs of the hybrid organisation. This raises questions about whether the

vailable guidance is useful and how it is applied in practice.Hyndman and McDonnell (2009), in their wide-ranging research agenda for the charities sector, ask whether good gover-

ance guides are useful in practice and useful for all charities, and whether, and if so why, charities adhere to the guidelines.quivalent questions are equally relevant in the case of hybrid partnerships. However, the reporting framework here addshree further specific questions. Firstly, do the guidelines adequately specify how accountability for the three streams andour elements ought to occur? Secondly, what information is needed to serve the needs of these streams and elements?hirdly, is there evidence, as in the private sector, of the adoption of different accountability and corporate governance sys-ems due to the different characteristics of the entities, and if so do these different systems achieve different accountabilityutcomes?

Does information flow across the boundaries of organisations adequately for the purposes of public accountability andorporate governance? Is there evidence that information can and does flow between organisations? If so, what are theractices that facilitate information flow across organisational boundaries? If not, how can information flows be improved?