SAMPLE BPP LEARNING MEDIA ACCA F7 Financial Reporting For exams in June 2014 SAMPLE

ACCA F7

Feb 26, 2016

SAMPLE. ACCA F7. Financial Reporting For exams in June 2014. Key to Icons. SAMPLE. Chapter 1 The conceptual framework. Conceptual framework and GAAP The IASB’s Conceptual Framework The objective of general purpose financial reporting Underlying assumption - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SAMPLE

BPP LEARNING MEDIA

ACCA F7Financial ReportingFor exams in June 2014SAMPLE

SAMPLE

BPP LEARNING MEDIA

Syllabus

Technical content

Question to consider

Answer

Past exam question

Answer to past exam question

Real world example

Diagram

Key model

Tackling the exam

Summary

Case study

Key to Icons

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Chapter 1

The conceptual framework

• Conceptual framework and GAAP• The IASB’s Conceptual Framework• The objective of general purpose

financial reporting• Underlying assumption• Qualitative characteristics of financial

statements• The elements of financial statements• Recognition and measurement of the

elements of financial statements• Fair presentation and compliance with

IFRS

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 1

• Describe what is meant by a conceptual framework of accounting

• Discuss whether a conceptual framework is necessary and what an alternative system might be

• Discuss what is meant by relevance and faithful representation and describe the qualities that enhance these characteristics

• Discuss whether faithful representation constitutes more than compliance with accounting standards

• Indicate the circumstances and required disclosures where a ‘true and fair’ override may apply

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 2

• Discuss what is meant by understandability and verifiability in relation to the provision of financial information

• Discuss the importance of comparability and timeliness to users of financial statements

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 3

• Define what is meant by ‘recognition’ in financial statements and discuss the recognition criteria

• Apply the recognition criteria to assets and liabilities and income and expenses

• Discuss revenue recognition issues and indicate when income and expense recognition should occur

• Demonstrate the role of the principle of substance over form in relation to recognising sales revenue

• Explain the measurement bases of historical cost, fair value / current cost, net realisable value and the present value of future cash flows and compute amounts using these bases

SAMPLE

BPP LEARNING MEDIA

Chapter summary diagram

Need for a conceptual framework

Generally accepted accounting practice

(GAAP)

True and fair view

Advantages and disadvantages

The IASB’s conceptual framework

Conceptual framework and GAAP

The conceptual frameworkSAMPLE

SAMPLE

BPP LEARNING MEDIA

Conceptual Framework and GAAP 1

What is a conceptual framework?• A statement of generally accepted theoretical principles

which form a frame of reference for financial reporting.• These provide a basis for developing new accounting

standards and a platform to evaluate those already in existence.

SAMPLE

BPP LEARNING MEDIA

Conceptual Framework and GAAP 2

Advantages of a conceptual framework• Having a consistent conceptual base should avoid

contradictions and inconsistencies in basic concepts and so produce standardised consistent accounting practices.

• The development of standards is less subject to political pressure.

• A consistent statement of financial position driven or profit or loss driven approach is used.

SAMPLE

BPP LEARNING MEDIA

Conceptual Framework and GAAP 3

Disadvantages of a conceptual framework• Financial statements have many users all with differing

needs. – A single framework cannot satisfy the needs of all

users.– There may be a need for a variety of accounting

standards, each produced for a different purpose with different conceptual bases.

• Having a conceptual framework may not make it any easier to prepare accounting standards.

SAMPLE

BPP LEARNING MEDIA

Conceptual Framework and GAAP 4Generally accepted accounting practice (GAAP)• Comprises the rules, from all sources, which govern

accounting.• The major components include:

– National accounting standards, for example the Financial Accounting Standards Board (FASB) in the USA

– National company law, for example the Companies Act in the UK

– Local stock exchange requirements– Regional bodies, such as the European Union. For

example, an Accounting Directive issued by the EU now requires companies listed on an EU stock exchange to prepare their consolidated financial statements using IFRSs.

SAMPLE

BPP LEARNING MEDIA

The IASB’s Conceptual Framework 1

• Published in September 2010 to update the IASB Framework for the Preparation and Presentation of Financial Statements which was issued in 1989.

• Joint project by the IASB and FASB to be completed in two phases.

SAMPLE

BPP LEARNING MEDIA

The IASB’s Conceptual Framework 2

• Currently comprises four chapters: – Chapters 1 – 3 are from the new Conceptual

Framework for Financial Reporting.– Chapter 4 consists of the parts of the former 1989

Framework which will be updated in phase 2 of the project.

SAMPLE

BPP LEARNING MEDIA

The IASB’s Conceptual Framework 3

• Chapter 1– The objective of general purpose financial reporting

• Chapter 2– The reporting entity (still to be issued)

• Chapter 3– Qualitative characteristics of useful financial

information

SAMPLE

BPP LEARNING MEDIA

The IASB’s Conceptual Framework 4

• Chapter 4– Remaining text of the 1989 Framework– Underlying assumption– The elements of financial statements– Recognition of the elements of financial statements– Measurement of the elements of financial

statements– Concepts of capital and capital maintenance.

SAMPLE

BPP LEARNING MEDIA

The objective of general purpose financial reporting 1

Chapter 1: The objective of general purpose financial reporting• To provide information about the reporting entity that is

useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity

• Such decisions are likely to include:– Decisions to buy, hold or sell equity investments– Assessment of management stewardship and

accountability– Assessment of the entity’s ability to pay employees– Assessment of the security of amounts lent to the entity

SAMPLE

BPP LEARNING MEDIA

The objective of general purpose financial reporting 2

Chapter 1: The objective of general purpose financial reporting (cont.)• The information required therefore relates to:

– The economic resources of the entity– The claims against the entity and– Changes in the entity’s economic resources and claims

• This information should be prepared on an accruals basis.

SAMPLE

BPP LEARNING MEDIA

Underlying assumption

Chapter 4: The Framework (1989) remaining textUnderlying assumption• Going concern:

– The financial statements are normally prepared on the assumption that the entity is a going concern and will continue to trade for the foreseeable future.

• It is assumed that the entity has neither the intention not the need to liquidate the business or curtail major operations.

• If it did the financial statements would be prepared on a different basis and this basis would be disclosed.

SAMPLE

BPP LEARNING MEDIA

Qualitative characteristics of financial information 1

Chapter 3: Qualitative characteristics of useful financial information• These describe the attributes that information needs to

have in order for it to be most useful for existing and potential investors, lenders and other creditors for making decisions about the reporting entity.

• They are categorised into two categories:– Fundamental qualitative characteristics– Enhancing qualitative characteristics

SAMPLE

BPP LEARNING MEDIA

Qualitative characteristics of financial information 2

Fundamental qualitative characteristics

Relevance Faithful representation

Relevant financial information is capable of making a difference in the decisions made by users, ie if it has• Predictive value, and/or• Confirmatory value

Information is material if omitting it or misstating it could influence decisions that users make on the basis of financial information.

To be useful, financial information must faithfully represent the phenomena it purports to represent.A perfect faithful representation would be:• Complete• Neutral• Free from errorMateriality

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Qualitative characteristics of financial information 3

Comparability

Information is more useful if it can be compared with similar information about• Other entities, and• Other periodsConsistency helps achieve comparability

Enhancing qualitative characteristics

Verifiability Timeliness Understandability

Assures users that information faithfully represents the economic phenomena it purports to representVerification can be direct or indirect

Having information available to decision-makers in time to be capable of influencing their decisions

Classifying, characterising and presenting information clearly and concisely

SAMPLE

SAMPLE

BPP LEARNING MEDIA

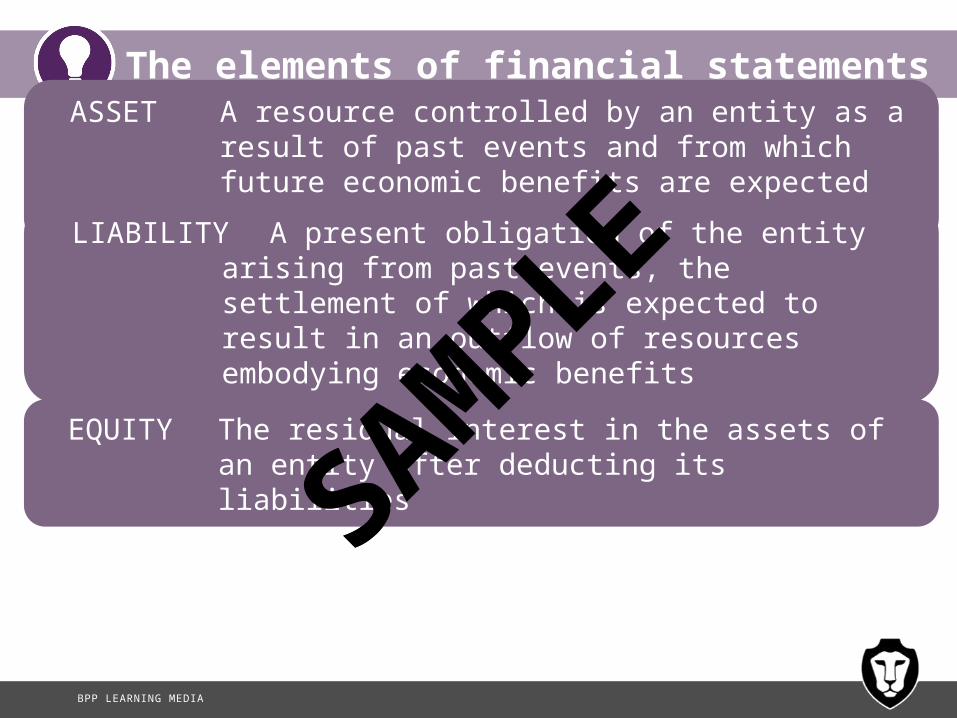

The elements of financial statements 1

Chapter 4: The Framework (1989) remaining textThe elements of financial statements• An item can only be recognised in the financial

statements if it can be defined as one of the following elements:– Asset– Liability– Equity– Income – Expense

SAMPLE

BPP LEARNING MEDIA

The elements of financial statements 2

ASSET A resource controlled by an entity as a result of past events and from which future economic benefits are expected to flow to the entity

LIABILITY A present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow of resources embodying economic benefits

EQUITY The residual interest in the assets of an entity after deducting its liabilitiesSAMPLE

SAMPLE

BPP LEARNING MEDIA

The elements of financial statements 3

INCOME Increases in economic benefits during the period other than contributions from equity participants

EXPENSE Decreases in economic benefits during the period other than distributions to equity participants

SAMPLE

SAMPLE

BPP LEARNING MEDIA

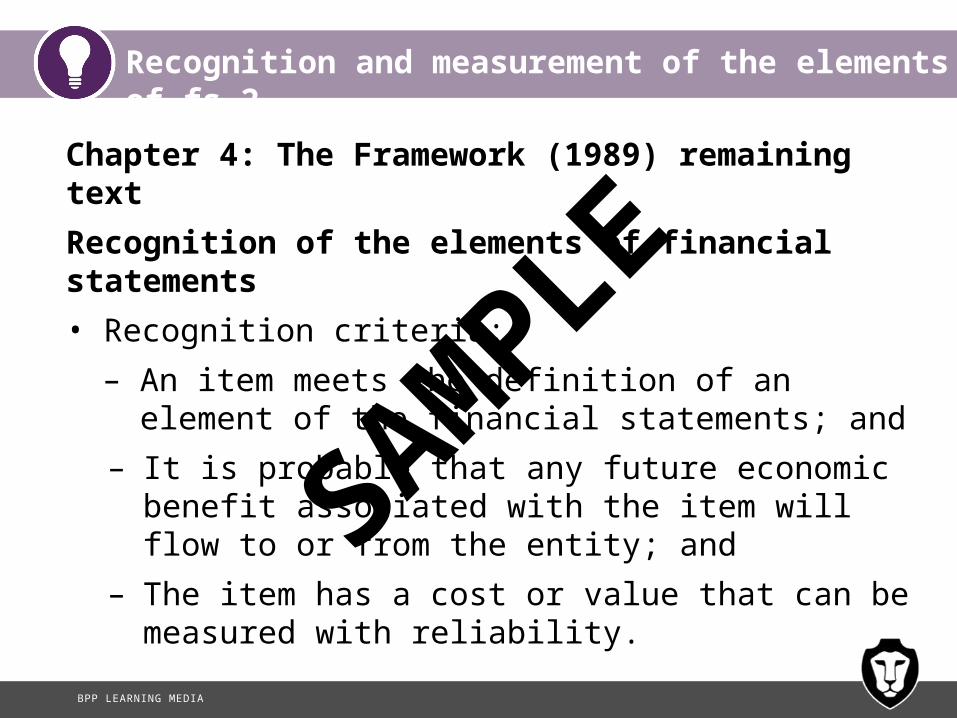

Recognition and measurement of the elements of fs 1

Chapter 4: The Framework (1989) remaining textRecognition of the elements of financial statements• Recognition is the process of recording or showing an

item in the financial statements.• An item can only be recognised in the financial statements

when it satisfies the recognition criteria.

SAMPLE

BPP LEARNING MEDIA

Recognition and measurement of the elements of fs 2

Chapter 4: The Framework (1989) remaining textRecognition of the elements of financial statements• Recognition criteria:

– An item meets the definition of an element of the financial statements; and

– It is probable that any future economic benefit associated with the item will flow to or from the entity; and

– The item has a cost or value that can be measured with reliability.

SAMPLE

BPP LEARNING MEDIA

Case study: Footballers 1

Are transfer fees paid for footballers an asset?

SAMPLE

BPP LEARNING MEDIA

Case study: Footballers 2

Are the recognition criteria satisfied?

• Firstly, is there an asset?– Control– Past event– Expected generation of future economic benefit

SAMPLE

BPP LEARNING MEDIA

Case study: Footballers 3

• Asset?– Control: the football club has purchased the right to

use the player for match fixtures/ training and merchandising (player rights)

– Past event: the transaction to purchase the player– Future economic benefits

SAMPLE

BPP LEARNING MEDIA

Case study: Footballers 4

What are the future economic benefits?

SAMPLE

BPP LEARNING MEDIA

Case study: Footballers 5

• Asset?– Yes, an intangible asset

• Secondly, is there probable future economic benefit?– Yes as discussed above

• Thirdly, can the amount be measured with reliability?– Fee paid → yes– Value of future ticket sales and merchandising → no

• Capitalise only the transfer fee paid as an intangible non-current asset

SAMPLE

BPP LEARNING MEDIA

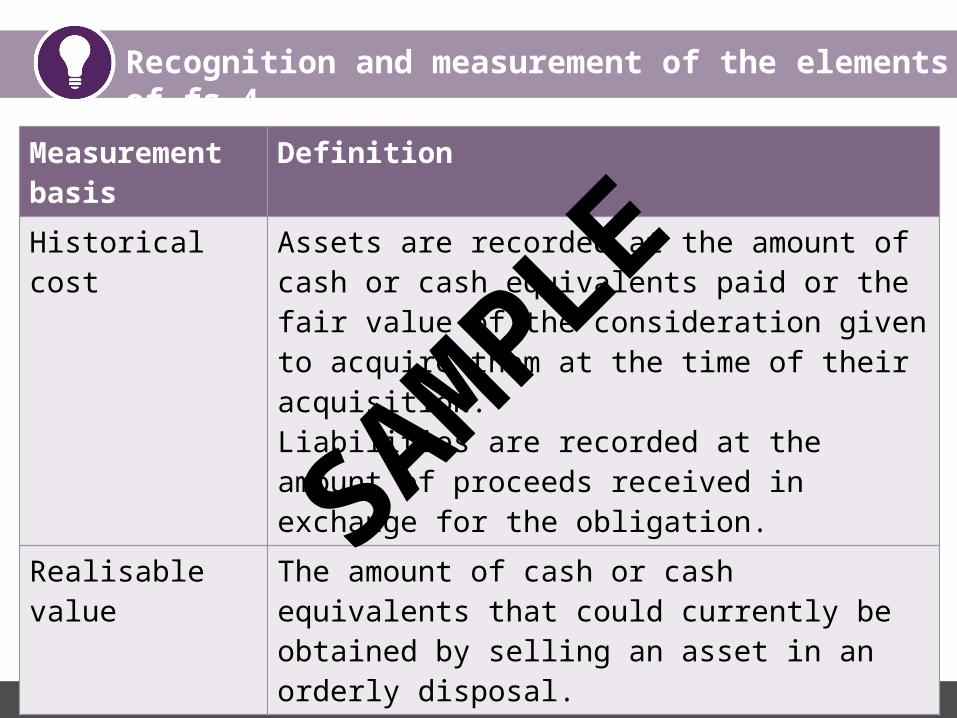

Recognition and measurement of the elements of fs 3

Chapter 4: The Framework (1989) remaining textMeasurement of the elements of financial statements• The process of determining the monetary amounts at

which the elements of the financial statements are to be recognised and carried in the statement of financial position and the statement of profit or loss.

• There are four choices available:– Historical cost– Realisable value– Current cost– Present value

SAMPLE

BPP LEARNING MEDIA

Recognition and measurement of the elements of fs 4

Measurement basis

Definition

Historical cost Assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given to acquire them at the time of their acquisition.Liabilities are recorded at the amount of proceeds received in exchange for the obligation.

Realisable value The amount of cash or cash equivalents that could currently be obtained by selling an asset in an orderly disposal.SAMPLE

SAMPLE

BPP LEARNING MEDIA

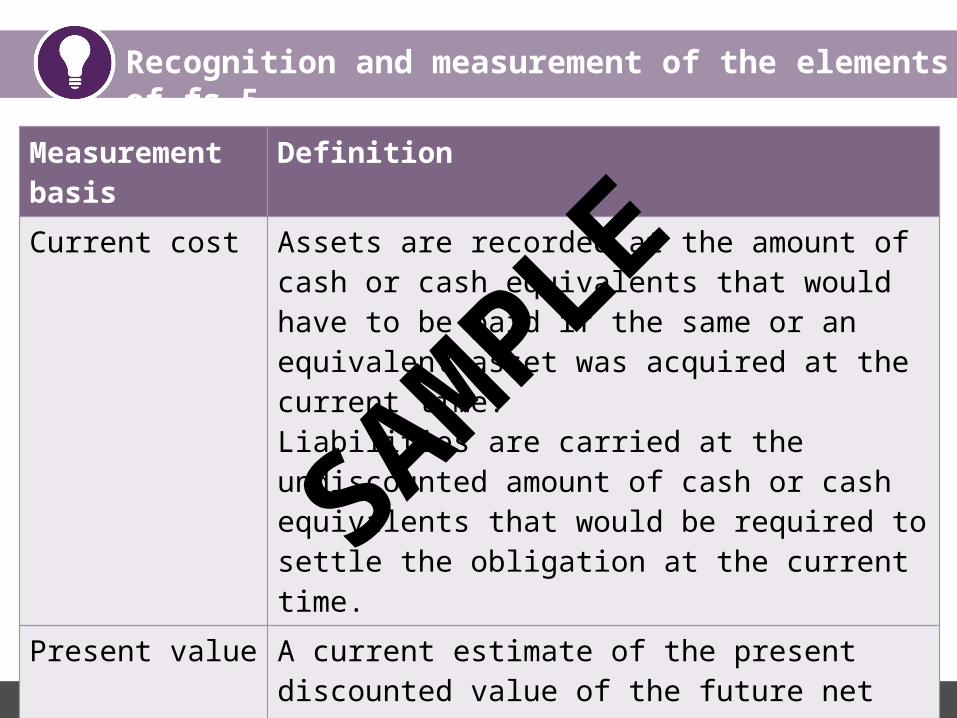

Recognition and measurement of the elements of fs 5

Measurement basis

Definition

Current cost Assets are recorded at the amount of cash or cash equivalents that would have to be paid if the same or an equivalent asset was acquired at the current time.Liabilities are carried at the undiscounted amount of cash or cash equivalents that would be required to settle the obligation at the current time.

Present value A current estimate of the present discounted value of the future net cash flows in the normal course of business.SAMPLE

SAMPLE

BPP LEARNING MEDIA

Fair presentation and compliance with IFRS 1

• Financial statements should present fairly the financial position, financial performance and cash flows of an entity.

• It is presumed that this fair presentation will be achieved where an entity complies with both the Conceptual Framework and IFRSs.

• Fair presentation also requires an entity to:– Select and apply appropriate accounting policies– Present information in a manner that provides relevance

information and which is a faithful representation– Provide additional disclosures where further information

is required to enable users to understand the impact of transactions

SAMPLE

BPP LEARNING MEDIA

Fair presentation and compliance with IFRS 2

• In extremely rare cases management may decide that compliance with an IFRS would make the financial statements misleading.

• Here departure from the IFRS is required in order for fair presentation to be achieved.

• Such departures must be disclosed in full including the reason for the departure and the financial impact of the departure on the financial statements.

SAMPLE

BPP LEARNING MEDIA

Recent exam questions

Nature of question Exam details

Discuss the meaning of understandability and comparability and the role of consistency when preparing financial statements

Q4 (a) Dec 2012

Use specific examples to show how IFRS disclosure can assist the predictive nature of historic financial statements

Q4 (a) June 2011

SAMPLE

SAMPLE

BPP LEARNING MEDIA

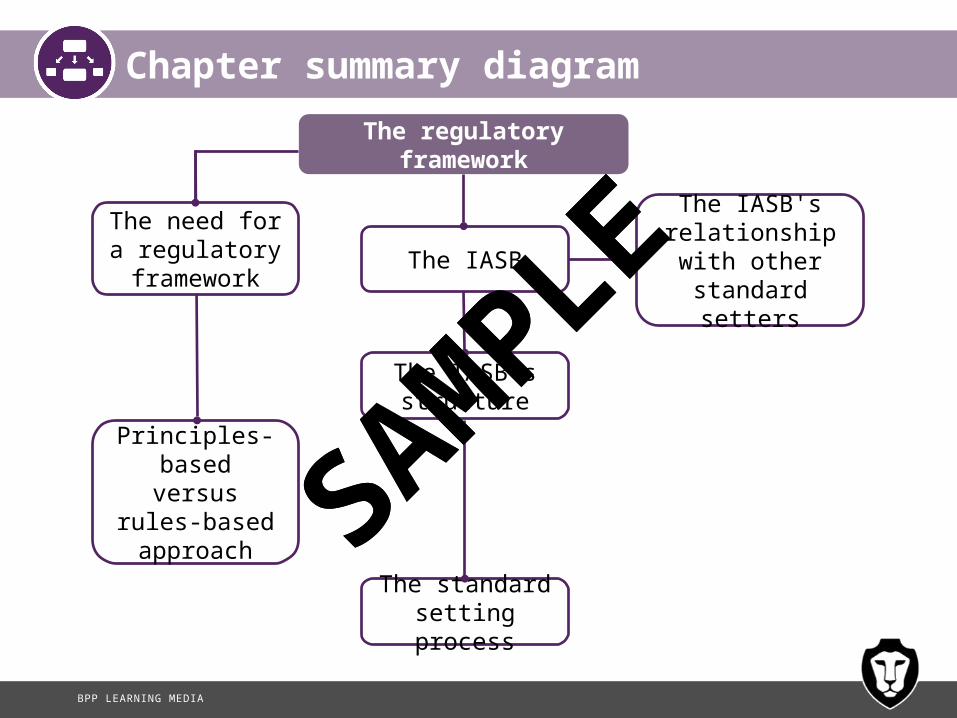

Chapter 2

The regulatory framework

• The need for a regulatory framework

• The International Accounting Standards Board (IASB)

• Setting of International Financial Reporting Standards

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 1

• Explain why a regulatory framework is needed, also including the advantages and disadvantages of IFRS over a national regulatory framework

• Explain why accounting standards on their own are not a complete regulatory framework

• Distinguish between a principles based and a rules based framework and discuss whether they can be complementary

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 2

• Describe the structure and objectives of the IFRS Foundation, the International Accounting Standards Board (IASB), the IFRS Advisory Council (IFRS AC) and the IFRS Interpretations Committee (IFRS IC)

• Describe the IASB’s Standard setting process including revisions to and interpretations of Standards

• Explain the relationship of national standard setters to the IASB in respect of the standard setting process

SAMPLE

BPP LEARNING MEDIA

Chapter summary diagram

Principles-based versus rules-based approach

The IASB's relationship with other standard

setters

The IASB

The regulatory framework

The IASB’s structure

The standard setting process

The need for a regulatory framework

SAMPLE

SAMPLE

BPP LEARNING MEDIA

The need for a regulatory framework 1

• A regulatory framework is required for two main reasons:– To act as a central source of reference of generally

accepted accounting practice (GAAP) in a given market

– To designate a system of enforcement of that GAAP to ensure consistency between companies

• Its aim is to narrow the areas of difference and choice in financial reporting and to improve comparability.

SAMPLE

BPP LEARNING MEDIA

The need for a regulatory framework 2

Principles-based vs. rules-based systems• A principles-based system works within a set of laid

down principles.• International Financial Reporting Standards use a

principles-based system: they are written based on the definitions of the elements of financial statements and the recognition and measurement principles as detailed in the Conceptual Framework for Financial Reporting.

• These principles are designed to cover a wide range of scenarios without the need for a set of rules which govern every eventuality.

SAMPLE

BPP LEARNING MEDIA

The need for a regulatory framework 3

Principles-based vs. rules-based systems• A rules-based system regulates for issues as they

arise, this means that accounting standards contain rules which apply to specific scenarios.

• US GAAP has historically used a rules-based system however many of the recent corporate accounting scandals have arisen as a direct result of companies acting in a way that avoids rules.

• Consequently the US is moving towards a more principles-based system.

SAMPLE

BPP LEARNING MEDIA

The need for a regulatory framework 4

There are both advantages and disadvantages of a principles vs. rules-based system:• Advantages:

– A principles-based approach on a single conceptual framework ensures that standards are consistent with each other.

– Rules can be broken and ‘loopholes’ found whereas principles are more likely to offer a ‘catch all’ scenario.

– Principles reduce the need for excessive detail in standards.

• Disadvantages:– Principles can become out of date and can be overly

flexible and therefore subject to manipulation.

SAMPLE

BPP LEARNING MEDIA

The IASB 1

• The International Accounting Standards Board (IASB) is an independent accounting standard setter established in 2001.

• It has three formal objectives:– To develop, in the public interest, a single set of high quality,

understandable and enforceable global accounting standards that require high quality, transparent and comparable information in general purpose financial statements

– To promote the use and vigorous application of those standards

– To work actively with national accounting standard setters to bring about convergence of national accounting standards and IFRS to high quality solutions

SAMPLE

BPP LEARNING MEDIA

The IASB 2

IFRS Foundation

Trustees

International Accounting

Standards Board (IASB)

IFRS Interpretations

Committee

IFRS Advisory CouncilSAMPLE

SAMPLE

BPP LEARNING MEDIA

The IASB 3

The IFRS Foundation• The IFRS Foundation is the parent entity of the IASB.• Its trustees appoint:

– The IASB’s Chairman and members of its Board;– The members of the IFRS Interpretations Committee – The members of the IFRS Advisory Council

• It also seeks to raise funds for the organisations’ activities.

SAMPLE

BPP LEARNING MEDIA

The IASB 4

The IFRS Advisory Council• The IFRS Advisory Council’s objective is to give advice

to the IASB on areas of work it should prioritise and on major standard setting projects.

SAMPLE

BPP LEARNING MEDIA

The IASB 5

The IFRS Interpretations Committee• The IFRS Interpretations Committee prepares

interpretations of IFRSAs for approval by the IASB.• It also provides guidance on financial reporting issues

not specifically addressed by IFRSs.

SAMPLE

BPP LEARNING MEDIA

Setting of IFRS 1Below are the key steps in the process used to issue an International Financial Reporting Standard:

IASB staff prepare an issues paper including studying the approach of national standards setters.The IFRS Advisory Council is consulted about the advisability of adding the topic to the IASB’s agenda.

A Discussion Paper may be published for public comment.

An Exposure Draft is published for public comment.

After considering all comments received, and IFRS is approved by a majority of the IASB. The final standard includes both a basis for conclusions and any dissenting opinions.

Issues Paper

Discussion Paper

Exposure Draft

International Financial Reporting Standard

SAMPLE

BPP LEARNING MEDIA

Setting of IFRS 2

• For the IASB to achieve its objective in relation to the harmonisation of accounting standards it is important that it works closely with other national standard setters.

• The IASB is trying to co-ordinate its work plan with national standard setters such that when it adds an item to its agenda that national standard setters do the same thing so that a standard can be agreed which has international consensus.

• There are also plans to review all standards where there are significant differences between IFRS and national standards.

SAMPLE

BPP LEARNING MEDIA

Setting of IFRS 3

Current standards examinable in paper F7 are:• IAS 1 (revised)• IAS 2• IAS 7• IAS 8• IAS 10• IAS 11• IAS 12• IAS 16• IAS 17• IAS 18

SAMPLE

BPP LEARNING MEDIA

Setting of IFRS 4

Current standards examinable in paper F7 are:• IAS 20• IAS 21• IAS 23• IAS 24• IAS 27 (revised)• IAS 28• IAS 32• IAS 33• IAS 34• IAS 36

SAMPLE

BPP LEARNING MEDIA

Setting of IFRS 5

Current standards examinable in paper F7 are:• IAS 37• IAS 38• IAS 39• IAS 40• IFRS 1• IFRS 3 (revised)• IFRS 5• IFRS 7• IFRS 9• IFRS 10• IFRS 13

SAMPLE

BPP LEARNING MEDIA

Recent exam questions

Nature of question Exam details

Explain the difference between a principles-based and a rules-based system and state which system is used by International Financial Reporting Standards.

Q5 (a) June 2012

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Chapter 3

Presentation of published financial statements

• IAS 1 (revised) Presentation of financial statements

• Statement of financial position• The current/ non-current distinction• Statement of profit or loss and

other comprehensive income• Changes in equity• Notes to the financial statements• Revision of basic accounts

SAMPLE

SAMPLE

BPP LEARNING MEDIA

Syllabus Guide detailed outcomes 1

• Describe the structure (format) and content of financial statements presented under IFRS

• Prepare any entity’s financial statements in accordance with the prescribed structure and content

• Prepare and explain the contents and purpose of the statement of changes in equity

• Describe and prepare a statement of changes in equity

SAMPLE

BPP LEARNING MEDIA

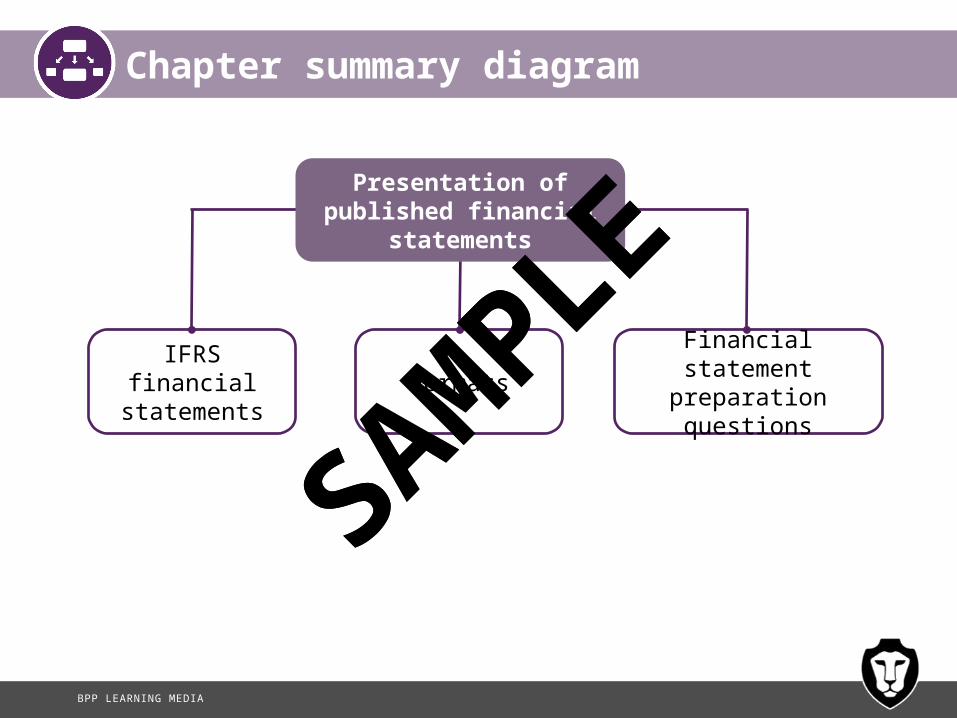

Chapter summary diagram

IFRS financial statements Formats Financial statement

preparation questions

Presentation of published financial statements

SAMPLE

SAMPLE

BPP LEARNING MEDIA

IAS 1 (revised) 1

IAS 1 applies to the preparation and presentation of general purpose financial statements in accordance with IFRSs and states that a complete set of financial statements comprises:• A statement of financial position at the end of the period• A statement of profit or loss and other comprehensive

income for the period• A statement of changes in equity for the period• A statement of cash flows for the period• Notes to the financial statements including a summary of

significant accounting policies an other explanatory information

SAMPLE

BPP LEARNING MEDIA

IAS 1 (revised) 2

• Financial statements should also disclose:– The name of the reporting entity– Whether the accounts relate to the single entity only or a group

of entities– The date of the end of the reporting period or the period

covered by the financial statements– The presentation currency – The level of rounding used in presenting amounts in the

financial statements• Financial statements must be prepared on a timely basis in order to

provide useful information to users.

SAMPLE

BPP LEARNING MEDIA

Statement of financial position 1XYZ GROUP – STATEMENT OF FINANCIAL POSITION FOR THE YEAR ENDED 31 DECEMBER 20X2

20X2 20X1 $’000 $’000

ASSETSNon-current assetsProperty, plant and equipment X XGoodwill X XOther intangible assets X XInvestments in associates X XInvestments in equity instruments X X

X XCurrent assetsInventories X XTrade receivables X XOther current assets X XCash and cash equivalents X X

X XTotal assets X X

SAMPLE

BPP LEARNING MEDIA

Statement of financial position 2 $’000 $’000

EQUITY AND LIABILITIESEquityShare capital X XRetained earnings X XOther components of equity X X

X XTotal equity X X

SAMPLE

BPP LEARNING MEDIA

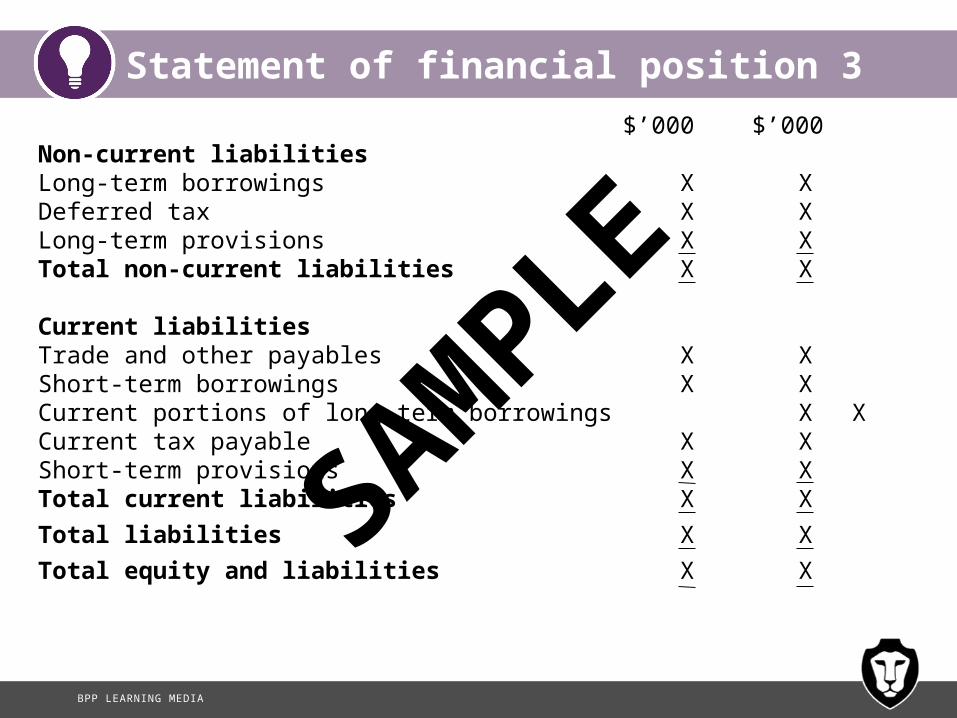

Statement of financial position 3 $’000 $’000

Non-current liabilitiesLong-term borrowings X XDeferred tax X XLong-term provisions X XTotal non-current liabilities X X

Current liabilitiesTrade and other payables X XShort-term borrowings X XCurrent portions of long-term borrowings X XCurrent tax payable X XShort-term provisions X XTotal current liabilities X XTotal liabilities X XTotal equity and liabilities X X

SAMPLE

BPP LEARNING MEDIA

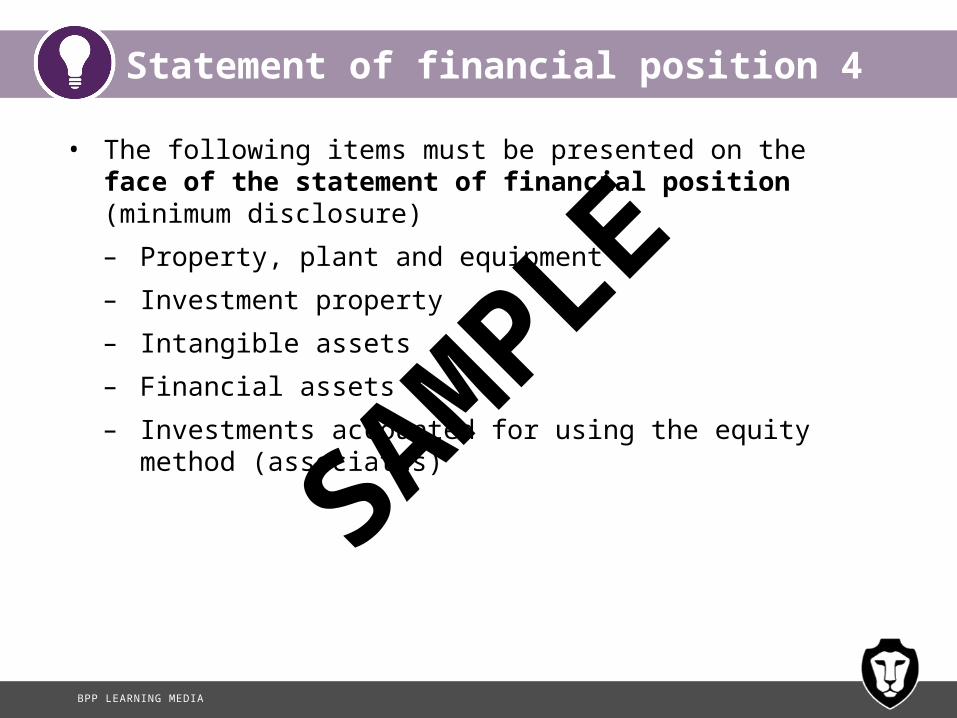

Statement of financial position 4

• The following items must be presented on the face of the statement of financial position (minimum disclosure)– Property, plant and equipment– Investment property– Intangible assets– Financial assets– Investments accounted for using the equity method

(associates)

SAMPLE

BPP LEARNING MEDIA

Statement of financial position 5

– Biological assets (not in syllabus)– Inventories– Trade and other receivables– Cash and cash equivalents– Assets classified as held for sale under IFRS 5– Trade and other payables– Provisions– Financial liabilities

SAMPLE

BPP LEARNING MEDIA

Statement of financial position 6

– Current tax liabilities and assets as in IAS 12– Deferred tax liabilities and assets– Liabilities included in disposal groups under IFRS 5– Non-controlling interests– Issued capital and reserves

• Other items can be presented in the notes to the financial statements unless they need to be disclosed on the face of the statement of financial position in order for users to properly understand the entity’s financial position.

SAMPLE

BPP LEARNING MEDIA

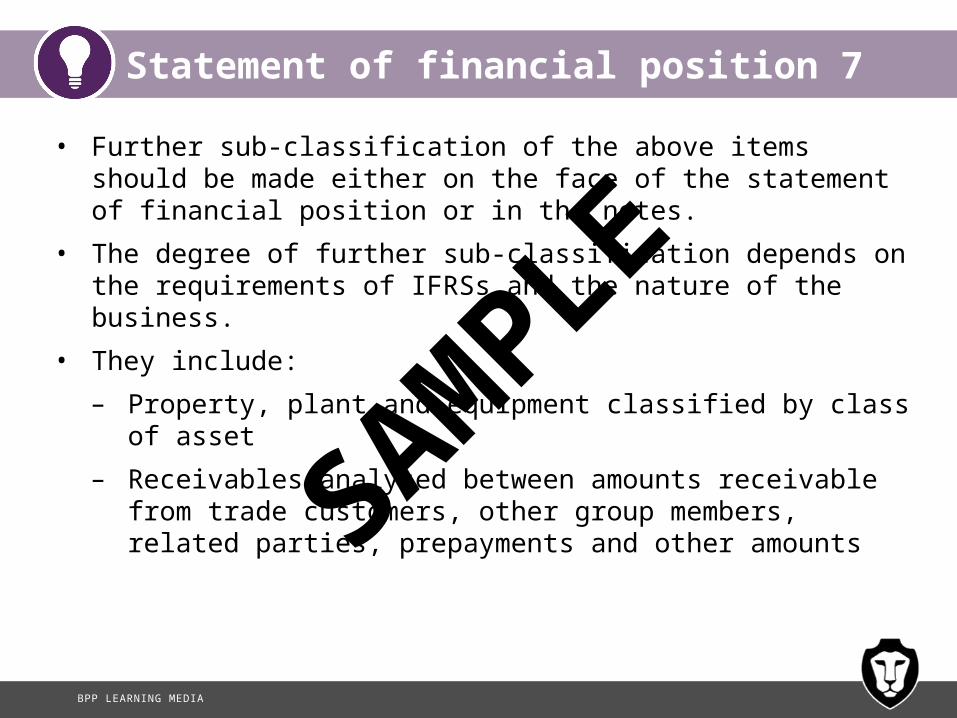

Statement of financial position 7

• Further sub-classification of the above items should be made either on the face of the statement of financial position or in the notes.

• The degree of further sub-classification depends on the requirements of IFRSs and the nature of the business.

• They include:– Property, plant and equipment classified by class of asset– Receivables analysed between amounts receivable from trade

customers, other group members, related parties, prepayments and other amounts

SAMPLE

BPP LEARNING MEDIA

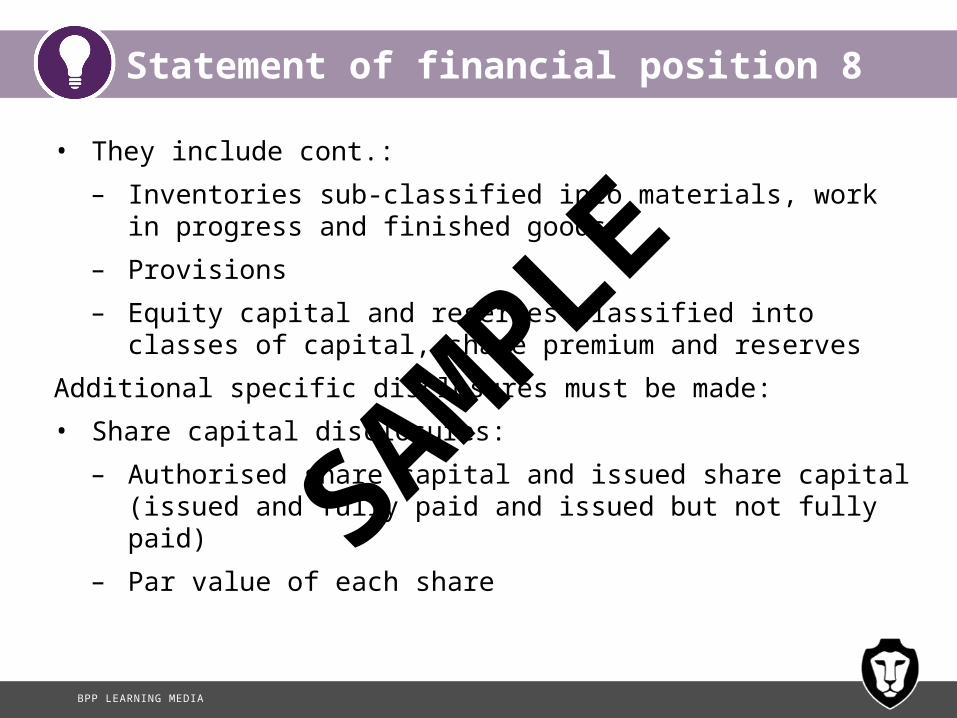

Statement of financial position 8

• They include cont.:– Inventories sub-classified into materials, work in progress and

finished goods– Provisions– Equity capital and reserves classified into classes of capital, share

premium and reserves

Additional specific disclosures must be made:• Share capital disclosures:

– Authorised share capital and issued share capital (issued and fully paid and issued but not fully paid)

– Par value of each share

SAMPLE

BPP LEARNING MEDIA

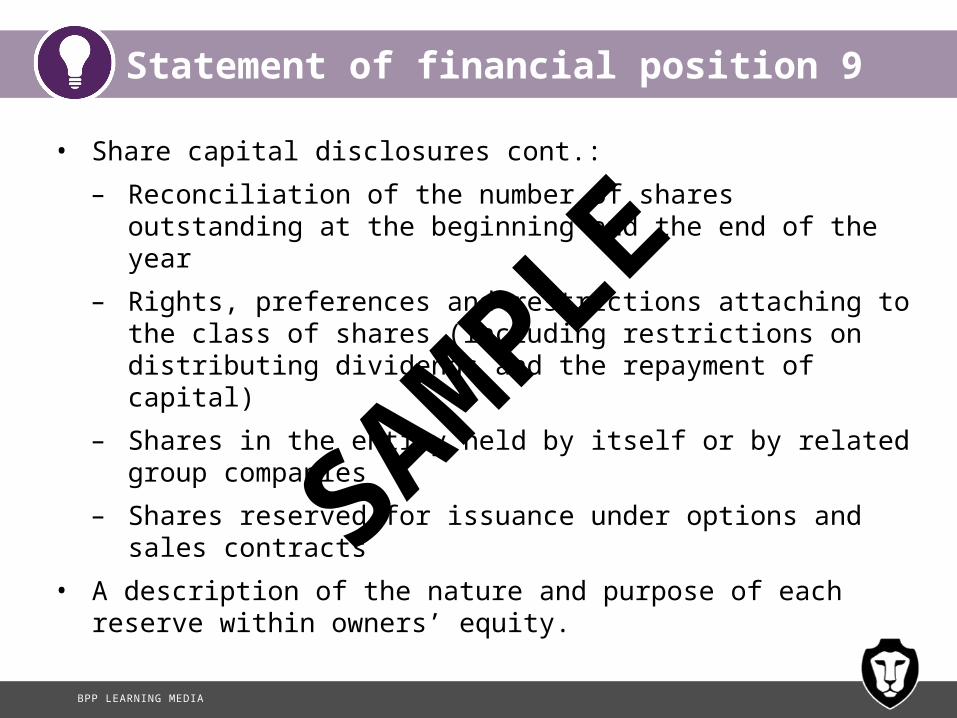

Statement of financial position 9

• Share capital disclosures cont.:– Reconciliation of the number of shares outstanding at the

beginning and the end of the year– Rights, preferences and restrictions attaching to the class of

shares (including restrictions on distributing dividends and the repayment of capital)

– Shares in the entity held by itself or by related group companies– Shares reserved for issuance under options and sales contracts

• A description of the nature and purpose of each reserve within owners’ equity.

SAMPLE

BPP LEARNING MEDIA

The current/ non-current distinction

• Assets and liabilities should be classified as either current or non-current on the face of the statement of financial position.

• Current assets and liabilities comprise assets and liabilities which relate to the operating cycle of the entity.

• The operating cycle of an entity is the time between the acquisition of assets for processing and their realisation in cash and cash equivalents.

• Non-current assets and liabilities are used in the long term operations of the entity and will typically be recovered or settled after more than twelve months.

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 1

IAS 1 (revised) allows income and expense items to be presented either:• In a single statement of profit or loss and other comprehensive

income• In two statements: a separate statement of profit or loss and a

statement of other comprehensive income

SAMPLE

BPP LEARNING MEDIA

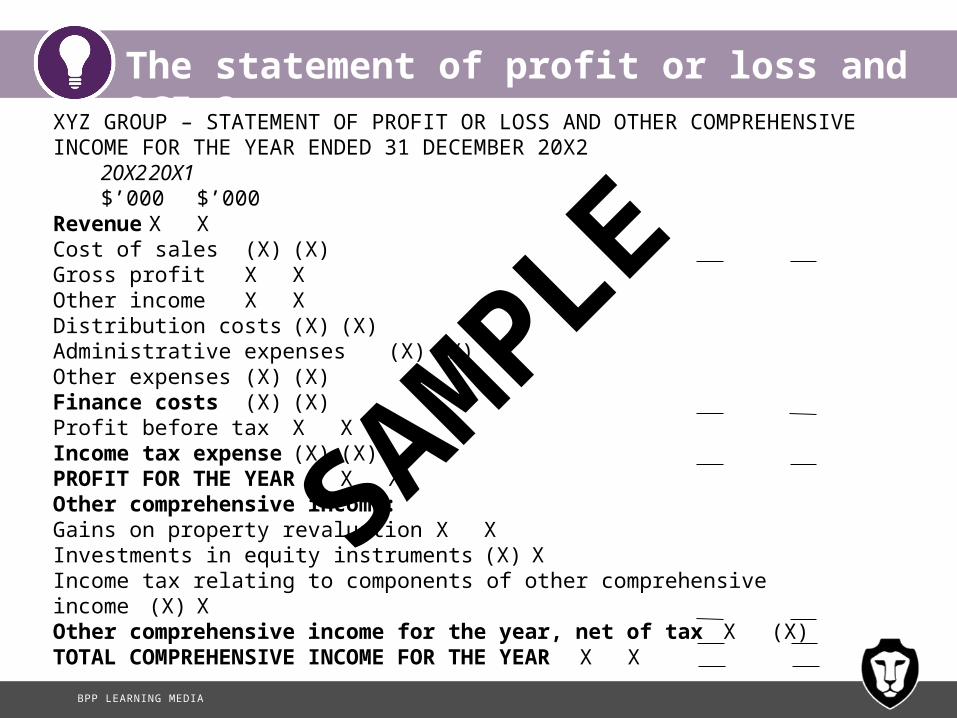

The statement of profit or loss and OCI 2XYZ GROUP – STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 20X2

20X2 20X1$’000 $’000

Revenue X XCost of sales (X) (X)Gross profit X XOther income X XDistribution costs (X) (X)Administrative expenses (X) (X)Other expenses (X) (X)Finance costs (X) (X)Profit before tax X XIncome tax expense (X) (X)PROFIT FOR THE YEAR X XOther comprehensive income:Gains on property revaluation X XInvestments in equity instruments (X) XIncome tax relating to components of other comprehensiveincome (X) XOther comprehensive income for the year, net of tax X (X)TOTAL COMPREHENSIVE INCOME FOR THE YEAR X X

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 3XYZ GROUP – STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 20X2 20X2 20X1

$’000 $’000

Revenue X X

Cost of sales (X) (X)

Gross profit X X

Other income X X

Distribution costs (X) (X)

Administrative expenses (X) (X)

Other expenses (X) (X)

Finance costs (X) (X)

Profit before tax X X

Income tax expense (X) (X)

PROFIT FOR THE YEAR X X

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 4XYZ GROUP – STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 20X2

20X2 20X1$’000 $’000

Profit for the year X X

Other comprehensive income:Gains on property revaluation X X

Investments in equity instruments (X) X

Income tax relating to components of other comprehensive

income (X) X

Other comprehensive income for the year, net of tax X (X)

TOTAL COMPREHENSIVE INCOME FOR THE YEAR X X

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 5

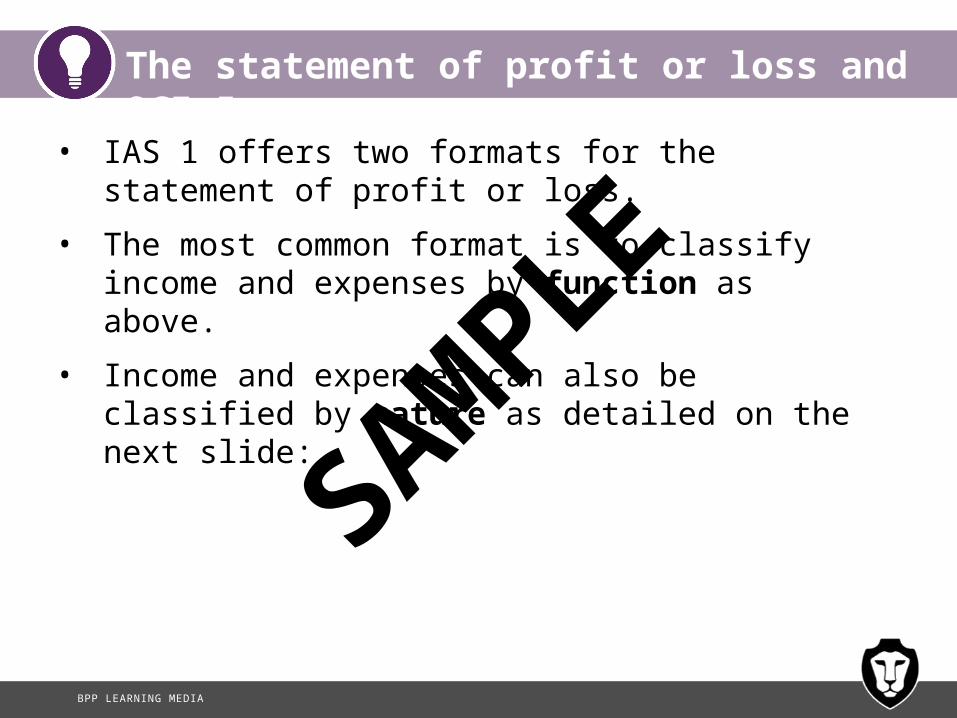

• IAS 1 offers two formats for the statement of profit or loss.

• The most common format is to classify income and expenses by function as above.

• Income and expenses can also be classified by nature as detailed on the next slide:

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 6XYZ GROUP – STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 20X2 20X2 20X1

$’000 $’000

Revenue X X

Other operating income X X

Changes in inventories of FG and WIP (X) X

Work performed by the entity and capitalised X X

Raw material and consumables used (X) (X)

Employee benefits expense (X) (X)

Depreciation and amortisation expense (X) (X)

Impairment of property, plant and equipment (X) (X)

Other expenses (X) (X)

Finance costs (X) (X)

Profit before tax X X

Income tax expense(X) (X)

PROFIT FOR THE YEAR X X

SAMPLE

BPP LEARNING MEDIA

The statement of profit or loss and OCI 7

• IAS 1 (revised) also requires the following items to be disclosed on the face of the statement of profit or loss (minimum disclosure)– Revenue– Finance costs– Tax expense– Profit or loss

• Note that dividends do not meet the IASB Conceptual Framework definition of an expense and so are not included in the statement of profit or loss and other comprehensive income.

• Rather they are shown as a deducted from retained earnings in the statement of changes in equity.

SAMPLE

BPP LEARNING MEDIA

Changes in equity

Share Ret’d Revaluation Totalcapital earnings surplus equity$’000 $’000 $’000 $’000

Balance at 1 January 20X1 X X X X Changes in accounting policy - (X) - (X) Restated balance X X X X Changes in equity for 20X1Dividends - (X) - (X) Total comprehensive income - X (X) X Balance at 31 December 20X1 X X X X Changes in equity for 20X2Issue of share capital X - - X Dividends (X) (X) Total comprehensive income - X X X Transfer to retained earnings - X (X) - Balance at 31 December 20X2 X X X X

SAMPLE

BPP LEARNING MEDIA

Notes to the financial statements

Notes to the accounts amplify the information given in the financial statements.Notes perform the following functions: • Provide information about the basis on which the financial

statements were prepared and which specific accounting policies were chosen.

• Disclose information required by IFRSs which has not been disclosed elsewhere in the financial statements.

• Show any additional information relevant to understanding the financial statements.

SAMPLE

BPP LEARNING MEDIA

Revision of basic accounts 1

• In the exam you will be required to prepare a basic set of company accounts from a trial balance incorporating additional information provided in the question.

• To be successful in these questions you must

– Practice as many examples of these questions as you can

– Adopt a methodical approach to completing them

SAMPLE

BPP LEARNING MEDIA

Revision of basic accounts 2

1. Read the requirements and scan the information in the question.

2. Set up four pages as necessary:

• Proforma statement of profit or loss and other comprehensive income

• Proforma statement of financial position

• Proforma statement of changes in equity

• A page for workings

3. Read the additional information given and make a mark by each caption in the trial balance that is going to change.

SAMPLE

BPP LEARNING MEDIA

Revision of basic accounts 3

4. Transfer the figures from the trial balance:

• Unaffected figures may be entered directly on your proforma

• Figures requiring adjustment can either be put into a working or brackets opened up on the face of your proforma solution

5. Work through the adjustments in the additional information dealing with both sides of the double entry. Once you have attempted all adjustments, balance off your workings and transfer the final figures to your proforma.

SAMPLE

BPP LEARNING MEDIA

Question: AZ Co

AZ Co is a quoted manufacturing company. Its finished products are stored in a nearby warehouse until ordered by customers. AZ Co has performed very well in the past, but has been in financial difficulties in recent months and has been reorganising the business to improve performance.

The trial balance for AZ Co at 31 March 20X3 was as follows:

SAMPLE

BPP LEARNING MEDIA

Question: AZ CoTRIAL BALANCE AT 31 MARCH 20X3 $'000 $'000Sales 124,900Cost of goods manufactured in the year to 31 March 20X3 (excluding depreciation) 94,000Distribution costs 9,060Administrative expenses 16,020Restructuring costs 121Interest received 1,200Debenture interest paid 639Land and buildings (including land $20,000,000) 50,300Plant and equipment 3,720 Accumulated depreciation at 31 March 20X2: Buildings 6,060 Plant and equipment 1,670Investment properties (at market value) 24,000Inventories at 31 March 20X2 4,852Trade receivables 9,330Bank and cash 1,190Ordinary shares of $1 each, fully paid 20,000Share premium 430Revaluation surplus 3,125Retained earnings at 31 March 20X2 28,077Ordinary dividends paid 1,0007% debentures 20X7 18,250Trade payables 8,120Proceeds of share issue 2,400

214,232 214,232

SPLOCI

SOFP

SAMPLE

BPP LEARNING MEDIA

Question: AZ Co

Additional information provided:

i. The property, plant and equipment are being depreciated as follows:• Buildings: 5% per annum straight line• Plant and equipment: 25% per annum reducing balance• Depreciation of buildings is considered an administrative cost

while depreciation of plant and equipment should be treated as a cost of sale.

ii. On 31 March 20X3 the land was revalued to $24,000,000.

iii. Income tax for the year to 31 March 20X3 is estimated at $976,000. Ignore deferred tax.

SAMPLE

BPP LEARNING MEDIA

Question: AZ Co

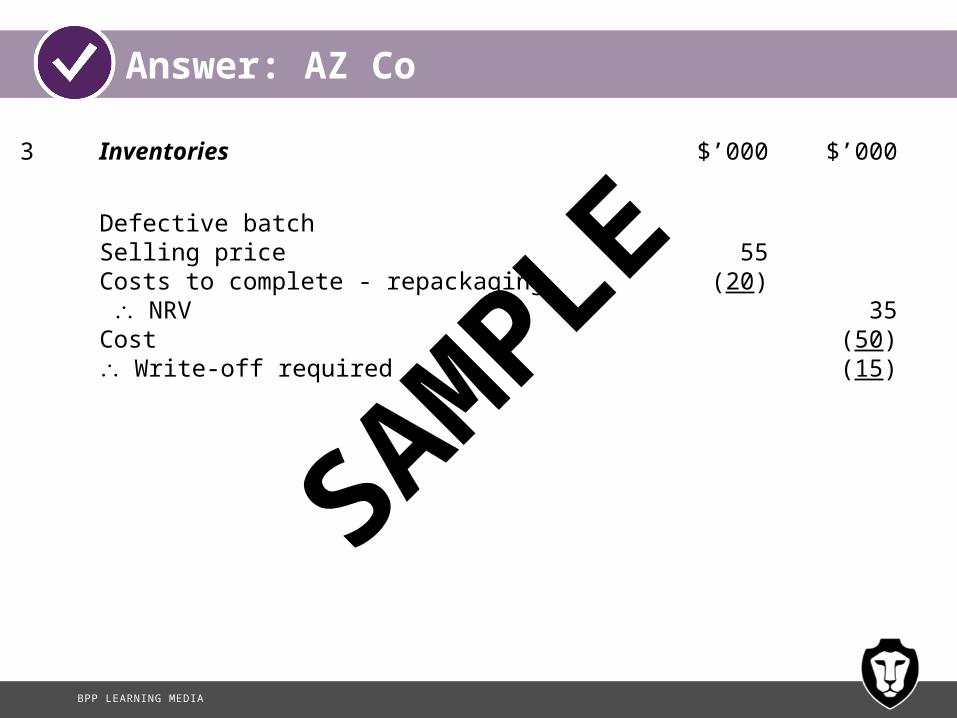

iv. The closing inventories at 31 March 20X3 were $5,180,000. An inspection of finished goods found that a production machine had been set up incorrectly and that several production batches, which had cost $50,000 to manufacture, had the wrong packaging. The goods cannot be sold in this condition but could be repacked at an additional cost of $20,000. They could then be sold for $55,000. the wrongly packaged goods were included in closing inventories at their cost of $50,000.

v. The 7% loan notes are ten year loans due for repayment by 31 March 20X7. Interest on these loan notes needs to be accrued for the six months to 31 March 20X3.

vi. The restructuring costs in the trial balance represent the cost of a major restructuring of the company to improve competitiveness and future profitability.

SAMPLE

BPP LEARNING MEDIA

Question: AZ Co

vii. No fair value adjustments were necessary to the investment properties during the period.

viii. During the year the company issued 2 million new ordinary shares for cash at $1.20 per share. The proceeds have been recorded as ‘proceeds of share issue’.

SAMPLE

BPP LEARNING MEDIA

Question: AZ Co

RequiredPrepare the statement of profit or loss and other comprehensive income and statement of changes in equity for AZ for the year to 31 March 20X3 and a statement of financial position at that date.Notes to the financial statements are not required, but all workings must be clearly shown.

SAMPLE

BPP LEARNING MEDIA

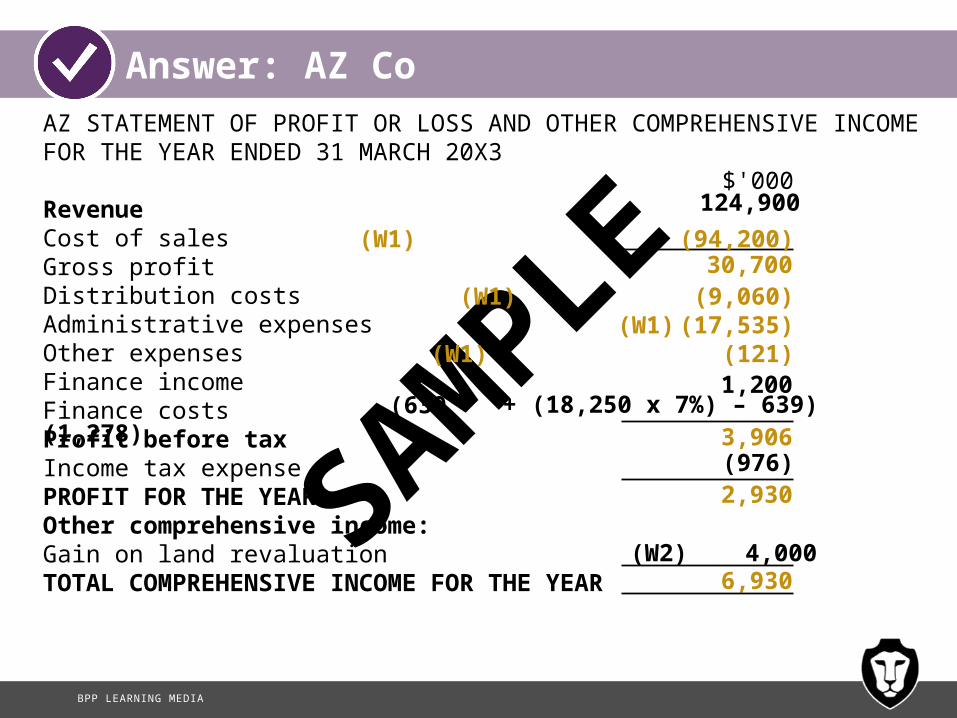

Answer: AZ CoAZ STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 20X3

$'000Revenue Cost of sales Gross profitDistribution costsAdministrative expensesOther expensesFinance incomeFinance costs Profit before taxIncome tax expense PROFIT FOR THE YEAROther comprehensive income:Gain on property revaluation TOTAL COMPREHENSIVE INCOME FOR THE YEAR

124,900

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

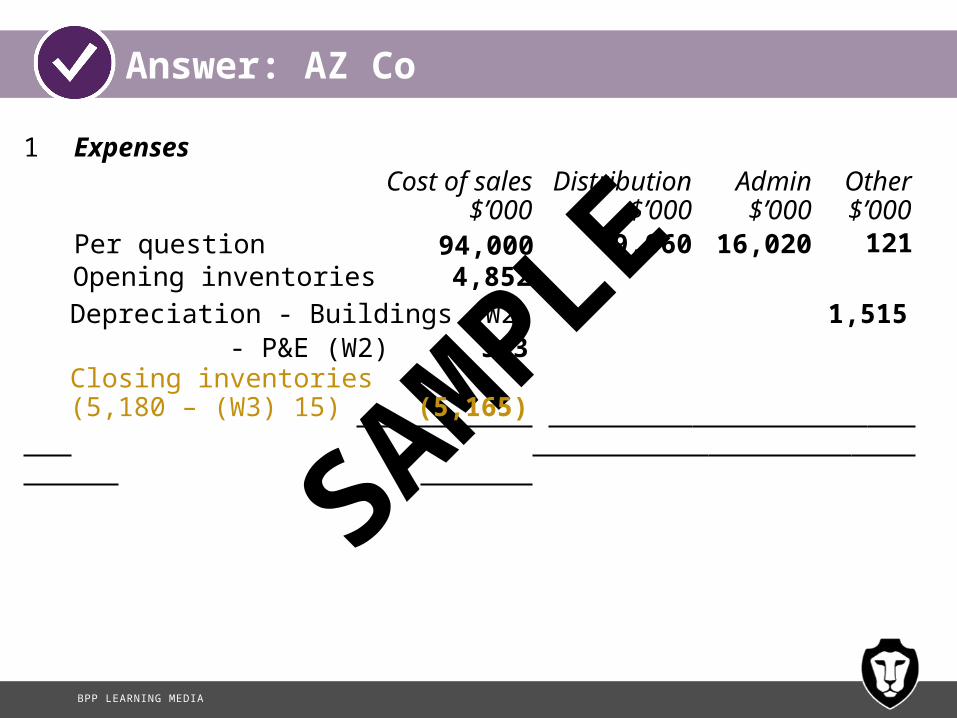

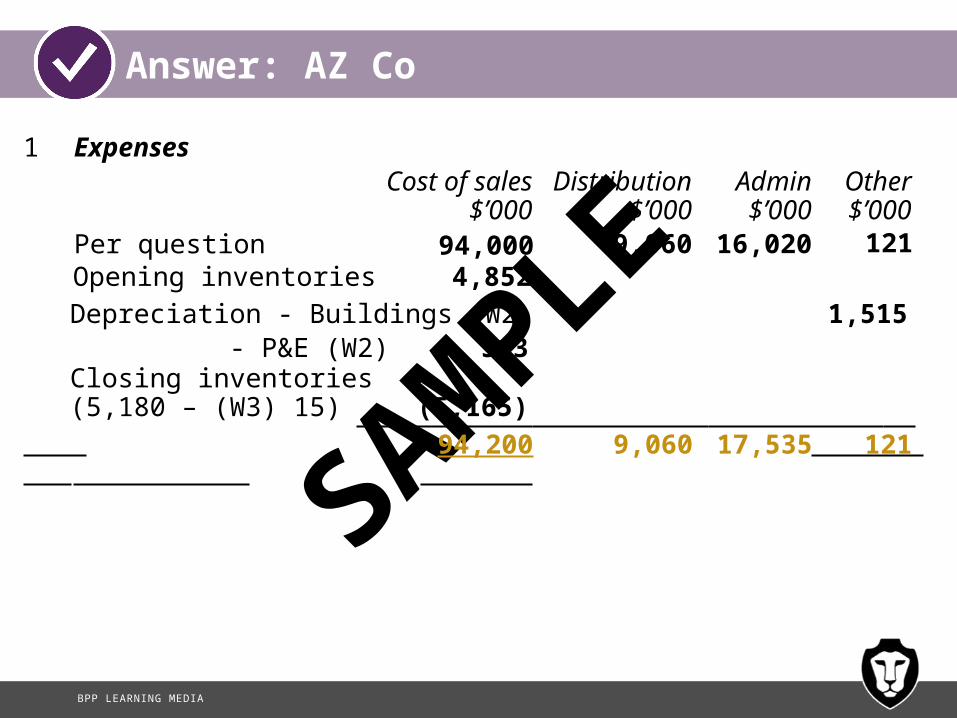

1 Expenses Cost of sales Distribution Admin Other

$’000 $’000 $’000$’000

Per question

16,02094,000 9,060 121

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoAZ STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 20X3

$'000Revenue Cost of sales Gross profitDistribution costsAdministrative expensesOther expensesFinance incomeFinance costs Profit before taxIncome tax expense PROFIT FOR THE YEAROther comprehensive income:Gain on land revaluation TOTAL COMPREHENSIVE INCOME FOR THE YEAR

124,900

1,200 (639)

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

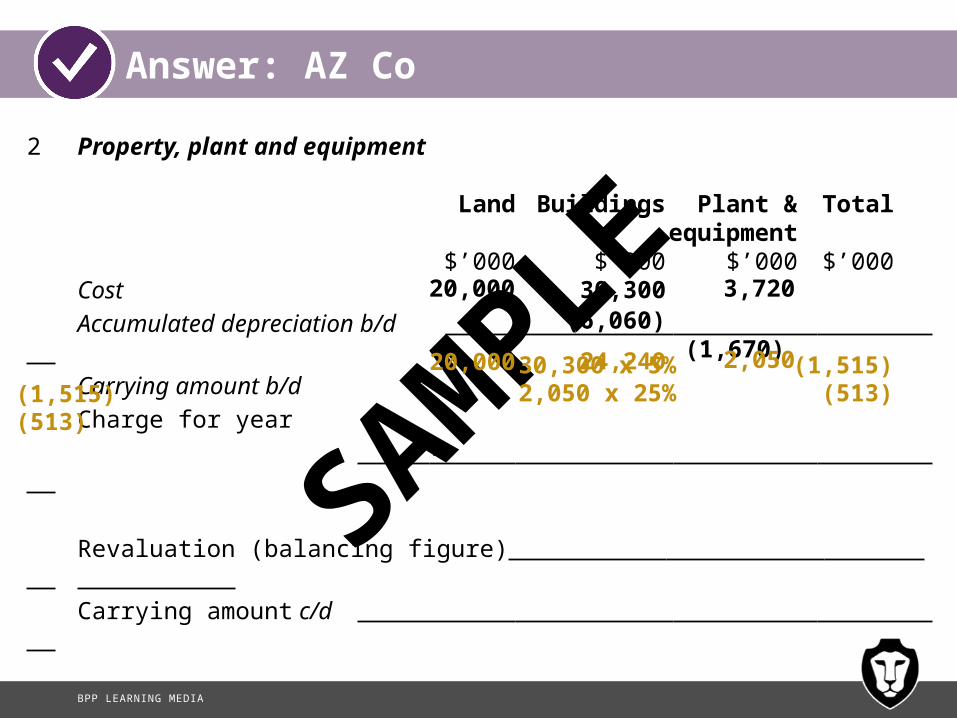

2 Property, plant and equipment

Land Buildings Plant & Total equipment

$’000 $’000 $’000 $’000CostAccumulated depreciation b/d - Carrying amount b/dCharge for year

-

Revaluation (balancing figure) Carrying amount c/d

(6,060)30,300

(1,670)3,72020,000

SAMPLE

BPP LEARNING MEDIA

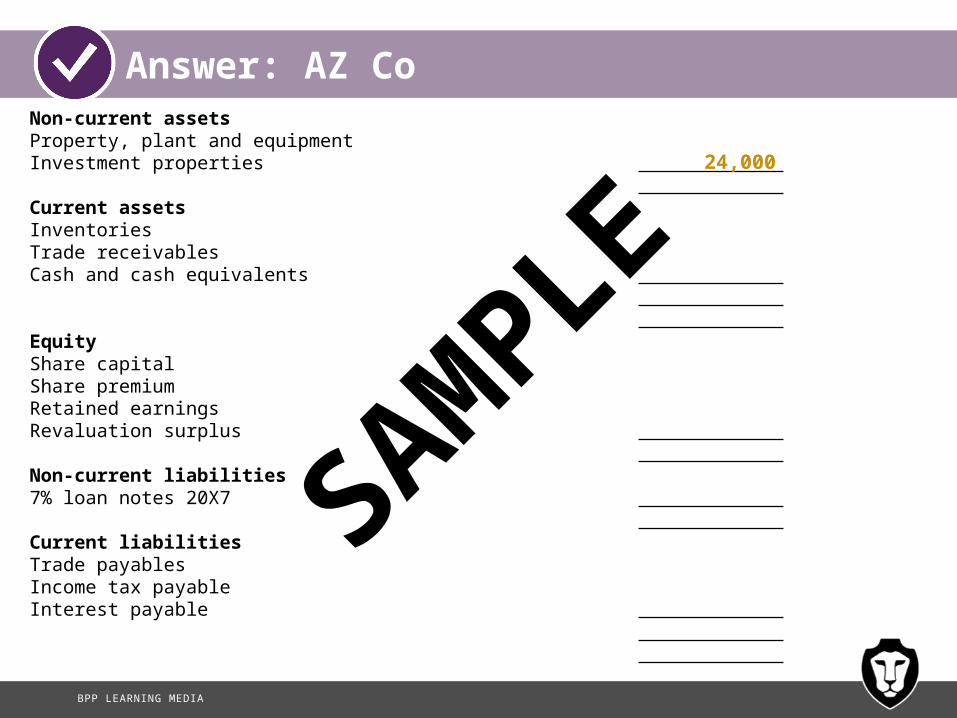

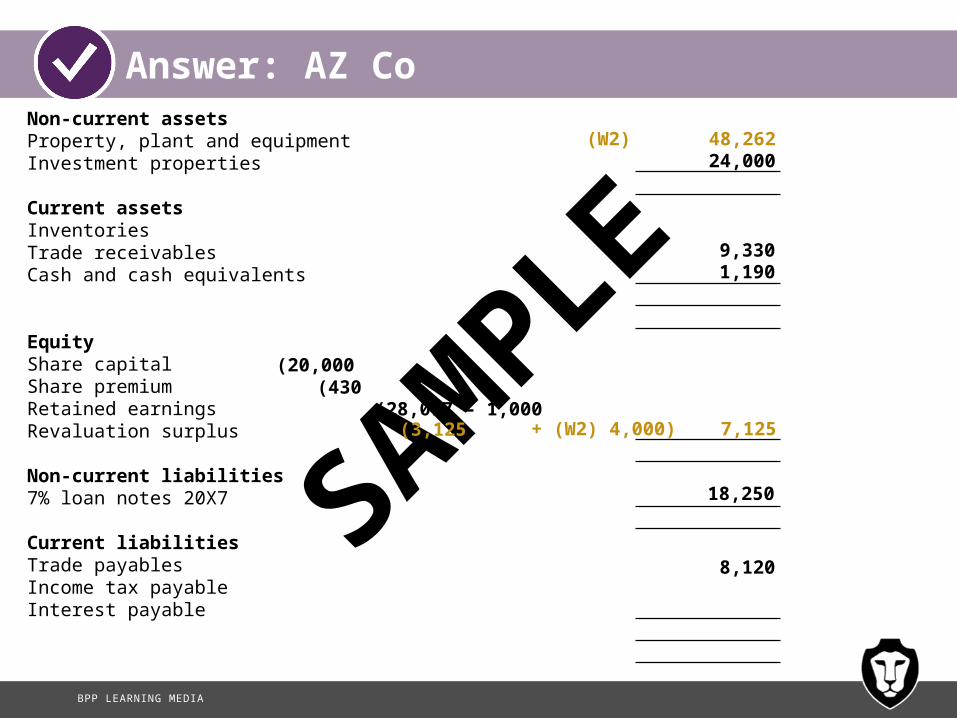

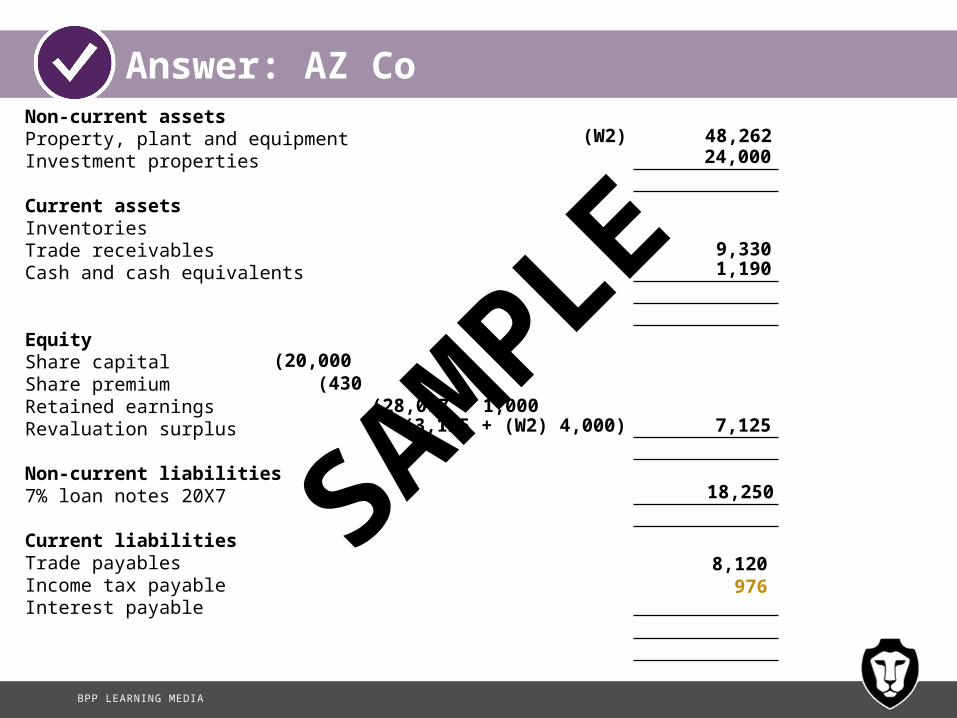

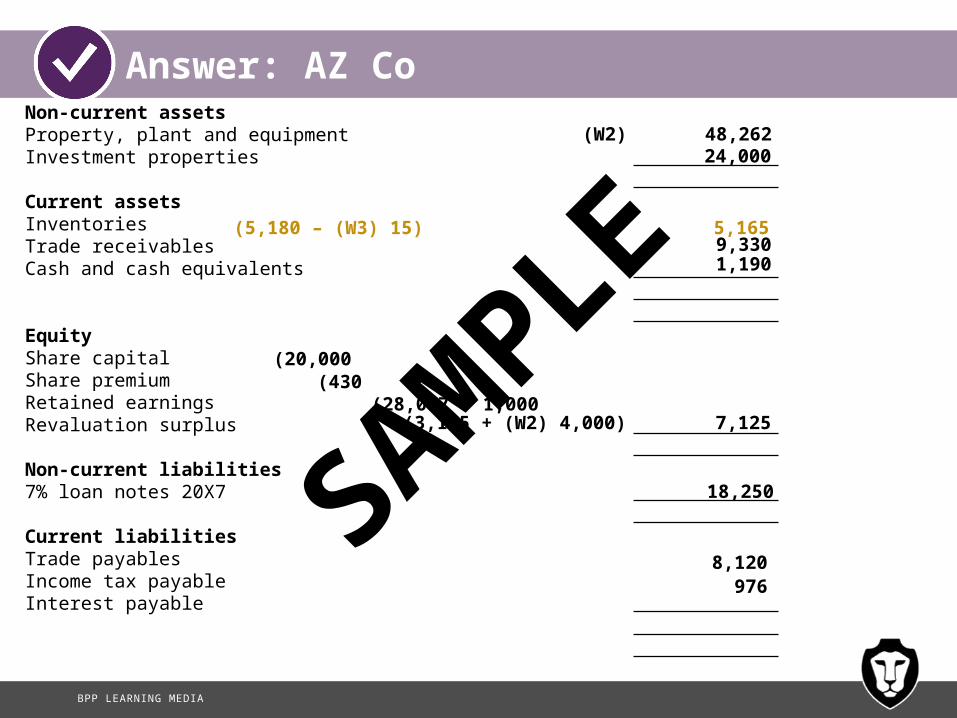

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

24,000

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

1 Expenses Cost of sales Distribution Admin Other

$’000 $’000 $’000 $’000Per question

16,02094,000 9,060 121 Opening inventories 4,852

SAMPLE

BPP LEARNING MEDIA

– 1,000

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

24,000

9,3301,190

(20,000 (430 (28,077 (3,125

18,250

8,120

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

2 Property, plant and equipment

Land Buildings Plant & Total equipment

$’000 $’000 $’000 $’000CostAccumulated depreciation b/d - Carrying amount b/dCharge for year

-

Revaluation (balancing figure) Carrying amount c/d

30,300(6,060) (1,670)

3,72020,000

24,240 2,050 30,300 x 5% (1,515) (1,515) 2,050 x 25% (513) (513)

20,000

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

1 Expenses Cost of sales Distribution Admin Other

$’000 $’000 $’000 $’000Per question

94,000 9,060 16,020 121Opening inventories 4,852Depreciation - Buildings (W2) 1,515

- P&E (W2) 513

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

2 Property, plant and equipment

Land Buildings Plant & Total equipment

$’000 $’000 $’000 $’000CostAccumulated depreciation b/d - Carrying amount b/dCharge for year

-

Revaluation (balancing figure) Carrying amount c/d

30,300(6,060) (1,670)

3,720

24,240 2,050 30,300 x 5% (1,515) (1,515) 2,050 x 25% (513) (513)

20,000

20,000

54,020(7,730)46,290

4,000 - - 4,000 24,000 22,725 1,537 48,262

20,000 22,725 1,537 44,262

SAMPLE

BPP LEARNING MEDIA

(3,125

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

(20,000 (430

24,000

1,190

8,120

9,330

(28,077 – 1,000

18,250

(W2) 48,262

+ (W2) 4,000) 7,125

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoAZ STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 20X3

$'000Revenue Cost of sales Gross profitDistribution costsAdministrative expensesOther expensesFinance incomeFinance costs Profit before taxIncome tax expense PROFIT FOR THE YEAROther comprehensive income:Gain on land revaluation TOTAL COMPREHENSIVE INCOME FOR THE YEAR

1,200

124,900

(639

(976)

(W2) 4,000

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

(430

24,000

1,190

8,120

9,330

(20,000

(28,077 – 1,000

(W2) 48,262

18,250

(3,125 + (W2) 4,000) 7,125

976

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

3 Inventories $’000 $’000

Defective batchSelling price 55Costs to complete - repackaging (20) NRV 35Cost (50) Write-off required (15)

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

(430

24,000

1,190

8,120

9,330

(20,000

(28,077 – 1,000

(W2) 48,262

18,250

(3,125 + (W2) 4,000) 7,125

976

(5,180 – (W3) 15) 5,165

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

1 Expenses Cost of sales Distribution Admin Other

$’000 $’000 $’000 $’000Per question

94,000 9,060 16,020 121Opening inventories 4,852Depreciation - Buildings (W2) 1,515

- P&E (W2) 513Closing inventories(5,180 – (W3) 15) (5,165)

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoAZ STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 20X3

$'000Revenue Cost of sales Gross profitDistribution costsAdministrative expensesOther expensesFinance incomeFinance costsProfit before taxIncome tax expensePROFIT FOR THE YEAROther comprehensive income:Gain on land revaluation TOTAL COMPREHENSIVE INCOME FOR THE YEAR

1,200

124,900

(639

(976)

(W2) 4,000

+ ((18,250 x 7%) – 639) (1,278)

SAMPLE

BPP LEARNING MEDIA

Answer: AZ CoNon-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

(430

24,000

1,190

8,120

9,330

(20,000

(28,077 – 1,000

(W2) 48,262

18,250

Revaluation surplus (3,125 + (W2) 4,000) 7,125

976 (1,278 – 639) 639

+ (2m x $1)) 22,000 + (2m x $0.20)) 830

(5,180 – (W3) 15) 5,165

SAMPLE

BPP LEARNING MEDIA

Answer: AZ Co

1 Expenses Cost of sales Distribution Admin Other

$’000 $’000 $’000 $’000Per question

94,000 9,060 16,020 121Opening inventories 4,852Depreciation - Buildings (W2) 1,515

- P&E (W2) 513Closing inventories(5,180 – (W3) 15) (5,165)

94,200 9,060 17,535 121

SAMPLE

BPP LEARNING MEDIA

30,700

3,906

2,930

6,930

Answer: AZ CoAZ STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 20X3

$'000Revenue Cost of sales Gross profitDistribution costsAdministrative expensesOther expensesFinance incomeFinance costs Profit before taxIncome tax expense PROFIT FOR THE YEAROther comprehensive income:Gain on land revaluation TOTAL COMPREHENSIVE INCOME FOR THE YEAR

1,200

124,900

(639

(976)

(W2) 4,000

+ (18,250 x 7%) – 639) (1,278)

(W1) (94,200)

(W1) (9,060) (W1) (17,535) (W1) (121)

SAMPLE

BPP LEARNING MEDIA

72,262

15,68587,947

59,962

18,250

9,73587,947

Non-current assetsProperty, plant and equipmentInvestment properties

Current assetsInventoriesTrade receivablesCash and cash equivalents

EquityShare capitalShare premiumRetained earnings Revaluation surplus

Non-current liabilities7% loan notes 20X7

Current liabilitiesTrade payablesIncome tax payableInterest payable

(430

24,000

1,190

8,120

9,330

(20,000

(28,077 – 1,000

(W2) 48,262

18,250

(3,125 + (W2) 4,000) 7,125

Answer: AZ Co

976 (1,278 – 639) 639

+ (2m x $1)) 22,000 + (2m x $0.20)) 830

(5,180 – (W3) 15) 5,165

+ 2,930) 30,007

SAMPLE

BPP LEARNING MEDIA

Balance at 1 April 20X2Issue of share capitalDividendsTotal comprehensive income Balance at 31 March 20X3

Answer: AZ Co

AZSTATEMENT OF CHANGES IN EQUITY

Share Share Ret’d Rev’n Totalcapital premium earnings surplus$’000 $’000 $’000 $’000 $’00020,000 430 28,077 3,125 51,632

2,000 400 2,400(1,000) (1,000)

2,930 4,000 6,93022,000 830 30,007 7,125 59,962

SAMPLE

BPP LEARNING MEDIA

Recent exam questionsNature of question Exam details

The financial statement preparation question is tested in Question 2 of the ACCA F7 exam.You should expect to see the following requirement:i. Prepare the statement of profit or

loss and other comprehensive income;

ii. Prepare the statement of changes in equity

iii. Prepare the statement of financial position.

Q2 in all past exams

SAMPLE

Related Documents