ACCA Paper P5 Advanced Performance Management For exams in 2012 theexpgroup.com Notes Visit www.theexpgroup.com for free full set

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACCA Paper P5 Advanced Performance Management For exams in 2012

theexpgroup.com

Notes

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 2 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Contents

About ExPress Notes 3

1. Strategic planning and control 7

2. External Influences on Organisational Performance X

3. Performance management systems and design X

4. Strategic performance management X

5. Performance evaluation and corporate failure X

6. Current developments and emerging issues in performance management

X

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 3 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

START About ExPress Notes

We are very pleased that you have downloaded a copy of our ExPress notes for this paper. We expect that you are keen to get on with the job in hand, so we will keep the introduction brief.

First, we would like to draw your attention to the terms and conditions of usage. It’s a condition of printing these notes that you agree to the terms and conditions of usage. These are available to view at www.theexpgroup.com. Essentially, we want to help people get through their exams. If you are a student for the ACCA exams and you are using these notes for yourself only, you will have no problems complying with our fair use policy.

You will however need to get our written permission in advance if you want to use these notes as part of a training programme that you are delivering.

WARNING! These notes are not designed to cover everything in the syllabus!

They are designed to help you assimilate and understand the most important areas for the exam as quickly as possible. If you study from these notes only, you will not have covered everything that is in the ACCA syllabus and study guide for this paper.

Components of an effective study system

On ExP classroom courses, we provide people with the following learning materials:

The ExPress notes for that paper The ExP recommended course notes / essential text or the ExPedite classroom

course notes where we have published our own course notes for that paper The ExP recommended exam kit for that paper. In addition, we will recommend a study text / complete text from one of the ACCA

official publishers, but we do not necessarily give this as part of a classroom course, as we think that it can sometimes slow people down and reduce the time that they are able to spend practising past questions.

ExP classroom course students will also have access to various online support materials, including:

The unique ExP & Me e-portal, which amongst other things allows “view again” of the classroom course that was actually attended.

ExPand, our online learning tool and questions and answers database

Everybody in the World has free access to ACCA’s own database of past exam questions, answers, syllabus, study guide and examiner’s commentaries on past sittings. This can be

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 4 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

an invaluable resource. You can find links to the most useful pages of the ACCA database that are relevant to your study on ExPand at www.theexpgroup.com.

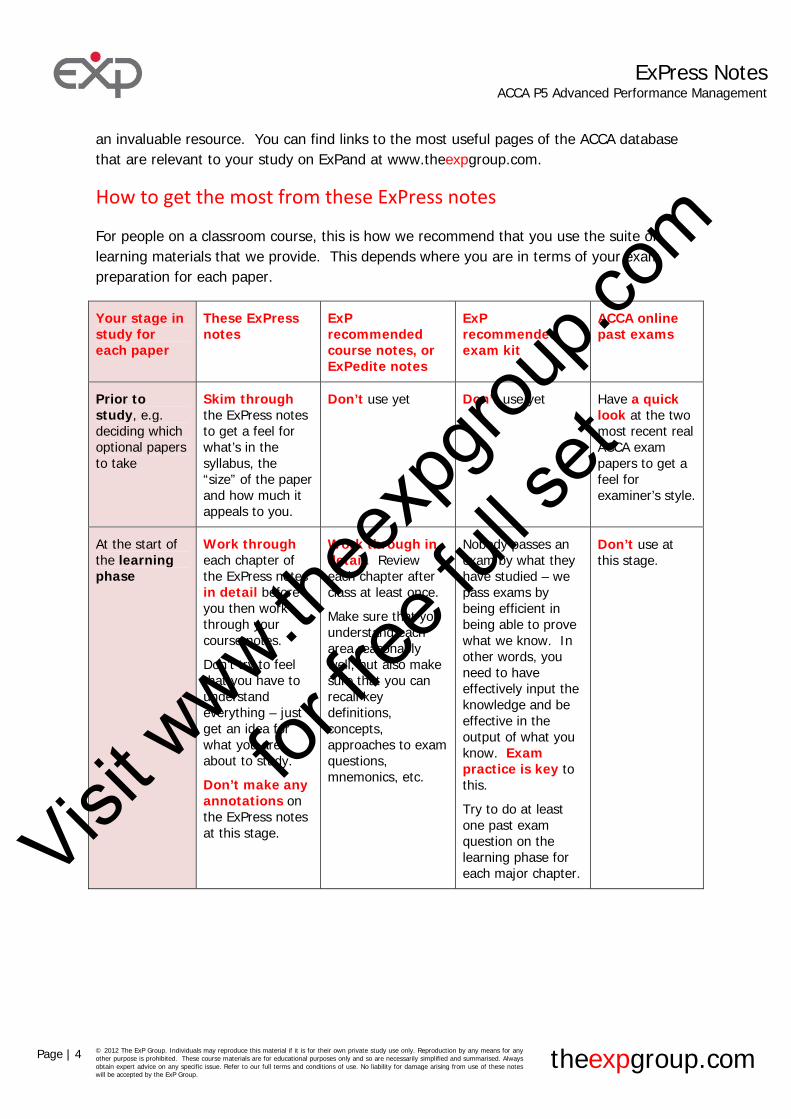

How to get the most from these ExPress notes

For people on a classroom course, this is how we recommend that you use the suite of learning materials that we provide. This depends where you are in terms of your exam preparation for each paper.

Your stage in study for each paper

These ExPress notes

ExP recommended course notes, or ExPedite notes

ExP recommended exam kit

ACCA online past exams

Prior to study, e.g. deciding which optional papers to take

Skim through the ExPress notes to get a feel for what’s in the syllabus, the “size” of the paper and how much it appeals to you.

Don’t use yet Don’t use yet Have a quick look at the two most recent real ACCA exam papers to get a feel for examiner’s style.

At the start of the learning phase

Work through each chapter of the ExPress notes in detail before you then work through your course notes.

Don’t try to feel that you have to understand everything – just get an idea for what you are about to study.

Don’t make any annotations on the ExPress notes at this stage.

Work through in detail. Review each chapter after class at least once.

Make sure that you understand each area reasonably well, but also make sure that you can recall key definitions, concepts, approaches to exam questions, mnemonics, etc.

Nobody passes an exam by what they have studied – we pass exams by being efficient in being able to prove what we know. In other words, you need to have effectively input the knowledge and be effective in the output of what you know. Exam practice is key to this.

Try to do at least one past exam question on the learning phase for each major chapter.

Don’t use at this stage.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 5 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

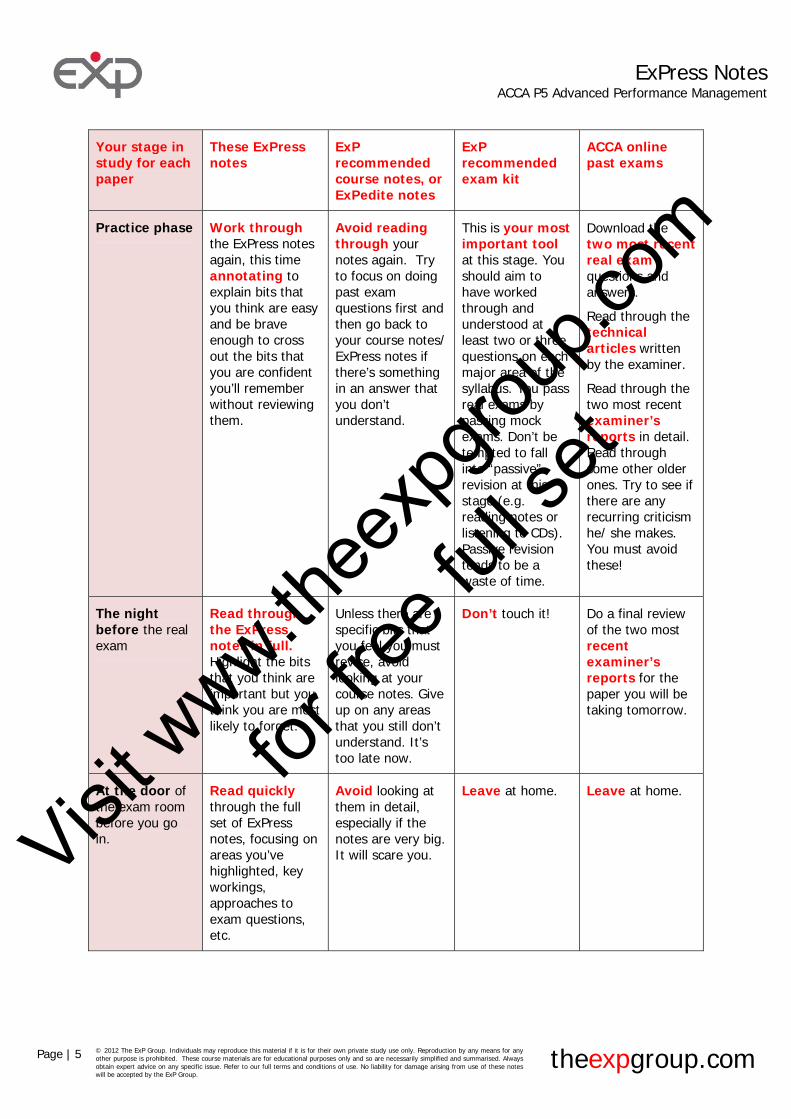

Your stage in study for each paper

These ExPress notes

ExP recommended course notes, or ExPedite notes

ExP recommended exam kit

ACCA online past exams

Practice phase Work through the ExPress notes again, this time annotating to explain bits that you think are easy and be brave enough to cross out the bits that you are confident you’ll remember without reviewing them.

Avoid reading through your notes again. Try to focus on doing past exam questions first and then go back to your course notes/ ExPress notes if there’s something in an answer that you don’t understand.

This is your most important tool at this stage. You should aim to have worked through and understood at least two or three questions on each major area of the syllabus. You pass real exams by passing mock exams. Don’t be tempted to fall into “passive” revision at this stage (e.g. reading notes or listening to CDs). Passive revision tends to be a waste of time.

Download the two most recent real exam questions and answers.

Read through the technical articles written by the examiner.

Read through the two most recent examiner’s reports in detail. Read through some other older ones. Try to see if there are any recurring criticism he/ she makes. You must avoid these!

The night before the real exam

Read through the ExPress notes in full. Highlight the bits that you think are important but you think you are most likely to forget.

Unless there are specific bits that you feel you must revise, avoid looking at your course notes. Give up on any areas that you still don’t understand. It’s too late now.

Don’t touch it! Do a final review of the two most recent examiner’s reports for the paper you will be taking tomorrow.

At the door of the exam room before you go in.

Read quickly through the full set of ExPress notes, focusing on areas you’ve highlighted, key workings, approaches to exam questions, etc.

Avoid looking at them in detail, especially if the notes are very big. It will scare you.

Leave at home. Leave at home.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 6 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

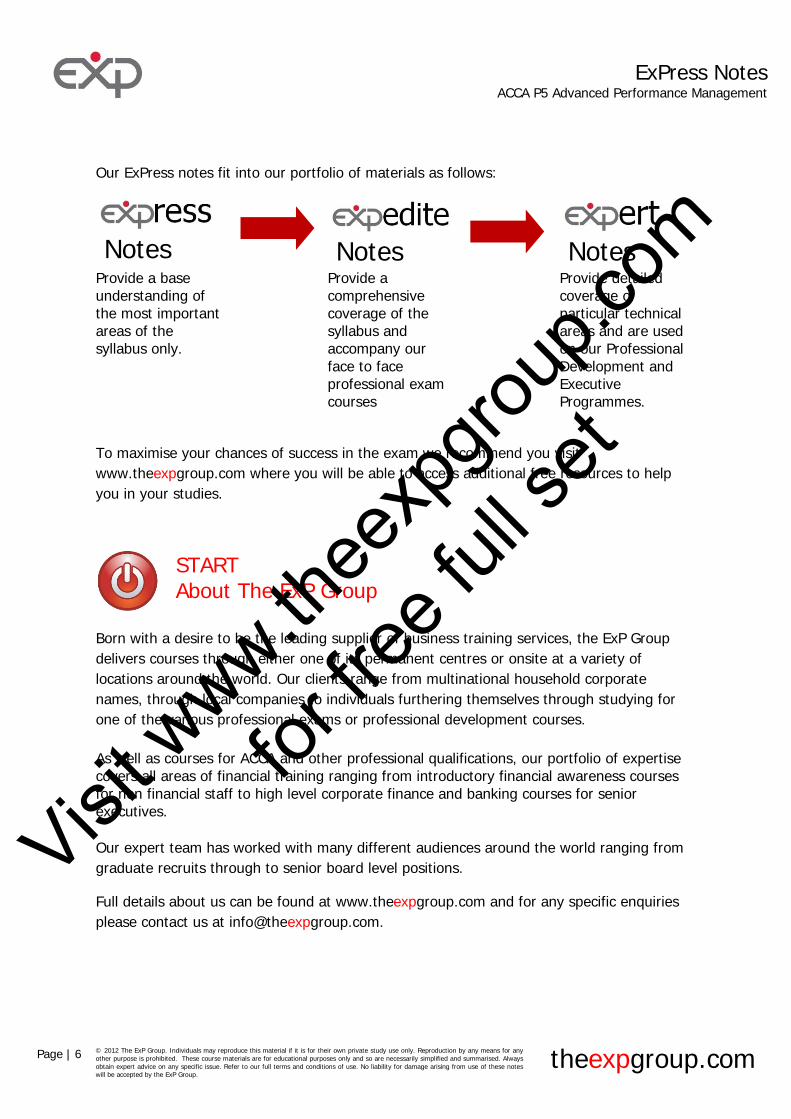

Our ExPress notes fit into our portfolio of materials as follows:

Notes

Notes

Notes

Provide a base understanding of the most important areas of the syllabus only.

Provide a comprehensive coverage of the syllabus and accompany our face to face professional exam courses

Provide detailed coverage of particular technical areas and are used on our Professional Development and Executive Programmes.

To maximise your chances of success in the exam we recommend you visit www.theexpgroup.com where you will be able to access additional free resources to help you in your studies.

STARTAbout The ExP Group

Born with a desire to be the leading supplier of business training services, the ExP Group delivers courses through either one of its permanent centres or onsite at a variety of locations around the world. Our clients range from multinational household corporate names, through local companies to individuals furthering themselves through studying for one of the various professional exams or professional development courses.

As well as courses for ACCA and other professional qualifications, our portfolio of expertise covers all areas of financial training ranging from introductory financial awareness courses for non financial staff to high level corporate finance and banking courses for senior executives.

Our expert team has worked with many different audiences around the world ranging from graduate recruits through to senior board level positions.

Full details about us can be found at www.theexpgroup.com and for any specific enquiries please contact us at [email protected].

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 7 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Chapter 1 Strategic Planning and Control

START The Big Picture

This Paper is concerned with management accounting issues at a strategic level. It is built on issues and methods contained in Paper F5. The main idea is that management accounting has experienced an upgrade in importance and status, given that its approach can be applied at a “total company” level with a time frame that extends well beyond the next financial/accounting/budgeting period. It is therefore vital that all levels of management are well-acquainted with these issues and that the senior management accountant is present at the strategy-planning process from the outset. The management accounting discipline is therefore inseparable from the corporate planning processes at a company. Here is a review of key concepts of the strategy-planning process:

Strategy: Various definitions exist but a straightforward view is “Strategy is a plan of action designed to achieve a particular goal”.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 8 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Strategic planning: An organisation’s process for ascertaining the strategy it should adopt, taking into account what they want to do, how they are going to do it and what resources they will need. Strategic planning covers where the organisation is planning on going, impacts on the whole organisation and involves the long term view. Note the distinction in what is meant by “long term” (for example the “long term” is different when comparing the airline industry with the fashion industry.)

Strategy is made at different levels of the organization (recall Anthony’s hierarchy):

Corporate strategy: covers the “big view” of the organisation. It answers the question “What business or businesses should we be in?

Business strategy: the strategy of a single business organisation or the strategies of strategic business units (SBUs)

Functional (or operational) strategy: the functional strategies involving items such as marketing, IT and HRM that support the business strategy.

It is important that the strategies support each other. For example, if the Business Strategy of a SBU revolves around providing high quality consultancy advice on certain areas, a functional strategy for HRM of minimising labour costs would cause problems.

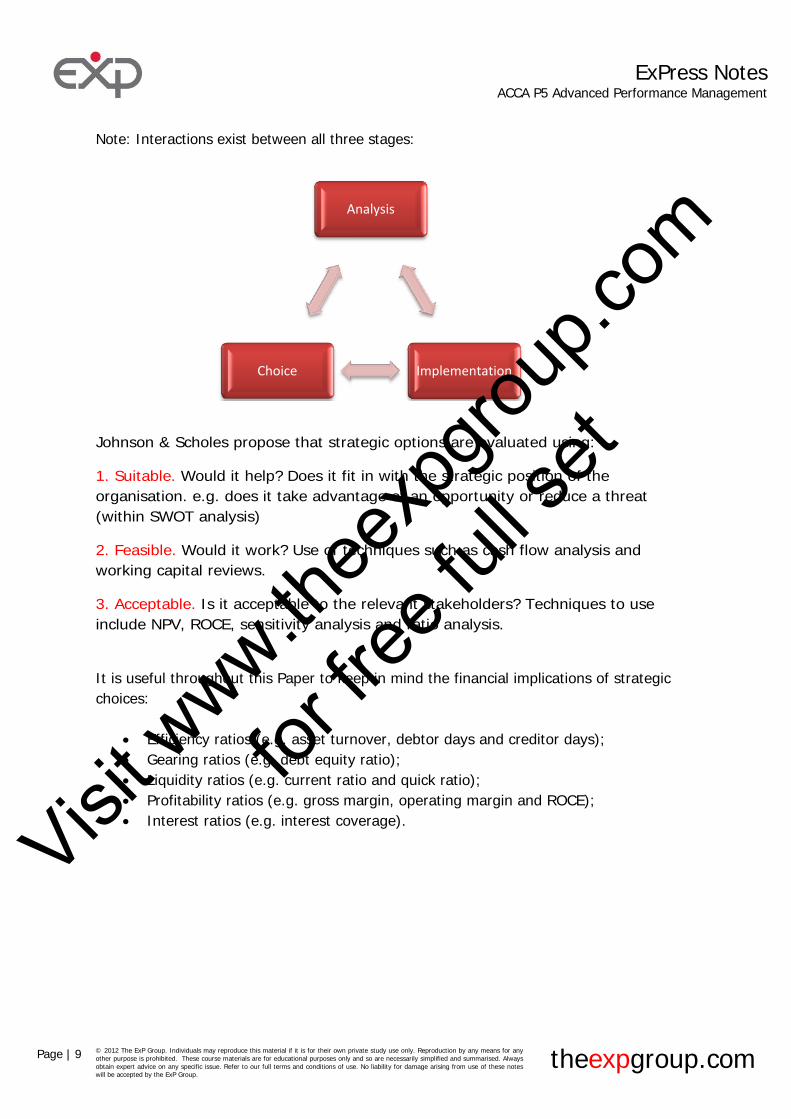

Johnson & Scholes describe the strategic planning process as consisting of three stages:

1. Analysis

2. Choice; and

3. Implementation

Corporate

Business

Functional

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 9 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Note: Interactions exist between all three stages:

Johnson & Scholes propose that strategic options are evaluated using:

1. Suitable. Would it help? Does it fit in with the strategic position of the organisation. e.g. does it take advantage of an opportunity or reduce a threat (within SWOT analysis)

2. Feasible. Would it work? Use of techniques such as cash flow analysis and working capital reviews.

3. Acceptable. Is it acceptable to the relevant stakeholders? Techniques to use include NPV, ROCE, sensitivity analysis and ratio analysis.

It is useful throughout this Paper to keep in mind the financial implications of strategic choices:

Efficiency ratios (e.g. asset turnover, debtor days and creditor days); Gearing ratios (e.g. debt equity ratio); Liquidity ratios (e.g. current ratio and quick ratio); Profitability ratios (e.g. gross margin, operating margin and ROCE); Interest ratios (e.g. interest coverage).

Analysis

ImplementationChoice

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 10 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Other analytic techniques covered in earlier papers (F5) are relevant to this one:

KEY KNOWLEDGESWOT analysis

Strengths (internal) e.g. resources and capabilities

Weaknesses (internal) e.g. lack of certain resources or capabilities

Opportunities (external) e.g. arrival of new technology

Threats e.g. arrival of substitute product

Alternative budgeting models The strengths and weaknesses of the various models in existence should be considered: Fixed

A fixed budget is not adjusted to the actual volume of output (activity level)

Flexible vs. Flexed

The distinction is sometimes overlooked: Flexible: designed to change according to actual volumes of output; usually done

before the start of the budgetary period as a sort of scenario planning;

Flexed: This is done “after the fact” and is based on the actual level of activity achieved.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 11 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Rolling

A rolling budget is one which is revised on an on-going basis by comparing actual results with the original budget when one period has expired, while simultaneously adding a new period to the budget period.

Example

An annual budget which is kept rolling on a quarterly basis, for example, may start with an (original) January – December forecast. At the end of March, the entire budget is revised on the basis of the first quarter, and a new set of forecasts relating to April (current year) – March (next year) are prepared, i.e. always with a 12 month range into the future.

Zero-based (ZBB)

Each year, budget owners must justify the entire budget (build it from zero) At odds with incremental budgeting (where only changes need justification, hence

encouraging the “spend it or lose it” mentality) A three-step approach to ZBB:

1. Define “decision packages” (i.e. activities that result in costs or revenues), distinguishing between “mutually exclusive packages” (alternative activities to achieve the same result) and “incremental packages” (base level of input needed + additional inputs)

2. Evaluate and rank packages (based on the benefit to the organisation) 3. Allocate resources across packages, considering ranking and seniority of

responsible managers

Activity-based (ABB)

No budget owners (departments, functions), but budgeted activity cost (ABC costing) Budgeted activity cost = demand for activity * unit cost of activity More detailed and accurate than traditional budgets, especially regarding indirect

costs

Incremental Such budgets are based on what went on during the period before. Typically, this approach results in modest changes and adjustments to the earlier budget. At worst, they retain and perpetuate inefficiencies and old assumptions. This might be termed the “lazy man’s budget”. “Beyond” budgeting: The future of budgets and alternatives to budgeting

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 12 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Can you imagine a budget process that takes up to six months and 20 percent of management's time?

Problems encountered when using conventional budgets:

• They invite “gaming” of the system;

• They can be inflexible;

• They are often imposed from the top – “Top Down”;

• There is an indirect connection with the company’s strategy;

• They are used for too many different purposes;

• They reinforce a centralizing tendencies in the company

The rationale for moving “beyond” budgeting

Context: Rapidly changing markets triggering the need for real-time response to events Aim of alternatives to budgeting Eliminate redundant elements of the traditional budgetary process, that is, elements performed at least as effectively and rigorously within other strategic management processes (e.g. communication and control) The pre-requisites of the “beyond budgeting” model, as alternative to traditional budgeting

Decentralization and divisional management empowerment within leaner organisational structure

Clear communication of company goals, of performance targets and of boundaries within which local/divisional managers have the freedom to act

Strong management performance evaluation system, based on dissipated responsibility, authority and accountability across responsibility centres

Head-office acts as provider of internal support services to responsibility centres, with most of co-ordination among centres achieved through market forces

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 13 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Implementation

Implementation of a Beyond Budgeting capability has decisive organizational implications.

These include:

Decentralisation

Customer focus

Management philosophy

Managing without budgets requires consideration of the following:

Planning Coordination Information Target setting Performance management Rewards

Business structure and management accounting Management accounting systems must be appropriate to the structure of the businesses they serve. We have seen that that “beyond budgeting” is based on the recognition of the limitations of traditional management accounting techniques, particularly in rapidly changing business environments. The way in which a business is organized – e.g. a functional, divisional or network form – has implications for the way in which performance is managed and measured. Modern approaches to business structure are “integrative” in nature, as they explicitly take into account the linkages between people, operations, strategy and technology. One example is: Porter’s value chain Visi

t www.th

eexp

group

.com

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 14 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

SupportActivities

Primary Activities

Technological Development

Human Resource Management

Firm Infrastructure

Procurement

Inbo

und

Logi

stic

s

Ope

ratio

ns

Out

boun

dLo

gist

ics

Mar

ketin

g &

Sal

es

Serv

ice

Strategic Choice to Purchase Some Activities From Outside Suppliers

Supp

ort

Prim

ary

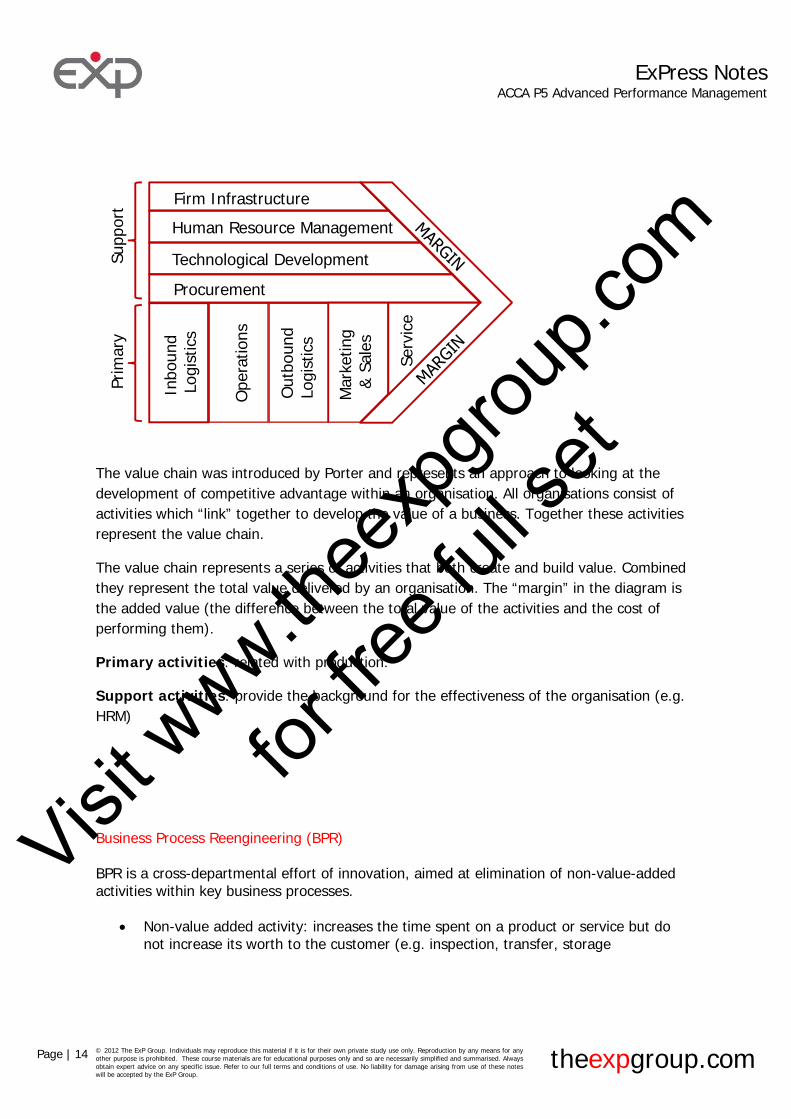

The value chain was introduced by Porter and represents an approach to looking at the development of competitive advantage within an organisation. All organisations consist of activities which “link” together to develop the value of a business. Together these activities represent the value chain.

The value chain represents a series of activities that both create and build value. Combined they represent the total value delivered by an organisation. The “margin” in the diagram is the added value (the difference between the total value of the activities and the cost of performing them).

Primary activities: related with production.

Support activities: provide the background for the effectiveness of the organisation (e.g. HRM)

Business Process Reengineering (BPR) BPR is a cross-departmental effort of innovation, aimed at elimination of non-value-added activities within key business processes.

Non-value added activity: increases the time spent on a product or service but do not increase its worth to the customer (e.g. inspection, transfer, storage

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 15 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

The Business Process Reengineering (BPR) Cycle:

Running a full BPR cycle usually involves substantial investment in information technology and retraining

Effects of adopting BPR

If successful, it brings dramatic improvement in operating performance, operating versatility and customer service.

Process teams replace functional departments

More multi-skilled staff needed

More staff empowerment, flatter organization structures

McKinsey 7S Model

The organisation can be understood as the sum of the following parts:

Structure Systems Strategy Shared values Style Skills Staff

Identify Processes

Review, Update Analyze As‐Is

Design

To‐Be

Test & Implement

To‐Be

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 16 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Information Technology (IT) and modern management accounting

Information technology has had a dramatic and far-reaching impact on the structure and conduct of business. IT has also been frequently poorly employed at great cost to companies. When implemented well, IT has made it possible for companies to exploit the benefits of:

ABC systems;

e-commerce;

POS (point-of-sales) information to management and suppliers In many cases, the benefits of IT have been an increase in the accuracy of information and faster decision-making.

A review of key IT with reference to business applications

Executive Information Systems (EIS/ESS)

Designed to provide senior management with easy-to-use information pulled out from internal and external sources

Features: flexible, sophisticated, real-time responsiveness

Management Information Systems (MIS)

Designed to provide summarised information files used for management accounting and reporting purposes (i.e. reporting enabling management to make timely structured decisions for planning, controlling and directing activities)

o Structured decisions: recurrent and relatively simple decisions addressing repetitive situations in a deterministic environment

Features: relatively inflexible, focused on internal processes

Enterprise-Wide Resource Planning (ERP) – discussed in Chapter 3

Decision Support Systems (DSS)

Combine data and analytical models to support management decision making on issues which are exposed to significant uncertainty

Provide the decision maker with alternatives, evaluating them under a range of possible conditions

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 17 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Expert Systems (ES)

A form of DSS consisting of a specialised database and a set of rules on how input data should be correlated and interpreted in order to indicate the best course of action

Example: loan application ES

KEY KNOWLEDGEMendelow Matrix

This gives an indication of how directors of a business should prioritise their time and give relative weighting to different stakeholder claims in the event of stakeholder conflict.

Leve

l of

influ

ence

Level of interest

Low High

Low Minimal effort required Keep informed

High Keep satisfied Key players (core stakeholders)

Ethical Issues An ethical approach to doing business is not just a matter of personal virtue, but needs to be addressed by policy (and action) at the company level as well. Ethical frameworks are not merely “nice to have”, but are considered crucial to building long-term professionalism. Their absence can undermine motivation and the sense of purpose a company must have in order to succeed.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 18 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Chapter 2

External Influences on Organisational Performance

START Effectiveness of Management Accounting Techniques

Because the buisness environment is changing so rapidly, it is important to be able to assess the effectiveness of traditional management accounting techniques and their relevance to business orgainisations in particular circumstances.

KEY KNOWLEDGE Risk and Uncertainty

Risk, whichever way it is defined, is a quantification of probability. In other words, it is susceptible to measurement, statistically or mathematically. Risk may be viewed as relating to objective probabilities. Uncertainty, in contrast to risk, is not capable of being quantified. It has also been referred to as subjective probability (or unmeasurable uncertainty).

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 19 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Expected Value

Profit/(Loss) Probability

Expected Value

340 10% 34.0766 20% 153.2278 50% 139.0450 18% 81.0

(230) 2% (4.6)100% 402.6

KEY KNOWLEDGEMaximax, maximin and minimax regret

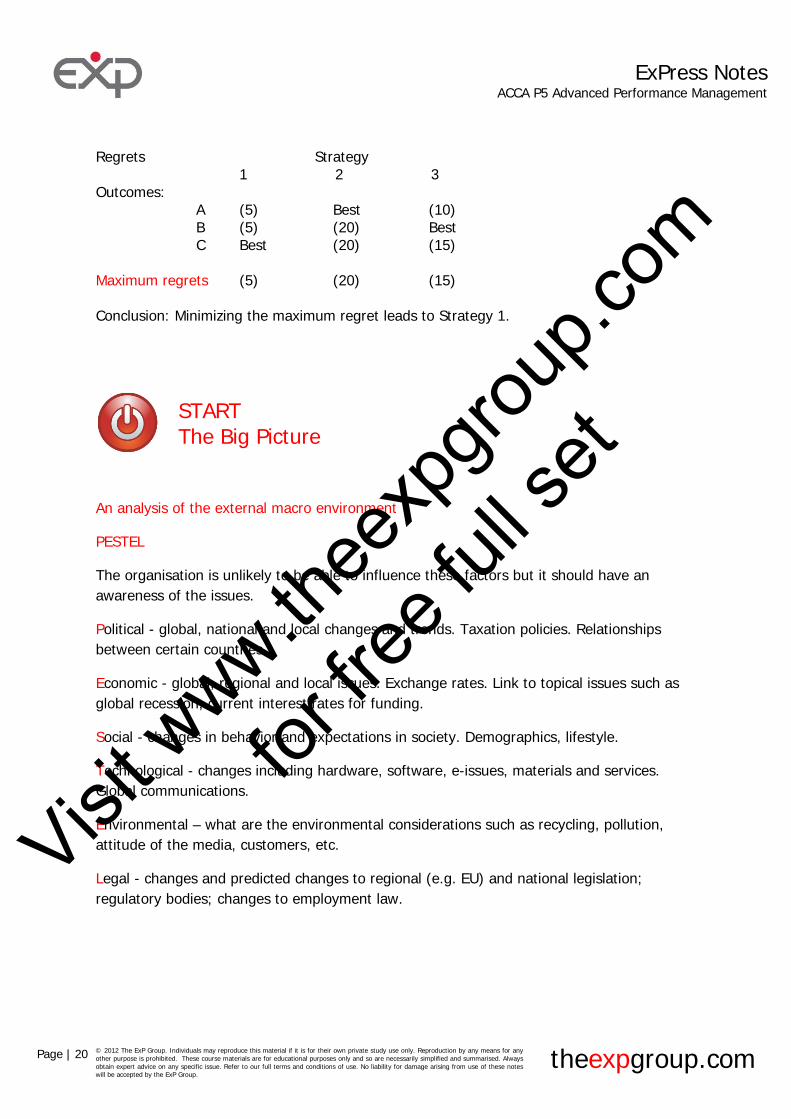

In the absence of (numerical) probabilities, a decision maker may act on the basis of his attitude toward uncertainty. Here are examples of three techniques as they relate to the following choices regarding developing a business: Profits Strategy 1 2 3 Outcomes: A 25 30 20 B 50 35 55 C 60 40 45 Maximax – going for the upside: Chooses Strategy 1 (to keep the door open to a profit of 60). Maximin – limit the downside: Choose Strategy 2 (one cannot do worse than 30). Minimax regret – limit the opportunity cost of getting it wrong. To determine this, one needs to quantify the “regrets” under each Outcome. For example: If the Outcome turns out to be A, then Strategy 2 (=30) would have been the best strategy. Regrets: Choosing Strategy 1 (=25) would have “missed” by 5 (30-25); while Choosing Strategy 3 (=20) would have “missed” by 10 (30-20). We can modify the table above to show all the regrets (opportunity costs) under each Outcome:

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

ExPress NotesACCA P5 Advanced Performance Management

Page | 20 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group.

theexpgroup.com

Regrets Strategy 1 2 3 Outcomes: A (5) Best (10) B (5) (20) Best C Best (20) (15) Maximum regrets (5) (20) (15) Conclusion: Minimizing the maximum regret leads to Strategy 1.

START The Big Picture

An analysis of the external macro environment

PESTEL

The organisation is unlikely to be able to influence these factors but it should have an awareness of the issues.

Political - global, national and local changes and trends. Taxation policies. Relationships between certain countries.

Economic - global, regional and local issues. Exchange rates. Link to topical issues such as global recession, current interest rates for funding.

Social - changes in behavior and expectations in society. Demographics, lifestyle.

Technological - changes including hardware, software, e-issues, materials and services. Global communications.

Environmental – what are the environmental considerations such as recycling, pollution, attitude of the media, customers, etc.

Legal - changes and predicted changes to regional (e.g. EU) and national legislation; regulatory bodies; changes to employment law.

Visit w

ww.thee

xpgro

up.co

m

for fre

e full

set

Related Documents