ACCA Paper F8 (INT) Audit and Assurance June 2011 Revision Mock – Answers To gain maximum benefit, do not refer to these answers until you have completed the final assessment questions and submitted them for marking.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACCA

Paper F8 (INT)

Audit and Assurance

June 2011

Revision Mock – Answers

To gain maximum benefit, do not refer to these answers until you have completed the final assessment questions and submitted them for marking.

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

2 KAPLAN PU BL ISHING

© Kaplan Financial Limited, 2011

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

All rights reserved. No part of this examination may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission from Kaplan Publishing.

REVIS ION MOCK : ANSWERS

KAPLAN PU BL ISHING 3

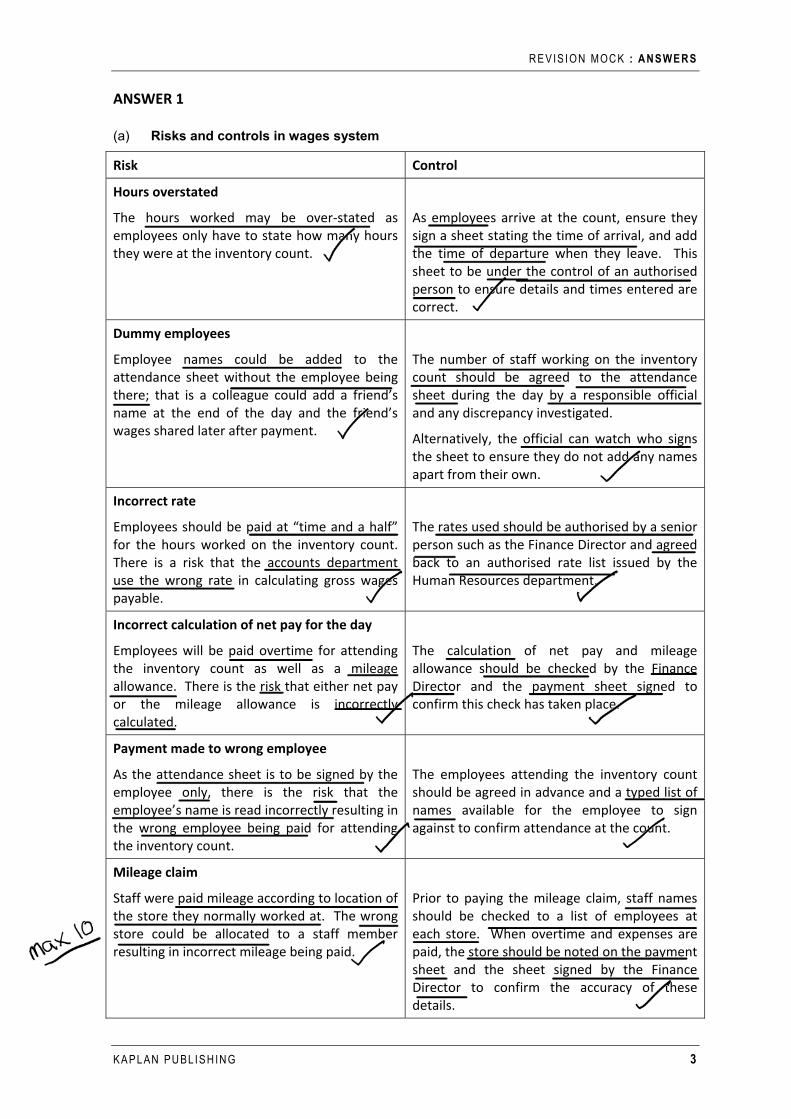

ANSWER 1

(a) Risks and controls in wages system

Risk Control

Hours overstated

The hours worked may be over-stated as employees only have to state how many hours they were at the inventory count.

As employees arrive at the count, ensure they sign a sheet stating the time of arrival, and add the time of departure when they leave. This sheet to be under the control of an authorised person to ensure details and times entered are correct.

Dummy employees

Employee names could be added to the attendance sheet without the employee being there; that is a colleague could add a friend’s name at the end of the day and the friend’s wages shared later after payment.

The number of staff working on the inventory count should be agreed to the attendance sheet during the day by a responsible official and any discrepancy investigated.

Alternatively, the official can watch who signs the sheet to ensure they do not add any names apart from their own.

Incorrect rate

Employees should be paid at “time and a half” for the hours worked on the inventory count. There is a risk that the accounts department use the wrong rate in calculating gross wages payable.

The rates used should be authorised by a senior person such as the Finance Director and agreed back to an authorised rate list issued by the Human Resources department.

Incorrect calculation of net pay for the day

Employees will be paid overtime for attending the inventory count as well as a mileage allowance. There is the risk that either net pay or the mileage allowance is incorrectly calculated.

The calculation of net pay and mileage allowance should be checked by the Finance Director and the payment sheet signed to confirm this check has taken place.

Payment made to wrong employee

As the attendance sheet is to be signed by the employee only, there is the risk that the employee’s name is read incorrectly resulting in the wrong employee being paid for attending the inventory count.

The employees attending the inventory count should be agreed in advance and a typed list of names available for the employee to sign against to confirm attendance at the count.

Mileage claim

Staff were paid mileage according to location of the store they normally worked at. The wrong store could be allocated to a staff member resulting in incorrect mileage being paid.

Prior to paying the mileage claim, staff names should be checked to a list of employees at each store. When overtime and expenses are paid, the store should be noted on the payment sheet and the sheet signed by the Finance Director to confirm the accuracy of these details.

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

4 KAPLAN PU BL ISHING

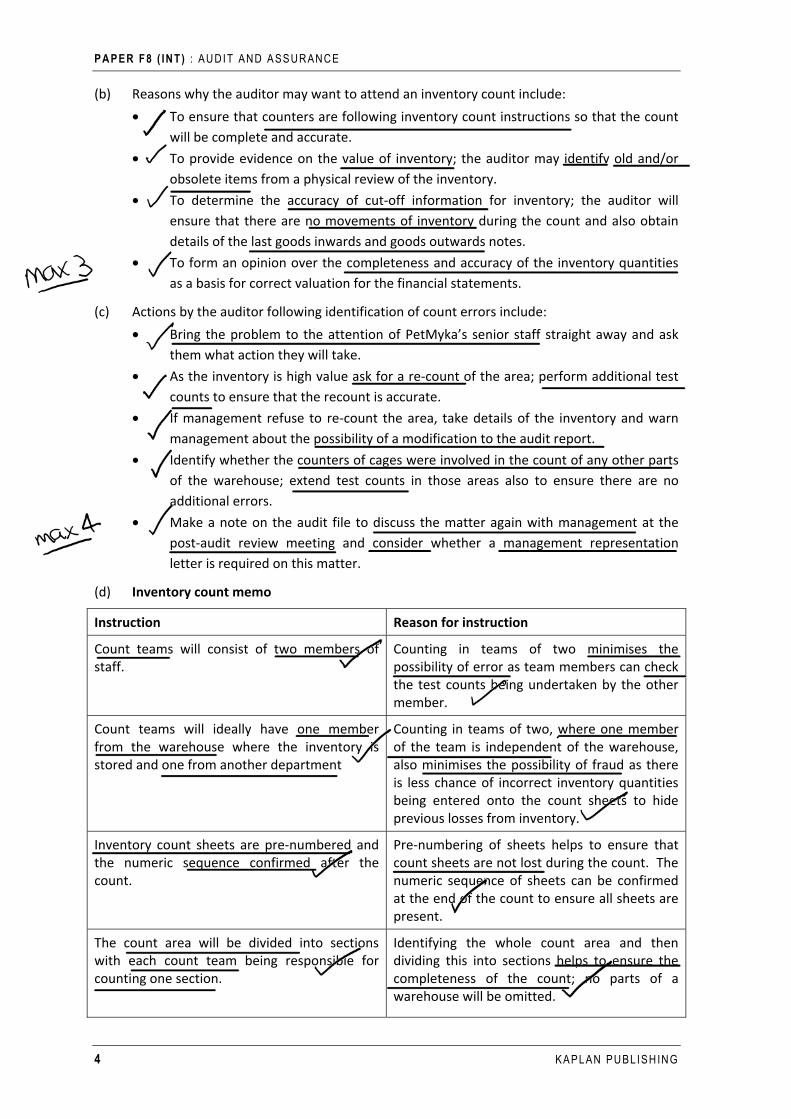

(b) Reasons why the auditor may want to attend an inventory count include:

• To ensure that counters are following inventory count instructions so that the count will be complete and accurate.

• To provide evidence on the value of inventory; the auditor may identify old and/or obsolete items from a physical review of the inventory.

• To determine the accuracy of cut-off information for inventory; the auditor will ensure that there are no movements of inventory during the count and also obtain details of the last goods inwards and goods outwards notes.

• To form an opinion over the completeness and accuracy of the inventory quantities as a basis for correct valuation for the financial statements.

(c) Actions by the auditor following identification of count errors include:

• Bring the problem to the attention of PetMyka’s senior staff straight away and ask them what action they will take.

• As the inventory is high value ask for a re-count of the area; perform additional test counts to ensure that the recount is accurate.

• If management refuse to re-count the area, take details of the inventory and warn management about the possibility of a modification to the audit report.

• Identify whether the counters of cages were involved in the count of any other parts of the warehouse; extend test counts in those areas also to ensure there are no additional errors.

• Make a note on the audit file to discuss the matter again with management at the post-audit review meeting and consider whether a management representation letter is required on this matter.

(d) Inventory count memo

Instruction Reason for instruction

Count teams will consist of two members of staff.

Counting in teams of two minimises the possibility of error as team members can check the test counts being undertaken by the other member.

Count teams will ideally have one member from the warehouse where the inventory is stored and one from another department

Counting in teams of two, where one member of the team is independent of the warehouse, also minimises the possibility of fraud as there is less chance of incorrect inventory quantities being entered onto the count sheets to hide previous losses from inventory.

Inventory count sheets are pre-numbered and the numeric sequence confirmed after the count.

Pre-numbering of sheets helps to ensure that count sheets are not lost during the count. The numeric sequence of sheets can be confirmed at the end of the count to ensure all sheets are present.

The count area will be divided into sections with each count team being responsible for counting one section.

Identifying the whole count area and then dividing this into sections helps to ensure the completeness of the count; no parts of a warehouse will be omitted.

REVIS ION MOCK : ANSWERS

KAPLAN PU BL ISHING 5

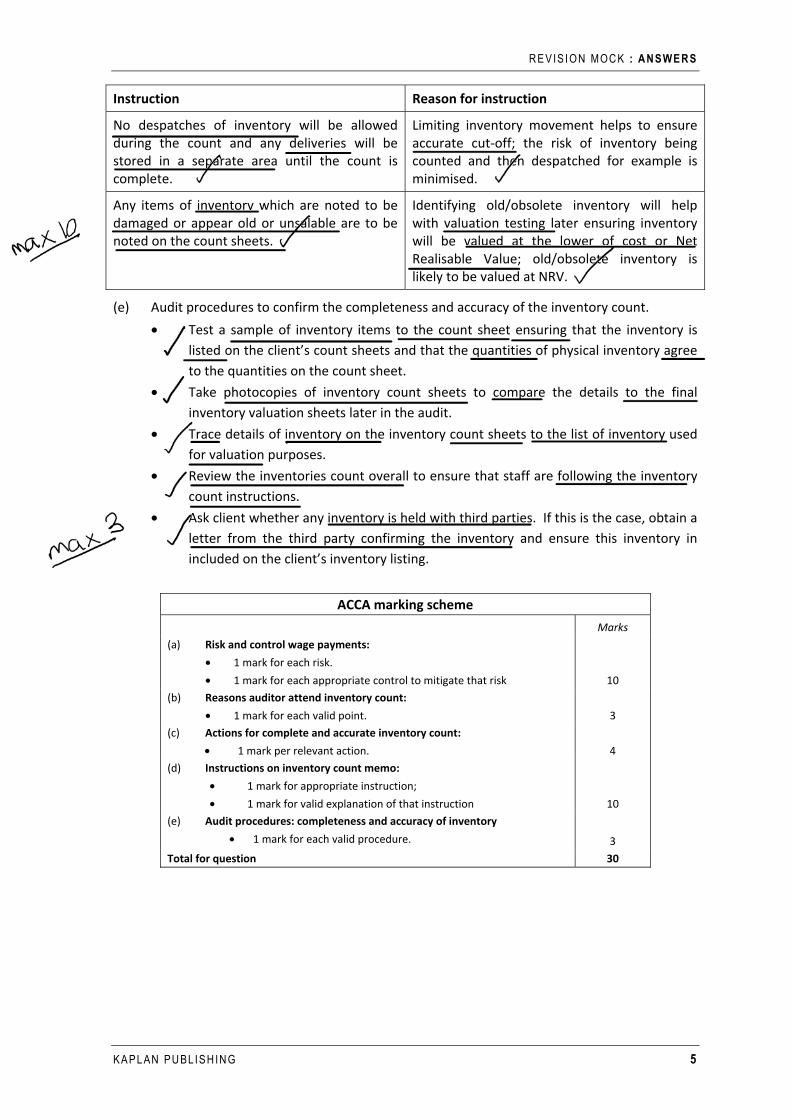

Instruction Reason for instruction

No despatches of inventory will be allowed during the count and any deliveries will be stored in a separate area until the count is complete.

Limiting inventory movement helps to ensure accurate cut-off; the risk of inventory being counted and then despatched for example is minimised.

Any items of inventory which are noted to be damaged or appear old or unsalable are to be noted on the count sheets.

Identifying old/obsolete inventory will help with valuation testing later ensuring inventory will be valued at the lower of cost or Net Realisable Value; old/obsolete inventory is likely to be valued at NRV.

(e) Audit procedures to confirm the completeness and accuracy of the inventory count.

• Test a sample of inventory items to the count sheet ensuring that the inventory is listed on the client’s count sheets and that the quantities of physical inventory agree to the quantities on the count sheet.

• Take photocopies of inventory count sheets to compare the details to the final inventory valuation sheets later in the audit.

• Trace details of inventory on the inventory count sheets to the list of inventory used for valuation purposes.

• Review the inventories count overall to ensure that staff are following the inventory count instructions.

• Ask client whether any inventory is held with third parties. If this is the case, obtain a letter from the third party confirming the inventory and ensure this inventory in included on the client’s inventory listing.

ACCA marking scheme

Marks

(a) Risk and control wage payments:

• 1 mark for each risk.

• 1 mark for each appropriate control to mitigate that risk 10

(b) Reasons auditor attend inventory count:

• 1 mark for each valid point. 3

(c) Actions for complete and accurate inventory count:

• 1 mark per relevant action. 4

(d) Instructions on inventory count memo:

• 1 mark for appropriate instruction;

• 1 mark for valid explanation of that instruction 10

(e) Audit procedures: completeness and accuracy of inventory

• 1 mark for each valid procedure. 3

Total for question 30

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

6 KAPLAN PU BL ISHING

ANSWER 2

(a) Observation. This is to look or observe a process being performed by others such as inventory counting by the client’s personnel.

External confirmation. This is audit evidence obtained by the auditor directly from a third party, either in written or electronic format.

Recalculation. This consists of checking the mathematical accuracy of documents or records.

Reperformance. This is where the auditor independently executes procedures or controls already performed as part of the entity’s internal control systems.

Analytical procedures. This is the evaluation of financial information through analysis of plausible relationships in both financial and non-financial data.

Inquiry. This consists of seeking information from knowledgeable persons (financial and non-financial) both within and external to the entity being audited.

(b) The purpose of a management representation letter is:

• To obtain confirmation that management and those charged with governance, have fulfilled their responsibility for the preparation of the financial statements; and

• To provide corroborating audit evidence on matters which otherwise would have been difficult to obtain sufficient relevant and reliable evidence by any other means.

Auditor actions if management refuse to provide this letter include:

• Discuss the matter with management to determine why the letter will not be provided.

• Offer to draft the letter for management so they only have to sign it.

• Re-asses the integrity of management and the possible effect on other evidence obtain from management.

• Inform management of the consequences of not providing the letter.

• If the letter still cannot be obtained, then modify the audit report with a qualified opinion; sufficient audit evidence has not been obtained.

ACCA marking scheme

Marks

(a) Audit procedures:

• 1/2 mark for each procedure, 1/2 mark for explanation of that procedure Max 5

(b) Management representation letter:

• 2 marks for purpose of letter

• 1 mark for each valid action (maximum 4 marks) 5

Total 10

REVIS ION MOCK : ANSWERS

KAPLAN PU BL ISHING 7

ANSWER 3

(a) Audit risk refers to the risk of an auditor expressing an inappropriate audit opinion. If audit risk is unacceptably high an audit firm will not be able to, or may choose not to, carry out an audit for a potential audit client. Consideration at the client acceptance stage will include the auditor’s actual or perceived independence and whether there are sufficient (or any!) safeguards available to overcome the risk.

(b) Production of Financial Statements

The directors of WH13 expect their auditors to produce the financial statements of the company. While producing financial statements is not barred for a non-listed company, this does provide the audit firm with a self-review threat of reviewing its own work.

To alleviate this threat, different staff will be needed to produce and then audit the financial statements of WH13.

Audit deadline

The audit report is expected in the next four weeks. This is difficult for MacPherson to achieve due to existing client commitments and being a first year audit – obtaining sufficient knowledge of the client to be able to provide an audit to an appropriate standard may require additional time.

To alleviate this threat, either more time is required to carry out the audit or MacPherson must decline the audit.

Finance Director’s son employed in audit firm

One of the reasons for MacPherson being approached to perform the audit of WH13 is that the Finance Director’s son is currently employed in the audit firm. This is a risk to MacPherson because if the Finance Director’s son is involved in the audit he will not be independent due to association with the Finance Director. He may be tempted to ignore any errors found.

To alleviate this threat, the Finance Director’s son must not be part of the audit team for WH13.

Director’s involved in tax investigation

Two years ago the directors of WH13 were involved in a tax investigation by the tax authorities in their country. While no prosecution was made, there is the implication that the directors may continue to attempt to minimise their own tax liabilities by potentially illegal means. This provides an association risk for MacPherson in that the audit firm may not want to be associated with the directors; adverse publicity on the directors may also affect the audit firm.

This threat can only be alleviated by not accepting the audit assignment.

Loan application to bank

WH13 is currently making trading losses and may find it difficult to continue in business without continued financial support from their bankers. One of the reasons for wanting the audit report so quickly is so the audited financial statements can be presented to the bank to support further borrowings. This presents a potential advocacy threat to MacPherson in that they may be seen to be supporting their audit client by producing the audit report required by their client.

This threat can be alleviated by either not taking on the audit work or by ensuring that sufficient time is available to carry out an audit according to the ISAs.

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

8 KAPLAN PU BL ISHING

Previous auditors

WH13’s previous auditors declined to accept re-appointment at the previous AGM; MacPherson is not aware of any reason why this action was taken. However, as one firm of auditors has decided not to be associated with WH13, then MacPherson need to find out whether they should be associated with WH13.

This threat can be alleviated by contacting the previous auditors of WH13 to determine whether there were any professional reasons why nomination was declined. The directors of WH13 can also be approached although their opinion may be biased.

(c) There are three safeguards provided within the auditing profession’s conceptual framework that aim to ensure an auditor’s work is maintained at a required standard.

Profession

This is guidance which requires and auditor to work in specific ways and have appropriate knowledge to carry out that work. In overview, the auditor must have knowledge to carry out an audit; this knowledge is obtained partly from examination training, partly from Continued Professional Development studies and partly from experience on-the-job. Some safeguards will also be jurisdiction specific such as legal requirements stating who can and cannot be an auditor.

Individual

Auditors are expected to ensure that they have the necessary knowledge and experience to carry out audit activities. This will include ensuring that they have knowledge of Auditing Standards so audits can be carried out correctly and also recognising ethical threats so these can be dealt with on a timely basis.

Work

Finally, there are safeguards implemented within the audit firm itself to try and ensure that audits are carried out to the appropriate standard.

Firstly, partners set the overall “tone” of the firm by following ethical standards themselves and making it clear that all staff are expected to follow those standards also.

Secondly, there is a system of controls within the audit firm which ensure audit work is carried out to appropriate standards. These controls include supervision of audit staff and a series of reviews of work by senior staff up to partner level. External reviews by the ACCA may also be carried out to ensure audit work is maintained at a high standard.

ACCA marking scheme Marks

(a) Audit risk:

• Up to 2 marks for audit risk explanation 2

(b) Issues:

• 1 mark for each issue identified

• 1 mark for explanation of how that issue can be alleviated 12

(c) Safeguards

• Up to 2 marks for discussion of each safeguard 6

Total 20

REVIS ION MOCK : ANSWERS

KAPLAN PU BL ISHING 9

ANSWER 4

(a) ISA 610 Using the work of internal audit is relevant to deciding the extent of reliance. The extent of reliance on internal audit depends on factors such as:

Whether members of the internal audit are qualified accountants. Qualification implies not only a higher standard of work but also following the ethical guidance of their institute.

How independent the internal audit function is within the company. Reporting to an audit committee rather than the Finance Director implies a higher degree of independence.

Whether work is properly planned, supervised and reviewed. Maintaining an appropriate standard of work implies that reliance can be placed on internal audit.

Whether internal audit recommendations are actioned by the company. If internal audit recommendations are actually followed, this implies that the department is thought to be of high quality and recommendations are of value.

(b) Advantages of outsourcing internal audit

Cost

Outsourcing may provide some cost benefits to Farnsworth as a fixed price contract can be agreed with the assurance firm. This cost may be less than employing six staff, especially if the firm is more efficient.

Expertise

The assurance firm will be able to provide staff with experience of internal audit in many companies. This may improve the quality of internal audit within Farnsworth, especially as the existing internal audit department does not have any qualified staff.

Staff turnover

The risk of staff turnover is passed onto the outsourcing firm. As Farnsworth does have a high staff turnover in the internal audit department, the company will avoid the administrative procedures and costs of employing new staff.

Improve independence

The assurance firm will be able to provide an independent assessment of the control systems within Farnsworth. Although there is no indication that the current internal audit department are not carrying out their duties correctly, the external firm will avoid familiarity and self-interest threats which can affect internal audit.

Audit methodology

Staff within Farnsworth’s internal audit department appear to view their job as an opportunity to gain experience. This may mean they are not experts in internal audit. An assurance firm will have up-to-date knowledge and experience of audit methodologies and may therefore provide a higher quality of work.

Disadvantages of outsourcing internal audit

Lack of knowledge

An external firm may not have detailed knowledge of the Farnsworth Company meaning that audit procedures will not be as effective as those provided by internal auditors. This may not be an issue in Farnsworth as internal audit staff do not appear to remain in the company for long periods of time anyway.

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

10 KAPLAN PU BL ISHING

Cost

Associated with lack of knowledge is the time and therefore cost that an external firm will incur obtaining knowledge of Farnsworth’s systems. It may be more expensive to outsource the department, and the assurance firm may require a contract of three to five years to ensure any loss in the first year of service is recouped in subsequent years.

Flexible working

The internal audit department in Farnsworth appears to be very flexible in travelling to different shops at short notice. An external firm may not be able to provide this flexibility due to lack of staff availability resulting in a decreased standard of service.

Annual contract renewal

Provision for an annual renewal of the outsourcing contract may limit the assurance provided by the contracting firm. There will be a temptation to provide reports expected by the directors in order to obtain contract (and therefore fee) renewal. Outsourcing may therefore not provide the enhanced standard of work expected.

(c) Benefits of carrying out an audit of procurement systems include:

Monitoring suppliers to ensure that the best price is obtained for inventory purchased. With many suppliers, internal audit can ensure that competitive quotes for goods are being obtained.

Ensuring inventory held is sufficient but not excessive. Farnsworth needs to ensure that goods are available for sale when required but also that the level of inventory is not excessive which increases working capital costs. Internal audit can monitor inventory levels to ensure this objective is being achieved.

Goods being sold must be of an appropriate quality to ensure customers are satisfied and limit adverse publicity from customers having to return unsatisfactory goods. The level and reasons for returns can be reviewed and where necessary alternative suppliers recommended where quality is below standard.

ACCA marking scheme Marks

(a) Reliance on internal audit:

• 1 mark for each well-explained point. 4

(b) Outsourcing internal audit

• Up to 2 marks for each well-explained advantage

• Up to 2 marks for each well-explained disadvantage

No limit on marks obtained from advantages or disadvantages Max 12

(c) Benefits from audit of procurement systems

• 1 mark for each valid point 4

Total for question 20

REVIS ION MOCK : ANSWERS

KAPLAN PU BL ISHING 11

ANSWER 5

(a) (i) Event 1

Tubman entering into receivership provides additional evidence of conditions at the statement of financial position date. The amount of €175,000 was owed by Tubman to Fargo at this date and the letter from the Receiver indicates that this amount may now not be paid.

The amount is material to profit (23% of profit) and net assets (15%). The value of receivables is therefore overstated by the material amount of €175,000 and a provision for a bad debt is required.

Event 2

The fire at the Caribbean hotel and the poor quality holidays took place in April, which is after the end of the reporting period. This event is therefore indicative of conditions after the statement of financial position date and so is not an adjusting event; the event could not be foreseen at the end of the reporting period.

No adjustment is needed to the financial statements.

However, a disclosure note may be required as customers have now employed a lawyer to claim compensation from Fargo.

(ii) Event 1

As the bad debt occurred after the end of the reporting period but before the audit report has been signed, the auditor is responsible for ensuring that Fargo’s financial statements are amended. The receivables balance should be decreased and a provision made on the income statement for the €175,000.

Audit procedures will include:

• Obtain a copy of the letter from the Receiver confirming that the balance due from Tubman of €175,000 will not be paid.

• Review the list of receivables making up the statement of financial position balance ensuring that this is the only debt due from Tubman and that the €175,000 is included in this list.

• Obtain the amended financial statements, ensuring that the directors of Fargo have included the provision as outlined above.

• If necessary (e.g. because the auditor is concerned about other receivables not being able to pay Fargo) obtain a letter of representation point confirming the accuracy and recoverability of any remaining outstanding debts.

Event 2

This event took place after the end of the reporting period but before the audit report was signed. The auditor has a responsibility to consider the impact on the compensation claim on the financial statements.

Audit procedures will include:

• Obtain a copy of the letter from the lawyer documenting the claim of the customers of Fargo.

• Discuss the matter with the directors and ask whether they will disclose the event in the financial statements.

PAPER F8 ( INT ) : AU DIT AND ASSURANCE

12 KAPLAN PU BL ISHING

• If disclosure will be made, then ask for the amended financial statements and ensure that disclosure is appropriate.

• If disclosure will not be made, consider whether any disclosure is necessary and inform the directors of this.

• Where disclosure is not made and the auditors consider disclosure is necessary, modify the audit opinion with a qualified opinion on the grounds of a material omission and explain the reason for this modification in the audit report. This is for lack of disclosure (not provision) as the event occurred after the statement of financial position date.

(b) Note that the letter from the lawyer has been received after the audit report has been signed.

Audit procedures will include:

• Initially, discuss the matter with the director to find out what action, if any, they propose to take.

• Ask the directors how likely it is that the claim will be successful.

• Discuss the matter with the lawyer to determine how the €500 per customer was derived.

• If necessary, obtain independent legal advice (or from Fargo’s lawyer) on the likelihood of the claim succeeding.

At present, quantifying any claim will be difficult; the auditor will need to decide whether or not some disclosure is required.

• If the auditor considers that disclosure of the event is required, ask the directors to amend the financial statements. If disclosure is sufficient then an unmodified report can be issued.

• If the directors will not amend the financial statements and the auditor considers that disclosure is necessary, then the auditor needs to consider other methods of bring the matter to the attention of the members. Speaking at the AGM may therefore be appropriate.

ACCA marking scheme Marks

(a) (i) Adjusting and non-adjusting events

For each of the two events

• Up to 2 marks for valid explanation Max 4

(ii) Auditor’s responsibility and audit procedures

For each of the two events

• 1 mark for explanation of auditor responsibility

• 1 mark for each valid audit procedure (max 5 marks) Max 12

(b) Additional audit procedures

• 1 mark for each explained point; 4

Total 20

Related Documents